pnasresearcharticle_arxiv \correspondingauthor1Corresponding author. E-mail: taro.takaguchi@nict.go.jp

Social dynamics of financial networks

Abstract

Abstract

The global financial crisis in 2007–2009 demonstrated that systemic risk can spread all over the world through a complex web of financial linkages, yet we still lack fundamental knowledge about the evolution of the financial web.

In particular, interbank credit networks shape the core of the financial system, in which a time-varying interconnected risk emerges from a massive number of temporal transactions between banks. The current lack of understanding of the mechanics of interbank networks makes it difficult to evaluate and control systemic risk.

Here, we uncover fundamental dynamics of interbank networks by seeking the patterns of daily transactions between individual banks.

We find stable interaction patterns between banks from which distinctive network-scale dynamics emerge.

In fact, the dynamical patterns discovered at the local and network scales share common characteristics with social communication patterns of humans.

To explain the origin of “social” dynamics in interbank networks, we provide a simple model that allows us to generate a sequence of synthetic daily networks characterized by the observed dynamical properties. The discovery of dynamical principles at the daily resolution will enhance our ability to assess systemic risk and could contribute to the real-time management of financial stability.

-2pt

Introduction

Financial systemic risk is one of the most serious threats to the global economy. The global financial crisis of 2007–2009 showed that a failure of one bank can lead to a financial contagion through a complex web of financial linkages, which are created by everyday transactions among financial institutions [1, 2]. Even after the crisis, many countries have experienced a prolonged recession, the so-called Great Recession, showing that the social cost of a financial crisis can be enormous [3, 4]. Evaluating and controlling systemic risk has therefore been recognized as one of the greatest challenges for interdisciplinary researchers across different fields of science [5, 6, 7, 8].

In the modern financial system, interbank markets play a fundamental role, in which banks lend to and borrow from each other (hereafter, we refer to all types of financial institutions as “banks" for brevity). Lending and borrowing in interbank markets are necessary daily tasks for banks to smoothen their liquidity management [9], but at the same time, they also form the center of a global web of interconnected risk; shocks to interbank markets may spill over to other parts of the global financial system through the financial linkages to which banks are connected [10, 6, 11]. Many previous studies attempt to assess systemic risk by simulating different scenarios of cascading bank failures on both real [12, 13, 14, 15, 16] and synthetic interbank credit networks [17, 18, 19, 11, 20, 21, 22]. Studies of financial cascades based on synthetic networks often assume a particular static structure, such as random [18, 19], bipartite [11, 23], and multiplex structures [21, 22], successfully revealing that the structural property affects the likelihood of default cascades to a large extent. However, since the great majority of real-world interbank transactions are in fact overnight [9, 24], interbank networks should be treated as dynamical systems with their structure changing on a daily basis. This temporal nature of real interbank networks inevitably limits the practical usefulness of the conventional static approach to systemic risk. Nevertheless, we still have little knowledge about how the structural characteristics of daily networks evolve over time. It has long been believed that the dynamics of interbank networks is random and thus has no meaningful regularity at the daily scale [25]. How the current network structure is correlated with the past structures, or more specifically, how banks choose current trading partners based on their trading history, is still unknown. The ambiguity of the structural dynamics of interbank networks itself may also become a source of systemic risk by veiling the complexity of interconnectivity [26]. The current lack of studies on the mechanics of real interbank networks is in stark contrast to the abundance of research on their static property [27, 12, 28, 29, 30, 15].

The main aim of this work is to uncover fundamental dynamics governing real interbank networks at both local and system-wide scales. For this purpose, we first seek dynamical regularities that would characterize interaction patterns between individual banks by looking at millions of overnight transactions conducted in the Italian interbank market during 2000–2015 [31]. We discover that there exist explicit interaction patterns that rule daily bank-to-bank transactions, which turn out to be essentially the same as the patterns characterizing human social communication; that is, banks trade with their partners in the same way that people interact with friends through phone calls and face-to-face conversations [32, 33]. In fact, those “social” interaction patterns of banks have been surprisingly stable over time, even amid the global financial crisis. On top of local interactions between banks, there emerges a system-wide scaling relationship between the numbers of banks and transactions, just as the number of phone-call pairs scales superlinearly with the size of population [34].

To explain the origin of social dynamics in interbank networks, we develop a model that generates a sequence of synthetic daily networks from which all the observed dynamical patterns simultaneously emerge at both local and network scales. Our discovery of the fundamental mechanism underpinning the daily evolution of interbank networks will enhance the predictability of systemic risk and provide an important step toward the real-time management of financial stability.

Results

The dataset to be analyzed in this work is the time series of daily networks identified from the time-stamped data of interbank transactions conducted in the Italian interbank market during 2000–2015 (Materials and Methods: Data). The daily interbank networks have directed edges originating from lending banks to borrowing banks. One may regard the amount of funds transferred from a lender to a borrower as edge weights, but here we regard the daily networks as unweighted, since we found that the dynamics of edge weights can be decoupled from the edge dynamics themselves (see Supplementary Materials (SM) for the analysis of edge weights).

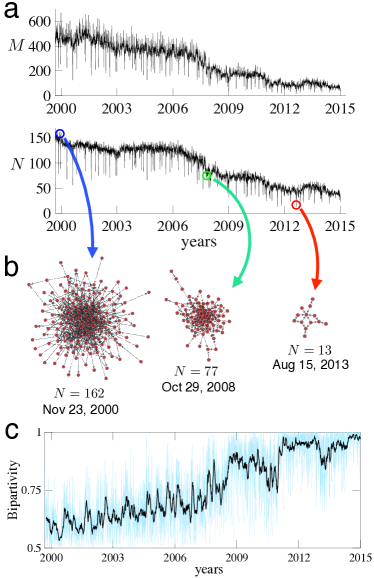

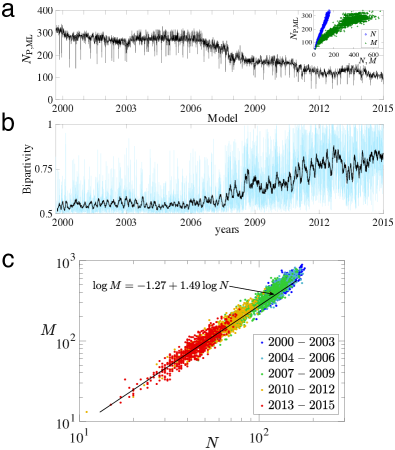

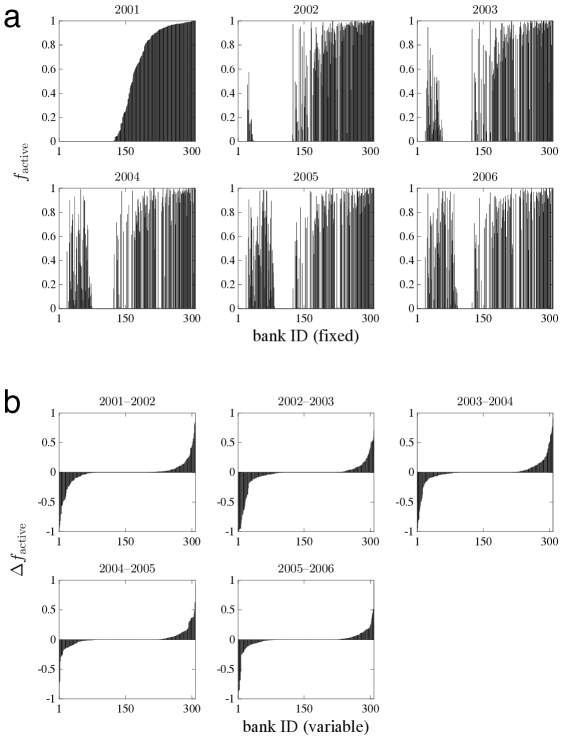

An important general observation regarding the dynamics of daily networks is that both the network size and number of edges have followed downward trends (Fig. 1 a and b). This led the networks closer to a bipartite structure between pure lenders and pure borrowers [35] (Fig. 1c and Table S1), entailing a rapid turnover in the set of banks participating in each daily network (see the turnover rate in Table 1 and Fig. S4). Table 1 summarizes the basic statistics, in which we divide the entire sample period into three subsample periods to observe whether a structural change around the global financial crisis in 2007–2009 is present.

| All | 2000–2006 | 2007–2009 | 2010–2015 | |

|---|---|---|---|---|

| # days | 3,922 | 1,618 | 767 | 1,537 |

| 94.23 | 129.69 | 98.92 | 54.56 | |

| 302.76 | 466.35 | 304.89 | 129.48 | |

| Turnover rate | 0.22 | 0.18 | 0.22 | 0.26 |

| Bipartivity | 0.77 | 0.64 | 0.78 | 0.92 |

and denote the average numbers of active banks and edges in the daily networks, respectively. The turnover rate is the average of the Jaccard distance , where is the set of active banks on day . See caption of Fig. 1c for a description of bipartivity.

Dynamical patterns of daily networks

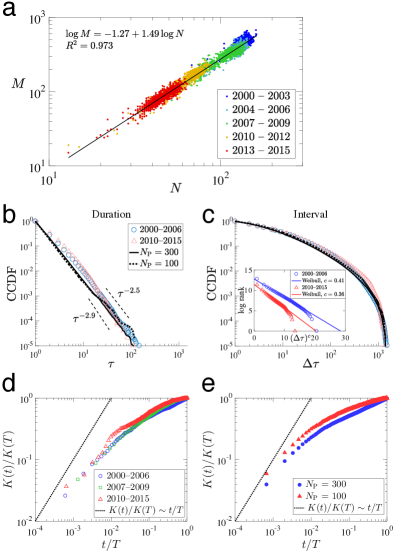

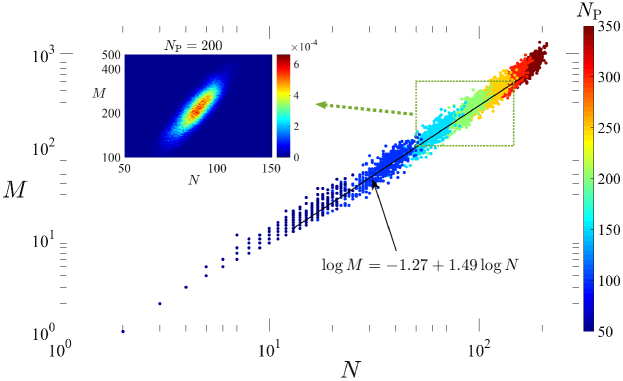

The downward trends in and , along with the intermittent spikes, left a broad range of daily combinations , which allows us to ask how the number of financial linkages is dynamically constrained by the number of banks. In fact, there arises a clear superlinearity, (Fig. 2a). This suggests that the average degree of a daily network increases with order , or . It should be noted that the fact that is given as a power-law function of is similar to a widely observed phenomenon in social networks, called superlinear scaling, in which the number of edges scales superlinearly with the number of nodes across different locations [38, 39, 40, 34].

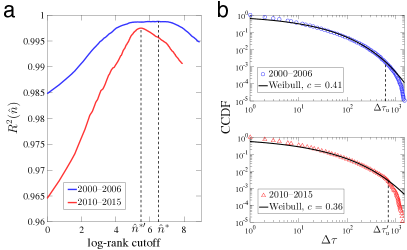

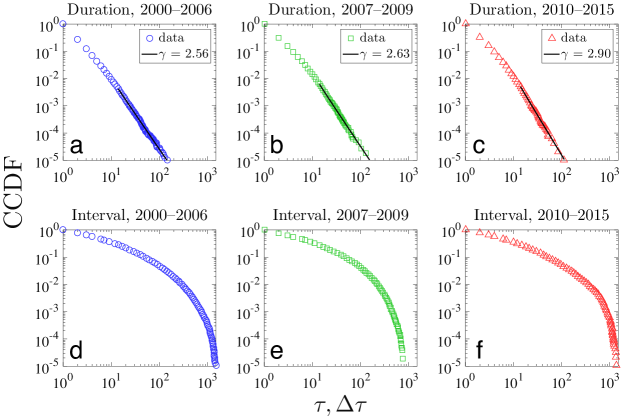

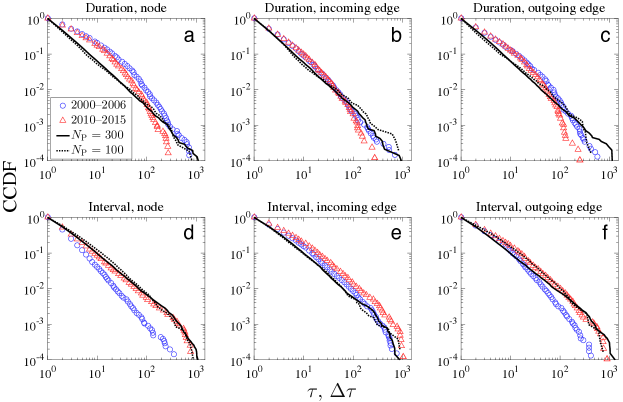

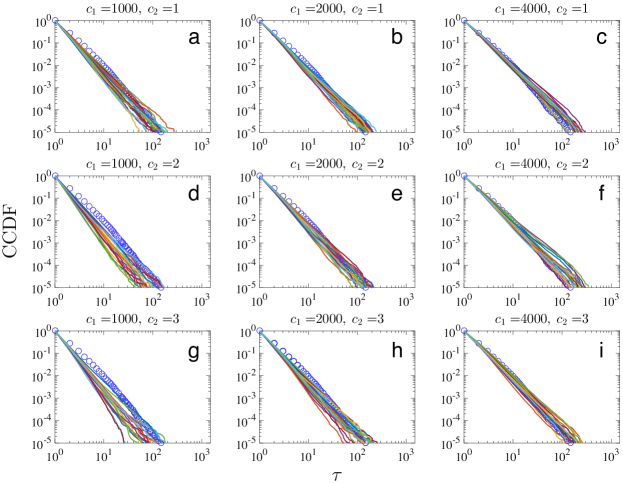

In addition to the macroscopic dynamics of and , we also find characteristic properties of the microdynamics of individual edges: edge duration and interval time. We define duration as the number of successive business days on each of which a bank pair performs at least one transaction. Aggregated over all trading pairs, follows a power-law distribution whose complementary cumulative distribution function (CCDF) has an exponent between and (Fig. 2b and Fig. S5 in SM. The exponents are estimated using the method proposed in Refs. [41, 42]). Similar power-law distributions are observed when we redefine as the duration of individual banks’ successive trading activity either for lending, borrowing, or both (Fig. S6 in SM).

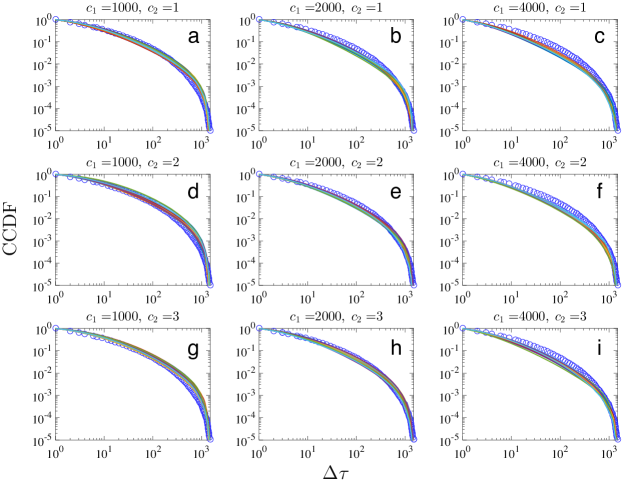

On the other hand, the interval time for a bank pair is defined as the interval length between two consecutive transactions during which the bank pair performs no transactions. In contrast to , does not follow a power-law distribution, while it still shows a long-tailed behavior (Fig. 2c). The interval distribution fits well with a Weibull distribution up to a certain cut-off level (Fig. 2c, Inset. See section S1 of SM for details on the fitting method [43, 44]).

We observe that the distributions of and have been quite stable throughout the whole data period. This observation is notable, not only because and continually fluctuate at a daily resolution over the course of the decreasing trends (Fig. 1a), but also because a large fraction of the set of participating banks changes day to day (Fig. S4). The high metabolism of the interbank market suggests that the stationarity of and is not necessarily attributed to the presence of steady relationships between particular banks.

While the dynamics of individual edges in daily networks is shown to follow particular patterns, it would also be meaningful to see the dynamics of aggregated edges (i.e., edges of aggregated networks). We focus on the aggregated degree , defined by the average cumulative number of unique trading partners up to time [45, 33]. The normalized aggregate degree, defined by , grows sublinearly in time (Fig. 2d), meaning that the rate at which banks find a new partner tends to decrease over time. Note that such sublinear growth patterns are also reported for the mobility pattern of mobile-phone users [45] and for contact networks of human individuals formed via face-to-face interactions [33].

Model of daily network evolution

The above findings show that the dynamical patterns of interbank transactions are robust across different periods, which leads us to consider that a universal mechanism generating daily interbank networks might exist. Here, we show that the emergence of these regularities can be reconstructed by a dynamical generalization of the fitness model [46, 47] (see Materials and Methods: Model).

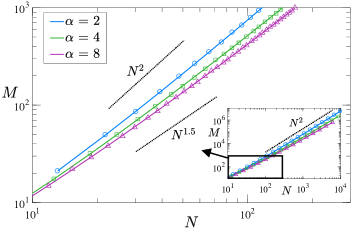

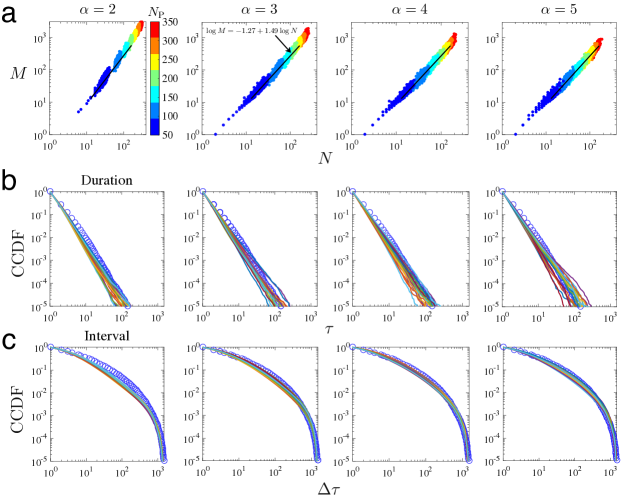

First, we show that variations in the system size of a simple fitness model can explain the empirical superlinear relation . For ease of exposition, suppose for the moment that the networks are undirected. In the fitness model, fitness value is assigned to bank , where represents the potential market size, given by the number of banks that may perform transactions during a day. In the context of interbank transactions, fitness value can be interpreted as the activity level, or willingness, of bank to trade. The probability that an edge is formed between and is given by . For each network generated by this rule, and denote the number of active banks with at least one edge (thus ) and the total number of edges, respectively.

By generating model networks with varying from 20 to 300 for a given , there arises a scaling relation with (symbols in Fig. 3). In previous studies [46, 48, 47], a theoretical analysis of the fitness model predicted , which differs from both our empirical observations (Fig. 2a) and numerical simulations (Fig. 3). In fact, this discrepancy is explained by the presence of isolated banks. In this model, the probability of a bank being isolated (i.e., no edges attached), defined by , is given by a function of :

| (1) |

where and are beta and incomplete beta functions, respectively (see section S2 for derivation). Consequently, and are given by

| (2) |

Since as , and hold true for a sufficiently large , which recovers the quadratic scaling shown in the previous studies [46, 48, 47]. However, for the range of network sizes observed from the data, is not negligible. A combination of derived from (2) for given values of perfectly fits the simulation result (lines in Fig. 3) .

While the superlinear relation can be explained by variations in , this simple model cannot reproduce the distributions of and (Fig. 2 b and c) and the sublinear growth of (Fig. 2d) since these characteristics come from the effect of memory in the formation of links between banks. To capture the memory effect, we introduce a fluctuation in fitness . We assume that at the beginning of day , is updated according to a random walk process or reset to a random value between 0 and 1 with probability (see Materials and Methods: Model). The reset probability is intended to capture the metabolism of interbank markets, in which some banks exit the market after continuous transactions, whereas other banks enter after a long resting periods (e.g., due to a change in the strategy of liquidity management).

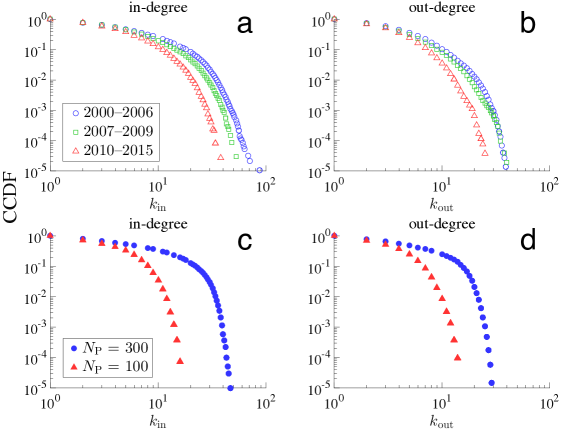

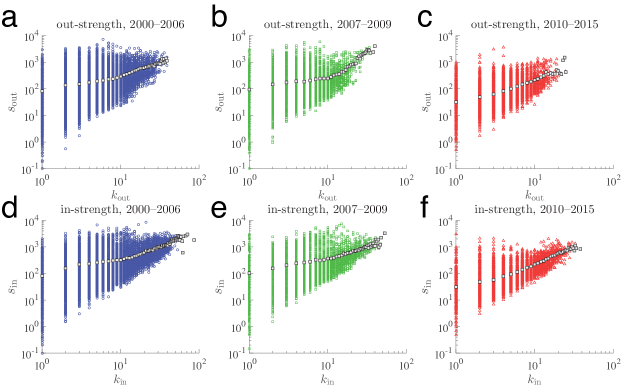

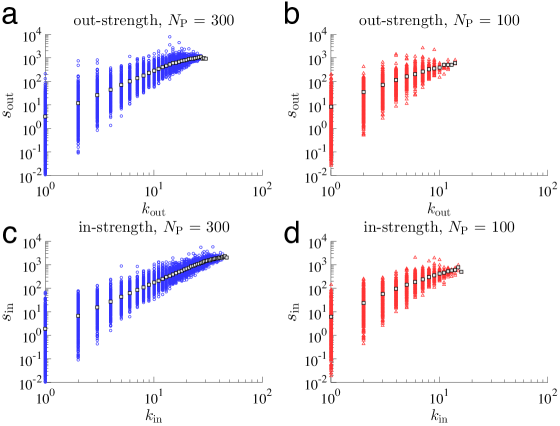

We find that the simulated distributions of duration and interval for pairwise transactions replicate the empirical distributions for a given (see lines in Fig. 2 b and c). We confirmed that the model can robustly reproduce the duration and interval distributions under different parameter settings (Figs. S7 b and c, S8 and S9). In addition, the growth pattern of the normalized aggregate degree is successfully reproduced (Fig. 2e). We also evaluate the model fit for other dynamical properties such as the degree distribution and the strength as a function of degree [49] (Figs. S10–S12).

It should be noted that while the activity level fluctuates with time independently from other banks’ activity levels, the model ensures that the size and the structure of generated networks are stationary for a given . In reality, however, the evolution of daily networks show a decreasing trend (Fig. 1 a and b) and the network size varies from day to day owing to various external factors (e.g., shifts in monetary policy [35] and the seasonality of money demand due to the national holidays and/or the reserve requirement system [9]). In the model, the averages of the network size and the number of edges are controlled by tuning parameter (Fig. 4a).

Fitting model to the data

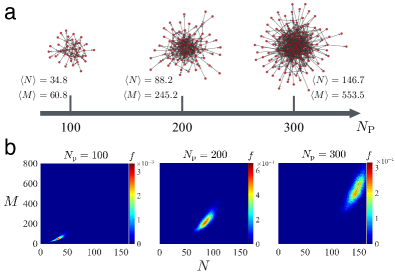

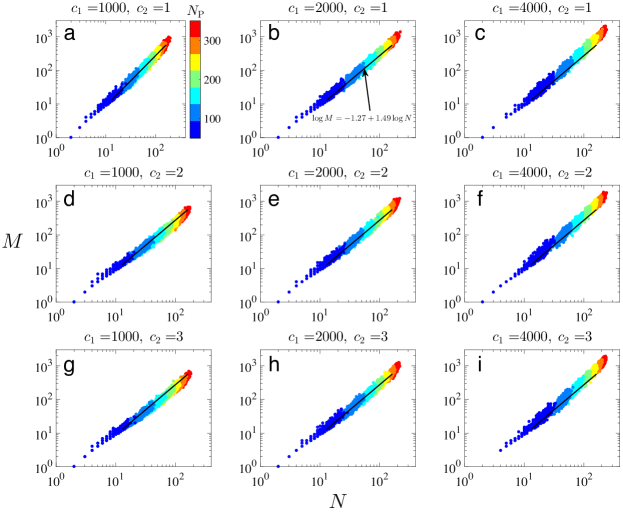

In practice, the influence of exogenous factors that would affect the network size might vary daily. Since in the model the average network size is controlled by tuning parameter , we need to estimate the daily sequence of to reconstruct time series of empirical daily networks. Here, we take the following steps. First, we generate sufficiently many instances of synthetic networks for a given to compute the histogram of (Fig. 4b). Generating networks over a sufficiently broad range of provides a conditional probability function that would cover the range of and observed in the empirical networks (Fig. S13). Second, for a given empirical daily network with , we choose a daily estimate of , denoted by , such that .

We find that simulated instances of concentrate tightly along the regression line of when we vary from to (Fig. S13). This agreement holds true even under alternative parameter values within a reasonable range of variation (Figs. S7a and S14). The sequence of daily estimates of , each of which is based on the empirical combination of a day, exhibit a long-term downward trend consistent with the empirical sequence of and (Fig. 5a). Specifically, is proportional to and increases nonlinearly in with saturation at (Fig. 5a, Inset).

A time series of model networks based on the daily estimates of reproduces the tendency toward a perfect bipartite structure (Fig. 5b), although we have not explicitly modeled how the network structure should change with . The tendency toward a bipartite structure may reflect the fact that the average degree of generated networks becomes smaller as the size of network shrinks. Indeed, the relationship between and across the fitted daily networks explains the emergence of superlinearity (Fig. 5c), which indicates that or .

Discussion

The time series of daily networks reveal many dynamical regularities encoded in millions of financial transactions. An important finding is that the transaction patterns between banks are similar to the social communication patters of humans, which have been observed at higher temporal resolutions (typically 2060 seconds) than a daily resolution. For instance, a power-law scaling in the distribution of the interaction duration has been found in human contact networks, such as face-to-face conversation networks of individuals [32, 33]. The sublinear growth pattern of aggregated degree has also been reported in the mobility pattern of mobile-phone users [45]. In addition, superlinear scaling at the network level (called “urban scaling" [38]) emerges in various social contexts, such as the relationship between the number of mobile connections and the population size of cities [34]. These similarities between financial transaction patterns of banks and social communication patterns of humans strongly suggest that banks choose trading partners in the same manner as individuals decide whom to talk with. The discovered dynamical patterns are quite robust and hold true even amid the global financial crisis, suggesting that there is a universal mechanism connecting financial and social dynamics.

The contribution of our work is not limited to the findings on the transition patterns of interbank networks. The model we propose here can be used as a generator of synthetic networks for studies of financial systemic risk. As is often the case, inaccessibility to empirical data on financial transactions forces academic researchers to use synthetic networks with limited empirical properties [11, 21] or to infer real network structure based on available partial information [14, 50, 51]. Our model provides a way to easily generate synthetic time series of networks that exhibit dynamical properties characterizing the daily evolution of real interbank networks. We hope that the current work will not only deepen our knowledge about the dynamic nature of interbank networks, but also help to improve the conventional approach of systemic-risk studies toward a more dynamic analysis.

We leave three remaining issues that need to be addressed in future research. First, while the observed dynamical patterns are quite robust and seem universal given the similarity to social network dynamics, it is worth investigating whether those findings hold true in other countries as well. Second, we might be able to find other dynamical patterns at different time resolutions such as intraday, weekly, and monthly. If that is the case, we need to see if those dynamical patterns found in different time scales are consistently explained by the current model. Finally, our finding reveals an independence of local interaction patterns of banks from a global-scale network evolution, such as the decreasing trend in network size. This implies that there is no feedback loop between micro and macroscopic phenomena, meaning that banks are not adaptive to their environments. Further research is needed to explain why such a decoupling phenomenon takes hold in financial networks.

Materials and Methods

Data

The original time-stamped data are commercially available from e-MID SIM S.p.A based in Milan, Italy [31]. The data contain all the unsecured euro-denominated transactions between financial institutions made via an online trading platform, e-MID. We focus on overnight (labelled as “ON") and overnight-large (“ONL") transactions. ON transactions refer to contracts that require borrowers to repay the full amount within one business day from the day the loans are executed. ONL transactions are a variant of the ON transactions, where the amount is no less than 100 million euros.

The data processing procedure is as follows. First, we extract transactions made between September 4, 2000 and December 31, 2015. The choice of the initial date is based on the introduction of the ONL category [9]. This leaves us with 1,119,258 ON and 73,480 ONL transactions, which comprise of all the transactions during that period. Next, we transform all the ON and ONL transactions into a sequence of daily networks by applying the daily time window of 8:00–18:00 [24]. We then extract the transactions that belong to the largest weakly connected component of each daily network, which account for of all the daily transactions on average (the minimum is ). We referred to this component as daily network throughout the analysis. Multiple edges between two banks are simplified. In the end, we have 1,187,415 transactions conducted by 308 financial institutions over 3,922 business days.

Model

The dynamic network formation proceeds by repeating the following two steps: (i) edge creation between banks and (ii) update of each bank’s activity level , . We consider three bank types: pure lenders, pure borrowers, and bidirectional traders. Pure lenders (pure borrowers) are the banks that may lend to (borrow from) but never borrow from (lend to) other banks. To take into account the fact that the interbank structure is almost perfectly bipartite when the network size is small (Fig. 1c), we assume that bidirectional traders may lend only to pure borrowers and borrow only from pure lenders. The fraction of each bank type is given as for pure borrowers, pure lenders, and bidirectional traders, respectively, based on the empirical average (Table S1). The type assigned to each bank is fixed throughout the simulation.

At the beginning of the edge-creation stage in day , the interbank system comprises isolated banks without any edges. Bank lends to bank (and thus a directed edge from to is formed) in day with probability , given by

| (3) |

where , , and denote the sets of pure lenders, pure borrowers, and bidirectional traders, respectively. After applying this procedure to every combination of , we remove all the edges and move on to day .

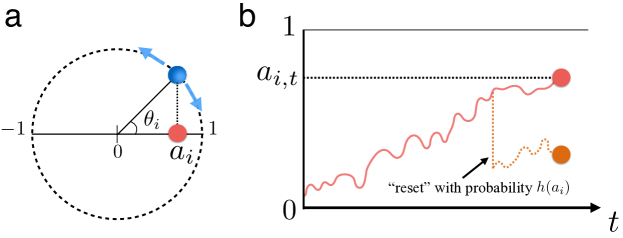

At the beginning of day , the activity level of bank is updated as follows. With probability , is reset to a random value drawn from the uniform distribution on . With probability , the activity level is updated according to a random walk process on the unit circle, given by

| (4) | ||||

| (5) |

where is a random-walk variable that describes the angle on the unit circle (see Fig. S15 for a schematic). Since an activity level must be on , is given by the absolute values of . is a random variable uniformly distributed on . The initial value for the angle is set such that , where is drawn from the uniform distribution on . The above two steps, edge creation and activity updating, are repeated until we reach the predefined terminal date .

The introduction of stochastic variable is meant to capture fluctuations in individual banks’ daily liquidity demand, which can lead to a turnover of participating banks (Fig. S4). Without a variability of (i.e., if is fixed), the metabolism of the model interbank market would be unrealistically low. The reset probability function is specified as .

In total, the model has four parameters: , , , and . Parameter is a key parameter of the model and we explain its role in the main text. The other parameters, , , and , affect the structure of networks through the edge-creation probability (3). We find that the combination gives the best fit to the observed superlinearity (Fig. 2a) and the distributions of and (Figs. S7–S9 in SM). We verified the robustness of the results against moderate changes in (Figs. S7–S9).

We set and discard the initial 5,000 simulation periods to eliminate the influence of the initial conditions. This leaves 1,500 effective simulation periods, which roughly correspond to 6 years of the empirical data.

Acknowledgements

T.K. acknowledges financial support from the Japan Society for the Promotion of Science Grants no. 15H05729 and 16K03551. The authors thank Naoki Masuda for useful comments on the manuscript and Research Project “Network Science” organized at International Institute for Advanced Studies for providing an opportunity to initiate the project.

References

- [1] Brunnermeier MK (2009) Deciphering the liquidity and credit crunch 2007–2008. J Econ Perspect 23:77–100.

- [2] Allen F, Carletti E (2010) An overview of the crisis: Causes, consequences, and solutions. Int Rev Finance 10:1–26.

- [3] Mishkin FS (2011) Monetary policy strategy: lessons from the crisis. NBER W. P. 16755.

- [4] Atkinson T, Luttrell D, Rosenblum H (2013) How bad is it? The costs and consequences of the 2007–09 financial crisis. Dallas Fed Staff Papers 20.

- [5] May RM, Levin SA, Sugihara G (2008) Complex systems: Ecology for bankers. Nature 451:893–895.

- [6] Schweitzer F et al. (2009) Economic networks: The new challenges. Science 325:422–425.

- [7] Helbing D (2013) Globally networked risks and how to respond. Nature 497:51–59.

- [8] Battiston S et al. (2016) Complexity theory and financial regulation. Science 351:818–819.

- [9] Beaupain R, Durré A (2008) The interday and intraday patterns of the overnight market: Evidence from an electronic platform. ECB W. P. 988.

- [10] Cifuentes R, Ferrucci G, Shin HS (2005) Liquidity risk and contagion. J Eur Econ Assoc 3:556–566.

- [11] Huang X, Vodenska I, Havlin S, Stanley HE (2013) Cascading failures in bi-partite graphs: model for systemic risk propagation. Sci Rep 3:1219.

- [12] Upper C, Worms A (2004) Estimating bilateral exposures in the German interbank market: Is there a danger of contagion? Europ Econ Rev 48:827 – 849.

- [13] Elsinger H, Lehar A, Summer M (2006) Risk assessment for banking systems. Manage Sci 52:1301–1314.

- [14] Lelyveld Iv, Liedorp F (2006) Interbank contagion in the dutch banking sector: A sensitivity analysis. Int J Cent Bank 2:99–133.

- [15] Cont R, Moussa A, Santos EB (2013) Network structure and systemic risk in banking systems in Handbook on Systemic Risk, eds. Fouque JP, Langsam JA. (Cambridge University Press, New York).

- [16] Bardoscia M, Battiston S, Caccioli F, Caldarelli G (2017) Pathways towards instability in financial networks. Nat Commun 8:14416.

- [17] Nier E, Yang J, Yorulmazer T, Alentorn A (2007) Network models and financial stability. J Econ Dyn Control 31:2033–2060.

- [18] Gai P, Kapadia S (2010) Contagion in financial networks. Proc R Soc Lond A Math Phys Sci 466:2401–2423.

- [19] Haldane AG, May RM (2011) Systemic risk in banking ecosystems. Nature 469:351–355.

- [20] Tedeschi G, Mazloumian A, Gallegati M, Helbing D (2013) Bankruptcy cascades in interbank markets. PLOS ONE 7:1–10.

- [21] Brummitt CD, Kobayashi T (2015) Cascades in multiplex financial networks with debts of different seniority. Phys Rev E 91:062813.

- [22] Burkholz R, Leduc MV, Garas A, Schweitzer F (2016) Systemic risk in multiplex networks with asymmetric coupling and threshold feedback. Physica D 323:64–72.

- [23] Caccioli F, Farmer JD, Foti N, Rockmore D (2015) Overlapping portfolios, contagion, and financial stability. J Econ Dyn Control 51:50–63.

- [24] Iori G et al. (2015) Networked relationships in the e-MID interbank market: A trading model with memory. J Econ Dyn Control 50:98–116.

- [25] Finger, K, Fricke, D, Lux (2013) Network analysis of the e-MID overnight money market: the informational value of different aggregation levels for intrinsic dynamic processes Comput Manag Sci 10:187–211.

- [26] Battiston S, Caldarelli G, May RM, Roukny T, Stiglitz JE (2016) The price of complexity in financial networks. Proc Natl Acad Sci USA 113:10031–10036.

- [27] Boss M, Elsinger H, Summer M, Thurner S (2004) Network topology of the interbank market. Quant Finance 4:677–684.

- [28] Soramäki K, Bech ML, Arnold J, Glass RJ, Beyeler WE (2007) The topology of interbank payment flows. Physica A 379:317–333.

- [29] Iori G, De Masi G, Precup OV, Gabbi G, Caldarelli G (2008) A network analysis of the Italian overnight money market. J Econ Dyn Control 32:259–278.

- [30] Imakubo K, Soejima Y (2010) The transaction network in Japan’s interbank money markets. Bank Japan Monet Econ Stud 28:107–150.

- [31] http://www.e-mid.it/.

- [32] Cattuto C et al. (2010) Dynamics of person-to-person interactions from distributed RFID sensor networks. PLOS ONE 5:1–9.

- [33] Starnini M, Baronchelli A, Pastor-Satorras R (2013) Modeling human dynamics of face-to-face interaction networks. Phys Rev Lett 110:168701.

- [34] Schläpfer M et al. (2014) The scaling of human interactions with city size. J R Soc Interface 11:20130789.

- [35] Barucca P, Lillo F (2015) The organization of the interbank network and how ECB unconventional measures affected the e-MID overnight market. arXiv:1511.08068.

- [36] https://graph-tool.skewed.de/.

- [37] Estrada E, Rodríguez-Velázquez JA (2005) Spectral measures of bipartivity in complex networks. Phys Rev E 72:046105.

- [38] Bettencourt LM, Lobo J, Helbing D, Kühnert C, West GB (2007) Growth, innovation, scaling, and the pace of life in cities. Proc Natl Acad Sci USA 104:7301–7306.

- [39] Bettencourt LM (2013) The origins of scaling in cities. Science 340:1438–1441.

- [40] Pan W, Ghoshal G, Krumme C, Cebrian M, Pentland A (2013) Urban characteristics attributable to density-driven tie formation. Nat Commun 4:1961.

- [41] Clauset A, Shalizi CR, Newman ME (2009) Power-law distributions in empirical data. SIAM REV 51:661–703.

- [42] http://tuvalu.santafe.edu/~aaronc/powerlaws/.

- [43] Sornette D (2006) Critical phenomena in natural sciences: Chaos, fractals, selforganization and disorder: Concepts and tools. (Springer).

- [44] Weibull W (1951) A statistical distribution of wide applicability. J APPL MECH-T ASME 103:293–297.

- [45] Song C, Koren T, Wang P, Barabási AL (2010) Modelling the scaling properties of human mobility. Nat Phys 6:818–823.

- [46] Caldarelli G, Capocci A, De Los Rios P, Muñoz MA (2002) Scale-free networks from varying vertex intrinsic fitness. Phys Rev Lett 89:258702.

- [47] De Masi G, Iori G, Caldarelli G (2006) Fitness model for the Italian interbank money market. Phys Rev E 74:066112.

- [48] Boguñá M, Pastor-Satorras R (2003) Class of correlated random networks with hidden variables. Phys Rev E 68:036112.

- [49] Gautreau A, Barrat A, Barthélemy M (2009) Microdynamics in stationary complex networks. Proc Natl Acad Sci USA 106:8847–8852.

- [50] Squartini T, van Lelyveld I, Garlaschelli D (2013) Early-warning signals of topological collapse in interbank networks. Sci Rep 3:3357.

- [51] Mastrandrea R, Squartini T, Fagiolo G, Garlaschelli D (2014) Enhanced reconstruction of weighted networks from strengths and degrees. New J Phys 16:043022.

S1 Fitting procedure for the interval distribution

As shown in Fig. 2c, the empirical distribution of transaction interval for each bank pair does not follow a power law. We instead find that the interval distribution nicely fits a Weibull distribution for , where denotes a cutoff value.

The complementary cumulative distribution function (CCDF) of a Weibull distribution [1] is given by

| (S1) |

where and are parameters. Distribution can also be written as , where is the total number of interval values observed, and is the rank of interval length (i.e., is the number of observed interval values such that ). By taking the logarithm of , we obtain the following expression [2]:

| (S2) |

where represents the interval length whose rank is (i.e., , and is defined as . We use Eq. (S2) to find and that give the best fit to a Weibull distribution. We introduce , the logged rank of cutoff value , and estimate parameters for a subset of the observed values of , in a similar way as is done in the standard estimation procedure for a power-law exponent [3]. The cutoff corresponds to the -th largest interval length. Parameters , , and are determined as follows.

-

1.

For a given pair , estimate in (S2) by the ordinary least squares (OLS). Repeat this for sufficiently many values of (we set because the tail of the empirical distribution of is apparently heavier than that of an exponential distribution). The estimate of is denoted by .

-

2.

For given in step 1, find the optimal value of , denoted by , such that the coefficient of determination for the OLS regression is maximized, in which case . Let denote the maximum of for a given .

-

3.

By repeating steps 1 and 2 for all the predefined values of , find the optimal cutoff value . In the end, the estimates of the parameters are given by , , and .

Figure S1a illustrates the determination of the optimal log-rank cutoff . The inset of Fig. 2c in the main text shows the OLS fit to (S2) when (note that corresponds to in that figure). Once is determined, it is straightforward to obtain the corresponding cutoff . Figure S1b verifies the goodness of fit between the empirical CCDF and the estimated Weibull distribution.

S2 Analytical solution for the fitness model with a finite size effect

S2.1 Relationship between and

As we described in the main text, we assume that initially there are many isolated nodes. Node is assigned a fitness which is drawn from density .

The probability of edge formation between two nodes and is denoted by . We define as the number of nodes connected with at least one edge and as the total number of edges in a network. We express and as functions of :

| (S3) |

where is the probability of a randomly chosen node being isolated (i.e., no edges attached) and is the average degree over all nodes including isolated ones. Thus, to obtain the functional forms of and , we need to get the functional forms of and . In the following, we first derive the functional forms of and in a general setting. Then, we will restrict our attention to the case with (i.e., a uniform distribution) and to explain the empirical superlinear relation between and in the same specification as in the main text.

S2.2 Average degree of networks including isolated nodes,

Given the fitnesses of all nodes , the probability that node has degree is

| (S4) |

where is the -element of the adjacency matrix and is the th column vector. Function denotes the Kronecker delta. Let us redefine a product term in the square bracket of (S4) as

| (S5) |

Since is the convolution of , its generating function

| (S6) |

is decomposed as

| (S7) |

where is the generating function of , given by

| (S8) |

Degree distribution is defined by the probability that node has degree and is related to such that

| (S9) |

where we define and . Therefore, differentiation of with respect to gives the average degree :

| (S10) |

From Eqs. (S5) and (S8), we have . It follows that

| (S11) | |||

| (S12) |

Substituting these into Eq. (S10) leads to

| (S13) |

It should be noted that (S13) is equivalent to Eq. (21) of Ref. [4].

S2.3 Probability of node isolation,

From (S9), the probability of a node being isolated, , is given by

| (S14) |

S2.4 Special case: and

Substituting and into Eq. (S13) gives

| (S15) |

Similarly, substituting the same conditions into Eq. (S14) gives

| (S16) |

By rewriting the integrand as , we have

| (S17) |

where is the beta function and () is the incomplete beta function. Combining these results with Eq. (S3), we end up with

| (S18) |

If is sufficiently large, then and thereby and . Therefore, the solution is consistent with that of the previous studies [5, 4, 6] in the absence of the finite-size effect.

S3 Dynamics of weights

S3.1 Empirical observation

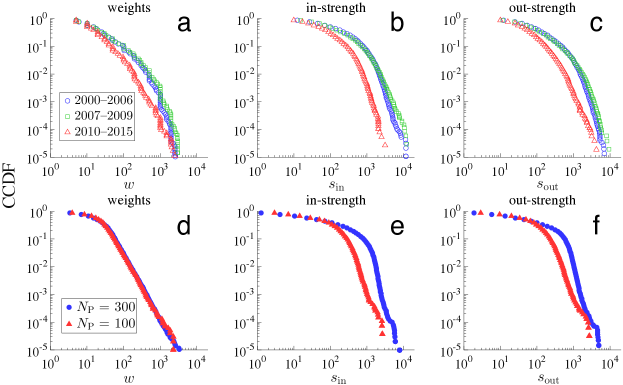

On top of the edge dynamics that we discussed in the main text, the dynamics of edge weights also exhibits specific patterns. Let us define the weight of an edge, , as the total amount of funds transferred from bank to on day . We define the growth rate of edge weights as for bank pair such that [7]. The distribution of , aggregated over all pairs and all , exhibits a symmetric triangular shape with a distinct peak at 0 (Fig. S2a). The shape of the distribution indicates that a large fraction of bank pairs do not change the amount of funds when they keep trading, and if they change the amount, the rate of change will be typically small. A similar sort of triangular-shaped distribution of the growth rate of weights has also been found in networks of email exchanges [8], airlines [7] and cattle trades between stock farming facilities [9].

S3.2 Model of weight dynamics

To reproduce the dynamics of edge weights, we add the following step to the model. Let us consider the edge between and formed in day . If there is an edge from to in day , then the edge weights in day is given by

| (S19) |

where random variable takes different values across bank pairs and are assumed to follow a power-law distribution with exponent to maximize the fit to (Fig. S2) and the empirical weight distribution (Fig. S3 a–c). Positive constant is introduced to match the scale of edge weights with that of the data (i.e., millions of euros). On the other hand, if there is no edge from to in day but there is in day , then

| (S20) |

Any non-adjacent pairs has .

We set the weight parameters as to fit and the simulated weight distributions with the empirical ones, respectively. Figures S2b and S3d–f show that our model of weight dynamics successfully replicates the empirical distributions.

![[Uncaptioned image]](/html/1703.10832/assets/x10.png)

| All | 2000–2006 | 2007–2009 | 2010–2015 | |

| Pure lender | 0.556 | 0.553 | 0.571 | 0.558 |

| Pure borrower | 0.335 | 0.300 | 0.318 | 0.380 |

| Others | 0.110 | 0.147 | 0.111 | 0.062 |

| “Pure lender" (“pure borrower") denotes the banks that lend to (borrow from) | ||||

| but never borrow from (lend to) other banks. | ||||

References

- [1] Weibull W (1951) A statistical distribution of wide applicability. J APPL MECH-T ASME 103:293–297.

- [2] Sornette D (2006) Critical phenomena in natural sciences: Chaos, fractals, selforganization and disorder: Concepts and tools. (Springer).

- [3] Clauset A, Shalizi CR, Newman ME (2009) Power-law distributions in empirical data. SIAM Review 51:661–703.

- [4] Boguñá M, Pastor-Satorras R (2003) Class of correlated random networks with hidden variables. Phys Rev E 68:036112.

- [5] Caldarelli G, Capocci A, De Los Rios P, Muñoz MA (2002) Scale-free networks from varying vertex intrinsic fitness. Phys Rev Lett 89:258702.

- [6] De Masi G, Iori G, Caldarelli G (2006) Fitness model for the Italian interbank money market. Phys Rev E 74:066112.

- [7] Gautreau A, Barrat A, Barthélemy M (2009) Microdynamics in stationary complex networks. Proc Natl Acad Sci USA 106:8847–8852.

- [8] Godoy-Lorite A, Guimera R, Sales-Pardo M (2016) Long-term evolution of email networks: Statistical regularities, predictability and stability of social behaviors. PLOS ONE 11:e0146113.

- [9] Bajardi P, Barrat A, Natale F, Savini L, Colizza V (2011) Dynamical patterns of cattle trade movements. PLOS ONE 6:1–19.

- [10] http://tuvalu.santafe.edu/~aaronc/powerlaws/.