Quadratic approximation of slow factor of volatility in a Multi-factor Stochastic volatility Model

Abstract.

In the present work, we propose a new multifactor stochastic volatility model in which slow factor of volatility is approximated by a parabolic arc. We retain ourselves to the perturbation technique to obtain approximate expression for European option prices. We introduce the notion of modified Black-Scholes price. We obtain a simplified expression for European option price which is perturbed around the modified Black-Scholes price and have also obtained the expression of modified price in terms of Black-Scholes price.

Keywords: Multifactor stochastic volatility; Slow volatility factor; Quadratic approximation; Volatility model; Option pricing

AMS subject classifications: 34E13, 60H15, 60H30, 60J60, 91B70, 91G20, 91G80

1. Introduction

Stochastic volatility models are prominent in option valuation literature as they are able to coalesce many stylized facts about volatility namely volatility smile, mean reversion, volatility clustering etc.(eg. see Bakshi, Cao and Chen , Bates , Chernov and Ghysels , Gatheral etc.). Single factor stochastic volatility models are being discussed in many papers(eg. see Hull and white , Stein-Stein , Heston , Ball-Roma etc.). Volatility smile can be generated by single factor stochastic volatility models but its time varying nature remains unexplained by these models.

Christoffersen et al. strongly argued the need of multifactor stochastic volatility models to capture some of the most salient stylized facts in index options. They demonstrated the role of multiple factors in capturing term structure and moneyness effects.

Multifactor stochastic volatility models are much recent and very significant in option valuation literature. Alizadeh et al. found the evidence of two factors in volatility with one highly persistent factor and other quickly mean reverting factor. Extending this idea, Fouque et al. proposed a two factor stochastic volatility model with one fast mean reverting factor and another slowly varying factor. They have showed that slow varying volatility factor is essential for options with longer maturity and used perturbation analysis in context of pricing options. For more details one can refer Fouque et al. . As persistence of volatility should be given importance and must be incorporated in any volatility model (Robert F Engle et al. ) and knowing the fact that multifactor stochastic volatility models give better results for the options with medium-longer maturity (Fatone et al. ), the slow factor of volatility, which is highly persistent, is important and its dynamics can not be ignored. Also in perturbation analysis given by Fouque et al. the approximate option price depends upon slow factor of volatility but independent of fast factor.

We propose a multifactor model to give importance to slow factor of volatility by taking it mean reverting and approximating it by a parabolic arc. Also, with this model we have derived the pricing formula for European call options. We have also introduced the notion of modified Black Scholes operator.

The paper is organised as follows: In Section we introduce the multifactor stochastic volatility model. Option pricing equation and asymptotic expansion of price is discussed in Section and respectively. Approximate price of European option is given in Section and Section includes the conclusion.

2. Model under consideration

Let be the price of underlying asset (non dividend paying), be the risk neutral probability measure and r be the risk free rate of interest. Under , the dynamics of be given by a diffusion process as:

| (1) |

Here,

| (2) |

is stochastic volatility driven by two factors and which are respectively the fast scale and slow scale factors of volatility. is standard Brownian motion. We consider the dynamics of fast volatility factor as given in Fouque et al. :

| (3) |

which is an Ornstein-Uhlenbeck (OU) process with long run distribution and is reverting on the short time scale around its long run mean value with as its rate of mean reversion. Its volatility of volatility (vol-vol) parameter is . is standard Brownian motion.

and have the correlation structure:

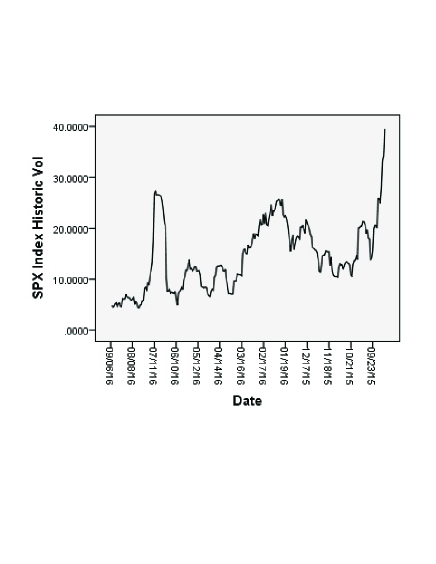

Where, represents the correlation between two standard Brownian motions. Slow factor of volatility is persistent and empirically it is mean reverting too. But mean reversion can be clearly observed for long term options. We take quadratic arc approximation to capture slow volatility factor given by:

| (4) |

where represents the error term in the approximation of with . We can justify this approximation of persistent factor of volatility, from historic volatility data given in

fig.1

We are also justifying this choice of approximation by considering slow volatility factor to follow a diffusion process:

| (5) |

where is also a standard Brownian motion having the correlation structure with and as :

where the correlation coefficients and are such that and for the positive definiteness of the covariance matrix of three Brownian motions.

Here, follows Ornstein-Uhlenbeck (OU)process with long run distribution and is reverting on long time scale around its long run mean value . The rate of mean reversion for is and its vol-vol parameter is .

On solving, becomes:

| (6) |

comparing it with , we obtain

and

Here, represents the initial value of slow factor of volatility. To assure that we assume that . is the truncation error and involving , is randomness in the value of slow factor of volatility .

We are assuming here that the error term is negligible as truncation error can be neglected and vol-vol parameter of slow factor of volatility can be neglected under parabolic approximation.

The approximated value of is a function of t. also,

| (7) |

and

| (8) |

where,

.

These expressions will be needed for pricing in the upcoming sections. So in the nutshell, our multifactor stochastic volatility model under risk neutral probability measure , which is already chosen by the market is:

| (9) |

where,

which we have obtained by considering diffusion process

for . Next we’ll write the pricing equation for European options.

3. Pricing Equation

The price of European call option with payoff function under the risk neutral probability measure is conditional expectation of discounted payoff given as:

| (10) |

By Feynman-Kac formula, satisfies the following parabolic PDE:

| (11) |

with the boundary condition

where the operator is given by:

| (12) |

with

| (13) |

| (14) |

and

| (15) |

On putting the value of and from and in and and on solving, we get

| (16) |

and

| (17) | ||||

where, is given by

From and we have,

| (18) |

This is the required pricing equation where is the solution of above parabolic PDE.

4. Asymptotic Expansion

For asymptotic expansion, expand in powers of , i.e.

| (19) |

Using it in gives

| (20) |

Similar expansion is considered in Fouque et al. for single factor and for two factors of volatility respectively. We have considered the expansion in powers of only because we have approximated the slow factor of volatility.

Terms of order :

| (21) |

which is independent of but depending on , the slow factor of volatility.

Terms of order :

as is independent of

| (22) |

which is again independent of but depending on , the slow factor of volatility.

Terms of order :

| (23) |

is independent of and it is Poisson equation in with respect to with Fredholm solvability condition:

| (24) |

where, is the average of w.r.t . For simplification, we neglect the error term involving truncation and randomness in assuming and vol-vol parameter of . Therefore, is reduced to

take,

with and

| (25) |

and,

| (26) |

where,

which is a function of slow factor of volatility. We call as modified Black-Scholes operator with volatility . So, in , is modified Black-Scholes price. After some calculation, expression of in terms of Black-Scholes price is given as:

| (27) |

where, is classical Black-Schole price and is the constant s.t. for . Equality holds at maturity to satisfy the boundary condition

To approximate the value of , we consider the numerical value of which can be calculated from options data. We consider SP index option data with option starting from January maturing on June . For different moneyness,we got

Also, from ,

| (28) |

Terms of order :

which is Poisson equation in with respect to with Fredholm solvability condition:

Considering from and after solving, we get

| (29) |

where,

On solving,

| (30) |

For first order approximation, we need the expression for along with . With some simplification, one can easily verify that the term

| (31) |

is the unique solution of with boundary condition

where is given by .

5. Approximate Option Price

From the above calculation we get the First order approximation of option price as

i.e.

| (32) |

where is given by

Now, can be written as:

| (33) |

Here,

| (34) |

and is the solution of

| (35) |

is given by .

Equation gives the required first order approximation of option price

where,

| (36) |

such that converges to zero at maturity.

We name as modification factor. We are interested in its value. Numerically, if we take , for and , we get . It will significantly improve the pricing. We have used the market data to obtain these parameters.

The accuracy of this first order approximation and calibration of effective stochastic volatility parameter can be done as already explained in Fouque et al. .

6. Conclusion

Slow factor of volatility is persistent and its dynamics can’t be ignored. No doubt it is stochastic, but approximating it with a deterministic arc makes the calculation easy and give a simplified expression for the price of European call option. This price is perturbed around the modified Black-Scholes price. We have also given the expression of modified price in terms of Black-Scholes price and have calculated the modification factor using SP index options data.

References

- [1] Alizadeh,S., M.Brandt and F.Diebold(Range Based Estimation in Stochastic Volatility) Journal of Finance Vol.57, 1047 – 1091, 2002.

- [2] Bakshi,G., C.Cao and Z.Chen(Empirical Performance of Alternative Option Pricing Models) The Journal of Finance Vol.52, No.5, 2003 – 2049, 1997.

- [3] Ball,C.A. and A.Roma(Stochastic Volatility Option Pricing) Journal of Financial and Quantitative Analysis Vol.29, 589 – 607, 1994.

- [4] Bates,D.S.(Post-’87 Crash Fears in the S&P500 Futures Option Market) Journal of Econometrics Vol.94, 2003 – 2049, 1997.

- [5] Christoffersen,P., S.Heston and K.Jacobs(The Shape and Term Structure of Index Option Smirk: Why Multifactor Stochastic Volatility Models Work So Well) Management Science Vol.55, 1914 – 1932, 2009.

- [6] Chernov, M. and E.Ghysels(A Study towards a Unified Approach to the Joint Estimation of Objective and Risk Neutral Measures for the Purpose of Option Valuation) Management Science Vol.56, No.3, 407 – 458, 2000.

- [7] Engle, R.F. and A.J.Patton (What good is a volatility model) Quantitative Finance Vol.1, 237 – 245, 2001.

- [8] Fouque,J.P., G.Papnicolau, K.R.Sircar and K.Solna(Multiscale Stochastic Volatility Asymptotics) Multiscale Modeling and Simulation Vol.2, No.1, 22 – 42, 2003a.

- [9] Fouque,J.P., G.Papnicolau, K.R.Sircar and K.Solna(Singular Perturbations in Option Pricing) SIAM Journal on Applied Mathematics Vol.63, No.5, 1648 – 1665, 2003b.

- [10] Fouque,J.P., G.Papnicolau, K.R.Sircar and K.Solna(Multiscale Stochastic Volatility for Equity, Interest rate and Credit Derivatives) Cambridge University Press, 2011.

- [11] Heston,S.(A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options) The Review of Financial Studies Vol.6, Issue 2, 327 – 343 , 1993

- [12] Hull,J., and A.White(The Pricing of Options on Assets with Stochastic Volatility) Journal of Finance Vol.42, 281 – 300, 1987.

- [13] J.Gatheral(The Volatility Surface: A Practitioner’s Guide) Hoboken, NJ: Wiley., 2006.

- [14] Stein,E.M. and J.C.Stein(Stock Price Distributions with Stochastic Volatility: An Analytic Approach) The Review of Financial Studies Vol.4, No.4, 727 – 752, 1991.