An orthogonal basis expansion method for solving path-independent stochastic differential equations

Abstract

In this article, we present an orthogonal basis expansion method for solving stochastic differential equations with a path-independent solution of the form . For this purpose, we define a Hilbert space and construct an orthogonal basis for this inner product space with the aid of 2D-Hermite polynomials. With considering as orthogonal basis expansion, this method is implemented and the expansion coefficients are obtained by solving a system of nonlinear integro-differential equations. The strength of such a method is that expectation and variance of the solution is computed by these coefficients directly. Eventually, numerical results demonstrate its validity and efficiency in comparison with other numerical methods.

keywords:

Stochastic Differential Equation , 2-D Hermite Polynomials , Orthogonal Basis ExpansionMSC:

[2010] 65L60 , 34B161 Introduction

A stochastic process on a filtered probability space is an It process if it satisfies the following stochastic differential equation (SDE):

| (1) |

where is a standard Wiener process, the drift function and the volatility function are Borel measurable and locally bounded. In addition, we assume and are under linear growth and locally Lipschits conditions:

these conditions imply equation (1) has a unique t-continuous solution adapted to filtration generated by the Wiener process ( see [1], [2], [3]) and

| (2) |

Also for simplicity is considered a non-random real number.

In the general case It process depends on the history of Wiener path, where , in the special case that depends only on (i.e,), it is called a path-independent solution of equation (1). Under some additional conditions for drift and volatility functions, if we have

Stochastic differential equations (SDEs) play a key role in modeling of phenomena that arise in vast variety of application areas including including Finance [5], Biology [6], Chemistry [7] and Physics[8]. Due to the fact that finding the analytical solution of SDEs is not easy, except for some special cases, the numerical simulation methods has become a favorite topic in the study of SDEs and devoted a lot of attention of researchers in recent years. At the present time several numerical methods such as Euler Maruyama (E.M.) , Milstein [9], chain Rule [11] and also stochastic Runge-Kutta methods[12] has been proposed.

In this paper, we propose an orthogonal basis expansion method for solving SDEs with path-independent solutions. The orthogonal basis expansion method is one of the most popular topics in functional analysis and widely implemented for solving Partial Differential Equations, Ordinary Differential Equations, and Integral Equations.

For this purpose, we define a Hilbert space appropriately and assume that path-independent solution of equation(1) belongs to this space. Then we construct an orthogonal basis For this inner product space. Afterward, we consider in the form of orthogonal basis expansion. Finally, for finding the coefficients of this expansion, we reduce to a system of nonlinear integro-differential equations. The properties of this represented method are similar to Wiener Chaos Expansion method (WCE) that is also referred to Hermite polynomial chaos expansion. (see, e.g. [13], [14], [15] and the references therein). There is a fundamental different between these two methods in basis construction. Introduced basis in WCE method is multi-variable Hermite polynomials of the Gaussian random process that have been generated by tensor product but in this new method, we represent 2-dimensional Hermite polynomials.

This paper is organized as follows. In section 2, we outline the theoretical foundation of stochastic Hermite polynomials as a basis and their properties. Section 3 constructs orthogonal basis expansion for functions of Wiener stochastic process and describes the general procedure by applying orthogonal basis expansion method. In addition, we find basic stochastic indicators of the solution such as expectation and variance. In section 4, numerical solution of some particular and well-known types of SDEs based on orthogonal basis expansion method is considered. Examples are surveyed and their exact solutions with both these solutions and other stochastic numerical simulation like predictor-corrector Euler Maruyama (E.M.) and method are compared. Finally, a brief conclusion is stated in Section 5.

2 Introducing a Stochastic Orthogonal Basis

Consider the space of square integrable functions with respect to the time-dependent Gaussian weight function :

| (4) |

where

| (5) |

Furthermore, the inner product and norm of this Hilbert space are defined as usual:

| (6) |

| (7) |

Consider the Hermite polynomials

| (8) |

The -th order monic Hermite polynomials are reached by substituting in (8):

| (9) |

In dimensional, -th order Hermite polynomials ([16] and [17]) are defined as follows:

| (10) |

where and it can be observed that,

The monic Hermite polynomials are generated by a three-term recursion relationship:

| (14) |

From (14), we can get a similar recursion relationship of the dimensional Hermite polynomials:

| (18) |

For initial condition , we have:

| (19) |

Therefore, considering (19), for , it is concluded that

| (20) |

Thus, using recursion formula (18), some of these Hermite polynomials compute as follows:

Since the classical Hermite polynomials of standard Gaussian random variables are orthogonal, we have:

| (21) | ||||

Thus, the sequence is an orthogonal set in :

| (22) |

Similar to the other orthogonal polynomials, 2-D Hermite polynomials enjoy a generating function [16]:

| (23) |

The generating function (23) is a crucial tool for studying the stochastic Hermite polynomials properties. We will utilize it frequently in our later derivations and results. If we replace with the Wiener process , this stochastic process is named Exponential Martingale [16] [1]. Applying ’s formula on this process, we obtain the following SDE:

| (24) |

Substituting for the Exponential Martingale in (24), we can infer the following theorem [16] that is well-known as the stochastic calculus with the stochastic Hermite polynomials.

Theorem 1

Let be a Wiener process and be the order stochastic Hermite polynomial in terms of . For each and , we have:

| (25) |

This theorem implies that the stochastic Hermite polynomials with respect to the filtration and measure are Martingale processes.

According to [18, 19], for a given positive weight function defined in time interval , there

exists a unique family of monic Orthogonal polynomials as basis of generated by a three-term recursion relationship such that:

| (26) |

The sequence is also an orthogonal set on the space For each , we possess:

Since the linear span of polynomials for are dense in , in order to indicate that is also an orthogonal basis, it would be enough to demonstrate all these polynomials can be generated by them.

Theorem 2

Each polynomial in terms of variables and can be generated by the orthogonal set .

proof: For each polynomial set , proof is done by induction on . For , since , we have:

Similarly, for , since , we have:

Assume for we have:

We must show that the same formula is true for :

On the other hand, using recursive equality (18), we get:

Afterward, we have:

But since and , the following equality is obtained:

and consequently the proof is completed by induction.

Because is an orthogonal basis in , therefore for any that belongs to this space we have :

| (27) |

where

| (28) |

Defining and applying (22), we obtain:

| (29) |

3 An expansion method for solving SDEs

In this section, we consider the general form of the stochastic differential equation:

| (30) |

where the drift and the diffusion coefficients and belong to and , respectively and we assume that relation (3) holds therefore the equation (30) has a unique path-independent solution. According to the (29), stochastic process yields in the following expansion:

| (31) |

Because is a normal random variable with mean zero and variance , we could obtain as below:

| (32) |

Consequently, the definition of and parseval’s equality lead to calculating the expectation and variance of the stochastic process in each point of time interval by corresponding expansion coefficients:

| (33) |

For each two It process , we have the following equality named It product formula:

Now as the first step to find the unknown coefficients , we apply It product formula for equations(30) and (25).

| (34) | |||

Rewriting this equation in integral form and taking expectation, we infer the following equation:

| (35) |

As a matter of fact, since is an integral and also a martingale process, its expectation is equal to zero. Afterward, employing the Fubini’s theorem which allows the order of integration to be changed in iterated integrals we have;

| (36) |

Thereby, considering Eq.(31) and taking derivation, we reach a system of integro-differential equations:

| (37) |

and so:

| (38) |

For solving this system of equations, we need to extract coefficients ,() as initial conditions. For , we get , and therefore . For , since is continuous we have:

Applying L’Hopital’s Rule into computing function limits, can be calculated as below:

| (39) |

So that according to the Euler approximation method has been put in place of . Afterwards, we consider a finite dimensional case of this system of integro-differential equations to compute truncation form of as follows:

| (40) |

After discretization of the time interval with , where , the subsequence equality is achieved as

But due to the singularity of the right side of this system of integro-differential equations in , we can not perform Rung-Kutta method from . To find a significant approximation of and in order to overcome the singularity in , we use the Euler method. Substituting for , the preceding equation converts to a system of integro-differential equations:

The numerical solution of final system(38), can be done with various one step methods as Euler and Rung- kutta of different orders[20]. In this paper, the numerical solution is computed based on second-order Rung-Kutta method.

4 Analytical and numerical results

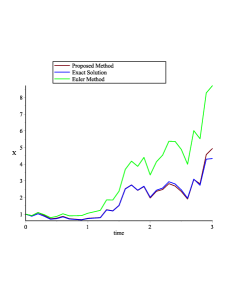

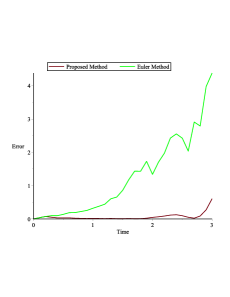

Example 1 Consider the Geometric Brownian Motion (GBM) model

| (41) |

where and are the time dependent and constant parameter, respectively. From the system of equations (38), we obtain the following equations:

| (42) | ||||

It can be verified that is the explicit solution of this system. Therefore,

| (43) |

From (23), we have , and finally the exact solution of the stock pricing model equation is:

In a particular case the obtained solution is the exponential martingale process.

| N=30 | N=40 | ||||||

|---|---|---|---|---|---|---|---|

| T | EM | PM | Exact | EM | PM | Exact | |

| 3 | 8.276397 | 4.575074 | 4.301673 | 13.521179 | 7.813891 | 7.848716 | |

| 2 | 1.410893 | 0.832558 | 0.855598 | 2.129019 | 1.35756 | 1.363187 | |

| 1.5 | 1.850382 | 1.201318 | 1.192680 | 1.0618345 | 0.762551 | 0.765961 | |

| 1 | 0.5971905 | 0.462382 | 0.465634 | 0.8095762 | 0.637728 | 0.638863 |

|

|

| a | b |

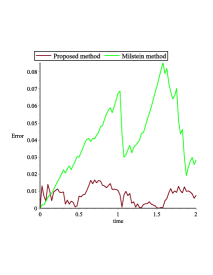

Example 2 Consider Cox-Ingersoll-Ross investment Model in the following special case

| (44) |

where and . By applying It formula on , we reach to the equation the prominent stochastic model Ornschten-Uhlenberg (Langevin process):

| (45) |

The exact solution of this equation by applying It formula on is:

| (46) |

In order to solve the equation (45) by Galerkin method based on 2-D Hermite polynomials, we put . Now multiplying Eq.(45) by , and taking expectation and derivation respectively, we obtain the following O.D.E. similar to (37):

| (47) |

|

|

| a | b |

Considering different initial conditions for indices , we could find by solving some equations in cases , and , respectively:

Consequently, answers of these equations are

Finally, we get the following equation:

| (48) |

Figure 2 depicts a different numerical example of this model with stochastic differential equation

| (49) |

with initial value and also absolute error for with points.

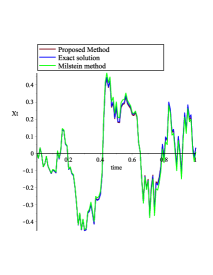

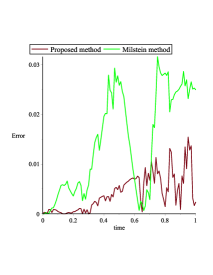

Example 3 Consider non-linear time dependent stochastic differential equation

| (50) |

The exact solution of this equation is The numerical solution of this equation based on proposed method with and is computed and the result is compared with method in Figure 3.

|

|

| a | b |

5 conclusion

In this article, we introduced an orthogonal basis expansion method to solve stochastic differential equations with a pathindependent solution. For a truncated form of the solution, the equation reached a closed nonlinear system of deterministic integro-differential equations for the related coefficients. The orthogonal basis expansion method provided careful analytical formulas for computing statistical moments such as mean and variance, which in this paper even the statistical moments up to the fourth order, was found. In the numerical experiments with stochastic equations, we compared the solution accuracy and the computational effectiveness of the orthogonal basis expansion and other stochastic numerical methods like the Monte Carlo (MC), E.M. and Milstein method.

References

References

- [1] B. K. ksendal: Stochastic Differential Equations: An Introduction with Applications, 4th ed., Springer, (1995).

- [2] Arnold, L.: Stochastic Differential Equations: Theory and Applications. John Wiley and Sons, New York (1974).

- [3] P.E. Kloeden, E. Platen.: Numerical Solution of Stochastic Differential Equations, in: Applications of Mathematics, Springer-Verlag, Berlin, (1999).

- [4] Van den Berg, I.:Stochastic differential equations with path-independent solutions. ArXiv e-prints (2012).

- [5] C.Fries.: Mathematical Finance, Theory, Modelling and Implementation.J. Wiley (2007).

- [6] Allen, L.J.S.: An Introduction To Stochastic Processes With Applications to Biology. Pearson Education Inc., Upper Saddle River, New Jersey (2003).

- [7] E. Allen: Modeling with Stochastic Differential Equations, Springer Series, (2007).

- [8] Hayes, J.G., Allen, E.J.: Stochastic point-kinetics equations in nuclear reactor dynamics. Annals of Nuclear Energy, 32 ,(2005), 572-587.

- [9] Sauer, T. : Computational solution of stochastic differential equations. WIREs Comput Stat. doi: 10.1002/wics.1272 (2013).

- [10] Milstein, G.N., Tretyakov, M.V.: Stochastic Numerics for Mathematical Physics. Springer-Verlag, Berlin (2004).

- [11] D. J. Higham: An algorithmic introduction to numerical simulation of stochastic differential equations, SIAM Review 43, 525-546 ,(2001).

- [12] K. Burrage, RM. BurrageHigh: strong order explicit Runge-Kutta methods for stochastic ordinary differential equations, Applied Numerical Mathematics 22, 81-101, (1996).

- [13] R. H. Cameron and W. T. Martin.: The orthogonal development of non-linear functionals in series of Fourier-Hermite functionals. Ann. Math. 48 ,(1947), 385-392.

- [14] J. P. Boyd. :Chebyshev and Fourier Spectral Methods. Dover Publication, New York,(2000).

- [15] Wuan Luo.: Wiener Chaos Expansion and Numerical Solutions of Stochastic Partial Differential Equations. California Institute of Technology Pasadena, California,(2006).

- [16] Lawrence C. Evans.:An Introduction to Stochastic Differential Equations Version 1.2 (2004).

- [17] Schoutens, W.: Stochastic Processes and Orthogonal Polynomials. Lecture Notes in Statist. 146. New York: Springer (2000).

- [18] Shen, J., Tang, T., Wang, L.: Spectral Methods: Algorithms, Analysis and Applications. Springer Series in Computational Mathematics, Vol. 41. Springer-Verlag, Berlin Heidelberg (2011).

- [19] W. Gautschi, Orthogonal polynomials: computation and approximation, Oxford University Press, (2004).

- [20] Frank de Hoog, Richard Weiss.: The Application of Runge-Kutta Schemes to Singular Initial Value Problems. mathematics of computation volume 44, number 169 ,(1985), 93 - 103.