Analysis of Realized Volatility for Nikkei Stock Average on the Tokyo Stock Exchange

Abstract

We calculate realized volatility of the Nikkei Stock Average (Nikkei225) Index on the Tokyo Stock Exchange and investigate the return dynamics. To avoid the bias on the realized volatility from the non-trading hours issue we calculate realized volatility separately in the two trading sessions, i.e. morning and afternoon, of the Tokyo Stock Exchange and find that the microstructure noise decreases the realized volatility at small sampling frequency. Using realized volatility as a proxy of the integrated volatility we standardize returns in the morning and afternoon sessions and investigate the normality of the standardized returns by calculating variance, kurtosis and 6th moment. We find that variance, kurtosis and 6th moment are consistent with those of the standard normal distribution, which indicates that the return dynamics of the Nikkei Stock Average are well described by a Gaussian random process with time-varying volatility.

1 Introduction

Statistical properties of asset returns have been extensively studied and it is found that asset price returns show some universal properties that are not explained well in the framework of the standard Brownian motion. The universal properties are now classified as the stylized facts of asset price returns which includes: fat-tailed return distributions, volatility clustering, long autocorrelation time in absolute returns and so on[1]. To explain the fat-tailed return distribution Mandelbrot introduced a class of stable processes such as stable Paretian[2]. An alternative idea to explain the asset price dynamics was given by Clark who related the volatility variation to volume and suggested to use the subordinated process to the asset price dynamics[3]. The idea for the asset price dynamics by Clark is also called the mixture of distributions hypothesis (MDH). The return process with the MDH does not conflict with major properties observed in asset returns, e.g. volatility clustering, fat-tailed return distributions. Under the MDH, the asset return at discrete time can be described by , where is a variance of the Gaussian distribution and is a standard normal random variable, and this indicates that the asset return process is viewed as a Gaussian random process with time-varying variance (volatility). Let be the conditional return distribution with and the probability distribution of volatility. The unconditional return distribution from this process is obtained by integrating the conditional return distribution and the probability distribution of volatility with respect to volatility, i.e. . Empirical studies suggested that the volatility distributions might be described by the inverse gamma distribution or log-normal distribution[3, 4, 5, 6] with which the unconditional return distributions become fat-tailed distributions.

The verification of the MDH can be made by testing the returns standardized by volatility, . Under the MDH, the standardized returns should behave as , i.e. standard normal random variables. This test has been conducted in the literature[8, 9, 10, 11, 12, 13, 14, 15] and it is shown that the MDH is hold for many cases. For this test it is crucial to use a precise measure of volatility. So far the most precise measure is the realized volatility[7] constructed from high-frequency price data. Under ideal circumstances the realized volatility goes to the integrated volatility in the limit of the infinite sampling frequency. However such circumstances are usually violated and the realized volatilities in empirical cases are biased. There exist two main sources of bias: microstructure noise and non-trading hours. Thus to verify the standard normality of the returns standardized by realized volatility it is important to control such biases. In [14], in order to avoid bias from non-trading hours the MDH is tested separately in morning and afternoon sessions for individual Japanese stocks and it is shown that after removing the finite-sample effect[17] the return dynamics becomes consistent with the MDH[15]. In this paper we focus on the realized volatility of the Nikkei Stock Average index and investigate whether the MDH can also apply for the price dynamics of the Nikkei Stock Average index.

2 Realized Volatility

We assume that the logarithmic price process follows a continuous time stochastic diffusion,

| (1) |

where stands for a standard Brownian motion and is a spot volatility at time . The assumption of a Brownian motion for the logarithmic price process is often used to model stock prices as in the Black-Scholes model[18, 19] and is most widely used to investigate stock price process. Using , the integrated volatility from to is defined by

| (2) |

where stands for the interval to be integrated, e.g. corresponds to one day for the daily integrated volatility.

The realized volatility is designed as a model-free estimate of volatility and constructed as a sum of squared returns[7]. The realized volatility at time is given by

| (3) |

where is the number of returns at sampling frequency , given by . The returns sampled at are given by log-price difference,

| (4) |

for . Eq.(3) goes to the integrated volatility defined by eq.(2) in the limit of . However what we observe in the real financial markets is not the returns given by eq.(4). The asset prices observed in the real financial markets are contaminated with the microstructure noise originating from discrete trading, bid-ask spread and so on. Following Zhou[20] let us assume that the microstructure noise introduces independent noises and the log-price observed in financial markets is given by

| (5) |

where is the observed log-price in the markets which consists of the true log-price and noise . Under this assumption the observed return is given by

| (6) |

where . The realized volatility actually observed at the financial market is obtained as a sum of the squared returns ,

| (7) | |||||

| (8) |

After averaging , we find that the bias in appears as which corresponds to . Thus with independent noise the diverges as . Another bias appeared in the realized volatility is due to the existence of the non-trading hours on the real financial markets. At the Tokyo Stock Exchange domestic stocks are traded in the two trading sessions: (1) morning trading session (MS) from 9:00 to 11:00. (2) afternoon trading session (AS) from 12:30 to 15:00. If we calculate the daily realized volatility without including returns during the non-traded periods it can be underestimated.

In order to avoid the non-trading hours issue we consider two realized volatilities:(i) , realized volatility in the morning session and (ii) , realized volatility in the afternoon session. Since these realized volatilities are calculated separately each volatility does not have bias due to the non-trading hours issue.

3 Normality of the Standardized Return

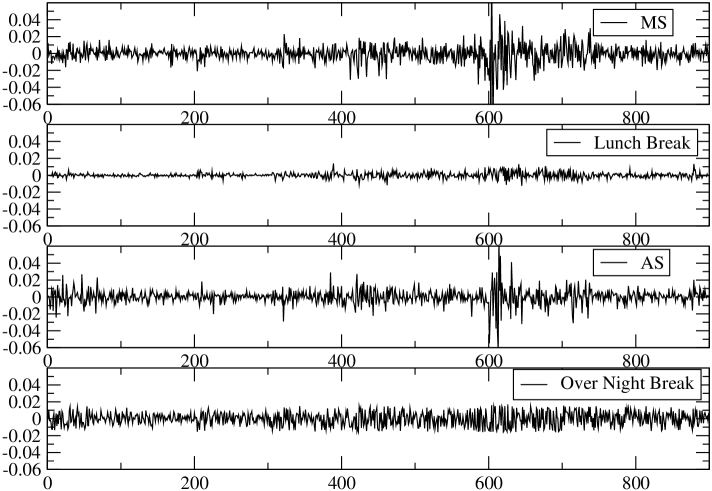

In this study we analyze the high-frequency data of Nikkei Stock Average (Nikkei225) index from May 1, 2006 to December 30, 2009, that corresponds to 900 working days. Figure 1 shows return time series of the Nikkei Stock Average in the different time zones of the Tokyo Stock Exchange.

In each zone the return is calculated by the log-price difference between the beginning and end prices in the corresponding zone. For instance let be the return in the morning session at day . is given by , where is the opening price of the morning session and the closing price of the morning session. Similarly the return in the afternoon session is given by . Moreover the return in the lunch break (LB), is given by and the return in the overnight break (ON), is given by . As seen in the figure returns in the lunch break and overnight break also vary. Variation of returns in the lunch break is small. This is because the lunch break duration takes only 90min. On the other hand considerable variation of returns is seen in the overnight break which has 18 hrs duration. Since returns in both breaks can vary the (daily) realized volatility without including the data in both breaks can not be accurate.

In order to avoid the non-trading hours issue we calculate two realized volatilities in the morning and afternoon session separately. Let be the realized volatility in the morning ( afternoon ) session. Then we analyze standardized returns separately in each session. is given by

| (9) |

where is the i-th intraday return in the MS on day , sampled at min. Similarly, is given by

| (10) |

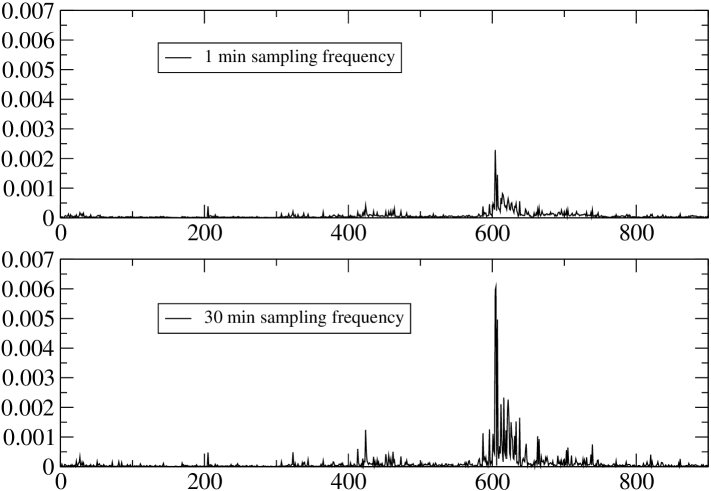

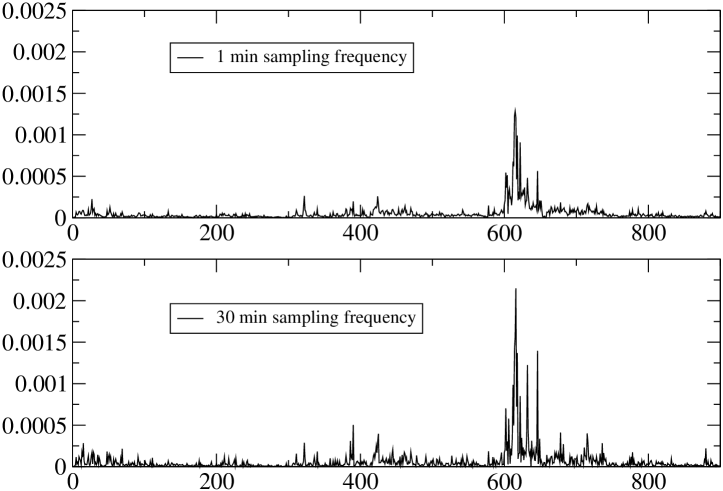

Here is the number of returns generated at sampling frequency during trading sessions. We calculate the realized volatility for . Figure 2 and 3 show the realized volatility in each trading session at and 30 as representative ones.

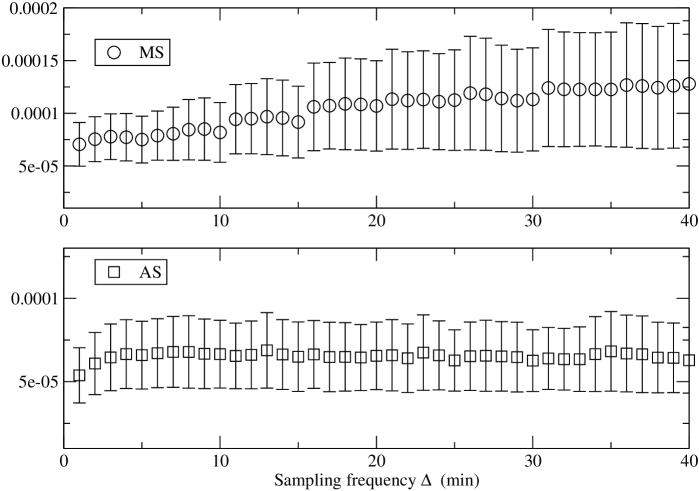

In figure 4 we show the average of realized volatility as a function of the sampling frequency . Such plot is also called volatility signature plot[16] and visualizes the effect of the microstructure noise. It seems that the average realized volatility decreases with the sampling frequency . This is the opposite result to the expectation of eq.(8) and empirical results of individual Japanese stocks[14] where the realized volatility diverges as the sampling frequency decreases. Thus for the Nikkei Stock Average the assumption of the independent noise of eq.(5) does not apply.

4 Normality of Standardized Returns

According to the MDH, let us assume that and are described by

| (11) |

| (12) |

respectively. is an integrated volatility in the morning (afternoon) and and are independent standard normal random variables . Substituting the realized volatility for the integrated volatility we standardize and as and . These standardized returns are expected to be standard normal variables provided that eqs.(11)-(12) are hold. However for the realized volatility constructed from the finite number of intraday returns the standardized return receives the finite-sample effect. Let be a standardized return. The distribution of the standardized return is given by[17]

| (13) |

where is the number of returns used to construct the realized volatility. The indicator function means that if is true and otherwise . Under this distribution the even moments of are also calculated to be[17]

| (14) |

Actually this finite-sample effect on the standardize return has been observed in empirical results[11, 12, 15] and also in the spin model simulation[21].

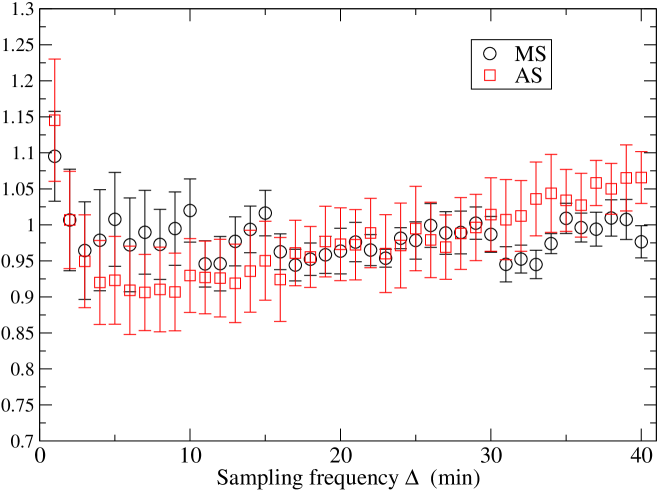

Figure 5 shows the variance of the standardized returns as a function of sampling frequency . Here note that from eq.(14) always takes one, i.e. the variance has no finite-sample effect. As seen in the figure the variance is very close to one through every sampling frequency. Only we see an increase at small , which may indicate the effect of the microstructure noise.

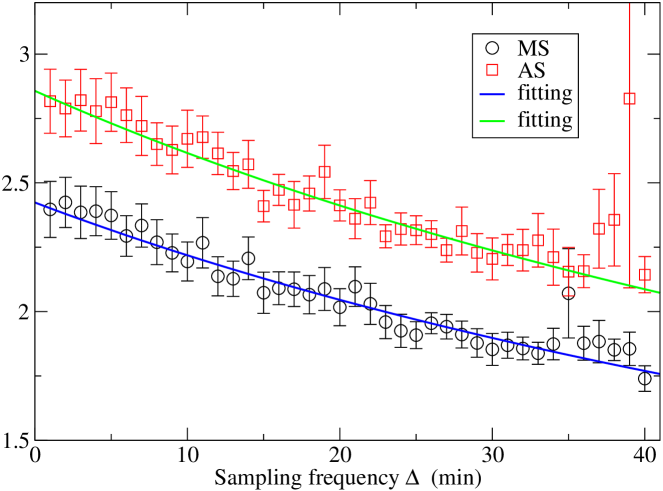

Figure 6 shows the kurtosis as a function of the sampling frequency . It is seen that the kurtosis decreases as the sampling frequency increases as expected from the functional form of the finite-sample effect in eq.(14). This behavior is also observed for individual stocks on the Tokyo Stock Exchange[15]. The solid lines in the figure are results fitted to a fitting function of where and are fitting parameters. corresponds to the kurtosis in the limit of . The fitting results are listed in Table 1. We obtain for the MS(AS). These values are close to 3 expected for the standard normal distributions although the value of the MS deviates slightly from 3.

We further analyze the 6th moment of the standardized returns. The higher moments of the standardized returns have been investigated in the spin financial model where no microstructure noise exists and it has been shown that the behavior of the higher moments with varying is consistent with the finite-sample effect described by eq.(14)[21].

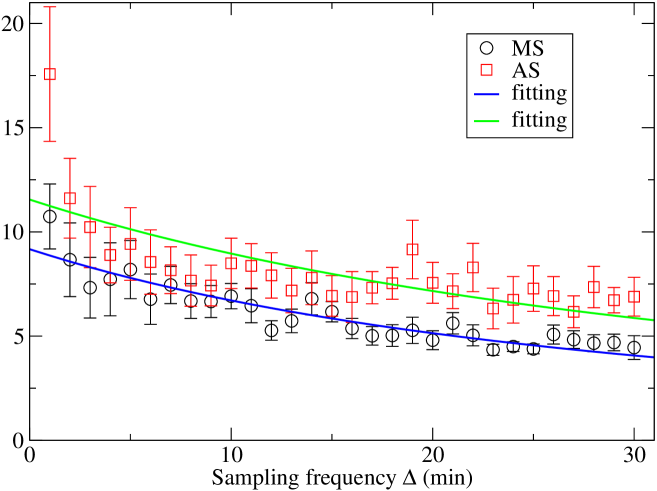

Figure 7 shows the 6th moment of the standardized returns as a function of . The 6th moment increases as the sampling frequency decreases and it seems that the 6th moment approaches the theoretical value, i.e. 15 as goes to zero. We assume that the 6th moment is fitted by a function of where , and and are fitting parameters. For this fitting function the value of the 6th moment at is obtained by . The fitting results are listed in Table 1 and we obtain for the MS(AS).

| Kurtosis (3) | 6th moment (15) | |||

|---|---|---|---|---|

| MS | 2.42 | 216.5 | 9.17 | 176.2 |

| AS | 2.86 | 216.7 | 11.6 | 219.7 |

5 Conclusion

We calculated realized volatility using high-frequency data of the Nikkei Stock Average (Nikkei225) Index on the Tokyo Stock Exchange. To avoid the bias from the non-trading hours issue realized volatility was calculated separately in the morning and afternoon trading sessions of the Tokyo Stock Exchange. As seen in figure 4 it is found that for the Nikkei Stock Average the microstructure noise decreases the realized volatility at small sampling frequency. This finding is the opposite result to the microstructure noise appeared on individual Japanese stocks[14]. Using realized volatility as a proxy of the true volatility we standardized returns in the morning and afternoon sessions and investigated the normality of the standardized returns by calculating variance, kurtosis and 6th moment. It is found that variance, kurtosis and 6th moment are consistent with those of the standard normal distribution, which indicates that the return dynamics of the Nikkei Stock Average are well described by Gaussian random process with time-varying volatility, expected from the mixture of distributions hypothesis.

Acknowledgements

Numerical calculations in this work were carried out at the Yukawa Institute Computer Facility and the facilities of the Institute of Statistical Mathematics. This work was supported by JSPS KAKENHI Grant Number 25330047.

References

References

- [1] Cont R 2001 Quantitative Finance 1 223

- [2] Mandelbrot B 1963 J. of Business 36 394

- [3] Clark P K 1973 Econometrica 41 135

- [4] Praetz P D 1972 J. of Business 45 49

- [5] Van der Straeten E and Beck C 2009 Phys. Rev. E 80 036108

- [6] Takaishi T 2010 Evolutionary and Institutional Economics Review 7 89

- [7] Andersen T G and Bollerslev T 1998 International Economic Review 39 885

- [8] Andersen T G, Bollerslev T, Diebold F X and Labys P 2000 Multinational Finance Journal 4 159

- [9] Andersen T G, Bollerslev T, Diebold F X and Labys P 2001 J. of the American Statistical Association 96 42

- [10] Andersen T G, Bollerslev T, Diebold F X and Ebens H 2001 Journal of Financial Economics 61 43

- [11] Andersen T G, Bollerslev T, and Dobrev D 2007 Journal of Econometrics 138 125

- [12] Andersen T G, Bollerslev T, Frederiksen P, and Nielsen M Ø2010 Journal of Applied Econometrics 25 233

- [13] Fleming J and Paye B S 2011 Journal of Econometrics 160 119

- [14] Takaishi T, Chen T T and Zheng Z 2012 Prog. Theor. Phys. Supplement 194 43

- [15] Takaishi T 2012 Procedia - Social and Behavioral Sciences 65 968

- [16] Andersen T G, Bollerslev T, Diebold F X and Labys P 2000 Risk Magazine 13 105

- [17] Peter R G and De Vilder R G 2006 Journal of Business & Economic Statistics 24 444

- [18] Black F and Scholes M 1973 Journal of Political Economy 81 637

- [19] Merton R C 1973 Bell Journal of Economics and Management Science 4 141

- [20] Zhou B 1996 J. of Business & Economics Statistics 14 45

- [21] Takaishi T 2014 JPS Conf. Proc. 1 019007