Parameter estimation for fractional Ornstein-Uhlenbeck processes of general Hurst parameter

Abstract

This paper provides several statistical estimators for the drift and volatility parameters of an Ornstein-Uhlenbeck process driven by fractional Brownian motion, whose observations can be made either continuously or at discrete time instants. First and higher order power variations are used to estimate the volatility parameter. The almost sure convergence of the estimators and the corresponding central limit theorems are obtained for all the Hurst parameter range . The least squares estimator is used for the drift parameter. A central limit theorem is proved when the Hurst parameter and a noncentral limit theorem is proved for . Thus, the open problem left in the previous paper [11] is completely solved, where a central limit theorem for least squares estimator is proved for .

1 Introduction

Consider the fractional Ornstein-Uhlenbeck process defined as the unique pathwise solution to the stochastic differential equation

| (1.1) |

with initial condition , where is a fractional Brownian (fBm) motion of Hurst parameter , is a positive parameter and the volatility is a stochastic process with -Hölder continuous trajectories, where . Under this condition on , the stochastic integral is well defined as a pathwise Riemann-Stieljes integral (see, for instance, [26]) and the above stochastic differential equation has a unique solution.

Assume that the parameters and are unknown and that the process can be observed continuously or at discrete time instants. We want to estimate the integrated volatility and the drift parameter for any . We assume that the Hurst parameter is known or it can be estimated by other methods (for example, see [5] and the references therein).

In the paper [10], Nualart, Corcuera and Woerner studied the asymptotic behavior of the power variation of the stochastic integral , defined as for any . They proved that if the process has finite -variation on any finite interval, for some , then, as ,

uniformly in probability in any compact sets of , where . The corresponding central limit theorem was also obtained for . These results can be applied to construct an estimator based on the power variation of to estimate the integrated volatility when . However, the condition is critical in [10]. The first objective of this paper is to remove this restriction. To this end, we shall use higher order power variations defined as , for any integer . In Section 3, we study the asymptotic behavior of these higher order power variations of the general stochastic integral . The application of these results to estimate the integrated volatility are presented in Section 4. In particular, when we can use to estimate , where is the constant introduced in (3.1). The uniform convergence in probability and central limit theorems of the estimators for both the integrated volatility and the volatility itself are established.

It is worth mentioning that the statistical estimation of the integrated volatility has already been studied in the recent decades. Barndorff-Nielsen et al [1] - [3]) studied estimation of volatility for Brownian semimartingale and Brownian semi-stationary processes by using power, bipower, or multipower variations. However, those results cannot be applied to the fractional Ornstein-Uhlenbeck process due to its lack of the semimartingale property.

As for the drift parameter , several estimators have been proposed previously. A summary of some relevant results are presented below.

- (i)

-

In the case of continuous observations, Kleptsyna and Le Breton ([13]) studied the maximum likelihood estimator (MLE) which is defined by

where

and with constants and depending on . They proved the almost sure convergence of to as tends to infinity. It is worth noting that Tudor and Viens ([24]) have also obtained the almost sure convergence of both the MLE and a version of the MLE using discrete observations for all . Bercu, Courtin and Savy proved in [4] the following central limit theorem for the MLE in the case of :

They claimed without proof that the above convergence is also valid for .

- (ii)

-

On the other hand, Hu and Nualart ([11]) proposed the least square estimator defined by

(1.2) where the integral with respect to is interpreted in the Skorohod sense. They also introduced another estimator based on the ergodic theorem given by

(1.3) Almost sure convergence and central limit theorems for these two estimators have been proved for .

However, when , the central limit theorems for the least square estimator have not been known yet. The first objective of Section 5 is to prove the asymptotic consistency of by using a new method, different from that in [11], which is valid for all . This method involves the relationship between the divergence and Stratonovich integrals and the integration by parts technique and it is based on the pathwise properties of the fractional Ornstein-Uhlenbeck process established in a paper [7] by Cheridito, Kawaguchi and Maejima. The next and the main objective of this paper is to establish a central limit theorem for the least square estimator for and a noncentral limit theorem for . In the later case, we can identify the limit as a Rosenblatt random variable. We will make a comparison of the asymptotic variance for these three estimators and show that the least square estimator performs better than the maximum likelihood estimator when . Since the ergodic-type estimator is a function of a pathwise Riemann integral that appears simpler than the other two estimators, we will use to construct a consistent estimator for high frequency data (if only discrete observations are available). The asymptotic behavior of in this case is also studied in this paper. The proofs of our results are highly technical and rely on some sophisticated computation, which we shall put in the Appendix. The main tool we use is Malliavin calculus which is recalled in Section 2. We use to denote a generic constant that may vary according to the context.

2 Preliminaries

In this section, we briefly recall some notions and results on fractional Brownian motion, -variation, and Malliavin calculus.

The fractional Brownian motion (fBm) with Hurst parameter is a zero mean Gaussian process, defined on a complete probability space , with the following covariance function

| (2.1) |

From (2.1), it is easy to see that . Then it follows from Kolmogorov’s continuity criterion that on any finite interval, almost surely all paths of fBm are -Hölder continuous with . Denote by the -Hölder coefficient of fBm on the interval , i.e.,

| (2.2) |

Clearly, for any , by the self-similarity property of fBm.

Let denote the -field obtained from the completion of the -field generated by . Let denote the space of all real valued step functions on . The Hilbert space is defined as the closure of endowed with the inner product

Under the convention that if , the mapping can be extended to a linear isometry between and the Gaussian space spanned by . We denote this isometry by . If and is a continuously differentiable function with compact support, we can use step functions in to approximate and and by a limiting argument we deduce

| (2.3) |

(see [12]). We can also use Fourier transform to compute , namely,

| (2.4) |

where (see [23]). When , for any , if we extend and to be zero on , then and we have the following simple identity

| (2.5) |

where .

For any , the -variation of a real-valued function on an interval is defined as

where the supremum runs over all partitions . If is -Hölder continuous on the interval , , then we set

It is known that an -Hölder continuous function on the interval has finite -variation on this interval. If and have finite -variation and finite -variation on the interval respectively and , the Riemann-Stieltjes integral exists (see Young [26]). By Young’s result, the stochastic integral is well defined as a pathwise Riemann-Stieltjes integral provided that the trajectories of the process have finite -variation on any finite interval for some

Next we define two types of stochastic integrals: Stratonovich integral and divergence integral. Given a stochastic process such that a.s. for all , the Stratonovich integral is defined as the following limit in probability if it exists

where is a symmetric approximation of :

Before we define the divergence integral, we present some background of Malliavin calculus. For a smooth and cylindrical random variable , with and ( and all of its partial derivatives are bounded), we define its Malliavin derivative as the -valued random variable given by

By iteration, one can define the -th derivative as an element of . For any natural number and any real number , we define the Sobolev space as the closure of the space of smooth and cylindrical random variables with respect to the norm defined by

The divergence operator is defined as the adjoint of the derivative operator in the following manner. An element belongs to the domain of , denoted by , if there is a constant depending on such that

for any . If , then the random variable is defined by the duality relationship

which holds for any . If is a stochastic process, whose trajectories belong to almost surely (with the convention if ) and , we make use of the notation and call the divergence integral of with respect to the fractional Brownian motion on . It is worth noting that the divergence integral of fBm with respect to itself does not exist if because the paths of the fBm are too irregular (see [8]). For this reason, in [8] the authors introduce an extended divergence integral such that and the extended divergence operator restricted to coincides with the divergence operator. In a similar way we can introduce the iterated divergence operator for each integer , defined by the duality relationship

for any , where .

For any integer , we use and to denote the -th tensor product and the -th symmetric tensor product of the Hilbert space , respectively. We denote by the closed linear subspace of generated by the random variables , where is the -th Hermite polynomial defined by

and . The space is called the Wiener chaos of order . The -th multiple integral of is defined by the identity , and in particular, for any . The map provides a linear isometry between (equipped with the norm ) and (equipped with norm) (see [20], Theorem 2.7.7). By convention, and .

Let us recall the definition of the Rosenblatt process that will appear in the the limit theorems of Section 5. Fix and . Consider the sequence of functions of two variables

Through a direct computation using (2.5) one can show that this sequence is Cauchy in and converges to distribution denoted by and defined by

| (2.6) |

for any test function on . It turns out (see [15] for the proofs) that the sequence converges in as tends to infinity to the Rosenblatt random variable . For any , we have the following formula, letting equal to zero on ,

| (2.7) |

The space can be decomposed into the infinite orthogonal sum of the spaces , which is known as the Wiener chaos expansion. Thus, any square integrable random variable has the following expansion,

where , and are uniquely determined by . We denote by the orthogonal projection onto the -th Wiener chaos . This means that for every .

Let be a complete orthonormal system in the Hilbert space . Given , and , the -th contraction between and is the element of defined by

The following result (known as the fourth moment theorem) provides necessary and sufficient conditions for the convergence of some random variables to a normal distribution (see [17, 18, 20]).

Theorem 2.1.

Let be a fixed integer. Consider a collection of elements such that for every . Assume further that

Then the following conditions are equivalent:

-

1.

.

-

2.

For every , .

-

3.

As tends to infinity, the -th multiple integrals converge in distribution to a standard Gaussian random variable .

-

4.

.

Remark 2.2.

In the paper [17], Nualart and Ortiz-Lattore apply the fourth moment theorem to establish the following weak convergence result for an arbitrary sequence of centered square integrable random vectors.

Theorem 2.3.

Let be a sequence of -dimensional centered square integrable random vectors with the following Wiener chaos expansions:

Suppose that:

-

(i)

.

-

(ii)

For every , , .

-

(iii)

For all , , where is a symmetric nonnegative definite matrix.

-

(iv)

For all , ,

Then, converges in distribution to the -dimensional normal law as tends to infinity.

We end this section by stating the following theorem proved in the paper [9] on the asymptotic behavior of weighted random sums. It will be used in the next section to prove the central limit theorem of the power variation of stochastic integrals.

Theorem 2.4.

Let be a complete probability space. Fix a time interval and consider a double sequence of random variables . Assume the double sequence satisfies the following hypotheses.

(H1) Denote . The finite dimensional distributions of the sequence of processes converges -stably to those of as , where is a standard Brownian motion independent of .

(H2) satisfies the tightness condition for any .

If is an Hölder continuous process with and we set , then we have the -stable convergence

in the Skorohod space .

3 Asymptotic behavior of power variation

In this section, we introduce high order power variations and prove some asymptotic results for the high order power variations of stochastic integrals with respect to fBm. The high order power variations will be used to construct estimators for the volatility and the integrated volatility of fractional Ornstein-Uhlenbeck processes in the next section.

Consider a sequence of random variables . Denote the first order difference . Define the -th order difference by induction as follows for , namely,

Let be a fBm with Hurst parameter . For any , we can write down the covariance function of the -th order difference of the sequences and as follows

Since all the moments of a mean zero Gaussian can be expressed by its variance, we see that the -th moment of is given by

| (3.1) |

Notice that the quantities and are independent of , due to the fact that the fBm has stationary increments.

From the fact that for large it follows that

Let and let be an integer. We define the -th order -variation of a stochastic process as

| (3.2) |

where we use the convention that the sum is zero if .

The following proposition shows the convergence of the -th order -variation for stochastic integrals of fractional Brownian motion, extending a result in [10] which is valid when .

Theorem 3.1.

Let and let . Suppose that is a stochastic process whose sample paths are Hölder continuous with exponent for a certain . Consider the pathwise Riemann-Stieltjes integral

Then for any , as ,

| (3.3) |

in probability, uniformly on , where is the constant introduced in (3.1).

Proof.

Denote by the supremum norm on . For any and any , by the definition of , we have

where , .

Because of the stationary property of the increments of , the high order difference sequence is stationary as well. Thus, for any fixed and , we apply the self-similarity property of to scale the high order difference sequence , and then apply the ergodic theorem to obtain

| (3.4) |

in probability as . This implies

| (3.5) |

in probability, for any fixed .

For the term , we apply arguments similar to those used in the proof of Theorem 1 in [10] together with the ergodic theorem (3.4) for the -th order difference to establish

| (3.6) |

where the convergence holds in probability.

The term is the remainder of a Riemann sum approximation. For all , using the Hölder continuity of , we have

| (3.7) |

almost surely.

It remains to deal with the term . We will use the following two elementary inequalities

| (3.8) | |||||

| (3.9) |

for any , and any . Using inequality (3.9), we obtain

| (3.10) | |||||

First, we use mathematical induction on to prove , almost surely. For , the result is true by the proof of Theorem 1 in [10]. Assume the convergence holds true for . We can express in the following way

where

and

Then, applying inequality (3.8) yields

Choosing , we can write

for some constant depending on , , , and . Using the induction hypothesis, and taking into account that , we conclude that converges to zero almost surely, as tends to infinity.

Finally, the infinity norm of the term can be bounded by

where again is a constant depending on , , , and . Then, goes to 0 almost surely, as .

Next we study the rate of the convergence of (3.3). We will use the notation

| (3.11) |

where and is a standard Gaussian random variable. We shall first deal with the case of the fractional Brownian motion () and then we shall deal with the general case of stochastic integral.

Proposition 3.2.

Fix a positive integer . Let , and . Then

| (3.12) |

in law in the space equipped with the Skorohod topology, where is defined by (3.11) and is a Brownian motion, independent of the fractional Brownian motion .

Proof.

The proof will be completed in two steps.

Step 1: We show the convergence of the finite-dimensional distributions. Let the intervals , be pairwise disjoint in . Define the random vectors and , where

and , for . We claim that

| (3.13) |

where are independent and is a centered Gaussian vector, whose components are independent and have variances . Here is defined in (3.11).

Set and . Then is a stationary Gaussian sequence. Introduce the random vectors and , where

By the self-similarity property of fBm, the convergence of (3.13) will follow from the convergence

| (3.14) |

We are going to prove (3.14) by Theorem 2.3. Consider the normalized sequence

| (3.15) |

Since the function has Hermite rank , the term can be decomposed as

where is the projection of on the -th Wiener chaos, and

with being a standard Gaussian random variable. We have the following five statements.

- (i)

-

for all .

- (ii)

-

, for all . This is clear because and with .

- (iii)

-

For all , we have

which equals the constant multiplying the tail of , and it converges to 0 as .

- (iv)

-

For all , we have

As , this quantity converges to

- (v)

-

For all , we have

which converges to in as goes to infinity. To show this, we explain the details for . The case can be treated in a similar way.

Denote . We can show that the sequence converges almost surely and in using the fact that and . Meanwhile, since given by (3.15) is stationary and ergodic so is . By the ergodic theorem, we have thus in

which equals for .

These can be used to verify the conditions in Theorem 2.3 to obtain the convergence and correspondingly the convergence (3.13) stands true.

Step 2: Let

| (3.16) |

We need to show that the sequence of processes is tight in . To this end we want to prove for any . First, let us compute for ,

Using the elementary inequality , we can bound the right-hand side of the above equation as follows

| (3.17) | |||||

where the second inequality follows from Proposition 4.2 in [25]. The constant is independent of , but it may depend on the function and the distribution of .

Now for , if , applying the above inequality (3.17), we have

Clearly, the right-hand side of the above inequality is at most .

If , then either and or and lie in the same subinterval for some . It suffices to look at the former case. By (3.16), . Using this fact and applying Cauchy-Schwarz inequality, we obtain

where in the last step we have used (3.17) for . The desired tightness property follows from Theorem 13.5 in [6]. ∎

Theorem 3.3.

Let and . Fix and suppose is a stochastic process with Hölder continuous sample paths of order so that the pathwise Riemann-Stieltjes integral is well-defined. Then

in law in the space equipped with the Skorohod topology, where is defined by (3.11), is a Brownian motion independent of the fractional Brownian motion .

Proof.

We start with the following decomposition of the concerned quantity

Using the Hölder continuity of , we can show almost surely. The fact that almost surely can be proved by the same arguments as in the proof of Theorem 3.1 under the condition . It remains to show that

| (3.18) |

in the Skorohod topology of . Denote

Then . In order to finish the proof of (3.18), we are going to apply Theorem 2.4. We shall verify the hypotheses and . By Proposition 3.2 and its proof, , so the sequence of processes satisfies the hypothesis . Using a similar argument as that for (3.17), namely by Proposition 4.2 in [25] again, the family of random variables satisfies the tightness condition . This concludes the proof of the theorem. ∎

Corollary 3.4.

If a stochastic process satisfies uniformly in probability on and if satisfies the conditions of Theorem 3.3, then

in law in equipped with the Skorohod topology, where is a Brownian motion independent of the fractional Brownian motion .

4 Estimation of the integrated volatility

This section is devoted to the estimation of the integrated volatility using the order power variations. Let the stochastic process satisfy (1.1). Motivated by Theorem 3.3, we construct the order power variation estimator for the integrated volatility as follows

| (4.1) |

where the order power variation is given by (3.2), and the normalizing constant is given by (3.1). For this estimator we have the following asymptotic consistency and the central limit theorem.

Theorem 4.1.

Let satisfy (1.1), where the sample path of is Hölder continuous of exponent . Assume and . Then the estimator defined by (4.1) converges in probability to uniformly on any compact interval . Furthermore, the following central limit theorem holds true.

in law in equipped with the Skorohod topology, where is defined by (3.11) and is a Brownian motion, independent of the fractional Brownian motion .

Proof.

When is time independent, Theorem 4.1 gives the following result.

Proposition 4.2.

Let and . Then the estimator converges almost surely to uniformly on any compact interval . Furthermore, as in law in equipped with the Skorohod topology, where is given by (3.11) and is a Brownian motion independent of the fractional Brownian motion .

This proposition gives another estimator for :

| (4.2) |

It is easy to see that Theorem 4.1 and Proposition 4.2 yield the following result.

Proposition 4.3.

When , set . When , set . Assume . Then, the estimator defined by (4.2) converges almost surely to . Furthermore, as , where the asymptotic variance is given by

| (4.3) |

Here is a standard Gaussian random variable.

Usually the variance in (4.3) is complicated to compute.

When , we compute the normalized asymptotic variance of

for some and in the following Table 1.

Table 1: Normalized Asymptotic variance (when )

1 2 3 4 5 0.1 2.7283 3.7127 4.4814 5.1354 5.7147 0.3 2.2504 3.3539 4.1909 4.8855 5.4924 0.5 2.0000 3.0000 3.8889 4.6200 5.2531 0.6 2.1639 2.8308 3.7364 4.4830 5.1282 0.7 3.6088 2.6704 3.5846 4.3443 5.0005 0.8 - 2.5215 3.4348 4.2047 4.8707 0.9 - 2.3872 3.2884 4.0651 4.7393

We see that when is small (for example when ), it is more efficient to use the first order power variation than the higher order ones. However, when is large (for example when ), the central limit theorem of the first order power variation does not hold, but we always have the central limit theorem for the second order power variation. As long as the central limit theorem of the power variation holds, it is preferable to use the lowest order.

5 Estimation of the drift

In this section we assume that the volatility is known and we want to estimate the drift parameter . There have been two popular types of estimators for this drift parameter. One is the maximum likelihood estimator and the other one is the least square estimator. In the Brownian motion case, they coincide, but for the fractional Ornstein-Uhlenbeck processes they are different (see [11] and [13]). We shall focus on the least square estimator as introduced in [11]:

| (5.1) |

where denotes the divergence integral. In the paper [11], the almost sure convergence of to is proved for and the central limit theorem is obtained for . In this paper, we shall extend these results for a general Hurst parameter . In addition, we shall also consider a less popular but very robust estimator: ergodic type estimator.

To simplify notation, we assume . In this case the solution to (1.1) is given by

| (5.2) |

Theorem 5.1.

For , a.s. as .

Proof.

Using integration by parts, we can write

| (5.3) |

Since is in the first Wiener chaos, we have the relationship between the divergence integral and the Stratonovich integral as

Making the substitutions , and then integrating first in the variable yield

| (5.6) |

In the above equation, we use the notation . Observe that converges to exponentially fast as . Then clearly we have

| (5.7) |

The next theorem shows the asymptotic laws for the least square estimator .

Theorem 5.2.

As , the following convergence results hold true.

-

(i)

For , , where

-

(ii)

For ,

-

(iii)

For , , where is the Rosenblatt random variable and is the Dirac-type distribution defined in (2.6).

Remark 5.3.

It is interesting to note that when , by the fact , we have

which is consistent with if . Moreover, we also see that .

Proof.

The case was proved in [11]. We shall use Malliavin calculus to prove the theorem for .

Step 1: We use Theorem 2.1 to prove the central limit theorem when . By (5.1) and (5.2), we can write our target quantity as

| (5.10) |

where

| (5.11) |

We introduce the function

Then is in the second Wiener chaos. Our main objective is to use Theorem 2.1 to obtain the central limit theorem for the term and then we apply Lemma 6.8 and Slutsky’s theorem for (5.10) to obtain the central limit theorem of . First of all, let us check the variance assumption in Theorem 2.1. By the isometry between the Hilbert space and the second chaos , we have

To compute the above norm, we shall use the definition of the tensor product space where the norm in the Hilbert space is defined by (2.3), namely,

| (5.12) |

By Equation (6.32) in Lemma 6.6, we have

| (5.13) |

Next, let us check the second condition in Theorem 2.1. The first contraction of the kernel is

| (5.14) |

We want to prove that the norm of the function in the Hilbert space goes to 0 as . Using the identity (2.4), we rewrite

Observe that is the inverse Fourier transformation of the following function

By the Parseval’s identity, the norm of the function in the space can be computed as

Now our task is to show the right-hand side of the above inequality goes to 0 as . Split into where and . Put for . Denote the functions

and

for . We shall use the inequality for any and some constant to bound the corresponding factors in (LABEL:g.ineq). The choices of are different on . Namely, we choose on and on . In this way, we obtain

| (5.16) | |||||

By the symmetry of in , we can assume that . Then by Lemma 6.4, for any satisfying , there exist some positive constants depending on such that

| (5.17) |

Similarly there exist some positive , depending on and , such that

| (5.18) |

Denote

where . We substitute (5.17), (5.18) into (5.16) and apply the elementary inequality to obtain

where and . The functions are integrable on . Thus,

By Theorem 2.1, as goes to infinity, the term converges in distribution to a centered Gaussian random variable with variance given by (5.13). Applying Slutsky’s theorem and Lemma 6.8 to the equation (5.10), we finish the proof of the theorem when .

Step 2: The case can be dealt with in a similar way as in the proof of Theorem 3.4 in [11]. But now we need to use Lemma 6.6.

Step 3: In this step we will prove the theorem when . Recall that the term is given by (5.11). By (5.1) and (5.2), we write

Denote

| (5.19) |

By the self-similarity property of the fBm, the process has the same law as . To prove part (iii) of the theorem, we need to show . It suffices to prove

| (5.20) |

By Equations (6.34) and (6.35), we see immediately that

where . On the other hand, we have

This shows (5.20) and hence completes the proof of the theorem. ∎

Theorem 5.4.

Define an ergodic-type estimator for the drift parameter by

| (5.21) |

Then almost surely as . Furthermore, we have the following central limit theorem () and noncentral limit theorem ().

Proof.

The paper [11] provides a proof of the theorem when . Here we present a proof valid for all . By Lemma 6.8, it is easy to see almost surely as .

We prove the central limit theorem when . For , the proof is similar. By (5.1) and (5.9), we can derive an expression for , and then express as a function of . In this way, we obtain

By Lemma 6.7 and (5.7) we have

Meanwhile, we can write

for some between and . Now the theorem follows from Theorem 5.2. ∎

Remark 5.5.

By the property for gamma function: for , we see .

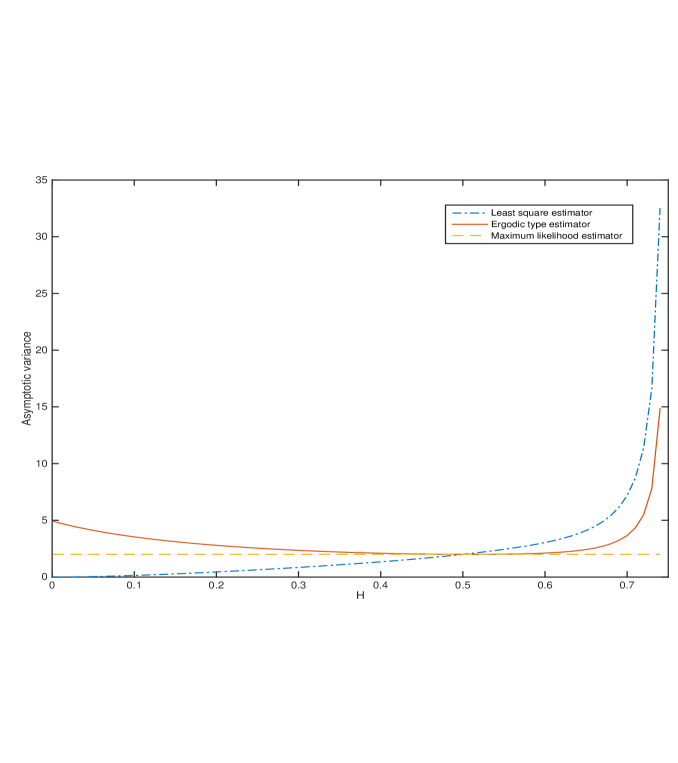

Now we have obtained the asymptotic law of the least square estimator (LSE) and the ergodic type estimator (ETE) . Next, we compare these two estimators with the maximum likelihood estimator by computing their asymptotic variance. For convenience, we assume . As it can be seen from Figure 1, the asymptotic variance of LSE increases as increases. When , the asymptotic variance of LSE is less than that of MLE, where the converse is true for . The asymptotic variance of ETE decreases on and then increases on ; however, it does not blow up as fast as LSE does when is close to . If we justify these three estimators only based on asymptotic variance, LSE performs best when and MLE performs best when . At , these three estimators have the same asymptotic variance.

The estimators and are based on continuous time data. In practice the process can only be observed at discrete time instants. This motivates us to construct an estimator based on discrete observations. We assume that the fractional Ornstein-Uhlenbeck process given by (5.2) can be observed at discrete time points . We shall use instead of for the time period of the observation. Here represents the observation frequency and it depends on . We will only consider the high frequency observation case, namely, we shall assume that as . We shall use ergodic type estimator since it can be expressed as a pathwise Riemann integral with respect to time. The following Theorem shows its asymptotic consistency and some results on its asymptotic law.

Theorem 5.6.

Assume the fractional Ornstein-Uhlenbeck process given by (5.2) is observed at discrete time points . Suppose that depends on and as , goes to 0 and converges to . In addition, we make the following assumptions on and :

-

(1)

When , for some as .

-

(2)

When , for some as .

-

(3)

When , for some as .

Set

| (5.22) |

Then converges to almost surely as . Moreover, as tends to infinity, we have the following central and noncentral limit theorems.

Before we prove Theorem 5.6, we state and prove an auxillary result in the following lemma about the regularity of sample paths of the fractional Ornstein-Uhlenbeck process .

Lemma 5.7.

Proof.

Consider the process . Using (5.3), for any and , we have

Note that

Using the above inequality for and Applying (2.2), with , for yield

∎

Proof of Theorem 5.6:.

Let , , and . Consider the function

Step 1: We claim that almost surely as . Applying Markov’s inequality for yields

| (5.24) |

We apply Minkowski’s inequality to obtain

Taking into account of Lemma 5.7, we have

where the ’s are defined in Lemma 5.7. By Hölder’s inequality and the fact for all , , we can write

where . Therefore,

where denotes a generic constant.

By (2.2), for . By the self-similarity property of fBm, . Using these observations, we obtain

and plugging this inequality to (5.24), we get

| (5.25) |

If the right-hand side of the above inequality is summable with respect to , then almost surely by the Borel-Cantelli Lemma. We show this summability when and the other cases are similar. The right-hand side of (5.25) can be written as

where

and ’s are the denominator of ’s. Note that the positive variables and can be arbitrarily small and can be arbitrarily large. In this way, we have and . If for some , then by carefully choosing these free variables.

Step 2: We prove the almost sure convergence of . Denote . Recall that is given in Theorem 5.4. By the mean value theorem, we can write

| (5.26) |

where .

The result in Step 1 also implies almost surely as , so a.s. for all . Meanwhile, for almost all , there exists such that for ,

Then for , . By the dominated convergence theorem,

Then it is clear that converges to almost surely.

Step 3: We prove the asymptotic laws of . Equation (5.26) yields

Using the result of Step 1 and the similar arguments in step 2, we obtain

Then it is clear that converges in law to the same random variable as when tends to infinity. By Theorem 5.4, we finish the proof.

∎

6 Appendix

This section contains some technical results needed in the proofs of the main theorems of the paper. First we need to identify the limits of some multiple integrals. Denote

| (6.1) |

| (6.2) | |||||

| (6.3) | |||||

| (6.4) | |||||

| (6.5) | |||||

| (6.6) | |||||

Fix an . Denote where and .

Lemma 6.1.

Let . When , we have the following estimates.

-

(i)

(6.7) -

(ii)

(6.8) -

(iii)

(6.9)

where is a constant independent of .

Proof.

First we prove (6.7). Observe that

| (6.10) |

where

It is clear that for

whereas for . Applying the mean value theorem for the second factor of yields

Integrating the right-hand side of the above two inequalities with respect to , we obtain

where we have used the inequality on (i.e., ). Thus, (6.7) follows from the above inequality and (6.10).

Next we prove (6.8). Note that the antiderivative of the function is , so we can compute as follows

| (6.11) |

Applying the inequality

and the triangular inequality to (6.11) yields

Finally, we prove (6.9). Denote

Let . Since and , the interval can be decomposed into the following three intervals, where

Then . We consider the above three integrals separately.

Case 1: When , we have

| (6.12) |

When falls in different subintervals of , we bound in different ways. Namely, if and ,

| (6.13) |

If ,

| (6.14) |

Applying (6.12) for the first summand in , (6.13) and (6.14) for the second summand, we can bound the integration of on as follows

Integrating with respect to yields

Case 2: For , we rewrite

which is nonnegative. In the above integrand, we bound by for the first summand. For the second summand, we apply the mean value theorem for the difference part and bound by . Then integrating yields

Case 3: For , we rewrite

which is nonnegative. In the above integrand, we bound by for the first summand. For the second summand, apply the mean value theorem for the difference part and bound by . Then integrating yields

In the last step we have applied the inequality . ∎

Proof.

We first prove (6.15). For the first summand, making the change of variables and yields

| (6.17) |

which goes to as . A similar argument could be applied to the second summand. For the third summand, by symmetry it suffices to consider the integral on the region . Making the change of variables , yields

| (6.18) |

which goes to as .

Next we show (6.16). Set

Making change of variables, , we can write

The above integral can be decomposed as follows

where

Making the change of variables and integrating , we obtain

Denote by the Beta function. Then

By setting and integrating in first, we deduce . To compute , by symmetry it suffices to integrate on the region . For the second integral, we make the change of variables . In this way, we obtain

The change of variables yields

Setting and integrating on , we obtain

Then, the lemma follows from the above computations of , and . ∎

Lemma 6.3.

Proof.

The proof of (6.19) is divided into the cases and .

Case : For , we evaluate the integral of on by making change of variables , and . In this way, we obtain

| (6.22) |

Clearly , so the integrand of the above triple integral is bounded by the function which is integrable on . As , . Applying the dominated convergence theorem, we have

| (6.23) |

The cases follows from (6.7), (6.8) and (6.9) and Lemma 6.2. ∎

Lemma 6.4.

Let . Denote where . Assuming and , we have the following results.

- (i)

-

For any , there exists some positive constants depending on such that

- (ii)

-

If , then there exists some positive constants depending on and such that

Proof.

We partition into three intervals: . We shall use the inequality

| (6.24) |

For any , we write and apply (6.24) for with . In this way, we obtain

| (6.25) | |||||

For , observe that

| (6.26) | |||||

where . For , writing and applying (6.24) with again (for the same as above), we obtain

| (6.28) |

Let . By (6.25), (6.26), and (6.28), the first part of lemma is obtained.

Now if , then

| (6.29) | |||||

where in the third step, we apply the inequality for . Here the constants , . This finishes the proof of the lemma.

∎

Lemma 6.5.

For , and , set

and

Then

-

(i)

For , ;

-

(ii)

For , .

Proof.

(i) For , we have

and

For the right-hand sides of the above two inequalities, we integrate first in to obtain

This yields (i) by letting .

Lemma 6.6.

Let , be defined by (5.11) and (5.19), respectively. Moreover, let be defined in Part (iii) of Theorem 5.2. Then we have the following convergence results.

- (i)

-

When we have

(6.32) - (ii)

-

When , we have

(6.33) - (iii)

-

When , we have

(6.34) (6.35) where .

In the above lemma, we do not give a statement when , because this case has been studied in [11].

Proof.

Part (i): Assume . Applying L’Hopital’s rule to (5.12) yields

| (6.36) |

where

| (6.37) |

To compute the limit of we will consider that of and .

Computation of : We first compute explicitly the partial derivatives in the integrand of . On the region , we make change of variables , and , and on the region , we make change of variables , and . In this way, can be written as

Reorganize the terms in the above integrals we have

| (6.39) |

Computation of : We first compute explicitly the partial derivatives in the integrand of (6.37). On the region , we make change of variables , and , and on the region , we make change of variables , and . In this way,

Note that

so can be simplified and rewritten as

| (6.42) |

where , and are given by (6.1), (6.5) and (6.6) respectively. By (6.40) and the result of (6.19) for , we have

| (6.43) |

Then part (i) follows from (6.36), (6.40), (6.43) and (6.16).

Part (ii) and (iii): Assume . Using (2.5), we have

| (6.44) |

where , and

| (6.45) |

Applying L’Hopital rule yields

| when | (6.46) | |||

| (6.47) |

where

Denote

Then, finding the limits (6.46) and (6.47) is reduced to the computation of .

Making the change of variables , and in the region and the change of variables , , in the region , we can write as follows

| (6.48) | |||||

Consider the functions

For the first integral of (6.48), we split the integration interval into . For the second integral of (6.48), we write the integration interval as . In this way, we can split into seven integrals. It turns out that some of them are bounded by a constant independent of and they do not contribute to the limit, because . More precisely, we can derive the following bounds:

where in the second step we integrated in and the last step follows from the inequality . It is trivial to show that

and

The last bounded integral is

where in the second step we have used the inequality and the last step follows from the following inequality

With these observations,

We make change of variables for the first term, for the second term, and for the third term. In this way, we obtain

Finally, the limits (6.33) and (6.34) follow from integrating in the variable and an application of Lemma 6.5.

We proceed now to the proof of (6.35). Assume . Recall that is given in Theorem 5.2 and is given by (5.19). By (2.7), we can write

We make the change of variables to rewrite the above equation as

By the symmetry of in the above equation, applying L’Hopital’s rule yields

| (6.49) | |||||

| (6.50) |

To compute , on the region we make the change of variables and on the region we make the change of variables . In this way we obtain

For the term , by symmetry it is sufficient to consider the region and making the change of variables , we obtain

Notice that the second summand of is bounded by . Therefore,

where the last step is due to Lemma 6.5. This finishes the proof of Lemma 6.6. ∎

Lemma 6.7.

Let be defined by

| (6.51) |

where

| (6.52) |

For any , converges almost surely to zero as tends to infinity.

Proof.

The case was proved in [11]. Here, we present a different proof valid for all . We denote , which is computed in Lemma 6.8. Notice that the covariance of the process for is computed as

We use integration by parts for both integrals in the above equation to rewrite

where

By Fubini theorem and the explicit form of the covariance of fBm,

When we compute the above double integral, we write the integrand as three items by distributing and then integrate the terms one by one. For the term involving , we make the change of variables and integrate in the variable first. Similarly,

Denote if . Notice that . Based on the above computations, for small, we have

The lemma now follows from Theorem 3.1 of Pickands [22].

∎

Lemma 6.8.

Let the stochastic process satisfy (1.1) (with ). Then a.s. and in , as .

Proof.

When , the Lemma is proved in [11]. We shall handle the case of general Hurst parameter in a similar way. The process defined by (6.51) is Gaussian, stationary and ergodic for all . By the ergodic theorem,

almost surely and in . This implies

as goes to infinity, almost surely and in . Moreover, integrating by parts yields

In the last step of the above computation, we use the same idea as near the end of the proof for Lemma 6.7. Namely, one writes out the explicit form of , split the integrand into three items by distributing to the summands of , and then integrate the three items one by one. For the item involving , noticing the symmetry of , one can make change of variables , and then integrate in the variable first. ∎

References

- [1] Barndorff-Nielsen, Ole E.; Corcuera,J.M.; Podolskij, M. Limit theorems for functionals of higher order differences of Brownian semi-stationary processes. Prokhorov and contemporary probability theory, 69-96, Springer Proc. Math. Stat., 33, Springer, Heidelberg, 2013.

- [2] Barndorff-Nielsen, Ole E.; Shephard, N. Multipower variation and stochastic volatility. Stochastic Finance, 73-82, Springer, New York, 2006.

- [3] Barndorff-Nielsen, Ole E.; Graversen, S.E.; Jacod,J.;Podolskij,M.;Shephard,N. A central limit theorem for realised power and bipower variations of continuous semimartingales. From Stochastic Calculus to Mathematical Finance, 33-68, Springer, Berlin, 2006.

- [4] Bercu, B.; Coutin, L.; Savy, N. Sharp large deviations for the fractional Ornstein-Uhlenbeck process. Theory Probab. Appl., Vol 55, No.4, 575-610, 2011.

- [5] Biagini, F.; Hu, Y.; Øksendal,B.; Zhang, T. Stochastic calculus for fractional Brownian motion and applications. Springer, 2008.

- [6] Billingsley, P. Convergence of probability measures. Second edition. Wiley Series in Probability and Statistics: Probability and Statistics. A Wiley-Interscience Publication. John Wiley & Sons, Inc., New York, 1999.

- [7] Cheridito, P.; Kawaguchi, H. and Maejima, M. Fractional Ornstein-Uhlenbeck processes. Electronic Journal of Probability 8 (2003) 1-14

- [8] Cheridito, P.; Nualart, D. Stochastic integral of divergence type with respect to fractional Brownian motion with Hurst parameter H . Ann. Institut Henri Poincaré 41 (2005) 1049-1081

- [9] Corcuera, J.M.; Nualart, D. and Podolski,M. Asymptotics of weighted random sums. Communications in Applied and Industrial Mathematics, ISSN 2038-0909, e-486.

- [10] Corcuera, J.M.; Nualart, D. and Woerner, J.H.C. Power variation of some integral fractional processes. Bernoulli, 12(4) 713-735, 2006.

- [11] Hu, Y. and Nualart, D. Parameter estimation for fractional Ornstein-Uhlenbeck processes. Statist.Probab.Lett, 80(11-12), 1030-1038, 2010.

- [12] Hu, Y.; Jolis, M. and Tindel, S. On Stratonovich and Skorohod stochastic calculus for Gaussian processes. The Annals of Probability, Vol. 41, No. 3A, 1656-1693, 2013.

- [13] Kleptsyna, M.L. and Le Breton, A. Statistical analysis of the fractional Ornstein-Uhlenbeck type process. Stat. Inference Stoch. Process. 5, 229-248, 2002.

- [14] Nourdin, I. Selected Aspects of Fractional Brownian Motion. Springer, 2012.

- [15] Nourdin, I.; Nualart, D. and Tudor, C. Central and non-central limit theorems for weighted power variations of fractional Brownian motion. Annales de l’Institut Henri Poincaré - Probabilités et Statistiques, Vol. 46, No. 4, 1055-1079, 2010.

- [16] Nualart, D. The Malliavin Calculus and Related Topics. Second edition, Springer, 2006.

- [17] Nualart,D. and Ortiz-Latorre,S. Central limit theorems for multiple stochastic integrals and Malliavin calculus. Stochastic Processes and their Applications, 118, 614-628, 2008.

- [18] Nualart, D. and Peccati, G. Central limit theorems for sequences of multiple stochastic integrals. Ann. Probab., 33, no. 1, 177-193.

- [19] Nualart, D. and Răşcanu, A. Differential equation driven by fractional Brownian motion. Collect. Math., 53, 55-81, 2002.

- [20] Nourdin, I. and Peccati, G. Normal Approximations with Malliavin Calculus: from Stein’s Method to Universality. Cambridge University Press, 2012.

- [21] Peccati, G. and Tudor, C. Gaussian Limits for Vector-valued Multiple Stochastic Integrals. Sém. Probab. XXXVIII, 247-262, 2004.

- [22] Pickands, J. Asymptotic properties of the maximum in a stationary Gaussian process. Trans. Amer. Math. Soc., 145, 75-86, 1969.

- [23] Pipiras,V. and Taqqu, M.S. Integration questions related to fractional Brownian motion. Probab. Theory Relat. Fields, 118, 251-291, 2000.

- [24] Tudor, C. and Viens, F. Statistical aspects of the fractional stochastic calculus. The Annals of Statistics, Vol 35, No. 3, 1183-1212, 2007.

- [25] Taqqu, M.S. Law of the iterated logarithm for sums of non-linear functions of Gaussian variables that exhibit a long range dependence. Z. Wahrscheinlichkeitstheorie Verw. Geb., 40, 203-238, 1977.

- [26] Young, L.C. An inequality of the Hölder type connected with Stieltjes integration. Acta Math., 67, 251-282, 1936.

Yaozhong Hu, David Nualart and Hongjuan Zhou: Department of Mathematics, University of Kansas, 405 Snow Hall, Lawrence, Kansas, 66045, USA.

E-mail address: yhu@ku.edu, nualart@ku.edu, zhj@ku.edu