Analysis of error control in large scale two-stage multiple hypothesis testing

Abstract

When dealing with the problem of simultaneously testing a large number of null hypotheses, a natural testing strategy is to first reduce the number of tested hypotheses by some selection (screening or filtering) process, and then to simultaneously test the selected hypotheses. The main advantage of this strategy is to greatly reduce the severe effect of high dimensions. However, the first screening or selection stage must be properly accounted for in order to maintain some type of error control. In this paper, we will introduce a selection rule based on a selection statistic that is independent of the test statistic when the tested hypothesis is true. Combining this selection rule and the conventional Bonferroni procedure, we can develop a powerful and valid two-stage procedure. The introduced procedure has several nice properties: (i) it completely removes the selection effect; (ii) it reduces the multiplicity effect; (iii) it does not “waste” data while carrying out both selection and testing. Asymptotic power analysis and simulation studies illustrate that this proposed method can provide higher power compared to usual multiple testing methods while controlling the Type 1 error rate. Optimal selection thresholds are also derived based on our asymptotic analysis.

AMS 1991 subject classifications. Primary 62J15, Secondary 62G10

KEY WORDS: screening, familywise error rate, filtering, high-dimensional, multiple testing

1 Introduction

Consider the multiple testing problem of simultaneously testing a large number of hypotheses. When is large, standard multiple testing procedures suffer from low “power” and are unable to distinguish between null and alternative effects because extremely small -values are required if one properly accounts for Type 1 error control, such as the familywise error rate (FWER); see Lehmann and Romano (2005). It is only by weakening the measure of error control, such as the false discovery rate (FDR), that some discoveries may be found (Benjamin and Hochberg, 1995). But, such discoveries are not as forceful as when they arise while controlling the FWER.

When “most” null hypotheses are “true”, a common and useful approach is to first reduce the number of hypotheses being testing in order to construct methods which are better able to distinguish alternative hypotheses. That is, one applies some selection, filtering or screening technique based on some selection statistics in order to reduce the number of hypotheses being tested. Then, one can use standard stepwise methods to test the reduced number of tests. Such two-stage methods have been extensively used in practice to deal with various problems of multiple testing (McClintick and Edenberg, 2006; Talloen et al., 2007; Hackstadt and Hess, 2009). As in the bulk of this paper, such approaches are called two-stage procedures. In the first stage, some screening or selection method is applied in order to reduce the number of tests. In the second stage, the reduced number of tests is tested. A major limitation of these methods is there lacks a systematic consideration of the selection effect. In other words, one cannot simply apply some method to the reduced number of hypotheses without accounting for selection in error control. That is, one cannot in general “forget” about the screening stage. In other words, in order to properly control Type 1 error rates, one must in general account for the screening stage by considering the error rate conditional on the method of selection. Otherwise, lose of Type 1 error control, whether it is FDR, FWER, or an alternative measure, results.

But, if screening statistics at the first stage are chosen to be independent of the testing statistics at the second stage (at least under the null hypothesis), then error control simplifies as the conditional distributions and unconditional distributions of the test statistics are the same (at least under its respective null distribution). Indeed, Bourgon, Gentleman, and Huber (2010) introduced such a novel approach of independence filtering to avoid the effect of selection, in which the selection or filtering statistics at the first stage are chosen to be independent of the test statistics (at least when the corresponding null hypotheses are true). Two new two-stage methods, which respectively combine the approach of independence filtering with the conventional Bonferroni and Benjamini-Hochberg procedures (Benjamini and Hochberg, 1995), are proposed and shown to control both the FWER and FDR under independence of test statistics. By using the same idea of independence filtering, Dai et al. (2012) develop several two-stage testing procedures to detect gene-environment interaction in genome-wide association studies. Kim and Schliekelman (2016) further discuss some key questions on how to best apply the approach of independence filtering and quantify the effects of the quality of the filter information, the filter cutoff and other factors on the effectiveness of the filter.

Another commonly used approach to avoid the selection effect is sample splitting in which the data is split in two independent parts. One uses the first part of the data to construct the selection or filtering statistics and the second part to construct the test statistics. By combining sample splitting with conventional stepwise procedures, one can develop two-stage procedures that guarantee control of Type 1 error rates (Cox, 1975; Rubin, Dudoit, and van der Laan, 2006; Wasserman and Roeder, 2009). These methods completely remove the effect of selection; however, they often result in power loss due to reduced sample size for testing (Skol, et al., 2006; Fithian, Sun and Taylor, 2014).

In recent years, there has been a growing interest in selective inference (Benjamin and Yekutieli, 2005; Benjamini, 2010; Taylor and Tibshirani, 2015) and several novel breakthroughs have been made in the context of high-dimensional regression (Berk et al 2013; Barber and Cands 2015; Lee et al 2016; Fithian et al. 2014). All of these developments take model selection rules as given and develop methods to preform valid inference after taking into account selection effects. Along these lines, a number of selective inference/post selection inference methods have been developed for various model selection algorithms (Barber and Candes, 2016; Benjamini and Bogomolov, 2014; Fithian et al., 2015; Heller et al., 2016; Tian and Taylor, 2015a, b; Weinstein, Fithian and Benjamini, 2013; Yekutieli; 2012). In this literature, the problem of how to choose selection rules is often overlooked; however, in practice one can often choose a desired selection rule to lead to favorable conditional properties of inference after selection. In contrast, rather than treat the selected hypotheses as given, we can propose a rule in both stages so that the overall procedure has good unconditional error control properties.

Another popular way of exploiting information in the data is, rather than completely eliminating tests under consideration, to construct weights for the null hypotheses and then develop data-driven weighted multiple testing procedures (Roeder and Wasserman, 2009; Poisson et al, 2012). The data-driven weighted methods are pretty general and filtering methods can regarded as its special case. A limitation of such methods is that it is not clear how to assign weights in a data-driven way to ensure control of the FWER or FDR. Very recently, by using “covariates” to construct weights which are independent of the test statistics under the null hypotheses, several Bonferroni-based and Benjamini-Hochberg based data driven weighted methods have been developed that increase power while controlling the FWER and FDR, respectively (Fino and Salmaso, 2007; Ignatiadis, et al, 2016; Li and Barber, 2016; Lei and Fithian, 2016; Ignatiadis and Huber, 2017). In addition, when developing more powerful multiple testing methods, there are several other ways of using such additional covariate information that have recently introduced in the literature, such as local FDR based approaches (Cai and Sun, 2009), stratified Benjamini-Hochberg (Yoo, et al., 2010), grouped Benjamini-Hochberg (Hu, Zhao and Zhou, 2010), and single-index modulated method (Du and Zhang, 2014), etc.

In summary, there is a growing literature of approaches to dimension reduction in high dimensional (single and multiple) hypothesis testing, including some useful, novel, and somewhat ad hoc procedures. The contribution of this paper is to perform a detailed error analysis in a large scale setting. We consider an ideal Gaussian model, as is often assumed in the literature. as described in the setup in Section 2. There, we introduce a specific two-stage procedure that we will analyze and compare later with other procedures. Control of the FWER is presented, though the less formal argument already appears in Bourgon, Gentleman and Huber (2010). (The analysis applies to the joint but single testing problem of testing all means zero against the alternative that at least one is not, but the exposition emphasizes the multiple testing problem.) The remainder of the paper is new. In Section 3, under a large asymptotic framework with a sparsity assumption on the number of false hypotheses, we present detection boundaries for mean levels that can (or cannot be) detected by the two-stage procedure. In Section 4, a refinement is obtained so that the exact cutoff is calculated. Section 5 considers the unknown variance case, where the basic finite sample control of the FWER is replaced by asymptotic control, but the same power analysis holds as when the variance is known. In Section 6, we allow for dependence between the test statistics. Section 7 theoretically compares the two-stage approach with other methods: Bonferroni and split-sample methods. By proper choice of how to split, the split sample technique can only perform as well as Bonferroni, with neither approach performing as well as the two-stage method. A simulation study is presented in Section 8. Both global tests of a single hypothesis (in a high dimensional setting) as well as multiple tests are considered. In the former case, the Higher Criticism (Donoho and Jin, 2004; Donoho and Jin, 2015) is also compared (but it cannot readily be used in the multiple testing case). In both cases, the two-stage approach offers both control of the Type 1 error rate as well as it performs quite well under various scenarios. In particular, the two-stage method shows good performance even when variances are unequal and especially under dependence.

2 The setup

A very stylized Gaussian setup is assumed, as is conventional in large scale testing. The problem is testing means from independent populations, where is large.

Assume that, for , a sample of size from a normal population with unknown mean and variance is observed; that is, data

where is the number of hypotheses of interest representing the number of samples or populations, and is the sample size for the th sample. The samples are assumed mutually independent. When is large, it is typically assumed that the are known as well, in which case one can take (by sufficiency). For now, we will assume and , though we will discuss the unknown variances case later.

For , consider testing hypotheses

(One may also treat the case of one-sided alternatives with easy modifications.) Define the following two statistics

| (1) |

and

| (2) |

where and are respectively the sample mean and (unbiased) sample variance for the th sample, i.e., and .

The basic two-stage strategy for our method is as follows. The statistics are first used to “select” which of the hypotheses to “test” in the second stage, at which point the statistics are used. There are various choices for the selection statistics, as well as test statistics. For example, one could use the -statistics in both stages. Regardless, the first consideration would then be how to set critical values in each stage in order to ensure some measure of Type 1 error control, such as the familywise error rate (FWER), the probability of at least one false rejection. We will be specific about the critical values soon, but the key motivation for the choice of the sum of squares selection statistic and test statistic is based on the following well-known facts. First, under (and ) we have that

that is, has the Chi-squared distribution with degrees of freedom and has the -distribution with degrees of freedom. But, the more important reason motivating our choice is that, by Basu’s theorem, and are independent under (Lehmann and Romano, 2005). Note that , so that larger values of are indicative of larger values of .

A simple selection rule is used for selecting which hypotheses are to be tested at the second stage. Given a threshold , is selected iff . Let denote the indices of selected hypotheses, with the number of selected hypotheses. At the second stage, one can simply apply the Bonferroni test; that is, reject iff , the quantile of the -distribution with degrees of freedom.

Lemma 2.1

For any choice of the threshold , the above two-stage procedure controls the FWER at level .

Like all proofs, see the appendix.

Remark 2.1

The proof of Lemma 2.1 requires that any test statistic be independent of the selection statistics , if is true. Note that it is not required that the test statistics are jointly independent of the selection statistics.

More generally, the two-stage procedure controls the familywise error rate when any test statistic is independent of the selection statistics, even outside our stylized Gaussian model.

The simple two-stage method can be improved by a Holm-type stepdown improvement. To describe the method, simply apply the Holm method (Holm, 1979) to the -values based on the selected set of hypotheses. More specifically, let denote the marginal -value when testing based on . Of course, in the model above, this is just the probability that a -distribution with degrees of freedom exceeds the observed value of . Let be one if is not selected and equal to if it is selected. Let

denote the ordered -values, so that is the index of the th most significant -value. Now, apply Holm’s procedure based on the -values with . Thus, is rejected if for .

Theorem 2.1

Under the setting of Lemma 2.1, apply the Holm method to the selected set of hypotheses. Then, this modified procedure controls the FWER at level .

Thus, one can do even better by using a Holm-like stepdown method, or even a stepdown version of Sidak’s procedure; see Lehmann and Romano (2005) and Guo and Romano (2007). Indeed, conditional on the selection statistics, all computed true null -values based on “detection” statistics at the second stage are conditionally uniform on and hence unconditionally as well. Thus, any multiple testing method based on -values is available. For example, one can also apply the Benjamini-Hochberg procedure based on the selected -values for controlling the false discovery rate (Benjamini and Hochberg, 1995). In all such cases, the motivation is that gains are possible because at the second stage only a reduced number of hypotheses are tested, with the hopes of increased ability to detect or discover false null hypotheses. Furthermore, both the selection and detection stages are based on the full data (rather than a split sample approach which is used to obtain independence of the stages) and there is no selection effect because of independence between the selection and test statistics when the corresponding hypothesis is true.

So far, the threshold for selection has been just generically set at some constant . We now discuss this choice. For our method, we will choose of the form , the quantile of . Since when is true, such a selection threshold ensures that roughly hypotheses are selected, at least if most null hypotheses are true. The question now is how to choose . Let and , where is a given positive constant satisfying . Then, roughly hypotheses are selected for testing. A choice of must still be specified.

Since Type 1 error control is ensured regardless of the choice of , we now turn to studying the power of the procedure. In our asymptotic analysis, the following is assumed.

Assumption A: , where is a nonnegative constant.

Note that as is equal to , or , the values of are respectively and . So, it is reasonable and often sufficient to characterize the relationship between and by imposing Assumption A. In applications, and (and hence ) are known, and generally we will have . We will consider the probability of rejecting a null hypothesis having mean , which without loss of generality can be taken to be positive. Further assume without loss of generality that it is that is false with mean . If is constant, then under Assumptions A and , we have . On the other hand, if varies with (and ) such that as approaches infinity, then Finally, if the sample size is very large, so that is very small compared to the sample size , then the value of should be taken to be 0. In the following, we mainly perform asymptotic power analyses under Assumption A. Sometimes, is assumed, in which case the case can either be treated separately with ease, or by a limiting argument as tends to zero.

3 Power analysis of two-stage procedure

In order to analyze the power of the two-stage procedure, we break up the analysis in two parts. The first part analyzes the probability of “selection” in the first stage, while the second will analyze the probability of “detection” in the second stage. Rejection of then occurs when both has been selected at the first stage and then detection occurs at the second stage. Roughly, the basic goal will be to determine how large in absolute value an alternative mean must be in order to ensure that the probability of rejection tends to one.

3.1 The probability of selecting

Consider the case where is a constant, so that is false. We now consider the asymptotic behavior of the probability that is selected in the first stage of the two-stage procedure. Recall that denotes the quantile of , the Chi-squared distribution with degrees of freedom, i.e., Hypothesis is selected if .

Lemma 3.1

(i) Under Assumption A, if

| (3) |

then

(ii) Under Assumption A, if

| (4) |

then

In Lemma 3.1(i), if , then the condition (3) always holds, while in (ii) if the condition (4) never holds, which implies is selected with probability tending to one.

Note that there exists a gap between the two detection thresholds in Lemma 3.1, but we will derive an improved, exact result in Section 4.

3.2 The probability of detecting

We now consider the probability that is detected at the second stage using the -statistic . That is, we now analyze the probability that exceeds , regardless of whether or not is selected at the first stage. Later, we will analyze the two stages jointly, but for now note that if is false, then it is no longer the case that the selection statistic and the detection statistic are independent.

First, in order to understand the detection probability, we need to understand , the number of selections from the first stage (as it is random). Let denote the indices of true null hypotheses from to , and let denote the indices of false null hypotheses from to . Let and denote the number of true and false null hypotheses, respectively, from .

We will assume some degree of sparsity in the sense

| (5) |

for some . We will even allow , treating the “needle in the haystack” problem, where exactly one alternative hypothesis is true.

Lemma 3.2

The number of selected hypotheses satisfies

| (6) |

If we assume the sparsity condition (5), then

| (7) |

and

| (8) |

as long as .

Lemma 3.3

Under Assumptions A and (5), we have

-

(i)

when , ;

-

(ii)

when , .

Obviously, if , then for any .

3.3 Asymptotic power analysis

We now combine the two stages to determine the value of that leads to rejection of . Let be the event that is selected in the first stage and let be the event that at the second stage. Note and are dependent in general. Then, the power of the two-stage method, i.e., the probability that is rejected, is

| (9) |

Therefore, in order for rejection of to occur with probability tending to one, it is sufficient to show both and have probability tending to one. Also, we have

| (10) |

Theorem 3.1

Under Assumption A and (5), we have

-

(i)

when ,

-

(ii)

when

Corollary 3.1

Under Assumption A with , for any given , (5) and any ,

Of course, in multiple testing problems, there are many notions of power one might wish to maximize: the probability of rejecting at least one false null hypothesis, the probability of rejecting all false null hypotheses, the probability of rejecting at least false null hypotheses (for any given ), the expected number (or proportion) of rejections among false null hypothesis, etc. Theorem 3.1 and Corollary 3.1 apply directly to the expected proportion of false null hypotheses rejected. For example, in the setting where all false null hypotheses have a common mean , then the expected proportion of correct rejections equals the probability that any one of them is rejected, which tends to one (or not) based on the threshold for .

4 Further improvement

In order to improve Theorem 3.1, we need to derive improved bounds on extreme Chi-squared quantiles. (Note the slack in the bounds provided in Lemmas 9.1 and 9.2.)

Let

| (11) |

which is increasing on . Then, define

| (12) |

which is decreasing in .

Lemma 4.1

Given the value used in stage one for selection with , and in Assumption A, with , define to be the solution of the equation

| (13) |

(i) For any and sufficiently large ,

| (14) |

(i) For any and sufficiently large ,

| (15) |

Lemma 4.2

Under Assumption A and (5), we have

-

(i)

when , .

-

(ii)

when , .

Theorem 4.1

Under Assumption A and (5), we have

-

(i)

when ,

-

(ii)

when ,

Remark 4.1

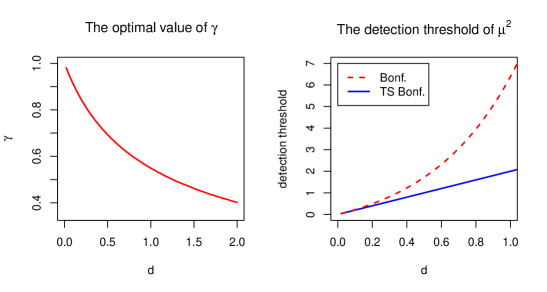

Theorem 4.1 offers an approach of determining the value of tuning parameter . By minimizing the right-hand side of the inequality in Theorem 4.1 (i) or (ii) with respect to , one can determine an optimal value of for each given value of , which maximizes probability of detecting any false null or average power asymptotically. As seen from Figure 4.1 (left), the chosen value of is decreasing in . Note that , thus is roughly increasing in if is fixed and decreasing in if is fixed. For instance, suppose and , then . By checking Figure 4.1 (left), the determined value of is about , which implies that about hypotheses are selected in the first stage for detection.

Based on the optimal value of , we can determine by Theorem 4.1 the upper bound of squared mean for our suggested two-stage Bonferroni procedure, which constitutes a sharp detection threshold. When is larger than the bound, we can always detect . Similarly, we can also determine by Theorem 7.1 the detection threshold of for the conventional Bonferroni procedure. Figure 4.1 (right) shows the detection thresholds of for these two procedures. As seen from Figure 4.1 (right), the detection thresholds of our suggested procedure are always lower than those of conventional Bonferroni procedure for different values of , and their differences are increasingly larger with increasing . This implies that our suggested two-stage Bonferroni procedure is more powerful than the conventional Bonferorni procedure and its power improvement over the Bonferroni procedure becomes increasingly larger with increasing . Specifically, the detection threshold of our suggested procedure is almost linear in terms of with the slope being about and that of the conventional Bonferroni procedure is an exponential function of .

5 Estimating

The goal of this section is to show asymptotic control of the FWER is retained when are the same as unknown and is estimated. To this end, let denote an overall estimator of which satisfies

| (16) |

actually, (16) can be weakened but it holds if we take the average or median of the sample variances computed from each of the samples. Consider the modified procedure based on the selection set

| (17) |

where and is the critical value used in selection when it is known that . The modified two-stage procedure is identical in the second stage in that, for each , is rejected if its corresponding -statistic exceeds the quantile of the -distribution with degrees of freedom, where denotes the number of selected hypotheses at the first stage.

Theorem 5.1

Assume Assumption A.

(i) For , the above modified two-stage procedure asymptotically controls the familywise error rate as .

(ii) For and , the above modified two-stage procedure asymptotically controls the familywise error rate as . In fact, the same is true if

where

and defined in (13).

Remark 5.1

The power analysis used to derive Theorems 3.1 and 4.1 applies equally well to the above modified procedure when is estimated. Of course, at the second stage, the detection probability analysis remains completely unchanged since there is no modification in the second stage. In the first stage, the argument for selection can be used along with the assumption (16) to yield the same results, as the argument is basically the same.

6 Dependence

We now extend the two-stage method when the tests are dependent. The setup is similar to that described in Section 2. Assume we have i.i.d. observations , where and the components of may be dependent. As before, is . (Note that it is not necessary to assume is multivariate Gaussian, but just that the one-dimensional marginal distributions are Gaussian.) We firstly discuss the case of known . For convenience, we still assume . The two-stage procedure is based on the same selection statistic and detection statistic as before. The two-stage procedure selects any for which and then rejects if also exceeds , where is the set of indices such that and is the number of selections at the first stage. Let and be the set of indices of the selected true null hypotheses, i.e.,

We make the following assumptions regarding and , in which the assumption regarding was already shown to hold under independence in Lemma 3.2.

Assumption B1: as where is a fixed constant.

In assumption B1, corresponds to sparsity. By assumption B1, we have

| (18) |

so one can expect the following assumption B2:

Assumption B2: as .

Theorem 6.1

Assume Assumptions B1 and B2. The two-stage procedure discussed in Lemma 2.1 with asymptotically controls the familywise error rate at level .

Remark 6.1

It is interesting to note that in Theorem 6.1, we do not make any assumption of dependence on false null statistics. Only some weak dependence is imposed on true null statistics.

Remark 6.2

Remark 6.3

When the selection statistics are weakly dependent, assumption B2 is satisfied. In the following, we present such an example of block dependence satisfying assumption B2.

Let for . Suppose forming blocks of sizes each, which are reformulated as for blocks, are independent to each other, with , and as , where . Note that In the following, we show that assumption B2 is satisfied under such block dependence. Note that

Thus, by block independence of , we have

We know that

Combining the above two inequalities,

Note that

By Chebychev’s inequality, we have

and thus assumption B2 is satisfied.

When are the same as unknown and is estimated, we consider the modified two-stage procedure discussed in Theorem 5.1. By using similar arguments as in the proof of Theorem 6.1, we can also show that asymptotic control of the FWER is retained for this procedure under dependence.

For any given and , define

Except for assumption B1, we also make the following two assumptions regarding and :

Assumption B3: .

Assumption B4: as where for some slowly.

We should note that assumption B3 has been presented in Section 5 and assumption B4 is a slight extension of assumption B2.

Theorem 6.2

Assume Assumptions B1, B3 and B4. The two-stage procedure discussed in Theorem 5.1 asymptotically controls the familywise error rate at level .

When the selection statistics are block dependent, if the overall estimate is chosen as

we can similarly show that assumptions B3 and B4 are satisfied under block dependence by using the similar arguments as in the case of known variance where we showed in Remark 6.3 that assumption B2 is satisfied under block dependence.

7 Alternative Methods

In this section, we perform a corresponding power analysis with some alternative methods.

7.1 Bonferroni

First, we consider the Bonferroni method, which rejects if . We consider the power or rejection probability of when is the mean.

Theorem 7.1

Assume Assumption A. For the original Bonferroni method,

(i) when ,

(ii) when ,

Remark 7.1

In Theorem 7.1, if , then the stated condition in (i) always holds, which implies is rejected by the Bonferroni procedure with probability tending to one. On the other hand, the stated condition in (ii) holds for any large if is large enough, which implies is rejected with probability tending to zero.

Remark 7.2

In the case of known variance, one can use a -statistic with a normal quantile . Similar to the proof of Theorem 7.1, it can be shown that the threshold can be replaced by .

7.2 Split Sample Method

A common way (Skol et al. 2006; Wasserman and Roeder 2009) to achieve a reduction in the number of tests is to split the sample in two independent parts. The first part, based on observations is used to determine which hypotheses will be selected. Then, those selected hypotheses are tested based on the independent set of observations. Since the two subsamples are independent (as we have been assuming all observations are i.i.d.), it is easy to control the FWER. Indeed, suppose the first subsample produces a reduced set of hypotheses with indices , so that the number of selected hypotheses is . Then, the Bonferroni procedure applied to the remaining observations evidently controls the FWER. Specifically, for , suppose denotes the -statistic computed on the th subsample of size for testing . Here, is selected if , for some cutoff . Here, we will take to be of the form

for some . If denotes the number of satisfying the inequality so that is selected, then is rejected at the second stage if also

For any cutoff used for selection, this procedure controls the FWER. We would like to determine the smallest value of where such a procedure has limiting power one.

Theorem 7.2

Assume Assumption A. Also assume and the sparsity condition (5). For the above split sample method,

(i) when ,

(ii) when ,

Remark 7.3

By Theorem 7.2, the detection threshold (or rather its square) of the split sample method is equal to

which depends on , which we set as , a choice of , as well as the choice of to determine the split sample sizes. We want the threshold to be as small as possible. With fixed, minimizing over both and requires minimizing . If is fixed, the optimizing choice of is , in which case the threshold becomes , which is the same as the original Bonferroni procedure. Note that there are infinitely many optimizing combinations of and as long as . Regardless, no claim can be made to an improvement over the Bonferroni procedure. (On the other hand, we could also apply the split sample method and then apply Holm method in the second stage, which if compared to the usual Holm method based on the full data could offer an improvement because critical values now change more rapidly at each step.)

8 Simulation Studies

In this section, we performed two simulation studies to evaluate the performances of our suggested two-stage Bonferroni method as a high-dimensional global testing method and as an FWER controlling method.

8.1 Numerical comparison for high dimensional global tests

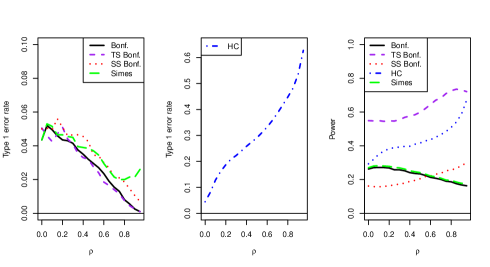

We performed a simulation study to compare the performance of our suggested modified two-stage Bonferroni method (See Section 5) with those of several existing global testing methods with respect to type 1 error rate and power. The methods we chose for comparison include the conventional Bonferroni test, Simes test (Simes, 1986), Higher Criterion method (Donoho and Jin, 2004, 2015), and sample-split Bonferroni test (Cox, 1975; Skol et al, 2006).

Each simulated data set is obtained by generating dependent normal random samples , with a common correlation and a sample size . Among the 1,000 mean values , or are drawn from and the remaining are equal to 0, where . The common variance is drawn from . For , consider using one-sample -statistic for testing individual hypothesis against . We then use the aforementioned five global testing methods for testing the global hypothesis against at level . For our suggested modified two-stage Bonferroni method, we use the sum of squares as the selection statistic for performing selection of the individual hypotheses. The selection threshold we chose is in Section 5, which roughly ensures of hypotheses to be selected. For the sample-split Bonferroni test, we use one-sample -statistics for both selection and testing, which are respectively constructed based on the first and second half samples. The selection threshold we chose is in Section 7. In addition, we always set in the simulations.

The simulation is repeated for times. The type 1 error rate and power are both estimated as the proportions of simulations where is rejected when is respectively true and false. In Figure 8.1 we compared the estimated type 1 error rates and powers of the aforementioned five global testing methods with respect to the common correlation. As seen from Figure 8.1, our suggested modified two-stage Bonferroni method always controls the type 1 error rate at level for all values of correlation while performing best in terms of power. However, for the Higher Criterion test, it completely loses the control of type 1 error rate even when the correlation is weak; and even though for its inflated type 1 error rate, it is still less powerful than our suggested method.

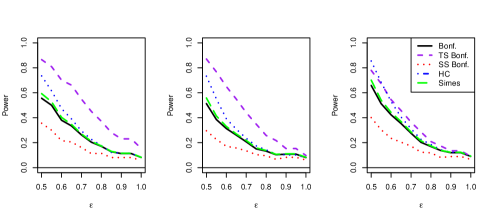

In Figure 8.2 we compared the estimated power of the aforementioned five methods under independence in the cases of equal and unequal variances with respect to with values from to . As seen from Figure 8.2, our suggested modified two-stage Bonferroni method performs best under equal variance in terms of power and its power improvements over the existing four methods are always pretty large for different values of . Under unequal variance, our suggested modified two-stage Bonferroni method still performs well compared to the existing methods, although the power improvements become smaller when the variability of variances becomes larger.

8.2 Numerical comparison for FWER controlling procedures

We also performed a simulation study to compare the performance of our suggested modified two-stage Bonferroni method (Section 5) with those of several existing multiple testing methods with respect to the FWER control and average power. The methods we chose for comparison include conventional Bonferroni procedure, Hochberg procedure, and sample-split Bonferroni procedure (Section 7).

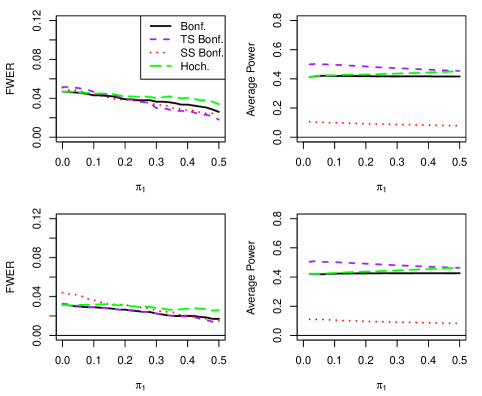

Each simulated data set is obtained by generating dependent normal random samples , with a common correlation and a sample size . Among the 100 ’s, are drawn from and the remaining are equal to 0, where is the proportion of . The common variance is drawn from . For all of these four procedures, we use one-sample -test statistics for testing the hypotheses against . For our suggested modified two-stage Bonferroni method, we use the sum of squares as the selection statistic for performing selection of the tested hypotheses. The selection threshold we chose is , which roughly ensures about hypotheses to be selected. Here, is the average of the sample variances of the samples and is the quantile of chi-square distribution with degrees of freedom . For the sample-split Bonferroni procedure, we use one-sample -statistics for performing selection of all of the hypotheses, which are constructed based on the first half sample with sample size . The selection threshold we chose is , the quantile of -distribution with degrees of freedom , which also roughly ensures about hypotheses to be selected. For testing the selected hypotheses, we also use one-sample -statistics, which are constructed based on the second half sample with sample size .

The aforementioned four procedures are then applied to test against simultaneously for at level . The simulation is repeated for times. The FWER is estimated as the proportion of simulations where at least one true null hypothesis is falsely rejected and the average power is estimated as the average proportion of rejected false null hypothesis among all false nulls across simulations. In Figure 8.3 we compared the estimated FWER and average power of these four procedures with respect to the proportion of false null hypotheses with values from to in the cases of (upper panel) or (bottom panel). As seen from Figure 8.3, our suggested modified two-stage Bonferroni method performs best in terms of average power while controlling the FWER at level , and its power improvements over the existing three methods are decreasing with the increasing proportion of false nulls.

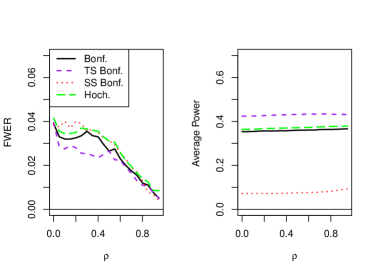

In Figure 8.4 we compared the estimated FWER and average power of these four procedures with respect to the common correlation with values from to . We observe from Figure 8.4 that for different values of correlation , our suggested modified two-stage Bonferroni method always performs best in terms of average power while controlling the FWER at level . In addition, we also observe that the average powers of these methods are not affected by the correlation and the estimated FWERs are basically decreasing in terms of the correlation.

9 Technical Details

Proof of Lemma 2.1 : Assume is true. Then, we claim the detection statistic is independent of all the selection statistics . For the univariate normal model with mean 0 and unknown variance, the -statistic is independent of by Basu’s theorem (because is ancillary and is a complete sufficient statistic). Hence, is independent of , and therefore independent of . Let be the indices of the true null hypotheses. Thus, the FWER is given by

| (19) |

This probability, conditional on the selection statistics is

| (20) |

which by Bonferroni’s inequality is bounded above by

| (21) |

Therefore, the unconditional probability is bounded above by , as required.

Proof of Theorem 2.1: As in the proof of Lemma 2.1, compute the probability of at least one false rejection conditional on the selection statistics. Let be the smallest (or first) for which is true and . Such an event implies that the smallest -value among the true null hypotheses which have been selected is less than or equal to . Indeed, the largest possible value for (leading to the largest possible critical value for the first true null hypothesis tested) is given if, out of the selected hypotheses, all of the false null hypotheses are rejected first in the stepdown procedure, where is the set of indices of the false null hypotheses. This occurs when , in which case

By Bonferroni, the conditional probability is bounded above by because it is the conditional probability that the minimum of true null -values is bounded above by . Thus, the unconditional probability of FWER is bounded above by .

Before proving Lemma 3.1, we will make use of the following lemmas.

Lemma 9.1

(Laurent and Massart, 2000). For every and every , we have

Lemma 9.2

(Inglot, 2010). For every and every , we have

Proof of Lemma 3.1: To show (i), it is enough to show that exceeds an upper bound to with probability tending to one. By Lemma 9.1 and the specification , we have:

Now, if is normalized to form , then by the Central Limit Theorem, it follows that

Thus, it suffices to show that with probability tending to one, where

But,

by the assumption on . Therefore, and so with probability tending to one.

To prove (ii), we argue similarly. By Lemma 9.2, when is sufficiently large, we have

| (22) | |||||

Therefore, it suffices to show

with probability tending to 0. In terms of , it suffices to show with probability tending to 0, where

But

Hence, and the result follows.

Proof of Lemma 3.2: For , let , where denotes the indicator function. Recall that the number of selected hypotheses is , so . Note that, for any true null hypothesis , , in which case

where

Then, if is true, and . In fact, since the Chi-squared family of distributions (with fixed degrees of freedom and varying noncentrality parameter) has monotone likelihood ratio, its power function is increasing in the noncentrality parameter; thus, regardless of whether or not is true. So,

as stated in (6) of the lemma.

Using indicators again to approximate the variance of yields

Therefore, making use of (25).

Thus, by Chebychev’s inequality, , yielding (7). Combining (7) and (25) yields (8).

9.1 The probability of detecting

In the second stage of the two-stage method, we need to be able to approximate the very upper tail quantiles of the normal and distributions. The approximation is well-known for large . In our application, we will apply this with random , and so some care must be taken to get good lower and upper bounds to the quantile.

Lemma 9.3

For any fixed and any , the following inequalities hold for all large enough :

| (26) |

Remark 9.1

In fact the approximations hold uniformly for for any and for all large enough .

Proof of Lemma 9.3: If denotes the standard normal density and , then the following inequalities are well-known (see Feller (1968), Lemma 2 in Chapter VII): for any ,

| (27) |

It follows from the right inequality that

as soon as . Therefore, the quantile of the standard normal distribution must be bounded above by as soon as . The first inequality is similar.

Let be the cdf of student’s with degrees of freedom, and be the cdf of . Consider the equation and let be the solution of the equation. Let

and

We will make use of the following result.

Lemma 9.4

(Fujikoshi and Mukaihata, 1993). For all , we have

-

(i)

-

(ii)

As before, let and denote the quantiles of and , respectively. Then

Lemma 9.5

Fix any and . Then, for all large enough,

| (28) |

and

| (29) |

Proof of Lemma 9.5: First, we show (29). By Lemma 9.4, we have

But since is an increasing function, we can replace by the upper bound provided for in Lemma 9.3, at least for all large . This gives the bound on the right side of (29).

Similarly, for all large , we have

which gives the lower bound in (28).

Proof of Lemma 3.3: To prove (i), detection occurs when exceeds , where is the number of selected hypotheses from the first stage. By Lemma 3.2, , and so by Lemma 9.5,

with probability tending to one. Hence,

where denotes a generic random variable having the -distribution with degrees of freedom. The quantity inside the probability to the left of divided by tends in probability to , i.e.,

But, using Lemma 3.2 and Assumption A, the quantity inside the probability to the right of divided by tends in probability to . Hence, by Slutsky’s theorem, the probability will tend to one if .

Similarly, to prove (ii), with probability tending to one we have

Call the expression on the right side . Then, the detection probability can be bounded above as

Note that the left side inside the last probability divided by tends in probability to to , while the right side, divided by tends in probability to . Hence, if for some , we have

| (30) |

then the probability of detection tends to 0. By continuity, if , then we can choose small enough so that (30) holds, and the result follows.

Proof of Lemma 4.1 We first argue that for any and sufficiently large,

| (31) |

where is a given positive constant satisfying . Along the proof of Theorem 4.1 in Inglot (2010), to prove the above inequality, it is enough to show that

where and . Then, it is in turn enough to show the following inequality when is sufficiently large,

| (32) |

But for given , is equivalent to , which in turn implies the inequality (32). Therefore, (31) holds if , where is defined in (12).

Specifically, if , under assumption A, we have . Thus, for given and sufficiently large , as , (31) holds. Thus, as , (i) holds.

To prove (ii), the proof is similar. When is sufficiently large, the lower bound of in Lemma 9.2 can be improved as

where .

By using the similar arguments as in the proof of Theorem 5.2 of Inglot (2010) and wherein letting , to prove the above inequality, it is enough to show that

where .

When is sufficiently large, we only need to show that

which is equivalent to . Therefore, when is sufficiently large, we have

if .

Specifically, if , by using a similar argument as above, we have

| (33) |

for .

Lemma 9.6

Let have the trinomial distribution based on trials and corresponding success probabilities . Then,

| (34) |

Proof of Lemma 9.6: Since , it suffices to show

| (35) |

The conditional distribution of given is is binomial based on trials and success probability . Hence,

The last sum is bounded above by one because if the sum included the index the sum would be the sum of binomial probabilities based on trials with success parameter . Thus,

and so

Proof of Theorem 5.1: Without loss of generality, assume . Also note that the FWER is maximized when all null hypotheses are true. Indeed, the number of hypotheses selected is an increasing function of , where is the mean of the th sample (since the non-central Chi-squared distribution has monotone likelihood ratio in the non-centrality parameter). But increasing the number of selections only makes the FWER smaller since (stochastically) more hypotheses are tested at the second stage than just the true nulls. Hence, we now assume all hypotheses are null.

For any , the event defined by

| (36) |

has probability tending to one. Let . For any , let

be the selection set when it is known ; in particular, we will always take . Then, with probability tending to one,

| (37) |

and correspondingly the numbers of elements in these index sets satisfy

| (38) |

| (39) |

The point is that, conditional on all the , the sets are determined, and the -statistics then remain conditionally independent (but not so if we condition on ). Hence, by the Bonferroni inequality, the last probability, conditional on the , is bounded above by . Hence, to complete the argument, we must show

| (40) |

Let be the number of in and be the number . Then, (40) reduces to showing

or equivalently

By Lemma 9.6, this last expression is bounded above by , and so we must show , where

| (41) |

But, the denominator in (41) satisfies

and so it suffices to show

| (42) |

The denominator in (41) is, by construction, . The numerator involves an integration over , the Chi-squared density with degrees of freedom. The mode of is . So, the integral can crudely be bounded above by , the density at the mode, multiplied by the length of the interval (). But,

which by Stirling’s formula is easily checked to be of order . Hence, the left side of (41) is bounded above by

Recalling that and shows the last expression is of order . For and slowly enough, this last expression tends to 0 as required.

For , one can improve the argument as follows. Note that the Chi-squared density is decreasing to the right of its mode. Rather than using , one can use with corresponding to (or approximating) the point in the interval closest to , i.e., . Note that

| (43) |

for some ; thus, for all large . Thus, we can bound the numerator in (42) by the length of the interval, multiple by the density at the value of the Chi-squared distribution with degrees of freedom. But, the Chi-squared density evaluated at is equal to

which by Stirlings formula is of order

Hence, the expression (42) is bounded above by order

Recalling that and shows the last expression is of order

| (44) |

Now, even for , this last expression (44) tends to 0 for sufficiently slowly, since .

Note (44) is equal to

Hence, this last expression will tend to 0 (with sufficiently slowly) if

| (45) |

But by (43), we can take any satisfying

| (46) |

Therefore, if we let be the right side of (46), then the result will follow for any satisfying (45) with replaced by , as claimed.

Proof of Theorem 6.1: For every , let denote the event . Under assumption B2, we have

| (47) |

Thus, the FWER is given by

Here, the second inequality follows from independence of and when is true, and the second last expression follows from (18) and (47).

Proof of Theorem 6.2: Let for some slowly such that under assumption B3, the event defined by has probability tending to one. For any , let denote the event . Under assumption B4, the event has also probability tending to one. Thus,

| (48) |

We still use to denote the indices of selected hypotheses, i.e., indices such that . Thus, the FWER is given by

Here, the second inequality follows from independence of and under and the Bonferroni inequality, and the second last expression follows from (48), assumption B1, and the proof of Theorem 5.1, in which it has been shown that

which in turn implies

Proof of Theorem 7.1: The rejection probability is

| (49) |

where denotes a generic random variable having the -distribution with degrees of freedom. But,

Moreover, by Lemma 9.5,

Hence, the limit of the rejection probability in (49) equals one or zero according to whether or not exceeds .

Proof of Theorem 7.2: We first show that is selected with probability 1 (or 0) if exceeds (or is less than) . This is the probability

where denotes a random variable having the -distribution with degrees of freedom, and is the sample standard deviation for the th component based on the first observations. But,

and, by Lemma 9.5,

and the first claim follows.

The detection analysis is the same as for Lemma 3.3, except that the number of selections is obtained differently. All that is needed is that . But the identical argument used to show this in Lemma 3.2 applies as well. Thus, using the same argument in Lemma 3.3, but with replaced by gives that is detected or not according to as whether is greater or less than . Combining this result with the first claim completes the proof.

Acknowledgements

The research of the first author was supported in part by NSF Grant DMS-1309162 and the research of the second author was supported in part by NSF Grant DMS-1307973. This work began during the first author’s sabbatical stay at Stanford University, and W.G. is thankful to Stanford for hosting him.

References

- [1]

- [2] Barber, R. and Cands, E. (2015). Controlling the false discovery rate via knockoffs. Ann. Statist. 43, 2055–2085.

- [3] Barber, R. and Cands, E. (2016). A knockoff filter for high-dimensional selective inference. arXiv preprint arXiv:1602.03574.

- [4] Benjamini, Y. (2010). Simultaneous and selective inference: Current successes and future challenges. Biometrical Journal 52, 708–721.

- [5] Benjamini, Y. and Bogomolov, M. (2014). Selective inference on multiple families of hypotheses. J. Roy. Statist. Soc. Ser. B 76, 297–318.

- [6] Benjamini, Y. and Hochberg, Y. (1995). Controlling the false discovery rate: A practical and powerful approach to multiple testing. J. Roy. Statist. Soc. Ser. B 57 289–300.

- [7] Benjamini, Y. and Yekutieli, D. (2005). False discovery rate-adjusted multiple confidence intervals for selected parameters. J. Amer. Statist. Assoc. 100, 71–93.

- [8] Berk, R., Brown, L., Buja, A., Zhang, K. and Zhao, L. (2013). Valid post-selection inference. Ann. Statist. 41, 802–837.

- [9] Bourgon, R., Gentleman, R. and Huber, W. (2010). Independent filtering increases detection power for high-throughput experiments. Proceedings of the National Academy of Sciences 107, 9546–9551.

- [10] Cai, T. and Sun, W. (2009). Simultaneous testing of grouped hypotheses: Finding needles in multiple haystacks. Journal of the American Statistical Association 104, 1467-1481.

- [11] Cox, D. R. (1975). A note on data-splitting for the evaluation of significance levels. Biometrika 62, 441–444.

- [12] Dai, J., Kooperberg, C., Leblanc, M. and Prentice, R. (2012). Two-stage testing procedures with independent filtering for genome-wide gene-environment interaction. Biometrika 99, 929–944.

- [13] Donoho, D. and Jin, J. (2004). Higher criticism for detecting sparse heterogeneous mixtures. Ann. Statist. 32, 962–994.

- [14] Donoho, D. and Jin, J. (2015). Higher criticism for large-scale inference, especially for rare and weak effects. Statist. Sci. 30, 1–25.

- [15] Du, L. and Zhang, C. (2014). Single-index modulated multiple testing. Ann. Statist. 42, 1262–1311.

- [16] Feller, W. (1968). An Introduction to Probability Theory and Its Applications, Vol. 1, 3rd edition, Wiley, New York.

- [17] Finos, L. and Salmaso, L. (2007). FDR-and FWE-controlling methods using data-driven weights. Journal of Statistical Planning and Inference 137, 3859–3870.

- [18] Fithian, W., Sun, D. and Taylor, J. (2014). Optimal inference after model selection. arXiv preprint arXiv:1410.2597.

- [19] Fithian, W., Taylor, J., Tibshirani, R. and Tibshirani, R. (2015). Selective Sequential Model Selection. arXiv preprint arXiv:1512.02565.

- [20] Fujikoshi, Y. and Mukaihata, S. (1993). Approximations for the quantiles of Student’s t and F distributions and their error bounds. Hiroshima Math. J. 23, 557-564.

- [21] Guo, W. and Romano, J. (2007). A generalized Sidak-Holm procedure and control of generalized error rates under independence. Statistical Applications in Genetics and Molecular Biology 6(1), Article 3.

- [22] Hackstadt, A. J. and Hess, A. M. (2009). Filtering for increased power for microarray data analysis. BMC Bioinformatics 10, 11.

- [23] Heller, R., Chatterjee, N., Krieger, A. and Shi, J. (2016). Post-selection inference following aggregate level hypothesis testing in large scale genomic data. bioRxiv, 058404.

- [24] Holm, S. (1979). A simple sequentially rejective multiple test procedure. Scandinavian Journal of Statistics 6, 65-70.

- [25] Hu, J., Zhao, H. and Zhou, H. (2010). False discovery rate control with groups. Journal of the American Statistical Association 105, 1215-1227.

- [26] Ignatiadis, N. and Huber, W. (2017). Covariate-powered weighted multiple testing with false discovery rate control. arXiv preprint arXiv:1701.05179.

- [27] Ignatiadis, N., Klaus, B., Zaugg, J. B. and Huber, W. (2016). Data-driven hypothesis weighting increases detection power in genome-scale multiple testing. Nature Methods 13, 577–580.

- [28] Inglot, T. (2010). Inequalities for quantiles of the chi-square distribution. Probability and Mathematical Statistics 30, 339-351.

- [29] Kim, S. and Schliekelman, P. (2016). Prioritizing hypothesis tests for high throughput data. Bioinformatics 32, 850–858.

- [30] Laurent, B. and Massart, P. (2000). Adaptive estimation of a quadratic functional by model selection. Ann. Statist. 28, 1302-1338.

- [31] Lee, J. D., Sun, D. L., Sun, Y. and Taylor, J. E. (2016). Exact post-selection inference, with application to the lasso. Ann. Statist. 44, 907–927.

- [32] Lehmann, E. and Romano, J. (2005). Testing Statistical Hypotheses, 3rd edition, Springer, New York.

- [33] Lei, L. and Fithian, W. (2016). AdaPT: An interactive procedure for multiple testing with side information. arXiv preprint arXiv:1609.06035.

- [34] Li, A. and Barber, R. (2016). Multiple testing with the structure adaptive Benjamini-Hochberg algorithm. arXiv preprint arXiv:1606.07926.

- [35] McClintick, J. and Edenberg, H. (2006). Effects of filtering by present call on analysis of microarray experiments. BMC Bioinformatics 7, 49.

- [36] Poisson, L., Sreekumar, A., Chinnaiyan, A. and Ghosh, D. (2012). Pathway-directed weighted testing procedures for the integrative analysis of gene expression and metabolomic data. Genomics 99, 265–274.

- [37] Roeder, K. and Wasserman, L. (2009). Genome-wide significance levels and weighted hypothesis testing. Statistical Science 24, 398-413.

- [38] Rubin, D., Dudoit, S. and Van der Laan, M. (2006). A method to increase the power of multiple testing procedures through sample splitting. Statistical Applications in Genetics and Molecular Biology 5(1).

- [39] Simes, R. J. (1986). An improved Bonferroni procedure for multiple tests of significance. Biometrika 73, 751–754.

- [40] Skol, A., Scott, L., Abecasis, G. and Boehnke, M. (2006). Joint analysis is more efficient than replication-based analysis for two-stage genome-wide association studies. Nature Genetics 38, 209-213.

- [41] Talloen, W., Clevert, D. A., Hochreiter, S., Amaratunga, D., Bijnens, L., Kass, S. and Ghlmann, H. W. (2007). I/NI-calls for the exclusion of non-informative genes: a highly effective filtering tool for microarray data. Bioinformatics 23, 2897-2902.

- [42] Taylor, J. and Tibshirani, R. J. (2015). Statistical learning and selective inference. Proceedings of the National Academy of Sciences 112, 7629–7634.

- [43] Tian, X. and Taylor, J. E. (2015a). Selective inference with a randomized response. arXiv preprint arXiv:1507.06739.

- [44] Tian, X. and Taylor, J. E. (2015b). Asymptotics of selective inference. arXiv preprint arXiv:1501.03588.

- [45] Wasserman, L. and Roeder, K. (2009). High-dimensional variable selection. Ann. Statist. 37, 2178-2201.

- [46] Weinstein, A., Fithian, W. and Benjamini, Y. (2013). Selection adjusted confidence intervals with more power to determine the sign. J. Amer. Statist. Assoc. 108, 165–176.

- [47] Yekutieli, D. (2012). Adjusted Bayesian inference for selected parameters. J. Roy. Statist. Soc. Ser. B 74, 515–541.

- [48] Yoo, Y., Bull, S., Paterson, A., Waggott, D. and Sun, L. (2010). Were genomewide linkage studies a waste of time? Exploiting candidate regions within genome-wide association studies. Genetic Epidemiology 34, 107–118.

- [49]