Inference via low-dimensional couplings

Abstract

We investigate the low-dimensional structure of deterministic transformations between random variables, i.e., transport maps between probability measures. In the context of statistics and machine learning, these transformations can be used to couple a tractable “reference” measure (e.g., a standard Gaussian) with a target measure of interest. Direct simulation from the desired measure can then be achieved by pushing forward reference samples through the map. Yet characterizing such a map—e.g., representing and evaluating it—grows challenging in high dimensions. The central contribution of this paper is to establish a link between the Markov properties of the target measure and the existence of low-dimensional couplings, induced by transport maps that are sparse and/or decomposable. Our analysis not only facilitates the construction of transformations in high-dimensional settings, but also suggests new inference methodologies for continuous non-Gaussian graphical models. For instance, in the context of nonlinear state-space models, we describe new variational algorithms for filtering, smoothing, and sequential parameter inference. These algorithms can be understood as the natural generalization—to the non-Gaussian case—of the square-root Rauch–Tung–Striebel Gaussian smoother.

Keywords: transport map, variational inference, graphical model, sparsity, joint parameter and state estimation

1 Introduction

This paper studies the low-dimensional structure of transformations between random variables. Such transformations, which can be understood as transport maps between probability measures [117], are ubiquitous in statistics and machine learning: they can be used for posterior sampling [80], possibly via deep neural networks [95]; for accelerating Markov chain Monte Carlo or importance sampling algorithms [83, 48]; or as the building blocks of implicit generative models [58, 44, 77] and flexible methods for density estimation [115, 30].

In the context of variational inference [9], a transport map can be used to define a deterministic coupling between a tractable reference measure that we can easily simulate (e.g., a standard Gaussian) and an arbitrary target measure that we wish to characterize (e.g., a posterior distribution). Given i.i.d. samples from the reference measure, we can evaluate the transport map to obtain i.i.d. samples from the target. In other words, the map allows any expectation over the target measure to be rewritten as an integral over the reference measure,

thus enabling the use of standard integration techniques for the tractable , including Monte Carlo sampling and deterministic quadrature [76, 118, 80, 29].

We focus on absolutely continuous measures on , for which the existence of a transport map is guaranteed [103]. Such a map, however, is seldom unique. Identifying a particular map requires imposing additional structure on the problem. Optimal transport maps, for instance, define couplings that minimize a particular integrated transport cost expressing the effort required to rearrange samples [117]. The analysis of such maps underpins a vast field that links geometry and partial differential equations, with applications in fluid dynamics, economics, statistics [32, 56], and beyond. In recent years, several other couplings have been proposed for use in statistical problems, e.g., parametric approximations [80] of the Knothe–Rosenblatt rearrangement [97, 61], couplings induced by the flows of ODEs [49, 1, 22], and couplings induced by the composition of many simple maps, including deep neural networks [69, 115, 95]. Yet the construction, representation, and evaluation of all these maps grows challenging in high dimensions. In the setting considered here, a transport map is a function from onto itself; without specifying further structure, representing such a map or even realizing its action is often intractable as increases.

The central contribution of this paper is to establish a link between the conditional independence structure of the reference-target pair—the so-called Markov properties [65] of and —and the existence of low-dimensional couplings. These couplings are induced by transport maps that are sparse and/or decomposable. A sparse map consists of scalar-valued component functions that each depend only on a few input variables, whereas a decomposable map factorizes as the exact composition of finitely many functions of low effective dimension (i.e., , where each differs from the identity map only along a subset of its components). These properties, and their combinations, dramatically reduce the complexity of representing a transport map and can be deduced before the map is explicitly computed.

The utility of these results is twofold. First, they make the construction of couplings—and hence the characterization of complex probability distributions—tractable for a large class of inference problems. In particular, these results can be exploited in state-of-the-art approaches for the numerical computation of transport maps, including normalizing flows [95] or Stein variational algorithms [1, 69, 27]. Second, these results suggest new algorithmic approaches for important classes of statistical models. For instance, our analysis of sparse triangular maps provides a general framework for describing continuous and non-Gaussian Markov random fields, and for exploiting the conditional independence structure of these fields in computation. Our analysis of decomposable transport maps yields new variational algorithms for sequential inference in nonlinear and non-Gaussian state space models. These algorithms characterize the full Bayesian solution to the smoothing and joint state–parameter inference problems by means of a decomposable transport map, which is constructed (recursively) in a single forward pass using local operations. These algorithms can be understood as the natural generalization, to the non-Gaussian case, of the square-root Rauch-Tung-Striebel Gaussian smoother. Moreover, the results presented in this paper underpin recent efforts in structure learning for non-Gaussian graphical models [78], and novel approaches to the filtering of high-dimensional spatiotemporal processes [109, Chapter 6]. Overall, we propose a range of techniques to address problems of inference in continuous non-Gaussian graphical models.

The paper is organized as follows. Section 2 introduces some notation used throughout the paper. Section 3 reviews the Knothe-Rosenblatt rearrangement, a key coupling for our analysis, while Section 4 briefly recalls some standard terminology for Markov random fields and graphical models. The main results are in Sections 5–7: Section 5 addresses the sparsity of triangular transports, while Section 6 introduces and develops the concept of decomposable transport maps for general Markov networks. These two sections can be read independently. Section 7 specializes the theory of Section 6 to state-space models, introducing new variational algorithms for filtering, smoothing, and parameter inference. Section 8 illustrates aspects of the theory with numerical examples. A final discussion is presented in Section 9. Appendix A collects some technical details on the Knothe-Rosenblatt rearrangement and its generalizations. Appendix B contains the proofs of the main results. Appendix C provides pseudocode for our variational algorithms applied to state-space models, and additional numerical experiments are described in Appendix D. Code and all numerical examples are available online.111http://transportmaps.mit.edu

2 Notation

Here, we collect some useful notation used throughout the paper.

Notation for functions, sets, and graphs

For a pair of functions and , we denote their composition by . We denote by the partial derivative of with respect to its th input variable. By , we mean that the function does not depend on its th input variable. Depending on the context, we can identify a matrix with its corresponding linear map, given by .

For all , we let denote the set of the first integers. For any pair of sets, means that is a subset of (including the possibility of ). We denote by the cardinality of .

Given a graph with vertices and edges , we denote by the neighborhood of a node in , while for any set , we denote by the subgraph given by and .

Notation for measures and densities

In this paper, we mostly consider probability measures on that are absolutely continuous with respect to the Lebesgue measure, , and that are fully supported. We denote the set of such measures by . The density of a measure will always be intended with respect to . For a pair of measures , means that is absolutely continuous with respect to .

For any measure and measurable map , we denote by the pushforward measure given by , where for any set , is the set-valued preimage of under . Similarly, we denote by the pullback measure given by . Given a measure with density and a map , we denote by the density of , provided it exists (depending on ). We call the pushforward density of by . Similarly, we define the pullback density as the density of , provided it exists. Whether the map preserves the absolute continuity of the measure depends on the regularity of . For instance, if is a diffeomorphism—i.e., a differentiable bijection with differentiable inverse—then one has:

| (2.1) |

where denotes the Jacobian of at . The regularity assumptions on can be substantially weakened as long as one modifies (2.1) appropriately [98, 112, 38]. We will give one such example shortly when dealing with triangular maps (see Section 3 or Appendix A). We denote by the integration of a measurable function with respect to a measure . For the Lebesgue measure, we simplify our notation as . Given a pair of probability densities and a map , we say that pushes forward to if and only if couples the corresponding probability measures, i.e., , with and for all measurable sets . (Notice that need not be given by (2.1) since we are not specifying any regularity on .)

When it is clear from context, we will freely omit the qualifier a.e. to indicate a property that holds up to a set of measure zero.

Notation for random variables

We use boldface capital letters, e.g., , to denote random variables on with , while we write scalar-valued random variables as . The law of a random variable defined on a probability space is given by . For a measure , means that has law . If is a collection of random variables and , then denotes a subcollection of . In the same way, for , . If has joint density and , we denote by the marginal of along , i.e., . If is the density of , we denote by the density of given , where

| (2.2) |

We denote independence of a pair of random variables by . In the same way, means that and are independent given a third random variable .

3 Triangular transport maps: a building block

An important transport for our analysis is the Knothe-Rosenblatt (KR) rearrangement on [97, 61, 10]. For a pair of measures , with densities and , respectively, the KR rearrangement is the unique monotone increasing lower triangular measurable map that pushes forward to , i.e., [13, 10]. Here, monotonicity is with respect to the lexicographic order on , while uniqueness is up to -null sets [10]. A lower triangular map is a multivariate function whose th component depends only on the first input variables, i.e.,

| (3.1) |

for some collection of functions and for all .

The distinction between lower, upper, or other more general forms of triangular map is a matter of convention. We will revisit this important point in Section 6. See Appendix A for a constructive definition of the KR rearrangement based on a sequence of one-dimensional transports. In our hypothesis, the KR rearrangement is always a bijection on , while each map

| (3.2) |

is homeomorphic (continuous bijection with continuous inverse), strictly increasing, and differentiable a.e. [103, 116]. Here, monotonicity with respect to the lexicographic order is equivalent to each (3.2) being an increasing function. The resulting rearrangement is far from being a diffeomorphism but is still regular enough to define a useful change of variables, as the following lemma proven in [10] shows.

Lemma 3.1.

If is a KR rearrangement pushing forward to , then -a.e.,

| (3.3) |

where exists a.e., and where is the density of .

In general, in (3.3) is not the determinant of the Jacobian of since the map may not be differentiable, in which case it would not be possible to define in the classical sense; this is why is redefined in the lemma. Nevertheless, it is known that inherits the same regularity as and , but not more [103, 10]. See Appendix A for additional remarks on the regularity of the map.

An essential feature of the triangular transport map is its anisotropic dependence on the input variables. That is, even though each component of the transport map does not depend on all inputs, the map is still capable of coupling arbitrary probability distributions. Informally, we can think of the KR rearrangement as imposing the sparsest possible structure that preserves generality of the coupling—in that the rearrangement is guaranteed to exist for any . (In fact, the transport can be defined under much weaker conditions [103].) In Section 6, we will show that the anisotropy of the KR rearrangement is crucial to proving that certain “complex” (and generally non-triangular) transports can be factorized into compositions of a few lower-dimensional triangular maps. Thus we can think of the KR rearrangement as the fundamental building block of a more general class of non-triangular transports.

The KR rearrangement also enjoys many attractive computational features. As shown in [80, 73], it can be characterized as the unique minimizer of the Kullback–Leibler (KL) divergence over the cone of monotone increasing triangular maps. From the perspective of function approximation, parameterizing a monotone triangular map is straightforward: it suffices to write each component of the map as222For computational efficiency, one may substitue the exponential function with any other strictly positive expression, like a positively shifted square function.

| (3.4) |

for some arbitrary functions and [7, 88]. For example, one could parameterize each using a linear expansion

| (3.5) |

in terms of multivariate Hermite polynomials and unknown coefficients ; alternatively, one could use a neural network representation [45] of and . The resulting transport map —parameterized by the coefficients —is monotone and invertible for all choices of . (In contrast, parameterizing general classes of monotone non-triangular maps is a difficult task.) The minimization of for a map in and for a pair of nonvanishing target () and reference () densities can be rewritten as [80, 73]:

where the expectation is taken with respect to the reference measure—which is the law of .

Two aspects of (3) are particularly important. First, for the purpose of optimization, the target density can be replaced with its unnormalized version . (This replacement is essential in Bayesian inference, where the posterior normalizing constant is usually unknown.) Second, (3) can be treated as a stochastic program and solved by means of sample-average approximation (SAA) [106] or stochastic approximation [63, 108, 11]. Recall that the reference measure is a degree of freedom of the problem and is chosen precisely to make the integration in (3) feasible using, for instance, quadrature, Monte Carlo, or quasi-Monte Carlo methods [24, 96, 28, 29].

Assuming some additional regularity for (e.g., at least differentiability) and using the monotone parameterization of (3.4), then (3) becomes an unconstrained and differentiable optimization problem. In particular, we can use the gradient of to obtain an unbiased estimator for the gradient of (3) [50, 41, 3]. Alternatively, if is unavailable, we can use the score method [42, 89] to produce an estimator that is still unbiased, but with higher variance. For concreteness, consider the realization of an i.i.d. sample from . Then a SAA of (3) reads as:

which is now amenable to deterministic optimization techniques. The numerical solution of (3) by means of an iterative optimization method (e.g., BFGS [120]) produces a sequence of maps that are increasingly better approximations of the KR rearrangement, in the sense defined by (3). In particular, we can interpret as a discrete time flow that pushes forward the collection of reference samples, , to the target distribution. See Figure 1 for a simple illustration. As shown in [80], the KL divergence for an approximate map can be estimated as:

| (3.8) |

up to second-order terms, in the limit of , even if the normalizing constant of is unknown. This convergence criterion is rather useful for any variational inference method, and is usually not available for techniques like MCMC. In the same way, [80] constructs effective estimators for the normalizing constant as

| (3.9) |

We refer the reader to [83, 73] for an alternative construction of the transport map that is useful when only samples from the target measure are available. An interesting application of the latter construction is the problem of density estimation [115] or Bayesian inference with intractable likelihoods [119, 71, 20]. In this case, it turns out that the inverse transport can be easily computed via convex optimization [84]. (Notice that is just an ordinary triangular transport map that pushes forward to . The “inverse” descriptor will help distinguish from the map that pushes forward the reference to the target distribution. We refer to as the direct transport.) We can then invert at to obtain the evaluation of the direct transport . Inverting a monotone triangular function is a computationally trivial task since it requires the solution of a sequence of one-dimensional root finding problems [83, 73]. In practice, one just needs to invert (3.2) for . It is also possible to compute the inverse transport from the unnormalized target density, rather than from samples; here, it suffices to minimize for . The resulting variational problem is equivalent to (3) with the identity . By symmetry of our formulation, has the same regularity as . In particular, Lemma 3.1 holds for as well, and gives a formula for the pushforward density as:

| (3.10) |

where exists a.e., and where is the density of .

There is a growing body of literature on the efficient numerical approximation of transport maps (see, e.g., [75, 95, 69, 115, 80, 7]). Essentially all of these approaches employ numerical optimization to construct or realize the action of a map, and thus harness optimization to enhance integration. Yet all these approaches face a fundamental challenge: the transport map is a function from onto itself, and in high dimensions (i.e., for large ) the representation and approximation of such functions becomes increasingly intractable. In the ensuing sections, on the other hand, we will show that a large class of transport maps are in fact only superficially high-dimensional; that is, they possess some hidden low-dimensional structure that can facilitate their fast and reliable computation. This low-dimensional structure is linked to the Markov properties of the target measure, which we briefly review in the next section.

4 Markov networks

Let be a collection of random variables with law and density . We can represent a list of conditional independences satisfied by —the so-called Markov properties—using a simple undirected graph , where each node is associated with a distinct random variable, , and where the edges in encode a specific notion of probabilistic interaction among these random variables [62]. In particular, we say that is a Markov network—or a Markov random field (MRF)—with respect to if for any triplet of disjoint subsets of , where is a separator set for and ,333 is a separator set for and if (1) is disjoint from and (2) Every path from to intersects . If and are disconnected components of , then is a separator set for and . the subcollections and are conditionally independent given , i.e.,

| (4.1) |

The measure is said to satisfy the global Markov property, relative to , if (4.1) holds [65]. We can also say that is globally Markov with respect to . The corresponding graph is then called an independence map (I-map) for [62].

Intuitively, a sparse graph represents a family of distributions that enjoy many conditional independence properties. I-maps are in general not unique. Of particular interest are minimal I-maps, i.e., the sparsest graphs compatible with the conditional independence structure of .

Conditional independence is associated with factorization properties of . For instance, if and only if a.e. [65]. We then say that factorizes according to some graph if there exists a version of the density of such that

| (4.2) |

for some nonnegative functions called potentials, where is the set of maximal cliques444 A clique is a fully connected subset of the vertices, whereas a maximal clique is a clique that is not a strict subset of another clique. of and is a normalizing constant. It is immediate to show that if factorizes according to , then satisfies the global Markov property relative to [65, Proposition 3.8]. The converse is true only under additional assumptions: for instance, if admits a continuous and strictly positive density (see the Hammersley-Clifford theorem [47, 65]).

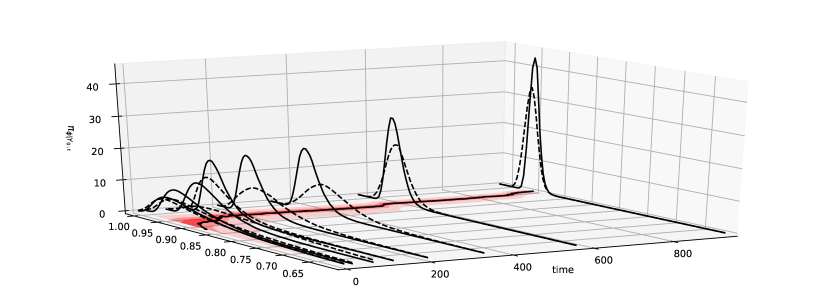

A critical question then is how to characterize a suitable I-map for a given measure. There are several answers. First of all, in many applications that involve probabilistic modeling, the target distribution is defined in terms of its potentials, as in (4.2), because this is just a more convenient way to specify a high-dimensional distribution and to perform inference (or general probabilistic reasoning) with it [62]. Finding a graph for which factorizes is then a trivial task. See Figure 4 (left) for an example. Applications where this commonly holds range from spatial statistics and image analysis to speech recognition [62, 99]. In Section 7, for example, we focus exclusively on discrete-time Markov processes, where the Markov structure of the problem is self-evident. More specifically, Section 7 tackles the problem of recursive smoothing and static parameter estimation for a state-space model. In this context, the target measure could represent the joint distribution of state and parameters, conditioned on all the available observations (see Figures 4 and 8). The reader might want to consider this sequential inference problem as a guiding application while reading the forthcoming Sections 5 and 6. We emphasize, however, that our theory is far more general and by no means restricted to any specific Markov structure.

In other settings, the graph is unknown and must be estimated. When only samples from are available, this is a question of model learning, as described in [62, Part III]; see also [51, 74, 124, 67] for various applications. In case of a known and smooth target density, we can characterize pairwise conditional independence in terms of mixed second-order partial derivatives, as shown by the following lemma.

Lemma 4.1 (Pairwise conditional independence).

If for a measure with smooth and strictly positive density , we have:

| (4.3) |

Thus, if we can evaluate and its derivatives (up to a normalizing constant), we can use Lemma 4.1 to assess pairwise conditional independence and to define a minimal I-map for as follows: add an edge between every pair of distinct nodes unless the corresponding random variables are conditionally independent [62, Theorem 4.5].

Regardless of the many ways to obtain an I-map, there is a fundamental connection between Markov properties of a distribution and the existence of low-dimensional transport maps. The rest of the paper will elaborate precisely on this connection.

5 Sparsity of triangular transport maps

We begin our investigation of low dimensional structure by considering the notion of sparse transport map. A sparse map is a multivariate function where each component does not depend on all of its input variables. According to this definition, a triangular transport is already sparse. In this section, however, we show that the KR rearrangement can be even sparser, depending on the Markov structure of the target distribution.

5.1 Sparsity bounds

Given a lower triangular function , we define its sparsity pattern, , as the set of all integer pairs , with , such that the th component of the map does not depend on the th input variable, i.e., . (We do not include pairs in the definition of since, for a lower triangular function, for by construction.)

Knowing the sparsity pattern of the KR rearrangement before computing the actual transport has important computational implications. For instance, in the variational characterization of the transport described in (3), we can restrict the feasible domain to the set of triangular maps with sparsity pattern given by , and still recover the desired KR rearrangement. That is, if , we can parameterize any candidate transport map by removing the dependence on the th input variable from the th component of the map. Thus, analyzing the Markov structure of the target distribution enables the representation and computation of maps in possibly higher-dimensional settings.

The following theorem, which is the main result of this section, characterizes bounds on the sparsity patterns of triangular transport maps given an I-map for the target measure. In the statement of the theorem, we denote the direct transport by and the inverse transport by (see Section 3). The theorem suggests that and can have quite different sparsity patterns.555 A note: as we already saw, the KR rearrangement is unique up to a set of measure zero. Theorem 5.1 characterizes the sparsity pattern of a particular version of the map, the one given by Definition A.2 in Appendix A. We will implicitly make this assumption throughout the paper.

Theorem 5.1 (Sparsity of Knothe–Rosenblatt rearrangements).

Let , with and a product measure on . Moreover, assume that is globally Markov with respect to , and define, recursively, the sequence of graphs as: (1) and (2) for all , is obtained from by removing node and by turning its neighborhood into a clique. Then the following hold:

-

1.

If is the sparsity pattern of the inverse transport map , then

(5.1) where is the set of integer pairs such that .

-

2.

If is the sparsity pattern of the direct transport map , then

(5.2) where is defined recursively as follows: for the pair if and only if for all .

-

3.

The predicted sparsity pattern of is always greater than or equal to that of , i.e.,

(5.3)

Several remarks are in order. First, we emphasize the fact that Theorem 5.1 characterizes sparsity patterns using only an I-map for , without requiring any actual computation of the transports. One only needs to perform simple graph operations on to build the sequence of graphs . See Figure 2 for an illustration of this procedure, with the corresponding sparsity patterns in Figure 3. We refer to as the marginal graphs. In fact, the sequence is precisely the set of intermediate graphs produced by the variable elimination algorithm [62, Ch. 9], when marginalizing with elimination ordering . This should not be surprising as the KR rearrangement is essentially a sequence of ordered marginalizations [117]. The hypothesis that is a product measure is important for the theorem to hold. If we pick a reference measure with an arbitrary Markov structure, there need not exist a sparse transport map coupling and , even if has a sparse I-map. The role of a reference measure is somewhat peculiar to the world of couplings and is usually not addressed in classical treatments of graphical models. Nonetheless, this assumption on is not restrictive in the present framework, since the reference distribution is considered a degree of freedom of the problem. Theorem 5.1 gives sufficient but not necessary conditions on for the existence of a sparse map. And it could not be otherwise: if then the identity map—the sparsest possible map—would be a valid coupling.

We also note that Theorem 5.1 does not provide the exact sparsity patterns of the triangular transport maps; instead, (5.1) and (5.2) provide subsets of and . In other words, the actual transport maps might be sparser than predicted by the sets and —but, crucially, they cannot be less sparse. Thus, we can think of Theorem 5.1 as providing bounds on the sparsity of triangular transports. An important fact is that, without additional information on , these bounds are sharp. That is, we can always find a pair of measures satisfying the hypotheses of Theorem 5.1 and such that the predicted and actual sparsity patterns coincide, i.e., or .

Part 3 of Theorem 5.1 shows that the predicted sparsity pattern of the inverse KR rearrangement is always larger than or equal to that of the direct transport, i.e., . This does not mean that for every pair of measures , the inverse triangular transport is always at least as sparse as the direct transport; in fact, it is possible to provide simple counterexamples. However, this result does imply that if we are only given an I-map for , then parameterizing candidate inverse triangular transports allows the imposition of more sparsity constraints than parameterizing candidate direct transports. In general, sparser transports are easier to represent. See Figure 4 (right) for a nontrivial example of sparsity patterns for a stochastic volatility model.

Indeed, (5.3) hints at a typical trend: inverse transport maps tend to be sparser (in many practical cases, much sparser) than their direct counterparts. Intuitively, the sparsity of a direct transport is associated with marginal independence in , whereas the inverse transport inherits sparsity from the conditional independence structure of . The latter is a weaker condition than mutual independence; for instance, the correlation length of a process modeled by a Markov random field may be much larger than the typical neighborhood size [99, 8]. Thus, given a sparse I-map for the target measure, it can be computationally advantageous to characterize an inverse transport rather than a direct one, because the inverse transport can inherit a larger sparsity pattern. Given an inverse triangular transport , we can then easily evaluate the direct transport at any point by inverting pointwise, as described in Section 3. There is no need to have an explicit representation of the direct transport as long as it can be implicitly defined through its inverse.

5.2 Connection to Gaussian Markov random fields

The reader familiar with Gaussian Markov random fields (GMRFs), might see links between the preceding results and widespread approaches to the modeling of Gaussian fields. In this section, we clarify the extent of these connections.

Many applications (e.g., image analysis, spatial statistics, time series) involve modeling by means of high-dimensional Gaussian fields. Dealing with large and dense covariances, however, is often impractical; both storage and sampling of the Gaussian field are problematic. The usual workaround is to replace or approximate the Gaussian field with a sparse GMRF—i.e., a Gaussian Markov network that enforces locality in the probabilistic interactions among the underlying random variables. The minimal I-map for the GMRF is thus sparse, and so is the precision matrix of the field [99]. The covariance matrix is still in general dense, but dealing with the sparse precision matrix is much easier. If is a (sparse) Cholesky decomposition of , then represents a linear triangular transport that pushes forward the joint distribution of the GMRF, , to a standard normal, . The key point is that for many Markov structures of interest, the Cholesky factor inherits sparsity from the underlying graph, so that sampling from can be achieved at low cost as follows: if is a sample from , then we can obtain a sample from simply by solving the sparse triangular linear system . There is no need to explicitly represent or store the dense factor , since we can implicitly represent its action by inverting a sparse triangular function.

Now the connection with Section 5.1 is clear: is an inverse triangular transport,666Actually, this transport is upper rather than lower triangular. This distinction plays no role in the following discussion, and the fact that a KR rearrangement is a lower triangular function is merely a matter of convention. while is a direct one. Moreover, solving a triangular linear system is just a particular instance of inverting a nonlinear triangular function by performing a sequence of one-dimensional root-findings. Thus the developments of the previous section, which consider arbitrary nonlinear maps, are a natural generalization—to the non-Gaussian case—of modeling and sampling techniques for high-dimensional GMRFs [99].

5.3 Ordering of triangular maps

The results of Theorem 5.1 suggest that the sparsity of a triangular transport map depends on the ordering of the input variables. See Figure 5 for a simple illustration. Indeed, the triangular transport itself depends anisotropically on the input variables and requires the definition of a proper ordering. A natural approach is then to seek the ordering that promotes the sparsest transport map possible.

Consider a pair of measures that satisfies the hypotheses of Theorem 5.1. We associate an ordering of the input variables with a permutation on , and define the reordered target measure as the pushforward of by the matrix that represents the permutation . In particular, , where is the th standard basis vector on . Moreover, if is an I-map for , then we denote an I-map for by . Notice that can be derived from simply by relabeling its nodes according to the permutation . Then we can cast a variational problem for the best ordering as:

where is the KR rearrangement that pushes forward the reordered target to and is the set of permutations of . The goal is to maximize the cardinality of the sparsity pattern of the inverse map, . We restrict our attention to the sparsity of the inverse transport, since we know from Section 5.1 that the direct transport tends to be dense, even for the most trivial Markov structures.

Ideally, we would like to determine a good ordering for the map before computing the actual transport, and to use the resulting information about the sparsity pattern to simplify the optimization problem for . However, evaluating the objective function of (5.3) requires computing a different inverse transport for each permutation . One possible way to relax (5.3) is to replace with the predicted sparsity pattern introduced in (5.1). The advantage of this approach is that the objective function of the relaxed problem can now be evaluated in closed form without computing any transport map, but rather by performing the simple sequence of graph operations on described by Theorem 5.1. The caveat is that, in general, , and thus maximizing amounts to seeking the tightest lower bound on the sparsity pattern of the inverse transport. From the definition of , it follows that the best ordering for the relaxed problem is one that introduces the fewest edges in the construction of the marginal graphs , whenever . Thus, for a given I-map , we denote by the - produced by the ordering . That is, is a set containing all the edges introduced in the construction of the marginal graphs from . A computationally feasible relaxation of (5.3) is then given by:

(5.3) is a standard problem in graph theory; it arises in a variety of practical settings, including (most relatedly) finding the best elimination ordering for variable elimination in graphical models [62], or finding the permutation that minimizes the fill-in of the Cholesky factor of a positive definite matrix [40, 101]. From an algorithmic point of view, (5.3) is NP-complete [123]. This should not be surprising, as best–ordering problems are typically combinatorial in nature. Nevertheless, given its widespread applicability, a host of effective polynomial-time heuristics for (5.3) have been developed in past years (e.g., min-fill or weighted-min-fill [62]). Most importantly, (5.3) can be solved without ever touching the target measure (assuming, of course, that an I-map for is known). As a result, the cost of finding a good ordering is often negligible compared to the cost of characterizing a nonlinear transport map via optimization.

6 Decomposability of transport maps

Thus far, we have investigated the sparsity of triangular transport maps and found that inverse transports tend to inherit sparsity from the underlying Markov structure of the target measure. Though direct triangular transports also inherit some sparsity according to Theorem 5.1, they tend to be more dense.

This section shows that direct transports enjoy a different form of low-dimensional structure: decomposability. A decomposable transport map is a function that can be written as the composition of a finite number of low-dimensional maps, e.g., for some integer . We use a very specific notion of low-dimensional map, as follows.

Definition 6.1 (Low-dimensional map with respect to a set).

A map is low-dimensional with respect to a nonempty set if

-

1.

for

-

2.

for and .

The effective dimension of is the minimum cardinality over all sets with respect to which is low-dimensional.

In particular, up to a permutation of its components, we can rewrite as:

| (6.1) |

where denotes the complement of in , and where for any map and set , denotes the multivariate function obtained by stacking together the components of with index in . Thus is the trivial embedding of a -dimensional function into the identity map and has effective dimension bounded by . It is not surprising, then, that a decomposable transport should be easier to represent than an ordinary map. A perhaps less intuitive feature, however, is that the computation of a high-dimensional decomposable transport can be broken down into multiple simpler steps, each associated with the computation of a low-dimensional map that accounts only for local features of the target measure.

The forthcoming analysis will consider general, and hence possibly non-triangular, transports. Thus its scope is much broader than that of Section 5, where we only focused on the sparsity of triangular transports. Yet, we will show that triangular maps are the building block of decomposable transports. The cornerstone of our analysis is Theorem 6.1, which characterizes the existence and structure of decomposable transports given only the Markov structure of the underlying target measure.

Our discussion will proceed in two stages: first, we show how to identify direct transports that decompose into two maps, i.e., , and then we explain how to apply this result recursively to obtain a general decomposition of the form .

6.1 Preliminary notions

Before addressing the decomposability of transport maps, we need to introduce two useful concepts: proper graph decompositions and generalized triangular functions. The decomposition of a graph is a standard notion [65].

Definition 6.2 (Proper graph decomposition).

Given a graph , a triple of disjoint subsets of the vertex set forms a proper decomposition of if (1) , (2) and are nonempty, (3) separates from , and (4) is a clique.

See Figure 6 (top left) for an example of a decomposition. Clearly, not every graph admits a proper decomposition; for instance, a fully connected graph does not have a separator set for nonempty and . The idea we will pursue here is that graph decompositions lead to the existence of decomposable transports.

The notion of a generalized triangular function is perhaps less standard, but still relatively straightforward:

Definition 6.3 (Generalized triangular function).

A function is said to be generalized triangular, or simply -triangular, if there exists a permutation of such that the th component of depends only on the variables , i.e., for all and for all .

We can think of a generalized triangular function as a map that is lower triangular up to a permutation. In particular, if is the identity on , then a -triangular function is simply a lower triangular map (see Section 3). To represent the permutation , we use the notation to denote an ordered set that collects the action of the permutation on the elements . For example, if is a -triangular map with defined as , then will be of the form:

| (6.2) |

for some collection . We regard each component as a map . We say that a -triangular function is monotone increasing if each component is a monotone increasing function of the input . Moreover, for any and for any permutation of , there exists a (-unique) monotone increasing -triangular map—which we call a -generalized KR rearrangement—that pushes forward to . We give a constructive definition for a generalized KR rearrangement in Appendix A.

A key property of a -generalized KR rearrangement is that it allows different sparsity patterns to be engineered, depending on , in a map that is otherwise fully general—in the sense of being able to couple arbitrary measures in . This feature will be essential to characterizing decomposable transport maps.

6.2 Decomposition and graph sparsification

We now characterize transports that decompose into a pair of low-dimensional maps, as described in the following theorem. We formulate the theorem for a generic target measure . Later we will apply the theorem recursively to a sequence of different targets.

Theorem 6.1 (Decomposition of transport maps).

Let , , with and tensor product measure. Denote by a pair of nonvanishing densities for and , respectively, and assume that factorizes according to a graph , which admits a proper decomposition . Then the following hold:

-

1.

There exists a factorization of of the form

(6.3) where is strictly positive and integrable, with .

-

2.

For any factorization (6.3) and for any permutation of with

(6.4) there exists a nonempty family, , of decomposable transport maps parameterized by such that each pushes forward to and where:

-

(a)

is a -generalized KR rearrangement that pushes forward to a measure with density and is low-dimensional with respect to .

-

(b)

is the set of maps that are low-dimensional with respect to and that push forward to the pullback .

-

(c)

If , then and in distribution.

-

(d)

factorizes according to a graph that can be derived from as follows:

-

–

Remove any edge from that is incident to any node in .

-

–

For any maximal clique with nonempty intersection , let be the maximum integer such that and turn into a clique.

-

–

-

(a)

We first look at the theorem for and let and , where denotes our usual target measure with I-map and where denotes a decomposition of .

Among the infinitely many transport maps from to , Theorem 6.1 identifies a family of decomposable ones. The existence of these maps relies exclusively on the Markov structure of : we just require to admit a (proper) decomposition.777 To obtain a proper decomposition of , one is free to add edges to in order to turn the separator set into a clique (see Definition 6.2); still factorizes according to any less sparse version of .

Each transport pushes forward to and is the composition of two low-dimensional maps, i.e., for a fixed defined in Theorem 6.1[Part 2a] and for some . (We also write .888 The notation here is intuitive: for a given and for a given set of functions from to , denotes the set of maps that can be written as for some . ) The structure of these low-dimensional maps is quite interesting. Up to a reordering of their components, Theorem 6.1[Parts 2a and 2b] show that and have an intuitive complementary form:

| (6.5) |

(If , one can just remove and from (6.5), and drop the dependence of the remaining components on .) In particular, and have effective dimensions bounded by and , respectively (see Definition 6.1). Even though and are low-dimensional maps, their composition is quite dense—in the sense of Section 5—and is in general nontriangular:

| (6.6) |

and thus more difficult to represent and to work with. The key idea of decomposable transports is that they can be represented implicitly through the composition of their low-dimensional factors, similar to the way that direct transports can be represented implicitly through their sparse inverses (Section 5).

The sparsity patterns of and in (6.5) are needed for the theorem to hold. In particular, must be a -triangular function with specified by (6.4). Notice that (6.4) does not prescribe an exact permutation, but just a few constraints on a feasible . Intuitively, these constraints say that should be a function whose components with indices in depend only on the variables in (whenever ), and whose components with indices in depend only on the variables in . Thus, there is usually some freedom in the choice of . Different permutations lead to different families of decomposable transports, and can induce different sparsity patterns in an I-map, , for (Theorem 6.1[Part 2d]).

Part 2d of the theorem shows how to derive a possible I-map —not necessarily minimal—by performing a sequence of graph operations on . There are two steps: one that does not depend on and one that does. Let us focus first on the former: the idea is to remove from any edge that is incident to any node in , effectively disconnecting from the rest of the graph. That is, if , then, regardless of , makes marginally independent of by acting locally on . And not only that: also ensures that the marginals of and agree along (see Theorem 6.1[Part 2c]). Thus we should really interpret as the first step towards a progressive transport of to . is a local map: it can depend nontrivially only upon variables in . Indeed, in the most general case, is the minimum effective dimension of a low-dimensional map necessary to decouple from the rest of the graph. The more edges incident to , the higher-dimensional a transport is needed. This type of graph sparsification requires a peculiar “block triangular” structure for as shown by (6.5): any -triangular function with given by (6.4) achieves this special structure. The second step of Part 2d shows that if , then it might be necessary to add edges to the subgraph , depending on .999 This is not always the case. For instance, if is a subset of every maximal clique of in that has nonempty intersection with , then, by Theorem 6.1[Part 2d], no edges need to be added. The relevant aspect of for this discussion is the definition of the permutation onto the first integers. In general, there are different permutations that could induce different sparsity patterns in . We shall see that permutations that add the fewest edges possible are of particular relevance.

6.3 Recursive decompositions

The sparsity of is important because it affects the “complexity” of the maps in : each pushes forward to . More specifically, by the previous discussion, we can see how the role of each is really only that of matching the marginals of and along . A natural question then is whether we can break this matching step into simpler tasks, or, in the language of this section, whether contains transports that are further decomposable. Intuitively, we are seeking a finer-grained representation for some of the transports in . The following lemma (for ) provides a positive answer to this question as long as is not fully connected in . From now on, we denote by , since we will be dealing with a sequence of different graph decompositions.

Lemma 6.1 (Recursive decompositions).

Let be defined as in the assumptions of Theorem 6.1 for a proper decomposition of , while let and be the resulting graph (Part 2d) and family of decomposable transports,101010 Whenever we do not specify a permutation or a factorization (6.3) in the definition of , it means that the claim holds true for any feasible choice of these parameters. respectively. Then there are two possibilities:

-

1.

is not a clique in . In this case, it is possible to identify a proper decomposition of for some that is a strict superset of by (possibly) adding edges to in order to turn into a clique. Let be defined as in Theorem 6.1 for the pair of measures and . Then the following hold:

-

(a)

and .

-

(b)

is low-dimensional with respect to and has effective dimension bounded by .

-

(c)

Each has effective dimension bounded by .

-

(a)

-

2.

is a clique in . In this case, the decomposition of Part 1 does not exist.

Lemma 6.1[Part 1] shows that if is not fully connected in , then there exists a proper decomposition of (obtained, possibly, by adding edges to in ) for which is a strict superset of . One can then apply Theorem 6.1 for the pair and the decomposition . As a result, Part 1a of the lemma shows that contains a subset of decomposable transport maps where both and each are local transports on , i.e., they are both low-dimensional with respect to . In particular, is responsible for decoupling from the rest of the graph and for matching the marginals of and along . The effective dimension of is bounded above by the size of the separator set plus the number of nodes in (Part 1b of the lemma). The effective dimension of each is bounded by the cardinality of and is, in the most general case, lower than that of the maps in (Part 1c). Moreover, by Part 1a, , which means that among the infinitely many decomposable transports that push forward to , there exists at least one that factorizes as the composition of three low-dimensional maps as opposed to two, i.e., for some .

If, on the other hand, is fully connected in , then by Lemma 6.1[Part 2] we know that the decomposition of Part 1 does not exist. As a result, we cannot use Theorem 6.1 to prove the existence of more finely decomposable transports in . In other words, if we want to match the marginals of and along , then we must do so in one shot, using a single transport map; no more intermediate steps are feasible.

The main idea, then, is to apply Lemma 6.1[Part 1], recursively, times, where is the first integer (possibly zero) for which is a clique in . After iterations, the following inclusion must hold:

| (6.7) |

which shows that there exists a decomposable transport,

| (6.8) |

for some , that pushes forward to . (Note that we can apply Lemma 6.1[Part 1] only finitely many times since is an integer function strictly decreasing in and bounded away from zero.) Each in (6.7) is a -triangular map for some permutation that satisfies (6.8), and is low-dimensional with respect to , i.e., for and up to a permutation of its components,

| (6.9) |

The map is low-dimensional with respect to and can also be chosen as a generalized triangular function. Intuitively, we can think of as decoupling nodes in from the rest of the graph in an I-map for . (Recall that by Lemma 6.1 all the sets are nested, i.e., .) Figure 6 illustrates the mechanics underlying the recursive application of Lemma 6.1.

We emphasize that the existence and structure of (6.8) follow from simple graph operations on , and do not entail any actual computation with the target measure . Notice also that even if each map in the decomposition (6.7) is -triangular, the resulting transport map need not be triangular at all. In other words, we obtain factorizations of general and possibly non-triangular transport maps in terms of low-dimensional generalized triangular functions. In this sense, we can regard triangular maps as a fundamental “building block” of a much larger class of transport maps.

Decomposable transports are clearly not unique. In particular, there are two factors that affect both the sparsity pattern and the number of composed maps in the family : the sequence of decompositions and the sequence of permutations . Usually, there is a certain freedom in the choice of these parameters, and each configuration might lead to a different family of decomposable transports. Of course some families might be more desirable than others: ideally, we would like the low-dimensional maps in the composition to have the smallest effective dimension possible. Recall that by Lemma 6.1 the effective dimension of each can be bounded above by (with the convention ). Thus we should intuitively choose a decomposition of and a permutation for that minimize the cardinality of , and that, at the same time, minimize the number of edges added from to . In principle, we should also account for the dimensions of all future maps in the recursion. In the most general case, this graph theoretic question could be addressed using dynamic programming [5]. In practice, however, we will often consider graphs for which a good sequence of decompositions and permutations is rather obvious (see Section 7). For instance, if the target distribution factorizes according to a tree , then it is immediate to show the existence of a decomposable transport that pushes forward to and that factorizes as the composition of low-dimensional maps , each associated to an edge of : it suffices to consider a sequence of decompositions with , where, for a given rooted version of , consists of a single node with the largest depth in , and where contains the unique parent of that node. Remarkably, each map has effective dimension less than or equal to two, independent of —the size of the tree.

At this point, it might be natural to consider a junction tree decomposition of a triangulation of [62] as a convenient graphical tool to schedule the sequence of decompositions needed to apply Lemma 6.1 recursively. Decomposable graphs are in fact ultimately chordal [65]. However, the situation might not be as straightforward. The problem is that the clique structure of , an I-map for , can be very different than that of , an I-map for ; Theorem 6.1[Part 2d] shows that might contain larger maximal cliques than those in , even if is chordal (see Figure 6 for an example). Thus, working with a junction tree might require a bit of extra care.

6.4 Computation of decomposable transports

Given the existence and structure of a decomposable transport like (6.8), what to do with it? There are at least two possible ways of exploiting this type of information. First, one could solve a variational problem like (3) and enforce an explicit parameterization of the transport map as the composition . In this scenario, one need only parameterize the low-dimensional maps and optimize, jointly, over their composition. The advantage of this approach is that it bypasses the parameterization of a single high-dimensional function, , altogether. See the literature on normalizing flows [95] for possible computational ideas in this direction.

An alternative—and perhaps more intriguing—possibility is to compute the maps sequentially by solving separate low-dimensional optimization problems—one for each map . By Theorem 6.1[Part 2a] and Lemma 6.1, there exists a factorization (6.3) of —a density of —for which is a -generalized KR rearrangement that pushes forward to a measure with density proportional to , where is a decomposition of and is an I-map for . In general depends on , and so the maps must be computed sequentially.111111 This is not always the case. For instance, given a rooted version of and a pair of consecutive depths (see the discussion at the end of Section 6.3), all the maps associated with edges connecting nodes at these two depths can be computed in parallel. In essence, decomposable transports break the inference task into smaller and possibly easier steps.

Note that we could define with respect to any factorization (6.3) with integrable: these different factorizations would lead to a family of decomposable transports with the same low-dimensional structure and sparsity patterns (as predicted by Theorem 6.1). Thus, as long as we have access to a sequence of integrable factors , we can compute each map individually by solving a low-dimensional optimization problem. (See Appendix A for computational remarks on generalized triangular functions.) Intuitively, since by Lemma 6.1[Part 1b] is low-dimensional with respect to , we really only need to optimize for a portion of the map, namely for , which can be regarded effectively as a multivariate map on . In the same way, the map can be computed as any transport (possibly triangular) that pushes forward to . Theorem 6.1[Part 2b] tells us that once again we only need to optimize for a low-dimensional portion of the map, namely, .

While it might be difficult to access a sequence of factorizations (6.3) for a general problem, there are important applications, such as Bayesian filtering, smoothing, and joint parameter/state estimation, where the sequential computation of the transports is always possible by construction. We discuss these applications in the next section.

7 Sequential inference on state-space models: variational algorithms

In this section, we consider the problem of sequential Bayesian inference (or discrete-time data assimilation [66, 94, 104]) for continuous, nonlinear, and non-Gaussian state-space models.

Our goal is to specialize the theory developed in Section 6 to the solution of Bayesian filtering and smoothing problems. The key result of this section is a new variational algorithm for characterizing the full posterior distribution of the sequential inference problem—e.g., not just a few filtering or smoothing marginals—via recursive lag– smoothing with transport maps. The proposed algorithm builds a decomposable high-dimensional transport map in a single forward pass by solving a sequence of local small-dimensional problems, without resorting to any backward pass on the state space model (see Theorem 7.1). These results extend naturally to the case of joint parameter and state estimation (see Section 7.3 and Theorem 7.2). Pseudocode for the algorithm is given in Appendix C.

A state-space model consists of a pair of discrete-time stochastic processes indexed by the time , where is a latent Markov process of interest and where is the observed process. We can think of each as a noisy and perhaps indirect measurement of . The Markov structure corresponding to the joint process is shown in Figure 7. The generalization of the results of this section to the case of missing observations is straightforward and will not be addressed here.

We assume that we are given the transition densities for all , sometimes referred to as the “prior dynamic,” together with the marginal density of the initial conditions . (For instance, the prior dynamic could stem from the discretization of a continuous time stochastic differential equation [81].) We denote by the likelihood function, i.e., the density of given , and assume that and are random variables taking values on and , respectively. Moreover, we denote by a sequence of realizations of the observed process that will define the posterior distribution over the unobserved (hidden) states of the model, and make the following regularity assumption in our theorems: for all . (The existence of underlying fully supported measures will be left implicit throughout the section for notational convenience.)

7.1 Smoothing and filtering: the full Bayesian solution

In typical applications of state-space modeling, the process is only observed sequentially, and thus the goal of inference is to characterize—sequentially in time and via a recursive algorithm—the joint distribution of the current and past states given currently available measurements, i.e.,

| (7.1) |

for all . That is, we wish to characterize based on our knowledge of the posterior distribution at the previous timestep, , and with an effort that is constant over time. We regard (7.1) as the full Bayesian solution to the sequential inference problem [104].

Usually, the task of updating to yield becomes increasingly challenging over time due to the widening inference horizon, making characterization of the full Bayesian solution impractical for large [104]. Thus, two simplifications of the sequential inference problem are frequently considered: filtering and smoothing [104]. In filtering, we characterize for all , while in smoothing we recursively update for increasing , where is some past state of the unobserved process. Both filtering and smoothing deliver particular low-dimensional marginals of the full Bayesian solution to the inference problem, and hence are often considered good candidates for numerical approximation [31, 104, 18].

The following theorem shows that characterizing the full Bayesian solution to the sequential inference problem via a decomposable transport map is essentially no harder than performing lag– smoothing, which, in turn, amounts to characterizing for all (an operation only incrementally harder than regular filtering). This result relies on the recursive application of the decomposition theorem for couplings (Theorem 6.1) to the tree Markov structure of . In what follows, let be an independent (reference) process with nonvanishing marginal densities , with each taking values on . See Figure 7 for the corresponding Markov network.

Theorem 7.1 (Decomposition theorem for state-space models).

Let be a sequence of -generalized KR rearrangements on , which are of the form

| (7.2) |

for some , , , and that are defined by the recursion:

-

–

pushes forward to ,

-

–

pushes forward to ,

where is a normalizing constant and where are functions on given by:

-

–

,

-

–

for .

Then, for all , the following hold:

-

1.

The map pushes forward to . [filtering]

-

2.

The map , defined as ( for )

(7.3) pushes forward to . [lag– smoothing]

-

3.

The composition of transport maps , where each is defined as

(7.4) pushes forward to . [full Bayesian solution]

-

4.

The model evidence (marginal likelihood) is given by

(7.5)

Theorem 7.1 suggests a variational algorithm for smoothing and filtering a continuous state-space model: compute the sequence of maps , each of dimension ; embed them into higher-dimensional identity maps to form according to (7.4); then evaluate the composition to sample directly from (i.e., the full Bayesian solution) and obtain information about any smoothing or filtering distribution of interest.

Successive transports in the composition are nested and thus ideal for sequential assimilation: given , we can obtain simply by computing an additional map of dimension —with no need to recompute . This step converts a transport map that samples into one that samples . This feature is important since is always a -dimensional map, while is a density on —a space whose dimension increases with time . In fact, from the perspective of Section 6, Theorem 7.1 simply shows that each can be represented via a decomposable transport . The sparsity pattern of each map , specified in (7.2), is necessary for Theorem 7.1 to hold: cannot be any transport map; it must be block upper triangular.

The proposed algorithm consists of a forward pass on the state-space model—wherein the sequence of transport maps are computed and stored—followed by a backward pass where the composition is evaluated deterministically to sample . This backward pass does not re-evaluate the potentials of the state-space model (e.g., transition kernels or likelihoods) at earlier times, nor does it perform any additional computation other than evaluating the maps in .

Though each map is usually trivial to evaluate—e.g., the map might be parameterized in terms of polynomials [73] and differ from the identity along only components—it is true that the cost of evaluating grows linearly with . This is hardly surprising since is a density over spaces of increasing dimension. A direct approximation of is usually a bad idea since the map is high-dimensional and dense (in the sense defined by Section 6); it is better to store implicitly through the sequence of maps , and sample smoothed trajectories by evaluating only when it is needed. If we are only interested in a particular smoothing marginal, e.g., for all , then we can define a general forward recursion to sample with a single transport map that is updated recursively over time, rather than with a growing composition of maps—and thus with a cost independent of . This construction is given in Section 7.4.

Also, it is important to emphasize that in order to assimilate a new measurement, say , we do not need to evaluate the full composition ; we only need to compute a low-dimensional map whose target density depends only on . The previous maps are unnecessary at this stage. Thus the effort of assimilating a new piece of data is constant in time—modulo the complexity of each .

The distribution is not represented via a collection of particles as increases, but rather via a growing composition of low-dimensional transport maps that yields fully supported approximations of . These maps are computed via deterministic optimization: there are no importance sampling or resampling steps. Intuitively, the optimization step for moves the particles on which the map is evaluated, rather than reweighing them.

Part 1 of Theorem 7.1 shows that the lower subcomponent of the map characterizes the filtering distribution for all , while Part 2 shows that each also characterizes the lag– smoothing distribution up to an invertible transformation of the marginal over . Thus, Theorem 7.1 implies a deterministic algorithm for lag– smoothing that in fact fully characterizes the posterior distribution of the nonlinear state-space model—much in the same spirit as the Rauch-Tung-Striebel (RTS) smoothing algorithm for Gaussian models. We clarify this connection in Section 7.2.

A related perspective on the proposed smoothing algorithm is that the composition of maps implements the following factorization of the full Bayesian solution,

| (7.6) |

wherein each map , due to its block upper triangular structure, is associated with a specific factorization of the lag– smoothing density,

| (7.7) |

Evaluating on samples drawn from the reference process amounts to sampling first from the final filtering marginal and then from the sequence of “backward” conditionals in (7.6). See also [59, 31, 43] for alternative approximations of the forward–filtering backward–smoothing formulas.

Note that the proposed approach does not reduce to the ensemble Kalman filter (EnKF) or to the ensemble Kalman smoother (EnKS) [35, 37], even if the maps are constrained to be linear. For one, the EnKF implements a two-step recursive approximation of each filtering marginal, which consists of (i) a particle approximation of the “forecast” distribution obtained by simulating the transition kernel , followed by (ii) a linear approximation of the forecast-to-analysis update (i.e., the update from to ). In contrast, our approach constructs a recursive variational approximation of each lag– smoothing distribution, essentially using numerical optimization to minimize the KL divergence between and its transport map approximation. We do not make a particle approximation of the forecast distribution by integrating the model dynamics, but instead require explicit evaluations of the transition density . If, however, the dynamics of the state-space model are linear, with Gaussian transition/observational noise and Gaussian initial conditions, then the proposed algorithm is equivalent to filtering and smoothing via “exact” Kalman formulas; in this case, the EnKF and EnKS can be interpreted as Monte Carlo approximations of the recursions defined by the proposed algorithm [87].

Numerical approximations.

In general, the maps must be approximated numerically (see Section 3). As a result, Monte Carlo estimators associated with the evaluation of are biased, although possibly with negligible variance, since it is trivial to evaluate the map a large number of times. This bias is only due to the numerical approximation of , and not to the particular factorization properties of . In practice, one might either accept this bias or try to reduce it. The bias can be reduced in at least two ways: (1) by enriching the parameterization of some , and thus increasing the accuracy of the variational approximation, or (2) by using the map-induced proposal density —i.e., the pushforward of a marginal of the reference process through —within importance sampling or MCMC (see Section 8). For instance, the weight function

| (7.8) |

is readily available, and can be used to yield consistent estimators with respect to the smoothing distribution. However, the resulting weights cannot be computed recursively in time, because even though the small dimensional maps are computed sequentially, the map-induced proposal changes entirely at every step.

In particle filters, the complexity of approximating the underlying distribution is given by the number of particles . In the proposed variational approach, the complexity of the approximation depends on the parameterization of each map . There is no single parameter like to describe the complexity of the latter—though, broadly, it should depend on the number of degrees of freedom in the parameterization. In some cases, one might think of using the total order of a multivariate polynomial expansion of each component of the map as a tuning parameter. But this is far from general or practical in high dimensions. The virtue of a functional representation of the transport map is the ability to carefully select the degrees of freedom of the parameterization. For instance, we might model local interactions between different groups of input variables using different approximation orders or even different sets of basis functions. This freedom should not be frightening, but rather embraced as a rich opportunity to exploit the structure of the particular problem at hand. (See [109, Chapter 6] for an example of this practice in the context of filtering high-dimensional spatiotemporal processes with chaotic dynamics.) In general, richer parameterizations of the maps are more costly to characterize because they lead to higher-dimensional optimization problems (3). Yet, richer parameterizations can yield arbitrarily accurate results. There is clearly a tradeoff between computational cost and statistical accuracy. We investigate this tradeoff numerically in Section 8, where we report the cost of computing a transport map under different parameterizations and inference scenarios.

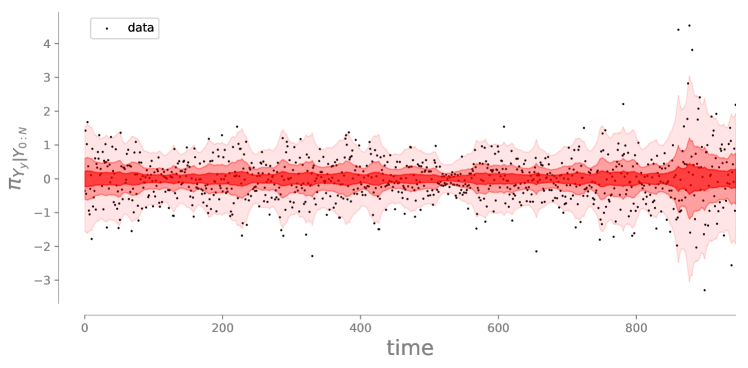

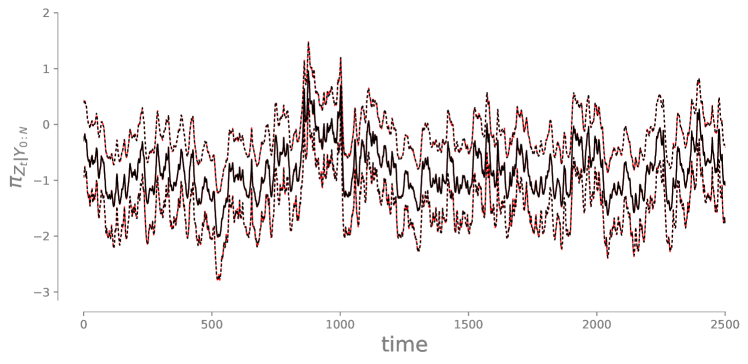

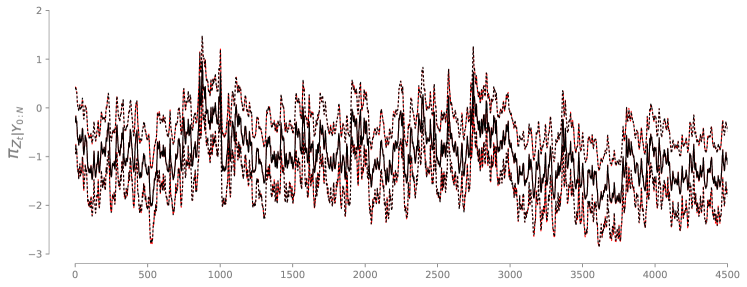

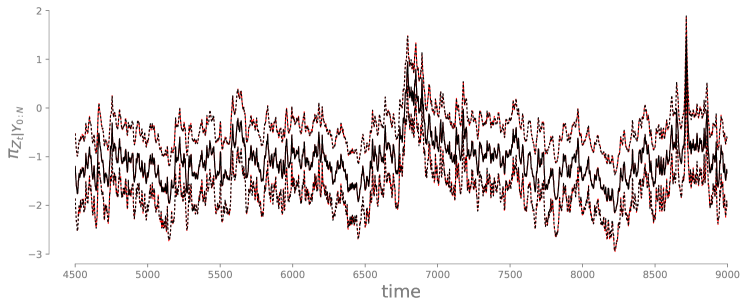

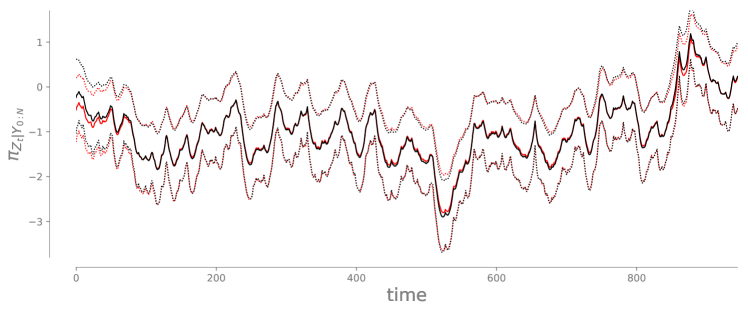

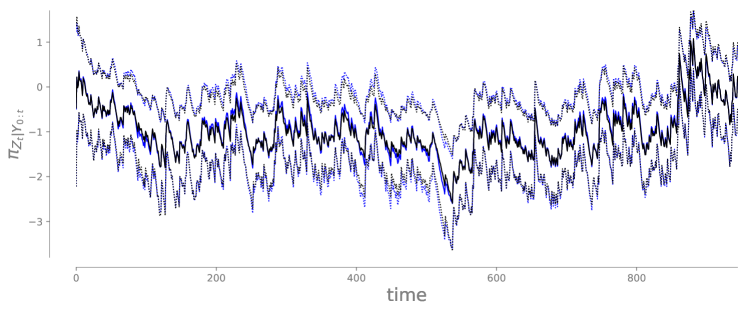

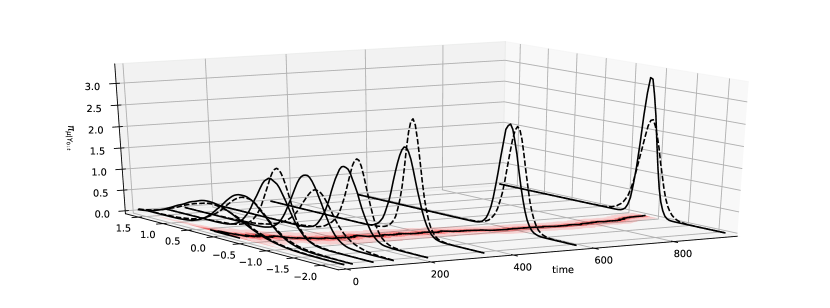

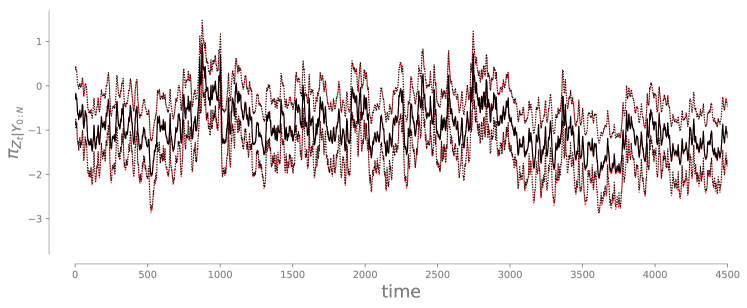

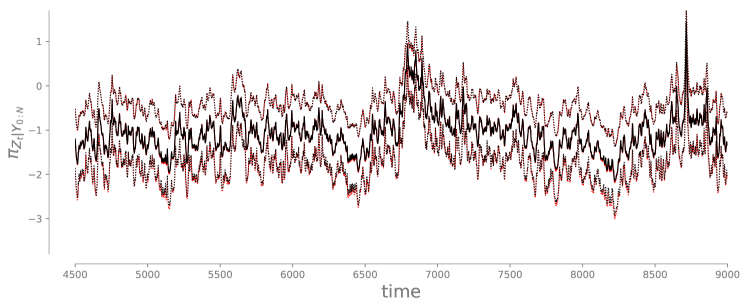

Another important note: the sequential approximation of the individual maps might present additional challenges due to the accumulation of error, since the target density for the -th map depends on the numerical approximation of the previous map, . This is not an issue with the factorization of per se, but rather with sequentially computing each element of the factorization. The analysis of sequential Monte Carlo methods (e.g., [18, 25, 107]) addresses a similar accumulation of error, but has not yet been extended to sequential variational inference techniques. In Section 8, we empirically investigate the stability of variational transport map approximations for a problem of very long time smoothing (see Figure 17), showing excellent results—at least for the reconstruction of low-order smoothing marginals.

As shown in (3.9), the computation of each is also associated with an approximation of the normalizing constant of its own target density, which then leads to a one-pass approximation of the marginal likelihood using (7.5).

One last remark: the proof of Theorem 7.1 shows that the triangular structure hypothesis for each can be relaxed provided that the underlying densities are regular enough. The following corollary clarifies this point.

Corollary 7.1.

Filtering and smoothing are of course very rich problems, and in this section we have by no means attempted to be exhaustive. Rather, our goal was to highlight some implications of decomposable transports on problems of sequential Bayesian inference, in a general non-Gaussian setting.

7.2 The linear Gaussian case: connection with the RTS smoother

In this section, we specialize the results of Theorem 7.1 to linear Gaussian state-space models, and make explicit the connection with the RTS Gaussian smoother [90].

Consider a linear Gaussian state-space model defined by

| (7.9) | |||||

for all , where , , , , and . Both and are independent of , while , and are symmetric positive definite matrices for all .

If we choose an independent reference process with standard normal marginals, i.e., , then the maps of Theorem 7.1 can be chosen to be linear:

| (7.10) |

for some matrices and . (Notice that in this case Corollary 7.1 applies and the matrices can be full and not necessarily triangular.) The following lemma gives a closed form expression for the maps with . ( can be derived analogously with simple algebra.)

Lemma 7.1 (The linear Gaussian case).

The formulas in Lemma 7.1 can be interpreted as one possible implementation of a square-root RTS smoother for Gaussian models: at each step of a forward pass, the filtering estimates are augmented with a collection of stored quantities, which can then be reused to sample the full Bayesian solution (or particular smoothing marginals) whenever needed, and without ever touching the state-space model again. In this sense, the algorithm proposed in Section 7.1 can be understood as the natural generalization—to the non-Gaussian case—of the square-root RTS smoother.

7.3 Sequential joint parameter and state estimation

In defining a state-space model, it is common to parameterize the transition densities of the unobserved process or the likelihoods of the observables in terms of some hyperparameters . The Markov structure of the resulting Bayesian hierarchical model, conditioned on the data, is shown in Figure 8. The state-space model is now fully specified in terms of the conditional densities , , , and the marginal . We assume that the hyperparameters take values on , and that the following regularity conditions hold: for all .

Given such a parameterization, one often wishes to jointly infer the hidden states and the hyperparameters of the model as observations of the process become available. That is, the goal of inference is to characterize, via a recursive algorithm, the sequence of posterior distributions given by

| (7.12) |

for all and for a sequence of observations. The following theorem shows that we can characterize (7.12) by computing a sequence of low-dimensional transport maps in the same spirit as Theorem 7.1. In what follows, let be an independent process with marginals as defined in Theorem 7.1 and let be a random variable on that is independent of and with nonvanishing density .

Theorem 7.2 (Decomposition theorem for joint parameter and state estimation).

Let be a sequence of -generalized KR rearrangements on , which are of the form

| (7.13) |

for some , , , , and that are defined by the recursion:

-

–

pushes forward to

(7.14) -

–

pushes forward to

(7.15)

where is a normalizing constant, the map for all , and where are functions on given by:

-

–

,

-

–

for .

Then, for all , the following hold:

-

1.

The map , defined as

(7.16) pushes forward to . [filtering]

-

2.

The composition of transport maps , where each is defined as

(7.17) pushes forward to . [full Bayesian solution]

-

3.

The model evidence (marginal likelihood) is given by (7.5).

Theorem 7.2 suggests a variational algorithm for the joint parameter and state estimation problem that is similar to the one proposed in Theorem 7.1: compute the sequence of maps , each of dimension ; embed them into higher-dimensional identity maps to form according to (7.17); then evaluate the composition to sample directly from (i.e., the full Bayesian solution). See Appendix C for more details. Each map is now of dimension twice that of the model state plus the dimension of the hyperparameters. This dimension is slightly higher than that of the maps considered in Theorem 7.1, and should be regarded as the price to pay for introducing hyperparameters in the state-space model and having to deal with the Markov structure of Figure 8 as opposed to the tree structure of Figure 7. By Theorem 7.2[Part 1], the composition of maps provides a recursive characterization of the posterior distribution over the static parameters, , for all . The latter is often the ultimate goal of inference [2]. In order to have a sequential algorithm for parameter estimation, we also need to keep a running approximation of using the recursion —e.g., via regression—so that the cost of evaluating does not grow with .

Even in the joint parameter and state estimation case, only a single forward pass with local computations is necessary to gather all the information from the state-space model needed to sample the collection of posteriors . Notice that the accuracy of the variational procedure is only limited by the accuracy of each computed map, and that the proposed approach does not prescribe an artificial dynamic for the parameters [60, 68], or an a priori fixed-lag smoothing approximation [86]. Yet there is no rigorous proof that the performance of the proposed sequential algorithm for parameter estimation does not deteriorate with time. Indeed, developing exact, sequential, and online algorithms for parameter estimation in general non-Gaussian state-space models is among the chief research challenges in SMC methods [52]. See [15, 19, 26] for recent contributions in this direction and [55] for a review of SMC approaches to Bayesian parameter inference. See also [34] for a hybrid approach that combines elements of variational inference with particle filters.

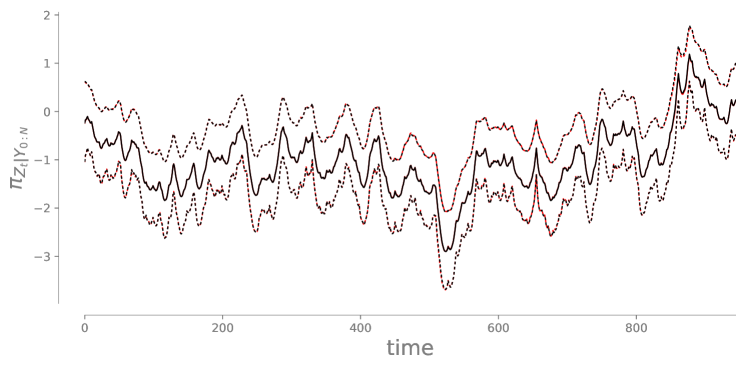

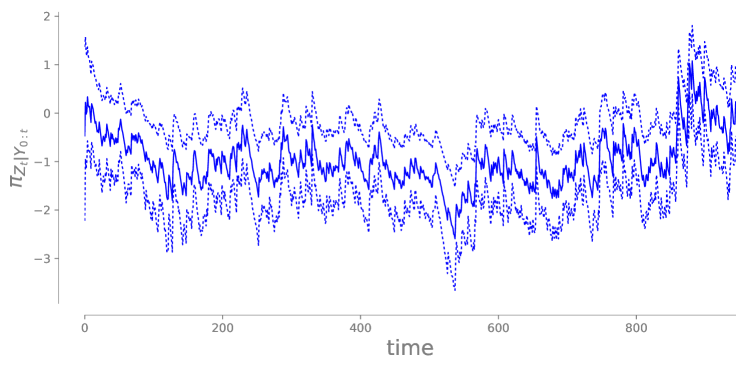

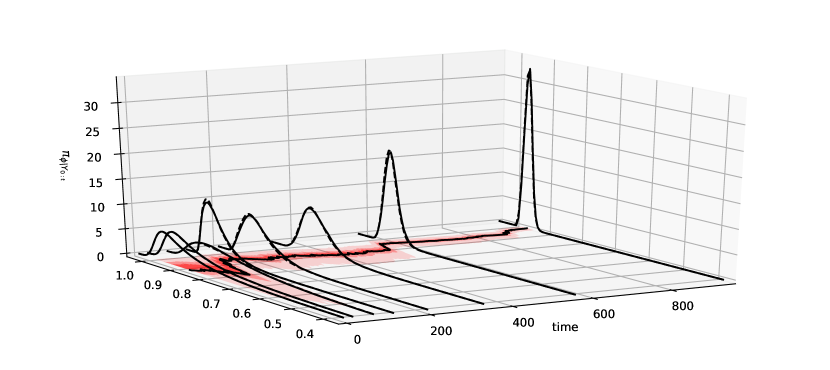

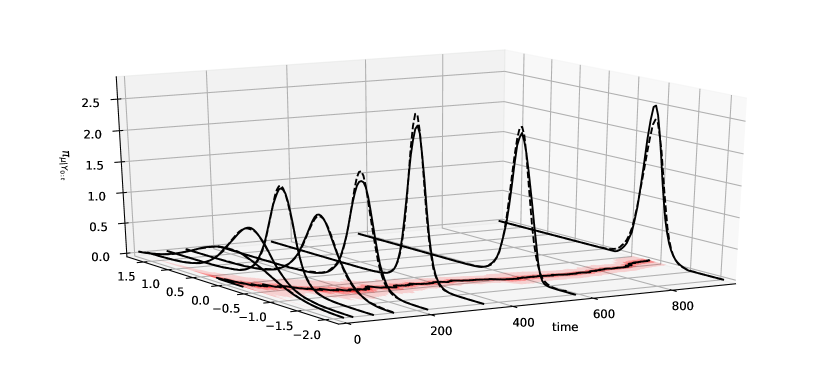

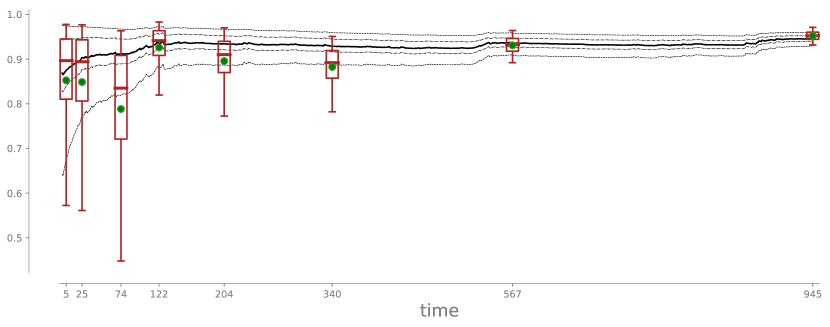

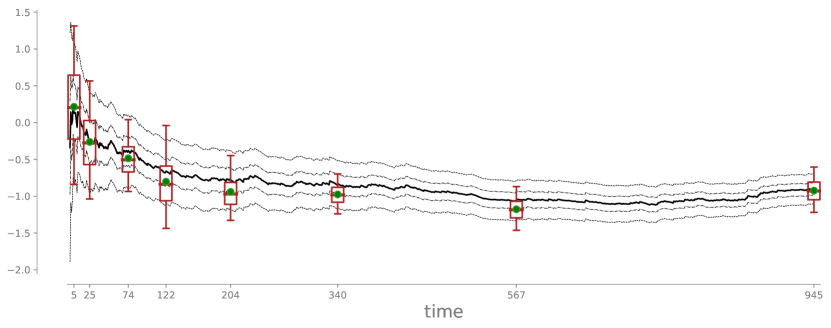

We refer the reader to Section 8 for a numerical illustration of parameter inference with transport maps involving a stochastic volatility model.

7.4 Fixed-point smoothing

Consider again the problem of sequential inference in a state-space model without static parameters (see Figure 7), and suppose that we are interested only in the smoothing marginal for all ; this is the fixed-point smoothing problem [104].