∎

Tianxiao Sun 22institutetext: Quoc Tran-Dinh 33institutetext: Department of Statistics and Operations Research, University of North Carolina at Chapel Hill (UNC)

318 Hanes Hall, CB# 3260, UNC Chapel Hill, NC 27599-3260

Email: {tianxias, quoctd}@email.unc.edu

Generalized Self-Concordant Functions: A Recipe for Newton-Type Methods

Abstract

We study the smooth structure of convex functions by generalizing a powerful concept so-called self-concordance introduced by Nesterov and Nemirovskii in the early 1990s to a broader class of convex functions which we call generalized self-concordant functions. This notion allows us to develop a unified framework for designing Newton-type methods to solve convex optimization problems. The proposed theory provides a mathematical tool to analyze both local and global convergence of Newton-type methods without imposing unverifiable assumptions as long as the underlying functionals fall into our class of generalized self-concordant functions. First, we introduce the class of generalized self-concordant functions which covers the class of standard self-concordant functions as a special case. Next, we establish several properties and key estimates of this function class which can be used to design numerical methods. Then, we apply this theory to develop several Newton-type methods for solving a class of smooth convex optimization problems involving generalized self-concordant functions. We provide an explicit step-size for a damped-step Newton-type scheme which can guarantee a global convergence without performing any globalization strategy. We also prove a local quadratic convergence of this method and its full-step variant without requiring the Lipschitz continuity of the objective Hessian mapping. Then, we extend our result to develop proximal Newton-type methods for a class of composite convex minimization problems involving generalized self-concordant functions. We also achieve both global and local convergence without additional assumptions. Finally, we verify our theoretical results via several numerical examples, and compare them with existing methods.

Keywords:

Generalized self-concordance Newton-type method proximal Newton method quadratic convergence local and global convergence convex optimizationMSC:

90C25 90-081 Introduction

The Newton method is a classical numerical scheme for solving systems of nonlinear equations and smooth optimization Nocedal2006 ; Ortega2000 . However, there are at least two reasons that prevent the use of such methods from solving large-scale problems. Firstly, while these methods often have a fast local convergence rate which can be up to a quadratic rate, their global convergence has not been well-understood Nesterov2006 . In practice, one can use a damped-step scheme utilizing the Lipschitz constant of the objective derivatives to compute a suitable step-size as often seen in gradient-type methods, or incorporate the algorithm with a globalization strategy such as line-search, trust-region, or filter to guarantee a descent property Nocedal2006 . Both strategies allow us to prove a global convergence of the underlying Newton-type method in some sense. Unfortunately, in practice, there exist several problems whose objective function does not have global Lipschitz gradient or Hessian such as logarithmic or reciprocal functions. This class of problems does not provide us some uniform bounds to obtain a constant step-size in optimization algorithms. On the other hand, using a globalization strategy for determining step-sizes often requires centralized computation such as function evaluations which prevent us from using distributed computation and stochastic descent methods. Secondly, Newton algorithms are second-order methods which often require a high per-iteration complexity due to the operations on the Hessian mapping of the objective function or its approximations. In addition, these methods require the underlying functionals to be smooth up to a given smoothness levels which does not often hold in many practical models.

Motivation:

In recent years, there has been a great interest in Newton-type methods for solving convex optimization problems and monotone equations due to the development of new techniques and mathematical tools in optimization, machine learning, and randomized algorithms Becker2012a ; byrd2016stochastic ; Deuflhard2006 ; erdogdu2015convergence ; Lee2014 ; Nesterov2006b ; Nesterov2008b ; pilanci2015newton ; polyak2009regularized ; Roosta-Khorasani2016 ; roosta2016sub ; Tran-Dinh2013b . Several combinations of Newton-type methods and other techniques such as proximal operators Bonnans1994a , cubic regularization Nesterov2006b , gradient regularization polyak2009regularized , randomized algorithms such as sketching pilanci2015newton , subsampling erdogdu2015convergence , and fast eigen-decomposition halko2009finding have opened up a new research direction and attracted a great attention in solving nonsmooth and large-scale problems. Hitherto, research in this direction remains focusing on specific classes of problems where standard assumptions such as nonsingularity and Hessian Lipschitz continuity are preserved. However, such assumptions do not hold for many other examples as shown in Tran-Dinh2013a . Moreover, if they are satisfied, then we often get a lower bound of possible step-sizes for our algorithm which may lead to a poor performance, especially in large-scale problems.

In the seminal work Nesterov1994 , Nesterov and Nemirovskii showed that the class of log-barriers does not satisfy the standard assumptions of the Newton method if the solution of the underlying problem is closed to the boundary of the barrier function domain. They introduced a powerful concept called “self-concordance” to overcome this drawback and developed new Newton schemes to achieve global and local convergence without requiring any additional assumption, or a globalization strategy. While the self-concordance notion was initially invented to study interior-point methods, it is less well-known in other communities. Recent works Bach2009 ; cohen2017matrix ; monteiro2015hybrid ; Tran-Dinh2013a ; TranDinh2016c ; zhang2015disco have popularized this concept to solve other problems arising from machine learning, statistics, image processing, scientific computing, and variational inequalities.

Our goals:

In this paper, motivated by Bach2009 ; TranDinh2014d ; zhang2015disco , we aim at generalizing the self-concordance concept in Nesterov1994 to a broader class of smooth and convex functions. To illustrate our idea, we consider a univariate smooth and convex function . If satisfies the inequality for all in the domain of and for a given constant , then we say that is self-concordant (in Nesterov and Nemirovskii’s sense Nesterov1994 ). We instead generalize this inequality to

| (1) |

for all in the domain of , and for given constants and .

We emphasize that generalizing from univariate to multivariate functions in the standard self-concordant case (i.e., ) Nesterov1994 preserves several important properties including the multilinear symmetry (Nesterov2004, , Lemma 4.1.2), while, unfortunately, they do not hold for the case . Therefore, we modify the definition in Nesterov1994 to overcome this drawback. Note that a similar idea has been also studied in Bach2009 ; TranDinh2014d for a class of logistic-type functions. Nevertheless, the definition using in these papers is limited, and still creates certain difficulty for developing further theory in general cases.

Our second goal is to develop a unified mechanism to analyze convergence (including global and local convergence) of the following Newton-type scheme:

| (2) |

where can be represented as the right-hand side of a smooth monotone equation , or the optimality condition of a convex optimization or a convex-concave saddle-point problem, is the Jacobian map of , and is a given step-size. Despite the Newton scheme (2) is invariant to a change of variables Deuflhard2006 , its convergence property relies on the growth of the Hessian mapping along the Newton iterative process. In classical settings, the Lipschitz continuity and the non-degeneracy of the Hessian mapping in a neighborhood of a given solution are key assumptions to achieve local quadratic convergence rate Deuflhard2006 . These assumptions have been considered to be standard, but they are often very difficult to check in practice, especially the second requirement. A natural idea is to classify the functionals of the underlying problem into a known class of functions to choose a suitable method for minimizing it. While first-order methods for convex optimization essentially rely on the Lipschitz gradient continuity, Newton schemes usually use the Lipschitz continuity of the Hessian mapping and its non-degeneracy to obtain a well-defined Newton direction as we have mentioned. For self-concordant functions, the second condition automatically holds, but the first assumption fails to satisfy. However, both full-step and damped-step Newton methods still work in this case by appropriately choosing a suitable metric. This situation has been observed and standard assumptions have been modified in different directions to still guarantee convergence of Newton-type methods, see Deuflhard2006 for an intensive study of generic Newton-type methods, and Nesterov1994 ; Nesterov2004 for the self-concordant function class.

Our approach:

We attempt to develop some background theory for a broad class of smooth and convex functions under the structure (1). By adopting the local norm defined via the Hessian mapping of such a convex function from Nesterov1994 , we can prove some lower and upper bound estimates for the local norm distance between two points in the domain as well as for the growth of the Hessian mapping. Together with this background theory, we also identify a class of functions using in generalized linear models mccullagh1989generalized ; nelder1972generalized as well as in empirical risk minimization vapnik1998statistical that falls into our generalized self-concordance class for many well-known loss-type functions as listed in Table 2.

Applying our generalized self-concordant theory, we develop a class of Newton-type methods to solve the following composite convex minimization problem:

| (3) |

where is a generalized self-concordant function in our context, and is a proper, closed, and convex function that can be referred to as a regularization term. We consider two cases. The first case is a non-composite convex problem in which is vanished (i.e., ). In the second case, we assume that is equipped with a “tractably” proximal operator (see (34) for the definition).

Our contribution:

To this end, our main contribution can be summarized as follows.

-

We generalize the self-concordant notion in Nesterov2004 to a more broader class of smooth convex functions which we call generalized self-concordance. We identify several loss-type functions that can be cast into our generalized self-concordant class. We also prove several fundamental properties and show that the sum and linear transformation of generalized self-concordant functions are generalized self-concordant for a given range of or under suitable assumptions.

-

We develop lower and upper bounds on the Hessian mapping, the gradient mapping, and the function values for generalized self-concordant functions. These estimates are key to analyze several numerical optimization methods including Newton-type methods.

-

We propose a class of Newton methods including full-step and damped-step schemes to minimize a generalized self-concordant function. We explicitly show how to choose a suitable step-size to guarantee a descent direction in the damped-step scheme, and prove a local quadratic convergence for both the damped-step and the full-step schemes using a suitable metric.

-

We also extend our Newton schemes to handle the composite setting (3). We develop both full-step and damped-step proximal Newton methods to solve this problem and provide a rigorous theoretical convergence guarantee in both local and global sense.

-

We also study a quasi-Newton variant of our Newton scheme to minimize a generalized self-concordant function. Under a modification of the well-known Dennis-Moré condition Dennis1974 or a BFGS update, we show that our quasi-Newton method locally converges at a superlinear rate to the solution of the underlying problem.

Let us emphasize the following aspects of our contribution. Firstly, we observe that the self-concordance notion is a powerful concept and has widely been used in interior-point methods as well as in other optimization schemes He2016 ; Lu2016a ; Tran-Dinh2013a ; zhang2015disco , generalizing it to a broader class of smooth convex functions can substantially cover a number of new applications or can develop new methods for solving old problems including logistic and multimonomial logistic regression, optimization involving exponential objectives, and distance-weighted discrimination problems in support vector machine (see Table 2 below). Secondly, verifying theoretical assumptions for convergence guarantees of a Newton method is not trivial, our theory allows one to classify the underlying functions into different subclasses by using different parameters and in order to choose suitable algorithms to solve the corresponding optimization problem. Thirdly, the theory developed in this paper can potentially apply to other optimization methods such as gradient-type, sketching and sub-sampling Newton, and Frank-Wolfe’s algorithms as done in the literature odor2016frank ; pilanci2015newton ; Roosta-Khorasani2016 ; roosta2016sub ; Tran-Dinh2013a . Finally, our generalization also shows that it is possible to impose additional structure such as self-concordant barrier to develop path-following scheme or interior-point-type methods for solving a subclass of composite convex minimization problems of the form (3). We believe that our theory is not limited to convex optimization, but can be extended to solve convex-concave saddle-point problems, and monotone equations/inclusions involving generalized self-concordant functions TranDinh2016c .

Summary of generalized self-concordant properties:

For our reference convenience, we provide a short summary on the main properties of generalized self-concordant (gsc) functions in Table 1.

| Result | Property | Range of |

|---|---|---|

| Definitions 1 and 2 | definitions of gsc functions | |

| Proposition 1 | sum of gsc functions | |

| Proposition 2 | affine transformation of gsc functions with |

for general

for over-completed |

| Proposition 3(a) | non-degenerate property | |

| Proposition 3(b) | unboundedness | |

| Proposition 4(a) | gsc and strong convexity | |

| Proposition 4(b) | gsc and Lipschitz gradient continuity | |

| Proposition 6 |

if is the conjugate of a gsc function

, then |

if (univariate)

if (multivariate) |

| Propositions 7, 8, 9, and 10 | local norm, Hessian, gradient, and function value bounds |

Although several results hold for a different range of , the complete theory only holds for . However, this is sufficient to cover two important cases: in Bach2009 ; Bach2013a and in Nesterov1994 .

Related work:

Since the self-concordance concept was introduced in 1990s Nesterov1994 , its first extension is perhaps proposed by Bach2009 for a class of logistic regression. In TranDinh2014d , the authors extended Bach2009 to study proximal Newton method for logistic, multinomial logistic, and exponential loss functions. By augmenting a strongly convex regularizer, Zhang and Lin in zhang2015disco showed that the regularized logistic loss function is indeed standard self-concordant. In Bach2013a Bach continued exploiting his result in Bach2009 to show that the averaging stochastic gradient method can achieve the same best-known convergence rate as in strongly convex case without adding a regularizer. In Tran-Dinh2013a , the authors exploited standard self-concordance theory in Nesterov1994 to develop several classes of optimization algorithms including proximal Newton, proximal quasi-Newton, and proximal gradient methods to solve composite convex minimization problems. In Lu2016a , Lu extended Tran-Dinh2013a to study randomized block coordinate descent methods. In a recent paper gao2016quasi , Gao and Goldfarb investigated quasi-Newton methods for self-concordant problems. As another example, peng2009self proposed an alternative to the standard self-concordance, called self-regularity. The authors applied this theory to develop a new paradigm for interior-point methods. The theory developed in this paper, on the one hand, is a generalization of the well-known self-concordance notion developed in Nesterov1994 ; on the other hand, it also covers the work in Bach2009 ; Tran-Dinh2013b ; zhang2015disco as specific examples. Several concrete applications and extensions of self-concordance notion can also be found in the literature including He2016 ; Kyrillidis2014 ; odor2016frank ; peng2009self . Recently, cohen2017matrix exploited smooth structures of exponential functions to design interior-point methods for solving two fundamental problems in scientific computing called matrix scaling and balancing.

Paper organization:

The rest of this paper is organized as follows. Section 2 develops the foundation theory for our generalized self-concordant functions including definitions, examples, basic properties, Fenchel’s conjugate, smoothing technique, and key bounds. Section 3 is devoted to studying full-step and damped-step Newton schemes to minimize a generalized self-concordant function including their global and local convergence guarantees. Section 4 considers to the composite setting (3) and studies proximal Newton-type methods, and investigates their convergence guarantees. Section 5 deals with a quasi-Newton scheme for solving the noncomposite problem of (3). Numerical examples are provided in Section 6 to illustrate advantages of our theory. Finally, for clarity of presentation, several technical results and proofs are moved to the appendix.

2 Theory of generalized self-concordant functions

We generalize the class of self-concordant functions introduced by Nesterov and Nemirovskii in Nesterov2004 to a broader class of smooth and convex functions. We identify several examples of such functions. Then, we develop several properties of this function class by utilizing our new definitions.

Notation:

Given a proper, closed, and convex function , we denote by the domain of , and by the subdifferential of at . We use to denote the class of three times continuously differentiable functions on its open domain . We denote by its gradient map, by its Hessian map, and by its third-order derivative. For a twice continuously differentiable convex function , is symmetric positive semidefinite, and can be written as . If it is positive definite, then we write .

Let and denote the sets of nonnegative and positive real numbers, respectively. We use and to denote the sets of symmetric positive semidefinite and symmetric positive definite matrices of the size , respectively. Given a matrix , we define a weighted norm with respect to as for . The corresponding dual norm is . If , the identity matrix, then , where is the standard Euclidean norm. Note that .

We say that is strongly convex with the strong convexity parameter if is convex. We also say that has Lipschitz gradient if is Lipschitz continuous with the Lipschitz constant , i.e., for all .

For , if at a given , then we define a local norm as a weighted norm of with respect to . The corresponding dual norm , is defined as for .

2.1 Univariate generalized self-concordant functions

Let be a three times continuously differentiable function on the open domain . Then, we write . In this case, is convex if and only if for all . We introduce the following definition.

Definition 1

Let be a and univariate function with open domain , and and be two constants. We say that is -generalized self-concordant if

| (4) |

The inequality (4) also indicates that for all . Hence, is convex. Clearly, if for any constants and , we have and . The inequality (4) is automatically satisfied for any and . The smallest value of is zero. Hence, any convex quadratic function is -generalized self-concordant for any . While (4) holds for any other constant , we often require that is the smallest constant satisfying (4).

Example 1

Let us now provide some common examples satisfying Definition 1.

-

(a)

Standard self-concordant functions: If we choose , then (4) becomes which is the standard self-concordant functions in introduced in Nesterov1994 .

-

(b)

Logistic functions: In Bach2009 , Bach modified the standard self-concordant inequality in Nesterov1994 to obtain , and showed that the well-known logistic loss satisfies this definition. In TranDinh2014d the authors also exploited this definition, and developed a class of first-order and second-order methods to solve composite convex minimization problems. Hence, is a generalized self-concordant function with and .

-

(c)

Exponential functions: The exponential function also belongs to (4) with and . This function is often used, e.g., in Ada-boost lafferty2002boosting , or in matrix scaling cohen2017matrix .

-

(d)

Distance-weighted discrimination (DWD): We consider a more general function on and studied in marron2007distance for DWD using in support vector machine. As shown in Table 2, this function satisfies Definition 1 with and .

-

(e)

Entropy function: We consider the well-known entropy function for . We can easily show that . Hence, it is generalized self-concordant with and in the sense of Definition 1.

-

(f)

Arcsine distribution: We consider the function for . This function is convex and smooth. Moreover, we verify that it satisfies Definition 1 with and . We can generalize this function to for , where and . Then, we can show that .

-

(g)

Robust Regression: Consider a monomial function for studied in yang2016rsg for robust regression using in statistics. Then, and .

As concrete examples, the following table, Table 2, provides a non-exhaustive list of generalized self-concordant functions used in the literature.

| Function name | Form of | Application | Reference | ||||

|---|---|---|---|---|---|---|---|

| Log-barrier | 2 | Poisson | no | Boyd2004 ; Nesterov2004 ; Nesterov1994 | |||

| Entropy-barrier | 2 | Interior-point | no | Nesterov2004 | |||

| Logistic | 1 | Classification | yes | Hosmer2005 | |||

| Exponential | 1 | AdaBoost, etc | no | cohen2017matrix ; lafferty2002boosting | |||

| Negative power | DWD | no | marron2007distance | ||||

| Arcsine distribution | Random walks | no | Goel2006 | ||||

| Positive power | Regression | no | yang2016rsg | ||||

| Entropy | 1 | KL divergence | no | Boyd2004 |

Remark 1

All examples given in Table 2 fall into the case . However, we note that Definition 1 also covers (zhang2015disco, , Lemma 1) as a special case when . Unfortunately, as we will see in what follows, it is unclear how to generalize several properties of generalized self-concordance from univariate to multivariable functions for , except for strongly convex functions.

Table 2 only provides common generalized self-concordant functions using in practice. However, it is possible to combine these functions to obtain mixture functions that preserve the generalized self-concordant inequality given in Definition 1. For instance, the barrier entropy is a standard self-concordant function, and it is the sum of the entropy and the negative logarithmic function which are generalized self-concordant with and , respectively.

2.2 Multivariate generalized self-concordant functions

Let be a smooth and convex function with open domain . Given the Hessian of , , and , we consider the function . Then, it is obvious to show that

for such that , where is the third-order derivative of . It is clear that . By using the local norm, we generalize Definition 1 to multivariate functions as follows.

Definition 2

A -convex function is said to be an -generalized self-concordant function of the order and the constant if, for any and , it holds

| (5) |

Here, we use a convention that for the case or . We denote this class of functions by (shortly, when is explicitly defined).

Let us consider the following two extreme cases:

- 1.

-

2.

If and , (5) reduces to , Definition 2 becomes the standard self-concordant definition introduced in Nesterov2004 ; Nesterov1994 .

We emphasize that Definition 2 is not symmetric, but can avoid the use of multilinear mappings as required in Bach2009 ; Nesterov1994 . However, by (Nesterov1994, , Proposition 9.1.1) or (Nesterov2004, , Lemma 4.1.2), Definition 2 with is equivalent to (Nesterov2004, , Definition 4.1.1) for standard self-concordant functions.

2.3 Basic properties of generalized self-concordant functions

We first show that if and are two generalized self-concordant functions, then is also a generalized self-concordant for any according to Definition 2.

Proposition 1 (Sum of generalized self-concordant functions)

Let be -generalized self-concordant functions satisfying (5), where and for . Then, for , , the function is well-defined on , and is -generalized self-concordant with the same order and the constant

Proof

It is sufficient to prove for . For , it follows from by induction. By (Nesterov2004, , Theorem 3.1.5), is a closed and convex function. In addition, . Let us fix some and . Then, by Definition 2, we have

Denote and for . We can derive

| (6) | |||||

Let and . Then, and . Hence, the term in the square brackets of (6) becomes

Since and , we can upper bound as

The right-hand side function is linear in on . It achieves the maximum at its boundary. Hence, we have

Using this estimate into (6), we can show that is -generalized self-concordant with .

Using Proposition 1, we can also see that if is -generalized self-concordant, and , then is also -generalized self-concordant with the constant . The convex quadratic function with is -generalized self-concordant for any . Hence, by Proposition 1, if is -generalized self-concordant, then is also -generalized self-concordant.

Next, we consider an affine transformation of a generalized self-concordant function.

Proposition 2 (Affine transformation)

Let be an affine transformation from to , and be an -generalized self-concordant function with . Then, the following statements hold:

-

If , then is -generalized self-concordant with .

-

If and , then is -generalized self-concordant with , where is the smallest eigenvalue of .

Proof

Since , it is easy to show that and . Let us denote by , , and . Then, using Definition 2, we have

| (7) |

(a) If , then we have . Hence, the last inequality (7) implies

which shows that is -generalized self-concordant with .

(b) Note that , where is the smallest eigenvalue of . If and , then we have . Combining this estimate and (7), we can show that is -generalized self-concordant with .

Remark 2

Proposition 2 shows that generalized self-concordance is preserved via an affine transformations if . If , then it requires to be over-completed, i.e., . Hence, the theory developed in the sequel remains applicable for if is over-completed.

The following result is an extension of standard self-concordant functions whose proof is very similar to (Nesterov2004, , Theorems 4.1.3, 4.1.4) by replacing the parameters and with the general parameters and (or ), respectively. We omit the detailed proof.

Proposition 3

Let be an -generalized self-concordant function with . Then:

-

If and contains no straight line, then for any .

-

If there exists , the boundary of , then, for any , and any sequence such that , we have .

Note that Proposition 3(a) only holds for . If we consider for a given affine operator , then the non-degenerateness of is only guaranteed if is full-rank. Otherwise, it is non-degenerated in a given subspace of .

2.4 Generalized self-concordant functions with special structures

We first show that if a generalized self-concordant function is strongly convex or has a Lipschitz gradient, then it can be cast into the special case or .

Proposition 4

Let be an -generalized self-concordant with . Then:

-

If and is also strongly convex on with the strong convexity parameter in -norm, then is also -generalized self-concordant with and .

-

If and is Lipschitz continuous with the Lipschitz constant in -norm, then is also -generalized self-concordant with and .

Proof

(a) If is strongly convex with the strong convexity parameter in -norm, then we have for any . Hence, . In this case, (5) leads to

Hence, is - generalized self-concordant with and .

(b) Since is Lipschitz continuous with the Lipschitz constant in -norm, we have for all which leads to for all . On the other hand, with , we can show that

Hence, is also -generalized self-concordant with and .

Proposition 4 provides two important properties. If the gradient map of a generalized self-concordant function is Lipschitz continuous, we can always classify it into the special case . Therefore, we can exploit both structures: generalized self-concordance and Lipschitz gradient to develop better algorithms. This idea is also applied to generalized self-concordant and strongly convex functions.

Given smooth convex univariate functions satisfying (4) for with the same order , we consider the function defined by the following form:

| (8) |

where and are given vectors and numbers, respectively for . This convex function is called a finite sum and widely used in machine learning and statistics. The decomposable structure in (8) often appears in generalized linear models bollapragada2016exact ; byrd2016stochastic , and empirical risk minimization zhang2015disco , where is referred to as a loss function as can be found, e.g., in Table 2.

Next, we show that if is generalized self-concordant with , then is also generalized self-concordant. This result is a direct consequence of Proposition 1 and Proposition 2.

Corollary 1

Finally, we show that if we regularize in (8) by a strongly convex quadratic term, then the resulting function becomes self-concordant. The proof can follow the same path as (zhang2015disco, , Lemma 2).

2.5 Fenchel’s conjugate of generalized self-concordant functions

Primal-dual theory is fundamental in convex optimization. Hence, it is important to study the Fenchel conjugate of generalized self-concordant functions.

Let be an -generalized self-concordant function. We consider Fenchel’s conjugate of as

| (9) |

Since is proper, closed, and convex, is well-defined and also proper, closed, and convex. Moreover, since is smooth and convex, by Fermat’s rule, if satisfies , then is well-defined at . This shows that .

Example 2

Let us look at some univariate functions. By using (9), we can directly show that:

-

1.

If , then .

-

2.

If , then .

-

3.

If , then .

Intuitively, these examples show that if is generalized self-concordant, then its conjugate is also generalized self-concordant. For more examples, we refer to (Bauschke2011, , Chapter 13). Let us generalize this result in the following proposition whose proof is given in Appendix A.1.

Proposition 6

If is -generalized self-concordant in such that for , then the conjugate function of given by (9) is well-defined, and -generalized self-concordant on

where and provided that if and if .

Moreover, we have and , where is a unique solution of the maximization problem in (9) for any .

Proposition 6 allows us to apply our generalized self-concordance theory in this paper to the dual problem of a convex problem involving generalized self-concordant functions, especially, when the objective function of the primal problem is generalized self-concordant with . The Fenchel conjugates are certainly useful when we develop optimization algorithms to solve constrained convex optimization involving generalized self-concordant functions, see, e.g., TranDinh2012e ; TranDinh2012c .

2.6 Generalized self-concordant approximation of nonsmooth convex functions

Several well-known convex functions are nonsmooth. However, they can be approximated (up to an arbitrary accuracy) by a generalized self-concordant function via smoothing. Smoothing techniques clearly allow us to enrich the applicability of our theory to nonsmooth convex problems.

Given a proper, closed, possibly nonsmooth, and convex function . One can smooth using the following Nesterov’s smoothing technique Nesterov2005c

| (10) |

where is the Fenchel conjugate of , is a smooth convex function such that , and is called a smoothness parameter. In particular, if is Lipschitz continuous, then is bounded Bauschke2011 . Hence, the operator in (10) reduces to the operator.

Our goal is to choose an appropriate smoothing function such that the smoothed function is well-defined and generalized self-concordant for any fixed smoothness parameter .

Example 3

Let us provide a few examples with well-known nonsmooth convex functions:

-

(a)

Consider the -norm function in . Then, it can be rewritten as

We can smooth this function by by choosing . In this case, we obtain . This function is clearly generalized self-concordant with , see (TranDinh2014d, , Lemma 4).

However, if we choose , then we get . In this case, is also generalized self-concordant with and .

-

(b)

The hinge loss function can be written as . Hence, we can smooth this function by with a smoothness parameter . Clearly, is generalized self-concordant with .

In many practical problems, the conjugate of can be written as the sum , where is a generalized self-concordant function, and is the indicator function of a given nonempty, closed, and convex set . In this case, in (10) becomes

| (11) |

If is a generalized self-concordant such that , and , then is generalized self-concordant with as shown in Proposition 6.

2.7 Key bounds on Hessian map, gradient map, and function values

Now, we develop some key bounds on the local norms, Hessian map, gradient map, and function values of generalized self-concordant functions. In this subsection, we assume that the Hessian map of is nondegenerate at any point in its domain.

For this purpose, given , we define the following quantity for any :

| (12) |

Here, if , then we require . Otherwise, we set if . In addition, we also define the function as

| (13) |

with if , and if . We also adopt the Dikin ellipsoidal notion from Nesterov2004 as .

The next proposition provides a bound on the local norm defined by a generalized self-concordant function . This bound is given for the local distances and between two points and in .

Proposition 7 (Bound of local norms)

Proof

We first consider the case . Let and . Consider the following univariate function

It is easy to compute the derivative of this function, and obtain

Using Definition 2 with and instead of , we have . This implies that . On the other hand, we can see that . Hence, we have contains . Using this fact and the definition of , we can show that contains . However, since , the condition is equivalent to . This shows that .

Since , integrating over the interval we get

Using in the last inequality, we get which is equivalent to

given that . Taking the power of in both sides, we get (14) for the case .

Now, we consider the case . Let . We consider the following function

Clearly, it is easy to show that .

Using again Definition 2 with and instead of , we obtain .

Since , integrating over the interval we get

Substituting into this inequality, we get . Hence, . This inequality leads to (14) for the case .

Next, we develop new bounds for the Hessian map of in the following proposition.

Proposition 8 (Bounds of Hessian map)

Proof

Let and . Consider the following univariate function on :

If we denote by , then , , and . By Definition 2, we have

which implies

| (17) |

Assume that . Then, by the definition of and , we have and . Using Proposition 7, we can derive

Hence, we can further derive

Integrating with respect to on and using the last inequality and (17), we get

Clearly, we can compute this integral explicitly as

Rearranging this inequality, we obtain

Since this inequality holds for any , it implies (15). If , then (15) obviously holds.

The following corollary provides a bound on the mean of the Hessian map whose proof is moved to Appendix A.2.

Corollary 2

We prove a bound on the gradient inner product of a generalized self-concordant function .

Proposition 9 (Bounds of gradient map)

For any , we have

| (19) |

where, if , then the right-hand side inequality of (19) holds if , and

| (20) |

Here, for all .

Proof

Let . By the mean-value theorem, we have

| (21) |

We consider the function defined by (13). It follows from Proposition 7 that

Now, we note that and , the last estimate leads to

Substituting this estimate into (21), we obtain

Using the function from (13) to compute the left-hand side and the right-hand side integrals, we obtain (19).

Finally, we prove a bound on the function values of an -generalized self-concordant function in the following proposition.

Proposition 10 (Bounds of function values)

Proof

For any , let . Then, . By the mean-value theorem, we have

Now, by Proposition 9, we have

Clearly, by the definition (12), we have and . Combining these relations, and the above two inequalities, we can show that

By integrating the left-hand side and the right-hand side of this estimate using the definition (20) of , we obtain (22).

3 Generalized self-concordant minimization

We apply the theory developed in the previous sections to design new Newton-type methods to minimize a generalized self-concordant function. More precisely, we consider the following non-composite convex problem:

| (24) |

where is an -generalized self-concordant function in the sense of Definition 2 with and . Since is smooth and convex, the optimality condition is necessary and sufficient for to be an optimal solution of (24).

The following theorem shows the existence and uniqueness of the solution of (24). It can be considered as a special case of Theorem 4.1 below with .

Theorem 3.1

Suppose that for given parameters and . Denote by and for . Suppose further that there exists such that and

Then, problem (24) has a unique solution in .

We say that the unique solution of (24) is strongly regular if . The strong regularity of for (24) is equivalent to the strong second order optimality condition. Theorem 3.1 covers (Nesterov2004, , Theorem 4.1.11) for standard self-concordant functions as a special case.

We consider the following Newton-type scheme to solve (24). Starting from an arbitrary initial point , we generate a sequence as follows:

| (25) |

and is a given step-size. We call a Newton direction.

-

•

If for all , then we call (25) a full-step Newton scheme.

-

•

Otherwise, i.e., , we call (25) a damped-step Newton scheme.

Clearly, computing the Newton direction requires to solve the following linear system:

| (26) |

Next, we define a Newton decrement and a quantity , respectively as

| (27) |

With and given by (27), we also define

| (28) |

Let us first show how to choose a suitable step-size in the damped-step Newton scheme and prove its convergence properties in the following theorem whose proof can be found in Appendix A.5.

Theorem 3.2

Example 4 (Better step-size for regularized logistic and exponential models)

Consider the minimization problem (24) with the objective function , where is defined as in (8) with being the logistic loss. That is

As we shown in Section 2 that is either generalized self-concordant with or generalized self-concordant with but with different constant .

Let us define . Then, if we consider , then we have due to Corollary 1, while if we choose , then due to Proposition 4. By the definition of , we have . Hence, using this inequality and the definition of and from (27), we can show that

| (31) |

For any , we have . Using this elementary result and (31), we obtain

This inequality has shown that the step-size given by Theorem 3.2 satisfies , where is a given step-size computed by (29) for and , respectively. Such a statement confirms that the damped-step Newton method using is theoretically better than using . This result will be empirically confirmed by our experiments in Section 6.

Next, we study the full-step Newton scheme derived from (25) by setting the step-size for all as a full-step. Let

be the smallest eigenvalue of . Since , we have . The following theorem shows a local quadratic convergence of the full-step Newton scheme (25) for solving (24) whose proof can be found in Appendix A.6.

Theorem 3.3

Let be the sequence generated by the full-step Newton scheme (25) by setting the step-size for . Let be defined by (12) and be defined by (27). Then, the following statements hold:

-

If and the starting point satisfies , then both sequences and decrease and quadratically converge to zero, where .

-

If , and the starting point satisfies , then both sequences and decrease and quadratically converge to zero, where is the unique solution of the equation in with given by (56).

-

If and the starting point satisfies , then the sequence decreases and quadratically converges to zero.

As a consequence, if locally converges to zero at a quadratic rate, then also locally converges to zero at a quadratic rate, where , the identity matrix, if ; if ; and if . Hence, locally converges to , the unique solution of (24), at a quadratic rate.

If we combine the results of Theorem 3.2 and Theorem 3.3, then we can design a two-phase Newton algorithm for solving (24) as follows:

- •

- •

We also note that the damped-step Newton scheme (25) can also achieve a local quadratic convergence as shown in Theorem 3.2. Hence, we combine this fact and the above two-phase scheme to derive the Newton algorithm as shown in Algorithm 1 below.

Per-iteration complexity:

The main step of Algorithm 1 is the solution of the symmetric positive definite linear system (26). This system can be solved by using either Cholesky factorization or conjugate gradient methods which, in the worst-case, requires operations. Computing requires the inner product which needs operations.

Conceptually, the two-phase option of Algorithm 1 requires the smallest eigenvalue of to terminate Phase 1. However, switching from Phase 1 to Phase 2 can be done automatically allowing some tolerance in the step-size . Indeed, the step-size given by (29) converges to as . Hence, when is closed to , e.g., , we can automatically set it to and remove the computation of to reduce the computational time.

In the one-phase option, we can always perform only Phase 1 until achieving an -optimal solution as shown in Theorem 3.2. Therefore, the per-iteration complexity of Algorithm 1 is in the worst-case. A careful implementation of conjugate gradient methods with a warm-start can significantly reduce this per-iteration computation complexity.

Remark 3 (Inexact Newton methods)

We can allow Algorithm 1 to compute the Newton direction approximately. In this case, we approximately solve the symmetric positive definite system (26). By an appropriate choice of stopping criterion, we can still prove convergence of Algorithm 1 under inexact computation of . For instance, the following criterion is often used in inexact Newton methods Deuflhard2006 , but defined via the local dual norm of :

for a given relaxation parameter . This extension can be found in our forthcoming work.

4 Composite generalized self-concordant minimization

Let , and be a proper, closed, and convex function. We consider the composite convex minimization problem (3) which we recall here for our convenience of references:

| (32) |

Note that may be empty. To make this problem nontrivial, we assume that is nonempty. The optimality condition for (32) can be written as follows:

| (33) |

Under the qualification condition , (33) is necessary and sufficient for to be an optimal solution of (32), where is the relative interior of .

4.1 Existence, uniqueness, and regularity of optimal solutions

Assume that is positive definite (i.e., nonsingular) at some point . We prove in the following theorem that problem (32) has a unique solution . The proof can be found in Appendix A.4. This theorem can also be considered as a generalization of (Nesterov2004, , Theorem 4.1.11) and (Tran-Dinh2013a, , Lemma 4) in standard self-concordant settings in Nesterov2004 ; Tran-Dinh2013a .

Theorem 4.1

Now, we recall a condition such that the solution of (32) is strongly regular in the following Robinson’s sense Robinson1980 . We say that the optimal solution of (32) is strongly regular if there exists a neighborhood of zero such that for any , the following perturbed problem

has a unique solution , and this solution is Lipschitz continuous on .

If , then is strongly regular. While the strong regularity of the solution requires a weaker condition than . For further details of the regularity theory, we refer the reader to Robinson1980 .

4.2 Scaled proximal operators

Given a matrix , we define a scaled proximal operator of in (32) as

| (34) |

Using the optimality condition of the minimization problem under (34), we can show that

Since is proper, closed, and convex, is well-defined and single-valued. In particular, if we take , the identity matrix, then , the standard proximal operator of . If we can efficiently compute by a closed form or by polynomial time algorithms, then we say that is proximally tractable. There exist several convex functions whose proximal operator is tractable. Examples such as -norm, coordinate-wise separable convex functions, and the indicator of simple convex sets can be found in the literature including Bauschke2011 ; friedlander2016efficient ; Parikh2013 .

4.3 Proximal Newton methods

The proximal Newton method can be considered as a special case of the variable metric proximal method in the literature Bonnans1994a . This method has previously been studied by many authors, see, e.g., Bonnans1994a ; Lee2014 . However, the convergence guarantee often requires certain assumptions as used in standard Newton-type methods. In this section, we develop a proximal Newton algorithm to solve the composite convex minimization problem (32) where is a generalized self-concordant function. This problem covers Tran-Dinh2013a ; Tran-Dinh2013 as special cases.

Given , we first approximate at by the following convex quadratic surrogate:

Next, the main step of the proximal Newton method requires to solve the following subproblem:

| (35) |

The optimality condition for this subproblem is the following linear monotone inclusion:

| (36) |

Here, we note that . Hence, . In the setting (32), may not be in . Our next step is to update the next iteration as

| (37) |

where is the proximal Newton direction, and is a given step size.

Associated with the proximal Newton direction , we define the following proximal Newton decrement and the -norm quantity of as

| (38) |

Our first goal is to show that we can explicitly compute the step-size in (37) using and such that we obtain a descent property for . This statement is presented in the following theorem whose proof is deferred to Appendix A.7.

Theorem 4.2

Next, we prove a local quadratic convergence of the full-step proximal Newton method (37) with the unit step-size for all . The proof is given in Appendix A.8.

Theorem 4.3

Suppose that the sequence is generated by (37) with full-step, i.e., for . Let be defined by (12) and be defined by (38). Then, the following statements hold:

-

If and the starting point satisfies , then both sequences and decrease and quadratically converge to zero, where .

-

If , and the starting point satisfies , then both sequences and decrease and quadratically converge to zero, where is the unique solution to the equation in with given in (56).

-

If and the starting point satisfies , then the sequence decreases and quadratically converges to zero, where .

As a consequence, if locally converges to zero at a quadratic rate, then also locally converges to zero at a quadratic rate, where , the identity matrix, if ; if ; and if . Hence, locally converges to , the unique solution of (32), at a quadratic rate.

Similar to Algorithm 1, we can also combine the results of Theorems 4.2 and 4.3 to design a proximal Newton algorithm for solving (32). This algorithm is described in Algorithm 2 below.

Implementation remarks:

The main step of Algorithm 2 is the computation of the proximal Newton step , or the trial point in (35). This step requires to solve a composite quadratic-convex minimization problem (35) with strongly convex objective function. If is proximally tractable, then we can apply proximal-gradient methods or splitting techniques Bauschke2011 ; Beck2009 ; Nesterov2007 to solve this problem. We can also combine accelerated proximal-gradient methods with a restarting strategy fercoq2016restarting ; Giselsson2014 ; Odonoghue2012 to accelerate the performance of these algorithms. These methods will be used in our numerical experiments in Section 6.

5 Quasi-Newton methods for generalized self-concordant minimization

This section studies quasi-Newton variants of Algorithm 1 for solving (24). Extensions to the composite form (32) can be done by combining the result in this section and the approach in Tran-Dinh2013a .

A quasi-Newton method for solving (24) updates the sequence using

| (40) |

where the step-size is appropriately chosen, and is a given starting point.

Matrix is symmetric and positive definite, and it approximates the Hessian matrix of at the iteration in some sense. The most common approximation sense is that satisfies the well-known Dennis-Moré condition Dennis1974 . In the context of generalized self-concordant functions, we can modify this condition by imposing:

| (41) |

Clearly, if we have , then, with a simple argument, we can show that (41) automatically holds. In practice, we can update to maintain the following secant equation:

| (42) |

There are several candidates to update to maintain this secant equation, see, e.g., Nocedal2006 . Here, we propose to use a BFGS update as

| (43) |

In practice, to avoid the inverse , we can update this inverse directly Nocedal2006 in lieu of updating as in (43). Note that the BFGS update (43) or its inverse version may not maintain the sparsity or block pattern structures of the sequence or even if is sparse.

The following result shows that the quasi-Newton method (40) achieves a superlinear convergence whose proof can be found in Appendix A.9.

Theorem 5.1

Assume that is the unique solution of (24) and is strongly regular. Let be the sequence generated by (40). Then, the following statements hold:

-

Assume, in addition, that the sequence of matrices satisfies the Dennis-Moré condtion (41) with . Then, there exist , and such that, for all , we have and locally converges to at a superlinear rate.

Note that the condition in Theorem 5.1(b) can be guaranteed if for some and . Hence, if locally converges to at a linear rate, then it also locally converges to at a superlinear rate.

6 Numerical experiments

We provide five examples to verify our theoretical results and compare our methods with existing methods in the leterature. Our algorithms are implemented in Matlab 2014b running on a MacBook Pro. Retina, 2.7 GHz Intel Core i5 with 16Gb 1867 MHz DDR3 memory.

6.1 Comparison with zhang2015disco on regularized logistic regression

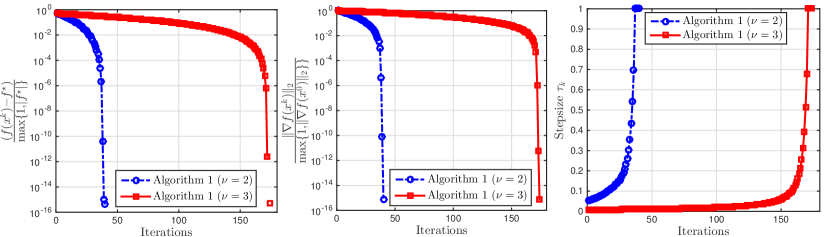

In this example, we empirically show that our theory provides a better step-size for logistic regression compared to zhang2015disco as theoretically shown in Example 4. In addition, our step-size can be used to guarantee a global convergence of Newton method without linesearch. It can also be used as a lower bound for backtracking or forward linesearch to enhance the performance of Algorithm 1.

To illustrate these aspects, we consider the following regularized logistic regression problem:

| (44) |

where is the logistic loss, is a given intercept, and are given as input data for , and is a given regularization parameter.

As shown previously in Proposition 5, can be cast into an -generalized self-concordant function with . On the other hand, can also be considered as an -generalized self-concordant with .

We implement Algorithm 1 using two different step-sizes and as suggested by Theorem 3.2 for and , respectively. We terminate Algorithm 1 if , where is an initial point. To solve the linear system (26), we apply a conjugate gradient method to avoid computing the inverse of the Hessian matrix in large-scale problems. We also compare our algorithms with the fast gradient method in Nesterov2004 using the optimal step-size for strongly convex functions which has an optimal linear convergence rate.

We test all algorithms on a binary classification dataset downloaded from CC01a at https://www.csie.ntu.edu.tw/~cjlin/libsvm/. As suggested in zhang2015disco , we normalize the data such that each row has for . The parameter is set to as in zhang2015disco .

As we can see from this figure that Algorithm 1 with outperforms the case . The right-most plot reveals the relative objective residual , the middle one shows the relative gradient norm , and the left-most figure displays the step-size and . Note that the step-size of Algorithm 1 depends on the regularization parameter . If is small, then is also small. In contrast, the step-size of Algorithm 1 is independent of .

Our second test is performed on six problems with different sizes. Table 3 shows the performance and results of the algorithms: Algorithm 1 with , Algorithm 1 with , and the fast-gradient method in Nesterov2004 . Here, is the number of data points, is the number of variables, iter is the number of iterations, error is the training error measured by , and is the objective value achieved by these three algorithms.

| Problem | Algorithm 1 () | Algorithm 1 () | Fast gradient method Nesterov2004 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Name | | | iter | time[s] | | error | iter | time[s] | | error | iter | time[s] | | error |

| a4a | 122 | 4781 | 22 | 0.57 | 3.250e-01 | 0.150 | 177 | 4.99 | 3.250e-01 | 0.150 | 1396 | 2.13 | 3.250e-01 | 0.150 |

| w4a | 300 | 6760 | 27 | 1.14 | 5.297e-02 | 0.013 | 246 | 8.41 | 5.297e-02 | 0.013 | 863 | 1.71 | 5.297e-02 | 0.013 |

| covtype | 54 | 581012 | 23 | 17.22 | 7.034e-04 | 0.488 | 272 | 235.40 | 7.034e-04 | 0.488 | 1896 | 318.32 | 7.034e-04 | 0.488 |

| rcv1 | 47236 | 20242 | 39 | 12.45 | 1.085e-01 | 0.009 | 218 | 60.80 | 1.085e-01 | 0.009 | 366 | 9.69 | 1.085e-01 | 0.009 |

| gisette | 5000 | 6000 | 40 | 109.23 | 1.090e-01 | 0.008 | 220 | 507.03 | 1.090e-01 | 0.008 | 2180 | 1183.67 | 1.090e-01 | 0.008 |

| real-sim | 20958 | 72201 | 39 | 22.69 | 1.287e-01 | 0.016 | 218 | 124.37 | 1.287e-01 | 0.016 | 271 | 24.74 | 1.287e-01 | 0.016 |

| news20 | 1355191 | 19954 | 42 | 86.47 | 1.602e-01 | 0.005 | 197 | 420.87 | 1.602e-01 | 0.005 | 623 | 153.22 | 1.602e-01 | 0.005 |

We observe that our step-size using works much better than using as in zhang2015disco . This confirms the theoretical analysis in Example 4. This step-size can be useful for parallel and distributed implementation, where evaluating the objective values often requires high computational effort due to communication and data transferring. Note that the computation of the step-size in Algorithm 1 only needs operations, and do not require to pass over all data points. Algorithm 1 with also works better than the fast gradient method Nesterov2004 in this experiment, especially for the case . Note that the fast gradient method uses the optimal step-size and has a linear convergence rate in this case.

Finally, we show that our step-size can be used as a lower bound to enhance a backtracking linesearch procedure in Newton methods. The Armijo linesearch condition is given as

| (45) |

where is a given constant. Here, we use which is sufficiently small.

-

•

In our backtracking linesearch variant, we search for the best step-size . This variant requires to compute which needs operations.

-

•

In the standard backtracking linesearch routine, we search for the best step-size .

Both strategies use a bisection section rule as starting from . The results on problems are reported in Table 4.

| Problem | Algorithm 1 (Standard linesearch) | Algorithm 1 (Linesearch with ) | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Name | | | iter | nfval | time[s] | | | error | iter | nfval | time[s] | | | error |

| covtype | 54 | 581012 | 25 | 68 | 14.99 | 5.8190e-09 | 7.034e-04 | 0.488 | 14 | 31 | 9.89 | 1.3963e-11 | 7.034e-04 | 0.488 |

| rcv1 | 47236 | 20242 | 9 | 21 | 1.85 | 1.3336e-11 | 1.085e-01 | 0.009 | 9 | 19 | 1.88 | 1.3336e-11 | 1.085e-01 | 0.009 |

| gisette | 5000 | 6000 | 8 | 22 | 18.28 | 1.2088e-09 | 1.090e-01 | 0.008 | 8 | 17 | 19.68 | 1.2088e-09 | 1.090e-01 | 0.008 |

As shown in Table 4, using the step-size as a lower bound for backtracking linesearch also reduces the number of function evaluations in these three problems. Note that the number of function evaluations depends on the starting point as well as the factor in (45). If we set too small, then the decrease on can be small. Otherwise, if we set too high, then our decrement may never be achieved, and the linesearch condition fails to hold. If we change the starting point , the number of function evaluations can significantly be increased.

6.2 The case : Matrix balancing

We consider the following convex optimization problem originated from matrix balancing cohen2017matrix :

| (46) |

where is a nonnegative square matrix in . Although (46) is a unconstrained smooth convex problem, its objective function is not strongly convex and does not have Lipschitz gradient. Existing gradient-type methods do not have a theoretical convergence guarantee as well as a rule to compute step-sizes. However, (46) is an important problem in scientific computing.

By Proposition 1 and Corollary 1, is generalized self-concordant with and . We implement Algorithm 1 and the most recent method proposed in cohen2017matrix (called Boxed-constrained Newton method (BCNM)) to solve (46). Note that cohen2017matrix is not directly applicable to (46), but it solves a regularization of this problem. Since is not positive definite, we use a projected conjugate gradient gradient (CG) method to solve the linear system in Algorithm 1. We use an accelerated projected gradient method (FISTA) Beck2009 to solve the subproblem for the method in cohen2017matrix . We terminate these subsolvers using either a tolerance or a maximum of iterations. For the outer loop, we terminate Algorithm 1 and BCNM using the same stopping criterion: . We choose as an initial point.

We test both algorithms on several synthetic and real datasets. The synthetic data is generated as in parlett1982methods with different structures. The basic matrix is a upper Hessenberg matrix defined as if , and otherwise. differs from only in that is replaced by ; differs from only in that is replaced by ; and . We use these matrices for in (46). We take , , , and . We name each problem instance by “Hdy”, where H stands for Hessenberg, and .

The real data is downloaded from https://math.nist.gov/MatrixMarket/searchtool.html with different structures from different application fields, suggested by chen2000balancing . Since we require the matrix to be nonnegative, we take (entry-wise). For the real data, if is highly ill-conditioned, then we add uniform noise to , where .

The final results of both algorithms are reported in Table 5, where is the size of matrix ; iter/siter is the maximum number of Newton-type iterations / CG or FISTA iterations; time[s] is the computational time in second; is the relative gradient norm defined above; is the ratio of the computational time between Algorithm 1 and BCNM; and is the relative difference between given by Algorithm 1 and BCNM.

| Datasets | Algorithm 1 | BCNM | Comparison | ||||||||

| Name | p | iter/siter | time[s] | | iter/siter | time[s] | | | t | | |

| Synthetic datasets | |||||||||||

| H1d1 | 1000 | 8/77 | 0.32 | 5.07e+05 | 3.52e-09 | 8/1028 | 1.55 | 5.07e+05 | 1.82e-10 | 4.88 | 4.0e-07 |

| H1d5 | 5000 | 7/66 | 2.54 | 1.45e+07 | 2.50e-10 | 7/648 | 24.99 | 1.45e+07 | 1.73e-10 | 9.84 | 3.8e-08 |

| H1d10 | 10000 | 7/64 | 8.74 | 6.24e+07 | 8.62e-14 | 6/461 | 61.61 | 6.24e+07 | 4.82e-09 | 7.05 | 7.6e-07 |

| H1d15 | 15000 | 7/63 | 18.63 | 1.48e+08 | 3.55e-14 | 6/395 | 120.41 | 1.48e+08 | 3.66e-10 | 6.47 | 2.1e-08 |

| H2d5 | 5000 | 7/62 | 2.53 | 1.45e+07 | 7.34e-10 | 7/640 | 20.36 | 1.45e+07 | 1.88e-10 | 8.04 | 1.1e-07 |

| H2d10 | 10000 | 7/64 | 9.16 | 6.24e+07 | 2.07e-13 | 6/467 | 61.44 | 6.24e+07 | 4.75e-09 | 6.71 | 7.6e-07 |

| H2d15 | 15000 | 7/63 | 19.66 | 1.48e+08 | 3.18e-14 | 6/395 | 119.16 | 1.48e+08 | 3.52e-10 | 6.06 | 1.9e-08 |

| H3d5 | 5000 | 4/32 | 1.34 | 1.25e+11 | 1.22e-11 | 3/15 | 2.28 | 1.25e+11 | 2.47e-11 | 1.70 | 6.7e-11 |

| H3d10 | 10000 | 4/32 | 4.52 | 1.00e+12 | 1.79e-11 | 3/14 | 8.21 | 1.00e+12 | 2.29e-11 | 1.82 | 2.6e-11 |

| H3d15 | 15000 | 4/28 | 8.72 | 3.38e+12 | 1.15e-11 | 3/12 | 18.06 | 3.38e+12 | 2.59e-10 | 2.07 | 4.9e-10 |

| Real datasets | |||||||||||

| bcs | 10974 | 4/362 | 43.95 | 2.28e+12 | 2.39e-12 | 9/438 | 87.89 | 2.28e+12 | 9.83e-09 | 2.00 | 2.1e-08 |

| bcs | 11948 | 4/204 | 31.23 | 9.30e+12 | 1.85e-12 | 14/305 | 91.19 | 9.30e+12 | 8.76e-09 | 2.92 | 4.8e-08 |

| bcs | 15439 | 4/36 | 11.89 | 1.53e+16 | 1.21e-12 | 3/16 | 19.13 | 1.53e+16 | 1.13e-10 | 1.61 | 4.4e-11 |

| bcsm | 15439 | 4/28 | 9.86 | 2.18e+11 | 1.98e-12 | 3/12 | 18.06 | 2.18e+11 | 2.52e-10 | 1.83 | 3.3e-10 |

| bwm | 2000 | 4/800 | 4.06 | 9.13e+07 | 2.62e-11 | 500/1680 | 72.15 | 9.13e+07 | 1.05e-08 | 17.77 | 7.3e-09 |

| e40r01 | 17281 | 5/178 | 59.65 | 9.86e+04 | 3.49e-12 | 4/230 | 92.36 | 9.86e+04 | 1.20e-09 | 1.55 | 4.6e-08 |

| e40r05 | 17281 | 6/279 | 92.71 | 1.02e+05 | 5.09e-13 | 5/476 | 170.58 | 1.02e+05 | 7.07e-10 | 1.84 | 3.0e-08 |

| e40r20 | 17281 | 7/489 | 160.63 | 1.48e+05 | 7.86e-14 | 6/751 | 278.32 | 1.48e+05 | 1.14e-09 | 1.73 | 1.6e-09 |

| e40r30 | 17281 | 7/492 | 159.09 | 1.90e+05 | 6.21e-14 | 6/759 | 260.82 | 1.90e+05 | 1.11e-09 | 1.64 | 2.0e-09 |

| e40r40 | 17281 | 7/486 | 152.54 | 2.36e+05 | 6.09e-14 | 6/726 | 247.59 | 2.36e+05 | 3.15e-09 | 1.62 | 3.8e-09 |

| fid011 | 16614 | 4/434 | 122.21 | 4.55e+11 | 7.23e-12 | 21/465 | 268.17 | 4.55e+11 | 9.56e-09 | 2.19 | 3.6e-09 |

| fid019 | 12005 | 4/241 | 37.62 | 1.69e+10 | 2.06e-12 | 13/306 | 84.94 | 1.69e+10 | 9.18e-09 | 2.26 | 5.3e-08 |

| fid035 | 19716 | 4/261 | 116.65 | 2.78e+10 | 5.24e-12 | 4/295 | 164.79 | 2.78e+10 | 3.67e-09 | 1.41 | 1.1e-08 |

| fidm09 | 4683 | 4/685 | 16.14 | 1.65e+05 | 2.60e-12 | 93/829 | 67.09 | 1.65e+05 | 9.85e-09 | 4.16 | 2.5e-08 |

| fidm11 | 22294 | 3/222 | 118.68 | 4.63e+03 | 2.93e-09 | 3/299 | 178.42 | 4.63e+03 | 9.16e-10 | 1.50 | 1.3e-07 |

| fidm13 | 3549 | 4/667 | 9.17 | 8.73e+02 | 9.86e-14 | 5/653 | 9.49 | 8.73e+02 | 1.68e-09 | 1.03 | 2.7e-08 |

| fidm15 | 9287 | 3/231 | 21.43 | 2.23e+03 | 7.48e-09 | 3/321 | 32.61 | 2.23e+03 | 2.03e-09 | 1.52 | 6.7e-07 |

| fidm29 | 13668 | 4/451 | 82.61 | 1.07e+04 | 1.51e-12 | 12/452 | 135.98 | 1.07e+04 | 9.67e-09 | 1.65 | 1.8e-08 |

| fidm33 | 2353 | 4/397 | 2.62 | 9.70e+03 | 1.31e-12 | 5/585 | 3.99 | 9.70e+03 | 9.88e-09 | 1.53 | 2.4e-08 |

| fidm37 | 9152 | 4/483 | 44.73 | 1.61e+10 | 1.23e-11 | 70/614 | 212.39 | 1.61e+10 | 9.84e-09 | 4.75 | 2.3e-08 |

| gre | 1107 | 6/595 | 1.23 | 1.07e+03 | 4.27e-10 | 6/927 | 1.93 | 1.07e+03 | 4.72e-09 | 1.57 | 5.6e-08 |

| lnsp | 3937 | 8/402 | 7.43 | 2.56e+12 | 4.03e-14 | 7/669 | 13.60 | 2.56e+12 | 3.10e-10 | 1.83 | 1.5e-08 |

| mah | 1258 | 8/77 | 0.45 | 4.57e+05 | 1.97e-11 | 8/1001 | 3.00 | 4.57e+05 | 7.25e-11 | 6.63 | 4.7e-09 |

| mem | 17758 | 4/32 | 14.51 | 4.57e+02 | 1.53e-13 | 3/15 | 26.57 | 4.57e+02 | 1.19e-11 | 1.83 | 4.8e-11 |

| mhd | 3200 | 4/165 | 2.22 | 5.09e+01 | 2.39e-14 | 4/437 | 6.26 | 5.09e+01 | 1.94e-09 | 2.82 | 1.7e-07 |

| mhd | 4800 | 4/136 | 3.97 | 5.30e+01 | 4.79e-14 | 3/423 | 11.88 | 5.30e+01 | 3.30e-09 | 2.99 | 1.3e-07 |

| olm | 2000 | 8/640 | 3.27 | 2.94e+07 | 2.05e-15 | 7/846 | 4.80 | 2.94e+07 | 1.30e-10 | 1.47 | 2.7e-09 |

| olm | 5000 | 7/426 | 11.42 | 5.41e+08 | 9.14e-11 | 6/651 | 20.75 | 5.41e+08 | 4.85e-10 | 1.82 | 3.5e-09 |

| ora678 | 2529 | 9/898 | 6.95 | 3.16e+02 | 9.95e-11 | 8/1512 | 11.92 | 3.16e+02 | 8.06e-09 | 1.71 | 1.1e-06 |

| pde | 2961 | 6/197 | 2.56 | 1.05e+04 | 5.65e-13 | 5/311 | 4.17 | 1.05e+04 | 6.14e-10 | 1.63 | 8.4e-09 |

As we can see from our experiment, both methods give almost the same result in terms of the objective values and approximate solutions . Given the same stopping criteria and solution quality, Algorithm 1 outperforms BCNM in all datasets in terms of average computational time which is specified by . In particular, for many asymmetric and/or ill-conditioned datasets (e.g., H2d5, or bwm), Algorithm 1 is approximately from to times faster than BCNM.

6.3 The case : Distance-weighted discrimination regression.

In this example, we test the performance of Algorithm 1 on the distance-weighted discrimination (DWD) problem introduced in marron2007distance . In order to directly use Algorithm 1, we slightly modify the setting in marron2007distance to obtain the following form:

| (47) |

where , ( and are given, and () are three regularization parameters for , and , respectively. Here, the variable consists of the support vector , the intercept , and the slack variable as used in marron2007distance . Here, we penalize these variables by using least squares terms instead of the -penalty term as in marron2007distance . Note that the setting (47) is not just limited to the DWD application above, but can also be used to formulate other practical models such as time optimal path planning problems in robotics Verscheure2009 if we choose an appropriate parameter .

Since is -generalized self-concordant with and , using Proposition 1, we can show that is -generalized self-concordant with (here, is the -th unit vector). Problem (47) can be transformed into a second-order cone program Grant2006 , and can be solved by interior-point methods. For instance, if we choose , then, by introducing intermediate variables and , we can transform (47) into a second-order cone program using the fact that is equivalent to .

We implement Algorithm 1 to solve (47) and compare it with the interior-point method implemented in commercial software: Mosek. We experienced that Mosek is much faster than other interior-point solvers such as SDPT3 Toh2010 or SDPA Yamashita2003 in this test. For instance, Mosek is from to times faster than SDPT3 in this example. Hence, we only present the results of Mosek.

We also incorporate Algorithm 1 with a backtracking linesearch using our step-size (LS with ) as a lower bound. Note that since does not have a Lipschitz gradient map, we cannot apply gradient-type methods to solve (47) due to the lack of a theoretical guarantee.

Since we cannot run Mosek on big data sets, we rather test our algorithms and this interior-point solvers on small and medium size problems using data from CC01a (https://www.csie.ntu.edu.tw/~cjlin/libsvm/). We choose the regularization parameters as and . Note that if the data set has the size of , then number of variables in (47) becomes . Hence, we use a built-in Matlab conjugate gradient solver to compute the Newton direction . The initial point is chosen as , and . In our algorithms, we use as a stopping criterion.

Note that, by the choice of for as , the objective function of (47) is strongly convex. By Proposition 4(a), we can cast this function into an (-generalized self-concordant with and , where is given above. We also implement Algorithm 1 using to solve (47).

| Problem | Algorithm 1 | Algorithm 1 (LS with ) | Algorithm 1 () | Mosek | |||||||||

| Name | | | iter | time[s] | | iter | time[s] | | iter | time[s] | | time[s] | |

| a1a | 1605 | 119 | 170 | 1.35 | 9.038e-12 | 13 | 0.12 | 4.196e-13 | 574 | 5.77 | 7.031e-14 | 0.49 | 1.806e-08 |

| a2a | 2265 | 119 | 192 | 2.71 | 1.661e-13 | 12 | 0.15 | 8.549e-09 | 633 | 7.67 | 8.903e-09 | 0.50 | 2.858e-08 |

| a4a | 4781 | 122 | 247 | 5.60 | 1.180e-13 | 12 | 0.27 | 5.380e-10 | 790 | 21.06 | 3.171e-13 | 0.94 | 1.740e-08 |

| leu | 38 | 7129 | 54 | 2.71 | 2.214e-10 | 15 | 0.58 | 3.995e-13 | 193 | 10.64 | 5.275e-12 | 0.72 | 2.828e-07 |

| w1a | 2270 | 300 | 169 | 2.88 | 9.752e-09 | 13 | 0.17 | 4.968e-09 | 676 | 10.44 | 8.678e-09 | 0.50 | 1.561e-08 |

| w2a | 3184 | 300 | 193 | 3.32 | 4.532e-13 | 13 | 0.27 | 1.428e-09 | 751 | 15.02 | 7.662e-14 | 0.61 | 1.793e-08 |

| a1a | 1605 | 119 | 166 | 2.28 | 6.345e-12 | 14 | 0.15 | 5.185e-13 | 1372 | 13.62 | 3.299e-09 | 0.48 | 1.617e-09 |

| a2a | 2265 | 119 | 186 | 2.63 | 3.028e-12 | 13 | 0.22 | 5.015e-09 | 1484 | 16.65 | 5.325e-09 | 0.56 | 3.070e-09 |

| a4a | 4781 | 122 | 235 | 5.03 | 8.676e-13 | 13 | 0.31 | 4.347e-10 | 1764 | 53.92 | 2.662e-09 | 1.25 | 4.039e-09 |

| leu | 38 | 7129 | 57 | 3.08 | 1.631e-10 | 16 | 0.63 | 2.754e-12 | 574 | 39.20 | 2.076e-12 | 0.73 | 6.436e-08 |

| w1a | 2270 | 300 | 146 | 2.15 | 1.311e-12 | 14 | 0.22 | 4.057e-09 | 1533 | 27.26 | 1.110e-09 | 0.59 | 1.295e-09 |

| w2a | 3184 | 300 | 165 | 3.43 | 3.397e-09 | 14 | 0.29 | 1.187e-09 | 1661 | 30.63 | 8.004e-09 | 0.71 | 1.653e-09 |

The results and performance of the four algorithms are reported in Table 6 for two cases: and . We can see that Algorithm 1 with outperforms the case in terms of iterations. The case is approximately from to times faster than the case . This is not surprising since depends on , and it is large since is small. Hence, the stepsize computed by using is smaller than computed from as we have seen in the first example. Mosek works really well in this example and it is slightly better than Algorithm 1 with . If we combine Algorithm 1 with a backtracking linesearch, then this variant outperforms Mosek. All the algorithms achieve a very high accuracy in terms of the relative norm of the gradient which is up to . We emphasize that our methods are highly parallelizable and their performance can be improved by exploiting this structure as studied in zhang2015disco for the logistic case.

6.4 The case : Portfolio optimization with logarithmic utility functions.

In this example, we aim at verifying Algorithm 2 for solving the composite generalized self-concordant minimization problem (32) with . We illustrate this algorithm on the following portfolio optimization problem with logarithmic utility functions ryu2014stochastic (scaled by a factor of ):

| (48) |

where for are given vectors presenting the returns at the -th period of the assets considered in the portfolio data. More precisely, as indicated in borodin2004can , measures the return as the ratio between the closing prices and of the stocks on the current day and on the previous day , respectively; is a vector of all ones. The aim is to find an optimal strategy to assign the proportion of the assets in order to maximize the expected return among all portfolios.

Note that problem (48) can be cast into an online optimization model hazan2006efficient . The authors in hazan2006efficient proposed an online Newton method to solve this problem. In this case, the regret of such an online algorithm showing the difference between the objective function of the online counterpart and the objective function of (48) converges to zero at a rate of as . If is relatively small (e.g., ), then the online Newton method does not provide a good approximation to (48).

Let be the standard simplex, and be the indicator function of . Then, we can formulate (48) into (32). The function defined in (48) is -generalized self-concordant with and .

We implement Algorithm 2 using an accelerated projected gradient method Beck2009 ; Nesterov2004 to compute the proximal Newton direction. We also implement the Frank-Wolfe algorithm and its linesearch variant in Frank1956 ; Jaggi2013 , and a projected gradient method using Barzilai and Borwein’s step-size to solve (48). We name these algorithms by FW, FW-LS, and PG-BB, respectively.

We emphasize that both PG-BB and FW-LS do not have a theoretical guarantee when solving (48). FW has a theoretical guarantee as recently proved in odor2016frank , but the complexity bound is rather pessimistic. We terminate all the algorithms using , where in Algorithm 2, in PG-BB, and in FW and FW-LS. We choose different accuracies for these methods due to the limitation of first-order methods for attaining high accuracy solutions in the last three algorithms.

We test these algorithms on two categories of dataset: synthetic and real stock data. For the synthetic data, we generate matrix with given price ratios as described above in Matlab. More precisely, we generate which allows the closing prices to vary about between two consecutive periods. We test with three instances, where , , and , respectively. We name these three datasets by PortfSyn1, PortfSyn2, and PortfSyn3, respectively. For the real data, we download a US stock dataset using an excel tool http://www.excelclout.com/historical-stock-prices-in-excel/. This tool gives us the closing prices of the US stock market in a given period of time. We generate three datasets with different sizes using different numbers of stocks from 2005 to 2016 as described in borodin2004can . We pre-processed the data by removing stocks that are empty or lacking information in the time period we specified. We name these three datasets by Stock1, Stocks2, and Stocks3, respectively.

The results and the performance of the four algorithms are given in Table 7. Here, iter gives the number of iterations, time is the computational time in second, error measures the relative difference between the approximate solution given by the algorithms and the interior-point solution provided by CVX Grant2006 with the high precision configuration (up to : .

| Problem | Algorithm 2 | PG-BB | FW | FW-LS | ||||||||||

| Name | | | iter | time[s] | error | iter | time[s] | error | iter | time[s] | error | iter | time[s] | error |

| Synthetic Data | ||||||||||||||

| PortfSyn1 | 1000 | 800 | 6 | 5.68 | 2.4e-04 | 645 | 3.98 | 2.3e-04 | 15530 | 96.47 | 2.3e-04 | 6509 | 47.88 | 2.3e-04 |

| PortfSyn2 | 1000 | 1000 | 6 | 6.96 | 6.8e-05 | 1207 | 11.54 | 7.5e-05 | 17201 | 166.89 | 1.7e-04 | 6664 | 70.15 | 1.4e-04 |

| PortfSyn3 | 1000 | 1200 | 7 | 12.91 | 3.2e-04 | 959 | 9.55 | 3.0e-04 | 16391 | 159.28 | 3.3e-04 | 5750 | 64.36 | 3.2e-04 |

| Real Data | ||||||||||||||

| Stocks1 | 473 | 500 | 8 | 1.22 | 7.1e-06 | 736 | 1.22 | 1.9e-06 | 16274 | 24.93 | 7.0e-05 | 2721 | 5.28 | 4.1e-04 |

| Stocks2 | 625 | 723 | 8 | 3.71 | 2.7e-05 | 1544 | 4.37 | 8.0e-06 | 11956 | 34.35 | 3.1e-04 | 2347 | 9.33 | 5.2e-04 |

| Stocks3 | 625 | 889 | 10 | 6.83 | 5.6e-05 | 1074 | 6.54 | 5.4e-06 | 13027 | 52.89 | 1.7e-04 | 2096 | 8.46 | 7.4e-04 |

From Table 7 we can see that Algorithm 2 has a comparable performance to the first-order methods: FW-LS and PG-BB. While our method has a rigorous convergence guarantee, these first-order methods remains lacking a theoretical guarantee. Note that Algorithm 2 and PG-BB are faster than the FW method and its linesearch variant although the optimal solution of this problem is very sparse. We also note that PG-BB gives a smaller error to the CVX solution. This CVX solution is not the ground-truth but gives a high approximation to . In fact, the CVX solution is dense. Hence, it is not clear if PG-BB produces a better solution than other methods.

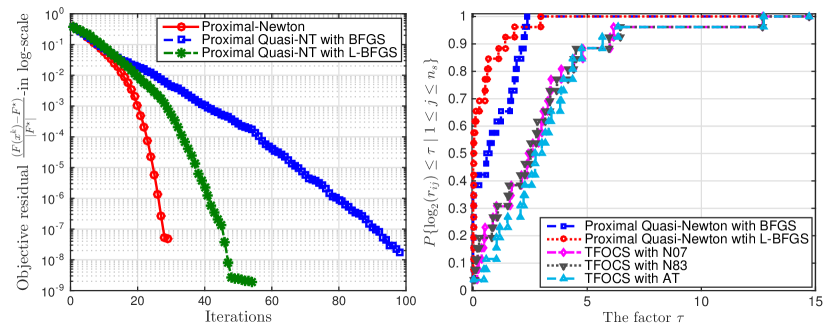

6.5 Proximal Quasi-Newton method for sparse multinomial logistic regression.

We apply our proximal Newton and proximal quasi-Newton methods to solve the following sparse multinomial logistic problem studied in various papers including Krishnapuram2005 :

| (49) |

where can be considered as a matrix variable of size formed from , is the vectorization operator, and is a regularization parameter. Both and are given as input data for and .

The function defined in (49) has a closed form Hessian matrix. However, forming the full Hessian matrix requires an intensive computation in large-scale problems when . Hence, we apply our proximal-quasi-Newton methods in this case. As shown in (TranDinh2014d, , Lemma 4), the function is -generalized self-concordant with and .

We implement our proximal quasi-Newton methods to solve (49) and compare them with the accelerated first-order methods implemented in a well-established software package called TFOCS Becker2011a . We use three different variants of TFOCS: TFOCS with N07 (using Nesterov’s 2007 method with two proximal operations per iteration), TFOCS with N83 (using Nesterov’s 1983 method with one proximal operation per iteration), and TFOCS with AT (using Auslender and Teboulle’s accelerated method).