11footnotetext: INDAM Unit, University of Brescia22footnotetext: Department of Mathematics and Applications,

University of Milano Bicocca

Polynomial Profits in Renewable Resources Management

Rinaldo M. Colombo1Mauro Garavello2

Abstract

A system of renewal equations on a graph provides a

framework to describe the exploitation of a biological resource. In

this context, we formulate an optimal control problem, prove the

existence of an optimal control and ensure that the target cost

function is polynomial in the control. In specific situations,

further information about the form of this dependence is

obtained. As a consequence, in some cases the optimal control is

proved to be necessarily bang–bang, in other cases the computations

necessary to find the optimal control are significantly reduced.

Keywords: Management of Biological Resources;

Optimal Control of Conservation Laws; Renewal Equations.

2010 MSC: 35L50, 92D25

1 Introduction

A biological resource is grown to provide an economical profit. Up to

a fixed age , this population consists of juveniles

whose density at time and age satisfies the usual

renewal equation [12, Chapter 3]

and being, respectively, the usual growth and mortality

functions, see also [5, 6, 11]. For further structured population models, we

refer for instance to [3, 4, 8, 9, 13].

At age , each individual of the population is selected and

directed either to the market to be sold or to provide new juveniles

through reproduction. Correspondingly, we are thus lead to consider

the and the populations whose evolution is described by the

renewal equations

with obvious meaning for the functions . Here, the

selection procedure is described by a parameter , varying in

, which quantifies the percentage of the population

directed to the market, so that

The overall dynamics is completed by the description of reproduction,

which we obtain here through the usual age dependent fertility

function using the following nonlocal boundary condition

In this connection, we recall the related results [1, 2, 7] in structured populations that take into

consideration a juvenile–adult dynamics.

Figure 1: The graph corresponding to the biological resource. At age

, juveniles reach the adult stage and are selected. The

part is used for reproduction. Portions of the population

are sold at ages .

Once the biological evolution is defined, we introduce the income and

cost functionals as follows. The income is related to the withdrawal

of portions of the population at given stages of its

development. More precisely, we assume there are fixed ages

, with

, where the

fractions of the population are kept,

while the portions are sold. A

very natural choice is to set , meaning that

nothing is left unsold after age . The dynamics of the whole

system has then to be completed introducing the selection

that takes place at the age , for .

Summarizing, the dynamics of the structured population is

thus described by the following nonlocal system of balance laws, see

also Figure 1:

(1.1)

where we inserted the initial data .

Our key result is the proof that for all and all , the

quantities , and are polynomial in

the values attained by the control parameters and .

We now pass to the introduction of the expressions of cost and

income. To this aim, we first fix a time horizon , with

. Then, a reasonable expression for the income is

(1.2)

The latter term above is the sum of the incomes due to the selling of

the individuals at the ages .

Typically, each value function can be chosen linear

in its second argument, but the present framework applies also to the

more general polynomial case. The former term in the right hand side

of (1.2), namely

, accounts for the

total amount of the population at time and it can also be seen

as the capital consisting of the biological resource at time .

Neglecting this term obviously leads to optimal strategies that leave

no juveniles at the final time . The value function

is also assumed to be polynomial, see Section 3.3.

To model the various costs, we use a general integral functional of

the form

(1.3)

The cost functions , for

, are assumed to be polynomial in , for

all and . In the simplest case of linear cost and

income, (1.2) and (1.3) reduce to

(1.4)

(1.5)

Here, is the unit value of juveniles of age , while

is the price at time per each individual of the

population sold at maturity . Similarly, the quantity

, for , is the unit cost related to

the keeping of individuals of the population , of age , at time

.

Below, we provide the essential tools to establish effective numerical

procedures able to actually compute the profit

(1.6)

as a function of the (open loop) control parameters and

. In particular, this also allows to find choices of the time

dependent control parameters and that allow to

maximize . Moreover, the procedures presented below

provide an alternative to the use of bang-bang controls. For

a comparison between the two techniques we refer to

Section 3.3.

The next section presents the main results of this note, while

specific examples are deferred to paragraphs 3.1,

3.2 and 3.3. All analytic proofs are in

Section 4.

2 Main Results

Throughout we denote , while

is the usual characteristic function of the set ,

so that if and only if , whereas

vanishes outside . The positive integers

and are fixed throughout, as also the positive

strictly increasing real numbers ,

. It is also of use to introduce the real

intervals ,

, and .

Below, for a real valued function defined on an interval , we

call its total variation, while is the set

of real valued functions with finite total variation, namely:

We posit the following assumptions:

(A)

For , the growth rate and mortality rate

satisfy

for a suitable , while the fertility function

satisfies .

(ID)

,

and

.

(P)

and for

. Moreover, the map , respectively

for , is a polynomial of degree at

most in for all , respectively in

for .

(C)

and

the map is a polynomial of degree at most

in , for .

Above, the restriction to of the initial data is

not necessary from the analytic point of view, but it is justified by

the biological meaning of the variables. Clearly, the extension to

the case of polynomials with different degrees is essentially a mere

problem of notation.

Recall, as in [6, 11], the

strictly increasing sequence of generation times

recursively defined for , by

(2.1)

the characteristic functions and being

defined in (4.3) for . If satisfies (A),

then the sequence is well defined and as

. The interval is the time

period when the juveniles of the -th generation are born.

The following results apply to the case of a constant and a

constant , when system (1.1) fits

into [5, Theorem 2.4] and turns out to be well

posed in .

Let (A) hold. For every ,

and every initial data as

in (ID), system (1.1) admits a unique solution

such that

and the stability estimates in [5, Theorem 2.4 and

Theorem 2.5] hold.

In order to exhibit the existence and to actually find a value of

and that maximizes as defined

in (1.6), we first investigate the regularity of

and , defined in (1.2)

and (1.3), as functions of the control parameters

and .

Pose conditions (A), (ID). For any

and ,

system (1.1) admits a unique solution. Moreover,

and there exists a function ,

with , dependent only on , , ,

, , and such that for all initial data

and and for all controls

, , and , the corresponding

solutions and to (1.1)

satisfy, for every , the following stability estimate:

Recall the following definition, which allows us to describe the form

of the cost, income, and profit as functions of the controls.

A map

is multiaffine if

is affine as a function of each , for ,

(keeping all other fixed).

The elementary property below of multiaffine functions plays a key

role in selecting those situations where a bang–bang control may

yield the optimal profit. Its proof is deferred to

Section 4.

Lemma 2.5.

Let and be

multiaffine and not constant. Then, admits neither points of

strict local minimum, nor points of strict local maximum. Hence,

is attained on a vertex of .

The two theorems below constitute the main results of the present

work.

Theorem 2.6.

Pose conditions (A), (ID). Introduce times

such that

(2.2)

and control parameters for .

Let be the solution to (1.1) corresponding to the

control

(2.3)

Then, for all and , the quantities , and

are multiaffine in .

Remark that the latter condition

in (2.2)

can always be met, through a suitable splitting of the intervals

.

Theorem 2.7.

Pose conditions (A), (ID). Introduce times

such that

and control parameters for

and . Let be the solution

to (1.1) corresponding to the controls

(2.4)

Then, for all , if

, the quantity is

multiaffine in the variables

.

Corollary 2.8.

Pose conditions (A), with constant in time,

(ID), (P) and (C). Choose controls

as in (2.2)–(2.3) and as

in (2.4). Then, the net profit defined

in (1.6) is polynomial in and of degree at

most in each of the (scalar) variables

separately. Moreover, globally, it is a polynomial of degree at most

in and of degree at most

in .

Thanks to the form of the costs and of the gains ensured

by (P) and (C), the proof is an immediate

consequence of Theorem 2.6 and

Theorem 2.7.

Remark 2.9.

A direct consequence of Corollary 2.8 in the

case (1.4)–(1.5) of linear gains and costs,

thanks to Lemma 2.5, is that optimal controls

, among those of

the form (2.4), can be found restricting the search to

only bang–bang controls, i.e., to those assuming only the values

and . Nevertheless,

in [6, Theorem 1.8], it is proved that

bang-bang controls well approximate the optimal ones, found in the

class of for and of

for , provided the cost and

income are linear, i.e. in the form (1.4)-(1.5).

3 Examples

The examples in paragraphs 3.1 and 3.2 rely

on several numerical integrations of (1.1). They were

accomplished using the explicit formula (4.2). To compute the

gains and the costs (1.2)–(1.3), we used

the standard trapezoidal rule.

For simplicity, we assume throughout that at age all the

population is sold; this corresponds to the case

.

3.1 A Generational Control

We particularize Theorem 2.3 to the case of as

in (2.2)–(2.3) with , so that

is constant on each generation. On the other hand, we keep

constant.

Corollary 3.1.

Pose conditions (A), (ID), (P)

and (C). Choose linear gains and costs as

in (1.4)–(1.5). Let be as

in (2.1). Set

(3.1)

and let be constant. Then, the net profit

defined in (1.6) is multiaffine in

. Therefore, the optimal profit can be

obtained through a bang–bang control.

In the present case (3.1) there are distinct bang–bang

controls: Corollary 3.1 ensures that one of them yields the

maximum profit. At the same time, the profit is a

multiaffine function in , so that it contains at most

terms. Therefore, the integration of suitable instances

of (1.1) permits to obtain all the coefficients in the

expression of as a function of and, hence, to

compute for all (i.e., not necessarily bang–bang)

possible controls (3.1).

Consider the situation corresponding to the time interval

, we have

and Corollary 3.1 ensures that the profit

defined at (1.4)–(1.5)–(1.6) is actually a

multiaffine function of , so that

In other words, thanks to the qualitative information provided by

Corollary 3.1, computing only times

allows to obtain the expression of

valid for all .

As an example, we consider the

setting (1.1)–(1.4)–(1.5) defined by the

choices:

Using the expression (4.2) of the exact solution

to (1.1) we obtain (up to the second decimal digit)

so that

(3.2)

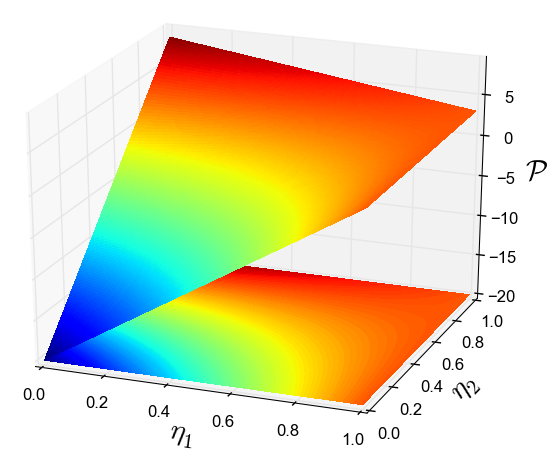

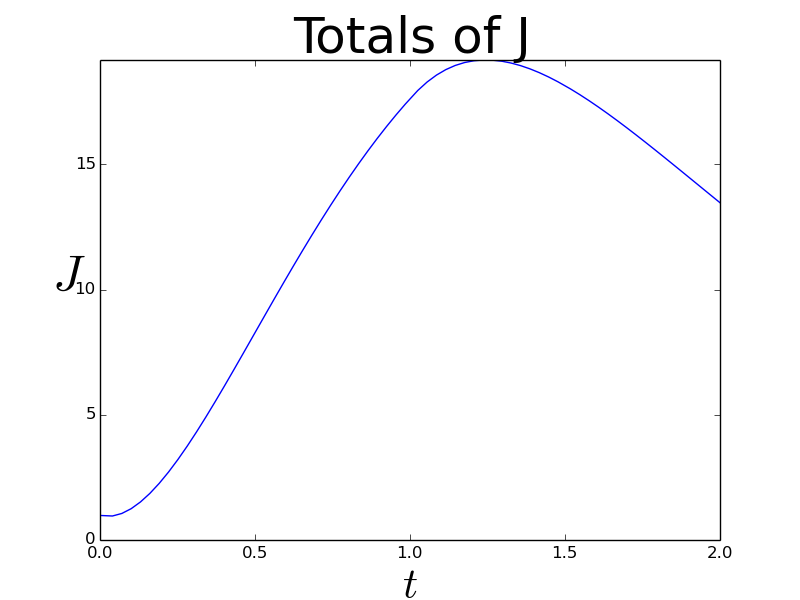

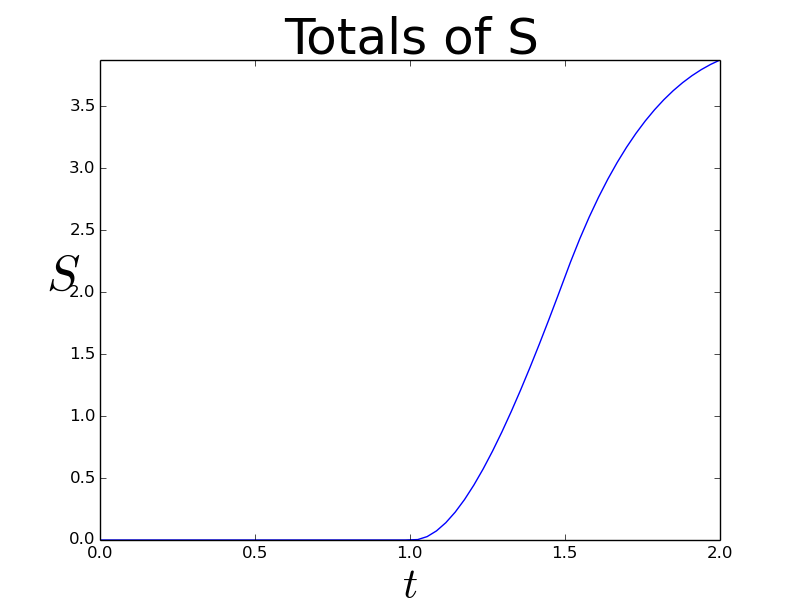

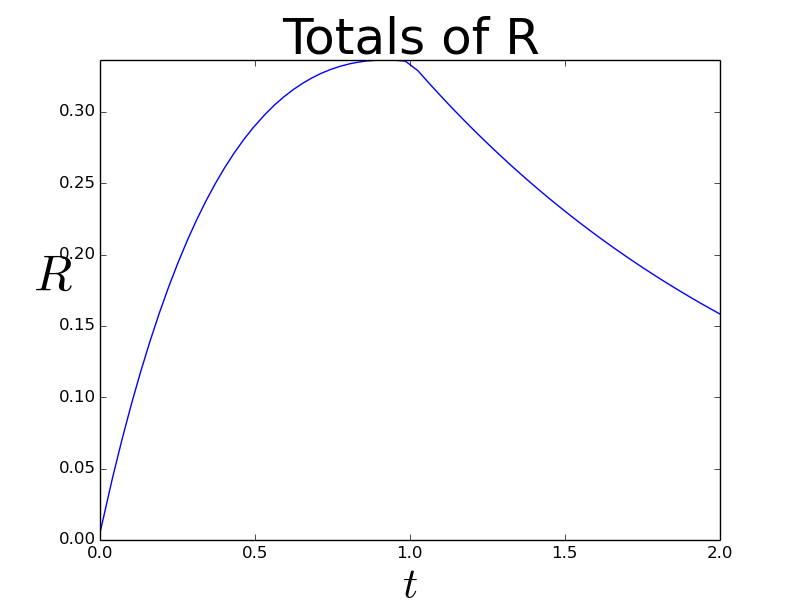

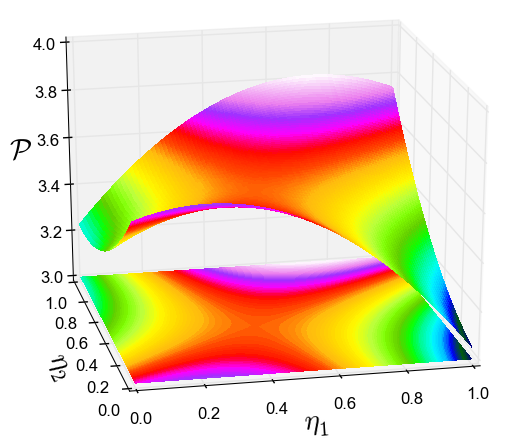

Figure 2: Left, graph of the profit (3.2): the maximum value

on is attained at

. Right, the total amounts of the

different populations as a function of time: top, and, bottom,

and .

Coherently with the results above, the maximum of is

attained at the bang–bang control , see

Figure 2. This strategy amounts to first keep all

juveniles for reproduction and then sell them all.

3.2 A Periodic Control

We now consider the case of a growth function independent of

time. Then, with reference to (2.1), we have

for all . It is then

natural to consider a piecewise constant control which is periodic and

with period :

(3.3)

Corollary 3.2.

Pose conditions (A), (ID), (P)

and (C). Assume that the growth function is

independent of time. Choose as in (3.3) with

for a given and let

be constant. Then, the net profit defined

in (1.4)–(1.5)–(1.6) is a polynomial of

degree at most in .

The proof is a direct consequence of Theorem 2.6 and is

hence omitted. Observe that a polynomial of degree in

variables contains at most

terms. Therefore, Corollary 3.2 reduces the problem of

maximizing (1.6) along the solutions to (1.1) to:

the solution to a linear system of equations in

variables,

3.

the maximization of a polynomial.

Consider the following example. In the case in (3.3),

choosing the time interval , i.e., , we set

(3.4)

corresponding to , and .

Corollary 3.2 ensures that is a

polynomial of degree at most separately in and ,

so that

(3.5)

and numerical integrations of (1.1) with the

consequent evaluation of (1.6) allow to obtain the coefficients

and, hence, the full knowledge of the profit as a

function of the control parameters.

We consider now the

setting (1.1)–(1.4)–(1.5) defined by the

choices:

Using the expression of the exact solution to (1.1) we obtain

(up to the second decimal digit)

(3.6)

The resulting profit is plotted in Figure 3 as a

function of . Remark that the resulting optimal

control is not bang–bang. At the times

the sharp changes in the graphs of

and are due to the sharp changes in the control, as

prescribed in (3.4).

Figure 3: Left, graph of the

polynomial (3.5)–(3.6): the

maximum gain on is attained at

. Right, the total amounts of the

different populations as a function of time: top, and, bottom,

and .

3.3 A Stabilizing Strategy

As a further example, we consider the case of a nonlinear profit. A

justification for this choice can be the necessity to stabilize the

juvenile population to reduce the running costs caused by the

population.

Therefore, we consider system (1.1), with an income function of

the type (1.2) and a nonlinear cost for the

population given by

(3.7)

Here, the fixed parameter can be seen as the juvenile density

that, say, minimizes the running costs. We are thus lead to the

maximization of the profit (1.6), with linear

income (1.4) and cost (3.7). Let be as

in (2.1) and consider a generational control as

in (3.1), and piecewise constant controls

() as

(3.8)

where for every

and

. Then, by the analysis in

Section 2, we can assert that the profit (1.6) is

a second order polynomial in whose first and

zeroth order terms are multiaffine in

:

(3.9)

which is a polynomial defined by

(3.10)

real coefficients.

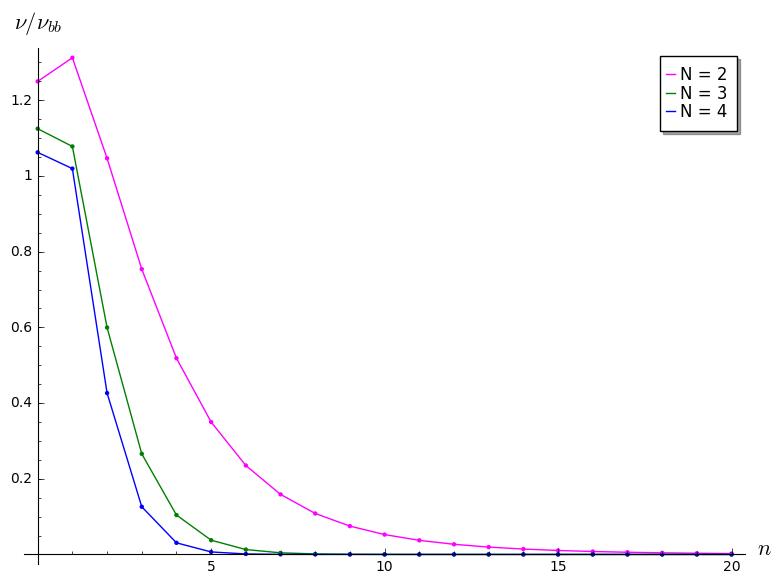

Figure 4: Ratio as a function of the number of

generations . As in (3.10), is the number of

integrations of (1.1) that are necessary to compute the

coefficients of

in (3.9) as a function of

as in (3.1) and as in (3.8). Here,

is the total number of bang–bang controls.

Thus, solving times the renewal equations (1.1),

computing the corresponding

profits (3.9), solving a

linear system to get the coefficients allows to

obtain an expression for valid for all possible

control parameters , .

As a comparison, we remark that the total number of bang–bang

controls in the present case is and there is no

guarantee that the optimal control is of bang–bang type. For a

comparison between and , refer to

Figure 4.

4 Technical Details

As in [5, 6, 12],

we recall that the initial – boundary value problem for the renewal

equation

(4.1)

admits a unique solution that can be explicitly computed integrating

along characteristics as

(4.2)

where the maps and

, with and

, are defined as

(4.3)

while the map is given by

(4.4)

Clearly, the knowledge of the maps ,

and does not require knowledge of the solution

to (4.1) but relies only on the solution to the ordinary

differential equation (4.3).

Proof of Lemma 2.5.

The proof is by induction on . If , then

and the proof follows by basic

calculus. Let now . Assume that is

a point of strict local maximum or minimum for the multiaffine

function . Then, one can write

for suitable multiaffine functions .

Since

has a point of strict local maximum or minimum at

, by the inductive assumption

the map is constant. Since, the map

may not attain a strict local maximum or minimum at

, the proof is completed.

Proof of Theorem 2.6 and Proof of

Theorem 2.7.

Fix an arbitrary time . Lengthy but elementary

computations based on Figure 5 show that the

component of the solution to (1.1) admits the following

representation, for and where we

used (4.2)–(4.3)–(4.4) for :

(4.5)

The population is given by

(4.6)

and, finally, the population for is

(4.7)

The expression of for directly follows. Note

that the right hand side in the explicit expression above depends

only on the values attained by at .

Figure 5: In the white regions, the quantities are

independent of . For , in the shaded

region is at most first order in . Similarly,

for , the shaded region describes where or

may depend on , at most at the first order.

Fix now an index . Clearly, , and

are all independent of for .

Consider the time interval

.

By (4.5), see also Figure 5, it is clear that

is independent of for

Clearly, , respectively , is independent of

whenever ,

respectively .

On the strip

,

the quantity is linear in

by (4.7). Similarly, on

,

by (4.6) is linear in . Again

by (4.6) and (4.7), , respectively ,

is independent of for

and , respectively

and

. Finally, the above considerations and (4.5)

ensure that is affine in for

and . The proof is thus completed for

.

On the basis of (4.5)–(4.6)–(4.7), a

straightforward iterative procedure allows to complete the proof

related to the dependence of on .

The proof concerning the dependence of on

directly follows from (1.1).

Proof of Corollary 3.1.

Apply Corollary 2.8 with , use the

assumption (3.1) and Lemma 2.5 to complete the

proof.

Acknowledgment: This work was partially supported by the 2015–INDAM–GNAMPA project Balance Laws in the Modeling of

Physical, Biological and Industrial Processes.

References

[1]

A. S. Ackleh and K. Deng.

A nonautonomous juvenile-adult model: well-posedness and long-time

behavior via a comparison principle.

SIAM J. Appl. Math., 69(6):1644–1661, 2009.

[2]

A. S. Ackleh, K. Deng, and X. Yang.

Sensitivity analysis for a structured juvenile–adult model.

Comput. Math. Appl., 64(3):190–200, 2012.

[3]

À. Calsina and J. Saldaña.

Global dynamics and optimal life history of a structured population

model.

SIAM J. Appl. Math., 59(5):1667–1685, 1999.

[4]

À. Calsina and J. Saldaña.

Basic theory for a class of models of hierarchically structured

population dynamics with distributed states in the recruitment.

Math. Models Methods Appl. Sci., 16(10):1695–1722, 2006.

[5]

R. M. Colombo and M. Garavello.

Stability and optimization in structured population models on graphs.

Mathematical Biosciences and Engineering, 12(2):311–335, 2015.

[6]

R. M. Colombo and M. Garavello.

Control of biological resources on graphs.

ESAIM: COCV, to appear, 2016.

[7]

J. M. Cushing.

A juvenile-adult model with periodic vital rates.

J. Math. Biol., 53(4):520–539, 2006.

[8]

O. Diekmann, M. Gyllenberg, J. A. J. Metz, and H. R. Thieme.

On the formulation and analysis of general deterministic structured

population models. I. Linear theory.

J. Math. Biol., 36(4):349–388, 1998.

[9]

J. Z. Farkas and T. Hagen.

Stability and regularity results for a size-structured population

model.

J. Math. Anal. Appl., 328(1):119–136, 2007.

[10]

J. H. Gallier.

Curves and surfaces in geometric modeling: theory and

algorithms.

Morgan Kaufmann series in computer graphics and geometric modeling.

Morgan Kaufmann Publishers, free web version edition, 2015.

[11]

M. Garavello.

Optimal control in renewable resources modeling.

Bulletin of the Brazilian Mathematical Society, New Series,

47(1):347–357, 2016.

[12]

B. Perthame.

Transport equations in biology.

Frontiers in Mathematics. Birkhauser Verlag, Basel, 2007.

[13]

G. F. Webb.

Theory of nonlinear age-dependent population dynamics,

volume 89 of Monographs and Textbooks in Pure and Applied Mathematics.

Marcel Dekker, Inc., New York, 1985.