Online Learning of Optimal Bidding Strategy

in Repeated Multi-Commodity Auctions

Abstract

We study the online learning problem of a bidder who participates in repeated auctions. With the goal of maximizing his T-period payoff, the bidder determines the optimal allocation of his budget among his bids for goods at each period. As a bidding strategy, we propose a polynomial-time algorithm, inspired by the dynamic programming approach to the knapsack problem. The proposed algorithm, referred to as dynamic programming on discrete set (DPDS), achieves a regret order of . By showing that the regret is lower bounded by for any strategy, we conclude that DPDS is order optimal up to a term. We evaluate the performance of DPDS empirically in the context of virtual trading in wholesale electricity markets by using historical data from the New York market. Empirical results show that DPDS consistently outperforms benchmark heuristic methods that are derived from machine learning and online learning approaches.

1 Introduction

We consider the problem of optimal bidding in a multi-commodity uniform-price auction (UPA) [1], which promotes the law of one price for identical goods. UPA is widely used in practice. Examples include spectrum auction, the auction of treasury notes, the auction of emission permits (UK), and virtual trading in the wholesale electricity market, which we discuss in detail in Sec. 1.1.

A mathematical abstraction of multi-commodity UPA is as follows. A bidder has goods to bid on at an auction. With the objective to maximize his T-period expected profit, at each period, the bidder determines how much to bid for each good subject to a budget constraint.

In the bidding period , if a bid for good is greater than or equal to its auction clearing price , then the bid is cleared, and the bidder pays . His revenue resulting from the cleared bid will be the good’s spot price (utility) . In particular, the payoff obtained from good at period is where indicates whether the bid is cleared. Let and be the vector of auction clearing and spot market prices at period , respectively. Similarly, let be the vector of bids for period . We assume that are drawn from an unknown joint distribution and, in our analysis, independent and identically distributed (i.i.d.) over time.111This implies that the auction clearing price is independent of bid , which is a reasonable assumption for any market where an individual’s bid has negligible impact on the market price.

At the end of each period, the bidder observes the auction clearing and spot prices of all goods. Therefore, before choosing the bid of period , all the information the bidder has is a vector containing his observation and decision history . Consequently, a bidding policy of a bidder is defined as a sequence of decision rules, i.e., , such that, at time , maps the information history to the bid of period . The performance of any bidding policy is measured by its regret, which is defined by the difference between the total expected payoff of policy and that of the optimal bidding strategy under known distribution of .

1.1 Motivating applications

The mathematical abstraction introduced above applies to virtual trading in the U.S. wholesale electricity markets that are operated under a two-settlement framework. In the day-ahead (DA) market, the independent system operator (ISO) receives offers to sell and bids to buy from generators and retailers for each hour of the next day. To determine the optimal DA dispatch of the next day and DA electricity prices at each location, ISO solves an economic dispatch problem with the objective of maximizing social surplus while taking transmission and operational constraints into account. Due to system congestion and losses, wholesale electricity prices vary from location to location.222For example, transmission congestion may prevent scheduling the least expensive resources at some locations. In the real-time (RT) market, ISO adjusts the DA dispatch according to the RT operating conditions, and the RT wholesale price compensates deviations in the actual consumption from the DA schedule.

The differences between DA and RT prices occur frequently both as a result of generators and retailers exercising locational market power [2] and as a result of price spikes in the RT due to unplanned outages and unpredictable weather conditions [3]. To promote price convergence between DA and RT markets, in the early 2000s, virtual trading was introduced [4]. Virtual trading is a financial mechanism that allows market participants and external financial entities to arbitrage on the differences between DA and RT prices. Empirical and analytical studies have shown that increased competition in the market due to virtual trading results in price convergence and increased market efficiency [2, 3, 5].

Virtual transactions make up a significant portion of the wholesale electricity markets. For example, the total volume of cleared virtual transactions in five big ISO markets was 13% of the total load in 2013 [4]. In the same year, total payoff resulting from all virtual transactions was around 250 million dollars in the PJM market [2] and 45 million dollars in NYISO market [6].

A bid in virtual trading is a bid to buy (sell) energy in the DA market at a specific location with an obligation to sell (buy) back exactly the same amount in the RT market at the same location if the bid is cleared (accepted). Specifically, a bid to buy in the DA market is cleared if the offered bid price is higher than the DA market price. Similarly, a bid to sell in the DA market is cleared if it is below the DA market price. In this context, different locations and/or different hours of the day are the set of goods to bid on. The DA prices are the auction clearing prices, and the RT prices are the spot prices.

The problem studied here may also find applications in other types of repeated auctions where the auction may be of the double, uniform-price, or second-price types. For example, in the case of online advertising auctions [7], different goods can correspond to different types of advertising space an advertiser may consider to bid on.

1.2 Main results and related work

We propose an online learning approach to the algorithmic bidding under budget constraints in repeated multi-commodity auctions. The proposed approach falls in the category of empirical risk minimization (ERM) also referred to as the follow the leader approach. The main challenge here is that optimizing the payoff (risk) amounts to solving a multiple choice knapsack problem (MCKP) that is known to be NP hard [8]. The proposed approach, referred to as dynamic programming on discrete set (DPDS), is inspired by a pseudo-polynomial dynamic programming approach to 0-1 Knapsack problems. DPDS allocates the limited budget of the bidder among goods in polynomial time both in terms of the number of goods and in terms of the time horizon . We show that the expected payoff of DPDS converges to that of the optimal strategy under known distribution by a rate no slower than which results in a regret upper bound of . By showing that, for any bidding strategy, the regret is lower bounded by , we prove that DPDS is order optimal up to a term. We also evaluate the performance of DPDS empirically in the context of virtual trading by using historical data from the New York energy market. Our empirical results show that DPDS consistently outperforms benchmark heuristic methods that are derived from standard machine learning methods.

The problem formulated here can be viewed in multiple machine learning perspectives. We highlight below several relevant existing approaches. Since the bidder can calculate the reward that could have been obtained by selecting any given bid value regardless of its own decision, our problem falls into the category of full-feedback version of multi-armed bandit (MAB) problem, referred to as experts problem, where the reward of all arms (actions) are observable at the end of each period regardless of the chosen arm. For the case of finite number of arms, Kleinberg et al. [9] showed that, for stochastic setting, constant regret is achievable by choosing the arm with the highest average reward at each period. A special case of the adversarial setting was studied by Cesa-Bianchi et al. [10] who provided matching upper and lower bounds in the order of . Later, Freund and Schapire [11] and Auer et al. [12] showed that the Hedge algorithm, a variation of weighted majority algorithm [13], achieves the matching bound for the general setting. These results, however, do not apply to experts problems with continuous action spaces.

The stochastic experts problem where the set of arms is an uncountable compact metric space rather than finite was studied by Kleinberg and Slivkins [14] (see [15] for an extended version). Since there are uncountable number of arms, it is assumed that, in each period, a payoff function drawn from an i.i.d. distribution is observed rather than the individual payoff of each arm. Under the assumption of Lipschitz expected payoff function, they showed that the instance-specific regret of any algorithm is lower bounded by . They also showed that their algorithm—NaiveExperts—achieves a regret upper bound of for any where is the isometry invariant of the metric space. However, NaiveExperts is computationally intractable in practice because the computational complexity of its direct implementation grows exponentially with the dimension (number of goods in our case). Furthermore, the lower bound in [14] does not imply a lower bound for our problem with a specific payoff. Krichene et al. [16] studied the adversarial setting and proposed an extension of the Hedge algorithm, which achieves regret under the assumption of Lipschitz payoff functions. For our problem, it is reasonable to assume that the expected payoff function is Lipschitz; yet it is clear that, at each period, the payoff realization is a step function which is not Lipschitz. Hence, Lipschitz assumption of [16] doesn’t hold in our setting.

Stochastic gradient descent methods, which have low computational complexity, have been extensively studied in the literature of continuum-armed bandit [17, 18, 19]. However, either the concavity or the unimodality of the expected payoff function is required for regret guarantees of these methods to hold. This may not be the case in our problem depending on the underlying distribution of prices.

A relevant work that takes an online learning perspective for the problem of a bidder engaging in repeated auctions is Weed et al. [7]. They are motivated by online advertising auctions and studied the partial information setting of the same problem as ours but without a budget constraint. Under the margin condition, i.e., the probability of auction price occurring in close proximity of mean utility is bounded, they showed that their algorithm, inspired by the UCB1 algorithm [20], achieves regret that ranges from to depending on how tight the margin condition is. They also provided matching lower bounds up to a logarithmic factor. However, their lower bound does not imply a bound for the full information setting we study here. Also, the learning algorithm in [7] does not apply here because the goods are coupled through the budget constraint in our case. Furthermore, we do not have margin condition, and we allow the utility of the good to depend on the auction price.

Some other examples of literature on online learning in repeated auctions studied the problem of an advertiser who wants to maximize the number of clicks with a budget constraint [21, 22], or that of a seller who tries to learn the valuation of its buyer in a posted price auction [23, 24]. The settings considered in those problems are considerably different from that studied here in the implementation of budget constraints [21, 22], and in the strategic behavior of the bidder [23, 24].

2 Problem formulation

The total expected payoff at period given bid can be expressed as

where the expectation is taken using the joint distribution of , and is the vector of indicator functions with the -th entry corresponding to . We assume that the payoff obtained at each period is a bounded random variable with support in ,333This is reasonable in the case of virtual trading because DA and RT prices are bounded due to offer/bid caps. and the auction prices are drawn from a distribution with positive support. Hence, a zero bid for any good is equivalent to not bidding because it will not get cleared.

The objective is to determine a bidding policy that maximizes the expected T-period payoff subject to a budget constraint for each individual period:

| (1) | |||||||

| subject to | |||||||

where is the auction budget of the bidder, denotes the bid determined by policy , and is equivalent to for all .

2.1 Optimal solution under known distribution

If the joint distribution of and is known, the optimization problem decouples to solving for each time instant separately. Since is i.i.d. over , an optimal solution under known model does not depend on and is given by

| (2) |

where is the feasible set of bids. Optimal solution may not be unique or it may not have a closed form. The following example illustrates a case where there isn’t a closed form solution and shows that, even in the case of known distribution, the problem is a combinatorial stochastic optimization, and it is not easy to calculate an optimal solution.

Example.

Let and be independent, be exponentially distributed with mean , and the mean of be for all . Since not bidding for good is optimal if , we exclude the case without loss of generality. For this example, we can use the concavity of in the interval , where , to obtain the unique optimal solution , which is characterized by

where the Lagrange multiplier is chosen such that is satisfied. This solution takes the form of a "water-filling" strategy. More specifically, if the budget constraint is not binding, then the optimal solution is to bid for every good . However, in the case of a binding budget constraint, the optimal solution is determined by the bid value at which the marginal expected payoff associated with each good is equal to , and this bid value cannot be expressed in closed form.

We measure the performance of a bidding policy by its regret444The regret definition used here is the same as in [14]. This definition is also known as pseudo-regret in the literature [25]., the difference between the expected T-period payoff of and that of , i.e.,

| (3) |

where the expectation is taken with respect to the randomness induced by . The regret of any policy is monotonically increasing. Hence, we are interested in policies with sub-linear regret growth.

3 Online learning approach to optimal bidding

The idea behind our approach is to maximize the sample mean of the expected payoff function, which is an ERM approach [26]. However, we show that a direct implementation of ERM is NP-hard. Hence, we propose a polynomial-time algorithm that is based on dynamic programming on a discretized feasible set. We show that our approach achieves the order optimal regret.

3.1 Approximate expected payoff function and its optimization

Regardless of the bidding policy, one can observe the auction and spot prices of past periods. Therefore, the average payoff that could have been obtained by bidding up to the current period can be calculated for any fixed value of . Specifically, the average payoff for a good as a function of the bid value can be calculated at period by using observations up to , i.e.,

For example, at the end of first period, as illustrated in Fig. 1a. For, , this can be expressed recursively;

| (4) |

Since each observation introduces a new breakpoint, and the value of average payoff function is constant between two consecutive breakpoints, we observe that is a piece-wise constant function with at most breakpoints. Let the vector of order statistics of the observed auction clearing prices and zero be , and let the vector of associated average payoffs be , i.e., . Then, can be expressed by the pair , e.g., see Fig. 1b.

For a vector , let denote the sequence of entries from to . Initialize at the beginning of first period. Then, at each period , the pair can be updated recursively as follows:

| (5) |

where at period .

Consequently, overall average payoff function can be expressed as a sum of average payoff functions of individual goods. Instead of the unknown expected payoff , let’s consider the maximization of the average payoff function, which corresponds to the ERM approach, i.e.,

| (6) |

Due to the piece-wise constant structure, choosing for some contributes the same amount to the overall payoff as choosing any if and any if . However, choosing utilizes a smaller portion of the budget. Hence, an optimal solution to (6) can be obtained by solving the following integer linear program:

| (7) | ||||||

| subject to | ||||||

where the bid value for good .

Observe that (7) is a multiple choice knapsack problem (MCKP) [8], a generalization of 0-1 knapsack. Unfortunately, (7) is NP-hard [8]. If we had a polynomial-time algorithm that finds an optimal solution to (6), then we could have obtained the solution of (7) in polynomial-time too by setting where for each . Therefore, (6) is also NP-hard, and, to the best of our knowledge, there isn’t any method in the ERM literature [27], which mostly focuses on classification problems, suitable to implement for the specific problem at hand.

3.2 Dynamic programming on discrete set (DPDS) policy

Next, we present an approach that discretizes the feasible set using intervals of equal length and optimizes the average payoff on this new discrete set via a dynamic program. Although this approach doesn’t solve (6), the solution can be arbitrarily close to the optimal depending on the choice of the interval length under the assumption of the Lipschitz continuous expected payoff function. To exploit the smoothness of Lipschitz continuity, discretization approach of the continuous feasible set has been used in the continuous MAB literature previously [17, 14]. However, different than MAB literature, in this paper, discretization approach is utilized to reduce the computational complexity of an NP-hard problem as well.

Let be an integer sequence increasing with and as illustrated in Fig. 2. Then, the new discrete set is given as . Our goal is to optimize on the new set rather than , i.e.,

| (8) |

Now, we use dynamic programming approach that has been used to solve 0-1 Knapsack problems including MCKP given in (7) [28]. However, direct implementation of this approach results in pseudo-polynomial computational complexity in the case of 0-1 Knapsack problems. The discretization of the feasible set with equal interval length reduces the computational complexity to polynomial time.

We define the maximum payoff one can collect with budget among goods when the bid value is restricted to the set for each good as

Then, the following recursion can be used to solve for which gives the optimal solution to (8):

| (9) |

This is the Bellman equation where is the maximum total payoff one can collect using remaining budget and remaining goods. Its optimality can be shown via a simple induction argument. Recall that for all pairs due to the assumption of positive day-ahead prices.

Recursion (9) can be solved starting from and proceeding to , where, for each , is calculated for all . Since the computation of requires at most comparison for any fixed value of and , it has a computational complexity on the order of once the average payoff values for all and are given. For each , computation of for all introduces an additional computational complexity of at most on the order of , which can be observed from the update step of , given in (5). Hence, total computational complexity of DPDS is at each period .

3.3 Convergence and regret of DPDS policy

Under the assumption of Lipschitz continuity, Theorem 1 shows that the value of DPDS converges to the value of the optimal policy under known model with a rate faster than or equal to if the DPDS algorithm parameter with . Consequently, the regret growth rate of DPDS is upper bounded by . If , then the computational complexity of the algorithm is bounded by at each period , and total complexity over the entire horizon is .

Theorem 1

Let denote the bid of DPDS policy for period . If is Lipschitz continuous on with p-norm and Lipschitz constant , then, for any and for DPDS parameter choice ,

| (10) |

and for with ,

| (11) |

Actually, we can relax the uniform Lipschitz continuity condition. Under the weaker condition of for all and for some constant , the incremental regret bound that is given in (10) becomes

The proof of Theorem 1 is derived by showing that the value of converges to the value of due to Lipschitz continuity, and the value of converges to the value of via the use of concentration inequality inspired by [20, 17].

Even though the upper bound of regret in Theorem 1 depends on the budget linearly, this dependence can be avoided in the expense of increase in computational complexity. For example, in the literature, the reward is generally assumed to be in the unit interval, i.e., and , and the expected reward is assumed to be Lipschitz continuous with Euclidean norm and constant . In this case, by following the proof of Theorem 1, we observe that assigning and for some gives a regret upper bound of for . Consequently, if , then regret is achievable by setting .

3.4 Lower bound of regret for any bidding policy

We now show that DPDS in fact achieves the slowest possible regret growth. Specifically, Theorem 2 states that, for any bidding policy and horizon , there exists a distribution for which the regret growth is slower than or equal to the square root of the horizon .

Theorem 2

Consider the case where , , and and are independent random variables with distributions

and , respectively. Let and . Then, for any bidding policy ,

either for or for .

As seen in Theorem 2, we choose a specific distribution for the auction clearing and spot prices. Observe that, for this distribution, the payoff function is Lipschitz continuous with Lipschitz constant because the magnitude of the derivative of the payoff function for and otherwise. So, it satisfies the condition given in Theorem 1.

The proof of Theorem 2 is obtained by showing that, every time the bid is cleared, an incremental regret greater than is incurred under the distribution with ; otherwise, an incremental regret greater than is incurred under the distribution with . However, to distinguish between these two distributions, one needs samples, which results in a regret lower bound of . The bound is obtained by adapting a similar argument used by [29] in the context of non-stochastic MAB problem.

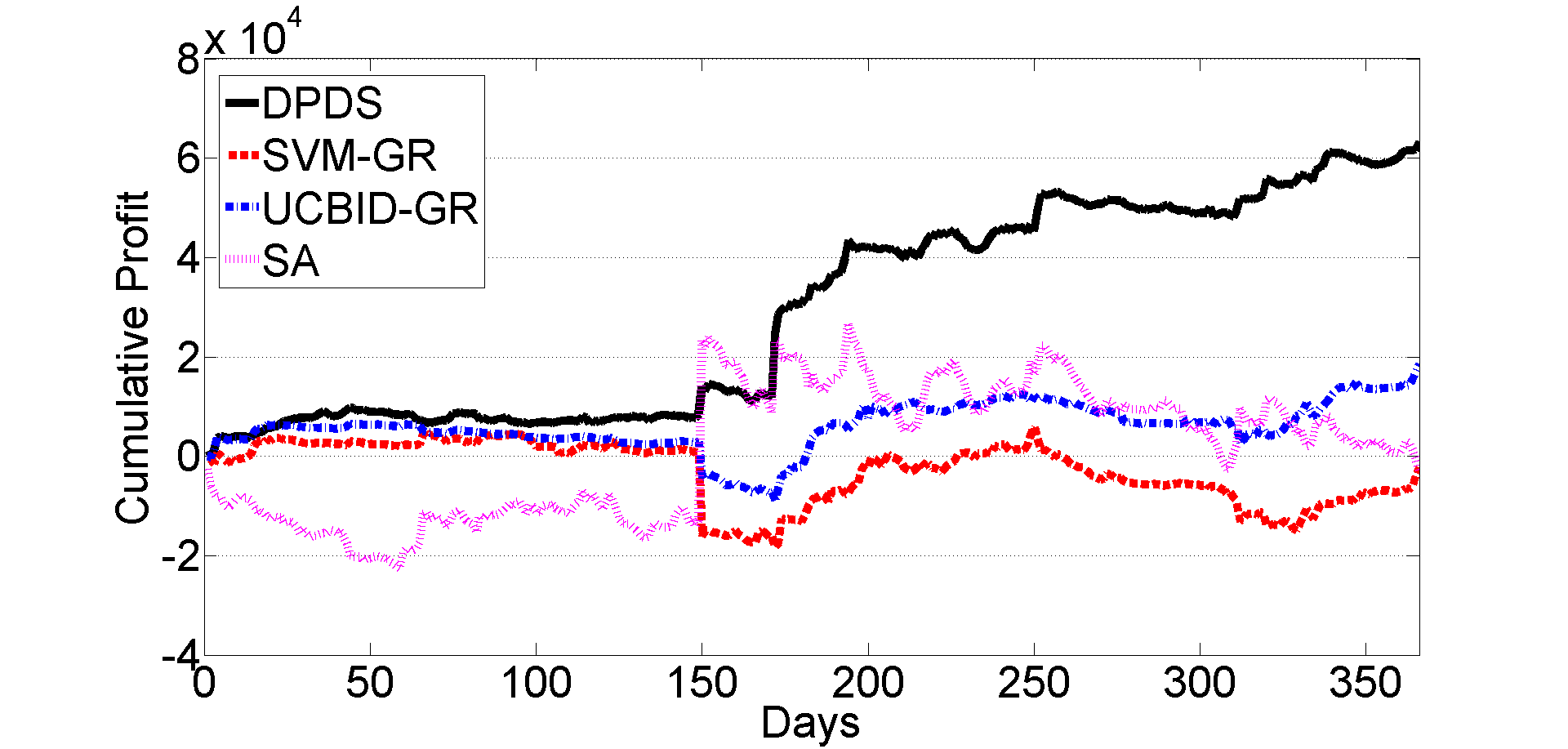

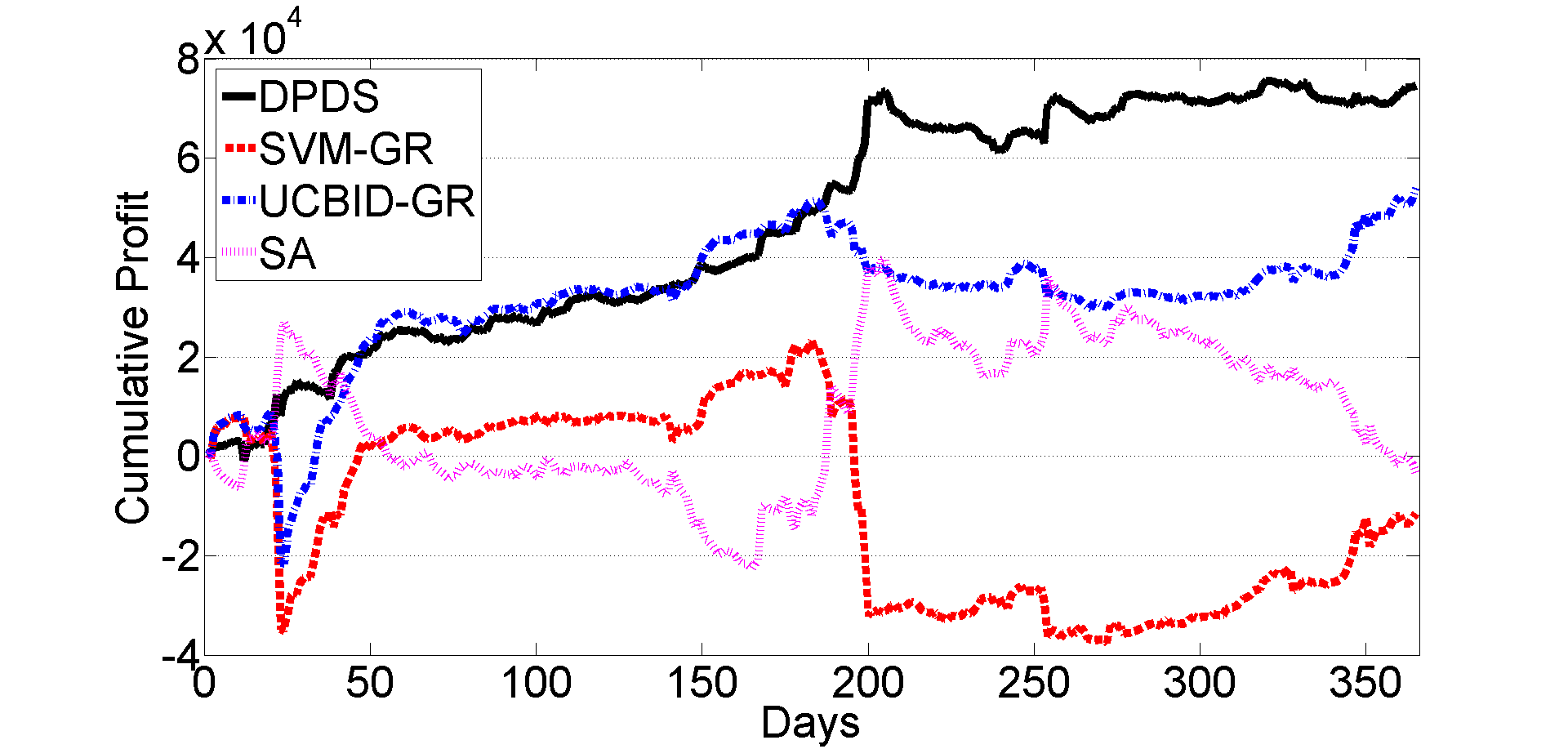

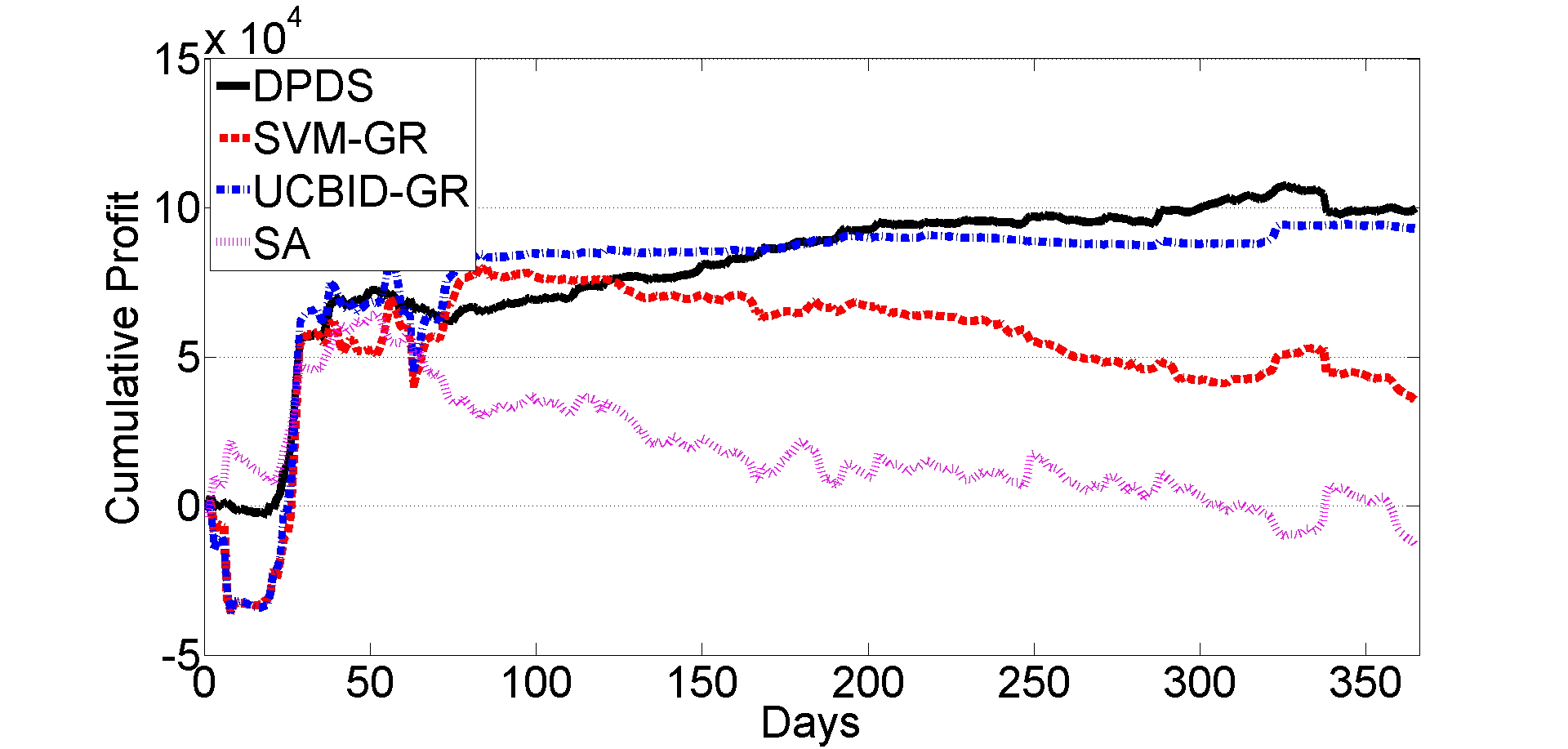

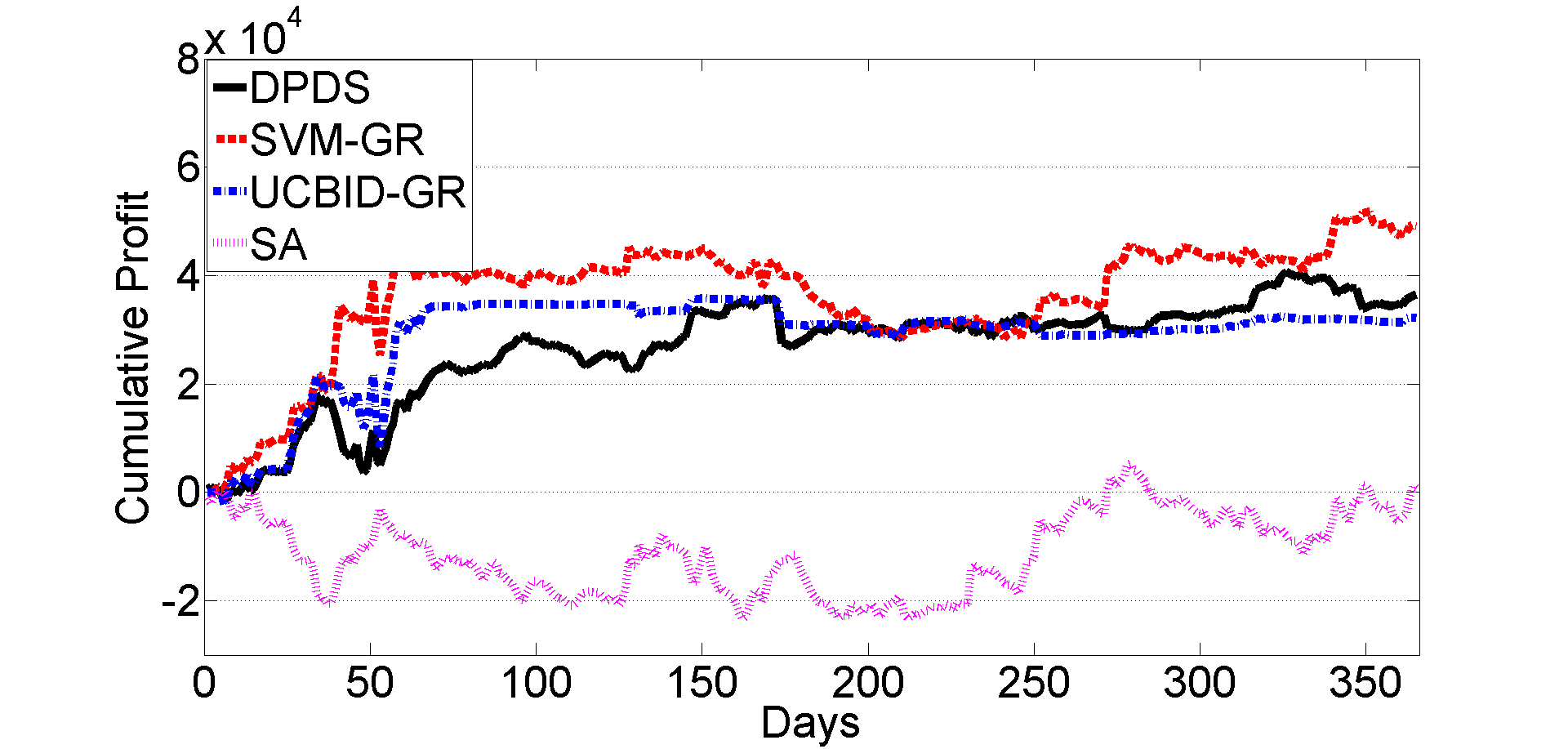

4 Empirical study

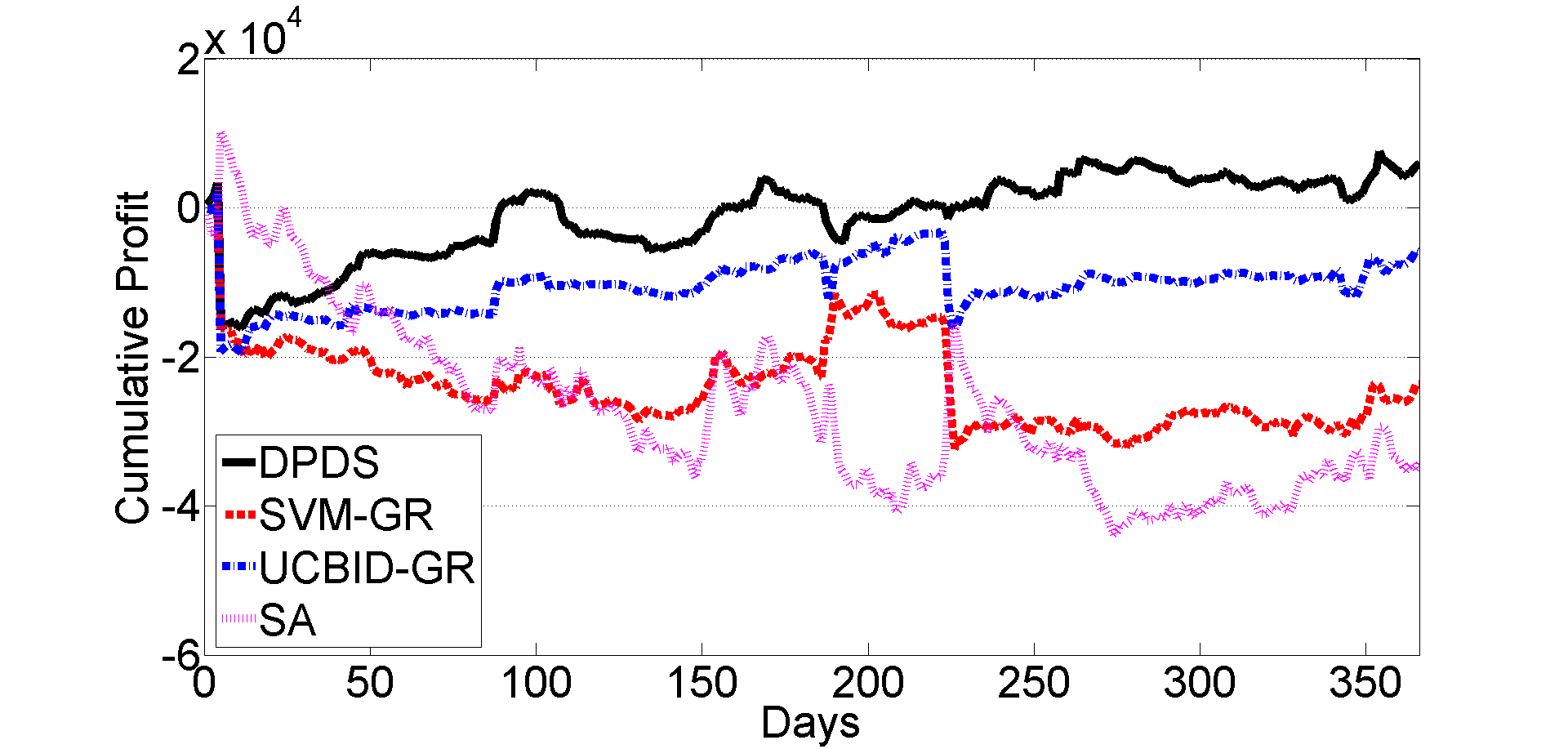

New York ISO (NYISO), which consists of zones, allows virtual transactions at zonal nodes only. So, we use historical DA and RT prices of these zones from 2011 to 2016 [30]. Since the price for each hour is different at each zone, there are different locations, i.e., zone-hour pairs, to bid on every day. The prices are per unit (MWh) prices. We also consider buy and sell bids simultaneously for all location. As explained in Sec. 1.1, a sell bid is a bid to sell in the DA market with an obligation to buy back in the RT market. Hence, the profit of a sell bid at period is . Generally, an upper bound for the DA prices is known, e.g. for NYISO. We convert a sell bid to a buy bid by using , , and instead of , , and . NYISO DA market for day closes at 5:00 am on day . Hence, the RT prices of all hours of day cannot be observed before the bid submission for day . Therefore, the most recent information used before the submission for day was the observations from day .

We compare DPDS with three algorithms. One of them is UCBID-GR, inspired by UCBID [7]. At each day, UCBID-GR sorts all locations according to their profitabilities, i.e., their price spread (the difference between DA and RT price) sample means. Then, starting from the most profitable location, UCBID-GR sets the bid of a location equal to its RT price sample mean until there isn’t any sufficient budget left.

The second algorithm, referred to as SA, is a variant of Kiefer-Wolfowitz stochastic approximation method. SA approximates the gradient of the payoff function by using the current observation and updates the bid of each as follows;

Then, is projected to the feasible set .

The last algorithm is SVM-GR, which is inspired by the use of support vector machines (SVM) by Tang et al. [31] to determine if a buy or a sell bid is profitable at a location, i.e., if the price spread is positive or negative. Due to possible correlation of the price spread at a location on day with the price spreads observed recently at that and also at other locations, the input of SVM for each location is set as the price spreads of all locations from day to day . To test SVM-GR algorithm at a particular year, for each location, the data from the previous year is used to train SVM and to determine the average profit, i.e., average price spread, and the bid level that will be accepted with 95% confidence in the event that a buy or a sell bid is profitable. For the test year, at each period, SVM-GR first determines if a buy or a sell bid is profitable for each location. Then, SVM-GR sorts all locations according to their average profits, and, starting from the most profitable location, it sets the bid of a location equal to the bid level with 95% confidence of acceptance until there isn’t any sufficient budget left.

To evaluate the performance of a year, DPDS, UCBID-GR, and SA algorithms have also been trained starting from the beginning of the previous year. The algorithm parameter of DPDS was set as ; and the step size and of SA were set as and , respectively.

For B=$100,000, the cumulative profit trajectory of five consecutive years are given in Fig. 3. We observe that DPDS obtains a significant profit in all cases, and it outperforms other algorithms consistently except 2015 where SVM-GR makes approximately 25% more profit. However, in three out of five years, SVM-GR suffers a considerable amount of loss. In general, UCBID-GR performs quite well except 2016, and SA algorithm incurs a loss almost every year.

5 Conclusion

By applying general techniques such as ERM, discretization approach, and dynamic programming, we derive a practical and efficient algorithm to the algorithmic bidding problem under budget constraint in repeated multi-commodity auctions. We show that the expected payoff of the proposed algorithm, DPDS, converges to that of the optimal strategy by a rate no slower than , which results in a regret. By showing that the regret is lower bounded by for any bidding strategy, we prove that DPDS is order optimal up to a term.

For the motivating application of virtual bidding in electricity markets (see Sec. 1.1), the stochastic setting, studied in this paper, is natural due to the electricity markets being competitive, which implies that the existence of an adversary is very unlikely. However, it is also of interest to study the adversarial setting to extend the results to other applications. For example, the adversarial setting of our problem is a special case of no-regret learning problem of Simultaneous Second Price Auctions (SiSPA), studied by Daskalakis and Syrgkanis [32] and Dudik et al. [33].

In particular, to deal with the adversarial setting, it is possible to use our dynamic programming approach as the offline oracle for the Oracle-Based Generalized FTPL algorithm proposed by Dudik et al. [33] if we fix the discretized action set over the whole time horizon. More specifically, let the interval length of discretization be , i.e., . Then, it is possible to show that a 1-admissible translation matrix with columns is implementable with complexity . Consequently, no-regret result of Dudik et al. [33] holds with a regret bound of if we measure the performance of the algorithm against the best action in hindsight in the discretized finite action set rather than in the original continuous action set considered here. Unfortunately, as shown by Weed et al. [7], it is not possible to achieve sublinear regret with a fixed discretization for the specific problem considered in this paper. Hence, it requires further work to see if this method can be extended to obtain no-regret learning for the adversarial setting under the original continuous action set.

Acknowledgments

We would like to thank Professor Robert Kleinberg for the insightful discussion.

This work was supported in part by the National Science Foundation under Award 1549989 and by the Army Research Laboratory Network Science CTA under Cooperative Agreement W911NF-09-2-0053.

References

- Milgrom [2004] Paul Milgrom. Putting auction theory to work. Cambridge University Press, 2004.

-

PJM [2015]

PJM.

Virtual transactions in the pjm energy markets.

Technical report, Oct 2015.

http://www.pjm.com/~/media/committees-groups/committees/mc/20151019-webinar/

20151019-item-02-virtual-transactions-in-the-pjm-energy-markets-

whitepaper.ashx. - Li et al. [2015] Ruoyang Li, Alva J. Svoboda, and Shmuel S. Oren. Efficiency impact of convergence bidding in the california electricity market. Journal of Regulatory Economics, 48(3):245–284, 2015.

- Parsons et al. [2015] John E. Parsons, Cathleen Colbert, Jeremy Larrieu, Taylor Martin, and Erin Mastrangelo. Financial arbitrage and efficient dispatch in wholesale electricity markets, February 2015. https://ssrn.com/abstract=2574397.

- Tang et al. [2016] Wenyuan Tang, Ram Rajagopal, Kameshwar Poolla, and Pravin Varaiya. Model and data analysis of two-settlement electricity market with virtual bidding. In 2016 IEEE 55th Conference on Decision and Control (CDC), pages 6645–6650, 2016.

-

Patton et al. [2015]

David B. Patton, Pallas LeeVanSchaick, and Jie Chen.

2014 state of the market report for the new york iso markets.

Technical report, May 2015.

http://www.nyiso.com/public/webdocs/

markets_operations/documents/Studies_and_Reports/Reports/

Market_Monitoring_Unit_Reports/2014/NYISO2014SOMReport__5-13-

2015_Final.pdf. - Weed et al. [2016] Jonathan Weed, Vianney Perchet, and Philippe Rigollet. Online learning in repeated auctions. In 29th Annual Conference on Learning Theory, page 1562–1583, 2016.

- Kellerer et al. [2004] Hans Kellerer, Ulrich Pferschy, and David Pisinger. The Multiple-Choice Knapsack Problem, pages 317–347. Springer Berlin Heidelberg, 2004.

- Kleinberg et al. [2008] Robert Kleinberg, Alexandru Niculescu-Mizil, and Yogeshwer Sharma. Regret bounds for sleeping experts and bandits. In 21st Conference on Learning Theory, pages 425–436, 2008.

- Cesa-Bianchi et al. [1993] Nicolò Cesa-Bianchi, Yoav Freund, David P. Helmbold, David Haussler, Robert E. Schapire, and Manfred K. Warmuth. How to use expert advice. In Proceedings of the Twenty-fifth Annual ACM Symposium on Theory of Computing, pages 382–391. ACM, 1993.

- Freund and Schapire [1995] Yoav Freund and Robert E. Schapire. A decision-theoretic generalization of on-line learning and an application to boosting. In Proceedings of the Second European Conference on Computational Learning Theory, pages 23–37. Springer-Verlag, 1995.

- Auer et al. [1995] Peter Auer, Nicolò Cesa-Bianchi, Yoav Freund, and Robert E. Schapire. Gambling in a rigged casino: The adversarial multi-armed bandit problem. In Proceedings of IEEE 36th Annual Foundations of Computer Science, pages 322–331, 1995.

- Littlestone and Warmuth [1994] Nick Littlestone and Manfred K. Warmuth. The weighted majority algorithm. Information and Computation, 108(2):212 – 261, 1994.

- Kleinberg and Slivkins [2010] Robert Kleinberg and Aleksandrs Slivkins. Sharp dichotomies for regret minimization in metric spaces. In Proceedings of the Twenty-first Annual ACM-SIAM Symposium on Discrete Algorithms, pages 827–846. Society for Industrial and Applied Mathematics, 2010.

- Kleinberg et al. [2015] Robert Kleinberg, Aleksandrs Slivkins, and Eli Upfal. Bandits and experts in metric spaces. arXiv preprint arXiv:1312.1277v2, 2015.

- Krichene et al. [2015] Walid Krichene, Maximilian Balandat, Claire Tomlin, and Alexandre Bayen. The hedge algorithm on a continuum. In Proceedings of the 32Nd International Conference on International Conference on Machine Learning - Volume 37, pages 824–832. JMLR.org, 2015.

- Kleinberg [2005] Robert D. Kleinberg. Nearly tight bounds for the continuum-armed bandit problem. In L. K. Saul, Y. Weiss, and L. Bottou, editors, Advances in Neural Information Processing Systems 17, pages 697–704. MIT Press, 2005.

- Flaxman et al. [2005] Abraham D. Flaxman, Adam Tauman Kalai, and H. Brendan McMahan. Online convex optimization in the bandit setting: Gradient descent without a gradient. In Proceedings of the Sixteenth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 385–394. Society for Industrial and Applied Mathematics, 2005.

- Cope [2009] Eric W. Cope. Regret and convergence bounds for a class of continuum-armed bandit problems. IEEE Transactions on Automatic Control, 54(6):1243–1253, 2009.

- Auer et al. [2002a] Peter Auer, Nicolò Cesa-Bianchi, and Paul Fischer. Finite-time analysis of the multiarmed bandit problem. Machine Learning, 47(2-3):235–256, 2002a.

- Amin et al. [2012] Kareem Amin, Michael Kearns, Peter Key, and Anton Schwaighofer. Budget optimization for sponsored search: Censored learning in mdps. In Proceedings of the Twenty-Eighth Conference on Uncertainty in Artificial Intelligence, pages 54–63. AUAI Press, 2012.

- Tran-Thanh et al. [2014] Long Tran-Thanh, Lampros Stavrogiannis, Victor Naroditskiy, Valentin Robu, Nicholas R Jennings, and Peter Key. Efficient regret bounds for online bid optimisation in budget-limited sponsored search auctions. In Proceedings of the Thirtieth Conference on Uncertainty in Artificial Intelligence, pages 809–818. AUAI Press, 2014.

- Amin et al. [2013] Kareem Amin, Afshin Rostamizadeh, and Umar Syed. Learning prices for repeated auctions with strategic buyers. In C. J. C. Burges, L. Bottou, M. Welling, Z. Ghahramani, and K. Q. Weinberger, editors, Advances in Neural Information Processing Systems 26, pages 1169–1177. Curran Associates, Inc., 2013.

- Mohri and Munoz [2014] Mehryar Mohri and Andres Munoz. Optimal regret minimization in posted-price auctions with strategic buyers. In Z. Ghahramani, M. Welling, C. Cortes, N. D. Lawrence, and K. Q. Weinberger, editors, Advances in Neural Information Processing Systems 27, pages 1871–1879. Curran Associates, Inc., 2014.

- Bubeck and Cesa-Bianchi [2012] Sébastien Bubeck and Nicolò Cesa-Bianchi. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends in Machine Learning, 5(1):1–122, 2012.

- Vapnik [1992] Vladimir Vapnik. Principles of risk minimization for learning theory. In J. E. Moody, S. J. Hanson, and R. P. Lippmann, editors, Advances in Neural Information Processing Systems 4, pages 831–838. Morgan-Kaufmann, 1992.

- Shalev-Shwartz and Ben-David [2014] Shai Shalev-Shwartz and Shai Ben-David. Understanding Machine Learning: From Theory to Algorithms. Cambridge University Press, 2014.

- Dudziński and Walukiewicz [1987] Krzysztof Dudziński and Stanisław Walukiewicz. Exact methods for the knapsack problem and its generalizations. European Journal of Operational Research, 28(1):3 – 21, 1987.

- Auer et al. [2002b] Peter Auer, Nicolò Cesa-Bianchi, Yoav Freund, and Robert E. Schapire. The nonstochastic multiarmed bandit problem. SIAM Journal on Computing, 32(1):48–77, 2002b.

-

Website [2017]

NYISO Website, 2017.

http://www.nyiso.com/public/markets_operations/

market_data/pricing_data/index.jsp. - Tang et al. [2017] Wenyuan Tang, Ram Rajagopal, Kameshwar Poolla, and Pravin Varaiya. Private communications, 2017.

- Daskalakis and Syrgkanis [2016] Constantinos Daskalakis and Vasilis Syrgkanis. Learning in auctions: Regret is hard, envy is easy. In 2016 IEEE 57th Annual Symposium on Foundations of Computer Science (FOCS), pages 219–228, 2016.

- Dudik et al. [2017] Miroslav Dudik, Nika Haghtalab, Haipeng Luo, Robert E. Shapire, Vasilis Syrgkanis, and Jennifer Wortman Vaughan. Oracle-efficient online learning and auction design. In 2017 IEEE 58th Annual Symposium on Foundations of Computer Science (FOCS), pages 528–539, 2017.

- Tsybakov [2009] Alexandre B. Tsybakov. Lower bounds on the minimax risk, pages 77–135. Springer New York, New York, NY, 2009.

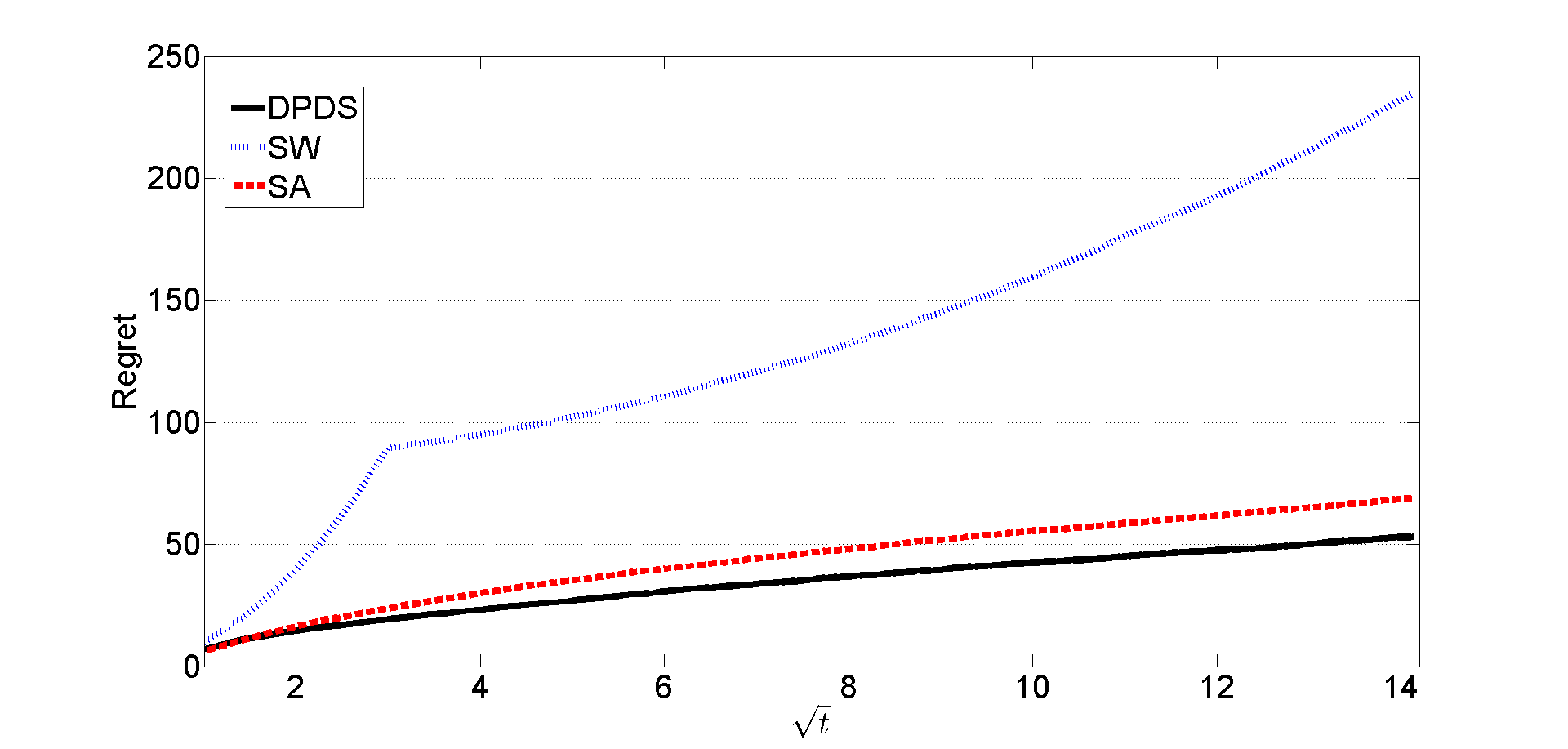

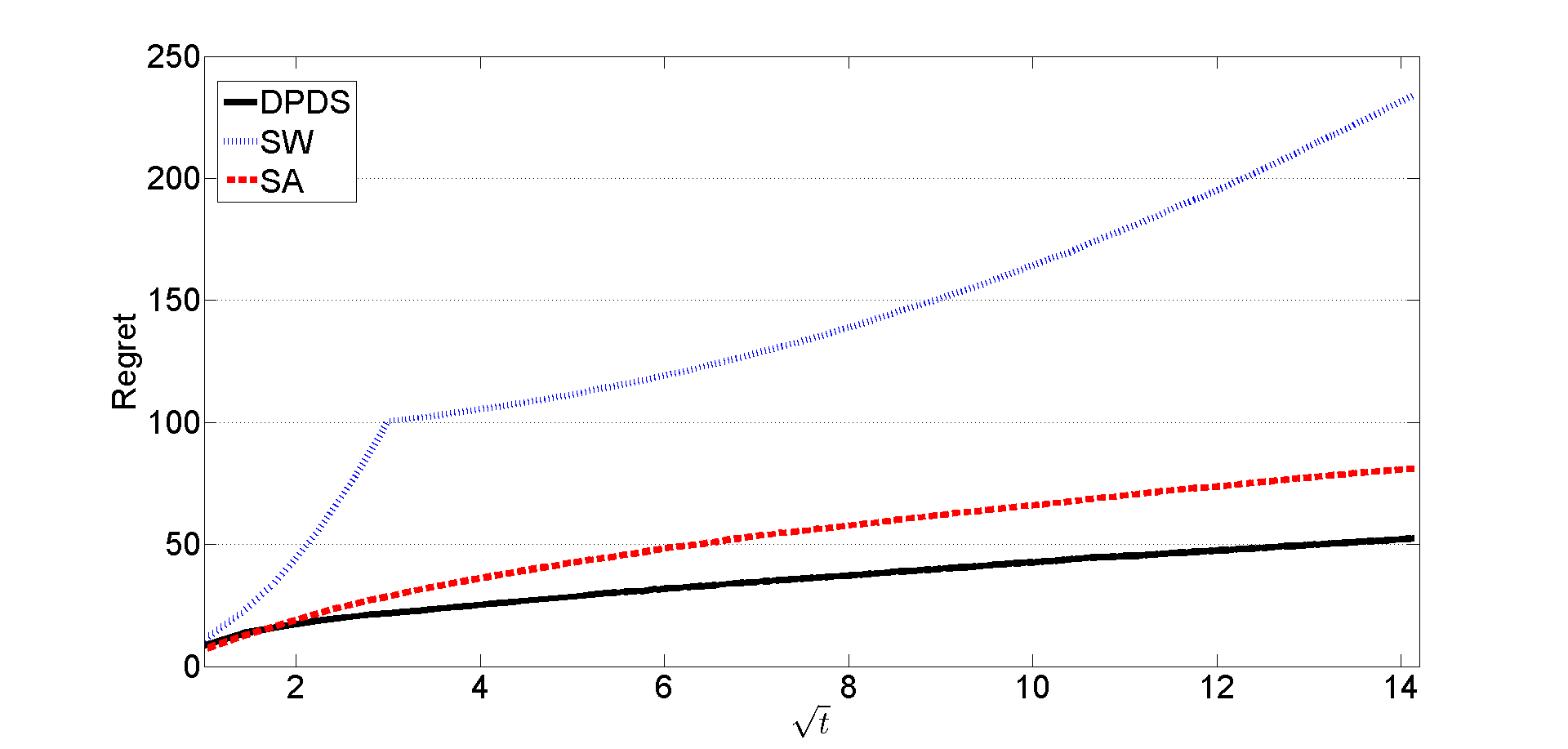

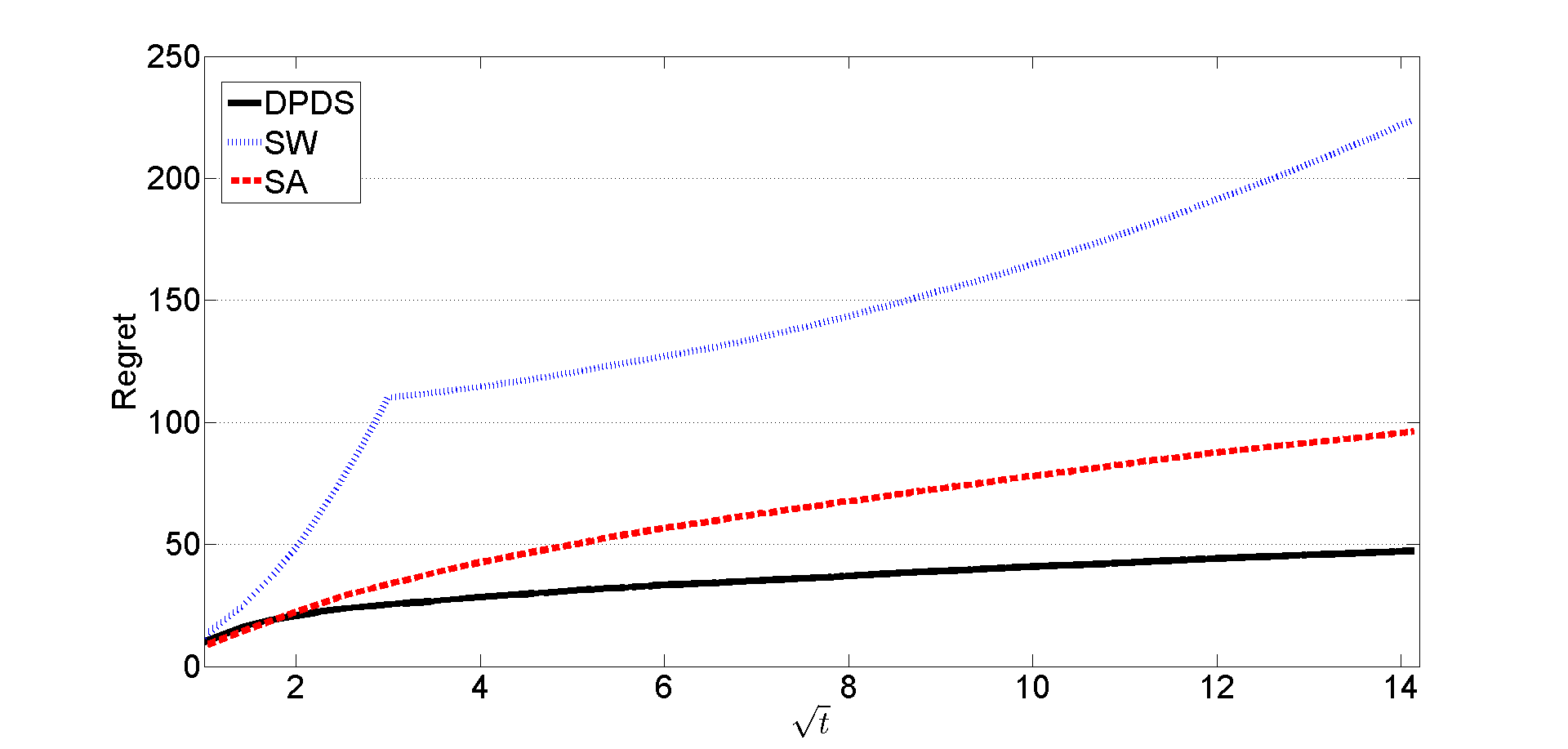

Appendix A Simulation study

Here, we present a simulation example to illustrate the regret growth rate of DPDS. We consider an example with . In this example, and are independent, is exponentially distributed with mean , and is uniformly distributed with mean and support in . Previously, in Sec. 2.1, we stated the characterization of the optimal solution for this example. By using this characterization, we determined the optimal solution and the associated budget for a range of values of the Lagrange multiplier of the budget constraint. More specifically, for the values ,,, and of , the corresponding values of are , , , , respectively. We evaluate the performance of algorithms for these four different values of .

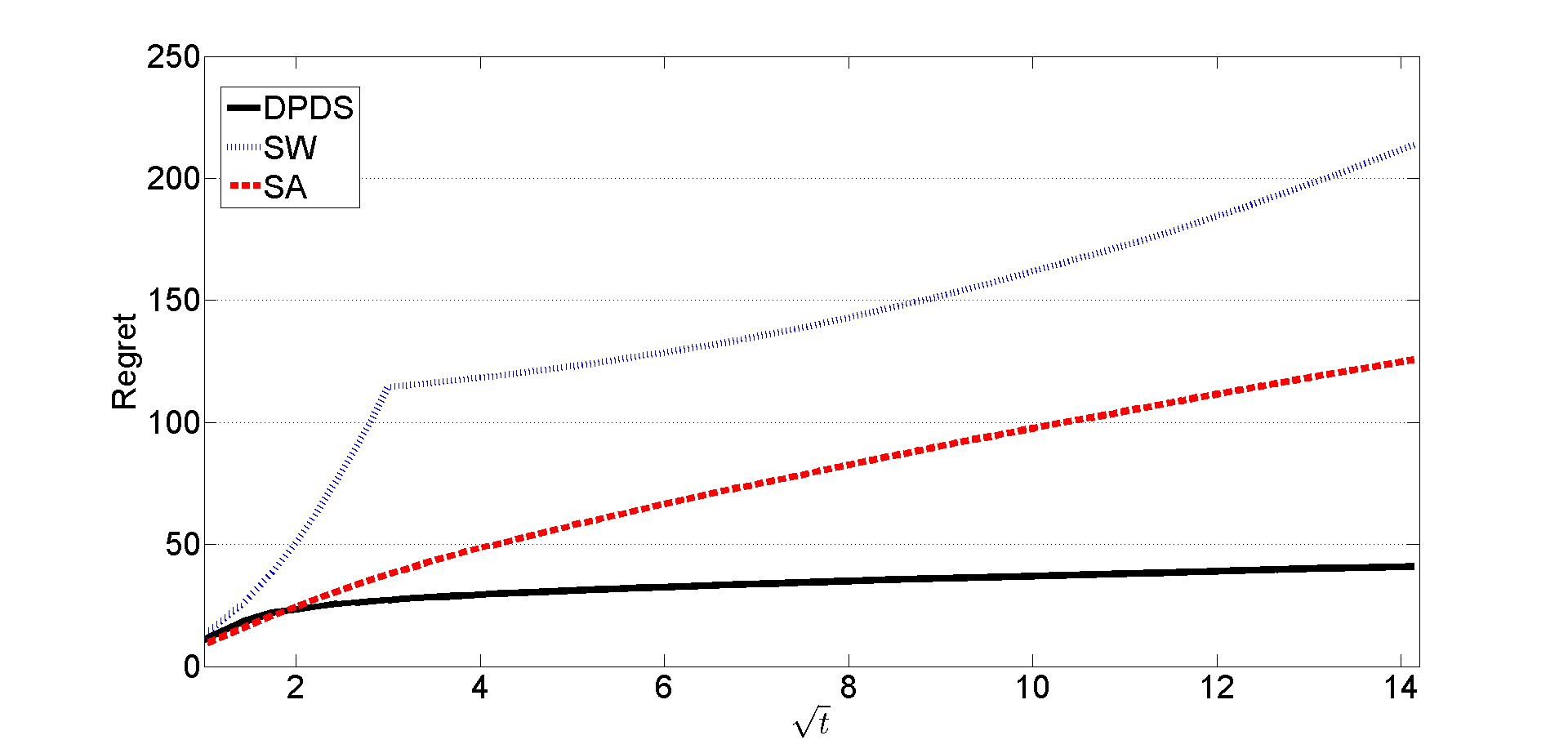

As a benchmark comparison we consider two different approaches.The first one is based on a sliding window (SW) forecasting approach that calculates the average payoff function of each good every day from the prices of last ten days only. Then, it determines the optimal solution maximizing the total average payoff by solving the integer linear program given in (7). The second one, referred to as SA, is a variant of Kiefer-Wolfowitz stochastic approximation method as explained in Sec. 4. Recall that SA approximates the gradient of the payoff function using the current observation and updates the bid of each as follows;

Then, SA projects to the feasible set . To give a good result for , step size and were carefully chosen to be and , respectively. We set the DPDS algorithm parameter .

To calculate the average performance, Monte Carlo runs were used. The regret performances for budgets , , and are given in Fig. 4. In all cases, DPDS outperforms, and its order of regret growth is actually better than . When the SA algorithm parameters are tuned well, we observe that its performance may get close to DPDS as in Fig. 4a. However, when we increase the budget to gradually, the performance of SA deteriorates significantly. Also, as seen in Fig. 4, the regret of SW is much higher than DPDS and SW because SW does not converge to the optimal solution due to fixed number of samples used in prediction.

Appendix B DPDS algorithm pseudo-code

Appendix C Proof of Theorem 1

Recall that and let . Hence, for any ,

We take for all , where denotes the largest integer smaller or equal to , so that and for all . Then, due to Lipschitz continuity of the expected payoff function on with p-norm and constant ,

| (12) |

Since the payoff obtained at each period is in and is Lipschitz, for any where . Then, for any ,

where the last inequality is obtained by the fact that at most one of the indicator functions can be equal to 1 due to the events being disjoint. For any , has to hold if holds. Hence, we can upper bound the last inequality obtained to get

Now, observe that for to hold for any satisfying , the event

holds and/or the event

holds. Consequently,

For any fixed value of , are i.i.d. random variables taking values in with mean . Therefore, by Hoeffding’s inequality, both and are upper bounded by . Using the fact that the cardinality of the set is upper bounded by for and , we get

| (13) |

For any , and . Hence, for any with and ,

Since , for any ,

Appendix D Proof of Theorem 2

Fix any policy . Since and are independent,

and

| (14) |

Let , , denote the distribution of and policy under the choice of , , and , respectively. Also, let and denote the expectation with respect to the distribution and the regret of policy under distribution , respectively.

Under distribution , observe that for any value of . Therefore, optimal solution under known distribution so that . Then, by using (14), the regret given in (3) in Sec. 2.1 can be expressed as

Similarly, under distribution , observe that for any value of . Therefore, optimal solution under known distribution so that . Then, by using (14), the regret can be expressed as

For any non-negative bounded function defined on information history such that for some and for any distributions and , the difference between the expected value of under the distributions and is bounded by a function of the KL-divergence between these distributions as follows:

| (15) |

where is the KL-divergence between and and the last inequality is due to Pinsker’s inequality [34], i.e., where is the variational distance between and . The bound given in (15) is inspired by a similar bound obtained by Auer et al. [29] in the proof of Lemma A.1 for the case of discrete distribution in the context of non-stochastic multi-armed bandit problem.

Now, since and , we use (15) to obtain

and

Consequently,

| (16) |

For any , we can express the distribution of observations in terms of conditional distributions as follows;

where the second equality is due to the independence of and from the past observations , the bid , and from each other. Also, the distribution of given does not depend on . Consequently, for ,

Then, by (16) and by setting , we get

where the last inequality follows from the fact that for .