Blockchains and Distributed Ledgers in Retrospective and Perspective

Abstract

We introduce blockchains and distributed ledgers and describe their potential applications to money and banking. The analysis compares public and private ledgers and outlines the suitability of various types of ledgers for different purposes. Furthermore, a few historical prototypes of blockchains and distributed ledgers are presented, and results of their hard forking are illustrated. Next, some potential applications of distributed ledgers to trading, clearing and settlement, payments, trade finance, etc. are outlined. Monetary circuits are argued to be natural applications for blockchains. Finally, the role of digital currencies in modern society is articulated and various forms of digital cash, such as central bank issued electronic cash, bank money, bitcoin and P2P money, are compared and contrasted.

Keywords: blockchains, distributed ledgers, digital currencies, modern monetary circuit; credit creation banking; interconnected banking network.

”PARATOV. The madness of passion soon passes, and what remains are chains and common sense that tells us that these chains are unbreakable. LARISA. Unbreakable chains!”

Alexander Ostrovsky, Without a Dowry, A drama in four acts

1 Introduction

In this paper, we discuss blockchains (BCs) and distributed ledgers (DLs) in retrospective and prospective, with an emphasis on their applications to money and banking in the 21st century. Additional aspects are discussed in [25], [28], [39].

Civilization is not possible without money, and, by extension, banking, and vice versa. Through the ages, money existed in many forms, stretching from the exquisite gold coins of the Phrygian King Midas, giant stones of Polynesia, cowry shells, the paper money of Khublai Khan and other rulers who came after him, to digital currencies, and everything in between. The meaning of money has preoccupied rulers and their tax collectors, traders, entrepreneurs, laborers, economists, philosophers, writers, stand-up comedians, and ordinary folks alike. It is universally accepted that money has several important functions, such as a store of value, a means of payments in general, and taxes in particular, and a unit of account. The author shares the view of Aristotle formulated in his Ethics: ”Money exists not by nature but by law.” Thus, money is linked to government and government to money. In fact, anything taken in lieu of tax eventually becomes money.

For the last five centuries, money has gradually assumed the form of records in various ledgers. This aspect of money is all-important in the modern world. At present, money is nothing more than a sequence of transactions, organized in ledgers maintained by various private banks, and by central banks who provide means (central bank cash) and tools (various money transfer systems) used to reconcile these ledgers. In addition to their ledger-maintaining functions, private banks play a very important role, which central banks are not equipped to perform. They are the system gatekeepers, who provide know your customer (KYC) services, and system policemen, who provide anti-money laundering services (AML). We argue that, in addition to the more obvious areas of application of distributed ledger technology (DLT), for instance, digital currencies (DC), including central bank issued digital currencies (CBDC), DLT can be used to solve such complex issues as trust and identity, with an emphasis on the KYC and AML aspects, [43]. Further, given that all banking activities boil down to maintaining a ledger, judicious applications of DLT can facilitate trading, clearing and settlement triad, payments, trade finance, etc.

The paper is organized as follows. We introduce DLs and briefly discuss their different types in Section 2. We present historical instances of BCs and DLs in Section 3, and describe what happened when they underwent hard forking. Bitcoin, the most popular current application of DLT, is covered in Section 4, where a few less well known facts about bitcoin are presented. Potential applications of DLT to banking are discussed in Section 5. As an interesting potential area of applications of BC/DLT, we introduce modern version of monetary circuit in Section 6 and show that it can benefit from the BC/DL framework because money moves in a gigantic circle (or several circles if the world economy as a whole is considered). In addition, in the process of money creation by the banking system as a whole, individual banks become naturally interconnected, so that DLs are particularly suitable to describing their interactions. We discuss topics related to CBDC in Section 7, where we explain the rational for its issuance and discuss practical aspects. In particular, we show that CBDC can be used to implement the famous Chicago plan, [2], [7], of moving away from the fractional reserve banking toward the narrow banking. We articulate the differences between Chaum’s and Nakamoto’s approaches to DC and consider their respective pros and cons. Conclusions are drawn in Section 8.

2 BCs and DLs

Databases with joint writing access have been known for decades. Several typical examples are worth mentioning: the concurrent versioning system (CVS), Wikipedia, and distributed databases used on board of naval ships [31].

We start with articulating differences between centralized and distributed databases. In a centralized database, storage devices are all connected to a common processor; in a distributed database, they are independent. Furthermore, in a centralized database, writing access is tightly controlled; in a distributed database, many actors have writing privileges. In the latter case, each storage device maintains its own growing list of ordered records, which, for the efficiency sake, can be organized in blocks, hence, the name Blockchain. To put it differently, in a traditional centralized ledger, the gatekeeper collects, verifies, and performs the write requests of multiple parties, tasks which are distributed in the DL. It should not be taken as fact that these tasks are best distributed: the considerations of efficiency and specialization are relevant as well.

The integrity of the distributed database is cryptographically ensured at two levels. First, only users possessing private keys, can make updates to ”their” part of the ledger. Second, notaries (also called miners) verify that users’ updates are legitimate. Once the updates are notarized, they are broadcast to the whole network, thus ensuring that all copies of the distributed database are in sync. There several types of distributed databases or ledgers. We list them in increasing order of complexity:

(A) traditional centralized ledger;

(B) permissioned private DL (R3 CEV, DAH, and other similar projects);

(C) permissioned public DL (Ethereum, Ripple, etc.);

(D) unpermissioned public DL (bitcoin and the myriad others).

To control the integrity of DL, a variety of mechanisms can be used - proof of work (PoW), proof of stake (PoS), third party verification, etc.

Which ledger should be used? It largely depends on the context. If no joint writing access is required, as is the case with most legacy banking applications, a centralized ledger can be used. If participants do need joint writing access, but know each other in advance, have aligned interests, and can be trusted, as is the case in clearing and settlement, a permissioned private DL can be employed. More details are given in [19].

The best known application of BC/DL is the famous bitcoin, which exists on an unpermissioned public DL whose integrity is maintained by anonymous miners via PoW mechanism. BC/DL can be used for issuing CBDC. However, the sheer scale of the economy precludes unpermissioned public ledger in the spirit of S. Nakamoto, [32] to be used for this purpose, due to the enormous computational effort required for PoW. Resurrecting digicash proposed by D. Chaum, [13], is an exciting possibility.

In many instances, building a DL just to be au courant with times might not be worth the effort.

3 Historical examples of BCs and DLs

3.1 Genealogical trees

The idea of a BC is certainly not new. BCs naturally occur whenever power, land, or property change hands. Some of the earliest examples of BC are the genealogical trees of royal (or, more generally, aristocratic or property owning) families. In such a tree (or BC) the transfer of power from one sovereign to the next is governed by well-defined rules and in most cases, occurs without commotion. However, when these rules become ambiguous and open to interpretation the tree can undergo a hard fork.

In addition to being a chain, a genealogical tree is a distributed ledger. In order to agree on their respective legitimacy and marriage eligibility, royal houses had to inform each other about births, deaths, marriages, and other life events, thus keeping their versions of BCs in sync. In Figure Blockchains and Distributed Ledgers in Retrospective and Perspective we show the genealogical tree of the House of Habsburg engraved by A. Durer. It was distributed to other royal houses, as well as all imperial cities in the Holy Roman Empire.

Usually forking of a succession tree is associated with wars and other acts of violence. This is a cautionary tale for proponents of ubiquitous applications of DLs without a possibility of resolving disputes outside of the ledger itself. Here are two (of many) examples.

In Figure Blockchains and Distributed Ledgers in Retrospective and Perspective we show a simplified genealogical tree of the House of Capet. For ten generation, starting with Hugh Capet, the transfer of power from father to son was smooth. However, the ambiguity occurred when all three sons of Philip IV died without surviving issue, thus creating a power vacuum. In order to resolve it, the peers of France applied the Salic law of Succession, by which persons descended from a previous sovereign only through a woman are not eligible to occupy the throne. The House of Plantagenet did not accept this outcome and started the Hundred Years’ War (1337-1453) against the House of Valois, a cadet branch of the Capetian dynasty, which was a dynastic conflict for control of the Kingdom of France. In the end, the Valois, established themselves as Kings of France at the expense of the Plantagenets.

Similar conflicts occurred with regularity and for very similar reasons throughout the history. For example, the War of the Austrian Succession (1740–1748), which involved all major powers of Europe, was fought to settle the question of the Pragmatic Sanction and decide whether the Habsburg hereditary possessions could be inherited by a woman. It was finally resolved in favor of Maria Theresa, who became the only female ruler of the Habsburg dominions.

Closer to our times, an interesting example of Ethereum hard forking happened in July of 2016, as a result of fixing a theft of $60 Mil worth of Ethereum from DAO. V. Buterin, [12], described the situation as follows:

”The foundation has committed to support the community consensus on the admittedly difficult hard fork decision. … That said, we recognize that the Ethereum code can be used to instantiate other blockchains with the same consensus rules, including testnets, consortium and private chains, clones and spinoffs, and have never been opposed to such instantiations.”

Once again, we see that ambiguity within a BC cannot be resolved via its intrinsic mechanisms.

3.2 Land titles

In more recent times, land registry title deeds are more relevant examples of blockchains. As per Land Registry,

”Title deeds are paper documents showing the chain of ownership for land and property. They can include: conveyances, contracts for sale, wills, mortgages and leases.”

It is clear that titles are blockchains currently held in a central repository; however, instead of miners, succession is verified by notaries. Titles are meaningful candidates for being treated on DL. However, there are still some issues which need to be resolved before it can be done. For example, recent lawsuits by Mark Zuckerberg seeking to force hundreds of Hawaiians to sell to him small plots of land located within the external boundaries of his 700-acre beachfront property on the island of Kauai, is a good case in point. It illustrates that in some instances, it is not possible to identify the first owner of land, and then build a chain of ownership from the original owner to the present, resulting in an ambiguous and potentially vulnerable BC.

4 The bitcoin ecosystem

Bitcoin is not the first digital currency by a long shot, and very likely is not the last major one either. The astute reader will recognize that apart from intriguing technical innovations, bitcoin does not differ that much from the fabled tally sticks used in the Middle Ages. Its precursors include e-cash and digicash invented by D. Chaum, and bitgold invented by N. Szabo, see [13], [33].111There is a heated debate of the true idenity of Satoshi Nakamoto. Nick Szabo is often mentioned as a potential inventor of bitcoin. Here is a small piece of evidence, which might be of interest. Nakamoto’s initials are SN, while Szabo’s are NS. However, Szabo is originally a Hungarian name, where the last name comes first, so his initials would be SN. An interesting coincidence.

All building blocks of bitcoin ecosystem have been known for some time, including two of the most important techniques in public-key cryptography, the Diffie-Hellman key exchange protocol and the RSA encryption system, see [17], [15], [35].222While these techniques were discovered in the academic community in 1976 and 1978 respectively, they were known in the intelligence community since at least 1974. Proof of work, based on cryptographic hash functions, specifically SHA-256, is similar to hashcash invented by Back, [4]; while Merkle trees were introduced in the seminal paper by Merkle, [30].

Ignoring such nuances as wallets, etc., we can describe the basic setup as follows. Participants of the system are represented by their public/private key pairs. The main control variable is the number of bitcoins belonging to a particular public key. This number is known to all participants at all times (in theory). The owner of a particular public key broadcasts their intend to send a certain quantity of bitcoins to another public key. Miners aggregate individual transactions into blocks, verify them to ensure that there is no double spend by competitively providing proof of work, and receive mining rewards in bitcoins. A transaction is confirmed if there are at least six new blocks built on the top on the block to which it belongs. A typical block is shown in Figure Blockchains and Distributed Ledgers in Retrospective and Perspective.

The size of mining rewards is halved at regular intervals; so that the total number of bitcoins in circulation converges to 21 Mil. Currently there are about 16 Mil bitcoins in circulation. It is believed that 3-5 Mil are irretrievably lost. Some 450,000 blocks have been mined so far; a new block is mined every ten minutes on average. Due to the fact that mining rewards are paid with new bitcoins, transaction costs are claimed to be very low. This is a nifty bit of sleight of hand however, because the value of existing bitcoins is constantly diluted. Some representative bitcoin statistics is given in Figure Blockchains and Distributed Ledgers in Retrospective and Perspective.

Bitcoin promises are grand. Its proponents expect it to become a supra-national currency eventually supplanting national currencies, which, in their minds, can be easily manipulated. Many even believe that bitcoin is the modern digital version of gold, due to the effort required for PoW, see, e.g., [33]. Whilst bitcoin is clearly an impressive breakthrough, reality is much less grand than perception, and is quite telling:

(A) A new block is created on average every 10 min.;

(B) The number of transactions per second (TpS) is approximately 7, compared to 2,000 TpS on average handled by VISA;

(C) In monetary terms, the amount of transactions is about 100 Mil USD/day;

(D) Current real (not nominal!) transaction costs are 1.5 Mil USD/day, 1.5% of total volume; in 2012 it was whopping 8%, in 2014 - 6%;

(E) Mining is a cost of electricity game. In high energy cost countries miners go bust: Swedish KnCMiner recently declared bankruptcy ahead of halving miner’s reward. While exact numbers are not known, it is believed that bitcoin consumes as much electricity as EBay, Facebook and Google combined;

(F) Miners are arranged in gigantic pools (so much for P2P mining!); AntPool - 18.7%, F2Pool - 17.7%, BitFury - 7.7%, BTCC Pool - 7.4%, BW.COM - 7.3%. Thus, a 51% attack becomes possible! There is a very high probability that six consecutive blocks will be mined by the same actor (so much for checks and balances!). Most of all these pools are Chinese, partly due to low electricity cost, partly due to high tech advances. Not only miners are predominantly Chinese, so are the players - 91% CNY, 7% USD, 1% EUR;

(G) At the moment, the main purpose of using bitcoin is for speculation and circumvention of capital controls in China.

It is truly amazing to see how miners are prepared to perform socially useless tasks, as long as they are paid for it. A telling historical analogy jumps to mind: During the contest for design of the dome of Santa Maria del Fiore, it was suggested to use dirt mixed with small coins to serve as scaffolding. After the dome’s completion the dirt was to be cleared away for free by the profit-seeking citizens of Florence (proto-miners). It is clear that BC/DL is still awaiting its Brunelleschi, [23].

T. J. Dunning, quoted by Karl Marx in Das Kapital, [29], put it succinctly:

”With adequate profit, capital is very bold. A certain 10 per cent. will ensure its employment anywhere; 20 per cent. certain will produce eagerness; 50 per cent., positive audacity; …”

5 Potential usages of DLT in banking

5.1 Banking X-Road

No bank, however big, is an island; banks can only operate as a group. In the process of their day-to-day activities, they become naturally interlinked. Due to these linkages between banks, DLT can provide a useful tool for facilitating, reconciling, and reporting their interactions. Given that internal technology is bank specific, it is impractical to standardize bank infrastructure. However, it is possible to bring them to a common denominator by emulating the success of the Estonian X-Road and creating a DL solution for banking operations, which, by analogy, can be called the e-bank X-Road. In this regard, DL will serve as an adapter, not dissimilar to an electrical adapter.

In 1997 Estonia started to move to digital government. In 2001, A. Ansper in his master thesis, [3], proposed a suitable design. He developed a distributed P2P secure information system called the e-Estonia X-Road based on the idea of adaptor. X-Road is the digital environment which links various heterogeneous public and private databases and enables them to operate in sync. A small company Cybernetica implemented this design for around 60 Mil EUR.333Other countries tried to follow suite but not all attempts were unqualified success.

Let’s describe a possible design for the e-bank X-Road. Given the non-scalable nature of PoW, and unclear security properties of PoS, X-road has to be controlled by trusted notaries or validators. Two financial institutions, represented by their public keys, use their respective adapters to agree on common terms on a deal. They digitally sign and execute a smart contract, hash it, and broadcast the hashed version to the X-Road participants. A quorum of notaries digitally signs the hash (”laminates” it), and re-posts the signed hash in the common X-Road layer. Validators are paid for their services, similarly to central securities depositories.444Corda, recently described in a white paper by R3, might be a step in this direction, [10].

It is worth noting that a blockchain does not by itself guarantee unambiguous ownership: steps are required to identify and resolve any ambiguities before moving to a BC, and in addition, tools and mechanisms to resolve ambiguities only discovered when the BC is already well established. Both of these requirements are underemphasized in current discussions of BC/DLT applications.

There are several smaller areas in which DLT can be used to reduce transaction costs and other frictions in the conventional system. Such areas include but are not limited to:

(A) post-trade processing;

(B) global payments;

(C) trade finance;

(D) rehypothecation;

(E) syndicated loans;

(F) real estate transactions.

5.2 Trade execution, clearing, settlement

The holy trinity of capital markets is trade execution, clearing, settlement. While initial public offering of stock is an important rite of passage for a new company, secondary trading is a mechanism for continually re-allocating ownership and control in a somewhat optimal fashion. In addition to stocks, many other products, such as equity derivatives, interest rate swaps, commodities, etc. are traded on public exchanges. Moving many over-the-counter (OTC) products to exchanges is an important regulatory imperative [38].

Currently, there are three necessary steps to trade public securities:

(A) Buyers and sellers have to be matched;

(B) The transaction has to be cleared, i.e. novated to a central clearing counterparty (CCP);

(C) The transaction has to be settled, i.e. delivery vs. payment (DvP) has to take place; so that title and money can be transferred as expected.

These steps are characterized by vastly different time scales - trading often takes place in milliseconds, while clearing and settlement take 1-3 days! Although the proverbial T+2, T+3 irritate many people, they might be a bit too fast to push for the T+15’ solution. The actual process is very involved and includes investors, custodial banks, exchanges, brokers (general clearing members of CCPs), CCPs, central securities depositories, regulators, etc.

It is natural to ask if a different design of exchanges can improve the overall process and make it more stable and less costly. The answer is yes and no. On the pros side, there are several issues which the current set-up solves very well:

(A) counterparty credit risk management;

(B) netting;

(C) DvP and credit risk more generally, which is addressed by collecting Initial Margin, Variation Margin, and Guarantee Fund contribution from clearing members;

(D) anonymity;

(E) ability to borrow stocks.555The thriller “Ronin” was not universally critically acclaimed: some critics struggled to identify what it was about [40]. In the author’s view, it takes the difficult challenges of transactions amoung many untrustworth parties which underlie many great thrillers and brings them to the fore, making “Ronin” arguably the greatest of all thrillers (perhaps the ending would have been different had the characters know about blockchain).

On the cons side, numerous issues are rather disconcerting:

(A) cost;

(B) speed;

(C) need for reconciliation and failures.

It is clear that straightforward attempts to apply a blockchain to clearing and settlement (thankfully, to the best of the author’s knowledge, nobody wants to use it in trading per se) cannot be successful. The reasons are simple - instantaneous settlement (T+15’ as it is occasionally called) obliterates all the aforementioned advantages of the current system. It increases the money sloshing around by at least an order of magnitude. Thus, slow clearing and settlement is not so much a consequence of the technological backwardness of exchanges and CCPs (although they are not always using cutting edge technology), but rather a result of their modus operandi.

By using permissioned private ledger(s) one can certainly cut costs, somewhat increase speed of clearing and settlement, and reduce the number of failures and hence the need for reconciliation. In particular, smart contracts, if they can be legally enforced, can solve a part of the DvP conundrum, which will require that both securities and cash are parts of the same ledger. While smart contracts cannot solve all problems, they represent a step in the right direction. A potential evolution of the trading-clearing-settlement triad is illustrated in Figure Blockchains and Distributed Ledgers in Retrospective and Perspective.

5.3 Global payments, trade finance, rehypothecation

Global payments is another area, where DLT can be potentially useful. It is important to note that, in spite of claims to the contrary, the payment system is not broken but rather expensive. For instance, Real-Time Gross Settlement system works well for domestic transactions but is inefficient and expensive for foreign transactions. Thus, some synergies can be gained if a DL, which supports several national currencies at once, is developed to replace the legacy system.

For trade finance, there is the potential to use BC/DL to simplify the flow of information among all participants and smart contracts to partially solve the DvP problem.

In the rehypothecation set-up, it is possible to use BC/DL to untangle the ownership of the collateral. However, this is more of an accounting tool, rather than a comprehensive solution because in many instances the actual legal ownership of collateral cannot be established with certainty.

6 Monetary circuit and money creation

6.1 Monetary circuit

For centuries, the origins, properties and functions of money have been debated in countless expositions. In the fourteenth century, the sagacious French abbot Gilles li Muisis lamented, [8]:

“Money and currency are very strange things; They keep on going up and down and no one knows why; If you want to win, you lose, however hard you try.”

In the twentieth century the great British economist John Maynard Keynes shrewdly observed, [22]:

“For the importance of money essentially flows from it being a link between the present and the future.”

As was mentioned earlier, money is inherently linked with banking, which, over many centuries, gradually evolved from full-reserve towards fractional reserve banking. For instance, the Bank of England founded in 1694 already operated as a fractional reserve bank.666The Bank of England was characterized by Marx, [29], as follows: ”At their birth the great banks, decorated with national titles, were only associations of private speculators, who placed themselves by the side of governments, and, thanks to the privileges they received, were in a position to advance money to the State. Hence the accumulation of the national debt has no more infallible measure than the successive rise in the stock of these banks, whose full development dates from the founding of the Bank of England in 1694.”

In modern societies commercial banks are almost exclusively fractional and produce money ”out of thin air”, see, [21], [42], [27]. This important fact is thoroughly misunderstood by the modern macroeconomic thinking, which incorrectly overemphasizes the intermediation aspect of banking and assigns the money creation role to central banks instead of commercial banks. In reality, commercial banks are not constrained by their deposits and can and do issue money at will. At the same time, their ability to do so is restricted by banking regulations, which impose floors on the amount of banks’ capital and liquidity, so that money creation cannot go ad infinitum.

To understand the role played by money in the economy, one needs to follow its flow and to account for non-financial and financial stocks (cumulative amounts), and flows (changes in these amounts). Here is how Michal Kalecki, the great Polish economist, summarizes the complexity of the issues at hand with his usual flair and penchant for hyperbole, [36]:

“Economics is the science of confusing stocks with flows.”

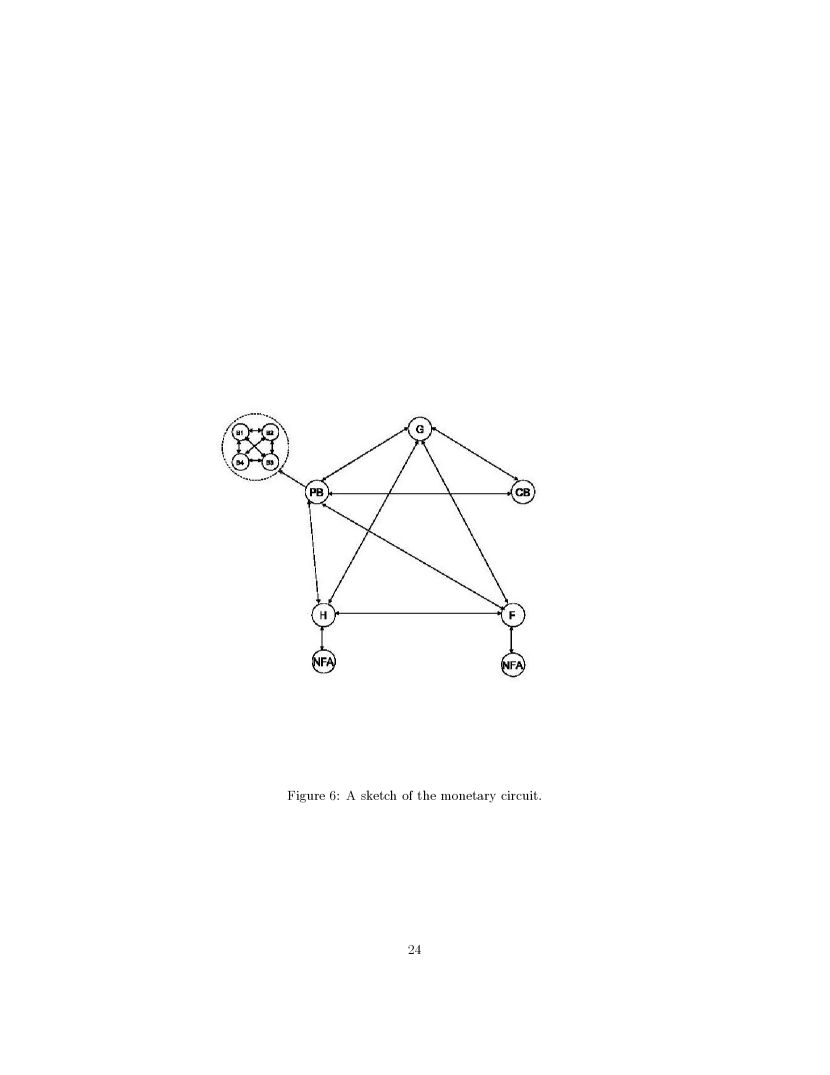

In the author’s opinion, the functioning of the economy and the role of money is best described by monetary circuit theory (MCT), which provides a unifying framework for specifying how money lubricates and facilitates production and consumption cycles in the society. MCT describes in the most precise way the dynamics of the economy and explains how and by whom money is created. More specifically, it describes the interactions among the five sectors, including government, central bank, private banks, firms, and households. As part of the MC, private banks play an outstanding role as credit money creators. In this framework, central banks don’t create money directly, but rather accelerate or slow down the process of money creation by private banks, by providing a unique universal medium in the form of electronic cash for different banks to control their inventories of assets and liabilities. A schematic representation of the monetary circuit is given in Figure 1, which represents money flowing among the above mentioned five sectors of the economy.

6.2 General aspects of money creation

Currently, there are three theories explaining money creation: the credit creation theory, the fractional reserve theory, and the financial theory of intermediation, see, e.g., [21], [42], [27] and references therein. The author firmly believes that only the credit theory advocated by Macleod, Hahn, Wicksell, and Keen among others, correctly reflects the mechanics of linking credit and money creation. Credit creation theory was popular in the nineteenth century, but, unfortunately, gradually lost ground and was overtaken by the fractional reserve theory of banking, which, in turn, was supplanted by the financial theory of intermediation. In the author’s view, the latter theory severely underemphasizes the unique and special role of the banking sector in the process of money creation, and cannot rationally explain things like the global financial crisis of 2007-2008 and other similar events, which happen with disconcerting regularity. This aspect is particularly important because currently there is a profound lack of appreciation on the part of the conventional economic paradigm of the special role of banks. For example, banks are excluded from widely used dynamic stochastic general equilibrium models, which are influential in contemporary macroeconomics and popular among central bankers, in spite of the fact that they systematically fail to produce any meaningful results [11]. It is clear that a vibrant financial system cannot operate without banks, and that the banking system is very complex and difficult to regulate because banks become interconnected as a part of their regular lending activities. In addition to their money creation role, banks regulate access to the monetary system, by providing KYC and AML services.

6.3 Money creation by individual banks

We start with the simplest situation, and consider a single bank, which lends money to a borrower who immediately deposits it with the same bank. Thus, the bank simultaneously creates assets and liabilities. The size of the loan is limited solely by regulations and bank’s own risk appetite. The full cycle from money creation to money annihilation is shown in Figure Blockchains and Distributed Ledgers in Retrospective and Perspective. Money is pumped into the system (created) when it is lent out by the bank and pumped out (annihilated) when it is repaid. If the borrower repays, the principal is destroyed, but the interest stays in the system. If the borrower defaults, the money stays in the system indefinitely. The chain of money transfers from one owner to the next is naturally described by a BC, ideally residing on DL.

6.4 Money creation by the banking system

A more complex case of asset creation by one bank and liabilities by a second bank is illustrated in Figures Blockchains and Distributed Ledgers in Retrospective and Perspective, Blockchains and Distributed Ledgers in Retrospective and Perspective. Linkages between these two banks occur because the first one has to borrow cash from the second, so that their central bank cash holdings reach suitable levels. In this setup, it is clear that central banks do not generate money themselves; instead, they play the role of liquidity providers (if, for example, the second bank does not want to lend money to the first), and system stabilizers (similar to the Watt’s centrifugal governor). Thus, central banks are the glue, which keeps the financial system together. It is clear that BC is even more relevant in the case in question.

6.5 Bank lending vs. bitcoin and P2P lending

In view of the above, the key distinction between bank money creation and bitcoin mining, P2P lending, etc., is evident. Banks create money ”out of thin air”. Since bitcoin transactions are not based on credit, they simply move existing money around. Same is true for P2P transactions - P2P operators are strictly intermediaries, they don’t create money at all! Therefore, banks and P2P operators lend on different scales: banks – money they don’t have, P2P - only money they have. Hence, the P2P impact on the financial system as a whole is very limited.

7 CBDC and negative interest rates

7.1 Why CBDC?

Can and should central banks issue DC? Recently, these discussions have been invigorated by the introduction of bitcoin, [32], and a persistence of negative interest rates, which plagued Medieval Europe in the form of demurrage,the Brakteaten system, and numerous variations of the same tune for centuries. Recall that demurrage was a tax on monetary wealth and required a massive apparatus of coercion to be imposed efficiently. Today, even the best-in-class economists seem to be unsure of its true nature; for instance, Prof. Rogoff equates it with currency debasement, which is a very different mechanism, [37]. The idea of scrip money, i.e. money which requires paying of periodic tax to stay in circulation, thus emulating demurrage, was proposed by S. Gesell, the German-Argentinian entrepreneur and self-taught economist, in the febrile post-WWI atmosphere, [20]. Subsequently, it was regurgitated by Irving Fisher during the great depression, [18].

In the author’s view, it is a sad reflection of the current state of economic affairs, and the level of economic insight, that the current low interest rate environment has prevailed for such a long time, in spite it being such an ineffective tool. Moreover, in some economies, such as Switzerland and Denmark, interest rates have reached seriously negative levels.777One cannot help but notice with a modicum of satisfaction, that critics of the celebrated Vasicek model for interest rates, [41], who vigorously attacked him for allowing short rates to become negative, proved to be completely wrong.

Negative interest rates can be used to simulate inflation; the crucial difference between these two regimes is that physical cash is very valuable under the former, and highly undesirable under the latter. The last line of defense between us and meaningfully negative rates is paper currency. However, in many societies, particularly in Scandinavia, cash is relegated to the far corners of the economy already. It is not hard to imagine that in a few years’ time instead of banknotes, we shall have CBDC, [5], [9], [26]. Once cash is abolished, interest can be made as negative as desired by central bankers.

7.2 How CBDC can be issued?

Currently, there are two approaches to creating digital currencies on a large scale. The first one, which has gained popularity since the invention of bitcoin, is based on unpermissioned DL, whose integrity is maintained by notaries (or miners), see, e.g., [14]. Participants in this BC are pseudo-anonymous since they are hidden behind their public keys. However, in principle, they can be identified by various inversion techniques applied to old recorded transactions, [34].

An earlier approach was developed by Chaum, who introduced a blind signature procedure for converting bank deposits into anonymous cash, see [13]. Chaum’s approach is much cheaper, faster and more efficient than the bitcoin-style one. However, it heavily relies on the integrity of the cash-issuing bank rather than on trustless integrity of bitcoin secured by computational efforts of miners. Central banks can follow either avenue for issuing digital cash. By doing so, central banks will be indirectly providing access to their balance sheets to general public. However, in either eventuality, central banks won’t be able to perform KYC and AML functions and would still have to rely on commercial banks, directly or indirectly, for doing so.

One possibility is as follows: a central bank issues numbered currency units into DL, whose trust is maintained by designated notaries receiving payments for their services. Thus, at any moment, there is an immutable record showing which public key is the owner of a specific currency unit. Given that notary efforts are significantly cheaper and faster than that of bitcoin miners, this construct is easily scalable to satisfy needs of the whole economy. Moreover, since the records of transactions are immutable, it is possible to de-anonymize transactions thus maintaining AML requirements.

In summary, modern technology makes it possible to abolish paper currency and introduce CBDC, which can also be used to address some of the societal ills, such as crime, drug trafficking, illegal immigration, etc., and eliminate costs of handling physical cash, which are of order of 1% of the country’s GDP. It will smooth the motion of the wheels of commerce and help the unbanked to become participants in the digital economy, thus positively affecting the society at large.

7.3 How CBDC can be used to implement the Chicago Plan

Moreover, CBDC makes the execution of the celebrated Chicago Plan of 1933, originally proposed by D. Ricardo in 1824, for introducing narrow (full-reserve) banking entirely possible - both firms and ordinary citizens can have accounts directly with central banks, thus negating the need of having deposits with commercial banks, see [2], [7], [6], [24]. In this case, banks will lose their central position in the economy and become akin to utility providers. They would have to maintain the amount of central bank cash equal to the amount of time deposits. Such narrow banks would in essence become the guardians of the system by providing KYC and AML services and executing simple transactions. In fact, in the wake of the global financial crisis, many central banks massively increased their balance sheets, while commercial banks have chosen to keep enormous quantities of non-mandatory deposits with them. Thus, the system de facto has moved towards narrow banking.

8 Conclusions

While the idea of BC/DLs is not new, modern technology gives it a new lease of life. DLT opens new possibilities for making conventional banking and trading activities less expensive and more efficient by removing unnecessary frictions. Moreover, if built with skill, knowledge, and ambition, it has potential for restructuring the whole financial system on new principles. We emphasize that achieving this goal requires overcoming not only technical, but also political obstacles.

While DLT has numerous applications, it is not entirely clear, which financial applications should be handled first. Exchanges, payments, trade finance, rehypothecation, syndicated loans, and other similar areas, where frictions are particularly high, are attractive candidates. DC, including CBDC, is another very promising venue.

Currently, many applications of DL and related technology appear to be misguided. In some cases, they are driven by a desire to apply these tools for their own sake, rather than because the result would be clearly superior. In other cases they are driven by a failure to appreciate that the current systems may not be as they are because of technological reasons, but rather because of business and other reasons.

So far, practical application of DLT in finance have been limited and a lot remains to be done in order to achieve real breakthroughs.

Acknowledgement 1

The invaluable help of Marsha Lipton from Numeraire Financial in thinking about and preparing this presentation cannot be overestimated. I am grateful to several colleagues, including Alex Pentland and David Shrier from MIT, Damir Filipovic from EPFL, Matheus Grasselli from McMaster, and Paolo Tasca from UCL for their help and suggestions. As a CEO of StrongHold Bank Labs, I am currently working on a new type of a digital bank, which will be utilizing some of the ideas presented in this paper. I am grateful to my colleague Julian Phillips from SHBLabs for his insightful and thorough feedback.

References

- [1] Acharya, V.V., Cooley, T.F., Richardson, M.P. and Walter, I. (Eds.) (2010), Regulating Wall Street: The Dodd-Frank Act and the new architecture of global finance, John Wiley & Sons, Hoboken, N.J.

- [2] Allen, W.R. (1993), ”Irving Fisher and the 100 percent reserve proposal”, The Journal of Law and Economics, Vol. 36 No. 2, pp.703-717.

- [3] Ansper, A., Buldas, A., Freudenthal, M. and Willemson, J. (2003), ”Scalable and efficient PKI for inter-organizational communication”, in Computer Security Applications, Proceedings of 19th Annual Conference, IEEE, pp. 308-318.

- [4] Back, A. (2002), ”Hashcash-a denial of service counter-measure”, Working Paper.

- [5] Barrdear, J. and Kumhof, M. (2016), ”The macroeconomics of central bank issued digital currencies”, Working Paper.

- [6] Baynham-Herd, X. (2016), ”Banking Balance Sheets and Blockchain: A Path to 100% Digital Money”, UBS Discussion Paper.

- [7] Beneš, J. and Kumhof, M. (2012), ”The Chicago plan revisited”, Working Paper.

- [8] Bloch, M. (1953), ”Mutations monétaires dans l’ancienne France: Première Partie, Annales. Economies, Societes, Civilisations”, Vol. 8 No. 2, pp. 145-158.

- [9] Broadbent, B. (2016), ”Central banks and digital currencies”, Speech at London School of Economics.

- [10] Brown, R.G., Carlyle, J., Grigg, I. and Hearn, M. (2016), ”Corda: An Introduction”, R3 CEV, Working Paper.

- [11] Buiter, W.H. (2009), ”The unfortunate uselessness of most ’state of the art’ academic monetary economics”, Working Paper.

- [12] Buterin, V. (2016), Blog post, https://blog.ethereum.org/2016/07/26/ onward_from_the_hard_fork/ .

- [13] Chaum, D. (1983), ”Blind signatures for untraceable payments”, in Advances in cryptology, Springer US, pp. 199-203.

- [14] Danezis, G. and Meiklejohn, S. (2015), ”Centrally banked cryptocurrencies, Working Paper.

- [15] Diffie, W. and Hellman, M. (1976), ”New directions in cryptography”, IEEE transactions on Information Theory, Vol. 22 No. 6, pp.644-654.

- [16] Dwyer, J. (2016), ”Central Bank-Issued Digital Currency: Assessing Central Bank Perspectives of DLT and Implications for Fiat Currency and Policy Stimulus”, Celent Working Paper.

- [17] Ellis, J.H. (1999) ”The history of non-secret encryption”, Cryptologia, Vol. 23 No. 3, pp.267-273.

- [18] Fisher, I., Cohrssen, H.R. and Fisher, H.W. (1933), Stamp scrip, Adelphi Company, New York, NY.

- [19] Greenspan, G. (2015), ”Avoiding pointless blockchain project”, Working Paper.

- [20] Ilgmann, C. (2015), ”Silvio Gesell:“A strange, unduly neglected” monetary theorist”, Journal of Post Keynesian Economics, Vol. 38 No. 4, pp.532-564.

- [21] Keen, S. (2001), Debunking economics: The naked emperor of the social sciences, Zed Books, London & New York.

- [22] Keynes, J.M. (1936), General theory of employment, interest and money, Macmillan, London.

- [23] King, R. (2013), Brunelleschi’s Dome: How a Renaissance Genius Reinvented Architecture, Walker & Company, New York, NY.

- [24] King, M. (2016), The End of Alchemy: Money, Banking, and the Future of the Global Economy, WW Norton & Company, New York, NY.

- [25] Lipton, A. (2016), ”Banks must embrace their digital destiny”, Risk Magazine, Vol. 29 No. 7.

- [26] Lipton, A. (2016), ”The decline of the cash empire”, Risk Magazine, Vol. 29 No. 10.

- [27] Lipton, A. (2016), ”Modern Monetary Circuit Theory, Stability of Interconnected Banking Network, and Balance Sheet Optimization for Individual Banks”, International Journal of Theoretical and Applied Finance, Vol. 19 No. 06, pp.1650034-1 - 1650034-57.

- [28] Lipton, A., Shrier, D. and Pentland, A. (2016), ”Digital Banking Manifesto: The End of Banks?”, in Frontiers of Financial Technology, VisionaryFuture, pp. 117-140.

- [29] Marx, K. (1867), Das Kapital: Kritik der Politischen Őkonomie, Verlag von Otto Meisner, Germany.

- [30] Merkle, R.C. (1987), ”A digital signature based on a conventional encryption function”, in Conference on the Theory and Application of Cryptographic Techniques, Springer Berlin Heidelberg, pp. 369-378.

- [31] Miller, S.J. (1993), ”A fully replicated distributed database system”, Research Note ERL-0719-RN, Electronics Research Laboratory.

- [32] Nakamoto, S. (2008), ”Bitcoin: A peer-to-peer electronic cash system”, Working Paper.

- [33] Popper, N. (2015), Digital gold: The untold story of Bitcoin, Penguin UK.

- [34] Reid, F. and Harrigan, M. (2013), ”An analysis of anonymity in the bitcoin system”, in Security and Privacy in Social Networks, Springer New York, pp. 197-223.

- [35] Rivest, R.L., Shamir, A. and Adleman, L. (1978), ”A method for obtaining digital signatures and public-key cryptosystems”, Communications of the ACM, Vol. 21 No. 2, pp.120-126.

- [36] Robinson, J. (1977), ”Michal Kalecki on the economics of capitalism”, Oxford Bulletin of Economics and Statistics, Vol. 39 No. 1, pp.7-17.

- [37] Rogoff, K.S. (2016), The Curse of Cash, Princeton University Press, Princeton and Oxford.

- [38] Skeel, D. (2010), The new financial deal: understanding the Dodd-Frank Act and its (unintended) consequences, John Wiley & Sons, Hoboken, NJ.

- [39] Tasca, P., Aste, T., Pelizzon, L. and Perony, N. (Eds.) (2016), Banking Beyond Banks and Money: A Guide to Banking Services in the Twenty-First Century, Springer, Switzerland.

- [40] Turan, K. (2004), Never Coming to a Theater Near You: A Celebration of a Certain Kind of Movie, PublicAffairs, New York.

- [41] Vasicek, O. (1977), ”An equilibrium characterization of the term structure”, Journal of financial economics, Vol. 5 No. 2, pp.177-188.

- [42] Werner, R.A. (2014), ”Can banks individually create money out of nothing? - The theories and the empirical evidence”, International Review of Financial Analysis, Vol. 36, pp.1-19.

- [43] Zyskind, G., Nathan, O. and Pentland, A. (2015), ”Enigma: Decentralized computation platform with guaranteed privacy”, Working Paper.

![[Uncaptioned image]](/html/1703.01505/assets/x1.png)

![[Uncaptioned image]](/html/1703.01505/assets/x2.png)

![[Uncaptioned image]](/html/1703.01505/assets/x3.png)

![[Uncaptioned image]](/html/1703.01505/assets/x4.png)

![[Uncaptioned image]](/html/1703.01505/assets/x5.png)

![[Uncaptioned image]](/html/1703.01505/assets/x7.png)

![[Uncaptioned image]](/html/1703.01505/assets/x8.png)

![[Uncaptioned image]](/html/1703.01505/assets/x9.png)