CoVaR-based portfolio selection

Abstract

We consider the portfolio optimization with risk measured by conditional

value-at-risk, based on the stress event of chosen asset being equal to the opposite of its value-at-risk level, under the normality assumption. Solvability conditions are given and illustrated by examples.

keywords:

portfolio optimization , conditional Value-at-Risk (CoVaR=) , value-at-risk , normal distributionMSC:

[2010] 91-G101 Introduction

What is the best asset allocation? Markowitz [1952] answered this question in his landmark article on mean-variance model of portfolio selection, followed few years later by a book— Markowitz [1959]—on the same subject and thus the Modern Portfolio Theory originated, providing its creator with Alfred Nobel Memorial Prize in Economic Sciences (1990)111Awarded jointly to Harry M. Markowitz, Merton H. Miller and William F. Sharpe. . Markowitz exceptional idea was to minimize portfolio variance or (equivalently) standard deviation for a fixed portfolio return . Therefore, the investor faces an optimization problem, given as follows:

| (1) |

where portfolio (i.e. investment strategy) meets the natural condition of summing up to and is defined as expected value of -dimensional random variable of returns on risky assets, , with being the univariate random variable of return on the portfolio. The constraint is optional and concerns the possibility of short-selling. Without it the model is known as the Black model—see Alexander and Francis [1986] and the original article of Black [1972].

To obtain a non-degenerate problem, two assumptions are made. First, , i.e. not every asset has the same expected return. Second, the covariance matrix of , is positive definite.

Merton solved problem (1) with those two assumptions satisfied and constraint dropped. His formulae in contemporary terms (cf. Merton [1972]) assume the following form:

| (2) |

where . The graph of is a line called the critical line. Portfolio is said to be efficient if there is no portfolio with either smaller for the same or greater , or greater for the same or smaller . Both terms first appear in Markowitz [1952]. The set of efficient portfolios is a subset of . Its image in mapping is known as the efficient frontier.

The main objective of this paper is to provide some insight into problem (1) with as the alternate risk measure, without constraint (if not stated differently), and under normality assumption added to original ones. We begin with briefly stating the reasons why is not of interest in that case and then proceed with -a conditional value at risk proposed by Adrian and Brunnermeier [2008, 2016], not to be confused with (Mean Excess Loss) as used by Rockafellar and Uryasev [2000] for the optimization problem. With the aid of examples the properties of the new risk measure, the critical set i.e. the set of minimum- portfolios for fixed expected value and the very existence of that set are discussed.

2 Risk measured by VaR

For -a random variable of an asset portfolio (the profit/loss approach) let value-at-risk be defined as . It is worth noting that is a downside risk measure, while is classified as a volatility measure. The former is monotone, translation invariant and positively homogeneous, lacking only subadditivity to be a coherent risk measure (cf. Artzner et al. [1999]), while the latter is just positively homogeneous. However, for and under normality assumption, is coherent, as Artzner et al. [1999] prove. It might seem promising, but as soon as we calculate the actual value-at-risk of portfolio, , we can clearly see that it yields the same solutions as (for formal proofs see Alexander and Baptista [2002]).

3 Risk measured by

In present section we begin by giving a definition of , as introduced by Adrian and Brunnermeier [2008, 2016], though notation is rather that of Mainik and Schaanning [2014] (cf. Bernardi et al. [2017]).

The first assumption to be made is that of normality, , . For bivariate Gauss distribution, where

and for , Mainik and Schaanning [2014] obtain formula:

| (3) |

The second assumption, , is only natural as investor interest in calculating lays chiefly in significance level being close to . Consequently, and are positive numbers which prevents us from dwelling on sub-cases.

This established, the distribution of is conditioned on one chosen variable , . Without loss of generality let that be . Naturally, and .

Investor faces the following optimization problem:

| (4) |

For there is a linear relationship between and . Consequently is a constant, hence respectively .

We observe (after applying formulae and (3), and a little manipulation) that the following is true:

| (5) |

where is defined as:

with being a symmetric positive definite matrix (see the Appendix) and where .

Since depends solely on for given , let us from now on denote is as . Therefore optimization problem (4) presents itself as follows:

| (6) |

Obviously for the critical set remains independent of . Function is convex (see Appendix) and positive homogeneous (of degree ), as is.

is not bounded above and it does not have to be bounded below222E.g. should partial derivative of with respect to , i.e. be a non-zero number, the function is not bounded below. On the other hand, consider an example with diagonal and where . Then function is bounded below. (contrary to which is always bounded below).

What conditions should be met in order for problem (6) to have a solution? Before introducing the main theorem of this work, we define , , ,

, and

with .

Theorem 1

Let vectors be linearly independent.

If then the optimization problem

| (7) |

equivalent to problem (6) has for a given a unique solution

and

Moreover, for and the following is true:

-

1.

For there is no -efficient portfolio.

-

2.

For only for are -efficient portfolios.

-

3.

For all portfolios constitute the set

of -efficient portfolios.

We relegate the proof to Appendix.

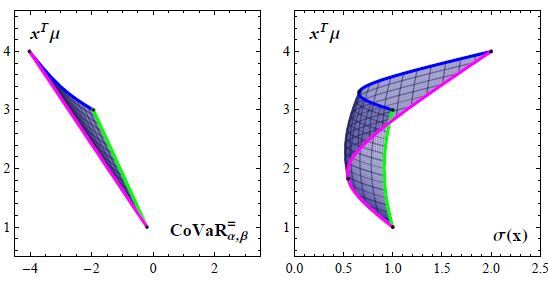

Now some examples will be presented. The first shows how unless condition is satisfied we obtain optimization problem without solution and suggests using constraint in such a case.

3.1 Example 1

By a straightforward calculation we get:

and Suppose —together with condition it implies and . Without constraint we can solve the optimization problem (6) for by minimizing over the following function:

Clearly, , hence does not attain minimum, which shows that even with additional constraints in this simple example may be unbounded below. Now we add the non-negativity constraint i.e. we minimize on the standard -simplex (equilateral triangle in ):

Figure (1) might be of use both as an illustration and providing comparisons.

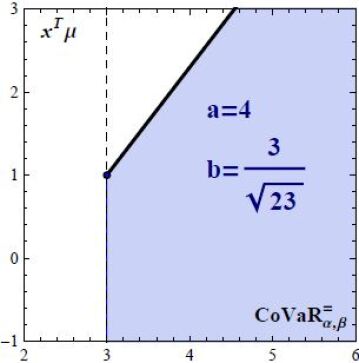

3.2 Example 2

In this case . Using just the ‘portfolio constraint’, from the optimization problem (6) generates a bounded below function with unique global minimum:

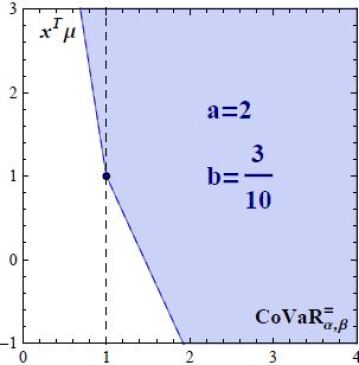

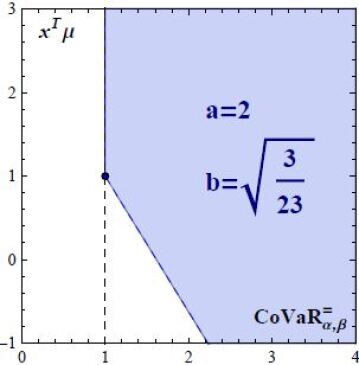

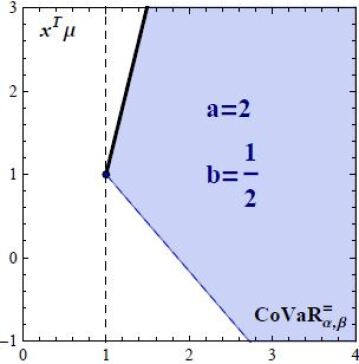

3.3 Example 3

where:

This example is essentially an illustration of the dependence between values of and the obtained set of -efficient portfolios. We have

Figure (2) presents five different possibilities, of which two first represent case in the theorem, two next—case and the last one case

The -efficient frontiers are marked by thick lines.

4 Appendix: proofs auxiliary results

4.1 Positive definiteness of and positive semidefiniteness of

For and there is:

Matrix has only one non-zero element (i.e. in first row, first column). In consequence has rank equal at least as its columns from second to last are the corresponding columns of . Therefore matrices and are of the rank , so that they are positive definite and positive semidefinite, respectively.

On the other hand, for and we have

so that if and only if (due to positive definiteness of ) which in problem (4) implies .

4.2 Convexity of function

Function is a norm induced by inner product and as such is convex on –indeed, due to being positively homogeneous of degree , the Jensen’s inequality can be rewritten as:

| (8) |

which is just triangle inequality, satisfied by every norm.

The fact that contradicts the strict convexity. However, as the inequality (8) is strict provided that , function is strictly convex on every line segment not contained in any half-line with the origin as its element.

The instantaneous implication is that is convex on . Function is convex as a linear combination of (proper) convex functions with positive coefficients.

4.3 A lemma about certain convex function

Lemma 1

Let us consider function , with . Then is convex and the following is true:

-

1.

For there is a global minimum attained

at -

2.

For there is no global minimum, but

-

3.

For function is not bounded below, .

Proof via direct calculation.

4.4 Proof of the main theorem

For linearly independent (which implies ) we solve the following problem:

| (9) |

and then vary the parameter in order to minimize the obtained solution with respect to . Naturally, is strictly convex.

Via the method of Lagrange multipliers we get . In consequence . Left multiplication of first equation (by ) and the second equation (by and ) gives us:

| (10) | ||||

| (11) | ||||

| (12) |

Scalars are easily obtained from (11) and (12). Ultimately,

where is the Gramian matrix of linearly independent vectors , with the inner product defined by matrix ( being positive definite implies positive definiteness of both and ). Unless this quadratic function of is positive and bounded from (in the former case is attained for and equation (10) yields ). Then,

We take . Then the obtained function is of the type from lemma 4.3 with . That means the global minimum is achieved for

under condition (i.e ) equivalent to as .

Then, yields formula for :

which is correct also for as . Formula for comes as the obvious consequence:

Now we find -efficient portfolios. The only ones that might satisfy the required conditions are portfolios as graph of is the lower boundary of . Function is a continuous piecewise function comprising two linear functions. It can be easily observed that whether for a given portfolio is -efficient depends solely on the ratio of and , or, to be more specific, on the inequalities between , and .

4.5 Additional remarks

First note that without assuming linear independence of there is (by previous assumption and are linearly independent). Therefore the optimization problem (7) would have the same critical set as that of Markowitz.

Observe also that for function converges to a linear function which is only to be expected by looking at the function defined in (7). Still, the problem is not equivalent to that of minimizing (or ) as , not , is minimized. A linear function is achieved in no other way, as due to linear independence of . Therefore, the image of the ‘-critical polyline’ in consist of two rays and with our assumption concerning is never a line.

Now let (i.e. ). Note here that from the lemma is not necessarily a positive number. Should we solve:

for any solution we would get (solution being unique for given only in case of ).

5 Future research

Present work but lightly touches the wide and complex subject of portfolio optimization for . For any question answered few more are raised. What if the normality assumption was to be dropped? What if the Gauss distribution was to be replaced by another one? Will the results hold for ? How solving the problem for various families of copulas, as done in Bernardi et al. [2017], would change the outcome? Also, Mainik and Schaanning [2014] show that is not monotonic with respect to —how badly does it affect the presented model?

Acknowledgments

The author thanks Professor Piotr Jaworski for his invaluable advice and insightful comments.

This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors.

References

- Adrian and Brunnermeier [2008] Adrian, T., Brunnermeier, M. K., 2008. Staff reports.

- Adrian and Brunnermeier [2016] Adrian, T., Brunnermeier, M. K., 2016. Covar. American Economic Review 106 (7), 1705–41.

- Alexander and Baptista [2002] Alexander, G. J., Baptista, A. M., 2002. Economic implications of using a mean-var model for portfolio selection: A comparison with mean-variance analysis. Journal of Economic Dynamics and Control 26 (7), 1159–1193.

- Alexander and Francis [1986] Alexander, G. J., Francis, J. C., 1986. Portfolio Analysis. Prentice-Hall foundations of finance series. Prentice-Hall.

- Artzner et al. [1999] Artzner, P., Delbaen, F., Eber, J.-M., Heath, D., 1999. Coherent measures of risk. Mathematical finance 9 (3), 203–228.

- Bernardi et al. [2017] Bernardi, M., Durante, F., Jaworski, P., 2017. Covar of families of copulas. Statistics & Probability Letters 120, 8–17.

- Black [1972] Black, F., 1972. Capital market equilibrium with restricted borrowing. The Journal of Business 45 (3), 444–455.

- Mainik and Schaanning [2014] Mainik, G., Schaanning, E., 2014. On dependence consistency of covar and some other systemic risk measures. Statistics & Risk Modeling 31 (1), 49–77.

- Markowitz [1952] Markowitz, H., 1952. Portfolio selection. The Journal of Finance 7 (1), 77–91.

- Markowitz [1959] Markowitz, H., 1959. Portfolio Selection: Efficient Diversification of Investments. New York : Wiley.

- Merton [1972] Merton, R. C., 1972. An analytic derivation of the efficient portfolio frontier. Journal of financial and quantitative analysis 7 (04), 1851–1872.

- Rockafellar and Uryasev [2000] Rockafellar, R. T., Uryasev, S., 2000. Optimization of conditional value-at-risk. Journal of risk 2, 21–42.