Optimal Investment and Pricing in the Presence of Defaults

Abstract.

We consider the optimal investment problem when the traded asset may default, causing a jump in its price. For an investor with constant absolute risk aversion, we compute indifference prices for defaultable bonds, as well as a price for dynamic protection against default. For the latter problem, our work complements [30], where it is implicitly assumed the investor is protected against default. We consider a factor model where the asset’s instantaneous return, variance, correlation and default intensity are driven by a time-homogenous diffusion taking values in an arbitrary region . We identify the certainty equivalent with a semi-linear degenerate elliptic partial differential equation with quadratic growth in both function and gradient. Under a minimal integrability assumption on the market price of risk, we show the certainty equivalent is a classical solution. In particular, our results cover when is a one-dimensional affine diffusion and when returns, variances and default intensities are also affine. Numerical examples highlight the relationship between the factor process and both the indifference price and default insurance. Lastly, we show the insurance protection price is not the default intensity under the dual optimal measure.

Introduction

The goal of this paper is to solve the optimal investment problem when the underlying asset may default, causing a jump to zero in its price. Our primary applications are the explicit pricing of defaultable bonds and dynamic default insurance protection; taking into account investor preferences, market incompleteness, and crucially, the ability of the investor to trade in the underlying prior to default.

The issue of default, or more generally, contagion risk, is of primary importance for risk managers during times of financial crisis. However, the precise relationship between optimal policies, defaultable bond prices, default insurance, and the factors which drive the larger economy is not well known if the investor may trade in the underlying asset. The current practice of "risk-neutral" pricing for defaultable bonds, while suffering from the well-known risk neutral measure selection issue, also suffers from a more significant problem in that it is implicity assumed there is separation between the defaulting entity and the traded assets. In practice, this is not always the case, and the hedging arguments which form the basis for risk neutral pricing are called into question.

To address the above issues, we consider the utility maximization problem for an investor with constant absolute risk aversion, who may invest in a defaultable asset, and who additionally owns a non-traded claim with payoff contingent upon the survival of the asset. As the default time is not predictable for the investor, the market is incomplete. We assume the "hybrid" model structure of [22, 30], where asset dynamics and default intensities are driven by an underlying time homogenous diffusion, representing a set of economic factors. Here, the certainty equivalent is identified with a degenerate elliptic semi-linear partial differential equation (PDE). Using powerful PDE existence results from [19, 9], in conjunction with well-known duality results for exponential utility (see, for example, [16, 4, 25]), we show the certainty equivalent is a classical solution to the PDE under minimal assumptions on the model coefficients. In particular, our results can handle when the factor process takes values in an arbitrary region in , and when the asset return, volatility and default intensity are unbounded functions of the factor process.

The utility maximization problem taking into account default has been widely studied. Through a complete literature review is too lengthy to give here, we wish to highlight where our work fits in regards to prior studies. First and foremost, our work fills a gap in the literature by considering the Markovian setting where one may solve the optimal investment problem using PDE techniques. In the PDE setting it is possible to obtain explicit solutions which highlight the dependency of optimal policies and bond prices upon broader economic factors. Though the Markovian case has been treated in some form dating at least back to [30, 23], to the best of our knowledge the problem has not been studied when one assumes the investor loses her dollar position in the stock upon default. Indeed, in contrast to [30], we do not assume the investor is fully protected against losses due to default.

The non-Markovian case has been much more thoroughly studied. For dynamics governed by Brownian adapted processes, the problem traces to [24, 20, 2] and the subsequent extensions in [15, 14, 21, 12]. In fact, our setting is closest to [20, Sections 2,3] where there is a single risky asset with pre-default dynamics governed by a univariate Brownian motion. Here, under general conditions, the value function is identified as a maximal sub-solution of a backward stochastic differential equation (BSDE), which under certain bounded-ness and/or compactness conditions becomes a true solution. In fact, as shown in the above extensions, the BSDE setting allows for model generalizations such as multiple defaults, or even credit related events, where "default" refers to any event which causes a jump in the asset’s value. However, explicit computations for optimal policies and/or prices are often absent (see [15, Section 4.3] for a notable exception). Thus, while on the one hand, by working in a diffusive environment for a single stock, our assumptions are more restrictive than what can be handled using BSDEs, on the other hand, by relying upon PDE techniques we are able to significantly relax the integrability assumptions made upon the model coefficients and provide explicit solutions. This enables our results to apply to a wide range of models used in industry: in particular our results cover the extended affine models of [3, 5, 7] (see Section 2).

Briefly, we now explain our model, assumptions, and main results. There is a diffusion satisfying , which represent the underlying economic factors. We allow to take values in a general region , and only require the diffusion matrix to be locally elliptic on . The riskless asset is normalized to , and a there is a single risky asset which, prior to default, has instantaneous return , variance , and correlation dependent upon . Thus, even absent default, the market is incomplete if ***Throughout, ”’” denotes transposition.. Given the factor process , the default time has an intensity driven by . The investor may trade in up to , but at she will lose her position in the stock, and may no longer trade. In addition to trading in , the investor owns a non-traded claim , which is received contingent upon the survival of the stock. The investor has constant absolute risk aversion and seeks to maximize her terminal wealth over the horizon . Assuming we write for the value function and the certainty equivalent.

In this setting, the HJB equation for is the semi-linear, degenerate elliptic PDE given in (1.17) below. Since we are working on unbounded domains with local ellipticity and unbounded coefficients, the task of solving the PDE is challenging. However, it is possible to obtain a solution under a mild exponential integrability assumption on the market price of risk . In particular, if the market absent default is "strictly incomplete" in that , we require (see Assumption 1.8) only that for some , the function is locally bounded on . This assumption is satisfied by virtually all models used in the literature. When is not bounded away from , we require locally uniform exponential integrability of under two additional probability measures: see Assumption 1.8, but, despite the seemingly complicated formulation, it still holds in many models used in industry.

Theorem 1.11 shows the certainty equivalent is a classical solution to the HJB equation (1.17). As an immediate consequence, we are able to identify the (buyer’s, per unit) indifference price for owning units notional of a defaultable bond: see Proposition 3.1. Furthermore, this indifference price is regular both in time and the factor process starting point.

The main application we consider is determining a fair price for dynamic insurance against default. Here, our work is motivated by [30], where a similar problem was considered but it was implicitly assumed the investor is protected from losses due to default. In other words, if the investor holds in the stock, then upon default, she does not lose her . It is natural to wonder how this is possible, and we take the perspective that she has entered into a contract protecting her from losses, and seek to determine how much this contract should cost. Of course, in reality, it may not be possible to enter into a contract which dynamically protects against default, but such a contract may be thought of a continuous time limit of opening and closing short term static contracts. To compute the contract price we assume the investor has two alternatives: she either does or does not purchase the protection. If she does purchase the protection, she pays a continuous cash flow rate of for a given dollar amount in the stock. Given , her optimal indirect utility is given by in the protected case, and in the unprotected case; where was determined in [30]. We thus seek so that , and in fact, is very easy to identify by equating the PDEs for the respectively certainty equivalents. We make this identification in Section 4, and show in Proposition 4.1 that never exceeds the default intensity under the dual optimal measure for the unprotected problem, but does exceed the default intensity under the physical measure.

The rest of the paper is organized as follows: we present the model in Section 1.1 and main results concerning the certainty equivalent in Section 1.3. Section 2 provides two examples highlighting the minimality of our assumptions. Section 3 gives the indifference price for units notional of a defaultable bond, and Section 4 computes the dynamics default insurance price. A numerical application in Section 5 when is a CIR process concludes: here we explicitly compute the time 0 indifference price as a function of both the notional and factor process, as well as the default insurance cost as a function of the factor process. Section 6 contains the lengthy proof of Theorem 1.11 and Appendix A contains a number of supporting lemmas. Lastly, we remark that the proof of Theorem 1.11 is lengthy since at the present level of generality, we are not able to automatically verify solutions to the PDE in (1.17) are the certainty equivalent , as it is difficult to estimate the gradient of solutions near the boundary of the state space. As such, we must first localize both the PDE and optimal investment problem. At the local level we are able to show existence and uniqueness of solutions. We then unwind the localization by enforcing the exponential integrability conditions in Assumptions 1.8, 1.9.

1. The Setup

1.1. The probability space and factor process

Consider a probability space rich enough to support a dimensional Brownian motion, written , where is -dimensional and one-dimensional; and a random variable independent of . We denote by (respectively ) the augmentation of the filtration generated by (resp ). Throughout, is a fixed constant.

There is a time homogenous diffusion factor process driven by , which takes values in a region satisfying:

Assumption 1.1.

is open and connected. Furthermore, there exists a sequence of sub-regions such that each is open, connected, and bounded with boundary . Lastly, and .

To construct we first assume:

Assumption 1.2.

and , where is the space of dimensional symmetric positive definite matrices. Furthermore, there is a (necessarily unique: see [31, Chapter 6]) solution to the martingale problem on for the operator

| (1.1) |

Here, with , and with .

Remark 1.3.

Denote by the unique symmetric positive definite square root of . In light of Assumption 1.2, for each and there is a unique strong solution to the SDE (see [28, Chapter IX])

For expectations with respect to we will write, for example, or if the starting point is clear. Alternatively, for expectations with respect to (which acts on the canonical space ) we will write .

Next, there is an intensity process for the asset default time. We assume

Assumption 1.4.

. As such, for each , .

1.2. The underlying asset and optimal investment problem

We assume a constant interest rate of . The risky asset may default, but prior to default has instantaneous return , variance , and correlation with the Brownian motion . are functions the factor process and satisfy

Assumption 1.5.

, and with . In particular, for each , .

We now identify the dynamics of . Throughout, is a fixed time horizon, is the fixed starting time, and is the fixed factor starting point. To alleviate notation, in this section we write rather that as the factor process, and in general, suppress .

The default time for is given by

| (1.2) |

As such, for : , so that is the intensity for given , and has conditional density . In particular, is atom-less. Next, we define the default indicator process

| (1.3) |

as well as the enlarged filtration as the augmentation of the filtration generated by the sigma-algebras

| (1.4) |

Lastly, we set

| (1.5) |

and note that is a local martingale. With the notation in place, we assume and

| (1.6) |

Thus, evolves as a geometric Brownian motion driven by until at which point it jumps to and stays there. Note that the given regularity assumptions, is well defined.

To describe the optimal investment problem, we first define the class of equivalent local martingale measures with finite relative entropy. Set

| (1.7) |

Write as the density of with respect to for . The relative entropy of with respect to on is given by

| (1.8) |

and we define

| (1.9) |

For now we assume but later on we will enforce this assumption via a requirement on the model coefficients (c.f. Assumptions 1.8, 1.9 below).

Next, let be a predictable process such that the stochastic integral is well defined. represents the dollar amount invested in at time . Denote by the resultant (self-financing) wealth process with initial value at . For , has dynamics

| (1.10) |

Note that upon default at the investor losses her dollar position , and after this point, there is no change in wealth. We then say is admissible, and write , if is a super-martingale for all .

In addition to trading in the stock, the investor owns a non-traded claim which is received at the horizon , contingent upon the survival of the stock. We consider claims of the form , so that the payoff may depend on the factor process. However, our interest primarily lies when either (no claim) or (defaultable bond). We make the common assumption that is bounded, along with a certain regularity requirement:

Assumption 1.6.

is bounded with

| (1.11) |

The investor’s preferences are described by the exponential utility function

| (1.12) |

where is the absolute risk aversion. The investor trades in in order to maximize her expected utility of terminal wealth, including her position in the contingent claim. Thus, for a given wealth we define (recall: the investment window starts at and the factor process starts at ):

| (1.13) |

It is clear for exponential utility that . As such, until Section 3 we consider . Lastly, we write as the certainty equivalent, defined by

| (1.14) |

1.3. Main result

Before presenting the main result, we must introduce one last piece of notation. For define as the unique solution to

| (1.15) |

is known as the "Product-Log" (Mathematica) or "Lambert-W" (Matlab) function. Further properties of are given in Lemma A.1 below. With this notation, for a smooth function on , define

| (1.16) |

A heuristic derivation using the dynamic programming principal indicates from (1.14) should solve the semi-linear, degenerate elliptic partial differential equation (PDE) or Hamilton-Jacoby-Bellman (HJB) equation (here, we suppress the function arguments and recall from (1.1))

| (1.17) |

The dynamic programming principal also suggests that if solves the above PDE then for any starting point the optimal trading strategy is

| (1.18) |

Remark 1.7.

We do not derive the HJB equation as it is standard. Furthermore, we will use direct methods to a) yield a solution to (1.17) and b) verify that it is the certainty equivalent, and the optimal policy. As such, we do not require the dynamic programming principal to hold.

We must enforce one more restriction to solve the optimal investment problem. Here, we split into cases depending on the correlation . The first is when the market absent default is "strictly incomplete" in that is bounded below , while the second places no restrictions on . We make this split because in the former case, the main result goes through under a very mild, and simple to state, condition upon the market price of risk . In the latter case, the condition we must assume is more complicated to formulate, but none-the-less holds in many models of interest: see Section 2.

First we consider when is bounded below , and recall the notation of Remark 1.3:

Assumption 1.8.

and there exists an so that for each

Next, we consider when is not bounded below :

Assumption 1.9.

There are no restrictions on . However,

-

(A)

There is a solution to the martingale problem on for the operator

With denoting the resultant solution, there is some so that for each :

-

(B)

For some there is a solution the martingale problem on for the operator

With denoting the resultant solution, we have for each that

Remark 1.10.

Note that each condition in Assumption 1.8 allows for unbounded . To gain intuition for why we split into two cases, note that if then one may obtain a measure via the density process

Since is independent of , we see that when Assumption 1.8 holds: in fact, this assumption is much stronger than what is actually needed, but is used in the delicate unwinding procedure of Proposition 6.10 below. However, when we are no longer able to "put" the market price of risk to the independent Brownian motion : here we instead consider the density process

Since is not independent of we must enforce the integrability requirements of Assumption 1.9 to obtain our results. But, as is shown in Section 2, Assumption 1.8, while seemingly complicated, is very easy to check, and holds under mild parameter restrictions for many common models.

With all the assumptions in place, we state the main result. For a definition of the parabolic Hölder space see Section 6.1 below, but for now we remark that .

Theorem 1.11.

Let Assumptions 1.1, 1.2, 1.4, 1.5, 1.6 and either 1.8 or 1.9 hold. Then, the certainty equivalent from (1.14) is in and solves the PDE in (1.17). Furthermore, for each , the optimal trading strategy is from (1.18) and the process defined by

| (1.19) |

is the density process of a measure which solves the dual problem given in (6.31) below.

2. Examples

2.1. OU factor process with constant default intensity

Consider when has dynamics (), taking values in , for which we set . The correlation is constant. For the asset dynamics we take and . The default intensity is . Clearly, Assumptions 1.1, 1.2, 1.4 and 1.5 hold. The claim is either or so that Assumption 1.6 holds as well. As for the more complicated Assumptions 1.8, 1.9 we note that

-

(1)

- (2)

-

(3)

for .

-

(4)

For small enough and , for , since is normally distributed with mean and variance continuous in .

Therefore, it is easy to see that both Assumptions 1.8, 1.9, hold with no additional parameter restrictions.

2.2. CIR factor process with affine default intensity

Consider when has dynamics . We assume so that (), , . The correlation is again constant. For the asset dynamics we take and . Lastly, we assume . Thus, the model falls into the "extended affine" class: see [3, 5, 7] amongst others. As with the OU case, Assumptions 1.1, 1.2, 1.4 and 1.5 clearly hold. As for Assumptions 1.8, 1.9 we have the following:

Lemma 2.1.

Proof of Lemma 2.1.

We first claim that if is a general CIR process with dynamics , then provided and we have for and that

where , , and . Indeed, note that and set , as the second order operator associated to . Then and by Itô’s formula we see that

where , and where the last inequality holds since imply , and since is a super-martingale. Next, note that , and that under each of the operators in Assumption 1.8, 1.9 is still a CIR process. The parameter restrictions imply does not explode under each of the operators (for small enough), and a straight-forward calculation yields Assumptions 1.8, 1.9. ∎

3. Indifference Pricing

As an immediate application of Theorem 1.11, we can obtain the indifference price for a defaultable bond, taking into account the investor’s ability to trade in the defaultable asset. Here, we assume the buyer holds notional of the defaultable bond, and seek to identify the (per unit notional) indifference price. Formally, we fix and define the (buyer’s average) indifference via the balance equation

| (3.1) |

Above, we have used (1.13) and written for and for . Qualitatively, (3.1) states that at the price the buyer of the claim is indifferent between not owning the claim and paying to purchase units of the claim. For exponential utility it is well known the initial wealth does not affect the indifference price so we write where

| (3.2) |

4. The Pricing of Dynamic Default Insurance

We now consider the problem of finding a fair price for dynamic insurance against default, which takes into account market incompleteness as well as investor preferences. The results of this section are meant to complement those in [30], where a similar optimal investment problem is considered, with the difference being that upon default of , it is implicitly assumed the investor is protected ‡‡‡Indeed, in [30, Section 2.1] the author’s state ”For simplicity, we assume she (the investor) receives full pre-default market value on her stock holdings on liquidation, though one might extend to consider some loss, or jump downwards in the stock price at default time.”. Specifically, if the investor owns a dollar amount at , she does not lose this dollar amount. Rather, the default only indicates that further trading is not possible.

Presently, we describe the method for obtaining a fair price of dynamic default insurance. In the model of Section 1.2 with no defaultable bond, we assume the investor has two potential strategies:

- (1)

-

(2)

The investor again chooses a strategy in the stock. However, she enters into a contract which offers dynamic protection against default. Prior to default, this contract costs a continuous payment rate of where is the (to-be-determined) per-dollar cost of the protection. At default, the investor does not lose her dollar-position , but is no longer able to trade in the underlying asset. In this scenario, for a given strategy , the wealth process evolves according to (see (1.10) for comparison)

(4.1) Here, is admissible if is predictable, such that the relevant integrals are well defined, and such that is a super-martingale for all , the class of equivalent local martingale measures with finite relative entropy in this market. She then seeks to solve the optimal investment problem

(4.2) and we denote by the certainty equivalent.

The goal is to find so that the investor is indifferent between the two alternatives; i.e. for all starting points . In light of Theorem 1.11, we can immediately identify by equating the PDEs for . Indeed, following the arguments in [30, Proposition 2.1], under the a-priori assumption that is functionally determined, the HJB equation for on is

| (4.3) |

The corresponding optimal trading strategy for is

| (4.4) |

Now, consider when Theorem 1.11 holds, so that solves (1.17) with . Upon comparison with (4.3) we see that will also solve (4.3) provided

This has two (real) solutions

as part of Lemma A.1 below at and shows the term within the square root is non-negative. Since the investor is paying for the default insurance, we take the perspective that she seeks the lowest possible cost and hence set the price of default insurance as

For defined above, we have the following proposition:

Proposition 4.1.

Let Assumptions 1.1, 1.2, 1.5, 1.4 and either of (1.8), 1.9 hold. Let from (1.14) be the certainty equivalent to (1.13) which solves the PDE in (1.17). Define as in (4) and consider the optimal trading strategy function from (1.18). Then we have the following facts regarding :

-

(1)

, the default intensity function of under from Theorem 1.11. Here, equality is achieved if and only if .

-

(2)

has the same sign (including ) as . In particular, when .

Proof of Proposition 4.1.

With and we see that . Now, (1.18) implies , and writing , we have by definition of that . Thus, and . Plugging in for in (4) gives

| (4.6) |

Straightforward analysis shows for that and so and follows since is the default intensity of under as can be seen from Lemma 6.3 and (6.40) below. As for , analysis shows there is a unique so that . For , and for , . Thus, has the same sign as . Simple calculation shows both and that has the same sign as . Plugging in and gives .

∎

4.0.1. Discussion

To interpret Proposition 4.1, consider when . Here, the investor will lose money upon default, and hence has motivation to pay for default insurance so that . Interestingly however, there is a threshold , where as long as the profit from immediate default does not outweigh the value of default protection if future positions rise: thus the investor is willing to pay for insurance. Below the level the profit from default is so significant that the investor will need to be compensated for giving this up and hence .

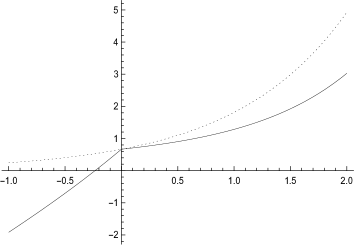

A full calculation of requires knowledge of , and can be difficult to calculate, especially when is multi-dimensional. However, for we can use (4.6) to provide a simple relationship between and . Indeed, since , if we substitute into (4.6) we see for that

| (4.7) |

Consider the models of Sections 2.1, 2.2, where in the latter model we enforce the affine condition by setting . In each case, is constant, and we can view solely as a function of . Figure 1 shows the relationship between and in this setting, along with the theoretical upper bound from of Proposition 4.1.

5. A Numerical Application

Consider the CIR model of Section 2.2 but restricted to the affine, rather than extended affine, case. In particular we assume . We also assume so that Theorem 1.11 holds under the assumption . The goal is to compute the indifference price of (3.2) for units notional of a defaultable bond, as well as per unit fair price of dynamic default insurance given in (4). To obtain these values, we solve the PDE (1.17) for and using the semi-linear PDE solver "pdepe" from Matlab, which can solve such PDEs in one spatial dimension¶¶¶Our code is available upon request by contacting the second author at ”scottrob@bu.edu”.. For and we use the same parameter values as in [11, Section 6]. For the instantaneous return and variance we assume at the long run mean of a variance of and mean of . For the default intensity we assume at the long run mean of we have a probability of default within one year is , which corresponds to . Lastly, we use a risk aversion of . This yields

| (5.1) |

The conditions of Lemma 2.1 are satisfied so Theorem 1.11, as well as Propositions 3.1, 4.1 go through. At time , Figure 2 shows the dynamic default insurance price and the indifference price as a function of the underlying state variable . For the dynamic insurance price we have also plotted the upper bound from Proposition 4.1 and the default intensity under , which in this case is also the intensity under the minimal martingale measure: see [8, 29]. Here, we see that the insurance price is increasing with the state variable, as intuition would dictate since the physical measure default intensity is linear in .

For the indifference prices, we have plotted the price as a function of the notional size and state variable for . As expected the price decreases in and increases in (recall: this is the price at which we would buy the defaultable bond).

6. Proof of Theorem 1.11

The proof of Theorem 1.11 is lengthy due to the facts that we are working in general domains, not assuming uniform ellipticity of the factor process, and not restricting the model coefficients to be bounded. The outline for proving Theorem 1.11 consists of the following steps:

-

(1)

Identify a local version of the PDE in (1.17), where we are able to use the theory of semi-linear elliptic equations with quadratic growth in both the solution and its gradient, to prove existence of solutions with bounded gradient.

-

(2)

Associate to the local PDE a local optimal investment problem, and show that any solution to the local PDE is the certainty equivalent of the local optimal investment problem, and hence solutions are unique.

-

(3)

Show that solutions to the local PDE are locally uniformly bounded, and hence there exists a solution to the full PDE.

-

(4)

Show that this solution to the full PDE is the certainty equivalent to the full optimal investment problem, and identify the optimal trading strategy and equivalent local martingale measure.

Throughout this section, as the function is fixed we write for the PDE in (1.17). Also, Assumptions 1.1, 1.2, 1.4, 1.5 and 1.6 are in force. As for Assumptions 1.8, 1.9, they are only required for Propositions 6.10, 6.11 below and their use will be made explicit.

6.1. Mollifiers and function spaces

We first introduce mollifiers in order to define the local PDE. To this end, we claim that without loss of generality we can re-index the sub-domains of Assumption 1.1 so that for each there exists a function such that

| (6.1) |

Indeed, set . Then set and . Lastly, set where is the standard mollifier (see [6, Appendix C]). Then with . Also, we have on , is supported in and on . So, (6.1) is satisfied on which also satisfies Assumption 1.1. Thus, we can relabel .

Next, we introduce the function spaces where our PDE solutions will lie. We use the notation of [19, Chapters 1.3,4.1]. Namely, let denote a region in and write for a typical point in . The parabolic distance between is given by , and for a given function on and we define

| (6.2) |

Next, for a given non-negative integer , define the norm via

| (6.3) |

Here is a multi-index with norm . is the derivative with respect to determined by and is the derivative with respect to . The parabolic Hölder space is the Banach space of all functions on with . When takes the special form , the space is the set of functions which are in for all bounded regions with . We pay special attention to when so that

| (6.4) |

and where .

6.2. The local PDE and optimal investment problem

With the mollifiers in place, consider a localized version of (1.17) on :

| (6.5) |

To conform to the notation in [19] we reverse time, defining , , and as the parabolic boundary of . Additionally, we write the PDE for as

| (6.6) |

In the above we have defined for .∥∥∥Comparing with [19, Equation (12.2)] we have and . Also, for we have set (recall from (1.15)):

| (6.7) |

With this notation, the following is an almost immediate consequence of [19, Theorem 12.16].

Proof of Proposition 6.1.

The result will follow from [19, Theorem 12.16] once the requisite hypothesis are met. To this end, the fact that is implies that . Furthermore, that and implies . Next, Lemma A.2 below implies [19, Equation (12.26)] and the local ellipticity of yields [19, Equation (12.25a)]. implies (i.e. is Lipschitz) for all bounded subsets of . The coefficient regularity also implies is in for all bounded subsets of .

Regarding [19, Equation (12.27)], first note [19, Equation (12.26)], which follows from Lemma A.2, implies an a-priori maximum principal for solutions to the PDE in (6.6). Indeed, using Lemma A.2 in conjunction with [19, Theorem 9.5] applied to both it follows that any solution to (6.6) satisfies the bound . Thus, any solution lies in a compact interval of . In view of this, Lemma A.3 below shows that is on the order of . It is also clear that and that is independent of and hence on the order of . Therefore the resultant hypotheses of [19, Theorem 12.16] are met and there exists a solution to the PDE in (6.6). Now, [19, Theorem 12.16] yields a solution which is defined in [19, Chapter 4]. However, since in (6.6) it follows that (the boundary term) satisfies the compatibility condition of the first order:

since vanishes on . Thus, as remarked at the end of [19, Theorem 12.16] (c.f. [19, Theorems 5.14,8.2]), it follows that . This gives the result.

∎

Remark 6.2.

We record that implies for some constant . This will be used in the proof of Proposition 6.5 below.

We next show is the certainty equivalent for a localized version of the optimal investment problem in Section 1.2. Indeed, fix and consider large enough so that . The factor process is the same as in Remark 1.3. Next, define a localized default time via

| (6.8) |

and the localized default indicator process and its compensator via and for . Set in a similar manner to (1.4) and note that is a martingale (c.f. [27, Theorems 1.51, 4.48]. The asset price process defined by and for :

| (6.9) |

Having localized the default intensity and asset dynamics, we next localize the optimal investment problem to stop when exits . To this end define

| (6.10) |

Set as the class of equivalent local martingale measures on (these are the measures so that stopped at is a local martingale on ) and let denote the subset with finite relative entropy with respect to on . Denote by the class of predictable trading strategies so that is integrable on and such that the resultant wealth process is a super-martingale for all . Here, has dynamics for :

| (6.11) |

For the starting point , the localized optimal investment problem is

| (6.12) |

Before identifying the certainty equivalent with from Proposition 6.1, we present two supplementary results concerning the structure of the local martingale measures in this setting. The first result is given in [1, Proposition 5.3.1]:

Lemma 6.3.

For any measure on there is the representation

where and are predictable processes. Additionally, is a Brownian motion stopped at where , , and is a martingale stopped at .

The second lemma characterizes when a measure on is in :

Lemma 6.4.

Let on , and let be as in Lemma 6.3. Then if and only if for almost all :

| (6.13) |

Proof of Lemma 6.4.

A heuristic use of the dynamic programming principle shows that the PDE for the certainty equivalent to is the same as in (6.5). The following proposition shows that indeed, from Proposition 6.1 is the certainty equivalent.

Proposition 6.5.

Proof of Proposition 6.5.

Write and note that below, is a constant which may change from line to line. Since solves (6.5) at we have

so satisfy the first order conditions for optimality. From the well known utility maximization results for exponential utility (see [4, 16, 10, 13]) the result will follow provided

-

(1)

is a super-martingale for all .

-

(2)

for some .

-

(3)

is a martingale.

Parts and follow immediately from Lemmas 6.3, 6.4 and Remark 6.2. Indeed, using (6.14) we have

Thus,

Since on (see Remark 6.2) and are bounded on it follows that almost surely , and hence is a martingale (c.f. [27, Theorems 1.51,4.48]). This gives and as well, provided we can show . To this end, a lengthy but straight-forward calculation using Itô’s formula in Lemma A.7 below shows has dynamics:

| (6.17) |

Remark 6.2 and (6.15) show that almost surely . Also, note that are predictable, and there is some so that . Therefore, by [26, Theorem 9] it follows that is a strictly positive martingale******Note that is a martingale since it has bounded quadratic variation: see [27, Theorems 1.51 and 4.48]. Clearly, the Brownian stochastic integrals are martingales.. It remains to show that defined by is in . First, that follows immediately from (A.8) in Lemma A.7 below in conjunction with Lemma 6.4. For the relative entropy, note that by definition of in (6.16), and (6.5) we obtain

Since , is bounded, is a martingale, and is deterministic, the fact that is a martingale implies the desired result. Thus, so that .

∎

6.3. Unwinding the localization: analytic results

We now provide two analytic results for unwinding the localization. The first uses the maximum principal to obtain a uniform lower bound for solutions to (6.5). The second proves existence of solutions to (1.17) provided locally uniform upper bounds for .

Proposition 6.6.

Proof of Proposition 6.6.

First, assume has a minimum in at . If then . If then . Also, . By the ellipticity of in , (6.5) implies at :

Above the second inequality uses Lemma A.1 below at and . Since and in we see which implies . But, we already know and . Thus, the result follows.

∎

The next proposition is significantly more involved. Though it can be deduced from [18, Theorem V.8.1], for transparency we offer a detailed proof using the results in [19, 9].

Proposition 6.7.

Proof of Proposition 6.7.

Step 1:

Use [19, Theorem 11.3(b)] and (6.19) to conclude that

| (6.20) |

To show this, we recall that where solves the PDE in (6.6) with therein defined in (6.7). Next, we define the Bernstein function (c.f. [19, Equation (8.3)]):

| (6.21) |

Note that by assumption we have that for and some . Next, we define the differential operators from [19, Chapter 11] which act on functions via

| (6.22) |

For the domain the quantities from [19, Equation (11.7)] become†††††† of [19, Equation (11.7)] is equal to : see right after [19, Equation (11.2)].

| (6.23) |

From Lemma A.5 below we see that the quantities of (A.3) are finite with and . Lastly, as noted right after [19, Equation (11.4)] we take , and use these values to verify [19, Equations (11.17abc)]. After all these preparations, we are ready to invoke [19, Theroem 11.3(b)]. First of all, note that [19, Equations (11.17ac)] hold. As for [19, Equation (11.17b)], take therein, and note that there is a constant so that in (this is the of [19, Equation (11.17b)]). Next, define

| (6.24) |

From Lemma A.5 below we see the quantity of (A.7) is finite and hence [19, Equation (11.17b)] holds for all with and sufficiently small. In fact, let and set . For such we have [19, Equation (11.17b)] and as such, for we deduce from [19, Theorem 11.3(b)] that

Here, depends on and on . However, as defined in [19, Chapter 2.1], so that , since for we have on . Lastly, the quantity is defined in [19, Section 4.1] but is bounded above in our case by

where the last equality comes from (6.18) and Proposition 6.6. Putting all this together and using the uniform continuity of on we obtain . If we re-index this by moving to we obtain (6.20).

Step 2:

Use (6.20) and [9, Theorem 4, Ch 7, Section 2] to show

| (6.25) |

where is defined in (6.2). Indeed, fix and . Now, instead of applying [9, Theorem 4, Ch 7, Section 2] directly to we will apply it to a truncated version of given by

| (6.26) |

Note that and that on . Using the PDE for in (6.6) it follows that solves the PDE

| (6.27) |

where

| (6.28) |

Note that vanishes at , and moreover, since

-

(1)

by construction.

- (2)

-

(3)

by (6.20).

-

(4)

hence by assumption,

we know that

| (6.29) |

Thus, by [9, Theorem 4, Ch 7, Section 2] we obtain . Now, since in the triangle inequality implies

This held for . Replacing with we see that for we have

which is what we wanted to show.

Step 3

: Use (6.25) and [19, Theorem (5.14)] to show

| (6.30) |

Let . We retain the notation from the previous step. Since satisfies the linear parabolic PDE in (6.27) in with boundary condition on , it follows by the well-known existence results on linear parabolic PDE (see, for example, [19, Theorem 5.14]) that

By (6.29) we already know that . However, from (6.28), (6.25) and the regularity of the model coefficients and it is easily seen that . This yields that . Since in we see that

Thus, replacing with it follows from that , which is precisely (6.30).

Step 4:

Use (6.30) to obtain the solution to (1.17). This proof is standard and follows a diagonal sub-sequence argument. Indeed, fix an integer . By (6.30) applied to we may extract a sub-sequence which converges in to a function . Clearly, solves (1.17) in with on . Then for we may take a further subsequence which converges in to a function satisfying the PDE in . By construction in and hence setting as this common function, is well defined in . Repeating this process for we obtain a function which solves the full PDE in with correct boundary condition. It is clear that for each and hence . This finished the proof.

∎

6.4. Unwinding the localization: probabilistic results

We now provide probabilistic results complementary to the analytic ones in Section 6.3. The first lemma is similar in spirit to Lemmas 6.3, 6.4, but contains an additional statement concerning the dual problem to (1.13). The dual problem is (recall we are starting at and the factor process satisfies ):

| (6.31) |

Lemma 6.8.

Proof of Lemma 6.8.

The same arguments as in Lemmas 6.3, 6.4 show that if then for :

where are predictable and where for almost every

We first claim that for , cannot be optimal for the dual problem unless are all stopped at . Indeed, implies that as above is a martingale and . Thus, is a sub-martingale. As such, since is in we have by the sub-martingale property and optional sampling theorem that

Thus, any optimizer must lie in the class where , which implies that almost surely . Hence, by uniqueness of the optimizer it must hold that the associated are of the form

| (6.34) |

Now, so far, need only be predictable. But, as shown in [1, Chapter 5], due to the specific structure of we have that coincide with predictable process on the interval . It therefore follows that almost surely

Define the predictable process

For any we have . But, for each we know , since has a density conditional on . As has Lebesgue measure we see that for all . A similar argument shows and hence almost surely

| (6.35) |

Now with as above assume there is an open interval , a set , and a constant so that on and . We then have

Clearly, . Additionally, , where the last inequality follows since and is continuous. This contradicts (6.35). A similar argument for shows that almost surely that , finishing the result. ∎

We next present a probabilistic counterpart to Proposition 6.7, which yields a candidate dual optimizer as well as an upper bound for the certainty equivalent.

Proposition 6.9.

Let be the unique solution to (6.5) from Propositions 6.1 and 6.5. As in Proposition 6.7, assume for each that

| (6.36) |

Let denote the solution to (1.17) from Proposition 6.7 and recall the subsequence (still labeled ) such that converges to in . Fix , and for this , define as in (1.18) and as in (1.19). Then

-

(1)

is the density process of a measure .

-

(2)

is a sub-martingale.

-

(3)

For as in (1.13)

(6.37)

Proof of Proposition 6.9.

Take large enough so that . From Proposition 6.5, is the certainty equivalent to (6.12). Additionally, the process from Proposition 6.5 defines a measure which solves the dual problem (similar to (6.31)). Thus,

| (6.38) |

where the last equality follows from (6.36). This shows that is uniformly integrable. Next, with we know almost surely that . determines the wealth process with dynamics

Recall the optimal wealth process from Proposition 6.5 with dynamics

For write

Note that

The last inequality follows from Lemma A.4 below which shows . Thus, by Lemma A.4 and Assumption 1.2 we have almost surely that . From here, the facts that is continuous, the model coefficients are continuous functions, and in imply that almost surely

This shows that the integrals with respect to , and in converge in probability to the respective integrals in uniformly on (see [17, Proposition 3.2.26]). Lastly, set

Lemma A.4 implies almost surely, and clearly almost surely as well. Thus, we have almost surely . But, as shown in the proof of Lemma 6.8, so that almost surely for each . Putting the above facts together gives in Probability. Next, as in (1.19) define

| (6.39) |

In light of the proceeding we have by construction of :

where the limit is in Probability. Again, since , we see in Probability. We have already shown that and is uniformly integrable. This shows that . Furthermore, a lengthly calculation using Itô’s formula, exactly mirroring that in Lemma A.7 below‡‡‡‡‡‡Indeed, the result may be recovered formally by setting therein., shows has dynamics

| (6.40) |

Also, as can be deduced from the calculations leading to (A.8) in Lemma A.7, the facts that solves the PDE in (1.17) and is as in (1.18) prove that almost surely

so that defined by is in . Fatou’s Lemma and in Probability imply

The last inequality follows from (6.38). This shows that and gives statement . Continuing, from (6.39) it follows that

| (6.41) |

where the inequality follows via Proposition 6.6 and . Since we see that is a local martingale bounded from below, hence super-martingale. Thus, since is a martingale we see that is a sub-martingale. This gives statement . The sub-martginality implies . Therefore, using the well-known duality results we obtain from (1.13), (6.41) that

| (6.42) |

Thus, (6.37) holds, finishing the result.

∎

With the above results we are ready to finish the proof of Theorem 1.11. Here we split the results according to whether Assumption 1.8 or Assumption 1.9 hold. To make the notation shorter, set

| (6.43) |

and note that Assumptions 1.8, 1.9 essentially concern the exponential integrability of .

Proof of Proposition 6.10.

Recall that we have fixed a starting point for the optimal investment problems of Sections 1.2 and 6.2. Furthermore, according to Proposition 6.5 for each there is a unique function solving (6.5), which is the certainty equivalent to (6.12). Thus, by the standard duality results

| (6.44) |

Now, define

| (6.45) |

If is the density process of a measure then, in the notation of Lemma 6.4, we have , and for . Since is predictable, it is also predictable, and a direct calculation shows that (6.13) is satisfied. Also

where the last equality follows by conditioning on and noting that is predictable and is independent of . Thus, is a martingale, and we see from Lemmas 6.3 and 6.4 that . In fact, using the independence of and we obtain:

Above, the inequality used that and . Now, recall that . Using the Markov property and the solution to the martingale problem for on from Assumption 1.2 we have

where the last inequality used for . Thus, from (6.44) and Assumption 1.8 we conclude that for each , , and we have

As such, the conclusions of Propositions 6.7, 6.9 hold. As in the latter proposition we denote by the optimal strategy from (1.18), the wealth process and the density process from (1.19). We now turn to proof the opposite inequality in (6.37). To this end, we use Lemma 6.8. Namely, let be of the form in Lemma 6.8 (from which any optimizer must lie) where are predictable process satisfying (6.33). Denote by the resultant density process. Create the predictable processes on via

A straight-forward calculation shows the market price of risk equation in (6.13) is satisfied. Then, create the local martingale by

We now show that is a martingale. First, Lemma A.8 below proves the technical facts which essentially hold because on :

| (6.46) |

Next, to simplify notation, define

| (6.47) |

and note that , . Also note that we have defined in terms of but the second equality above comes from Lemma A.8. With this notation, (6.46) and (6.45), we have using iterative conditioning on , and the independence of and :

The last equality follows since by hypothesis is a martingale (as a density process for ) and the optional sampling theorem. Thus, is the density of a martingale measure . As for the relative entropy:

| (6.48) |

As is a martingale, and , the first term is bounded from above by . For the second term, we use inequality for . This gives

| (6.49) |

From (6.43) and Assumption 1.8, we obtain for that

So, using Assumption 1.8 we see that for

| (6.50) |

This shows that and hence from Proposition 6.5 and (6.44)

| (6.51) |

Continuing, from (6.46) we see . Since it is clear that almost surely. Furthermore, (6.50) implies is uniformly integrable. Thus, by the dominated convergence theorem:

where the last equality holds since . As for , come back to (6.48):

Fatou’s lemma and the sub-martingale property of imply . As for the second term, since we have almost surely that . Furthermore, as shown in (6.49) for , this term is bounded from above by

But, this term is uniformly integrable since it converges in probability and in as argued above. Thus is uniformly integrable and hence we see from (6.51) that

Now, this result holds for all for the form in Lemma 6.8, but as argued there-in, the dual problem is obtained by minimizing over this class. Thus,

| (6.52) |

This, combined with (6.37) in Proposition 6.9 proves is the certainty equivalent for the optimal investment problem. Now, at this point we have proved from the above and Proposition 6.9

-

(1)

That is the certainty equivalent.

- (2)

-

(3)

The existence of a trading strategy so that for the resultant wealth process , , so that achieves the optimal utility. Furthermore, since the inequalities in (6.42) are all equalities, .

The last thing to show is that , which will follow if is a super-martingale for all . This is hard to show directly, so at this point we appeal to the well-known duality results for exponential utility with locally bounded semi-martingales. Namely, as there exists an optimal to the primal problem (c.f. [25]), and since solves the dual problem, we already know from the necessary and sufficient conditions for optimality that with probability one:

This shows that almost surely. Next, from part (2) of Proposition 6.9 we know is a sub-martingale. But, along with the sub-martingale property imply that is a martingale. The abstract theory tells us that is also martingale under . This gives, for that almost surely, and hence by right continuity they are indistinguishable on . Lastly, the abstract theory implies is a sub-martingale for all and so the same is true for . Thus, and the proof is complete.

∎

Lastly, we turn to the case of Assumption 1.9.

Proof of Proposition 6.11.

The proof is similar to that of Proposition 6.10 and hence we just show the differences, appealing to former proof to fill in the steps. As such, there are two things to show/do:

- (1)

-

(2)

For and , appropriately adjust in the random interval to create a measure and then show the relative entropy associated to this adjustment vanishes as . This will establish the upper bound (6.52) for , from which the remaining theorem statements follow exactly as in the last paragraphs of the proof of Proposition 6.10.

We first consider . By part of Assumption 1.9, for , there is a unique solution to the SDE , , and hence the process

is an martingale which defines a measure on . Note also that we have since is bounded that

| (6.53) |

The last inequality follows by the Markov property of under , and the estimate for . Next, let be large enough so , recall the definition of in (6.47), and define the predictable processes for via and . It is clear that the market price of risk equations (6.13) are satisfied and that the resultant density process satisfies for . Since , by construction of we know is a martingale, and hence defines a measure by . Furthermore,

Above, the second equality follows from the conditional density of . The first inequality holds since is in and since (6.53) implies is a sub-martingale. The last inequality also follows from (6.53). Thus, , and by (6.44) and part (A) of Assumption 1.9 we conclude that for each , , and

As such, part above holds and we may apply Propositions 6.7, 6.9. As before, we denote by the optimal strategy from (1.18), the wealth process and the density process from (1.19). We now turn to above which will yield (6.52). To this end, let be of the form in Lemma 6.8 where are predictable process satisfying (6.33). Denote by the resultant density process. Create the predictable processes on via , and . Again, the market price of risk equation (6.13) is satisfied. Then, create the process by

To show is a martingale, we use Lemma A.8, iterative conditioning on , that is bounded, and that is a martingale (since ) to deduce

Thus, is the density of a martingale measure . Next, we note that is in fact a martingale as well, since is a martingale, is predictable and for . Thus, we can extend to via . As for the relative entropy, again, using that is bounded and the conditional Bayes’ formula:

| (6.54) |

As before, the first term is bounded above by . As for the second term, we again use for which gives

The first term is again bounded by . For the second term:

where (cf Lemma 6.3). Continuing, we have for the of in Assumption 1.9:

For the right-most term above, we use part (A) of Assumption 1.9 and take . Then for large enough so and we have

As for the other term, we have by part of Assumption 1.9 and the convexity of that for and large enough so that and :

where the last inequality follows from of Assumption 1.9. Putting all this together, we obtain that for :

| (6.55) |

Thus, and by Proposition 6.5 and (6.44)

| (6.56) |

Continuing, again from (6.46) we can write and hence we know almost surely. Furthermore, (6.55) implies is uniformly integrable. Thus,

As for , come back to (6.54):

As before, it suffices to show that the second term above vanishes as . But, for

The first term is uniformly integrable. As for the second term we have for some and the of Assumption 1.9 that

The first term on the right was already shown to be finite. For the second term, we take small enough so that for any we have . This shows that is bounded in for all and hence uniformly integrable. Thus,

is uniformly integrable, and since it converges to almost surely, it vanishes in expectation. We thus have . This gives

Thus, we have shown part . From this point on, the proof is same as in Proposition 6.10, starting with the sentence right above (6.52). ∎

Appendix A Supporting Lemmas

Lemma A.1.

Let be defined as in (1.15). Then

-

(1)

For , .

-

(2)

.

-

(3)

For and

(A.1) For each of the above inequalities, there is equality if and only if .

Proof of Lemma A.1.

is clearly smooth, and follows by direct calculation since . As for , it is clear that as . l’Hospital’s rule then implies

where second to last equality follows from . Lastly, for , set as the left hand side of the first equation in (A.1). Then

The last two equalities follow from . Thus, for a fixed , has a unique minimum when but this can only happen when since by construction . In this case we have which gives the result. As for the second inequality, it is equivalent to showing that . Calculation using (1) shows the partial derivative with respect to of this function is . However, and is strictly increasing in with a only at . Thus, the left-hand side of the second equation in (A.1) is uniquely minimized at for a value of .

∎

Lemma A.2.

For defined in (6.7), there is a constant so that for .

Proof of Lemma A.2.

To alleviate notation, we suppress the function argument, but leave in the function argument. Also, is a constant which may change from line to line. At we have

| (A.2) |

When it follows from Lemma A.1 that

and hence . For it follows by the strict positivity of that

since is supported on and are all bounded on . Thus, we have that .

∎

Lemma A.3.

For the function from (6.7), and any interval

Proof of Lemma A.3.

We again suppress the function argument, but leave in the arguments. Since and are all bounded on we need only consider the term

Since this is bounded above by . By Lemma A.1 this is bounded below by . The result readily follows.

∎

Proof of Lemma A.4.

Fix . Since are continuous and we have , so that and hence exists almost surely. Also, since we have , which gives and hence . But

Thus and hence , which gives the result. ∎

Lemma A.5.

Let be as in (6.23). For any constant we have that

| (A.3) |

Proof of Lemma A.5.

Since does not depend upon we have that . Additionally, we have so that . This shows that which trivially gives the result. As for we first have, since does not depend on that

By the ellipticity and regularity of on , this term is on the order of so that

Next, we must evaluate . By grouping terms according to in (6.7) we obtain

| (A.4) |

This implies that

| (A.5) |

where the last term follows by Lemma A.1 which implies that for any smooth function and constant that . Here, we apply this to and . We therefore have

By the ellipticity of and coefficient regularity assumptions, the first term above is on the order of , uniformly on , as . From the definition of in (6.7) and Lemma A.1 we deduce that uniformly for and hence the second term above is also on the order of , uniformly over . Thus

Lastly, we must consider . We first evaluate

Clearly, this is on the order of so that

| (A.6) |

Next, we must evaluate

From (A.4) and Lemma A.1 we see that , which by Lemma A.1 is on the order of . Next, we have from (A.4) that

The terms on the first two lines above are on the order of . Using (6.7) and Lemma A.1 we obtain

Again, using (6.7) and Lemma A.1 we see this is on the order of . Thus, we see that

is on the order of which implies that is on the order of as well. Thus, we deduce that

is on the order of so that

finishing the proof. ∎

Lemma A.6.

Let be as in (6.24). For any constant we have that

| (A.7) |

Proof of Lemma A.6.

Lemma A.7.

Proof of Lemma A.7.

Write where . Itô’s formula implies

| (A.9) |

where is the continuous part of . From (6.9) and the integration by parts formula:

Collecting terms, this implies

| (A.10) |

and

| (A.11) |

Note that will only jump at if . In this case so that . It thus follows that

| (A.12) |

Collecting the results in (A.10),(A.10), (A.11) and using them in (A.12) gives, in differential notation,

| (A.13) |

where, at

Now, for any we have (suppressing function arguments), using that solves (6.5):

Plugging this into the above gives

Note that factors out of the right hand side above. Grouping by , the remaining terms are

We next plug in for from (6.15). This gives

There are a number of cancellations here. The remaining terms are

where the last equality follows by the definition of . Therefore, from (A.13) the first result follows. It remains to show (A.8). To this end, we have

Note the factors out. The remaining terms are, after plugging in for from (6.15)

where the last equality follows by the definition of . Thus, (A.8) holds. ∎

Lemma A.8.

Proof of Lemma A.8.

We prove the first equality in (A.14). Indeed, if then

since on . This shows that , but we already know from Lemma A.4 that so in fact they are equal. If and then . Lastly, if and then

which shows that , a contradiction. This yields the first result. Next, since , on we immediately see that

It remains to consider the stochastic exponential for the jump processes. Here

Now, the above argument showed that implies and it is not possible for and so that in fact implies . Thus, if then

Similarly, if then

Therefore, (A.14) holds finishing the proof.

∎

References

- [1] T. R. Bielecki and M. Rutkowski, Credit Risk: Modeling, Valuation and Hedging, Springer Science & Business Media, 2004.

- [2] S. Choukroun, S. Goutte, and A. Ngoupeyou, Mean-variance hedging under multiple defaults risk, Stoch. Anal. Appl., 33 (2015), pp. 757–791.

- [3] Q. Dai and K. Singleton, Specification Analysis of Affine Term Structure Models, The Journal of Finance, 55 (2000), pp. 1943–1978.

- [4] F. Delbaen, P. Grandits, T. Rheinländer, D. Samperi, M. Schweizer, and C. Stricker, Exponential hedging and entropic penalties, Math. Finance, 12 (2002), pp. 99–123.

- [5] D. Duffie, D. Filipović, and W. Schachermayer, Affine processes and applications in finance, Ann. Appl. Probab., 13 (2003), pp. 984–1053.

- [6] L. C. Evans, Partial differential equations, vol. 19 of Graduate Studies in Mathematics, American Mathematical Society, Providence, RI, 1998.

- [7] D. Filipović, A general characterization of one factor affine term structure models, Finance and Stochastics, 5 (2001), pp. 389–412.

- [8] H. Föllmer and M. Schweizer, Hedging of contingent claims under incomplete information, in Applied stochastic analysis (London, 1989), vol. 5 of Stochastics Monogr., Gordon and Breach, New York, 1991, pp. 389–414.

- [9] A. Friedman, Partial differential equations of parabolic type, Prentice-Hall, Inc., Englewood Cliffs, N.J., 1964.

- [10] M. Frittelli, The minimal entropy martingale measure and the valuation problem in incomplete markets, Math. Finance, 10 (2000), pp. 39–52.

- [11] V. Gorovoy and V. Linetsky, Intensity-based valuation of residential mortgages: an analytically tractable model, Math. Finance, 17 (2007), pp. 541–573.

- [12] S. Goutte and A. Ngoupeyou, The use of BSDEs to characterize the mean-variance hedging problem and the variance optimal martingale measure for defaultable claims, Stochastic Process. Appl., 125 (2015), pp. 1323–1351.

- [13] P. Grandits and T. Rheinländer, On the minimal entropy martingale measure, Ann. Probab., 30 (2002), pp. 1003–1038.

- [14] Y. Jiao, I. Kharroubi, and H. Pham, Optimal investment under multiple defaults risk: a BSDE-decomposition approach, Ann. Appl. Probab., 23 (2013), pp. 455–491.

- [15] Y. Jiao and H. Pham, Optimal investment with counterparty risk: a default-density model approach, Finance Stoch., 15 (2011), pp. 725–753.

- [16] Y. M. Kabanov and C. Stricker, On the optimal portfolio for the exponential utility maximization: remarks to the six-author paper “Exponential hedging and entropic penalties” [Math. Finance 12 (2002), no. 2, 99–123; MR1891730 (2003b:91046)] by F. Delbaen, P. Grandits, T. Rheinländer, D. Samperi, M. Schweizer and C. Stricker, Math. Finance, 12 (2002), pp. 125–134.

- [17] I. Karatzas and S. E. Shreve, Brownian motion and stochastic calculus, vol. 113 of Graduate Texts in Mathematics, Springer-Verlag, New York, second ed., 1991.

- [18] O. A. Ladyˇzenskaja, V. A. Solonnikov, and N. N. a. Uralceva, Linear and quasilinear equations of parabolic type, Translated from the Russian by S. Smith. Translations of Mathematical Monographs, Vol. 23, American Mathematical Society, Providence, R.I., 1968.

- [19] G. M. Lieberman, Second order parabolic differential equations, World Scientific Publishing Co., Inc., River Edge, NJ, 1996.

- [20] T. Lim and M.-C. Quenez, Exponential utility maximization in an incomplete market with defaults, Electron. J. Probab., 16 (2011), pp. no. 53, 1434–1464.

- [21] , Portfolio optimization in a default model under full/partial information, Probab. Engrg. Inform. Sci., 29 (2015), pp. 565–587.

- [22] V. Linetsky, Pricing equity derivatives subject to bankruptcy, Math. Finance, 16 (2006), pp. 255–282.

- [23] S. Lukas, On pricing and hedging defaultable contingent claims, Humboldt-Universität zu Berlin, 2001.

- [24] M.-A. Morlais, Utility maximization in a jump market model, Stochastics, 81 (2009), pp. 1–27.

- [25] M. P. Owen and G. Žitković, Optimal investment with an unbounded random endowment and utility-based pricing, Math. Finance, 19 (2009), pp. 129–159.

- [26] P. Protter and K. Shimbo, No arbitrage and general semimartingales, in Markov processes and related topics: a Festschrift for Thomas G. Kurtz, vol. 4 of Inst. Math. Stat. (IMS) Collect., Inst. Math. Statist., Beachwood, OH, 2008, pp. 267–283.

- [27] P. E. Protter, Stochastic integration and differential equations, vol. 21 of Stochastic Modelling and Applied Probability, Springer-Verlag, Berlin, 2005. Second edition. Version 2.1, Corrected third printing.

- [28] D. Revuz and M. Yor, Continuous martingales and Brownian motion, vol. 293 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences], Springer-Verlag, Berlin, third ed., 1999.

- [29] M. Schweizer, On the minimal martingale measure and the Föllmer-Schweizer decomposition, Stochastic Anal. Appl., 13 (1995), pp. 573–599.

- [30] R. Sircar and T. Zariphopoulou, Utility valuation of credit derivatives: single and two-name cases, in Advances in mathematical finance, Appl. Numer. Harmon. Anal., Birkhäuser Boston, Boston, MA, 2007, pp. 279–301.

- [31] D. W. Stroock and S. R. S. Varadhan, Multidimensional diffusion processes, Classics in Mathematics, Springer-Verlag, Berlin, 2006. Reprint of the 1997 edition.