fit,shapes

Lowest Unique Bid Auctions

with Resubmission Opportunities

Abstract

The recent online platforms propose multiple items for bidding. The state of the art, however, is limited to the analysis of one item auction without resubmission. In this paper we study multi-item lowest unique bid auctions (LUBA) with resubmission in discrete bid spaces under budget constraints. We show that the game does not have pure Bayes-Nash equilibria (except in very special cases). However, at least one mixed Bayes-Nash equilibria exists for arbitrary number of bidders and items. The equilibrium is explicitly computed for two-bidder setup with resubmission possibilities. In the general setting we propose a distributed strategic learning algorithm to approximate equilibria. Computer simulations indicate that the error quickly decays in few number of steps. When the number of bidders per item follows a Poisson distribution, it is shown that the seller can get a non-negligible revenue on several items, and hence making a partial revelation of the true value of the items. Finally, the attitude of the bidders towards the risk is considered. In contrast to risk-neutral agents who bids very small values, the cumulative distribution and the bidding support of risk-sensitive agents are more distributed.

Keywords: Auction, Bayes-Nash Equilibrium, Pareto optimality, Learning Mechanism.

1 Introduction

Information technology has revolutionized the traditional structure of economic and financial markets. The removal of geographical and time constraints has fostered the growth of online auction markets, which now include millions of economic agents and companies worldwide and annual transaction volumes in the billions of US dollars. Here, we study bidders’ learning and behavior of a little studied type of online auctions called lowest unique bid auction (LUBA). LUBAs are online auctions which have reached a considerable success during last decade. Their key feature is that they are reverse auctions: rather than the bidder with the highest bid (as in the case of traditional auctions), the winner is the bidder who makes the lowest unique bid. The recent online platforms propose even multiple items and bidders can submit their bidders over several rounds [before a winner is decided]. The bidding status that a bidder observes changes according to the actions (bids) chosen by all the (active) bidders on the corresponding item. Due to limited number of items and budget restrictions, bidders need to manage their decision in a strategic way.

Literature review

One-item Auctions: The theory of auctions as games of incomplete information originated in 1961 in the work of Vickrey [2]. While auctions with homogeneous valuation distributions (symmetric auctions) and self-interested non-spiteful bidders is well-investigated in the literature, auction with asymmetric bidders remain a challenging open problem (see [3, 4, 5] and the references therein). With asymmetric auctions, the expected “revenue equivalence theorem” [6] does not hold, i.e., there is a class of cumulative valuation distribution function such that the revenue of the seller (auctioneer) depends on the auction mechanism employed. In addition, there is no ranking revenue between the auction mechanisms (first, second, English or Deutch).

Multi-Item Auctions: There are few research articles on multi-item auctions [7, 8, 9, 10]. Most of these works present computer simulation and numerical experiments results. However, no analysis of the outcome of the multi-item auction is available. There is no analysis of the equilibrium seeking algorithm therein.

The above mentioned works do not consider the the resubmission feature. Note however that the possibility for a bidder to resubmit another bid for the same item is already implemented in practice in the online auction markets.

LUBA: LUBA is very different than the second price auctions. The particularity of LUBA is that it focuses on the lowest unique bid, which creates lot of difficulties in terms of analysis. LUBA is different that the lowest cost auction called procurement auction which is widely used in e-commerce and cloud resource pooling [11] or in demand-supply matching in power grids [12]. Single-item LUBAs are a special case of unmatched bid auctions which have been studied by other researchers [13, 14, 15, 19, 16, 1]. The authors [14] run laboratory experiments with minbid auctions. They consider the case where players are restricted to only one bid and compare the results from their laboratory experiment with a Monte Carlo simulation. The authors in [15] consider high and low unique bid auctions where bidders are also restricted to a single bid. They provide a numerical approximation of the solution for a game-theoretic model and compare it with the results of a laboratory experiment. The work in [19] conducts a lowest unique positive integer experiment and contrast the observed behavior with the solution of a Poisson game with a single bid per player. [16, 17, 18] conducted field experiments on Lowest-Unmatched Price Auctions with mostly large prizes involving large numbers of participants (tens and hundreds of thousands). [20] studies truthful multi-unit transportation procurement auctions. The work in [21] discusses security and privacy issues of multi-item reverse Vickrey auction by designing more secure protocols. Most of the above works restrict the number of submissions per bidder to one. The recent focus within the auction field has been multi-item auctions where bidders are not restricted to buying only one item of the merchandise. The bidder can also place multiple bids for each item. It has been of practical importance in Internet auction sites and has been widely executed by them.

Contribution

Our contribution can be summarized as follows. Mimicking online platform auctions, we propose and analyze a multi-item LUBA game with budget constraint, registration fee and resubmission cost. We show that the analysis can be reduced into a constrained finite game (with incomplete information) by eliminating the bids that are higher than the value of the item. Using classical fixed-point theorems, there is at least one Bayes-Nash equilibrium in mixed strategies. Next, we address the question of computation and stability of such an equilibrium. We provide explicitly the equilibrium structure in special cases. We provide a learning algorithm that is able to locate equilibria. An imitative combined fully distributed payoff and strategy learning (imitative CODIPAS learning) that is adapted to LUBA is proposed to locate/approximate equilibria. We examine how the bidders of the game are able to learn about the online system output using their own-independent learning strategies and own-independent valuation. The numerical investigation shows that the proposed algorithm can effectively learn Nash equilibrium in few steps. It is shown that the auctioneers can make a positive revenue when the number of bidders per bid exceeds a certain threshold. We then examine the attitude of the bidders towards the risk. In contrast to risk-neutral agents who bids very small values, the cumulative distribution and the bidding support of risk-sensitive agents are more distributed.

Structure of the paper

The paper is organized as follows. In Section 2, we introduce LUBA mechanism. In Sect 3 we set up the problem statement, whose solution approach is given in Section 5.5. We provide an imitative learning algorithm for approximating Nash equilibria in Section 4.2. Section 5 focuses on risk-sensitive bidders’ behaviors. Section 6 concludes the paper.

We summarize some of the notations in Table 1.

| Symbol | Meaning |

|---|---|

| set of potential bidders | |

| cardinality of | |

| bid (action) space | |

| set of items (from auctioneers) | |

| cardinality of | |

| bid set of bidder on item | |

| payoff of the auctioneer | |

| payoff of bidder | |

| indicator function. | |

| cumulative distribution of the valuation matrix | |

| (marginal) cumulative distribution of | |

| the valuation vector of bidder |

2 Background on LUBA

A lowest unique bid auction operates under the following three main rules:

-

•

Whoever bids the lowest unique positive amount wins.

-

•

If there is no unique bid then no one wins. In particular, the bid of the winner should be unmatched.

-

•

No participant can see bids placed by other participants.

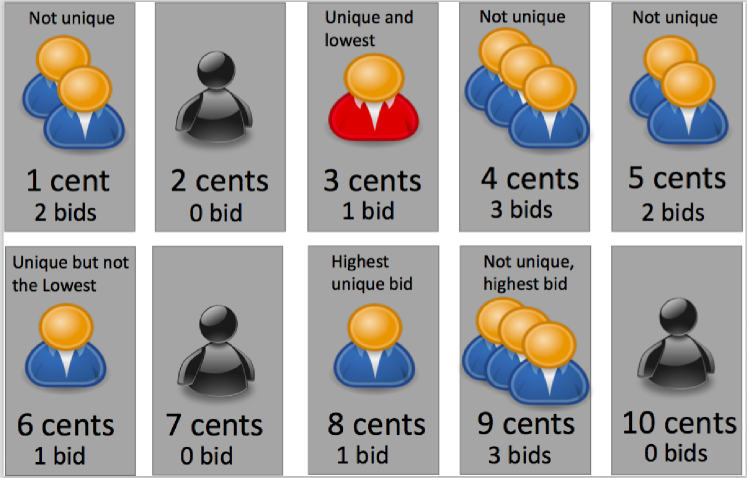

The term ”lowest unique bid” means is the lowest amount that nobody else has bid and its computation is illustrated in Table 2 and Fig.2 below.

| Bid Amount | Number of Bids | Status |

|---|---|---|

| 1 cent | 2 | Not unique |

| 2 cents | 0 | |

| 3 cents | 1 | Lowest Unique Bid! |

| 4 cents | 3 | Not Unique |

| 5 cents | 2 | |

| 6 cents | 1 | Unique but not the Lowest |

| 7 cents | 0 | |

| 8 cents | 1 | Highest unique bid |

| 9 cents | 3 | Not unique, highest bid |

| 10 cents | 0 |

Bids may be any amount between and allowing people to buy an item at an incredibly low price. The cost of the item is covered by the entry/administration/bid fee paid by all participants and by the resubmission fee to make a bid.

In this example the Bid of 3 cents is the Lowest Unique Bid and is awarded the auction result and would have to pay only 3 cents after the registration fee. He/she has therefore purchased an item for 3 cents + the Administration fee paid when he/she placed the bid and the registration fee. If the Bidder of the successful bid had more than one bid they would need to add a certain cost for each additional bid placed.

Each bidder can decide to participate or not. A participant can start bidding in just few steps:

-

•

Register - complete the registration form. Your password will then be emailed to the email address you provide us. It is vital you keep your username and password confidential, otherwise you may allow others to access your Bid Bank and place bids from your account.

The user is fully responsible for all activities that occur through your subscription and under your password and account.

-

•

Login - once the user receive its password via email, he/she login using her email address as your username and your password. For security issue the user can change her password.

-

•

Purchase Credit - Buy Credits from your account. Smiles or other related credits can be converted into a auction credit.

3 Problem Statement

Multi-item contest

A multi-item contest is a situation in which players exert effort for each item in an attempt to win a prize. Decision to participate or not is costly and left to the players. All the efforts are sunk while only the winner gets the prize. An important ingredient in describing a multi-item contest with the set of potential participants , the set of auctioneers proposing the set of items is the contest success function, which takes the efforts of the agents and converts them into each agent’s probability of winning per item:

The (expected) payoff of a risk-neutral player with a value of winning item and a cost of effort function is

Multi-item LUBA

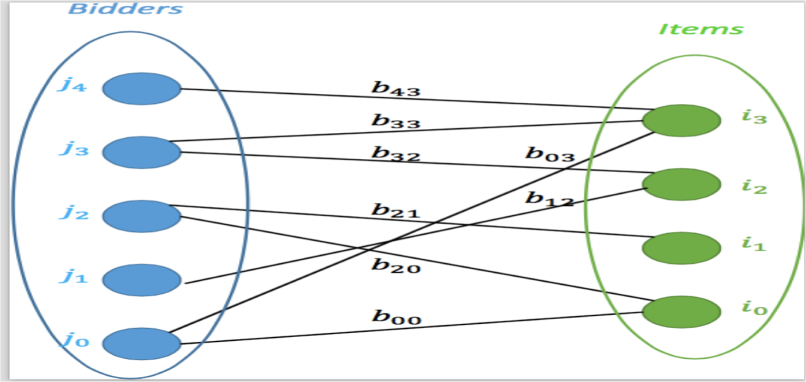

One very popular multi-item contest used in online platform is multi-item LUBA. In multi-item LUBA, Multiple sellers (auctioneers) have multiple items (objects) to sell on the online platform. These sellers have adopted a lowest unique bid auction (LUBA) rule. The multi-item LUBA game (with resubmission) is as follows.

There are bidders for items proposed by the sellers. A bidder’s assessment of the worth of the offered object for auction is called a value. In an multi-item auction context a bidder has a vector of values, one value per good.

Incomplete information about the others: A bidder may have its own valuation vector but not the valuation vector of the others.

The bidders are assumed to have (possibly heterogeneous) valuation distributions. Each bidder independently submits a possibly several bid per item without seeing the others’ bids. The submission fee per bid on item is If there is only a unique lowest bid, the object is sold to the bidder with unique lowest bid. Each bidder pays the cost for the registration and administration fee. In addition, the winner pays her winning bid on item , that is, the price is the lowest unique bid on that item. Note that the existence of a winning bid is not guaranteed, as for example, identical bids demonstrate. In the absence of a winner, the item remains with the auctioneer. Note that, a tie-breaking rule can be used in that case. We denote by the valuation of bidder for item The random variable has support where Each bidder has a initial total budget of to be used for all items. Each bidder knows its own-valuation vector and own-bid vector but not the valuation of the other bidders. Note that each bidder can resubmit bids a certain number of times subject to her available budget, each resubmission for item will cost If bidder has (re)submitted times on item her total submission/bidding cost would be in addition to the registration fee. Denote the set that contains all the bids of bidder on item by Thus, is the cardinality of the strictly positive bids by on item The set of bidders who are submitting on item is denoted by

In order to get the set of all unique bids, we introduce the following: The set of all positive natural numbers that were chosen by only one bidder on item is

If then there is no winner on item at that round (after all the resubmission possibilities). If then there is a winner on item and the winning bid is and winner is The payoff of bidder on item at that round would be

if is a winner on item , and

if is not a winner on item The payoff of bidder on item is zero if is reduced to (or equivalently the empty set).

where the infininum of the empty set is zero.

| (2) |

The instant payoff of the auctioneer of item is

where is the realized valuation of the auctioneer for item The instant payoff of the auctioneer of a set of item is Bidders are interested in optimizing their payoffs and the auctioneers are interested in their revenue.

3.1 Solution Concepts

Since the game is of incomplete information, the strategies must be specified as a function of the information structure.

Definition 1.

A pure strategy of a bidder is a choice of a subset of natural numbers given the own-value and own-budget. Thus, given its own valuation vector bidder will choose an action that satisfies the budget constraints

The set of multi-item bid space for bidder is

A pure strategy is a mapping A constrained pure strategy is a mapping A mixed strategy is a probability measure over the set of pure strategies.

The action set is finite because of budget limitation. A bid is hence less than

3.2 Bidders’ equilibria

We define a solution concept of the above game with incomplete information: Bayes-Nash equilibrium.

Definition 2.

A mixed Bayes-Nash strategy equilibrium is a profile such that for all bidders

for any strategy

4 Analysis: Risk-Neutral Case

We are interested in the equilibria, equilibrium payoffs of the bidders and revenue of the auctioneer. Note that the information structure is significantly reduced. Since does not know the distribution of the random matrix which may influence it is unclear how can bidder evaluate the expected payoff Therefore the expected payoff needs to be learned by

Proposition 1.

Let Any realized value of item such that leads to a trivial choice (i.e., ) for bidder Any participative bidding strategy on item such that is dominated by the strategy Any strategy such is dominated by on item

Proof of Proposition 1.

By budget constraint, s bids must fulfill the budget restriction

If agent bids on item with then gets in the bets case which is negative (loss) and could guarantee zero as payoff by not participating. Therefore the strategy dominates any higher than Thus, the bid space of agent on item can be reduced to

such that

This completes the proof. ∎

As a consequence of Proposition 1,

-

•

the number of resubmissions on item needs to be bounded by to be rewarding.

-

•

when analyzing Bayes-Nash equilibria one can limit the action space to all the subsets of the finite set

Proposition 2.

Generically (under feasible budget), the LUBA game with resubmission has no pure Bayes-Nash equilibria.

Proof of Proposition 2 .

Let and consider a pure behavioral strategy profile with a generic budget If does not contain a winning bid then can be reduced by saving the resubmission cost, i.e., an empty set or But if is not participating on item (while its budget allows) then there is another player who could also save by decreasing its bid set. However, the action cannot be an equilibrium because player can deviate and bids with higher than the maximum bid in action Hence, there always a player who can deviate and benefits if budget allows and if the value is not reached in terms of bidding cost.

If contains a winning bid then there is another player such that does not contain the winning bid and one can apply the reasoning above with Iterating this for all items, we deduce that the action is not a best response to itself. Hence, cannot be a Bayes-Nash equilibrium. This completes the proof. ∎

Note however that there are trivial cases with pure equilibria:

-

•

if multiple resubmissions are not allowed i.e., then the action profile is an equilibrium profile of that item whenever the realized value is such that Putting together, the set of pure equilibria in this very special case game with is the cumulative distribution of the set of action where the set of decomposition/partition of the number is given by

where

-

(a)

-

(b)

and

-

(c)

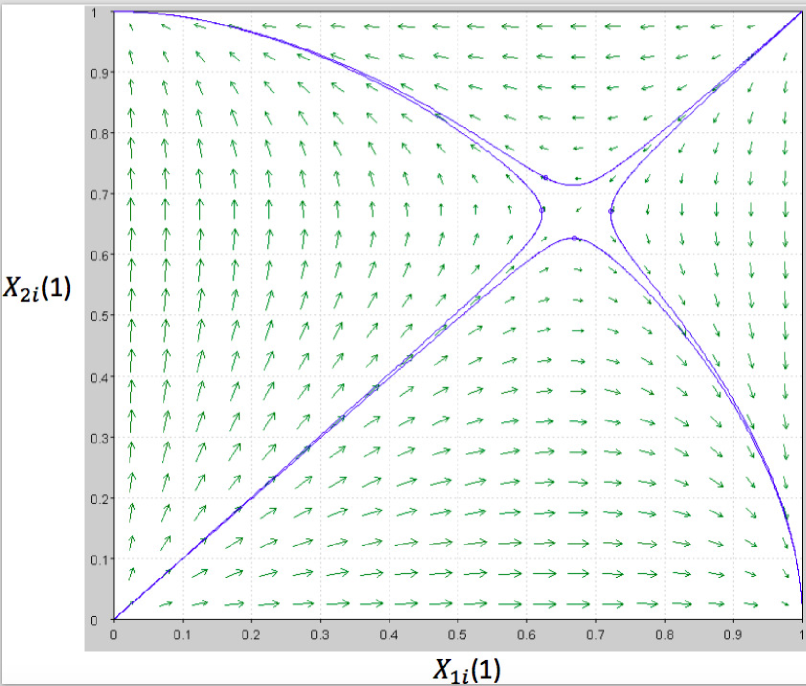

Figure 3: The vector field of the learning dynamics when Convergence to equilibrium. As shown in Figure 3, the learning algorithm always converges to one of pure Nash equilibria except when they are symmetric, however, the probability of symmetric situation is zero.

-

(a)

-

•

If it is not interesting to bid higher than because of negative payoff.

-

•

when the realized value is below the action is better for on

Non-potential game

As a corollary of Proposition 2 we deduce that LUBA is NOT a potential game because one can exhibit the following cycle of action profiles for item

which is a finite (better-reply) improvement cycle.

The following result provides existence of equilibria in behavioral mixed strategies.

Proposition 3.

The multi-item Bayesian LUBA game (with resubmission) but with arbitrary number of bidders has at least one Bayes-Nash equilibrium in mixed strategies under budget restrictions. Moreover, at a (generic) mixed equilibrium, the expected payoff of the bidder is zero.

Proposition 3 provides existence of at least one Bayes-Nash equilibrium. However, it does not tell us what are those equilibria.

Proof of Proposition 3.

By Proposition 1 the constrained game has a finite number of action. By standard fixed-point theorem, the multi-item Bayesian LUBA game (with resubmission) but with arbitrary number of bidders has at least one Bayes-Nash equilibrium in mixed strategies under budget restrictions.

∎

Below we explicitly compute mixed equilibrium for two bidders with resubmission.

Proposition 4.

Let and The game has a partially mixed equilibrium which is explicitly given by

where is the maximum number such that

Proof of Proposition 4.

Let be the largest integer such that . When bidder 2’s strategy is the expected payoff of bidder 1 when bidding is equal to zero in equilibrium due to the indifference condition, for each . The cost of such a bid is equal to .

On the other hand, the expected gain can be computed as follows. With probability , bidder 2 will not post any bid, the winning bid is 1, and the gain is thus for any For the bidder 2 bids with probability and the winner bid is from bidder 1, and 1’s gain will The expected payoff of bidder 1 when playing is therefore given by

It turns out that

For between and we make the difference between line and line to get:

Thus, the partially mixed strategy

is an equilibrium strategy. The equilibrium payoff is zero. This completes the proof.

∎

Note that the framework can easily capture situations in which the number of potential participants can be unbounded. We introduce the statistics of the bidding data as which is the number of bidders who place on item The random matrix contains enough information that will allow any player to compute its payoff. Therefore one can work directly on bid statistics The knowledge of the total number of participants is not required. The payoff function of on item is The dependence on the mean-field term is expressed as following: if and only if is the smallest non-zero bid such that

4.1 Revenue of the auctioneers

We now investigate how much money the online platform can make by running multi-item LUBA. Since the platform will be running for a certain time before the auction ends, each bidder is facing a a random number of other bidders, who may bid in a stochastic strategic way. Their valuation is not known. We need to estimate the set of bids and the bid values on item We denote by the random number of bidders who bid on If follows a Poisson distribution with parameter , and that all variables are independent. The value is assumed to be non-decreasing with The expected payoff of the seller on item is

Proposition 5.

Let with The expected revenue of the seller on item is exceeds the value of the item for small value of whenever

Proof of Proposition 5.

The expected payoff of the seller on item is equal to As we assume that follows a Poisson distribution with parameter and that all are independent, we can calculate that Rewriting the expected payoff of the auctioneer, we get that it is equal to Then, we can easily induce the condition for the expected revenue of the seller exceeds the value of is

∎

Note that in all-pay auction (with resubmission cost) if the probability to win is (uniform lottery) then the revenue of the seller is Thus, the difference between the two schemes is the expected winning bid if the action profile generates similar distribution

Proposition 3 provides existence of at least one Bayes-Nash equilibrium. However, it does not tell us how to learn or to reach those equilibria. Below we provide a learning procedure for equilibria.

4.2 Learning Algorithm

Imitative learning is very important in many applications [22] including cloud networking, power grid, security & reliability, information dissemination and evolution of protocols and technologies. It has been successfully used to capture animal behavior as well as human learning.

Based on randomly disturbed games à la Harsanyi [23] who showed that the equilibria of a game are limit points of sequences of Nash as the parameter vanishes, the imitative learning follows the same line as a perturbed payoff-based scheme. So, when trying to learn the equilibria of a game it makes sense to consider imitative Boltzmann-Gibbs strategy with a small parameter The number is sometimes interpreted as a rationality level of the player. Small is therefore seen as big rationality level.

Surprisingly, it also makes sense to consider imitative Boltzmann-Gibbs with big parameter because when the parameter approaches infinity, the limiting of the imitative logit dynamics is the so-called “imitate the better” dynamics [24]. The actions that are initially not present in the support of the strategy will never be tried with imitative dynamics, so we always consider initial points in the interior of the strategy space.

What is the information-theoretic function associated to the imitative Boltzmann-Gibbs (iBG) strategy? The information-theoretic metric behind the imitative Boltzmann-Gibbs learning is the relative entropy. This is an important connection between imitative learning and information theory since the relative entropy covers the mutual information, information gain and the Shannon entropy as particular case. We introduce relative entropy as a cost of moves in the LUBA games. One can interpret relative entropy as a cost of moves in the learning process. Specially, the next Proposition 6 shows that the imitative Boltzmann-Gibbs strategy (or imitative logit strategy, i-logit) is the maximizer of the perturbed payoff where is the relative entropy from strategy to (also called Kullback-Leibler divergence) and is the rationality level of player

The instant payoff of bidder on item at time/round is a realized value of

where is an observation/measurement noise. Bidder wins on item at time if its bid is the lowest unique bid on item and is feasible in terms of the available budget of at time if bidder does not participate to item This algorithm describes how to update the reward and the strategy in the bid space. Let be the estimation of reward corresponding the -th bidder to -th item at round if she decides the bid set corresponding to the index of and

Initialization: Estimate reward on item at round zero.

For Round

For every bidder and every item:

Update S:

Normalize S:

Let be a vector in the relative interior of the -dimensional simplex of This means that the cost to move for player from to is given by

where This cost is added to the expected estimated payoff which is Thus, we associate the following problem to player

| (3) |

We introduce the Legendre-Fenchel transform of the relative entropy function

| (4) |

where is a positive parameter. corresponds to the best expected estimated payoff with cost of learning.

Proposition 6.

The following statements hold:

(i) The strategy is the optimal strategy solution to (4).

Proof of Proposition 6.

Let The function

is strictly concave (the Hessian matrix with entries and ) and the domain (simplex) is convex. Thus, the Karush-Kuhn-Tucker (KKT) conditions are necessarily and sufficient for the problem in (4). Using KKT conditions, one has

where is the Lagrange multiplier associated to the simplex equality equation of player . It follows that

Taking the exponential yields

Summing over the set of actions, one gets which implies that

Thus, the optimal strategy is

The Lagrange multiplier is

and

∎

The next Proposition specifies the error bound in terms of the parameter

Proposition 7.

There exists such that

| (5) |

Moreover,

Proof of Proposition 7.

The proof follows immediately from the definition of and the fact that the entropy function of player is between and ∎

Proposition 8.

The following results hold:

-

•

High rationality regime:

-

•

Low rationality regime:

Proof of Proposition 8.

The first limit follows from Proposition 7. We now prove the second limit. By changing the variable one gets that goes to zero and the limit becomes

| (6) | |||

| (7) |

by Hospital’s rule. This completes the proof. ∎

It is important to notice that when goes to zero then the rationality level tends infinity and player gets closer to the maximum payoff This result also says that when goes to infinity, one gets the expected payoff. Hence it gives a stationary point of the replicator equation. We retrieve a well-known result in evolutionary process which states that the evolution of phenotypes and genes has a tendency NOT to maximize the fitness but the mixability of system which is somewhat captured with the mixture term

Relationship with replicator dynamics

Following [25] the scaled stochastic process from follows a replicator dynamics given by

when the learning rate which is random matrix, vanishes.

4.3 Second Learning Algorithm

The complexity of the bid space in the lowest unique bid system is . Take for an example, the bid space of LUBA with resubmission is when the unit is 1 cent. This limits considerably the usability of the proposed algorithm. There is a need for reducing the curse of dimensionality or complexity. We utilize Monte Carlo to approximate the Nash-Equilibrium. The basic idea is that we utilize information provided by the system to guide the behavior of bidders, and then the frequency of winner’s output is utilized as the approximation of Nash-Equilibrium.

During the bidding process, after placing a bid, the following information is provided by the system to the bidder.

-

1.

Currently, whether the bid wins or not.

-

2.

If not, the reason is:

-

(a)

is non-unique.

-

(b)

is too high.

-

(a)

Initialization:

-

1.

For bidder , initial

-

2.

Generate bid from

-

3.

Based on the system output information, update

-

(a)

is non-unique: .

-

(b)

is too-high:

-

(a)

For Round

For every bidder and every item:

Update S:

Normalize S:

4.4 Pareto optimality and global optima for bidders

Pareto optimality (PO) for bidders’, is a configuration in which it is not possible to make any one bidder better off without making at least one bidder worse off.

Proposition 9.

Let

| (8) | |||||

Then, any profile in is a Pareto optimal solution and the global payoff of the bidders at these PO is

The global optimum (GO) payoff of the bidders consists to select the maximum value for each item and place 1 cent for that bidder if its budget allows to do so.

The proof is immediate.

The inefficiency gap between total bidders’ payoff at mixed Bayes-Nash equilibrium (which is ) and GO payoff is

4.5 Numerical Investigation

In this subsection we introduce the experiment setting for the learning equilibria of LUBA game.

4.5.1 Illustration of Proposition 4: 2 bidders for 1 item

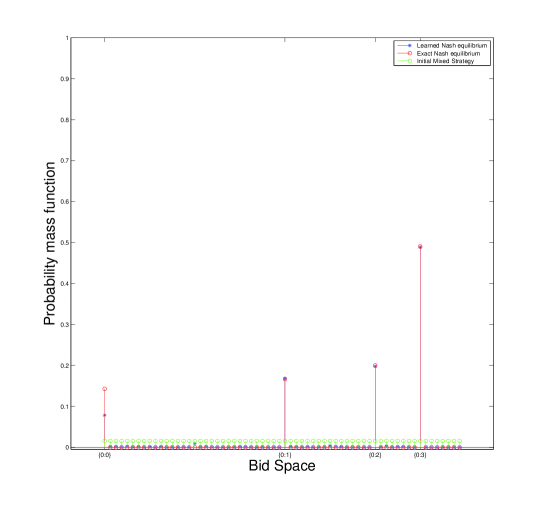

First we introduce the simulation of Proposition 4. Table 3 shows the experiment setting. We observe from Figure 4 that the algorithm provides a satisfactory result for approaching the mixed Bayes-Nash equilibrium distribution.

| 2 | 1 | ||

| 6 | 8 | ||

| 0.5 | 0.1 | ||

| Assumption | Symmetric | Assumption | Static Budget |

4.5.2 Two players for one item (asymmetric situation)

Let The action profile of bidder 1 is and that of bidder 2 is Registration fee and submission cost The parameters assumption in this simulation conveys different bidders have different valuation target same item. Table 4 represents the payoffs matrix of bidder 1 and 2. The row player is player 1 and the column player is player 2. The ceil list rewards of each bidder and bidder 1 come first.

| {0} | {01} | {012} | {0123} | |

|---|---|---|---|---|

| {0} | ||||

| {01} | ||||

| {012} |

Let the mixed strategy of bidder 1 be and that of bidder 2 . According to the indifferent condition we can derive the mixed Nash equilibrium is . We now analyze the mixed strategy of bidder 1. According to the indifferent condition, we can derive the following set of equations.

As the action provides an expected payoff which is strictly higher than obtained with the action The action is not in the support of the mixed Nash equilibrium. Assume the rewards of action and are equal, then we can derive the Nash equilibrium of bidder 1 is The Nash equilibrium of bidder 2 can be derived utilizing the same method.

4.5.3 Three bidders - One item

Let Table 8 represents the payoffs of bidder 1. The bid profile of bidders 2 and 3 are displayed in the column. Bidder 1 choice is a row of the matrix.

| {0} {0} | {1} {0} | {0} {1} | {1} {1} | |

|---|---|---|---|---|

| {0} | 0 | 0 | 0 | 0 |

| {1} | ||||

| {2} | ||||

| { 3} | ||||

| {12} | ||||

| {13} | ||||

| {23} | ||||

| {123} |

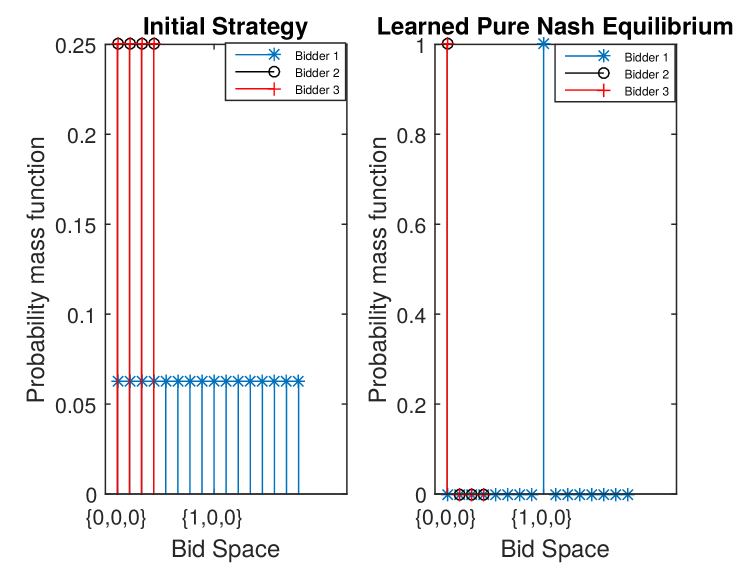

If then player 1 will not participate because the value of the item is below the cost to get it. Due to the unfeasible budget from bidders 2 and 3 who cannot bid 2 cents, the pure action is a Bayes-Nash equilibrium if If then bidder 1 can guarantee a positive payoff by playing the action Therefore, player will participate for sure because her action dominates in that case.

From Figure 5, which is the corresponding simulation results, we can conclude that the learning algorithms converged to the Nash equilibrium described in Table 8.

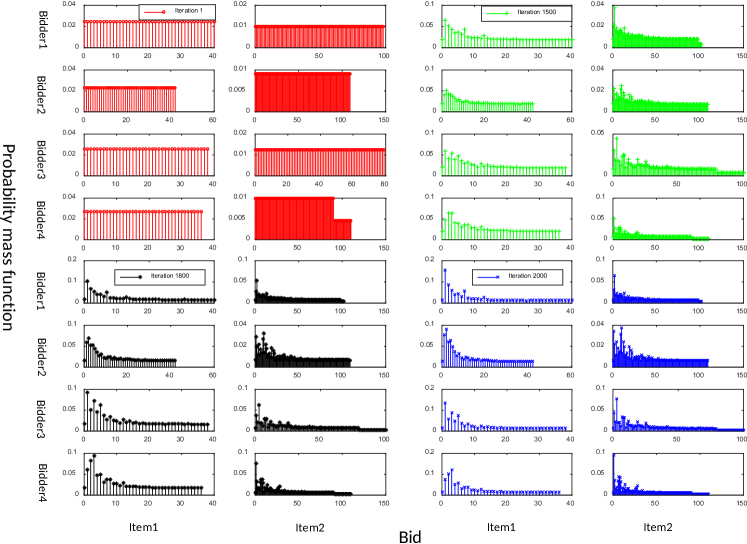

4.5.4 Four bidders - Two items

| Symbol | Setting |

|---|---|

| 4 | |

| 2 | |

| 0.001 | |

| 0.01 | |

| 1 | |

| Resource for item 1 and 2 | [2000 1500] |

| Initial of Budget | [100 120 80 90] |

| Initial of | 0.0001 |

| for | [40,102],[42,109],[38,100],[36,110] |

4.5.5 Impact of Parameters

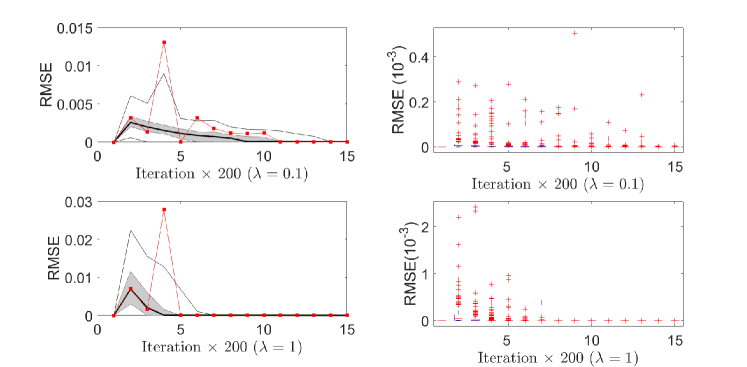

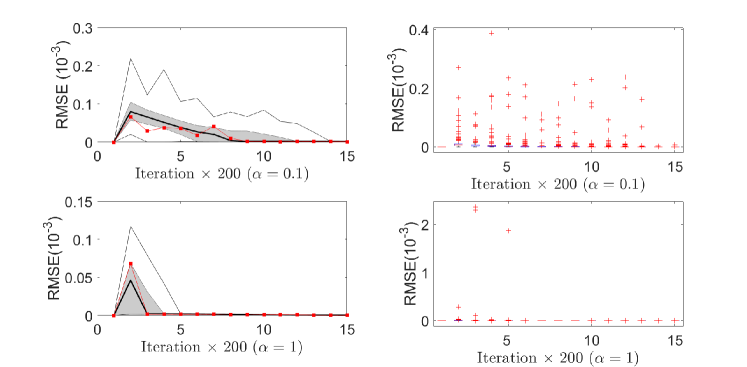

We investigate the impact of parameters in the proposed learning algorithm described.Table 7 shows experiment setting details. In order to analyze the numerical convergence of the learning scheme we introduce root mean square error RMSE between two sequential round strategies.

Figure 7 and 8 present the statistic properties of RMSE evolution with the bid round obtained by the proposed learning algorithm. Compared to and , the results shows a quickly converged property. The plot shows that the large parameter setting results less outliers in the experiment results. According to the results in Figure 7 and 8, the parameter and influence the convergence of the proposed algorithm equally and a large can reduce disturbance and outliers more effectively.

| Symbol | Original Setting | Compared Setting |

| 0.1 | 1 | |

| 0.1 | 1 |

5 Risk-Sensitive Problem Statement

Multi-Item contest

A multi-item contest is a situation in which players exert effort for each item in an attempt to win a prize. Decision to participate or not is costly and left to the players. An important ingredient in describing a multi-item contest with the set of potential participants the set of auctioneers proposing the set of items is the contest success function, which takes the efforts of the agents and converts them into each agent’s probability of winning per item: The (expected) payoff of a risk-neutral player with the realized value of winning item and a cost of effort function is The risk sensitive payoff is where is a one-to-one mapping.

Multi-Item LUBA: Risk-Sensitive Case

Multiple sellers (auctioneers) have multiple items (objects) to sell on the online platform. The payoff of bidder on item at that round would be if is a winner on item , and if is not a winner on item and The instant payoff of bidder on item is zero if is reduced to (or equivalently the empty set).

where the infininum of the empty set is zero.

| (10) |

The risk-sensitive instant payoff of bidder is Each bidder has a budget constraint

The instant payoff of the auctioneer of item is

where is the realized valuation of the auctioneer for item The instant payoff of the auctioneer of a set of item is The risk-sensitive instant payoff of the auctioneer of a set of item is

Bidders are interested in optimizing their risk-aware payoffs and the auctioneers are interested in their revenue under risk.

5.1 Risk-Sensitive Solution Concepts

Since the risk-sensitive game is of incomplete information, the strategies must be specified as a function of the information structure.

Definition 3.

A pure strategy of bidder is a choice of a subset of natural numbers given the own-value and own-budget. Thus, given its own valuation vector bidder will choose an action that satisfies the budget constraints

The set of multi-item bid space for bidder is

A pure strategy is a mapping A constrained pure strategy is a mapping A mixed strategy is a probability measure over the set of pure strategies.

5.2 Continuum approximation of discrete bid space

Let be a currency/coin point in which the bidding will take place. is a rational number. The bid space is When the bid units are very small (below or in the order of ) the bid space is huge and the complexity is exponential. One standard method is to consider this set as discretization of the continuous set under the budget constraint

However, the continuous bid space case provides different outcomes as explained below.

We investigate the smooth function case. For each item the random variable has a continuously differentiable () cumulative distribution function Note that the event for is of measure zero since the valuation has a continuous probability density function. Thus, the risk-sensitive LUBA analysis reduces to the (non-zero) lowest price on each item and their attitudes towards the risk.

Lemma 1.

In the continuous bid space case, the terms and are decreasing in

Proof.

It is because the cumulative distribution function increases with and the function deceases with Observing that can be written as the assertion follows. ∎

Lemma 1 provides a structural property of the better response bid in the continuous bid space case. The monotonicity properties above say that one can improve the payoff by approaching the bid to zero. However, zero is not allowed bid. When do not participate to the LUBA its payoff is The risk-sensitive participation constraint yields

5.3 Bid Resubmissions

Let be the time space of one round of LUBA game, for At each time-step the bidders have opportunity to revise and resubmit another bid. A bidder has also the option not to resubmit and save the resubmission cost. A sequence of actions on item by bidder is where can be a bid in or

Note that each bidder can resubmit bids a certain number of times subject to her available budget, each resubmission for item will cost Let be the set of the non-zero (strictly positive) component of the action The cardinality of is If bidder has (re)submitted times on item her total submission/bidding cost would be in addition to the registration fee. Denote the set that contains all the bids of bidder on item by The set of bidders who are submitting on item is denoted by

The set of all positive natural numbers that were chosen by only one bidder on item is If then there is no winner on item at that round (after all the resubmission possibilities). If then there is a winner on item and the winning bid is and winner is The payoff of bidder on item at that round would be if is a winner on item , and if is not a winner on item The payoff of bidder on item is zero if is reduced to (or equivalently the empty set).

where the infininum of the empty set is zero. The payoff is and the risk-sensitive payoff is We choose the exponential function (with risk-sensitive index )to simplify the analysis.

5.4 Risk-sensitive equilibria

Proposition 10 (Two bidders).

Let The risk-sensitive LUBA with resubmission has a mixed strategy given by

with ,

and

if

where .

Proof.

Let be the largest integer such that . When bidder 2’s strategy is the expected payoff of sensitive bidder 1 when bidding is equal to 1 in equilibrium due to the indifference condition, for each . The cost of such a bid is equal to .

On the other hand, the expected gain can be computed as follows. With probability , bidder 2 will not post any bid, the winning bid is 1, and the gain is thus for any For the bidder 2 bids with probability and the winner bid is from bidder 1, and 1’s gain will Take the risk-sensitive perspective into consideration, The of bidder 1 when playing is therefore given by

It turns out that

For between and we make the difference between line and line to get:

Thus, the partially mixed strategy

is an equilibrium strategy. The equilibrium sensitive-risk payoff is . ∎

Note that, for two bidders the equilibrium strategy has monotone support. The set of actions such that is an increasing inclusion:

it means that etc.

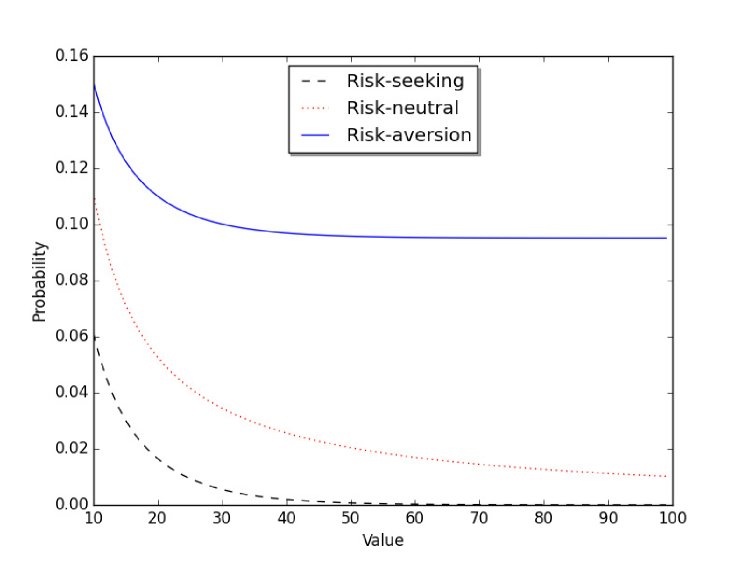

We analyze the Nash-Equilibrium of LUBA with resubmission in which the risk-sensitive payoffs are considered. Without losing generalization meaning, we specify . So the risk-sensitive instant payoffs of bidder j is where . For , the is equal to . The bidder can be divided into different categories based on

-

1.

The bidder is risk-seeking for

-

2.

The bidder is risk neutrality for

-

3.

The bidder is risk aversion for

We analyze the simple case under the above assumption, where 2 bidders participate in the LUBA. We analyze different combinations of and give corresponding payoff matrix. In order to simplify the analysis, we assume that the bid space of each bidders is Despite the simplification, this methodology can be extended to the general situation.

| 0 | 1 | |

|---|---|---|

| 0 | (1, 1) | (1, ) |

| 1 | (, 1) | (, ) |

-

1.

Pure Nash-Equilibrium: Table 9 shows how the payoff matrix for risk-sensitive can be converted to the risk-neural payoff matrix when analyzing pure Nash Equilibrium. So there are two pure Nash equilibrium.

Table 9: Two risk neutral bidders - One item 0 1 0 (0, 0) 1 (-1,-1) -

2.

Mixed Nash-Equilibrium: For bidder 2 the mixed strategy is:

-

(a)

Bidder 1:

-

(b)

Bidder 2:

-

(a)

As shown in Figure 9, the probability of participating in a risk-seeking bidder is greater than that of a risk-neutral one. And the probability of participating in a risk-aversion bidder is less than that of a risk-neutral one. This observation shows that over assumption on risk function is reasonable.

The next Theorem shows that this monotonicity property of the mixed equilibrium is lost when three or more bidders are involved.

Proposition 11 (Three or more bidders).

Suppose the realized parameters of the risk-sensitive LUBA are symmetric with three or more bidders. Then the risk-sensitive LUBA with resubmission has a symmetric equilibrium in mixed strategies. However, there is no symmetric mixed equilibrium with monotone strategies.

The existence of symmetric mixed equilibrium in finite symmetric game is by now standard. We omit the details proofs of the non-monotonicity of the optimal strategies when three or more bidders are involved. The example below illustrates the result in the three-bidder case.

We analyze another simple example to show the properties of LUBA with resubmission. We assume 3 bidders participate in a symmetric LUBA game. The submission fee is , and the bid space is The specific parameters setting is and their combinations. The payoff matrix is shown in the Table 10.

| 0,0 | 1,0 | 2,0 | 1.2,0 | 0,1 | 1,1 | 2,1 | 1.2,1 | 0,2 | 1,2 | 2,2 | 1.2 ,2 | 0,1.2 | 1,1.2 | 2,1.2 | 1.2,1.2 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 1 | v-c-1 | -c | v-c-1 | -c | -c | -c | -c | -c | v-c-1 | -c | v-c-1 | -c | -c | -c | -c | -c |

| 2 | v-c-2 | -c | -c | -c | -c | v-c-2 | -c | -c | -c | -c | -c | -c | -c | -c | -c | -c |

| 1,2 | v-2c-1 | v-2c-2 | v-2c-1 | -2c | v-2c-2 | v-2c-2 | -2c | -2c | v-2c-1 | -2c | v-2c-1 | -2c | -2c | -2c | -2c | -2c |

Based on the payoff matrix, we introduce the following indifferent condition:

-

1.

-

2.

-

3.

-

4.

where , and . As we assume that the proposed system is a symmetric LUBA game with three bidders, thus we can induce the following equations according the above indifferent condition equations.

-

1.

-

2.

-

3.

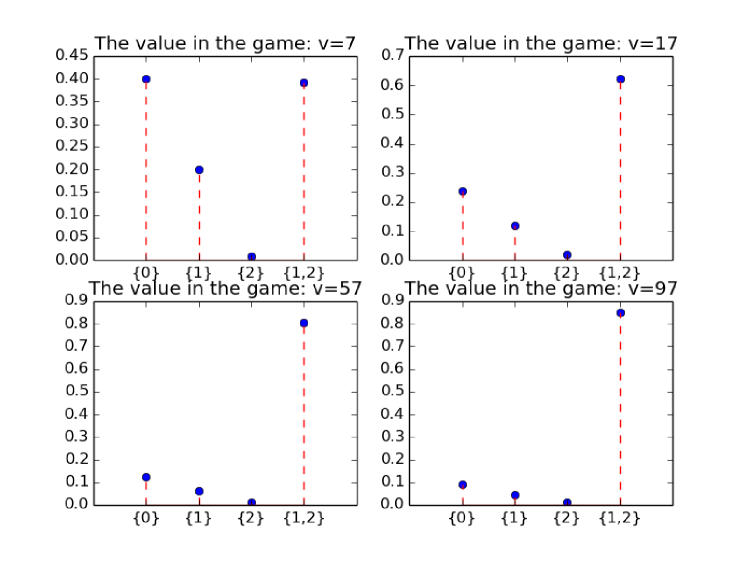

Then we can induce the following equations: , , and Combining the truth that we can derive the Nash-Equilibrium of this simple example is We calculate four Nash-Equilibrium of different value, and the result is shown in Figure 10.

We can observe that the probability of placing the combination bid is increasing with the value variable. Intuitively, it makes sense that when the valuation of the product is very high, the bidder is willing to take a risk for multi-bids. And when the value goes very high, the bid choice of dominates the whole bid choice space, as shown in the Figure 10: ’the value in the game: ’.

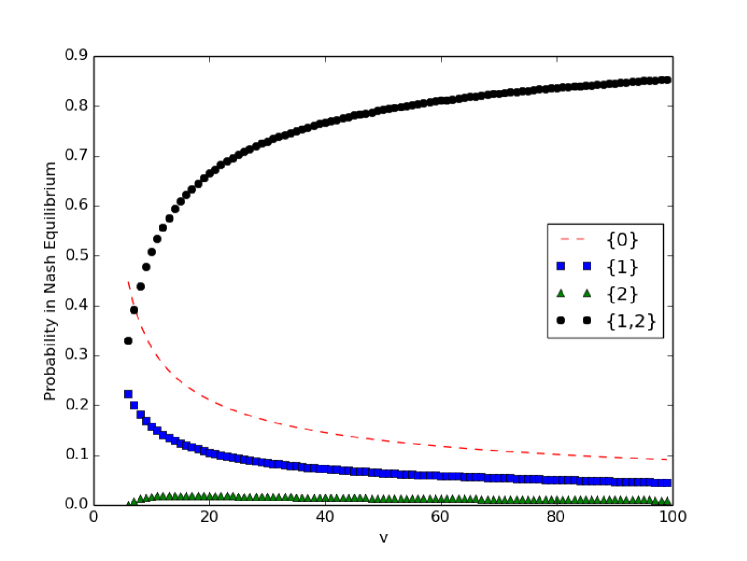

In a more general case, we show the evolution of Nash-Equilibrium with the value of the bidders targeting the item in Figure 11. By observing results, we can conclude that:

-

1.

The probability of is higher than and in a Nash-Equilibrium.

-

2.

The probabilities of single bid actions in the bid space decrease with the value in a Nash-Equilibrium

-

3.

The probability of in a Nash-Equilibrium increases with the value.

-

4.

The option of is dominant in action space when the valuation of bidders is very high.

5.5 Simulations of the Risk-Sensitive Scenarios

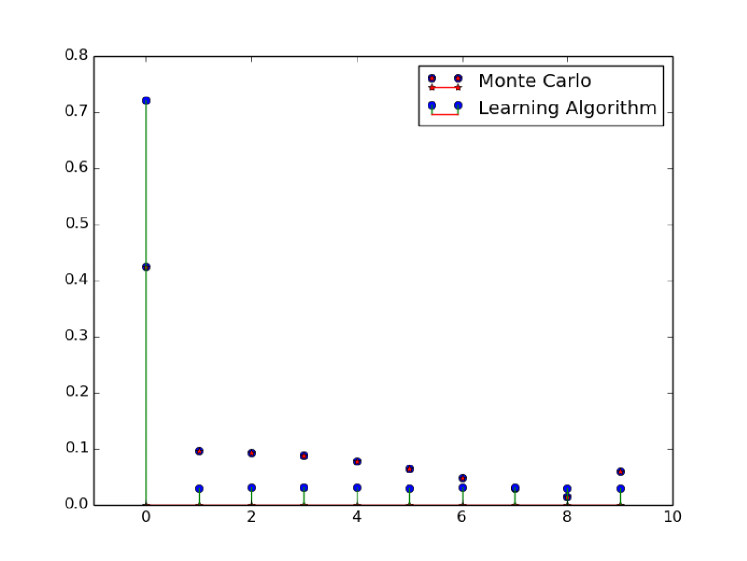

This section we will show and analyze the results from out proposed learning algorithm. In order to show the effectiveness of our Monte Carlo algorithm, we conduct a comparison experiment. In the comparison experiment, we compare the results of our proposed learning algorithm and our Monte Carlo algorithm under the same experiment parameters setting. The specific setting is shown in table 11.

| n | 10 | m | 1 |

| 10 | c | 1 | |

| 0.05 | 0.05 |

We analyze the frequencies of each single bid from zero to nine, and the results is shown in Figure 12. As shown in Figure 12, the equilibria, learned by both of proposed algorithms, show the same tendency. Obviously, they are not exactly same. The reason of this phenomenon is that the Monto-Carlo algorithm is an approximate method and doesn’t take consideration of value variable. However, the difference between the approximate result(obtained by Monte-Carlo algorithm) and the precise results(obtained by proposed learning algorithm) is very small. This phenomenon shows that our Monto-Carlo can effectively calculate the approximate Nash-Equilibrium in LUBA.

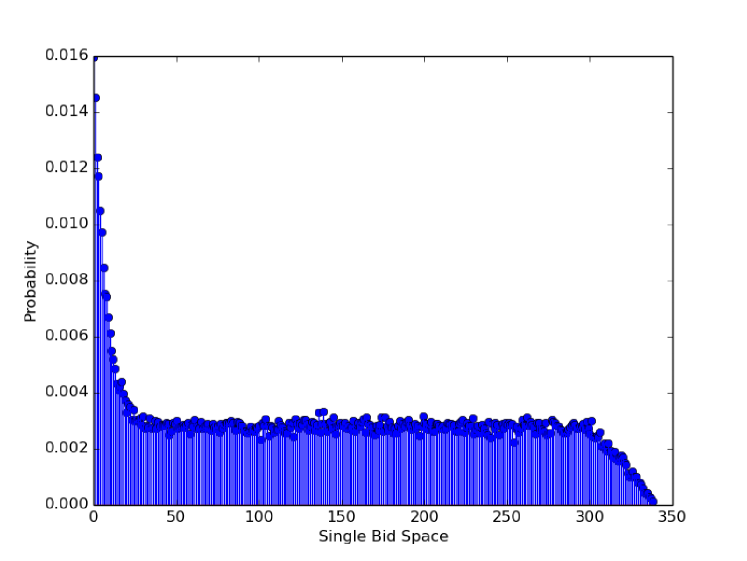

Note that we show the effectiveness of our Monte-Carlo algorithm in small bid space, now we show the application of our Monte-Carlo algorithm in large bid space situation. We assume that 100 bidders participate the game, their budgets are sampled from 300 to 350 in a uniform distribution, and the value variable is from 90 to 100. The result is shown in Figure 13.

From the results we can draw the following conclusions. The tendency of approximated Nash Equilibrium is same as the small bid space situations. Practically, the strategy form like the tendency shown in Figure 13 is a suboptimal solution of approximating Nash Equilibrium. It makes sense for that if a bidder want to win the LUBA game, he or she has to block the small bid. And, in a multi bidders LUBA with resubmission, any relative big bids have a chance to win the product as the probability of placing a non-unique bid is high in this experiment setting.

6 Conclusion and Future Work

In this paper, we have investigated multi-item lowest unique bid auctions in discrete bid spaces under heterogeneous budget constraints and incomplete information. Except for very special cases, the game does not have equilibria in pure strategies. As a constrained finite game, there is at least one mixed Bayes-Nash equilibrium. A mixed equilibrium is explicitly computed in two bidder setup with resubmission possibilities. We have proposed a distributed strategic learning algorithm to approximate equilibria in the general setting. The numerical investigation has shown that the proposed algorithm can effectively learn Nash equilibrium in few number of steps. It is shown that the auctioneers can make a positive revenue when the number of bidders per bid exceeds a certain threshold.

References

- [1] Marco Scarsini, Eilon Solan, Nicolas Vieille: Lowest Unique Bid Auctions, Preprint 2010.

- [2] Vickrey, W.: Counterspeculation, auctions, and competitive sealed tenders. J. Finance 16, 8–37.1961.

- [3] Maskin E. S., Riley J. G. Asymmetric auctions. Rev. Econom. Stud. 67, 413-438, 2000.

- [4] Lebrun B: First-price auctions in the asymmetric bidder case. International Economic Review 40:125-142, (1999)

- [5] Lebrun B.: Uniqueness of the equilibrium in first-price auctions. Games and Economic Behavior 55:131-151, 2006.

- [6] Myerson R., Optimal Auction Design, Mathematics of Operations Research, 6 (1981),pp. 58-73.

- [7] Bang-Qing Li, Jian-Chao Zeng, Meng Wang and Gui-Mei Xia, A negotiation model through multi-item auction in multi-agent system, Machine Learning and Cybernetics, 2003 International Conference on, 2003, pp. 1866-1870 Vol.3.

- [8] C. Yi and J. Cai, Multi-Item Spectrum Auction for Recall-Based Cognitive Radio Networks With Multiple Heterogeneous Secondary Users, IEEE Transactions on Vehicular Technology, vol. 64, no. 2, pp. 781-792, Feb. 2015.

- [9] N. Wang and D. Wang, Model and algorithm of winner determination problem in multi-item E-procurement with variable quantities, The 26th Chinese Control and Decision Conference (2014 CCDC), Changsha, 2014, pp. 5364-5367.

- [10] Rituraj and A. K. Jagannatham, Optimal cluster head selection schemes for hierarchical OFDMA based video sensor networks,” Wireless and Mobile Networking Conference (WMNC), 2013 6th Joint IFIP, Dubai, 2013, pp. 1-6.

- [11] J. Zhao, X. Chu, H. Liu, Y. W. Leung and Z. Li, Online procurement auctions for resource pooling in client-assisted cloud storage systems, IEEE Conference on Computer Communications (INFOCOM), 2015, pp. 576-584.

- [12] R. Zhou, Z. Li and C. Wu, An online procurement auction for power demand response in storage-assisted smart grids, IEEE Conference on Computer Communications, INFOCOM, 2015, pp. 2641-2649.

- [13] H. Houba, D. Laan, D. Veldhuizen, Endogenous entry in lowest-unique sealed-bid auctions,Theory and Decision, 71, 2, 2011, pp. 269-295

- [14] Stefan De Wachter and T. Norman, The predictive power of Nash equilibrium in difficult games: an empirical analysis of minbid games, Department of Economics at the University of Bergen, 2006

- [15] Rapoport, Amnon and Otsubo, Hironori and Kim, Bora and Stein, William E.: Unique bid auctions: Equilibrium solutions and experimental evidence, MPRA Paper 4185, University Library of Munich, Germany, Jul 2007.

- [16] J.Eichberger and D. Vinogradov, Least Unmatched Price Auctions : A First Approach, Discussion Paper Series 471, 2008

- [17] J. Eichberger, Dmitri Vinogradov: Lowest-Unmatched Price Auctions, International Journal of Industrial Organization, 2015, Vol. 43, pp. 1-17

- [18] J. Eichberger, Dmitri Vinogradov: Efficiency of Lowest-Unmatched Price Auctions, Economics Letters, 2016, Vol. 141, pp. 98?102

- [19] Erik Mohlin, Robert Ostling, Joseph Tao-yi Wang, Lowest unique bid auctions with population uncertainty, Economics Letters, Vol. 134, Sept. 2015, Pages 53-57.

- [20] Huang, G.Q., Xu, S.X., 2013. Truthful multi-unit transportation procurement auctions for logistics e-marketplaces. Transport. Res. Part B: Methodol. 47, 127-148.

- [21] Dong-Her Shih, David C. Yen, Chih-Hung Cheng, Ming-Hung Shih, A secure multi-item e-auction mechanism with bid privacy, Computers and Security 30 (2011) 273-287

- [22] Tembine H.: Distributed strategic learning for wireless engineers, Master Course, CRC Press, Taylor & Francis, 2012.

- [23] Harsanyi, J. 1973. Games with randomly disturbed payoffs: A new rationale for mixed strategy equilibrium points. Internat. J. Game Theory 2, 1-23.

- [24] Weibull, J., Evolutionary game theory, MIT Press, 1995.

- [25] Xin Luo, Hamidou Tembine: Evolutionary coalitional games for random access control, Annals of Operations Research, p1-34, 2016, DOI: 10.1007/s10479-016-2198-0

Author Information

Yida Xu received the B.Sc. degree in Electronic Information Engineering from Chongqing University and the M.S. degree in Information and Communication Engineering from Zhejiang University in China. He is a NYUAD Global Network Ph.D. candidate in the department of Electrical and Computer Engineering at New York University Tandon School of Engineering. His research interests include auction theory, game theory and machine learning.

Hamidou Tembine (S’06-M’10-SM’13) received the M.S. degree in Applied Mathematics from Ecole Polytechnique in 2006 and the Ph.D. degree in Computer Science from University of Avignon in 2009. His current research interests include evolutionary games, mean field stochastic games and applications. In December 2014, Tembine received the IEEE ComSoc Outstanding Young Researcher Award for his promising research activities for the benefit of the society. He was the recipient of 7 best article awards in the applications of game theory. Tembine is a prolific researcher and holds 150 scientific publications including magazines, letters, journals and conferences. He is author of the book on ”distributed strategic learning for engineers” (published by CRC Press, Taylor & Francis 2012), and co-author of the book ”Game Theory and Learning in Wireless Networks” (Elsevier Academic Press). Tembine has been co-organizer of several scientific meetings on game theory in networking, wireless communications and smart energy systems. He is a senior member of IEEE.