Semi-parametric Network Structure Discovery Models

Abstract

We propose a network structure discovery model for continuous observations that generalizes linear causal models by incorporating a Gaussian process (GP) prior on a network-independent component, and random sparsity and weight matrices as the network-dependent parameters. This approach provides flexible modeling of network-independent trends in the observations as well as uncertainty quantification around the discovered network structure. We establish a connection between our model and multi-task GPs and develop an efficient stochastic variational inference algorithm for it. Furthermore, we formally show that our approach is numerically stable and in fact numerically easy to carry out almost everywhere on the support of the random variables involved. Finally, we evaluate our model on three applications, showing that it outperforms previous approaches. We provide a qualitative and quantitative analysis of the structures discovered for domains such as the study of the full genome regulation of the yeast Saccharomyces cerevisiae.

1 Introduction

Networks represent the elements of a system and their interconnectedness as a set of nodes and arcs (connections) between them. Applications of network analysis range from biological systems such as gene regulatory networks and brain connectivity networks, to social networks and interactions between financial indices. Another application is modeling the relationship between property prices in different suburbs of a city, where each suburb is a node in the network and the property prices over time are the observations. In many such applications the structure of the network is unobserved and we wish to discover this structure from measurements Linderman & Adams (2014).

When dealing with continuous observations, a commonly used framework for this purpose is linear causal models (Bollen, 1989; Pearl, 2000; Spirtes et al., 2000), in which the data-generation process is defined such that the observations from each node are a linear sum of the observations from other nodes and additive noise. Such methods then use techniques such as independent component analysis (e.g. Spirtes et al., 2000) to recover the dependencies between the nodes.

An assumption in these models is that temporal variations in the observations from a node are either associated to the other nodes in the network, or to the changes in latent confounders; i.e., in the absence of any change in these two components, observations from a node are assumed to follow the noise distribution. However, one can assume that observations from a node can also follow a network-independent trend; for example property prices in a certain region can follow a decreasing/increasing trend over time, independent of other regions.

Main contribution. In this paper we propose a network structure discovery model that generalizes linear causal models in two directions. Firstly, it incorporates a network-independent component for each node, which is determined by a Gaussian process (GP) prior capturing the inter-dependencies between observations over time. Consequently, the output of a node is now given by a sum of the network-independent component and a (noisy) linear combination of the observations from the other nodes. Secondly, it considers the parameters of this linear combination, which ultimately determine the structure of the network, as random variables. These parameters are given by a binary adjacency matrix and a continuous weight matrix (similar in spirit to the work by Linderman & Adams, 2014), which allow for representing the sparsity and the strength of the connections in the network.

The practical advantage of this modeling approach is twofold. Firstly, because of the non-parametric nature of the Gaussian process prior, it provides a more flexible data-generation process, which also allows for network-independent trends in the observations. Secondly, by considering the network-independent component and the network-structure parameters as random variables, it enables the incorporation of probabilistic prior knowledge; a fully Bayesian treatment of the variables of interest; and uncertainty quantification around the discovered network structure.

Inference. In terms of inference in our model we show that, by marginalizing the latent functions corresponding to the network-independent components, our approach is closely related to multi-task GP models under a product covariance (Bonilla et al., 2008; Rakitsch et al., 2013). In particular, when conditioning on the network-dependent parameters, our model is a multi-task GP with a task-covariance constrained by the network parameters. This connection allows us to exploit properties of Kronecker products in order to compute the marginal likelihood (conditioned on the network parameters) efficiently. We estimate the posterior over the network-dependent parameters building upon recent breakthroughs in variational inference (Rezende et al., 2014; Kingma & Welling, 2014; Maddison et al., 2016), making our framework amenable to large-scale stochastic optimization.

Theoretical analysis. We investigate the numerical stability of our approach theoretically and discuss practical impacts. In particular, we show that all critical quantities of interests (i) can theoretically be sampled without assumptions, and (ii) can practically be computed “easily" almost everywhere in their respective supports. In doing so, we show that our approach makes somewhat weaker assumptions than previous work Linderman & Adams (2014).

Results. We investigate problems of discovering brain functional connectivity (brain), modeling property prices in Sydney (sydney), and understanding regulation in the yeast genome (yeast). We provide a qualitative analysis and a quantitative evaluation of our approach showing that in controlled scenarios such as brain, i.e. when the underlying network is constrained by a directed acyclic graph, our approach tends to outperform previous methods specifically designed for these settings. In more general settings of unconstrained networks such as sydney, we outperform previous work and show that our results are more realistic in discovering spatially-constrained trends. Finally, investigating the full yeast genome regulation (yeast), we find that even in a large network (up to 38,000,000+ arcs), our technique is able to recover both high-level and low-level prior knowledge and hints on original findings.

The rest of this paper is organized as follows: §2 states our model specifications, §3 presents the marginal likelihood given network parameters, §4 details variational inference in our model. §5 states our theory related to numerical stability, and §6 discusses related works. Finally, §7 presents our experiments, and a last section discusses and concludes. An appendix, (starting page 9) details all proofs and full experiments.

2 Model Specification

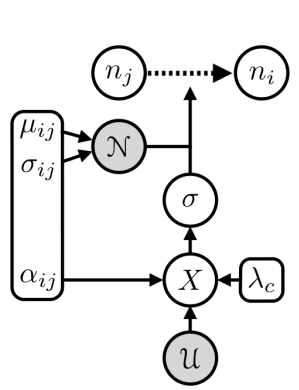

Given a dataset of vector-valued observations and their corresponding times from nodes in a network, our goal is to infer the existence and strength of the arcs between the nodes. To this end, let be the output of node at time ,

| (1) |

where is the observation-noise variance. To model latent function , we assume that it is generated by two sources: (i) a network-independent component, which is denoted by , and (ii) a network-dependent component, i.e., a weighted sum of the inputs received from the rest of the network:

| (2) | ||||

| (3) |

where represents the existence of an arc from node to node and determines the weight of the connection from node to node (assuming ). These are elements of the adjacency matrix and weight matrix , respectively, which we will refer to as network parameters. The network-independent component is drawn from a Gaussian process (GP; Rasmussen & Williams, 2005) with covariance function and hyperparameters . Since is non-parametric and are parametric components, we refer to the model above as a semi-parametric model.

2.1 Prior over Network Parameters

Eq. (1) defines the likelihood of our observations and eqs. (2) and (3) define the prior over the latent functions given the network parameters . As our goal is to infer the structure of the network, these parameters are also random variables and their prior is defined as:

| (4) | |||

| (5) |

where denotes a Bernoulli distribution with parameter .

2.2 Inference Task

Our main inference task is to estimate the posterior over the network parameters . To this end, by exploiting the closeness of GPs under linear operators, we will first show in §3 the exact expression for the (conditional) marginal likelihood obtained when marginalizing latent functions (eq. (6) below). Furthermore, by establishing a relationship of our model to multi-task learning (Rakitsch et al., 2013; Bonilla et al., 2008), we show how to compute this marginal likelihood efficiently. Subsequently, due to the highly nonlinear dependence of on , we will approximate the posterior over these network parameters using variational inference in §4.

3 Marginal Likelihood Given Network Parameters

Let us denote the values of all latent functions at time with , and similarly . Hence, we can rewrite eq. (2) as:

| (6) |

where is Hadamard product. We refer the model in eq. (6) as the inverse model. Using this inverse model, we can see now that, for fixed , since all the distributions are Gaussians and we are only applying linear operators, the resulting distribution over , and consequently over , is also a Gaussian process. Hence, we only need to figure out the mean function and the covariance function of the resulting process. Below we present the main results and leave the details of the derivations to the appendix.

Let and define the following intermediate matrices (which are a function of the network parameters):

| (7) | |||||

| (8) |

Then we have that the mean function and covariance function of latent process are given by:

| (9) | ||||

| (10) |

where denotes the entry of matrix .

Consequently, the distribution of the noisy process is also a Gaussian process and can be further understood by assuming synchronized observations, i.e. that the observations for all nodes lie on a grid in time, . Let be the matrix of observations and define , where takes the columns of the matrix argument and stacks them into a single vector. Therefore, the log-marginal likelihood conditioned on the network parameters is given by ( is Kronecker product):

| (11) | ||||

| (12) |

where ; is the covariance matrix induced by evaluating the covariance function at all observed times; and are defined as in eqs. 7, 8; and is the total number observations.

3.1 Relationship with Multi-task Learning

Remarkably, the marginal likelihood of the model described in eqs. (11) and (12) reveals an interesting relationship with multi-task learning when using Gaussian process priors. Indeed, it boils down to the marginal likelihood of multi-task GP models under a product covariance (Bonilla et al., 2008; Rakitsch et al., 2013).

In our case, the nodes in the network can be seen as the tasks in a multi-task GP model and are associated with a task-dependent covariance , which is fully determined by the parameters of the network . This contrasts with multi-task models where is, in general, a free parameter (Bonilla et al., 2008). Similarly, the input covariance is the covariance of the observation times.

Finally, conditioned on , our model’s marginal likelihood exhibits a more complex noise covariance , which depends strongly on the network parameters. Such a covariance structured was not studied by Bonilla et al. (2008), as they considered only diagonal noise-covariances. However, Rakitsch et al. (2013) did consider the more general case of Gaussian systems with a covariance given by the sum of two Kronecker products. In the following section, we exploit their results in order to compute, for fixed , the marginal likelihood of our model.

3.2 Computational efficiency

In this section we show an efficient expression for the computation of the log-marginal likelihood in eq. (11). For simplicity, we consider the synchronized case where all the nodes in the network have observations at the same times and, as before, we denote the total number of observations with . The main difficulties of computing the log-marginal likelihood above are the calculation of the log-determinant of an dimensional matrix, as well as solving an -dimensional system of linear equations. Our goal is to show that we never need to solve these operations on an -dimensional matrix, which are but instead use operations. The results in this section have been previously shown by Rakitsch et al. (2013) for covariances with a sum of two Kronecker products.

We show our derivations in the appendix and present the results specific to our model here. To give some intuition behind such derivations, the main idea is to “factor-out" the noise matrix from the covariance matrix and then apply properties of the Kronecker product. Hence, given the following matrix definitions along with their eigen-decompositions:

the log-determinant term in eq. (11) is given by

| (13) |

and the quadratic term can be computed as:

| (14) |

where , and is the eigen-decomposition of .

We see that the above computations only require the eigen-decomposition of the matrix and the matrix , while avoiding matrix operations on the whole matrix of covariances .

4 Variational Inference

Having marginalized the latent functions corresponding to the network-independent component, our next step is to use variational inference to approximate the true posterior with a tractable family of distributions that factorizes as

| (15) |

where , and . Following the variational-inference desiderata we aim to optimize the variational objective, so-called evidence lower-bound (), which is given by:

| (16) | ||||

| (17) | ||||

| (18) |

where denotes the Kullback-Leibler divergence between distributions and , and is the prior over the network-dependent parameters as defined in eqs. 4 and 5.

Given a specification of the approximate posteriors , our goal is to maximize wrt their corresponding parameters. While computing and its gradients is straightforward, we note that requires expectations of the log conditional likelihood, which depends on in a highly-nonlinear fashion. Fortunately, we can address this issue by exploiting recent advances in variational inference with regards to large-scale optimization of stochastic computation graphs (Rezende et al., 2014; Kingma & Welling, 2014; Maddison et al., 2016; Jang et al., 2016).

4.1 The Reparameterization Trick

The main challenge of dealing with in the optimization of the variational objective is that of devising low-variance unbiased estimates of its gradients using, for example, Monte Carlo sampling. This can be overcome by re-parametrizing as a deterministic function of its parameters and a fixed-noise distribution. Such an approach has come to be known as the reparametrization trick (Kingma & Welling, 2014) or stochastic back-propagation Rezende et al. (2014). Hence we can define our approximate posterior over as:

| (19) |

which can be reparametrized easily as a function of a standard normally-distributed variable , i.e. .

4.1.1 The Concrete Distribution

In order to define our approximate posteriors over we face the additional challenge that the reparametrization trick cannot be applied to discrete distributions Kingma & Welling (2014). We address this problem by using a continuous relaxation of discrete random variables known as the Concrete distribution (Maddison et al., 2016). We note that, contemporary to the Concrete distribution, a similar approach has been proposed by Jang et al. (2016) and it is also known as the Gumble-Softmax trick.

The main idea of this trick is to replace the discrete random variable with their continuous relaxation, which is simply obtained by taking the softmax of logits perturbed by additive noise. Interestingly, in the zero-temperature limit the Concrete distribution corresponds to its discrete counterpart. More importantly, this continuous relaxation has a closed-form density and a simple reparameterization. For our purposes, we focus on using the Concrete distribution corresponding to the Bernoulli case for , i.e. , and show how we sample from it using its reparameterization:

| (20) | ||||

| (21) | ||||

| (22) |

where are variational parameters and is a constant.

4.1.2 Preservation of the Variational Lower-Bound

As pointed out by Maddison et al. (2016), optimization of now implies replacing all discrete variables with their Concrete versions using the relaxation described above. This means that we also relax our priors using the same procedure. Furthermore, in order to preserve the evidence-lower-bound nature of the variational objective, we need to match the log-probabilities in with their sampling distribution. For the approximate posterior these are given by:

| (23) |

and similarly for .

Having relaxed our discrete variables, we proceed with optimization of the in eq. (16) by using Monte Carlo samples from to estimate . For computing we use samples from and their log-probabilities as defined in eq. (23). Finally, for we use the analytical form for the KL-divergence between two Gaussians.

5 Numerical Stability

Because is straightforward to compute, we investigate the numerical impact of computing . We first show that we get samplability “for free" — i.e., compared to other sophisticated methods whose formal operating regime calls for additional assumptions Hyvärinen & Smith (2013); Linderman & Adams (2014); Shimizu et al. (2011).

Theorem 1

For any parameterization of the concrete distributions ( and ()), is non-singular with probability one.

Theorem 2

For any parameterization of the concrete distributions ( and ()) and any , with probabiliy one for any .

(Proofs in appendix, §9.1, §9.2.) Therefore, it also holds that is finite. The proofs build upon a trivial but key feature of concrete distributions: they can be designed so as not to break absolute continuity of their input densities.

Under specific assumptions, reminiscent to those of Hyvärinen & Smith (2013); Linderman & Adams (2014), we show that can be sandwiched in a precise interval which makes its computation numerically easy almost everywhere on its support, i.e. sampling may have little chance of local non-zero measure falling under machine zero (with the potential trouble when inverting relevant matrices). Most importantly, this holds for a sampling model (M) which is more general than ours, meaning that one could make different choices from the concrete distributions we use and yet keep the same property:

-

()

() (i) weight is picked as (), and (ii) adjacency is picked as with , where is any random variable with support in (letting ).

We define the total (squared) expected input (resp. output) to node as (resp. ), and the total input (resp. output) variance as (resp. ). We also define averages, , (same for outputs), and biased weighted proportions, , (again, same for outputs). Finally, we define two functions as:

For any diagonalizable , denotes its eigenspectrum, and , .

Theorem 3

Fix any constants and and let and . Under sampling model , suppose that

| (26) |

If is larger than some constant depending on and , then with probability over the sampling of and , we have that .

(Proof in appendix, §9.3.) To be non empty, the interval puts the implicit constraint that for some constant , i.e. roughly, the expected square signal (node-wise) has to be bounded. Such a bound in the signal’s statistics or values is an assumption that can be found in Hyvärinen & Smith (2013); Linderman & Adams (2014). As a corollary, if the kernel () or noise parameters () are, say, above machine zero, there is reduced risk for numerical instabilities in sampling .

Corollary 4

6 Related Work

Linear causal models with Gaussian noise (e.g. Bollen, 1989; Pearl, 2000) are different from ours in three key aspects: (i) they assume that the underlying network is a directed acyclic graph (e.g. Spirtes et al., 2000); (ii) they do not represent the connection strengths using random matrices; and (iii) they do not incorporate the network-independent Gaussian process component. Unlike our work, other approaches assume a non-Gaussian additive noise (Shimizu et al., 2006) or a nonlinear transformation of the network-dependent component (Hoyer et al., 2009).

As observations in our model are generated from several latent Gaussian processes, our framework is related to GP latent variable models (Lawrence, 2005; Zhang et al., 2010). However, our goal is to recover the underlying network structure, instead of carrying out dimensionality reduction or predicting observations for the nodes. On a different vein, our use of random matrices representing network structure is similar to the model in Linderman & Adams (2014), but that model is focused on point-process data rather than continuous-valued observations. Finally, with regards to multi-task GP models Bonilla et al. (2008); Rakitsch et al. (2013) and more general frameworks for modeling vector-valued outputs (Wilson & Ghahramani, 2010), other approaches have considered Bayesian inference in multi-task learning subject to specific constraints, such as rank constrains (Koyejo & Ghosh, 2013). However, their work is mostly focused on dealing with the problem of large-dimensionality data instead of network discovery.

7 Experiments

We evaluate our approach on three distinct domains: discovering brain functional connectivity (brain), modeling property prices in Sydney (sydney) and regulation in the yeast genome (yeast). We used the squared exponential covariance function and optimized variational parameters, hyperparameters, and likelihood parameters in an iterative fashion using Adam Kingma & Ba (2014). For details of prior setting and optimization specifics see the appendix.

7.1 Methods compared

We considered the methods used in Peters et al. (2014) as baselines for comparison. These include: (1) pc algorithm (Spirtes et al., 2000); (2) Conservative pc algorithm denoted by cpc (Ramse et al., 2006); and (3) lingam (Shimizu et al., 2006); In addition to the above, we considered two more algorithms: (4) iamb Tsamardinos et al. (2003), and (5) Pairwise LiNGAM (pw-lingam), which has been recently developed for discovering connectivity between different brain regions Hyvärinen & Smith (2013). For the reasons detailed in the appendix other methods used in Peters et al. (2014) were not applicable to the datasets analyzed here.

7.2 brain domain

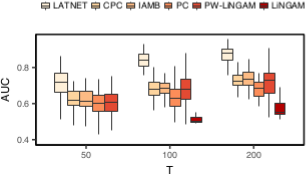

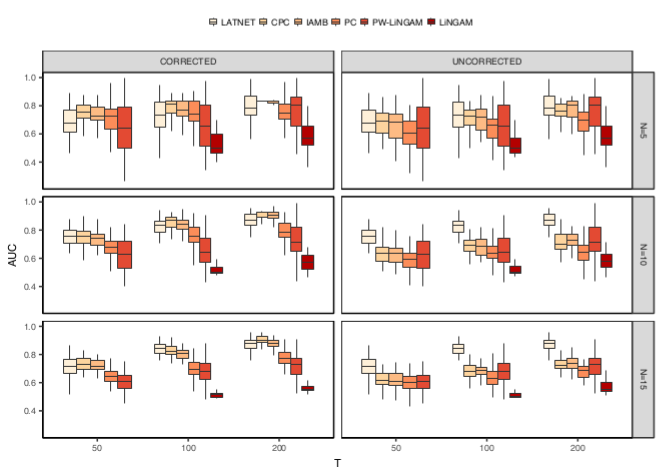

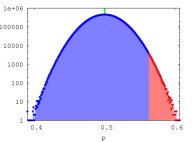

The aim is to discover the connectivity between different brain regions is crucial in neuroscience studies. We analyze the benchmarks of Smith et al. (2011), in which the activity of different brain regions is recorded at different time points and the aim is to find which brain regions are connected to each other. Each benchmark consists of data from 50 subjects, each consisting of 200 time points (). We used network sizes , and the true underlying connectivity network is a directed acyclic graph (DAG). Networks discovered by latnet are not restricted to DAGs, and therefore baseline methods assuming the underlying network is a DAG have a de facto favorable bias.

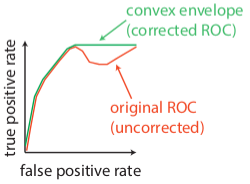

Results are evaluated using the area under the ROC curve (AUC) and shown in Figure 1 for using box-plots (top and bottom edges of the box correspond to the first and third quartiles respectively). The appendix (§10.2) presents details on how the AUC is computed for the different methods and the results for . We see that, although other methods are favorably biased about the underlying structure, latnet provides significantly better performance than such baselines. We note that lingam was unable to perform inference for small and its output is reported only for . We also note that pc, cpc and iamb may generate non-concave ROCs. Curves can be post-processed for concave envelopes which improves the AUC, but this artificial post-processing that equivalently mixes outputs does not guarantee the existence of parameters that will in effect produce networks with the corresponding performances. This is discussed in the appendix §10.2, along with the results with concavification.

.

7.3 sydney domain

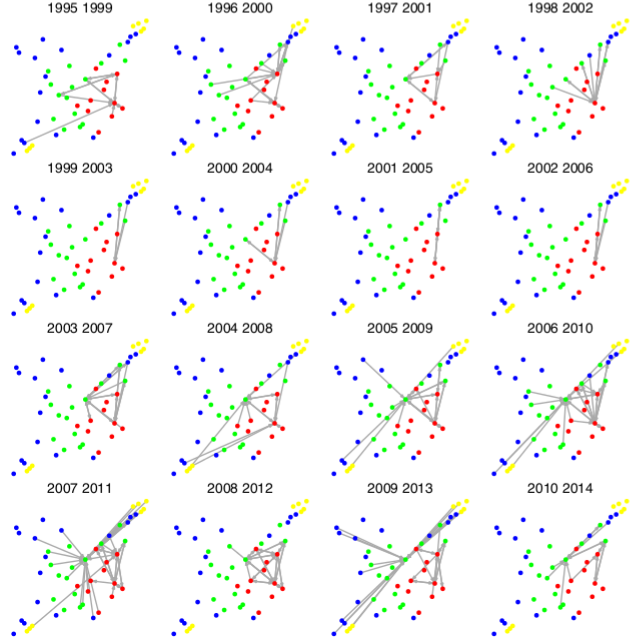

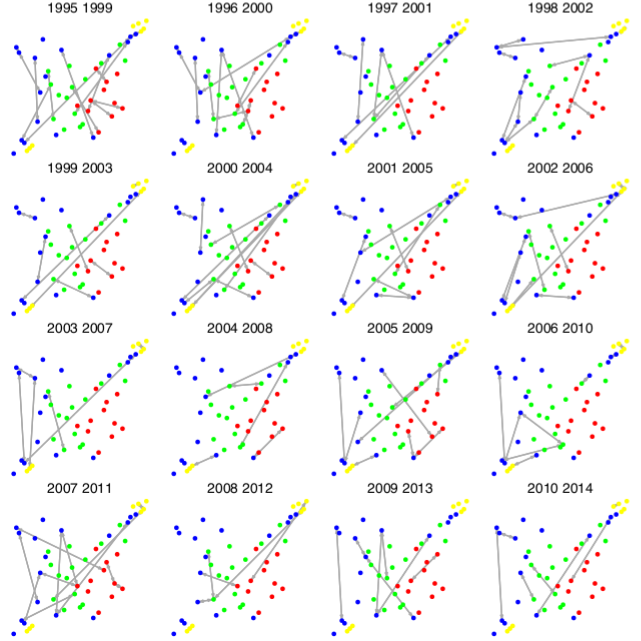

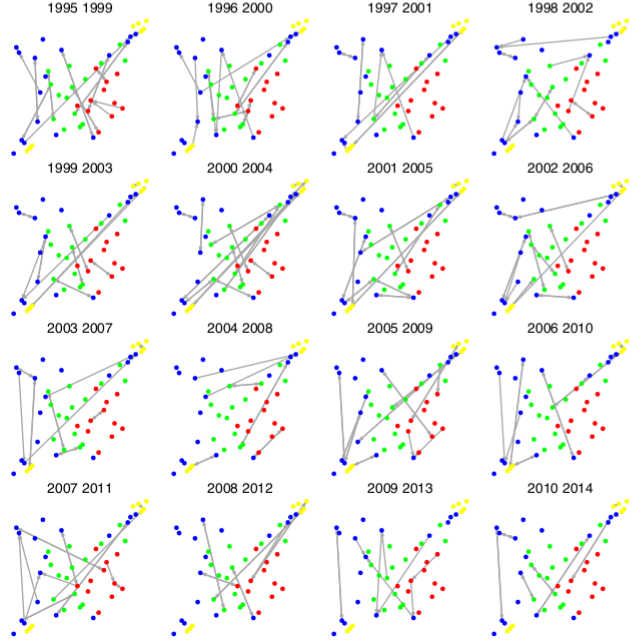

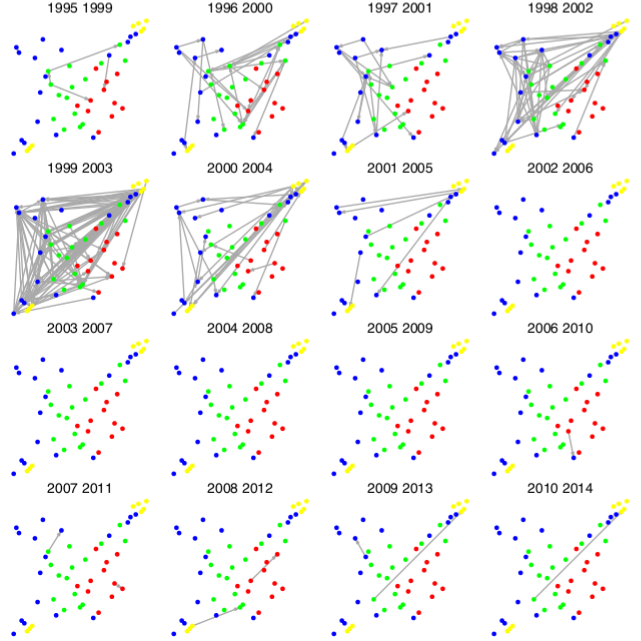

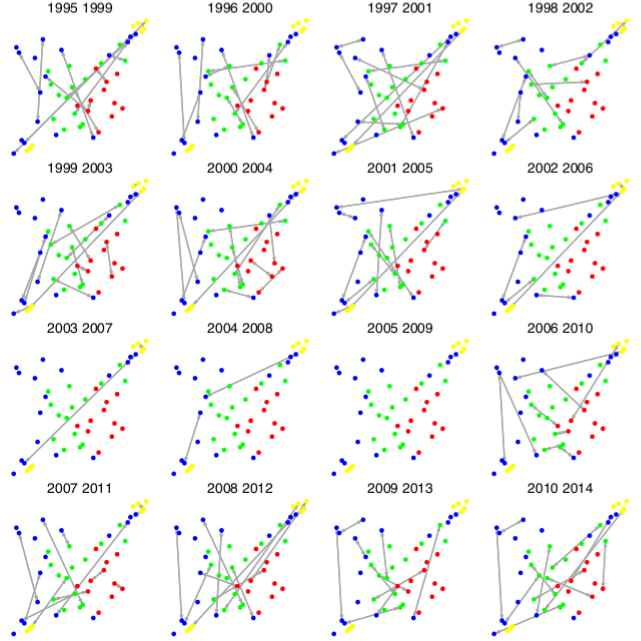

The aim is to discover the relationship between property prices in different suburbs of Sydney. The data includes quarterly median sale prices for 51 suburbs in Sydney and surrounding area from 1995 to 2014. We kept the analysis window to five years ( since data is quarterly) and starting from 1995–1999 the window is shifted by one year each time until 2010-2014. Some major patterns are expected, like the presence of hubs or authorities related to mass transfers between suburbs.

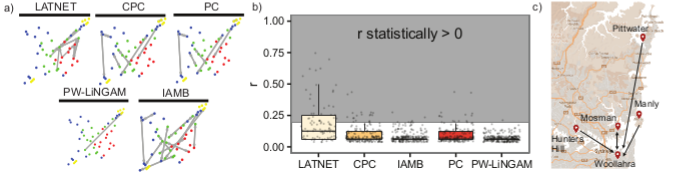

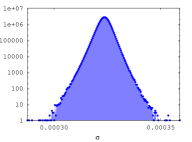

Figure 2(a) shows the inferred arcs for years 2010-2014, where the nodes are positioned according to their geographical locations. See the appendix for the full map of the discovered arcs for all years and for details of the thresholds used for finding significant arcs. We see that the network discovered by latnet is more regionally localized compared to the other methods, and displays major authorities. Note that lingam was unable to perform inference. To complete with a quantitative analysis, we computed for each algorithm and for each pair of nodes, the proportion of networks in which an arc was discovered. Then, we computed a distribution of the values in the networks, emphasizing the “stable” arcs with statistically (risk ). Figure 2(b) shows the values for the different methods. Less than , of pc and cpc arcs were significant, respectively, while more than 29 of latnet arcs are significant. Interestingly, iamb and pw-lingam did not find significant arcs.

What turns out to be interesting is the actual arcs found for those in the 29 that represent the highest -values. Figure 2(c) shows the top-6 of these arcs inferred by latnet. They clearly indicate that one area of Sydney, Woollahra, acts like an authority in the network, since it receives lots of arcs from other major areas (Hunters Hill, Manly, Mosman, Pittwater). These areas all share common features: they are in central-north Sydney, all have coastal areas, and they happen to be well-known prestigious areas with the highest median property price in Sydney Campion (2011), so the observed percolation is no surprise.

7.4 yeast domain

|

|

|

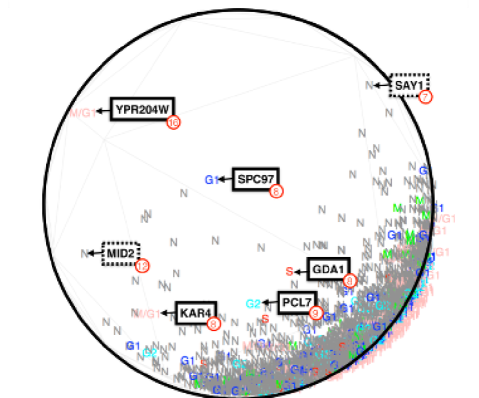

The aim is to infer genome regulation patterns for one extensively studied species, (Saccharomyces cerevisiae, Spellman et al., 1998)’s. In numbers, this represents 100,000+ data points and a network with up to 38,000,000+ arcs. Biology tells us that this network is directed. The complete set of experiments and results is available in the appendix, §10.3. In addition to the full genome analysis, we have performed a finer grained analysis on a tenth known to be involved in a heavily regulated and key part of the yeast’s life, the yeast cell cycle (YCC). These genes are the so-called sentinels of the YCC Spellman et al. (1998). In each experiments, we have scrutinized the subset of strong arcs, for which both () and () are large, that is, in top-, in top-. These arcs happen to be indeed very significant, with risk for the rejection of hypothesis that is not larger than random existence (). The discovered networks’ information is far beyond the scope of this paper, but some striking points can be noted, taking as references the cell cycle transcriptionally regulated genes (Rowicka et al., 2007) and http://www.yeastgenome.org as a more general resource.

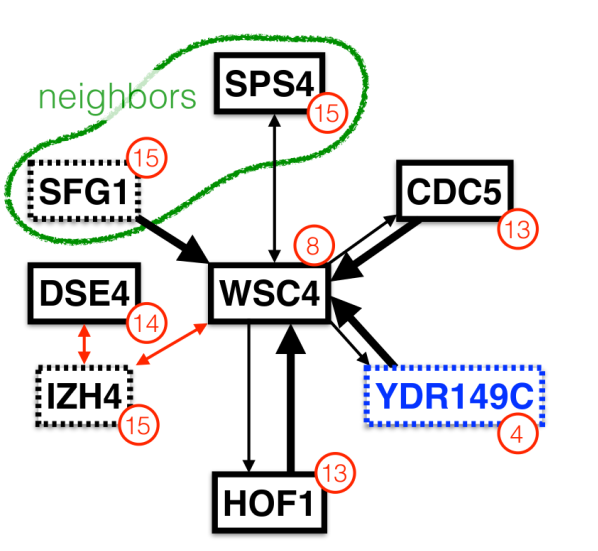

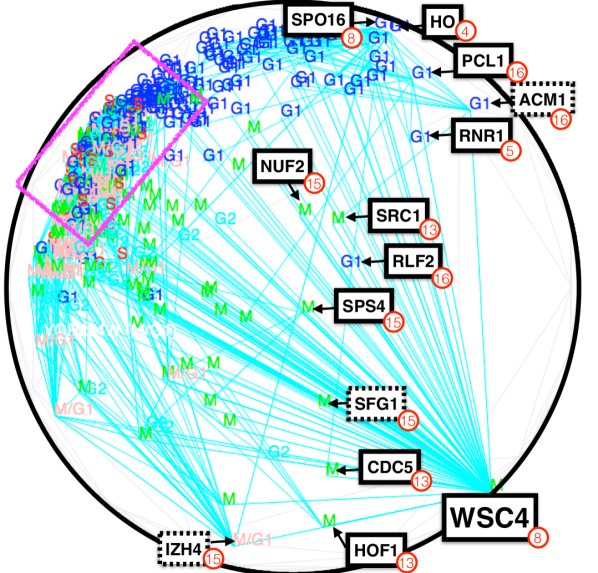

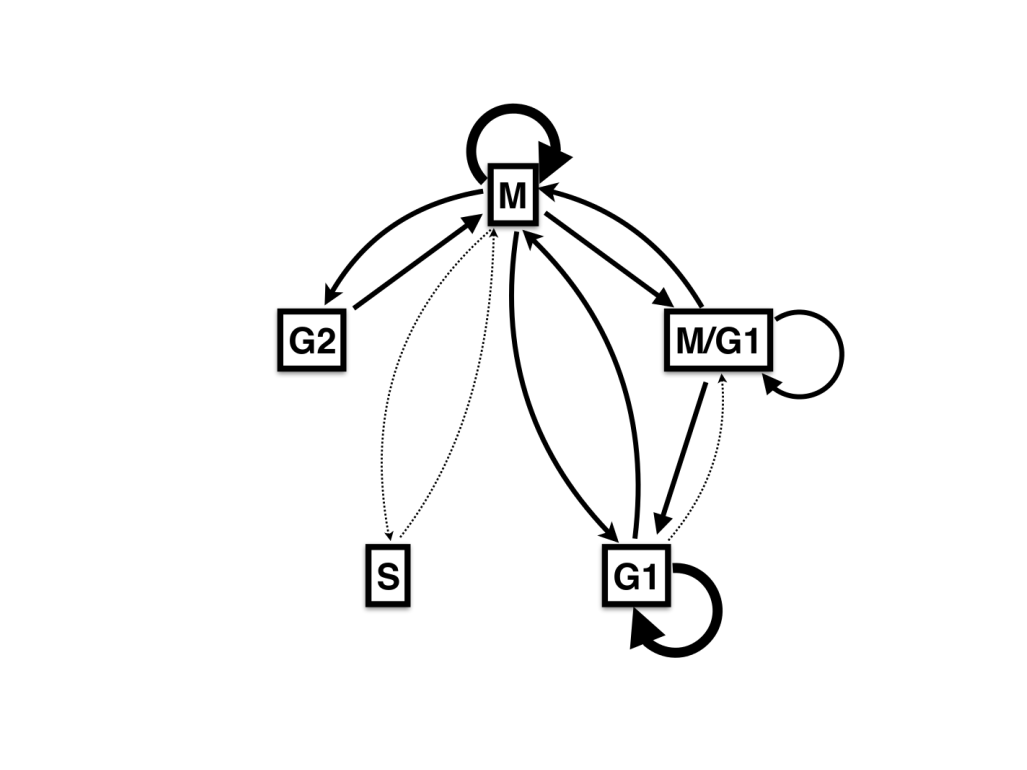

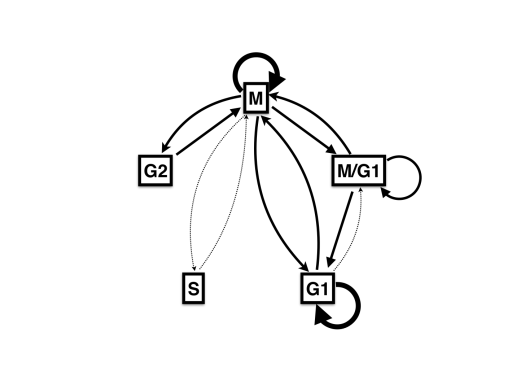

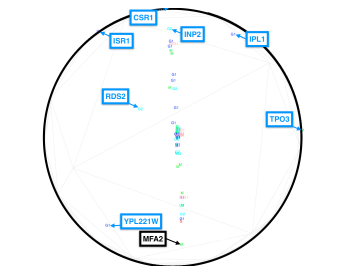

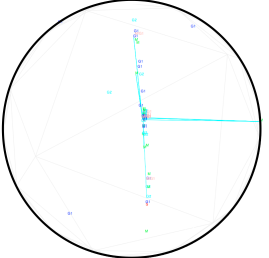

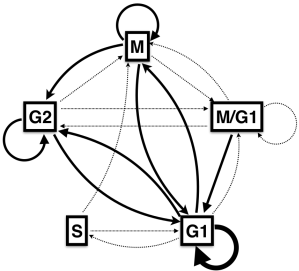

Analysis of the YCC. Figure 3 summarizes qualitatively the results obtained by latnet. The topmost strong arcs belong to a small connected component () organized around gene WSC4, asymmetric (both in terms of arcs and values) and with apparent patterns of positive / negative regulation (sign of ). The key genes are involved in the cell structure dynamics (DSE4, WSC4, CDC5, HOF1). The IZH4 arcs with negative are perhaps not surprising: WSC4 and DSE4 are involved into cell walls (integrity for the former, degradation for the latter). IZH4 is a man-in-the-middle: it has activity elevated in zinc deficient cells, and it turns out that zinc is crucial for hundreds of enzymes, e.g. for protein folding. Strikingly, SPS4 and SFG1 happen to be neighbors on the same chromosome. Figure 3 (center) shows the broad picture, with a display of the manifold coordinates induced by the network’s graph, built upon Meila & Shi (2001). It displays that a small number of key genes drive the coordinates. Most of these genes have been pinned down as cell cycle transcriptionally regulated (Rowicka et al., 2007), and they essentially turn out to be heavily involved in both a/sexual reproduction. Last, Figure 3 (right) summarizes the broad picture of strong arcs between YCC phases: it should come at no surprise that cell splitting, (M)itosis, has the largest number of these arcs.

Analysis of the full genome (results in appendix, 10.4). The following patterns emerge: first, the network is highly asymmetric: more than twice strong arcs go outside the YCC compared to arcs coming in the YCC from non-YCC genes. Second, the leading YCC genes are still major genes, but they tend to be outnumbered by genes that are perhaps more “all-purpose”. Last, the predominance of gap phase G1 compared to G2 is in fact a known feature of Saccharomyces cerevisiae (compared to other yeast species such as Saccharomyces pombe).

8 Conclusion & Discussion

We introduced a framework for network structure discovery when continuous-valued observations from the nodes are given, which can be seen as a generalization of linear causal models. We have established an interesting connection of the model with multi-task learning and developed an efficient variational inference method for estimating the posterior distribution over the network structure. We have demonstrated the benefits of our approach on real applications by providing qualitative and quantitative analyses. Besides computational efficiency, our theoretical analysis shows that the traditional constraints for numerical stability and identifiability in networks are alleviated. Indeed, from a theoretical standpoint, the state of the art goes with substantial constraints that can be related to the fact that the true model exists, is unique and can be properly recovered. Such constraints go with an abstraction of the dynamical model that looks like a series of the type , where symbolizes discrete time and can be a real, complex or matrix argument Hyvärinen & Smith (2013); Linderman & Adams (2014). The trick of replacing the analysis overall s by one over a window, rather than alleviating the constraint, substitutes it for other stationarity constraints that can be equally restrictive Shimizu et al. (2006). In our case, such constraints do not appear because time is absorbed in a GP. The finiteness of the evidence lower-bound (ELBO) is essentially obtained “for free". What we get with additional assumptions that parallel traditional ones is a non-negligible uplift in the easiness of the expected log-likelihood part, the bottleneck of the ELBO. This result also holds for a broader class of posteriors than the ones we use, opening interesting avenues of applications for concrete distributions.

Finally, experiments display that latnet is able to perform sound inference already on small domains, and scales to large domains with the ability to pinpoint meaningful local properties of the networks, as well as capture important high-level network features like global patterns of emigration between wealthy suburbs in Sydney or species characteristics for the yeast.

References

- Abramowitz & Stegun (1964) Abramowitz, M. and Stegun, I.-A. Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables. U. S. Government Printing Office, 1964.

- Bollen (1989) Bollen, K.-A. Structural equations with latent variables. John Wiley & Sons, 1989.

- Bonilla et al. (2008) Bonilla, E.-V., Chai, K.-M. A, and Williams, C.-K.-I. Multi-task Gaussian process prediction. In NIPS, 2008.

-

Campion (2011)

Campion, Vikki.

http://www.dailytelegraph.com.au/

archive/money/property-prices-in-sydneys-traditional-blue-collar-suburbs-are-booming-with-cabramatta-best-performing-residex-reports/news-story/6971cf79862fdf4f2b3fea3cf2917b5f, 2011. - Chickering (2002) Chickering, D.-M. Optimal structure identification with greedy search. Journal of machine learning research, 3(Nov):507–554, 2002.

- Cho et al. (1998) Cho, R.-J., Campbell, M.-J., Winzeler, E.-A., Steinmetz, L., Conway, A., Wodicka, L., Wolfsberg, T.-G., Gabrielian, A.-E., Landsman, D., Lockhart, D.-J., and Davis, W. A genome-wide transcriptional analysis of the mitotic cell cycle. Molecular Cell, 2:65–73, 1998.

- Hoyer et al. (2009) Hoyer, P.-O., Janzing, D., Mooij, J.-M., Peters, J., and Schölkopf, B. Nonlinear causal discovery with additive noise models. In NIPS, 2009.

- Hyvärinen & Smith (2013) Hyvärinen, A. and Smith, S.-M. Pairwise likelihood ratios for estimation of non-Gaussian structural equation models. JMLR, 14:111–152, 2013.

- Jang et al. (2016) Jang, E., Gu, S., and Poole, B. Categorical reparameterization with gumbel-softmax. arXiv:1611.01144, 2016.

- Kalisch et al. (2012) Kalisch, M., Mächler, M., Colombo, D., Maathuis, M.-H., and Bühlmann, P. Causal inference using graphical models with the R package pcalg. Journal of Statistical Software, 47(11):1–26, 2012.

- Kingma & Ba (2014) Kingma, D.-P. and Ba, J. Adam: A Method for Stochastic Optimization. arXiv:1412.6980, 2014.

- Kingma & Welling (2014) Kingma, D.P. and Welling, M. Auto-Encoding Variational Bayes. In The International Conference on Learning Representations (ICLR), 2014.

- Koyejo & Ghosh (2013) Koyejo, O. and Ghosh, J. Constrained bayesian inference for low rank multitask learning. In UAI, 2013.

- Lawrence (2005) Lawrence, N. Probabilistic non-linear principal component analysis with Gaussian process latent variable models. JMLR, 6:1783–1816, 2005.

- Linderman & Adams (2014) Linderman, S.-W. and Adams, R.-P. Discovering Latent Network Structure in Point Process Data. In ICML, 2014.

- Maddison et al. (2016) Maddison, C.-J., Mnih, A., and Teh, Y.-W. The Concrete Distribution: A Continuous Relaxation of Discrete Random Variables. arXiv:1611.00712, 2016.

- Marco (2010) Marco, S. Learning Bayesian networks with the bnlearn R package. Journal of Statistical Software, 35(3), 2010.

- Meek (1997) Meek, C. Graphical Models: Selecting causal and statistical models. PhD thesis, PhD thesis, Carnegie Mellon University, 1997.

- Meila & Shi (2001) Meila, M. and Shi, J. Learning segmentation by random walks. In NIPS, volume 14, 2001.

- Pearl (2000) Pearl, J. Causality: Models, Reasoning, and Inference. Cambridge University Press, New York, NY, USA, 2000. ISBN 0-521-77362-8.

- Peters et al. (2014) Peters, J., Mooij, J.-M., Janzing, D., and Schölkopf, B. Causal discovery with continuous additive noise models. JMLR, 15(1):2009–2053, 2014.

- Rakitsch et al. (2013) Rakitsch, B., Lippert, C., Borgwardt, K., and Stegle, O. It is all in the noise: Efficient multi-task Gaussian process inference with structured residuals. In NIPS, 2013.

- Ramse et al. (2006) Ramse, J, Zhang, J., and Spirtes, P. Adjacency-faithfulness and conservative causal inference. In Uncertainty in Artificial Intelligence (UAI), 2006.

- Rasmussen & Williams (2005) Rasmussen, C.-E. and Williams, C.-K.-I. Gaussian Processes for Machine Learning (Adaptive Computation and Machine Learning). The MIT Press, 2005. ISBN 026218253X.

- Rezende et al. (2014) Rezende, D.-J., Mohamed, S., and Wierstra, D. Stochastic backpropagation and approximate inference in deep generative models. In ICML, pp. 1278–1286, 2014.

- Rowicka et al. (2007) Rowicka, M., Kudlicki, A., Tu, B.-P., and Otwinowski, Z. High-resolution timing of cell cycle-regulated gene expression. PNAS, 104(43):16892–16897, 2007.

- Santoni et al. (2013) Santoni, D., Castiglione, F., and Paci, P. Identifying correlations between chromosomal proximity of genes and distance of their products in protein-protein interaction networks of yeast. PLoS ONE, 8, 2013.

- Shimizu et al. (2006) Shimizu, S., Hoyer, P.-O., Hyvärinen, A., and Kerminen, A. A linear non-Gaussian acyclic model for causal discovery. JMLR, 7:2003–2030, 2006.

- Shimizu et al. (2011) Shimizu, S., Inazumi, T., Sogawa, Y., Hyvärinen, A., Kawahara, Y., Washio, T., Hoyer, P.-O., and Bollen, K. DirectLiNGAM: A direct method for learning a linear non-gaussian structural equation model. JMLR, 12:1225–1248, 2011.

- Simon et al. (2001) Simon, I., Barnett, J., Hannett, N., Harbison, C.-T., Rinaldi, N.-J., Volkert, T.-L., Wyrick, J.-J., Zeitlinger, J., Gifford, D.-K., Jaakkola, T.-S., and Young, R.-A. Serial regulation of transcriptional regulators in the yeast cell cycle. Cell, 106:697–708, 2001.

- Smith et al. (2011) Smith, S.-M., Miller, K.-L., Salimi-Khorshidi, G., Webster, M., Beckmann, C.-F., Nichols, T.-E., Ramsey, J.-D., and Woolrich, M.-W. Network modelling methods for FMRI. NeuroImage, 54(2):875–891, 2011.

- Spellman et al. (1998) Spellman, P.-T., Sherlock, G., Zhang, M.-Q., Iyer, V.-R., Anders, K., Eisen, M.-B., Brown, P.-O., Botstein, D., and Futcher, B. Comprehensive identification of cell cycle-regulated genes of the yeast Saccharomyces cerevisiae by microarray hybridization. Molecular Biology of the Cell, 9:3273–3297, 1998.

- Spirtes et al. (2000) Spirtes, P., Glymour, C.-N., and Scheines, R. Causation, prediction, and search. MIT press, 2000.

- Tao (2008) Tao, T. Singularity and determinant of random matrices, 2008. Lewis Memorial Lecture.

- Tsagris et al. (2014) Tsagris, M., Beneki, C., and Hassani, H. On the folded normal distribution. Mathematics, 2:12–28, 2014.

- Tsamardinos et al. (2003) Tsamardinos, I., Aliferis, C.-F., Statnikov, A. R, and Statnikov, E. Algorithms for Large Scale Markov Blanket Discovery. In FLAIRS, volume 2, 2003.

- Vu (2014) Vu, V.-H. Modern Aspects of Random Matrix Theory. Proceedings of Symposia in Applied Mathematics. American Mathematical Society, 2014.

- Wilson & Ghahramani (2010) Wilson, A.-G. and Ghahramani, Z. Generalised wishart processes. In UAI, 2010.

- Zhang et al. (2010) Zhang, K., Schölkopf, B., and Janzing, D. Invariant Gaussian Process Latent Variable Models and Application in Causal Discovery. In UAI, 2010.

9 Proofs and algorithms

9.1 Proof of Theorem 1

|

Theorem 5

For any and (), is non-singular with probability one.

Proof:

Denote for short . The proof is split in three

cases, (I) and , (II)

and , and finally

(III) and .

(Case I: , ) The coordinates take on constant values on the diagonal

(), and random values outside the diagonal

(). The density of equals , where and with

| (27) |

and is uniform on interval (Maddison et al., 2016). The proof that is invertible adapts a standard argument (for example, Tao (2008)). For any111Whenever , is always invertible. , denote the columns of , that is, . Each of them can be thought of as a random vector where one coordinate takes value 1 with probability 1, an this coordinate is different for all vectors. is non invertible iff is linearly dependent. Remark that none of the s can be the null vector, so if is not invertible, then

| (28) |

As a consequence,

| (29) |

where the distribution is the product distribution over the columns of . Fix any belonging to the respective supports of the columns, and let

| (30) |

Because the uniform and normal distributions are both absolutely continuous with respect to Lebesgue measure and (it is also Lipschitz) for any , so is the density of for any , and thereby the density of for any . Along with the fact that has strictly positive codimension for any , it comes

| (31) |

Integrating over the choices of , we get and so from ineq. (29). As a consequence, is non-singular with probability

one, as claimed.

(Case II: , ) this boils down to

choosing a Bernoulli

distribution over , corresponding to the limit case

with (Maddison et al., 2016):

| (32) |

In this case, the distribution of is not

absolutely continuous but a trick allows to truncate the distribution

on a subset over which it is absolutely continuous, and therefore

reduce to Case I to handle it.

The only atom eventually having non-zero

probability is the canonical

basis vector , which has probability to be sampled. We now perform a sequence of recursive row-column

(row followed by column or the reverse)

permutations, starting on , which by definition do not change its

invertibility status but only the sign of its determinant. The first

row-column permutation is carried out in such a way that the first

column of the new matrix, , is the first canonical

basis vector, . We then repeat this operation to have the

second canonical basis vector in the second column, and so on until

until it cannot

be done anymore to make appear on the left block a new canonical basis

vector. Assuming we have done sequences, we obtain from

the final matrix with:

| (35) |

Here, . Now, we are going to carry out again, but on the lower-right block, . Removing dimension-dependent indexes, we obtain matrix

| (38) | |||||

| (43) |

We then keep on doing the same transformation on block until it is not possible anymore. When it is not possible anymore, we know that the current submatrix, say , does not contain any canonical basis vector as column, as depicted in Figure 5.

|

Lemma 6

.

Proof: We proceed by induction. The key observation is the following standard linear algebra identity. Denoting with a single index the order of a general square matrix, like , we have for any non-singular,

| (52) |

for any . Taking determinants, we note that because they are triangular with unit diagonal, and so

| (57) | |||||

| (58) |

because the right hand-side in eq. (57) is block

diagonal. Matching the left hand-side of eq. (57) with

eq. (35), so putting and , we obtain , and therefore

. We then

just recursively use eq. (52) on the lower-right block

(, for ) and get the

statement of the Lemma.

(End of the proof of Lemma 6).

So, is invertible iff is invertible and:

| (59) | |||||

where is the property that no column of

is a canonical basis vector.

Notice the change: no column in is allowed

to be a canonical basis vector, and therefore the support for the

density of the columns of is such that its

distribution is now absolutely continuous. We are thus left with the

same case as in Case I, which yields , and brings

as well.

(Case III: , for some

) Remark that if , and if ,

this boils down from Case II (eq. (32)) to

choosing a Bernoulli

distribution over , so both cases coincide with being

chosen as , implying . We are left with the same

transformation as in Case II — the main difference being that some

is surely zero, but it changes nothing to the reasoning done

in case II. Therefore, again.

9.2 Proof of Theorem 2

It comes from Theorem 1 that can always be computed with probability

one with respect to the random sampling of , and there is no

constraint on the parameterization of the concrete distribution for

invertibility (Maddison et al., 2016). Interestingly perhaps, the story would be

completely different for the invertibility of , as the argument

for cases (II) and (III) break down because with

positive probability that would be easy to lower-bound, would in

fact be not invertible.

The important consequence of Theorem 5 relies on the computation of the log likelihood, which we recall:

| (60) |

We now prove Theorem 2. We recall the main matrix component of eq. (60):

| (61) |

We observe that the following two matrices are positive semi-definite222As remarked above, depending on the choices of parameters and , the null space of is indeed not always reduced to the null vector. Therefore, may be not positive definite with strictly positive probability.: , , while are positive definite (with probability 1 for that last one, see Theorem 5). Hence, a sufficient condition for the combination in to be positive definite is , as claimed. This brings the finiteness of with probability one, and the statement of Theorem 2.

9.3 Proof of Theorem 3

We split the proof in two main parts, the first of which focuses on a simplified version of the model in which the Bernoulli parameter () is sampled according to a Dirac — e.g. in the context of inference, from the prior standpoint, it is maximally informed. The results might be useful outside our framework, if is sampled from a distribution different from the ones we use.

We state the main notations involved in the Theorem. We define the total (squared) expected input (resp. output) to node as (resp. ), and the total input (resp. output) variance as (resp. ). We also define averages, , (same for outputs), and biased weighted proportions, , (again, same for outputs).

Now, we define two functions as:

where is Matsushita’s entropy. For any diagonalizable matrix , we let denote its eigenspectrum, and , . Our simplified version of Theorem 3, which we first prove, is the following one.

Theorem 7

Assume with , and , being fixed for any . Fix any constants and and let

| (64) |

Suppose that:

| (65) |

If is larger than some constant depending on and , then with probability over the sampling of and , the following holds true:

| (66) |

9.3.1 Helper tail bounds and properties for arcs, row and columns in matrix

To obtain concentration bounds on , we need to map the arc signal onto the real line, including e.g. when (in which case there cannot exist an arc between the two corresponding nodes, so there is no observable "weight" per se). We follow the convention for the Hawkes model of Linderman & Adams (2014), and associate to these "no signal" events the real zero, which makes sense since for example it matches the Dirac case when — which corresponds to an arc with weight always zero —. Define for short

| (67) | |||||

| (68) | |||||

| (69) |

so that

| (70) |

We remark that the eigenspectrum of is the same as for : if u is an eigenvector of , then is equivalent to , equivalent to (letting ), finally equivalent to . Therefore, bounding the eigenspectra of , plus adequate assumptions on that of , shall lead to bounding the eigenspectra of , but to get al these bounds, we essentially need properties and concentration inequalities for the coordinates of and their row- or column- sums. This is what we establish in this Section.

We first derive a tail bound for arc weight, removing indexes for clarity, and assuming and (see Figure 4). Let denote the random variable taking the arc weight. We recall that random variable is -sub-Gaussian () iff (Vu, 2014):

| (71) |

Theorem 8

Let . The following holds true:

| (72) |

Furthermore, is -sub-Gaussian with satisfying:

-

•

if ,

-

•

if .

Proof: Denote for short two random variables and . We trivially have and:

| (73) | |||||

| (74) |

for any , as claimed for eq. (72). Eq. (73) comes from the moment generating function for Gaussian . Now, it is clear that

-

•

is sub-Gaussian with parameter in the following two cases: (i) , (ii) . For this latter case, we have indeed (using Jensen’s inequality on ). Furthermore, sub-Gaussian parameter cannot be improved in both cases.

-

•

the trivial case leads to sub-Gaussianity for any .

Otherwise (assuming thus and ), we can immediately rule out the case (for any ), by noticing that, for , we have for

| (75) |

and so, for this value of , . In the following, we therefore consider , and .

Lemma 9

, we have

| (76) |

where is (unnormalized) Matsushita’s entropy.

Remark: ineq. (76) is probably close to be

optimal analytically.

Replacing by a dominated

entropy like Gini’s (i.e. with

finite derivatives on the right of 0 and left of 1) seems to break the result.

Proof:

The proof makes use of several tricks to counter the fact that

the right-hand side of ineq. (76) is essentially concave –

but not always – in , and essentially convex – but not always –

in , and matches the left-hand side as . In a

first step, we show that ineq. (76) holds for (and any ), then Step 2 shows that ineq. (76) holds for (and ). Step 3 uses a symmetry argument on the right-hand side of

ineq. (76) to extend the result to any (and any ), thereby finishing the proof.

Step 1. We remark that satisfies the following properties:

-

(i)

, ;

-

(ii)

for any .

Denote for short . We have:

| (77) | |||||

| (78) |

It comes and so because of (i). Since , we have in a neighborhood of 0. Also, we can check as well that because of (ii), so is concave in a neighborhood of . For the same reasons, is concave in a neighborhood of and since , we also have in a neighborhood of 1. Now, to zero the second derivative, we need equivalently:

| (79) |

or, equivalently again:

| (80) |

with . We have (letting for short and ),

| (81) |

and we can check that when . We can also check that when , so eq. (79) has in fact no solution whenever , regardless of the choice of . Hence, in

this case, is concave in and we get , for any .

Step 2. Suppose now that . We have

| (82) | |||||

| (83) |

We have and convexity is ensured as long as

| (84) |

It happens that , so whenever , is convex in . To finish Step 2, considering only the case , it is sufficient to show that , or equivalently,

| (85) |

It can be shown that the first derivative,

| (86) |

is for any — so, since both limits in 0 for eq. (85) coincide, eq. (85) holds for any . The second derivative (fixing ),

| (87) |

is strictly negative for — so, since both limits in 1

for eq. (85) coincide, eq. (85) is strictly concave

for , it sits above its chord which

itself sits above for , so eq. (85) holds for any

. This achieves the proof of Step 2.

Step 3. We now have that ineq. (76) holds for any and any . To finish the argument, we just have to remark that satisfies the following symmetry:

| (88) |

so assuming that , we have , so we reuse Steps 1 and 2 together with eq. (88) to obtain that for any ,

| (89) | |||||

as claimed, where the inequality makes use of Steps 1, 2. This

achieves the proof of Lemma 9.

To finish the proof of Theorem 8, we make use of Lemma

9 as follows, starting from eq. (72):

| (92) | |||||

Ineq. (9.3.1) uses the fact that , and ineq. (92) uses Lemma

9 with . Hence, is

sub-Gaussian with parameters and , as

claimed. This ends the proof of Theorem 8.

Theorem 8 leads to the following concentration inequality

for the row- and column-sums of , which are key to bound

eigenvalues.

Lemma 10

Let , , , , and let (and so on for the other averages ). Finally, let , and

| (93) | |||||

| (94) |

where is (normalized) Matsushita’s entropy. Then the following holds for any :

| (95) | |||||

| (96) |

Proof: Since the sum of independent random variables respectively -sub-Gaussian () brings a sub-Gaussian random variable, Theorem 8 immediately yields:

| (97) |

Since is concave, we have:

| (98) | |||||

We finally obtain using ineq. (98),

| (99) |

and we would obtain by symmetry:

| (100) |

as well. This ends the proof of Lemma 10.

Let us define function with:

| (103) |

which collects the key parts in the concentration inequalities for row- / column-sums. We need in fact slightly more than Lemma 10, as we do not just want to bound row- or column-sums, but we need to bound their norms (which, since by the triangle inequality, yields a bound on row- or column-sums). It can be verified that is -sug-Gaussian with the same as for , but because now integrates a folded Gaussian random variable (Tsagris et al., 2014) instead of a Gaussian, its expectation is non trivial. We have not found any (simple) bound on the expectation of such a folded Gaussian, so we provide a complete one here for , which integrates as well Bernoulli parameter .

Lemma 11

We have:

| (104) |

where . Furthermore, (104) is optimal in the sense that both sides coincide when (in this case, ).

Proof: We now have (removing indices for readability, Tsagris et al. (2014)):

| (105) |

where is the CDF of the standard Gaussian, so it is clear that the statement of the Lemma holds (and is in fact tight) when , as in this case . Otherwise, assume . For any , let

| (106) |

where is a constant. It comes from (Abramowitz & Stegun, 1964, Inequality 7.1.3):

| (107) |

and so, if ,

| (108) | |||||

and we would obtain the same bound for . There just remains to remark that ():

and we obtain the statement of Lemma 11.

Using Lemma 11 , we can extend Lemma 10 and obtain

the following Lemma.

Lemma 12

Let and denote the event:

| (109) |

Then for any ,

| (110) |

where and are respectively row- and column-sums in , and .

The way we use Lemma 12 is the following: pick

| (111) |

We get that with probability , we shall have both

| (112) | |||||

| (113) |

for all columns and rows in , with . There is a balance between the two summands in (112), (113) that we need to clarify to handle the upperbounds. This is achieved through the following Lemma.

Lemma 13

For any ,

where , .

9.3.2 Proof of Theorem 7

Let us define function with:

| (121) |

which collects the bounds in ineqs (117) and (118), and let . Let

| (122) |

is be the quantity we need to handle all eigenspectra, but for this objective, let us define assumption (Z) as:

-

(Z)

(call it the domination assumption for short) and

(123)

Assumption (Z) is a bit technical: we replace it by a simpler one, (A), which implies (Z). Suppose a constant, and assume without loss of generality; fix for some constant ,

| (124) | |||||

| (125) | |||||

Condition (123) is now ensured provided

| (126) |

while the domination condition is ensured, with ( a constant) large enough so that , as long as

| (127) |

So let us simplify assumption (Z) by the following assumption, which implies (Z):

-

(A)

and being constants such that , we have:

(128)

Again, (A) implies (Z).

Remark 1: the upperbound of (128) is quantitatively not so different from Linderman & Adams (2014)’s assumptions. They work with two assumptions, the first of which being (129) (we consider variances for the assumption to rely on same scales as ours), and also pick network parameters in such a way that large deviations for edge weights are controlled with high probability, with a condition that roughly looks like: (130) for some constant . This constraint is relevant to the same stability issues as the ones we study here, and can be found in a slightly different form (but equivalent) in (Hyvärinen & Smith, 2013, Section 4), where it is mandatory for the estimation of ICA model parameters.. Finally, (Linderman & Adams, 2014) make the heuristic choice to enforce at least one of the two ineqs. (129, 130). Remark 2: the sampling constraint akin to eq. (130) is in fact very restrictive for ICA estimation of models (Hyvärinen & Smith, 2013, Section 4), since typically each coordinate in has to be bounded with high probability, whereas in our case, it is sufficient to control sums (, row- or column-wise) with high probability. We can therefore benefit from concentration properties on large networks that such approaches may not have.

What is interesting from (128) is the hints that provide the lowerbound of (128) for Theorem 7 (main file) to hold. The main difference between and is indeed (omitting factor in variance terms) the switch between (for ) and (for ). Figure 6 explains that the lowerbound may be violated essentially only on networks with very unlikely arcs almost everywhere, because has infinite derivative333And it seems that such entropy-like penalties with infinite derivatives in a neighborhood of zero are necessary to obtain Lemma 9 — as explained in the Lemma — if we want to keep the sub-Gaussian characterization of the s. as . Also, it gives a justification for the name of the two functions and , where maximizing tends to favor arcs with close to ( stands for Equivocal), while maximizing tends to favor arcs with close to ( stands for Unequivocal).

|

() We now have all we need to bound the eigenspectra of . Let (resp. ) denote the maximal (resp. minimal) eigenvalue of the argument matrix. We obtain that with probability ,

(ineq. (9.3.2) comes from Hölder inequality) and similarly for the minimal eigenvalue,

which implies that for this latter bound not to be vacuous ( is defined in eq. (122)). As long as , it is not hard to see that dominates in for large networks so we can assume large enough so that, for some small ,

| (132) |

which brings .

In this case, if , then

. Furthermore, it is not hard

to check that we also get . To

summarize, as long as assumption (Z) (and so, as long as (A)) holds,

the complete eigenspectra of , and by

extension , , all lie within with

high probability.

() We finish with the eigenspectrum of . We also easily obtain that

and obviously , which is all we need.

() We now finish the proof of Theorem 7, recalling that can be summarized as:

| (133) |

with has an eigensystem which is the (Minkowski) product of the eigensystems of its two matrices, and therefore is within ; on the other hand, has eigensystem which is the one of (eigenvalues have different algebraic multiplicity though), which therefore is within . Hence, simplifying a bit, we can bound the complete eigenspectrum of , , as:

| (134) |

under assumption (A), with probability , as claimed. This ends the proof of Theorem 7.

9.3.3 From Theorem 7 to Theorem 3

We now assume with , where is a random variable

satisfying and

(the support of ). The proof essentially follows

that of Theorem 7, with the following minor changes.

() The derivation of eq. (74) now satisfies, since is maximal in ,

| (135) | |||||

() Assumption (A) now reads, for some constants and such that , we have:

| (136) |

where does not change but

9.4 Marginal Likelihood Given the Network Parameters

When calculating the expected log-likelihood it is easier to work with the inverse model:

| (138) | ||||

| (139) | ||||

| (140) | ||||

| (141) | ||||

| (142) |

where ; ; denotes the row of matrix . Here we analyse the conditional likelihood by integrating out everything but . Clearly, for fixed , since all the distributions are Gaussians, and we are only applying linear operators, the resulting distribution over , and consequently over , is also a Gaussian process. Hence, we only need to figure out the mean function and the covariance function of the resulting process. For the expectation we have that:

| (143) |

since both and are zero-mean processes. For the covariance function we have that:

| (144) | ||||

| (145) | ||||

| (146) |

where we have defined the entry of matrix and the matrix of latent node covariances and noise covariances as:

| (147) | ||||

| (148) |

The covariance function of the observations is then given by:

| (149) |

For further understanding of this model, let us assume that the observations lie on a grid in time, and is a matrix of observations with hence the likelihood of all observations is:

| (150) | ||||

| (151) |

where denotes the Kronecker product; If we use this setting then we obtain:

| (152) |

Interestingly, the model above has been studied in statistics and in machine learning, see e.g. Bonilla et al. (2008); Rakitsch et al. (2013). Furthermore, inference and hyperparameter estimation can be done efficiently by exploiting properties of the Kronecker product, e.g. an evaluation of the marginal likelihood can be done in . Nevertheless, unless there is a substantial overlapping between the locations of the observations across the nodes (i.e. times), the Kronecker formulation becomes intractable.

9.5 Marginal likelihood

Assuming the general case (i.e. non-grid observations), let us refer to as the covariance of the marginal process over , as induced by the covariance function in Equation (149), where is the covariance matrix induced by the covariance function in Equation (146). Therefore, the prior, conditional likelihood, and marginal likelihood of the model are:

| (153) | ||||

| (154) | ||||

| (155) |

where we have omitted the dependencies of the above equation on the network parameters . Because of the marginalization property of GPs it is easy to see that all the above distributions are -dimensional, where , where is the number of observations per node. Hence the cost of evaluating the exact marginal likelihood is .

9.6 Efficient Computation of Marginal Likelihood Given Network Parameters

For simplicity, we consider here the synchronized case where all the nodes in the network have observations at the same times. i.e. the total number of observations is . Here we show an efficient expression for the log marginal likelihood:

| (156) | ||||

| (157) | ||||

| (158) | ||||

| (159) |

The main difficulty of computing this expression is the calculation of the log determinant of an dimensional matrix, as well as solving an -dimensional system of linear equations. Our goal is to show that we never need to solve these operations on an -dimensional matrix, which are but instead use operations.

Given the eigen-decomposition of the above matrices

| (160) | ||||

| (161) |

It is possible to show that the marginal covariance is given by

| (162) | ||||

| (163) | ||||

| (164) |

For these matrices we also define their eigen-decomposition analogously to above:

| (165) | ||||

| (166) |

9.6.1 Log-determinant Term

| (167) | ||||

| (168) | ||||

| (169) |

9.6.2 Quadratic Term

| (170) | ||||

| (171) |

Let us define

| (172) | ||||

| (173) | ||||

| (174) |

Hence the quadratic form above becomes:

| (175) | ||||

| (176) |

| (177) |

and , are the vectors obtained by stacking the columns of the matrices and respectively.

10 Experiments

As mentioned in the main paper, the choice of baseline comparisons was based on Peters et al. (2014). Other than the methods discussed in the main paper, there are four other methods considered by Peters et al. (2014): (1) Brute-force search; (2) Greedy DAG Search (gds, see e.g. Chickering, 2002); (3) Greedy equivalence search (ges, Chickering, 2002; Meek, 1997); (4) Regression with subsequent independence test (resit, Peters et al., 2014).

In the experiments reported in section 7.2, since the ground truth is known, the evaluation criteria is AUC (area under the ROC curve). Calculating AUC values requires a discriminative threshold to generate ROCs. In the case of gds and ges there was no clear parameter that could be considered as the discriminative threshold, and therefore results for these algorithms are not reported. In the case of resit, there is a threshold, but the threshold values for which the method produces different results were not provided, making it infeasible to calculate AUC, and therefore the output of this algorithm is not reported. In the experiments reported in section 7.2, the implementations of ges, gds and resit that we used returned an error (possibly because the number of nodes was greater than the observations from each node). Therefore their results are not reported. Finally, for the experiment in section 7.4 we compared the results with cpc, which provided comparatively good performance in other experiments. Also, we did not include the brute-force method, which is not feasible to perform in networks with more than four nodes, and therefore makes it inapplicable in the experiments studied here.

The pc and cpc algorithms are constrain-based structure learning methods for directed acyclic graphs (DAG). The algorithms require a conditional independence test, for which we used the test for zero partial correlation between variables. The iamb method is a two-phase algorithm for Markov blanket discovery. Linear correlation is used for the test of conditional independence required by this algorithm. The lingam method is a Linear non-Gaussian Additive Model (LiNGAM) for estimating structural equation models. pw-lingam provides the direction of connection between the two connected nodes. We used partial correlation for determining whether two nodes are connected, and the magnitude of the correlation was used as the discriminative threshold. For connected nodes at the threshold pw-lingam was used to determine the direction of the connection.

For [pc, cpc ges], iamb and lingam implementations provided by R packages Kalisch et al. (2012), Marco (2010), Kalisch et al. (2012) were used respectively. For pw-lingam the code provided by the authors was re-implemented in R and was used. For gds and resit implementation provided by authors of Peters et al. (2014) in R was used.

10.1 Prior setting and optimization specifics

Similarly to Maddison et al. (2016), different values are used for the prior and posterior distributions. For experiments with , following Maddison et al. (2016) we used for priors and for posterior distributions. For the experiments in section 7.2, in which , we used the first subject () as the validation data and selected for priors and for posterior distributions. The number of Monte Carlo samples was selected based on computational constraints, and were , and samples for small-scale (§7.2, 7.2), medium-scale (§7.4), and large-scale (§7.4) experiments respectively.

Prior over is assumed to be zero-mean Gaussian distribution with variance similar to Linderman & Adams (2014). Prior over is assumed to be , which implies that the probability that a link exists between two nodes is :

| (178) |

10.2 Brain functional connectivity data

AUC computation. This is obtained by varying the discrimination threshold and drawing the false-positive rate (fpr) vs true-positive rate (tpr). In the case of latnet, this threshold is the absolute expected value of the overall connection strength between the nodes (). In the case of pc, cpc and iamb algorithms, the discrimination threshold is the -value (target type I error rate) of the conditional independence test, and in the case of lingam and pw-lingam, absolute values of the estimated linear coefficients and partial correlation coefficients are used as the discrimination thresholds respectively. The ROC curve from which the AUC is calculated, is required to be an increasing function, however, in the case of pc, cpc and iamb algorithms, the fpr/tpr curve can be decreasing in some parts. This is because these algorithms might remove an edge from the graph after increasing the significance level in order to ensure that the resulting graph is a DAG. In such cases, one can removed the decreasing parts by computing the AUC from the non-decreasing portions of the curve (Figure 8; concave envelope of the curve). This correction provides an upper-bound on the AUC of these methods. Figure 7 shows the AUC of the methods for different network sizes bot both corrected AUC (corrected) and uncorrected AUC (uncorrected).

10.3 Spellman’s sentinels of the yeast cell cycle

|

|

|

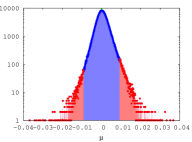

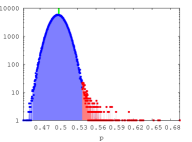

We have analyzed the signals of 799 (one gene was missing in our data, out of the 800 tagged in the original paper) sentinels of the yeast cell cycle (YCC) from Spellman et al. (1998), for a total of 13,600 data points. Figure 9 presents the counting histograms for and found among all inferred arcs. Let us denote as strong arcs arcs that jointly belong to the red areas of both curves (meaning that both is in top 99.9 quantile and in top 99 quantile). We remark that the scale for is roughly in the tenth of that for , so that for strong arcs, distributions with in its top 99 quantile can be considered encoding non-void arc connection (even when small in an absolute scale). We also notice that the distribution in admits relatively large values (), so that its top percentile can be encoding arc probability strictly larger than .

| G1(P) | FKS1, CLN3, CDC47, RAD54, PCL2, MNN1, RAD53, CLB5 | 8/16 |

| G1/S | DPB2, CDC2, PRI2, POL12, CDC9, CDC45, CDC21, RNR1, CLB6, POL1, MSH2, RAD27, ASF1, | |

| POL30, RFA2, PMS1, MST1, RFA1, MSH6, SPC42, CLN2, PCL1, RFA3 | 23/28 | |

| S | MCD1, HTA2, SWE1, HTB1, KAR3, HSL1, HHF2, HHT1, HTB2, CIK1, CLB4 | 11/17 |

| G2 | CLB1, CLB2, BUD8, CDC5 | 4/4 |

| G2/M | SWI5, CWP1, CHS2, FAR1, DBF2, MOB1, ACE2, CDC6 | 8/9 |

| M(P) | CDC20 | 1/2 |

| M(M) | TEC1, RAD51, NUM1 | 3/4 |

| M(A) | TIP1, SWI4, KIN3, ASF2, ASH1, SIC1, PCL9, EGT2, SED1 | 9/15 |

| M(T) | 0/1 | |

| M/G1 | PSA1, RME1, CTS1 | 3/3 |

| G1 | HO | 1/4 |

| late G1 | 0/3 |

We have analyzed arcs belonging to at least one of these categories ( is in top 99.9 quantile or in top 99 quantile), the intersection of both representing strong arcs. Intuitively, this top list should contain most of the (much shorter) "A-lists" of cell-cycle genes as recorded in the litterature. One of these lists (Cho et al., 1998) has been curated and can be retrieved from (Rowicka et al., 2007, Table 4 SI). It contains 106 genes. Table 1 gives the genes we retrieve, meaning that at least one significant arc appear for each of them ( is in top 99.9 quantile or in top 99 quantile). The values given in the Table allow to concluce that almost of the 106 genes are retrieved as having at least one significant arc. Since the total number of genes with strong arcs we retrieve is 177, out of the 799, the probability that the result observed in Table 1 is due to chance is zero up to more than thirty digits. Hence, assuming the list of genes in Table 1 is indeed a most important one, we can conclude in the reliability of our technique for network discovery for this domain.

| M | M/G1 | G1 | S | G2 | |

|---|---|---|---|---|---|

| M | 18 | 4 | 7 | 3 | 6 |

| M/G1 | 5 | 7 | 3 | 0 | 1 |

| G1 | 5 | 4 | 23 | 1 | 0 |

| S | 2 | 0 | 0 | 2 | 1 |

| G2 | 4 | 1 | 0 | 0 | 0 |

|

As a next step, Table 2 presents the breakdown for the relative distribution of strong arcs in the YCC as a function of the YCC phase, using as reference the original one from Spellman et al. (1998), collapsing the vertices in their respective phase of the YCC to obtain a concise graph of within and between phase dependences (Figure 10 gives a schematic view of the most significant part of the distribution — arcs between different genes of the same YCC phase create the loops observed). We can draw two conclusions: (i) the graph of dependences between phases is not symmetric. Furthermore, (ii) M and G1 appear as the phases which concentrate more than half of the strong arcs, which should be expected given the known regulatory importance in these two phases (Spellman et al., 1998).

| Gene | Phase | out/in-degree ratio | ||

| in-degree out-degree | ASH1 | M/G1 | 5.0 | |

| YIL158W | M | 3.0 | ||

| MSH6 | G1 | 3.0 | ||

| SWI5 | M | 3.0 | ||

| RAD53 | G1 | 3.0 | ||

| YNR009W | S | 2.5 | ||

| MET3 | G2 | 2.3333333333333335 | ||

| YOX1 | G1 | 2.0 | ||

| SVS1 | G1 | 2.0 | ||

| YOL007C | G1 | 2.0 | ||

| CDC20 | M | 2.0 | ||

| YKR041W | G2 | 2.0 | ||

| CDC5 | M | 2.0 | ||

| MET28 | S | 2.0 | ||

| YML034W | M | 2.0 | ||

| SMC3 | G1 | 2.0 | ||

| HHO1 | S | 2.0 | ||

| YDL039C | M | 2.0 | ||

| RAD27 | G1 | 2.0 | ||

| FAR1 | M | 2.0 | ||

| DIP5 | M | 1.75 | ||

| YPL267W | G1 | 1.6 | ||

| CDC45 | G1 | 1.5 | ||

| RNR1 | G1 | 1.5 | ||

| PCL9 | M/G1 | 1.5 | ||

| LEE1 | S | 1.5 | ||

| YOR314W | M | 1.5 | ||

| YIL025C | G1 | 1.4444444444444444 | ||

| AGP1 | G2 | 1.3333333333333333 | ||

| CWP1 | G2 | 1.3333333333333333 | ||

| ALD6 | M | 1.2 | ||

| YOL132W | M | 1.1666666666666667 | ||

| YNR067C | M/G1 | 1.0666666666666667 | ||

| in-degree out-degree | YNL078W | M/G1 | 1.0 | |

| YCL013W | G2 | 1.0 | ||

| RME1 | G1 | 1.0 | ||

| CLB1 | M | 1.0 | ||

| RPI1 | M | 1.0 | ||

| YIL141W | G1 | 1.0 | ||

| BUD4 | M | 1.0 | ||

| YLR235C | G1 | 1.0 | ||

| YOR315W | M | 1.0 | ||

| YER124C | G1 | 1.0 | ||

| YPR156C | M | 1.0 | ||

| YGL028C | G1 | 1.0 | ||

| BUD3 | G2 | 1.0 | ||

| STE3 | M/G1 | 1.0 | ||

| HST3 | M | 1.0 | ||

| ALK1 | M | 1.0 | ||

| CHS2 | M | 1.0 | ||

| YLL061W | S | 1.0 | ||

| YFR027W | G1 | 1.0 | ||

| LAP4 | G1 | 1.0 | ||

| YNL173C | M/G1 | 1.0 | ||

| YML033W | M | 1.0 | ||

| SEO1 | S | 1.0 | ||

| YOR264W | M/G1 | 1.0 | ||

| NUF2 | M | 1.0 | ||

| YOR263C | M/G1 | 1.0 | ||

| YBR070C | G1 | 1.0 | ||

| YNL300W | G1 | 1.0 | ||

| YPR045C | M | 1.0 | ||

| YOR248W | G1 | 1.0 | ||

| MYO1 | M | 1.0 | ||

| RLF2 | G1 | 1.0 | ||

| in-degree out-degree | YOL101C | M/G1 | 0.9444444444444444 | |

| YDR355C | S | 0.8 | ||

| HTB2 | S | 0.75 | ||

| YRO2 | M | 0.7142857142857143 | ||

| YDR380W | M | 0.6666666666666666 | ||

| FET3 | M | 0.6666666666666666 | ||

| YDL163W | G1 | 0.6666666666666666 | ||

| CLB6 | G1 | 0.6666666666666666 | ||

| ECM23 | G2 | 0.6666666666666666 | ||

| YBR089W | G1 | 0.6666666666666666 | ||

| YGR221C | G1 | 0.6666666666666666 | ||

| YDL037C | M | 0.6 | ||

| MF(ALPHA)2 | G1 | 0.6 | ||

| YLR183C | G1 | 0.5714285714285714 | ||

| PDR12 | M | 0.5555555555555556 | ||

| YER150W | M/G1 | 0.5555555555555556 | ||

| POL1 | G1 | 0.5 | ||

| YHR143W | G1 | 0.5 | ||

| SPS4 | M | 0.5 | ||

| PCL1 | G1 | 0.5 | ||

| YGL184C | S | 0.5 | ||

| EGT2 | M/G1 | 0.5 | ||

| CTS1 | G1 | 0.5 | ||

| YDR149C | G2 | 0.5 | ||

| GAP1 | G2 | 0.5 | ||

| HO | G1 | 0.5 | ||

| WSC4 | M | 0.4673913043478261 | ||

| SPO16 | G1 | 0.46153846153846156 | ||

| YMR032W | M | 0.4 | ||

| YGP1 | M/G1 | 0.4 | ||

| SPH1 | G1 | 0.3333333333333333 | ||

| YCL022C | G1 | 0.3333333333333333 | ||

| YCLX09W | G2 | 0.3333333333333333 | ||

| PIR1 | M/G1 | 0.25 | ||

| ARO9 | M | 0.16666666666666666 |

To make more precise in observation (i) that the network is indeed imbalanced, we have computed the ratio out-degree in-degree for all genes admitting strong edges of both kinds (i.e. with the gene as in- / out- node). Table 3 presents all genes collected. A total of 100 genes is found, the majority of which (68) is imbalanced. We also remark that roughly 80 of them is associated to M and/or G1 (only 19 are associated to phases S or G2), which is consistent with the findings of Table 2.

| Gene | Phase | out-degree |

|---|---|---|

| WSC4 | M | 43 |

| YOL101C | M/G1 | 17 |

| YNR067C | M/G1 | 16 |

| YIL025C | G1 | 13 |

| YDL037C | M | 12 |

| YOR264W | M/G1 | 10 |

| YER124C | G1 | 10 |

| HO | G1 | 9 |

| YPL267W | G1 | 8 |

| YLR183C | G1 | 8 |

| MET3 | G2 | 7 |

| DIP5 | M | 7 |

| SEO1 | S | 7 |

| YOL132W | M | 7 |

| ALD6 | M | 6 |

| YGL028C | G1 | 6 |

| PCL9 | M/G1 | 6 |

| SPO16 | G1 | 6 |

| YDL039C | M | 6 |

| YOL007C | G1 | 6 |

| YER150W | M/G1 | 5 |

| YRO2 | M | 5 |

| PDR12 | M | 5 |

| PCL1 | G1 | 5 |

| YNR009W | S | 5 |

| RME1 | G1 | 5 |

| ASH1 | M/G1 | 5 |

| AGP1 | G2 | 4 |

| GAP1 | G2 | 4 |

| YOR263C | M/G1 | 4 |

| YNL173C | M/G1 | 4 |

| CWP1 | G2 | 4 |

| FAR1 | M | 4 |

| MCD1 | G1 | 4 |

| YOX1 | G1 | 4 |

| YDR355C | S | 4 |

| YOR314W | M | 3 |

| MSH6 | G1 | 3 |

| SPT21 | G1 | 3 |

| LEE1 | S | 3 |

| YIL158W | M | 3 |

| YLR049C | G1 | 3 |

| RNR1 | G1 | 3 |

| HTB2 | S | 3 |

| GLK1 | M/G1 | 3 |

| SWI5 | M | 3 |

| MF(ALPHA)2 | G1 | 3 |

| CDC45 | G1 | 3 |

| RAD53 | G1 | 3 |

| Gene | Phase | in-degree |

|---|---|---|

| WSC4 | M | 92 |

| YDL037C | M | 20 |

| HO | G1 | 18 |

| YOL101C | M/G1 | 18 |

| YNR067C | M/G1 | 15 |

| YLR183C | G1 | 14 |

| SPO16 | G1 | 13 |

| YOR264W | M/G1 | 10 |

| YER124C | G1 | 10 |

| PCL1 | G1 | 10 |

| YIL025C | G1 | 9 |

| PDR12 | M | 9 |

| YER150W | M/G1 | 9 |

| GAP1 | G2 | 8 |

| SEO1 | S | 7 |

| YRO2 | M | 7 |

| ARO9 | M | 6 |

| SPH1 | G1 | 6 |

| YOL132W | M | 6 |

| YGL028C | G1 | 6 |

| MF(ALPHA)2 | G1 | 5 |

| YMR032W | M | 5 |

| ALD6 | M | 5 |

| YPL267W | G1 | 5 |

| YGP1 | M/G1 | 5 |

| YDR355C | S | 5 |

| RME1 | G1 | 5 |

| YOR263C | M/G1 | 4 |

| YGL184C | S | 4 |

| PCL9 | M/G1 | 4 |

| PIR1 | M/G1 | 4 |

| HTB2 | S | 4 |

| DIP5 | M | 4 |

| YNL173C | M/G1 | 4 |

| SPS4 | M | 4 |

| YCL022C | G1 | 3 |

| YOL007C | G1 | 3 |

| MET3 | G2 | 3 |

| YGR221C | G1 | 3 |

| YDL039C | M | 3 |

| CWP1 | G2 | 3 |

| YCLX09W | G2 | 3 |

| YDR380W | M | 3 |

| AGP1 | G2 | 3 |

| CLB6 | G1 | 3 |

| YBR089W | G1 | 3 |