Probability density of lognormal fractional SABR model

Jiro Akahori, Xiaoming Song and Tai-Ho Wang

Jiro Akahori

Department of Mathematical Sciences

Ritsumeikan University

Noji-higashi 1-1-1, Kusatsu, Shiga, 525-8577, Japan

akahori@se.ritsumei.ac.jpXiaoming Song

Department of Mathematics

Drexel University

32nd and Market Streets, Philadelphia, PA 19096

song@math.drexel.eduTai-Ho Wang

Department of Mathematics

Baruch College, The City University of New York

1 Bernard Baruch Way, New York, NY10010

and

Department of Mathematical Sciences

Ritsumeikan University

Noji-higashi 1-1-1, Kusatsu, Shiga, 525-8577, Japan

tai-ho.wang@baruch.cuny.edu

Abstract.

Instantaneous volatility of logarithmic return in the lognormal fractional SABR model is driven by the exponentiation of a correlated fractional Brownian motion. Due to the mixed nature of driving Brownian and fractional Brownian motions, probability density for such a model is less studied in the literature. We show in this paper a bridge representation for the joint density of the lognormal fractional SABR model in a Fourier space. Evaluating the bridge representation along a properly chosen deterministic path yields a small time asymptotic expansion to the leading order for the probability density of the fractional SABR model. A direct generalization of the representation to joint density at multiple times leads to a heuristic derivation of the large deviations principle for the joint density in small time. Approximation of implied volatility is readily obtained by applying the Laplace asymptotic formula to the call or put prices and comparing coefficients.

The celebrated Black and Black-Scholes-Merton models have been the benchmark for European options on currency exchange, interest rates, and equities since the inauguration of the trading on financial derivatives. However, empirical evidences have shown that the main drawback of these models is the assumption of constant volatility; the key parameter required in the calculation of option premia under such models. The volatility parameters induced from market data are in fact nonconstant across markets; dubbed as volatility smile. The Stochastic (SABR for short hereafter) model, suggested by Hagan, Lesniewski, and Woodward in [13], is one of the models, such as local volatility models, stochastic volatility models, and exponential Lévy type of models etc, that attempts to capture the volatility smile effect.

Furthermore, as opposed to local volatility models, in SABR model the volatility smile moves in the same direction as the underlying with time, see [12].

The SABR model is depicted by the following system of stochastic differential equations (SDEs):

(1.1)

(1.2)

with , where is the forward price and is the instantaneous volatility. and are correlated Brownian motions with constant correlation coefficient .

The SABR model is at times referred to as the lognormal SABR model when .

The SABR formula is an asymptotic expansion for the implied volatilities of call options with various strikes in small time to expiry. For reader’s convenience, we reproduce the SABR formula in the following. Let be the implied volatility of a vanilla option struck at and time to expiry . The SABR formula states

(1.3)

as time to expiry approaches 0. The function and the parameter involved in (1.3) are defined respectively as

and

Generally, the SABR formula is given one order higher, up to order . Here we present only up to zeroth order for our own purpose.

The geometry of SABR model is isometrically diffeomorphic to the two dimensional hyperbolic space or the Poincaré plane. This isometry leads to a derivation of the SABR formula (1.3) based on an expression of the heat kernel, known as the McKean kernel, on Poincaré plane. In particular, the lowest order term in (1.3) has a geometric interpretation. The function is the shortest geodesic distance from the spot value to the vertical line in the upper half plane . Hence, the lowest order term in (1.3) is indeed the ratio between the absolute value of logmoneyness, i.e., , and the shortest geodesic distance from to the vertical line in the upper half plane. We refer readers interested in this topic to [13] for more detailed discussions. As expression for heat kernel on hyperblic space is concerned, Ikeda and Matsumoto in [15] provided a probabilistic approach and obtained, among other interesting results, a representation for the transition density of hyperbolic Brownian motion, i.e., the heat kernel over the Poincaré plane. See Theorem 2.1 in [15] for details.

The aforementioned nice isometry between SABR model and Poincaré plane breaks down if the volatility process, i.e., the process in (1.1), is driven by a fractional Brownian motion such as the second equation in (2.3) considered in the paper. Moreover, due to the lack of Markovianity of fractional Brownian motions and thus the nonexistence of the forward and backward Kolmogorov equations, the classical asymptotic expansion approaches, such as the heat kernel or WKB expansion, are no longer applicable either. In this regard, the probabilistic approach in [15] is more applicable and tractable when dealing with processes driven by fractional Brownian motions.

The volatility process is generally conceived behaving “fractionally” in that the driving noise is a fractional process, e.g., a fractional Brownian motion with Hurst exponent other than a half. For a far from exhausting list, models that attempt to incorporate the fractional feature of volatility include:

the ARFIMA model in [10] and the FIGARCH model [1] for discrete time models; the long memory stochastic volatlity model in [3] and the affine fractional stochastic volatilility model in [4] for continuous time models.

Somewhat on the contrary, in a recent study in [9], the Hurst exponent is estimated as being less than a half; thereby indicating antipersistency as opposed to persistency of the volatility process. It is also worth mentioning that generalizations of Heston model to fractional version have been recently considered in [7] and [11].

Heston related models are usually dealt with via the characteristic and/or moment generating functions. However, in this paper we take the approach following closely the methodology in [15].

In order to embed the empirically observed fractional feature of the volatility process into the classical SABR model, we suggest in this paper a fractional version of the SABR model as in (2.3). Modulo a mean-reversion component, this model aligns with the model statistically tested in [9]. The main observation in [9] is that, using square root of the realized/integrated variance as a proxy for the instantaneous volatility, the logarithm of the volatility process behaves like a fractional Brownian motion in almost any time scale of frequency. The Hurst exponent inferred from the time series data is less than a half; indeed, . This observation of small Hurst exponent in the volatility process makes the analysis of the model more technical and challenging from stochastic analysis point of view. To our knowledge, most of the small time asymptotic expansions for processes driven by fractional Brownian motions have restrictions on the Hurst exponent of the driving fractional Brownian motion, mostly . One of the advantage of the approach undertaken in the current paper is that it works without restriction on the Hurst exponent . The key ingredient is a representation in a Fourier space, which we call the bridge representation in Section 2, for the joint density of log spot and volatility, see (2.6).

A small time asymptotic expansion of the joint density is readily obtained from the bridge representation. The idea is to approximate the conditional expectation in the bridge representation by a judiciously chosen deterministic path since, conditioned on the initial and terminal points, at each point in time a Gaussian process will not wander too far away from its expectation.

As long as an asymptotic expansion for the density of the underlying asset is available, to obtain an expansion for implied volatility is almost straightforward by basically comparing the coefficients with a similar expansion obtained by using the lognormal density on the Black or the Black-Scholes-Merton side.

The methodology of deriving the bridge representation (2.6) can be generalized directly to obtain a bridge representation for the joint density of multiple times; hence inducing a representation for finite dimensional distributions of the fractional SABR model, see Theorem 5.1. Based on this bridge representation for finite dimensional distributions, Section 5 is devoted to a heuristic yet appealing derivation of the large deviations principle for the joint density of the fractional SABR model in small time. This large deviations principle in a sense can be regarded as defining a “geodesic distance” over the fractional SABR plane since, as we shall show in Section 5, it recovers the energy functional on the Poincaré plane when . We leave the rigorous proof of the large deviations principle in a future work. An immediate consequence of this large deviation principle is the fractional SABR formula (to the lowest order) (5.6) which recovers the classical SABR formula when . The fractional SABR formula (5.6) pertains the guiding principle that the lowest order term in the implied volatility expansion is given by the ratio between the absolute value of the logmoneyness and the geodesic distance to the vertical line .

The rest of the paper is organized as follows. The fractional SABR model is specified and the bridge representation for joint density is shown in Section 2. Sections 3 and 4 provide small time asymptotic expansions of the joint density and of the implied volatilities respectively. Section 5 presents the bridge representation for finite dimensional distributions and the large deviations principle. Finally, the paper concludes in Section 6 with discussions.

2. Model specification

Throughout the text, and denote two independent standard Brownian motions defined on the filtered probability space satisfying the usual conditions. Let be a fractional Brownian motion with Hurst exponent generated by (see [5]), i.e.,

where is the Molchan-Golosov kernel

(2.1)

with and is the Gauss hypergeometric function. Also, the autocovariance function of a fractional Brownian motion is denoted by and defined as

(2.2)

Lastly, we assume that all random variables and stochastic processes are defined on .

2.1. The model

We study the following lognormal fractional SABR (fSABR) model in a risk neutral probability (for simplicity, interest and dividend rates are both assumed zero in this paper):

(2.3)

where and are the given time zero (current observed) values for the processes and respectively, and .

In other words, the underlying price follows a stochastic volatility model with the (instantaneous) volatility process , and is given by the exponentiation of a correlated fractional Brownian motion.

The main purpose of this section is to derive the bridge representations (2.6) and (2.1) for the joint densities of . The bridge representation is the crucial starting line in obtaining expansions and approximations of the joint densities to be discussed in Section 3.

By making the change of variables

the system (2.3) can be written more explicitly as

(2.4)

where and .

2.2. Malliavin calculus with respect to Brownian motion

We provide some preliminaries on Malliavin calculus with respect to the two Brownian motions and in this subsection. We refer the reader to [14] and [16] for more details.

For any fixed , let be the separable Hilbert space of all

square integrable real-valued functions on the interval

with scalar product denoted by . The norm of an element will be denoted by . For any

, we put and .

For any , denote by the set of all infinitely

differentiable functions such that and all of its partial derivatives have

polynomial growth. We make use of the notation whenever .

Let denote the class of smooth and cylindrical random variables such

that a random variable has the form

(2.5)

where belongs to , and

are in , and .

For a smooth and cylindrical random variable of the

form (2.5), its Malliavin derivative with respect to is the -valued random variable

given by

and respectively its Malliavin derivative with respect to is given by

For any , we will denote the domain of in

by , meaning that is the

closure of the class of smooth and cylindrical random variables with

respect to the norm

We tailor Theorem 2.1.2 in [16] to the following lemma which yields a result on the absolute continuity of the law of a random vector with respect to the Lebesgue measure.

Lemma 2.1.

Let be a random vector in . If the Malliavin matrix of is invertible a.s.. Then the law of is absolutely continuous with respect to the Lebesgue measure on . Consequently, the joint density of the random variables exists.

2.3. Bridge representation for the joint density

In this subsection, we show the existence of the joint density of for any by using Malliavin calculus. We also give a bridge representation for the joint density by adapting the methodology introduced in Ikeda and Matsumoto [15].

Theorem 2.1.

For any , the law of satisfying (2.4) is absolutely continuous with respect to the Lebesgue measure on . Moreover, the joint probability density of has the following bridge representation

(2.6)

where and .

Remark 2.1.

The bridge representation (2.6) can be regarded as a generalization of the well-known McKean kernel, namely, the classical heat kernel over a 2-dimensional hyperbolic space. For reader’s reference, the McKean kernel reads

where is the geodesic distance from to . The geodesic distance satisfies . Note that the McKean kernel is a density with respect to the Riemannian volume form . Indeed, in the case where , and , Ikeda-Matsumoto in [15] showed how to recover the McKean kernel from (2.6). See also Cheng and Wang [2] for a different representation in terms of Bessel bridge for the hyperbolic heat kernel.

Now we fix any . Then according to Sections 2.2 and 5.2 in [16], the Malliavin derivatives of and are given as follows

and

Thus, the Malliavin matrix of is given by

where

and

Then it follows from the Cauchy-Schwarz inequality that almost surely

which implies that the Malliavin matrix is invertible a.s.. Hence, by Lemma 2.1 the law of is absolutely continuous with respect to the Lebesgue measure on .

Next, we calculate the joint probability density of as follows. For any bounded and continuous function defined on , we have

(2.7)

Note that conditioned on , is normally distributed since and are independent. Moreover,

Plugging (2.9) into the right-hand side of (2.8), we get

Finally, we end up with the following bridge representation of the density (2.6).

∎

By transforming back to the original variables , we obtain a bridge representation for the joint density of in (2.3).

Corollary 2.1.

The joint density of the lognormal fractional SABR model (2.3) has the following bridge representation

3. Expansion around deterministic path

To gain more intuition and in particular a more practical form for applications in obtaining approximations of implied volatility, this section is devoted to deriving an expansion to the lowest order of the bridge representation (2.6) around a properly chosen deterministic path.

The expansion will be shown useful in deriving a small time approximation for implied volatility in Section 4.

Recall that the joint density of has the representation given in (2.6) as

Let us start with a few naïve calculations as follows. We expand the above conditional expectation around the deterministic path , for , that is determined by the conditional expectation of given its terminal point . Precisely,

where is defined in (2.2). By Taylor’s expansion, we have, for ,

Thus, even for obtaining a naïve expansion, we shall need a systematic way of computing the conditional expectations of the form, for either or ,

which is pretty complicated if not impossible. Nevertheless, as leading order is concerned, small time expansion of the joint density to the lowest order (i.e., ) is still manageable. The result is summarized in the following theorem.

In the following sequel, for simplification of the notation, we use to denote , where . A function is denoted by as if it satisfies

Theorem 3.1.

The joint probability density of the process satisfying (2.4) has the following asymptotic to the lowest order

where

Proof.

To the lowest order, is given by

(3.2)

We consider the conditional expectation in the above expression.

Note that and are jointly Gaussian. We apply the following identity to evaluate the conditional expectation: if and are jointly normal with mean 0, we can decompose as

where and are independent and is standard normal. Hence,

In our case, and , hence

Therefore,

Thus, by substituting the above expression into (3.2), we obtain

(3.3)

We postpone the detailed error analysis to Section 7.1 in the appendix.

∎

Remark 3.1.

We remark that in the logarithmic scale, (3.1) can be expressed in a more concise form as

Notice that in this case represents the Brownian motion in hyperbolic plane whose transition density (with respect to the Riemannian area measure) has the leading term in small time asymptotic as

where denotes the geodesic distance between and in the hyperbolic plane. For reader’s reference, the hyperbolic cosine of the geodesic distance has the closed form expression

can be regarded as an approximation of the hyperbolic geodesic distance. The complete recovery of the hyperbolic geodesic distance is demonstrated in Section 5 below.

4. Small time approximation of option price and implied volatility

We derive in this section the small time asymptotics of the premium of a call option and its associated implied volatility by applying the small time asymptotics for the probability density obtained in Section 3 when .

It is documented, for exmaple, in Ekström and Lu [6], that if the underlying asset is governed by an exponential Lévy model, the induced implied volatilities of non ATM options may explode if jumps exist and the underlying process jumps towards the strike. As we shall see in the following, when , the small time approximation of implied volatility also explodes; creating a jump like behavior in the underlying process.

Let be the logmoneyness, the time to expiry, and recall that . Though equivalently, we shall be primarily working with the process as in (2.4) rather than the process in (2.3) hereafter. We write the price of a call as a function of and as

To evaluate the last integral, we approximate the joint density by the small time asymptotics obtained in Theorem 3.1, then, as , apply Laplace asymptotic formula to the resulting integral. For reader’s convenience, we provide with proof in Secton 7.2 a variation of the Laplace asymtotic formula that is tailored for our own use.

Lemma 4.1.

Let .

For out-of-money call options, i.e., , the call price has the following asymptotic as

(4.1)

where is the minimizer

Proof.

The proof is a straigtforward application of the Laplace asymptotic formula (7.1) in Lemma 7.1. Let and . By using the asymptotic density (3.1), consider

Applying the Laplace asymptotic formula (7.1) to the lowest order term in the last expresion yields

where, for fixed , is the minimizer of the function

Since the objective function is continuous in and it is a quadratic function in , it follows that when is small enough, thereby

∎

Remark 4.1.

For the case , from asymptotic density (3.1) it implies

When is small enough, the minimum value of

is not attained at the boundary of . Hence, the Laplace asymptotic formula cannot be applied in this case. However, when , we can still present the following uniqueness of the minimal point graphically in the following Remark.

Remark 4.2.

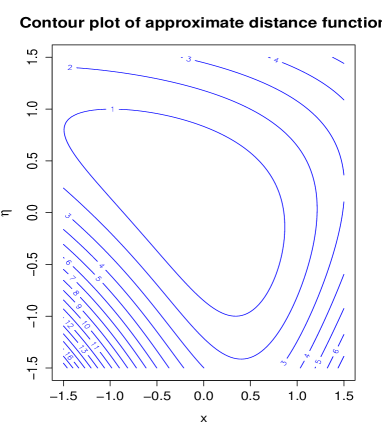

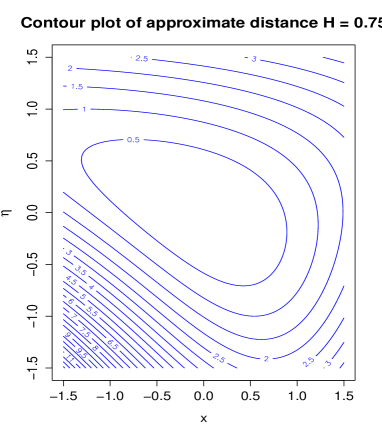

The plots in Figure 1 shows graphically the uniqueness of the minimal point for and . In theses particular examples, the contours are convex in the half plane , which corresponds to the out-of-money calls. For out-of-money puts, , though the contours are not convex, the uniqueness of sustains.

Figure 1. The contour plots. Parameters , , , . on the right; , on the left.

So long as we establish an asymptotic for the log price for , by using the following small time asymptotic for implied volatility in [8] or [17]

(4.2)

an asymptotic formula for implied volatility follows immediate. We summarize the result in the following theorem but omitting its proof.

Theorem 4.1.

Let and let be the log moneyness and .

The implied volatility for out-of-money calls () has the following asymptotic in small time to expiry

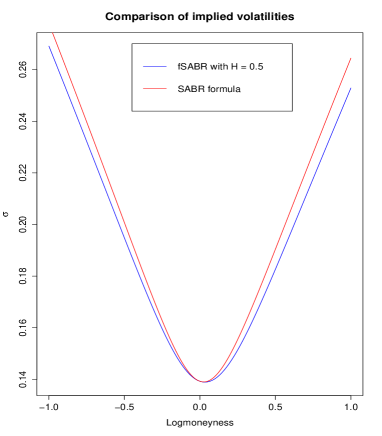

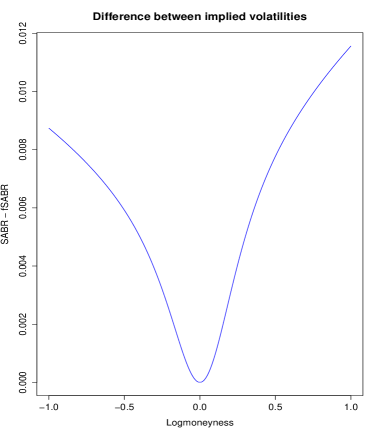

Note that (4.3) does not recover the SABR formula when . The derivation of the SABR formula relies heavily on the geometry and symmetry of the underlying SABR plane which is isometric to the Poincaré plane. Figure 2 shows the comparison between the two formulas with time to expiry . Parameters are chosen so as to reproduce the figures in [12]. In this set of parameters, the maximal difference between the two approximate implied volatility curves is about 1% for logmoneyness .

Figure 2. The plot on the left shows the approximate implied volatility curves versus logmoneyness with time to expiry produced by (4.3) (in blue) the SABR formula (1.3) (in red). Parameters are set as , , . The plot on the right shows the difference between the two curves.

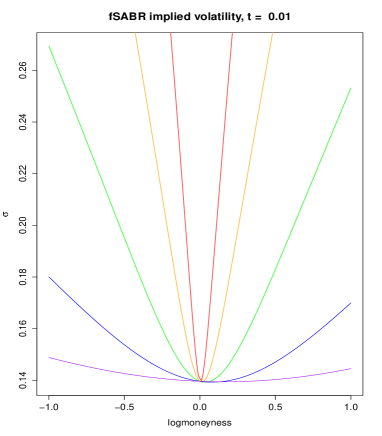

We conclude the section by remarking that, as time to expiry approaches zero, the approximate implied volatility flattens out with ;

whereas the whole surface explodes with except for the at-the-money option . Figure 3 shows the plots of approximate implied volatilities given in (4.3)

versus logmoneyness for time to expiry and respectively, and various Hurst exponenets . As in Figure 2, parameters are chosen as , , and . The numerical determination of the ’s is relatively efficient since it is basically a one-dimensional optimization problem.

Figure 3. The implied volatility curves for on the left, on the right. Parameters are set as , , . in red, in orange, in green, in blue, in purple.

5. A heuristic large deviation principle

In this section, we provide a heuristic derivation of the sample path large deviation principle for in small time by bootstrapping the bridge representation to multiperiod. For notational simplicity, we introduce the following vector notations.

Theorem 5.1.

The multiperiod joint density of

has the following bridge representation

where , , and for . Recall that .

Proof.

For any bounded measurable function , consider the expectation

Let , and thus accordingly , . Note that, conditioned on , the random variables ’s are independent normal with mean and variance .

We calculate the conditional expectation as follows.

This completes the proof of bridge representation (5.1) since is arbitrary.

∎

To move onto a heuristic derivation of the sample path large deviation principle for in small time, we take logarithm on both sides of (5.1) and obtain

(5.3)

In the following, we ignore the last term on the right hand side of (5.3) and intuitively calculate the limits as of the first two terms. Note that to the leading order we have

where is the covariance matrix of . We further discretize the autovariance of fractional Brownian motion as

where denotes the upper triangular matrix

Thereby, . Let be the solution to the linear system

It follows that

Also in the limit as , we obtain .

On the other hand, for the first term on the right hand side of (5.3), we have

Note that conditioned on , we have

as well as

It follows that the first term in (5.3) has the limit

as .

Putting the two limits together, we obtain heuristically for that

(5.4)

where satisfies the integral equation

for all . We remark that (5.4) should serve as the rate function for the sample path large deviation principle in small time for . Moreover, one may define the “geodesic” from the initial point to the terminal point in the fSABR plane as the path which minimizes the functional (5.4), i.e.,

where again is determined by solving the integral equation

(5.5)

Also, the minimizer can be regarded as the “geodesic” connecting and .

Remark 5.1.

Note that is indeed determined by the inverse operator applied to . In particular, with this inverse operator reduces to the usual derivative. Thus, with ,

The last expression is the energy functional (up to the constant factor ) associated with the Riemann metric . The diffusion process associated with this Riemann metric is governed by the SDEs

where and are correlated Brownian motion with constant correlation , which up to a linear transformation is the upper plane model of the Poincaré space. In other words, with , the functional (5.4) recovers the energy functional for the classical Poincaré space, which is isometric to the SABR plane.

Lastly, with the aid of sample path large deviation principle (5.4), it is nearly a common practice, say by applying the Laplace asymptotic formula, to conclude that the log premium of an out-of-money call in small time has the asymptotic as

where denotes the optimal path that minimizes the functional (5.4) subject to the constraint and , satisfy the integral equation (5.5). Thus, by applying (4.2), an approximation of implied volatility in small time is readily obtained. We summarize the result in the following proposition which, with , recovers the SABR formula (1.3). However, for , the numerical implementation of (5.6) is more involved than that of (4.3) since, as opposed to a one dimensional optimization problem, it is subject to solving a two-dimensional constrained variational problem.

Proposition 5.1.

(fSABR formula)

Let be the log moneyness.

The implied volatility in small time to expiry has the asymptotics

(5.6)

where is the minimizer of the variational problem

with and satisfying

for . Notice that (5.6) recovers the SABR formula (1.3) with .

6. Conclusion and discussion

We showed in this paper a bridge representation in Fourier space and a small time asymptotic for the joint probability of lognormal fractional SABR model for general .

An application of the asymptotics of the joint density is an approximation of the implied volatility in small time. Due to the different nature of methodologies, the newly obtained approximation of implied volatilities in small time does not recover the celebrated SABR formula for implied volatility (to the zeroth order) when the Hurst exponent equals a half. To recover the SABR formula, we presented a heuristic derivation of the sample path large deviation principle for the lognormal fractional SABR model by bootstrapping via the multiperiod joint density. We emphasize once again that the same trick is applicable to general fractional SABR models, i.e., to include a local volatility component in the process for underlying asset. We leave the rigorous proof of the sample path large deviation principle for fractional SABR models in a future work. Lastly, the bridge representation methodology is also applicable to the case in which the volatility process is governed by an exponential fractional Ornstein-Uhlenbeck process since a fractional Ornstein-Uhlenbeck process is Gaussian as well. However, as time to expiry approaches zero, the mean reversion part does not really play a role in the large deviation regime.

Acknowledgement

We are grateful for helpful discussions with the participants of the conferences: At the Frontiers of Quantitative Finance at

International Centre of Mathematical Sciences, Edinburgh, UK and Mathematics of Quantitative Finance at Mathematisches Forschungsinstitut Oberwolfach, Oberwolfach, Germany. JA is supported by JSPS KAKENHI Grant Number ,

, and , and the project RARE-318984 (an FP7 Marie Curie IRSES).

THW is partially supported by the Natural Science Foundation of China grant 11601018.

7. Appendix - Technical proofs

In the appendix, we provide a detailed error analysis of the asymptotic expansion for (3.1) and a version of Laplace asymptotic formula that is readily applicable to our case.

7.1. Error analysis

Let be the space of smooth functions defined on with compact support.

For a given , recalling , from (2.6) we have

(7.1)

where

is the Fourier transform of with respect to .

Note that the right-hand side of (3.1) equals the right-hand side of (3.2). We compare (7.1) with the following expression obtained by using the approximate joint density in (3.1) and obtain

For simplification, denote

and

Then the modulus of the difference between (7.1) and (7.1) is equal to

(7.3)

The goal is to show that (7.3) converges to zero in the order of as , for every .

By applying the following inequality, for any ,

where denotes the real part of , we have

(7.4)

since for all and .

Apparently, and are given by

In the following, denotes a generic constant whose value may vary in different contexts. Then, by (7.3), (7.4) and

Hölder’s inequality, we have

(7.5)

for some and , .

Since , it is easy to show the following properties of :

(i)

for any , ;

(ii)

for any and , .

Note that property (ii) can be easily obtained by property (i).

By the above property (ii), we can show that

(7.6)

We compute the second term in (7.5) separately as follows. By changing variables, we get

(7.7)

where

By property (ii) of , it is easy to see that

(7.8)

For , by Jensen’s inequality and Hölder’s inequality, we have

where with .

Therefore, using property (ii) again, we can easily show

: Choosing such that , by Hölder’s inequality, the Burkholder-Davis-Gundy inequality, Jensen’s inequality and a change of variables, we obtain

Notice that

By property (ii) we have

Thus, we can see that as .

•

and : The asymptotic behavior of and is the same as that of , and hence, as .

•

: By using the same technique to , we have

and as .

Thus, putting all the estimates for the ’s together we get

(7.11)

for any , as .

Therefore, it implies from (7.5), (7.6), (7.10) and (7.11) that

that is, (7.3) converges to zero in the order of as , for every .

7.2. Laplace asymptotic formula

We prove the following form of Laplace asymptotic formula required in the derivation of the small time asymptotic of the price of an out-of-money call.

Lemma 7.1.

(Laplace asymptotic formula)

Let be a closed and convex set in with nonempty and smooth boundary . Suppose that , with , has continuous second-order partial derivatives in , and, for every sufficiently small, the function is locally convex in and attains its minimum uniquely at . Moreover, there is such that for any , there exist and for which

where is the open ball of radius centered at .

Assume that has continuous second-order partial derivatives in , is integrable over (i.e., ) and that vanishes identically in and on the boundary but the inward normal directional derivative of at is nonzero.

Then, we have the asymptotic expansion, as ,

where and are the second derivatives of and respectively in the tangential direction to at .

Proof.

For any , we split the integral on the left side of (7.1) into two parts as

(7.13)

We treat the two terms on the right hand side of (7.13) individually. For the first term, since the integration region is restricted to a subset of the small ball , it can be reparametrized by so that in the -coordinates the set corresponds to and the vectors form a local orthonormal frame around . For simplicity, we further assume that in the -coordinates is located at the origin. Note that in the -coordinates the vector is parallel to as well as the inward normal vector of at .

We shall use the convention that repeated indices are summed up over their respective ranges. Denote partial derivatives by subindices, we have for

since for attains its minimum at the boundary point .

Thus, in the -coordinates

the first integral on the right-hand side of (7.13) reads

(7.14)

Now, by a change of variables

we can write the above integral on the right-hand side of (7.14) as

Note that, for any real numbers , by dominated convergence theorem, we have

As , we calculate the each integral individually as follows. For , since the function in is an odd function and integral interval for is symmetric about the origin, we obtain

(7.17)

For and , notice that and , and hence, we obtain

(7.18)

and

(7.19)

Therefore, it implies from (7.14)-(7.19) that, in the -coordinates,

(7.20)

For the second term on the right-hand side of (7.13), we get

(7.21)

As a result, the second term is exponentially small (at the rate ) as compared to the expansion (7.1) obtained for the first term, hence it does not contribute to the asymptotic expansion.

Finally, by (7.13), (7.20) and (7.21) we obtain the Laplace expansion (7.1) by rewriting the expressions for the right-hand side of (7.20) in the -coordinates.

∎

References

[1]Baillie, R.T., Bollerslev, T., and Mikkelsen, H.O.,

Fractionally integrated generalized autoregressive conditional heteroskedasticity,

Journal of Econometrics, 74, pp.3-30, 1996.

[2]Cheng, X. and Wang, T.-H.,

Bessel bridge representation for heat kernel in hyperbolic space,

Preprint, available in ArXiv, 2016.

[3]Comte, F. and Renault, E.,

Long memory in continuous-time stochastic volatility models,

Mathematical Finance, 8(4), pp.291–323, 1998.

[4]Comte, F., Coutin, L. and Renault, E.,

Affine fractional stochastic volatility models,

Annals of Finance, 8, pp.337–378, 2012.

[5]Decreusefond, L. and Üstünel, A. S.

Stochastic analysis of the fractional Brownian motion.

Potential Anal., 10(2), pp177–214, 1999.

[6]Ekström, E. and Lu, B.,

Short-time implied volatility in exponential Lévy models,

International Journal of Theoretical and Applied Finance, 18(4), 2015.

[7]El Euch, O. and Rosenbaum, M.,

The characteristic function of rough Heston models,

Preprint, 2016.

[8]Gao, K. and Lee, R.,

Asymptotics of implied volatility to arbitrary order,

Finance and Stochastics, Forthcoming, 2015.

[9]Gatheral, J., Jaisson, T. and Rosenbaum, M.,

Volatility is rough,

Preprint, 2014.

[10]Granger, C.W.J. and Joyeux, R.,

An introduction to long memory time series models and fractional differencing,

Journal of Time Series Analysis, 1, pp.15-39, 1980.

[11]Guennoun, H., Jaquier, A. and Roome, P.,

Asymptotics of the fractional Heston model,

Preprint, 2014.

[12]Hagan, P., Kumar, D., Lesniewski, A., and Woodward, D.,

Managing smile risk,

Wilmott Magazine, September, pp.84–108, 2002.

[13]Hagan, P., Lesniewski, A., and Woodward, D.,

Probability distribution in the SABR Model of stochastic volatility,

Springer Proceedings in Mathematics & Statistics,

Large Deviations and Asymptotic Methods in Finance, 110, pp.1–35, 2015.

[14]Hu, Y., Analysis on Gaussian space.

World Scientific, Singapore, 2017.

[15]Ikeda, N. and Matsumoto, H.,

Brownian Motion on the Hyperbolic Plane and Selberg Trace Formula,

Journal of Functional Analysis, 163, pp.63–100, 1999.

[16]Nualart, D., The Malliavin Calculus and Related Topics. Second

edition. Springer 2006.

[17]Roper, M. and Rutkowski, M.,

A note on the behaviour of the Black-Scholes implied volatility close to expiry,

International Journal of Theoretical and Applied Finance, 12(4), pp.427–441, 2009.