High dimensional deformed rectangular matrices with applications in matrix denoising

Abstract

We consider the recovery of a low rank matrix from its noisy observation in the high dimensional framework when is comparable to . We propose two efficient estimators for under two different regimes. Our analysis relies on the local asymptotics of the eigenstructure of large dimensional rectangular matrices with finite rank perturbation. We derive the convergent limits and rates for the singular values and vectors for such matrices.

keywords:

1 Introduction

Matrix denoising is important in many scientific endeavors. They appear prominently in singal processing [37], image denoising [12], machine learning [38], statistics [13, 14, 16], empirical finance [6, 20] and biology [31]. In these applications, researchers are interested in recovering the true deterministic matrix from a noisy observation. Consider that we can observe a noisy data matrix , where

| (1.1) |

the deterministic matrix is known as the signal matrix and the noise matrix. In the classic framework where is much smaller than the truncated singular value decomposition (TSVD) is the default technique, see for example [15]. This method recovers with an estimator using the truncated singular value decomposition, where denotes the truncation level, are the singular values and vectors of . We usually need to provide a threshold to choose and use the singular values only when Two popular methods are the soft thresholding [11] and hard thresholding [13].

In recent years, the advance of technology has lead to the observation of massive scale data, where the dimension of the variable is comparable to the length of the observation. In this situation, the TSVD will lose its validity. To address this problem, in the present paper, we consider the matrix denoising problem (1.1) by assuming is comparable to and estimate in the following two regimes:

Regime (1). is of low rank and we have prior information that its singular vectors are sparse;

Regime (2). is of low rank and we have no prior information on the singular vectors.

In regime (1), is called simultaneously low rank and sparse matrix. This type of matrix has been heavily used in biology. A typical example is from the study of gene expression data [31]. In [38], Yang, Ma and Buja also consider such problem but from a quite different perspective. They do not take the local behavior of singular values and vectors into consideration. Instead, they use an adaptive thresholding method to recover in (1.1). In regime (2), we are interested in looking at what is the best we can do in this case. A natural (and probably necessary) assumption is rotation invariance [5], as the only information we know about the singular vectors is orthonormality. It is notable that, in this case, our result coincides with the results proposed by Gavish and Donoho [14], where they consider the estimator from another perspective and restrict the estimator to be conservative (see Definition 3 in [14]).

In this paper, we will study the convergent limits and rates of the singular values and vectors for the sequence of matrices defined in (1.1). For the rest of the paper, we will omit the subscript for convenience and write

| (1.2) |

To avoid repetition, we summarize the technical assumptions of the noise matrix .

Assumption 1.1.

We assume is a white noise matrix, where the entries of are i.i.d random variables such that

Furthermore, we assume that for there exists some constant such that

| (1.3) |

Denote the SVD of as

| (1.4) |

where and where are orthonormal vectors and is a fixed constant. We also assume Then (1.2) can be written as

| (1.5) |

Throughout the paper, we are interested in the following setup

| (1.6) |

It is well-known that for the noise matrix the spectrum of satisfies the celebrated Marchenco-Pastur (MP) law [24] and the largest eigenvalue satisfies the Tracy-Widom (TW) distribution [36]. Specifically, denote , where as the eigenvalues of in a decreasing fashion, we have that

| (1.7) |

holds with high probability. Furthermore, denote as the singular vectors of for some large constant with high probability, we have [8]

To sketch the behavior of we consider the case when in (1.5). Assuming that the distribution of the entries of is bi-unitarily invariant, Benaych-Georges and Nadakuditi established the convergent limits in [2] using free probability theory. Denote they proved that when would detach from the spectrum of the MP law and become an outlier. And when converges to and sticks to the spectrum of the MP law. For the singular vectors, denote as the left and right singular vectors of They proved that when would be concentrated on cones with axis parallel to respectively, and the apertures of the cones converged to some deterministic limits. And when will be asymptotically perpendicular to respectively. We point out that similar results have been proved for the Wigner matrices with additive deformation and covaraince matrices with multiplication perturbation. For such results, we refer the readers to [1, 4, 9, 18, 19, 27, 30, 32].

Our computation and proof rely on the isotropic local MP law [3, 17, 29]. These results say that the eigenvalue distribution of the sample covariance matrix is close to the MP law, down to the spectral scale containing slightly more than one eigenvalue. These local laws are formulated using the Green functions,

| (1.8) |

To illustrate our results and ideas, we give an overview of the present paper. As we have seen from [8, 10], the self-adjoint linearization technique is quite useful in dealing with rectangular matrices. Hence, in a first step, we denote by

| (1.9) |

where are defined as

| (1.10) |

Next we will give a heuristic description of our results. We will always denote as the eigenvalues of and as the singular vectors of And we denote as the Green function of . Consider in (1.5) and by a standard perturbation discussion (see Lemma 4.7), we find that satisfies the equation Using the isotropic local law in [17], we find that (see Lemma 4.9) has a deterministic limit when is large enough. Heuristically, the convergent limit of is determined by the equation An elementary calculation shows that, when , where is defined in (2.6).

When the largest eigenvalue will detach from the bulk and become an outlier around its classical location . We would expect this happens under a scale of This can be understood in the following ways: increasing beyond the critical value , we expect to become an outlier, where its location is located at a distance greater than from By using mean value theorem, the phase transition will take place on the scale when

| (1.11) |

When (1.11) happens, we also prove that

| (1.12) |

Below this scale, we would expect the spectrum of to stick to that of . Especially, the largest eigenvalue still has the Tracy-Widom distribution with the scale , which reads as

| (1.13) |

For the singular vectors, when we have where are deterministic functions of and defined in (2.9). For the local behavior, we will use an integral representation of Greens functions (see (5.17)). Under the assumption that ’s are well-separated and satisfy (1.11), we prove that

| (1.14) |

Below the scale of (1.11), we prove that

| (1.15) |

Armed with (1.12), (1.13), (1.14) and (1.15), we can go to the matrix denoising problem (1.5) under the two different regimes. In the first regime, we assume there exists sparse structure of the singular vectors, in the case when we would expect to be sparse as well. Hence, will be of sparse structure. Therefore, by suitably choosing a submatrix of and doing SVD for the submatrix, we can get an estimator for the singular vectors. Our novelty is to truncate singular values and vectors simultaneously. For the estimation of singular values, we can reverse (1.12) to get the estimator for For the singular vectors, based on (1.15), the truncation level should be much larger than and we will use K-means clustering algorithm to choose such level. However, when we can estimate nothing according to (1.13) and (1.15).

In the second regime, as we have no prior information whatsoever on the true eigenbasis of the only possibility is to use the eigenbasis of This is equivalent to the assumption of rotation invariance. We will propose a consistent rotation invariant estimator (RIE) which satisfies the following condition,

| (1.16) |

where are orthogonal (rotation) matrix in respectively. Before concluding this section, we list our main contributions of this paper:

(i). We systematically study the local behavior of the singular values and vectors for finite rank perturbation of large dimensional rectangular matrices of model (1.5). We compute the convergent limits and rates for them.

(ii). We provide two efficient estimators for the matrix denoising model (1.5) under two different regimes. We provide practical algorithms to compute the estimators. For the sparse estimation, as far as we know, our paper is the first one to truncate the singular values and vectors simultaneously.

This paper is organized as follows. In Section 2, we give the main results of this paper. In Section 3, we propose the estimators for (1.5) under two regimes. In Section 4, we record the basic tools for the proof of the main theorems. In Section 5, we prove the main theorems listed in Section 2.

Conventions. For two quantities and depending on , the notation means that for some positive constant , and means that for some positive constants as . We also use the notation if and . We define the minimum of any two reals by For any matrix , we denote by as the transpose of and the Frobenius norm of . We will also use to denote the spectrum for any square matrix And for any rectangular matrix we use to denote its -th largest singular value.

2 Main results

Throughout the paper, we always use for a small constant and for a large constant. Denote and as a subset of of by

| (2.1) |

and the number of outlier singular values as

| (2.2) |

Our results can be extended to a more general domain by denoting We will not pursue this generalization. For more details, we refer to [4]. For any subset we define the projections on the left and right singular subspace of by

| (2.3) |

We also need the non-overlapping condition, which was firstly introduced in [4].

Definition 2.1.

For the non-overlapping condition is written as

| (2.4) |

where is defined in (2.1) and is defined by

| (2.5) |

With the above preparation, we state our main results of the singular values of Denote

| (2.6) |

Recall defined in (1.5) and are the eigenvalues of

Theorem 2.2.

The above theorem gives precise location of the outlier singular values and the extremal non-outlier singular values. For the outliers, they locate around their classical locations and for the non-outliers, they locate around The results of the singular vectors are given by the following theorem. Denote

| (2.9) |

Theorem 2.3.

Remark 2.4.

The assumption ensures that for some constant . When it is guaranteed as we will see from Lemma 4.12 that We need for the technical purpose of the application of the local laws.

Next we will give some examples to illustrate our results. We assume that

Example 2.5.

(1). Consider the right singular vectors and let , we have

This implies that, the cone concentration of the singular vector holds if and the non-overlapping condition (2.4) holds. Furthermore, if is well-separated from both the critical point and the other outliers, the error bound is of order

(2). Let and for , we have

Hence, if then will be completely delocalized in any direction orthogonal to

(3). If then we have

Hence, when or will be completely delocalized in the direction of The first case reads as is an outlier and the second case as that is in the bulk of the spectrum of

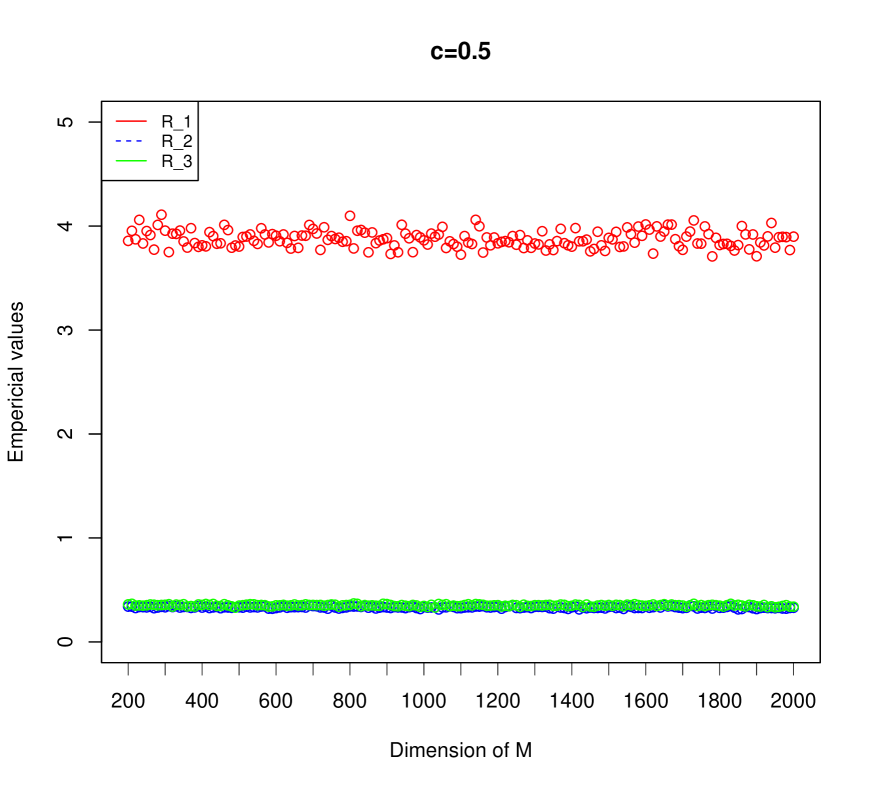

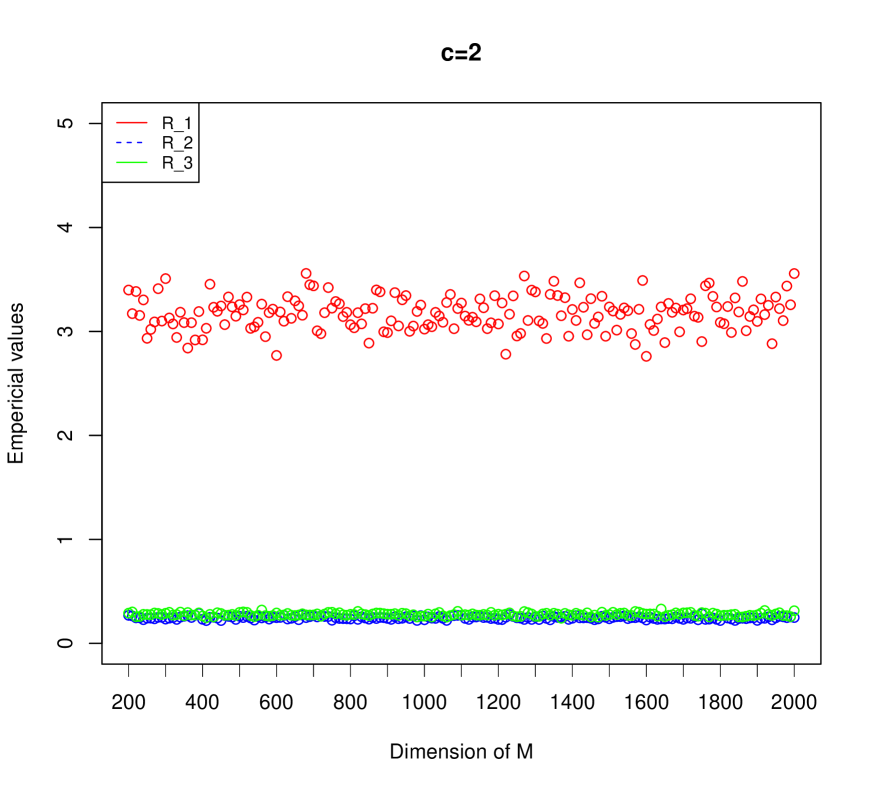

Before concluding this section, we use the following figure to illustrate the accuracy of the proposed bounds in (2.7), (2.10) and (2.11). We consider the rank one perturbation where is a Gaussian random matrix with mean zero and variance and are sparse vectors generated from the package .

To avoid the influence of the constant, we consider the ratio between the empirical bound and dominated part, i.e., for we will consider

where and We consider the cases and and choose For each we record the averaged ratios for using 1,000 repetitions and plot these ratios for a variety of choices (in total 181) of between and We can conclude from Figure 1 that these ratios are around some fixed constants independent of

3 Statistical applications

3.1 Sparse estimation

In the present application, we study the denoising problem (1.2), where is sparse in the sense that the nonzero entries are assumed to be confined on a block. We assume that are sparse and introduce the following definition to precisely describe the sparsity.

Definition 3.1.

For any vector , is a sparse vector if there exists a subset with such that

Next we will propose an estimator for by estimating the singular values and vectors separately. As can been see from Theorem 2.2, we can estimate the true outlier singular values from their corresponding sample values. To ease our discussion, we impose the following stronger assumptions on the outlier singular values of

Assumption 3.2.

For we assume that there exists some constant such that

Note that the above assumption is a stronger version of (2.1) and widely used in the practical applications [14, 25, 26, 28]. We first estimate the number of outlier singular values. In [26], is referred as the effective number of identifiable signals and the author provided an information theoretic estimator by minimizing the Akaike Information Criterion (AIC). Furthermore, some other useful statistics have been proposed to effectively estimate the number of spikes in the spiked covariance matrix model, for instance the differences between consecutive eigenvalues in [28]. By Theorem 2.2, when we expect will be away from one and when it will be close to one. In the present paper, we will employ the ratios of consecutive sample singular values [21] as our statistic. For satisfying

| (3.1) |

we denote (Recall .)

| (3.2) |

We summarize the property of as the following proposition and its proof can be found in the supplementary material [7].

Proposition 3.3.

In practice, for the choice of , we employ the automatic calibration procedure of [28, Section 4]. The idea is to use the ratio of the first two largest eigenvalues of a Wishart matrix, i.e., an random Gaussian matrix satisfying Assumption 1.1. Indeed, we need to search the eigenvalue index such that the ratio of two consecutive eigenvalues of is much larger than corresponding to that of . In detail, we will use the following procedure to calibrate

-

(1).

Generate a sequence (say 1,000) of random Gaussian matrices satisfying Assumption 1.1. Calculate the ratios of the first and second eigenvalue of and write them as

-

(2).

For a given large probability (say as suggested by [28]), find the value such that

For we find that for and for These will be used later for our simulation studies.

With the above notations, we provide the stepwise SVD Algorithm 1 to recover in (1.2). As are sparse, we need to find a submatrix of by a suitable truncation. Instead of simply truncating the singular values [14, 38], we truncate the singular values and vectors simultaneously.

| (3.3) |

Algorithm 1 provides us a way to recover stepwisely. We first estimate using the estimation then by analyzing In each step, we only need to look at the largest singular value and its associated singular vectors. It is notable that, we drop all the eigenvalues of when and

| (3.4) |

Our methodology relies on truncating singular values and vectors simultaneously. As illustrated in (3.3), the thresholds and play the key roles in recovering the sparse structure of the singular vectors. It will be proved in Section 2 that any threshold satisfying (3.3) should work when is sufficiently large. In the finite sample framework (when is not quite large), we employ the K-means algorithm [16, Section 10.3.1] to stabilize the recovery of the sparse structure of . The reason behind is, the entries in the singular vectors can be well classified into two categories. Denote the index sets getting from the K-means algorithm, where they satisfy

| (3.5) |

We now replace (3.3) with the following step:

-

•

Do K-means clustering to partition the entries of into two classes, where

(3.6) where satisfy (3.5).

Next, we summarize the theoretical properties of Algorithm 1 as the following theorem and leave its proof into the supplementary material [7].

Theorem 3.4.

Before concluding this subsection, we compare our method with other different algorithms. In [38], the authors proposed another algorithm from a quite different perspective. They did not take the properties of the singular values and vectors of into consideration. Instead, they used iterative thresholding on the rows of to get an estimator. The algorithm is called sparse SVD. Their algorithm can be regarded as the extension of TSVD on the submatrix of .

We use Table 1 to compare the results of three algorithms, our stepwise SVD(SWSVD), the sparse SVD(SSVD) proposed by [38] and the truncated SVD(TSVD). For the implementation of SSVD, we use the package in R which is contributed by the first author of [38]. From Table 1, we find that our method outperforms both the SSVD and TSVD in all the cases . Furthermore, the standard deviation is small, which implies that our estimation is quite stable.

| M=300 | M=500 | ||||||

|---|---|---|---|---|---|---|---|

| Sparsity | error norm | Std | Sparsity | error norm | Std | ||

| SWSVD | 0.05 | 0.043 | 0.175 | 0.05 | 0.045 | 0.189 | |

| 0.1 | 0.614 | 0.178 | 0.1 | 0.6 | 0.16 | ||

| 0.2 | 0.822 | 0.126 | 0.2 | 0.825 | 0.137 | ||

| 0.45 | 1.1 | 0.114 | 0.45 | 1.09 | 0.09 | ||

| SSVD | 0.05 | 4.01 | 0.002 | 0.05 | 4.01 | 0.002 | |

| 0.1 | 4.01 | 0.004 | 0.1 | 4.02 | 0.002 | ||

| 0.2 | 4.04 | 0.004 | 0.2 | 4.03 | 0.004 | ||

| 0.45 | 4.06 | 0.005 | 0.45 | 4.08 | 0.004 | ||

| TSVD | 0.05 | 53.9 | 6.872 | 0.05 | 53.75 | 6.63 | |

| 0.1 | 53.72 | 6.63 | 0.1 | 53.38 | 6.71 | ||

| 0.2 | 52.33 | 7.01 | 0.2 | 52.2 | 6.65 | ||

| 0.45 | 51.043 | 2.49 | 0.45 | 52.4 | 4.3 |

3.2 Rotation invariant estimation

This subsection is devoted to recovering in (1.2) assuming that no prior information about is available. In this regime, we will consider the rotation invariant estimator (RIE) satisfying (1.16). We conclude from [5] that any RIE shares the same singular vectors as To construct the optimal estimator, we use the Frobenius norm as our loss function. Denote we have

| (3.7) |

Therefore, the form of the RIE can be written in the following way

| (3.8) |

where is the class of matrices whose left singular vectors are and right singular vectors are Suppose denote then by an elementary computation, we find

| (3.9) |

Therefore, is optimal if

| (3.10) |

In the present paper, we use the following estimator for and will prove its consistency in Section 2. Recall (3.2), the estimator is denoted as

| (3.11) |

where and are defined in (2.9). Denote

| (3.12) |

It is notable that the convergent limits for the shrinkage and MSE for have already been computed in [25]. We next summarize the theoretical properties of our estimators as the following theorem. Its proof can be found in the supplementary material [7].

Theorem 3.5.

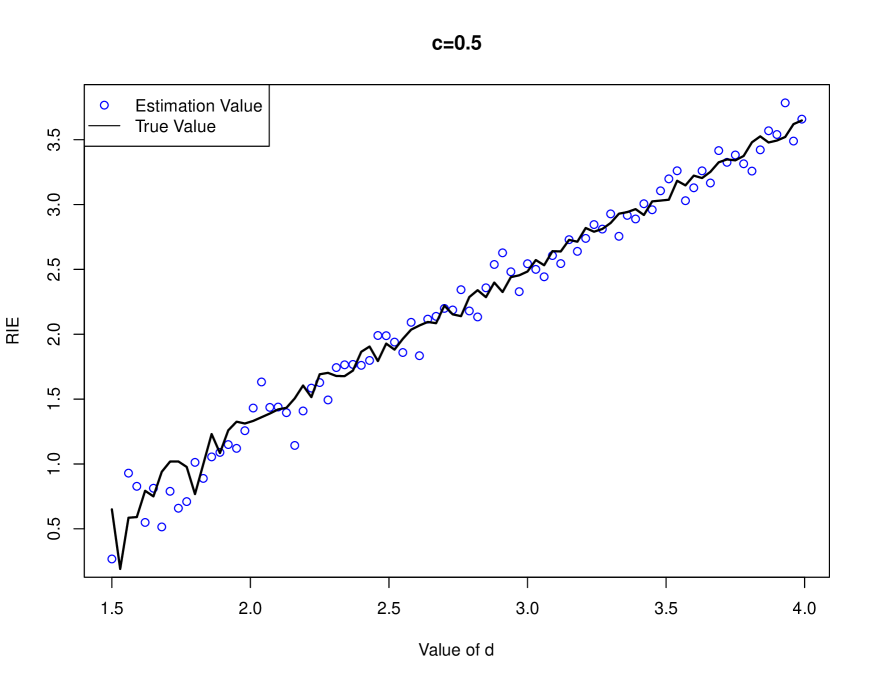

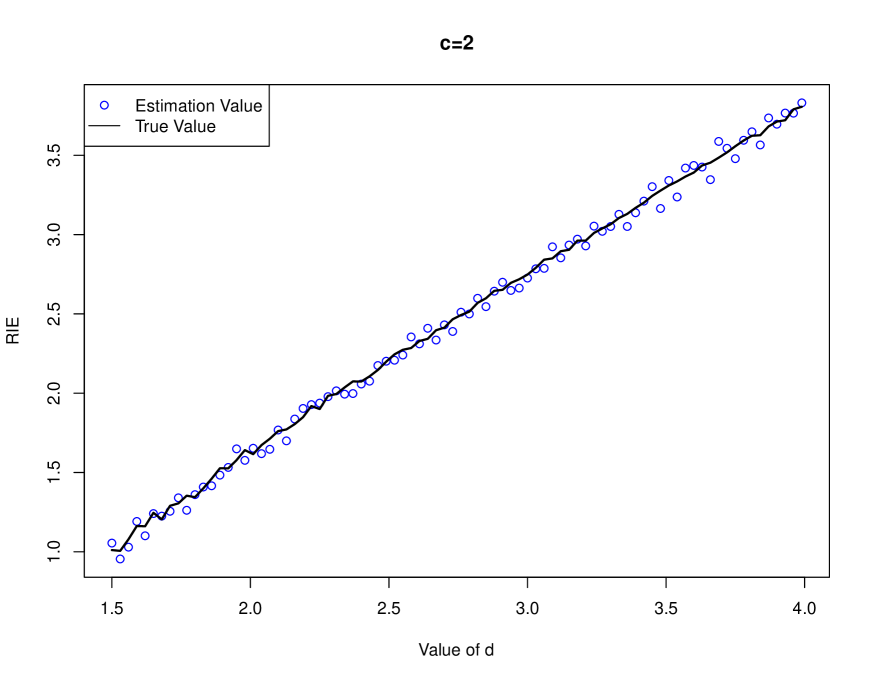

Figure 2 are two examples of the estimations of . From the graph, we find that our estimator is quite accurate. Figure 3 records the relative improvement in average loss (RIAL) compared to TSVD, where the RIAL is defined as

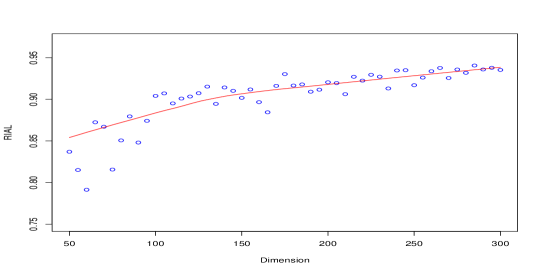

| (3.14) |

and where is the TSVD estimation and the RIE. We conclude from the figure that our method provides better estimation compared to the TSVD. Similar results have been shown for the estimation of covariance matrices by Ledoit and Péché in [23].

Remark 3.6.

In [14], Donoho and Gavish get similar results from the perspective of optimal shrinkage. However, they need two more assumptions: (1). they drop the last two error terms in (3.2) by assuming they are small enough (see Lemma 4 in their paper); (2). their estimators are assumed to be conservative, where they assume the shrinker vanishes when the sample singular values are below defined in (1.7), i.e., for some constant

However, we find that the estimator defined in (3.11) can still be consistent even without these assumptions.

4 Basic tools

In this section, we introduce some notations and tools which will be used in this paper. Recall that the empirical spectral distribution (ESD) of an symmetric matrix is defined as

We define the typical domain for by

| (4.1) |

where is a small constant. Recall (1.6), we assume that

Definition 4.1.

The Stieltjes transform of the ESD of is given by

where is defined in (1.8). Similarly, we can also define .

Denote be the Stieltjes transforms of limiting spectral distributions of . Using the identity we have

| (4.2) |

Definition 4.2.

Remark 4.3.

Recall (1.9) and by Schur’s complement [17], it is easy to check that

| (4.7) |

for defined in (1.8). Denote the index sets Then we have

Similarly, we denote where is defined in (1.9). Next we introduce the spectral decomposition of . By (4.7), we have

| (4.8) |

As we have seen in (2.6), the function plays a key role in describing the convergent limits of the outlier singular values of An elementary computation yields that attains its global minimum when and , and

| (4.9) |

To precisely locate the outlier singular values of we need to analyze

| (4.10) |

By (4.4) and (4.5), when we have

| (4.11) |

Next we collect the preliminary results of the properties of , whose proof will be provided in the supplementary material [7].

Lemma 4.4.

Suppose , then we have that there exist solutions of and they are write

| (4.12) |

Furthermore, denote

| (4.13) |

is a strictly monotone decreasing function when

For defined in (4.1), denote

| (4.14) |

By (4.11), it is easy to check that

| (4.15) |

The following lemma summarizes the basic properties of and , the estimates are based on the elementary calculations of (4.11) and (4.15). Their proofs can be found in [3, Lemma 3.3] and [4, Lemma 3.6].

Lemma 4.5.

The next lemma provides the local estimate on the derivative of on the real axis. We put its proof in the supplementary material [7].

Lemma 4.6.

For denote where is defined in (2.1). Then we have that

| (4.17) |

The following perturbation identity plays the key role in our proof, as it naturally provides us a way to incorporate the Green functions using a deterministic equation. Its proof can be found in [18, Lemma 6.1].

Lemma 4.7.

Recall (1.9), assume and , then if and only if

| (4.18) |

The following lemma establishes the connection between the Green functions of and defined in (1.9), which is proved in the supplementary material [7].

Lemma 4.8.

For we have

| (4.19) |

and

| (4.20) |

One of the key ingredients of our computation are the local laws. We firstly introduce the anisotropic local law, which can be found in [17, Theorem 3.6]. Denote

| (4.21) |

and as the unique solution of the equation

Recall (4.7), the following lemma shows that converges to a deterministic matrix with high probability.

Lemma 4.9.

Fix , then for all , with probability, for any unit deterministic vectors we have

| (4.22) |

where is defined as

| (4.23) |

It is notable that in general, depends on and Lemma 4.5 also holds for However, in our computation, we can replace with due to the following local MP law, which is proved in [29, Theorem 3.1].

Lemma 4.10.

Fix , then for all , with probability, we have

Beyond the support of the limiting spectrum of the MP law, we have stronger results all the way down to the real axis. More precisely, define the region

| (4.24) |

then we have the following stronger control on The proof can be found in [3, Theorem 3.12] and [17, Theorem 3.7].

Lemma 4.11.

For with probability, we have

for all unit vectors Similar result holds for Furthermore, for any deterministic vectors , we have

| (4.25) |

Denote the non-trivial classical eigenvalue locations of as , where is defined in (4.3). The consequent result of Lemma 4.9 is the rigidity of eigenvalues, which can be found in [4, Theorem 3.5].

Lemma 4.12.

Fix any small for with probability, we have

Furthermore, if the above estimate holds for all

5 Proofs of Theorem 2.2 and 2.3

5.1 Singular values

In this subection, we focus on the singular values of and prove Theorem 2.2. We will follow the basic idea of [18] and slightly modify the proof. A key deviation from their proof is that our matrix defined in (1.10) is not diagonal, it appears that in order to analyze (4.18), they only need to deal with the diagonal elements but we need to control the whole matrix. We will make use of the following interlacing theorem for rectangular matrices, the proof can be found in [35, Exercise 1.3.22].

Lemma 5.1.

For any matrices , denote as the -th largest singular value of , then we have

The proof relies on two main steps: (i) fix a configuration independent of , establish two permissible regions, of components and where the outliers of are allowed to lie in and each component contains precisely one eigenvalue and the non-outliers lie in ; (ii) a continuity argument where the result of (i) can be extended to arbitrary dependent .

The following matrix plays the key role in our analysis

| (5.1) |

By Lemma 4.7, if and only if Using Lemma 4.10 and 4.11, we find that , where is defined in (4.10). As behaves differently in and we will use different strategies to prove (2.7) and (2.8).

We remark that, our discussion is slightly easier than [18, Section 6], in particular the counting argument of the non-outliers. The reason is, for the application purpose, we only need the result of (2.8) to locate the eigenvalues around However, in [18], they have stronger results to stick the eigenvalues of around those of We will not pursue this generalization in this paper.

Proof of Theorem 2.2.

Denote and write

where we adapt the convention

Next we define the sets

| (5.2) |

| (5.3) |

and the sets of allowed which is Denote the following sequence of intervals

| (5.4) |

where satisfies the following condition

| (5.5) |

For we denote and , where satisfies .

For a first step, we show that is our permissible region which keeps track of the outlier eigenvalues of And the rest of the eigenvalues corresponding to will lie in We fix a configuration that is independent of in this step.

Lemma 5.2.

For any , with probability, we have

| (5.6) |

where is the set of the outlier eigenvalues of associated with Moreover, each interval contains precisely one eigenvalue of . Furthermore, we have

| (5.7) |

where is the set of the non-outlier eigenvalues corresponding to

Proof.

First of all, it is easy to check that using (4.9) and the fact . Denote In order to prove (5.6), we first consider the case when It is notable that by Lemma 4.12, (4.9) and (5.5). Recall (4.23) and (5.1), using the fact is bounded and Lemma 4.11, with probability, we have

| (5.8) |

It is well-known that if then therefore, we have that for defined in (4.1). Recall (4.10), by (4.9), (4.17) and (5.5), with probability, we have

| (5.9) |

Using the formula

Lemma 4.10, (4.6) and (5.8), we conclude that

| (5.10) |

Next we will use Roché’s theorem to show that inside the permissible region, each interval contains precisely one eigenvalue of . Let and pick a small -independent counterclockwise (positive-oriented) contour that encloses but no other . For large enough define By the definition of determinant, the functions are holomorphic on and inside And has precisely one zero inside On it is easy to check that

where we use (5.8) and Lemma 4.10. Hence, has only one zero in according to Rouché’s theorem. This concludes the proof of (5.6) using Lemma 4.7. In order to prove (5.7), using the following fact: for any two rectangular matrices , we have and Lemma 4.12, we find that

| (5.11) |

For the non-outliers, we assume that otherwise the proof is already done. Now we assume by (5.6) and (5.11), we only need to discuss the case when In this case, we will prove that is non-singular by comparing with where and is some small positive constant. Denote the spectral decomposition of as

Denote as the -th column in defined in (1.10) and abbreviate as and using spectral decomposition and the fact we have

Therefore, by Lemma 4.10 and 4.11, with probability, we have

Using Lemma 4.5 and a similar discussion to (5.9), we have

By Lemma 4.5 and 4.10, we find that where we use the assumption that Therefore, is non-singular as we have assumed . This concludes the proof of (5.7). ∎

In the second step, we will extend the proof to any configuration depending on using the continuity argument. This is done by a bootstrap argument by choosing a continuous path connecting and . It is recorded as the following lemma and its proof will be provided in the supplementary material [7].

∎

5.2 Singular vectors

In this section, we focus on the local behavior of singular vectors. We will follow the discussion of [4, Section 5 and 6]. We first deal with the outlier singular vectors and then the non-outlier ones. Due to similarity, we only prove (2.11) and (2.13), (2.10) and (2.12) can be handled similarly.

Proof of (2.11).

It is notable that, by Lemma 4.11 and Theorem 2.2, for there exists a constant for large enough, with probability , we can choose an event such that for all defined in (4.24)

| (5.12) |

Next we will restrict our discussion on the event Recall (2.5) and for , we define for each the radius

| (5.13) |

Under the assumption of (2.4), we have (see the equation (5.10) of [4])

| (5.14) |

We define the contour as the boundary of the union of discs , where is the open disc of radius around We summarize the basic properties of as the following lemma, its proof can be found in [4, Lemma 5.4 and 5.5].

Lemma 5.4.

Armed with the above results, we now start the proof of the outlier singular vectors. Our starting point is an integral representation of the singular vectors. By (4.7), we have

| (5.15) |

where is the natural embedding of with . Recall (2.3), using the spectral decomposition of Lemma 5.4 and Cauchy’s integral formula, we have

| (5.16) |

By Lemma 4.8, Cauchy’s integral formula, (5.15) and (5.16), we have

| (5.17) |

where are defined as Recall (4.23), as is of finite dimension, by Lemma 4.10, 4.11, (4.6) and (5.12), we can now use as

Next we decompose by

| (5.18) |

It is notable that can be controlled by Lemma 4.10 and 4.11. Using the resolvent expansion to the order of one on (5.18), we have

| (5.19) |

where

By an elementary computation, we have

| (5.20) |

Using the fact and the residual theorem, we have

| (5.21) |

Next we control the term Applying (5.20) on , we have

| (5.22) |

where and are defined as

We now use the change of variable as in (5.16) and rewrite as

where we use the fact By (4.9), Lemma 4.5 and 4.11, we conclude that

| (5.23) |

Denote

As is holomorphic inside the contour by Cauchy’s differentiation formula, we have

| (5.24) |

where the contour is the circle of radius centered at Hence, by (4.9), (5.23), (5.24) and the residual theorem, we have

| (5.25) |

In order to estimate we consider the following three cases (i) (ii) (or ), (iii) . By the residual theorem, when case (iii) happens. Hence, we only need to consider the cases (i) and (ii). For the case (i), when , by the residual theorem and (5.25), we have

When , by the residual theorem, we have For the case (ii), when , by the residual theorem and (5.12), we have

We can get similar results when Putting all the cases together, we find that

| (5.26) |

Finally, we need to estimate Here the residual calculations can not be applied directly as is not necessary to be diagonal and a relation comparable to does not exist. Instead, we need to precisely choose the contour We record the result as the following lemma, whose proofs will be given in the supplementary material [7].

Lemma 5.5.

When is large enough, with probability, for some constant we have

| (5.27) |

Therefore, plugging (5.21), (5.2) and (5.51) into (5.19), we conclude the proof of (2.11). Before concluding this subsection, we briefly discuss the proof of (2.10). By Lemma 4.8 and Cauchy’s integral formula , we have

Then we can use a similar discussion as (5.19), computing the convergent limit from and controlling the bounds for and We remark that the convergent limit is different because we use in (5.20), which results in

This concludes the proof of (2.10). ∎

For the non-outliers, the proof strategy for the outlier singular vectors will not work as we cannot use the residual theorem. We will use a spectral decomposition for our proof.

Proof of (2.13).

Denote

| (5.28) |

where is defined as the smallest solution of

| (5.29) |

As we assume or we conclude that has a constant lower bound. Therefore, by Lemma 4.9, 4.10 and 4.11, with probability, we have

| (5.30) |

Recall (4.14), abbreviating by Lemma 4.5 and (2.8), we find that (see [4, (6.5) and (6.6)])

| (5.31) |

For defined in (5.28), by the spectral decomposition, we have

| (5.32) |

where is the natural embedding of By Lemma 4.8, we have

Similar to (5.19), using a simple resolvent expansion and (5.20) , we have

| (5.33) |

where is defined in (5.22). To estimate the right-hand side of (5.2), we use the following error estimate

where we use (5.30) and Lemma 4.10. By a similar resolvent expansion, there exists some constant such that

We therefore get from (5.2), the definition of and (5.30) that

| (5.34) |

By (5.32), we have

| (5.35) |

By (4.16), (5.29) and (5.31), we have

For the other item, by Lemma 4.5, we have Putting all these estimates together, we have

The rest of the proof leaves to give an estimate of We summarize it as the following lemma and put its proof in the supplementary material [7].

Lemma 5.6.

Recall (4.3), for all there exists a constant such that

Therefore, we have

where we use the fact that (see the equation (6.14) of [4]). This concludes the proof of (2.13). For the proof of (2.12), we will use the spectral decomposition

and

Then by the resolvent expansion similar to (5.2) and control the items using Lemma 4.5, 4.9, 4.10 and 4.11, we can conclude the proof. ∎

Acknowledgements.

The author would like to thank Zhigang Bao, Jeremy Quastel, Bálint Virág, Ke Wang and Zhou Zhou for fruitful discussions and valuable suggestions, which have greatly improved the paper. The author is also grateful to an anonymous referee, the associated editor and editor for providing detailed and constructive suggestions and comments, which have improved the paper significantly.

Supplementary material

References

- [1] J. Baik, G. Ben Arous, and S. Péché. Phase transition of the largest eigenvalue for nonnull complex sample covariance matrices. Ann. Prob., 33:1643–1697, 2005. \MR2165575

- [2] F. Benaych-Georges and R. Nadakuditi. The singular values and vectors of low rank perturbations of large rectangular random matrices. J. Multivar. Anal., 227:494–521, 2011. \MRMR2944410

- [3] A. Bloemendal, L. Erdős, A. Knowles, H.-T. Yau, and J. Yin. Isotropic local laws for sample covariance and generalized Wigner matrices. Electron. J. Probab., 19:1–53, 2014. \MRMR3183577

- [4] A. Bloemendal, A. Knowles, H.-T. Yau, and J. Yin. On the principal components of sample covariance matrices. Prob. Theor. Rel. Fields, 164:459–552, 2016. \MRMR3449395

- [5] J. Bun, R. Allez, J. Bouchaud, and M. Potters. Rotational invariant estimator for general noisy matrices. IEEE Trans. Inf. Theory, 62:7475–7490, 2016. \MRMR3599095

- [6] J. Bun, J.-P. Bouchaud, and M. Potters. Cleaning large correlation matrices: Tools from random matrix theory. Physics Reports, 666:1–109, 2017. \MRMR3590056

- [7] X. Ding. Supplement to ”High dimensional deformed rectangular matrices with applications in matrix denoising,” 2019.

- [8] X. Ding. Singular vector distribution of covariance matrices. Advances in Applied Probability (In press), 2019.

- [9] X. Ding. Asymptotics of empirical eigen-structure of general covariance matrices. arXiv: 1708.06296, 2017.

- [10] X. Ding and F. Yang. A necessary and sufficient condition for edge universality at the largest singular values of covariance matrices. Ann. Appl. Probab., 28: 1679-1738, 2018. \MRMR3809475.

- [11] D. Donoho. De-noising by soft-thredholding. IEEE Trans. Inf. Theory, 41:613–627, 1995. \MRMR1331258

- [12] M. Elad. Sparse and redundant representations: from theory to applications in signal and image processing. Springer, 2010. \MRMR2677506

- [13] M. Gavish and D. Donoho. The optimal hard threshold for singular values is . IEEE Trans. Inf. Theory, 60:5040–5053, 2014. \MRMR3245370

- [14] M. Gavish and D. Donoho. Optimal shrinkage of singular values. IEEE Trans. Inf. Theory, 63:2137–2152, 2017. \MRMR3626861

- [15] G. Golub and C. Van Loan. Matrix computation, 3rd edition. The Johns Hopkins University Press, 1996. \MRMR1417720

- [16] G. James, D. Witten, T. Hastie, and R. Tibshirani. An Introduction to Statistical Learning. Springer, 2013. \MRMR3100153

- [17] A. Knowles and J. Yin. Anisotropic local laws for random matrices. Probability Theory and Related Fields, 169: 257–352, 2017.

- [18] A. Knowles and J. Yin. The isotropic semicircle law and deformation of Wigner matrices. Comm. Pure Appl. Math., 11:1663–1749, 2013. \MRMR3103909

- [19] A. Knowles and J. Yin. The outliers of a deformed Wigner matrix. Ann. Probab., 5:1980–2031, 2014. \MRMR3262497

- [20] L. Laloux, P. Cizeau, M. Potters, and J. Bouchaud. Random matrix theory and financial correlations. Int. J. Theor. Appl. Finan., 3:391–397, 2000.

- [21] C. Lam, and Q. Yao. Factor modeling for high-dimensional time series: Inference for the number of factors. Ann. Statist. , 40:694–726, 2012. \MRMR2933663

- [22] M. Lee, H. Shen, J. Huang, and J. Marron. Biclustering via sparse singular value decomposition. Biometrics, 66:1087–1095, 2010. \MRMR2758496

- [23] O. Ledoit, and S. Péché. Eigenvectors of some large sample covariance matrix ensembles. Probab. Theory Related Fields, 151:233–264, 2011. \MRMR2834718

- [24] V. A. Marčenko and L. A. Pastur. Distribution of eigenvalues for some sets of random matrices. Mathematics of the USSR-Sbornik, 1:457, 1967.

- [25] R. Rao Nadakuditi. OptShrink: an algorithm for improved low-rank signal matrix denoising by optimal, data-driven singular value shrinkage. IEEE Trans. Inform. Theory, 60: 3002–3018, 2014. \MRMR3200641

- [26] R. Rao Nadakuditi and A. Edelman. Sample Eigenvalue Based Detection of High-Dimensional Signals in White Noise Using Relatively Few Samples. IEEE Trans. Signal Process., 56: 2625 – 2638, 2008. \MRMR1500236

- [27] D. Paul. Asymptotics of sample eigenstructure for a large dimensional spiked covariance model. Statist. Sinica, 17:1617–1642, 2007. \MRMR2399865

- [28] D. Passemier, and J. Yao. Estimation of the number of spikes, possibly equal, in the high-dimensional case. J. Multivariate Anal. , 127:173–183, 2014. \MRMR3188885

- [29] N. S. Pillai and J. Yin. Universality of covariance matrices. Ann. Appl. Probab., 24:935–1001, 2014. \MRMR3199978

- [30] A. Pizzo, D. Renfrew, and A. Soshnikov. On finite rank deformations of Wigner matrices. Ann. Inst. Henri Poincaré Probab. Stat. , 49:64–94, 2013. \MRMR3060148

- [31] B. Pontes, R. Giráldez, and J. Aguilar-Ruiz. Biclustering on expression data: A review. J. Biomed. Inform., 57:163–180, 2015.

- [32] D. Renfrew and A. Soshnikov. On finite rank deformations of Wigner matrices II: Delocalized Perturbations. Random Matrices Theory Appl., 2:1250015, 2013. \MRMR3039820

- [33] J. W. Silverstein. The Stieltjes transform and its role in eigenvalue behavior of large dimensional random matrices. Random Matrix Theory and its Applications, Lecture Notes Series. World Scientific, Singapore, 2009. \MRMR2603192

- [34] D. Sun and J. Sun. Strong semismoothness of eigenvalues of symmetric matrices and its application to inverse eigenvalue problem. SIAM J. Numer. Anal., 40:2352-2367, 2003.

- [35] T. Tao. Topics in Random Matrix Theory. American Mathematical Society, 2012. \MRMR2906465

- [36] C. Tracy and H. Widom. On orthogonal and symplectic matrix ensembles. Comm. Math. Phys., 177:727–754, 1996. \MRMR1385083

- [37] D. Tufts and A. Shah. Estimation of a signal waveform from noisy data using low-rank approximation to a data matrix. IEEE Trans. Sig. Proc., 41:7475–7490, 1993.

- [38] D. Yang, Z. Ma, and A. Buja. Rate optimal denoising of simultaneously sparse and low rank matrices. J. Mach. Learn. Res., 17:1–27, 2016. \MRMR3543498

Supplement to ”High dimensional deformed rectangular matrices with applications in matrix denoising”

Proof of Proposition 3.3.

For under the assumptions of Theorem 2.2 and Assumption 3.2 of the paper, with probability, we have that

Using Assumption 3.2 of the paper, with probability, we have that

| (5.36) |

And for with probability, we have that

| (5.37) |

By definition, we have that

| (5.38) |

Under Assumption 3.2 and the fact that is sufficiently small, for we can conclude our proof using (5.36), (5.37) and (Proof of Proposition 3.3.). ∎

Proof of Theorem 3.4.

Denote we have

It is easy to check that

| (5.39) |

where is defined as The first term on the right-hand side of (5.39) is bounded by using equation (2.8) of the paper. For the second term, we only need to control and by Cauchy-Schwarz inequality. Due to similarity, we only prove for the right singular vectors.

Under the sparsity assumption, the non-zero entries of are confined on a block matrix of some fixed dimension Denote if our algorithm can correctly choose the positions of the non-zero entries of (i.e. ) with probability, we can conclude our proof using the fact (see [34, Lemma 4.3])

where are the right singular vectors of respectively. Therefore, under the assumption that is of variance we have that with probability, This concludes our proof.

The rest of the proof leaves to show that equation (3.3) of the paper can correctly find the positions of the non-zero entries (i.e. ) with probability, which is summarized as the following lemma and we will put its proof in the supplementary material.

Lemma 5.7.

For denote as the index set of the non-zero entries of for some constant there exists some with probability, we have

By Lemma 5.7, we have that with probability, which implies that Algorithm 1 can correctly recover the sparse structure of the singular vectors. Finally, we prove Lemma 5.7.

Proof of Lemma 5.7.

For definiteness, we assume that is non-negative. By (3.9) of the paper, it is easy to check that with probability, we have

| (5.40) |

where we use the fact that is sparse and Markov inequality. When assume that using (5.40) and Markov inequality, we conclude that

which is a contradiction. Hence, for all we have When (5.40) reads as

| (5.41) |

where we use Definition 2.1 of the paper. Assume that denote as the minor of by deleting the -th columns with and as the subvector of by deleting the entries with indices in As by (5.41), with probability, we have

This yields that

Using Rayleigh quotient and the continuity of eigenvalues, when is large enough, we conclude that with probability

which is a contradiction by (2.8) of the paper. Here we use the fact is a sample covariance matrix satisfying the MP law. Hence, for all we have ∎

∎

Proof of Theorem 3.5.

We start with the proof of (1). The consistency of is an immediate result of [2, Theorem 2.9]. For the convergent rate, by definition

Hence, the proof follows from Theorem 2.2 and 2.3 of the paper. Next, we prove (2). Using a similar discussions to equations (3.9) and (3.10) of the paper, for some constant with probability, we have

where we use Theorem 2.2 and 2.3 of the paper and (1) of Theorem 3.5. Therefore, the proofs come from part (1) of Theorem 3.5 and Proposition 3.3 of the paper. ∎

Proof of Lemma 4.4.

(4.12) of the paper is from an elementary calculation. For the proof of (4.13) and its monotonicity, choose any we have

where When we have

where we need to ensure the positiveness of . Hence, by the mean value theorem, we conclude the proof. ∎

Proof of Lemma 4.6.

By an elementary computation on (4.13) of the paper , we have

It is easy to check that there exists a constant such that for This concludes our proof by mean value theorem.

∎

Proof of Lemma 4.8.

To prove (4.19) of the paper, we write

The proof follows from the Woodbury matrix identity

with For the proof of (4.20), by (4.19) of the paper, we have

the proof follows from the following identity

with ∎

Proof of Lemma 5.3.

We first deal with (3.6). As is finite, we can choose a path connecting and having the following properties:

(i) For all , the point .

(ii) If for a pair then for all

Denote where is a diagonal matrix with elements As the mapping is continuous, we find that is continuous in for all where are the eigenvalues of Moreover, by Lemma 5.2 of the paper, we have

| (5.42) |

In the case when the intervals are disjoint, we have

where we use property (ii) of the continuous path, (5.42) and the continuity of In particular, it holds true for Now we consider the case when they are not disjoint. Define as a partition of and denote the equivalent relation as

Therefore, we can decompose It is notable that each contains a sequence of consecutive integers. Choose any without loss of generality, we assume is not the smallest element in Since they are not disjoint, we have

where we use the fact that and (5.4) of the paper. This implies that

for some constant By (5.5) of the paper, we have

Therefore, by repeating the process for the remaining we find

where we use the fact that This immediately yields that

for some constant This completes the proof of (3.6) of the paper. Finally, we deal with the extremal non-outlier eigenvalues (3.7) of the paper. By the continuity of and Lemma 5.2 of the paper, we have

| (5.43) |

In particular it holds true for This concludes our proof. ∎

Proof of Lemma 5.5.

A crucial estimate is the following lemma, which can be found in [4, Lemma 5.6]. Define the boundary of as then we have

Lemma 5.8.

Denote

then for , and , recall (5.13) of the paper, we have

| (5.44) |

By (4.9), (5.12) of the paper and the fact is finite, it is easy to check that

| (5.45) |

We now assume by the resolvent expansion, we have

| (5.46) |

By (5.12) of the paper, we have

| (5.47) |

For by Lemma 4.6 and (4.9) of the paper, there exists some constant , such that

| (5.48) |

where in the last step we use (5.14) of the paper. Hence, by (5.20) of the paper, (Proof of Lemma 5.5.) and (5.47), we have

| (5.49) |

Decomposing into , by (5.44), (5.45), (5.49) and the fact has length , we have

| (5.50) |

for some constant To estimate the right-hand side of (5.50), for by (5.14) of the paper, we have that

from which we conclude

where we use the fact that is finite. Similarly, for we have . Combining with the fact for all , we have

for some constant Combine with (5.50), we have

| (5.51) |

for some constant ∎

Proof of Lemma 5.6.

In the case we have that (see the equation above (6.11) of [4])

By [4, (6.11)], we have that for any

| (5.52) |

For by Lemma 4.5 and (5.31) of the paper, using in (5.52), we find that there exists some constant such that

When choosing in (5.52) and using (5.31) of the paper, we get

When by Lemma 4.5 of the paper, for we have

∎