Sketchy Decisions: Convex Low-Rank Matrix Optimization

with Optimal Storage

Including supplementary appendix

Alp Yurtsever Madeleine Udell Joel A. Tropp Volkan Cevher EPFL Cornell Caltech EPFL

Abstract

This paper concerns a fundamental class of convex matrix optimization problems. It presents the first algorithm that uses optimal storage and provably computes a low-rank approximation of a solution. In particular, when all solutions have low rank, the algorithm converges to a solution. This algorithm, SketchyCGM, modifies a standard convex optimization scheme, the conditional gradient method, to store only a small randomized sketch of the matrix variable. After the optimization terminates, the algorithm extracts a low-rank approximation of the solution from the sketch. In contrast to nonconvex heuristics, the guarantees for SketchyCGM do not rely on statistical models for the problem data. Numerical work demonstrates the benefits of SketchyCGM over heuristics.

1 MOTIVATION

This paper discusses a fundamental class of convex matrix optimization problems with low-rank solutions. We argue that the main obstacle that prevents us from solving these problems at scale is not arithmetic, but storage. We exhibit the first provably correct algorithm for these problems with optimal storage.

1.1 Vignette: Matrix Completion

To explain the challenge, we consider the problem of low-rank matrix completion.

Let be an unknown matrix, but assume that a bound on the rank of is available, where . Suppose that we record noisy observations of a subset of entries from the matrix:

The variables model (unknown) noise. The goal is to approximate the full matrix .

Matrix completion arises in machine learning applications, such as recommendation systems [34].

We can frame the matrix completion problem as a rank-constrained optimization:

| (1) |

In general, the formulation (1) is intractable. Instead, we retrench to a tractable convex problem [34, 7]:

| (2) |

The Schatten -norm returns the sum of the singular values of its argument; it is an effective proxy for the rank [13]. Adjusting the value of the parameter modulates the rank of a solution of (2). If we have enough data and choose well, we expect that each solution approximates the target matrix .

The convex problem (2) is often a good model for matrix completion when the number of observations , where suppresses log-like factors; see [34, 7]. We can write a rank- approximation to a solution using parameters. Thus, we can express the problem and an approximate solution with storage.

Nevertheless, we need fully numbers to express the decision variable for the optimization problem (2). The cost of storing the decision variable prevents us from solving large-scale instances of (2), even without worrying about arithmetic.

This discrepancy raises a question: Is there an algorithm that computes an approximate solution to (2) using the optimal storage ?

1.2 Vignette: Phase Retrieval

Here is another instance of the same predicament.

Fix a vector . Suppose that we acquire noisy quadratic measurements of with the form

| (3) |

The are known measurement vectors, and the model measurement noise. Given the data and the vectors , the phase retrieval problem asks us to reconstruct up to a global phase shift.

Phase retrieval problems are prevalent in imaging science because it is easier to measure the intensity of light than its phase. In practice, the vectors are structured because they reflect the physics of the imaging system. For more details, see Appendix B.3 and the examples in [3, 10, 8, 22].

Let us outline a convex approach [3, 10, 8, 22] to the phase retrieval problem. The data (3) satisfies

Thus, we can formulate phase retrieval as

| (4) | ||||||

| s.t. |

Now, pass to the convex problem

| (5) | ||||||

| s.t. |

We can estimate the parameter from and ; see [39, Sec. II]. To approximate the true vector , we compute a top eigenvector of a solution to (5).

This procedure is often an effective approach for phase retrieval when the number of measurements ; see [36, Sec. 2.8]. Once again, we recognize a discrepancy. The problem data and the approximate solution use storage , but the matrix variable in (5) requires storage.

We may ask: Is there an algorithm that computes an approximate solution to (5) using the optimal storage ?

1.3 Low-Rank Matrix Optimization Methods

Matrix completion and phase retrieval are examples of convex low-rank matrix optimization (CLRO) problems. Informally, this class contains convex optimization problems whose decision variable is a matrix and whose solutions are (close to) low rank. These problems often arise as convex relaxations of rank-constrained problems; however, the convex formulations are important in their own right.

There has been extensive empirical and theoretical work to validate the use of CLROs in a spectrum of applications. For example, see [16, 13, 7, 8, 22].

Over the last 20 years, optimization researchers have developed a diverse collection of algorithms for CLRO problems. Surprisingly, every extant method lacks guarantees on storage or convergence (or both).

Convex optimization algorithms dominated the early literature on algorithms for CLRO. The initial efforts, such as [21], focused on interior-point methods, whose storage and arithmetic costs are forbidding. To resolve this issue, researchers turned to first-order convex algorithms, including bundle methods [20], (accelerated) proximal gradient methods [32, 2, 35], and the conditional gradient method (CGM) [15, 25, 19, 11, 23].

Convex algorithms are guaranteed to solve a CLRO. They come with a complete theory, including rigorous stopping criteria and bounds on convergence rates. They enjoy robust performance in practice. On the other hand, convex algorithms from the literature do not scale well enough to solve large CLRO problems because they operate on and store full-size matrices.

The CGM iteration is sometimes touted as a low-storage method for CLRO [23]. Indeed, CGM is guaranteed to increase the rank of an iterate by at most one per iteration. Nevertheless, the algorithm converges slowly, so intermediate iterates can have very high rank. CGM variants, such as [31, 39], that control the rank of iterates lack storage guarantees or may not converge to a global optimum.

Recently, many investigators have sought recourse in nonconvex heuristics for solving CLROs. This line of work depends on the factorization idea of Burer & Monteiro [6], which rewrites the matrix variable as a product of two low-rank factors. There are many heuristic procedures, e.g., [6, 24, 4, 5], that use clever initialization and nonlinear programming schemes in an attempt to optimize the factors directly. The resulting algorithms can have optimal storage costs, and they may achieve a fast rate of local convergence.

There has been an intensive effort to justify the application of nonconvex heuristics for CLRO. To do so, researchers often frame unverifiable statistical assumptions on the problem data. For example, in the matrix completion problem (2), it is common to assume that the entries of the matrix are revealed according to some ideal probability distribution [24, 7]. When these assumptions fail, nonconvex heuristics can converge to the wrong point, or they may even diverge.

Contributions. This paper explains how to extend the convex optimization algorithm CGM to obtain an approximate solution to a class of CLRO problems using optimal storage. Our algorithm operates much like CGM, but it never forms the matrix variable explicitly. Instead, we maintain a small randomized sketch of the matrix variable over the course of the iteration by means of a bespoke sketching method [37]. After the optimization method converges, we extract an approximate solution from the sketch. This technique achieves optimal storage, yet it converges under the same conditions and with the same guarantees as CGM.

In summary, this paper presents a solution to the problems posed above: the first algorithm for convex low-rank matrix optimization problems that provably uses optimal storage to compute an approximate solution.

1.4 Notation

We write for the Euclidean norm, for the Frobenius norm, and for the Schatten 1-norm (aka the trace norm or the nuclear norm). Depending on context, refers to the Euclidean or Frobenius inner product. The symbol ∗ denotes the conjugate transpose of a vector or matrix, as well as the adjoint of a linear map. The dagger † refers to the pseudoinverse. The symbol stands for a best rank- Frobenius-norm approximation of the matrix . The function returns the minimum Frobenius-norm distance from to a set . The symbol denotes the semidefinite order. We use the computer science interpretation of the order notation .

2 A LOW-RANK MATRIX OPTIMIZATION PROBLEM

Let us begin with a generalization of the convex matrix completion formulation (2). In §5.5, we return to the psd setting of the phase retrieval problem (5).

We consider a convex program with a matrix variable:

| (6) |

The linear operator and its adjoint take the form

| (7) | ||||

Each coefficient matrix .

We interpret as a set of linear measurements of the matrix . For example, in the matrix completion problem (2), the image lists the entries of indexed by the set .

The function is convex and continuously differentiable. In many situations, it is natural to regard the objective function as a loss: for a vector of measured data.

By choosing the parameter to be sufficiently small, we can often ensure that each minimizer of (6) is low-rank or close to low-rank.

Our goal is to develop a practical algorithm that provably computes a low-rank approximation of a solution to the problem (6).

To validate (6) as a model for a given application, one must undertake a separate empirical or theoretical study. We do not engage this question in our work.

2.1 Storage Issues

Suppose that we want to produce a low-rank approximation to a solution of a generic instance of the problem (6). What kind of storage can we hope to achieve?

It is clear that we need numbers to express a rank- approximate solution to (6). We must also understand how much extra storage is incurred because of the specific problem instance .

It is natural to instate a black-box model for the linear map , its adjoint , and the objective function . For arbitrary vectors and and , assume we have routines that can compute

| (8) |

We also assume routines for evaluating the function and its gradient for any argument . We may neglect the storage used to compute these primitives. Every algorithm based on these primitives must use storage just to represent their outputs.

Thus, under the black-box model, any algorithm that produces a rank- solution to a generic instance of (6) must use storage . We say that an algorithm is storage optimal if it achieves this bound.

The parameter often reflects the amount of data that we have acquired, and it is usually far smaller than the dimension of the matrix variable in (6).

The problems that concern us are data-limited; that is, . This is the situation where a strong structural prior (e.g., low rank or small Schatten 1-norm) is essential for fitting the data. This challenge is common in machine learning problems (e.g., matrix completion for recommendation systems), as well as in scientific applications (e.g., phase retrieval).

To the best of our knowledge, no extant algorithm for (6) is guaranteed to produce an approximation of an optimal point and also enjoys optimal storage cost.

3 CONDITIONAL GRADIENT

To develop our algorithm for the model problem (6), we must first describe a standard algorithm called the conditional gradient method (CGM). Classic and contemporary references include [15, 25, 19, 11, 23].

3.1 The CGM Iteration

Here is the CGM algorithm for (6). Start with a feasible point, such as

| (9) |

At each iteration , compute an update direction using the formulas

| (10) | ||||

MaxSingVec returns a left/right pair of maximum singular vectors. Update the decision variable:

| (11) |

where . The convex combination (11) remains feasible for (6) because and are feasible.

CGM is a valuable algorithm for (6) because we can efficiently find the rank-one update direction by means of the singular vector computation (10). The weak point of CGM is that the rank of typically increases with , and the peak rank of an iterate is often much larger than the rank of the solution of (6). See Figures 6 and 7 for an illustration.

3.2 The CGM Stopping Rule

The CGM algorithm admits a simple stopping criterion. Given a suboptimality parameter , we halt the CGM iteration when the duality gap :

| (12) |

Let be an optimal point for (6). It is not hard to show [23, Sec. 2] that

| (13) |

Thus, the condition (12) ensures that the objective value is -suboptimal. The CGM iterates satisfy (12) within iterations [23, Thm. 1].

3.3 The Opportunity

The CGM iteration (9)–(11) requires storage because it maintains the matrix decision variable . We develop a remarkable extension of CGM that provably computes a rank- approximate solution to (6) with working storage . Our approach depends on two efficiencies:

-

•

We use the low-dimensional “dual” variable to drive the iteration.

-

•

Instead of storing , we maintain a small randomized sketch with size .

It is easy to express the CGM iteration in terms of the “dual” variable . We can obviously rewrite the formula (10) for computing the rank-one update direction in terms of . We obtain an update rule for by applying the linear map to (11). Likewise, the stopping criterion (12) can be evaluated using and . Under the black-box model (8), the dual formulation of CGM has storage cost .

Yet the dual formulation has a flaw: it “solves” the problem (6), but we do not know the solution!

4 MATRIX SKETCHING

Suppose that is a matrix that is presented to us as a stream of linear updates, as in (11). For a parameter , we wish to maintain a small sketch that allows us to compute a rank- approximation of the final matrix . Let us summarize an approach developed in our paper [37].

4.1 The Randomized Sketch

Draw and fix two independent standard normal matrices and where

| (14) |

The sketch consists of two matrices and that capture the range and co-range of :

| (15) |

We can efficiently update the sketch to reflect a rank-one linear update to of the form

| (16) |

Both the storage cost for the sketch and the arithmetic cost of an update are .

4.2 The Reconstruction Algorithm

The following procedure yields a rank- approximation of the matrix stored in the sketch (15).

| (17) |

The matrix has orthonormal columns that span the range of . The extra storage costs of the reconstruction are negligible; its arithmetic cost is . See [37, §4.2] for the intuition behind this method. It achieves the following error bound.

Theorem 1 (Reconstruction error [37, Thm. 5.1]).

5 SKETCHING + CGM

We are now prepared to present SketchyCGM, a storage-optimal extension of the CGM algorithm for the convex problem (6). This method delivers a provably accurate low-rank approximation to a solution of (6). See Algorithm 1 for complete pseudocode.

5.1 The SketchyCGM Iteration

Fix the suboptimality and the rank . Draw and fix standard normal matrices and as in (14). Initialize the iterate and the sketches:

| (18) |

At each iteration , compute an update direction via Lanczos or via randomized SVD [17]:

| (19) | ||||

Set the learning rate . Update the iterate and the two sketches:

| (20) | ||||

The iteration continues until it triggers the stopping criterion:

| (21) |

At any iteration , we can form a rank- approximate solution of the model problem (6) by invoking the procedure (17) with and .

5.2 Guarantees

Suppose that the CGM iteration (9)–(11) generates the sequence of decision variables and the sequence of update directions. It is easy to verify that the SketchyCGM iteration (18)–(20) maintains the loop invariants

| (22) |

In view of the inequality (13) and the invariant (22), the stopping rule (21) ensures that is an -suboptimal solution to (6) when the iteration halts. Furthermore, Theorem 1 ensures that the computed solution is a near-optimal rank- approximation of at each time .

5.3 Storage Costs

The total storage cost is for the dual variable , the random matrices , and the sketch . Owing to the black-box assumption (8), the algorithm completes the singular vector computations in (19) with working storage. At no point during the iteration do we instantiate an matrix! Arithmetic costs are on the same order as the standard version of CGM.

5.4 Convergence Results for SketchyCGM

SketchyCGM is a provably correct method for computing a low-rank approximation of a solution to (6).

Theorem 2.

SketchyCGM always works in the fundamental case where each solution of (6) has low rank.

Theorem 3.

Suppose that the solution set of the problem (6) contains only matrices with rank or less. Then SketchyCGM attains .

Suppose that the optimal point of (6) is stable in the sense that the value of the objective function increases as we depart from optimality. Then the SketchyCGM estimates converge at a controlled rate.

Theorem 4.

See Appendix A for the proofs of these results.

5.5 SketchyCGM for PSD Optimization

Next, we present a generalization of the convex phase retrieval problem (5). Consider the convex template

| (24) |

As before, is a linear map, and is a differentiable convex function.

It is easy to adapt SketchyCGM to handle (24) instead of (6). To sketch the complex psd matrix variable, we follow the approach described in [37, Sec. 7.3]. We also make small changes to the SketchyCGM iteration. Replace the computation (19) with

MinEig returns the minimum eigenvalue and an associated eigenvector of a conjugate symmetric matrix. This variant behaves the same as SketchyCGM.

6 COMPUTATIONAL EVIDENCE

In this section, we demonstrate that SketchyCGM is a practical algorithm for convex low-rank matrix optimization. We focus on phase retrieval problems because they provide a dramatic illustration of the power of storage-optimal convex optimization. Appendix B adduces additional examples, including some matrix completion problems.

6.1 Synthetic Phase Retrieval Problems

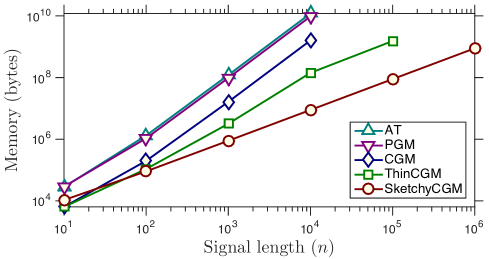

To begin, we show that our approach to solving the convex phase retrieval problem (5) has better memory scaling than other convex optimization methods.

We compare five convex optimization algorithms: the classic proximal gradient method (PGM) [32]; the Auslender–Teboulle (AT) accelerated method [2]; the classic CGM algorithm [23]; a storage-efficient CGM variant (ThinCGM) [39] based on low-rank SVD updating; and the psd variant of SketchyCGM from §5.5 with rank parameter .

All five methods solve (24) reliably. The proximal methods (PGM and AT) perform a full eigenvalue decomposition of the iterate at each step, but they can be accelerated by adaptively choosing the number of eigenvectors to compute. The methods based on CGM only need the top eigenvector, so they perform less arithmetic per iteration.

To compare the storage costs of the five algorithms, let us consider a synthetic phase retrieval problem. We draw a vector from the complex standard normal distribution. Then we acquire phaseless measurements (3), corrupted with independent Gaussian noise so that the SNR is 20 dB. The measurement vectors derive from a coded diffraction pattern; see §B.3.2 for details. We solve the convex problem (5) with equal to the average of the measurements ; see [39, Sec. II]. Then we compute a top eigenvector of the solution.

Figure 1(a) displays storage costs for each algorithm as the signal length increases. See §B.3.2 for the numerical data. We approximate memory usage by reporting the total workspace allocated by MATLAB for the algorithm. PGM, AT, and CGM have static allocations, but they use a matrix variable of size . ThinCGM attempts to maintain a low-rank approximation of the decision variable, but the rank increases steadily, so the algorithm fails after . In contrast, SketchyCGM has a static memory allocation of . It already offers the best memory footprint for , and it still works when .

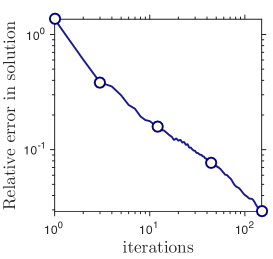

In fact, SketchyCGM can tackle even larger problems. We were able to reconstruct an image with pixels, treated as a vector , given noiseless coded diffraction measurements, as above. Figure 1(b) plots the convergence of the relative error: , where is a top eigenvector of the SketchyCGM iterate . After 150 iterations, the algorithm produced an image with relative error and with PSNR 36.19 dB. Thus, we can solve (24) when the psd matrix variable has complex entries!

As compared to other convex optimization algorithms, the main weakness of SketchyCGM is the iteration count. Some algorithms, such as AT, can achieve iteration count, but they are limited to smaller problems. Closing this gap is an important question for future work.

6.2 Fourier Ptychography

Up to now, it has not been possible to attack phase retrieval problems of a realistic size by solving the convex formulation (5). As we have shown, current convex optimization algorithms cannot achieve scale. Instead, many researchers apply nonconvex heuristics to solve phase retrieval problems [14, 27, 9, 22]. These heuristics can produce reasonable solutions, but they require extensive tuning and have limited effectiveness. In this section, we demonstrate that, without any modification, SketchyCGM can solve a phase retrieval problem from an application in microscopy. Furthermore, it produces an image that is superior to the results obtained using major nonconvex heuristics.

We study a phase retrieval problem that arises from an imaging modality called Fourier ptychography (FP) [22]. The authors of [22] provided measurements of a slide containing human blood cells from a working FP system. We treat the sample as an image with pixels, which we represent as a vector . The goal is to reconstruct the phase of the image, which roughly corresponds with the thickness of the sample at a given location.

The data consists of 29 illuminations, each containing pixels. The number of measurements . The measurement vectors are obtained from windowed discrete Fourier transforms. We can formulate the problem of reconstructing the sample using the convex phase retrieval template (5) with the parameter . In this instance, the psd matrix variable has complex entries.

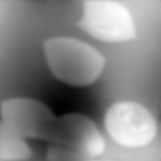

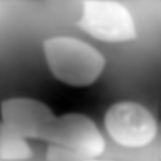

To solve (5), we run the SketchyCGM variant from §5.5 with the rank parameter for iterations. We factor the rank-one matrix output to obtain an approximation of the sample. Figure 2(a) displays the phase of the reconstruction .

Figure 2 also includes comparisons with two nonconvex heuristics. The authors of [22] provided a reconstruction obtained via the Burer–Monteiro method [6]. We also applied Wirtinger Flow [9] with the recommended parameters. SketchyCGM yields a smooth and detailed phase reconstruction. Burer–Monteiro produces severe artifacts, which suggest an unphysical oscillation in the thickness of the sample. Wirtinger Flow fails completely. These results are consistent with [22, Fig. 4], which indicates 5–10 dB improvement of convex optimization over heuristics.

The quality of phase reconstruction can be essential for scientific purposes. In this particular example, some of the blood cells are infected with malaria parasites (Figure 2(a), red boxes). Diagnosis is easier when the visual acuity of the reconstruction is high.

Appendix B.3 contains additional details and results on Fourier ptychographic imaging.

7 DISCUSSION

We have shown that it is possible to construct a low-rank approximate solution to a large-scale matrix optimization problem by sketching the decision variable. Let us contrast our approach against other low-storage techniques for large-scale optimization.

Sketchy Decisions. To the best of our knowledge, there are no direct precedents for the idea and realization of an optimization algorithm that sketches the decision variable. This work does partake in a broader vision that randomization can be used to design numerical algorithms [17, 26, 38].

Researchers have considered sketching the problem data as a way to reduce the size of a problem specification in exchange for additional error. This idea dates to the paper of Sarlós [33]; see also [26, 38, 30]. There are also several papers [29, 12, 1] in which researchers try to improve the computational or storage footprint of convex optimization methods by sketching internal variables, such as Hessians.

None of these approaches address the core issue that concerns us: the decision variable may require much more storage than the solution.

Dropping Nonconvexity. We have already discussed a major trend in which researchers develop algorithms that attack nonconvex reformulations of a problem. For example, see [6, 24, 4, 5]. The main advantage is to reduce the size of the decision variable; some methods also have the ancillary benefit of rapid local convergence. On the other hand, these algorithms are provably correct only under strong statistical assumptions on the problem data.

Prospects. Our work shows that convex optimization need not have high storage complexity for problems with a compact specification and a simple solution. In particular, for low-rank matrix optimization, storage is no reason to drop convexity.

It has not escaped our notice that the specific pairing of sketching and CGM that we have postulated immediately suggests a possible mechanism for solving other structured convex programs using optimal storage.

Acknowledgments

JAT and MU were supported in part by ONR Awards N00014-11-1-0025 and N00014-17-1-2146 and the Gordon & Betty Moore Foundation. VC and AY were supported in part by the European Commission under Grant ERC Future Proof, SNF 200021-146750, and SNF CRSII2-147633. The authors thank Dr. Roarke Horstmeyer for sharing the blood cell data.

Appendix A Convergence of SketchyCGM

In this appendix, we develop a basic convergence theory for the SketchyCGM algorithm. We focus on situations where the low-rank estimates produced by SketchyCGM converge to a low-rank solution of the model problem (6).

Preliminaries.

We rely on the following standard convergence result for CGM.

Theorem 2: A basic convergence result.

First, we study the case where the standard CGM iteration (9)–(11) converges. In this setting, we can show that SketchyCGM produces iterates that tend toward a matrix close to the limiting value of CGM.

Proof of Theorem 2.

According to the triangle inequality,

The error bound for reconstruction from the sketch, Theorem 1, shows that

The second inequality holds because is a best rank- approximation of with respect to Frobenius norm, whereas is an undistinguished rank- matrix.

Combine the last two displays to obtain

The second inequality and the last line follow from the limit .

If , then . Therefore, we may conclude that . ∎

Theorem 3: When all solutions are low rank.

Next, we examine the situation where all of the solutions to the model problem (6) have low rank. In this case, we can show that SketchyCGM produces a sequence of approximations that approaches the solution set of the problem. This point does not follow formally from Theorem 2 because CGM need not produce a convergent sequence of iterates.

Proof of Theorem 3.

As a consequence of the triangle inequality,

We claim that the second term . If so, then the first term converges to zero:

The first inequality is Theorem 1. The second bound holds because is a best rank- approximation of , while is an unremarkable set of rank- matrices. These observations complete the proof.

Let us turn to the claim. Abbreviate the objective function of (6) as . The continuous function attains its minimal value on the compact feasible set of (6). The standard convergence result for CGM, Fact 5, shows that . Now, fix a number . Define

If is empty, then . Otherwise, the continuous function attains the value on the compact set . In either case, because contains no optimal point of (6). Since , we must have for all sufficiently large . Therefore, for large . We conclude that for large , as required. ∎

Theorem 4: Rate of convergence.

Finally, we identify a setting where we can bound the rate at which the estimates produced by SketchyCGM converge to an optimal point of (6). To do so, we assume that the optimal point is stable in the sense that feasible perturbations away from optimality are reflected in increases in the value of the objective function.

Proof of Theorem 4.

Since the CGM iterate is feasible for (6), we can use the stability hypothesis (23) to calculate that

The second inequality holds because has rank , while is a better rank- approximation of . The last inequality follows from Theorem 1.

The latter display implies that

To complete the proof, invoke the standard convergence result for CGM, Fact 5, to bound the quantity . Last, simplify the constant. ∎

Appendix B More computational evidence

This appendix elaborates on the phase retrieval experiments described in §6. It also presents additional experiments on matrix completion and phase retrieval.

B.1 Loss functions

Our experiments involve a number of different models for data, so we require several elementary loss functions. Each of these maps is an extended convex function . Define

The objectives correspond, respectively, to the negative log-likelihood of observing the data under a Gaussian model, a Gauss–Laplace model, a Bernoulli model, and a Poisson model.

B.2 Matrix completion

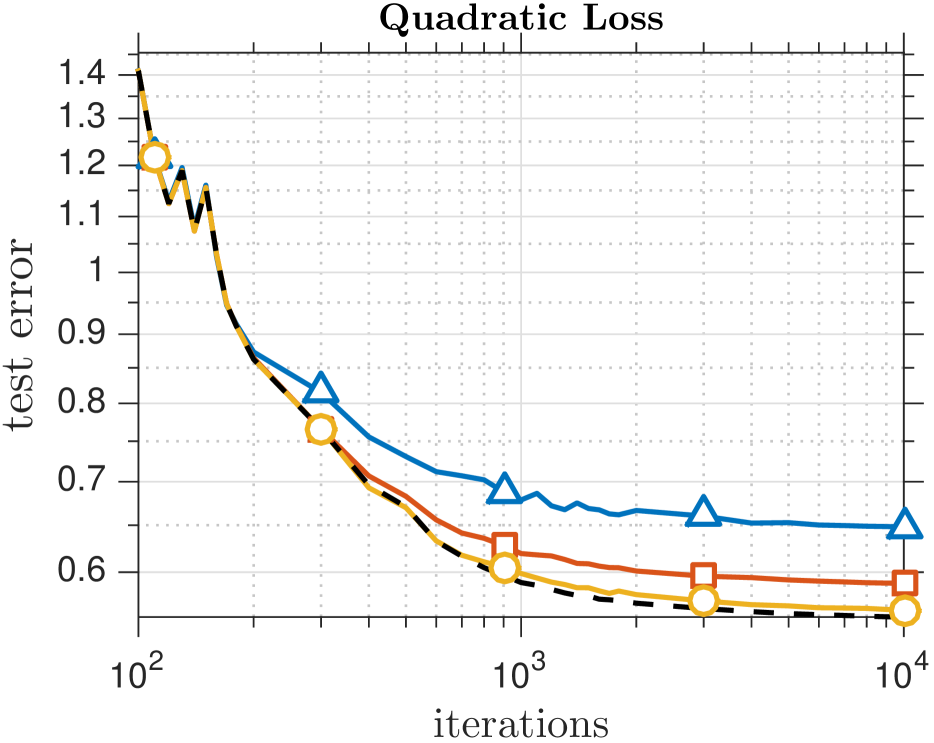

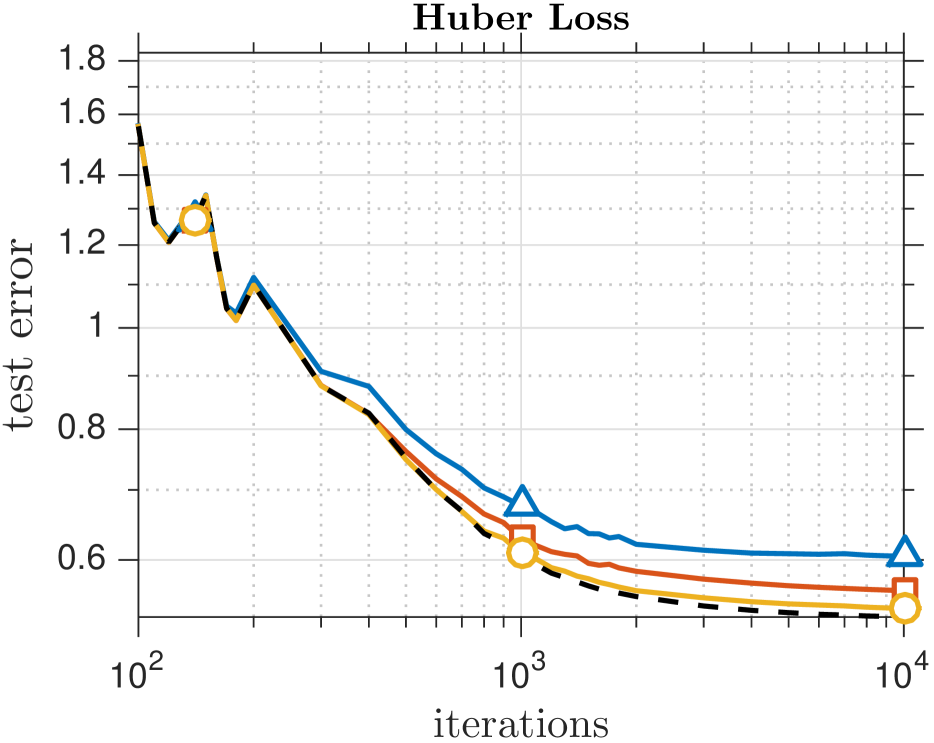

One principal advantage of SketchyCGM is its flexibility. Without any modification, the algorithm can provably solve any convex optimization problem with a smooth objective and a Schatten 1-norm constraint. To demonstrate this point numerically, we present the results of fitting the benchmark MovieLens 100K and 10M datasets [18] with three different loss functions.

The MovieLens dataset contains (about) ratings that users of a website assigned to a collection of movies. Suppose that there are users and movies. The data consists of triples where is a user, is a movie, and is the rating of movie by user .

We preprocess the data minimally. We remove the movies that are not rated by any user, as well as the users that have not provided any ratings. To fit a logistic model, we also binarize the ratings by replacing all values above 3.5 with and the rest with . Thus, the logistic model seeks a classifier that separates high ratings (4 and 5) from low ratings (1, 2, and 3).

We can use low-rank matrix completion to fit a model to the MovieLens data. To see why, introduce a target matrix that tabulates all ratings (known and unknown) of movies by users. One may imagine that has low rank because a lot of the variation in the ratings is explained by the quality of the movie, its genre, and a user’s preference for that genre. We only observe a subset of the entries of , and our goal is to predict the remaining entries.

We model this matrix completion problem using the formulation (6). Let be a training set of user–movie pairs, and let list the associated ratings. Introduce the linear map where

The objective function has the form

where .

Suppose that is an estimate for the target matrix . Let be the test set of user–movie pairs, with ratings listed in . Define the test error

Once again, .

For the 100K dataset, we use the default ub partition of the data into training and test sets. For each loss function, we sweep from to in steps of . As expected, the rank of a solution of the problem (6) increases with . We select the value of that provides the best test error after iterations of CGM.

A similar procedure applies to the 10M dataset, with the default rb partition. This time, we sweep from to in steps of .

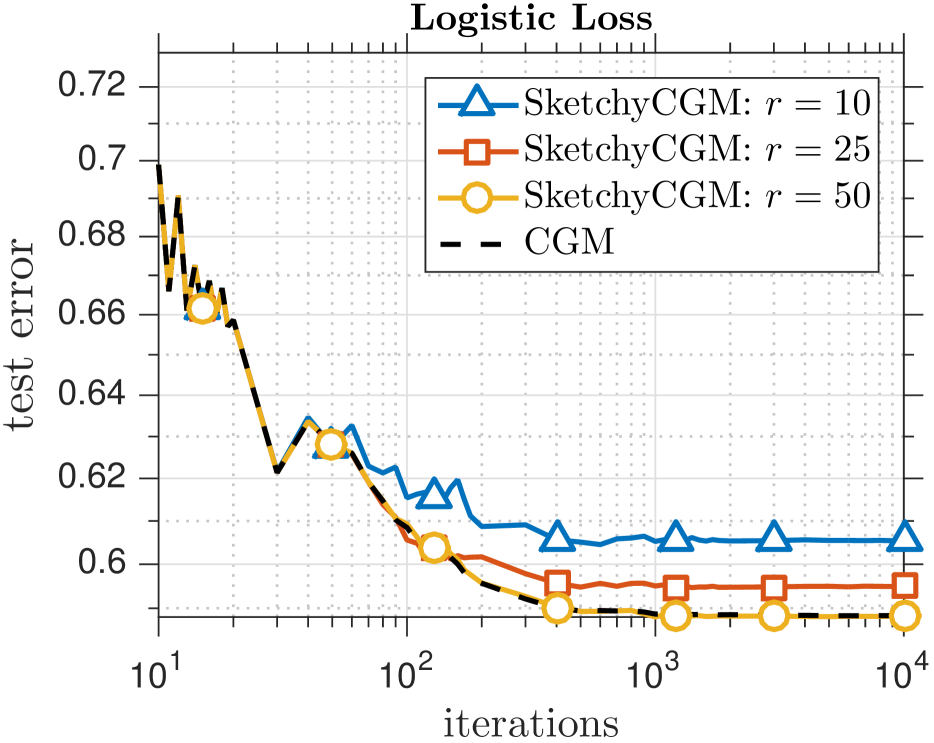

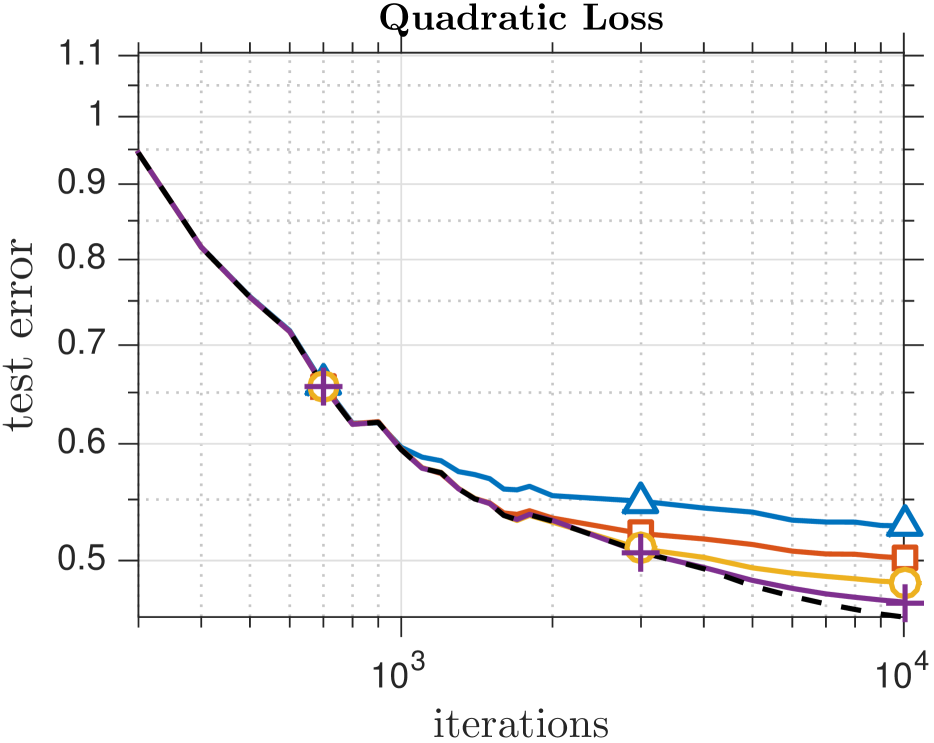

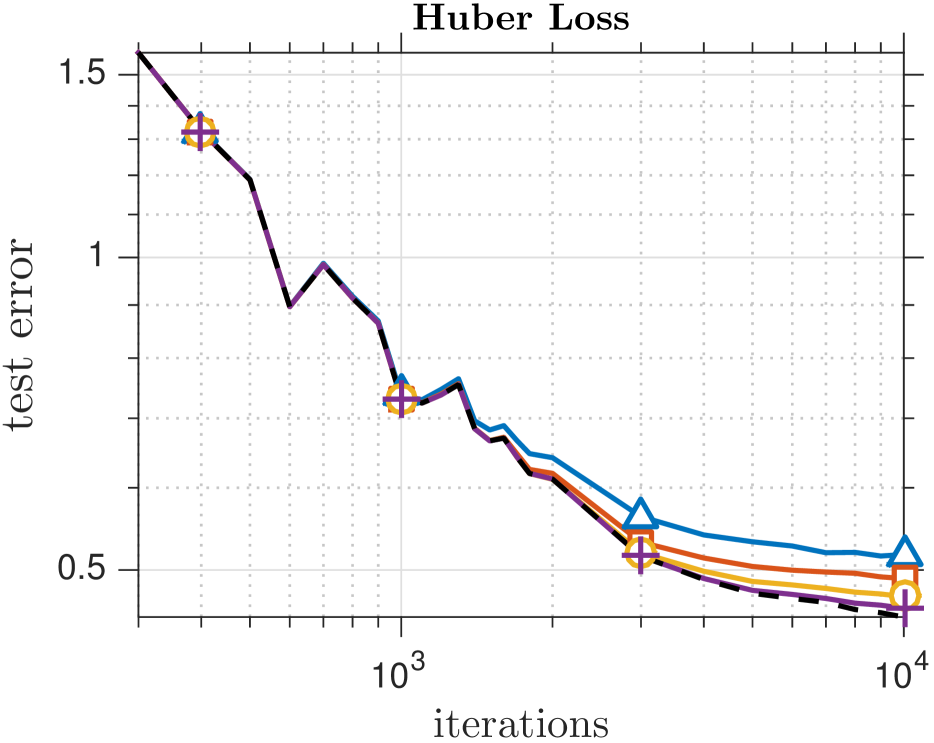

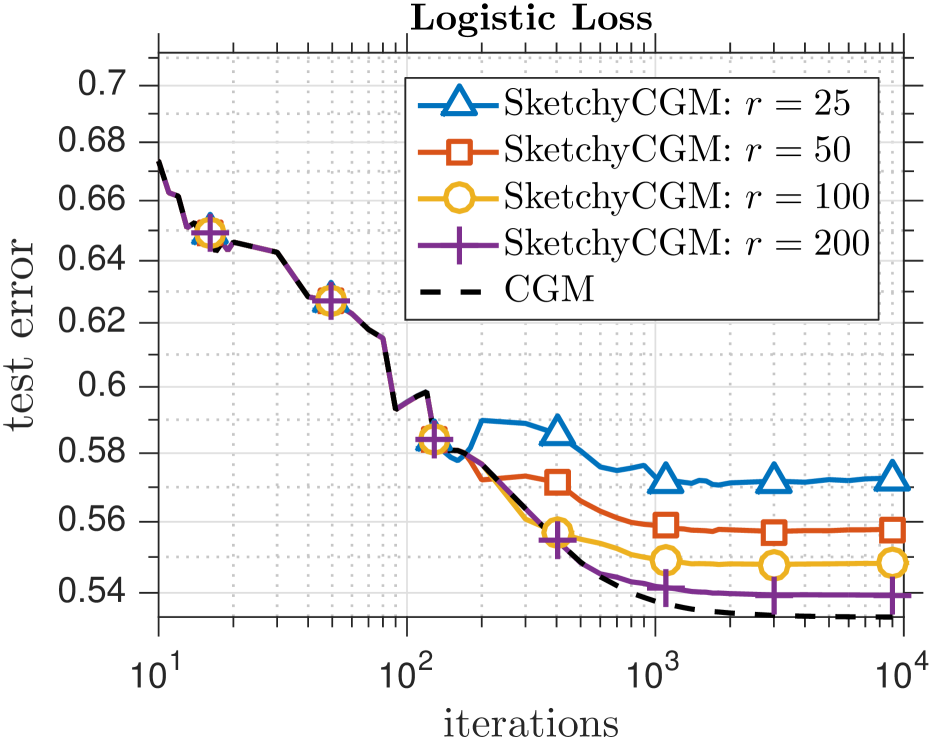

For each dataset and each loss function, we fit the model (6) with the designated value of by applying SketchyCGM. Figures 3 and 4 show how the test error for the SketchyCGM reconstruction varies as we change the rank parameter in SketchyCGM. For the 100K dataset, rank yields test error similar with the CGM solution. For the 10M dataset, rank yields equivalent performance.

B.3 Phase retrieval problems

Section 6 showcases the empirical performance of SketchyCGM on a family of phase retrieval problems. This section provides details of these experiments, as well as some related examples.

B.3.1 Overview

The setup is the same as in §1.2. Let be a vector, and suppose we acquire measurements

| (25) |

We can modify the measurement vectors to obtain a range of problems. We can also adjust the distribution of the noise .

To model the measurement process (25), it is convenient to form the matrix whose rows are the measurement vectors . Then define a linear map and its adjoint via

| (26) | ||||

The map extracts the diagonal of a matrix; maps a vector into a diagonal matrix. When is psd, note that .

We instantiate the convex optimization template (24) with the linear map (26) and the objective function

Here, the parameter . Following [39, Sec. II], we usually set . We approximate the true vector by means of a maximum eigenvector of a solution to (24).

| Signal length | ||||||

|---|---|---|---|---|---|---|

| AT | — | — | ||||

| PGM | — | — | ||||

| CGM | — | — | ||||

| ThinCGM | — | |||||

| SketchyCGM |

B.3.2 Synthetic phase retrieval

In §6.1, we considered a measurement model based on random coded diffraction patterns. This is a synthetic setup inspired by an imaging system where one can modulate the image before diffraction occurs [9].

For this example, the matrix appearing in (26) takes the form

| (27) |

In this expression, is the discrete Fourier transform (DFT) matrix, and are diagonal matrices that describe modulating waveforms. The parameter represents the number of -dimensional views of the target vector that we acquire. The total number of measurements .

We generate each diagonal entry of each matrix independently at random. Each one is the product of two independent random variables and , where is chosen uniformly from and is drawn from with probabilities and .

In this setting, we can represent the linear map in (26) using bits, and we can apply it efficiently using the FFT algorithm.

For the scaling experiments in §6.1, the measurements take the form (25) where the are the rows of (27). We solve (24) with the loss , the linear map (26)–(27), and set to the average of the data . The remaining details appear in §6.1. Table 1 summarizes the storage costs for solving this type of synthetic phase retrieval problem with five different convex optimization algorithms.

B.3.3 Synthetic Poisson phase retrieval

In many imaging systems, a Poisson noise model is more appropriate than a Gaussian noise model. Let us demonstrate that the SketchyCGM algorithm can solve synthetic phase retrieval problems with the loss . This work highlights the importance of adapting the loss function to the noise distribution.

The setup is similar to §B.3.2. Fix a small image with pixels. Acquire measurements of the form (25) using the coded diffraction model (26)–(27). Each realization of the noise is drawn iid from a Poisson distribution, whose mean is chosen so that the SNR of the measurements is 20 dB.

We formulate the phase retrieval problem using the template (24) with the loss , the linear map (26)–(27), and with set to the average of the measurements .

To solve this problem via SketchyCGM, it is necessary to make some small modifications [28]. We initialize the algorithm with the dual vector and set the learning rate . The rank parameter , and the algorithm runs for 100 iterations.

B.3.4 Fourier ptychography

In §6.2, we discussed a real-world phase retrieval problem arising from Fourier ptychography [22]. Let us explain the mathematical model for this problem and present some additional numerical work.

For Fourier ptychography, the matrix appearing in (26) has the following structure.

| (28) |

In this expression, is the 2D discrete Fourier transform, and is a low-dimensional 2D discrete Fourier transform. The sparse matrices describe bandpass filters; each column of has at most one nonzero entry. The number of measurements . See [22] for details about the physical setup and the mathematical model.

Section 6.2 describes a specific instance of Fourier ptychography imaging, applied to a slide containing red blood cells. To perform phase retrieval, we use the optimization problem (24) with loss and with . The measurement vectors are the rows of (28). We apply several algorithms, including a moderate number of iterations of CGM, SketchyCGM with rank parameter , the Burer–Monteiro method [6, 22], and Wirtinger flow [9].

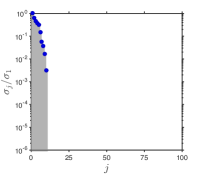

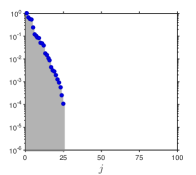

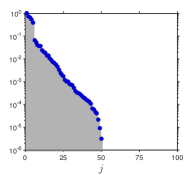

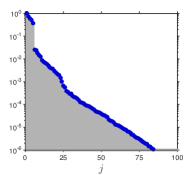

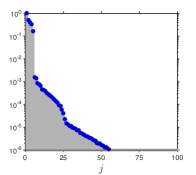

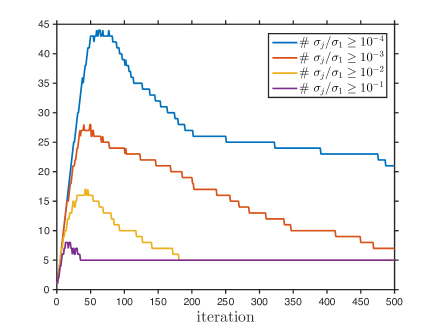

Figure 6 and 7(a) provide information about the spectrum of the CGM iterates. For several values of , we observe that the -rank111The -rank of a matrix is the number of singular values that exceed , where is the th largest singular value. of the iterates becomes large before declining to the value five. This type of behavior is typical for CGM, and it scuttles CGM variants that try to control the rank of the iterates directly.

Ideally, the solution to the convex formulation (5) of a phase retrieval problem has rank one. But these computations suggest that, for the blood cell data, the solution actually has rank five. The increase in rank is due to nonidealities in the imaging system, such as the spatial incoherence of the light source. In essence, the measurements capture a superposition of several slightly different images. Regardless, the convex model (5) is still effective, and a top eigenvector of the solution still provides a good approximation to the image [22].

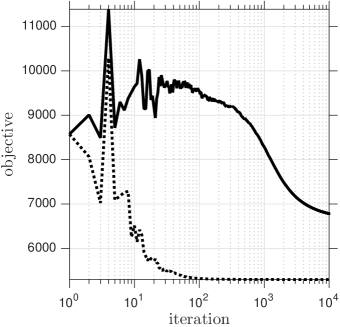

Figure 7(b) charts the objective value attained by the SketchyCGM iterates. We can implicitly compute the objective value for the CGM iterate using the loop invariant (22). Note that achieves a much smaller objective value than the rank-one approximation produced by SketchyCGM. The discrepancy is due to the fact that the solution to the optimization problem has approximate rank five.

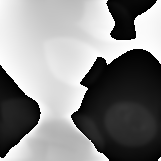

Figure 8 displays snapshots of the SketchyCGM iterates as the algorithm proceeds. We see that SketchyCGM already achieve a diagnostic quality image after iterations, but the algorithm continues to resolve the image as it runs.

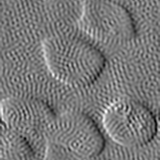

Last, Figure 9 shows the phase gradient of the solution to (5) obtained with three different algorithms; these plots provide an alternative view of Figure 2. Roughly, the phase gradient indicates the change in the thickness of the sample at a given location. Therefore, absolute changes in the value of the phase gradient are meaningful. Note the unphysical oscillations in the reconstruction via Burer–Monteiro [6, 22]. The reconstruction via Wirtinger Flow [9] contains no information at all.

References

- Agarwal et al. [2016] N. Agarwal, B. Bullins, and E. Hazan. Second-order stochastic optimization in linear time. Available at http://arXiv.org/abs/1602.03943, Feb. 2016.

- Auslender and Teboulle [2006] A. Auslender and M. Teboulle. Interior gradient and proximal methods for convex and conic optimization. SIAM J. Optim., 16(3):697–725 (electronic), 2006.

- Balan et al. [2009] R. Balan, B. G. Bodmann, P. G. Casazza, and D. Edidin. Painless reconstruction from magnitudes of frame coefficients. J. Fourier Anal. Appl., 15(4):488–501, 2009.

- Bhojanapalli et al. [2016] S. Bhojanapalli, A. Kyrillidis, and S. Sanghavi. Dropping convexity for faster semi-definite optimization. J. Mach. Learn. Res., 49:1–53, 2016.

- Boumal et al. [2016] N. Boumal, V. Voroninski, and A.S. Bandeira. The non-convex Burer-Monteiro approach works on smooth semidefinite programs. In Adv. Neural Information Processing Systems 29, pages 2757–2765. Curran Associates, Inc., 2016.

- Burer and Monteiro [2003] S. Burer and R. D. C. Monteiro. A nonlinear programming algorithm for solving semidefinite programs via low-rank factorization. Math. Program., 95(2, Ser. B):329–357, 2003.

- Candès and Plan [2010] E. J. Candès and Y. Plan. Matrix completion with noise. Proc. IEEE, 98(6):925–936, 2010.

- Candès et al. [2013] E. J. Candès, Y. C. Eldar, T. Strohmer, and V. Voroninski. Phase retrieval via matrix completion. SIAM J. Imaging Sci., 6(1):199–225, 2013.

- Candès et al. [2015] E. J. Candès, X. Li, and M. Soltanolkotabi. Phase retrieval via Wirtinger Flow: Theory and algorithms. IEEE Trans. Inform. Theory, 61(4):1985–2007, 2015.

- Chai et al. [2011] A. Chai, M. Moscoso, and G. Papanicolaou. Array imaging using intensity-only measurements. Inverse Problems, 27(1):015005, 2011.

- Clarkson [2010] K. L. Clarkson. Coresets, sparse greedy approximation, and the Frank-Wolfe algorithm. ACM Trans. Algorithms, 6(4):Art. 63, 30, 2010.

- Erdoğdu and Montanari [2015] M. A. Erdoğdu and A. Montanari. Convergence rates of sub-sampled Newton methods. In Adv. Neural Information Processing Systems 28, pages 3052–3060. Curran Associates, Inc., 2015.

- Fazel [2002] M. Fazel. Matrix rank minimization with applications. PhD Dissertation, Stanford Univ., Palo Alto, 2002.

- Fienup [1982] J. R. Fienup. Phase retrieval algorithms: a comparison. Appl. Optics, 21(15):2758–2769, 1982.

- Frank and Wolfe [1956] M. Frank and P. Wolfe. An algorithm for quadratic programming. Naval Res. Logist. Quart., 3:95–110, 1956.

- Goemans and Williamson [1995] M. X. Goemans and D. P. Williamson. Improved approximation algorithms for maximum cut and satisfiability problems using semidefinite programming. J. Assoc. Comput. Mach., 42(6):1115–1145, 1995.

- Halko et al. [2011] N. Halko, P. G. Martinsson, and J. A. Tropp. Finding structure with randomness: probabilistic algorithms for constructing approximate matrix decompositions. SIAM Rev., 53(2):217–288, 2011.

- Harper and Konstain [2015] F. M. Harper and J. A. Konstain. The MovieLens datasets: history and context. ACM. Trans. Interactive Intell. Sys., 5(4):Article 19, Dec. 2015. doi: http://dx.doi.org/10.1145/2827872.

- Hazan [2008] E. Hazan. Sparse approximate solutions to semidefinite programs. In Proc. 8th Latin American Theoretical Informatics Symposium, Apr. 2008.

- Helmberg and Rendl [2000] C. Helmberg and F. Rendl. A spectral bundle method for semidefinite programming. SIAM J. Optim., 10(3):673–696, 2000.

- Helmberg et al. [1996] C. Helmberg, F. Rendl, R. J. Vanderbei, and H. Wolkowicz. An interior-point method for semidefinite programming. SIAM J. Optim., 6(2):342–361, 1996.

- Horstmeyer et al. [2015] R. Horstmeyer, R. Y. Chen, X. Ou, B. Ames, J. A. Tropp, and C. Yang. Solving ptychography with a convex relaxation. New J. Physics, 17(5):053044, 2015.

- Jaggi [2013] M. Jaggi. Revisiting Frank–Wolfe: Projection-free sparse convex optimization. In Proc. 30th Intl. Conf. Machine Learning, Atlanta, 2013.

- Jain et al. [2013] P. Jain, P. Netrapalli, and S. Sanghavi. Low-rank matrix completion using alternating minimization. In STOC ’13: Proc. 45th Ann. ACM Symp. Theory of Computing, pages 665–674, Palo Alto, Dec. 2013.

- Levitin and Poljak [1966] E. S. Levitin and B. T. Poljak. Minimization methods in the presence of constraints. Ž. Vyčisl. Mat. i Mat. Fiz., 6:787–823, 1966. ISSN 0044-4669.

- Mahoney [2011] M. W. Mahoney. Randomized algorithms for matrices and data. Foundations and Trends® in Machine Learning, 3(2):123–224, 2011.

- Netrapalli et al. [2015] Netrapalli, P. Jain, and S. Sanghavi. Phase retrieval using alternating minimization. IEEE Trans. Signal Processing, 63(18):4814–4826, 2015.

- Odor et al. [2016] G. Odor, Y.-H. Li, A. Yurtsever, Y.-P. Hsieh, Q. Tran-Dinh, M. El Halabi, and V. Cevher. Frank-Wolfe works for non-Lipschitz continuous gradient objectives: scalable Poisson phase retrieval. In 41st IEEE Intl. Conf. Acoustics, Speech and Signal Processing (ICASSP), 2016.

- Pilanci and Wainwright [2015a] M. Pilanci and M. Wainwright. Newton sketch: A linear-time optimization algorithm with linear-quadratic convergence. Available at http://arXiv.org/abs/1505.02250, May 2015a.

- Pilanci and Wainwright [2015b] M. Pilanci and M. J. Wainwright. Randomized sketches of convex programs with sharp guarantees. IEEE Trans. Inform. Theory, 61(9):5096–5115, 2015b.

- Rao et al. [2015] N. Rao, P. Shah, and S. Wright. Conditional gradient with enhancement and truncation for atomic-norm regularization. Available at http://people.inf.ethz.ch/jaggim/NIPS-workshop-FW-greedy/papers/rao_shah_wright_final.pdf, 2015.

- Rockafellar [1976] R. T. Rockafellar. Monotone operators and the proximal point algorithm. SIAM J. Control Optim., 14(5):877–898, 1976.

- Sarlós [2006] T. Sarlós. Improved approximation algorithms for large matrices via random projections. In Proc. 47th Ann. IEEE Symp. Foundations of Computer Science, Berkeley, 2006.

- Srebro et al. [2004] N. Srebro, J. Rennie, and T. Jaakkola. Maximum-margin matrix factorizations. In Adv. Neural Information Processing Systems 17, Vancouver, Dec. 2004.

- Toh and Yun [2010] K.-C. Toh and S. Yun. An accelerated proximal gradient algorithm for nuclear norm regularized linear least squares problems. Pacific J. Optim., 6(615-640):15, 2010.

- Tropp [2015] J. A. Tropp. Convex recovery of a structured signal from independent random linear measurements. In G. Pfander, editor, Sampling Theory, a Renaissance, chapter 2, pages 67–101. Birkhäuser, 2015.

- Tropp et al. [2017] J. A. Tropp, A. Yurtsever, M. Udell, and V. Cevher. Randomized single-view algorithms for low-rank matrix reconstruction. ACM Report 2017-01, Caltech, Jan. 2017. Available at http://arXiv.org/abs/1609.00048.

- Woodruff [2014] D. P. Woodruff. Sketching as a tool for numerical linear algebra. Found. Trends Theor. Comput. Sci., 10(1-2):iv+157, 2014.

- Yurtsever et al. [2015] A. Yurtsever, Y.-P. Hsieh, and V. Cevher. Scalable convex methods for phase retrieval. In 6th IEEE Intl. Workshop on Computational Advances in Multi-Sensor Adaptive Processing, 2015.