An Empirical Bayes Approach for High Dimensional Classification

Abstract

We propose an empirical Bayes estimator based on Dirichlet process mixture model for estimating the sparse normalized mean difference, which could be directly applied to the high dimensional linear classification. In theory, we build a bridge to connect the estimation error of the mean difference and the misclassification error, also provide sufficient conditions of sub-optimal classifiers and optimal classifiers. In implementation, a variational Bayes algorithm is developed to compute the posterior efficiently and could be parallelized to deal with the ultra-high dimensional case.

Keywords: Empirical Bayes, High Dimensional Classification, Dirichlet Process Mixture

1 Introduction

Nowadays high dimensional classification is ubiquitous in many application areas, such as micro-array data analysis in bioinformatics, document classification in information retrieval, and portfolio analysis in finance.

In this paper, we consider the problem of constructing a linear classifier with high-dimensional features. Suppose data from class are generated from a -dimensional multivariate Normal distribution where and the prior proportions for two classes are , respectively. It is well-known that the optimal classification rule, i.e., the Bayes rule, classifies a new observation to class if and only if

| (1) |

where and . For simplicity, we assume both prior proportions and sample proportion of two classes are equal, but our theory could be easily extended to the case when two classes have unequal sample size but the ratio is bounded between 0 and 1. Therefore (1) could be simplified as we classifies to class 1 if and only if

| (2) |

Since parameters are unknown and we are given a set of a random samples , we can estimate those unknown parameters and classify to class if

where is the overall average of the data, is the sample mean difference between the two classes, and is the pooled estimator of the covariance matrix. This is also known as the linear discriminant analysis (LDA).

LDA, however, doesn’t perform well when is much larger than . Bickel and Levina (2004) have shown that when the number of features grows faster than the sample size, LDA is asymptotically as bad as random guessing due to the large bias of in terms of the spectral norm. RDA by Friedman (1989), thresholded covariance matrix estimator by Bickel and Levina (2008) and Sparse LDA by Shao et al. (2011) use regularization to improve the estimation of by assuming sparsity on off-diagonal elements of the covariance matrix. Cai and Liu (2012) assume is sparse and proposed LPD based on the sparse estimator of .

A seemingly extreme way is to set all the off-diagonal elements of to be zero, i.e., ignore the correlation among the features, and use the following Independence Rule:

| (3) |

where . Theoretical studies such as Domingos and Pazzani (1997) and Bickel and Levina (2004) have shown that worst case misclassification error of Independence Rule is well controlled and ignoring the correlation structure of doesn’t lose much if the correlation matrix is well conditioned.

To achieve good classification performance in a high-dimensional setting, it is not enough to regularize just the covariance matrix. As pointed out by Fan and Fan (2008) and Shao et al. (2011), even if we use Independence Rule, the classification performance of could still be as bad as random guessing due to the error accumulation through all dimensions of . In Theorem 1 of Fan and Fan (2008), essentially using to estimate results in strong condition of signal strength with respect to dimension . If is sparse and we use a regularized estimator of in Independence Rule, conditions on signal strength should be weakened, which is summarized in Theorem 1 in this paper.

Since estimating sparse is equivalent to estimating a sparse high dimensional Gaussian sequence, empirical Bayes methods could be used to get a regularized estimator. First we normalize : denote the normalized mean difference as , the sample version . We assume

where is unknown prior. is an empirical Bayes estimator of based on . Independence Rule of this scaled version of could be written as

| (4) |

From now on we stick to this scaled version of Independence Rule. Subscript indicates this Independence Rule is induced by .

One branch of empirical Bayes approaches, such as Brown and Greenshtein (2009), Jiang and Zhang (2009) and Koenker and Mizera (2014), directly work on marginal likelihood of . Greenshtein and Park (2009) proposed an empirical Bayes classifier inspired by the empirical Bayes estimator in Brown and Greenshtein (2009) (denoted as EB). Recently, Dicker and Zhao (2016) also proposed a empirical Bayes classifier based on Koenker and Mizera (2014)’s work. Our goal is to justify that a good empirical Bayes estimator indeed leads to an asymptotically optimal linear classifier, which fills the gap in estimation accuracy and classification performance.

Besides working on marginal likelihood, to take advantage of sparsity structure of , Johnstone and Silverman (2004) and Martin and Walker (2014) assume a two-group prior with a positive mass at 0. Recently Ouyang and Liang (2017) proposed a two-group prior with the continuous part being a normal mixture and they showed the resulting posterior mean could achieve asymptotical minimax rate established by Donoho et al. (1992). Therefore applying this estimator (denoted as DP) and its sparse variant (denoted as Sparse DP) could result in a good classification rule.

In this paper, we proposed two empirical Bayes classifiers based on DP estimator and Sparse DP estimator. Compared with Greenshtein and Park (2009), we establish the theoretical connection between the classification error of (3) and the estimation error of explicitly. In particular, we provide sufficient conditions for a estimator to achieve asymptotical optimal classification accuracy, i.e., the resulting Independence Rule is asymptotically as good as the Bayes rule (2).

The rest of the paper is organized as follows: in Section 2 we establish the relationship between the estimation error and the classification error. In Section 3, we introduce a variational inference algorithm which returns DP and Sparse DP classifier. We present the empirical results in Section 4 and conclusions and future work in Section 5.

2 Relationship between the Estimation Error and the Classification Error

We regard the linear classifier construction as a two step procedure. First we calculated and proposed a estimator based on . Second we compute the classifier : we classifies to class 1 iff . We call a Independence Rule induced by .

We use 0-1 loss function to evaluate a linear classifier. Without loss of generality, we assume the new observation comes from class 1 due to symmetry of our rule. Let denote the training data used to construct , the posterior misclassification error of given parameters is

| (5) |

where

is standard Normal cumulative distribution function. Let be the correlation matrix and . Consider the following parameter space with three pre-specified constants with respect to ( will depend on dimension ):

Note that we only bound the largest eigenvalues of but the smallest eigenvalue could diverge, leading to diverging condition number of , which is more general than Bickel and Levina (2004).

Based on , worst case posterior error is defined as

Worst case misclassification error is the expectation of over training data: . According to Dominance Convergence Theorem, if converges to a constant , as well. Therefore we only need to study .

The misclassification error of the optimal rule given is . Therefore

| (6) |

We aim to find a linear classifier such that the performance is as good as the optimal rule asymptotically. The worst case classification error of a good classifier should be approximately equal to the worst case classification error of the optimal Bayes rule. We define the asymptotical optimality and sub-optimality of a classifier in terms of worst case classification error, which is similar with definitions in Shao et al. (2011)

Definition 1

is asymptotically optimal if .

Definition 2

is asymptotically sub-optimal if .

is related with the estimation accuracy of . Since in many high dimensional classification problems most features are irrelevant, we assume is a -sparse vector, where is the number of nonzero elements of . Without loss of generality, is the non-zero index set while is the zero index set of . , , and are -dimensional, is -dimensional. error to estimate nonzero elements of is . We assume the following two conditions on

Condition 1

If , then .

Condition 2

.

Remember . Condition 1 says is a thresholded estimator while Condition 2 implies the tail of isn’t too heavy for zero elements. Condition 1 and 2 are used to control .

To compare the performance of our classifier with the optimal rule, the key quantity involved is weighted squared Euclidean distance . Theorem 1 shows is asymptotically close to as both and are diverging with growth rate constraints among , and .

Theorem 1

Suppose satisfies Condition 1-2. is the classification rule induced by . We assume , , , and . We have

Furthermore, if , and then

If , is asymptotically optimal; if , is asymptotically sub-optimal.

Theorem 1 reveals the relationship between estimation accuracy measure and worst case classification error explicitly. Bad performance of Independence Rule in Theorem 1 by Fan and Fan (2008)and LDA in Theorem 1-2 by Shao et al. (2011) is due to simply using sample mean difference to estimate . In those theorems need to dominate to overcome the estimation loss. However, if we put sparsity assumptions on and use a thresholded estimator satisfying Condition 1-2, the condition on could be relaxed: should have larger order than . In Ouyang and Liang (2017), is bounded by . Therefore only needs to grow faster than to guarantee optimality or sub-optimality of , which weakens conditions.

Meanwhile, we have 2 remarks based on Theorem 1.

Remark 1

could grow exponentially with respect to .

If , , centered distribution with the degree of freedom . Otherwise follows distribution with the degree of freedom and the noncentrality parameter . is chosen to satisfy and , which separates relevant features and irrelevant features with the large probability. implicitly determines the relative growth rate between and . Since and , could have almost the same growth rate as in the high dimensional sparse case when .

Remark 2

The simple hard thresholding estimator using satisfies all the technical conditions.

These conditions are not strict. We illustrate them using a hard thresholding estimator . Then using Central Limit Theorem we have . If , we could get an asymptotically sub-optimal classifier. If nonzero components of are bounded away from 0, is guaranteed. Besides, the fourth moment of central distribution exists. Therefore the simple hard thresholding estimator satisfies all the technical conditions.

One interesting case is when , what conditions we need to put to guarantee optimality. Theorem 2 provides an answer.

Theorem 2

Suppose satisfies Condition 1-2. is the classification rule induced by . If , , , and , then is asymptotic optimal as , and .

We need slower growth rate of in Theorem 2. If diverges to infinitely fast, the classification task is relatively easy, but converges to 0 faster than the rate of . Therefore our classification rule is not optimal. However, if diverges to infinity slowly, convergence rates of and are comparable. We could prove the ratio of these two converges to 1.

could still grow exponentially fast with respect to but we need more constraints about . If , we have . Therefore if and , with the proper choice of , our classifier is asymptotically optimal. If , we have . Therefore must grow slower than , since we need enough data to estimate nonzero elements accurately to guarantee we have small estimation error.

Any good estimator of the sparse mean difference should have small estimation error leading to small growth rate of . Our previous work have shown clustering algorithm based estimators have the estimation error . Hence, our proposed Dirichlet process mixture method based estimator as a special example, is asymptotically optimal in the minimax criteria. We can gain estimation accuracy in the first step, resulting in the better classification performance.

3 Dirichlet Process Mixture Based Linear Classifier

3.1 Dirichlet Process Prior

Given , in this section we build an empirical Bayes model with Dirichlet process prior to estimate . We assume and , where is prior unknown. Since most of ’s are sparse, ’s will concentrate around zero, forming a large cluster at 0 and several other clusters far away from 0. Dirichlet process mixture model is one of Bayesian tools to capture clustering behaviors (see Lo (1984)). We build a hierarchical Bayes model and assume , where is the concentration parameter and is the base measure.

An important formulation of Dirichlet process is stick breaking process proposed by Sethuraman (1994). We represent the random distribution function as , where is drawn i.i.d. from the base measure , while . is drawn i.i.d. from . To guarantee has a positive mass at 0, we model as Normal distribution with a point mass at 0, that is, , where and are 2 pre-specified parameters. is a dirac function at 0.

3.2 Variational Inference

To calculate the posterior for stick breaking process representation of Dirichlet process, a common technique is to pre-specify as the upper bound of the number of clusters. Then we have the following truncated version of stick breaking process using as the base measure:

| (7) | |||

| (8) | |||

| (9) | |||

| (10) | |||

| (11) | |||

| (12) |

The observed data are and the parameters are . contains all unique values of .

The number of parameters we estimate is , making MCMC converging very slowly. Instead, we use a variational Bayes algorithm to compute the posterior distribution which has the similar performance as traditional MCMC algorithms. Blei and Jordan (2006) propose variational inference algorithms for Dirichlet process mixture model for the exponential family base measure . Although Normal distribution with a positive mass at 0 doesn’t belong to exponential family, we could use the similar framework to derive our own variational Bayes algorithm.

We assume the following fully factorized variational distribution:

Shown in the Appendix, we’ve proved

-

•

, where , , , and , where is Normal density with mean and variance .

-

•

, where , , is Beta Distribution with parameters .

-

•

; where ,, , , is Multinomial distribution with parameters .

The algorithm is summarized in Algorithm 1. Via iterating these steps we could update the variational parameters. After convergence of , , , , and , we get an approximation of the posterior by plugging in these estimated parameters. The parameters we are interested in are , and . (In the algorithm means the element-wise maximum absolute value; .)

3.3 Constructing Linear Classifier

Given approximate posterior estimates , , , we get a MAP (maximum a posterior) estimator of . is the nonzero center and is the probability mass of zero of component indexed by . Each entry of is the posterior probability of belonging to the cluster . Furthermore, approximate posterior distribution of is . The most probable posterior assignment of based on above posterior is denoted as . MAP estimate of cluster weights including zero clusters is and . Then the estimated prior is .

Based on , the posterior distribution of given is

where is the posterior weight. We propose a posterior mean estimator . The linear classification rule induced by is: we classifies to class 1 iff

We refer to as DP estimator and the corresponding classifier as Dirichlet process linear classifier (DP linear classifier).

Additional sparsity could be introduced to DP estimator. Since we use the posterior mean as the estimator, the resulting is a shrinkage estimator of the true mean difference but not necessarily sparse. To have better performance in the high dimensional extremely sparse case, we revise the original DP estimator via thresholding posterior probability at 0: if the posterior weight , , otherwise , where is a tuning parameter which could be determined by cross validation. In all the simulation studies we fix since choosing the threshold at 0.5 is equivalent to getting a MAP estimator of index set of zeros. We refer to as Sparse DP estimator and the resulting linear classifier as Sparse DP linear classifier. Sparse DP estimator is a thresholded estimator whereas DP estimator isn’t. Therefore Sparse DP estimator satisfies Condition 1. Sparse DP estimator could eliminate noise of irrelevant features completely to enhance classification performance.

One practical issue of both DP and sparse DP estimator, is when is extremely sparse, we might end up with a MAP estimator occasionally. This is due to the “Rich gets richer” property of Dirichlet Process prior. A remedy in this extreme case is to randomly equally divide all sample mean differences into folds. For each fold of data we use Dirichlet process mixture model to estimate the discrete prior . Then we average all the discrete priors to get a overall estimate . For DP estimator and Sparse DP estimator we both use this refinement to estimate . The rationale behind this “batch” processing idea is when we divide elements of a high-dimensional vector into several batches, not only do the relatively large elements pop out because the maximum of the noise decreases as the sample size is smaller, but also the probability of all s equal to 0 is extremely small. The chance of detecting signals is increased. This refinement naturally leads to a parallelized variational Bayes algorithm: we could parallelize our algorithm for every batch and then average the estimated prior.

4 Empirical Studies

In this section, we conducted three simulation studies and applied our method to one real data example. The corresponding R package VBDP is available in https://github.com/yunboouyang/VBDP, which includes code to estimate sparse Gaussian sequence and code to construct DP and Sparse DP classifiers. Real data example is also included in this package. The source code and simulation results are available in https://github.com/yunboouyang/EBclassifier. Parameter specification is also summarized in the source code.

We also include a column “Hard Thresh DP” for comparison: Hard Threshold DP classifier uses the same threshold as Sparse DP classifier, but instead of using posterior mean, Hard Threshold DP classifier just uses sample mean difference to estimate if the posterior probability at 0 is below threshold. is large for Hard Threshold DP classifier but small for DP classifier and Sparse DP classifier because only the last two methods apply shrinkage. The purpose to include Hard Threshold DP classifier is to demonstrate the influence of on classification error . If is large, should be large. We don’t recommend to use Hard Threshold DP classifier in practice.

4.1 Simulation Studies

We conducted three simulation studies. The first two are the same in Greenshtein and Park (2009). In the third simulation study we compare our methods with Fan and Fan (2008) in the same setting.

Simulation Study 1. We assume has only diagonal elements. Without loss of generality, we set and . We use to denote different configurations of : the first coordinates in are all valued while the remaining entries are all 0 or sampled from . In the first simulation study, , where and . The sample size of each class is . We compute the theoretical misclassification rate using the true mean and true covariance matrix. We repeat our procedures 100 times and the average theoretical misclassification rates are reported in Table 1 and Table 2 corresponding to different . Bold case in all tables indicates the lowest misclassification rate across each row.

| Hard Thresh DP | Sparse DP | DP | EB | IR | FAIR | glmnet | |

|---|---|---|---|---|---|---|---|

| (1,2000) | 0.0046 | 0.0003 | 0.0002 | 0.0004 | 0.0049 | 0.1211 | 0.4280 |

| (1,1000) | 0.0874 | 0.0454 | 0.0283 | 0.0428 | 0.0885 | 0.2393 | 0.4500 |

| (1,500) | 0.2423 | 0.2036 | 0.1858 | 0.2015 | 0.2435 | 0.3423 | 0.4750 |

| (1.5,300) | 0.1756 | 0.1303 | 0.1059 | 0.1160 | 0.1767 | 0.2222 | 0.4146 |

| (2,200) | 0.1362 | 0.0540 | 0.0412 | 0.0518 | 0.1372 | 0.1039 | 0.3046 |

| (2.5,100) | 0.1937 | 0.0449 | 0.0422 | 0.0585 | 0.1947 | 0.0852 | 0.2126 |

| (3,50) | 0.2652 | 0.0470 | 0.0677 | 0.0772 | 0.2665 | 0.0982 | 0.1498 |

| (3.5,50) | 0.1957 | 0.0066 | 0.0175 | 0.0152 | 0.1965 | 0.0229 | 0.0655 |

| (4,40) | 0.1883 | 0.0023 | 0.0059 | 0.0072 | 0.1901 | 0.0101 | 0.0332 |

| Hard Thresh DP | Sparse DP | DP | EB | IR | FAIR | glmnet | |

|---|---|---|---|---|---|---|---|

| (1,2000) | 0.0035 | 0.0002 | 0.0001 | 0.0003 | 0.0038 | 0.1128 | 0.4216 |

| (1,1000) | 0.0699 | 0.0395 | 0.0241 | 0.0352 | 0.0710 | 0.2311 | 0.4551 |

| (1,500) | 0.2046 | 0.1948 | 0.1686 | 0.1751 | 0.2063 | 0.3280 | 0.4783 |

| (1.5,300) | 0.1450 | 0.1173 | 0.0976 | 0.0996 | 0.1465 | 0.2075 | 0.4190 |

| (2,200) | 0.1102 | 0.0470 | 0.0372 | 0.0431 | 0.1113 | 0.1011 | 0.3158 |

| (2.5,100) | 0.1583 | 0.0392 | 0.0415 | 0.0488 | 0.1595 | 0.0815 | 0.1945 |

| (3,50) | 0.2248 | 0.0444 | 0.0674 | 0.0687 | 0.2265 | 0.0969 | 0.1692 |

| (3.5,50) | 0.1637 | 0.0065 | 0.0119 | 0.0146 | 0.1655 | 0.0226 | 0.0640 |

| (4,40) | 0.1539 | 0.0019 | 0.0056 | 0.0057 | 0.1551 | 0.0088 | 0.0324 |

Table 1 and Table 2 compare DP and Sparse DP linear classifier with several existing methods: Empirical Bayes classifier (EB) by Greenshtein and Park (2009), Independence Rule (IR) by Bickel and Levina (2004), Feature Annealed Independence Rule (FAIR) by Fan and Fan (2008) and logistic regression with lasso using R package glmnet (denoted as glmnet).

DP and Sparse DP methods dominate other methods in the diagonal covariance matrix case whether the mean difference is sparse or not. If the mean difference vector is extremely sparse while the signal is strong, Sparse DP classifier outperforms DP classifier. In the relatively dense signal case, DP classifier outperforms sparse DP classifier. Overall DP and sparse DP estimators could improve estimation accuracy of the nonzero true mean difference while ruling out irrelevant features. Hard Thresh DP classifier has similar performance as IR, indicating if estimation error is not well controlled, classification accuracy could not be guaranteed.

Simulation Study 2. We consider AR(1) covariance structure of , where . That is, the correlation satisfies . . Sample size of each class is . We consider 3 different configurations of in this simulation study. The simulation results are shown in Table 3 to Table 5 based on 100 repetitions to compare theoretical misclassification rates.

| Hard Thresh DP | Sparse DP | DP | EB | IR | FAIR | glmnet | |

|---|---|---|---|---|---|---|---|

| 0.3 | 0.0089 | 0.0031 | 0.0021 | 0.0022 | 0.0092 | 0.1276 | 0.4325 |

| 0.5 | 0.0235 | 0.0135 | 0.0105 | 0.0096 | 0.0237 | 0.1393 | 0.4340 |

| 0.7 | 0.0714 | 0.0539 | 0.0468 | 0.0430 | 0.0712 | 0.1800 | 0.4437 |

| 0.9 | 0.2079 | 0.1929 | 0.1867 | 0.1758 | 0.2073 | 0.2702 | 0.4586 |

| Hard Thresh DP | Sparse DP | DP | EB | IR | FAIR | glmnet | |

|---|---|---|---|---|---|---|---|

| 0.3 | 0.0237 | 0.0081 | 0.0056 | 0.0068 | 0.0243 | 0.0546 | 0.2315 |

| 0.5 | 0.0481 | 0.0233 | 0.0183 | 0.0203 | 0.0483 | 0.0699 | 0.2792 |

| 0.7 | 0.1036 | 0.0686 | 0.0612 | 0.0619 | 0.1033 | 0.1095 | 0.2978 |

| 0.9 | 0.2472 | 0.2111 | 0.2054 | 0.2024 | 0.2466 | 0.2308 | 0.3603 |

| Hard Thresh DP | Sparse DP | DP | EB | IR | FAIR | glmnet | |

|---|---|---|---|---|---|---|---|

| 0.3 | 0.0233 | 0.0037 | 0.0032 | 0.0038 | 0.0238 | 0.0226 | 0.0913 |

| 0.5 | 0.0478 | 0.0139 | 0.0129 | 0.0138 | 0.0475 | 0.0374 | 0.1290 |

| 0.7 | 0.1069 | 0.0508 | 0.0493 | 0.0502 | 0.1069 | 0.0801 | 0.1747 |

| 0.9 | 0.2445 | 0.1827 | 0.1871 | 0.1834 | 0.2441 | 0.2067 | 0.2971 |

DP family and EB are among the best methods in this AR(1) correlation structure except Hard Thresh DP. If the correlation is severe and there aren’t very large mean difference, EB has better performance. If the correlation isn’t extremely severe or there are some large mean difference, DP classifier has better performance. As gets larger, the misclassification rate keeps increasing for each method, Sparse DP classifier and DP classifier is still considered as 2 relatively good classifiers since we only have very few data points.

Simulation Study 3. We consider the same setting used in Fan and Fan (2008). The error vector is no longer normal and the covariance matrix has a group structure. All features are divided into 3 groups. Within each group, features share one unobservable common factor with different factor loadings. In addition, there is an unobservable common factor among all the features across 3 groups. and . To construct the error vector, let be a sequence of independent standard normal random variables, and be a sequence of independent random variables of the same distribution as . Let and be factor loading coefficients. Then the error vector for each class is defined as

where except that for , for , and for . Therefore and , and in general within-group correlation is greater than the between-group correlation. The factor loadings and are independently generated from uniform distributions and . The mean vector is taken from a realization of the mixture of a point mass at 0 and a double exponential distribution: , where . . There are only very few features with signal levels exceeding 1 standard deviation of the noise. We apply Hard Thresh DP, Sparse DP, FAIR and glmnet to 400 test samples generated from the same process and calculate the average error rate. We also compare these methods to oracle procedure, which we know the location of each nonzero element in vector and use these nonzero elements to construct Independence Rule based classifier. We have 100 repetitions. The boxplot and scatter plot of misclassification error of these 4 methods are summarized in Figure 1 and the average error is summarized in Table 6.

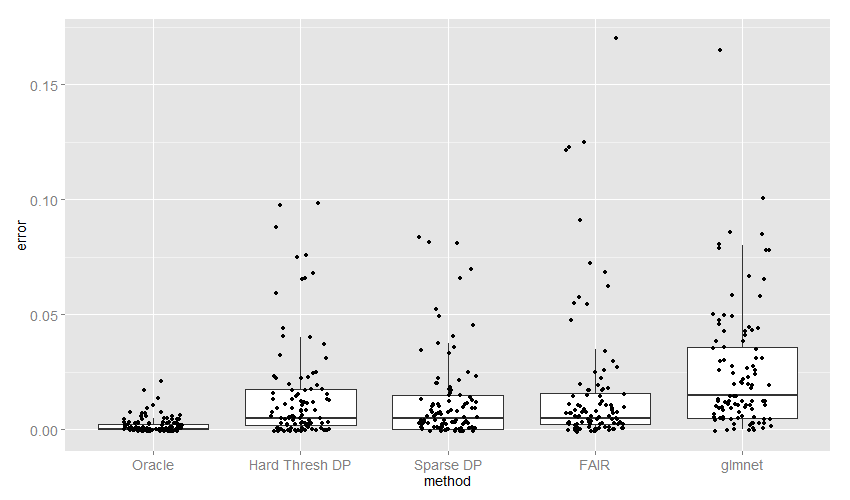

| Oracle | Hard Thresh DP | Sparse DP | FAIR | glmnet |

| 0.0021 | 0.0150 | 0.0126 | 0.0168 | 0.0252 |

Both Hard Thresh DP and Sparse DP classifier are better than FAIR and outperforms the logistic regression with Lasso. Even though on average oracle procedure’s misclassification error is smaller than that of DP family classifiers, we could conclude from the plot the misclassification error of majority of 100 trials for Sparse DP classifier is comparable to the misclassification error of the oracle procedure. Sparse DP classifier still has very good performance except some extreme cases.

4.2 Real Data Example

We consider a leukemia data set which was first analyzed by Golub et al. (1999) and widely used in statistics literature. The data set can be downloaded in http://www.broad.mit.edu/cgi-bin/cancer/datasets.cgi. There are 7129 genes and 72 samples generated from two classes, ALL (acute lymphocytic leukemia) and AML (acute mylogenous leukemia). Among the 72 samples, the training data set has 38 (27 data points in ALL and 11 data points in AML) and the test data set has 34 (20 in ALL and 14 in AML). We compared DP and sparse DP classifier with IR, EB and FAIR, which was summarized in Table 7. For DP and sparse DP classifier, we set , , and we split 7129 entries into 7 batches.

| Method | Training error | Test error |

|---|---|---|

| FAIR | 1/38 | 1/34 |

| EB | 0/38 | 3/34 |

| IR | 1/38 | 6/34 |

| DP | 1/38 | 2/34 |

| Sparse DP | 1/38 | 2/34 |

| Hard Thresh DP | 1/38 | 2/34 |

From Table 7 we conclude DP family classifiers outperform EB classifier. EB classifier has the same performance as IR. Improvement of EB compared with IR is marginal but using DP and Sparse DP classifier could result in some improvement. Both DP and EB classifier shrink the mean difference but doesn’t eliminate any irrelevant feature. Sparse DP classifier selects 2092 features but has the same performance in terms of test error as DP classifier. This might be due to the fact that this dataset is relatively well separated. Thresholding might not improve a lot.

5 Discussion

The contribution of this paper is three-folds: first we established the relationship between the estimation error and the classification error theoretically; second we proposed two empirical Bayes estimators for the normalized mean difference and the induced linear classifiers. Third, for estimating , we develop a variational Bayes algorithm to approximate posterior distribution of Dirichlet process mixture model with a special base measure and we could parallelize our algorithm using the “batch” idea.

Yet, there are still many open problems and many possible extensions related to this work. For example, instead of using the Independence Rule, we could develop a Bayes procedure to threshold both the mean difference and the sample covariance matrix, in a spirit similar to Shao et al. (2011), Cai and Liu (2012) and Bickel and Levina (2008). Another extension is to relax normality assumption: LDA is suitable for any elliptical distribution, therefore our work could also be extended to a bigger family of distributions under sub-Gaussian constraints.

A Proofs of 2 Theorems

Proof [Proof of Theorem 1] could be written as

which is lower bounded by

By Lemma A.2. of Fan and Fan (2008) we have . Therefore . Therefore we have .

We first consider the denominator,

If =0, , according to distribution tail probability inequality, we have

for any , using Markov Inequality and Cauchy-Schwartz Inequality,

The last equivalence holds since . The probability goes to 0 since .

Remember . According to triangular inequality,

We put these terms together to approximate the order of denominator as .

For numerator, denote , and , where . we have the following decomposition:

For , we have the following decomposition since :

Using Markov Inequality,

Therefore . Similarly . Hence . Suppose where denotes the corresponding submatrix of relevant features and denotes the corresponding submatrix of irrelevant features. Similarly for denote the corresponding submatrix of irrelevant features as . Denote the sub-vector of and . For we have the following decomposition:

Since , we use Cauchy-Schwartz Inequality to get an upper bound. We have

is , meanwhile, is . Therefore . Similarly .

Note that . , therefore . Similarly .

For , according to Cauchy-Schwartz Inequality, we have

Asymptotically, we have

Therefore

| (13) |

Since , we have

If , and , then and are the leading terms of denominator and numerator respectively. We have

Proof [Proof of Theorem 2] Conditions in Theorem 2 implies the conditions in Theorem 1. Therefore

Using Lemma 1 in Shao et al. (2011), we let and

Using the conditions and , we could easily verify that , and , therefore

B Variational Inference Algorithm Derivation

We will derive the variational inference algorithm for Dirichlet process mixture model. , , , and the data vector is given in advance. The data generating process is summarized in (3)-(8). We treat as latent variables and as parameters. Posterior distribution of all the parameters and latent variables is proportional to

Recall that under the fully factorized variational assumption, we have

Define . First we find the optimal form of , which satisfies

where . Therefore the optimal form of is fully factorized across different clusters: In order to determine the updating formula for , we use Method of Undetermined Coefficients. Suppose , therefore . Even though there’s a normalizing constant, but the difference between multipliers of and is invariant with respect to the constant. Therefore we have the following equation:

which holds for any . The solutions are given as follows:

Next we deal with the optimal form for , which satisfies

where , , , . Thus we proved

Besides, follows Beta Distribution with parameters , follows Beta Distribution with parameters ,, follows Beta Distribution with parameters .

Finally, we deal with . We have the following optimal form

therefore we proved . Since , we have

Therefore is the probability mass function of Multinomial Distribution. Once we fix , , where .

References

- Bickel and Levina (2004) Peter J. Bickel and Elizaveta Levina. Some theory for Fisher’s linear discriminant function,’naive Bayes’, and some alternatives when there are many more variables than observations. Bernoulli, 10(6):989–1010, 2004.

- Bickel and Levina (2008) Peter J. Bickel and Elizaveta Levina. Regularized estimation of large covariance matrices. The Annals of Statistics, 36(1):199–227, 2008.

- Blei and Jordan (2006) David M. Blei and Michael I. Jordan. Variational inference for Dirichlet process mixtures. Bayesian Analysis, 1(1):121–143, 2006.

- Brown and Greenshtein (2009) Lawrence D. Brown and Eitan Greenshtein. Nonparametric empirical bayes and compound decision approaches to estimation of a high-dimensional vector of normal means. The Annals of Statistics, pages 1685–1704, 2009.

- Cai and Liu (2012) Tony Cai and Weidong Liu. A direct estimation approach to sparse linear discriminant analysis. Journal of the American Statistical Association, 106(496):1566–1577, 2012.

- Dicker and Zhao (2016) Lee H Dicker and Sihai D Zhao. High-dimensional classification via nonparametric empirical bayes and maximum likelihood inference. Biometrika, page asv067, 2016.

- Domingos and Pazzani (1997) Pedro Domingos and Michael Pazzani. On the optimality of the simple bayesian classifier under zero-one loss. Machine learning, 29(2-3):103–130, 1997.

- Donoho et al. (1992) David L. Donoho, Iain M. Johnstone, Jeffrey C. Hoch, and Alan S. Stern. Maximum entropy and the nearly black object. Journal of the Royal Statistical Society. Series B (Methodological), 54(1):41–81, 1992.

- Fan and Fan (2008) Jianqing Fan and Yingying Fan. High dimensional classification using features annealed independence rules. The Annals of Statistics, 36(6):2605–2637, 2008.

- Friedman (1989) Jerome H. Friedman. Regularized discriminant analysis. Journal of the American statistical association, 84(405):165–175, 1989.

- Golub et al. (1999) Todd R. Golub, Donna K. Slonim, Pablo Tamayo, Christine Huard, Michelle Gaasenbeek, Jill P. Mesirov, Hilary Coller, Mignon L. Loh, James R. Downing, Mark A. Caligiuri, et al. Molecular classification of cancer: class discovery and class prediction by gene expression monitoring. Science, 286(5439):531–537, 1999.

- Greenshtein and Park (2009) Eitan Greenshtein and Junyong Park. Application of non parametric empirical bayes estimation to high dimensional classification. The Journal of Machine Learning Research, 10:1687–1704, 2009.

- Jiang and Zhang (2009) Wenhua Jiang and Cun-Hui Zhang. General maximum likelihood empirical bayes estimation of normal means. The Annals of Statistics, 37(4):1647–1684, 2009.

- Johnstone and Silverman (2004) Iain M. Johnstone and Bernard W. Silverman. Needles and straw in haystacks: Empirical bayes estimates of possibly sparse sequences. Annals of Statistics, (32):1594–1649, 2004.

- Koenker and Mizera (2014) Roger Koenker and Ivan Mizera. Convex optimization, shape constraints, compound decisions, and empirical bayes rules. Journal of the American Statistical Association, 109(506):674–685, 2014.

- Lo (1984) Albert Y Lo. On a class of bayesian nonparametric estimates: I. Density estimates. The annals of statistics, 12(1):351–357, 1984.

- Martin and Walker (2014) Ryan Martin and Stephen G. Walker. Asymptotically minimax empirical bayes estimation of a sparse normal mean vector. Electronic Journal of Statistics, 8(2):2188–2206, 2014.

- Ouyang and Liang (2017) Yunbo Ouyang and Feng Liang. A nonparametric bayesian approach for sparse sequence estimation. arXiv preprint arXiv:1702.04330, 2017.

- Sethuraman (1994) Jayaram Sethuraman. A constructive definition of Dirichlet priors. Statistica Sinica, 4:639–650, 1994.

- Shao et al. (2011) Jun Shao, Yazhen Wang, Xinwei Deng, and Sijian Wang. Sparse linear discriminant analysis by thresholding for high dimensional data. The Annals of statistics, 39(2):1241–1265, 2011.