Uncertain Volatility Models with Stochastic BoundsJean-Pierre Fouque and Ning Ning

\externaldocumentex_supplement

Uncertain Volatility Models with Stochastic Bounds††thanks: Submitted February 15, 2017.

\fundingResearch supported by NSF grant DMS-1409434.

Jean-Pierre Fouque

Department of Statistics & Applied Probability, University of California, Santa Barbara, CA 93106-3110

().

fouque@pstat.ucsb.edu, ning@pstat.ucsb.eduNing Ning 22footnotemark: 2

Abstract

In this paper, we propose the uncertain volatility models with stochastic bounds. Like the regular uncertain volatility models, we know only that the true model lies in a family of progressively measurable and bounded processes, but instead of using two deterministic bounds, the uncertain volatility fluctuates between two stochastic bounds generated by its inherent stochastic volatility process. This brings better accuracy and is consistent with the observed volatility path such as for the VIX as a proxy for instance. We apply the regular perturbation analysis upon the worst case scenario price, and derive the first order approximation in the regime of slowly varying stochastic bounds. The original problem which involves solving a fully nonlinear PDE in dimension two for the worst case scenario price, is reduced to solving a nonlinear PDE in dimension one and a linear PDE with source, which gives a tremendous computational advantage. Numerical experiments show that this approximation procedure performs very well, even in the regime of moderately slow varying stochastic bounds.

In the standard Black–Scholes model of option pricing [3], volatility is assumed to be known and constant over time, which seems unrealistic. Extensions of the Black–Scholes model to model ambiguity have been proposed, such as the stochastic volatility approach [10, 11], the jump diffusion model [1, 17], and the uncertain volatility model [2, 16]. Among these extensions, the uncertain volatility model has received intensive attention in Mathematical Finance for risk management purpose.

In the uncertain volatility models (UVMs), volatility is not known precisely and assumed between constant upper and lower bounds and . These bounds could be inferred from extreme values of the implied volatilities of the liquid options, or from high-low peaks in historical stock- or option-implied volatilities.

Under the risk-neutral measure, the price process of the risky asset satisfies the following stochastic differential equation (SDE):

(1)

where r is the constant risk-free rate, () is a Brownian motion and the volatility process belongs to a family of progressively measurable and -valued processes.

When pricing a European derivative written on the risky asset with maturity and nonnegative payoff , the seller of the contract is interested in the worst-case scenario. By assuming the worst case, sellers are guaranteed coverage against adverse market behavior if the realized volatility belongs to the candidate set. It is known that the worst-case scenario price at time is given by

(2)

where is the conditional expectation given with respect to the risk neutral measure.

Following the arguments in stochastic control theory, is the viscosity solution to the following Hamilton-Jacobi-Bellman (HJB) equation, which is the generalized

Black–Scholes–Barenblatt (BSB) nonlinear equation in Financial Mathematics,

(3)

It is well known that the worst case scenario price is equal to its Black–Scholes price with constant volatility (resp. ) for convex (resp. concave) payoff function (see [19] for instance). For general terminal payoff functions, an asymptotic analysis of the worst case scenario option prices as the volatility interval degenerates to a single point is given in [6].

In fact, for contingent claims with longer maturities, it is no longer consistent with observed volatility to assume that the bounds are constant (for instance by looking at the VIX over years, which is a popular measure of the implied volatility of S&P 500 index options).

Therefore, instead of modeling fluctuating between two deterministic bounds,

we consider the case that the uncertain

volatility moves between two stochastic bounds,

where and are two constants such that , and can be any other positive stochastic process.

In this paper, we consider

the general three-parameter CIR process with evolution

(4)

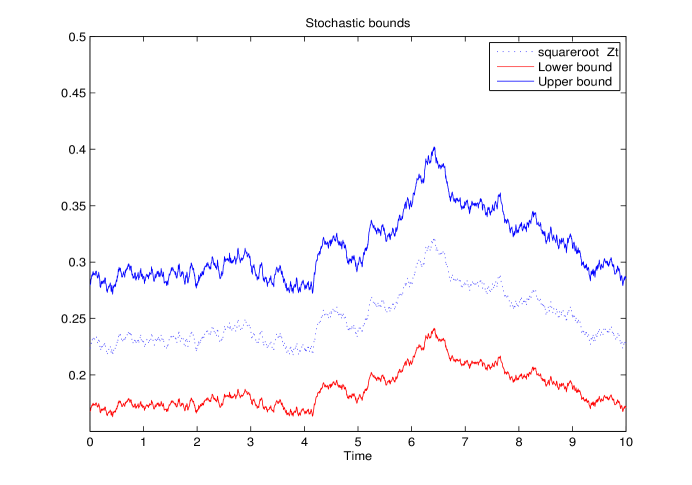

Here, and are strictly positive parameters with the Feller condition satisfied to ensure that stays positive, is a small positive parameter that characterizes the slow variation of the process , and () is a Brownian motion possibly correlated to () driving the stock price, with for . One realization of these processes is shown in Figure 1 with . Denoting , then the uncertainty in the volatility can be

absorbed in the uncertain adapted slope

.

Figure 1: Simulated stochastic bounds where is the (slow) mean-reverting CIR process (4).

In order to study the asymptotic behavior, we emphasize the importance of and reparameterize the SDE of the risky asset price process as

(5)

When , note that the CIR process is frozen at , and then the risky asset price process follows the dynamic

(6)

Both and start at the same point .

Suppose that is a European derivative written on the

risky asset with maturity and payoff . We denote its smallest riskless selling price (worst case scenario) at

time as

(7)

where

is the conditional expectation given with and . When , we represent the smallest riskless selling price as

(8)

where the subscripts in also means that and given the same filtration

. Notice that corresponds to in (2) with constant volatility bounds given by and .

The rest of the paper proceeds as follows. In Section 2, we first explain the convergence of the worst

case scenario price and its second derivative as goes to . We then write down the pricing nonlinear parabolic PDE (10) which characterizes the option price as a function of the present time , the value of the underlying asset, and the levels of the volatility driving process. At last, we introduce the main result that the first order approximation to is with accuracy in the order of , where we define and in (12) and (17) respectively. The proof of the main result is presented in Section 3. In Section 4, a numerical illustration

is presented. We conclude in Section 5. Some technical proofs are given in the Appendices.

2 Main Result

In this section, we first prove the Lipschitz continuity of the worst

case scenario price with respect to the parameter .

Then, we derive the main BSB equation that the worst case scenario price should follow and further identify the first order approximation when is small enough. We reduce the original problem of solving the fully nonlinear PDE (10) in dimension two to solving the nonlinear PDE (12) in dimension one and a linear PDE (17) with source. The accuracy of this approximation is given in Theorem 2.15, the main theorem

of this paper.

2.1 Convergence of

It is established in Appendix A that

and have finite moments uniformly in , which leads to the following result:

Proposition 2.1.

Let satisfies the SDE (5) and satisfies the SDE (6), then, uniformly in ,

We impose more regularity conditions on the terminal function , i.e.,

Lipschitz continuity, differentiability up to the fourth order and

polynomial

growth conditions on the first four derivatives of :

(9)

where for , , and are positive constants.

Theorem 2.4.

Under Assumption 2.3,

as a family of functions of and indexed by , uniformly converge to in with rate ,

for all .

Proof 2.5.

For given by (7) and given by (8), using the Lipschitz continuous of and by the Cauchy-Schwartz inequality, we have

where is a positive constant independent of , as desired.

2.2 Pricing Nonlinear PDEs

We now derive and , the leading order term and the first correction for the approximation of the worst-case scenario price ,

which

is the solution to the HJB equation associated to the corresponding control problem given by the generalized BSB nonlinear equation:

(10)

with terminal condition . For simplicity and without loss of generality, is assumed for

the rest of paper.

In this section, we use the regular perturbation approach to formally expand the value function as follows:

(11)

Inserting this expansion into the main BSB equation (10), by Theorem 2.4, the leading order term is the solution to

(12)

In this case, is just a positive parameter, we can achieve the existence and uniqueness of a smooth solution to (12), which is referred in the classical work of [7] and [19].

2.2.1 Convergence of

The main references on the regularity for uniformly parabolic equations are [4], [21] and [22]. In order to use these results, we have to make a log transformation to change variable to . Then because is bounded away from 0 in , (10) is uniformly parabolic.

Note that given , which satisfies Assumption 2.3, it is known that belongs to ( for polynomial growth). We conjecture that the result can be extended to for fixed. Since a full proof is beyond the scope of this paper, here we just assume this property.

Assumption 2.6.

Throughout the paper, we make the following assumptions on :

(i) belongs to ( for polynomial growth), for fixed.

(ii) and are uniformly bounded in .

Then under this assumption, we have the following Proposition:

Proposition 2.7.

Under Assumptions 2.3 and 2.6, the family of functions of and indexed by , converges to as tends to with rate , uniformly on compact sets in and , for .

Proof 2.8.

Under Assumptions 2.3 and 2.6, and by Theorem 2.4, the Proposition can be obtained by following the arguments in Theorem 5.2.5 of [8].

Denote the zero sets

of as

Define the set where and take different signs as

(13)

Assumption 2.9.

We make the following assumptions:

(i) There is a finite number of zero points of , for any . That is, and .

(ii) There exists a constant such that the set defined in (13) is included in , where

Remark 2.10.

Here we explain the rationale for Assumption 2.9 (ii).

Suppose has a third derivative with respect to , which does not vanish on the set . By Proposition 2.7, converges to with rate , therefore

we conclude that there exists a constant such that on , and have the same sign, and Assumption 2.9 (ii) would follow. This is illustrated in Figure 7 with an example with two zero points for .

Otherwise, would have a larger radius of order for , and then the accuracy in the Main Theorem 2.15 would be , but in any case of order

.

2.2.2 Optimizers

The optimal control in the nonlinear PDE (12) for , denoted as

is given by

(14)

The optimizer to the main BSB equation (10) is given in the following lemma:

Lemma 2.11.

Under Assumption 2.9, for sufficiently small and

for , the optimal control in the nonlinear PDE (10) for , denoted as

is given by

(15)

Proof 2.12.

To find the optimizer to

we firstly relax the restriction to .

Denote

By the result of Proposition 2.7 that uniformly converge to as goes to ,

for , the optimizer of is given by

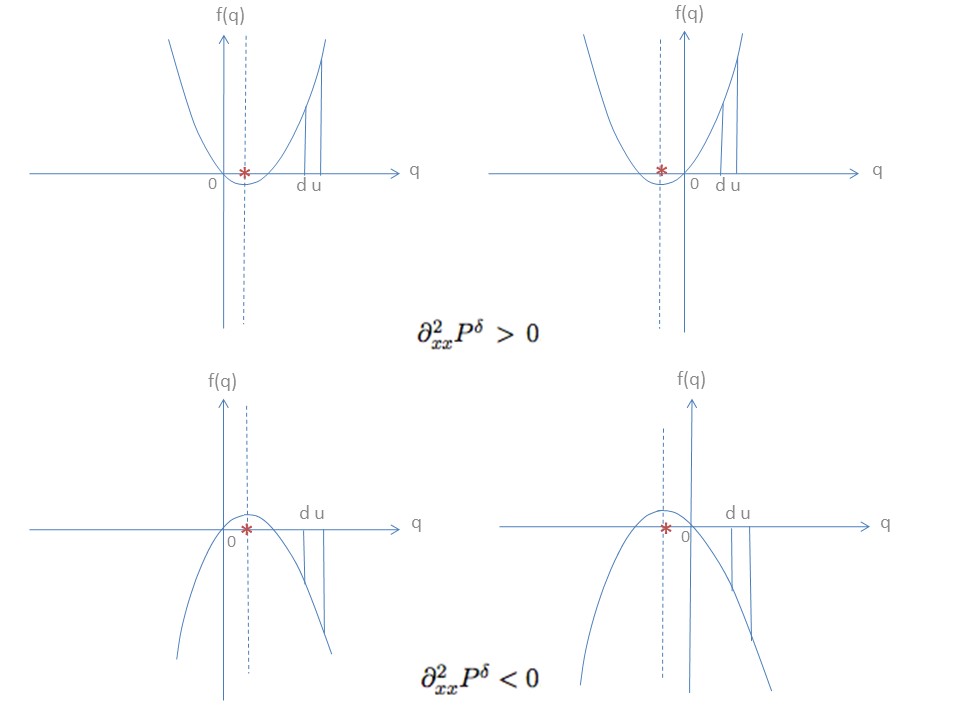

Since and are strictly positive, the sign of the coefficient of in is determined by the sign of . We have the following cases represented in Figure 2, from which we can see that for sufficiently small such that , the optimizer is given by

.

Figure 2: Illustration of the derivation of : if , whether is positive or negative, with the requirement , ; otherwise .

Remark 2.13.

When is convex (resp. concave), since supremum and expectation preserves convexity (resp. concavity), one can see that the worst case scenario price

is convex (resp. concave) with (resp. ), and thus (resp. ). In these two cases, we are back to perturbations around Black–Scholes prices which have been treated in [5].

In this paper, we work with general terminal payoff functions, neither convex nor concave.

Plugging the optimizer given by Lemma 2.11, the BSB equation (10) can be rewritten as

(16)

with terminal condition .

2.2.3 Heuristic Expansion and Accuracy of the Approximation

We insert the expansion (11) into the main BSB equation (16) and collect terms in

successive powers of . Under Assumption 2.9 that as , without loss of accuracy, the first order correction term is chosen as the solution to the linear equation:

Since (17) is linear, the existence and uniqueness result of a smooth solution can be achieved by firstly change the variable , and then use the classical result of [7] for the parabolic equation (17) with diffusion coefficient bounded below by .

Note that that the source term is proportional to the parameter .

We shall show in the following that under additional regularity conditions imposed on the derivatives of and , the approximation error is of order .

Assumption 2.14.

We assume polynomial growth for the following derivatives of and :

(18)

where are positive integers for .

Theorem 2.15 (Main Theorem).

Under Assumptions 2.3, 2.9 and 2.14, the residual function defined by

(19)

is of order . In other words, , there exists a positive constant

C, such that , where may depend on

but not on .

Recall that a function is of order , denoted , for , there exists a positive constant depend on

but not on , such that

Applying the operator to the error term, it follows that

where and are given in (14) and (15) respectively.

The terminal condition of is given by

3.1 Feynman–Kac representation of the error term

For sufficiently small, the optimal choice to the main BSB equation (10) is given explicitly in Lemma 2.11. Correspondingly, the asset price in the worst case scenario is a stochastic process which satisfies the SDE (1) with and , i.e.,

(24)

Given the existence and uniqueness result of proved in Appendix C, we have the following probabilistic representation of by Feynman–Kac formula:

where

Note that for given in (14) and given in (15) , we have

In order to show that is of order , it suffices to show that is of order , is of order , and and are uniformly bounded in . Clearly, is the main term that directly determines the order of the error term .

3.2 Control of the term

In this section, we are going to handle the dependence in of the process by a time-change argument.

Theorem 3.1.

Under Assumptions 2.3, 2.6 and 2.9, there exists a positive constant , such that

where may depend on

but not on .

That is, is of order .

Proof 3.2.

By Proposition 2.7 and being compact, there exists a constant such that

Then, since , we have

(27)

In order to show that is of order , it suffices to show that there exists a constant such that

Then according to Theorem 4.6 (time-change for martingales) of [13], we know that

is a standard one-dimensional Brownian motion on .

From the definition of given above, we have

which tells us that the inverse function of is

(29)

Next use the substitution

and for any , we have

(30)

Note that on the set , we have

where is a positive constant,

and then by (29) we have

(31)

Then from (30) and (31), by decomposing in and for any , we obtain

(32)

with details for this last step given in Appendix D.

By finite union over the ’s we deduce (28) and the theorem follows.

Remark 3.3.

As we noted in Remark 2.10, if the third derivative of with respect to vanishes on the set , the size of is of order for . In that case, (3.2) still holds but (32) would be of order ,

and then the result of Theorem 3.1 and the accuracy in the Main Theorem 2.15 would be of order .

3.3 Control of the term

Theorem 3.4.

Under Assumptions 2.3, 2.6, 2.9 and 2.14, there exists a constant , such that

where may depend on

but not on .

That is, is of order .

Using the same techniques in proving Theorem 3.1, the result that and have finite moments uniformly in , and on , we can deduce that is of order .

With the result of theorem 3.1 that is of order , the result of theorem 3.4 that is of order , and the result that and are uniformly bounded in where derivation of these bounds are given in the appendix E, we can see that

is of order , which completes the proof of the main Theorem 2.15.

4 Numerical Illustration

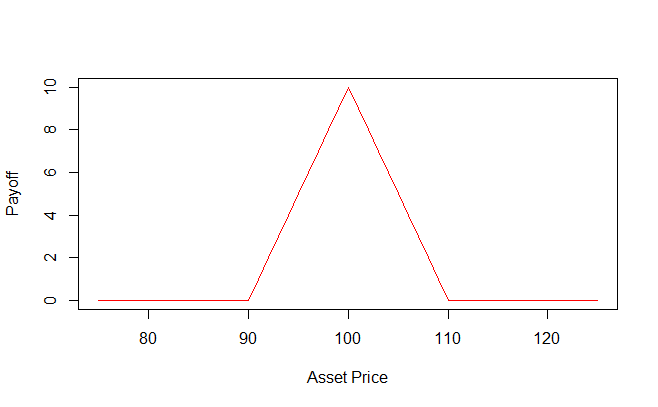

In this section, we use the nontrivial example in [6], and

consider a symmetric European butterfly spread with the payoff function

(33)

presented in Figure 3. Although this payoff function does not satisfy the conditions imposed in this paper, we could consider a regularization of it, that is to introduce a small parameter for the regularization and then remove this small parameter asymptotically without changing the accuracy estimate. This can be achieved by considering as the regularized payoff (see [18] for details on this regularization procedure in the context of the Black–Scholes equation).

.

Figure 3: The payoff function of a symmetric European butterfly spread.

The original problem is to solve the fully nonlinear PDE (10) in dimension two for the worst case scenario price, which is not analytically solvable in practice. In the following, we use the Crank–Nicolson version of the weighted finite difference method in [9], which corresponds to the case of solving in one dimension. To extend the original algorithm to our two dimensional case, we apply discretization grids on time and two state variables. Denote , and , where stands for the index of time, stands for the index of the asset price process, and stands for the index of the volatility process. In the following, we build a uniform grid of size and use time steps.

We use the classical discrete approximations to the continuous derivatives:

To simplify our algorithms and facilitate the implementation by matrix operations, we denote the following operators without any parameters:

4.1 Simulation of and

Note that in the PDE (17) for , must be solved in the PDE (12) for . Therefore, we solve and together in each space grids and iteratively back to the starting time.

Algorithm 1 Algorithm to solve and

1: Set

and .

2: Solve (predictor)

with

3: Solve (corrector)

with

4: Solve

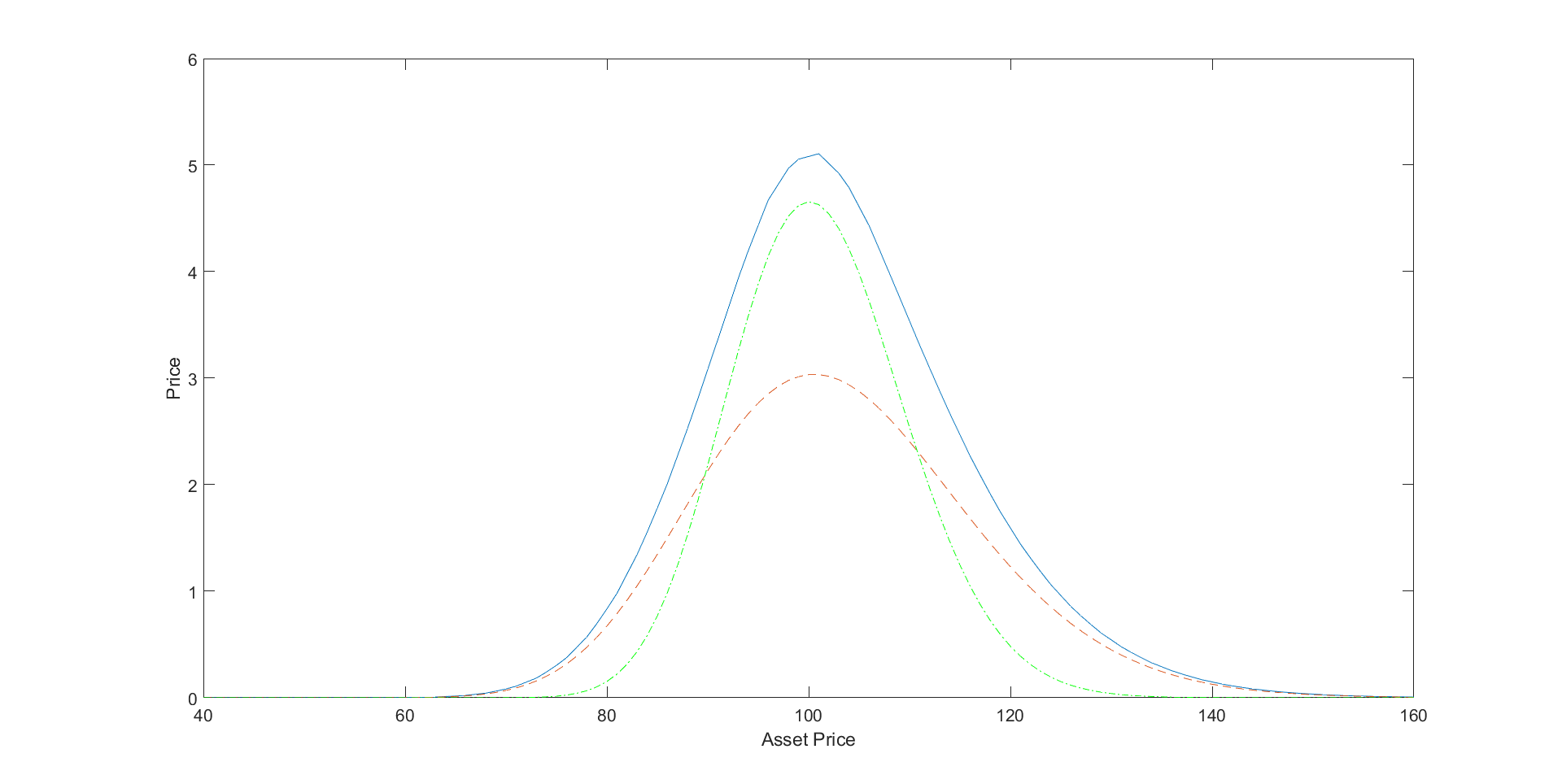

Throughout all the experiments, we set , , , , , and . Therefore, the two deterministic bounds for are given by

and , which are standard Uncertain Volatility model bounds setup. From Figure 4, we can see that is above the Black–Scholes prices with constant volatility and all the time, which corresponds to the fact that we need extra cash to superreplicate the option when facing the model ambiguity. As expected, the Black–Scholes prices with constant volatility (resp. ) is a good approximation when is convex (resp. concave).

.

Figure 4: The blue curve represents the usual uncertain volatility model price with two deterministic bounds and , the red curve marked with ”- -” represents the Black–Scholes prices with , the green curve marked with ’-.’ represents the Black–Scholes prices with .

4.2 Simulation of

Considering the main BSB equation given by (10),

if we relax the restriction

to , the optimizer of

is given by

and the maximum value of is given by

Therefore,

To simplify the algorithm, we denote

Algorithm 2 Algorithm to solve

1: Set

.

2: Predictor:

with

3: Corrector:

with

We set and , which satisfies the Feller condition required in this paper.

4.3 Error analysis

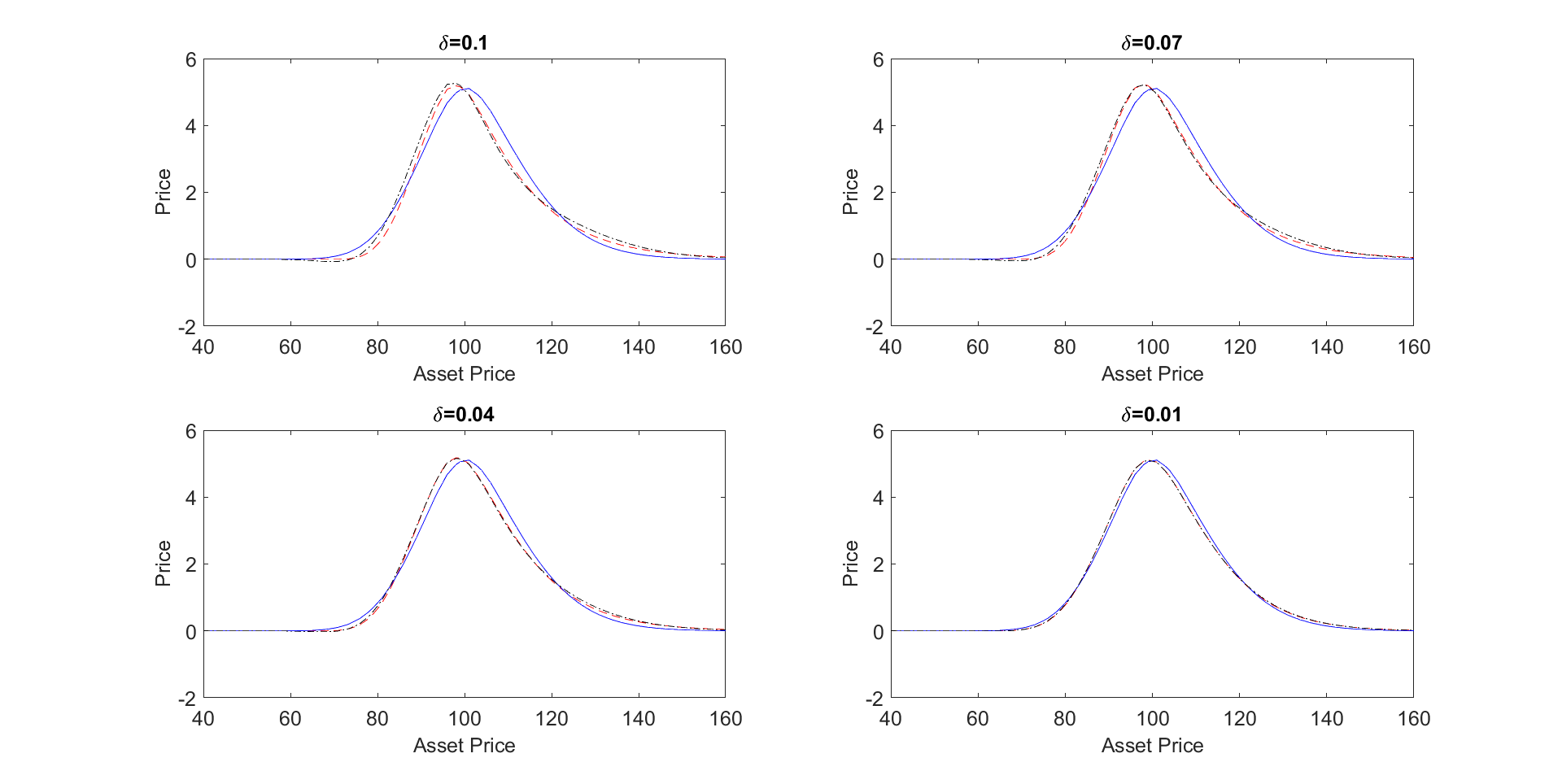

To visualize the approximation as vanishes, we plot , and with ten equally

spaced values of from to , and consider a typical case of correlation (see [12]). In Figure 5, we see that the first order prices capture the main feature of the worst case scenario prices for different values of . As can be seen, for very small, the approximation performs very well and it worth noting that, even for not very small such as , it still performs well.

.

Figure 5: The red curve marked with ”- -” represents the worst case scenario prices ; the blue curve represents the leading term ; the black curve marked with ’-.’ represents the approximation .

.

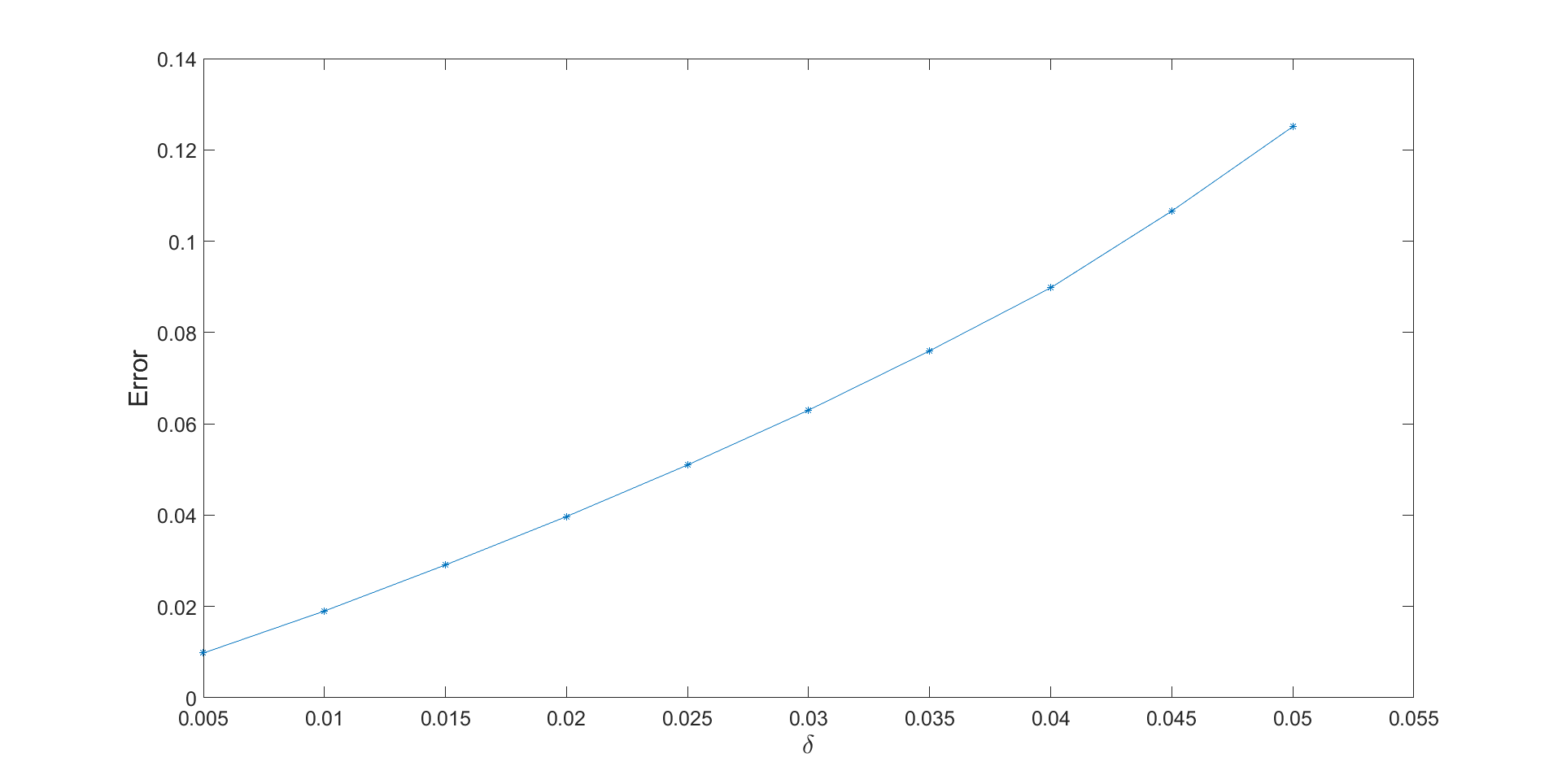

Figure 6: Error for different values of

.

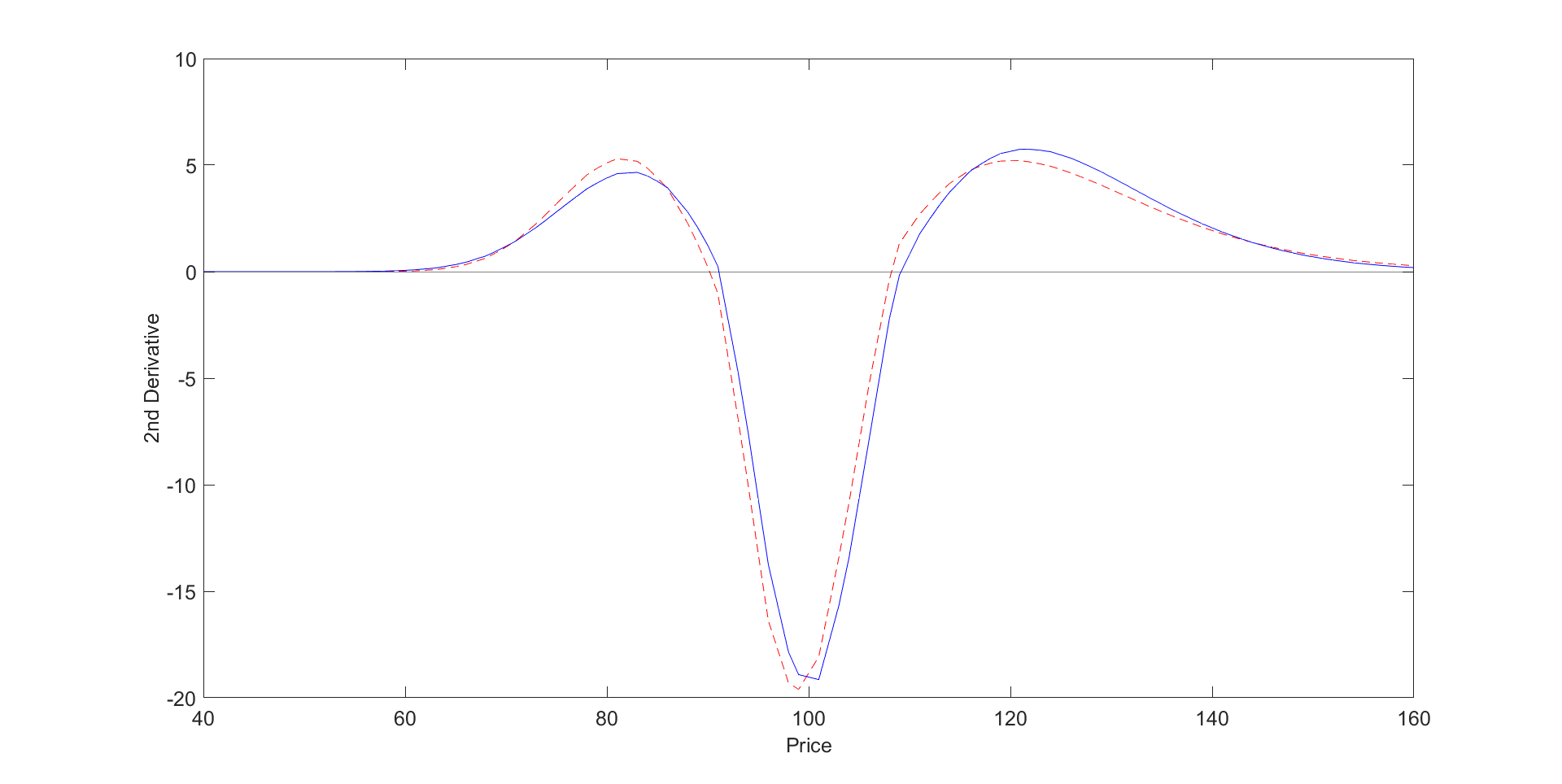

Figure 7: The red curve marked with ”- -” represents ; the blue curve represents .

To investigate the convergence of the error of our approximation as decrease, we compute the error of the approximation for each as following

As shown in Figure 6, the error decreases linearly as decreases (at least for small enough), as predicted by our Main Theorem 2.15.

Remark 4.1.

In Remark 2.10, for the case that has a third derivative with respect to , which does not vanish on the set , we have Assumption 2.9 (ii) as a direct result. In Figure 7, we can see that the slopes at the zero points of and are not , hence for this symmetric butterfly spread, Assumption 2.9 (ii) is satisfied.

5 Conclusion

In this paper, we have proposed the uncertain volatility models with stochastic bounds driven by a CIR process. Our method is not limited to the CIR process and can be used with any other positive stochastic processes such as positive functions of an OU process. We further studied the asymptotic behavior of the worst case

scenario option prices in the regime of slowly varying stochastic bounds. This study not only helps

understanding that uncertain volatility models with stochastic bounds are more flexible than uncertain volatility models with constant bounds for option pricing and risk management, but also provides

an approximation procedure for worst-case scenario option prices when the bounds are slowly varying. From the

numerical results, we see that the approximation procedure works really well even when the payoff function does not satisfy the requirements enforced in this paper, and even when is not so small such as .

Note that as risk evaluation in a financial management requires more accuracy and efficiency nowadays, our approximation procedure highly improves the estimation and still maintains the

same efficiency level as the regular uncertain volatility models.

Moreover, the worst case scenario price (10) has to be recomputed for any change in its parameters , and . However, the PDEs (12) and (17) for and

are independent of these parameters, so the approximation requires only to compute and once for

all values of , and .

Appendix A Moments of and

Proposition A.1.

The process has finite moments of any order uniformly in for .

Denote the moment generating function of the integrated CIR process given as

and then we have the following lemma:

Proposition A.2.

For independent of and , is bounded uniformly in and . That is , where is independent of and .

Proof A.3.

The moment generating function of the integrated CIR process has an explicit form, which is presented in Section 5 of [15]. That is

where

and

In the following, we are going to show , where is independent of and .

•

If , we have and

Since , we have . Therefore

•

If , let which is positive, then

–

In the limit of small , since

we have

There exists independent of and , such that for ,

Note that corresponds to a open region of , namely .

–

Consider , and then consider in a small neighborhood of . Near these points, notice that is not in a small neighborhood of , which implies that is not in a small neighborhood of .

From applied to

, we deduce that there exists an open subset , such that , which is independent of and .

–

Lastly, on , which is a closed region and thus compact, is well-defined and continuous with respect to and . So there exists independent of and , such that .

In sum, taking , which is independent of and , we have

,

as desired.

By this result, we have the following Proposition:

Proposition A.4.

The process has finite moments of any order uniformly in for .

Proof A.5.

For the process satisfying the SDE

where and is the CIR process satisfies SDE (4),

for each finite , we have

and the last step follows by the inequality .

The Novikov condition is satisfied thanks to Proposition A.2, that is,

Notice that only the upper bound of is used, which gives the uniform convergence in . Also note that using the result that and have finite moments uniformly in , we can show that ,

where is independent of .

For the existence and uniqueness of , we consider the transformation

which is well defined for any , where for any ,

By Itô’s formula, the process satisfies the following SDE:

(41)

Note that the diffusion coefficient satisfies

and is bounded away from , hence by Theorem 1 in section 2.6 of [14] and the result 7.3.3 of [20], the SDE (41) has a unique weak solution. Consequently, we have a unique solution to the SDE (24) until for any . In order to show (24) has a unique solution, it suffices to prove that

Note that is a martingale and thus is a nonnegative submartingale, thus by Doob’s martingale inequality and since the process has finite moments uniformly in ,

(46)

where may depend on but not on .

Next, by the Doob’s martingale inequality in form, we have

(47)

Finally, by inequalities (32), (43), (46) and (47), we have

where a positive constant and does not depend on .

Appendix E Proof of Uniform Boundedness of and on

With the help of Assumption 2.14, Cauchy–Schwarz inequality and the uniformly bounded moments of and processes given in Appendix A, we are going to prove that and are uniformly bounded in .

First recall that

and denote

Then we have

and

where , and are positive constants.

Next recall that

and denote

Then we have

and

where , are positive constants.

References

[1]L. Andersen and J. Andreasen, Jump-diffusion processes: Volatility

smile fitting and numerical methods for option pricing, Review of

Derivatives Research, 4 (2000), pp. 231–262.

[2]M. Avellaneda, A. Levy∗, and A. Parás, Pricing and hedging

derivative securities in markets with uncertain volatilities, Applied

Mathematical Finance, 2 (1995), pp. 73–88.

[3]F. Black and M. Scholes, The pricing of options and corporate

liabilities, Journal of political economy, 81 (1973), pp. 637–654.

[4]M. G. Crandall, M. Kocan, and A. Świech, Lp-theory for fully

nonlinear uniformly parabolic equations: Parabolic equations, Communications

in Partial Differential Equations, 25 (2000), pp. 1997–2053.

[5]J.-P. Fouque, G. Papanicolaou, R. Sircar, and K. Sølna, Multiscale stochastic volatility for equity, interest rate, and credit

derivatives, Cambridge University Press, 2011.

[6]J.-P. Fouque and B. Ren, Approximation for option prices under

uncertain volatility, SIAM Journal on Financial Mathematics, 5 (2014),

pp. 360–383.

[7]A. Friedman, Stochastic differential equations and applications.

vol. 1. aca# demic press, New York, (1975).

[8]M.-H. Giga, Y. Giga, and J. Saal, Nonlinear partial differential

equations: Asymptotic behavior of solutions and self-similar solutions,

vol. 79, Springer Science & Business Media, 2010.

[9]J. Guyon and P. Henry-Labordère, Nonlinear option pricing, CRC

Press, 2013.

[10]S. L. Heston, A closed-form solution for options with stochastic

volatility with applications to bond and currency options, Review of

financial studies, 6 (1993), pp. 327–343.

[11]J. Hull and A. White, The pricing of options on assets with

stochastic volatilities, The journal of finance, 42 (1987), pp. 281–300.

[12]K. In’t Hout and S. Foulon, Adi finite difference schemes for option

pricing in the heston model with correlation, International journal of

numerical analysis and modeling, 7 (2010), pp. 303–320.

[13]I. Karatzas and S. Shreve, Brownian motion and stochastic calculus,

vol. 113, Springer Science & Business Media, 2012.

[14]N. V. Krylov, Controlled diffusion processes, vol. 14, Springer

Science & Business Media, 2008.

[15]T. Lepage, S. Lawi, P. Tupper, and D. Bryant, Continuous and

tractable models for the variation of evolutionary rates, Mathematical

biosciences, 199 (2006), pp. 216–233.

[16]T. J. Lyons, Uncertain volatility and the risk-free synthesis of

derivatives, Applied mathematical finance, 2 (1995), pp. 117–133.

[17]R. C. Merton, Option pricing when underlying stock returns are

discontinuous, Journal of financial economics, 3 (1976), pp. 125–144.

[18]G. Papanicolaou, J.-P. Fouque, K. Solna, and R. Sircar, Singular

perturbations in option pricing, SIAM Journal on Applied Mathematics, 63

(2003), pp. 1648–1665.

[19]H. Pham, Continuous-time stochastic control and optimization with

financial applications, vol. 61, Springer Science & Business Media, 2009.

[20]D. W. Stroock and S. S. Varadhan, Multidimensional diffusion

processes, Springer, 2007.

[21]L. Wang, On the regularity theory of fully nonlinear parabolic

equations: I, Communications on Pure and Applied Mathematics, 45 (1992),

pp. 27–76.

[22]L. Wang, On the regularity theory of fully nonlinear parabolic

equations: Ii, Communications on pure and applied mathematics, 45 (1992),

pp. 141–178.