Multi-Dimensional Pass-Through and Welfare Measures under Imperfect Competition††thanks: We are grateful to Yong Chao, Germain Gaudin, Makoto Hanazono, Hiroaki Ino, Konstantin Kucheryavyy, Laurent Linnemer, Carol McAusland, Babu Nataha, and Glen Weyl as well as conference and seminar participants for helpful discussions. Adachi and Fabinger acknowledge a Grant-in-Aid for Scientific Research (C) (15K03425) and a Grant-in-Aid for Young Scientists (A) (26705003) from the Japan Society for the Promotion of Science, respectively. Adachi also acknowledges financial support from the Japan Economic Research Foundation. Any remaining errors are solely ours.

Abstract

This paper provides a comprehensive analysis of welfare measures when oligopolistic firms face multiple policy interventions and external changes under general forms of market demands, production costs, and imperfect competition. We present our results in terms of two welfare measures, namely, marginal cost of public funds and incidence, in relation to multi-dimensional pass-through. Our arguments are best understood with two-dimensional taxation where homogeneous firms face unit and ad valorem taxes. The first part of the paper studies this leading case. We show, e.g., that there exists a simple and empirically relevant set of sufficient statistics for the marginal cost of public funds, namely unit tax and ad valorem pass-through and industry demand elasticity. We then specialize our general setting to the case of price or quantity competition and show how the marginal cost of public funds and the pass-through are expressed using elasticities and curvatures of regular and inverse demands. Based on the results of the leading case, the second part of the paper presents a generalization with the tax revenue function specified as a general function parameterized by a vector of multi-dimensional tax parameters. We then argue that our results are carried over to the case of heterogeneous firms and other extensions.

1 Introduction

In many economic situations, it is important to understand the impact of changes in government policies, market conditions, or production technology. Both the impact on the economic equilibrium and the associated change in the welfare of individual economic agents are of interest to the policymaker. A convenient framework for studying these questions is laid out in Weyl and Fabinger (2013) for the case of constant changes in marginal cost such as a unit tax. In this paper, we provide a substantial generalization of this framework under general forms of market demands, production costs, and imperfect competition. We allow not only for changes in costs proportional to the value of the goods such as an ad-valorem tax but also for much more general interventions such as different kinds of market regulation. In addition, we provide a new perspective on the case of heterogeneous firms.

The range of possibilities for governments’ intervention is much richer than just specific and ad-valorem taxes, on which the existing literature has focused (see Section 2), especially if we consider regulations of various kinds. Governments often intervene in the marketplace by restricting sales. Examples include restrictions of sales on Sundays and holidays in many European countries, or restrictions of sales of alcohol, both in terms of time of sales and in terms of locations where sales are allowed. Governments also often regulate the labor market. Examples include restrictions on the number of working hours or stipulation of a minimum wage. Besides these, governments also impose reporting requirements that influence the degree to which non-compliant firms misreport their marketplace data to minimize their tax bill.

Given that there are many possible interventions, it is convenient to summarize the interventions of interest in a (multi-dimensional) vector. The impact of infinitesimal changes in these interventions on prices then corresponds to a vector (or more generally a matrix), which may be termed multi-dimensional pass-through. The relative size of its components then provides insight into the relationship between the impact of individual interventions, for example, the impact of specific vs. ad-valorem taxes. We show that the multi-dimensional pass-through is an important determinant of the welfare effects of various kinds of interventions.111The usefulness of pass-through in welfare analysis has been verified by related studies such as Cowan (2012); Miller, Remer, and Sheu (2013); Weyl and Fabinger (2013); Gaudin and White (2014); MacKay, Miller, Remer, and Sheu (2014); Adachi and Ebina (2014a,b); Chen and Schwartz (2015); Gaudin (2016); Cowan (2016); Alexandrov and Bedre-Defolie (2017); Mrázová and Neary (2017); and Chen, Li and Schwartz (2018). See also Ritz (2018) for an excellent survey of theoretical studies on pass-through and pricing under imperfect competition. In the context of antitrust analysis, Froeb, Tschantz, and Werden (2005) theoretically compare the price effects when no synergies in cost reduction realize when they are passed through as a form of price reduction. See also Alexandrov and Koulayev (2015) for discussions on the role of pass-through in antitrust analysis.

Our arguments are best understood with two-dimensional taxation where homogeneous firms face unit and ad valorem taxes. Therefore, in the first part of the paper (Sections 2 and 3), we derive succinct formulas that relate the marginal cost of public funds to pass-through of these taxes. We also establish a relationship that connects pass-through of unit taxes and pass-through of ad-valorem taxes in the same market. Furthermore, we derive convenient expressions for values of unit and ad valorem pass-through that are valid under a “general” type competition and have not appeared in the previous literature. In addition, we show how the marginal cost of public funds and pass-through are expressed in terms of elasticities and curvatures of demand and inverse demand when the setting is specialized to price (differentiated Bertrand) or quantity (pure or differentiated Cournot) competition. We also provide numerical examples. Our results also apply without a change to symmetric oligopoly with multi-product firms. Throughout the analysis, we allow for non-zero levels of unit and ad valorem taxes. However, we also discuss some additional simplifications that appear when instead the initial level of taxes is zero.

Inspired by the results of this setting of two-dimensional taxation, the second part of the paper generalizes our model in two directions (Sections 4, 5, and 6). First, we allow for interventions that are more general than just specific and ad valorem taxes. Second, we introduce firm heterogeneity. We find that these more general relationships have a form that still relatively simple and succinct. This substantially expands the applicability of our results.

From both theoretical and empirical standpoints, it is desirable to be able to understand the welfare properties of oligopolistic markets with a fairly general type of competition. In real-world situations, firms’ behavior may not simply be categorized into either the idealized price competition or the idealized quantity competition. Price competition does not allow for any friction in scaling production levels up or down, yet in reality there tend to be substantial frictions, such as those related to financial constraints or the labor market. Quantity competition implies that the firm will not be able to increase production levels when its competitor suddenly decides to increase prices. In reality, such adjustment is probably feasible, since capacity utilization is typically less than complete, and even if the firm is operating at full capacity, boosting production levels is possible by overtime work or by hiring temporary workers. Moreover, firms may behave, to some extent, in a collusive way. Although the realities of competition by firms may be complicated, it is possible to capture their essence by working with a “general” type of competition, using the conduct index.222Our conduct index is a generalization of what is known as “conduct parameter” in the empirical industrial organization literature, where it is supposed to be constant for any level of industry output as a target of estimation (see, e.g., Bresnahan 1989; Genesove and Mullin 1998; Nevo 1998; Corts 1999; Delipalla and O’Donnell 2001; and Shcherbakov and Wakamori 2017). It has also been successfully applied to more general situations, such as selection markets (Mahoney and Weyl 2017) or supply chains (Gaudin 2018). In this paper, we generalize this concept by allowing it to vary across different levels of output: we thus opt for the term “conduct index” to make it explicit that it is a variable. In a less general setting, such “conduct index” was used by Weyl and Fabinger (2013), where it was still referred to as “conduct parameter”.

Besides working with a more general type of competition, it is also useful to relax the assumption of constant marginal costs that often appears in the literature. Production technologies often have a non-trivial structure, and so does the internal organization of the firm. For example, if a firm decides to operate at a larger scale, it may take advantage of technological and logistical economies of scale, but at the same time, it may face more severe principal-agent problems as top managers have to delegate responsibilities to lower-level managers. The interplay between these forces can lead to a non-trivial dependence of the marginal cost of production on the scale of the operation. A notable benefit from our general framework is that one does not necessarily have to assume constant marginal cost in conducting welfare assessment in a precise manner.

In this spirit, the aim of Weyl and Fabinger’s (2013) study is to analyze imperfect competition in a way that does not rely on limiting functional form assumptions. It is followed by Fabinger and Weyl (2018), who propose using further flexible functional forms to make economic models or their parts solvable in closed form. The present paper goes in a different direction: we focus on more general market interventions and exogenous market changes without requiring that the models or their parts be solved in closed form. As mentioned above, ad valorem taxes are not studied in Weyl and Fabinger (2013). In this paper, we provide a more general framework that allows not only for ad valorem taxes but for other interventions in a general manner.

The rest of the paper mainly consists of two parts: the first part focuses on the canonical situation of two-dimensional taxation where symmetric firms face unit and ad valorem taxes, and the second part extends these results to a more general framework of multiple government interventions and external changes, allowing firm heterogeneity. First, in the next section, we set up a framework of two-dimensional taxation under imperfect competition and provide general formulas for marginal cost of public funds and incidence in relation to unit tax and ad valorem tax pass-throughs and industry demand elasticity. In Section 3, we specialize this setting to the case of price or quantity competition. Then, in the second part of the paper, Section 4 generalizes the results from unit and ad valorem taxation to much more flexible taxation parameterized by different tax parameters and discusses the implications of these general results. We also discuss other types of government/exogenous interventions that are suitable for our framework. Then, in Section 5 we generalize our formulas to include heterogeneous firms. Finally, Section 6 generalizes our previous results to include changes in both production costs and taxes. Section 7 concludes the paper.

2 Taxation and Welfare in Symmetric Oligopoly

We begin with a canonical setting where firms face two types of taxation: unit and ad valorem taxes. This issue has been in the central part of the existing literature on government interventions. The welfare cost of taxation has been extensively studied at least since Pigou (1928). The majority of the studies simply assume perfect competition (with zero initial taxes).333See, e.g., Vickrey (1963), Buchanan and Tullock (1965), Johnson and Pauly (1969), and Browing (1976) for early studies. A study of unit and ad valorem taxation under imperfect competition with homogeneous products dates back to Delipalla and Keen (1992). See Auerbach and Hines (2002) and Fullerton and Metcalf (2002) for comprehensive surveys for this field. As is widely known, under perfect competition, unit tax and ad valorem tax are equivalent, and whether consumers or producers bear more is determined by the relative elasticities of demand and supply (Weyl and Fabinger, 2013, p. 534). The initial attempt to relax the assumption of perfect competition started with an analysis of homogeneous-product oligopoly under quantity competition, i.e., Cournot oligopoly. Notably, Delipalla and Keen (1992), Skeath and Trandel (1994), and Hamilton (1999) compare ad valorem and unit taxes in such a setting. Then, Anderson, de Palma, and Kreider (2001a) extend these results to the case of differentiated oligopoly under price competition. In particular, Anderson, de Palma, and Kreider (2001a) find that whether the after-tax price for firms and their profits rise by a change in ad valorem tax depends importantly on the ratio of the curvature of the firm’s own demand to the elasticity of the market demand.444This curvature is denoted in their notation, whereas we instead use below, and this elasticity is denoted in their notation, whereas we instead use below.

In this section, we extend Anderson, de Palma, and Kreider’s (2001a) setting and results in a number of important directions. First, we consider a “general” mode of competition, captured by the conduct index, including both quantity and price competition. Second, we provide a complete characterization of tax burdens that enables one to quantitatively compare consumers’ burden with producers’ burden, whereas Anderson, de Palma, and Kreider’s (2001a) focus only on the effective prices for consumers and producers’ profits. Third, while Anderson, de Palma, and Kreider’s (2001a) assume constant marginal cost, we allow non-constant marginal cost and show how this generalization makes a difference in our general formulas. Fourth, we further generalize the initial tax level. When they analyze the effects of a unit tax, Anderson, de Palma, and Kreider (2001a) assume that ad valorem tax is zero, and vice versa. In contrast, we allow non-zero initial taxes in both dimensions. Finally, and importantly, we generalize these results to the case of a very general type of taxation, as well as to production cost changes. This opens up the possibility to study a wider range of interventions/taxes and to derive convenient sufficient statistics for characteristics, including welfare characteristics, of the markets of interest.555Our framework is in line with the “sufficient-statistics” approach to connecting structural and reduced-form methods, as advocated by Chetty (2009), which has been successful in empirical economics. For example, in the study by Atkin and Donaldson (2016), the pass-through rate provides a sufficient statistic for welfare implications of intra-national trade costs in low-income countries, without the need for a full demand estimation. Similarly, Ganapati, Shapiro, and Walker (2018) examine the welfare effects of input taxation, where a unit tax is levied on the input. These effects are related to the effects of unit taxes on output, but not identical. See also Fabra and Reguant (2014); Shrestha and Markowitz (2016); Stolper (2016); Hong and Li (2017); Duso and Szücs (2017); Gulati, McAusland, and Sallee (2017); and Muehlegger and Sweeney (2017) for studies with the same spirit. In contrast, Kim and Cotterill (2008) is among the first studies that structurally estimate cost pass-through in differentiated product markets, followed by Bonnet, Dubois, Villas-Boas, and Klapper (2013); Bonnet and Réquillart (2013); Campos-Vázquez and Medina-Cortina (2015); Miller, Remer, Ryan, and Sheu (2016); Conlon and Rao (2016); Miller, Osborne, and Sheu (2017); and Griffith, Nesheim, and O’Connell (2018).

2.1 Setup

Below, we study oligopolistic markets with symmetric firms and a general (first-order) mode of competition and the resulting symmetric equilibria.666Although for brevity we speak of a general mode of competition, we consider only “first-order” competition, in the sense of the firms making decisions based on marginal cost and marginal revenue. This excludes, for example, the possibility of vertical industries, an important issue left for future research. Our discussion applies to single-product firms as well as to multi-product firms if intra-firm symmetry conditions are satisfied, as discussed in Appendix A.1.12. For simplicity of exposition, we use terminology corresponding to single-product firms here, and later we discuss how to interpret the results in the case of multi-product firms.

Formally, the demand for firm ’s product depends on the vector of prices charged by the individual firms. The demand system is symmetric and the cost function is the same for all firms. We assume that and are twice differentiable and conditions for the uniqueness of equilibrium and the associated second-order conditions are satisfied. We denote by the per-firm industry demand corresponding to symmetric prices: . The elasticity of this function, defined as and referred to as the price elasticity of industry demand, should not be confused with the elasticity of the residual demand that any of the firms faces.777The elasticity here corresponds to in Weyl and Fabinger (2013, p. 542). Note that for any two distinct indices and . We will define the firm’s elasticity and other related concepts in Section 3. We also use the notation for the reciprocal of this elasticity as a function of . For the corresponding functional values, when we do not need to specify explicitly their dependence on either or , we use interchangeably with .

As mentioned above, we introduce two types888This specification corresponds to a two-dimensional (tax) instrument , which is a special case of multi-dimensional instruments. For example, if the cost function had an additional technology parameter , we could describe the situation using a three-dimensional instrument In Section 4, we introduce a framework for multi-dimensional pass-through. For now, we specialize to the two-dimensional case of specific and ad valorem taxes, which are very common: for example, in the United States both types of taxes are imposed on the sales of soda, alcohol and cigarettes. of taxation: a unit tax and an ad valorem tax , with firm ’s profit being . At symmetric quantities the government tax revenue per firm is , and we denote by the fraction of firm’s pre-tax revenue that is collected by the government in the form of taxes: . We now introduce the conduct index , which measures the industry’s competitiveness (a lower corresponds to a fiercer level of competition). Here, it is determined independently of the cost side but potentially can change for different values of the industry’s output, . Then, the symmetric equilibrium condition is written as

| (1) |

where is the marginal cost of production.999As already noted in Footnote 2 above, is a generalization of conduct parameter in the sense that it is a function of rather than a constant for any . Hence, Equation (1) should not be interpreted as an equation that defines . For our analysis we introduce in an implicit manner: is a function independent of the cost side of the problem such that Equation (1) is the symmetric first-order condition of the equilibrium. For specific types of ("first-order") competition, such as those discussed in Section 3, it is possible to derive explicit expressions for that can replace our implicit definition. Presumably, it is natural to assume : a smaller amount of production is associated with a smaller degree of competitiveness in the industry due to other reasons than non-cooperative and simultaneous pricing (modeled here), such as (unmodeled) tacit collusion. However, this restriction is not necessary for the following analysis. Also, note that is not necessarily excluded, although in most interesting cases it lies in . We denote by the functional value of at the equilibrium quantity. This is also understood as the elasticity-adjusted Lerner index: the markup rate should be adjusted by the industry-wide elasticity to reflect the competitiveness in the industry, where is interpreted as the effective marginal cost.101010Accordingly, one can write the modified Lerner rule under as which implies the restriction on : . We emphasize here that once the conduct index is introduced, one is able to describe oligopoly in a synthetic manner, without specifying whether it is price or quantity setting, or whether it exhibits strategic substitutability or complementarity.

2.2 The marginal cost of public funds and pass-through

The marginal cost of public funds, i.e., the marginal social welfare loss associated with raising additional tax revenue, is a crucial characteristic that a policymaker needs to take into account when designing an optimal system of taxes.111111In the absence of other considerations, the marginal cost of public funds should be equalized across markets in order to maximize social welfare. In the special case of linear demand and constant marginal cost, Häckner and Herzing (2016, p. 147) explain that as long as the initial level of taxes is zero, the marginal cost of public funds for unit taxation equals , where is the unit-tax pass-through rate (the marginal effect of unit taxes on prices), and is the conduct index. For ad valorem taxes, Häckner and Herzing (2016) provide a similar formula. They argue, however, that if we let the initial level of taxes be non-zero, those formulas are no longer valid. For this reason, they are forced to analyze the magnitude of the marginal cost of public funds on a case-by-case basis using explicit solutions to specific models.

This situation represents a puzzle. If there are simple formulas for the marginal cost of public funds that were valid at zero taxes, is there no compact generalization of these expressions in the case of non-zero taxes? If there is no such generalization, that would be an obstacle to empirical work, since we would have to make additional modeling assumptions before obtaining empirical estimates of the marginal cost of public funds. Our paper provides a solution to this problem. In particular, Proposition 1 below presents formulas for the marginal cost of public funds that are valid even when the initial level of (both ad valorem and unit) taxes is non-zero. They are a bit longer than , but still very manageable. They also represent a starting point for the topics discussed in the rest of the paper. These results with a non-zero initial taxes being allowed, which are differentiated from Weyl and Fabinger (2013) and Häckner and Herzing (2016), should be useful if one needs to evaluate the marginal cost of taxation when some tax has been already implemented.

The marginal welfare cost or of raising government revenue by the unit tax or the ad valorem tax , i.e. the marginal cost of public funds associated with such a tax, is defined as

where is the social welfare per firm, which includes consumer surplus, producer surplus, and government tax revenue. We define the unit tax pass-through rate and the ad valorem tax pass-through semi-elasticity as:121212Note that Häckner and Herzing (2016) use the symbol for the ad valorem tax pass-through rate , which corresponds to in our notation.

Consider an infinitesimal change in the unit tax, with the initial tax level . As mentioned in the introduction, in the special case of zero initial taxes, linear demand, and constant marginal cost, Häckner and Herzing (2016, p. 147) show that and , noting that at non-zero initial taxes the formula no longer applies. In the absence of such formula, they were forced to study the marginal cost of public funds on a case-by-case basis, for different specifications of demand and cost.

Intuitively, there are at least two reasons why fails to be an accurate measure of the marginal cost of public funds when a unit tax is raised.131313An analogous argument applies for and the marginal cost of public funds of tax . First, the expression is simply proportional to , but when is large, the firms sell at prices that are too high from the social perspective not mainly because of a lack of competitiveness, but primarily because the tax effectively raises their perceived cost. When is large, we would expect the marginal cost of public funds to be less sensitive to , for a given value of . Second, the expression does not explicitly feature the level of the unit tax . However, a situation where is large and small is very different from a situation where is small and large, even if the equilibrium prices and quantities are the same. In the former case, raising additional tax revenue is quite harmful, since firms’ production cuts will not substantially decrease the total technological (i.e., pre-tax) cost of production. In the latter case, raising additional tax revenue is less harmful since it leads to reduced total technological cost. Based on this intuition, we would expect the marginal cost of public funds to be an increasing function of .141414In the sense of making the change , and simultaneously in order to keep , , and at some fixed values.

Thus, we are led to find a generalization of the formula and that would be applicable even at non-zero initial taxes. It turns out that it is possible to identify a formula with precisely these properties, as the following proposition shows.

Proposition 1.

Marginal cost and total of public funds for unit and ad valorem taxations. Under symmetric oligopoly with a possibly non-constant marginal cost, the marginal cost of public funds associated with a unit tax may be expressed as

and the marginal cost of public funds associated with an ad valorem tax may be expressed as

The proposition is proven in Appendix A.1.1 and the intuition behind it is discussed in detail in Appendix A.1.2. Here in the main text we just include Figure I, which documents that these expressions for the marginal cost of public funds and evaluated at realistic values of taxes and other economic variables are very different from the values of the expressions and (discussed above) that would be equal to and if taxes were zero.

2.3 Incidence and pass-through

We define the incidence of unit taxation as the ratio of changes in (per-firm) consumer surplus and changes in (per-firm) producer surplus induced by an infinitesimal increase in the unit tax . The incidence of ad valorem taxation is defined analogously. We obtain the following succinct results for the incidence of taxation at non-zero unit and ad valorem taxes.

Proposition 2.

Incidence of taxation. Under symmetric oligopoly with a general type of competition and with a possibly non-constant marginal cost, the incidence of unit taxes and of ad valorem taxes is given by

The proposition is proven in Appendix A.1.3, and we discuss it in detail in Appendix A.1.4. Note that in the case of zero ad valorem tax, the expression for reduces to Weyl and Fabinger’s (2013, p. 548) Principle of Incidence 3. Next we show how and are related in the following proposition.

Proposition 3.

Relationship between pass-through of ad valorem and unit taxes. Under symmetric oligopoly with a possibly non-constant marginal cost, the pass-through semi-elasticity of an ad valorem tax may be expressed in terms of the unit tax pass-through rate , the conduct index , and the industry demand elasticity as

| (2) |

The proposition is proven Appendix A.1.5, and Appendix A.1.6 provides a detailed discussion. Combined with Proposition 1, it is consistent with the well-known result that unit tax and ad valorem tax are equivalent in the welfare effects under perfect competition: if , then . Under imperfect competition, , and . This provides another look of Anderson, de Palma, and Kreider’s (2001b) result that unit taxes are welfare-inferior to ad valorem taxes.151515Under Cournot competition, Equation (6.13) of Auerbach and Hines (2002) coincides with Equation (2) above. Proposition 3 shows that this equation holds more generally. We thank Germain Gaudin for pointing this out.

By combining Propositions 1 and 3, we find that and can be expressed without the degree of competitiveness .

Proposition 4.

Sufficient statistics for marginal costs of public funds. Under symmetric oligopoly with a possibly non-constant marginal cost, the unit pass-through rate , the ad valorem pass-through semi-elasticity , and the elasticity of industry demand (together with the tax rates and the fraction of the firm’s pre-tax revenue collected by the government in the form of taxes) serve as sufficient statistics for the marginal cost of public funds both with respect to unit taxes and ad valorem taxes. In particular:

The proof is simple: Proposition 3 allows us to express the conduct index as . Substituting this into the relationships in Proposition 1 then gives the desired result. For a detailed discussion of related intuition, see Appendix A.1.7.

As the last result presented in this section, the following proposition shows how the two forms of pass-through are characterized.

Proposition 5.

Pass-through under symmetric oligopoly. Under symmetric oligopoly with a general (first-order) mode of competition and with a possibly non-constant marginal cost:

where the derivative is taken with respect to and is the elasticity of the marginal cost with respect to quantity. Further,

The proof and a related discussion are in Appendix A.1.8. Further, we discuss a relationship with Weyl and Fabinger (2013) in Appendix A.1.9, provide a comparison of perfect and oligopolistic competition in Appendix A.1.10, and show the applicability of these results to exchange rate changes in Appendix A.1.11.

2.4 Global changes in surplus measures

So far, we have discussed local, i.e. infinitesimal, changes in surplus measures (, , , ). For larger changes in some tax , it is desirable to have an understanding of global changes in surplus measures. Consider surplus measures and . Their finite changes and induced by a tax change from to are related to their incidence ratios . In particular, is a weighted average of over the interval :

where is a weight normalized to one on the corresponding interval: . The weight is positive as long as has the same sign as , which is typically satisfied in useful applications. In many useful cases and are zero at infinite . Then

For example,

In the case of a per-unit tax, we obtain161616Note that in this case

3 Taxation and Welfare under Specific Types of Competition

In this section, we show that for price competition and quantity competition in differentiated oligopoly, our general expressions of the marginal cost of public funds and pass-through lead to expressions in terms of demand primitives such as the elasticities and the curvatures, and the marginal cost elasticity defined above.171717The question of whether quantity- or price-setting firms are more appropriate depends on the nature of competition. As Riordan (2008, p. 176) argues, quantity competition is a more appropriate model if one depicts a situation where firms determine the necessary capacity for production. However, price-setting firms are more suitable if firms in the industry of focus can quickly adjust to demand by changing their prices. Although the real-world case of competition is not as clear-cut as this, as we have emphasized in Introduction, we argue below that it is possible to provide another useful characterization for the marginal costs of public funds and the pass-through rates by specifying the mode of competition. Throughout this section, we assume that firms’ conduct is simply described by one-shot Nash behavior, without any other further possibilities such as tacit collusion. As seen below, this assumption enables one to express the conduct index in terms of demand and inverse demand elasticities, using Equation (1) directly (see Subsection 3.2). We also provide parametric examples for these results.

3.1 Elasticities and curvatures of the demand system

Direct demand. Following Holmes (1989, p. 245), we define the own price elasticity and the cross price elasticity of the firm’s direct demand by

where and is an arbitrary pair of distinct indices. These are related to the industry demand elasticity by .181818Holmes (1989) shows this for two symmetric firms, but it is straightforward to verify this relation more generally. See the equation in Footnote 7 above. Note that the equation simply means that the percentage of consumers who cease to purchase firm ’s product in response to its price increase is decomposed into (i) those who no longer purchase from any of the firms () and (ii) those who switch to (any of) the other firms’ products (). Thus, measures the firm’s own competitiveness: it is decomposed into the industry elasticity and the degree of rivalry. In this sense, these three price elasticities characterize “first-order competitiveness,” which determines whether the equilibrium price is high or low, but one of them is not independently determined from the other two elasticities. Next, we define the curvature of the industry’s direct demand , the own curvature of the firm’s direct demand and the cross curvature of the firm’s direct demand:191919The curvature here corresponds to of Aguirre, Cowan, and Vickers (2010, p. 1603).

where again the derivatives are evaluated at , and and is an arbitrary pair of distinct indices. These curvatures satisfy and are related to the elasticity of by (see Appendix A.2.1 for the derivation and a related discussion).

Inverse demand. We introduce analogous definitions for inverse demand. We define the own quantity elasticity and the cross quantity elasticity of the firm’s inverse demand as

for arbitrary distinct and . These satisfy .202020The identity means that as a response to firm ’s increase in its output, the industry as a whole reacts by lowering firm ’s price (). However, each individual firm (other than ) reacts to this firm ’s output increase by reducing its own output. This counteracts the initial change in the price ), and thus a percentage reduction in the price for firm ) is smaller than , which does not take into account strategic reactions. Note here that , not , measures the industry’s competitiveness. Thus, these three quantity elasticities characterize “first-order competitiveness,” which determines whether the equilibrium quantity is high or low. We define the curvature of the industry’s inverse demand , the own curvature of the firm’s inverse demand and the cross curvature of the firm’s inverse demand by:

where again the derivatives are evaluated at and the indices and are distinct. These curvatures represent an oligopoly counterpart of monopoly of Aguirre, Cowan, and Vickers (2010, p. 1603). They satisfy the relationship and are related to the elasticity of by (see Appendix A.2.2 for the derivation and a related discussion).

3.2 Expressions for conduct index and pass-through

In the case of price competition, the conduct index is , which is verified by comparing the firm’s first-order condition with Equation (1). The marginal cost of public funds and the incidence are obtained by substituting these expressions into those of Propositions 1 and 2.

Proposition 6.

Pass-through under price competition. Under symmetric oligopoly with price competition and with a possibly non-constant marginal cost:

Next, in the case of quantity competition, the conduct index is given by , which is, again, verified by comparing the firm’s first-order condition with Equation (1). Again, the marginal cost of public funds and the incidence are obtained by substituting these expressions into those of Propositions 1 and 2. For the proof and a related discussion, see Appendix A.2.5 and A.2.6.

Proposition 7.

Pass-through under quantity competition. Under symmetric oligopoly with quantity competition and with a possibly non-constant marginal cost:

3.3 Simple parametric examples

Although our formulas are general, it is illustrative to work through a few simple examples. Below we provide two parametric examples with symmetric firms and constant marginal cost: . In this case, the pass-through expressions are simplified to

under price competition, where , and

under quantity competition, where .

3.3.1 Linear demand

One is the case wherein each firm faces the following linear demand, , where and , implying that all firms produce substitutes and measures the degree of substitutability (firms are effectively monopolists when ).212121These linear demands are derived by maximizing the representative consumer’s net utility, , with respect to and . See Vives (1999, pp. 145-6) for details.,222222In our notation below, the demand in symmetric equilibrium is given by , whereas it is written as in Häckner and Herzing’s (2016) notation, where is the parameter that measures substitutability between (symmetric) products. Thus, if our is determined by , , and , given Häckner and Herzing’s (2016) , then our results below can be expressed by Häckner and Herzing’s (2016) notation as well. Note here that our formulation is more flexible in the sense that the number of the parameters is three. This is because the coefficient for the own price is normalized to one: , which is analytically innocuous, and Häckner and Herzing’s (2016) is the normalized parameter. Under symmetric pricing, the industry’s demand is thus given by . The inverse demand system is given by

implying that under symmetric production. Obviously, both the direct and the indirect demand curvatures are zero: . Thus, the pass-through rates are simply given by

under price competition, where , and (where and are the equilibrium price and output under price setting), and

under quantity competition, where and (where and are the equilibrium output and price under quantity setting).

Now, from Propositions 1 and 2, the marginal cost of public funds and the incidence are given by

under price competition, with is additionally provided, where and are the equilibrium price and output under price setting, and

under quantity competition, with is additionally provided, where and are the equilibrium price and output under quantity setting. Thus, it suffices to solve for the equilibrium price and output under both settings to compute the pass-through rate and the marginal cost of public funds for all four cases.

| (a) Linear Demand | |

| Price setting | Quantity setting |

| (b) Logit Demand | |

| Price setting | Quantity setting |

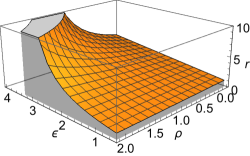

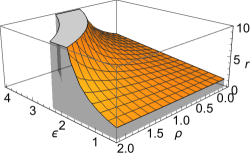

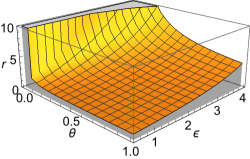

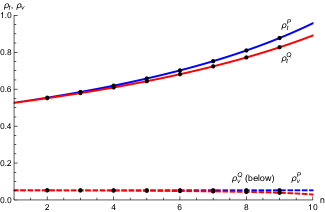

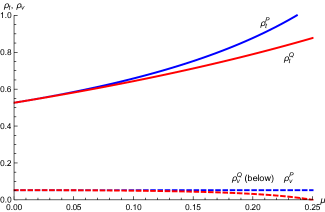

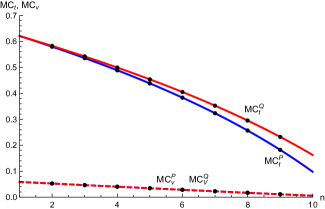

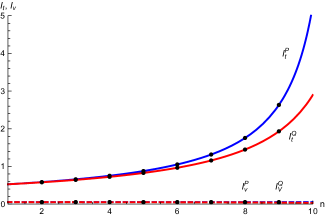

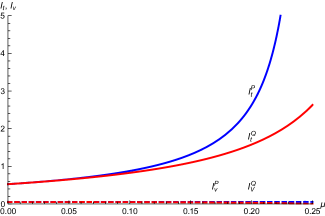

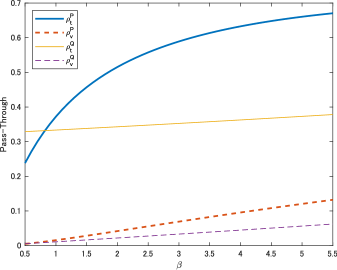

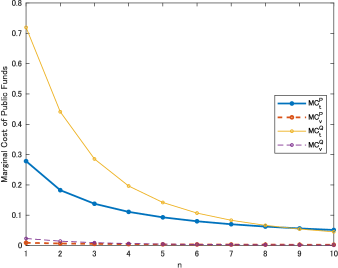

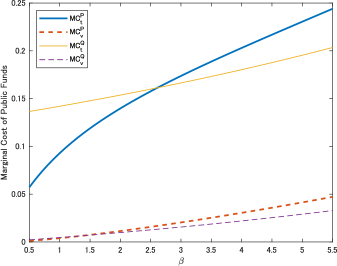

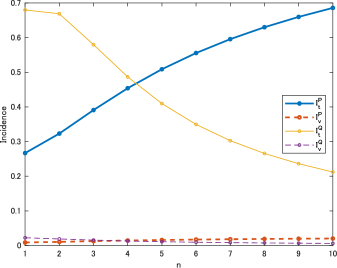

Table I (a) summarizes the key variables that determine the pass-through rates and the marginal costs of public funds. It is verified that under both price and quantity competition, and . To focus on the roles of these two parameters, and , which directly affect the degree of competition, we employ the following simplification to compute the ratio in equilibrium: , , and (see Appendix A.2.7 for the actual expressions of the equilibrium prices and outputs under price and quantity competition).

The top two panels in Figure II illustrate how and behave as the number of firms (; the left) or the sustainability parameter (; the left) increases, with the superscript denoting price () or quantity () setting. Similarly, the middle and the bottom panels draw and , and and , respectively. It is observed that the ad valorem tax pass-through rates are close to zero because in this case both and are close to 1. As competition becomes fiercer, both and become larger, although the discrepancy also becomes larger. In the case of linear demand, the difference in the mode of competition does not yield a significant difference in each of the three measures. As is verified by Anderson, de Palma, and Kreider (2001b), the ad valorem tax is more efficient than the unit tax: the dashed lines in the two middle panels lie below the solid lines. This ranking is related inversely to the pass-through and the incidence: as the pass-through or the incidence becomes larger, the marginal cost of public funds becomes smaller.

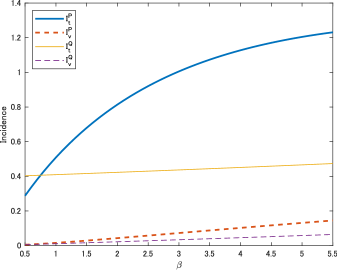

3.3.2 Logit demand

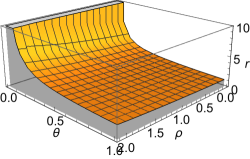

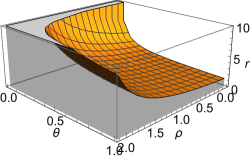

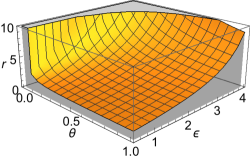

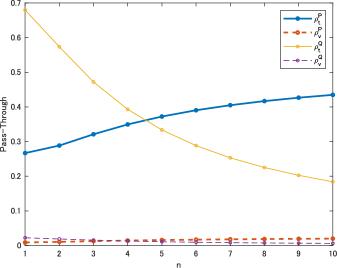

The next parametric example is the logit demand. Each firm faces the following demand: , where is the (symmetric) product-specific utility and is the responsiveness to the price.232323Here, is derived by aggregating over individuals who choose product (the total number of individuals is normalized to one): individual ’s net utility from consuming is given by , whereas is the net utility from consuming nothing, and are independently and identically distributed according to the Type I extreme value distribution for all individuals. See Anderson, de Palma, and Thisse (1992, pp. 39-45) for details. We work in terms of market share variables and , instead of and , which is consistent with the usual notation in the industrial organization literature. We define as the share of all outside goods. Table I (b) summarizes the key variables that determine the pass-through rates and the marginal costs of public funds. We need to numerically solve for the equilibrium price and market share under both settings to compute the pass-through rate, the marginal cost of public funds, and incidence for all four cases. To focus on the two parameters, and , we assume that and . Because , the first-order conditions for the symmetric equilibrium price and the market share satisfy and . If and are solved numerically, then , , and can also be numerically computed.242424It can be verified that is convex as long as because . However, the second-order condition is always satisfied because . In symmetric equilibrium with and , the largest market share is attained as when the equilibrium price is zero, which implies that the market share of the outside goods is no less than each firm’s market share: . Next, we consider the inverse demands under quantity competition. Then, as in Berry (1994), firm ’s inverse demand is given by , which implies that . Thus, the first-order conditions for the symmetric equilibrium price and the market share satisfy and . Then, as above, , , and are computed by numerically solving the first-order conditions for and . Interestingly, it is verified that in symmetric equilibrium under quantity setting, : the equilibrium price is the same irrespective of the number of firms, whereas the individual market share is decreasing in the number of firms: . On the other hand, both the equilibrium price and market share are decreasing in the price coefficient, .

Figure III illustrates the pass-through rate, the marginal cost of public funds, and the incidence, in analogy with Figure II. The right panels now show the variables’ dependence on the price coefficient . Overall, as in the case of linear demand, an increase in the ad valorem tax has a small impact on these measures for each of and , whereas an increase in the unit tax has a large effect. However, there are important differences between the cases of linear and logit demand. First, the unit tax pass-through under quantity competition is decreasing in the number of firms. To understand this, compare the difference in the denominators of and . As decreases (i.e., as competition becomes fiercer), the second term in the denominator of decreases, and thereby increases as increases. However, increases as decreases, and thus decreases. This difference in the denominators is also reflected in the fact that is decreasing in as well. Naturally, is decreasing in as in the case of linear demand because becomes larger (see the formulas in Proposition 1). Second, while the pass-through rate and the incidence increase as increases, the marginal cost of public funds is also increasing in contrast to the case of linear demands. The reason is that the effect on of decreases in is weaker than the effect of the increase in : the industry’s demand becomes elastic quickly as consumers become more sensitive to a price increase.

4 Multi-Dimensional Pass-Through Framework

Now, we generalize our previous results to a more general specification of taxation that involves multiple tax instruments. We define two different types of pass-through vectors: (i) the pass-through rate vector and (ii) pass-through quasi-elasticity. We study their properties and show that they play a central role in evaluating welfare changes in response to changes in taxation.

4.1 Pass-through, conduct index, and welfare: A general discussion

4.1.1 Generalized pass-through and tax sensitivities

Consider a tax structure under which a firm’s tax payment is expressed as , where is a -dimensional vector of tax instruments252525To be precise, represents a simplified notation for a function with arguments. so that the firm’s profit in symmetric equilibrium is written as . Note that the argument so far is a special case of two dimensional pass-through: , where . The components of the (per-firm) tax revenue gradient vector are

Here, as in other parts of the paper, we use the symbol for the -dimensional gradient with respect to . The arguments and in are treated as fixed for the purposes of taking this gradient. We also denote by a vector components . We denote the equilibrium price function262626Unlike the inverse demand function , the function takes the vector of taxes as arguments, and its functional value is the price in the resulting equilibrium. by and its gradient, the pass-through rate vector, by Further, we use the components of the and to define the pass-through quasi-elasticity vector as

Note that the components of are all dimensionless. We define the (first-order) price sensitivity of the tax revenue and the (first-order) quantity sensitivity of the (per-firm) tax revenue as follows:

and their derivatives are

The analogous definitions for the second-order sensitivities are:

The first-order and second-order sensitivities are dimensionless, as are the components of . In this section, we keep the same definition of the elasticities and as before.

4.1.2 Generalized conduct index

We introduce the conduct index as a function, independently of the cost-side of the oligopoly game, so that in equilibrium the following condition holds:

| (3) |

In the case of unit and ad valorem taxation, this definition reduces to the conduct index defined earlier (Equation 1), where and : this is the reason why we can keep using below. In principle, there are many possible definitions that agree with the earlier definition in the case of unit and ad valorem taxation. However, we find the specification of Equation 3 particularly convenient.

4.1.3 Relationships for the pass-through vector components

We now establish the following relationship for the relative size of pass-through vector component.

Proposition 8.

The pass-through rates and quasi-elasticities satisfy 272727If the denominators are zero, the fractions become ill-defined. In that case, of course, the statement does not apply.

The proposition is proven in Appendix A.3.1. Since the components have known proportions, we can write them using a common factor as

| (4) |

with the factor determined in the following proposition.

Proposition 9.

The value of the factor introduced in Equation (4) is given by:

| (5) |

where with the prime denoting a derivative with respect to the quantity

The proof is in Appendix A.3.2.282828If , then and First, and Next, because and . Then, since and

4.1.4 Welfare changes and their relationship to pass-through vectors

Now, we establish the general formulas for the marginal cost of public fund and incidence in the multi-dimensional pass-through framework. Welfare component changes in response to an infinitesimal change in taxes can be found as follows. The (per-firm) consumer surplus change in response to an infinitesimal change in the tax is

which means that in vector notation, . The change in (per-firm) producer surplus is

where we utilize Equation (3) to eliminate the marginal cost. In vector notation, this is , since . The change in tax revenue is

In vector notation, . Finally, for the change in social welfare, we have

In vector notation, .

Note that the welfare components , and are all treated as functions of taxes only and represent the equilibrium outcomes. This is different from the tax revenue function , which has also and as arguments and which is specified by the government irrespective of the equilibrium. We summarize these findings in the following proposition.

Proposition 10.

The tax gradients of consumer surplus, producer surplus, tax revenue, and social welfare with respect to the taxes all belong to a two-dimensional vector space spanned by and . The precise linear combinations of and are

These relationships, considered component-wise, immediately imply the following results for welfare change ratios and generalize Propositions 1 and 2.292929Remember that the component of the vector is .

Proposition 11.

The marginal cost of public funds of a tax , , is

The incidence of this tax, , equals:

Similarly, the social incidence, , equals:

4.2 Pass-through, conduct index, and welfare: special cases

The results of the previous subsection contain our results for ad valorem and unit taxes as special cases, but provide much greater generality, since the taxes (government interventions) may be specified in a very flexible way.

4.2.1 Exogenous competition and depreciating licenses

Weyl and Fabinger’s (2013) results under symmetric oligopoly can be interpreted as special cases of the present results. In particular, Weyl and Fabinger’s (2013) analysis considers either unit taxes or exogenous competition (an exogenous quantity supplied to the market). The case of unit taxes is clearly included in the present results, which has motivated this paper. At the same time, it turns out that the case of exogenous competition is included as well. The reasoning is as follows.

Consider a tax of the form: . Then, the firm’s profit is given by:

The firm, therefore, has the same profit function as in the case of exogenous competition in Weyl and Fabinger (2013). Proposition 11 above (specialized to constant marginal cost and zero initial ) then implies the social incidence result in Principle of Incidence 3 in Weyl and Fabinger (2013, p. 548).

Similarly, the relationships between pass-through of unit taxes and of exogenous competition are implied by the general result of Proposition 8 for the tax specification , ,

To obtain the absolute size of the two types of pass-through, one can straightforwardly use Proposition 9. More generally, is extended as

where an ad valorem tax is also considered. As an example, one can think of a government which procures goods from abroad and supplies them to the market in order to lower domestic prices.

In the special case of a monopolist with constant marginal cost, the mathematics allow for another interesting interpretation: It is isomorphic to the case of “depreciating licenses” in Weyl and Zhang (2017). Depreciating licenses correspond to a tax scheme where the owner of an asset announces a reservation price at which she is willing to sell it and gets taxed a fixed fraction of that prices. Another agent in the economy may buy the asset at the announced price. The owner then faces a tradeoff between announcing a low price and paying low taxes and announcing a high price in order to be able to keep the asset and derive utility from it. The optimization problem then leads to exactly the same mathematical form as the problem of a monopolist with constant marginal cost facing exogenous competition. We include a more detailed explanation in Appendix A.3.3.303030We thank Glen Weyl for suggesting this relationship between Weyl and Zhang (2017) and our analysis.

4.2.2 Sales restrictions

Governments often regulate when, where, and to whom products may be sold. For example, there are restrictions on weekend sales, store locations, etc. A simple way of modeling this situation is to assume that due to the restrictions a firm loses a fixed proportion of its customers. If the absence of the regulation and taxation, the profit function is . The new profit function will be , where is the fraction of customers lost. The only change is in the argument of the inverse demand function: for the firm to sell quantity , each remaining customer needs to buy times more than in the absence of the regulation, and the price would have to be correspondingly lower. This change may be described using as:

For demand with constant elasticity , , independently of .

4.2.3 Tax evasion/tax avoidance and concealment costs

Tax evasion, clearly, is a very important problem in many situations since economic agents do not always strictly follow the law (Choi, Furusawa, and Ishikawa 2017).

For simplicity, consider a firm that needs to pay an ad valorem tax , where is the price reported to the government and may differ from the true price . We capture the cost associated with deceiving the government by introducing a concealment cost of the form:

The firm then chooses the reported price to minimize the sum of these two additional costs:

The corresponding first-order condition implies , which gives the effective additional cost

The government needs to pay additional enforcement cost inversely related to , which needs to be remembered in the welfare analysis.

5 Heterogeneous Firms

In this section, we extend our results to the case of heterogeneous firms (i.e. asymmetric firms), where each firm controls a strategic variable , which could be, for example, the price or quantity of its product. We allow for the tax function to depend explicitly on the identity of the firm; we write for its derivative with respect to tax . Similarly, the sensitivities , , etc., now also have the firm index . The marginal cost of firm is also allowed to depend on the identity of the firm, and we denote its elasticity

5.1 Pricing strength index and pass-through

We define the pricing strength index of firm to be a function independent of the cost side of the economic problem such that the first-order condition for firm is:

In the special case of symmetric firms, this definition reduces to .

We express the pass-through rate in terms of these pricing strength indices. Specifically, the pass-through rate is an matrix with rows and elements . It is shown that the pass-through rate equals

| (6) |

where the factors on the right-hand side are defined as follows. The matrix is an matrix, independent of the choice of , with elements

where is the Kronecker delta, and

For each tax , is an -dimensional vector with components

In the case of symmetric firms and at symmetric prices, the pass-through rate expression in Equation (6) agrees with the expression represented by Equations (4) and (5) in Section 4.313131To confirm this agreement, note that at symmetric prices, . Note also that and for , .

To generalize the notion of pass-through quasi-elasticity to the case of heterogeneous firms, we define the pass-through quasi-elasticity matrix as an matrix with elements

and with rows denoted .

5.2 Welfare changes

In the following, for each , is an -dimensional vector with its -th component equal to . For the tax gradients of welfare components corresponding to individual firms we obtain:

The corresponding gradients of total welfare components are then obtained by adding up contributions from individual firms. For example, . Denoting the total quantity as , this means that is a weighted average of , with the weights proportional to . The arguments for the other welfare components are similar. This generalizes Proposition 10 above.

We can also consider ratios of welfare changes corresponding to some tax :

where The ratios of the corresponding total welfare changes will be weighted averages of these firm-specific ratios. The weights correspond to the sizes of the denominators times . For example, will lie between and . The same reasoning also holds for the other ratios. This generalizes Proposition 11 above.

5.3 Conduct index and welfare changes

For heterogeneous firms, we introduce the conduct index of firm so that

holds. In the special case of only unit taxation, this definition reduces to Weyl and Fabinger’s (2013, p. 552) Equation (4). In the special case of symmetric firms the definition reduces to our Equation (3) with .

The conduct index is closely connected to the pricing strength index , but not as closely as it would be in the case of symmetric oligopoly. Using the definitions of the indices, it is shown that

For symmetric oligopoly, this equation reduces simply to

The conduct index is used to express welfare component changes in response to infinitesimal changes in taxes. The relationships are a bit more complicated than in the case of using the pricing strength index: they can be expressed as follows. We define the price response to an infinitesimal change in the strategic variable of firm as

Since the vectors , , … , form a basis in the -dimensional vector space to which for a given belongs, we can write as a linear combination of them for some coefficients :

For changes in consumer and producer surplus, we obtain:

where we used the notation

These surplus change expressions represent a generalization of the surplus expressions in Weyl and Fabinger’s (2013) Section 5.

5.4 Aggregative games

In the case of oligopoly in the form of aggregative games, where all other firms’ actions are summarized as an aggregator in each firm’s profit, we can further manipulate the above formulas for pricing strength and conduct indices.323232Here, we consider a setup in Anderson, Erkal, and Piccinin’s (2016) Section 2. We identify the firm’s strategic variable with an action the firm can take, which contributes to an aggregator . The prices and quantities are functions of just two arguments: and . Their derivatives that take into account the dependence of on the action of firm are and . The firm’s first-order condition is:

which gives us a relatively simple expression for the pricing strength index:

The expression for the conduct index also simplifies:

where is a normalized version of unnormalized “weights” ,

and

These simplified formulas would be used for further analysis of pass-through and welfare in aggregative oligopoly games.

6 Pass-Through and Welfare under Production-Cost and Taxation Changes

In the previous sections, we have studied changes in taxation, but not changes in production costs. Here, we generalize our main results to incorporate both taxation and production costs. As shown below, the generalization to production cost changes turns out to be straightforward. These more general formulas may be applied to a range of economic situations such as cost changes due to exchange rate movements or movements in the world prices of commodities.

The additional cost to the firm is denoted as before, but the tax bill of firm , denoted , is different, in general. Here is a vector of interventions (by the government or by external circumstances), which may or may not include traditional taxes. We recover the previous case of only taxation by setting . If all of the additional cost to the firm comes from the production side, we have . In general, is the production part of the additional cost .

6.1 Symmetric firms

In addition to the notation used in the previous section, we define . First, we obtain a generalization of the formulas for the tax gradients of welfare components in Proposition 10. The equilibrium outcome depends only on the additional cost and not on its split between taxes and production costs. For this reason, the formulas for consumer and producer surplus will be unchanged. The government revenue and therefore also total social welfare depends on . In the formula for the gradient of government revenue, will be replaced by , and the formula for social welfare will be adjusted to reflect this difference. Hence, the generalization of the results in Proposition 10 is:

We further define , which represents the fraction of an increase in additional cost () to the firm (due to a change in the tax parameter ) that is collected by the government in the form of taxes (). In other words, is the government’s share in increases of the additional costs induced by marginal changes in . If is a pure tax, then , and if is a pure production cost with no tax component, then . By taking ratios of the components of the tax gradients above, we obtain a generalization of Proposition 11: The marginal cost of public funds associated with intervention , , is

The incidence of this intervention, , equals:

Similarly, the social incidence, , equals:

6.2 Heterogeneous firms

The adjustments to our formulas needed to generalize the results of Subsection 5.2 are analogous to the case of symmetric firms we just discussed. For each firm , we define For the welfare gradients, we obtain:

Similarly, for each firm , we define . For the firm-specific welfare change ratios, we obtain:

7 Concluding Remarks

In this paper, we characterize the welfare measures of taxation and other external changes in oligopoly with a general specification of competition, market demand and production cost. For symmetric oligopoly, we first derive formulas for marginal welfare losses from unit and ad valorem taxation, and , using the unit tax pass-through rate and the ad valorem tax pass-through semi-elasticity (Proposition 1) as well as the formulas for tax incidence, and (Proposition 2). We then show that can be expressed in terms of (Proposition 3). These relationships are used to derive sufficient statistics for and (Proposition 4). The pass-through is also characterized, generalizing Weyl and Fabinger’s (2013) formula (Proposition 5). In the case of price or quantity competition, we explain how and can be written only in terms of the demand elasticities, the demand curvatures, and the marginal cost elasticity (Propositions 6 and 7). We have discussed the relationships to other quantities of interest, as well as illustrative special cases.

The second part of the paper extends the results beyond the two-dimensional taxation problem. Specifically, we show that the previous results have a very natural generalization to a general specification of the tax revenue function as a function parameterized by a vector of tax parameters (Propositions 8, 9, 10, and 11). We further discuss an extension of our analysis to the case of asymmetric oligopoly, where the firms face different costs and possibly also different taxes (Section 5).333333By allowing (constant) asymmetric marginal costs, Anderson, de Palma, and Kreider (2001b) show that under quantity competition with homogeneous products (i.e., Cournot competition), ad valorem taxation is still preferable to unit taxation, although they were not able to verify if the same conclusion held under quantity competition with product differentiation. However, Anderson, de Palma, and Kreider (2001b) discuss a specific demand system (with perfectly inelastic individual demand) under which unit taxation is preferable to ad valorem taxation if the required tax revenue is sufficiently high. We conjecture that one could obtain further generalization by allowing the conduct index to be firm-specific. See also Zimmerman and Carlson (2010) for a parametric analysis of asymmetric firms.,343434Interestingly, Tremblay and Tremblay (2017) study tax incidence in an asymmetric duopoly where one firm competes in price and the other firm competes in quantity, focusing on unit taxation. The pass-through rates can be different for the two identical firms (in terms of demand and cost): the quantity-competing firm has a higher pass-through rate than the price-competing firm has. This is in contrast with the result that the pass-through rate under price competition is generally higher under quantity competition. In addition, we provide a generalization of our results to the case of changes in both production costs and taxes (Section 6).

As already mentioned above, it would be possible to extend our analysis to the case of supply chains (Peitz and Reisinger 2014). Other possible directions include the case of two-sided platform competition (White and Weyl 2016; and Tremblay 2018) and the case of the interactive effects of taxation for multiple imperfectly competitive product markets.353535Among many others, Ballard, Shoven, and Whalley (1985) study this issue for perfectly competitive markets. In addition, our methodology could be utilized to study other important issues of pricing in general such as the welfare effects of oligopolistic third-degree price discrimination (Adachi and Fabinger 2018). One may also study, for example, advertising pass-through (Draganska and Vitorino 2017).363636The firm’s demand can be modeled as , where is firm ’s investment in advertising. Free-riding, because of the spillover effect, may be more or less serious, depending on the conduct index and other related indices. Furthermore, it would be of interest to develop flexible, but analytically solvable examples along the lines of Fabinger and Weyl (2018).

Appendix A Appendix

A.1 Proofs and discussions for Section 2

A.1.1 Proof of Proposition 1

Using Equation (1) to substitute for , we first obtain a useful expression for the markup: . Now consider an infinitesimal change in the unit tax that induces a change in the equilibrium price and a change in the equilibrium quantity. These are related by . The corresponding change in social welfare per firm is , and the change in tax revenue per firm is . Combining these relationships gives the result

Next, consider an infinitesimal change in the ad valorem tax that induces a change in the equilibrium price and a change in the equilibrium quantity, related by . The change in social welfare per firm is again . The change in tax revenue per firm can be written as . Combining these relationships leads to the result

A.1.2 Intuition behind Proposition 1

The intuition behind Proposition 1 for the case of unit taxation can explained as follows. The argument for ad valorem taxation is analogous. First, the firm’s per-output profit margin is decomposed into two parts: (1) tax payment, and (2) surplus from imperfect competition, . Under imperfect competition, the effects of an increase in unit tax, , on the social welfare can be written as , which implies that the firm’s per-output profit margin serves as a measure for welfare change.373737The welfare change is further decomposed into: where can be further simplified (see below). On the other hand, the effects of an increase in unit tax, , on the tax revenue are:

where term (1) expresses (direct) gain, multiplied by the output , and term (2) shows (indirect) gain, due to the associated price increase, multiplied by , whereas term (3) is the part that exhibits (indirect) loss from the output reduction for both unit tax revenue and ad valorem tax revenue. Now recall that and . Thus, and , which implies that

Now, in the per-price term, the denominator and the numerator in are expressed as follows:

A.1.3 Proof of Proposition 2

The impact of a change in the tax on consumer surplus (per firm) is . The impact on producer surplus is

Substituting for from Equation (1) as gives

The reciprocal of the incidence ratio is

For infinitesimal changes in ad valorem taxes, we proceed analogously. The change in consumer surplus is For the change in producer surplus we have

Manipulating the last four terms on the right-hand side in the same way as before leads to

The reciprocal of the incidence ratio then becomes

A.1.4 Intuition behind Proposition 2

The intuitive reasoning behind Proposition 2 can be provided as follows. First, the effects of an increase in unit tax, , on the producer surplus can be decomposed into the following five parts:

where term (1) shows the (direct) loss from an increase in unit tax: the tax increase multiplied by the output , and term (2) is another (indirect) loss from a reduction in production, multiplied by the ad valor em tax adjusted unit price , whereas term (3) corresponds to the (direct) gain from the associated price increase, mitigated by , due to the ad valorem tax, multiplied by the output , and finally terms (4) and (5) are (indirect) gains from cost savings by the output reduction, , and from unit tax saving by the output reduction, , respectively. Note here that the equation above is rewritten as

Now, in symmetric equilibrium, the marginal cost, , is equal to the marginal benefit, , which implies

Under perfect competition, part (2) is equal to the sum of parts (4) and (5), and thus only parts (1) and (3) survive. However, under imperfect competition, the marginal cost is less than , thus part (2) is greater than the sum of parts (4) and (5). The third term in the equation above now expresses the difference between part (2) and the sum of parts (4) and (5). Now, recall that and . Thus,

On the other hand, . Thus, while it is always the case that , it is possible that .383838One can also define by and in association with a small change in and , respectively. Hereafter, we focus on and as measures of welfare burden in society, and and as measures of loss in consumer welfare. We provide general formulas for social incidence in the context of multi-dimensional pass-through after Section 4.

A.1.5 Proof of Proposition 3

Let us consider a simultaneous infinitesimal change and in the taxes and that leaves the equilibrium price (and quantity) unchanged, which requires the effective marginal cost in Equation (1) to remain the same. This implies the comparative statics relationship

Note that here we do not need to take derivatives of even though it depends on , simply because by assumption the quantity is unchanged. The total induced change in price, which generally would be expressed as , must equal zero in this case, implying the result

A.1.6 Intuition behind Proposition 3

To understand this proposition (3) intuitively, note that to keep prices and quantities constant, and must satisfy:

Thus, the relative that must be offset by a reduction equal to : , which, together with , leads to . Now, recall the Lerner rule:

which implies that , as Proposition 3 claims. Now, implies that

A.1.7 Intuition behind Proposition 4

To gain a perspective in Proposition 4, recall from Proposition 1 that

Now, Proposition 4 states that it is also understood as

Of course, it is true that is expressed by the empirical measures such as . For example, in the case of the assumption of Cournot competition, researchers often may observe the number of firms and conclude that the value of conduct index is . However, even in the case of homogeneous products, the “true” conduct may be higher than due to such reasons as collusion.393939See Miller and Weinberg (2017) for an empirical study of the possibility of oligopolistic collusion in a different manner from directly estimating the conduct parameter. Proposition 4 above circumvents this difficulty in estimating and .404040Similarly, the incidence of a unit tax is expressed as and analogously for the case of an ad valorem tax. Conversely, one would be able to estimate using the proposition above once , , and are estimated.

A.1.8 Proof of Proposition 5

Here we provide a proof of Proposition 5, as well as related intuitive arguments. Consider the comparative statics with respect to a small change in the per-unit tax . Following Weyl and Fabinger (2013, p. 538), we define : this is the negative of marginal consumer surplus. Then, the Learner condition becomes:

where is consumer surplus for the infra-marginal consumers. Importantly, measures how much consumer surplus rises for a small increase in output, and it is largest under monopoly. Now consider a small change in unit tax expressed by . Then, in equilibrium,

Thus, using the equation is rewritten as

Now, consider term (1). Note first so that because by definition . Here, for a small increase ,

so that . By definition, . Thus, . Now note that . Thus,

Next, consider term (2). A change in the marginal cost, , is expressed in terms of by . To see this, note first that )). Then, in this expression can be eliminated rewriting , which leads to . Then, in terms of the per-unit revenue burden, , that is, . Finally, using the expressions for and ,

A.1.9 Relationship to Weyl and Fabinger (2013)

It can be verified that our formula for above is a generalization of Weyl and Fabinger’s (2013, p. 548) Equation (2):

where , ( is defined in the proof of Proposition 5 just above), and and here are our and , respectively. First, the denominator in our formula is rewritten as:

because

Next, since , it is verified that , implying that

where is replaced by because and thus . Then, it is readily verified that

In summary, Weyl and Fabinger’s (2013, p. 548) original Equation (2) is generalized to

with non-zero initial ad valorem tax, which is equivalent to our formula for :

A.1.10 Comparison of perfect and oligopolistic competition

One can further interpret the formula for in comparison to the case of perfect competition (with zero initial taxes), when the unit tax pass-through rate is given by (see Weyl and Fabinger 2013, p. 534): . An analogous argument can be made for as well.

First, through the term in the denominator of in Proposition 5, as competitiveness becomes fiercer (i.e., a lower ) the pass-through rate lowers, that is, the pass-through becomes smaller as the degree of competition becomes closer to perfect competition. This is interpreted as the negative effect of competitiveness on the pass-through rate, via the first-order characteristics of demand and supply, captured by and , respectively.414141Here, with fixed , the denominator becomes smaller, and thus, the pass-through rate becomes larger as the demand becomes inelastic (i.e., becomes larger, although cannot be too large; recall the restriction, ) or the supply becomes inelastic (i.e., becomes larger).

However, through the other term , competitiveness raises the pass-through rate . To see this, suppose that is close to a constant. Then, , which implies that a larger is associated with a higher value of the pass-through rate. With an abuse of notation, this situation is interpreted as the case when is small: the effect of imperfect competition on the output reduction is small, implying less distortion, an important feature if the degree of competition is close to perfect competition.

The argument so far is clearer if , as often assumed, is a constant. Then, the second term is now so that

Thus, if the marginal cost is constant (), becomes larger as the degree of competition becomes closer to perfect competition. Here, with fixed , the pass-through rate is also larger as becomes smaller. Recall that measures how quick the marginal surplus lowers as a response to a decrease in output . Thus, a lower is associated with less distortion. Overall, Weyl and Fabinger’s (2013, p. 548) Equation (2) and our formula for show how it is influenced by the industry’s competitiveness which is captured by the conduct index.

A.1.11 Application to exchange rate changes

Let us also point out that the exchange rate pass-through can be included naturally in our framework of Section 2.424242See, e.g., Feenstra (1989); Feenstra, Gagnon, and Knetter (1996); Yang (1997); Campa and Goldberg (2005); Hellerstein (2008); Gopinath, Itskhoki, and Rigobon (2010); Goldberg and Hellerstein (2013); Auer and Schoenle (2016); and Chen and Juvenal (2016) for empirical studies of exchange rate pass-through. Suppose that domestic firms in a country of interest use some imported inputs for production. For concreteness, let us specify the profit function of firm as , where the constant coefficient measures the importance imported inputs and is the exchange rate. Notice that the firm’s profit is rewritten as . Since the first factor on the right-hand side is constant, the firm will behave as if its profit function was simply , with and . By utilizing the explicit expressions for the derivatives and , one can analyze the effect of a change in the exchange rate on social welfare. Note that this is simply interpreted as the cost pass-through as well (see the references in Footnote 42 for empirical studies). Alternatively, one may use the results of Section 6 to study the consequences of exchange rate movements.

A.1.12 Oligopoly with multi-product firms

Here, we argue that the results obtained in Sections 2 and 3 can be extended to the case of multi-product firms just by a reinterpretation of the same formulas (without modifying them).434343Lapan and Hennessy (2011) study unit and ad valorem taxes in multi-product Cournot oligopoly. Alexandrov and Bedre-Defolie (2017) also study cost pass-through of multi-product firms in relation to the Le Chatelier–Samuelson principle. Assume there are product categories, and the demand for firm ’s -th product is given by , where for each .444444See, e.g., Armstrong and Vickers (2018) and Nocke and Schutz (2018) for recent studies of multi-product oligopoly. The firms are symmetric, and for each firm, the product it produces are also symmetric. The firm’s profit per product is

We work with an equilibrium in which any firm sets a uniform price for all of its products: , and consequently sells an amount of each of them: .454545For brevity, we do not explicitly discuss the standard conditions for the existence and uniqueness of non-cooperative Nash equilibria of the different underlying oligopoly games. In this case, the profit per product equals which is formally the same as for single-product firms. For this reason, we can identify the prices and quantities of Section 2 with the prices and quantities introduced here in this paragraph. The discussion in Section 2 was general and applies to this case of symmetric oligopoly with multi-product firms as well. We can use the same definitions for the variables of interest, including the industry demand elasticity and the conduct index .