Estimating VaR in credit risk: Aggregate vs single loss distribution

Abstract

Using Monte Carlo simulation to calculate the Value at Risk (VaR) as a possible risk measure requires adequate techniques. One of these techniques is the application of a compound distribution for the aggregates in a portfolio. In this paper, we consider the aggregated loss of Gamma distributed severities and estimate the VaR by introducing a new approach to calculate the quantile function of the Gamma distribution at high confidence levels. We then compare the VaR obtained from the aggregation process with the VaR obtained from a single loss distribution where the severities are drawn first from an exponential and then from a truncated exponential distribution. We observe that the truncated exponential distribution as a model for the severities yields results closer to those obtained from the aggregation process. The deviations depend strongly on the number of obligors in the portfolio, but also on the amount of gross loss which truncates the exponential distribution.

1 Introduction

One main challenge of credit risk management is to estimate the loss distribution for credit portfolios. The loss distribution depends on the distribution of defaults within the portfolio and on the losses associated with each default. Given a loss distribution, the Value at Risk (VaR) is a widely used measure to calculate the risk of loss. There are various methods to estimate the loss distribution and to compute the VaR. Monte Carlo simulation is one of these methods [BOW10]. The estimation of VaR demands adequate quantification techniques especially if the portfolio is rather large. One of these techniques is the application of a compound distribution for the aggregates in a portfolio [LM03].

Consider a portfolio of obligors with similar exposure. One possible way to model the entire loss of the portfolio is to calculate

| (1) |

where is a random variable obtained from a Bernoulli distribution which models the default of the -th obligor, and is a random variable from an arbitrary distribution, so-called severity distribution, modeling the amount of loss of the -th obligor. In case of a large portfolio applying Monte Carlo to simulate the loss of each obligor can greatly increase the calculation effort. This motivates the use of another approach to model the total loss of a given portfolio, namely to consider all obligors under certain conditions as a single obligor (aggregation process). The total loss is then given by

| (2) |

where is a discrete random variable representing the loss frequency and are independent and identically distributed random variables representing the loss severity. The distribution of the sum in equation (2) is called a compound distribution. A compound distribution is a mix of two distributions. From the first one, called frequency distribution, one obtains an integer , and then generates random variables using the second distribution, called severity distribution. In this paper, we compare the two approaches for the calculation of the total loss. To this end, we estimate the quantiles of the single and aggregate loss and study the deviations between them.

The paper is structured as follows. In section 2, we consider the aggregate loss distribution with a Poisson distribution as a frequency distribution and a Gamma distribution as a severity distribution. Since there is no closed form for the compound distribution in equation (2), we introduce an approximation for the VaR of the aggregate loss. To this end, we introduce a new approach to calculate the quantile function of the Gamma distribution at high confidence levels. In section 3, we consider the single loss distribution. In section 3.1, we apply an exponential distribution as a severity distribution and a Bernoulli distribution as a default distribution to calculate the VaR of the single loss distribution and compare the results with those obtained from the aggregation process. In section 3.2, we apply a truncated exponential distribution as the severity distribution and compare the results with those obtained in the previous sections. We conclude our findings in section 4.

2 Aggregate Loss Distribution

In the following, we discuss the distribution of the aggregate loss (2) for Gamma distributed severities. Analytically, the compound distribution can be calculated using the method of convolutions [DP85]. In case of Gamma distributed severities, the aggregate loss is thus given by the -fold convolution of Gamma distributions, which is a Gamma distribution itself [JRY08]. Having calculated the compound distribution, one obtains the VaR at a confidence level , the -quantile, as its inverse function

| (3) |

However, there is no closed form for the inverse function of the Gamma distribution. In section 2.1, we thus discuss a closed-form approximation for the VaR at high confidence levels proposed in [BK05] and use it to estimate the quantile of the aggregate loss (2). To this end, we introduce an approximation of the Gamma quantile function in section 2.2.

2.1 Closed-Form Approximation for VaR

Consider independent and identically distributed severities from a heavy-tailed distribution and a frequency distribution which can be a Poisson, a binomial or a negative binomial distribution. Then, the -quantile of the aggregate loss satisfies the approximation

| (4) |

where is the mean of the frequency distribution. This approximation has been proposed by [BK05] in the context of the Loss Distribution Approach (LDA) to modeling operational risk.

In our setting, is the Gamma distribution and the frequency distribution is a Poisson distribution. We evaluate the -quantile of the aggregate loss in equation (2) at the new confidence level

| (5) |

We note that is the confidence level of in Solvency II and in Basel III over a capital horizon of one year. Take into account that the closer to 1 the more precise is the approximation as discussed in [BK05]. Thus, we can approximate the VaR for the aggregate loss as

| (6) |

where and are the shape and rate parameter of the Gamma distributed severities.

2.2 Gamma Quantile Approximation

To calculate the VaR of the aggregate loss explicitly, we need the quantile function of the Gamma distribution. There is, however, no closed form for the quantile function of the Gamma distribution; as a result, approximate representations are usually used. These approximations generally fall into one of four categories, series expansions, functional approximations, numerical algorithms or closed form expressions written in terms of a quantile function of another distribution, see e.g. references [SS08, KB12, MS12].

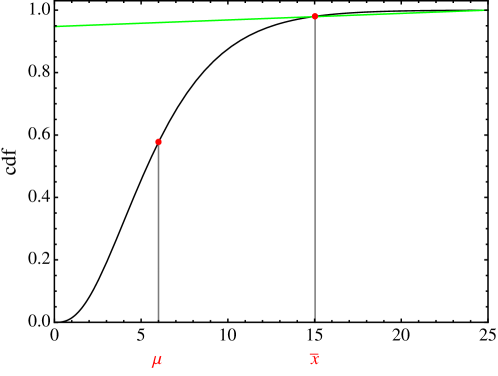

Here, we introduce an approach to estimate the quantile function of the Gamma distribution at high confidence levels. To this end, we consider the tail of the Gamma distribution. In the tail of the distribution the CDF shows nearly linear behavior, see figure 1.

Thus, we can estimate the CDF of the Gamma distribution in the tail by a linear equation

| (7) |

is the slope of the linear equation. It can be calculated as the derivative of the CDF which should be evaluated at

| (8) |

where denotes the mean of the Gamma distribution, see figure 1, and is a shift which we will calculate later on. To find the y-intercept , we use the fact that the slope of the line should be constant, i.e., we obtain the same slope for the extension of the line to the y-axis. As

| (9) |

we obtain

| (10) |

To calculate the quantile function , we insert equations (8) and (10) into equation (7) and invert. This leads to

| (11) |

where

| (12) |

Note that represents the Gamma function and is the incomplete Gamma function defined as

| (13) |

The factor is a correction factor which depends only on and . For a fixed and , it has to be chosen so that the quantile function (11) reaches a maximum value. We studied the factor numerically in the range and and found that it can be described by the following expression

| (14) |

where and are polynomial functions of . For further details see appendix A. In the following, we compare the estimated result with the theoretical Gamma quantile . Table 1 shows the relative error

| (15) |

for different , and a fixed . We observe that the deviations are smaller than , which illustrates the goodness of the approximation.

| relative error in | relative error in | ||||

| 0.95 | 1 | -0.01 | 0.99 | 1 | -0.02 |

| 5 | -0.02 | 5 | -0.08 | ||

| 10 | -0.00 | 10 | -0.00 | ||

| 50 | -0.00 | 50 | -0.00 | ||

| 100 | -0.00 | 100 | -0.01 | ||

| 500 | -0.06 | 500 | -0.17 | ||

| 1000 | -0.08 | 1000 | -0.24 | ||

| relative error in | relative error in | ||||

| 0.995 | 1 | -0.01 | 0.999 | 1 | -0.10 |

| 5 | -0.05 | 5 | -0.88 | ||

| 10 | -0.00 | 10 | -0.34 | ||

| 50 | -0.02 | 50 | -0.08 | ||

| 100 | -0.00 | 100 | -0.15 | ||

| 500 | -0.18 | 500 | -0.53 | ||

| 1000 | -0.28 | 1000 | -0.63 |

3 Single Loss Distribution

In the following, we discuss the distribution of the single loss (1) for different severity distributions. We derive the compound distribution using the method of convolutions and calculate the -quantile at high confidence levels. In section 3.1, we consider exponential severities and compare the quantile at confidence level with the results obtained using the aggregation process. In section 3.2, we take severities from a truncated exponential distribution and compare the results with those obtained in the previous sections.

3.1 Exponential Severities

Consider a portfolio of obligors. We are interested in the distribution of the total loss

| (16) |

with severities drawn from an exponential distribution with the PDF

| (17) |

where is the parameter of the distribution and is the Heaviside step function with . Note that the default of each obligor is modeled by a Bernoulli distribution, which takes the value of 1 if a default occurs and 0 if it does not. Here, we consider the default of all obligors, i.e., we assume . So, we rewrite equation (16) as

| (18) |

Thus, to calculate the distribution of the total loss we have to consider the convolution of exponential distributions. For the sake of simplicity, we assume that all generating PDFs have the same parameter given by

| (19) |

We obtain the -fold convolution of exponential distributions via a Laplace transformation, which leads to the so-called Erlang distribution

| (20) |

The corresponding CDF is given by

| (21) |

We note the resemblance with the CDF of the Gamma distribution

| (22) |

where we identify with and with . This allows us to apply the previous result (11) to calculate the quantile function of at high confidence levels

| (23) |

We now compare the quantile of the single loss distribution at confidence level with the quantile of the aggregate loss

| (24) |

We recall the relation and set . Note that the parameters , and have to be chosen in a way that the mean of the Erlang and the Gamma distributions are equal, i.e. . In the following, we study the difference between the quantiles and

| (25) |

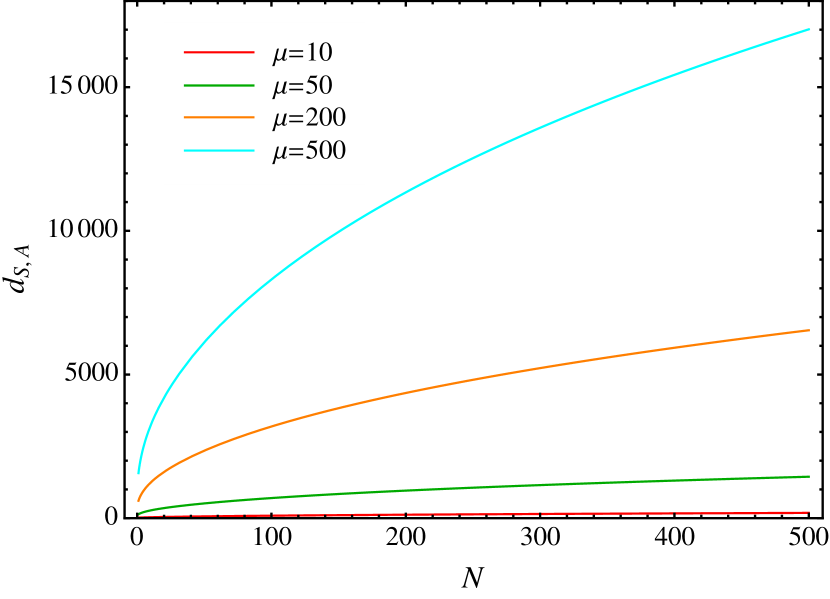

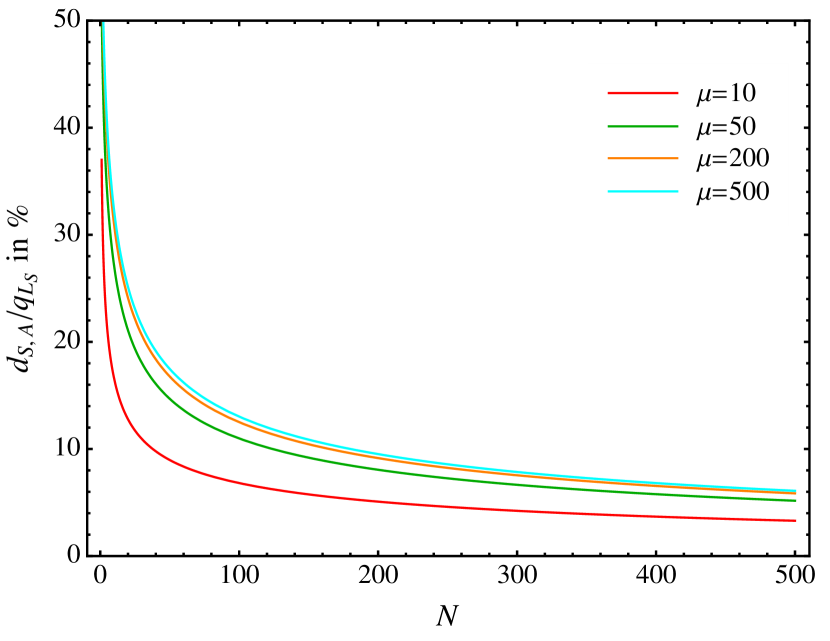

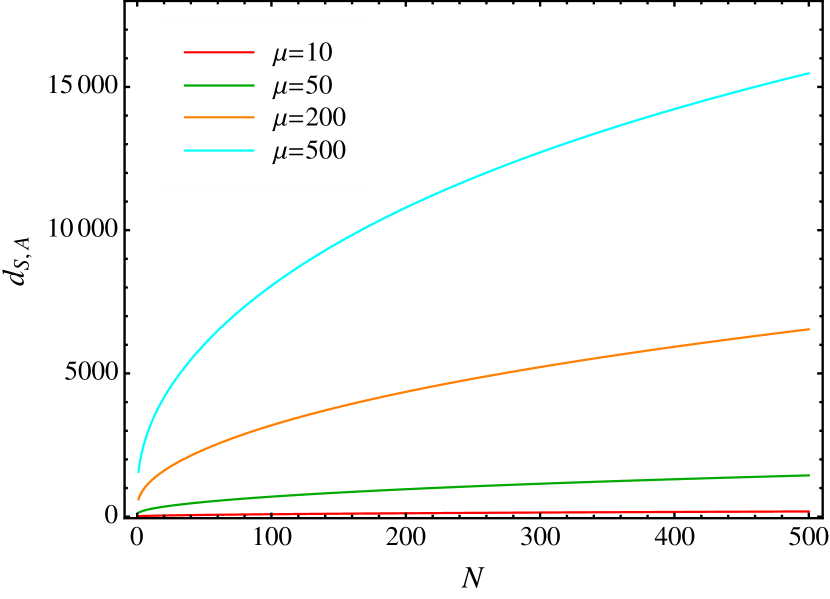

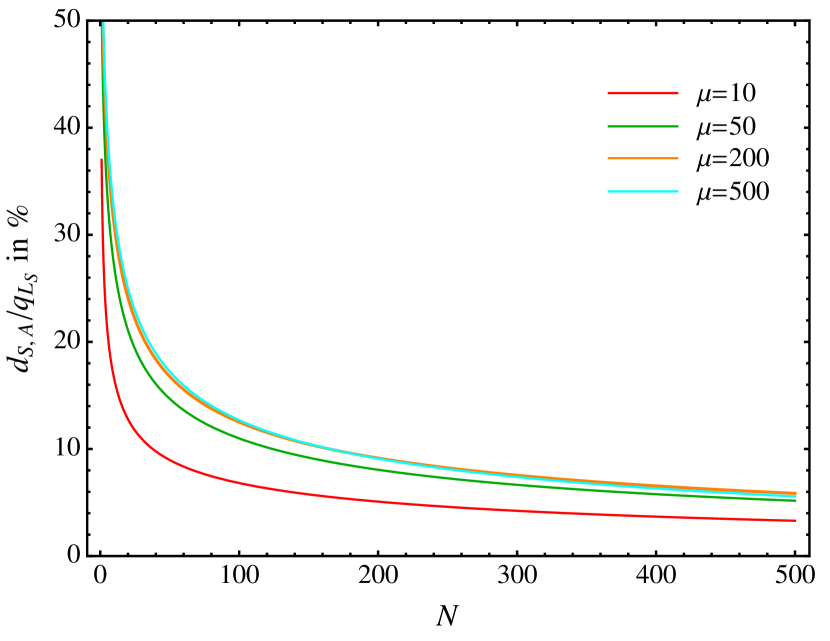

Figure 2 shows the absolute and the relative difference between the quantiles. Although the absolute difference is increasing as the mean and the number of obligors grow, the relative difference decreases.

This is due to the fact that the absolute value of the quantile is growing faster than the absolute difference. Furthermore, we observe that the relative difference shows a convergent behavior for high values which is independent of the value of the mean .

3.2 Truncated Exponential Severities

In practice, the total loss cannot be greater than the gross exposure , i.e., the maximum possible loss. Therefore, a truncated distribution is often used to cut the loss distribution at the gross exposure. A truncated distribution is a conditional distribution obtained by restricting the domain of some other probability distribution [HPR15]. Here, we apply a truncated exponential distribution to model the severities of the total loss (16). The corresponding PDF reads

| (26) |

where denotes the gross exposure. As in the previous section we assume . Thus, to calculate the loss distribution we need the convolution of truncated exponential distributions with . Again, applying a Laplace transformation, we obtain

| (27) |

Then, the corresponding CDF reads

| (28) |

where in the last step we used the relation between the incomplete and the upper Gamma function . Again, we recognize the resemblance with the CDF of the Gamma distribution up to the factor . Applying our result (11), we obtain the quantile function

| (29) |

where

| (30) |

As in the previous section, we are interested in the difference between the quantiles and

| (31) |

It is important that we have to choose the parameters , , and in a way that the mean of truncated exponential distribution is equal to the mean of the Gamma distribution, i.e.,

| (32) |

Usually, the gross loss is fixed, i.e., we have to set and . We assume that

| (33) |

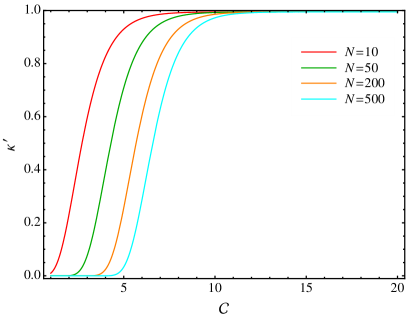

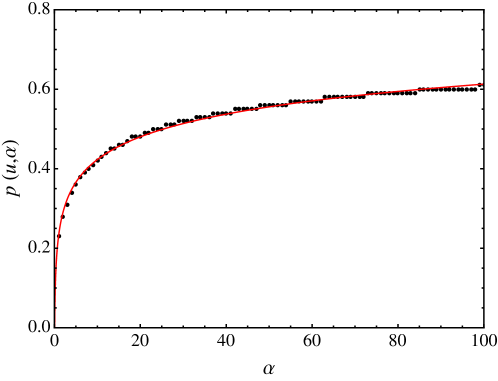

The gross loss can be viewed as a multiple of the mean of the underlying exponential distribution. Then, the constant results from the chosen model. Note that occurs in the power of the exponential function in equation (30) and plays an important role for the determination of the quantile function. We can see in figure 3 that depends mainly on but also on . Since we determined equation (11) for the range we have to take into account that should be greater than 9 in our consideration.

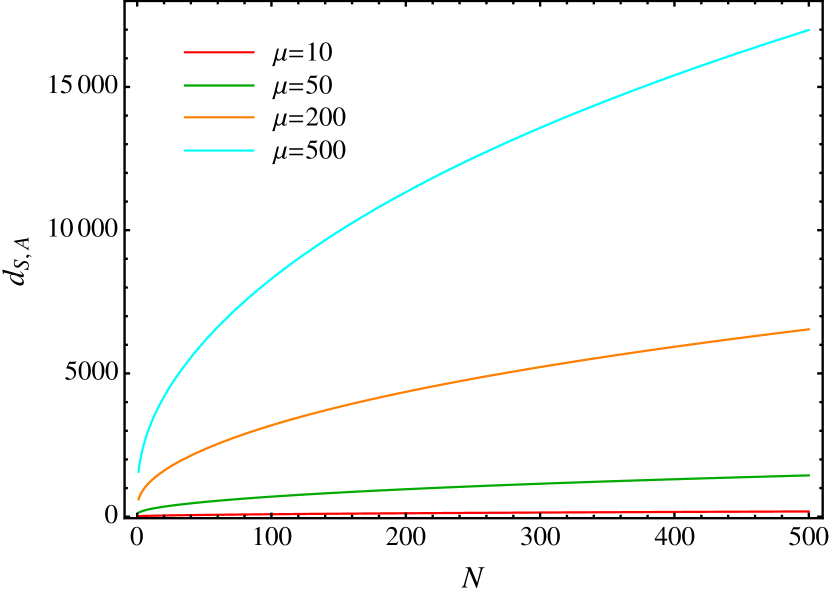

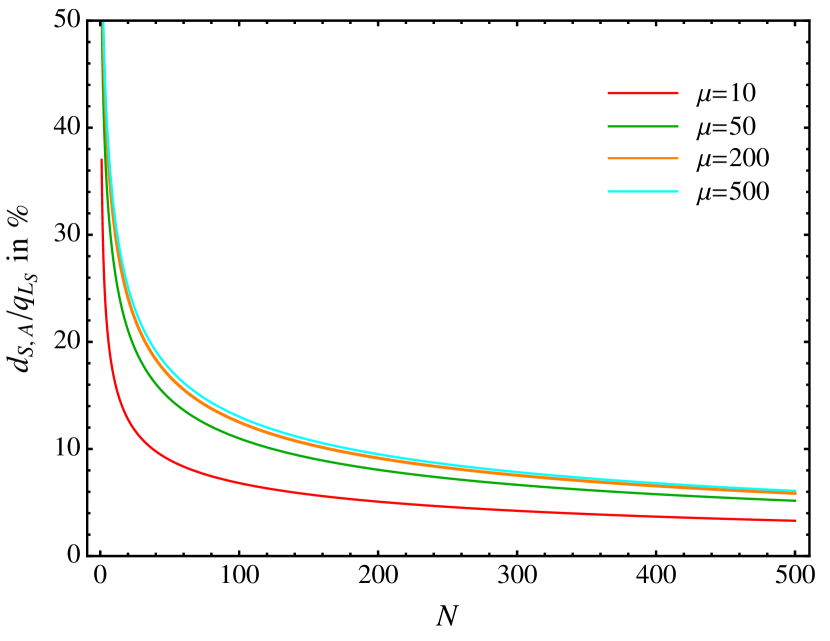

In the following, we study the absolute as well as the relative difference between and (24) for two different values of the gross exposure and , see figures 4 and 5, respectively. To this end, we set and in equation (24) and determine from equation (32) for a fixed .

We observe that both the absolute and the relative difference decrease the lower the gross loss becomes. An interesting observation in figure 4(b) is that the relative difference for falls quicker than the one for . The reason is that for approaches the limit quicker and decreases quicker. To illustrate this the values of and are shown in table 2 for both and with and . According to equation (30) the confidence level is shifted from to . In addition, table 2 shows a comparison with the case of the exponential severities discussed in section 3.1. As grows the truncated exponential model approaches the results obtained in the simple exponential model. However, the truncated exponential distribution as a model for the severities yields results closer to those obtained from the aggregation process.

| Exponential severities |

|

||||

|---|---|---|---|---|---|

| 17013.22 | 15475.54 | 16985.01 | |||

| 6.09 | 5.57 | 6.08 | |||

4 Conclusion

We considered an aggregation process, where obligors in a huge portfolio are put together under certain conditions and considered as a single obligor, and estimated the VaR for Gamma distributed severities at high confidence levels. To this end, we introduced an approach for the semi-analytical calculation of the quantile function of the Gamma distribution and derived an expression which showed a good approximation to the theoretical Gamma quantile function at high confidence levels.

In addition, we calculated the VaR for a single loss distribution where the severities are drawn first from an exponential and then from a truncated exponential distribution. To this end, we used the method of convolutions and derived an expression for the VaR in both cases. We compared the VaR for the single loss distribution with the VaR for the aggregation process and studied the difference between both quantiles. The relative difference depends on the number of obligors in the portfolio, but also on the amount of gross loss in case of truncated exponential severities. We observe that the truncated exponential distribution as a model for the severities yields results closer to those obtained from the aggregation process.

Appendix A Determination of the correction factor

Here, we present some details of the determination of the correction factor in equation (12).

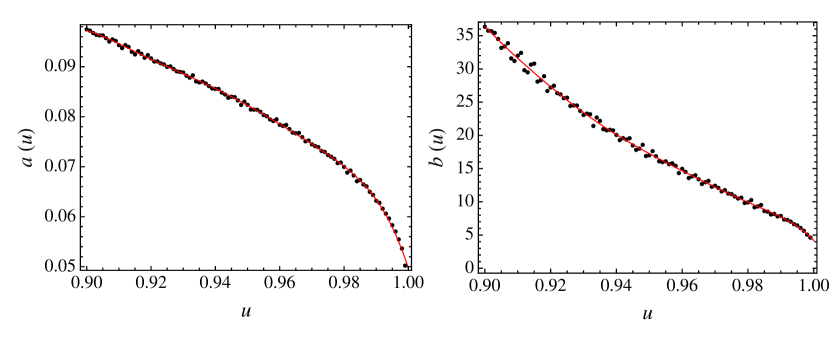

We study the quantile function (11) numerically in the range and by varying the correction factor between and and determine the correction factor which maximizes the quantile function. For a fixed , we observe that the correction factor grows as a function of , see figure 6. The dependence can be described by a log-function of the form

| (34) |

with constants and .

Note that the value of the constants depends on the chosen . In the range , we observe a decreasing trend for both constants, see figure 7. This behavior can be approximated by polynomial expressions of the form

| (35) | ||||

| (36) |

Thus, we finally obtain

| (37) |

Note that the precision of the quantile function (11) depends highly on the precision of the fit functions and the considered ranges of the parameters and .

References

- [BK05] Klaus Böcker and Claudia Klüppelberg. Operational VAR: a closed-form approximation. Risk, 8:90–93, 2005.

- [BOW10] Christian Bluhm, Ludger Overbeck, and Christoph Wagner. Introduction to Credit Risk Modeling. Chapman & Hall/CRC financial mathematics series. Chapman & Hall, Boca Raton, London, New York, 2010.

- [DP85] Nelson De Pril. Recursions for convolutions of arithmetic distributions. ASTIN Bulletin: The Journal of the International Actuarial Association, 15(02):135–139, 1985.

- [HPR15] Alexandre Hocquard, Nicolas Papageorgiou, and Bruno Remillard. The payoff distribution model: an application to dynamic portfolio insurance. Quantitative Finance, 15(2):299–312, 2015.

- [JRY08] Lancelot F. James, Bernard Roynette, and Marc Yor. Generalized Gamma convolutions, Dirichlet means, Thorin measures, with explicit examples. Probability Surveys, 5:346–415, 2008.

- [KB12] Andreas Kleefeld and Vytaras Brazauskas. A statistical application of the quantile mechanics approach: MTM estimators for the parameters of t and gamma distributions. European Journal of Applied Mathematics, 23:593–610, 2012.

- [LM03] Filip Lindskog and Alexander J. McNeil. Common Poisson Shock Models: Applications to Insurance and Credit Risk Modelling. ASTIN Bulletin: The Journal of the International Actuarial Association, 33(02):209–238, 2003.

- [MS12] Asad Munir and William Shaw. Quantile mechanics 3: Series representations and approximation of some quantile functions appearing in finance. 2012. arXiv:1203.5729.

- [SS08] György Steinbrecher and William T. Shaw. Quantile mechanics. European Journal of Applied Mathematics, 19:87–112, 2008.