One-Switch Discount Functions

Abstract. Bell [9] introduced the one-switch property for preferences over sequences of dated outcomes. This property concerns the effect of adding a common delay to two such sequences: it says that the preference ranking of the delayed sequences is either independent of the delay, or else there is a unique delay such that one strict ranking prevails for shorter delays and the opposite strict ranking for longer delays. For preferences that have a discounted utility (DU) representation, Bell [9] argues that the only discount functions consistent with the one-switch property are sums of exponentials. This paper proves that discount functions of the linear times exponential form also satisfy the one-switch property. We further demonstrate that preferences which have a DU representation with a linear times exponential discount function exhibit increasing impatience ([26]). We also clarify an ambiguity in the original Bell [9] definition of the one-switch property by distinguishing a weak one-switch property from the (strong) one-switch property. We show that the one-switch property and the weak one-switch property definitions are equivalent in a continuous-time version of the Anscombe and Aumann [7] setting.

Keywords: Discount function, One-switch property, Time preferences, Linear times exponential, Increasing impatience.

JEL Classification: D90.

In this paper we analyse the one-switch property for intertemporal preferences introduced by Bell [9]. The one-switch property was initially formulated for preferences over lotteries [9]. It says that the preference ranking of any two lotteries is either independent of wealth, or else there is a unique level of wealth such that one strict ranking prevails for lower wealth levels and the opposite strict ranking for higher wealth levels. For preferences with an expected utility representation, the one-switch property restricts the form of the Bernoulli utility function. As demonstrated by Bell [9], the utility functions that satisfy this property are the quadratic, the sum of exponentials, the linear plus exponential and the linear times exponential. The properties of these functions, and their possible applications, have been extensively investigated in risk theory (see, for example, [1], [2], [11] and [12]). However, it is less well known that Bell [9] also defined an analogous one-switch property for preferences over sequences of dated outcomes. In this case, the one-switch property concerns the effect of adding a common delay to two sequences of dated outcomes: it says that the preference ranking of the delayed sequences is either independent of the delay, or else there is a unique delay such that one strict ranking prevails for shorter delays and the opposite strict ranking for longer delays. Bell [9] claims that if preferences have a discounted utility representation, then the only discount functions consistent with the one-switch property are sums of exponentials.

However, in this paper we show that the one-switch property is also compatible with another form of discount function: the linear times exponential. To the best of our knowledge, this type of discount function has not been previously used in intertemporal context. As we demonstrate in the paper, linear times exponential discount functions exhibit strictly increasing impatience (II). While strictly II has not been a very frequent experimental observation [18], some recent empirical findings support this type of impatience [13, 25, 26]. We also analyse the distinction between the weak one-switch property and the (strong) one-switch property in the time preference context. This distinction is based on whether weak or strict preferences are reversed at the switch point. While this distinction is inconsequential in the risk set-up with an expected utility representation, matters are not so clear for the intertemporal context, even assuming a discounted utility representation. We show, however, that these two properties are equivalent in a set-up analogous to that of Anscombe and Aumann [7].

The paper is organized as follows. We start by giving some preliminaries in Section 1. Section 2 is devoted to revising Bell’s characterisation [9, Proposition 2] of the discount functions that exhibit the one-switch property. We first discuss an ambiguity in Bell’s [9] definition of this property, and distinguish a standard (strong) version from an alternative ‘‘weak" one-switch property. We show that the discount functions consistent with the (standard) one-switch property are those which have the sum of exponentials or the linear time exponential form. We also explore the relationship between the one-switch property restricted to preferences over single dated outcomes and the impatience properties of such preferences. In Section 3 we study the weak one-switch property. In the context of expected utility preferences over lotteries, where the one-switch property refers to the effect of wealth level on the ranking of two lotteries, the results in [9] imply that the weak one-switch property is equivalent to the standard one. In the intertemporal context, we establish that the equivalence also holds if we endow with a mixture set structure and work in an environment similar to of Anscombe and Aumann in [7]. Finally, Section 4 summarizes the results.

1 Preliminaries

Consider preferences over sequences of dated outcomes. We work in a continuous time environment throughout this paper. Points in time are elements of the set , where the present time corresponds to . The set of outcomes is initially assumed to be the interval , though we will re-define to be an arbitrary mixture set in Section 3.

Let be the set of sequences with dated outcomes. Define the set of alternatives as follows: The set consists of all sequences of finitely many dated outcomes. Elements of are called dated outcomes.

Consider a preference order on the set of alternatives .

We say that is a discounted utility (DU) representation for , if represents and there exist , such that is a utility function (continuous, strictly increasing with ), is a discount function (strictly decreasing, and ) and

for all and every . Necessary and sufficient conditions for a DU representation were provided by Harvey [19, Theorem 2.1].

We denote the set of positive integers by , and the set of non-negative integers by , so .

2 The one-switch property

2.1 One-switch discount functions

For any sequence of dated outcomes and any delay , let

denote the delayed sequence.

Definition 1 ([9]).

We say that the preferences on exhibit the one-switch property if for every pair the ranking of and is either independent of , or there exists , such that

or

It is worth mentioning that Bell’s [9] original verbal definition of the one-switch property uses the ambiguous word ‘‘preferred’’, which does not specify whether the preference order is used in a strong or weak sense. Bell’s Lemma 3 [9] implicitly suggests that weak preference is intended, but this Lemma also shows that either interpretation leads to the same restriction on expected utility preferences. Abbas and Bell [3] introduce a formal definition which is explicit about preference being strict. Therefore, we define the one-switch property using strict preference order.

The one-switch property can be stated in a weaker variant, as follows:

Definition 2 ([9]).

We say that the preferences on exhibit the weak one-switch property if for every pair the ranking of and is either independent of , or there exists , such that

or

In other words, there do not exist and with such that

or with all strict preferences reversed.

In the intertemporal context it is not known whether this alternative ‘‘weak" version is equivalent (given a DU representation) to Definition 1. This question will be investigated is Section 3, where we adapt Bell’s Lemma 3 [9] to the temporal setting. We demonstrate that the one-switch property and the weak one-switch property are equivalent in an intertemporal version of the Anscombe and Aumann (AA) [7] environment similar to that investigated in [5].

If preferences on have a DU representation , then the one-switch property means that for any the function

either has constant sign or else there is some such that if and only if and if and only if and are on the same side of . That is,

| (1) | ||||

Figure 1 provides an illustration of for preferences which exhibit the one-switch property and have a DU representation. Note that only the sign of is relevant.

Note that the assumed properties of imply for some or . We say that a discount function satisfies the extended one-switch property if the function defined by

| (2) |

satisfies (1) for any , any and any .

Lemma 3.

Proof.

“Only If”. This part is straightforward.

“If”. Suppose that there exists such that defined by (2) satisfies (1) for any , any and any . The proof is by contradiction. Assume that there is some , and some such that the function defined by

violates property (1). Then the function will also violate (1) for any . Let be such that and . This is a contradiction to the initial assumption that (2) satisfies (1) for any , any and any . ∎

In other words, Lemma 3 states that given preferences with a DU representation, the range of is irrelevant to whether or not the preferences satisfy the one-switch property. It follows that the one-switch property does not impose any additional restrictions on the shape of . In other words, given a DU representation for , the one-switch property restricts only . We therefore say that a discount function, , exhibits the one-switch property if there is some utility function, , such that the preferences with DU representation exhibit the one-switch property. Bell [9, Proposition 8] argues that sums of exponentials are the only discount functions compatible with the one-switch property. However, we will demonstrate in this section that linear times exponential discount functions also have the one-switch property.

The following proposition gives the restrictions on the parameters of linear times exponential and sum of exponential functions under which they satisfy the properties of a discount function.

Proposition 4.

-

(a)

The linear times exponential function is a discount function if and only if ; i.e., , where and .

-

(b)

The sum of exponentials function , where , is a discount function if and only if

-

•

and , or

-

•

and .

Equivalently, , where , .

-

•

Proof.

We need to find the parameters of linear times exponential functions and sums of exponentials such that the following four properties are satisfied:

-

1.

,

-

2.

for all ,

-

3.

is strictly decreasing, and

-

4.

.

(a) Linear times exponential. Assume that . Obviously, if and only if .

Next, to satisfy the first and the second conditions simultaneously, that is, to have and for all , it is necessary and sufficient that and (since for all ).

To check whether is strictly decreasing, consider its first order derivative:

Since for all , the sign of the derivative depends on the sign of the linear expression . Therefore, is strictly decreasing if and only if

This condition is equivalent to requiring that one of the following two conditions is satisfied:

-

•

and ,

-

•

and .

Since , in the first case we have . In the second case . We can summarize both cases as follows:

Therefore, the first three properties of discount functions are satisfied if and only if .

Finally, the limit of the linear times exponential function is

If this limit is 1. This case is ruled out since from the previous step . Then, by L’Hopital’s rule we have

Therefore, satisfies all four properties of discount functions if and only if . Denote and . Then we have , where and .

(b) Sums of exponentials. The proof is analogous to [9, Proposition 8] and is given here for completeness. Assume that with .

The condition is satisfied if and only if .

We must also have for all . Note that

if and only if for all (since for all ). From the first condition we know that . Substituting this expression to the inequality we must have for all . Therefore, the first two properties of discount functions are satisfied if and only if and one of the following two conditions holds:

-

(i)

and ; or

-

(ii)

and .

Next, it is necessary to have strictly decreasing. Consider its first order derivative

Since for all , the function is strictly decreasing if and only if

Recall that from the first two conditions we have and [(i) or (ii)] holds. Therefore, for all and is strictly decreasing if and only if all of the following conditions hold:

Note that

Therefore, we must have

| (3) | ||||

| (4) | ||||

| (5) |

Consider case (i) of (5). Then condition (3) holds if and only if . Given (3), condition (4) holds if and only if , which is equivalent – in case (i) – to and . Thus, in case (i), the first three properties of a discount function are satisfied if and only if and . Since , the fourth property is also satisfied.

Next, consider case (ii) of (5). The argument is similar to case (i). The condition (3) holds if and only if . Given (3), condition (4) holds if and only if , which is equivalent – in case (ii) – to and . Therefore, in case (ii), the first three properties of a discount function are satisfied if and only if and . Since , the fourth property is also satisfied.

In case (i) of (5) let and . It follows that . Since it requires that . We then have , where , .

Analogously, in case (ii) of (5) let and . We then obtain the same functional from and parameter restrictions as in case (i), that is, , where , . ∎

The following proposition demonstrates that these two types of discount function are compatible with the one-switch property.

Proposition 5.

Suppose that the preference order on has a DU representation , where

-

•

, where and , or

-

•

, where , and .

Then exhibits the one-switch property.

Proof.

The proof adapts Bell’s argument [9, Proposition 2] to the time preference framework. We need to prove that for any , the following function changes sign at most once:

(a) Linear times exponential. Consider the discount function , where and . Then

Rearranging,

Let

and

Then

This expression can be rewritten as follows

Since , the sign of equals the sign of . Since the latter is linear its sign is constant or else changes once at a unique value.

(b) Sums of exponentials. Consider the function , where , and . Then

It can be rearranged so that

Denote

and

Then

This expression can be factorized as follows

Since , the sign of equals the sign of . Therefore, is either constant or else changes once at unique value. ∎

Since Proposition 5 establishes that linear times exponential discount functions and sum of exponentials discount functions satisfy the one-switch property, they must also satisfy the weak one-switch property.

2.2 The one-switch property for dated outcomes and monotonic impatience

In this section we consider preferences on the set of dated outcomes. When the preferences are restricted to , then a DU representation becomes for any . Necessary and sufficient conditions for this representation are given in [17]. We assume that satisfy Fishburn and Rubinstein’s axioms [17] throughout this section.

Definition 6.

We say that exhibits the one-switch property for dated outcomes if exhibits the one-switch property on .111The related concept of an ordinal one-switch utility function is introduced in [3].

Obviously, if exhibits the one-switch property on , it implies that also exhibits the one-switch property for dated outcomes.

Consider the following notions of decreasing and increasing impatience.

Definition 7 ([22]).

We say that exhibits [strictly] decreasing impatience, if for all such that and for all : if then for any we have

| (6) |

We say that exhibits

When preferences have a DU representation, these properties only restrict the discount function. The next proposition follows directly from the definition.

Proposition 8.

The following proposition provides a complete characterisation.

Proposition 9 ([22], [6]).

Suppose that restricted to has a DU representation.Then exhibits

-

•

[strictly] DI if and only if is [strictly] log-convex,222A function is called log-convex if for all and is convex; and strictly log-convex if for all and is strictly convex. We say that a function is [strictly] log-concave, if is [strictly] log-convex.

-

•

[strictly] II if and only if is [strictly] log-concave,

-

•

constant impatience if and only if with .

Proposition 9 extends [22, Corollary 1] to increasing impatience and strictly decreasing (and strictly increasing) impatience. The proof is omitted here, since it only requires a minor adjustment of Prelec’s original proof.333The proof of the proposition can also be found in the working paper [6].

The following lemma re-expresses the definition of the one-switch property for dated outcomes in terms of a common advancement () and a common delay () applied to a pair of dated outcomes between which the decision-maker is indifferent.

Lemma 10.

Let such that , and . Then exhibits the one-switch property for dated outcomes only if either

-

(i)

for all , or

-

(ii)

for , and for , or

-

(iii)

for , and for .

Proof.

Let such that , and . Assume also that exhibits the one-switch property for dated outcomes. Therefore, by definition of the one-switch property we have

-

(i∗)

for all , or

-

(ii∗)

for all , or

-

(iii∗)

for all .

We need to analyse the situation when . The proof is by contradiction.

In case (i∗), assume that there exists such that and . Let and . Using this notation, we obtain

This contradicts the one-switch property for dated outcomes, so (i) follows. If the proof is analogous.

In case (ii∗), assume that there exists such that and . With the same notation as in the previous case and gives us

which is a contradiction.

In case (iii∗) the proof is symmetric to case (ii∗). ∎

The relation between impatience properties and the one-switch property for dated outcomes is established in the following lemma.

Lemma 11.

Suppose that has a DU representation . Then exhibits the one-switch property for dated outcomes if and only if also exhibits either stationarity or strictly DI or strictly II.

Proof.

“Only If”. Assume that exhibits the one-switch property for dated outcomes.

Consider some such that , and . To see that we can always find such a pair, suppose that , and . Then it follows by the continuity of and the fact that is strictly decreasing that there exists such that . Alternatively, suppose that , and . Then it follows by the continuity of and the fact that is strictly decreasing that there exists such that .

It follows by the one-switch property for dated outcomes and Lemma 10 that either

-

Case 1.

for all , or

-

Case 2.

for , and for , or

-

Case 3.

for , and for .

We will analyse each case separately.

Case 1. Note that letting and we have

Using the DU representation it follows that

| (8) |

Consider some . Then (8) implies

Rearranging,

| (9) |

By continuity we can choose such that

| (10) |

Hence, it follows from (9), (10) that

Then the one-switch property implies that

Since were arbitrary, it follows by Proposition 8 that exhibits constant impatience.

Case 2. Defining as for Case 1, we have

Therefore, using the DU representation

Hence,

Rearranging

| (11) |

By continuity we can choose such that

| (12) |

It follows from (11), (12) and the one-switch property that

| (13) |

for any whenever .

Consider some . There are three possible sub-cases:

-

(a)

,

-

(b)

, and

-

(c)

.

We will show that, in each of these three sub-cases,

| (14) |

From Proposition 8 we may then conclude that the preferences exhibit strict DI.

In sub-case (b) choose such that . Let and . It follows from (13) that

| (15) |

for all . Let . Then we have

| (16) |

By continuity we can choose such that

| (17) |

Therefore, it follows from (16), (17) and the one-switch property that (14) holds.

In sub-case (c) choose such that . Let and . Then it follows from (13) that

| (18) |

for all . Let . Then we have

| (19) |

Choose such that

| (20) |

Therefore, (14) follows by (19), (20) and the one-switch property.

Therefore, in Case 2 exhibits strictly DI.

Finally, in Case 3 we may show that exhibits strictly II by a symmetric proof to that for Case 2.

“If”. Suppose that there are some with and some such that . It suffices to show that either

| (21) |

or

| (22) | ||||

| (23) |

If then . It follows by monotonicity that . Hence, satisfies the one-switch property for dated outcomes.

Assume that and exhibits constant impatience. It follows that for all , or for all . To show that satisfies the one-switch property for dated outcomes we need to demonstrate that for all such that , or for all such that . The proof is by contradiction. Suppose that there exists such that, say, with . By continuity and impatience there exist such that . Then, since exhibits constant impatience it follows that for all . Let . Then we obtain . Since it implies by impatience that . Hence, , a contradiction.

Suppose that and exhibits strictly DI. It follows that for all , or for all . We now need to show that for all , or for all such that . The proof is by contradiction. Suppose there exist such that and .

First consider with and . Then, since satisfy strictly DI it follows that for all . Let . Then we have , which is a contradiction. Secondly, consider with and . It follows by continuity and impatience that there exist such that . Hence, since exhibit strictly DI it implies that for all with and . Let . Then we have . Since it follows by impatience that , therefore, , a contradiction.

If we assume that exhibits strictly II, the proof is analogous. ∎

While the assumption of a DU representation is not necessary for the ‘‘If" part of the proof, it is essential for our proof of the ‘‘Only If" part. The necessity of a DU representation for the ‘‘Only If" result of Lemma 11 remains an open question.

It was demonstrated in the working paper [6], that for differentiable discount functions a strictly increasing time preference rate corresponds to strictly II, while a strictly decreasing time preference rate corresponds to strictly DI.444The time preference rate, , is defined as follows: . The proof is along the lines of [6, Lemma 11]. We use this result to prove the following proposition.

Proposition 12.

Suppose that has a DU representation .

-

•

If , where and , then exhibits strictly II when and exhibits stationarity when .

-

•

If , where , , then exhibits strictly DI when , strictly II when and stationarity when .

Proof.

(a) Linear times exponential. Assume first that . Since , the time preference rate is:

The derivative of time preference rate is , therefore, linear times exponential discount function exhibits strictly increasing impatience. Otherwise, if , then and the preferences exhibit stationarity (see, for example, [17]).

(b) Sums of exponentials. The time preference rate is

The derivative of time preference rate is

The sign of the derivative depends on the sign of the numerator of this expression:

Simplifying :

Recall that and . Therefore, if , is strictly negative if and is strictly positive if and . Hence, the time preference rate is constant if , strictly decreasingif and strictly increasing if . This in turn implies that exhibit stationarity if , strictly DI if and strictly II if . ∎

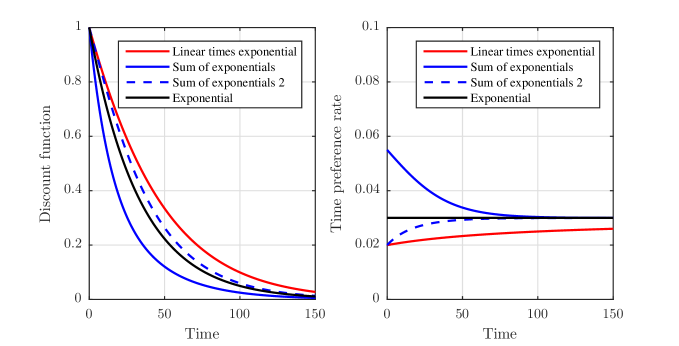

A linear times exponential discount function and two sum of exponentials discount functions, with their associated rates of time preference, are illustrated in Figure 2.

It is worth mentioning that Bell’s [9] definitions of the terms ‘‘decreasing impatience" and ‘‘increasing impatience" are different from the ones used here. Bell’s definitions are given below:

Definition 13 ([9]).

Let on have a DU representation with a discount function . Then we say that preferences exhibit DI∗ [II∗] if

Note that Bell’s [9] DI∗ (II∗) corresponds to strict log-superadditivity (log-subadditivity) of . Obviously, strict log-superadditivity (strict log-subadditivity) is a special case of strict log-convexity (strict log-concavity). Therefore, Bell’s definitions of DI∗ and II∗ are weaker properties than our strictly DI and strictly II. Bell [9, Proposition 8] specifies the parameter values for a sum of exponentials discount function such that exhibit DI∗/II∗:

Proposition 14 ([9, Proposition 8]).

Let , where and . Then it is DI∗ if and II∗ if .555Bell [9, Proposition 8] uses a strict inequality to guarantee that when . However, if when and for all , then is strictly decreasing on . Therefore, we allow , since this weak inequality is consistent with the properties of a discount function.

Comparing Proposition 14 to Proposition 11, it is easy to see that strictly II and II∗ have the same implications for the parameters for a sum of exponentials discount function (and similarly for strictly DI and DI∗). It is also straightforward to observe that the restrictions imposed by the properties of strictly II and II∗ on the parameters for a linear times exponential discount function coincide.

2.3 Representation of preferences with the one-switch

property

We first observe that constant impatience is equivalent to the zero-switch property:

Definition 15.

We say that on exhibit the zero-switch property if for every pair the ranking of and is independent of .

It follows from this definition that if on exhibit the zero-switch property, then for any , if there exists such that , then for any .

The following proposition amends [9, Proposition 8].

Proposition 16.

Let on have a DU representation .Then exhibit the one-switch property only if has one of the following forms:

-

•

, with and ,

-

•

, where and .

We adapt Bell’s [9, 10] method of proof for the risk (expected utility) context to our time preference framework. The required adaptation is non-trivial. The main reason is that probabilities sum up to one, whereas utilities of outcomes do not. In the original Bell proof [9] this property of probabilities was used to obtain a system of two equations in two variables. The conditions under which the solutions of this system exist are well-known. In the time preference setting, we use Lemma 11 to obtain two sequences of dated outcomes that are indifferent at two different points of delay. As a result of which we obtain a homogeneous second order linear difference equation. The solutions of this equation extended to continuous time give us three types of functions. We further show that only linear times exponential and sums of exponentials (with suitable parameter restrictions) satisfy the one-switch property and the properties of a discount function (using Proposition 4). It is also worth mentioning that in the risk setting Bell [9, 10] obtains a third order difference equation, rather than the second order difference equation that we obtain in the time preference framework.

Proof.

Fix some . Suppose we can find such that

| (24) |

Then, since has a DU representation, it implies that

where , and , .

We first show that for any we can always find such that (24) holds. The first equation of 24 implies , which we may substitute into the second equation as follows:

Simplifying

| (25) |

Since preferences satisfy the one-switch property they will also satisfy the one-switch property for dated outcomes, and hence it follows by Lemma 11 that exhibits strictly DI, strictly II or stationarity. Assume first that exhibits strictly DI. Then, by Proposition 8 we have

Therefore, and , and hence, by continuity it is always possible to find such that (25) holds.

Since , we have

Hence, , which implies that

If exhibits strictly II the argument is analogous with the inequalities reversed.

In the case when exhibits stationarity, we have and , therefore (25) holds for any . Hence, we can choose such that .

Therefore, we have found two sequences of dated outcomes such that

Then, since satisfies the one-switch property it must be true that

In particular, .

Since , we can write , where , .

For some and some let , . We then obtain a homogeneous second order linear difference equation

| (26) |

It is well known (see, for example, [21]) that this equation has three types of solutions, which are derived from the characteristic equation: . These three solutions are as follows:

-

Solution 1.

If , then there are two distinct real roots denoted as and . In this case the two linearly independent solutions to (26) are and , where . The general solution is , where .

-

Solution 2.

If , then the roots coincide so . In this case the two linearly independent solutions to (26) are and . The general solution is , where .

-

Solution 3.

If , the roots are complex

where , , and with (since ). Then the two linearly independent solutions to (26) are and . The general solution is

where

Note that by letting , , and , Solution 3 can be rewritten as follows:

Recall that . Therefore, Solution 3 can be excluded because it implies multiple changes of sign (it does not satisfy monotonicity).

Note that equation (26) holds for arbitrary and arbitrary , though the roots and and the constants and may depend, in a continuous fashion, on and . Bell [10, 9] argues that D must therefore satisfy the corresponding limit of one of these solutions, as .666Romanian mathematician Radó [23] proved a more general result which was recently extended to multidimensional case in [4]. Radó [23, Theorem 2] proves that the set of continuous functions , which satisfy the equation with continuous functions , where and with , coincides with the set of functions which satisfy a linear differential equation for some real coefficients . When it is well-known that the solutions to such a differential equation coincide with the limits of our three solution types. The solutions of (26) converge, respectively to

-

Solution 1.

(Sum of exponentials): , where ,

-

Solution 2.

(Linear times exponential): .

By Proposition 4 it follows that:

-

Solution 1.

, where , and ;

-

Solution 2.

, where and . Note that this solution includes the exponential discount function as a special case. That is, if , then , where .

∎

Corollary 17.

Let on have a DU representation . Then exhibits the one-switch property if and only if has one of the following forms:

-

•

, with and ,

-

•

, where and .

3 The weak one-switch property

3.1 The weak one-switch property and mixtures of sequences of dated outcomes

The one-switch property is equivalent to the weak one-switch property in the risk setting when preferences over lotteries have an expected utility representation [9]. This equivalence follows from [9, Lemma 3], where mixture linearity and other properties of expected utility are used to show that if two lotteries are indifferent at two wealth levels then they should be indifferent for any wealth level. In the intertemporal framework of this paper a direct adaptation of the proof of this equivalence is not possible, even if we assume that preferences have a DU representation, because a DU representation is, in general, not mixture linear. However, we can adapt the Anscombe and Aumann (AA) setting [7] to preferences over streams of consumption lotteries. Working in this environment it is possible to establish the equivalence of the weak one-switch property and the one-switch property for time preferences with a discounted expected utility representation. We first have to adapt the AA framework to continuous time for this purpose.

Assume that is a mixture set ([16]); that is, for every and every , there exists satisfying:

-

•

,

-

•

,

-

•

.

We assume that contains a ‘‘neutral’’ outcome, denoted by . We can think of as a set of lotteries with monetary outcomes, and corresponds to the lottery which pays with certainty.

We next introduce a mixture operation for sequences of dated outcomes, analogous to the AA mixing operation. To do so, we recall that the neutral outcome obtains at any date not specified in the sequence. First, define

| (27) |

where is defined the usual way (see [16]).

Let with and let . Define where and . An example of concatenation procedure for time vectors and is given in Figure 3.

For any and any define the mixture operation as follows:

| (28) |

where is defined so that if , then , otherwise , and is defined so that if , then , otherwise . Note that and are identical sequences of dated outcomes, and likewise and are identical sequences. Figure 4 illustrates the transformation of the sequence to the sequence and the sequence to the sequence . Note that .

It is not hard to see that is a mixture set.

The utility function is called mixture linear if for every we have .

We say that preferences in this environment have a DEU (discounted expected utility) representation if they have a DU representation in which is mixture linear on . We next show that the induced utility on sequences of dated outcomes is mixture linear on . It follows from (28) that

| (29) |

where . Since is mixture linear it follows that

Hence, is mixture linear on .

It is worth mentioning that the problem of finding axiomatic foundations for a DEU representation remains an open question. It is natural to assume that Fishburn and Rubinstein’ s axioms [17] should be satisfied for restricted to with being a mixture set.777For example, Bleichrodt et al. [14] assume the existence of DU representation for on , where is not necessarily restricted to reals. Similarly, Rohde [24] applies the DU representation to on requiring only that is a connected topological space which contains a “neutral” outcome. However, it is beyond the scope of the present paper to address this issue.

The following lemma is a part of [9, Lemma 3]. The proof is given for completeness.

Lemma 18 (cf., [9]).

Let preference on have a DU representation. If on exhibit the weak one-switch property, then for any if there exist such that and , and , then for any .

Proof.

Suppose and are such that with

We need to show that for any . The proof is by contradiction. Assume that we can have such that . Consider , where is sufficiently small so that (by continuity, such can always be found). However, and , which implies a double switch. We obtained the desired contradiction. The case is similar. Therefore, . ∎

Lemma 18 implies the following corollary:

Corollary 19.

The weak one-switch property implies that is a closed (possibly empty) interval.

In the next proposition the mixtures of sequences of dated outcomes will be used. It adapts [9, Lemma 3] to the time preference setting. Proposition 20 is proved by contradiction. We first need to find two sequences of dated outcomes such that their DEU difference changes its sign as the delay increases. Using Corollary 19 we then consider two cases depending on whether the just obtained DEU difference equals zero at a unique point or on the interval. A double switch (contradiction to the weak one-switch property) can be obtained in each case by introducing suitable mixtures of sequences of dated outcomes. The illustrations to support the proof are given in the Appendix.

Proposition 20 (cf., [9, Lemma 3]).

Let preference on have a DEU representation. If exhibits the weak one-switch property, then for any if and for some and some , then for any .

Proof.

Suppose and

By Lemma 18 it follows that

| (30) |

The weak one-switch property implies weak preference in one direction above and in the other direction below . We assume that is weakly preferred to above . The other case can be treated similarly.

Let . Therefore,

Given the DEU representation we can always find and such that

Let , where . Analogously, define . Consider the function

Then for sufficiently small we have (see Figure A.1 in the Appendix888Note that for all figures in Appendix only sign is relevant in the vertical dimension.):

Therefore, by continuity, there must exist at least one such that . By Corollary 19 there are two possible cases: either is unique, or for (see Figure A.2 in the Appendix).

Case 1. Assume first that is unique; i.e., (using the one-switch property) if and if . Consider the reflection of about the -axis; i.e., . Then if and if . Next, choose and shift the function to the left as follows

so that for the shifted function (see Figure A.3 in the Appendix):

Define the mixtures and . Analyse the function

Choosing sufficiently small we obtain (see Figure A.4 in the Appendix):

Therefore, we have arrived at a contradiction to the one-switch property.

Case 2. We next assume that there exist such that if and only if . Also, by the one-switch property, we must have if , and if . We consider the reflection of about the -axis and shift it to the left by a small amount to obtain as follows

Then (see Figure A.5 in the Appendix):

Define the mixtures and . Analyse the function

Choosing sufficiently small we obtain (see Figure A.6 in the Appendix):

Finally, mixing and we have

Recall that for all . Letting be sufficiently small we obtain a double switch (see Figure A.7 in the Appendix):

which is a contradiction. ∎

The implication of Proposition 20 is as follows:

Corollary 21.

If preferences on have a DEU representation, then the one-switch property is equivalent to the weak one-switch property.

3.2 The weak one-switch property for dated outcomes and impatience

In this section we consider preferences on and return to the initial assumption that .

Definition 22.

We say that exhibits the weak one-switch property for dated outcomes if exhibits the weak one-switch property on .

The following proposition gives a partial characterisation of the weak one-switch property for dated outcomes.

Proposition 23.

Let restricted to has a DU representation. Then preferences exhibit the weak one-switch property for dated outcomes if exhibit DI or II.

Proof.

We show that if exhibits II or DI it must also exhibit the weak one-switch property for dated outcomes. The proof is by contradiction. Suppose that for some and some such that we can have:

| (32) | ||||

| (33) | ||||

| (34) |

W.l.o.g. assume that . Then we also must have that , otherwise (33) contradicts impatience and monotonicity. By continuity we can find such that . Therefore, by II we have . By impatience, , hence, by transitivity, , which is a contradiction to (33). Therefore, we have shown that if does not satisfy the one-switch property for dated outcomes it also does not exhibit II.

The proof for DI is analogous. Indeed, consider , with , , as before. By continuity we can find such that . Since , let for some . From the equivalence it follows by DI that , or, equivalently, . Since , impatience implies that . Therefore, we must have , which brings us to a contradiction to (34). ∎

We have not been able to establish the converse to Proposition 23. The arguments used in Lemma 11 do not adapt straightforwardly to the present situation. However, Proposition 23, together with previous characterisation of the one-switch property for dated outcomes (Lemma 11), already imply that the one-switch property for dated outcomes and the weak one-switch property for dated outcomes are not equivalent for intertemporal preferences with a DU representation.

4 Discussion

This paper fills a gap in Bell’s original characterisation [9, Proposition 8] of discount functions compatible with the one-switch property for sequences of dated outcomes. We showed that functions of the linear times exponential form also have this property and that such discount functions exhibit strictly increasing impatience. Although decreasing impatience is commonly found in experiments [18], there is also much evidence for increasing impatience (see, for example, [8], [26]). To the best of our knowledge, the linear times exponential function has not been used in the literature on time preferences before. Therefore, we introduce a new type of a discount function that accommodates strictly increasing impatience and the one-switch property.

With regard to sums of exponentials, there has recently been some interest in this type of discount function. In their experiments, McClure et al. [20] used magnetic neuro-images of individuals’ brains to study intertemporal choice. They found that making a decision is a result of the interaction of two separate neural systems with different levels of impatience. To describe the involvement of these two brain areas in discounting, they suggested sum of exponential discount functions which they refer to as double exponential discounting. The recent empirical study by Cavagnaro et al. [15] demonstrates that double exponential discounting provides a better fit to actual time preferences than exponential, quasi-hyperbolic, proportional hyperbolic and generalized hyperbolic discounting.

A second contribution of this paper is to clarify the definition of the original one-switch rule introduced by Bell [9], by considering two definitions: the weak one-switch property and the (strong) one-switch property. We demonstrate that if is a mixture set and if preferences have a DEU representation, then the one-switch property is equivalent to the weak one-switch property.

Third, we prove that if preferences have a DU representation, then preferences exhibit the one-switch property for dated outcomes if and only if they exhibit either strictly increasing impatience, or strictly decreasing impatience, or constant impatience. A partial analogue is obtained for the weak one-switch property for dated outcomes. That is, the preferences exhibit the weak one-switch property for dated outcomes if they exhibit increasing impatience or decreasing impatience.

Acknowledgments

I thank my supervisor Matthew Ryan for valuable suggestions and detailed comments. I am grateful to participants of 6th Microeconomic Theory Workshop at Victoria University of Wellington for helpful comments. Financial support from the University of Auckland is gratefully acknowledged.

Appendix A Appendix

A.1 Illustrations for the proof of Proposition 20

In this appendix we provide the illustrations to accompany the proof of Proposition 20. Note that for all the figures in the appendix only the sign (but not the value) of a vertical coordinate of a point is relevant.

References

- [1] A. E. Abbas and D. E. Bell. One-switch independence for multiattribute utility functions. Operations Research, 59(3):764--771, 2011.

- [2] A. E. Abbas and D. E. Bell. Methods-one-switch conditions for multiattribute utility functions. Operations Research, 60(5):1199--1212, 2012.

- [3] A. E. Abbas and D. E. Bell. Ordinal one-switch utility functions. Operations Research, 63(6):1411--1419, 2015.

- [4] J. M. Almira. On Popoviciu-Ionescu functional equation. Annales Mathematicae Silesianae, 30(1):5--15, 2016.

- [5] N. Anchugina. A simple framework for the axiomatization of exponential and quasi-hyperbolic discounting. Theory and Decision, 2016. doi:10.1007/s11238-016-9566-8.

- [6] N. Anchugina, M. Ryan, and A. Slinko. Aggregating time preferences with decreasing impatience. arXiv preprint arXiv:1604.01819, 2016.

- [7] F. J. Anscombe and R. J. Aumann. A definition of subjective probability. Annals of Mathematical Statistics, 34(1):199--205, 1963.

- [8] A. E. Attema, H. Bleichrodt, K. I. M. Rohde, and P. P. Wakker. Time-tradeoff sequences for analyzing discounting and time inconsistency. Management Science, 56(11):2015--2030, 2010.

- [9] D. E. Bell. One-switch utility functions and a measure of risk. Management Science, 34(12):1416--1424, 1988.

- [10] D. E. Bell. Risk, return, and utility. Management Science, 41(1):23--30, 1995.

- [11] D. E. Bell and P. C. Fishburn. Utility functions for wealth. Journal of Risk and Uncertainty, 20(1):5--44, 2000.

- [12] D. E. Bell and P. C. Fishburn. Strong one-switch utility. Management Science, 47(4):601--604, 2001.

- [13] H. Bleichrodt, Y. Gao, and K. I. M. Rohde. A measurement of decreasing impatience for health and money. Journal of Risk and Uncertainty, 52(3):213--231, 2016.

- [14] H. Bleichrodt, K. I. M. Rohde, and P. P. Wakker. Non-hyperbolic time inconsistency. Games and Economic Behavior, 66(1):27--38, 2009.

- [15] D. R. Cavagnaro, G. J. Aranovich, S. M. McClure, M. A. Pitt, and J. I. Myung. On the functional form of temporal discounting: an optimized adaptive test. Journal of Risk and Uncertainty, 52(3):233--254, 2016.

- [16] P. C. Fishburn. The foundations of expected utility, volume 31. Dordrecht: Reidel Publishing Co, 1982.

- [17] P. C. Fishburn and A. Rubinstein. Time preference. International Economic Review, 23(3):677--694, 1982.

- [18] S. Frederick, G. Loewenstein, and T. O’Donoghue. Time discounting and time preference: a critical review. Journal of Economic Literature, 40(2):351--401, 2002.

- [19] C. M. Harvey. Proportional discounting of future costs and benefits. Mathematics of Operations Research, 20(2):381--399, 1995.

- [20] S. M. McClure, K. M. Ericson, D. I. Laibson, G. Loewenstein, and J. D. Cohen. Time discounting for primary rewards. The Journal of Neuroscience, 27(21):5796--5804, 2007.

- [21] R. Mickens. Difference equations. New York: Van Nostrand Reinhold, 1991.

- [22] D. Prelec. Decreasing impatience: a criterion for non-stationary time preference and hyperbolic discounting. Scandinavian Journal of Economics, 106(3):511--532, 2004.

- [23] F. Radó. Caractérisation de l’ensemble des intégrales des équations différentielles linéaires homogènes à coefficients constants d’ordre donné. Mathematica (Cluj), 4(27):131--143, 1962.

- [24] K. I. M. Rohde. The hyperbolic factor: a measure of time inconsistency. Journal of Risk and Uncertainty, 41(2):125--140, 2010.

- [25] S. Sayman and A. Öncüler. An investigation of time inconsistency. Management Science, 55(3):470--482, 2009.

- [26] K. Takeuchi. Non-parametric test of time consistency: present bias and future bias. Games and Economic Behavior, 71(2):456--478, 2011.