Making matrices better:

Geometry and topology of polar and singular value decomposition

Dennis DeTurck, Amora Elsaify, Herman Gluck, Benjamin Grossmann

Joseph Hoisington, Anusha M. Krishnan, Jianru Zhang

Abstract

Our goal here is to see the space of matrices of a given size from a geometric

and topological perspective, with emphasis on the families of various ranks

and how they fit together. We pay special attention to the nearest orthogonal

neighbor and nearest singular neighbor of a given matrix, both of which play

central roles in matrix decompositions, and then against this visual backdrop examine

the polar and singular value decompositions and some of their applications.

MSC Primary: 15-02, 15A18, 15A23, 15B10;

Secondary: 53A07, 55-02, 57-02, 57N12, 91B24, 91G30, 92C55.

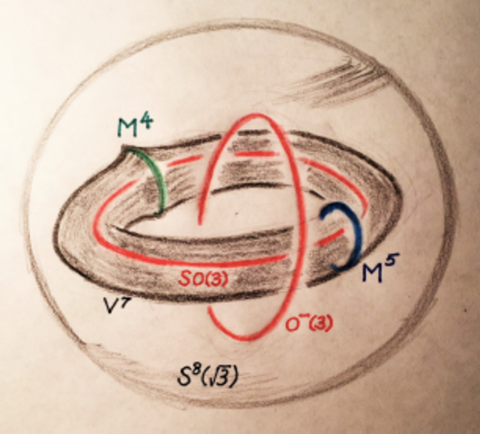

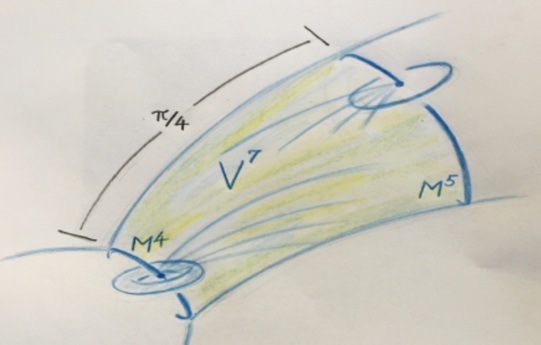

Figure 1 is the kind of picture we have in mind, in which we focus on matrices,

view them as points in Euclidean 9-space , ignore the zero matrix at the origin,

and scale the rest to lie on the round 8-sphere of radius , so as to include

the orthogonal group .

The two components of appear as real projective 3-spaces in the8-sphere, each the core of a open neighborhood of nonsingular matrices, whose cross-sectional fibres are triangular 5-dimensional cells lying on great5-spheres. The common boundary of these two neighborhoods is the 7-dimensional algebraic variety of singular matrices.

This variety fails to be a submanifold precisely along the 4-manifold of matrices of rank 1. The complement , consisting of matrices of rank 2, is a large tubular neighborhood of a core 5-manifold consisting of the “best matrices of rank 2”, namely those which are orthogonal on a 2-plane through the origin and zero on its orthogonal complement. is filled by geodesics, each an eighth of a great circle on the 8-sphere, which run between points of and with no overlap along their interiors. A circle’s worth of these geodesics originate from each point of , leaving it orthogonally, and a 2-torus’s worth of these geodesics arrive at each point of , also orthogonally.

We will confirm the above remarks, determine the topology and geometry of all these pieces, and the interesting cycles (families of matrices) which generate some of their homology, see how they all fit together to form the 8-sphere, and then in this setting visualize the polar and singular value decompositions and some of their applications.

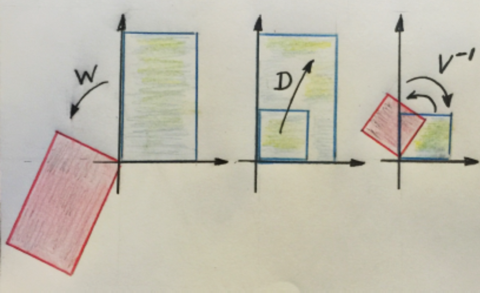

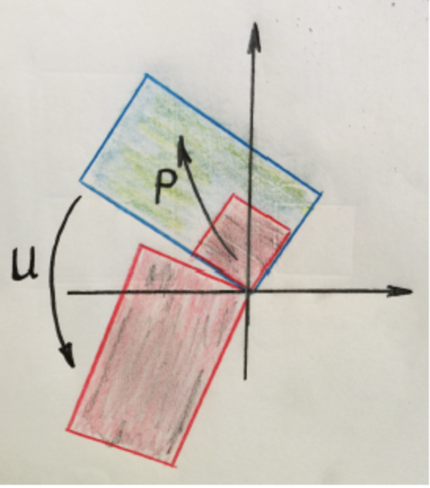

In Figure 2, we start with a matrix with positive determinant on , and show its polar and singular value decompositions, its nearest orthogonal neighbor , and its nearest singular neighbor on that 8-sphere.

Since , lies inside the tubular neighborhood of on the 8-sphere. The nearest orthogonal neighbor to is at the center of the 5-cell fibre of containing , while the nearest singular neighbor to lies on the boundary of that 5-cell.

These two nearest neighbors play a central role in the applications.

The positive definite symmetric matrix lies on the corresponding fibre of centered at the identity . Orthogonal diagonalization of yields the diagonal matrix on that same fibre, with .

Then we have the two matrix decompositions

Polar and singular value decompositions have a wealth of applications, from which we sample the following: least squares estimate of satellite attitude as well as computational comparative anatomy (both instances of nearest orthogonal neighbor, and known as the Orthogonal Procrustes Problem); and facial recognition via eigenfaces as well as interest rate term structures for US treasury bonds (both instances of nearest singular neighbor and known as Principal Component Analysis).

To the reader.

In the first half of this paper, we focus on the geometry and topology of spaces of matrices, quickly warm up with the simple geometry of matrices, and then concentrate entirely on the surprisingly rich and beautiful geometry of matrices. Hoping to have set the stage well in that case, we go no further on to higher dimensions, but invite the inspired reader to do so.

In the second half of the paper, we consider matrices of arbitrary size and shape, as we focus on their singular value and polar decompositions, and applications of these, and suggest a number of references for further reading.

As usual, figures depicting higher-dimensional phenomena are at best artful lies, emphasizing some features and distorting others, and need to be viewed charitably and cooperatively by the reader.

Acknowledgments.

We are grateful to our friends Christopher Catone, Joanne Darken, Ellen Gasparovic, Chris Hays, Kostis Karatapanis, Rob Kusner and Jerry Porter for their help with this paper.

Geometry and topology of spaces of matrices

matrices

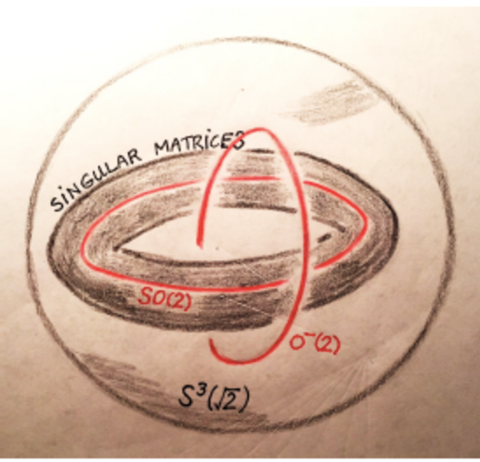

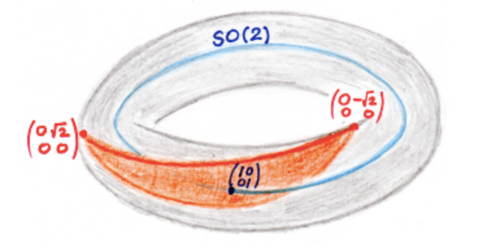

We begin with matrices, view them as points in Euclidean 4-space , ignore the zero matrix at the origin, and scale the rest to lie on the round 3-sphere of radius , so as to include the orthogonal group .

(1) First view. A simple coordinate change reveals that within this 3-sphere, the two components and of appear as linked orthogonal great circles, while the singular matrices appear as the Clifford torus halfway between these two great circles (Figure 3). The complement of this Clifford torus consists of open tubular neighborhoods and of and , each an open solid torus.

(2) Features.

-

(i)

On , the determinant function det takes its maximum value of on , its minimum value of on and its intermediate value of 0 on the Clifford torus of singular matrices.

-

(ii)

The level sets of det on are tori parallel to the Clifford torus, and the great circles and .

-

(iii)

The orthogonal trajectories to these level sets (i.e., the gradient flow lines of det) are quarter circles which leave orthogonally and arrive at orthogonally.

-

(iv)

The symmetric matrices on lie on a great 2-sphere with and as poles and with as equator. Inside the symmetric matrices, the diagonal matrices appear as a great circle through these poles, passing alternately through the tubular neighborhoods and of and , and crossing the Clifford torus four times.

-

(v)

On the great 2-sphere of symmetric matrices, the round disk of angular radius centered at is one of the cross-sectional fibres of the tubular neighborhood of . It meets orthogonally at its center, and meets the Clifford torus orthogonally along its boundary, thanks to (i), (ii) and (iii) above.

-

(vi)

The tangent space to at the identity matrix decomposes orthogonally into the one-dimensional space of skew-symmetric matrices (tangent to ), and the two-dimensional space of traceless symmetric matrices, tangent to the great 2-sphere of symmetric matrices. Within the traceless symmetric matrices is the one-dimensional space of traceless diagonal matrices, tangent to the great circle of diagonal matrices.

-

(vii)

Left or right multiplication by elements of are isometries of which take this cross-sectional fibre of at to the corresponding cross-sectional fibres of at the other points along . Left or right multiplication by elements of take this fibration of to the corresponding fibration of .

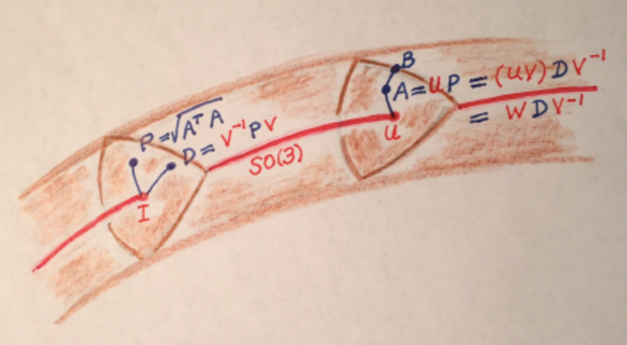

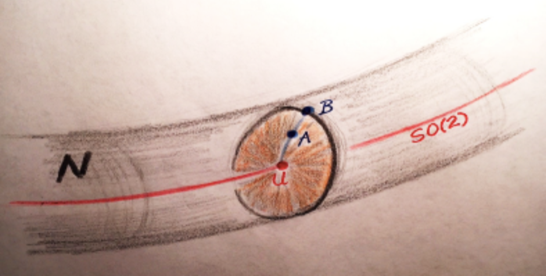

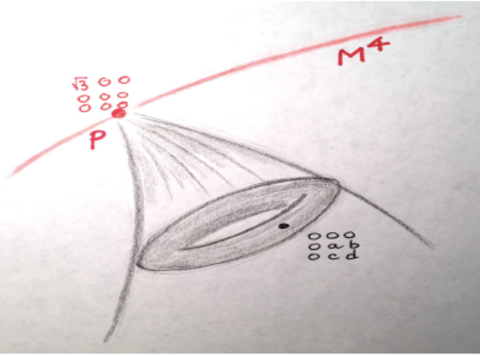

(3) Nearest orthogonal neighbor. Start with a nonsingular matrix on and suppose, to be specific, that lies in the open tubular neighborhood of . We claim that the nearest orthogonal neighbor to on that 3-sphere is the center of the cross-sectional fibre of on which it lies.

To see this, note that a geodesic (great circle arc) from to its nearest neighbor on must meet orthogonally at , and therefore must lie in the cross-sectional fibre of through . It follows that also lies in that fibre, whose center is at , confirming the above claim.

(4) Nearest singular neighbor. Start with a nonsingular matrix on . We claim that the nearest singular neighbor to on that -sphere is on the boundary of the cross-sectional disk on which it lies, at the end of the ray from its center through .

To see this, recall from (1) that the level surfaces of det on are tori parallel to the Clifford torus, and that their orthogonal trajectories are the quarter circles which leave orthogonally and arrive at orthogonally. It follows that the geodesics orthogonal to the Clifford torus lie in the cross-sectional disk fibres of the tubular neighborhoods and of and .

Now a geodesic (great circle arc) from to its nearest singular neighbor on the Clifford torus must meet that torus orthogonally at , and hence must lie in one of these cross-sectional disk fibres (Figure 4). If is not orthogonal, then lies at the end of the unique ray from the center of this fibre through , and hence is uniquely determined by . If is orthogonal, then can lie at the end of any of the rays from the center of this fibre, and so every point on the circular boundary of this fibre is a closest singular neighbor to on .

(5) Gram-Schmidt. Having just looked at the geometrically natural map which takes a nonsingular matrix to its nearest neighbor on the orthogonal group , it is irresistable to compare this with the Gram-Schmidt orthonormalization procedure. This procedure depends on a choice of basis for , hence is not “geometrically natural”, that is to say, not equivariant.

We see this geometric defect in Figure 5, where we restrict the Gram-Schmidt procedure to , and display the inverse image of the identity on that 3-sphere.

The inverse images of the other points on are rotated versions of . It is visually evident that this picture, and hence the Gram-Schmidt procedure itself, is not equivariant with respect to the action of via conjugation, which fixes pointwise, but rotates within itself.

matrices

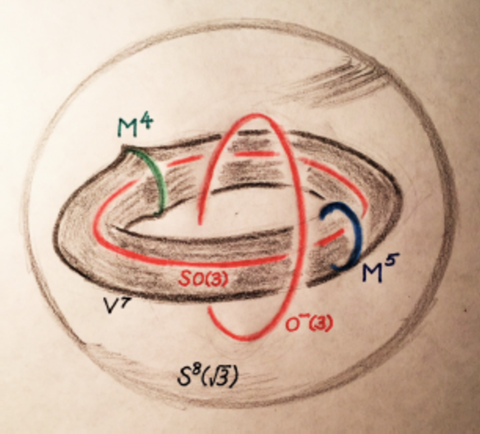

We turn now to matrices, view them as points in Euclidean 9-space , once again ignore the zero matrix at the origin, and scale the rest to lie on the round 8-sphere of radius , so as to include the orthogonal group .

(1) First view. The two components and of appear as real projective 3-spaces on , while the singular matrices (ranks 1 and 2) on this 8-sphere appear as a 7-dimensional algebraic variety separating them.

Contrary to appearances in Figure 6, the two components of are too low-dimensional to be linked in the 8-sphere. The subspaces , and in the figure were defined in the introduction, and will be examined in detail as we proceed.

(2) The tangent space to at the identity matrix decomposes orthogonally into the three-dimensional space of skew-symmetric matrices (tangent to ), and the five-dimensional space of traceless symmetric matrices, tangent to the great 5-sphere of symmetric matrices. Within the traceless symmetric matrices is the two-dimensional space of traceless diagonal matrices, tangent to the great 2-sphere of diagonal matrices in .

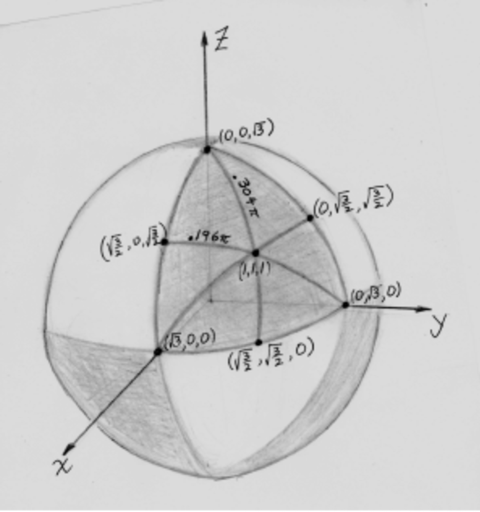

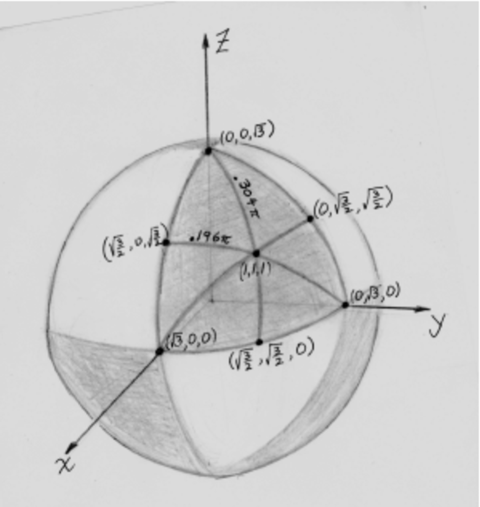

(3) A 2-sphere’s worth of diagonal matrices. The great 2-sphere of diagonal matrices on will play a key role in our understanding of the geometry of matrices as a whole.

In Figure 7, the diagonal matrix is located at the point , and indicated “distances” are really angular separations.

This 2-sphere is divided into eight spherical triangles, with the shaded ones centered at the points , , and of , and the unshaded ones centered at points of .

The interiors of the shaded triangles will lie in the open tubular neighborhood (yet to be defined) of on , the interiors of the unshaded triangles will lie in the open tubular neighborhood of , while the shared boundaries lie on the variety of singular matrices, with the vertices of rank 1, the open edges of rank 2, and the centers of the edges “best of rank 2”.

(4) Symmetries. We have acting as a group of isometries of our space of all matrices, and hence of the normalized ones on , via the map

This action is a rigid motion of the 8-sphere which takes the union of the two s representing to themselves (possibly interchanging them), and takes the variety of singular matrices separating them to itself.

“Natural geometric constructions” for matrices are those which are equivariant with respect to this action of .

(5) Tubular neighborhoods of and in . We expect, by analogy with matrices, that the complement in of the variety of singular matrices consists of open tubular neighborhoods of the two components and of the orthogonal group, with fibres which lie on the great 5-spheres which meet these cores orthogonally.

At the same time, our picture of the great 2-sphere’s worth of diagonal matrices alerts us that we cannot expect the fibres of these neighborhoods to be round 5-cells; instead they must somehow take on the triangular shapes seen in Figure 7.

Indeed, look at that figure and focus on the open shaded spherical triangle centered at the identity and lying in the first octant. Let act on this triangle by conjugation,

and the image will be a corresponding open triangular shaped region centered at the identity on the great 5-sphere of symmetric matrices, and consisting of the positive definite ones. Going from to is like fluffing up a pillow.

This open 5-cell is the fibre centered at the identity of the tubular neighborhood of , and the remaining fibres can be obtained by left (say) translation of by the elements of .

Why are these fibres disjoint? That is, why will two left translates of along be disjoint?

We can see from Figure 7 that it is going to be a close call, since the closures of the spherical triangles centered at and at meet at the point , even though their interiors are disjoint.

Consider a closed geodesic on , such as the set of transformations

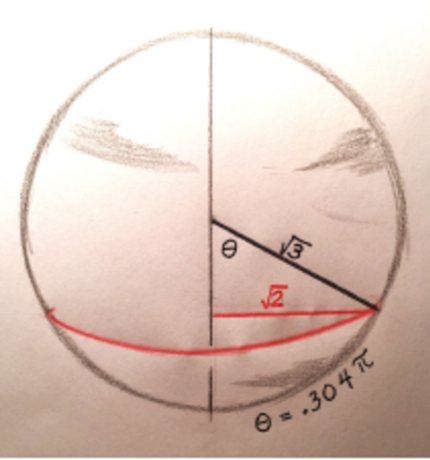

Figure 8 is a picture of that closed geodesic, appearing as a small circle of radius on .

In this picture, two great circles which meet the small circle orthogonally will come together at the south pole, after traveling an angular distance , but not before.

Since any two points and of lie together on a common closed geodesic (which is a small circle of radius on an 8-sphere of radius ), and since the maximum angular separation between the center of the 5-disk and its boundary is , it follows that the open 5-disks and must be disjoint.

In this way, we see that the union of the disjoint open 5-disks , as ranges over , forms an open tubular neighborhood of in . This tubular neighborhood is topologically trivial under the map

In similar fashion, we get an open tubular neighborhood of , likewise topologically trivial. The common boundary of these two tubular neighborhoods is the variety of singular matrices on .

(6) The determinant function on . The determinant function det on takes its maximum value of on , its minimum value of on , and its intermediate value of 0 on .

Unlike the situation for matrices, the orthogonal trajectories of the level sets of det are not geodesics, since the 5-cell fibres of the tubular neighborhoods N and of and are not round. In Figure 9, we see the level curves of det on the great 2-sphere of diagonal matrices.

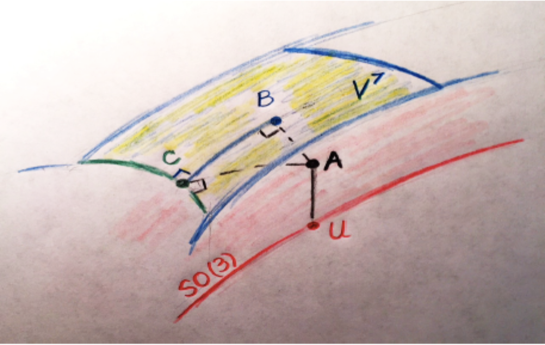

(7) The 7-dimensional variety of singular matrices on . The singular matrices on fill out a 7-dimensional algebraic variety defined by the equations . Nothing in our warmup with matrices prepares us for the incredible richness in the geometry and topology of this variety, which is sketched in Figure 10.

At the lower left is the 4-manifold of matrices of rank 1, along which fails to be a manifold, and at the upper right is the 5-manifold of best matrices of rank 2 .

The little torus linking signals (in advance of proof) that a torus’s worth of geodesics on shoot out orthogonally from each of its points, while the little circle linking signals that a circle’s worth of geodesics on shoot out orthogonally from each of its points.

These are the same geodesics, each an eighth of a great circle, and they fill with no overlap along their interiors.

(8) What portion of is a manifold? Identifying the set of all matrices with Euclidean space , we consider the determinant function .

Let be a given matrix. Then one easily computes the gradient of the determinant function to be

where is the cofactor of in .

Thus vanishes if and only if all the cofactors of vanish, which happens only when has rank .

The subvariety of consisting of the singular matrices is the zero set of the determinant function .

If is a matrix of rank 2 on then and the gradient vector is nonzero there, when det is considered as a function from . Since for all real numbers , the vector must be orthogonal to the ray through , and hence tangent to . Therefore is also nonzero when det is considered as a function from . It follows that is a submanifold of at all its points of rank 2.

But fails to be a manifold at all its points of rank 1, that is, along the subset , as we will confirm shortly.

(9) The 5-cell fibres of and meet orthogonally along their boundaries. This was noted earlier for matrices on .

Lemma 1. On , the gradient vector field of the determinant function, when evaluated at a diagonal matrix, is tangent to the great-sphere of diagonal matrices.

Proof. Looking once again at the gradient of the determinant function,

where is the cofactor of in , we see that if is a diagonal matrix, then is tangent to the space of diagonal matrices because each off-diagonal cofactor is zero, and if lies on , then the projection of to is still tangent to the space of diagonal matrices there.

Lemma 2. More generally, this gradient field is tangent to the -dimensional cross-sectional cells of the tubular neighborhoods and of and .

Proof. If is the 2-dimensional cell of diagonal matrices in the tubular neighborhood of on , then its isometric images , as ranges over , fill out the cross-sectional 5-cell of at the identity . Since the determinant function is invariant under this conjugation, its gradient is equivariant, and so must be tangent to this at each of its points. Then, using left translation by elements of , we see that the gradient field is tangent to all the cross-sectional 5-cells of …and likewise for .

Proposition 3. The cross-sectional -cell fibres of the tubular neighborhoods and of and on meet the variety of singular matrices orthogonally at their boundaries.

Proof. The gradient vector field of the determinant function on is orthogonal to the level surface of this function, and at the same time it is tangent to the cross-sectional 5-cell fibres of and . So it follows that these 5-cell fibres meet orthogonally at their boundaries.

(10) The submanifold of matrices of rank 1. First we identify as a manifold. Define to be the quotient of by the equivalence relation , a space which is (coincidentally) also homeomorphic to the Grassmann manifold of unoriented 2-planes through the origin in real 4-space. It is straightforward to confirm that is homeomorphic to .

Define a map by sending the pair of points and on to the matrix , scaled up to lie on . Then check that this map is onto, and that the only duplication is that and go to the same matrix.

Remarks. (1) is an orientable manifold because the involution of is orientation-preserving.

(2) is a single orbit of the action.

(3) The integer homology groups of are

an exercise in using Euler characteristic and Poincaré duality (Hatcher [2002]). Thus has the same rational homology as the 4-sphere .

(11) Tangent and normal vectors to . At the point , the tangent and normal spaces to within are

We leave this to the interested reader to confirm.

(12) The singularity of along . Let be a matrix with . Then a geodesic (i.e., great circle) on which runs through the rank 1 matrix at time , and is orthogonal there to has the form

If the matrix above has rank 2, then immediately has rank 3 for small . But if has rank 1, then has only rank 2 for small .

We know from our study of matrices that those of rank 1 form a cone (punctured at the origin) over the Clifford torus in . Thus the tubular neighborhood of in is a bundle over whose normal fibre is a cone over the Clifford torus. We indicate this pictorially in Figure 11.

One can use the information above to show that

(1) is a “tubular” neighborhood of , whose cross-sections are great circle cones of angular radius over Clifford tori on great 3-spheres which meet orthogonally.

(2) The 2-torus’s worth of geodesic rays shooting out from each point of in terminate along a full 2-torus’s worth of points in .

(13) The submanifold . Recall that the “best” matrices of rank 2 are those which are orthogonal on a 2-plane through the origin, and zero on its orthogonal complement.

An example of such a matrix is , representing orthogonal projection of -space to the -plane.

We let denote the set of best matrices of rank 2, scaled up to lie on . This set is a single orbit of the action on .

Claim: is homeomorphic to .

Proof. Let be one of these best matrices of rank 2 . Then the kernel of is some unoriented line through the origin in , hence an element of .

An orthogonal transformation of to a 2-plane through the origin in can be uniquely extended to an orientation-preserving orthogonal transformation of to itself, hence an element of .

Then the correspondence gives the homeomorphism of with , equivalently, with .

Remark. is non-orientable, and its integer homology groups are

an exercise in using the Künneth formula (Hatcher [2002]) for the homology of a product.

(14) Tangent and normal vectors to . At the point , the tangent and normal spaces to within are

and is spanned by , as the reader can confirm.

(15) The tubular neighborhood of inside .

Claim: is a tubular neighborhood of , whose cross sections are round cells of angular radius on great -spheres which meet orthogonally.

Proof. We start on at the scaled point , which represents orthogonal projection of -space to the -plane. Then we consider the tangent vectors

which are an orthogonal basis for .

If we exponentiate the vector in given by , with , from the point , we get

which has rank 2 for . All these matrices have the same kernel and same image as . But , which only has rank 1, and therefore lies on .

The set of points is one-eighth of a great circle on , beginning at the point on and ending at the point on . Let’s call this set a ray.

We see from the entries in the above matrix that the circle’s worth of rays shooting out from the point orthogonal to in terminate along a full circle’s worth of points on . We can think of this as an “absence of focusing”.

Since is a single orbit of the action on , the above situation at the point on is replicated at every point of , confirming the claim made above.

(16) The wedge norm on . Recall that for matrices viewed as points in and then restricted to , the determinant function varies between a maximum of 1 on and a minimum of on , with the middle value zero assumed on the Clifford torus of singular matrices. The level sets of this for values strictly between and 1 are tori parallel to the Clifford torus, and are principal orbits of the action. Their orthogonal trajectories are the geodesic arcs leaving orthogonally and arriving at orthogonally a quarter of a great circle later.

We seek a corresponding function on the variety of singular matrices on , whose level sets fill the space between and , and to this end, turn to the wedge norm , defined as follows.

If is a linear map between the real vector spaces and , then the induced linear map between spaces of 2-vectors is defined by

with extension by linearity. If , then the space is one-dimensional, and is simply multiplication by , while if , then the space is three-dimensional, and coincides with the matrix of cofactors of .

The wedge norm is defined by , and is easily seen to be -invariant, and thus constant along the orbits of this action. It has the following properties:

-

(1)

On the wedge norm takes its maximum value of on and its minimum value of 0 on .

-

(2)

The level sets between these two extreme values are 6-dimensional submanifolds which are principal orbits of the action.

-

(3)

The orthogonal trajectories of these level sets are geodesic arcs, each an eighth of a great circle, meeting both and orthogonally.

(17) Concrete generators for the 4-dimensional homology of . If we remove both components of the orthogonal group from the 8-sphere , then what is left over deformation retracts to the variety , since each cross-sectional 5-cell in the tubular neighborhoods of these two components has now had its center removed, and so can deformation retract to its boundary along great circle arcs.

Therefore has the same integer homology as , which can be computed by Alexander duality (Hatcher [2002]), and we learn that

while the remaining homology groups are zero. The variety is orientable because it divides into two components, but its homology is excused from satisfying Poincaré duality because it is not a manifold.

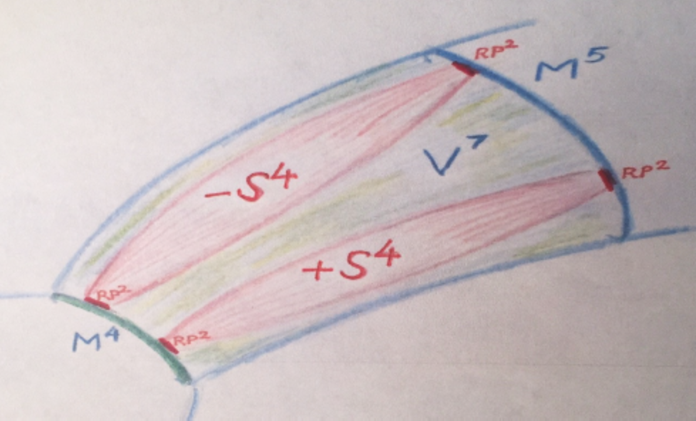

We seek concrete cycles generating .

Pick a point on each component of , for example, the identity on , and on . Then go out a short distance in the cross-sectional 5-cells of the two tubular neighborhoods, and we will have a pair of 4-spheres, each linking the corresponding component of , and therefore generating . Pushing these 4-spheres outwards to along the great circle rays of these two 5-cells provides the desired generators for .

How are these generators positioned on ?

The key to the answer can be found in the diagonal matrices. In Figure 12, consider the spherical triangle centered at . We noted earlier that the three vertices of this triangle lie in , and the centers of its three edges in . The six half-edges are geodesics, each an eighth of a great circle.

Conjugating by promotes this triangle to the cross-sectional 5-cell centered at the identity in the tubular neighborhood of , and promotes the decomposition of the boundary of the triangle to a decomposition of the boundary of this 5-cell.

This is enough to reveal the positions of our two generators of . We show this in Figure 13, where

-

(1)

The lower 4-sphere links in , and is the set of symmetric positive semi-definite matrices there which are not positive definite.

-

(2)

The upper 4-sphere links , and is the set of symmetric negative semi-definite matrices on which are not negative definite.

-

(3)

Each of these 4-spheres has an end in and another end in , and is smooth, except at the end in .

-

(4)

The action by conjugation on each 4-sphere is the same as that on the unit 4-sphere in the space of traceless, symmetric matrices described by Blaine Lawson [1980] . The principal orbits are all copies of the group of unit quaternions, modulo its subgroup , the singular orbits are the ends, and the orthogonal trajectories are geodesic arcs, each an eighth of a great circle.

(18) Nearest orthogonal neighbor. Start with a nonsingular matrix on and suppose, to be specific, that lies in the open tubular neighborhood of .

We claim that the nearest orthogonal neighbor to on that -sphere is the center of the cross-sectional fibre of on which it lies.

To see this, note that a geodesic (great circle arc) from to its nearest neighbor on must meet orthogonally at , and therefore must lie in the cross-sectional fibre of through . It follows that also lies in that fibre, whose center is at , confirming the above claim.

(19) Nearest singular neighbor. Start with a nonsingular matrix on , say with .

We claim that the nearest singular neighbor to on that -sphere lies on the boundary of the cross-sectional -cell of the tubular neighborhood of which contains .

Lemma. Let be a nonsingular matrix on , and let be the closest singular matrix to on this 8-sphere. Then has rank .

Proof. Suppose has rank 1, and therefore lies in . Since acts transitively on , we can choose orthogonal matrices and so that , and this will then be the closest singular matrix to the nonsingular matrix . So we can assume that already.

Since is nonsingular, it must have at least one nonzero entry for some and . Now let be the matrix with all zeros except in the th spot, with . Then also lies on and is orthogonal to .

Hence the matrices lie on as well, and

The derivative of this inner product with respect to at is

Therefore, for small values of , is a matrix of rank 2 on that is closer to than was. This contradicts the assumption that was closest to , and proves the lemma.

Remarks. (1) For visual evidence in support of this lemma, look at the front shaded spherical triangle on the great 2-sphere of diagonal matrices in Figure 12, and note that if is an interior point of this triangle, then the closest boundary point cannot be one of the vertices.

(2) More generally, let be an matrix of rank on . Then the matrix on of rank that is closest to actually has rank .

Now given the nonsingular matrix on , its nearest neighbor on must have rank 2, and therefore lies in the manifold portion of . It follows that the shortest geodesic from to is orthogonal to , and since we saw in section 9 that the 5-cell fibres of meet orthogonally along their boundaries, this geodesic must lie in the 5-cell fibre of containing .

Therefore lies on the boundary of this 5-cell fibre, as claimed.

Remark. Because the 5-cell fibres of are not round, the nearest singular neighbor is typically not at the end of the ray from the center of the cell through , as was true for matrices. We will shortly state the classical theorem of Eckart and Young which describes this nearest singular neighbor explicitly in terms of singular values.

Matrix Decompositions

Singular value decomposition

Let be an matrix, thus representing a linear map .

We seek a matrix decomposition of ,

where is a orthogonal matrix, where is an diagonal matrix,

with , and where is an orthogonal matrix.

The message of this decomposition is that takes some right angled-dimensional box in to some right angled box of dimension in , with the columns of the orthogonal matrices and serving to locate the edges of the domain and image boxes, and the diagonal matrix reporting expansion and compression of these edges (Figure 14). See Golub and Van Loan [1996] and Horn and Johnson [1991] for derivation of this singular value decomposition.

Remarks. (1) Consider the map , and note that

with eigenvalues and if , then also with zero eigenvalues. The orthonormal columns of are the corresponding eigenvectors of , since for example

and likewise for .

(2) In similar fashion, consider the map , note that

with eigenvalues , and if , then also with zero eigenvalues. The orthonormal columns of are the corresponding eigenvectors of .

(3) The singular value decomposition was discovered independently by the Italian differential geometer Eugenio Beltrami [1873] and the French algebraist Camille Jordan [1874a, b] , in response to a question about the bi-orthogonal equivalence of quadratic forms. Later, Erhard Schmidt [1907] introduced the infinite-dimensional analogue of the singular value decomposition and addressed the problem of finding the best approximation of lower rank to a given bilinear form.

Carl Eckart and Gale Young [1936] extended the singular value decomposition to rectangular matrices, and rediscovered Schmidt’s 1907 theorem about approximating a matrix by one of lower rank.

(4) Since finding the singular value decomposition of a matrix is equivalent to computing the eigenvalues and orthonormal eigenvectors of the symmetric matrices and , all of the computational techniques that apply to positive (semi)definite symmetric matrices apply, in particular the celebrated QR-algorithm, which was proposed independently by John Francis [1961] and Vera Kublanovskaya [1962]. Its later refinement, the implicitly shifted QR algorithm, was named one of the top ten algorithms of the 20th century by the editors of SIAM news (Cipra [2000]). For more historical details, we recommend Stewart [1993].

Polar decomposition

The polar decomposition of an matrix is the factoring

where is orthogonal and is symmetric positive semi-definite.

The message of this decomposition is that takes some right angled -dimensional box in to itself, edge by edge, expanding and compressing some while perhaps sending others to zero, after which moves the image box rigidly to another position (Figure 15).

See Golub and Van Loan [1996] and Horn and Johnson [1991] for derivation of this polar decomposition.

Remarks. (1) Existence of the polar decomposition follows immediately from the singular value decomposition for :

Furthermore, if , then , and hence

Now the symmetric matrix is positive semi-definite, and has a unique symmetric positive semi-definite square root .

(2) In the polar decomposition , the factor is uniquely determined by , while the factor is uniquely determined by if is nonsingular, but not in general if is singular.

(3) If and is nonsingular, with polar decomposition , and if we scale to lie on , then will also lie on that sphere, and the polar decomposition of is just the product coordinatization of the open tubular neighborhoods and of and .

(4) An matrix of rank has a factorization , with best of rank and symmetric positive semi-definite, and with both factors and uniquely determined by and having the same rank as .

(5) Let be a real nonsingular matrix, and let be its polar decomposition. Then is the nearest orthogonal matrix to , in the sense of minimizing the norm over all orthogonal matrices .

(6) Let be an matrix of rank with best of rank and symmetric positive semi-definite. Then is the nearest best of rank matrix to , in the sense of minimizing the norm over all best of rank matrices .

(7) The decomposition is called right polar decomposition, to distinguish it from the left polar decomposition Given the right polar decomposition , we can write to get the left polar decomposition. If is nonsingular, then the unique orthogonal factor is the same for both right and left polar decompositions, but the symmetric positive semi-definite factors and are not. No surprise about the orthogonal factor being the same, since in either case it is the unique element of the orthogonal group closest to .

(8) Léon Autonne [1902], in his study of matrix groups, first introduced the polar decomposition of a square matrix , where is unitary and is Hermitian, and quickly proved its existence.

The Nearest Singular Matrix

Theorem (Eckart and Young, 1936). Let be an matrix of rank , with singular value decomposition , where is a orthogonal matrix, where is an diagonal matrix,

and where is an orthogonal matrix.

Then the nearest matrix of rank is given by ,

with and as above, and with

We illustrate this in Figure 16 in the setting of 3 x 3 matrices.

In that figure, we start with a matrix on , having positive determinant and thus lying within the tubular neighborhood of , with its nearest orthogonal neighbor. If is the nearest singular matrix on to , and is the nearest rank 1 matrix on to , then will also be the nearest rank 1 matrix there to .

Principal component analysis

Consider the singular value decomposition of an matrix , where is a orthogonal matrix, where is an diagonal matrix,

with , and where is an orthogonal matrix.

Suppose that the rank of is , and that . Then from the Eckart-Young theorem, we know that the nearest matrix of rank is given by , with and as above, and with

The image of has the orthonormal basis , which are the first columns of the matrix .

The columns of are the vectors , and are known as the principal components of the matrix , and the first of them span the image of the best rank approximation to .

If the matrix is used to collect a family of data points, and these data points are listed as the columns of , then the orthonormal columns of are regarded as the principal components of this family of data points.

But if the data points are listed as the rows of , then it is the orthonormal columns of which serve as the principal components.

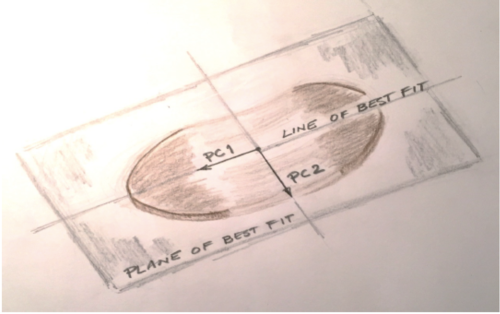

Remark. Principal Component Analysis began with Karl Pearson [1901]. He wanted to find the line or plane of closest fit to a system of points in space, in which the measurement of the locations of the points are subject to errors in any direction.

His key observation was that to achieve this, one should seek to minimize the sum of the squares of the perpendicular distances from all the points to the proposed line or plane of best fit. The best fitting line is what we now view as the first principal component, described earlier (Figure 17).

The actual term “principal component” was introduced by Harold Hotelling [1933].

For further reading about the history of these matrix decompositions, we recommend Horn and Johnson [1991], pages 134–140, and Stewart [1993] as excellent resources.

Applications of nearest orthogonal neighbor

The orthogonal Procrustes problem

Let and be two ordered sets of points in Euclidean -space . We seek a rigid motion of -space which moves as close as possible to , in the sense of minimizing the disparity between and , where .

It is easy to check that if we first translate the sets and to put their centroids at the origin, then this will guarantee that the desired rigid motion also fixes the origin, and so lies in . We assume this has been done, so that the sets and have their centroids at the origin.

Then we form the matrices and whose columns are the vectors and , and we seek the matrix in which minimizes the disparity between and .

We start by expanding

Now which is fixed, and likewise is fixed, so we want to maximize the inner product by appropriate choice of in . But

and so, reversing the above steps, we want to minimize the inner product

which means that we are seeking the orthogonal transformation which is closest to in the space of matrices.

The above argument was given by Peter Schönemann [1966] in his PhD thesis at the University of North Carolina.

When , we don’t have a simple explicit formula for , but it is the orthogonal factor in the polar decomposition

Visually speaking, if we scale to lie on the round sphere of radius in-dimensional Euclidean space , then is at the center of the cross-sectional cell in the tubular neighborhood of which contains , and is unique if .

A least squares estimate of satellite attitude

Let be unit vectors in 3-space which represent the direction cosines of objects observed in an earthbound fixed frame of reference, and the direction cosines of the same objects as observed in a satellite fixed frame of reference. Then the element in which minimizes the disparity between and is a least squares estimate of the rotation matrix which carries the known frame of reference into the satellite fixed frame at any given time. See Wahba [1966].

Errors incurred in computation of can result in a loss of orthogonality, and be compensated for by moving the computed to its nearest orthogonal neighbor.

Procrustes best fit of anatomical objects

The challenge is to compare two similar anatomical objects: two skulls, two teeth, two brains, two kidneys, and so forth.

Anatomically corresponding points (landmarks) are chosen on the two objects, say the ordered set of points on the first object, and the ordered set of points on the second object. They are translated to place their centroids at the origin, and then the Procrustes procedure is applied by seeking a rigid motion of 3-space so as to minimize the disparity between and , where .

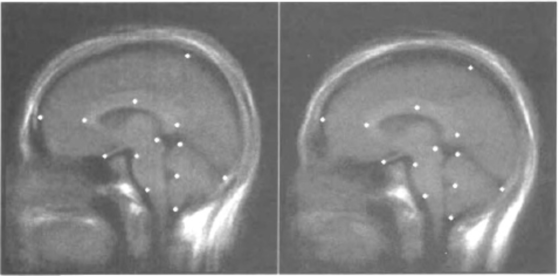

In Figure 18, the left brain slice is actually an average over a group of doctors, and the right slice an average over a group of patients, each with 13 corresponding landmark points, from the paper by Bookstein [1997].

If size is not important in the comparison of two shapes, then it can be factored out by scaling the two sets of landmarks, and , so that .

For modifications which allow comparison of any number of shapes at the same time, see for example Rohlf and Slice [1990].

The effectiveness of this Procrustes comparison naturally depends on appropriate choice and placement of the landmark points, and leads one to seek an alternative approach which does not depend on this. To that end, see Lipman, Al-Aifari and Daubechies [2013] in which the authors propose a continuous Procrustes distance, and then prove that it provides a metric for the space of “shapes” of two-dimensional surfaces embedded in three-space.

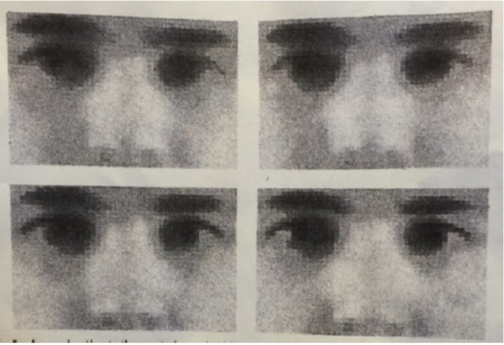

Facial recognition and eigenfaces

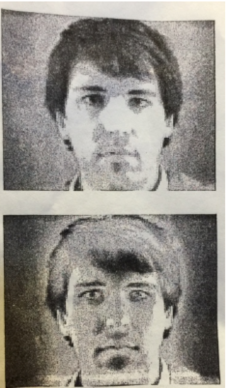

We follow Sirovich and Kirby [1987] in which the principal components of the data base matrix of facial pictures are suggestively called eigenpictures.

The authors and their team assembled a file of 115 pictures of undergraduate students at Brown University. Aiming for a relatively homogeneous population, these students were all smooth-skinned caucasian males. The faces were lined up so that the same vertical line passsed through the symmetry line of each face, and the same horizontal line through the pupils of the eyes. Size was normalized so that facial width was the same for all images.

Each picture contained pixels, with a grey scale determined at each pixel. So each picture was regarded as a single vector ,, called a face, in a vector space of dimension .

The challenge was to find a low-dimensional subspace of best fit to these 115 faces, so that a person could be sensibly recognized by the projection of his picture into this subspace.

To make sure that the subspace passes through the origin (i.e., is a linear rather than affine subspace), the data is adjusted so that its average is zero, as follows.

Let be the average face, where , and then let be the deviation of each face from the average. The authors refer to each such deviation as a caricature. Figure 19 shows a sample face, and its caricature.

The collection of caricatures was then regarded as a matrix , with each caricature appearing as a column of .

If the singular value decomposition of is , with a orthogonal matrix,

a diagonal matrix, and a orthogonal matrix, then the orthonormal columns of are the principal components of the matrix .

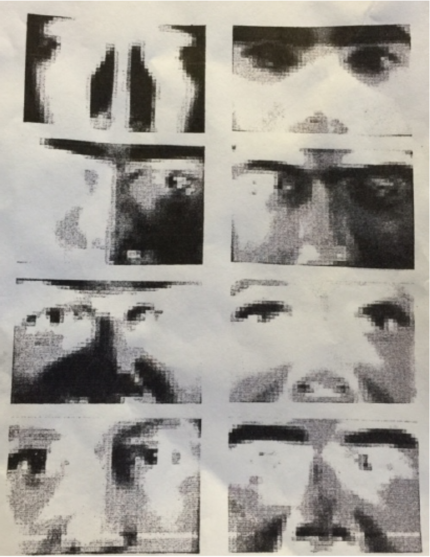

It was found that the first 100 principal components of span a subspace sufficiently large to recognize any of the faces by projecting its caricature into this subspace and then adding back the average face:

Figure 20 shows the first eight eigenpictures starting at the upper left, moving to the right, and ending at the lower right, in which each picture is cropped to focus on the eyes and nose. Since the eigenpictures can have negative entries, a constant was added to all the entries to make them positive for the purpose of viewing

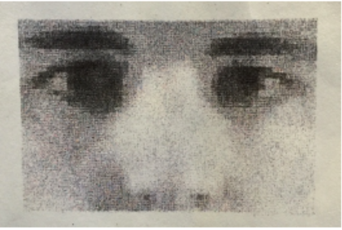

Figure 21 shows a sample face, correspondingly cropped,

and Figure 22 shows the approximations to that sample face, using 10, 20, 30 and 40 eigenpictures.

After working with the initial group of 115 male students, the authors tried out the recognition procedure on one more male student and two females, using 40 eigenpictures, with errors of 7.8%, 3.9%, and 2.4% in these three cases.

Remarks.

-

(1)

In the pattern recognition literature, the Principal Component Analysis method used in this paper is also known as the Karhunen-Loeve expansion.

-

(2)

Another very informative and nicely written paper on this approach to facial recognition is Turk and Pentland [1991]. The section of this paper on Background and Related Work is a brief but very interesting survey of alternative approaches to computer recognition of faces. An overview of the literature on face recognition is given in Zhao et al [2003].

Principal component analysis applied to

interest rate term structure

How does the interest rate of a bond vary with respect to its term, meaning time to maturity? The answer involves one of the oldest and best known applications of Principal Components Analysis (PCA) to the field of economics and finance, originating in the work of Litterman and Scheinkman [1991].

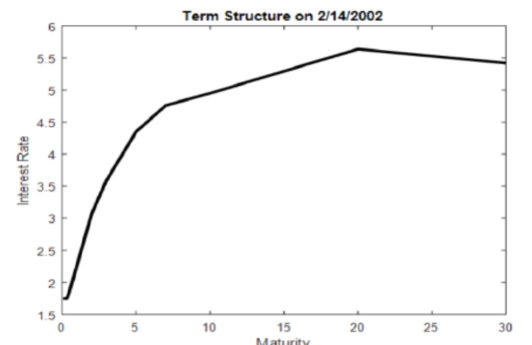

To begin, economists plot the interest rate for a given bond against a variety of different maturities, and call this a yield curve. Figure 23 shows such a curve for US Treasury bonds from an earlier date, when interest rates were higher than they are now.

Predicting the relation shown by such a curve can be crucial for investors trying to determine which assets to invest in, and for governments who wish to determine the best mix of Treasury maturities to auction on any given day. For this reason, a number of investigators have tried to understand whether there are common factors embedded in the term structure. In particular, identifying whether there are factors which affect all interest rates equally, or which affect interest rates for bonds of certain maturities but not of others, is important for understanding how the term structure behaves.

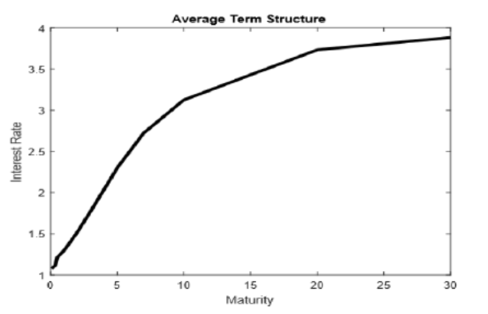

To help understand how these questions are answered, we replicated the methodology in the Litterman and Scheinkman paper, using a newer data set which gives the daily interest rate term structure for US Treasury bonds over a long span of time, 2,751 days between 2001 and 2016. For each of these days, we recorded the interest rates for bonds of 11 different maturities: 1, 3 and 6 months, and 1, 2, 3, 5, 7, 10, 20 and 30 years. Each data vector is an 11-tuple of interest rates, which we collect as the rows of a matrix.

The average of the rows is depicted graphically in Figure 24.

We subtracted this average from each of the rows, and called the resulting matrix . The rows of are our adjusted data vectors, which now add up to zero.

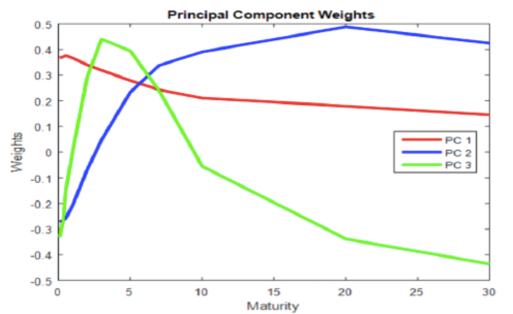

Let be the singular value decomposition of , where is an orthogonal matrix, is a diagonal matrix, and is a orthogonal matrix. Since the data points are the rows of , the principal components are the 11 orthonormal columns of .

These principal components reveal the line of best fit, the plane of best fit, the 3-space of best fit, and so forth for our 2,751 data points. They were obtained using the PCA package of MATLAB. The first three principal components are shown graphically in Figure 25.

The first principal component is more constant than the other two, and captures the fact that most of the variation in term structures comes from changes which affect the levels of all yields.

The second most important source of variation in term structure comes from the second principal component, which reflects changes that most affect yields on bonds of longer maturities, while the third principal component reflects changes that affect medium term yields the most. These features of the first three principal components were called level, steepness, and curvature in the foundational paper by Litterman and Scheinkman.

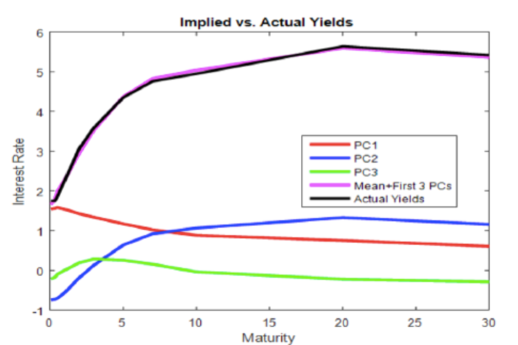

In Figure 26, the black curve is the term structure on 2/14/2002, duplicating the first figure in this section. We subtract the average term structure from this particular one, project the difference onto the one-dimensional subspaces spanned in turn by the first three principal components, and show these projections below in red, blue and green. Finally, we sum up these three projections, add back the average term structure, show the result in purple, and see how closely this purple curve approximates the black curve we started with.

REFERENCES

- 1873

-

E. Beltrami, Sulle funzioni bilineari, Giornali di Mat. ad Uso degli Studenti Delle Universita, 11, 98–106

- 1874a

-

C. Jordan, Memoire sur les formes bilineares, J. Math. Pures Appl., 2nd series, 19, 35–54

- 1874b

-

C. Jordan, Sur la reduction des formes bilineares, Comptes Rendus de l’Academie Sciences, Paris 78, 614–617

- 1901

-

Karl Pearson, On Lines and Planes of Closest Fit to Systems of Points in Space, Philosophical Magazine 2, 559–572.

- 1902

-

L. Autonne, Sur les groupes lineaires, reels et orthogonaux, Bull. Soc. Math. France, 30, 121–134

- 1907

-

E. Schmidt, Zur Theorie des linearen und nichlinearen Integral gleichungen, I Teil. Entwicklung willkurlichen Funktionen nach System vorgeschriebener, Math. Ann. 63, 433 – 476

- 1933

-

H. Hotelling, Analysis of a complex of statistical variables into principal components, J. Ed. Psych, 24, 417 – 441 and 498 – 520

- 1936

-

C. Eckart and G. Young, The approximation of one matrix by another of lower rank, Psychometrika, I, 211 – 218.

- 1947

-

Kari Karhunen, Uber lineare Methoden in der Wahrscheinlichkeitsrechnung, Ann. Acad. Sci. Fennicae, Ser. A. I. Math-Phys 37, 1–79.

- 1961

-

John Francis, The QR transformation, parts I and II, Computer J. Vol. 4, 265–272 and 332–345.

- 1962

-

Vera Kublanovskaya, On some algorithms for the solution of the complete eigenvalue problem, USSR Comput. Math. and Math. Physics. vol 1, 637–657.

- 1966

-

Peter H. Schönemann, A generalized solution of the orthogonal Procrustes problem, Psychometrika, Vol. 31, No. 1, March, 1 – 10.

- 1966

-

Grace Wahba, A Least Squares Estimate of Satellite Attitude, SIAM Review, Vol. 8, No. 3, 384 – 386.

- 1976

-

Wolfgang Kabsch, A solution for the best rotation to relate two sets of vectors, Acta Crystallographica 32, 922, with a correction in 1978, A discussion of the solution for the best rotation to relate two sets of vectors, Ibid, A-34, 827–828.

- 1980

-

H. Blaine Lawson, Lectures on Minimal Submanifolds, Publish or Perish Press.

- 1985

-

Roger Horn and Charles Johnson, Matrix Analysis, Cambridge University Press.

- 1986

-

Nicholas J. Higham, Computing the polar decomposition – with applications, SIAM J. Sci. Stat. Comput. Vol. 7, No. 4 October, 1160 – 1174.

- 1987

-

L. Sirovich and M. Kirby, Low-dimensional procedure for the characterization of human faces, J. Optical Society of America, Vol. 4, No. 3, 519 – 524,

- 1990

-

F. James Rohlf and Dennis Slice, Extensions of the Procrustes method for the optimal superimposition of landmarks, Syst. Zool. 39 (1), 40 – 59.

- 1991

-

Roger Horn and Charles Johnson, Topics in Matrix Analysis, Cambridge University Press.

- 1991

-

Robert Litterman and José Scheinkman, Common factors affecting bond returns, J. Fixed Income, June, 54 – 61.

- 1991

-

Matthew Turk and Alex Pentland, Eigenfaces for Recognition, Journal of Cognitive Neuroscience, Vol. 3, No. 1, 71 – 86.

- 1993

-

G.W. Stewart, On the early history of the singular value decomposition, SIAM Review, Vol. 35, No. 4, 551 – 566

- 1996

-

Gene Golub and Charles Van Loan, Matrix Computations, Third Edition, Johns Hopkins University Press.

- 1997

-

Fred L. Bookstein, Biometrics and brain maps: the promise of the Morphometric Synthesis, in S. Kowlow and M. Huerta, eds., Neuroinformatics: An Overview of the Human Brain Project, Progress in Neuroinformatics, Vol. 1, 203 – 254.

- 2000

-

Barry Cipra, The Best of the 20th Century: Editors Name Top 10 Algorithms, SIAM News, Vol. 33, No. 4, 1–2.

- 2002

-

Allen Hatcher, Algebraic Topology, Cambridge University Press.

- 2003

-

W. Zhao, R. Chellappa, P.J. Phillips and A. Rosenfeld, Face Recognition: A Literature Survey, ACM Computing Surveys, Vol. 35, No. 4, 399 – 458.

- 2009

-

G. H. Golub and F. Uhlig, The QR algorithm: 50 years later its genesis by John Francis and Vera Kublanovskaya and subsequent developments, IMA J. Numer. Anal. Vol. 29, 467–485.

- 2011

-

David S. Watkins, Francis’s Algorithm, American Mathematical Monthly Vol. 118, May, 387–403.

- 2013

-

Yaron Lipman, Reema Al-Aifari and Ingrid Daubechies, The continuous Procrustes distance between two surfaces, Comm. Pure Appl. Math. 66, 934 – 964,

University of Pennsylvania

Philadelphia, PA 19104

Dennis DeTurck: deturck@math.upenn.edu

Amora Elsaify: aelsaify@wharton.upenn.edu

Herman Gluck: gluck@math.upenn.edu

Benjamin Grossmann: bwg25@drexel.edu

Joseph Hoisington: jhois@math.upenn.edu

Anusha M. Krishnan: anushakr@math.upenn.edu

Jianru Zhang: jianruzh@math.upenn.edu