On the Efficiency of Connection Charges—

Part I: A Stochastic Framework

Abstract

This two-part paper addresses the design of retail electricity tariffs for distribution systems with distributed energy resources such as solar power and storage. In particular, the optimal design of dynamic two-part tariffs for a regulated monopolistic retailer is considered, where the retailer faces exogenous wholesale electricity prices and fixed costs on the one hand and stochastic demands with inter-temporal price dependencies on the other. Part I presents a general framework and analysis for revenue adequate retail tariffs with advanced notification, dynamic prices and uniform connection charges. It is shown that the optimal two-part tariff consists of a dynamic price that may not match the expected wholesale price and a connection charge that distributes uniformly among all customers the retailer’s fixed costs and a price-volume risk premium. A sufficient condition for the optimality of the derived two-part tariff among the class of arbitrary ex-ante tariffs is obtained. Numerical simulations quantify the substantial welfare gains that the optimal two-part tariff may bring compared to the optimal linear tariff (without connection charge). Part II focuses on the impact of two-part tariffs on the integration of distributed energy resources.

Index Terms:

Retail tariff design, connection charges, dynamic pricing, distributed energy resources, optimal demand response.I Introduction

The electric power industry is experiencing an important transformation driven by disruptive innovation in distributed renewable generation and energy storage systems [1]. A concern of this transformation is the impact of the inclining adoption of said distributed energy resources (DERs) on the financial viability of regulated distribution grid operators [2]. In particular, under the restriction to volumetric and net-metering tariffs, the gradual decline in energy sales could compromise the ability of grid operators to recover their predominantly fixed operational and capital expenditures. This could result in the need to increase retail prices further above wholesale electricity prices, thereby amplifying the entailed economic inefficiencies, inter-customer cross-subsidies, and incentives for DER adoption in a vicious circle.

This two-part paper aims to shed lights on the effectiveness of connection charges as a means to mitigate the negative impacts of the sustained adoption of DERs. To this end, Part I develops a framework to analyze the efficiency of retail electricity tariffs set for a regulated retailer who serves a heterogeneous population of residential customers under demand and wholesale price uncertainties.

In particular, we are interested in two practical and fairly general ex-ante retail pricing models: a volumetric linear tariff and a two-part tariff consisting of a volumetric linear charge and a connection charge. Our goal in Part I is to gain insights into the structure of the optimal revenue adequate linear and two-part tariffs that allow us to analyze, in Part II, the effects of integrating customer and retailer-owned DERs.

I-A Related Work

There is a vast literature on efficient retail pricing of electricity, the economic foundations of which reside in the classical theory of peak-load pricing [3]—known more recently as dynamic pricing [4]. Recent reviews of the subject along with a brief history of its adoption by regulators and electric utilities can be found in [5, 6]. In this context, connection charges have been considered as a means to raise additional revenue to recover the predominantly fixed costs of electric utilities [3]. In the U.S., mild connection charges are prevalent with exceptions such as California, where the large investor-owned utilities have default volumetric residential tariffs with virtually no connection charges111PG&E and SDG&E have no connection charge whereas SCE’s charges $0.99/month. While these utilities have a minimum bill of $10/month or less, it is binding on extremely few customers, and thus practically irrelevant [7]. [7].

In the last two decades, while the adoption of time-varying prices has been particularly slow in the U.S. [4], the advent of cheaper smart meters, small-scale renewable energy installations, battery storage technologies and home energy management tools has stimulated research in dynamic pricing (see [8, 9] and references therein) as sophisticated technologies can enable customers to react to price signals [10]. Of particular interest is real-time pricing (RTP), a form of dynamic pricing widely known to be a critical feature of efficient electricity markets [11]. An overview of dynamic pricing and a recent analysis of its limited adoption in the U.S. are available in [11] and [4], respectively.

Economic approaches to dynamic pricing often rely on functional demand models to characterize competitive equilibrium prices when smart meters become available to customers [12, 13, 14].The most relevant analysis is [14] where the socially optimal linear and two-part retail tariffs subject to a retailer revenue sufficiency constraint are derived. Unlike our work, however, this analysis does not accommodate inter-temporal demand dependencies nor the integration of DERs.

Most engineering approaches, on the other hand, focus on analyzing demand response models in smart grids [8, 9]. These approaches often involve modeling customer behavior [15, 16], sometimes down to the appliance level [17, 18, 19, 20], by characterizing customers’ response to certain pricing scheme. Appliances modeled include thermostatically controlled loads (TCL) [19, 20], electric vehicles [18], and batteries [17]. Other works focus on designing said pricing schemes to induce a desired behavior anticipating customers’ response [21, 22, 23, 24, 25, 26]. For example, the work in [21] considers utility-maximizing consumers and a social-welfare-maximizing supplier that procures electricity in two steps (day-ahead and in real-time). In a multiperiod and deterministic setting, the authors derive the socially optimal retail prices: a time-differentiated linear tariff. In a similar setting where only the real-time market and a stylized TCL model are considered, the work in [26] derives optimal day-ahead retail prices while accommodating cost and demand uncertainty and an implicit retailer revenue requirement222The revenue requirement is incorporated indirectly into the formulation through a weighted social welfare objective..

I-B Summary of Results and Contributions

The main contribution of Part I is the explicit characterization of the optimal revenue adequate ex-ante two-part tariff for a stochastic demand with inter-temporal dependencies. The results in Part I lay the foundation for analyzing the welfare impacts of integrating DERs such as solar power and energy storage under different retail tariffs, which we address in Part II. Here we apply the classical Ramsey pricing theory with extensions to accommodate the uncertainty and inter-temporal dependencies of demand that arise with the integration of behind-the-meter renewables and storage. While economic literature has disregarded said extensions, engineering approaches to dynamic pricing and demand response have ignored the revenue adequacy objective of retail tariff design, which our work addresses explicitly. In this context, there are no existing comparable studies in the open literature with the exception of a preliminary work in [27]. To a large extent, our results are an examination of emerging issues in smart distribution systems through the lens of classical economic results on the fundamental efficiency of two-part tariffs in stylized economic models [3].

The main results of this paper are as follows. We consider the design of ex-ante retail tariffs from the perspective of a regulated retailer subject to a revenue sufficiency constraint. The ex-ante tariffs considered here include traditional tariffs with long lag times as well as some of the more sophisticated tariffs that are being considered for smart distribution systems. Examples include time-of-use tariffs, critical peak pricing, variable peak pricing, and real-time pricing [10]. The retailer considered in this paper is a regulated monopoly which, on one hand, serves heterogeneous residential customers with elastic demands. The demand model considered here is stochastic and captures inter-temporal price dependencies. On the other hand, the retailer interfaces with an exogenous wholesale market with stochastic real-time prices. We describe the models in our formulation in Section II.

Within this general setting, we characterize the structure of optimal linear and two-part tariffs in the presence of demand and wholesale price uncertainty in Section III. In particular, we show that the optimal ex-ante two-part tariff consists of a time-varying retail price that not always matches the expected wholesale price and a connection charge that allocates uniformly among all customers the retailer’s fixed costs and risk-related costs caused by the ex-ante determination of the tariff. We further show that the optimal volumetric tariff, referred hereafter as linear tariff, is characterized by a time-varying price markup—relative to the optimal two-part tariff’s price—that depends on the retailer’s fixed costs and the price elasticity of demand.

We further compare the efficiency of the linear and two-part tariff in Section III-C. Specifically, we present a parametric characterization of the social welfare (SW) or total surplus and the consumer surplus (CS) as a function of the retailer’s fixed costs. We show that the two-part tariff achieves the same SW regardless of the retailer’s fixed costs. For the linear tariff, in contrast, the SW decreases as the fixed costs increase, thus characterizing a trade-off between fixed costs and efficiency. We also provide a sufficiency condition under which the two-part tariff is optimal among all ex-ante nonlinear tariffs.

We demonstrate the performance of the derived tariffs numerically using publicly available data from NYISO and the largest utility company in New York City in Section IV. Contingent on the deployment of enabling technologies and smart meters, our results estimate that the optimal day-ahead linear tariff could bring loses ( of the utility’s revenue) relative to the utility’s suboptimal two-part flat tariff due to the lack of a connection charge. The optimal day-ahead two-part tariff, on the other hand, could bring significant gains ( of the utility’s revenue). From a societal perspective, these loses and gains manifest themselves as reductions and increments in electricity consumption, respectively. These estimates assume a realistic own-price elasticity of demand and a stylized model for TCL. Some concluding remarks and proofs are included in Section V and the Appendix, respectively.

I-C Notations

We use to denote the expectation of a random vector and to denote the cross-covariance matrix of two random vectors , . Let also denote the entry of a vector and its transpose.

II Model

Given our focus on the retail electricity market, we assume the state of the wholesale market is represented by an exogenous discrete-time random process , which represents the wholesale RTP of electricity at time in a single location of interest. We assume that the time periods partition a billing cycle, which is the time horizon relevant for our formulation. Moreover, we assume the wholesale RTP accurately reflects the social marginal cost of electricity [7].

II-A A Retail Tariff Model

In this paper, we consider time-differentiated retail electricity tariffs that are set and announced in advance (i.e., ex-ante) by a regulated retailer with a fixed lag time. These tariffs are fixed before the beginning of a billing period of certain length (e.g., a month or a day) with a fixed lag time (e.g., several days or hours), specify a pricing rule that depends on the temporal consumption profile within the billing period rather than on the accumulated consumption, and are allowed to vary dynamically from one billing period to the next. In the context of retail tariffs, the tariff lag time induces a tradeoff between advanced price notification and price signal accuracy [11]. The tariff model considered here captures both the traditional long term flat tariff that has months or years of lag time as well as more sophisticated dynamic tariffs such as those with days or hours of advanced notification, but it generally excludes ex-post tariffs such as those indexed to the wholesale RTP.

Formally, some time before the billing cycle starts, the retailer announces a tariff that maps the metered consumption power profile of each customer to a scalar charge . While the entry of is a single customer’s metered consumption in period of the billing period, the amount (in dollars) represents the total bill. Note that this form of tariff captures the intertemporal dependencies of pricing and consumption within each billing cycle (but not between several billing cycles).

Given a tariff , customers rationally choose in real-time how much electricity to purchase from the retailer during each consumption period of the current billing cycle. The retailer then pays for the aggregate demand at the wholesale RTP.

Although in practice retailers buy certain portions of the aggregate demand in forward markets (including the day-ahead market), we can neglect such purchases in our formulation without loss of generality for the following reason. In perfectly competitive and well-functioning two-settlement markets, forward transactions are essentially used to hedge against the volatility of the RTP. Here, we consider risk-neutral decision markers that deal with uncertainty by taking expectations. Thus, in our setting, forward markets would bring no significant advantages to any stakeholder. This justifies the reliance of the retailer in the RTP to purchase electricity, which is an assumption that simplifies our exposition considerably.

II-B Consumer Model

We consider customers (indexed by ) who obtain a monetary benefit (i.e., gross surplus) from consuming a power profile throughout the billing cycle. This benefit is contingent on , where is an exogenous random process that represents customer ’s local state. We assume that is continuously differentiable in .

Accordingly, customer exhibits a consumption profile when facing a tariff and a sequence of local states . Customers are rational in that sense that the sequence of consumptions solves the multistage stochastic program

| (1) |

where the expectation is taken over , and represents customer ’s expected surplus. Correspondingly, a tariff yields an (aggregate) expected consumer surplus

| (2) |

where the expectation is taken over .

Of particular interest is the demand response to tariffs with constant gradient , where is a time-varying per-unit price, such as the tariff with the affine form . For such tariffs we use the notation

| (3) |

for customer ’s demand profile, thus implicitly assuming that it depends on only through . Hence, is a standard demand function which we assume to be nonnegative and continuously differentiable in , and its Jacobian , with entry , negative definite. Under the regularity assumptions made on and , one can show that is decreasing and convex in (see Prop. 3 in Appendix). We further define the aggregate demand function as . A consumer model similar to the one decribed in this section for is proposed and discussed with more detail in [14].

For example, for a linear tariff , the consumption of a TCL may be modeled with a linear demand function , with deterministic and positive definite . Such demand function can be derived from an additive and temporally-separable quadratic benefit function via stochastic dynamic programming [26].

II-C Retailer Model

We consider the case of a retail monopoly and refer to the single entity as the retailer, utility, or load-serving entity (LSE). In procuring an aggregate demand profile , we assume that the retailer incurs a variable cost , where is the wholesale RTP333While in practice the time granularity of the wholesale RTP is finer than that of retail rates, we assume they are equal to simplify our exposition. Hence, a tariff yields the expected retailer surplus

| (4) |

where the expectation is taken over the global state . For notational convenience, we define the RS collected from the volumetric charge of an affine tariff as so that and

| (5) |

III Retail Tariff Design

In our retail tariff design framework, we assume that the regulator mandates the retailer to choose a tariff that maximizes the expected consumer surplus. Moreover, in order to recover the upstream fixed costs incurred to deliver electricity, the tariff should satisfy the revenue adequacy constraint , where is a target approved by the regulator.

Formally, the regulator’s problem can be stated as

| (6) |

In general, this problem falls in the category of Ramsey-Boiteux pricing and peak-load pricing in economics [28], which are main components of the theory of public utility pricing [3, Sec. 4.5]. See [6] for a recent overview of this problem in the context of electricity pricing.

In this section, we study linear and two-part tariffs—two of the most widely used tariffs in electricity industry. The restriction to two-part tariff can in fact be made without loss of generality under certain conditions (Theorem 3). We begin by making the following assumption that guarantees the existence and uniqueness of solutions to problem (6).

Assumption 1.

is such that the Jacobian matrix is negative definite (nd).

This assumption—made mainly for analytical convenience—is common is economics [14] and essentially imposes a limitation on the curvature of the demand function444In particular, for a linear demand , is nd since is nd. Moreover, for a demand with additive disturbances , A1 holds for if each is concave in since . Concave demand functions are common in economic models since they guarantee profit and welfare maximization problems to be well defined [29]. See, for example, Prop. 4 in the Appendix. . Intuitively, the demand can be generally linear, concave, or convex in ; however, when convex, restrictions on the “amount” of convexity are required for Assumption 1 to hold.

III-A Structure of Optimal Two-Part Tariff

By restricting the regulator’s problem to two-part tariffs of the form , problem (6) can be reformulated as a convex program under Assumption 1. We emphasize here that our analysis implicitly assumes that no customer chooses to avoid the connection charge by not consuming electricity at all555This assumption is widely accepted for services such as electricity and water since “it is extremely unlikely that a customer will drop out of the market, however high the tariff” [3, Sec. 4.5]. Studies suggest, however, that more cost-effective DERs might challenge this assumption in future years [2].. The following result characterizes the optimal solution.

Theorem 1.

(Optimal two-part tariff) The two-part tariff that solves problem (6) is characterized by

| (7) | ||||

| (8) |

Theorem 1 implies that the optimal price is characterized by a period-specific price markup relative to the expected RTP, . Examination of (7) reveals that this markup is essentially determined by the cross-covariance between the price sensitivity of demand and the RTP666In expression (7), the second expectation is a second-order expectation that can be thought as the cross-covariance between a matrix and a vector. To gain intuition into (7), consider a demand independent across time777That is, a demand with independent of for all , case in which

| (9) |

for each , where we use

| (10) |

to represent the (own or cross-time) price elasticity of demand at time with respect to the price at time . The latter result resembles the (second-best optimal) ex-ante two-part tariff derived in [14, Sec. 3] for the single period case ()888Which also applies to the continuous time case where , the demand and prices are deterministic, and demand is independent across time..

The expression (8) for the optimal connection charge also has an intuitive interpretation. The first term corresponds to a uniform contribution towards the retailer’s target . And, the second term corresponds to a uniform preallocation of the surplus that the retailer expects to collect from the volumetric charge , , which—as noticeable from (5)—may be positive or negative in general.

To gain additional insights into these results, we have the following corollary.

Corollary 1.

If and are uncorrelated, then and .

Corollary 1 indicates that has a very simple and appealing structure that resembles the result for the deterministic case where and . Note that the assumption made in Corollary 1 is valid for many situations. It is certainly true for demands that are not much affected by consumers’ local randomness999More precisely, this assumption is satisfied by demands whose sensitivity to prices depends on the customers’ set of appliances and idiosyncratic preferences rather than on random exogenous factors affecting the wholesale prices, such as random temperature fluctuations., such as the charging of electric vehicles and typical household appliances. Even for loads from smart HVAC systems that are affected by random temperature fluctuations, the assumption in Corollary 1 holds because the demand function takes the form [26].

As for the simpler structure of , it may not be surprising since the efficiency of marginal cost pricing (i.e., ) is a classical result for the deterministic case [3, Sec. 4.5][14]. Intuitively, marginal cost pricing is efficient because it induces customers to increase consumption until the derived marginal benefit matches the marginal cost of procuring electricity.

The expression for in Corollary 1 also has an intuitive interpretation. While the first term remains unchanged from (8), the second term becomes a risk premium associated to the cross-correlation that the demand and the RTP may exhibit. When such cross-correlation is positive (as in practice [30]), the retailer is likely to face additional variable costs since the expected variable cost is larger than the variable revenue . Intuitively, this fee represents a uniform risk premium that customers pay to face a deterministic price rather than the volatile RTP. Presumably, the inter-customer cross-subsidies arising from the uniform allocation of this risk premium are negligible compared to the differences. However, the integration of behind-the-meter renewables could make these cross-subsidies worth adjusting, for example, through the use of discriminatory connection charges consistent with the cost-causation principle described in [31]. A discussion on cross-subsidies is held in Part II [MunozTong16partII].

III-B Structure of the Optimal Linear Tariff

A tariff of the form —a linear tariff—is an ex-ante two-part tariff with no connection charge. While such purely volumetric tariff may be simpler, it has two fundamental disadvantages. First, a closed form expression of the optimal linear tariff is not available under general assumptions. Second, such restriction introduces a fundamental trade-off between the retailer surplus target and the attainable social welfare. These drawbacks are noticeable in Theorem 2 and Corollary 3, respectively.

When restricted to linear tariffs, a unique solution to problem (6) can be obtained due to Assumption 1. We characterize the optimal solution in the following result.

Theorem 2.

(Optimal linear tariff) Consider the regime where is large, i.e., . If feasible, the linear tariff that solves problem (6) is characterized by

| (11) |

or, equivalently, by

| (12) |

where , the Lagrange multiplier of (6), satisfies and is such that . In this regime of , the problem is feasible if and only if , where is the price that maximizes over , which matches as .

In Theorem 2, expression (11) reveals that the structure of the optimal linear tariff is characterized by a period-specific price markup relative to the price of the optimal two-part tariff . The scalar , often called the Ramsey number, adjusts markups in all periods uniformly to the point where the expected retailer surplus matches the target . A closer examination of (11), which can be rewritten as (12), shows that the own and cross price elasticities of demand determine altogether the markup for each period within the billing cycle.

To understand (12), it is informative to consider the case where the demand is independent across time, namely, for . In this case, the product of the markup and the own-price elasticity remains constant in time and equal to the Ramsey number. This means that periods with inelastic demands get high markups and periods with elastic demands get low markups. For this reason, this pricing rule is known in economics as the inverse elasticity rule [3, Sec. 3.3].

Even simpler is the single period case, also derived in [14, Sec. 3]. Notably, when , the scalar price can be obtained directly from the constraint , and it must be set so that it pays for the average total cost of the procured electricity, i.e., .

A specialized application of this result was developed in [26], where a model for TCLs under a day-ahead hourly pricing scheme was considered. In this case, the demand function for each consumer is linear and the surplus function is quadratic [26]. The aggregated demand is therefore also linear. The consumers as a collective have a quadratic aggregated surplus [26]. Specifically,

| (13) | ||||

| (14) |

where is deterministic, positive definite (and symmetric). Letting and and applying Theorem 2 readily yields

| (15) |

where induces and is the Ramsey number, which is set so that . Intuitively, varies within inducing prices that vary between and the profit-maximizing price as varies between and the maximum profit .

III-C Tariff Performance Comparison

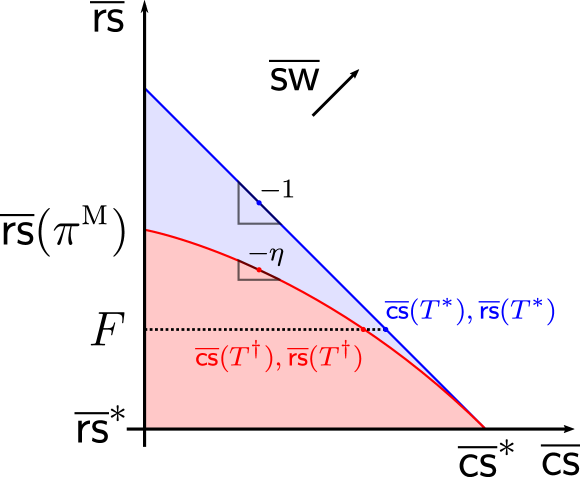

We now discuss the performance of the derived tariffs in terms of social welfare (expected total surplus) leveraging the graphical representation provided in Fig. 1. Therein, a Pareto front for each tariff illustrates the expected CS and SW induced by the tariff for different RS targets . On one hand, Theorem 1 has the following implication.

Corollary 2.

As a tariff parametrized by , the two-part tariff induces an expected total surplus that is independent of and .

In Corollary 2, denotes the constant SW attained by the price , where . Implicit in this result is that for any affine tariff one can check that

| (16) |

depends on but not on . Corollary 2 thus implies that under the tariff , collecting additional revenue from customers to cover larger fixed costs embedded in reduces consumer welfare but does not compromise social welfare. This “iso-efficient” trade-off between retailer and consumer surplus is illustrated in Fig. 1 with a linear Pareto front with negative and unitary slope in the - plane. Intuitively, suboptimal two-part tariffs101010As the ones currently used by most utilities in the U.S., due in part to additional bill stability and alleged equity concerns imposed by regulators. can achieve any point in the - plane in the shaded area below the linear Pareto front in Fig. 1, but no ex-ante two-part tariff can achieve points above this front.

Theorem 2, on the other hand, has a analogous implication.

Corollary 3.

The quantities and induced by as a tariff parametrized by are decreasing and concave in with and for .

Corollary 3 reveals that, unlike the tariff , the optimal linear tariff compromises not only consumer welfare but also social welfare when collecting additional revenue from customers is required to cover larger fixed costs embedded in . This trade-off is depicted in Fig. 1 with a decreasing and concave Pareto front in the - plane that bends away from the efficiency level attained by the tariff as increases from until it reaches . As before, suboptimal linear tariffs can achieve any point in the shaded area below the curved Pareto front in Fig. 1, but no ex-ante linear tariff can achieve points above this front.

From the previous analysis, it is clear that two-part tariffs dominate linear tariffs in terms of expected consumer surplus in the regime of practical relevance where . A natural question to ask is whether two-part tariffs can be dominated by more complex nonlinear ex-ante tariffs. We now argue that, under certain sufficient condition, the two-part tariff is indeed optimal for the regulator’s problem (6) among all ex-ante arbitrary tariffs. To establish such result it suffices to show that induces the same expected consumer surplus that would be achieved by a social planner who makes consumption decisions on behalf of customers with the unconstrained objective of maximizing the expected total surplus. This is because the social planner’s problem provides a trivial upper bound to the regulator’s problem.

Because we are interested in comparing ex-ante tariffs only, the social planner’s problem should incorporate such implicit restriction. The restriction to ex-ante tariffs translates into a restriction for the social planner to use only the information observable by each customer when choosing their consumption, namely their local state . Hence, the social planner’s problem can be stated as

| (17) |

where the expectation is taken with respect to , and is causally contingent on (i.e., adapted to) the local state . Finally, under the assumption that each and are independent, we show that the optimal solution to (17) is , which matches the demand induced by the optimal two-part tariff. This result and the implied optimality of are summarized in the following Theorem.

Theorem 3.

If (A2) the wholesale RTP and the local state of each customer are statistically independent, then the two-part tariff is an optimal solution of (6) among all arbitrary tariffs with the same lag time.

Theorem 3 indicates that the restriction to two-part tariffs may imply no loss of generality. This applies—less generally than Corollary 1—for demands that are not affected by consumers’ local randomness111111In other words, demands that, given a retail price vector , are independent from random exogenous factors affecting the wholesale prices ., such as washers and dryers, computers, and the charging of electric vehicles. For all the other cases, where the sufficient condition (A2) does not hold, Theorem 3 sheds lights on the performance of the optimal ex-ante two-part tariff . While it is clear that the ex-ante restriction entails some efficiency loss when (A2) is not satisfied121212This is because relaxing the ex-ante restriction enables the use of the ex-post two-part tariff which trivially achieves the maximum social welfare a social planner could achieve (first-best)., it is not clear whether the restriction to two-part tariffs does entail efficiency losses. In other words, is there a necessary condition for to be an optimal solution of (6)?

IV Numerical Example

We now estimate the performance of the optimal linear and two-part day-ahead tariffs in a practical setting. Using publicly available data from ConEdison (New York City’s largest utility) and NYISO for the 2015 Summer season, we estimate the average daily gains in consumer surplus that both tariffs would have brought relative to the utility’s default two-part tariff with flat rate. Here we assume a linear demand model (13)-(14) and day-ahead linear and two-part tariffs.

The utility’s monthly residential energy sales131313For June through August 2015, which can be found in the EIA-826 database at http://www.eia.gov/electricity/data/eia826/. and an estimated residential hourly load profile141414For a residential building in NYC, available in the NREL OpenEI building load database http://en.openei.org/datasets/files/961/pub/. The location/model with ID 725033-TMY3-BASE was used. were used to obtain ( days hr) aggregate hourly consumption data points. We used these points as iid realizations of the random vector , where is ConEdison’s flat rate151515NYC’s residential default flat rate during Jun-Aug 2015 was cents/kWh ( of which correspond to supply charges and to delivery charges). Available at http://www.coned.com/rates/supply_charges.asp and http://www.coned.com/documents/elecPSC10/SCs.pdf., to fit and then to estimate . Due to the its low-dimensional structure, fitting can be reduced to determining a scaling parameter after assuming certain own-price elasticity of demand at 161616This is facilitated by assuming a homogeneous thermal parameter across customers, which implies some loss of customer heterogeneity. See [26] for details of the model, where is used in a case study.

where denotes the sample mean of . While here we assume a value of , which is a reasonable estimate of the short-term own-price elasticity of electricity demand [33], a sensitivity analysis over is presented in [34]. We further assumed a total of million of residential customers and used ConEdison’s default residential connection charge, which amounts to $/day, to roughly estimate the utility’s average daily revenue from residential customers as or million USD. As for the prices , we used the day-ahead prices for NYC as iid realizations to estimate and with sample mean and covariance estimators.

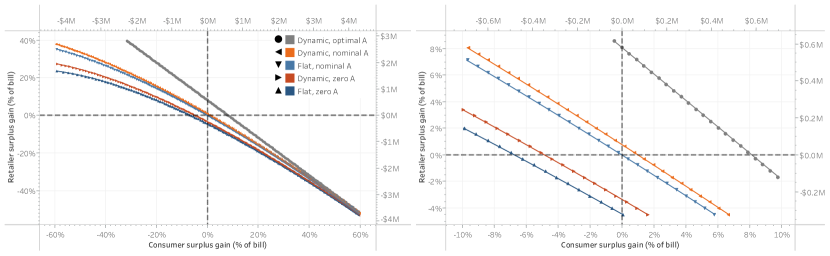

We plot in Fig. 2(a) the Pareto fronts

| (18) |

induced by the optimal linear and two-part tariffs and three other relevant tariffs that satisfy the revenue sufficiency constraint: an optimized linear flat tariff with rate , an optimized two-part tariff with fixed connection charge and rate , and an optimized two-part flat tariff with fixed connection charge and rate . The latter can be thought as ConEdison’s adjusted tariff. In (18), and denote the surplus gains (losses if negative) relative to the corresponding surplus achieved by . For instance, for the optimal two-part tariff .

Fig. 2(a) compares the tariffs’ performances in consumer surplus gains for different retail surplus targets. At ConEdison’s estimated net revenue level , which corresponds to , significant performance differences can be observed among the computed tariffs. These differences are more evident in Fig. 2(b), which magnifies Fig. 2(a) around the origin. Due to its nonzero connection charge, ConEdison’s tariff clearly outperforms the tariffs without connection charges, but is outperformed by the other tariffs with connection charges, which are further optimized. It is particularly interesting that switching to the optimal linear tariff would bring loses in CS ( or k USD/day). Namely, by virtue of a connection charge, even a simple flat tariff can outperform a fairly sophisticated day-ahead hourly volumetric tariff. Moreover, fully optimizing ConEdison’s rate (but not its connection charge) brings rather limited CS gains ( or k USD/day). However, switching to the optimal two-part tariff would bring significant gains in CS ( or k USD/day). This corroborates how effective connection charges can be at increasing the retailer surplus without sacrificing economic efficiency. This optimal two-part tariff, which features a connection charge of $/day or nearly $/month, induces bill reductions for customers larger than the average customer and bill increments for all other customers. Clearly, such charges may be politically unacceptable for low-income customers and may require cross-subsidized reduced tariffs, which have been an industry standard [3, Sec. 7.4].

V Conclusions

In this first part, we derive consumer-welfare-maximizing, revenue adequate, and ex-ante linear and two-part dynamic tariffs from the perspective of a regulated retailer. This initial analysis is for the case without renewables or storage in the distribution system. Our results generalize previous works by deriving said tariffs for a stochastic and multi-period demand model with intertemporal dependencies and a predetermined lag time between the announcement of the tariff and the beginning of the billing period. We established that if the wholesale prices and each customer’s consumption are statistically independent, then the optimal two-part tariff is optimal among the class of arbitrary tariffs with the same lag time.

While the optimal two-part tariff mitigates inefficiencies induced by the optimal linear tariff, inequity concerns inconsistent with cost causation arise from the structure of the connection charge. These concerns may become significant with the sparse adoption of behind-the-meter renewables. While tariff design criteria beyond efficiency and revenue adequacy are out of the scope of our work, it is worth mentioning that allowing discriminatory connection charges can give flexibility to the regulator to achieve different objectives (such as inter-customer cost-causation equity) and provide effective long-term signals (e.g., location within the distribution network and investment in on-site generation) [31].

References

- [1] Greentech Media (GTM), “Evolution of the grid edge: Pathways to transformation,” White paper, 2015. [Online]. Available: https://www.greentechmedia.com

- [2] Rocky Mountain Institute, “The economics of load defection,” Tech. Rep., 2015. [Online]. Available: http://www.rmi.org/

- [3] S. J. Brown and D. S. Sibley, The theory of public utility pricing. Cambridge University Press, 1986.

- [4] P. L. Joskow and C. D. Wolfram, “Dynamic pricing of electricity,” The American Economic Review, vol. 102, no. 3, pp. 381–385, 2012.

- [5] S. Braithwait, D. Hansen, and M. O’Sheasy, “Retail electricity pricing and rate design in evolving markets,” Edison Electric Institute, Tech. Rep. July, 2007.

- [6] L. Wood, J. Howat, R. Cavanagh, and S. Borenstein, “Recovery of utility fixed costs: Utility, consumer, environmental and economist perspectives,” LBNL, Tech. Rep., 2016.

- [7] S. Borenstein. (2014) What’s so great about fixed charges? Energy Institute at HAAS Blog. [Online]. Available: https://energyathaas.wordpress.com

- [8] R. Deng, Z. Yang, M.-Y. Chow, and J. Chen, “A Survey on Demand Response in Smart Grids: Mathematical Models and Approaches,” Industrial Informatics, IEEE Trans. on, vol. 11, no. 3, pp. 1–1, 2015.

- [9] J. S. Vardakas, N. Zorba, and C. V. Verikoukis, “A Survey on Demand Response Programs in Smart Grids: Pricing Methods and Optimization Algorithms,” Communications Surveys & Tutorials, IEEE, vol. 17, no. 1, pp. 152–178, jan 2015.

- [10] A. Faruqui, R. Hledik, and J. Palmer, “Time-Varying and Dynamic Rate Design,” The Brattle Group, Tech. Rep. July, 2012.

- [11] S. Borenstein, M. Jaske, and A. Rosenfeld, “Dynamic pricing, advanced metering, and demand response in electricity markets,” Center for the Study of Energy Markets, Tech. Rep., 2002.

- [12] S. Borenstein, “The long-run efficiency of real-time electricity pricing,” Energy Journal, vol. 26, no. 3, pp. 93–116, 2005.

- [13] S. Borenstein and S. Holland, “On the efficiency of competitive electricity markets with time-invariant retail prices,” The Rand Journal of Economics, vol. 36, no. 3, p. 469, 2005.

- [14] P. Joskow and J. Tirole, “Retail electricity competition,” The RAND Journal of Economics, vol. 37, no. 4, pp. 799–815, 2006.

- [15] A. H. Mohsenian-Rad and A. Leon-Garcia, “Optimal residential load control with price prediction in real-time electricity pricing environments,” Smart Grids, IEEE Trans. on, vol. 1, no. 2, pp. 120–133, 2010.

- [16] A. H. Mohsenian-Rad, V. W. S. Wong, J. Jatskevich, R. Schober, and A. Leon-Garcia, “Autonomous demand-side management based on game-theoretic energy consumption scheduling for the future smart grid,” Smart Grid, IEEE Trans. on, vol. 1, no. 3, pp. 320–331, 2010.

- [17] B. Daryanian, R. Bohn, and R. Tabors, “Optimal demand-side response to electricity spot prices for storage-type customers,” Power Systems, IEEE Trans. on, vol. 4, no. 3, 1989.

- [18] S. Shao, M. Pipattanasomporn, and S. Rahman, “Demand response as a load shaping tool in an intelligent grid with electric vehicles,” Smart Grid, IEEE Trans. on, vol. 2, no. 4, pp. 624–631, 2011.

- [19] J. L. Mathieu, M. Kamgarpour, J. Lygeros, G. Andersson, and D. S. Callaway, “Arbitraging intraday wholesale energy market prices with aggregations of thermostatic loads,” Power Systems, IEEE Trans. on, vol. 30, no. 2, pp. 763–772, 2015.

- [20] S. Li, W. Zhang, J. Lian, and K. Kalsi, “Market-based coordination of thermostatically controlled loads–Part I: A mechanism design formulation,” Power Systems, IEEE Trans. on, vol. 31, no. 2, 2016.

- [21] L. Chen, N. Li, L. Jiang, and S. H. Low, “Optimal demand response: problem formulation and deterministic case,” in Control and optimization methods for electric smart grids. Springer, 2012, ch. 3, pp. 63–85.

- [22] C. Li, S. Tang, Y. Cao, Y. Xu, Y. Li, J. Li, and R. Zhang, “A New Stepwise Power Tariff Model and Its Application for Residential Consumers in Regulated Electricity Markets,” Power Systems, IEEE Trans. on, vol. 28, no. 1, pp. 300–308, 2013.

- [23] P. Yang, G. Tang, and A. Nehorai, “A game-theoretic approach for optimal time-of-use electricity pricing,” Power Systems, IEEE Trans. on, vol. 28, no. 2, pp. 884–892, 2013.

- [24] F.-L. Meng and X.-J. Zeng, “A Stackelberg game-theoretic approach to optimal real-time pricing for the smart grid,” Soft Computing, vol. 17, no. 12, pp. 2365–2380, 2013.

- [25] M. T. Bina and D. Ahmadi, “Stochastic Modeling for the Next Day Domestic Demand Response Applications,” Power Systems, IEEE Trans. on, vol. 30, no. 6, pp. 2880–2893, 2015.

- [26] L. Jia and L. Tong, “Dynamic pricing and distributed energy management for demand response,” Smart Grid, IEEE Trans. on, vol. 7, 2016, earlier arXiv version: http://arxiv.org/abs/1601.02319.

- [27] D. Munoz-Alvarez and L. Tong, “Distributed renewables and storage and the efficiency of connection charges,” in Information Theory and Applications Workshop (ITA), 2016, pp. 1–6. [Online]. Available: http://ita.ucsd.edu/workshop/16/files/paper/paper_4289.pdf

- [28] M. A. Crew, C. S. Fernando, and P. R. Kleindorfer, “The theory of peak-load pricing: A survey,” Journal of Regulatory Economics, vol. 8, no. 3, pp. 215–248, nov 1995.

- [29] I. Aguirre, S. Cowan, and J. Vickers, “Monopoly price discrimination and demand curvature,” American Economic Review, vol. 100, no. 4, pp. 1601–1615, 2010.

- [30] M. Burger, B. Graeber, and G. Schindlmayr, Managing Energy Risk: An Integrated View on Power and Other Energy Markets, ser. The Wiley Finance Series. John Wiley & Sons, 2007, vol. 425.

- [31] I. J. Pérez-Arriaga and Y. Smeers, “Guidelines on Tariff Setting,” in Transport Pricing of Electricity Networks. Springer US, 2003, no. l, pp. 175–203.

- [32] D. Munoz-Alvarez and L. Tong, “On the Efficiency of Dynamic Retail Tariffs with Connection Charges—Part II: Distributed Renewable and Storage Resources,” ArXiv Preprint, 2017.

- [33] Electric Power Research Institute (EPRI), “Price Elasticity of Demand for Electricity : A Primer and Synthesis,” Tech. Rep., 2008.

- [34] D. Muñoz-Álvarez, “Regulatory approaches to the integration of renewable and storage resources into electricity markets,” Ph.D. dissertation, Cornell University, 2017.

Proof of Theorem 1

Solving in (6) for and substituting in the objective yields the expression

Differentiating the objective over yields

| (19) |

where the second equality follows from Prop. 2 below. Now, the assumption that each is negative definite implies that is invertible. Hence, one can rewrite the necessary first-order condition (FOC), which is obtained from equating , as (7). Given the expression (7) for , (8) can be obtained by solving the equality constraint for . Lastly, these FOC are sufficient for the optimality of since is strictly concave in according to Prop. 4.

Proposition 1.

For each , satisfies

| (20) |

where the conditional expectation is taken over conditioned on .

Proof.

(20) are FOCs of customer ’s multi-stage decision problem (1) of sequentially choosing contingent on the so-far observed local states to maximize his expected net utility or surplus, i.e.,

| (21) |

given a tariff known in advance (ex-ante). Hence, the optimal solution of (21) must satisfy these necessary optimality conditions.

Each of these stationarity (KKT) FOCs is obtained by differentiating the objective in (21) with respect to and equating the result to zero. To see that, note that for each time one can use the law of total expectation to rewrite the objective in terms of an expectation conditioned on the information observed up to , i.e.,

The FOC in (20) follows since .

Proposition 2.

satisfies the equation

| (22) |

where the expectations are taken over .

Proof.

We establish this vectorial identity proving each component separately. Assuming the differentiation and expectation operators can be exchanged, we apply the chain rule to the -th component of the left-hand-side of (22) yielding the following sequence of equalities

where the second equality follows from the law of total expectation, the third equality is due to the causality of , and the last equality is due to Prop. 1. The identity (22) readily follows.

Proposition 3.

For any affine tariff , is strictly convex and (componentwise) decreasing in .

Proof.

Differentiating with respect to (using the chain rule) and leveraging on the expression (22) from Prop. 2 one readily obtains Because is nonnegative, the expression above implies that is componentwise decreasing . Moreover, we have that

| (23) |

Recall that a function is strictly convex (over a convex domain) if its Hessian is positive definite (over said domain). Hence, the strict convexity of in readily follows from the assumed negative definiteness of each matrix .

Proposition 4.

Consider an affine tariff . If Assumption 1 holds then and the weighted surplus are strictly concave in for any .

Proof.

First, we differentiate twice with respect to . Using Prop. 2 and some algebra one obtains the Hessian

| (24) |

Recall that a function is strictly concave (over a convex domain) if its Hessian is negative definite (over said domain). Hence, the assumed negative definiteness of and of (Assumption 1) readily imply the negative definiteness of and thus the strict concavity of in .

Proof of Corollary 1

-1 Proof of Corollary 2

Leveraging on (2) and (4), the expected total surplus induced by the tariff characterized in Thm. 1 can be written as

Clearly, is a function of but not of or . It remains to show that does not depend on . But the FOC characterizing is obtained by differentiating with respect to and equating it to zero. It follows that does not on . Moreover, since must hold at optimality, it readily follows that

-2 Proof of Theorem 2

Consider the Lagrangian of problem (6)

| (25) |

where is the multiplier of the equality constraint. Differentiating over yields

| (26) |

where we use Prop. 2 to obtain the second equality. The necessary FOC in (11) follows from equating (26) to zero after some algebra. These operations use the negative definiteness and thus invertibility of the matrix and the expression for in (7) (Thm. 1).

The expressions in (12) characterizing componentwise can be obtained from (11) after some algebraic manipulations using the definition of price elasticity in (10). In particular, subtracting from both sides of (11) and left-multiplying by one obtains

Componentwise, for each , we have

As for the last statement of the theorem, consider that maximizing (or equivalently ) over yields the related stationarity FOC

| (27) |

This condition, which is similar to (11), characterizes the unregulated monopoly price . Indeed, (27) can be obtained from (11) by replacing by , or equivalently, by letting on both sides of (11).

Now, because maximizes and over , there does not exist such that . Hence, when restricted to linear tariffs, problem (6) is infeasible for all . For all the other values of within the considered regime, i.e., , the fact that and achieve and , respectively, and the concavity of (Prop. 4) imply the feasibility of problem (6) over said interval of . Concluding, in the regime , problem (6) over linear tariffs is feasible if and unfeasible otherwise.

-3 Proof of Corollary 3

At optimality, we have that and thus . The envelope theorem further implies that the derivative of the value function of problem (6) with respect to the parameter can be computed as . The total derivative of the expected total surplus with respect to is then . Hence, to show that and are decreasing and concave functions of over , it suffices to show that , as a function of , satisfies and over .

Moreover, it is clear from the Lagreangian in (25) that must be a decreasing function of the parameter . Conversely, the constraint implies that is a strictly increasing function of . Hence, we have that increases as increases, and thus .

-4 Proof of Theorem 3

We prove this result by showing that the optimal two-part tariff characterized by Theorem 1 attains an upper bound for the performance of all ex-ante tariffs. This upper bound is the performance achieved by a social planner who directly makes all decisions on behalf of consumers. The social planner is unlike the regulator who is limited to coordinate such decisions indirectly through a tariff. To obtain a tight upper bound for ex-ante tariffs only (rather than a looser bound for all possibly ex-post tariffs), the social planner makes customers’ decisions relying only on the information observable by each of them (i.e., ) as opposed to based on global information (e.g., ).

Consider the social planner’s problem in (17), which corresponds to the regulator’s problem (6) in the absence of any DERs. Therein, the notation indicates the restriction of the social planner to make (causal) decisions contingent only on the local state of each customer . Recall from (1) that the expected consumer surplus for a given ex-ante tariff is given by , where

and the corresponding expected retailer surplus is given by

and the expected total surplus by

The following sequence of equalities/inequalities shows that problem (17) provides an upper bound to problem (6).

| (28) | ||||

| (29) | ||||

| (30) |

In particular, the inequality in (29) holds because depends on only through . This implies that maximizing directly over rather than indirectly over is a relaxation of the optimization in (28). Clearly, the problem in (29) corresponds to the social planner’s problem in (30) and (17).

It suffices to show now that attains the upper bound in (30). To that end, we use the independence sufficient condition . We show that, under said condition, the expected total surplus matches the upper bound. First note that the condition allows to rewrite the upper bound in (29) and (30) as follows.

The last equality follows from the definition of the demand function in (3) as the optimal response of customers to deterministic prices.

The result follows since the tariff induces the same expected total surplus if , i.e.,