Variations on branching methods for non linear PDEs

Abstract

The branching methods developed in [9], [11] are effective methods to solve some semi linear PDEs and are shown numerically to be able to solve some full non linear PDEs. These methods are however restricted to some small coefficients in the PDE and small maturities. This article shows numerically that these methods can be adapted to solve the problems with longer maturities in the semi-linear case by using a new derivation scheme and some nested method. As for the case of full non linear PDEs, we introduce new schemes and we show numerically that they provide an effective alternative to the schemes previously developed.

1 Introduction

The resolution of low dimensional non linear PDEs is often achieved by some deterministic methods such as finite difference schemes, finite elements and finite volume. Due the curse of dimensionality, these methods cannot be used in dimension greater than three : both the computer time and the memory required are too large even for supercomputers. In the recent years the probabilistic community has developed some representation of semi linear PDE:

| (1.1) |

by means of backward stochastic differential equations (BSDE), as introduced by [13]. Numerical Monte Carlo algorithms have been developed to solve efficiently these BSDE by [2], [14]. The representation of the following full non linear PDE:

| (1.2) |

has been given by the mean of second order backward stochastic differential equation (SOBSDE) by [4].

A numerical algorithm developed by [6] has been derived to solve these full non linear PDE by the mean of SOBSEs.

The BSDE and SOBSDE schemes developed rely on the approximation of conditional expectation and the most effective implementation is based on regression methods as developed in [8], [12].

These regression methods develop an approximation of conditional expectations based on an expansion on basis functions. The size of this expansion has to grow exponentially with the dimension of the problem so we have to face again the curse of dimensionality.

Notice that the BSDE methodology could be used in dimension 4 or 5 as regressions has been successfully used in dimension 6 in [3] using some local regression function.

Recently a new representation of semi linear equations (1.1) for a polynomial function of and has been given by [9] : this representation

uses the automatic differentiation approximation as used in [7], [1], [10], and [5].

The authors have shown that the representation gives a finite variance estimator only for small maturities or small non linearities and numerical examples until dimension 10 are given. Besides, they have shown that the given scheme using Malliavin weights cannot be used to solve the full non linear equation (1.2).

[11] have introduced a re-normalization technique improving numerically the convergence of the scheme diminishing the variance observed for the semi linear case. Besides, the authors haved introduced a scheme to solve the full non linear equation (1.2). Without proof of convergence they numerically have shown that the developed scheme is effective.

The aim of the paper is to provide some numerical variation on the algorithm developed in [9, 11].

In a first part we will show, with simple ideas, that it is possible to deal with longer maturities than the ones possible with the initial algorithm.

In a second part we give some alternative schemes to the one proposed in [11] and, testing them on some numerical examples, we show that they are superior than the scheme previously developed.

In the numerical results presented in the article, all errors are estimated as the of the standard deviation observed divided by the square root of the number of particles used and these errors are plotted as a function of the of the number of particles used. As our methods are pure Monte Carlo methods we expect to have lines with slope when the numerical variance is bounded.

2 The Semi Linear case

Let be some constant non-degenerate matrix, be some constant vector , and bounded Lipschitz functions, we consider the semi linear parabolic PDE:

| (2.1) |

with terminal condition where for two matrices , .

When is a polynomial in in the form

for some , , where is a sequence of valued bounded continuous functions defined on , and is a sequence of bounded continuous functions defined on . [9] obtained a probabilistic representation to the above PDE by branching diffusion processes under some technical conditions. In the sequel, we simplify the setting by taking as a constant (in , ) plus a monomial in , , :

| (2.2) |

for some , where is a sequence of valued bounded continuous function defined on , supposing that , and is a bounded continuous function defined on . We note .

Remark 2.1.

The case with a general polynomial only complexifies the notation : it can be simply treated as in [9] by introducing some probability mass function (i.e. and ) that are used to select with monomial to consider during the branching procedure. Another approach can be used : instead of sampling the monomial to use, it is possible to consider successively all terms of the but this doesn’t give a representation as nice as the one in [9].

2.1 Variation on the original scheme of [9]

In this section we present the original scheme of [9] and explain how to diminish the variance increase the maturities of the problem.

2.1.1 The branching process

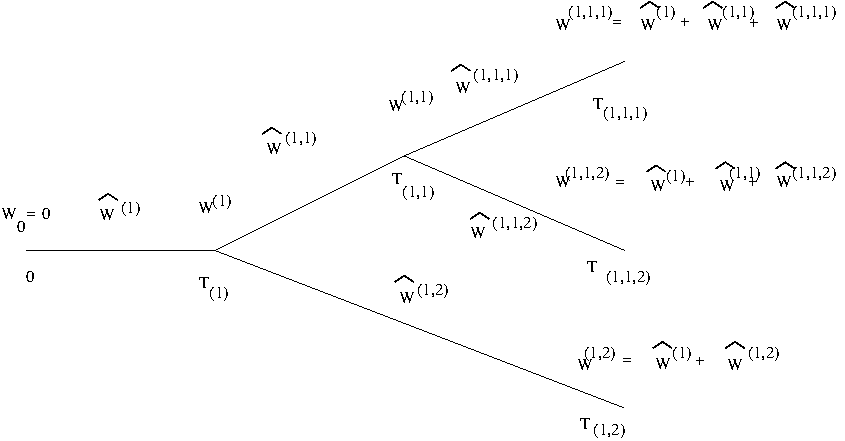

Let us first introduce a branching process with arrival time of distribution density function . At the arrival time, the particle branches into offsprings.

We introduce a sequence of i.i.d. positive random variables with all the values , for .

We construct an age-dependent branching process using the following procedure :

-

1.

We start from a particle marked by , indexed by , of generation , whose arrival time is given by .

-

2.

Let be a particle of generation , with arrival time that branches into offspring particles noted for . We define the set of its offspring particles by

We first mark the particles by 0, the next by 1 , and so on, so that each particle has a mark for .

-

3.

For a particle of generation , we denote by the “parent” particle of , and the arrival time of is given by . Let us denote .

-

4.

In particular, for a particle of generation , and is its birth time and also the arrival time of . Moreover, for the initial particle , one has , and .

We denote further

and also

Clearly, (resp. ) denotes the set of all living particles (resp. of generation ) in the system at time ,

and (resp. ) denotes the set of all particles (resp. of generation ) being alive at or before time .

We next equip each particle with a Brownian motion in order to define a branching Brownian motion. Let be a sequence of independent -dimensional Brownian motion, which is also independent of . Define for all and then for each , define

| (2.3) |

Then is a branching Brownian motion.

2.1.2 The original algorithm

Let us denote . Denoting for all and and by the expectation operator conditional on the starting data at time , we obtain from the Feynman-Kac formula the representation of the solution of equation (2.1) as:

| (2.4) |

where , and

| (2.5) |

On the event , using the independence of the we are left to calculate

| (2.6) |

Using differentiation with respect to the heat kernel, i.e. the marginal density of the Brownian motion we get :

| (2.7) |

Using equations (2.4) and (2.1.2) recursively and the tower property , we get the following representation

| (2.8) |

where is given by the backward recursion : let for every , then let

| (2.9) |

where

| (2.10) |

and we have used that .

This backward representation is slightly different from the elegant representation introduced in [9].

Clearly on our case the variance of the method used will be lower than with the representation in [9] for a similar computational cost.

In the case where the operator is linear and a function of the gradient (, and ) using the arguments in [5] it can be easily seen by conditioning with respect to the number of branching that equation (2.8) is of finite variance if as with .

When follows for example a gamma law with parameters and , the finite variance is proved as soon as for PDE coefficients and maturities small enough.

In the non linear case, [9] have shown that the variance is in fact finite for maturities small enough and small coefficients as soon as but numerical results show that is optimal in term of efficiency: for a given the numerical variance is nearly the same for the values of between 0.4 and 0.5 but a higher value limits the number of branching thus meaning a smaller computational cost.

2.1.3 Variation on the original scheme

As indicated in the introduction, the method is restricted to small maturities or small non linearities.

Having a given non linearity we are interested in adapting the methodology in order to be able to treat longer maturities. A simple idea consists in noting that the Monte Carlo method is applied by sampling the conditional expectation for appearing in equation (2.1.2) only once. Using nested Monte Carlo, so by sampling each term of equation (2.1.2) more that one time

one can expect a reduction in the variance observed. A nested method of order is defined as a method using sampling to estimate each function or at each branching.

Of course the computational time will grow exponentially with the number of samples taken and for example

trying to use a gamma law with a non linearity of Burger’s type with is very costly: due to the high values of the density near , trajectories can have many branching.

Some different strategies have been tested to be able to use this technique :

-

•

A first possibility consists in trying to re-sample more at the beginning of the resolution and decreasing the number of samples as time goes by or as the number of branching increases. The methodology works slightly better than a re-sampling with a constant number of particles but has to be adapted to each maturity and each case so it has been given up.

-

•

Another observation is that the gamma law is only necessary to treat the gradient term: so it is possible to use two laws: a first one, an exponential law, will be used to estimate the function while an gamma law will be used for the terms. This second technique is the most effective and is used for the results obtained in the section.

For a given dimension , we take , ,

where and

With terminal condition , the explicit solution of semi linear PDE (2.1) is given by

Our goal is to estimate at , .

This test case will be noted test A in the sequel.

We use the nested algorithm with two distributions for :

-

•

an exponential law with density with to calculate the terms,

-

•

a gamma distribution with

and the parameters , to calculate the terms.

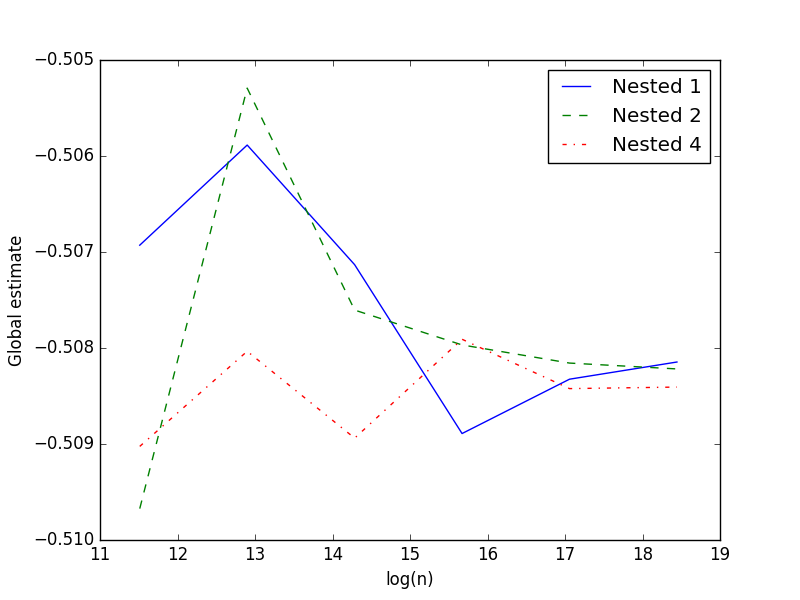

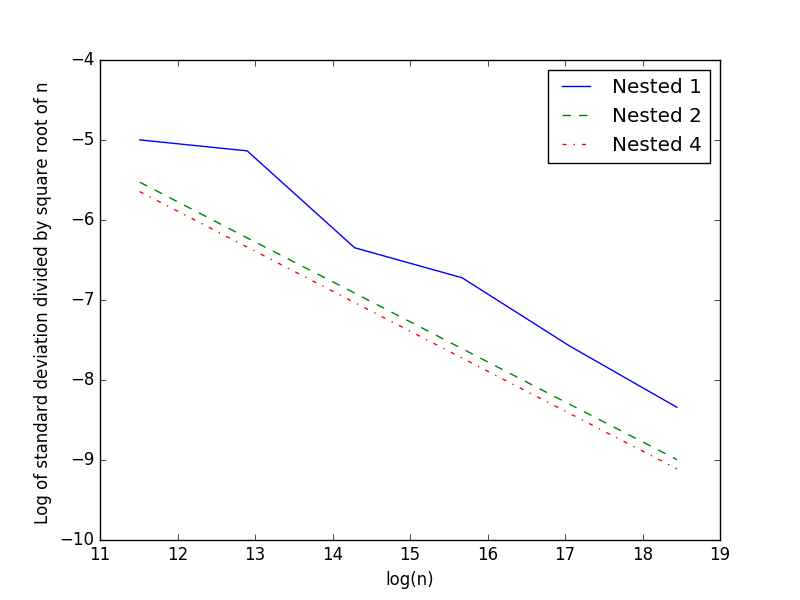

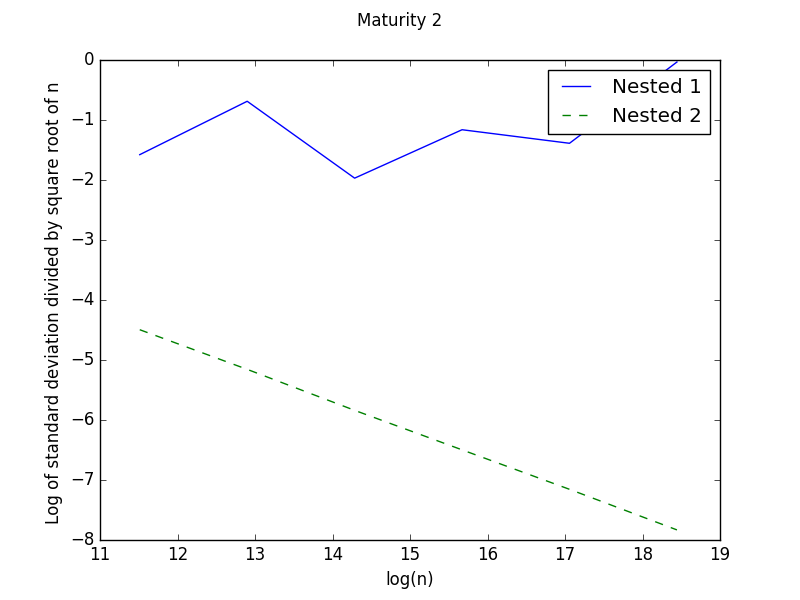

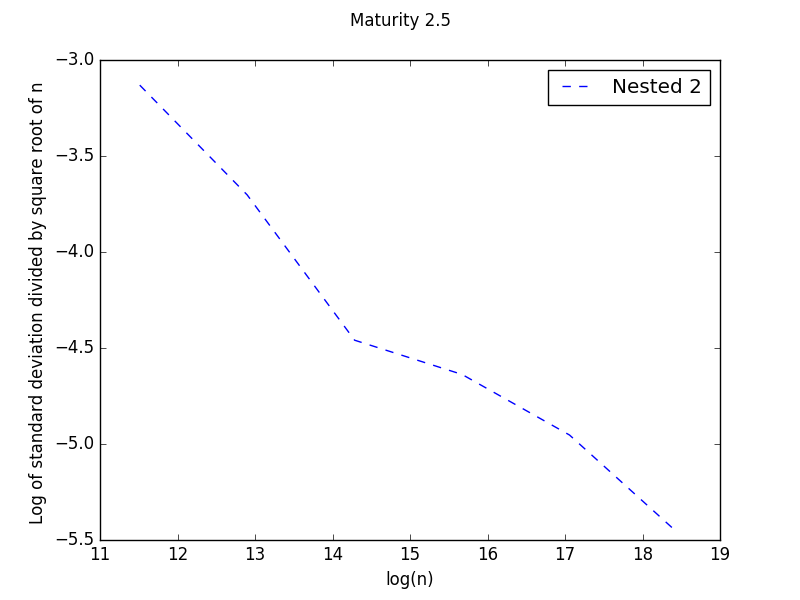

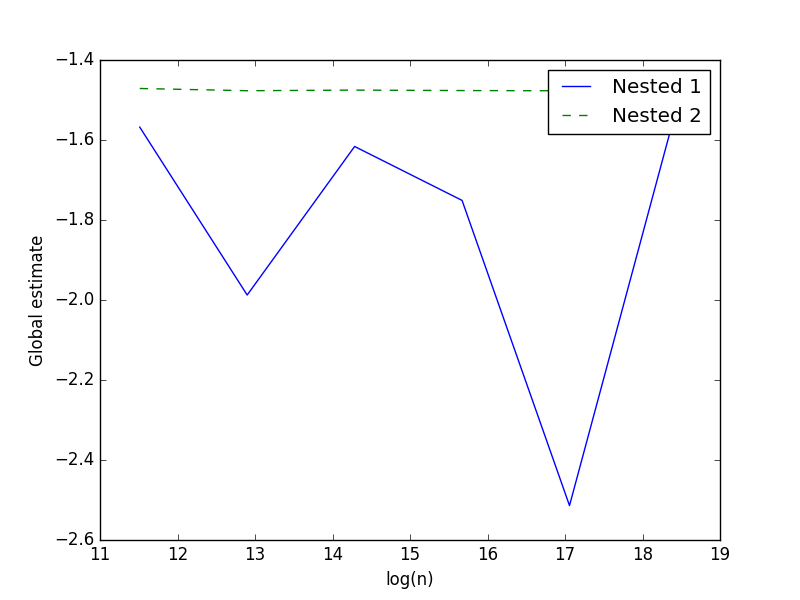

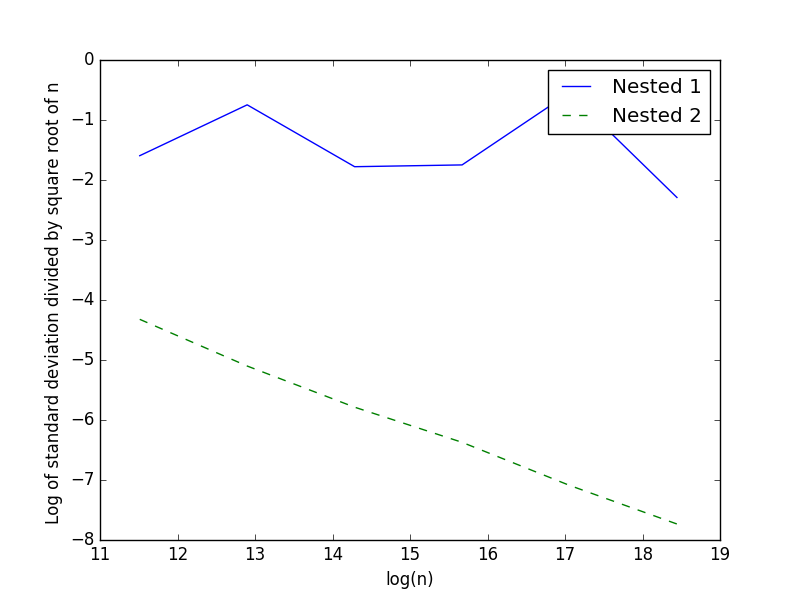

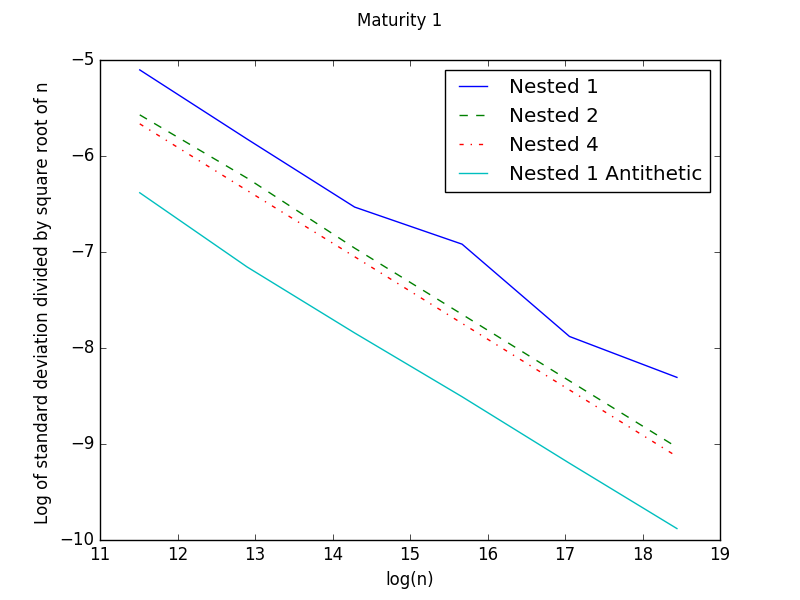

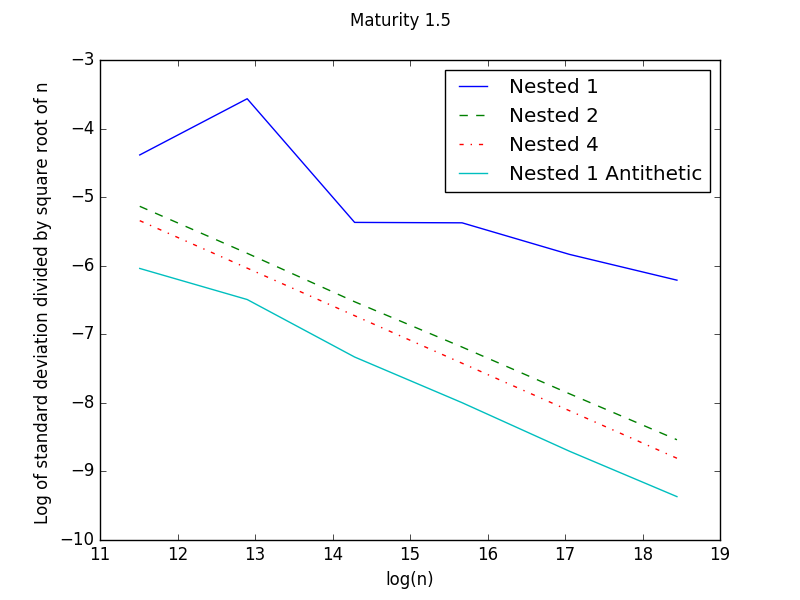

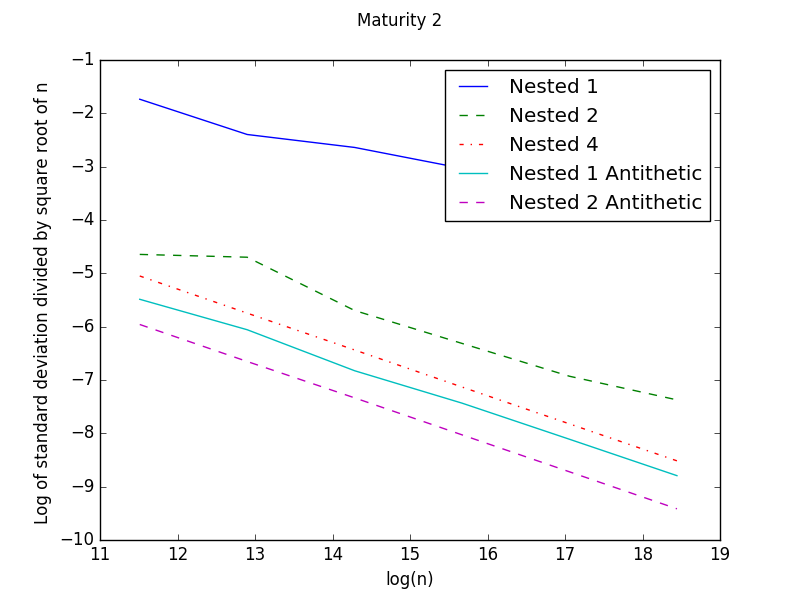

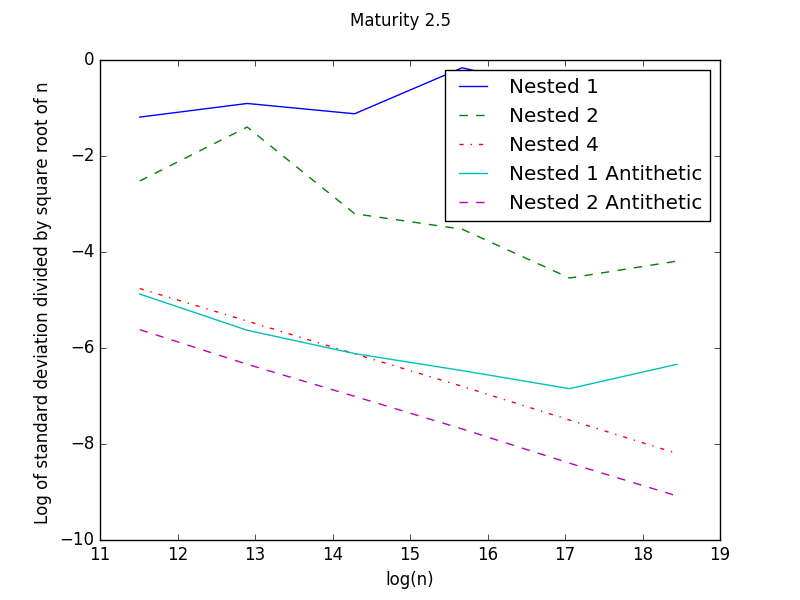

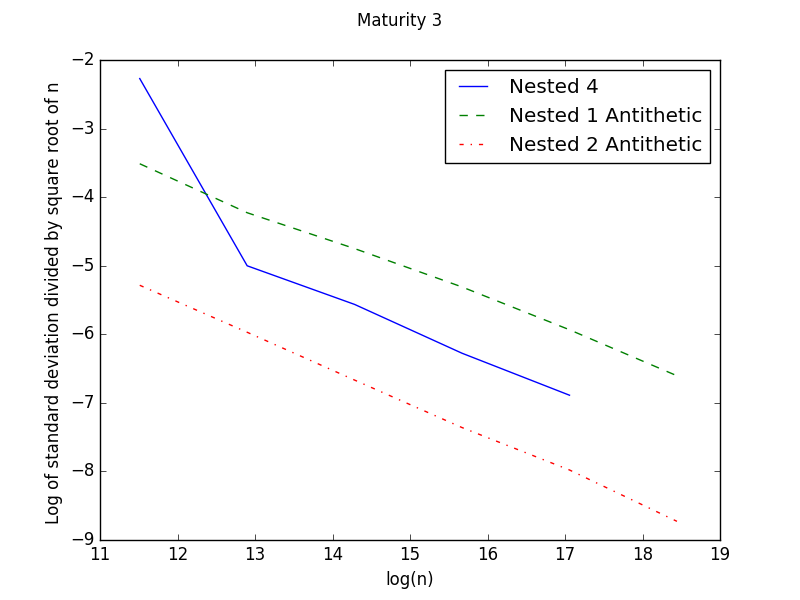

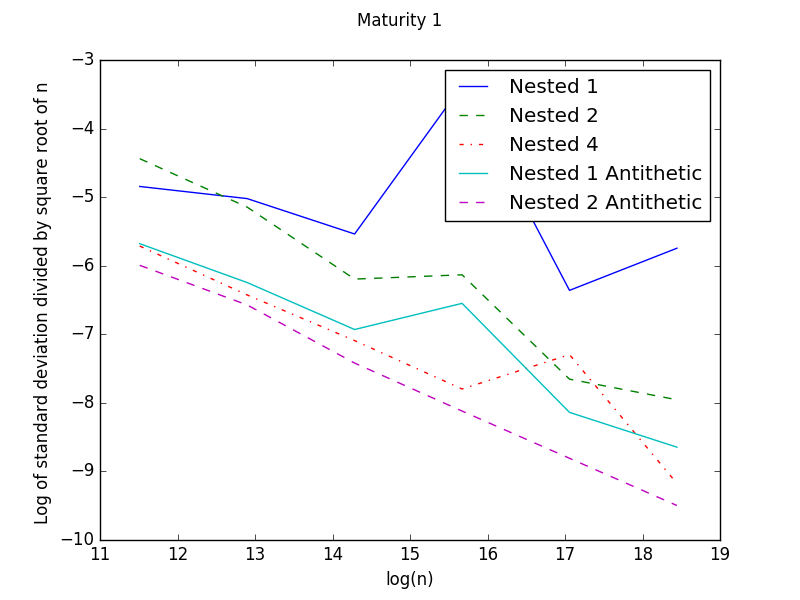

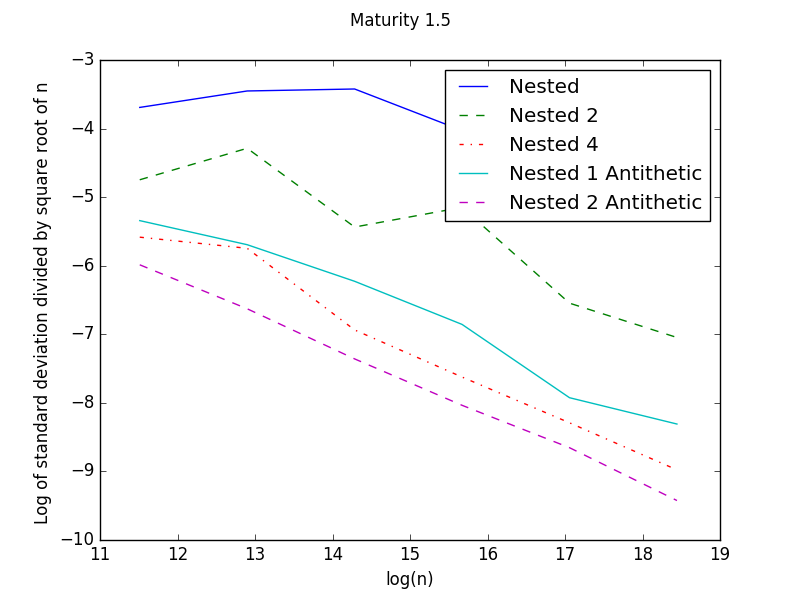

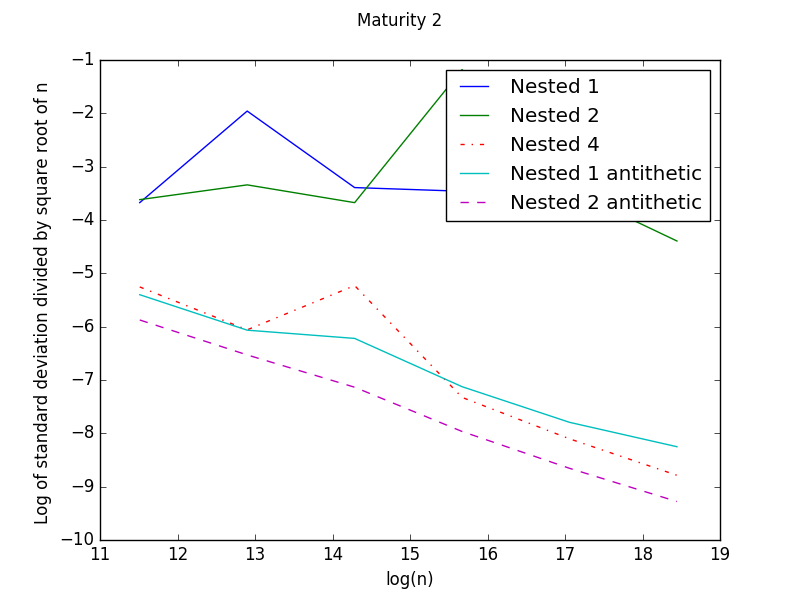

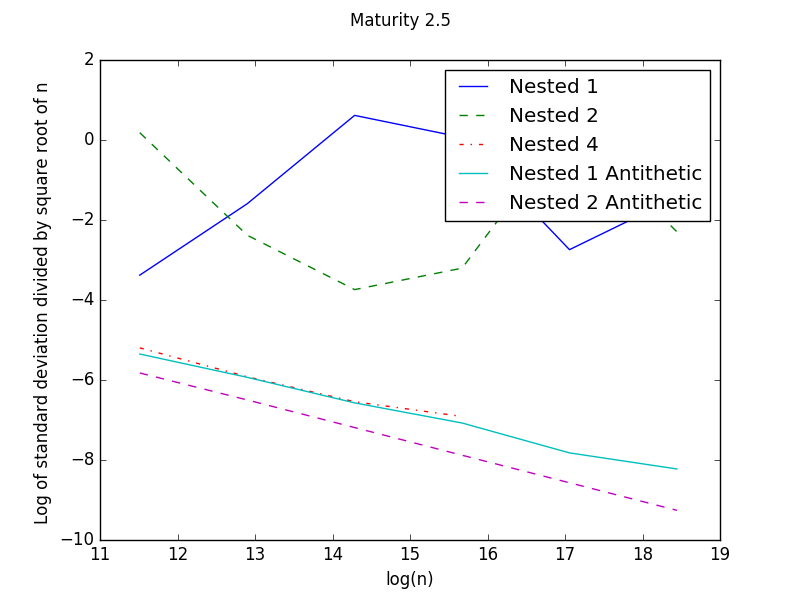

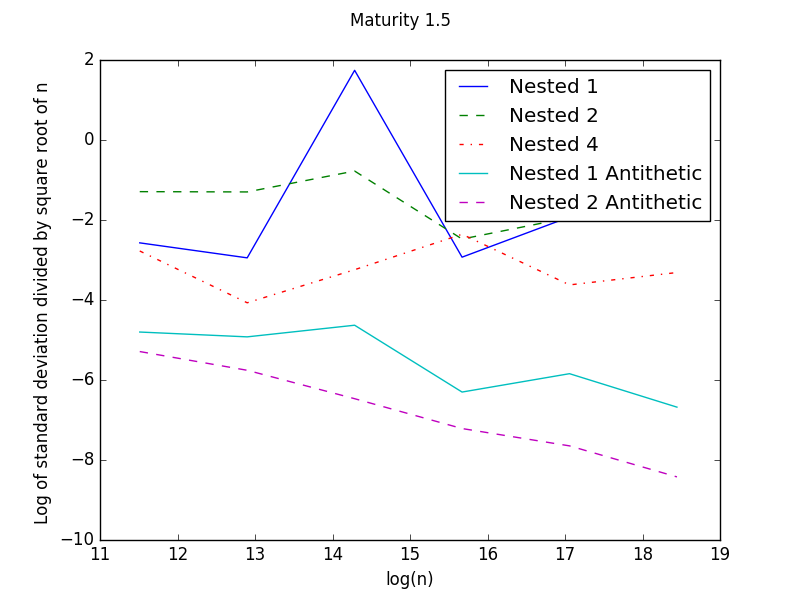

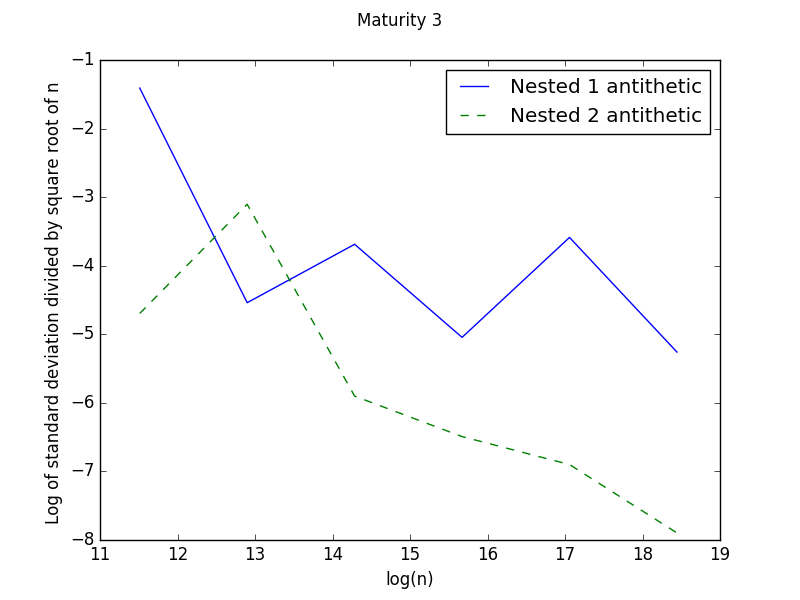

We first give on figures 1, 2 and 3 the results obtained for test A for different maturities and a dimension so the analytical solution is . We plot for each maturity :

-

•

the solution obtained by increasing the number of Monte Carlo scenarios used,

-

•

the error calculated as explained in the introduction.

Nested curves stand for the curves using the nested method of order , so the Nested curve stands for the original method.

On figure 3, for maturity the error observed with the orignal method (Nested 1) is around 1000 so it has not been plotted.

Because of the number of branching due to the gamma law, it seems difficult to use a nested method of order for long maturities : the time needed explodes. But clearly the nested method permits to have accurate solution for longer maturities.

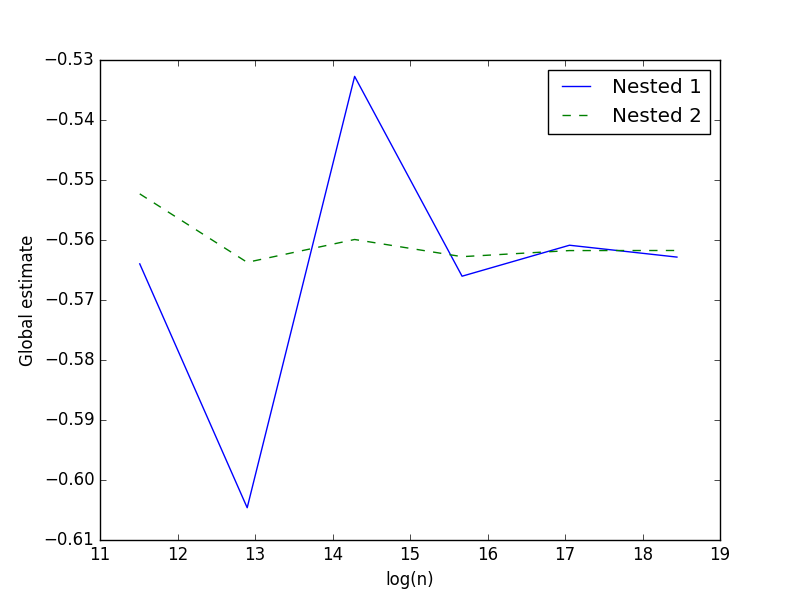

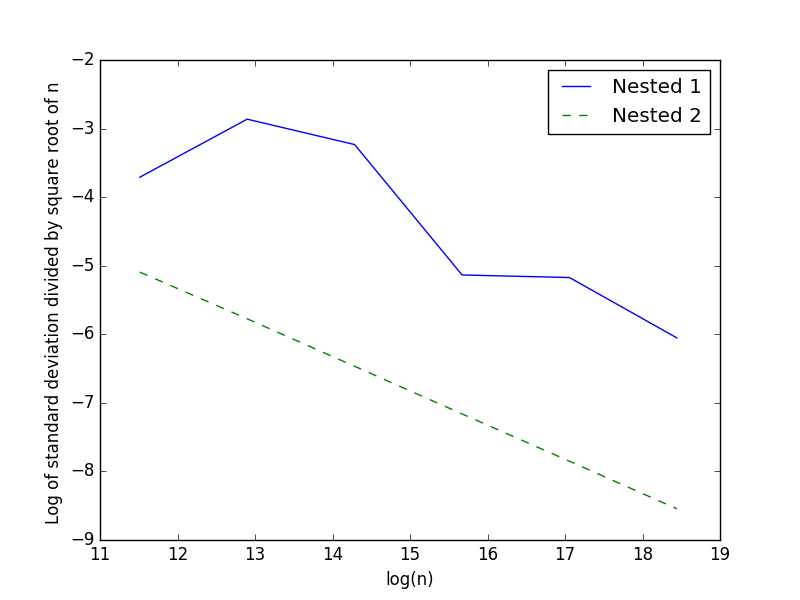

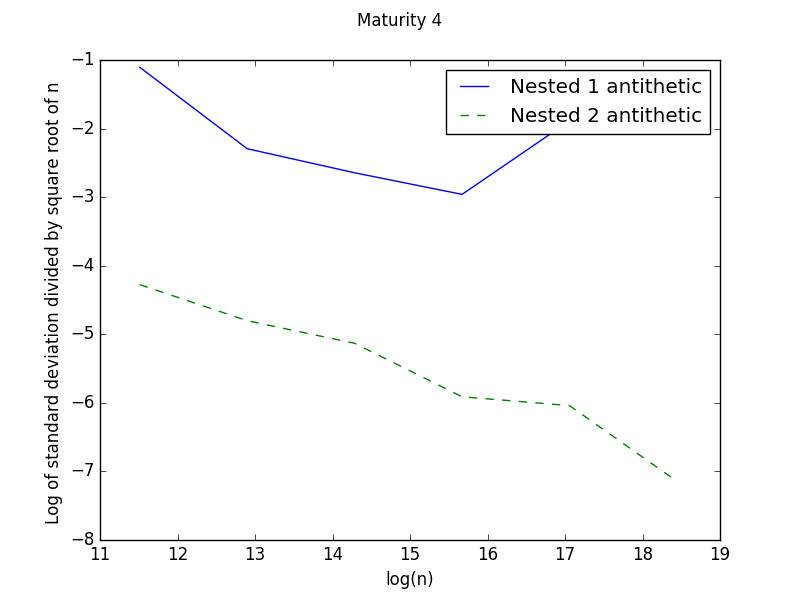

For a maturity of we also give the results obtained in dimension on figure 4 giving an analytical solution : once again the original method fails to converge while the nested one give good results.

2.2 Adaptation of the original branching to the re-normalization technique

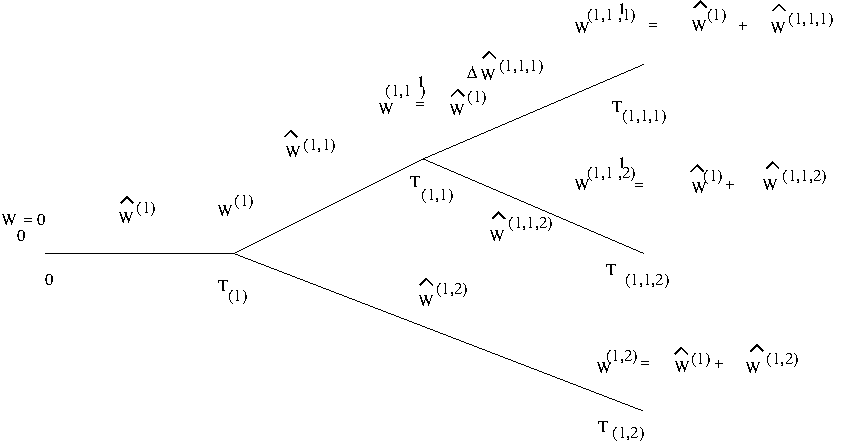

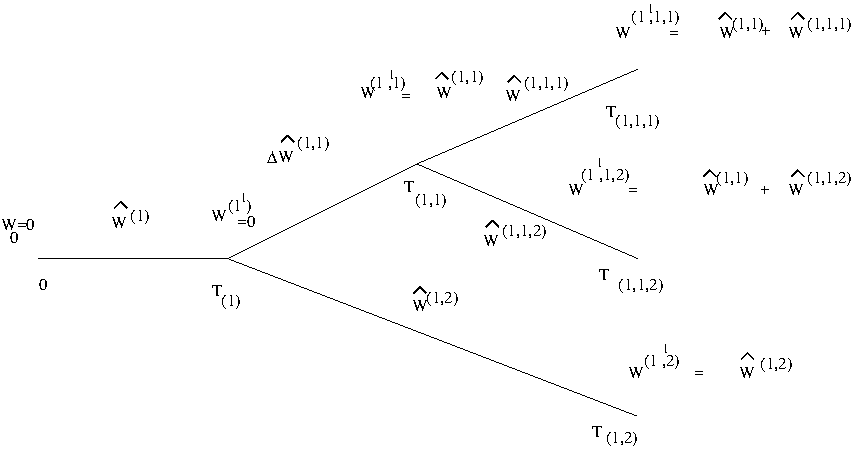

As introduced in [11], we introduce a modification of the original branching process that let us use exponential laws for the branching dates to treat the terms in the method previously described. Recall that , we introduce an associated ghost particle, denoted by , and denote . Next, given the collection of all particles (as well as ghost particles) of generation , we define the collection as follows. For every , we denote by its original particles, where when . Further, when is such that , we denote . The mark of will be the same as its original particle , i.e. ; and , and . Define also . For every , we still define the set of its offspring particles by

and the set of ghost offspring particles by

Then the collection of all particles (and ghost particles) of generation is

Define also

2.2.1 The original re-normalization technique

We next equip each particle with a Brownian motion in order to define a branching Brownian motion. Further, let , and for every , let

| (2.11) |

On figure 5, we give the original Galton-Watson tree and the ghost particles associated.

The initial equation (2.4) remains unchanged (first step of the algorithm) but equation (2.1.2) is modified by replacing the term

by

| (2.12) |

Notice that since has been obtained by (2.11), and are orthogonal so that adding the second term acts as a control variate. Recursively using the modified version of equation (2.1.2) induced by the use of (2.12), [11] gave defined the re-normalized estimator by a backward induction: let for every , then let

| (2.13) |

where the weights are given by equation (2.10), so we have

As explained in section 2.1.2, equation (2.1.2) used in representation (2.8) force us to take laws for branching dates with a high probability of low values that leads to a high number of recursions defined by equation (2.9).

Besides such laws using some rejection algorithm, as gamma laws, are very costly to generate.

The use of (2.12) permits us to use exponential laws very cheap to simulate and with a low probability of small values.

Indeed it can be easily seen in the linear case ( function of the gradient with , and ) by conditioning with respect to the number of branching that the variance is bounded for small maturities

and coefficients if

| (2.14) |

By construction using regularity, it is easily seen that for small time steps , as and (2.14) is satisfied for every densities.

2.2.2 Re-normalization techniques and antithetic

We give a version of the re-normalization technique using antithetic variables. Equation (2.11) is modified by :

| (2.15) |

for every .

Then equation (2.1.2) is modified by :

-

•

First , replacing the term tacking into account the power of

by

-

•

and the term taking into account the gradient

by

Notice that with this version the variance of the gradient term is finite with the same argument as in the original re-normalization version in subsection 2.2.1.

By backward induction we get the re-normalized antithetic estimator modifying (2.13) by:

| (2.16) |

where the weights are given by equation (2.10). Then we have

2.2.3 Numerical result for semi linear with re-normalization

We apply our nested algorithm on the original re-normalized technique and on the re-normalization technique with antithetic variables on two test cases.

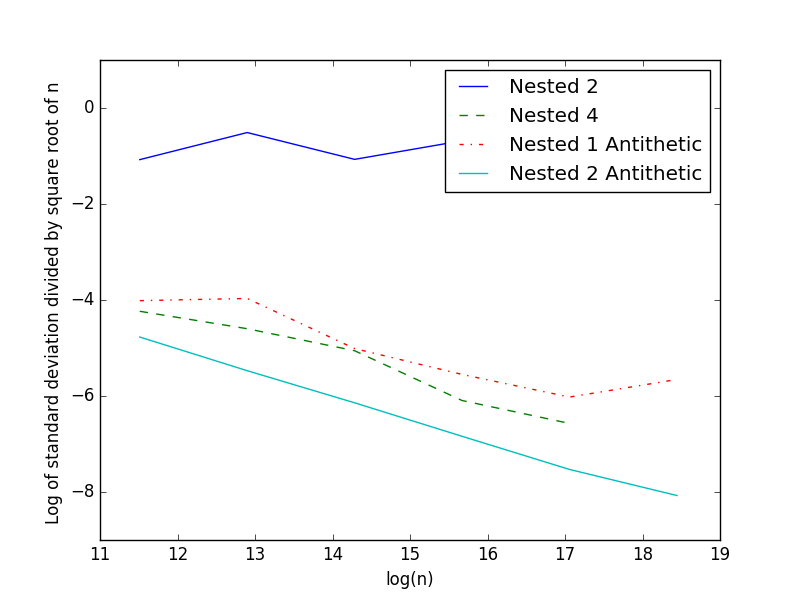

First we give some results for test case A in dimension 4.

We give the Monte Carlo error obtained by the nested method on figure 7.

For the maturity , without nesting the error of the original re-normalization technique has an order of magnitude of 2000 so the curve has not been given.

For the maturity , the nested original re-normalization technique with an order 2 doesn’t seem to converge.

As the maturity increases, nesting with a higher order becomes necessary. Notice that with the re-normalization it is possible to use the nested method of a high order because of the small number of branching used. For example, for , for an accuracy of , in dimension :

-

•

the original method in section 2.1.2 with a nested method of order 2 achieves an accuracy of for a CPU time of seconds using 28 cores,

-

•

the re-normalized version of section 2.2.1 with a nested method of order 4 reaches the same accuracy in seconds,

-

•

the re-normalized version with antithetic of section 2.2.2 without nesting reaches the same accuracy in seconds.

For the same test case A we plot in dimension 6 the error on figure 9 to show that the method converges in high dimension.

Besides on figure 8, we show that the derivative is accurately calculated.

We then use a second test case B : For a given dimension , we take , ,

with a terminal condition . This test case cannot be solve by the nested method without re-normalization due to the high cost involved by the potential high number of branching. We give the results obtained for case B by the re-normalization methods of section 2.2.1 and 2.2.2 in dimension 4 on figure 9.

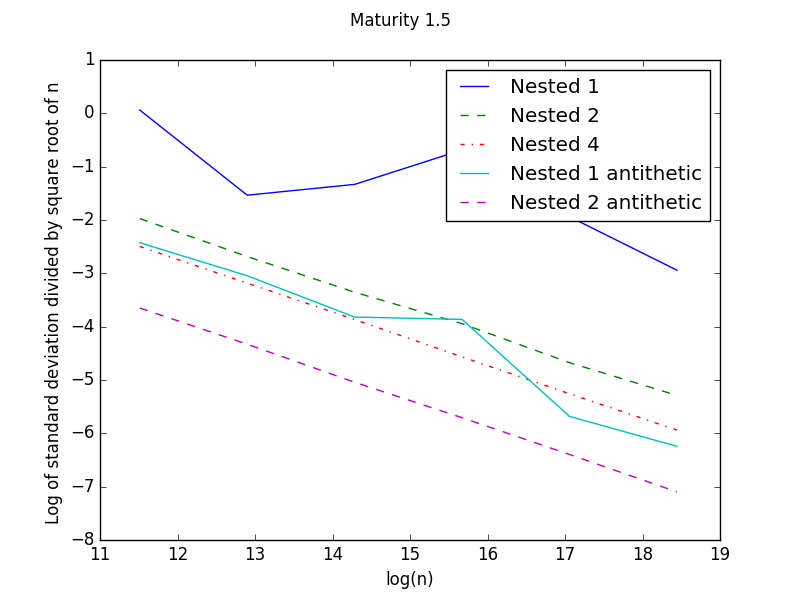

At last we give the results obtained in dimension pour and on figure 10.

The nested method with re-normalization and antithetic appears to be the most effective and permits to solve semi-linear equations with quite long maturities. The re-normalization technique is however far more memory consuming than the original scheme of section 2.1.2. This memory cost explodes with very high maturities. The nested version of the original scheme of section 2.1.2 isn’t affected by these memory problems but is affected by an explosion of the computational time with longer maturities.

2.3 Extension to variable coefficients

In the case of time and space dependent coefficients and of the PDE, it is possible to use the method consisting in “freezing” the coefficients first proposed in [10] for non fixed and extended in the general case in [5]. This method increases the variance of the estimator, therefore it is more efficient for treating log maturities to use an Euler scheme to take into account the variation of the coefficients. Introducing an Euler time step , between the dates and , the SDE is discretized as :

where , and

is a sequence of independent -dimensional Brownian motion.

Using an integration by part on the first time step, in the original scheme of section 2.1, the gradient term in equation (2.1.2) is replaced

| (2.17) |

In the case of the renormalization technique of section 2.2.1, the ghost is obtained from the original particule by removing the part associated to the first brownian. Then for every , the particule dynamic is given by

if and

otherwise.

The renormalization technique of section 2.2.1 leads to the following estimation of the gradient in equation (2.1.2):

| (2.18) |

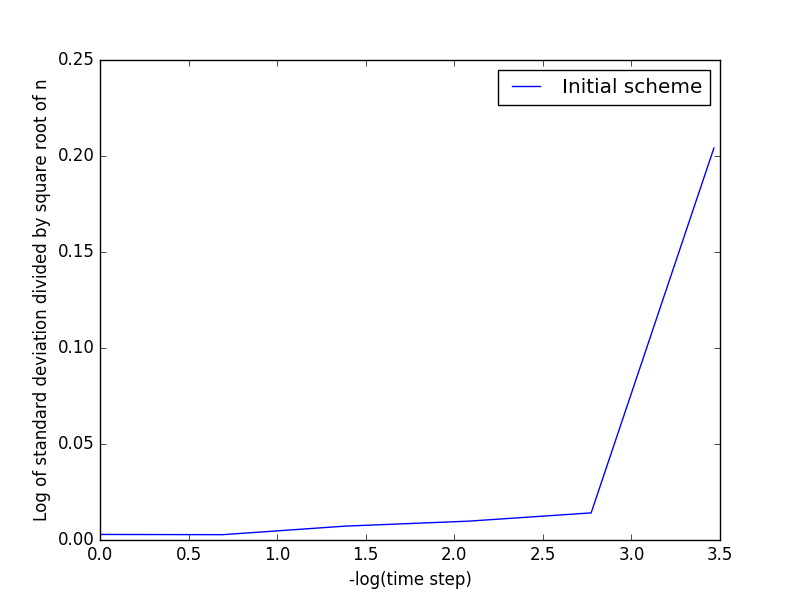

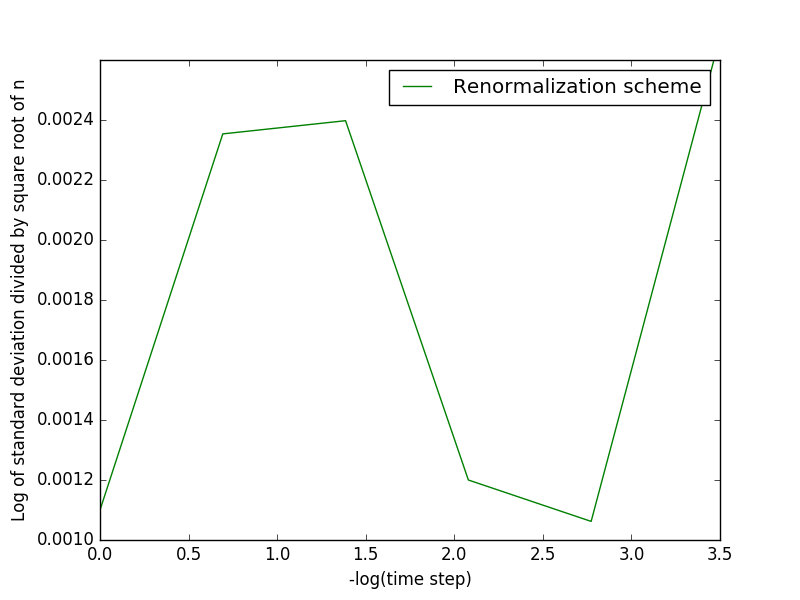

Remark 2.2.

Of course using equation (2.17) we expect that variance of the scheme will degrade with the diminution of the time step and we expect the scheme (2.18) to correct this behaviour. On figure 11 we give the error estimations given by the original scheme and the renormalization technique (with anithetics of section 2.2.1) depending on the time step for a case with burgers non linearity in dimension 4 with particles: as we refine the time step the scheme (2.17) becomes unusable while the scheme (2.18) gives stable results.

3 The full non linear case

In order to treat some full non linear case, so with a second order derivative in , the re-normalization technique is necessary as no distribution can meet the finite variance requirement

even when is linear in (see [9]).

Suppose that the function is as follows :

for a given ,

, for are bounded continuous,

is a bounded continuous function, and , for are bounded continuous functions.

We note .

We use a similar algorithm to the one proposed in section 2.1.2.

Instead of approximating using representation (2.1.2), we have to take into account the term :

| (3.1) |

The terms

and

are approximated by the different schemes previously seen. It remains to give an approximation of the term.

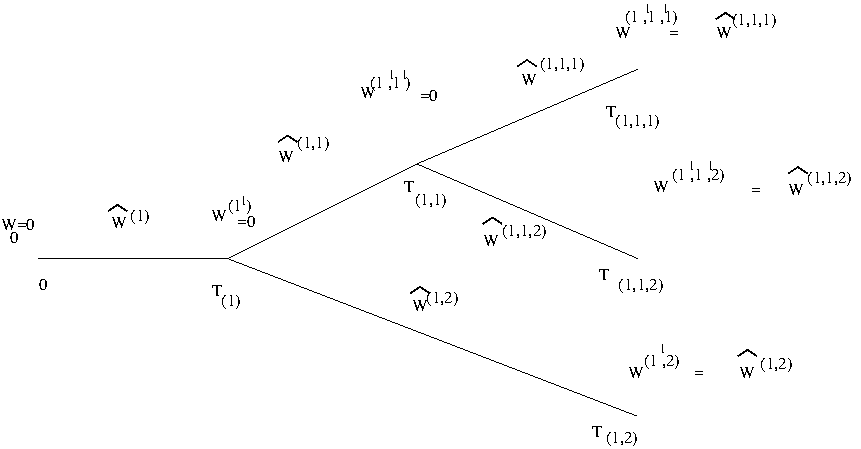

3.1 Ghost particles of dimension

We extend the definition given in [11] of ghost tree for the full non linear case. For a particle in dimension of generation , we introduce associated ghost particles denoted for . Let Then given the collection of all particles and ghost particles of generation , we define as follows. Given , we denote by its original particle; and when , we denote for and is noted the order of . The function allows us to give the order of a particle for :

The variables as well as the mark inherits that of the original particle . Similarly . Denote also . For every , we define the collection of its offspring particles by

and generalizing the definition in section 2.2, we introduce collections of all offspring ghost particles:

Then the collection of all particles and ghost particles of generation is given by

3.2 approximations

In this section, we give some different schemes that can be used to approximate the term and that we will compared on some numerical test cases.

3.2.1 The original approximation

The approximation developed in this paragraph was first proposed in [11] and uses some ghost particle of dimension . To obtained the position of a particle, we freeze its position if its order is and inverse its increment if its order is , so for every

| (3.2) |

3.3 A second representation

This second representation uses some ghost particle of dimension . Let

be a sequence of independent -dimensional Brownian motion, which is also independent of . The dynamic of the original particles and the ghosts is given by :

| (3.5) |

We then replace (3.2.1) by

| (3.6) |

where

This scheme can be can be easily obtained by applying the differentiation rule used for semi linear equations on two successive steps with size . A simple calculation shows that the original scheme has a variance bounded by while this one has variance bounded by so we expect a diminution of the variance observed with this new scheme.

Remark 3.1.

This derivation on two consecutive time steps has already been used implicitly for example in [6] and already was numerically superior to a scheme directly using second order Malliavin weight.

Recursively the re-normalized estimator is defined by a backward induction: let for every , then let

| (3.7) |

where

| (3.8) |

Then we have

3.4 A third representation

This representation is only the antithetic version of the second one and uses some ghost particle of dimension . The dynamic of the original particles and the ghosts is given by :

| (3.9) |

We then replace (3.2.1) by

| (3.10) |

where

and the weights are still given by equation (3.3). The backward induction is defined as follows: let for every , then let

| (3.11) |

where the weights are given by equation (3.3). And as usual we have

Remark 3.2.

Extension to schemes for derivatives of order more than 3 is obvious with the two last schemes.

3.5 Numerical results

For all test cases in this section we take , and we want to evaluate . We test the 3 schemes previously described :

-

•

Version 1 stands for the original version of the scheme using backward recursion (3.2.1),

-

•

Version 2 stands for the second representation using second backward recursion (3.3),

-

•

Version 3 stands for the third representation corresponding to the antithetic version of the second representation and using backward recursion (3.4). Notice that in this case all terms in in are treated with antithetic ghosts.

We give results for the non nested version as the nested version doesn’t improve the results very much.

-

•

We first choose a non linearity

where , and

with . We suppose that the final solution is given by such that the analytical solution is

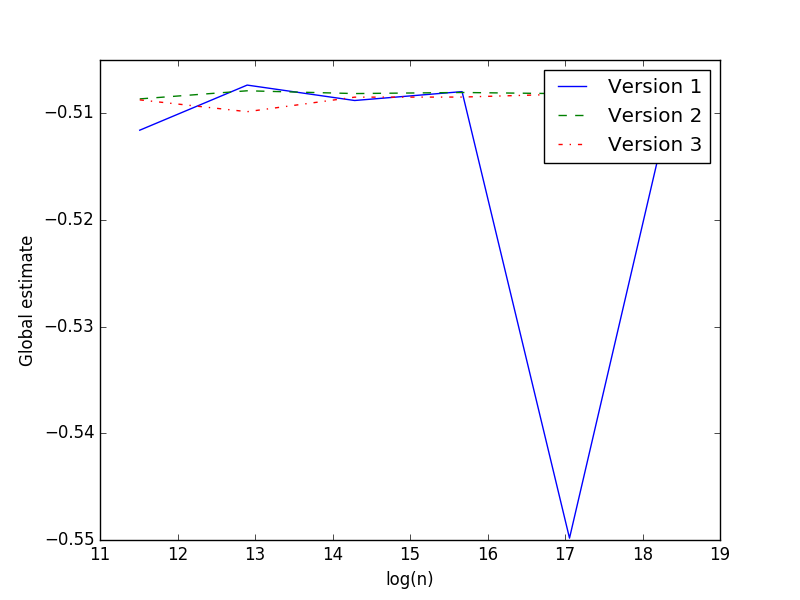

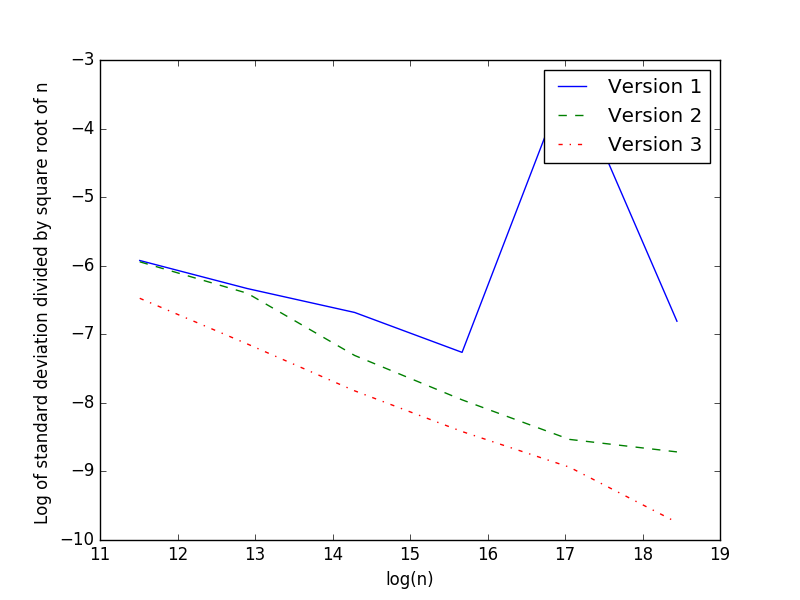

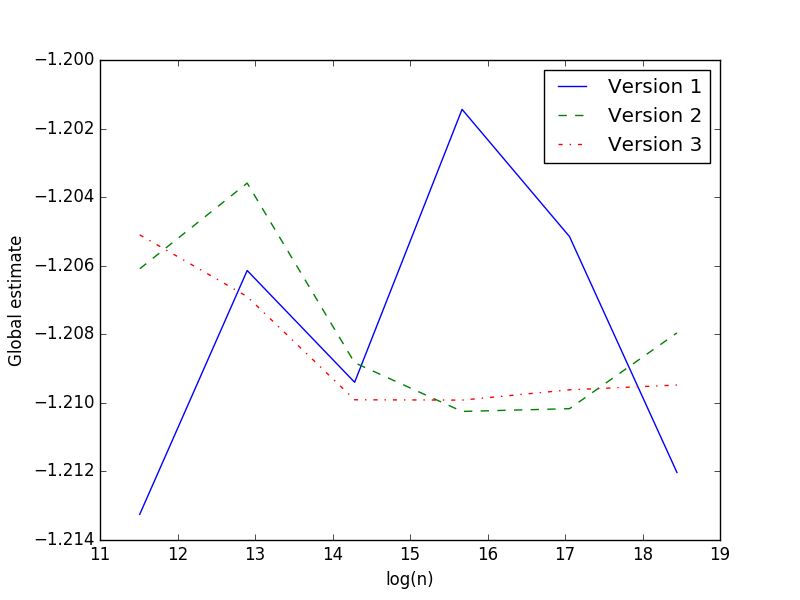

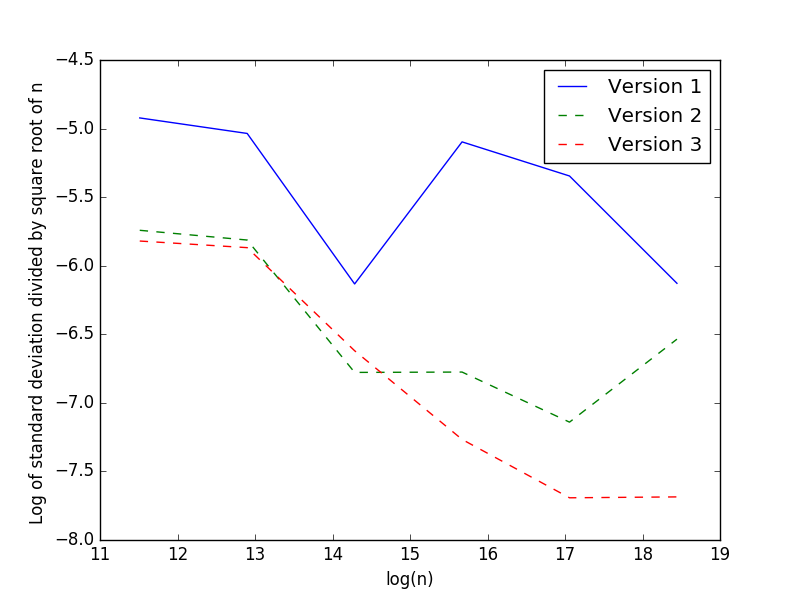

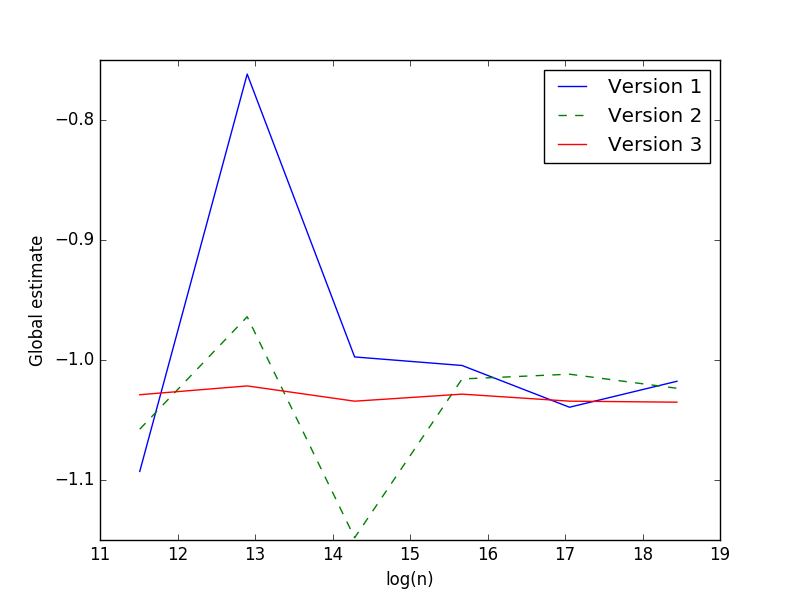

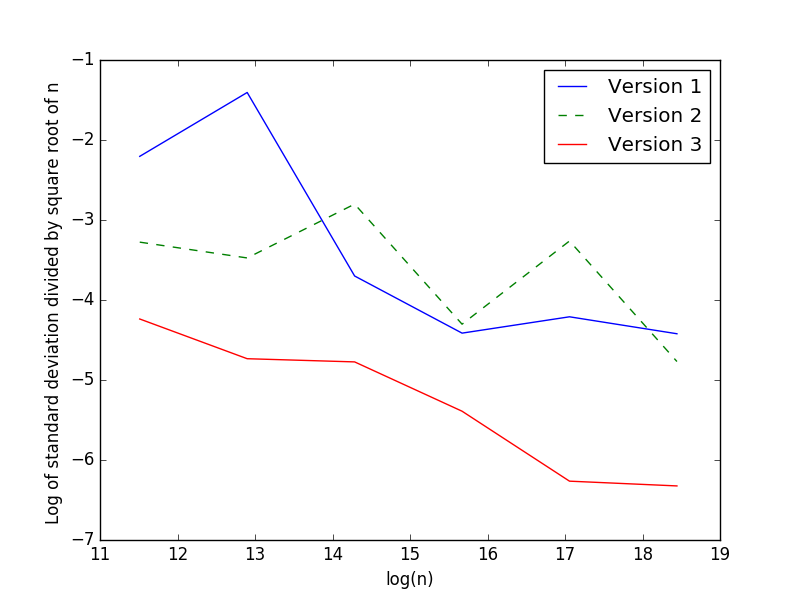

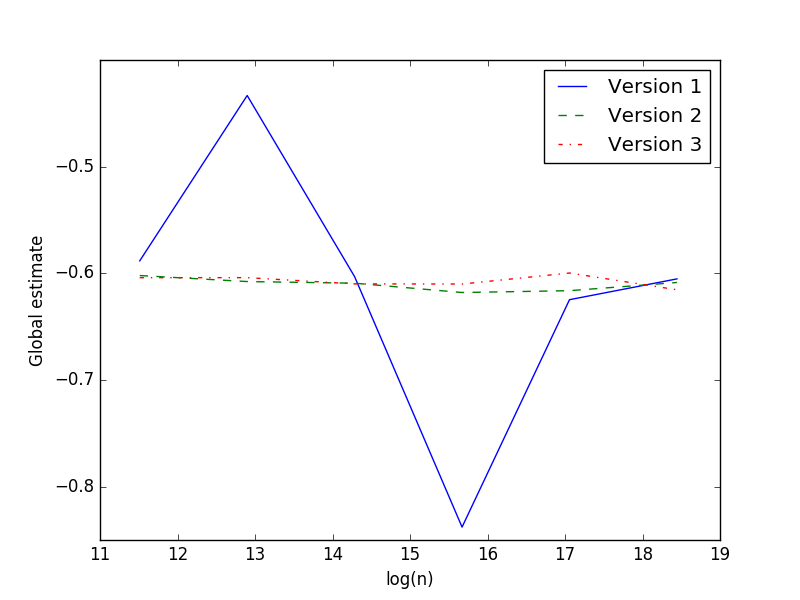

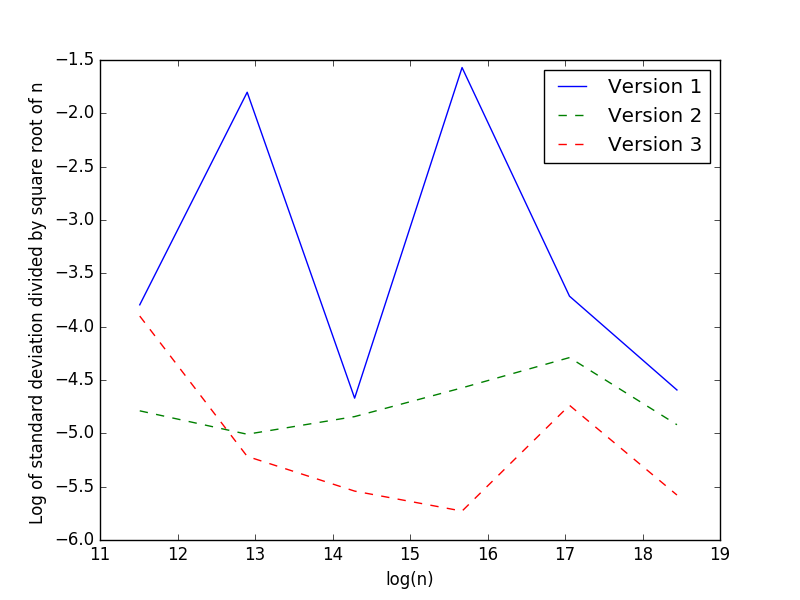

This test case will be noted test C. In the example we want evaluate . First we take and give the results obtained for different maturities on figures 12 and 13.

Figure 12: Solution and error obtained in for test case C with , analytical solution is .

Figure 13: Solution and error obtained in for test case C with , analytical solution is . We then test in dimension 6 the different schemes on figure 14. Besides on figure 15 we show that the schemes provide a good accuracy for the computation of the derivatives by plotting for the three versions : as expected the accuracy is however slightly less good than for the function evaluation.

Figure 14: Solution obtained and error in for test case C with , analytical solution is .

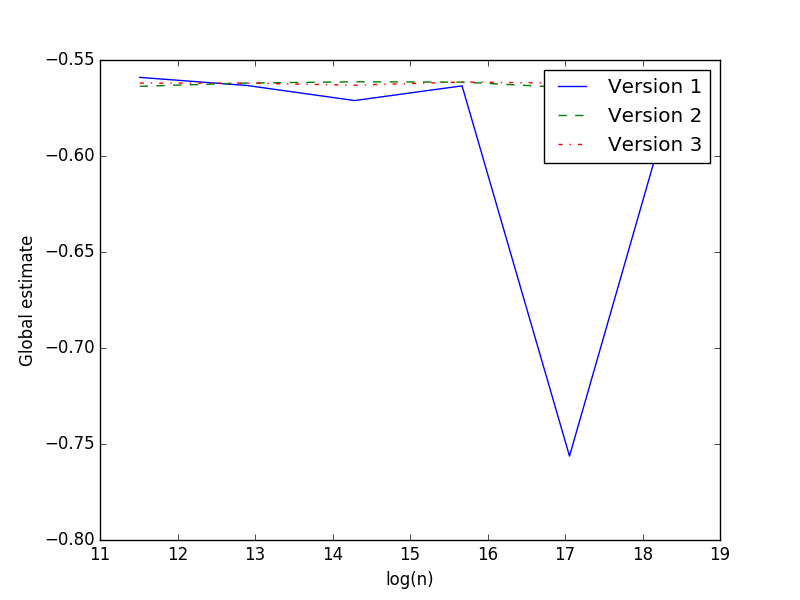

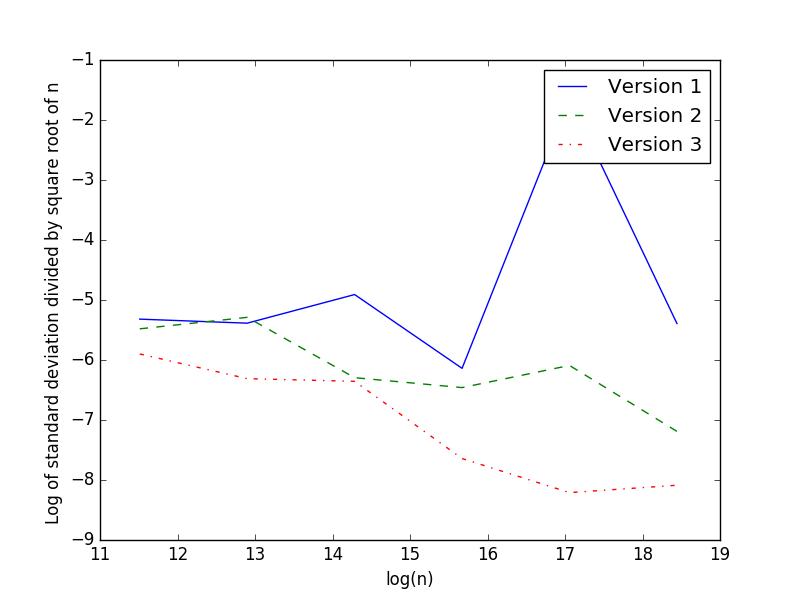

Figure 15: Derivative obtained and error in for test case C with . -

•

At last we consider the test D where , and

We give the solution and error obtained for the 3 methods on figure 16.

Figure 16: Solution and error obtained for for test case D with .

On all the test cases, the last representation using antithetic variables gives the best result in term of variance reduction but at a price of memory consumption increase: as order of the ghost representation increase so does the memory needed.

4 Conclusion

As the scheme and methods developped here let us extend the maturities than can be used to evaluate the solution of some semi linear and full non linear equation. This is achieved by an increase of the computational time and the memory consumption.

References

- [1] Bruno Bouchard, Ivar Ekeland, and Nizar Touzi. On the malliavin approach to monte carlo approximation of conditional expectations. Finance and Stochastics, 8(1):45–71, 2004.

- [2] Bruno Bouchard and Nizar Touzi. Discrete-time approximation and monte-carlo simulation of backward stochastic differential equations. Stochastic Processes and their applications, 111(2):175–206, 2004.

- [3] Bruno Bouchard and Xavier Warin. Monte-carlo valuation of american options: facts and new algorithms to improve existing methods. In Numerical methods in finance, pages 215–255. Springer, 2012.

- [4] Patrick Cheridito, H Mete Soner, Nizar Touzi, and Nicolas Victoir. Second-order backward stochastic differential equations and fully nonlinear parabolic pdes. Communications on Pure and Applied Mathematics, 60(7):1081–1110, 2007.

- [5] Mahamadou Doumbia, Nadia Oudjane, and Xavier Warin. Unbiased monte carlo estimate of stochastic differential equations expectations. to appear in ESAIM P&S, 2017.

- [6] Arash Fahim, Nizar Touzi, and Xavier Warin. A probabilistic numerical method for fully nonlinear parabolic pdes. The Annals of Applied Probability, pages 1322–1364, 2011.

- [7] Eric Fournié, Jean-Michel Lasry, Jérôme Lebuchoux, Pierre-Louis Lions, and Nizar Touzi. Applications of malliavin calculus to monte carlo methods in finance. Finance and Stochastics, 3(4):391–412, 1999.

- [8] Emmanuel Gobet, Jean-Philippe Lemor, and Xavier Warin. A regression-based monte carlo method to solve backward stochastic differential equations. The Annals of Applied Probability, 15(3):2172–2202, 2005.

- [9] Pierre Henry-Labordere, Nadia Oudjane, Xiaolu Tan, Nizar Touzi, and Xavier Warin. Branching diffusion representation of semilinear pdes and monte carlo approximation. arXiv preprint arXiv:1603.01727, 2016.

- [10] Pierre Henry-Labordere, Xiaolu Tan, and Nizar Touzi. Unbiased simulation of stochastic differential equations. arXiv preprint arXiv:1504.06107, 2015.

- [11] Pierre Henri Labordère, Xiaolu Tan, Nizar Touzi, and Xavier Warin. Truncation and renormalization techniques for solving the nonlinear pdes by branching processes, 2017.

- [12] Jean-Philippe Lemor, Emmanuel Gobet, and Xavier Warin. Rate of convergence of an empirical regression method for solving generalized backward stochastic differential equations. Bernoulli, 12(5):889–916, 2006.

- [13] Etienne Pardoux and Shige Peng. Adapted solution of a backward stochastic differential equation. Systems & Control Letters, 14(1):55–61, 1990.

- [14] Jianfeng Zhang. A numerical scheme for bsdes. the annals of applied probability, 14(1):459–488, 2004.