The impact of stochastic lead times

on the bullwhip effect under correlated demand

and moving average forecasts

Abstract

We quantify the bullwhip effect (which measures how the variance of replenishment orders is amplified as the orders move up the supply chain) when random demands and random lead times are estimated using the industrially popular moving average forecasting method. We assume that the lead times constitute a sequence of independent identically distributed random variables and correlated demands are described by a first-order autoregressive process.

We obtain an expression that reveals the impact of demand and lead time forecasting on the bullwhip effect. We draw a number of conclusions on the bullwhip behaviour with respect to the demand auto-correlation and the number of past lead times and demands used in the forecasts. Furthermore, we find the maxima and minima in the bullwhip measure as a function of the demand auto-correlation.

Keywords: supply chain, bullwhip effect, order-up-to replenishment policy, AR(1) demand, stochastic lead time, moving average forecasting method.

1 Introduction

The variability of replenishment orders often increases as they flow upstream in supply chains. This phenomenon is known as the bullwhip effect and has been discussed in the economics and operations management literature for 100 and 50 years, respectively – see Mitchell [38] and Forrester [21]. The celebrated works of Lee et al., [33] and [34] promoted this problem to the forefront of the supply chain and operations management field. Wang and Disney [51] provide a recent literature review of the bullwhip field, categorising contributions according to the five causes of bullwhip of Lee et al.: demand forecasting, non-zero lead time, supply shortage, order batching and price fluctuation. Of particular importance to this paper are the results of Chen et al., [13], [14] and Dejonckheere et al., [15]. These contributions investigate the bullwhip consequences of using the moving average forecasting method inside the order-up-to (OUT) replenishment policy.

Recently Michna and Nielsen [39] identified another critical cause of the bullwhip – the forecasting of lead times. While the issue of stochastic lead times in bullwhip studies has not been intensively investigated, Michna and Nielsen [39] and Michna et al., [41] provide a recent literature review of this problem. Of particular importance is the work of Duc et al., [20] and Kim et al., [31] where the impact of stochastic lead times on bullwhip is quantified. These works characterise the impact of random lead times on the bullwhip effect via mean values and variances. However, they do not consider the consequences of having to estimate the lead time distribution (a.k.a. lead time forecasting). As identified by Michna and Nielsen [39] and Michna et al., [41] this can be a significant cause of the bullwhip effect. In Duc et al., [20] lead times are assumed to be stochastic and drawn from a known distribution and thus are not forecasted when placing an order. Kim et al., [31] used the moving average technique to forecast lead time demand, as did Michna et al., [40].

The influence of stochastic lead time on inventory is a more established field and we refer to the work of Bagchi et al., [2], Chaharsooghi et al., [9], Song [46] and [47], and Zipkin [53]. Stochastic lead time inventory research can be classified into two general streams: those with order crossovers and those without crossovers. An order crossover happens when replenishments are received in a different sequence from which the orders were placed (see e.g. Bischak et al., [3], Bradley and Robinson [7], Disney et al., [18] and Wang and Disney [51]). Disney et al., [18] consider the safety stock and inventory cost consequences of using the OUT and proportional order-up-to (POUT) replenishment policies under i.i.d. demand. They show that the POUT policy is always more economical than the OUT policy when order-crossover is present. Wang and Disney [51] show that the POUT policy outperforms the OUT policy in the presence of order crossovers in the sense of minimizing inventory variance when demand is an Auto-Regressive, Moving Average process with auto-regressive terms and moving average terms, ARMA(p,q).

The papers of Boute at el. [4], [5], [6] investigate endogenous lead times in supply chains. Endogenous lead times are dependent on the state of the system as they are function of the previous orders. Here the supplier is modelled as a queue and orders are processed on a first come, first served basis, hence there is no order-crossover. However, as the sojourn time in the queue increases in the variance of the demand placed on the manufacturer, a lead time reduction can be obtained by smoothing the replenishment orders. This lead time reduction can potentially reduce safety stock requirements. Hum and Parlar [28] also model lead times using queueing theory, analyzing the proportion of demand that can be met within a specific lead time.

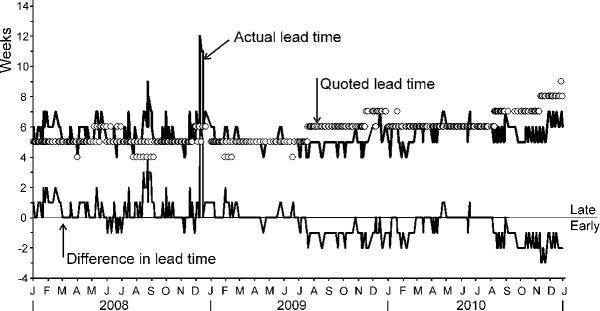

We have observed that stochastic lead times and order-crossovers are quite common within factories (see Fig. 1). The data represents a single, high volume, product from a supplier of industrial measuring and testing equipment. The distribution of the lead times is discrete and aggregated into weekly buckets to reflect the actual practice of creating weekly production plans using the OUT policy (for more information on why this is so, we refer to the assumptions and modelling choices discussed later in this section). Fig. 1 also highlights the number of queue positions each production batch gained or lost between the two lists of date sorted production releases and production completions. As this manufacturer manually moved totes of products between process steps within its job shop, a large number of order-crossovers is present. Disney et al., [18] present similar findings in global supply chains (see Figs. 1 and 2 of [18]), where stochastic lead times and order crossovers could be observed in global shipping lanes. Here containers could also gain or lose positions in the date ordered list of dispatches and receipts. We also observe differences in quoted (at the time of shipping) and actual (realised when the container arrives) lead times in global shipping lanes (see Fig. 2).

We consider a model where a supply chain member (who could be a retailer, manufacturer, or supplier for example, but we call a manufacturer for convenience) observes both random demands from his customer and random lead times from his supplier which we assume to be exogenous (that is, they are independent of all other system states). The manufacturer generates replenishment orders to maintain inventory levels by projecting his customers’ future demands over his supplier’s lead time, accounting for both the available inventory and the open orders in the replenishment pipeline.

This research differs from previous research in several ways. Most importantly we show that lead time forecasting is a major cause of bullwhip when demands are auto-correlated. This confirms and extends the results of Michna and Nielsen [39]. We also quantify the impact of the stochastic auto-correlated demands and stochastic lead times on the bullwhip effect under the assumption that demands and lead times are forecasted separately using moving averages. Furthermore, we investigate the bullwhip effect as a function of the demand auto-correlation, the characteristics of the lead time distribution and the number of past demands and the delay parameter in the moving average lead time forecasts. The bullwhip conclusions differ depending on how the parameters are combined. We find maxima and minima in the bullwhip metric as a function of the demand auto-correlation.

Moreover our main result contains, as special cases, the bullwhip formulas of Chen et al., [13] (a constant lead time) and Th. 1 in Michna and Nielsen [39] (mutually independent demands). The formulation presented in this research involves more parameters, is more general, and allows us to understand more intricate supply chain settings.

Our major assumptions and modelling choices are summarised as follows:

-

a)

The supply chain consists of two stages – a manufacturer who receives client’s demands and deliveries from a supplier (or manufacturing process).

-

b)

A periodic replenishment system exists where the demands, , are satisfied and previous orders placed are received during a time period, indexed by the subscript . At the end of the period, the inventory level, demand and lead times of received orders are observed and a new replenishment order, , is placed. The length of the period could be an hour, day, week or month, but in our experience it is often a week in manufacturing contexts. Note that the receipt of an order is observed only at the end of the period and the lead time is a non-negative integer. An order with zero lead time would be received instantaneously after the order was placed, but its receipt would only be incorporated into the order made at the end of the next period due to the sequence of events delay.

-

c)

The demand constitutes an autoregressive model of order one, AR(1). We have elected to use the AR(1) model as it is the simplest demand process with autocorrelation, a feature commonly observed in real demand patterns, Lee et al., [35]. It is also a frequently adopted assumption in the bullwhip literature (e.g. in Chen at el. [13] and [14], Duc et al., [20] and Lee et al., [35]), allowing comparison of our new results to established theory.

-

d)

The lead times constitute a sequence of independent identically distributed (iid) random variables which are independent of all system states, including the manufacturer’s demand. Moreover we assume that lead times are bounded (e.g. periods) and that the lead time forecasts are based on lead time information that is at least periods old. This allows use to create lead time forecasts that are unbiased. For example, if we based our lead time forecasts on the most recent lead time information (which we observe when we receive orders), some of the orders placed would still be open (not yet received) and our lead time estimates would only be based on those orders with short lead times. Basing our lead time estimates on data that is at least periods old is possible as lead times are assumed to be temporally independent and thus constitute a valid dataset for forecasting all future lead times. Practically this approach has the desirable characteristic that we can base our lead time estimates on realised lead times, rather than quoted lead times from the supplier or shipper, see Fig. 2. Furthermore, for ease of data organisation (and modelling) we can retrospectively assign the lead time of an order to the period the order was generated in our database (simulation).

-

e)

The OUT policy is used to generate the orders placed onto the supplier. The OUT policy is industrially popular as it is commonly available native in many ERP/MRP systems. It has also been studied extensively in the academic literature (see e.g. Bishak at el. [3], Chen at el. [13] and [14], Dejonckheere at el. [15] and [16], Duc at el. [20] and Kim at el. [31]). The OUT policy is also the optimal linear replenishment policy for minimizing inventory holding and backlog costs if orders do not cross (see Kaplan [30] and Wang and Disney [51]).

-

f)

The manufacturer predicts the future demands over future lead times based on predictions generated using the moving average forecasts of past demand and observations of the lead times of previously received orders. Thus, the forecast of lead time demand is as follows

(1) where is the forecast of the lead time of the next order made at the beginning of period and denotes the forecast for a demand for the period made at the beginning of a period .

As Michna and Nielsen [39], the novel aspect of our approach is the last point f) and differs from much of the previous literature. For example, Duc et al., [20] assume the lead time of the order placed at time is known when placing order leading to

However, we assume the manufacturer would not know the value of until that order has been completed (arrived, received).

In Kim et al., [31] the lead time demand is predicted with

where is the past known (realized) lead time demand.

A different approach was taken by Bradley and Robinson [7] and Disney et al., [18] where it is assumed beforehand that the lead time distribution is known. That is, the lead time distribution can be observed from previous realisations of the lead time.

In our approach we show that the bullwhip effect measure contains new components depending on the lead time forecasting parameter, and the correlation coefficient between demands. This was not quantified in Michna and Nielsen [39], neither was it included in the study of ARMA(p,q) demand in Wang and Disney [51]. These new terms amplify the value of the bullwhip measure and are evidence that lead time estimation in itself is a significant cause of the bullwhip effect, perhaps equally as important as demand forecasting.

2 Supply chain model

We want to consider temporally dependent demands and the simplest way to achieve this is to model a manufacturer observing periodic customer demands, , constituting of a stationary first-order autoregressive, AR(1), process,

| (2) |

where and is a sequence of independent identically distributed random variables such that and . Under the stationarity assumption it can be easy found that , and (see for example, Chen et al., [13] and Duc et al., [20]). The distribution of can be arbitrary but its second moment must be finite.

A random lead time is assigned to each order at the beginning of time . It is observed and used to predict future lead time when the order is received. The random lead times are mutually iid random variables that is also assumed in Duc et al., [20], Kim et al., [31], Robinson et al., [43] and Disney et al., [18]. The expected value of the discrete lead times is where is the probability that the lead time is periods long, . We do not impose any assumptions on the distribution of but that its second moment is finite and is non-negative. The sequences and are mutually independent.

The lead time demand at the beginning of a period is defined as follows

| (3) |

which reflects the demand over the lead time. At the beginning of a period the manufacturer does not know this value of so he must forecast its value before calculating his replenishment order (see (1)).

Let us notice that there is a dependency between and due to (1). That is, the lead time demand forecast is a function of past lead times. Employing the moving average forecast method with the delay parameter for demand forecasting we get

| (4) |

where and are previous demands which have been observed at the beginning of period . Here we use a simple moving average method. Thus the -period ahead forecast of demand is a moving average of previous demands. Note all future forecasts, regardless of , are straight line predictions of the current forecast. Clearly this is not an optimal, minimum mean squared error, forecast for AR(1) demand. However, it does reflect common industrial practice as the moving average forecast is available in many commercial ERP systems and can be readily incorporated into spreadsheets by analysts. It has also been studied from a theoretical basis (see Chen et al., [13], Dejonckheere et al., [15], Kim and Ryan [32], Chatfield at el., [11] and Chatfield and Hayya [10]).

The manufacturer also predicts a lead time but here he has to be careful because the previous orders cannot be completely observed. Precisely, using the moving average forecast method with for lead time forecasting we obtain

| (5) |

where are lead times which are guaranteed to have been observed by the manufacturer at the beginning of a period (or earlier) as they are at least periods old (see item d of our discussion of assumptions in 1). Knowing the average lead time (in practice estimating it) we are able to find the average unrealized orders (see Robinson et al., [43] and Disney et al., [18]). However our procedure of collecting lead times avoids bias resulting from the open orders with long lead times that may not have been received when we make the lead time forecast. Thus by (1), (4) and (5) we propose the following forecast for a lead time demand (see also Michna and Nielsen [39]).

| (6) |

It is easy to notice that (6) is a slight modification of (1) when demands and lead times are predicted using the moving average method. The motivation for the lead time demand forecasting given in (6) is also the fact that see (3) (under the assumption that demands and lead times are mutually independent) and employing the natural estimators of and we arrive at (6). Eq. (6) has previously been used by Chatfield et al., [11] in a simulation study that highlighted the relationship between lead time forecasting and the bullwhip effect.

We assume that the manufacturer uses the OUT policy. Let be the desired inventory position at the beginning of a period ,

| (7) |

where TNS is a constant, time invariant, target net stock (safety stock), set to achieve a desired level of availability or to minimize a set of unit inventory holding () and unit backlog () costs via the newsvendor principle, Silver et al., [44]. It is often assumed, in constant lead time scenarios, that the demand and the inventory levels, are normally distributed and thus

holds, where is the cumulative probability density function (cdf) of the standard normal distribution and

is the variance of the forecast error for the lead time demand. In some articles (for example Chen et al., [13]) is defined more practically. That is, instead of the variance, one takes the sample variance of . This complicates the theoretical calculations somewhat and the estimation of increases the bullwhip effect which can be deduced from the fact that Chen et al.’s [13] formula is a lower bound for the bullwhip measure whereas we get an equality.

Note however, in our setting, even when demand is normally distributed, neither the inventory levels, nor the orders, are normally distributed. Rather the stochastic lead times create a multi-modal inventory distribution (as it did in Disney et al., [18]) and the lead time forecasting mechanism creates a multi-modal order distribution (which was not present in the setting considered by Disney et al., [18] as the lead time distribution was assumed to be known beforehand). Thus in our case here, the TNS must be set with

where is the cdf of the inventory levels (arbitrary distribution).

Thus the order quantity placed at the beginning of a period by the OUT policy is

| (8) |

Note that by (6), (7) and (8) the quantity of the order placed by the manufacturer to the supplier depends upon the supplier’s lead time.

Our main purpose is to find and then to calculate the following bullwhip ratio

This is one of the typical supply chain performance measurements (see e.g. Towill et al., [48]).

Proposition 1

The variance of the forecast error over the lead time demand does not depend on that is .

Proof: The variance of the forecast error is the expected value of a function of and whose distribution is independent of . The stationarity of the sequences and and their mutual independence yield the assertion.

Since the variance of the forecast error for the lead time demand is independent of we get from (7) and (8) that

| (9) |

allowing us to derive the exact bullwhip expression.

Theorem 1

The measure of the bullwhip effect has the following form

| (10) |

Proof: The proof of Theorem 1 is given in Appendix 1.

Remarks on Theorem 1 The first summand (10) describes the impact of lead time variability, demand and lead time forecasting and the demand correlation. The second summand shows an impact of lead time forecasting, demand mean and variance and lead time variance on the bullwhip effect. The first two summands are not present in the constant lead time case. The third term gives the amplification of the variance by demand forecasting, the demand correlation and the mean lead time.

If lead times are deterministic that is then the bullwhip effect is described by

which coincides with Eq. 5 in Chen et al., [13]. Note that Duc et al., [20] also obtained the result of Chen et al., [13] in a special case and as an exact value (not a lower bound). Chen et al., [13] obtain this expression as a lower bound because they define the error (see (7)) as the sample variance of , indicating that the estimation of the variance of amplifies the bullwhip effect.

The following limits exist:

| (11) |

| (12) |

| (13) |

It is easy to see from (10) that bullwhip is strictly decreasing in , but this is not true for as there is an odd-even effect in for negative . When then the BM is a linear function in as

| (14) |

which always has a negative gradient in (unless and , in which case the gradient is zero).

For i.i.d. demand the following bullwhip measure exists

| (15) |

which is strictly decreasing in and and the result is consistent with Michna and Nielsen [39]. The derivative of the bullwhip measure in (10) at is

| (16) |

which is always positive when .

As then the following expression defines the bullwhip measure

| (17) |

which is independent of and decreasing in . Notice if

| (18) |

holds. Eq. (18) together with (16) provides a sufficient (but not necessary) condition for the presence of at least one stationary point in the region if (see Fig. 4). Notice that if the lead time is a constant then .

If then

| (19) |

which is decreasing in , but the odd-even impact of can be clearly seen. When is even then

| (20) |

Numerical investigations (see Figs. 4, 6, 8, and 10) seem to suggest that there are no stationary points in the region when is even, but we remain unable to prove so. However this is congruent with our previous results that and .

When is odd then

| (21) |

Finally, if

| (22) |

When (22) holds and there must be at least one stationary point between because of the positive derivative at , see (16). Note this is again a sufficient, but not a necessary condition. Extensive numerical investigations (see Figs. 4 and 6) suggest that only one stationary point exists in this area though we can not prove it. Moreover for large the derivative at is almost zero, see (16) and Figs. 8 to 10.

3 Numerical investigations

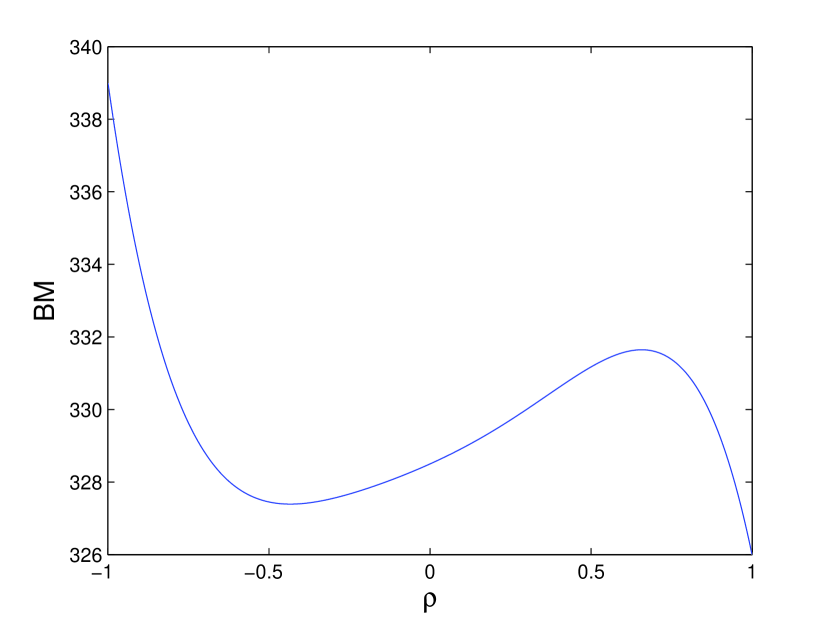

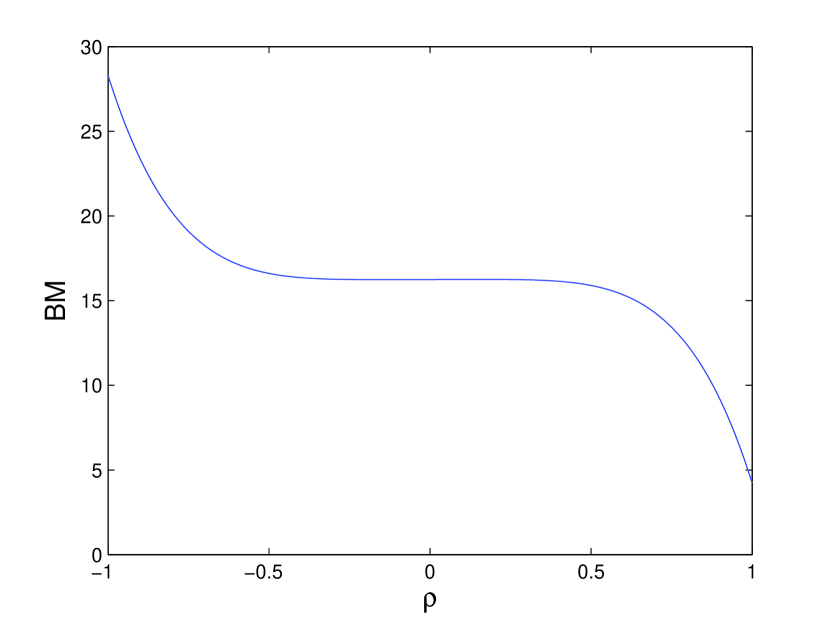

Let us further investigate the influence of the demand correlation on the bullwhip effect by analyzing some concrete numerical examples. We plot the bullwhip effect measure as a function of the demand correlation parameter . Fixing , , , we depict the bullwhip measure in four different scenarios. That is when: and are small, one of them is small and the other is large and both are large. If is small, we need to distinguish two further cases; that is, whether is even or odd.

Thus if and (small and odd ) the bullwhip measure has a minimum at and and a maximum at and (see Fig. 4). The bullwhip measure behavior for and can be predicted by taking the limit as the AR(1) model is well-defined when . In Duc et al., [20] the minimal value of is attained for near or and the maximal value of is for around or . Their results are very close to ours if and are small and is odd (see Fig. 4) because their model does not predict the lead time, corresponding to the small values of and in our model.

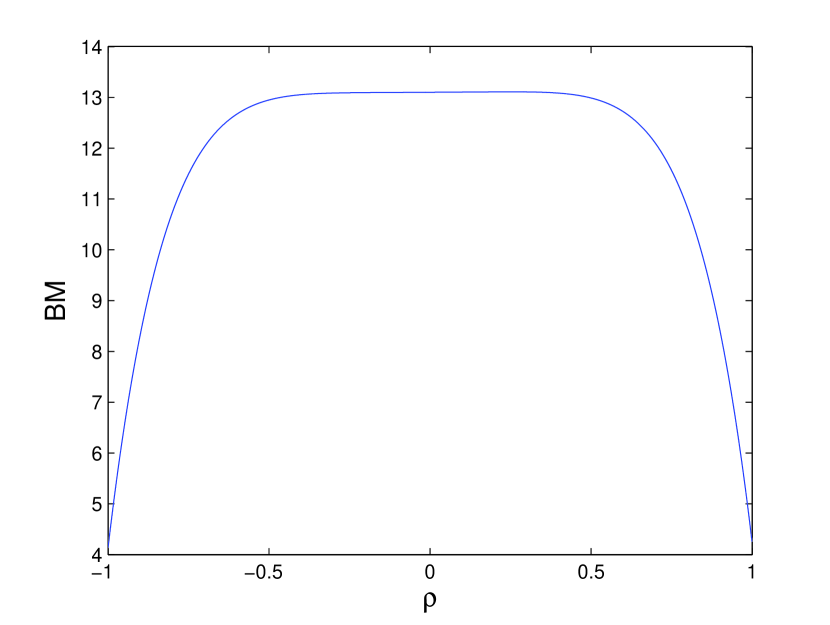

For and (small and even ) we observe a different behavior. Specifically, the smallest value of the bullwhip effect is attained for and the largest for (see Fig. 4). This concurs with Kahn [29] who revealed positively correlated demands result in the bullwhip effect. We also notice that the bullwhip effect is very large if and are small.

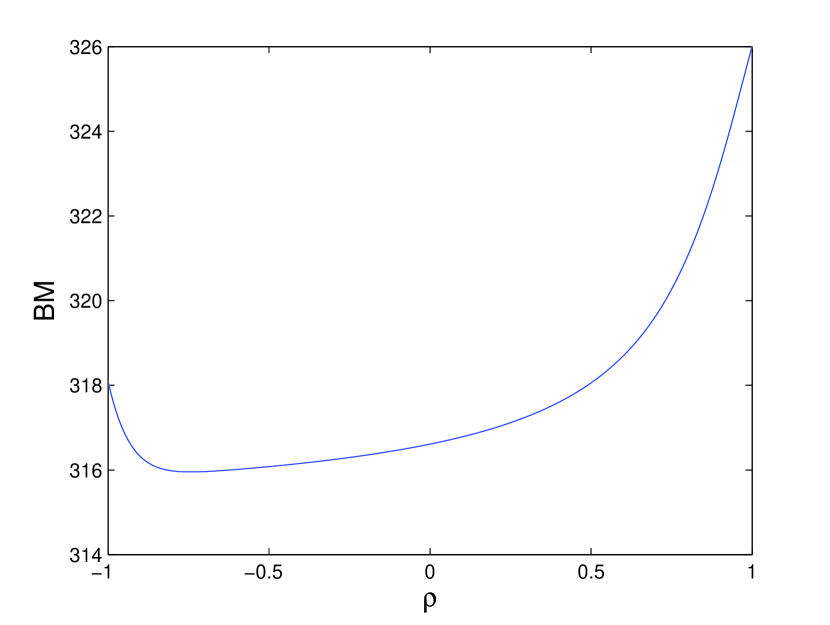

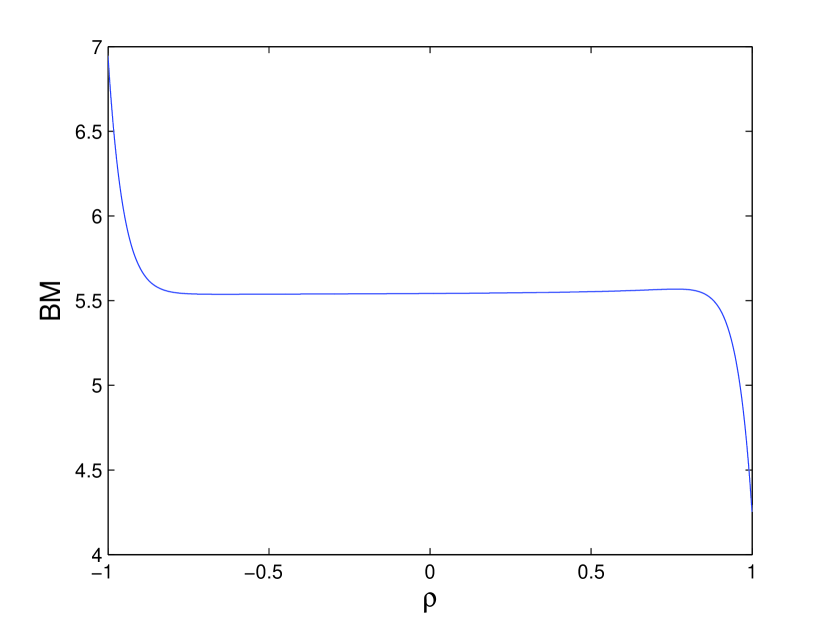

The situation changes if is large and is small (see Figs. 6 and 6). Then the bullwhip measure is almost an increasing function of the demand correlation except for odd and close to where we observe a minimum. Moreover bullwhip increases quite slowly in the region of . The odd-even effects in are now much less noticeable. These observations are consistent with our theoretical analysis in the previous section.

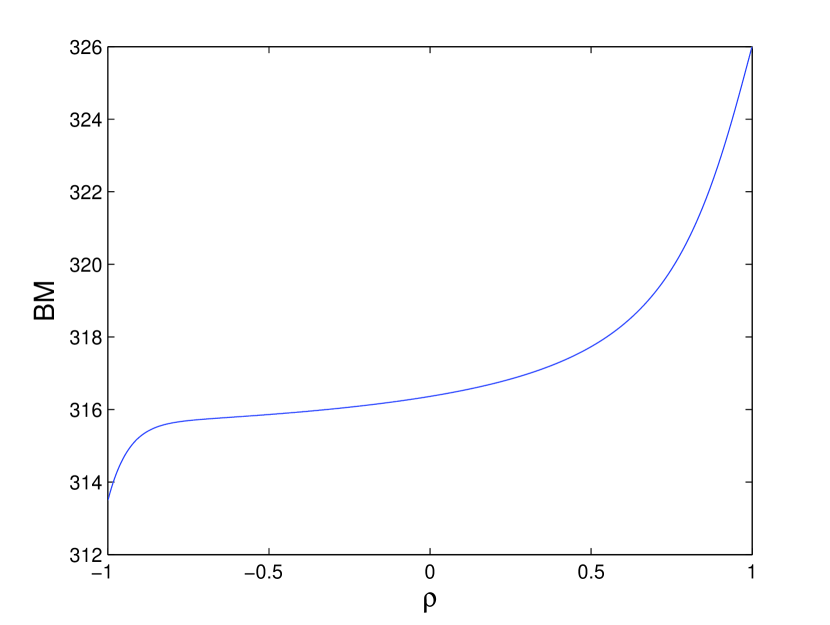

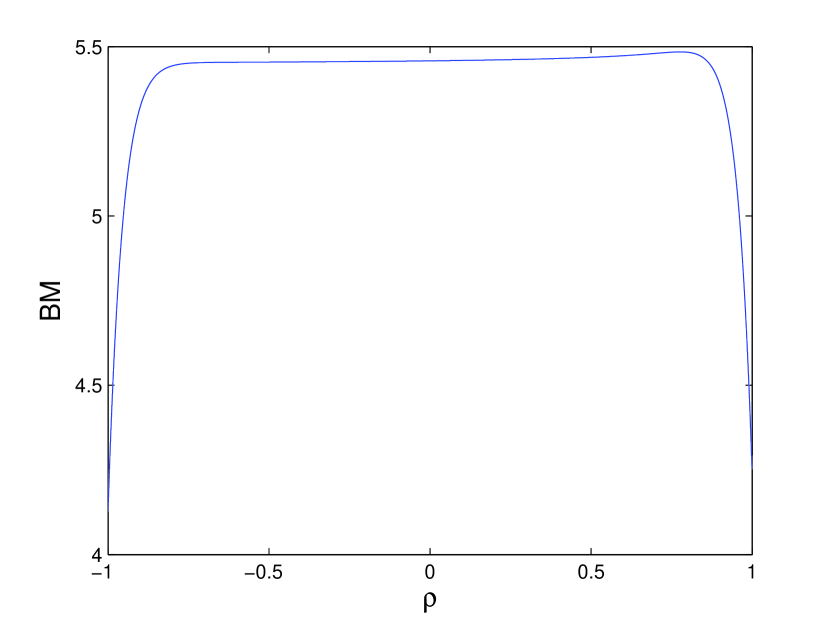

As , the number of periods used in the moving average forecast of the lead time increases, the bullwhip effect becomes independent of the demand correlation regardless of the number of periods used in the moving average forecast of demand, . That is, bullwhip remains almost constant except near . Figs. 8 to 10 confirm this independence for the cases when , , , and . This is caused by the first summand of (10) which vanishes as or and the third summand is rather insensitive to . For close to or the bullwhip effect can dramatically increase or decrease. Moreover much less bullwhip is generated with large values of and . Reduced bullwhip with large is congruent with the results of Disney et al., [18] and Wang and Disney [51].

4 Conclusions and further research opportunities

We quantified the bullwhip effect when demands and lead times must be forecasted. Demand and lead time forecasting are necessary when placing an order if demands and lead times are stochastic. We have confirmed, extended and sharpened the conclusion of Michna and Nielsen [39] that lead time forecasting is a major cause of the bullwhip effect. We assumed that demands constitute a first order autoregressive process and we obtained quantitative results which link bullwhip and the demand correlation when demands and lead times are to be predicted separately. We conclude that how one goes about forecasting demand and lead time is important as it can cause significant amounts of bullwhip. Moreover the dependence of the bullwhip measure on the demand correlation parameter is different according to the forecasting parameters used to make lead time and demand predictions. In particular, an even number of data points in the moving average demand forecast can significantly reduce bullwhip when demand has a strong negative correlation.

Future bullwhip research could be focused on the impact of lead time forecasting under the assumption that lead times are correlated, either temporally, or with other system states such as customer demand. For example if large orders lead to long lead times, there is a correlation between the lead time and the order size and this dependence should be captured somehow. This seems to be difficult to quantify analytically.

Other opportunities lie in studying the impact of different forecasting methods for lead times and demands (see Zhang [52] for the case of demand forecasting). Another big challenge is to quantify bullwhip in the presence of unrealized previous orders when placing an order. More precisely, forecasting the most recent lead times when some orders are not yet received will distort the lead time distribution and have an impact on bullwhip. The quantification of this issue seems to be a difficult task, but it will become important when the lead times are temporally correlated.

An important challenge is the investigation of the variance amplification of orders and the variance amplification of inventory levels simultaneously because an improper focus on bullwhip reduction can amplify the variability of inventory levels (see Chen and Disney [12], Devika et al., [17], Disney at el. [18] and Wang and Disney [51]) which can be as harmful as the bullwhip. Moreover, the POUT replenishment policy, Disney and Towill [19], should be investigated under the assumption of lead time forecasting.

5 Appendix

Proof of Th. 1. We apply the law of total variance to find variance of . Namely, let us put

and then

| (23) |

Using (9) it can be seen that

| (24) | |||||

revealing that . Moreover from the second expression for it follows that

which gives

| (25) |

To calculate the conditional variance of we express it as a function of and the error terms which are mutually independent. Thus by (24) and (2) we get

which gives

| (26) |

where

and

Thus we get

and

To calculate it is necessary to find and by (26). We compute them finding variance and adding the square of the first moment. Thus, to obtain the variance of and , we express them as a sum of independent random variables that is

and

Hence we obtain

and

So we get

| (27) |

and

Summing the last expression we obtain

| (28) | |||||

Plugging (28), (27), (26), (25) into (23) yields the formula from the assertion after a simple algebra.

Acknowledgments

The first author acknowledges support by the National Science Centre grant 2012/07/B//HS4/00702.

References

- [1] Babai, M.Z., Boylan, J.E., Syntetos, A.A., Ali, M.M., 2016. Reduction of the value of information sharing as demand becomes strongly auto-correlated. International Journal of Production Economics, 181, 130–135.

- [2] Bagchi, U., Hayya, J., Chu, C., 1986. The effect of leadtime variability: The case of independent demand. Journal of Operations Management 6, 159–177.

- [3] Bischak, D.P., Robb, D.J., Silver, E.A., Blackburn, J.D., 2014. Analysis and management of periodic review order-up-to level inventory systems with order crossover. Production and Operations Management 23(5), 762–772.

- [4] Boute R.N., Disney, S.M., Lambrecht, M.R., Van Houdt, B., 2008. A win-win solution for the bullwhip problem. Production Planning and Control 19(7), 702–711.

- [5] Boute, R.N., Disney, S.M., Lambrecht, M.R.,Van Houdt, B., 2009. Designing replenishment rules in a two-echelon supply chain with a flexible or an inflexible capacity strategy. International Journal of Production Economics 119, 187–198.

- [6] Boute, R.N., Disney, S.M., Lambrecht, M.R., Van Houdt, B., 2014. Coordinating lead-times and safety stocks under auto-correlated demand. European Journal of Operational Research 232(1), 52–63.

- [7] Bradley, J.R., Robinson, L.W., 2005. Improved base-stock approximations for independent stochastic lead times with order crossover. Manufacturing and Service Operations Management 7(4), 319–329.

- [8] Buchmeister, B., Pavlinjek, J., Palcic, I., Polajnar, A., 2008. Bullwhip effect problem in supply chains. Advances in Production Engineering and Management 3(1), 45–55.

- [9] Chaharsooghi, S.K., Heydari, J., 2010. LT variance or LT mean reduction in supply chain management: Which one has a higher impact on SC performance? International Journal of Production Economics 124, 475–481.

- [10] Chatfield, D.C., Hayya, J.C., 2007. All-zero forecasts for lumpy demand: a factorial study. International Journal of Production Research 45(4), 935–950.

- [11] Chatfield, D.C., Kim, J.G., Harrison, T.P., Hayya, J.C., 2004. The bullwhip effect - Impact of stochastic lead time, information quality, and information sharing: a simulation study. Production and Operations Management 13(4), 340–353.

- [12] Chen, Y.F., Disney, S.M., 2007. The myopic order-up-to policy with a feedback controller. International Journal of Production Research 45(2), pp351–368.

- [13] Chen, F., Drezner, Z., Ryan, J.K., Simchi-Levi, D., 2000. Quantifying the bullwhip effect in a simple supply chain. Management Science 46(3), 436–443.

- [14] Chen, F., Drezner, Z., Ryan, J.K., Simchi-Levi, D., 2000. The impact of exponential smoothing forecasts on the bullwhip effect. Naval Research Logistics 47(4), 269–286.

- [15] Dejonckheere, J, Disney, S.M., Lambrecht M.R., Towill, D.R., 2003. Measuring and avoiding the bullwhip effect: a control theoretic approach. European Journal of Operational Research 147(3), 567–590.

- [16] Dejonckheere, J, Disney, S.M., Lambrecht M.R., Towill, D.R., 2004. The impact of information enrichment on the Bullwhip effect in supply chains: A control engineering perspective. European Journal of Operational Research 153(3), 727–750.

- [17] Devika, K., Jafarian, A., Hassanzadeh, A., Khodaverdi, R., 2015. Optimizing of bullwhip effect and net stock amplification in three-echelon supply chains using evolutionary multi-objective metaheuristics. Annals of Operations Research 242(2), 457–-487.

- [18] Disney, S.M., Maltz, A., Wang, X., Warburton, R.D.H., 2016. Inventory management for stochastic lead times with order crossovers. European Journal of Operational Research 248, 473–486.

- [19] Disney, S.M., Towill, D.R., 2003. On the bullwhip and inventory variance produced by an ordering policy. Omega: The International Journal of Management Science 31, 157–167.

- [20] Duc, T.T.H., Luong, H.T., Kim, Y.D., 2008. A measure of the bullwhip effect in supply chains with stochastic lead time. The International Journal of Advanced Manufacturing Technology 38(11-12), 1201–1212.

- [21] Forrester, J.W., 1958. Industrial dynamics - a major break-through for decision-making. Harvard Business Review 36(4), 37–66.

- [22] Geary, S., Disney, S.M., Towill, D.R., 2006. On bullwhip in supply chains–historical review, present practice and expected future impact. International Journal of Production Economics 101, 2–18.

- [23] Hayya, J.C., Bagchi, U., Kim, J.G., Sun, D., 2008. On static stochastic order crossover. International Journal of Production Economics 114(1), 404–413.

- [24] Hayya, J.C., Harrison, T.P., He, X.J., 2011. The impact of stochastic lead time reduction on inventory cost under order crossover. European Journal of Operational Research 211(2), 274–281.

- [25] Hayya, J.C., Kim, J.G., Disney, S.M., Harrison, T.P., Chatfield, D., 2006. Estimation in supply chain inventory management. International Journal of Production Research 44(7), 1313–1330.

- [26] Hayya, J.C., Xu, S.H., Ramasesh, R.V., He, X.X., 1995. Order crossover in inventory systems. Stochastic Models 11(2), 279–309.

- [27] He, X.X., Xu, S.H., Ord, J.K., Hayya, J.C., 1998. An inventory model with order crossover. Operations Research 46(3), 112-119.

- [28] Hum, S.H., Parlar, M., 2014. Measurement and optimisation of supply chain responsiveness. IIE Transactions 46(1), 1-22.

- [29] Kahn, J.A., 1987. Inventories and volatility of production. American Economic Review 77, 667–679.

- [30] Kaplan, R.S., 1970. A dynamic inventory model with stochastic lead times. Management Science 16(7), 491–507.

- [31] Kim, J.G., Chatfield, D., Harrison, T.P., Hayya, J.C., 2006. Quantifying the bullwhip effect in a supply chain with stochastic lead time. European Journal of Operational Research 173(2), 617–636.

- [32] Kim, H.K., Ryan, J.K., 2003. The cost impact of using simple forecasting techniques in a supply chain. Navel Research Logistics 50, 388–411.

- [33] Lee, H.L., Padmanabhan, V., Whang, S., 1997. The bullwhip effect in supply chains. Sloan Management Review 38(3), 93–102.

- [34] Lee, H.L., Padmanabhan, V., Whang, S., 1997. Information distortion in a supply chain: the bullwhip effect. Management Science 43(3), 546–558.

- [35] Lee, H.L., So, K.C., Tang, C.S., 2000. The value of information sharing in a two-level supply chain. Management Science 46(5), 626–643.

- [36] Luong, H.T., 2007. Measure of bullwhip effect in supply chains with autoregressive demand process. 2007. European Journal of Operational Research 180, 1086–1097.

- [37] Luong, H.T., Pien, N.H., 2007. Measure of bullwhip effect in supply chains: the case of high order autoregressive demand process. European Journal of Operational Research 183, 197–209.

- [38] Mitchell, T., 1923. Competitive illusion as a cause of business cycles, Quarterly Journal of Economics 38, 631–652.

- [39] Michna, Z., Nielsen, P., 2013. The impact of lead time forecasting on the bullwhip effect. Preprint available online at http://arxiv.org/abs/1309.7374.

- [40] Michna, Z., Nielsen, I.E., Nielsen, P., 2013. The bullwhip effect in supply chains with stochastic lead times. Mathematical Economics 9, 71–88.

- [41] Michna, Z., Nielsen, P., Nielsen, I.E., 2014. The impact of stochastic lead times on the bullwhip effect. Preprint available online at http://arxiv.org/abs/1411.4289.

- [42] Riezebos, J., 2006. Inventory order crossovers. International Journal of Production Economics 104, 666-675.

- [43] Robinson, L.W., Bradley, J.R., Thomas, L.J., 2001. Consequences of order crossover under order-up-to inventory policies. Manufacturing and Service Operations Management 3(3), 175–188.

- [44] Silver, E.A., Pyke, D.F., Peterson, R., 1998. Inventory management and production planning and scheduling. Third Edition. John Wiley & Sons, New York.

- [45] So, K.C., Zheng, X., 2003. Impact of supplier’s lead time and forecast demand updating on retailer’s order quantity variability in a two-level supply chain. International Journal of Production Economics 86, 169–179.

- [46] Song, J., 1994. The effect of leadtime uncertainty in simple stochastic inventory model. Management Science 40, 603–613.

- [47] Song, J., 1994. Understanding the leadtime effects in stochastic inventory systems with discounted costs. Operations Research Letters 15, 85–93.

- [48] Towill, D.R., Zhou, L., Disney, S.M., 2007. Reducing the bullwhip effect: Looking through the appropriate lens. International Journal of Production Economics 108, 444–453.

- [49] Tyworth, J.E., O’Neill,L., 1997. Robustness of the normal approximation of lead-time demand in a distribution setting. Naval Research Logistics 44(2), 165–186.

- [50] Wang, X., Disney, S.M., 2016. The bullwhip effect: progress, trends and directions. European Journal of Operational Research 250, 691–-701.

- [51] Wang, X., Disney, S.M., 2017. Mitigating variance amplifications under stochastic lead-time: The proportional control approach. European Journal of Operational Research 256(1), 151–162.

- [52] Zhang, X., 2004. The impact of forecasting methods on the bullwhip effect. International Journal of Production Economics 88, 15–27.

- [53] Zipkin, P., 1986. Stochastic leadtimes in continuous-time inventory models. Naval Research Logistics Quarterly 33, 763–774.