Martingale optimal transport with stopping

Abstract.

We solve the martingale optimal transport problem for cost functionals represented by optimal stopping problems. The measure-valued martingale approach developed in [6] allows us to obtain an equivalent infinite-dimensional controller-stopper problem. We use the stochastic Perron’s method and characterize the finite dimensional approximation as a viscosity solution to the corresponding HJB equation. It turns out that this solution is the concave envelope of the cost function with respect to the atoms of the terminal law. We demonstrate the results by finding explicit solutions for a class of cost functions.

Key words and phrases:

martingale optimal transport, dynamic programming, optimal stopping, stochastic Perron method, viscosity solutions, concave envelope, distribution constraints2010 Mathematics Subject Classification:

60G40, 93E20, 91A10, 91A60, 60G07.1. Introduction

The aim of this article is to solve a class of martingale optimal transport problems for which the cost functional can be represented as an optimal stopping problem of the underlying cost function. Specifically, given a continuous and bounded cost function we are interested in solving the martingale optimal transport problem

| (1.1) |

The outer supremum is taken over - the set of all pairs of filtered probability spaces and continuous martingales on them such that the filtration is generated by a Brownian motion and the terminal law is under . The inner stopping problem is over - the set of all -stopping times taking values in for and some fixed terminal time .

The duality between martingale optimal transport and robust pricing problems was studied in a related setting in Dolinsky and Soner [8] for general path-dependent European-type cost functionals (i.e. payoffs) and continuous models. Recently Bayraktar and Miller [1] and Beiglböck et al. [5] obtained solutions to distribution-constrained optimal stopping problems by using dynamic programming and martingale transport methods, respectively. In contrast to our setting, however, the constraints in [1] and [5] are on the distribution of the stopping times and not on the marginal distribution at the terminal time. By using the concept of measure-valued martingales Cox and Kallbläd [6] studied the robust pricing of Asian-type options subject to a marginal distribution constraint. The authors cast the original problem into a control theoretic framework and obtained a viscosity characterization of the solution.

Here we employ the control theoretic approach of [6] and [1] to analyze optimal martingale transport problems with cost functionals which are of American type. The difficulty in our setting is that we have an additional optimal stopping component. However, the fact that we optimize over continuous models allows us to prove that the resulting value function is time-independent up to the terminal time. Since the original problem is infinite dimensional we use the continuity with respect to the terminal law to restrict it only to measures with finitely many atoms. Working in a Brownian filtration allows us to recast this finite dimensional approximation as a recursive sequence of controller-stopper problems with exit-time components. We prove that the value functions of these problems are viscosity solutions to the corresponding sequence of elliptic obstacle problems satisfying exact Dirichlet boundary conditions. We achieve this by applying the stochastic Perron’s approach in the spirit of Bayraktar and Sirbu [4] where the obstacle problems are associated with Dynkin games and Rokhlin [14] where an elliptic Dirichlet boundary problem arose from exit-time stochastic control. We circumvent the potential difficulty of proving a strong comparison result for viscosity sub/supersolutions satisfying generalized boundary conditions (see [14]) by using the recursive structure of the problem to show the exact attainment of these boundary conditions.

The main result in this paper, Theorem 3.1, is the characterization of the value function of the finite dimensional martingale transport problem as the concave envelope of the pay-off with respect to the probability weights of the terminal law’s atoms. In this final step we use a recent result of Oberman and Ruan [11] on characterizing convex envelopes as unique viscosity solutions to obstacle problems with appropriate Dirichlet boundary conditions. One possible application of our results is the robust pricing of American options. Indeed, the martingales over which we optimize can be seen as different models for the stock price with a given marginal distribution at the terminal time.

The rest of the paper is organized as follows: In Section 2, we formulate the finite dimensional approximation of the Martingale Optimal Transport problem, see (2.12). In Section 3, we employ the stochastic Perron’s method to characterize the value function as the unique viscosity solution of the corresponding Dirichlet obstacle problem and to show its concave envelope form in an appropriate phase space. Section 4 illustrates how our results can be achieved in a probabilistic framework and provides concrete examples.

2. Problem formulation

We define the set of measures as

and suppose that the terminal law of the martingales in the optimal transport problem (1.1) satisfies . In the usual optimal transport framework we can regard the probability measures contained in as transporting the initial Dirac measure (i.e. the law of ) to the terminal law under the cost functional - both of these laws are known at time . On the other hand, notice that the continuous martingale satisfies

| (2.1) |

where is the conditional law of given under the measure . In particular, we have that and . Therefore, similarly to the method proposed in [6], we can rewrite (1.1) in its measure-valued martingale formulation as

| (2.2) |

where is the set of all terminating measure-valued (i.e. -valued) martingales (see Definition 2.7 in [6]) such that is a continuous process a.s. with respect to the filtered probability space for all , where is a Brownian filtration. Moreover, as in [6], we fix the probability space which does not materially change our conclusions.

Let us write (2.2) in the Markovian form

| (2.3) |

and note that we have the following variant of Lemma 3.1 in [6] the proof of which can be found in the appendix:

Lemma 2.1.

If is non-negative and Lipschitz then the function is continuous in (in the Wasserstein-1 topology) and independent of for .

The continuity in allows us to apply the finite dimensional reduction from Section 3.2 in [6]. In particular, we introduce the set where and let and for any , where resp. denote the sets of all measures on resp. . We assume from now on that the terminal law (i.e. also ) is an atomic measure and satisfies . Since we work in a Brownian filtration, by martingale representation for any terminating -valued martingale it is true that the (nonnegative) martingales solve an SDE of the form

| (2.4) |

for and , where the vector of weights satisfies , and implies that . The following result, by analogy to Corollary 3.6 in [6], follows directly from Lemma 3.4 in [6] and allows us to work with a bounded set of controls:

Lemma 2.2.

Under the above assumption that , the value function in (2.3) for reduces to the value function

| (2.5) |

where the admissible control set is defined as

with the disk being the intersection of the open unit ball with the hyperplane in , and is the continuous inverse of

| (2.6) |

where the strictly positive time change rate process satisfies

| (2.7) |

The role of the time change in (2.6) is to stretch/compress the original time scale so as to bound the volatility of the state process (i.e. the control process ). Thus we avoid technical difficulties arising from unbounded control sets later when proving the viscosity characterization of the value function.

Now notice that the value function can be identified with where for , and , with , we introduce the sequence of problems

| (2.8) |

with

| (2.9) | ||||

| (2.10) |

and for . From now on we will denote the time changed filtration as and suppress its dependence on for notational purposes. The following lemma shows that we can ignore controls which are small enough and that we can work with stopping times in the time changed filtration.

Lemma 2.3.

The value function can be written as

| (2.11) |

where for any and is the set of all -stopping times for an appropriately time changed filtration .

Proof.

For any time change rate we have for and from (2.7) it follows that . Moreover, since is strictly positive, we have that and are strictly increasing. It follows immediately that if is an -stopping time then is a -stopping time and, conversely, if is a -stopping time then is an -stopping time. Therefore in (2.8) we can substitute with and with .

What is left is to prove that we can take the outer supremum in (2.8) over . For and any we can choose defined as where

and is the right-continuous inverse of the (non-strictly) increasing continuous function given by

From (2.4) we see that (corresponding to the control ) has the same distribution as (corresponding to the control ). Hence, for any -stopping time we have that is a -stopping time such that has the same law as . We conclude from (2.8). ∎

Before going further we introduce some additional notation. Let be the subset of elements in to which the atomic measure prescribes nonzero probability and notice that we have the consistency conditions

For every with it is true that where . Hence, we can identify every with the vector where and . We let

| (2.12) |

where . For any and we also let , where is the unique strong solution to (2.4) with control and initial condition for . Denote by the -valued martingale corresponding to , i.e. . For short we let and .

3. Viscosity characterization of the value function using stochastic Perron’s method

We want to obtain the viscosity characterization of the value function . Fix and with for some integer . Using (2.12) rewrite the value function from (2.11) as

| (3.1) |

where . Our aim is to show that is the unique viscosity solution (see e.g. Definition 7.4 in [7]) to the associated Dirichlet obstacle problem given by

| (3.2) | ||||

| (3.3) |

where and correspond to the nonzero components of and , and . The derivative is to be understood in the directional sense - i.e. we restrict ourselves to second directional derivatives w.r.t. directions lying in the set .

We are now ready to state the main result of the paper - its proof relies on the stochastic Perron’s method and we present it in the next section.

Theorem 3.1.

The function defined in (3.1) is the unique continuous viscosity solution of the obstacle problem (3.2) satisfying the Dirichlet boundary condition (3.3). Moreover, is the concave envelope of on - i.e. denoting the projection of onto by and the projected functions as

| (3.4) | ||||

| (3.5) |

the function is the concave envelope of .

3.1. Proof of Theorem 3.1

We begin by introducing the notions of stochastic sub- and supersolutions.

Definition 3.1.

The set of stochastic subsolutions to the PDE (3.2) with the boundary condition (3.3), denoted by , is the set of functions that have the following properties:

-

(i)

They are continuous and bounded, and satisfy the boundary condition

(3.6) -

(ii)

For each and with there exists a control such that for any with we have a.s. that

(3.7) where the -stopping times and are defined as

(3.8) (3.9)

Definition 3.2.

The set of stochastic supersolutions to the PDE (3.2) with the boundary condition (3.3), denoted by , is the set of functions that have the following properties:

-

(i)

They are continuous and bounded, and satisfy the boundary condition

(3.10) -

(ii)

For each and with , for any control and any with we have a.s. that

(3.11) where is defined as in (3.8).

Clearly (resp. ) is nonempty since is bounded from below (resp. above) and any constant which is small (large) enough belongs to (resp. ). Actually, we can easily verify that . The following lemma proves an important property of the sets and .

Lemma 3.1.

For any two we have that . For any two we have that .

Proof.

We will only prove the first part of the lemma - the second part follows in a similar way. Denote and notice that item (i) in Definition 3.1 is clearly satisfied by . Now fix and as in item (ii) of Definition 3.1 and introduce the sequence of stopping time, control and state process triples defined recursively as follows:

where are the controls corresponding to the stochastic subsolutions starting at the pair , and for :

-

(i)

if then we set

-

(ii)

if for then we set

where is the control process corresponding to the stochastic subsolution starting at the pair , and is defined as in (3.9).

Define the control by

and notice that by construction for and any . For any stopping time denote . By the definition of the sequence we get that

and by iterating the above we conclude that

| (3.12) |

for any . Now we apply the same reasoning as in the proof of Lemma 2.3 in [4] to conclude that

By taking in (3.12) and using the bounded convergence theorem we finally obtain that satisfies (3.7) and, hence, is a stochastic subsolution. ∎

We introduce the assumption:

Assumption 3.1.

The boundary function is continuous on .

Proposition 3.1.

Proof.

The proof uses ideas from Theorem 3.1 (and Theorem 4.1) in [3] and Theorem 2 in [14]. We repeat the key steps for the lower stochastic envelope .

Denote for short . It is clear that since in item (ii) of Definition 3.1 we can choose , a constant and for some control , and use the condition (3.6) and (3.9).

We will prove the viscosity supersolution property of by contradiction. Take a test function such that achieves a strict local minimum equal to 0 at some boundary point (the case when is simpler). Assume that is not a viscosity supersolution and hence

where

It follows that there exists such that

| (3.13) |

By the continuity of , and the lower semicontinuity of we can find a small enough open ball and a small enough such that

Using Proposition 4.1 in [2] together with Lemma 3.1 above, we obtain an increasing sequence of stochastic subsolutions with . In particular, since and the ’s are continuous we can use an argument identical to the one in Lemma 2.4 in [4] to obtain for any fixed a corresponding such that

Now we can choose small enough such that satisfies

We define

and notice that is continuous and . Since condition (3.6) clearly also holds, we see that satisfies item (i) of Definition 3.1. What is left is to check item (ii) in Definition 3.1 and obtain which will lead to a contradiction since .

Choose and with , and, similarly to the proof of Lemma 3.1 above, introduce the sequence of stopping time, control and state process triples defined recursively as follows:

where is the control corresponding to the stochastic subsolution starting at the pair , the event is given by

and for :

-

(i)

if then we set

- (ii)

-

(iii)

otherwise we set

where is the control process corresponding to the stochastic subsolution starting at the pair .

By construction we have that where the control is defined as

Introduce the event

and notice that for each there exists such that

| (3.14) | ||||

| (3.15) | ||||

| (3.16) |

for . Denoting and noticing that for we take the limit in (3.16) to obtain

| (3.17) |

Now assume there exists such that for each we have

and conclude from (3.14)-(3.15) that there exists large enough positive integer such that for all we have

By taking above we get on . Hence, by using (3.17) we see that

on . On the other hand, on we have

and again from (3.17) we get

on . It follows that on and from the definition of we conclude that .

Now take any with , let and notice that, by Itô’s formula applied to and the subsolution property of , we have

and by iterating the above we conclude that

| (3.18) |

By taking in (3.18) and using the bounded convergence theorem we obtain that satisfies item (ii) in Definition 3.1 Hence and we obtain contradiction and consequently the supersolution property of . ∎

Assumption 3.2.

The boundary function is the concave envelope of on the simplex faces for all .

Proposition 3.2.

Under Assumption 3.2 we have that on .

Proof.

Let be the concave envelope of on the whole of . From Assumption 3.2 it follows that on and satisfies item (i) of Definition 3.2. Now take any , with , and with , and notice that, by the Itô-Tanaka formula (see e.g. Theorem VI.1.5 in [13]) applied to the concave function we have

where is the left derivative, the second derivative is understood in the sense of a negative measure and is the local time at of the process . Hence, item (ii) of Definition 3.2 is also satisfied and is a stochastic supersolution. Since satisfies (3.10) and it follows that on .

Fix a constant control and define the function by

| (3.19) |

The continuity of follows from the boundedness of the control and standard results on optimal stopping problems (see e.g. Theorem 3.1.5 in [9]). We have that for and we obtain that item (i) of Definition 3.1 is satisfied. Moreover, the optimal stopping time in (3.19) exists and is equal to and it follows that is a martingale (see e.g. Theorems I.2.4 and I.2.7 in [12]). This means that (3.7) is satisfied with equality and is a stochastic subsolution. By definition we know that on and . Hence, we conclude that on . ∎

Proof of Theorem 3.1.

It is clear that if then where for some and . We continue by induction and assume that we have proven the statement for all . By the induction hypothesis is the concave envelope of on the corresponding to simplex face and hence Assumption 3.2 is satisfied. Moreover, value functions coincide on the intersection of their corresponding simplex faces, and therefore Assumpton 3.1 is also satisfied. Define the Hamiltonian as

and notice that for small enough the set contains all directions in . On the other hand, is a viscosity solution to (3.2) on if and only if the projected function defined in (3.4) is a viscosity solution of

| (3.20) |

on , where is the projection of onto . Hence, the function is a viscosity solution to if and only if is a viscosity solution to , where is the largest eigenvalue of the Hessian . Therefore we can apply Theorem 1 in [10] to obtain that any continuous viscosity solution to (3.20) is concave. Moreover, uniqueness of the solution to (3.20) together with the projected boundary condition

| (3.21) |

follows from the comparison principle for Dirichlet problems stated in Theorem 2.10 of [11]. This leads to uniqueness and comparison principle for our original problem (3.2)-(3.3). In particular, by Propositions 3.1 and 3.2 we have that on . On the other hand, by Proposition 3.1 we also have on . Therefore, we can conclude that on and is the unique viscosity solution of (3.2) with the boundary condition (3.3), and the same is true for the projected versions.

Remark 3.1.

The value function can be regarded as the concave envelope on the simplex of the modified cost function . Indeed, we can ignore one direction in the state space vector due to the fact that is a k-dimensional simplex and any concave function on a k-dimensional simplex in is concave in any of its variables (and vice versa). Note that the optimal control weight vector may not be unique. It is determined by the direction on the simplex for which the second directional derivative of the value function is zero - if the value function is linear at a point then clearly many directions satisfy this condition.

Remark 3.2.

When applying the stochastic Perron method to controlled exit time problems one needs a comparison result for the corresponding PDE in order to characterize the value function as a viscosity solution (see e.g. Definition 2 and Remark 1 in [14]). These comparison results are of a slightly different nature than the standard ones of e.g. Theorems 7.9 and 8.2 in [7] - the latter require an apriori knowledge of the behaviour of the stochastic semisolutions at the boundary. We were able to exploit the specific structure of our exit time problem in Proposition 3.2 to obtain the behaviour at the boundary of the stochastic semisolutions. This allowed the application of the comparison result in [11].

4. Examples

Let us first provide some intuition behind the choice of optimal controls and stopping times. We will consider a general class of cost functions - namely all bounded, non-negative Lipschitz continuous functions . This is the class for which Theorem 3.1 holds. We will use our concave envelope characterization to choose the optimal controls and verify that Brownian exit times are optimal.

We abuse notation and regard as a function on the projected set of probability vectors . Denote by the concave envelope of on . For any initial probability vector corresponding to some terminal law , e.g.

we will find a candidate optimal control weight process taking values in the projected admissible set (i.e. the projection of onto ) and a candidate optimal stopping time such that the resulting value function will be .

The usual characterization of optimal stopping times leads us to choose the candidate as

| (4.1) |

In particular, if the initial probability vector is such that we can simply set . Assume now that and note that the point belongs to a planar region of the graph of that contains a point such that . In other words, all points on the line between and are also part of the graph of . We choose the control weight process as a constant vector in the direction of , i.e. , where the constant is such that is admissible. Therefore the probability vector process evolves along the direction and either hits the point or hits the boundary of at some point . The point can be regarded as belonging to a lower dimensional projected set where . If , we repeat the same procedure when choosing a control on this lower dimensional set - clearly this can happen at most times.

For simplicity’s sake assume that . In other words, by looking at (2.4) and (4.1), we get that is the first exit time of a Brownian motion from the interval with endpoints and . Using the formula for the Brownian exit times from an interval we obtain that the projected value function as defined in (3.4) satisfies

and the point lies on the line going through and , hence . Similar calculation is valid for the case .

Finally, by application of the Itô-Tanaka formula as in the proof of Proposition 3.2 we conclude that bounds the value function from above, and therefore the two coincide.

Remark 4.1 (Generalized Put options).

In fact, if the cost function is of the form

for some concave function , by direct calculation we can check that the candidate control and stopping time described above are optimal among those controls that follow a fixed direction and those stopping times that are Brownian exit times from an interval. By applying Theorem 3.1 we see that optimization over this class is sufficient.

In what follows, using the observations above, we will construct the optimal controls and stopping times explicitly for a piece-wise linear cost function which can be thought of as a call option spread.

4.1. Call option spread

We let take the form

for , and , which can be seen as a bull call spread. Set , and assume that the law of is given by

for such that . Therefore, the initial probability vector is

where . From the definition of the process in (2.1) it follows that

| (4.2) |

where and for . We introduce the constants , , and corresponding to the value of taking various atoms of into account. We use the notation and .

We will now describe how to obtain a guess for the value function which, as expected, will turn out to be the concave envelope of the modified cost function . Notice that is nondecreasing and achieves its maximum for any and its minimum for any . Therefore, for the martingale state process (or equivalently the law process ), we want to offset any decrease of probability mass on the interval with a corresponding decrease on the interval . We consider the following cases:

-

(1)

Assume . Then it is optimal to stop immediately, i.e. choose an optimal stopping time and obtain .

-

(2)

Assume and let the constant be such that . Then it is optimal to choose a stopping time and a control process for any , where the constant is such that is an admissible control and the optimal stopping time is the first exit time of from the interval . Note that this choice of is not unique.

Equivalently, by using (4.2), we see that is the first exit time of from the interval . This corresponds to letting the law evolve until the stopping time when it separates into two measures of the form

By the definition of we have that and therefore .

-

(3)

Assume and let the constant be such that . Then we choose a stopping time and a control process for any , where the constant is such that is an admissible control and the stopping time is the first exit time of from the interval . Equivalently, by using (4.2), we see that is the first exit time of from the interval . This corresponds to letting the law evolve until time when it separates into two measures of the form

In addition, if , we choose the optimal stopping time as and we have . This is due to the fact that if (i.e. the atom dies) it is not worth to evolve the law further because the cost function will be under any combination of the atoms . In other words we gain nothing from transferring probability mass between the atoms and .

On the other hand, if we also have that , on the event we let the control process be for and set the optimal stopping time

where the stopping time is the first exit time of from the interval for . Equivalently, by using (4.2), we see that is the first exit time of from the interval for . This corresponds to further evolving the law until at the stopping time it splits into three measures of the form

Therefore we have

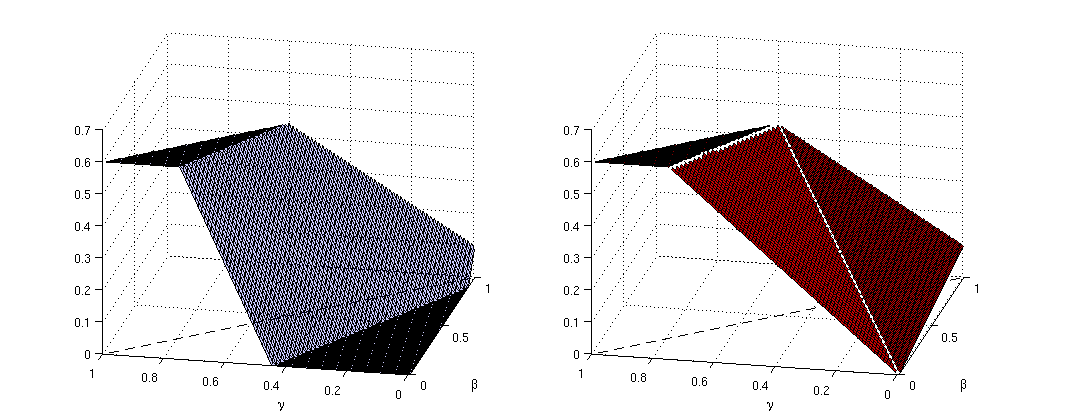

The candidate value function is given by

and it is the concave envelope of (see Figure 1). 111It turns out that the value function in this example is the same as in the Asian option setting of [6]; see the example in Section 4.2 therein. This is because under their optimal model the stock price is a fixed random variable which is given by the average of our measure valued martingale at using (2.1).

Appendix A Proof of Lemma 2.1

Proof.

In order to prove the independence in the variable we choose and notice that . Indeed, the supremum in (2.3) corresponding to is taken over a larger set of stopping times than the one corresponding to . Conversely, for any and we can choose and such that

with and . This choice leads to

which allows us to conclude that and hence and we have independence in for .

To prove the continuity in we first observe (e.g. see Lemma 3.1 in [6]) that if with and (here is the Wasserstein-1 metric) then there is with such that for all with some fixed . Indeed, we know that and we can define

where the Borel family of probability measures is obtained by the disintegration of the transport plan such that , and . By optional stopping we get

and hence

Denote by the process corresponding to the measure-valued martingale from (2.1). By the Lipschitz property of and the above inequality we get

Now fix and consider such that . From the reasoning above, we can choose with and such that and . Therefore we obtain

and by symmetry we get and continuity follows.

References

- [1] E. Bayraktar and C. W. Miller. Distribution-constrained optimal stopping. Mathematical Finance. To appear.

- [2] E. Bayraktar and M. Sirbu. Stochastic Perron’s method and verification without smoothness using viscosity comparison: the linear case. Proceedings of the American Mathematical Society, 140(10):3645–3654, 2012.

- [3] E. Bayraktar and M. Sirbu. Stochastic Perron’s method for Hamilton–Jacobi–Bellman equations. SIAM Journal on Control and Optimization, 51(6):4274–4294, 2013.

- [4] E. Bayraktar and M. Sirbu. Stochastic Perron’s method and verification without smoothness using viscosity comparison: obstacle problems and Dynkin games. Proceedings of the American Mathematical Society, 142(4):1399–1412, 2014.

- [5] M. Beiglböck, M. Eder, C. Elgert, and U. Schmock. Geometry of distribution-constrained optimal stopping problems. 2016, Preprint.

- [6] A. M. G. Cox and S. Källblad. Model-independent bounds for Asian options: a dynamic programming approach. To appear in SIAM Journal on Control and Optimization, 2017.

- [7] M. G. Crandall, H. Ishii, and P.-L. Lions. User’s guide to viscosity solutions of second order partial differential equations. Bulletin of the American Mathematical Society, 27(1):1–67, 1992.

- [8] Y. Dolinsky and H. M. Soner. Martingale optimal transport and robust hedging in continuous time. Probability Theory and Related Fields, 160(1-2):391–427, 2014.

- [9] N.V. Krylov. Controlled Diffusion Processes. Stochastic Modelling and Applied Probability. Springer Berlin Heidelberg, 2008.

- [10] A. M. Oberman. The convex envelope is the solution of a nonlinear obstacle problem. Proceedings of the American Mathematical Society, 135(6):1689–1694, 2007.

- [11] A. M. Oberman and Y. Ruan. A partial differential equation for the rank one convex envelope. Archive for Rational Mechanics and Analysis, 224(3):955–984, 2017.

- [12] G. Peskir and A. N. Shiryaev. Optimal Stopping and Free-Boundary Problems. Birkhäuser, Basel, 2006.

- [13] D. Revuz and M. Yor. Continuous Martingales and Brownian Motion. Springer, 1999.

- [14] D. B. Rokhlin. Verification by stochastic Perron’s method in stochastic exit time control problems. Journal of Mathematical Analysis and Applications, 419(1):433–446, 2014.