Bank monitoring incentives under moral hazard and adverse selection 111The authors gratefully acknowledges the support of the French Ministry of Foreign Affairs and the Merlion programme.

Abstract

In this paper, we extend the optimal securitisation model of Pagès [50] and Possamaï and Pagès [51] between an investor and a bank to a setting allowing both moral hazard and adverse selection. Following the recent approach to these problems of Cvitanić, Wan and Yang [14], we characterise explicitly and rigorously the so-called credible set of the continuation and temptation values of the bank, and obtain the value function of the investor as well as the optimal contracts through a recursive system of first-order variational inequalities with gradient constraints. We provide a detailed discussion of the properties of the optimal menu of contracts.

Key words: bank monitoring, securitisation, moral hazard, adverse selection, principal–agent problem

AMS 2000 subject classification: 60H30, 91G40

JEL classifications: G21, G28, G32

1 Introduction

Principal–Agent problems with moral hazard have an extremely rich history, dating back to the early static models of the 70s, see among many others Zeckhauser [68], Spence and Zeckhauser [63], or Mirrlees [42, 43, 44, 45], as well as the seminal papers by Grossman and Hart [26], Jewitt, [33], Holmström [30] or Rogerson [57]. If moral hazard results from the inability of the Principal to monitor, or to contract upon, the actions of the Agent, there is a second fundamental feature of the Principal-Agent relationship which has been very frequently studied in the literature, namely that of adverse selection, corresponding to the inability to observe private information of the Agent, which is often referred to as his type. In this case, the Principal offers to the Agent a menu of contracts, each having been designed for a specific type. The so-called revelation principle, states then that it is always optimal for the Principal to propose menus for which it is optimal for the Agent to truthfully reveal his type. Pioneering research in the latter direction were due to Mirrlees [46], Mussa and Rosen [47], Roberts [55], Spence [62], Baron and Myerson [7], Maskin and Riley [38], Guesnerie and Laffont [27], and later by Salanié [59], Wilson [67], or Rochet and Choné [56]. However, despite the early realisation of the importance of considering models involving both these features at the same time, the literature on Principal-Agent problems involving both moral hazard and adverse selection has remained, in comparison, rather scarce. As far as we know, they were considered for the first time by Antle [2], in the context of auditor contracts, and then, under the name of generalised Principal-Agent problems, by Myerson [48]555There were earlier attempts in this direction, but providing a less systematic treatment of the problem; see the income tax model of Mirrlees [46], the Soviet incentive scheme study of Weitzman [66], or the papers by Baron and Holmström [6] and Baron [3].. These generalised agency problems were then studied in a wide variety of economic settings, notably by Dionne and Lasserre [17], Laffont and Tirole [35], McAfee and McMillan [39], Picard [54], Baron and Besanko [4, 5], Melumad and Reichelstein [40, 41], Guesnerie, Picard and Rey [28], Page [49], Zou [69], Caillaud, Guesnerie and Rey [10], Lewis and Sappington [36], or Bhattacharyya [8]666We refer the interested reader to the more recent works of Faynzilberg and Kumar [22], Theilen [65], Jullien, Salanié and Salanié [34], Gottlieb and Moreira [25]..

All the previously mentioned models are either in static or discrete–time settings. The first study of the continuous time problem with moral hazard and adverse selection was made by Sung [64], in which the author extends the seminal finite horizon and continuous–time model of Holmström and Milgrom [31]. A more recent work, to which our paper is mostly related has been treated by Cvitanić, Wan and Yang [14], where the authors extend the famous infinite horizon model of Sannikov [60] to the adverse selection setting. If one of the main contributions of Sannikov [60] was to have identified that the continuation value of the Agent was a fundamental state variable for the problem of the Principal, [14] shows that in a context with both moral hazard and adverse selection, the Principal has also to keep track of the so-called temptation value, that is to say the continuation utility of the Agent who would not reveal his true type. Although close to the latter paper, our work is foremost an extension of the bank incentives model of Pagès and Possamaï [51], which studies the contracting problem between competitive investors and an impatient bank who monitors a pool of long term loans subject to Markovian contagion (we also refer the reader to the companion paper by Pagès [50] for the economic intuitions and interpretations of the model).

The home loan crash of 2008 has strongly highlighted the inherent weaknesses of the securitisation agreements created during the 2000s, and was at the heart of the decision from the US government to impose tight deadlines for the adoption of new and tighter regulations for credit risk retention. Among these, one of particular interest for us is the Dodd–Frank Act, which prescribes that sponsors retain at least five percent of the credit risk in most securitisation transactions. The purpose of [50, 51] was to study optimal securitisation when the sponsor remains involved with its retail originations, and can engage in unobservable actions that result in private benefits at the expense of performance. The assumption that the bank itself can have impact on the default rate of the pool over time is a metaphor for the distinction between its exogenous base quality and the endogenous default probability obtained after monitoring. Moral hazard then emerges because the bank has more "skin in the game" than the investors, and has the opportunity, ex ante and ex post, to exercise a (costly) monitoring of the non–defaulted loans. This is a stylised way to sum up all the actions that the bank can enter into to ensure itself of the solvability of the borrowers. There is much that the bank can do to improve performance over the life of a transaction. First, a strong quality control process helps lenders exercise due diligence in evaluating borrowers’ current income, and keep track of those who might be getting closer to default. This is a surveillance action which has to be undertaken continuously, and not only prior to the inception of the contract. Second, the bank can efficiently assist troubled borrowers by acting early and firmly, before mortgages become seriously delinquent. The selection of bank employees in charge of these actions is also usually assumed to potentially affect loss severity by as much as 30%. For instance, Agarwal et al. [1] have put into light important and systematic changes in the default rates of state–chartered banks’ real estate loans, when a so–called "rotation" policy between federal and state supervisors at predetermined time periods is put into place. This clearly shows that banks are perfectly able to enter into corrective actions in the event of delinquencies, when they have incentives to do so.

The findings of [50, 51] were that since the investors cannot observe the monitoring effort of the bank, they proposed CDS type contracts offering remuneration to the bank, and giving it incentives through postponement of payments and threat of stochastic liquidation of the contract (similarly to the seminal paper of Biais, Mariotti, Rochet and Villeneuve [9]). In the present paper, we assume furthermore that there are two types of banks, which we call good and bad, co–existing in the market, differing by their efficiency in using their remuneration (or equivalently differing by their monitoring costs). Even if the investor is supposed to know the distribution of the type of banks, that is to say the probability with which the bank he is currently discussing with is good or bad, he cannot know for sure what her type is. Again, this is a stylised way to express the fact that "skin in the game" might significantly vary from one bank to the other. The fact that we consider only two types is mainly for simplicity and tractability, and because fully multidimensional screening problems are already extremely hard to solve in static one–period models, and except for specific models (see Section 2.1 for details), nothing more than existence of an optimal contract can be hoped for, see for instance Carlier [11].

Mathematically speaking, we follow the general dynamic programming approach of Cvitanić, Possamaï and Touzi [13], as well as that on adverse selection problems initiated by [14]. Intuitively, these approaches require first, using martingale (or more precisely backward SDEs) arguments, to solve the (non-Markovian) optimal control problem faced by the two types of banks when choosing contracts. This requires obviously, using the terminology introduced above, to keep track of both the continuation value and the temptation value of the banks, when they choose the contract designed for them or not. The problem of the Principal rewrites then as two standard stochastic control problems, one in which he hires the good bank, and one in which he hires the bad one. Each of these problems uses in turn the aforementioned two state variables (and these two only, because the horizon is infinite and the Principal is risk-neutral), with truth-telling constraint, asserting that the continuation value should always be greater than the temptation value. This leads to optimal control problems with state constraints, and thus to Hamilton-Jacobi-Bellman (HJB for short) equations (or more precisely variational inequalities with gradient constraints, since our problem is actually a singular stochastic control problem) in a domain, which, following [14], we call the credible set. This set is defined as the set containing the pair of value functions of the good and bad bank under every admissible contract offered by the investor. The determination of this set is the first fundamental step in our approach. Following the the orignal ideas of [14], we prove that the determination of the boundaries of this set can be achieved by solving two so-called double-sided moral hazard problems, in which one of the type of banks is actually hiring the other one. Fortunately for us, it turned out to be possible to obtain rigorously777Notice that in this respect the study in [14] was more formal, and our paper provides, as far as we know, the first rigorous derivation of this credible set. explicit expressions for these boundaries by solving the associated system of HJB equations and using verification type arguments. We also would like to emphasise that unlike in [14], there is certain dynamic component in our model, since we have to keep track of the number of non-defaulted loans, through a time inhomogeneous Poisson process. This leads to a dynamic credible set, as well as, in the end, to a recursive system of HJB equations characterising the value function of the Principal.

After having determined the credible set itself, we pursue our study by concentrating on two specific forms of contracts: the shutdown contract in which the investor designs a contract which will be accepted only by the good bank, and the more classical screening contract, corresponding to a menu of contracts, one for each type of bank, which provides incentives to reveal her true type and choose the contract designed for her. These two contracts correspond simply to the offering, over the correct domain of expected utilities of the banks (so as to satisfy the proper truth–telling and participation constraints), of the best contracts that the investor can design independently for hiring the good and the bad bank.

Since we characterise, under classical verification type arguments, the value function of the investor through a system of HJB equations, we also have classically access to the optimal contracts through this value function and its derivatives. This allows us to provide an associated qualitative and quantitative analysis. It turns out that the optimal contracts designed for the good and the bad bank share the same attributes, and are close in spirit to the ones derived in the pure moral hazard case in [51]. On the boundaries of the credible set, the value function of the bad bank plays the role of a state process. The payments of the optimal contracts are postponed until the moment the state process reaches a sufficiently high level, depending on the current size of the project. Similarly, when one of the loans in the pool defaults, the project is liquidated with a probability that decreases with the value of the state process. If the value function of the bad bank at the default time is below some critical level, the project will be liquidated for sure under the optimal contracts. On the other side, if the value function of the bad bank is high enough at the default time, the project will be maintained. In the interior of the credible set, the continuation value and the temptation value of the banks are the state processes for the optimal contracts. It is possible to identify zones of good performance inside of the credible set, where the agents are remunerated and the project is maintained in case a default occurs. It is also possible to identify zones of bad performance, where the agents are not paid and the project is liquidated in case of default. In the rest of the credible set the optimal contracts provide intermediary situations.

The rest of the paper is organised as follows. In Section 2, we present the model, we define the set of admissible contracts and we state the investor’s problem. In Section 3, we recall the results obtained in [51] for the case of pure moral hazard, which will be useful later on for us. In Section 4, we formally study the credible set and obtain an explicit expression for it. In Section 5, we study both the optimal shutdown and screening contract, describing their characteristics and the behaviour of the banks when they accept these contracts. The Appendix contains all the technical proofs of the paper.

Notations: Let denote the set of non–negative integers. For any , we identify with the set of dimensional column vectors. The associated inner product between two elements will be denoted by . For simplicity of notations, we will sometimes write column vectors in a row form, with the usual transposition operator , that is to say for some , . Let denote the set of non–negative real numbers, and the associated Borel algebra. For any fixed non–negative measure on , the Lebesgue–Stieljes integral of a measurable map will be denoted indifferently

2 The model

This section is dedicated to the description of the model we are going to study, presenting the contracts as well as the criterion of both the Principal and the Agent. As recalled in the Introduction, it is actually an adverse selection extension of the model introduced first by Pagès in [50] and studied in depth by Pagès and Possamaï [51].

2.1 Preliminaries

We consider a model in continuous time, indexed by . Without loss of generality and for simplicity, the risk–free interest rate is taken to be .888As already pointed out in the seminal paper of Biais, Mariotti, Rochet and Villeneuve [9], see also [51], the only quantity of interest here is the difference between the discounting factors of the Principal and the Agent. Our first player will be a bank (the Agent, referred to as "she"), who has access to a pool of unit loans indexed by , , which are ex ante identical. Each loan is a perpetuity yielding cash flow per unit time until it defaults. Once a loan defaults, it gives no further payments. As is commonplace in the Principal–Agent literature, especially since the paper of Sannikov [60], the infinite maturity assumption is here for simplicity and tractability, since it makes the problem stationary, in the sense that the value function of the Principal will not be time–dependent. We assume that the banks in the market are different, and that two types of banks coexist, each one being characterised by a parameter taking values in the set with . We call the bank good (respectively bad) if its type is (respectively ). Furthermore, it is considered to be common knowledge that the proportion of the banks of type , , is .

Denote by

the sum of individual loan default indicators, where is the default time of loan . The current size of the pool is, at some time , . Since all loans are a priori identical, they can be reindexed in any order after defaults. The action of the banks consists in deciding at each time whether they monitor any of the loans which have not defaulted yet. These actions are summarised by the functions , where for , if loan is monitored at time by the bank of type , and otherwise. Non-monitoring renders a private benefit per loan and per unit time to the bank, regardless of its type. The opportunity cost of monitoring is thus proportional to the number of monitored loans. Once more, more general cost structures could be considered, but this choice has been made for the sake of simplicity.

The rate at which loan defaults is controlled by the hazard rate specifying its instantaneous probability of default conditional on history up to time . Individual hazard rates are assumed to depend on the monitoring choice of the bank and on the size of the pool. In particular, this allows to incorporate a type of contagion effect in the model. Specifically, we choose to model the hazard rate of a non–defaulted loan at time , when it is monitored (or not) by a bank of type as

| (2.1) |

where the parameters are positive constants representing individual “baseline” risk under monitoring when the number of loans is , and is the proportional impact of shirking on default risk. We assume that the impact of shirking is independent of the type of the bank. There are two main reasons for this choice. First of all, it is well–known that as soon as the dimension of the type is greater or equal to , we enter into the field of multidimensional screening, which, already for static one period models is notoriously hard to analyse, and deriving meaningful economic interpretations is most often elusive (see the seminal paper of Rochet and Choné [56] or the more recent contribution of Figalli et al. [23] for more details). Notwithstanding this difficulty, we also found out that differentiating between the banks in this regard created degeneracy in the model. We refer the reader to Section F.2 in the Appendix for a more detailed explanation.

For , we define the shirking process as the number of loans that the bank of type fails to monitor at time . Then, according to (2.1), the corresponding aggregate default intensity is given by

| (2.2) |

The banks can fund the pool internally at a cost . They can also raise funds from a competitive investor (the Principal, referred to as "he") who values income streams at the prevailing risk–less interest rate of zero. We assume that both the banks and the investor observe the history of defaults and liquidations, as well as the parameters and , but the monitoring choices and the type of the bank are unobservable for the investor.

2.2 Description of the contracts

Before going on, let us now describe the stochastic basis on which we will be working. We will always place ourselves on a probability space on which is a point process with intensity , which is defined by (2.2) when all loans are monitored at all times, that is

We denote by the completion of the natural filtration of . We call the liquidation time of the whole pool and let be the liquidation indicator of the pool. We denote by the minimal filtration containing and that makes a stopping time. We note that this filtration satisfies the usual hypotheses of completeness and right–continuity.

Contracts are offered by the investor to the bank and agreed upon at time . As usual in contracting theory, the bank can accept or refuse the contract, but once accepted, both the bank and the investor are fully committed to the contract. More precisely, the investor offers a menu of contracts , specifying on the one hand a desired level of monitoring for the bank of type , which is a predictable process such that for any , takes values in (this set is denoted by ), as well as a flow of payment . These payments belong to set of processes which are càdlàg, non–decreasing, non–negative, predictable and such that there exists some

| (2.3) |

We do not rule out the possibility of immediate lump–sum payments at the initialisation of the contract, and therefore the processes in are assumed to satisfy Hence, if , it means that a lump–sum payment has indeed been made. Notice also that since the intensities of and under are bounded, we know that has at least some exponential moments under , meaning that any bounded payment belongs to .

The contract also specifies when liquidation occurs. We assume that liquidations can only take the form of the stochastic liquidation of all loans following immediately default. Hence, the contract specifies the probability , which belongs to the set of valued, predictable processes, with which the pool is maintained given default (), so that at each point in time, if the bank has indeed chosen the contract

With our notations, given a contract , the hazard rates associated with the default and liquidation processes and are, if the bank does choose the contract , and , respectively. The above properties translate into

For ease of notations, a contract will be said to be admissible if . As is commonplace in the Principal–Agent literature, we assume that the monitoring choices of the banks affect only the distribution of the size of the pool. To formalise this, recall that, by definition, any shirking process is predictable and bounded. Then, by Girsanov’s theorem, we can define a probability measure on , equivalent to , such that is a martingale. More precisely, we have on

where is the unique solution of the following SDE

Then, if the bank of type chooses the contract , her utility at , if she follows the recommendation , is given by

| (2.4) |

while that of the investor is

| (2.5) |

The parameter actually discriminates between the two types of banks through the way they derive utility from the cash–flows delivered by the investor. Hence, for a same level of salary, the good bank will get more utility than a bad bank. Such a form of adverse selection is also considered in the paper of Cvitanić, Wan and Yang [14]. Notice that de dependence of the value functions of both the bank and the investor depend on the contract through the process , but also through the stopping time , whose distribution depends both on and the effort choice of the bank.

2.3 Formulation of the investor’s problem

We assume that the bank of type has an outside opportunity to the contract which provides her reservation utility . The investor’s problem is to offer a menu of admissible contracts which maximises his utility (2.5), subject to the three following constraints

| (2.6) | ||||

| (2.7) | ||||

| (2.8) |

Condition (2.6) is the usual participation constraint for the banks. Condition (2.7) is the so–called incentive compatibility condition, stating that given , the recommended effort is an optimal monitoring choice for the bank of type . Finally, Condition (2.8) means that if a bank adversely selects a contract, she cannot get more utility than if she had truthfully revealed her type at time . Following the literature, we call such a contract a screening contract.

In the sequel, we will start by deriving the optimal contract in the pure moral hazard case, then we will look into the so–called optimal shutdown contract, for which the investor deliberately excludes the bad bank, before finally investigating the optimal screening contract. We will invoke some results from [50] in this paper, for this reason we will require later the assumptions of their main result, Theorem 3.15, which are the following.

Assumption 2.1.

Let be the harmonic mean of the ,

We have for all ,

Individual default risk is non–decreasing with past default,

2.4 Comments on the modelling choices and assumptions

Let us start by discussing Assumption 2.1. Concerning , under monitoring, the expected duration until the next default in a pool of loans is . Hence, the average revenue from the pool over that period will be given by , of which is ascribed to the original loan. The payoff of a loan corresponds then to summing this quantity over , and the obtained result must be above the initial unit cost for the loan to be worth anything at all under monitoring. Assumption 2.1 imposes an upper bound on the bank’s discount rate, and basically states that it should not be so large that the cost of the rent extracted by a monitoring bank outweighs the pecuniary gains stemming from the use of the monitoring technology. Finally Assumption 2.1 simply models a contagion effect, translating the fact that past defaults impact positively the likelihood of a further default to happen.

A second important point in the model is the liquidation policy of the contract. Even though liquidations are inefficient in the first–best situation without moral hazard nor adverse selection (see [50]), they are necessary in the second–best in order to restore incentives to monitor when performance is poor. However, liquidation can take many forms, and for instance liquidating all loans with state–dependent probability is not necessarily better than partially liquidating the pool with fixed probability. Another option would be to downsize the pool by a potentially larger number of loans, possibly state–dependent as well, whenever a default occurs. Given that in practice liquidations are rarely decided in such a random fashion, it is of the utmost importance to verify that such liquidation policies cannot improve on social welfare. In the case of pure moral hazard, [50, Proposition 6] has shown that stochastic liquidation was optimal among all policies under an assumption which is met if changes in default intensities for the loans are gradual. Since the capital structure of subprime mortgage–backed securities is typically split up into a large number of tranches, where it is then reasonable to assume that default intensities are constant, such an assumption will be verified in the real–world applications of the model.

Another very important assumption here is the fact that we consider a "full commitment" dynamic contracting problem between the investor and the bank. In other words, both parties are fully committed to the long–term dynamic contract at the onset of the relationship. However, one of the central features of banks, namely the fragility of their capital structures, stems from the fact that there is usually a limited commitment in the relationship between clients and banks, since, as highlighted by the seminal paper of Diamond and Dybvig [16], bank cleints can withdraw funds from banks at any time. We are perfectly conscient of this fact and have chosen to postpone the discussion of how to integrate non–commitment in our model to Section 6.2 below, since the mathematics behind are similar.

In our model, adverse selection stems only from the monitoring costs of the two types of banks. A possible extension of our model could rely on a further differentiation between the work of the banks, i.e. when both good bank and bad bank work, the good one would be more efficient in the sense that the associated default intensity is strictly smaller than that of the bad bank. This would also be a possible way to model the fact that the pool of loans of each bank could have different qualities. However, as will be explained in Appendix F.2, such a feature would actually make the problem degenerate, in the sense that the upper boundary of the credible set that will be defined in Section 4 becomes infinite. This would be a rather undesirable feature of the model and would create unwanted discontinuities. We give potential solutions to extend the model in this direction in Appendix F.2, but leave the exact study to future research.

3 The pure moral hazard case

In this section, we assume that the type of the bank is publicly known and is fixed to be some , , which makes the problem exactly similar to the one considered in [51] (up to the modification of some constants). In particular, the investor only offers one contract. The results we obtain here, in particular the dynamics of the continuation utilities of the banks, will be crucial to the study of the shutdown and screening contracts later on. Therefore, they will be used throughout the paper without further references.

In this setting, the utility of the investor, when he offers a contract is given by

| (3.1) |

for which we define the following dynamic version for any

3.1 The bank’s problem

As usual, the so–called continuation value of the bank (that is to say her future expected payoff) when offered plays a central role in the analysis. It is defined, for any by

We also define the value function of the bank for any

Departing slightly from the usual approach in the literature, initiated notably by Sannikov [60, 61], we reinterpret the problem of the bank in terms of BSDEs, which, we believe, offers an alternative approach which may be easier to apprehend for the mathematical finance community. Of course, such an interpretation of optimal stochastic control problem with control on the drift is far from being original, and we refer the interested reader to the seminal papers of Hamadène and Lepeltier [29] and El Karoui and Quenez [19] for more information, as well as to the recent articles by Cvitanić, Possamaï and Touzi [12, 13] for more references and a systematic treatment of Principal–Agent type problems with this backward SDE approach. Before stating the related result, let us denote by the unique (super–)solution (existence and uniqueness will be justified below) to the following BSDE

| (3.2) |

where

Uniqueness holds among processes and which are respectively progressively measurable and continuous, and predictable, and satisfy

| (3.3) |

where is the exponent associated to by (2.3). We have the following proposition, which is basically a reformulation of [51, Proposition 3.2]. The proof is postponed to Appendix A

Proposition 3.1.

For any , the value function of the bank has the dynamics, for ,

where is the second component of the solution to the BSDE (3.2). In particular, the optimal monitoring choice of the bank is given by

Notice that the above result implies that the monitoring choices of the bank are necessarily of bang–bang type, in the sense that she either monitors all the remaining loans, or none at all, which in turn implies that the investor can never give the bank incentives to monitor only a fraction of the loans at a given time999We assume here, as is commonplace in the Principal–Agent literature, that in the case where the bank is indifferent with respect to her monitoring decision, that is when , she acts in the best interest of the investors, and thus monitors all the remaining loans..

3.2 Introducing feasible sets

Following the terminology of Cvitanić, Wan and Yang [14], let us discuss the so–called feasible set for the banks.

Definition 3.1.

We call the feasible set for the expected payoff of banks of type , starting from some time , that is to say all the possible utilities that a bank of type can get from all the admissible contracts offered by the investor from time on.

Our next result gives an explicit form of the the feasible set , which turns out to be independent of the type of the bank. The proof is relegated to Appendix A, and requires the introduction of , the strategy of a bank which does not monitor any loan at any time, i.e. for every

Lemma 3.1.

For and for any , we have that , with

4 Credible set

In this section we come back to the case in which there are two types of banks in the market, and study the so–called credible set, which is formed by the pairs of value functions of the banks under the admissible contracts. As in [14], we do not expect all the points in the feasible set to correspond to a pair of reachable values of the banks under some admissible contract. We will therefore follow the approach initiated by [14] and we will characterise the credible set. We emphasise an important difference with [14] though, in the sense that in our context, the credible set becomes dynamic as it depends on the current size of the pool. In this section we work with generic contracts , not necessarily designed for a particular type of bank.

4.1 Definition of the credible set and its boundaries

We introduce some notations first. Let be the default intensity under when there are loans left, that is to say

Observe that for every such that . Define then for any integer between and , the set . Observe that the feasible set

satisfies for every , so the only dependence of the feasible set in time is due to the number of loans left. The rigorous definition of the credible set is the following.

Definition 4.1.

For any time , we define the credible set as the set of such that there exists some admissible contract satisfying , and for every , a.s.

Given a starting time and , define the set of contracts under which the value function of the bad bank at time is equal to

We denote by the largest value that the good bank can obtain from all the contracts . We also denote the lowest value by . Next, define

We will prove in Proposition 4.4 below that for every , and that the dependence on time of the credible set, exactly as for the feasible set, only comes from the value of . In particular, this allows us to call respectively the functions and the lower and upper boundary of the credible set when there are loans left. The aim of the next sections is prove all these claims and to obtain explicit formulas for the boundaries. We start with some useful technical results concerning specific contracts for which the banks do not monitor the loans at all.

4.2 Utility of not monitoring

Consider any starting time such that and any . The continuation utility that the banks get from always shirking (without considering the payments) is

| (4.1) |

This quantity is obviously non–decreasing in , so that (4.1) attains its minimum value under any contract with , which is equal to The following proposition provides the value of (4.1) when the pool is liquidated exactly after a fixed number of defaults .

Proposition 4.1.

Fix some and let . For , let be such that the pool is liquidated exactly after the th default occurring after time , that is

The utility that the bank of type gets from shirking is

In particular, under any contract such that , (4.1) attains its maximum value, which is equal to

| (4.2) |

4.3 Lower boundary of the credible set

The lower boundary of the credible set is the simpler of the two boundaries and it can be computed directly. We will see that it is a piecewise linear function corresponding to two lines with different slopes. All proofs for this section are collected in Appendix C. The next proposition states the main inequalities that determine the lower boundary.

Lemma 4.1.

For any and any admissible contract , the value functions of the good and the bad banks satisfy, a.s.

| (4.3) | |||

| (4.4) |

where the function is defined in (4.2).

Using Lemma 4.1, we prove the following characterisation of the lower boundary of the credible set.

Proposition 4.2.

For any , and any , the lower boundary of the credible set is given by

In particular, the dependence in of only comes from the number of non–defaulted loans at time and we can define for any , the quantity given by

for which we have .

Remark 4.1.

Of course, the computations of this section depend on our modelling choices, and are unlikely to be directly adaptable to other situations. There is however a generic way of finding the lower boundary as well as the upper one which we give details in the next section. It amounts to solving a fictitious contract situation where the good bank hires the bad one and minimises maximises for the upper boundary her utility over her monitoring choices, and over all contracts for which the bad bank receives a fixed utility . The dynamic value function of this control problem is exactly , since it corresponds to the minimal utility that the good bank can have when the bad one receives .

4.4 Upper boundary of the credible set

The upper boundary of the credible set is not as simple to obtain as the lower boundary and we have to solve a specific stochastic control problem to identify it. Notice that this approach is similar to the one used in [14].

Let us fix any contract . We remind the reader that thanks to Proposition 3.1, we know that there exist predictable integrable processes satisfying the second integrability condition in (3.3) and such that

| (4.5) |

where the optimal monitoring choice is given by . Similarly, there exist predictable processes satisfying the second integrability condition in (3.3) and such that

| (4.6) |

with We will use the dynamics (4.4)–(4.4) to define a simple set of admissible contracts in which we will reinterpret both the value functions of the agents as controlled diffusion processes, where the controls are , and which satisfy the instantaneous conditions (A.3). Obviously, doing so makes us, at least at first sight, look at a larger class of "contracts", in the sense that in the above representation of the value functions of the bank, the choice of the processes is not free, since they are completely determined by the choice of . Nonetheless, as we will see below, this still describes exactly the same set of contracts.

In the meantime, let us denote by the set of non–negative, predictable processes satisfying for some

We abuse notations and define, for every , the processes and which satisfy the following SDEs

| (4.7) | ||||

| (4.8) |

where we defined

Remark 4.2.

In the model, there is no need to consider and as positive processes and we do this just for technical reasons. Intuitively, the optimal contracts should satisfy this additional constraint because the investor does not benefit from earlier defaults and if a contract increases the banks’ continuation utilities after one of the defaults, the banks should increase the default intensity as much as possible.

Remark 4.3.

It is immediate from the definition that given , the dynamics of only depends on , while the dynamics of only depends on . We will thus sometimes also use the notations , , and when .

For fixed , we define the set of contracts as the set of such that (4.7) and (4.8) have at least one weak solution101010In general, all the processes in could for instance functionals of the paths of and , in which case wellposedness of the SDEs has to be assumed as part of the definition., which satisfies the first integrability condition in (3.3), and in addition

What we claimed above is that all processes can be obtained from a contract , meaning that we are not enlarging at all the class of admissible contracts in our reformulation. Indeed, we already know by the results from Section 3, that the continuation utilities of the good and the bad bank given a contract were completely characterised as being the unique solutions of the corresponding BSDEs (3.2) satisfying in addition (3.3). If we take some , then it is immediate that the processes , solve the corresponding BSDEs (3.2), since the dynamics is the correct one by definition, we have , and all the required integrability conditions are satisfied. By uniqueness of the solution to the BSDEs, we thus must have , and .

To describe the stochastic control problem for the upper boundary of the credible set, we need to introduce additional notations. For any starting time and for every , we let be the set of quadruplets such that (4.8) has at least one weak solution, which satisfies the first integrability condition in (3.3) as well as

We will abuse notations and also call elements of contracts. The upper boundary solves the following control problem

subject to the dynamics

Indeed, the above stochastic control problem corresponds to the highest value that the good bank can obtain from any admissible contract, while ensuring that when the bad bank takes said contract, she receives exactly , which is exactly the definition of the upper boundary of the credible set. Another way to interpret this problem is that it corresponds to the (fictitious) situation where the good bank hires the bad one, when the latter wants to receive a utility of , and maximises her utility among all contracts ensuring that this constraint is satisfied. The importance of the results of Proposition 3.1 is that it allows us to obtain easily the dynamic behaviour of the continuation utility of the bad bank for any initial utility, which in turns allows us to express simply the constraint in the problem for the good bank through the set and the state variable .

The next subsections are devoted to first obtaining the HJB equation associated with the above problem, its resolution and then finally to the proof of a verification theorem adapted to our framework. Notice that the above is actually a singular stochastic control problem, since the control is a non–decreasing process, which is not necessarily absolutely continuous with respect to the Lebesgue measure. We refer the reader to the monograph by Fleming and Soner [24] for more details. In particular, this implies that the HJB equation associated to the problem will be a variational inequality with gradient constraints.

4.4.1 HJB equation for the upper boundary

Exactly as in the case of the lower boundary, we expect that the time dependence of of the upper boundary only comes from the current number of remaining loans. In such a case, the HJB equations that will describe the behaviour of the upper boundary necessarily form a recursive system, with the upper boundary when loans are left depending on the one with loans left. We will write down this system, solve it explicitly, and prove a verification theorem ensuring that our initial guess was indeed correct.

Fix some , and define for every , The system of HJB equations associated to the previous control problem is given by , and for any and

| (4.9) |

with the additional boundary condition and where we defined for simplicity

as well as

Remark 4.4.

Notice that if our guess on the time dependence of the upper boundary is correct, we must have for any , . Then. the incentive compatibility condition for the good bank is implicit in the HJB equation. Indeed, at every we have

which implies that on the upper boundary and . Therefore

At the points where , the first term of the variational inequality (4.9) must be equal to zero, so the upper boundary must satisfy the following equation

| (4.10) |

We will refer to this equation as the diffusion equation.

Step 1: case of 1 loan, solving the diffusion equation

Before dealing with the variational inequality (4.9), we will solve the diffusion equation (4.10). When , it reduces to

| (4.11) |

with .

Remark 4.5.

Notice that the boundary condition is implicit in the equation.

Our first result is the following, whose proof is deferred to Appendix D.

Lemma 4.2.

There is a family of continuously differentiable solutions to the diffusion equation (4.10), indexed by some constant , which are given by

where .

Step 2: case of 1 loan, solving the HJB equation

In this case the variational inequality (4.9) reduces to

| (4.12) |

We already found the solutions of the diffusion equation inside of this variational inequality and now we will take care of the whole HJB equation. We expect the upper boundary to saturate the second term in the variational inequality for big values of , so we will search for a solution of (4.12) satisfying the following condition: there exists such that

| (4.13) |

At first sight it could seem that by doing this we face the risk of not finding the correct solution of the dynamic programming equation. Nevertheless, this is not the case and we will prove later a verification result which assures us that the solution that we find under this condition corresponds indeed to the upper boundary of the credible set. The proof of the following Lemma will be given in Appendix D.

Lemma 4.3.

As an illustration, in Figure 1 we show the credible set which corresponds to the region delimited by its upper and lower boundaries. In this example, we considered , , , , .

Step 3: solving the HJB equation in the general case

In the general case, when , we can reduce the number of variables and rewrite the diffusion equation (4.10) in an equivalent form

| (4.15) |

where we recall that and the set of constraints is now given by

| (4.16) |

When we proved that the lower boundary of the credible set is reachable we used contracts of maximum duration, which maintain the pool until the last default. This gives us the intuition that the longer the contract lasts, the smaller the difference between the utilities of the banks will be. Therefore the upper boundary of the credible set, where the difference between both utilities is maximal, should be reachable with contracts of minimum duration, which terminate the contractual relationship immediately after the first default. In the model this means that is equal to zero and the resulting HJB equation for the upper boundary has the same form as the one in the case with one loan left. We expect then that the solution of the diffusion equation will be the of the same form as (4.14). The object of the next proposition is to prove our guess rigorously. We postpone the proof to Appendix D.

Proposition 4.3.

4.4.2 Verification theorem

According to the maximisers in equation (4.15) we define the following controls

| (4.18) |

Before stating the verification result for the upper boundary, we make a comment about the domain of the functions . Rigorously speaking, it is possible for the utilities of the banks to be zero but this happens only at time when all the pools are liquidated. The domain of is the set but in the proof of the verification theorem it will be implicitly understood that . In any case, we do not need the functions to be defined at zero because Itô’s formula will be used on intervals which do not contain .

Theorem 4.1.

Consider any starting time . For any , let the process be the unique solution of the following SDE

| (4.19) |

Then, under the contract defined for by

the value function of the bad bank is and the one of good bank is . Moreover, and for any other contract which belongs to , the value function of the good bank under such a contract is less or equal to . In particular, this implies that

To conclude the section, we state that is indeed equal to the credible set with loans left and therefore the functions and correspond to its upper and lower boundaries.

Proposition 4.4.

For every , .

5 Optimal contracts

In this section we study two kind of contracts that the investor can offer to the bank, the shutdown contract, which corresponds to a single contract designed to be accepted only by the good bank and the screening contract, corresponding to a menu of contracts, one for each type of agent, providing incentives to the bank to accept the contract designed for her true type.

5.1 Shutdown contract

In the so–called shutdown contract, the investor designs a contract only for the good bank and makes sure that the bad bank will not accept it. Under these conditions the utility of the investor at time is

| (5.1) |

So the investor will offer a contract which maximises (5.1) subject to the constraints

Recalling the dynamics (4.4)–(4.4), we can rewrite the investor’s maximisation problem as follows

where

Remark 5.1.

We will use the notation for the value function that the bad bank gets if she does not reveal her true type and accepts the contract designed for the good bank. We make a distinction between this process and , which corresponds to the value function that the bad bank obtains if she accepts the contract designed for her by the investor. We make the same distinction between the associated processes , and , .

As in the previous section, we will define a simple set of contracts and consider the value functions of the agents as diffussion processes controlled by . As explained before, by doing so we do not look at a larger class of "contracts".

Define for any , to be the set of such that (4.7) and (4.8) have at least one weak solution, which satisfy the first integrability condition in (3.3), and in addition, for any

We will also consider in the sequel the following standard control problem, for any

We abuse notations and also call elements of contracts.

5.1.1 Value function of the investor

In this section, we characterise the value function of the investor when he offers only shutdown contracts. We will start by computing the value function on the boundaries of the credible set, before explaining how it can be characterised by a specific HJB equation in the interior of the credible set, under reasonable assumptions.

Value function of the investor on the lower boundary

Recall the lower boundary with loans left

Consider any starting time . For , we denote by the value function of the investor on the lower boundary, that is

| (5.2) |

The following two propositions are proved in Appendix E and give explicitly the value of .

Proposition 5.1.

For every , if then the value function of the investor on the lower boundary is given by

Proposition 5.2.

Fix some . For every , with , let be the unique solution of the following equation in

where is the density of the law of under and where

Then the value function of the investor in the lower boundary is given by

Value function of the investor on the upper boundary

The next proposition states that the upper boundary of the credible set is absorbing in the following sense: if under any contract the pair of value functions of the banks reaches the upper boundary at some time, the pair will stay on the upper boundary until the pool is liquidated.

Proposition 5.3.

Fix a triplet such that . For any contract , we have for every .

The next proposition states an important property satisfied by the contracts which make the continuation utilities of the banks lie in the upper boundary of the credible set.

Proposition 5.4.

Fix a triplet such that . For any contract , we have

-

for every such that .

-

If for some then and for every .

We are now ready to give the value function of the investor on the upper boundary of the credible set. In the last region of the upper boundary, in which both the good and the bad agent are monitoring all the loans, it coincides with the value function of the sub–problem111111The authors only look at the contracts for which the agent performs the maximum effort, that is, monitors all the loans at every time. studied in[50], denoted by . For the sake of presentation, we recall the results of [50] in Appendix E.1.

Value function of the investor in the credible set

We define, for any and any , the value function of the investor in the credible set by

| (5.4) |

The system of HJB equations associated to this control problem is given by , and for any , on

| (5.9) |

where we defined and the set of constraints

The boundary conditions of (5.9) are given, for every by

| (5.10) |

The last step is now to use classical arguments to prove that is a viscosity solution of the above PDE for every and that the functions are sufficiently smooth (at least weakly dfferentiable) in order to obtain the optimal contract as the maximisers above. This program can in principle be carried out using standard arguments in viscosity theory of Hamilton–Jacobi equations. However, given the length of the paper, we believe that it would not serve a specific purpose and decided to just describe the main steps that lead to this result. We list them below

-

For , let us define the penalised Hamiltonians for the diffusion equation, with loans left. Given , define for instance

(5.11) Let be the value function of the penalised version of our problem, in which payments are absolutely continuous with bounded density. Then it can be argued as in [21] that is a viscosity solution to , with appropriate credible set and boundary conditions.

-

Note that is convex in , as a supremum of linear functionals and composition of convex functions. Moreover, for any we have

is also locally Lipschitz and as for any . Finally, noticing that interior maximisers take place in the interior of the credible set (to be more precise, boundary maximisers correspond to contracts leading the agents to the absorbing boundaries of the credible set) and by using the envelope theorem, we can show that is actually strictly convex on the interior of the credible set and therefore satisfies

By Theorem 3.3 in Lions [37], it follows then that and is SSH (semi–super harmonic).

Finally, since is differentiable almost everywhere, we can define the optimal contract through the maximisers in the Hamiltonian (5.9). Then, using the classical result (see for instance [32] for related arguments) that the domain in which the diffusion equation is not saturated is bounded, it follows that the optimal controls are bounded and the corresponding SDEs admit weak solutions

Indeed, this can be proved by noticing that in–between two jump times, the above are actually first–order ODEs, which admit weak solutions in appropriately exponentially weighted space (to make sure that bounded functions are integrable over the credible set), thanks to Carathéodory’s theorem for ODEs. Thus, we have the equivalence

5.2 Screening contract

Recall that in the screening contract the investor designs a menu of contracts, one for each agent, and his expected utility is given by

| (5.12) |

In this case, we will have to keep track of the value functions of both banks, when they choose the contract designed for them, as well as when they do not truthfully reveal their type. We will denote by the maximal utility that the investor can get out of the screening contract.

where

Different from the study of the shutdown contract, where the investor contracts only the good bank, in order to obtain the optimal screening contract we need to characterise also the value function of the investor when he contracts the bad bank. We will therefore follow Section 5.1.1, but by replacing the good bank by the bad bank. Hence, we define similarly, for any the set . We also introduce the following stochastic control problem for any

The aim of the next sections is to compute the function , representing the utility of the investor when hiring the bad bank. We start by studying it on the boundary of the credible set.

5.2.1 Boundary study

We denote by the value function of the investor in the lower boundary, when hiring the bad bank, defined by

| (5.13) |

The first result is that the value function of the investor on the lower boundary of the credible set is the same when hiring either the bad or the good bank. This is mainly due to the fact that both banks shirk on the lower boundary.

Proposition 5.6.

For every , we have .

Let us now consider the upper boundary. We denote by the value function of the investor on the upper boundary when hiring the bad agent.

| (5.14) |

We have the following result.

5.2.2 Study of the credible set

We define, for any and any , the value function of the investor in the credible set when hiring the bad bank by

| (5.15) |

The system of HJB equations associated to this control problem is given by , and for any

| (5.16) |

With and the same set of constraints as in the system of HJB equations associated to the functions . The boundary conditions of (5.16) are given, for every by

Similarly to the shutdown contract, we can argue that the functions are viscosity solutions to the system (5.16), differentiable almost everywhere and the maximizers in the Hamiltonian define an admissible contract. This implies the equivalence

5.3 Description of the optimal contracts

In this section we describe the optimal contracts for the investor when he designs a contract for the good or the bad bank. We explain in detail the optimal contracts on the boundaries of the credible set, which can be obtained explicitly from the value function of the investor. In the interior of the credible set, we discuss the properties we expect the optimal contracts to have given the verification results described in the previous sections.

5.3.1 Optimal contracts on the boundaries of the credible set

We start with the upper boundary of the credible set. The following result is a direct consequence of the proofs of Proposition 5.5 and 5.7, and the optimal contract for the pure moral hazard case. In the last part of the upper boundary, in which both agents monitor all the loans, the optimal contract coincides with the one of the subproblem studied in [50]. Their main results can be found in Appendix E.1.

Proposition 5.8.

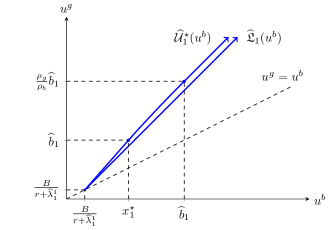

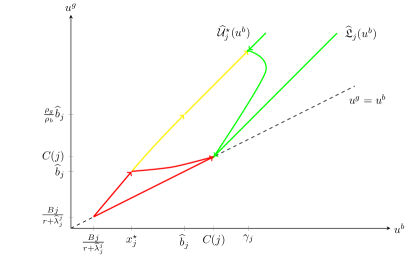

Let us comment the optimal contract for the investor on the upper boundary of the credible set. It is the same if he designs a contract for the good or the bad bank. The state process defined by (5.17) corresponds to the value function of the bad bank under the optimal contract. The optimal contract offers no payments to the banks when is smaller than . In this case the continuation utility of the bad bank is an increasing process and eventually reaches the value , if no default happens in the meantime. Payments are postponed until this moment. If the initial value for the bad agent is greater than , a lump-sum payment is made at in order to have . When , the banks receive constant payments which keep the value function of the bad bank constant at this level. Concerning the liquidation of the project, if, at the default time , it holds that , then the project is liquidated. In case of , the project will continue with probability which will be closer to one as gets closer to . If , the project will be maintained. Finally, the bad bank will monitor all the loans only when her value function is greater than , whereas the good bank will monitor when the value of the bad bank is greater than . Figure 2 depicts the optimal contract of the investor on the upper boundary of the credible set, denoting .

For the lower boundary of the credible set, we have the following result.

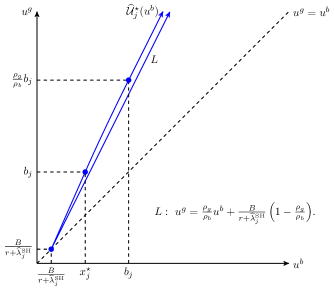

Proposition 5.9.

Under Assumption 2.1, consider for any and the process as the solution of the following SDE on

| (5.18) |

with initial value at , and with

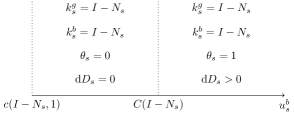

On the lower boundary of the credible set, the optimal contract for the investor also does not depend on the type of the bank. If the initial value of the bad bank is greater than , the banks receive a lump-sum payment such that . This is the only payment offered by the contract. If there is a default at some time such that , the project is liquidated. When the contract maintains the project until the last default. Since the optimal contract does not provides incentives to the banks to monitor the loans, the good and the bad bank shirk until the liquidation of the project. Figure 3 depicts the optimal contract of the investor on the lower boundary of the credible set.

5.3.2 Discussion about the optimal contracts in the interior of the credible set

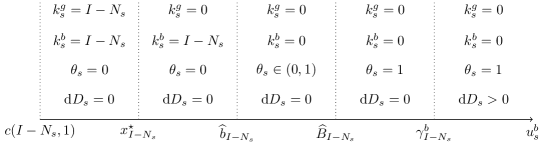

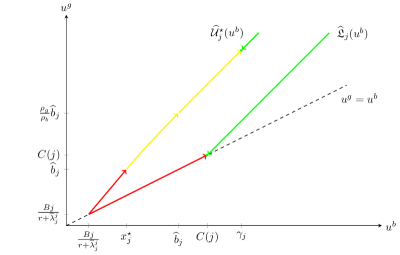

Figure 4 represents the optimal contracts on the boundaries of the credible set as well as the movements of the values of the banks along these curves. The green zone corresponds to the region where the contract offers payments to the agents and the project is maintained if there is a default. The red zone corresponds to the region where there are no payments and the project is liquidated immediately after a default. Intermediate situations correspond to the yellow zone. We remark that the banks are paid only on the green zone.

Let us now consider the whole credible set and explain how the green and red zones on the boundaries propagate towards the interior region, given that the optimal contracts for problems (5.4) and (5.15) correspond to the maximisers in the Hamiltonian of the systems (5.9) and (5.16). Recall that payments only take place when the value function of the investor saturates the gradient constraint. Therefore, if at some point of the credible set the banks are paid, this will also be the case under movements in the direction . The interpretation of this property is that the green region, where the banks are paid and the project is maintained after a default, is formed by the points where the banks have a good performance and they are rewarded. A movement in the direction correspond to a better performance of both banks, so it seems unnatural to deprive them of the reward. We can do the opposite interpretation for the red region, consisting of the points where the banks receive no payments and the project is liquidated after a default. In consequence, under the optimal contracts, it is possible to identify red and green areas in the credible set, where the characteristics described in the boundaries will remain, and that will be delimited by some curves similar to those shown in Figure 5 below. Mathematically, these curves are delimiting the region where the gradient constraint is saturated.

5.4 A word on implementability of the contracts

Any real–world application of our model requires to discuss the practical implementability of the contract. Fortunately for us, the form of the menus of contracts we obtained is completely similar to the one obtained in [50, 51], in the sense that all rely on a probation zone, where stochastic liquidation may occur, and a zone of good performance, where the liquidation never occurs. The only difference is of course that in [50, 51] these zones are simply intervals, while they are more complex regions of the plan in our case, since we have to keep track of both the continuation and the temptation values of the Agent. Nonetheless, the practical implementation proposed by Pagès [50, Proposition 7] can readily be adapted to our context. Given the length of the paper, we leave the exact detail to the reader, and simply recall how the implementation works.

First, a natural way of implementing the contract is to replicate dynamically both the continuation and the temptation values of the Agent by use of two cash reserve accounts. The accounts should be managed by an independent trust, and actually serves to both provide protection to the investors, and to manage exactly the performance–based compensation scheme described in the optimal contract. The current balances reveal outright performance of both type of banks, and can be used to determine the amount and timing of fees that are released. Then, the implementation basically takes the form of a whole loan sale with monitoring retained. The reserve accounts then offer protection in the form of ABS credit default swaps (ABCDS), and serve as instruments to tie the amount and timing of compensation to performance (meaning that payments are made from the cash reserve only when the continuation and temptation values of the Agent are in the domain where the gradient constraint is satisfied). The reserve account reveals the level of underlying performance, which reduces the rent of the monitoring bank and allows it to retain risk at a lower cost than if it were funded with deposits.

6 Extensions

6.1 Endogenous reservation utility

In a standard Principal–Agent problem, it is assumed that the Agent possesses a minimum level of utility that must be provided by the Principal in order to make him accept the contract. This reservation value represents the utility that the Agent would obtain if the contract offered by the Principal was not sufficiently attractive and he made use of an outside option (see Condition (2.6) in Section 2.3).

In this section we provide an endogenous characterisation of the reservation utilities of the banks by assuming that if they do not enter in a contractual relationship with the investor, they can manage the project by themselves. When the outside option of a bank is to manage the pool of loans on its own, we can find the explicit value of its reservation utility. Moreover, we outline an extension of our model to the case in which the bank can break the contract at any time if it can do better by itself. Different from the full-commitment problem studied in the previous sections, the ability of the bank to break the contract makes the investor offer only the so called renegotiation-proof contracts, which keep the utility of bank above a dynamic reservation utility until the end of the contract.

If the bank of type manages the project, it receives the cash flows from the loans and does not face the threat of liquidating the whole pool when one of the loans defaults. Consequently, its reservation utility is given by the following expression

| (6.1) |

The value of can be obtained as an application of the results from the previous sections, since (6.1) corresponds to the utility of the bank under a contract with no liquidation at all, , and with absolutely continuous payments, . Its explicit value is provided in Proposition 6.1.

Proposition 6.1.

Define the recursive sequence of numbers

with . The endogenous reservation utility of the bank of type is given by . Moreover, the optimal action in Problem (6.1) is constant in every interval and it is equal to if the maximum in the definition of is attained at the first term, and to if the maximum is attained at the last term.

6.2 Renegotiation–proof contracts

Suppose that the bank of type can decide at any time to break the contract with the investors and manage the loans by itself. By doing so, the bank’s utility at time would be

Notice that the previous expression depends on only through the number of loans left at the time. It is straightforward then that , for every .

In this setting, a shutdown contract is one which is never broken by the bank of type and is rejected by the bank of type , who prefers to run the project on its own. That is, for every and . To find the optimal shutdown contract, we need to characterize first the new credible set which includes additional state constraints for the good bank. Let us mention immediately that the right of the bank to break the contract generates differences between the credible sets associated to the shutdown and the screening problem, which are no longer equal.

Define the renegotiation–proof feasible set for the good bank with loans left

Definition 6.1.

For any time , we define the shutdown renegotiation–proof credible set as the set of such that there exists an admissible contract satisfying , and for every ,

Given a starting time and , define the set of contracts which are not broken by the good bank and under which the value function of the bad bank at time is equal to ,

We denote by the largest value that the good bank can obtain from all the contracts and by the lowest one. Again, these sets can be proved to depend on only through the value of so defining and we finally have

As depicted in Figure 4, the upper boundary in the problem with full commitment is absorbing and it generates a movement of the utilities of the banks in the direction . We conclude that the upper boundary in this extension is the same as before and it is given by

On the other hand, since the former lower boundary generates a movement in the direction , it cannot be used to obtain which is the solution to the following control problem

subject to the dynamics, for

with

and where is defined similarly as in Section 4. Once the boundaries are determined and the credible set is found, a system of recursive HJB equations can be associated to the Principal’s problem, as in the original problem, and the same kind of study explained in Section 5 follows.

The optimal screening renegotiation–proof problem can be studied analogously, by defining the corresponding credible set, which is no longer equivalent to the credible set for the shutdown problem but will also keep the upper boundary from the original problem with full commitment of the banks.

References

- [1] S. Agarwal, D. Lucca, A. Seru, and F. Trebbi. Inconsistent regulators: evidence from banking. The Quarterly Journal of Economics, 129(2):889–938, 2014.

- [2] R. Antle. Moral hazard and auditor contracts : an approach to auditors’ legal liability and independence. PhD thesis, Stanford university, 1980.

- [3] D.P. Baron. A model of the demand for investment banking advising and distribution services for new issues. The Journal of Finance, 37(4):955–976, 1982.

- [4] D.P. Baron and D. Besanko. Monitoring, moral hazard, asymmetric information, and risk sharing in procurement contracting. The RAND Journal of Economics, 18(4):509–532, 1987.

- [5] D.P. Baron and D. Besanko. Monitoring of performance in organizational contracting: the case of defense procurement. The Scandinavian Journal of Economics, 90(3):329–356, 1988.

- [6] D.P. Baron and B. Holmström. The investment banking contract for new issues under asymmetric information: delegation and the incentive problem. The Journal of Finance, 35(5):1115–1138, 1980.

- [7] D.P. Baron and R.B. Myerson. Regulating a monopolist with unknown costs. Econometrica, 50(4):911–930, 1982.

- [8] N. Bhattacharyya. Good managers work more and pay less dividends – a model of dividend policy. Technical report, University of British Columbia, 1997.

- [9] B. Biais, T. Mariotti, J.-C. Rochet, and S. Villeneuve. Large risks, limited liability, and dynamic moral hazard. Econometrica, 78(1):73–118, 2010.

- [10] B. Caillaud, R. Guesnerie, and P. Rey. Noisy observation in adverse selection models. The Review of Economic Studies, 59(3):595–615, 1992.

- [11] G. Carlier. A general existence result for the principal–agent problem with adverse selection. Journal of Mathematical Economics, 35(1):129–150, 2001.

- [12] J. Cvitanić, D. Possamaï, and N. Touzi. Moral hazard in dynamic risk management. Management Science, 63(10):3328–3346, 2017.

- [13] J. Cvitanić, D. Possamaï, and N. Touzi. Dynamic programming approach to principal–agent problems. Finance and Stochastics, 22(1):1–37, 2018.

- [14] J. Cvitanić, X. Wan, and H. Yang. Dynamics of contract design with screening. Management Science, 59(5):1229–1244, 2013.

- [15] R.W.R. Darling and É. Pardoux. Backwards SDE with random terminal time and applications to semilinear elliptic PDE. The Annals of Probability, 25(3):1135–1159, 1997.

- [16] D.W. Diamond and P.H. Dybvig. Bank runs, deposit insurance, and liquidity. Journal of Political Economy, 91(3):401–419, 1983.

- [17] G. Dionne and P. Lasserre. Dealing with moral hazard and adverse selection simultaneously. Cahier de recherche 8559, Département de sciences économiques, université de Montréal, 1985.

- [18] O. El Euch, T. Mastrolia, M. Rosenbaum, and N. Touzi. Optimal make–take fees for market making regulation. arXiv preprint arXiv:1805.02741, 2018.

- [19] N. El Karoui and M.-C. Quenez. Dynamic programming and pricing of contingent claims in an incomplete market. SIAM Journal on Control and Optimization, 33(1):29–66, 1995.

- [20] N. El Karoui and X. Tan. Capacities, measurable selection and dynamic programming part II: application in stochastic control problems. arXiv preprint arXiv:1310.3364, 2013.

- [21] R. Élie, L. Moreau, and D. Possamaï. On a class of non–Markovian singular stochastic control problems. SIAM Journal on Control and Optimization, to appear, 2017.

- [22] P.S. Faynzilberg and P. Kumar. On the generalized principal–agent problem: decomposition and existence results. Review of Economic Design, 5(1):23–58, 2000.

- [23] A. Figalli, Y.-H. Kim, and R.J. McCann. When is multidimensional screening a convex program? Journal of Economic Theory, 146(2):454–478, 2011.

- [24] W.H. Fleming and H.M. Soner. Controlled Markov processes and viscosity solutions, volume 25 of Stochastic modelling and applied probability. Springer–Verlag New York, 2nd edition, 2006.

- [25] D. Gottlieb and H. Moreira. Simultaneous adverse selection and moral hazard. Technical report, The university of Pennsylvania and escola Brasileira de economia e finanças, 2011.

- [26] S.J. Grossman and O.D. Hart. An analysis of the principal–agent problem. Econometrica, 51(1):7–45, 1983.

- [27] R. Guesnerie and J.-J. Laffont. A complete solution to a class of principal–agent problems with an application to the control of a self-managed firm. Journal of Public Economics, 25(3):329–369, 1984.

- [28] R. Guesnerie, P. Picard, and P. Rey. Adverse selection and moral hazard with risk neutral agents. European Economic Review, 33(4):807–823, 1989.

- [29] S. Hamadène and J.-P. Lepeltier. Backward equations, stochastic control and zero–sum stochastic differential games. Stochastics: An International Journal of Probability and Stochastic Processes, 54(3-4):221–231, 1995.

- [30] B. Hölmstrom. Moral hazard and observability. The Bell Journal of Economics, 10(1):74–91, 1979.

- [31] B. Holmström and P. Milgrom. Aggregation and linearity in the provision of intertemporal incentives. Econometrica, 55(2):303–328, 1987.

- [32] R. Hynd. The eigenvalue problem of singular ergodic control. Communications on Pure and Applied Mathematics, 65(5):649–682, 2012.

- [33] I. Jewitt. Justifying the first–order approach to principal–agent problems. Econometrica, 56(5):1177–1190, 1988.

- [34] B. Jullien, B. Salanié, and F. Salanié. Screening risk–averse agents under moral hazard: single–crossing and the CARA case. Economic Theory, 30(1):151–169, 2007.

- [35] J.-J. Laffont and J. Tirole. Using cost observation to regulate firms. The Journal of Political Economy, 94(3, part 1):614–641, 1986.

- [36] T.R. Lewis and D.E.M. Sappington. Optimal capital structure in agency relationships. The RAND Journal of Economics, 26(3):343–361, 1995.

- [37] P.-L. Lions. Generalized solutions of Hamilton–Jacobi equations, volume 69 of Research notes in mathematics. Pitman Advanced Publishing Program, Boston, London, Melbourne, 1982.

- [38] E. Maskin and J. Riley. Monopoly with incomplete information. The RAND Journal of Economics, 15(2):171–196, 1984.

- [39] R.P. McAfee and J. McMillan. Bidding for contracts: a principal–agent analysis. The RAND Journal of Economics, 17(3):326–338, 1986.

- [40] N.D. Melumad and S. Reichelstein. Centralization versus delegation and the value of communication. Journal of Accounting Research, 25:1–18, 1987.

- [41] N.D. Melumad and S. Reichelstein. Value of communication in agencies. Journal of Economic Theory, 47(2):334–368, 1989.

- [42] J.A. Mirrlees. Population policy and the taxation of family size. Journal of Public Economics, 1(2):169–198, 1972.

- [43] J.A. Mirrlees. Notes on welfare economics, information and uncertainty. In M.S. Balch, D.L. McFadden, and S.Y. Wu, editors, Essays on economic behavior under uncertainty, pages 243–261. Amsterdam: North Holland, 1974.

- [44] J.A. Mirrlees. The optimal structure of incentives and authority within an organization. The Bell Journal of Economics, 7(1):105–131, 1976.

- [45] J.A. Mirrlees. The theory of moral hazard and unobservable behaviour: part I (reprint of the unpublished 1975 version). The Review of Economic Studies, 66(1):3–21, 1999.

- [46] James A Mirrlees. An exploration in the theory of optimum income taxation. The review of economic studies, 38(2):175–208, 1971.

- [47] M. Mussa and S. Rosen. Monopoly and product quality. Journal of Economic Theory, 18(2):301–317, 1978.

- [48] R.B. Myerson. Optimal coordination mechanisms in generalized principal–agent problems. Journal of Mathematical Economics, 10(1):67–81, 1982.

- [49] F.H.Jr. Page. Optimal contract mechanisms for principal–agent problems with moral hazard and adverse selection. Economic Theory, 1(4):323–338, 1991.

- [50] H. Pagès. Bank monitoring incentives and optimal ABS. Journal of Financial Intermediation, 22(1):30–54, 2013.

- [51] H. Pagès and D. Possamaï. A mathematical treatment of bank monitoring incentives. Finance and Stochastics, 18(1):39–73, 2014.

- [52] A. Papapantoleon, D. Possamaï, and A. Saplaouras. Existence and uniqueness for BSDEs with jumps: the whole nine yards. Electronic Journal of Probability, 23(121):1–68, 2018.

- [53] S. Peng. Probabilistic interpretation for systems of quasilinear parabolic partial differential equations. Stochastics and Stochastic Reports, 37(1-2):61–74, 1991.

- [54] P. Picard. On the design of incentive schemes under moral hazard and adverse selection. Journal of Public Economics, 33(3):305–331, 1987.

- [55] K.W.S. Roberts. Welfare considerations on nonlinear pricing. The Economic Journal, 89(353):66–83, 1979.

- [56] J.-C. Rochet and P. Choné. Ironing, sweeping, and multidimensional screening. Econometrica, 66(4):783–826, 1998.

- [57] W.P. Rogerson. The first–order approach to principal–agent problems. Econometrica, 53(6):1357–1368, 1985.

- [58] M. Royer. Backward stochastic differential equations with jumps and related non–linear expectations. Stochastic Processes and their Applications, 116(10):1358–1376, 2006.

- [59] B. Salanié. Sélection adverse et aversion pour le risque. Annales d’Économie et de Statistique, 18:131–149, 1990.

- [60] Y. Sannikov. A continuous–time version of the principal–agent problem. The Review of Economic Studies, 75(3):957–984, 2008.

- [61] Y. Sannikov. Contracts: the theory of dynamic principal–agent relationships and the continuous–time approach. In D. Acemoglu, M. Arellano, and E. Dekel, editors, Advances in economics and econometrics, 10th world congress of the Econometric Society, volume 1, economic theory, number 49 in Econometric Society Monographs, pages 89–124. Cambridge University Press, 2013.