Mean-Reverting Portfolio Design with Budget Constraint

Abstract

This paper considers the mean-reverting portfolio design problem arising from statistical arbitrage in the financial markets. We first propose a general problem formulation aimed at finding a portfolio of underlying component assets by optimizing a mean-reversion criterion characterizing the mean-reversion strength, taking into consideration the variance of the portfolio and an investment budget constraint. Then several specific problems are considered based on the general formulation, and efficient algorithms are proposed. Numerical results on both synthetic and market data show that our proposed mean-reverting portfolio design methods can generate consistent profits and outperform the traditional design methods and the benchmark methods in the literature.

Index Terms:

Portfolio optimization, mean-reversion, cointegration, pairs trading, statistical arbitrage, algorithmic trading, quantitative trading.I Introduction

Pairs trading [2, 3, 4, 5, 6] is a well-known trading strategy that was pioneered by scientists Gerry Bamberger and David Shaw, and the quantitative trading group led by Nunzio Tartaglia at Morgan Stanley in the mid 1980s. As indicated by the name, it is an investment strategy that focuses on a pair of assets at the same time. Investors or arbitrageurs embracing this strategy do not need to forecast the absolute price of every single asset in one pair, which by nature is hard to assess, but only the relative price of this pair. As a contrarian investment strategy, in order to arbitrage from the market, investors need to buy the under-priced asset and short-sell the over-priced one. Then profits are locked in after trading positions are unwound when the relative mispricing corrects itself in the future.

More generally, pairs trading with only two trading assets falls into the umbrella of statistical arbitrage [7, 8], where the underlying trading basket in general consists of three or more assets. Since profits from such arbitrage strategies do not depend on the movements and conditions of the general financial markets, statistical arbitrage is referred to as a kind of market neutral strategies [9, 10]. Nowadays, statistical arbitrage is widely used by institutional investors, hedge fund companies, and many individual investors in the financial markets.

In [11, 12], the authors first came up with the concept of cointegration to describe the linear stationary and hence mean-reverting relationship of underlying nonstationary time series which are named to be cointegrated. Later, the cointegrated vector autoregressive model [13, 14, 15, 16, 17] was proposed to describe the cointegration relations. Empirical and technical analyses [18, 19, 20, 21] show that cointegration can be used to get statistical arbitrage opportunities and such relations really exist in financial markets. Taking the prices of common stocks for example, it is generally known that a stock price is observed and modeled as a nonstationary random walk process that can be hard to predict efficiently. However, companies in the same financial sector or industry usually share similar fundamental characteristics, then their stock prices may move in company with each other under the same trend, based on which cointegration relations can be established. Two examples are the stock prices of the two American famous consumer staple companies Coca-Cola and PepsiCo and those of the two energy companies Ensco and Noble Corporation. Some examples for other financial assets, to name a few, are the future contract prices of E-mini S&P 500 and E-mini Dow, the ETF prices of SPDR S&P 500 and SPDR DJIA, the US dollar foreign exchange rates for different countries, and the swap rates for US interest rates of different maturities.

Mean-reversion is a classic indicator of predictability in financial markets and used to obtain arbitrage opportunities. Assets in a cointegration relation can be used to form a portfolio or basket and traded based upon their stationary mean-reversion property. We call such a designed portfolio or basket of underlying assets a mean-reverting portfolio (MRP) or sometimes a long-short portfolio which is also called a “spread”. An asset whose price shows naturally stationarity is a spread as well. The profits of statistical arbitrage come directly from trading on the mean-reversion of the spread around the long-run equilibrium. MRPs in practice are usually constructed using heuristic or statistical methods. Traditional statistical cointegration estimation methods are Engle-Granger ordinary least squares (OLS) method [12] and Johansen model-based method [14]. In practice, inherent correlations may exist among different MRPs. However, when having multiple MRPs, they are commonly traded separately with their possible connections neglected. So a natural and interesting question is whether we can design an optimized MRP based on the underlying spreads that could outperform every single one. In this paper, this issue is clearly addressed.

Designing one MRP by choosing proportions of various assets in general is a portfolio optimization or asset allocation problem [22]. Portfolio optimization today is considered to be an important part in portfolio management as well as in algorithmic trading. The seminal paper [23] by Markowitz in 1952 laid on the foundations of what is now popularly referred to as mean-variance portfolio optimization and modern portfolio theory. Given a collection of financial assets, the traditional mean-variance portfolio design problem is aimed at finding a tradeoff between the expected return and the risk measured by the variance. Different from the requirements for mean-variance portfolio design, in order to design a mean-reverting portfolio, there are two main factors to consider: i) the designed MRP should exhibit a strong mean-reversion indicating that it should have frequent mean-crossing points and hence bring in trading opportunities, and ii) the designed MRP should exhibit sufficient but controlled variance so that each trade can provide enough profit while controlling the probability that the believed mean-reversion equilibrium breaks down could be reduced.

In [24], the author first proposed to design an MRP by optimizing a criterion characterizing the mean-reversion strength which is a model-free method. Later, authors in [25] realized that solving the problem in [24] could result in a portfolio with very low variance, then the variance control was taken into consideration and also new criteria to characterize the mean-reversion property were proposed for the MRP design problem. In [24, 25], semidefinite programming (SDP) relaxation methods were used to solve the nonconvex problem formulations; however, these methods are very computationally costly in general. Besides that, the design methods in [24, 25] were all carried out by imposing an -norm constraint on the portfolio weights. This constraint brings mathematically convenience to the optimization problem, but its practical significance in financial applications is dubious since the -norm is not meaningful in a financial context. In this paper, we propose to use investment budget constraints in the design problems.

The contributions of this paper can be summarized as follows. First, a general problem formulation for MRP design problem is proposed based on which several specific problem formulations are elaborated by considering different mean-reversion criteria. Second, Two classes of commonly used investment budget constraints on portfolio weights are considered, namely, dollar neutral constraint and net budget constraint. Third, efficient algorithms are proposed for the proposed problem formulations, it is shown that some problems after reformulations can be tackled readily by solving the well-known generalized eigenvalue problem (GEVP) and the generalized trust region subproblem (GTRS). The other problems can be easily solved based on the majorization-minimization (MM) framework by solving a sequence of GEVPs and GTRSs, which are named iteratively reweighted generalized eigenvalue problem (IRGEVP) and iteratively reweighted generalized trust region subproblem (IRGTRS), respectively. An extension for IRGEVP with closed-form solution in every iteration named EIRGEVP (extended IRGEVP) is also proposed.

The remaining sections of this paper are organized as follows. In Section II, we introduce the design of mean-reverting portfolios. In Section III, we give out some mean-reversion criteria for an MRP, and a general formulation for the MRP design problem is proposed together with two commonly used investment budget constraint. Section IV develops the solving methods for GEVP and GTRS. The MM framework and MM-based solving algorithms are elaborated in Section V. The performance of the proposed algorithms are evaluated numerically in Section VI and, finally, the concluding remarks are drawn in Section VII.

Notation: Boldface upper case letters denote matrices, boldface lower case letters denote column vectors, and italics denote scalars. The notation and denote an all-one column vector and an identity matrix with proper size, respectively. denotes the real field with denoting positive real numbers and denoting the -dimensional real vector space. denotes the natural field. denotes the integer circle with denoting positive integer numbers. denotes the -dimensional symmetric matrices. The superscripts and denote the matrix transpose and inverse operator, respectively. Due to the commutation of the inverse and the transpose for nonsingular matrices, the superscript denotes the matrix inverse and transpose operator. denotes the (th, th) element of matrix and denotes the th element of vector . denotes the trace of a matrix. denotes the vectorization of a matrix, i.e., is a column vector consisting of all the columns of stacked. denotes the Kronecker product of two matrices.

II Mean-Reverting Portfolio (MRP)

For a financial asset, e.g., a common stock, a future contract, an ETF, or a portfolio of them, its price at time index or holding period is denoted by , and the corresponding logarithmic price or log-price is computed as , where is the natural logarithm.

If we consider a collection of assets in a basket, their log-prices can be accordingly denoted by . Based on this basket, an MRP is accordingly defined by the portfolio weight or hedge ratio and its (log-price) spread is defined as . Vector indicates the market value proportion invested on the underlying asset111If the spread is designed based on asset price instead of the log-price, indicates the asset amount proportion measured in shares.. For , , , and mean a long position (i.e., the asset is bought), a short position (i.e., the asset is short-sold, or, more plainly, borrowed and sold), and no position, respectively.

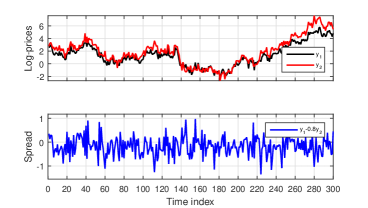

In Figure 1, the spread of a designed MRP together with the log-prices of the two underlying assets is given. It is worth noting that an MRP can be interpreted as a synthesized stationary asset. The spread accordingly means its log-price which could be easier to predict and to make profits from in comparison with the underlying component assets in this MRP.

Suppose there exist MRPs with their spreads denoted by . Different spreads may possess different mean-reversion and variance properties in nature. Our objective is to design an MRP to combine such spreads into an improved overall spread with better properties. In particular, we denote the portfolio by , where denotes the market value on the underlying spread. The resulting overall spread is then given by

| (1) |

III MRP Design Problem Formulations

Traditional portfolio design problems are based on the Nobel prize-winning Markowitz portfolio theory [23, 26, 27, 28]. They aim at finding a desired trade-off between return and risk, the latter being measured traditionally by the variance or, in a more sophisticated way, by value-at-risk and conditional value-at-risk. The recently proposed risk-parity portfolios [29, 30, 31] can also be categorized into this design problem.

For the mean-reverting portfolio, we can formulate the design problem by optimizing some mean-reversion criterion quantifying the mean-reversion strength of the spread , while controlling its variance and imposing an investment budget constraint.

III-A Mean-Reversion Criteria

In this section, we introduce several mean-reversion criteria that can characterize the mean-reversion strength of the designed spread . We start by defining the th order (lag-) autocovariance matrix for a stochastic process as

| (2) |

where . Specifically, when , stands for the (positive definite) covariance matrix of .

Since for any random process , we can get its centered counterpart as , in the following, we will use to denote its centered form .

III-A1 Predictability Statistics

Consider a centered univariate stationary autoregressive process written as follows:

| (3) |

where is the prediction of based on the information up to time , and denotes a white noise independent from . The predictability statistics [32] is defined as

| (4) |

where and . If we define , then from (4), we can have in the denominator. When is small, the variance of dominates that of , and behaves like a white noise; when is large, the variance of dominates that of , and can be well predicted by . The predictability statistics is usually used to measure how close a random process is to a white noise.

Under this criterion, in order to design a spread as close as possible to a white noise process, we need to minimize . For a spread , we assume the spread follows a centered vector autoregressive model of order (VAR()) as follows:

| (5) |

where is the autoregressive coefficient and denotes a white noise independent from . We can get from the autocorrelation matrices as . Multiplying (5) by and further defining and , we can get , and , where . High order models VAR(), with , can be trivially reformulated into VAR() with proper reparametrization [33]. Then the estimator of predictability statistics for is computed as

| (6) |

III-A2 Portmanteau Statistics

The portmanteau statistics of order [34] for a centered univariate stationary process is defined as

| (7) |

where is the th order autocorrelation (autocorrelation for lag ) of defined as . The portmanteau statistics is used to test whether a random process is close to a white noise. From the above definition, we have and the minimum of is attained by a white noise process, i.e., the portmanteau statistics for a white noise process is for any .

Under this criterion, in order to get a spread close to a white noise process, we need to minimize for a prespecified order . For an MRP , the th order autocorrelation is given by

| (8) |

Then we can get the expression for as

| (9) |

III-A3 Crossing Statistics and Penalized Crossing Statistics

Crossing statistics (zero-crossing rate) of a centered univariate stationary process is defined as

| (10) |

where is the indicator function defined as , and the event here is . Crossing statistics is used to test the probability that a stationary process crosses its mean per unit of time and it is easy to notice that . According to [35, 36], for a centered stationary Gaussian process , we have the following relationship:

| (11) |

Remark 1.

As a special case, if is a centered stationary AR(1),

| (12) |

where and is a Gaussian white noise, then and accordingly the crossing statistics is .

Using this criterion, in order to get a spread having many zero-crossings, instead of directly maximizing , we can minimize . For a spread , we can try to minimize the first order autocorrelation of given in (8). In [25], besides minimizing the first order autocorrelation, it is also proposed to ensure the absolute autocorrelations of high orders s () are small at the same time which can result in good performance. In this paper, we also adopt this criterion and call it penalized crossing statistics of order defined by

| (13) |

where is a positive prespecified penalization factor.

III-B General MRP Design Problem Formulation

The MRP design problem is formulated as the optimization of a mean-reversion criterion denoted in general as , which can be taken to be any of the criteria mentioned before. This unified criterion can be written into a compact form as

| (14) |

which particularizes to i) , when , , and ; ii) , when , and ; iii) , when , , and ; and iv) , when , , , and . The matrices s in (14) are assumed symmetric without loss of generality since they can be symmetrized.

The variance of the spread should also be controlled to a certain level which can be represented as . Due to this variance constraint, the denominators of can be removed. Denoting the portfolio investment budget constraint by , the general MRP design problem can be formulated as follows:

| (15) |

where the objective function is denoted by in the following. The problem in (15) is a nonconvex problem due to the nonconvexity of the objective function and the constraint set.

III-C Investment Budget Constraint

In portfolio optimization, constraints are usually imposed to represent the specific investment guidelines. In this paper, we use to denote it and we focus on two types of budget constraints: dollar neutral constraint and net budget constraint.

Dollar neutral constraint, denoted by , means the net investment or net portfolio position is zero; in other words, all the long positions are financed by the short positions, commonly termed self-financing.222Dollar neutral constraint generally cannot be satisfied by the traditional design methods, like methods in [12] and [14], and the methods in [25]. It is represented mathematically by

| (16) |

Net budget constraint, denoted by , means the net investment or net portfolio position is nonzero and equal to the current budget which is normalized to one.333The net portfolio position can be positive or negative under net budget constraint. Since the problem formulation in (15) is invariant to the sign of , only the case that budget is normalized to positive 1 is considered. It is represented mathematically by

| (17) |

It is worth noting that, for two trading spreads defined by and , they are naturally the same, because in statistical arbitrage the actual investment not only depends on , which defines a spread, but also on whether a long or short position is taken on this spread in the trading.

IV Problem Solving Algorithms via GEVP and GTRS Algorithms

In this section, solving methods for the MRP design problem formulations using and (i.e., (15) with ) are introduced.

IV-A GEVP - Solving Algorithm for MRP Design Using and with

For notational simplicity, we denote the matrices in and in by matrix in general and recast the problem as follows:

| (18) |

where is a positive constant. The above problem is equivalent to the following nonconvex quadratically constrained quadratic programming (QCQP) [37] formulation:

| (19) |

where . By using the matrix lifting technique, i.e., defining , the above problem can be solved by the following convex SDP relaxation problem:

| (20) |

The following theorem gives a useful relationship between the number of variables and the number of equality constraints.

Theorem 2 ([38, Theorem 3.2]).

Given a separable SDP as follows:

| (21) |

Suppose that the separable SDP are strictly feasible. Then, the problem has always an optimal solution such that

Observe that if there is only one variable , that is to say, , we can get . Further, if the number of constraints , a rank- solution can always be attainable.

In other words, by solving the convex SDP in (20), there always exists a rank- solution for which is the solution for the original problem (18), however, in practice, to find such a solution, rank reduction methods [39] should be applied which could be computationally expensive.

As an alternative to the SDP procedure mentioned above, we find the problem in (18) can be efficiently solved as a generalized eigenvalue problem (GEVP) [40] by reformulation. Considering , where is the kernel that spans the null space of , i.e., , and also required to be semi-unitary, i.e., , we can define and which is positive definite, then the problem (18) is equivalent to the following problem:

| (22) |

which is still a nonconvex QCQP. However, this problem becomes the classical GEVP problem and can be easily dealt with using tailored algorithms. Here, we will apply the steepest descent algorithm [41] to solve it. The procedure to solve problem (18) is summarized in Algorithm 1.

IV-B GTRS - Solving Algorithm for MRP Design Using and with

As before, for generality, we denote matrices in and in as . Then the problems can be rewritten as

| (23) |

where is a positive constant. As before, rewriting the constraint as (since the problem is invariant with respect to a sign change in ) and using the matrix lifting technique, the problem in (23) can be solved by the following convex SDP problem:

| (24) |

Like before, the nonconvex problem in (23) has no duality gap. Besides the above SDP method, here we introduce an efficient solving approach by reformulating (23) into a generalized trust region subproblem (GTRS) [42]. Considering where is any vector satisfying and is the kernel of satisfying and a semi-unitary matrix satisfying . Let us define , , , which is positive definite, , and , then the problem in (23) is equivalent to the following problem:

| (25) |

which is a nonconvex QCQP and QCQPs of this type are specially named GTRSs. Such problems are usually nonconvex but possess necessary and sufficient optimality conditions based on which efficient solving methods can be derived. We first introduce the following useful theorem.

Theorem 4 ([42, Theorem 3.2]).

Consider the following QCQP:

| (26) |

Assume that the constraint set is nonempty and that . A vector is a global minimizer of the problem (26) together with a multiplier if and only if the following conditions are satisfied:

and the interval set defined by

is not empty.

According to Theorem 4, the optimality conditions for the primal and dual variables of problem (25) are given as follows:

| (27) |

We assume 444The limiting case being singular (i.e., ) can be treated separately. The assumption here is reasonable since the case when is very rare to occur theoretically and practically. , then we can see that the optimal solution is given by

| (28) |

and is the unique solution of the following equation with definition on the interval :

| (29) |

where the function is defined by

| (30) |

and the interval consists of all for which , which implies that

| (31) |

where is the minimum generalized eigenvalue of matrix pair .

Theorem 5 ([42, Theorem 5.2]).

Assume is not empty, then the function is strictly decreasing on unless is constant on .

In practice, the case is constant on cannot happen. So from Theorem (5), we know when is strictly decreasing on , then a simple line search algorithm like bisection algorithm can be used to find the optimal over . The algorithm for problem (23) is summarized in Algorithm 2.

V Problem Solving Algorithms via Majorization-Minimization Method

In this section, we first discuss the majorization-minimization or minorization-maximization (MM) method briefly, and then solving algorithms for the MRP design problem formulations using (i.e., (15) with and ) and (i.e., (15) with , , and ) are derived based on the MM framework and the GEVP and GTRS algorithms mentioned in the previous section.

V-A The MM Method

The MM method [43, 44, 45] refers to the majorization-minimization or minorization-maximization which is a generalization of the well-known expectation-maximization (EM) algorithm. The idea behind MM is that instead of dealing with the original optimization problem which could be difficult to tackle directly, it solves a series of simple surrogate subproblems.

Suppose the optimization problem is

| (32) |

where the constraint set . In general, there is no assumption about the convexity and differentiability on . The MM method aims to solve this problem by optimizing a sequence of surrogate functions that majorize the objective function over the set . More specifically, starting from an initial feasible point , the algorithm produces a sequence according to the following update rule:

| (33) |

where is the point generated by the update rule at the th iteration and the surrogate function is the corresponding majorizing function of at point . A surrogate function is called a majorizing function of at point if it satisfies the following properties:

| (34) |

That is to say, the surrogate function should be an upper bound of the original function over and coincide with at point . Although the definition of gives us a great deal of flexibility for choosing it, in practice, the surrogate function must be properly chosen so as to make the iterative update in (33) easy to compute while maintaining a fast convergence over the iterations.

The MM method iteratively runs until some convergence criterion is met. Under this MM method, the objective function value is decreased monotonically in every iteration, i.e.,

| (35) |

The first inequality and the third equality follow from the first and second properties of the majorizing function in (34) respectively and the second inequality follows from (33).

V-B IRGEVP and IRGTRS - Solving Algorithms for MRP Design Using and

We rewrite the problems using and in the general formulation as follows:

| (36) |

where the specific portfolio weight constraints are implicitly replaced by .

To solve the problems in (36) via majorization-minimization, the key step is to find a majorizing function of the objective function such that the majorized subproblem is easy to solve. Observe that the objective function is quartic in . The following mathematical manipulations are necessary. We first compute the Cholesky decomposition of which is , where is a lower triangular with positive diagonal elements. Let us define , , and . The portfolio weight set is mapped to under the linear transformation . Then problem (36) can be written as

| (37) |

Since (recall the s are assumed symmetric), problem (36) can be reformulated as

| (38) |

where in the objective function

| (39) |

Specifically, we can have the expressions for portmanteau statistics (i.e., and ) and penalized crossing statistics (i.e., and ) as follows:

| (40) |

Now, the objective function in (38) is a quadratic function of , however, this problem is still hard to solve due to the rank-1 constraint . We then consider the application of the MM trick on this problem (38) based on the following simple result.

Lemma 6 ([41, Lemma 1]).

Let and such that . Then for any point , the quadratic function is majorized by at .

According to Lemma 6, given at the th iteration, we know the second part in the objective function of problem (38) is majorized by the following majorizing function at :

| (41) |

where is a scalar number depending on and satisfying . Since the first term and the last term only depends on , they are just two constants.

On the choice of , according to Lemma 6, it is obvious to see that can be easily chosen to be . In the implementation of the algorithm, although only needs to be computed once for the whole algorithm, it is still not computationally easy to get. In view of this, we introduce the following lemma to obtain more possibilities for which could be relatively easy to compute.

According to the above relations, can be chosen to be any number is larger than but much easier to compute.

| (42) |

which can be further written as

| (43) |

By changing back to , problem (43) becomes

| (44) |

where in the objective function, is defined in this way . Finally, we can undo the change of variable , obtaining

| (45) |

where in the objective function

| (46) |

More specifically, for portmanteau statistics (i.e., , and ) and penalized crossing statistics (i.e., , and ), we have the following expressions:

| (47) |

Finally, in the majorization problems (44) and (45), the objective functions become quadratic in the variable rather than quartic in the variable as in the original problem (36). Depending on the specific form of , problem (45) is either the GEVP or GTRS problems discussed in the previous sections. So, in order to handle the original problem (36) directly which could be difficult, we just need to iteratively solve a sequence of GEVPs or GTRSs. We call these MM-based algorithms iteratively reweighted GEVP (IRGEVP) and iteratively reweighted GTRS (IRGTRS) respectively which are summarized in Algorithm 3.

V-C EIRGEVP - An Extended Algorithm for IRGEVP

In the MM-based algorithms mentioned above, it would be much desirable if we could get a closed-form solution for the subproblems in every iteration. In fact, for IRGEVPs, applying the MM trick once again, a closed-form solution is attainable at every iteration. To illustrate this, we rewrite the subproblem (44) of IRGEVP again as follows:

| (48) |

Considering the trick used to eliminate the linear constraint to get problem (22), we can get the following equivalent formulation:

| (49) |

where and are defined as before; . Considering the Cholesky decomposition with to be a lower triangular with positive diagonal elements, we can have the variable transformation . Then the problem (48) becomes

| (50) |

where .

Applying Lemma 6 again, the objective function of problem (50) is majorized by the following majorizing function at :

| (51) |

where can be chosen using the results from Lemma 7. The first and last parts are just two constants. Note that although in the derivation we have applied the MM scheme twice, it can be viewed as a direct majorization for the objective of the original problem at . The following lemma summarizes the overall majorizing function.

Lemma 8.

For problem (36) with , the majorization in (41) together with (51) can be shown to be a majorization for the objective function of the original problem at over the constraint set by the following function:

| (52) |

where the last two terms are constants.

Proof:

See Appendix A. ∎

Then, the majorized problem of (50) becomes

| (53) |

where for the majorization in (51). By Cauchy-Schwartz inequality, we have , and the equality holds only when and are aligned in the opposite direction. Considering the constraint, we can get the optimal solution of (53) as . We call this algorithm extended IRGEVP (EIRGEVP) which is summarized in Algorithm 4.

VI Numerical Experiments

A statistical arbitrage strategy involves several steps of which the MRP design is a central one. Here, we divide the whole strategy into four sequential steps, namely: assets pool construction, MRP design, unit-root test, and mean-reversion trading. In the first step, we select a collection of possibly cointegrated asset candidates to construct an asset pool, on which we will not elaborate in this paper. In the second step, based on the candidate assets from the asset pool, MRPs are designed using either traditional design methods like Engle-Granger OLS method [12] and Johansen method [13] or the proposed methods in this paper. In the third step, unit-root test procedures like Augmented Dickey-Fuller test [46] and Phillips-Perron test [47] are applied to test the stationarity or mean-reversion property of the designed MRPs. In the fourth step, MRPs passing the unit-root tests will be traded based on a designed mean-reversion trading strategy.

In this section, we first illustrate a mean-reversion trading strategy and based on that the performance of our proposed MRP design methods in Sections IV and V using both synthetic data and real market data are shown accordingly.

VI-A Mean-Reversion Trading Design

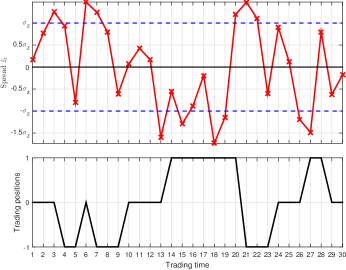

In this paper, we use a simple trading strategy where the trading signals, i.e., to buy, to sell, or simply to hold, are designed based on simple event triggers. Mean-reversion trading is carried out on the designed spread which is tested to be unit-root stationary. A trading position (either a long position denoted by or a short position denoted by ) denotes a state for investment and it is opened when the spread is away from its long-run equilibrium by a predefined trading threshold and closed (denoted by ) when crosses its equilibrium . (A common variation is to close the position after the spread crossed the equilibrium by more than another threshold .) The time period from position opening to position closing is defined as a trading period.

In order to get a standard trading rule, we introduce a standardization technique by defining which is a normalized spread as follows:

| (54) |

where and are the mean and the standard deviation of the spread and computed over an in-sample look-back period in practice. For , it follows that and . Then, we can define , for some value of (e.g., ).

In a trading stage, based on the trading position and observed (normalized) spread value at holding period , we can get the trading actions at the next consecutive holding period . The mean-reversion trading strategy is summarized in Table I and a simple trading example based on this strategy is illustrated in Figure 2.

| Trading Position at | Normalized Spread | Action(s) Taken within Holding Period | Trading Position at |

|---|---|---|---|

| 1 | Close the long pos. & Open a short pos. | -1 | |

| Close the long pos. | 0 | ||

| No action | 1 | ||

| 0 | Open a short pos. | -1 | |

| No action | 0 | ||

| Open a long pos. | 1 | ||

| -1 | No action | -1 | |

| Close the short pos. | 0 | ||

| Close the short pos. & Open a long pos. | 1 |

VI-B Performance Metrics

After an MRP is constructed, we need to define the relation between the designed MRP with the underlying financial assets. Recall that the spread for the designed MRP is , where with for . By defining with , we get the spread , where denotes the portfolio weight directly defined on the underlying assets.

Based on the mean-reversion trading strategy introduced before and the MRP defined by here, we employ the following performance metrics in the numerical experiments.

VI-B1 Portfolio Return Measures

In the following, we first give the return definition for one single asset, and after that, several different return measures for an MRP are talked about.

For one single asset, the return or cumulative return at time for holding periods is defined as , where in the parentheses denotes the period length and is usually omitted when the length is one. Here, the return as a rate of return is used to measure the aggregate amount of profits or losses (in percentage) of an investment strategy on one asset over a time period .

Profit and Loss (P&L)

The profit and loss (P&L) measures the amount of profits or losses (in units of dollars) of an investment on the portfolio for some holding periods.

Within one trading period, if a long position is opened on an MRP at time and closed at time , then the multi-period P&L of this MRP at time () accumulated from is computed as , where denotes the length of the holding periods, and is the return vector. More generally, the cumulative P&L of this MRP at time for () holding periods is defined as

| (55) |

where we define . Then we have the single-period P&L (e.g., daily P&L, monthly P&L) denoted by at time (i.e., ) is computed as

| (56) |

Likewise, within one trading period, if a short position is opened on this MRP, then multi-period P&L is and the single-period P&L is . About the portfolio P&L calculation within the trading periods, we have the following lemma.

Lemma 9 (P&L Calculation for Mean-Reversion Trading).

Within one trading period, if the price change of every asset in an MRP is small enough, then the P&L in (55) can be approximately calculated by the change of the log-price spread . Specifically,

1) for a long position opened on the MRP, ; and

2) for a short position opened on the MRP, .

Proof:

See Appendix B. ∎

This lemma reveals the philosophy of the MRP design and also the mean-reversion trading by showing the connection between the log-price spread value and the portfolio return.

Since there is no trading conduct between two trading periods, the P&L measures (both the multi-period P&L and single-period P&L) are simply defined to be 0.

Cumulative P&L

In order to measure the cumulative return performance for an MRP, we define the cumulative P&L in one trading from time to as

| (57) |

Return on Investment (ROI)

Since different MRPs may have different leverage properties due to , we introduce another portfolio return measure (rate of return) called return on investment (ROI).

Within one trading period, the ROI at time () is defined to be the single-period P&L at time normalized by the gross investment deployed which is (that is the gross investment exposure to the market including the long position investment and the short position investment) written as

| (58) |

Like the P&L measures, between two trading periods, is defined to be 0.

VI-B2 Sharpe Ratio (SR)

The Sharpe ratio (SR) [48] is a measure for calculating risk-adjusted return. It describes how much excess return one can receive for the extra volatility (square root of variance).

Here, the Sharpe ratio of ROI (or, equivalently, Sharpe ratio of P&L) for a trading stage from time to is defined as follows:

| (59) |

where and . In the computation of the Sharpe ratio, we set the risk-free return to , in which case it reduces to the information ratio.

VI-C Synthetic Data Experiments

For synthetic data experiments, we generate the sample path of log-prices for financial assets using a multivariate cointegrated systems [49, 33], where there are long-run cointegration relations and common trends. We divide the sample path into two stages: in-sample training stage and out-of-sample backtesting or trading stage. All the parameters like spread equilibrium , trading threshold , and portfolio weight are decided in the training stage. The out-of-sample performance of our design methods are tested in the trading stage.

In the synthetic experiments, we set and and only show the performance of the MRP design methods under net budget constraint . We estimate spreads using the generated sample path. Based on these spreads, an MRP is designed as . The simulated log-prices and the spreads for the trading stage are shown in Figure 3.

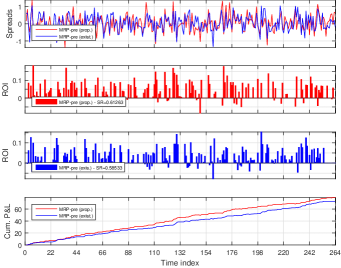

The performance of the MRP designed using our proposed methods are compared with those of one underlying spread and the method in [25] based on and , which are shown in Figure 4 and Figure 5. From our simulations, we can conclude that our designed MRPs do generate consistent positive profits. And simulation results also show that our designed portfolios can outperform the underlying spreads and the MRPs designed using methods in [25] with higher Sharpe ratios of ROIs and higher cumulative P&Ls.

VI-D Market Data Experiments

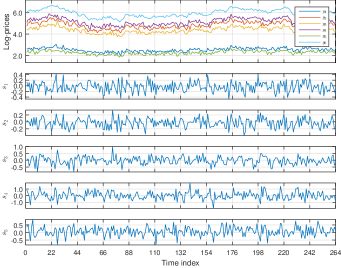

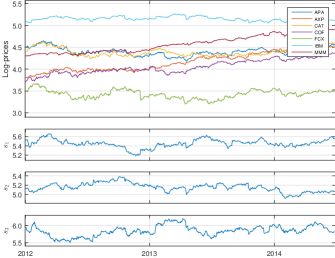

We also test our methods using real market data from the Standard & Poor’s 500 (S&P 500) Index, which is usually considered as one of the best representatives for the U.S. stock markets. The data are retrieved from Yahoo! Finance555http://finance.yahoo.com and adjusted daily closing stock prices are employed. We first choose stock candidates which are possibly cointegrated to form stock asset pools. One stock pool is , where the stocks are denoted by their ticker symbols. Three spreads are constructed from this pool. Then MRP design methods are employed and unit-root tests are used to test their tradability. The log-prices of the stocks and the log-prices for the three spreads are shown in Figure 6.

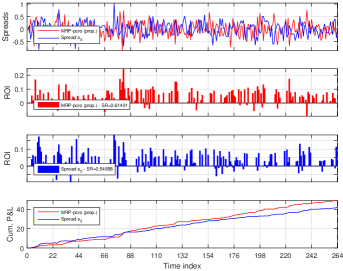

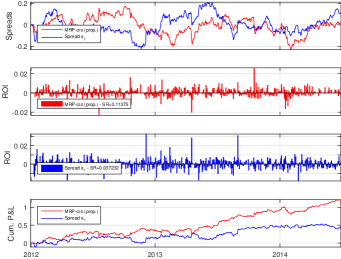

Based on the mean-reversion trading framework mentioned before, one trading experiment is carried out from February 1st, 2012 to June 30th, 2014. In Figure 7, we compare the performance of our designed MRP with the underlying spread . The log-prices for the designed spreads, and the out-of-sample performance like ROIs, Sharpe ratios of ROIs, and cumulative P&Ls are reported. It is shown that using our method, the designed MRP can achieve a higher Sharpe ratio and a better final cumulative return.

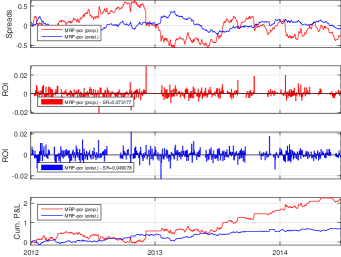

We also compare our proposed design method with the method in [25] using in Figure 8. We can see that our method can outperform the benchmark method in terms of Sharpe ratio and the return performance.

VII Conclusions

The mean-reverting portfolio design problem arising from statistical arbitrage has been considered in this paper. We have formulated the MRP design problem in a general form by optimizing a mean-reversion criterion characterizing the mean-reversion strength of the portfolio and, at the same time, taking into consideration the variance of the portfolio and an investment budget constraint. Several specific optimization problems have been proposed based on the general design idea. Efficient algorithms have been derived to solve the design problems. Numerical results show that our proposed methods are able to generate consistent positive profits and significantly outperform the the design methods in literature.

Appendix A Proof for Lemma 8

For problem (36) with , the majorizing function in the first majorization step (41) is denoted by , and the majorizing function in the second step (51) is denoted by . From the majorization properties in (34), then we can have have this relationship: .

Then we can get the overall majorization in for the objective function of the original problem at over the constraint set by the following function:

where the last two terms in every step of the derivations are constants since they are independent of the optimization variables.

Appendix B Proof for Lemma 9

Since the spread is defined as , then the multi-period P&L at time for holding periods is given by

The approximation in the fourth step follows from when , where denotes the natural logarithm. Similarly, for a short position on the MRP, the calculation of is given by .

References

- [1] Z. Zhao and D. P. Palomar, “Mean-reverting portfolio design via majorization-minimization method,” arXiv preprint arXiv:1611.08393, 2016.

- [2] G. Vidyamurthy, Pairs Trading: quantitative methods and analysis. John Wiley & Sons, 2004, vol. 217.

- [3] D. S. Ehrman, The handbook of pairs trading: Strategies using equities, options, and futures. John Wiley & Sons, 2006, vol. 240.

- [4] R. Bookstaber, A Demon of Our Own Design: Markets, Hedge Funds, and the Perils of Financial Innovation. John Wiley & Sons, 2007.

- [5] W. Goetzmann, K. G. Rouwenhorst et al., “Pairs trading: Performance of a relative value arbitrage rule,” Yale School of Management, Tech. Rep., 1998.

- [6] E. Gatev, W. N. Goetzmann, and K. G. Rouwenhorst, “Pairs trading: Performance of a relative-value arbitrage rule,” Review of Financial Studies, vol. 19, no. 3, pp. 797–827, 2006.

- [7] A. Pole, Statistical arbitrage: algorithmic trading insights and techniques. John Wiley & Sons, 2011, vol. 411.

- [8] S. F. LeRoy and J. Werner, Principles of financial economics. Cambridge University Press, 2014.

- [9] B. I. Jacobs and K. N. Levy, Market Neutral Strategies. John Wiley & Sons, 2005, vol. 112.

- [10] J. G. Nicholas, Market Neutral Investing: Long/Short Hedge Fund Strategies. Bloomberg Press, 2000.

- [11] C. W. Granger, “Cointegrated variables and error correction models,” unpublished USCD Discussion Paper 83-13a, Tech. Rep., 1983.

- [12] R. F. Engle and C. W. Granger, “Co-integration and error correction: representation, estimation, and testing,” Econometrica: Journal of the Econometric Society, pp. 251–276, 1987.

- [13] S. Johansen, “Statistical analysis of cointegration vectors,” Journal of economic dynamics and control, vol. 12, no. 2, pp. 231–254, 1988.

- [14] ——, “Estimation and hypothesis testing of cointegration vectors in gaussian vector autoregressive models,” Econometrica: Journal of the Econometric Society, pp. 1551–1580, 1991.

- [15] R. Larsson and S. Johansen, “Likelihood-based inference in cointegrated vector autoregressive models,” 1997.

- [16] S. Johansen, “Modelling of cointegration in the vector autoregressive model,” Economic modelling, vol. 17, no. 3, pp. 359–373, 2000.

- [17] ——, Likelihood-Based Inference in Cointegrated Vector Autoregressive Models, ser. OUP Catalogue. Oxford university press, May 1995, no. 9780198774501.

- [18] M. Avellaneda and J.-H. Lee, “Statistical arbitrage in the US equities market,” Quantitative Finance, vol. 10, no. 7, pp. 761–782, 2010.

- [19] C. L. Dunis, G. Giorgioni, J. Laws, and J. Rudy, “Statistical arbitrage and high-frequency data with an application to Eurostoxx 50 equities,” Liverpool Business School, Working paper, 2010.

- [20] J. F. Caldeira and G. V. Moura, “Selection of a portfolio of pairs based on cointegration: The brazilian case,” Federal University of Rio Grande do Sul, Federal University of Santa Catarina, Brazil, 2012.

- [21] S. Drakos, “Statistical arbitrage in S&P500,” Journal of Mathematical Finance, vol. 6, no. 01, p. 166, 2016.

- [22] J. L. Farrell and W. J. Reinhart, Portfolio management: theory and application. McGraw-Hill, 1997.

- [23] H. M. Markowitz, “Portfolio selection,” The Journal of Finance, vol. 7, no. 1, pp. 77–91, 1952.

- [24] A. d’Aspremont, “Identifying small mean-reverting portfolios,” Quantitative Finance, vol. 11, no. 3, pp. 351–364, 2011.

- [25] M. Cuturi and A. d’Aspremont, “Mean reversion with a variance threshold,” in Proceedings of the 30th International Conference on Machine Learning (ICML-13), 2013, pp. 271–279.

- [26] H. M. Markowitz, “The optimization of a quadratic function subject to linear constraints,” Naval research logistics Quarterly, vol. 3, no. 1-2, pp. 111–133, 1956.

- [27] W. F. Sharpe, “Capital asset prices: A theory of market equilibrium under conditions of risk,” The journal of finance, vol. 19, no. 3, pp. 425–442, 1964.

- [28] H. M. Markowitz, Portfolio selection: efficient diversification of investments. Yale university press, 1968, vol. 16.

- [29] E. Qian, “Risk parity and diversification,” Journal of Investing, vol. 20, no. 1, p. 119, 2011.

- [30] D. B. Chaves, J. C. Hsu, F. Li, and O. Shakernia, “Risk parity portfolio vs. other asset allocation heuristic portfolios,” Journal of Investing, vol. 20, no. 1, pp. 108–118, 2011.

- [31] Y. Feng and D. P. Palomar, “SCRIP: Successive convex optimization methods for risk parity portfolio design,” IEEE Transactions on Signal Processing, vol. 63, no. 19, pp. 5285–5300, 2015.

- [32] G. E. Box and G. C. Tiao, “A canonical analysis of multiple time series,” Biometrika, vol. 64, no. 2, pp. 355–365, 1977.

- [33] H. Lütkepohl, New introduction to multiple time series analysis. Springer, 2007.

- [34] G. E. Box and D. A. Pierce, “Distribution of residual autocorrelations in autoregressive-integrated moving average time series models,” Journal of the American statistical Association, vol. 65, no. 332, pp. 1509–1526, 1970.

- [35] N. D. Ylvisaker, “The expected number of zeros of a stationary gaussian process,” The Annals of Mathematical Statistics, vol. 36, no. 3, pp. 1043–1046, 1965.

- [36] B. Kedem and S. Yakowitz, Time series analysis by higher order crossings. IEEE press Piscataway, NJ, 1994.

- [37] S. Boyd and L. Vandenberghe, Convex optimization. Cambridge university press, 2004.

- [38] Y. Huang and D. P. Palomar, “Rank-constrained separable semidefinite programming with applications to optimal beamforming,” IEEE Transactions on Signal Processing, vol. 58, no. 2, pp. 664–678, 2010.

- [39] ——, “Randomized algorithms for optimal solutions of double-sided qcqp with applications in signal processing,” IEEE Transactions on Signal Processing, vol. 62, no. 5, pp. 1093–1108, 2014.

- [40] R. A. Horn and C. R. Johnson, Matrix analysis. Cambridge university press, 2012.

- [41] J. Song, P. Babu, and D. P. Palomar, “Optimization methods for designing sequences with low autocorrelation sidelobes,” IEEE Transactions on Signal Processing, vol. 63, no. 15, pp. 3998–4009, 2015.

- [42] J. J. Moré, “Generalizations of the trust region problem,” Optimization methods and Software, vol. 2, no. 3-4, pp. 189–209, 1993.

- [43] D. R. Hunter and K. Lange, “A tutorial on MM algorithms,” The American Statistician, vol. 58, no. 1, pp. 30–37, 2004.

- [44] M. Razaviyayn, M. Hong, and Z.-Q. Luo, “A unified convergence analysis of block successive minimization methods for nonsmooth optimization,” SIAM Journal on Optimization, vol. 23, no. 2, pp. 1126–1153, 2013.

- [45] Y. Sun, P. Babu, and D. P. Palomar, “Majorization-minimization algorithms in signal processing, communications, and machine learning,” IEEE Transactions on Signal Processing, vol. PP, no. 99, p. 1, 2016.

- [46] D. A. Dickey and W. A. Fuller, “Distribution of the estimators for autoregressive time series with a unit root,” Journal of the American statistical association, vol. 74, no. 366a, pp. 427–431, 1979.

- [47] P. C. Phillips and P. Perron, “Testing for a unit root in time series regression,” Biometrika, vol. 75, no. 2, pp. 335–346, 1988.

- [48] W. F. Sharpe, “The sharpe ratio,” The journal of portfolio management, vol. 21, no. 1, pp. 49–58, 1994.

- [49] R. S. Tsay, Analysis of financial time series. John Wiley & Sons, 2005, vol. 543.