Breaking the Target: An Analysis of

Target Data Breach and Lessons Learned

Abstract

This paper investigates and examines the events leading up to the second most devastating data breach in history: the attack on the Target Corporation. It includes a thorough step-by-step analysis of this attack and a comprehensive anatomy of the malware named BlackPOS. Also, this paper provides insight into the legal aspect of cybercrimes, along with a prosecution and sentence example of the well-known TJX case. Furthermore, we point out an urgent need for improving security mechanisms in existing systems of merchants and propose three security guidelines and defenses. Credit card security is discussed at the end of the paper with several best practices given to customers to hide their card information in purchase transactions.

Index Terms:

Data breach, information leak, point-of-sale malware, cybercrime, network segmentation, security alert, system integrity, credit card security, EMV, tokenization1 Introduction

Between November 27 and December 18, 2013, the Target Corporation’s network was breached, which became the second largest credit and debit card breach after the TJX breach in 2007. In the Target incident, 40 million credit and debit card numbers and 70 million records of personal information were stolen. The ordeal cost credit card unions over two hundred million dollars for just reissuing cards.

Target Corp. is not the only target of data breaches. Up to the 23rd of September, 568 data breaches are reported in the year 2014 [1]. The latest significant breach, i.e., the Home Depot breach, came to light in September 2014. As of September 14, it is known that 23 out of 28 Home Depot stores in the State of Alabama were breached [2]. The entire plot could involve a large portion of the 2,200 Home Depot stores in the states and 287 stores overseas, which might result in a larger breach than the Target breach. We list four other significant breaches in the last two years. The increasing number and scale of data breach incidents are alarming.

-

•

Sally Beauty Supply discovered in March 2014 that 282,000 cards were stolen [3].

-

•

Neiman Marcus reported that 1.1 million cards were stolen during July to October, 2013 [4].

-

•

Michaels and Aaron Brother reported that 3 million cards were stolen from May 2013 to January 2014 [5].

-

•

P.F. Chang’s data breach occurred from September 2013 to June 2014 impacting over 7 million cards [6].

Securing massive amounts of connected systems is known to be technically challenging, especially for retailers those possess vast networks across the nation, like Target and Home Depot. Target security division attempted to protect their systems and networks against cyber threats such as malware and data exfiltration. Six months prior to the breach, Target deployed a well-known and reputable intrusion and malware detection service named FireEye [7], which was guided by the CIA during its early development [8]. Unfortunately, multiple malware alerts were ignored. Some prevention functionalities were turned off by the administrators who were not familiar with the FireEye system. Target Corp. missed the early discovery of the breach.

This paper analyzes Target’s data breach incident from both technical and legal perspectives. The description of the incident and the analysis of the involved malware explain how flaws in the Target’s network were exploited and why the breach was undiscovered for weeks. The Target data breach is still under investigation and there is no arrest made known to the public. Even if the perpetrators are identified, cyber crimes involving extradition are notorious to prosecute. We discuss the difficulties of data breach discovery, investigation and prosecution with respect to legislation and international cooperation. An earlier incident, TJX data breach in 2007, is presented as the precedent for arresting and sentencing criminals committing financial cybercrimes.

As we observe an increasing number of data breaches, these incidents bring us to rethink the effectiveness of existing security mechanisms, solutions, deployments and executions. Credit card breach has a huge negative impact on every entity in the payment ecosystem, including merchants, banks, card associations and customers. In this paper, we provide several insights into weak links in the payment ecosystem, specifically in existing security techniques and practices. We give several best practice suggestions for merchants and customers to enforce their data security and to minimize information leak.

The contributions of our work are summarized as follows.

-

•

We gather and verify information from multiple sources and describe the process of the Target data breach in details (Section 2).

-

•

We provide an in-depth analysis of the major malware used in the Target breach, including its design features for circumventing detections as well as the marketing of the malware (Section 3).

-

•

We discuss the complexities and challenges in data breach investigation and criminal prosecution, specifically from the legal perspective. We describe the TJX breach in 2007 as a precedent for arresting and sentencing cyber criminals (Section 4).

-

•

We provide three security guidelines for merchants to enhance their payment system security: i) payment system integrity enforcement, ii) effective alert system design, and iii) proper network segmentation (Section 5).

-

•

We discuss the current status of credit card security, point out problems in the credit card system, and give customers best practices to hide their information in purchase transactions (Section 6).

2 The Target Incident

The systems and networks of Target Corp. were breached in November and December, 2013, which results in 40 million card numbers and 70 million personal records stolen [9]. Multiple parties get involved in the federal investigation of the incident. The list includes United State Secret Service, iSIGHT Partners, DELL SecureWorks, Seculert, the FBI, etc. In addition, companies like HP, McAfee and IntelCrawler provide analysis of the discovered malware, i.e., BlackPOS, and the marketing of the stolen cards.

2.1 Breach Into Target

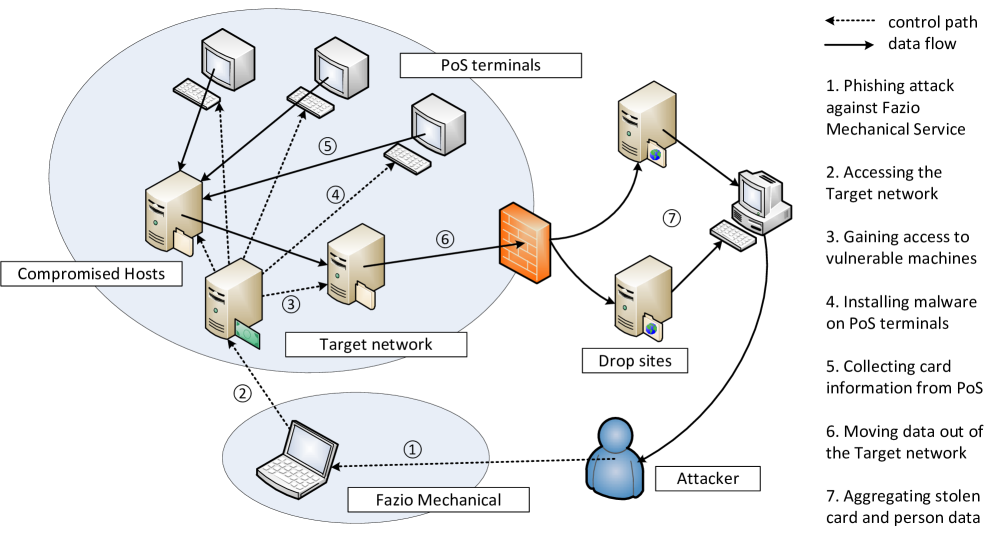

There are multiple theories on how the criminals initially hacked into Target, and none of them have yet been confirmed by Target Corporation. However, the primary and most well-supported theory is that the initial breach didn’t actually occur inside Target [10]. Instead, it occurred in a third party vendor, Fazio Mechanical Services, which is a heating, ventilation, and air-conditioning firm.

According to this theory, we present the timeline of the incident in Fig. 1 and steps of the plot in Fig. 2. Attackers first penetrated into the Target network with compromised credentials from Fazio Mechanical. Then they probed the Target network and pinpointed weak points to exploit. Some vulnerabilities were used to gain access to the sensitive data, and others were used to build the bridge transferring data out of Target. Due to the weak segmentation between non-sensitive and sensitive networks inside Target, the attackers accessed the point of sale networks.

2.1.1 Phase I: Initial Infection

At some point the Fazio Mechanical Services system was compromised by what is believed to be a Citadel Trojan [11]. This Trojan was initially installed through a phishing attempt. Due to the poor security training and security system of the third party, the Trojan gave the attackers full range of power over the company’s system [10]. It is not known if Fazio Mechanical Services was targeted, or if it was part of a larger phishing attack to which it just happened to fall victim. But it is certain that Fazio Mechanical had access to Target’s Ariba external billing system, or the business section of Target network.

2.1.2 Phase II: PoS Infection

Due to Target’s poor segmentation of its network, all that the attackers needed in order to gain access into Target’s entire system was to access its business section. From there, they gained access to other parts of the Target network, including parts of the network that contained sensitive data. Once they gained access into Target’s network they started to test installing malware onto the point of sales devices. The attackers used a form of point of sales malware called BlackPOS, which is further discussed in Section 3.

2.1.3 Phase III: Data collection

Once BlackPOS was installed, updated and tested. The malware started to scan the memory of the point of sales to read the track information, especially card numbers, of the cards that are scanned by the card readers connected to the point of sales devices.

2.1.4 Phase IV: Data exfiltration

The card numbers were then encrypted and moved from the point of sales devices to internal repositories, which were compromised machines. During the breach the attackers took over three FTP servers on Target’s internal network and carefully chose backdoor user name “Best1_user” with password “BackupU$r”, which are normally created by IT management software Performance Assurance for Microsoft Servers. During peak times of the day, the malware on the point of sale devices would send credit card information in bulk to the closest FTP Server [12]. The stolen card information is then relayed to other compromised machines and finally pushed to drop sites in Miami and Brazil [13].

2.1.5 Phase V: Monetization

Sources indicate the stolen credit card information was aggregated at a server in Russia, and the attackers collected 11 GB data during November and December 2013. The credit cards from the Target breach were identified on black market forums for sell [14]. At this point, it is unclear how these sellers, e.g., Rescator (nick name), is connected with the stolen card and personal information. In Section 4.3, we describe the well studied case of TJX credit card breach. It hints possible paths of peddling stolen credit cards in the black market.

2.2 Targets Security

Target did not run their systems and networks without security measures. They had firewalls in place and they attempted to segment their network using Virtual local area networks (VLAN) [7]. Target also deployed FireEye, a well-known network security system, six months prior to the breach. FireEye provides multiple levels of security from malware detection to network intrusion detection system (NIDS).

However, the breach demonstrates that sensitive data in Target, e.g., credit card information and personal records, is far from secure. Target failed at detecting or preventing the breach at several points, among which we list the four most vital ones:

-

•

Target did not investigate into the security warnings generated by multiple security tools, e.g., FireEye, Symantec, and certain malware auto-removal functionalities were turned off [15].

-

•

Target did not take correct methods to segment their systems, failing to isolate their sensitive network assets from easily accessed network sections. The VLAN technique used for segmentation is reported easy to get around [16].

-

•

Target did not harden their point of sale terminals, allowing unauthorized software installation and configuration. The settings resulted in the spread of malware and sensitive card information read from point of sale terminals.

-

•

Target did not apply proper access control on verities of accounts and groups, especially the ones from third party partners [17]. The failure resulted in the initial break-in from the HVAC company Fazio Mechanical Services Inc.

2.3 After the Breach

The former CEO of the company, Gregg Steinhafel, resigned after the breach. Target appointed a new chief information officer Bob DeRodes and provided details on enhancing their security with 100 million dollars [18]. The plan includes upgrading insecure point of sale machines and deploying chip-and-PIN-enabled technology for payment. Defenses such as better segmentation of the network, comprehensive log analysis and stricter access control are also mentioned in the plan.

3 BlackPOS

BlackPOS, seen on underground forums since February 2013 [19], is believed to be the major malware used in the data breaches at Target (2013), P.F. Chang’s (2013), and Home Depot (2014). The malware is a form of memory scrapper that takes a chunk of a systems memory and looks for credit card numbers. We describe the functionalities of BlackPOS captured in the Target breach, discuss its design features for circumventing detection techniques, and present the investigations of POS malware development and marketing.

3.1 Components and Functionalities of BlackPOS

Belonging to the BlackPOS family, the malware discovered in the Target breach is designed to infect Windows-based POS machines. The functionality of BlacksPOS is not complicated and we present its components in Fig. 3.

When a POS terminal is infected, the malware registers itself as a Windows service named “POSWDS”. The service automatically starts with the operating system, then i) it scans a list of processes which could interact with the card reader, and ii) it communicates with a compromised server (internal network repository) to upload retrieved credit card information. Predefined rules apply for matching the sensitive processes, as well as checking the time before sending obtained credit card numbers. Only during the busy office hours in the daytime, the repository aggregation function could be enabled and the card information is sent to the internal repository.

Memory of target processes are read and analyzed in chunks, each of which is 10,000,000 bytes. BlackPOS uses a custom logic to search credit card numbers in the memory trunks. It is believed that this method is more efficient and incurs less overhead than generally used regular expressions [20]. Retrieved credit card information are encrypted and stored in file “C:\WINDOWS\system 32\winxml.dll” and then periodically uploaded to the internal repository via NetBIOS and SMB protocols.

3.2 Design Features for Evading Detections

BlackPOS evolves quickly during the past few years. The earliest versions of it are discovered by McAfee in November 2011 as PWS-FBOI and BackDoor-FBPP. They only contain the bare-bone logic for retrieving and leaking sensitive information from individual machines [21]. However, the modern versions – known to be used in the Target breach (2013) and the Neiman Marcus breach (2013) – are heavily customized for specific internal networks and perform sophisticated behaviors to hide themselves from common detection mechanisms. We detail multiple observed behaviors of BlackPOS in the Target breach to illustrate how it is designed to circumvent detections.

-

•

Multi-phase data exfiltration. Infected POS terminals do not send sensitive data to the external network directly. Instead, they gather data to a compromised internal server, which is used as a repository and one of the relies to reach the external network [22]. The multi-phase data exfiltration scheme minimizes anomalous data flows across network boundaries.

-

•

String obfuscation. Critical strings in the malware executables are obfuscated to evade signature-based anti-virus detection [21]. The strings include critical process names for scanning and NetBIOS commands for uploading data to the internal repository.

-

•

Self-destructive code. The malware avoids unnecessary infections to minimize its exposure. It destroys/deletes itself if the infected environment is not within its targets [23]. This behavior reduces the risk of being detected in an unfamiliar environment.

-

•

Data encryption. The retrieved credit card information is encrypted in the file “Winxml.dll” in each POS terminal before it is sent to the internal repository. The encryption guarantees that no credit card numbers are sent in plaintext, which hides the leak from traditional data loss prevention (DLP) systems.

-

•

Constrained communication. Communications in the internal network are programed during office hours of the day [20]. Busy office hour traffic helps hide anomalous communications between infected POS terminals and the compromised internal repository.

-

•

Customized attack vector. Internal IP addresses and login credentials of compromised servers are hardcoded in the malware. It indicates the malware author is aware of the internal network. The countermeasures against detections are deliberately designed along with the data exfiltration process.

3.3 Malware Development and Marketing

The Target breach attracts considerable attention to BlackPOS and similar POS malware, e.g., vSkimmer [24] and Dexter [25]. Several investigations have been performed to disclose the development and marketing of these pieces of malware. Terrogence web intelligence company tracked the sales of the malware on underground markets and pointed out BlackPOS was first posted for sale in February 2013 [19]. Cybercrime intelligence firm IntelCrawler indicated Rinat Shibaev, a 17-year-old boy, and Rinat Shabayev, a 23-year-old Russian man, are the principle developers of BlackPOS [26]. Andrew Komarov, CEO of the company, also hinted that 6 more retailer breaches are linked to BlackPOS [27]. iSIGHT Partners, working with United States Secret Service, investigated the POS malware market and concluded a growing demand for such malware since 2010. FBI tracked about 20 data breach attacks in recent years and warned retailers about this increasing threat [28].

4 Prosecution of Data Breaches

The Target data breach is still under investigation and there is no arrest known to the public. Tracking down data breach perpetrators is notoriously difficult, because the criminals usually operate across the world to set barriers for investigation and prosecution in terms of various laws and complex treaties among countries. In this section, we discuss i) the laws that apply to cybercrimes, especially data breaches, ii) the difficulties in data breach discovery and prosecution, and iii) a precedent of investigation and sentence in the TJX breach case happened in 2007.

4.1 Cybercrime Law and Regulations

The federal Computer Fraud and Abuse Act (CFAA) is the most applicable cybercrime law that applies to the Target breach itself. Other laws against theft and misuse of the wires apply, as well as specific laws prohibiting the sale of credit cards and identity theft [29]. Under the CFAA, unauthorized access to a computer engaged in interstate commerce, which causes damage over $5,000, is a crime punishable by 5 to 10 years in prison and up to $250,000 damages, per offense. Subsequent violations increase the potential penalty, and there are different provisions and penalties for unauthorized access to government or financial computers. The Federal Bureau of Investigation leads investigations and cases are prosecuted by the Department of Justice Computer Crimes and Intellectual Property Division.

4.2 Barriers to Data Breach Investigation

Businesses, for a long time, declined to publically disclose a data breach in fear that the information would hurt their reputation in the eyes of customers and investors would. Today, 47 states have data breach notification laws. Although not uniform, these laws generally require a business to report a data breach to affected customers when personally identifiable information has been lost. The requirement to report a data breach can aid law enforcement in tracking down the criminals, and arguably is an incentive for businesses to increase their security.

In data breach plots, attackers usually hide their identities carefully using relays across the world in both the penetration phase (hacking into the system) and the exfiltration phase (leaking the data out). The international relays pose significant challenges for investigation and prosecution. In the Target breach case, two drop sites are found in Miami and Brazil, and the final aggregation server where all data is sent is discovered in Russia. There is no guarantee that all involved countries take the same level of effort as the United States to help investigate the incident. Each country is affected differently by the breach, let alone the complicated relations mixed with cooperation and divergences among them.

In addition, if cyber criminals are from outside the United States then an arrest requires extradition from the foreign country. In order to extradite for prosecution, the United States and the country must be signatories to a treaty agreeing to such cooperation. Many countries in Asia, Africa and the Middle East do not have treaties with the United States. Even with a treaty, extradition involves a complicated process.

4.3 TJX Breach and the Sentence

Before the Target data breach, 45.6 million credit card numbers and PINs were stolen in the TJX data breach [30]. The breach was fully investigated and the criminals were prosecuted and sentenced. The case sets a record for credit card breach as well as the stiffest sentence for a cybercrime. We describe details of the investigation from both technical and legal aspects.

Albert Gonzalez, an American hacker, plotted the TJX data breach from July 2005 to January 2007. In addition to the TJX case, he was also charged with data breaches in BJ’s Wholesale Club, Boston Market, Barnes & Noble, Sports Authority, Forever 21, DSW and OfficeMax [31].

All aforementioned data breaches done by Gonzalez were carried out with similar schemes. Taking the TJX case as an example, Gonzalez started with war-driving along Route No. 1 in Miami to discover vulnerable retailer’s hotspots. With the help of his accomplices – especially Stephen Watt, the author of the sniffer used in the data breaches – Gonzalez employed delicate SQL injections to gain access to the database and to install the sniffer software into the servers. Credit cards information was sniffed using ARP spoofing techniques and was uploaded onto two foreign servers leased by Gonzalez in Latvia and Ukraine.

After obtaining the credit card information, Gonzalez sold the credit card numbers and PINs to a Ukrainian card seller Maksym Yastremskiy. Yastremskiy paid Gonzalez totaling $400,000 through 20 electronic funds transfers via e-gold during 2006 [32]. He peddled the stolen credit card information to other card sellers in the underground market. In 2007, Yastremskiy was arrested on a separate charge, i.e., hacking into 12 banks in Turkey.

In May 2008, Gonzalez was apprehended with $1.1 million cash, a 2006 BMW, a diamond and other assets. He schemed to earn $15 million from a series of data breaches, according to his chat logs found by the government. He worked as an informant for the U.S. Secret Service before he was arrested.

Gonzalez was sentenced on March 25th and 26th, 2010 for the TJX case and the Heartland Payment Systems case, respectively. U.S. District Judge Patti Saris sentenced Gonzalez to 20 years in prison, and U.S. District Court Judge Douglas P. Woodlock sentenced Gonzalez to 20 years for the Heartland Payment Systems case. According to the negotiation between Gonzalez and the government, the sentences run concurrently [33] and Gonzalez would be imprisoned for a total of 20 years, which has reached record high on cybercrime [34].

5 Lessons Learned Toward Better and More Effective Security Solutions

As we discussed in Section 2.2, there are several mistakes made by Target in the incident, including i) ignoring critical security alerts, ii) improper segmentation of its network and iii) insecure point of sale data handling. In this section, we analyze these three points in details and propose better design and more effective practices for developing and deploying security solutions.

5.1 Enforcing Payment System Integrity

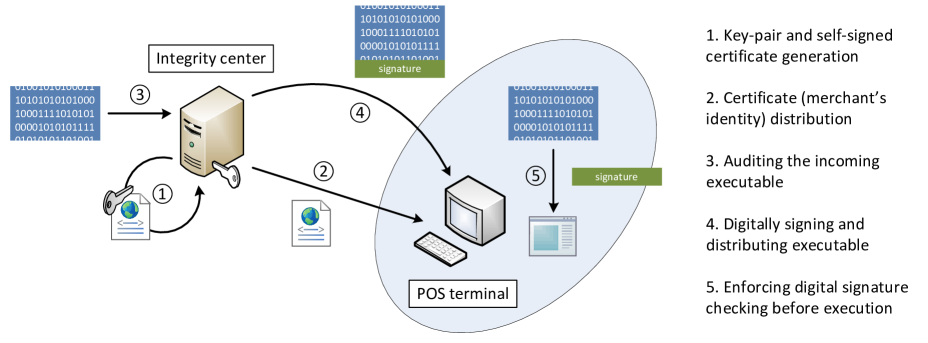

In the Target breach, BlackPOS was installed on Target’s point of sale terminals, and the integrity of POS systems was compromised. This key step for data breach can be prevented by enforcing the integrity of point of sale terminals. Therefore, we provide a practical scheme using digital signatures and certificates for ensuring the integrity of operating systems on point of sales.

The workflow of our POS integrity scheme is shown in Fig. 4. Our key idea is to allow only trusted executables running on POS machines. An executable is trusted if it is verified/audited and digitally signed by the merchant, i.e., Target Corp.

Executable verification techniques such as digital signature for executables are known for a long time, and many modern operating systems provide utilities toward the goal, e.g., Microsoft Authenticode [35]. However, the execution policy is usually difficult to be enforced on a normal consumer’s computer because there are a variety of software providers on the Internet. Users may install software or run programs from providers whose identify cannot be verified. Public key infrastructure (PKI) helps relieve the issue, but it does not completely solve it due to the complexity introduced by the variety of software providers.

However, this approach is useful and practical in the dedicated environment where i) POS terminals are specifically used for processing transaction and ii) they are possessed and controlled by the merchant, e.g., Target Corp. The first property ensures the software or programs running on POS terminals are limited and feasible to be audited. The second property guarantees one centralized integrity center auditing and signing all executables can be created.

There are two players, integrity center and POS terminal and 5 steps in our integrity enforcement scheme. The integrity center has four tasks: i) key generation, ii) key distribution, iii) file auditing and iv) file signing. The POS terminal is hardened by a policy that only binaries signed by the merchant can execute. The five-step-protocol is:

-

1.

The integrity center generates a public-private key pair and creates a self-signed certificate Cert containing .

-

2.

The integrity center distributes Cert to every POS terminal in the company. Cert is placed in the root certificate list at each terminal.

-

3.

The integrity center audits every binary that needs to be executed on POS, e.g., programs, installers, system patches, etc. and signs the binary with (encrypting the hash of the binary with ).

-

4.

The signed binary is sent over the merchant network to POS terminals.

-

5.

The POS terminal checks the binary signature using in Cert (encrypting the signature with to verify whether it is the hash of the binary) and executes only the ones correctly signed with .

Adopting our payment system integrity enforcement protocol, merchants can achieve the following two security goals in their system.

-

•

system integrity: only trusted programs are allowed to be executed or installed on the payment system, which excludes the possibility of malware infection on point of sale devices.

-

•

program authenticity: every program or piece of software should pass the test at integrity center before it is executed on point of sale machines, which allows merchants to have the full control of the payment system functionalities.

5.2 Developing Effective Security Alert Systems

Target had been warned multiple times by a malware detection tool produced by FireEye Inc [36, 37]. Unfortunately, the monitoring team in Bangalore for Target Corp. took no actions in response to these alerts. They also turned off the functionality that can automatically remove a detected malware. These two serious mistakes hindered the detection of the leakage of millions of credit card information. For large corporations, processing a large number of security alerts produced by protection systems is challenging, if possible at all. Many of these alerts are usually false alarms, which seasoned security analysts learn to safely ignore. In this subsection, we first discuss the design of FireEye alerts, and then explore new out-of-box design strategies to improve the effectiveness of alerts.

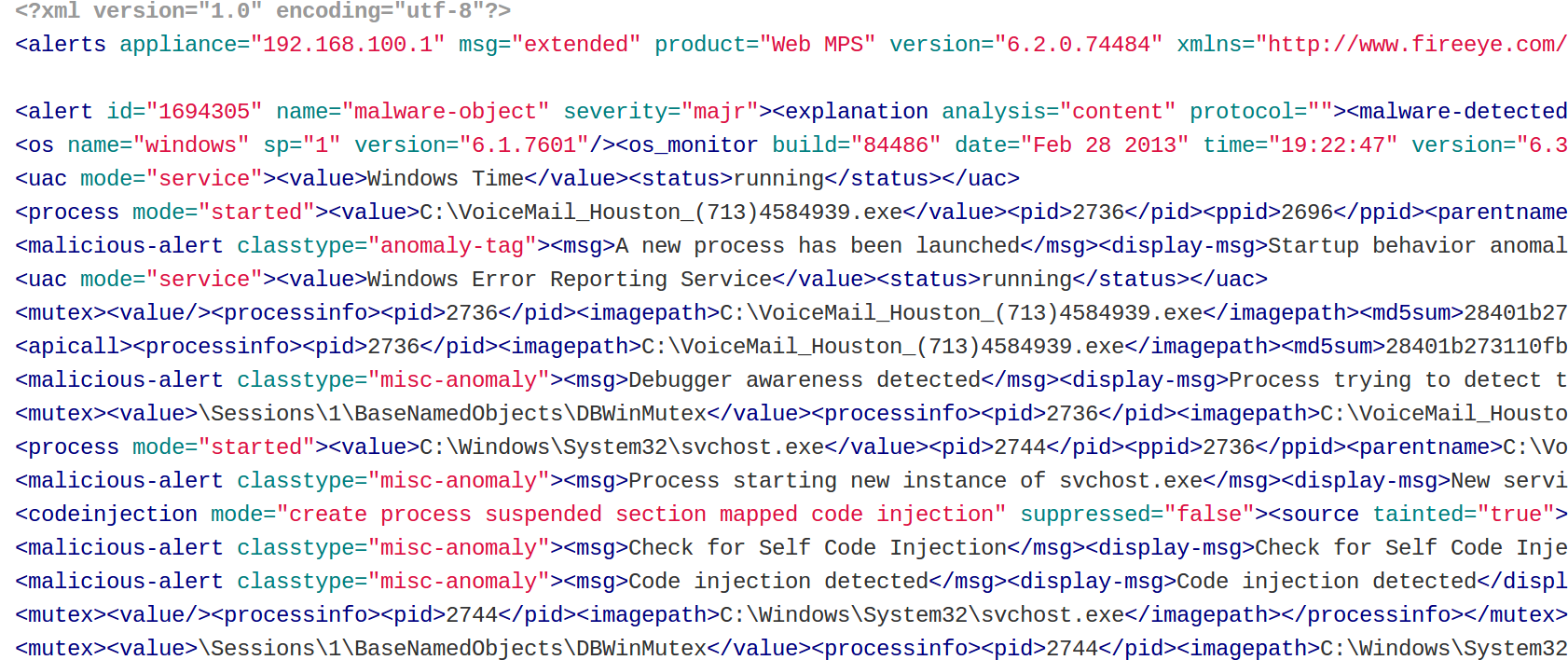

5.2.1 FireEye Alerts

The raw data output from FireEye Threat Prevention Platform is in XML structure. Fig. 5 shows a FireEye alert of a piece of malware [38]. Basic information about the malware is provided, such as type and severity. Anomalous behaviors of the malware are tracked and listed in malicious-alert. The classtype=“anomaly-tag” indicates that this alert is triggered because of anomaly behavior detected. The and briefly describe the content of this alert.

In the Target case, FireEye alerted the administrators with type “malware”, which is commonly seen in large companies or organizations. However, no sufficient detailed information was provided, e.g., the name of the malware or the data exfiltration behavior of the malware. Since the BlackPOS software, which extracts and steals sensitive financial information, is regarded as a zero-day malware and few administrators have experience dealing with it, the alerts were ignored [37].

5.2.2 Security Alert Design

Security alert systems are at the front line of cyber defense. They represent the first opportunity to detect, prevent, and stop attacks. Because human analysts are error-prone and tend be undertrained, making alert systems more usable and intelligent is critical.

The needs for designing effective security warnings have been studied. Sunshine et al. studied the effectiveness of SSL warning [39]. Akhawe and Felt investigated the browser warnings including malware, phishing and SSL warnings [40]. Modic and Anderson proposed to adopt social-psychological techniques to increase the compliment for the warnings [41].

Our thesis advocated in this paper on warnings differs from the existing security alert research. We consider the security protection needs for large companies and corporations that produce hundreds of alerts on daily basis. In these scenarios, the alert systems need to handle and differentiate warnings with a varying degrees of urgency.

We argue that the design of alert systems needs to be adaptive and intelligent, beyond simply sending a list of alerts. Specifically, we propose two design strategies for security alerts:

-

•

Adaptive warning strength. Existing security systems provide severity information along with each alert, but there is no guarantee that important alerts are not ignored by administrators. Thus, we propose two methods to strengthen the efficiency of alerts:

-

–

Raise the severity level of an alert when it is not handled within a limited amount of time. The purpose is to force security analysts to take actions toward severe alerts. This method is not applicable to all alerts, especially the less severe ones. Otherwise, it requires the administrators to address all alerts in the end, which may not be practical.

-

–

Besides color, font size, length of the alert bar, the system can raise alerts in different forms. For example, popping up flashing messages for the most critical alerts, emailing different level of alerts to different group of people.

The multiform alarming method utilizes different ways to interact with different people. It also informs people who are not directly in charge of the issue to remind security analysts if issues are not solved for a long time.

-

–

-

•

Mining and presenting connections among alerts. One drawback of existing detection solution is the lack of ability to correlate alert events. Some alert events could belong to a single attack vector and happen in sequence. Sophisticated modern attacks are usually well planned and realized in steps. An alert may be triggered for each step, e.g., malware injected, file transmission. Connecting these alerts can reveal a grander scheme of the plot.

One approach to connect alerts is to analyze the consequences of each malicious event. The consequences can be used to bridge alerts, connecting multiple alerts in different types to a plot. If the collection alerts indicate potential grander data breach, then sever alerts should be raised.

5.3 Controlling Information Flow with Network Segmentation

Target failed to segment its sensitive assets from normal network portions, which allows an attacker to escalate the intrusion if he/she attacks from the inside. We explain the severity of this issue.

The most common strategies used in network architecture are techniques based on building a strong exterior, so that only those a system can trust can get inside. Because the only people inside are those who can be trusted, security on the internal network is either low or none existent. An example of this goes back to the Target breach. Once the attacker obtained the security credentials from Fazio Mechanical Services, they then had the ability to gain access into Target’s network. From there they compromised three FTP servers and installed malware on many point of sales devices [7].

The security principle advocated in a zero trust network [16] is simply don’t trust anyone. This means all traffic is identified, authorized, and monitored. This makes all parts of the network secure regardless of location. In addition, virtual LANs cannot provide much security defense, because they cannot stop an intruder from gaining access into other portions of the network. The Target incidence demonstrates that virtual LANs, especially when not configured properly, is ineffective against the criminals.

While the zero trust strategy protects from outsider attacks it also protects against insider attacks because all traffic is monitored and analyzed. If a member of a network does something unusual, e.g. deletes several entries in a database that he or she usually does not access, the network administrators can detect the change in behaviors. However, this strategy has the trade-off for usability because monitoring all traffic leads to extremely huge computation power. And it is not convenient for practical usage in large scale networks.

6 Credit Card Security and Best Practices for customers

Target and other breach incidents, e.g., Neiman Marcus, Sally’s Beauty and PF Chang’s, suggests that there is a high risk at current credit card regulation and technology. In this section, we discuss the issues in credit card regulation as well as advantages and problems of new technologies for securing credit card transactions.

6.1 Credit Card Administration and Regulation

Payment card security is self-regulated by the contract between the merchant and the card company. Major credit card companies require compliance with the Payment Card Industry Data Security Standard (PCI-DSS) [42]. The description of Target’s security, such as weak password at the POS, would not seem to meet many of the standards, thus drawing attention to whether the private contract self-regulation framework is effective.

6.2 EMV: Toward a More Secure Payment System

EMV (Europay, MasterCard, and Visa) payment system is the major technology developed to address the security issue in credit cards [43]. The EMV system adds a temper-resistant chip to a credit card. The chip stores confidential account information and provides on-chip cryptographic computations such as encryption and digital signing. The system works by authenticating through the chip and identifying the user by either a signature or a pin; this is where the system gets its name of chip and pin. The difference between the EMV system and the traditional magnetic strip system is that the data on the card’s chip is encrypted. Therefore it would be much more difficult for an attacker to commit fraud.

However, a flaw is found in the design of the transaction protocol, which makes EMV ineffective. A no-pin attack is the scenario where the criminal has the card but not the pin. Murdech et al. show that by using an electric device between the card and the terminal, the terminal can be tricked into believing that the criminal has the correct pin even though he doesn’t [44].

Another vulnerability is found in Point of Sale terminals. A POS terminal in the EMV system is assumed temper-resistant, meaning that no one can open the POS box and read/write to the internal circuits. Unfortunately, real EMV-equipped POS terminals can be tempered and authentication codes can be obtained and used at a later time on the same terminal to make additional transactions. Several criminals in Spain made use of this vulnerability as well as a vulnerability found in ATM random number generators. An ATM may generate predictable random numbers which gives criminals temporary access to credit card spending if the number is guessed correctly.

Besides the two vulnerabilities, the most severe flaw in the EMV system is the card not present (such as when a purchase is made online) fraud abbreviated as CNP fraud. CNP fraud now accounts for over fifty percent of fraud in the United Kingdom where the EMV system is currently being used [45]. The EMV system is designed for securing card-present transactions, and it has nothing in place to prevent CNP fraud from occurring, which is why criminals are now using CNP fraud as their go to choice in fraudulent purchases.

6.3 Tokenization and Best Practices for Customers

Tokenization is a payment technology to minimize credit card information by merchants during transactions. In this section, we describe the technology and explain why it helps protect personal account information. We give customers best practices to hide their credit card information when shopping.

With tokenization a customer asks an acquirer to act between he/she and the merchant. The acquirer i) takes the customer’s credit card information , ii) generates a one-time token based on ( is independent of ), and iii) sends to the merchant to process the transaction. is bound to the merchant and can be nullified after the transaction.

There are two approaches to utilize an acquirer. One is to pay through acquirer systems. Available systems include PayPal, Amazon payment, Google wallet and Apple pay. For example, customer Alice wants to buy an item in Amazon market from seller Bob. Alice can pay through the Amazon payment system and Bob only receives a token to process the transaction. Google wallet and Apple pay extend the service from online shopping to in-store purchases. They also provide contactless feature through near field communication (NFC), so that Alice does not need to swipe a card to authorize a purchase.

The second approach to utilize an acquirer is to generate a one-time credit card number at acquirer banks. Bank of America and Citibank provide such service, namely ShopSafe and virtual card number, respectively. PayPal used to have a similar service and Discover terminated its virtual card service on March 16, 2014.

7 Conclusion

There is no silver bullet in cyber space against data breaches. With the increasing amount of data leak incidents in recent years, it is important to analyze the weak points in our systems, techniques and legislations and to seek solutions to the issue. In this paper, we presented a comprehensive analysis of the Target data breach and related incidents, such as the TJX breach. We described several security guidelines to enhance security in merchants’ systems. We presented the state-of-the-art credit card security techniques, and gave customers best practices to hide card information during purchase transactions.

Acknowledgments

This work has been supported in part by NSF grant CAREER CNS-0953638 and ARO grant YIP W911NF-14-1-0535.

References

- [1] “ITRC breach report,” http://www.idtheftcenter.org/images/breach/ITRC_Breach_Report_2014.pdf.

- [2] I. Hoppe, “The Home Depot data breach: a map of affected ZIP codes in Alabama,” September 2014.

- [3] B. Krebs, “Sally Beauty confirms card data breach,” March 2014.

- [4] E. A. Harris, N. Perlroth, and N. Popper, “Neiman Marcus data breach worse than first said,” January 2014.

- [5] B. Krebs, “3 million customer credit, debit cards stolen in Michaels, Aaron Brothers breaches,” April 2014.

- [6] “Updated statement from Rick Federico CEO of P.F. Chang’s,” August 2014.

- [7] B. Krebs, “A first look at the Target intrusion, malware,” January 2014.

- [8] M. Riley, “Fighting cyberthreats with FireEye,” May 2014.

- [9] B. Krebs, “The Target breach, by the numbers,” May 2014.

- [10] M. J. Schwartz, “Target ignored data breach alarms,” March 2014.

- [11] ——, “Target breach: Phishing attack implicated,” February 2014.

- [12] M. Oh, “Hacking POS terminal for fun and non-profit,” July 2014.

- [13] K. Jarvis and J. Milletary, “Inside a targeted point-of-sale data breach,” January 2014.

- [14] B. Krebs, “Who’s selling credit cards from Target?” December 2013.

- [15] D. Chiacu, “Target missed many warning signs leading to breach: U.S. Senate report,” March 2014.

- [16] Forrester Research, “Developing a framework to improve critical infrastructure cybersecurity,” NIST, April 2013, in Response to: RFI# 130208119-3119-01.

- [17] B. Krebs, “Email attack on vendor set up breach at Target,” February 2013.

- [18] “Target appoints new chief information officer, outlines updates on security enhancements,” April 2014.

- [19] A. Keren, “Cyber criminals ’TARGET’ Point of Sale devices,” January 2014.

- [20] M. Oh, “An evolution of BlackPOS malware,” January 2014.

- [21] McAfee Labs, “EPOS data theft,” McAfee Labs Threat Advisory, January 2014.

- [22] B. Krebs, “New clues in the Target breach,” January 2014.

- [23] ——, “These guys battled BlackPOS at a retailer,” February 2014.

- [24] C. Shah, “VSkimmer botnet targets credit card payment terminals,” McAfee blog center, March 2013.

- [25] A. Raff, “Dexter – draining blood out of Point of Sales,” seculert research lab, December 2012.

- [26] IntelCrawler, “The teenager is the author of BlackPOS/Kaptoxa malware (Target), several other breaches may be revealed soon,” January 2014.

- [27] T. Kitten, “6 more retailers breached?” January 2014.

- [28] FBI Cyber Division, “Recent cyber intrusion events directed toward retail firms,” January 2014.

- [29] C. Doyle, “Cybercrime: an overview of the federal computer fraud and abuse statute and related federal criminal laws,” http://fas.org/sgp/crs/misc/97-1025.pdf.

- [30] J. Vijayan, “TJX data breach: At 45.6m card numbers, it’s the biggest ever,” March 2007.

- [31] K. Poulsen, “Feds charge 11 in breaches at TJ Maxx, OfficeMax, DSW, others,” May 2008.

- [32] “The indictment: The U.S. v. Albert Gonzalez, 08-CR-10223, case,” August 2008, http://www.yalelawtech.org/wp-content/uploads/usvgonzalez.pdf.

- [33] “United States district court district of Massachusetts government’s sentencing memorandum,” http://www.wired.com/images_blogs/threatlevel/2010/03/gonzalez_gov_sent_memo.pdf.

- [34] K. Zetter, “TJX hacker gets 20 years in prison,” March 2010.

- [35] Microsoft Authenticode technology, http://msdn.microsoft.com/en-us/library/ie/ms537364.aspx.

- [36] M. Riley, B. Elgin, D. Lawrence, and C. Matlack, “Missed alarms and 40 million stolen credit card numbers: How Target blew it,” March 2014.

- [37] J. Finkle and S. Heavey, “Target says it declined to act on early alert of cyber breach,” March 2014.

- [38] FireEye alert examples https://github.com/warewolf/fireeye/blob/master/Alert_Details_example.com_20131025_181223.xml.

- [39] J. Sunshine, S. Egelman, H. Almuhimedi, N. Atri, and L. F. Cranor, “Crying wolf: An empirical study of SSL warning effectiveness.” in USENIX Security Symposium, 2009, pp. 399–416.

- [40] D. Akhawe and A. P. Felt, “Alice in warningland: A large-scale field study of browser security warning effectiveness,” in USENIX Security Symposium, 2013.

- [41] D. Modic and R. J. Anderson, “Reading this may harm your computer: The psychology of malware warnings,” 2014.

- [42] Payment card industry payment application data security standard, https://www.pcisecuritystandards.org/documents/PA-DSS_v3.pdf.

- [43] R. Anderson and S. J. Murdoch, “EMV: why payment systems fail,” Communications of the ACM, vol. 57, no. 6, pp. 24–28, 2014.

- [44] S. J. Murdoch, S. Drimer, R. J. Anderson, and M. Bond, “Chip and PIN is broken,” in 31st IEEE Symposium on Security and Privacy, S&P 2010, 16-19 May 2010, Berleley/Oakland, California, USA, 2010, pp. 433–446.

- [45] “Challenges & opportunities for merchant acquirers,” 2012, Capgemini.