A Black–Scholes inequality: applications and generalisations

Abstract.

The space of call price functions has a natural noncommutative semigroup structure with an involution. A basic example is the Black–Scholes call price surface, from which an interesting inequality for Black–Scholes implied volatility is derived. The binary operation is compatible with the convex order, and therefore a one-parameter sub-semigroup gives rise to an arbitrage-free market model. It is shown that each such one-parameter semigroup corresponds to a unique log-concave probability density, providing a family of tractable call price surface parametrisations in the spirit of the Gatheral–Jacquier SVI surface. An explicit example is given to illustrate the idea. The key observation is an isomorphism linking an initial call price curve to the lift zonoid of the terminal price of the underlying asset.

1. Introduction

We define the Black–Scholes call price function by the formula

where is the standard normal density and is its distribution function. Recall the financial context of this definition: a market with a risk-free zero-coupon bond of unit face value, maturity and initial price ; a stock with initial price that pays no dividend; and a European call option written on the stock with maturity and strike price . In the Black–Scholes model, the initial price of the call option is given by the formula

where is the volatility of the stock price. In particular, the first argument of plays the role of the moneyness and the second argument plays the role of the total standard deviation of the terminal log stock price.

The starting point of this note is the following observation.

Theorem 1.0.1.

For and we have

with equality if and only if

While it is fairly straight-forward to prove Theorem 1.0.1 directly, the proof is omitted as it is a special case of Theorem 3.2.4 below. Indeed, the purpose of this note is to try to understand the fundamental principle that gives rise to such an inequality. As a hint of things to come, it is worth pointing out that the expression appearing on the left-hand side of the inequality corresponds to the sum of the standard deviations – not the sum of the variances. From this observation, it may not be surprising to see that a key idea underpinning Theorem 1.0.1 is that of adding comonotonic – not independent – normal random variables. These vague comments will be made precise in Theorem 2.3.3 below.

Before proceeding, we re-express Theorem 1.0.1 in terms of the Black–Scholes implied total standard deviation function, defined for to be the inverse function

such that

In particular, the quantity denotes the implied total standard deviation of an option of moneyness whose normalised price is . We will find it notationally convenient to set for . With this notation, we have the following interesting reformulation which requires no proof:

Corollary 1.0.2.

For all and for , we have

with equality if and only if

where for .

To add some context, we recall the following related bounds on the function and ; see [31, Theorem 3.1].

Theorem 1.0.3.

For all , , and we have

with equality if and only if

Equivalently, for all , and we have

where for .

In [31], Theorem 1.0.3 was used to derive upper bounds on the implied total standard deviation function by selecting various values of to insert into the inequality.

The function has appeared elsewhere in various contexts. For instance, it is the value function for a problem of maximising the probability of hitting a target considered by Kulldorff [27, Theorem 6]. (Also see the book of Karatzas[23, Section 2.6].) In insurance mathematics, the function is often called the Wang transform and was proposed in [33] as a method of distorting a probability distribution in order to introduce a risk premium. In a somewhat unrelated context, Kulik & Tymoshkevych [26] observed, while proving a certain log-Sobolev inequality, that the family of functions forms a semigroup under function composition. We will see that this semigroup property is the essential idea of our proof of Theorem 1.0.1 and its subsequent generalisations.

The rest of this note is arranged as follows. In section 2 we introduce a space of call price curves and explore some of its properties. In particular, we will see that it has a natural noncommutative semigroup structure with an involution. The binary operation has a natural financial interpretation as the maximum price of an option to swap the one asset for a fixed number of shares of a second asset. In section 3, we introduce a space of call price surfaces and provide in Theorem 3.1.2 equivalent characterisations in terms of either one supermartingale or two martingales. Furthermore, it is shown that the binary operation is compatible with the decreasing convex order, and therefore a one-parameter semigroup of the space of call curves can be associated with an arbitrage-free market model. A main result of this article is Theorem 3.2.7: each one-parameter semigroup corresponds to a unique (up to translation and scaling) log-concave probability density, generalising the Black–Scholes call price surface and providing a family of reasonably tractable call surface parametrisations in the spirit of the SVI surface. In section 4, further properties of these call price surfaces, including the asymptotics of their implied volatility, are explored. In addition, an explicit example is given to illustrate the idea, and is calibrated to real world call price data. In section 5, the proof of Theorem 3.2.7 is given. The key observation is that the Legendre transform is an isomorphism converting the binary operation on call price curves to function composition. The isomorphism has the additional interpretation as the lift zonoid of the terminal price of the underlying asset.

2. The algebraic properties of call prices

2.1. The space of call price curves

For motivation, consider a market with two (non-dividend paying) assets whose prices at time are and . We assume that both prices are always non-negative and that the initial prices and are strictly positive. We further assume that there exists a martingale deflator , that is, a positive adapted process such that the processes and are both martingales. The assumption of the existence of a martingale deflator ensures that there is no arbitrage in the market. (Conversely, in discrete time, no arbitrage implies the existence a martingale deflator, even if the market does not admit a numéraire portfolio; see [32].)

Now introduce an option to swap one share of asset with shares of asset at a fixed time , so the payout is . If the asset is a risk-free zero-coupon bond of maturity and unit face value, then the option is a standard call option. It will prove useful in our discussion to let asset be arbitrary, but we shall still refer to this option as a call option.

There is no arbitrage in the augmented market if the time price of this call option is

In particular, setting

the initial price of this option, normalised by the initial price of asset can be written as

where the moneyness is given by

The above discussion motivates the following definition:

Definition 2.1.1.

A function is a call price curve iff there exist non-negative random variables and defined on some probability space such that

and

in which case the ordered pair of random variables is called a basic representation of . The set of all call price curves is denoted .

From a practical perspective, the normalised call price is directly observed, while the law of the pair is not. Therefore, a theme of this note is to try to express notions in terms of the call price curve. Here is a first result of this type.

Theorem 2.1.2.

Given a function , the following are equivalent:

-

(1)

.

-

(2)

There exists a non-negative random variable with such that

-

(3)

is convex and such that for all .

Furthermore, in case (2) we have that

and more generally that

where denotes the right-derivative of .

Proof.

The implications (1)(3) and (2)(3) are straightforward, so their proofs are omitted. Furthermore, the claim that the distribution of can be recovered from is essentially the Breeden & Litzenberger [3] formula.

(3)(2): By convexity, the right-derivative is defined everywhere and is non-decreasing and right-continuous. Furthermore, since for all we have for all . Let be a random variable such that . Note that

by Fubini’s theorem and the absolute continuity of the convex function .

It remains to show that either (2)(1) or (3)(1). That is, we must construct a basic representation from either the random variable or the function . We will give a construction showing (2)(1) in the proof of Theorem 2.3.2, and a rather different construction showing (3)(1) in the proof of Theorem 3.1.2. To avoid repetition, we omit a construction here. ∎

By definition, a call price curve is determined by two random variables and . However, the distribution of the pair cannot be inferred solely from . In contrast, Theorem 2.1.2 above says that a call price curve is also determined by a single random variable , and furthermore, the law of is unique and can be recovered from . This observation motivates the following definition.

Definition 2.1.3.

Given a call price curve , suppose that is a non-negative random variable such that for all . Then is called a primal representation of .

Remark 2.1.4.

As hinted by the name primal, we will shortly introduce a dual representation.

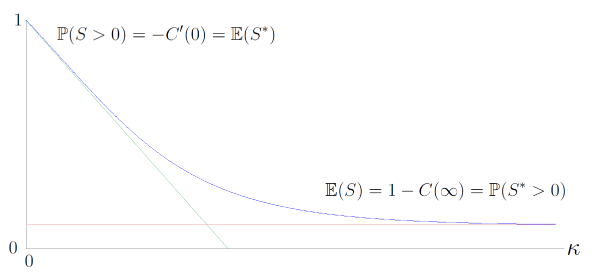

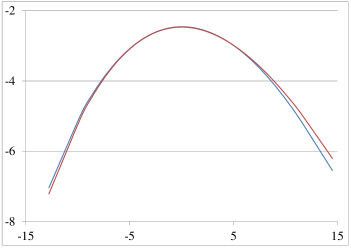

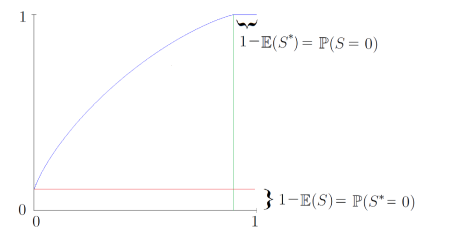

Figure 1 plots the graph of a typical element .

Remark 2.1.5.

An example of an element of is the Black–Scholes call price function for any . A primal representation is

where has the standard normal distribution.

Remark 2.1.6.

We note that there are alternative financial interpretations of call price curves in the case . One popularised by Cox & Hobson [10] is to model the primal representation as the terminal price of an asset experiencing a bubble in the sense that the price process discounted by the price of the risk-free -zero coupon bond is a strictly local martingale under a fixed -forward measure. For this interpretation, the option payout must be modified: rather than the payout of standard (naked) call option, in this interpretation the quantity models the normalised price of a fully collateralised (covered) call with payout

In my view, there are two related shortcomings of this interpretation. Firstly, this type of bubble phenomenon can only arise in continuous time models, since in discrete time non-negative local martingales are necessarily true martingales. Secondly, in the case where the underlying stock is not priced by expectation, it is not clear from a modelling perspective why the market should then price the call option by expectation Both shortcomings highlight the subtlety of continuous time arbitrage theory, in particular, the sensitive dependence on the choice of numéraire on the definition of arbitrage (and related arbitrage-like conditions).

2.2. The involution

There is a natural involution on the space of call prices:

Definition 2.2.1.

Given a call price curve with basic representation , the function is the call price curve with basic representation .

This leads to a straightforward financial interpretation of the involution. As described above, we may think of as the initial price, normalised by , of the option to swap one share of asset for shares of asset , where . Then is the initial price, normalised by , of the option to swap one share of asset for shares of asset , where .

We now record a fact about this involution ∗, expressed directly in terms of call prices. The proof is a straightforward verification, and hence omitted.

Theorem 2.2.2.

Fix . Then and

Remark 2.2.3.

As an example, notice for the Black–Scholes call function we have

by the classical put-call symmetry formula.

Remark 2.2.4.

The function is related to the well-known perspective function of the convex function defined by ; see, for instance, the book of Boyd & Vanderberghe [6, Section 3.2.6].

As hinted at above, we can define another random variable in terms of this involution:

Definition 2.2.5.

Given a call price curve , a non-negative random variable is a dual representation of iff is a primal representation of the call price curve .

That this dual random variable should be called a representation of a call price is due to the following observation. Again the proof is straightforward and hence omitted.

Theorem 2.2.6.

Given a call price with dual representation we have

In particular, we have

Finally, for all we have

2.3. The binary operation

We have introduced one algebraic operation, the involution ∗, to the set of call price curves. We now come to the second algebraic operation which will help to contextualise the Black–Scholes inequality of Theorem 1.0.1. To motivate it, consider a market with three assets with time prices and . We know the initial cost of an option to swap one share of asset with shares of asset , as well as the initial cost of an option to swap one share of asset with shares of asset , for various values of and , where all of the options mature at a fixed date . Our goal is the find an upper bound on the cost of an option to swap one share of asset for shares of asset , for the same maturity date .

Definition 2.3.1.

For call price curves , define a binary operation on by

where the supremum is taken over non-negative random variables defined on the same probability space such that is a basic representation of and is a basic representation of .

At this stage, it is not immediately clear that given two call price curves and one can find a triple satisfying the definition of the binary operation , and in principle, we should complete the definition with the usual convention that . Fortunately, this caveat is not necessary as can be deduced from the following result:

Theorem 2.3.2.

For call price curves we have

where the supremum is taken over random variables and defined on the same space, where is a primal representation of and is a dual representation of .

Proof.

First, let be a primal representation of and be a dual representation of , defined on the same probability space. We will exhibit random variables such that is a basic representation of and is a basic representation of .

For the construction, we introduce Bernoulli random variables , independent of and each other, with

If then set

and if almost surely, set and . Similarly, if then set

and if almost surely, set and . Finally set

It is easy to check that the triplet is the desired representation. This shows

For the reverse inequality, given a basic representation of and a basic representation of defined on the same probability space , we let

and an absolutely continuous measure by It is easy to check that is a primal representation of and is a dual representation of under and that

∎

Given the laws of two random variables and and a convex function , it is well-known that the quantity

is maximised when and are comonotonic. See, for instance, the paper of Kaas–Dhaene–Vyncke–Goovaerts– Denuit [22] for a proof. By rewriting the expression

we see that the supremum defining the binary operation is achieved when and are countermonotonic. We will recover this fact in the following result, which also continues our theme of expressing notions directly in terms of the call prices. In this case, the binary operation can be expressed via a minimisation problem:

Theorem 2.3.3.

Let be a primal representation of , and a dual representation of , where and are defined on the same probability space. Then

for all and , with convention . There is equality if the following hold true:

-

(1)

and are countermonotonic, and

-

(2)

and

In particular, we have

Proof.

Recall that for real we have

with equality if . Hence, fixing , we have

for all .

Now pick such that

and

Also assume that and are countermonotonic so that

and

Notice that in this case, we have

and hence there is equality in the inequality above. ∎

Remark 2.3.4.

This result is related to the upper bound on basket options found by Hobson, Laurence & Wang [20, Theorem 3.1].

Remark 2.3.5.

In light of the formula for the binary operation appearing in Theorem 2.3.3, the Black–Scholes inequality of Theorem 1.0.1 amounts to the claim that for we have

This is a special case of Theorem 3.2.4, stated and proven below.

We now come to the key observation of this note. To state it, we distinguish two particular elements defined by

Note that the random variables representing and are constant, with representing and representing . The following result shows that is a noncommutative semigroup with respect to with involution ∗, where is the identity element is the absorbing element. The proof is straightforward, and hence omitted.

Theorem 2.3.6.

For every we have

-

(1)

-

(2)

-

(3)

.

-

(4)

-

(5)

We conclude this section by introducing two useful subsets of the set of call price curves.

Definition 2.3.7.

Let

and

That is, fix a call price curve with primal representation and dual representation . The call price curve is in if and only if , while is in if and only if .

Remark 2.3.8.

As an example, notice that for the Black–Scholes call function we have

The subsets and are closed with respect to the binary operation.

Proposition 2.3.9.

Given we have

-

(1)

if and only if both and .

-

(2)

if and only if both and .

3. One-parameter semigroups, peacocks and lyrebirds

3.1. The space of call price surfaces

With the motivation at the beginning of section 2 we consider the family of prices of options when the maturity date is allowed to vary. We now introduce the following definition:

Definition 3.1.1.

A call price surface is a function such that there exists an pair of non-negative martingales such that

and

Our goal is to understand the structure the space of call price surfaces, and relate this structure to the binary operation introduced in the last section.

Theorem 3.1.2.

Given a function the following are equivalent:

-

(1)

is a call price surface

-

(2)

There exists a non-negative supermartingale such that and

-

(3)

There exists a non-negative supermartingale such that and

-

(4)

For all , there exist bounded non-negative martingales and such that and

and such that for all .

-

(5)

is non-decreasing with for all , and is convex for all .

Proof.

The implications () (5) for are easy to check by the conditional version of Jensen’s inequality.

The implications (5) (2) and (5) (3) are proven as follows. By Theorems 2.1.2 and 2.2.6 there exist families of random variables and such that

for all and . The assumption that is non-decreasing implies that both families of random variables (or more precisely, both families of laws) are non-decreasing in the decreasing-convex order. The implications then follow from Kellerer’ theorem [24].

Implication (4) (1) is obvious. So it remains to show the implication (5) (4). Fix and let

It is straightforward to verify that satisfies hypothesis (5). Hence there exists a non-negative supermartingale such that

But since for all we can conclude that for all we have both and a.s. In particular, is a true martingale so that

or equivalently

where as claimed. ∎

Remark 3.1.3.

The implication (5) (2) is well-known, especially in the case where for all where the supermartingale is a martingale. See, for instance, the paper of Carr & Madan [7]. However, implication (5) (4) seems new.

3.2. One-parameter semigroups

Returning to the topics of Section 2, we note that the operation interacts well with the natural partial ordering on the space of call price curves:

Proposition 3.2.1.

For any , we have

Proof.

Let be a primal representation of and a dual representation of . Suppose and are independent. Then by Theorem 2.3.2 we have

by first conditioning on and applying the conditional Jensen inequality, and then using the bound . The other implication is proven similarly. ∎

Combining Theorem 3.1.2 and Proposition 3.2.1, brings us to the main observation of this paper: if is a one-parameter sub-semigroup of then is a call price surface. Fortunately, we will see that all such sub-semigroups can be explicitly characterised and are reasonably tractable.

With the motivation of finding tractable family of call price surfaces, we now study the family of sub-semigroups of indexed by a single parameter . We change notation from to , since the will correspond to total implied standard deviation in the Black–Scholes framework, so . In particular, we will think of not literally as the maturity date of the option, but rather an increasing function of that date.

We will make use of the following notation. For a probability density function , let

for and . Note that

for , where is the standard normal density.

It will be useful to distinguish a special class of densities:

Definition 3.2.2.

A probability density function is log-concave iff is concave.

We will use repeatedly a useful characterisation of log-concave densities due to Bobkov [4, Proposition A.1]:

Proposition 3.2.3 (Bobkov).

Let be a probability density, with on the interval . Let be the corresponding cumulative distribution function, and its quantile function. The following are equivalent:

-

(1)

is log-concave.

-

(2)

is concave on for each .

-

(3)

is concave on .

Let be a log-concave density supported on where . Recall that log-concavity implies that is continuous on the open interval , but may have discontinuities at the end points. However, without any loss of generality, we will assume throughout that is continuous on .

We now present a family of one-parameter sub-semigroups of .

Theorem 3.2.4.

Let be a log-concave probability density function. Then

While Theorem 3.2.4 is not especially difficult to prove, we will offer two proofs with each highlighting a different perspective on the operation . The first is below and the second is in Section 5.

Proof.

Letting be a random variable with density , note that is a primal representation of . Note also that by log-concavity of , when the function is non-increasing. Similarly, is a dual representation of and is non-decreasing. In particular, the random variables and are countermonotonic, and hence by Theorem 2.3.3 we have

The conclusion follows from changing variables in the integral on the right-hand side. ∎

The upshot of Theorem 3.2.4 and Proposition 3.2.1 is that, given a log-concave density , the function is non-decreasing for each . Hence, given an increasing function , we can conclude from Theorem 3.1.2 that we can define a call price surface by

The above formula is reasonably tractable, and could be seen to be in the same spirit as the SVI parametrisation of the implied volatility surface given by Gatheral & Jacquier [14]. Note that we can recover the Black–Scholes model by setting the density to the standard normal density and the increasing function to where is the volatility of the stock. We provide another worked example in section 4.2.

At this point we explain the name of this section. We recall the definitions of terms popularised by Hirsh, Profeta, Roynette & Yor [18] and Ewald & Yor [12] among others:

Definition 3.2.5.

A lyrebird is a family of integrable random variables such that there exists a submartingale defined on some other probability space such that for all . A peacock is a family of random variables such that both and are lyrebirds; i.e. there exists a martingale with the same marginal laws as .

The term peacock is derived from the French acronym PCOC, Processus Croissant pour l’Ordre Convexe, and lyrebird is the name of an Australian bird with peacock-like tail feathers.

Combining Proposition 3.2.1 and Theorem 3.2.4 yields the following tractable family of lyrebirds and peacocks.

Theorem 3.2.6.

Let be a log-concave density, and let be a random variable have density and let be increasing. Set

The family of random variables is a lyrebird. If the support of is of the form , then is a peacock.

Note that the the semigroup does not correspond to a unique log-concave density. Indeed, fix a log-concave density and set

for , . Note that

However, we will see below that the semigroup does identify the density up to arbitrary scaling and centring parameters.

Also, note that by varying the scale parameter we can interpolate between two possibilities. On the one hand, we have for all and that

and on the other hand, when that

by the dominated convergence theorem.

Recall that the call price curve is the identity element for binary operation . Hence the family defined by for all is another example of a subsemigroup of .

Similarly, the call price curve is the absorbing element for . Hence, the family defined by and for all is yet another example of a subsemigroup of .

The following theorem says that the above examples exhaust the possibilities.

Theorem 3.2.7.

Suppose

and

Then exactly one of the following holds true:

-

(1)

for all ;

-

(2)

for all ;

-

(3)

for a log-concave density .

In case (3) the density is uniquely defined by the semigroup, up to centring and scaling.

The proof appears in Section 5.

Remark 3.2.8.

One could certainly consider other binary operations on the space which are also compatible with the partial order. For instance, we could let

where the primal representation of is independent of the dual representation of . Note that this binary operation is commutative, and indeed we have

where is a primal representation of , again independent of . In fact, the binary operation can be expressed (somewhat awkwardly) in terms of the call price curves and :

As described above, one could construct call price surfaces by studying one parameter semigroups for this binary operation . Indeed, such semigroups are easy to describe since their primal representations are essentially exponential Lévy processes. Unfortunately, the call prices given by an exponential Lévy process are not easy to write down in general. However, we have seen that the one-parameter semigroup of call prices for the binary operation are extremely simple to write down. It is the simplicity of these formulae that is the claim to practicality of the results presented here.

4. Calibrating the surface

4.1. An exploration of

We have argued that if is a log-concave density and is an increasing function, then the family is a call price surface as defined in Section 3.1, where the notation is defined in Section 3.2. The motivation of this section is to bring this observation from theory to practice. In particular, to calibrate the functions and to market data, it is useful to have at hand some properties, including asymptotic properties, of the function .

In what follows we will assume that the density has support of the form for some constants . Recall that we assume is continuous on . Now let be random variable with density . For each , define a non-negative random variable by

Note that is well-defined since almost surely, and hence almost surely. In this notation, we have for all that

so that by Theorem 2.1.2 we have and that is a primal representation of .

Note also that almost surely for while for we have

and

In particular, for we have

and

where the sets and are defined in Section 2.3.

By changing variables, we find that a dual representation of is given by

and therefore

It is interesting to observe that the call price surface satisfies the put-call symmetry formula if the density is an even function.

By implication (2) of Proposition 3.2.3 we have that for that the map is non-increasing. Let

with the convention that . Note that if and only if . With this notation, we have

where is the cumulative distribution corresponding to .

Remark 4.1.1.

The standard normal density is log- concave and we have the computation

yielding the usual Black–Scholes formula.

The first result may seem like a curiosity, but in fact is a useful alternative formula for computing numerically, given the density . In particular, the following formula does not require the evaluation of the function defined above. This is a generalisation of Theorem 3.1 of [31]. The proof is essentially the same, but included here for completeness. We will use the notation

Theorem 4.1.2.

For , we have

Proof.

Fix and let . Note that

Given , there is equality when . ∎

The next result gives an asymptotic expression for call prices at short maturities and close to the money. In what follows, we will use the notation

where is the right-derivative of . Recall that always exists on the interval .

Theorem 4.1.3.

As we have that

Proof.

Let be a maximum of so that for and for . We only consider the case , as the cases and are similar.

Fix and , and write

where

Note that for we have

so

by the dominated convergence theorem.

For the second term, note that by the continuity of at the point we have

as . In particular, we have

Finally, for the third term apply the put-call parity formula to get

again by the dominated convergence theorem. The conclusion follows from another application of put-call parity and recombining the integrals. ∎

There are two interesting consequences of Theorem 4.1.3 above. The first is that the density can be recovered from short time asymptotics. We will use the notation

for . The proof follows the same pattern as that of Theorem 4.1.2, so is omitted.

Theorem 4.1.4.

For all we have

Remark 4.1.5.

Given the function , we can recover , up to centring, as follows: Fix and set . Then we have

We note in passing that the call price function satisfies a non-linear partial differential equation featuring the function when is suitably well-behaved enough:

Proposition 4.1.6.

Let be a strictly log-concave density supported on all of . Suppose that is and such that

Then

on .

Proof.

By log-concavity, we have for all and that

and hence

Also, by the strict log-concavity of the map is strictly decreasing. This shows that is finite for all and that

By the differentiability of and the implicit function theorem, the function is differentiable on .

One checks that

and

The conclusion follows. ∎

We now comment on a second interesting consequence of Theorem 4.1.3. Note that for the limit for the Black–Scholes call function is

The function has an interesting financial interpretation. Recall that in the Bachelier model, assuming zero interest rates, the initial price of a call option of maturity and strike is given by

where is the initial price of the stock, and is its arithmetic volatility. Hence can be interpreted as a normalised call price function in the Bachelier model.

Following the motivation of this section, we are interested not only in the call price surface itself, but also in the corresponding implied volatility surface. Recall that the function is defined by

We will use the notation

Recall that if the normalised price of a call of moneyness and maturity is given by , then the option’s implied volatility is given by .

Remark 4.1.7.

A word of warning: We have noted that the function is the restriction of the function to . However, it is not the case that the function is a restriction of the function . Indeed, the second argument of is a number in while the second argument of is a number in .

With this set-up, we now present a result that gives the asymptotics of the implied volatility surface in the short maturity, close to the money limit.

Theorem 4.1.8.

We have as that

and more generally, that

where is defined by

Proof.

Fix and . Let . By Theorem 4.1.3, there exists such that

while

for all . Hence and hence

A lower bound is established similarly. The conclusion follows form the continuity of . ∎

For the final theorem of this section, we fix the maturity date and now compute extreme strike asymptotics of the implied volatility. In what follows, we will say that an eventually positive function varies regularly at infinity with exponent iff

Regular variation at zero is defined similarly.

Theorem 4.1.9.

Suppose that is a log-concave density such that varies regularly at infinity with exponent and varies regularly at zero with exponent . Then for we have

and

Proof.

The key observation is that is Lebesgue integrable if and only if . Indeed, since is integrable and log-concave, there exist constants with such that , and hence is bounded from above by an integrable function for and bounded from below by a non-integrable function for .

Fix . The moment generating function of is calculated as

where

By assumption

or equivalently, where as , yielding the expression

The exponent of on the right-hand side is eventually positive, implying is finite, if

and the exponent is eventually negative, implying is infinite, if

On the other hand, where as . Writing

we see that for any , the exponent of on right-hand side is eventually positive, implying is finite.

Therefore, we have shown that

By Lee’s moment formula [28], we have

from which the first conclusion follows. The calculation of the left-hand wing is similar. ∎

4.2. A parametric example

In this section we consider a parametrised family of log-concave densities in which several interesting calculations can be performed explicitly. We then try to fit this family to real call price data as a proof-of-concept.

Consider family of densities of the form

for parameters and real , with normalising constant

where is the complementary incomplete gamma function. It is straightforward to check that is a log-concave probability density.

Letting and , and then sending recovers the Black–Scholes model . Roughly speaking, controls the left wing, the right wing, the at-the-money skew, the at-the-money convexity. Although there are four parameters, recall from Section 3.2 that we have

for , and . Hence, there is no loss of generality if we insist, for instance, that , leaving us with only three free parameters.

The distribution function is given explicitly by

The function can be calculated explicitly when the absolute log-moneyness is sufficiently large:

Otherwise is the unique root of the equation

which can be calculated numerically, for instance, by the bisection method.

The call price curve can be calculated by the formula

Note that this formula is rather explicit when the absolute log-moneyness is sufficiently large, and furthermore, it is numerically tractable in all cases.

This choice of has the advantage that call prices can be calculated very quickly. Also, for other vanilla options, numerical integration is very efficient since the density function is smooth and decays quickly at infinity. Alternatively, rejection sampling is available, since the density is bounded, for instance, by a Gaussian density.

When it comes to calibrate the model, we must find parameters and an increasing function such that

where is the observed normalised price of a call option of moneyness and maturity , where is the set of pairs for which there is available market data. Equivalently, we fit the parameters and the function to try to approximate the observed implied volatility surface.

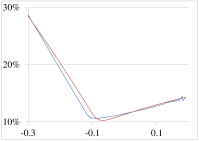

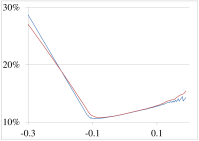

For this exercise, I downloaded E-mini S&P MidCap 400 call options call and put option price data from ftp://ftp.cmegroup.com/pub/settle/stleqt on 12 July 2018, for maturities years for all available strikes. Letting be the set of available strikes for maturity , we have and observations. There are six parameters to find: and , to fit observations.

To speed up the calibration, we can use the asymptotic implied total standard deviation calculations of Section 4.1. In particular, we can apply Theorem 4.1.9 by noting that

However, we can do better and replace each limsup with a proper limit by applying standard asymptotic properties of the complementary incomplete gamma function and the tail-wing formula of Benaim–Friz [2] and Gulisashvili [15] to find

and

Figure 2 shows a calibration of this family of call prices to real market data. It is important to stress that there is no a priori reason why this data should resemble the call surfaces generated by this family of models. Nevertheless, although the fit is not perfect, it does seem to indicate that this modelling approach is worth pursuing further.

4.3. A non-parametric calibration

In this section, we take a somewhat different approach. Rather than assuming that the log-concave density is a fixed parametric family, we use the results of section 4.1 to estimate non-parametrically. In particular, we assume that

where now the function is unknown. Since the fit of the parametric model was reasonably good, we will set to be the same value found in section 4.2.

Recall that Theorem 4.1.3 says that

It is straightforward to check that if satisfies as mild regularity condition as in the hypothesis of Proposition 4.1.6 then we have the slightly improved asymptotic formula

Hence, we will assume that

since is small. Theorem 4.1.4 tells us that

An estimate of the density can now be computed numerically.

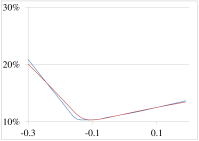

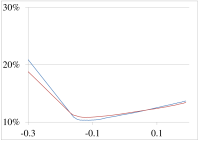

Figure 3 compares , when estimated non-parametrically versus the calibrated parametric example from the last section. Considering the fact that the non-parametric density is estimated from the earliest maturity date, while the parametric density is calibrated using all three maturity dates, the agreement is uncanny.

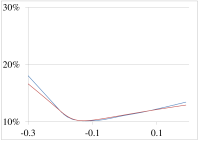

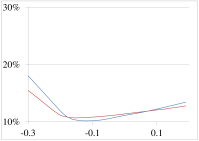

Given that the calibrated parametric density seems to recover market date reasonably well, and that the non-parametric density agrees with parametric reasonably well, it is natural to compare the market implied volatility to that predicted by the non-parametric model. Recall that the model call surface is determined by the density and the increasing function . We have estimated from the short maturity call prices and the assumption that , where was found from the parametric calibration. However, we still need to estimate the function for . For a lack of a better idea, we let for as well.

Figure 4 compares the market implied volatility (the same as in figure 2), with the implied volatility computed from the non-parametric model. Since the estimated density is not given by an explicit formula, I have used the formula in Theorem 4.1.2 to compute the call prices. Again, given that the density is estimated using only the call price curve, it is interesting that the model implied volatility for maturities and should match the market data at all.

5. An isomorphism and lift zonoids

5.1. The isomorophism

In this section, to help understand the binary operation on the space we show that there is a nice isomorphism of to another function space which converts the somewhat complicated operation into simple function composition .

We introduce a transformation on the space which will be particularly useful: for we define a new function on by the formula

We quickly note that the notation introduced here is, in fact, consistent with the prior occurrence of this notation in Section 4.1. Indeed, the connection between the transformation defined here and the conclusion of Theorem 4.1.4 is explored in Section 5.2 below.

Given a call price curve , we can immediately read off some properties of the new function . The proof is routine, and hence omitted.

Proposition 5.1.1.

Fix with primal representation and dual representation .

-

(1)

is non-decreasing and concave.

-

(2)

is continuous and

-

(3)

For and such that

we have

-

(4)

-

(5)

for all .

Figure 5 plots the graph of a typical element .

The next result identifies the image of the map , and further shows that is a bijection:

Theorem 5.1.2.

Suppose is continuous and concave with . Let

Then and

The above theorem is a minor variant of the Fenchel biconjugation theorem of convex analysis. See the book of Borwein & Vanderwerff [5, Theorem 2.4.4].

The following theorem explains our interest in the bijection : it converts the binary operation to function composition . A version of this result can be found in the book of Borwein & Vanderwerff [5, Exercise 2.4.31].

Theorem 5.1.3.

For we have

Proof.

By the continuity of a function at , we have the equivalent expression

Hence for any we have

∎

In light of Theorem 5.1.3, Theorem 2.3.6 says that the set of conjugate functions is a semigroup with respect to function composition , with identity element and absorbing element . The involution on induced by ∗ is identified in Theorem 5.3.2 below.

In preparation for reproving Theorem 3.2.4 and proving Theorem 3.2.7 we identify the image of the set of functions under the isomorphism . As the notation introduced in section 4.1 suggests, we have

by Theorems 4.1.2 and 5.1.2. For notational ease, we will continue to use the notation

Another proof of Theorem 3.2.4.

We now come to proof of Theorem 3.2.7.

Proof of Theorem 3.2.7 .

If a function satisfies the hypotheses of the theorem, then the conjugate function is such that

and satisfies the translation equation

The conclusion of the theorem is that there are only three types of solutions to the above functional equation such that for all :

-

(1)

for all and ,

-

(2)

for all and ,

-

(3)

for all and where and is a log-concave probability density.

Once we have ruled out cases (1) and (2), we can appeal to the result of Cherny & Filipović [9]: concave solutions of the translation equation on are of the form where

for a positive concave function and fixed . Note that for the integral is well-defined and finite as is positive and continuous by concavity. Let and , and define a function as the inverse function , and extend to all of by for and for . Note that we can compute the derivative as

Setting , we have . Since is concave, Bobkov’s result Proposition 3.2.3 implies that is log-concave.

∎

Remark 5.1.4.

An earlier study of the translation equation without the concavity assumption can be found in the book of Aczél [1, Chapter 6.1].

5.2. Infinitesimal generators and the inf-convolution

In this section we briefly and informally discuss the connection between the binary operation defined in section 2.3 and the well-known inf-convolution .

Let be a log-concave density with distribution function , and let

The content of Theorem 3.2.7 is that, aside from the trivial and null semigroups, the only semigroups of with respect to composition are of the above form. The infinitesimal generator is given by

where and we have taken the version of which is continuous on its support . Note that this equation also holds for the trivial semigroup with .

The key property of the function is that it is non-negative and concave. Let

Note that for every element of , aside from , one can assign a unique (up to centring) log-concave density by the discussion of section 4.1.

The space is closed under addition. Furthermore, we have for every non-null one-parameter semigroup that

for some . Let and be two such semigroups. Note that

implying that function composition near the identity element of amounts to addition in the space of generators .

Similarly, let

For , let

One can check that is a bijection between the sets and by a version of the Fenchel biconjugation theorem. In particular, the space can be identified with the generators of one-parameter semigroups in .

Recall that the inf-convolution of two functions is defined by

The basic property of the inf-convolution (see [5, Exercise 2.3.15] for example) is that it becomes addition under conjugation:

in analogy with Theorem 5.1.3. Since there is an exponential map lifting function addition to function composition in , we can apply the isomorphism to conclude that there is an exponential map lifting inf-convolution to the binary operation in .

Indeed, let be a one parameter semigroup with generator , so that

Letting and be two such semigroups, we have

5.3. Lift zonoids

Finally, to see why one might want to compute the Legendre transform of a call price with respect to the strike parameter, we recall that the zonoid of an integrable random -vector is the set

and that the lift zonoid of is the zonoid of the -vector given by

The notion of lift zonoid was introduced in the paper of Koshevoy & Mosler [25].

In the case , the lift zonoid is a convex set contained in the rectangle

where The precise shape of this set is intimately related to call and put prices as seen in the following theorem.

Theorem 5.3.1.

Let be an integrable random variable. Its lift zonoid is given by

Note that if we let

then we have

by Fubini’s theorem. Also if we define the inverse function for by

then by a result of Koshevoy & Mosler [25, Lemma 3.1] we have

from which Theorem 5.3.1 can be proven by Young’s inequality. However since the result can be viewed as an application of the Neyman–Pearson lemma, we include a short proof for completeness.

Proof.

For any measurable function valued in and we have

with equality when is such that

Now suppose so that and for some . Hence, computing expectations in the inequality above yields

with equality if

By replacing with , we see that if and only if , yielding the lower bound. ∎

We remark that the explicit connection between lift zonoids and the price of call options has been noted before, for instance in the paper of Mochanov & Schmutz [29]. In the setting of this paper, given represented by , the lift zonoid of is given by the set

We recall that a random vector is dominated by in the lift zonoid order if . Koshevoy & Mosler [25, Theorem 5.2] noticed that in the case, that the lift zonoid order is exactly the convex order.

We conclude this section by exploiting Theorem 5.3.1 to obtain an interesting identity. A similar formula can be found in the paper of Hiriart-Urruty & Martínez-Legaz [17].

Theorem 5.3.2.

Given , let

Then

Proof.

Let be a primal representation and be a dual representation of .

Note that for all we have

and hence for any we have

where we have used the observation that the optimal in the final maximisation problem assigns zero weight to the event . ∎

5.4. An extension

Let be the distribution function of a log-concave density which is supported on all of , so that and in the notation of section 3. Let

By Theorem 4.1.2 we have

It is interesting to note that the family of functions is a group under function composition, not just a semigroup. Indeed, we have

Note that is increasing for all , is concave if but is convex if . In particular, when the function is not the concave conjugate of a call function in . Unfortunately, the probabilistic or financial interpretation of the inverse is not readily apparent.

For comparison, note that for we have by Theorem 5.3.2 that

6. Acknowledgement

I would like to thank the Cambridge Endowment for Research in Finance for their support. I would also like to thank Thorsten Rheinländer for introducing me to the notion of a lift zonoid, and Monique Jeanblanc for introducing me to the notion of a lyrebird. I would like to thank the participants of the London Mathematical Finance Seminar Series and the Oberwolfach Workshop on the Mathematics of Quantitative Finance, where this work was presented. After the original submission of this work, I learned that Peter Carr and Greg Pelts [8] independently proposed modelling call price curves via their Legendre transform. I would like to thank Johannes Ruf for noticing this connection.

I would also like to thank Johannes for a useful discussion of the implication (5) (1) in Theorem 3.1.2. Originally, I had a complicated proof of this implication only in the discrete-time case. The original argument was similar to the construction in the proof of Theorem 2.3.2: given the implication (5) (2), to apply the discrete-time Itô–Watanabe decomposition to the supermartingale , as in the construction of Föllmer’s exit measure. The difficulty in extending this argument to the continuous-time case is that the local martingale appearing in the continuous-time Itô–Watanabe decomposition may not be a true martingale. While discussing this technical point, Johannes inspired me to try to prove that, in fact, the stronger implication (5) (4) holds.

Finally, I would like to thank the referees for their useful comments on the content and presentation of this work. In particular, I thank them for encouraging me to expand section 4.

References

- [1] J. Aczél. Lectures on Functional Equations and Their Applications. Mathematics in Science and Engineering 19. Academic Press. (1966)

- [2] S. Benaim and P. Friz. Regular variation and smile asymptotics. Mathematical Finance 19(1): 1–12. (2009)

- [3] D.T. Breeden and R.H. Litzenberger. Prices of state-contingent claims implicit in option prices. The Journal of Business 51(4): 621–651. (1978)

- [4] S. Bobkov. Extremal properties of half-spaces for log-concave distributions. Annals of Probabilty 24(1): 35–48. (1996)

- [5] J.M. Borwein and J.D. Vanderwerff. Convex Functions: Constructions, Characterizations and Counterexamples. Encyclopedia of Mathematics an Its Applications 109. Cambridge University Press. (2010)

- [6] S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press. (2004)

- [7] P. Carr and D. Madan. A note on sufficient conditions for no arbitrage. Finance Research Letters 2: 125–130. (2005)

- [8] P. Carr and G. Pelts. Duality, deltas, and derivatives pricing. Presentation available at http://www.math.cmu.edu/CCF/CCFevents/shreve/abstracts/P.Carr.pdf (2015)

- [9] A. Cherny, D. Filipović. Concave distortion semigroups. arXiv:1104.0508 (2011)

- [10] A.M.G. Cox, D.G. Hobson. Local martingales, bubbles and option prices. Finance and Stochastics 9: 477–492. (2005)

- [11] S. De Marco, C. Hillairet, A. Jacquier. Shapes of implied volatility with positive mass at zero. SIAM Journal on Financial Mathematics 8: 709–737. (2017)

- [12] C.-O. Ewald, M. Yor. On peacocks and lyrebirds: Australian options, Brownian bridges, and the average of submartingales. Mathematical Finance 28: 536–549. (2018)

- [13] H. Föllmer. The exit measure of a supermartingale. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete 21(2): 154–166. (1972)

- [14] J. Gatheral, A. Jacquier. Arbitrage-free SVI volatility surfaces. Quantitative Finance 14(1): 59–71. (2014)

- [15] A. Gulisashvili. Asymptotic formulas with error estimates for call pricing functions and the implied volatility at extreme strikes. SIAM Journal on Financial Mathematics 1: 609–641. (2010)

- [16] G. Guo, A. Jacquier, C. Martini, L. Neufcourt. Generalised arbitrage-free SVI volatility surfaces. SIAM Journal on Financial Mathematics 7(1): 619–641. (2016)

- [17] J-B. Hiriart-Urruty and J-E. Martínez-Legaz. New formulas for the Legendre–Fenchel transform. Journal of Mathematical Analysis and Applications. 288: 544–555 (2003)

- [18] F. Hirsh, Ch. Profeta, B. Roynette and M. Yor. Peacocks and Associated Martingales, with Explicit Constructions. Bocconi & Springer Series. (2011)

- [19] F. Hirsh and B. Roynette. A new proof of Kellerer’s theorem. ESAIM: Probability and Statistics 16: 48–60. (2012)

- [20] D. Hobson, P. Laurence, and T-H. Wang. Static-arbitrage upper bounds for the prices of basket options. Quantitative Finance 5(4): 329–342. (2005)

- [21] A. Jacquier and M. Keller-Ressel. Implied volatility in strict local martingale models. SIAM Journal on Financial Mathematics 9: 171–189. (2018)

- [22] R. Kaas, J. Dhaene, D. Vyncke, M.J. Goovaerts, M. Denuit. A simple geometry proof that comonotonic risks have the convex-largest sum. ASTIN Bulletin 32: 71–80. (2002)

- [23] I. Karatzas. Lectures on the Mathematics of Finance. CRM Monograph Series, American Mathematical Society. (1997)

- [24] H.G. Kellerer. Markov-Komposition und eine Anwendung auf Martingale. Mathematische Annalen 198: 99–122. (1972)

- [25] G. Koshevoy and K. Mosler. Lift zonoids, random convex hulls and the variability of random vectors. Bernoulli 4: 377–399. (1998)

- [26] A.M. Kulik and T.D. Tymoshkevych. Lift zonoid order and functional inequalities. Theory of Probability and Mathematical Statistics 89: 83–99. (2014)

- [27] M. Kulldorff. Optimal control of favorable games with a time-limit. SIAM Journal on Control and Optimization 31(1): 52–69. (1993)

- [28] R. Lee. The moment formula for implied volatility at extreme strikes. Mathematical Finance 14(3): 469–480. (2004)

- [29] I. Molchanov and M. Schmutz. Multivariate extension of put-call symmetry. SIAM Journal on Financial Mathematics 1(1): 396–426. (2010)

- [30] V. Strassen. The existence of probability measures with given marginals. Annals of Mathematical Statistics 36: 423–439. (1965)

- [31] M.R. Tehranchi. Uniform bounds on Black–Scholes implied volatility. SIAM Journal on Financial Mathematics 7(1): 893–916. (2016)

- [32] M.R. Tehranchi. Arbitrage theory without a numéraire. Available at http://arxiv.org/abs/1410.2976 (2015)

- [33] S.S. Wang. A class of distortion operators for pricing financial and insurance risks. The Journal of Risk and Insurance 67(1): 15–36. (2000)