Adversarial and Amiable Inference in Medical Diagnosis,

Reliability, and Survival Analysis

Abstract

In this paper, we develop a family of bivariate beta distributions that encapsulate both positive and negative correlations, and which can be of general interest for Bayesian inference. We then invoke a use of these bivariate distributions in two contexts. The first is diagnostic testing in medicine, threat detection, and signal processing. The second is system survivability assessment, relevant to engineering reliability, and to survival analysis in biomedicine. In diagnostic testing one encounters two parameters that characterize the efficacy of the testing mechanism, test sensitivity, and test specificity. These tend to be adversarial when their values are interpreted as utilities. In system survivability, the parameters of interest are the component reliabilities, whose values when interpreted as utilities tend to exhibit co-operative (amiable) behavior. Besides probability modeling and Bayesian inference, this paper has a foundational import. Specifically, it advocates a conceptual change in how one may think about reliability and survival analysis. The philosophical writings of de Finetti, Kolmogorov, Popper, and Savage, when brought to bear on these topics constitute the essence of this change. Its consequence is that we have at hand a defensible framework for invoking Bayesian inferential methods in diagnostics, reliability, and survival analysis. Another consequence is a deeper appreciation of the judgment of independent lifetimes. Specifically, we make the important point that independent lifetimes entail at a minimum, a two-stage hierarchical construction.

keywords:

Bayesian inference; Bivariate beta distributions; Chance; de Finetti’s Theorem; Independence; Risk analysis; Signal processing; System survivability; Threat detection.0 Introduction: Motivation and Overview

The work described here is motivated by two scenarios, one from the medical sciences, and the other from systems science. A resolution of the problems posed by these scenarios entails probability modeling and statistical inference, the former spawned by the needs of the latter. This paper demonstrates an interplay between these two specialties as they come together to constitute the spirit of statistical science.

In medical diagnosis, and also matters of national security – like threat detection and signal processing – testing for abnormalities using diagnostic instruments plays a key role. Diagnostic tests are characterized by two parameters, test sensitivity, , and test specificity, . There are different ways to interpret these parameters, and interpretation dictates methodology. We interpret and as the degree of propensity [or chance] in the sense of Popper (1959) [de Finetti (1937)], and not as probabilities, as is currently done.

Specifically, is to be seen as the “tendency” of a diagnostic instrument declaring a diseased individual as diseased, and as the “tendency” of the instrument declaring a healthy person as healthy. Looking at and as propensities provides a proper foundation for making Bayesian inferences about these parameters via probability statements, where probability to us is a two-sided bet in the sense of de Finetti (1937). Were and be interpreted as probabilities, and probability interpreted as a two-sided bet, then endowing a prior probability to and for the purpose of Bayesian inference is tantamount to assigning personal probabilities to a personal probability, and this could be a matter of debate, if not flawed.

Irrespective of interpretation, one would want diagnostic instruments with and equal to one. However, such instruments are expensive to build, and thus one settles for and being close to one. But a caveat here is that and are adversarial in the sense that an increase in leads to a decrease in , and mutatis-mutandis. Indeed, were one to equate the value of a propensity with utility, then the behavior of the two parameters can be likened to a two-person zero-sum game; thus our use of the term adversarial inference.

Noting the fact that and are akin to the Type-I and Type-II errors of a Neyman-Pearson test of a hypothesis, one may still be inclined to interpret and as probabilities, and declare propensity as another label for probability. However, there is an operational difference. In the Neyman-Pearson scheme, one designs tests with specified errors, whereas a diagnostic test’s specificity and sensitivity are the consequences of an instrument’s engineered design, which a user likes to estimate. In a sense sensitivity and specificity are more akin to the -values of Fisher’s significance test. The difference is that whereas -values help validate a hypothesis, inferences about and help assess the efficacy of an instrument. The underlying message here is that in the context of diagnostics, interpreting and as propensities and not as probabilities, makes sense because propensities encapsulate the physical characteristics of an instrument, and making inferences about them is a meaningful endeavor. However, in the context of testing hypotheses, such parameters are rightly interpreted as probabilities, because such probabilities encapsulate the consequences of ones inductive behavior in the sense of Neyman (1957).

Moving to systems science, assessing the survivability of multi-component systems – like networks or a biological organism, is of importance. This is because survivability is a key ingredient of a system’s performance, where survivability is ones personal probability of an item’s propensity to survive (c.f. Lindley and Singpurwalla, 2002). It is often the case that the components of complex systems experience commonalities with respect to attributes like materials, manufacture, the operating environment, etc. A consequence is that propensity to survive of each of the system’s components experience a positive dependence. That is, the propensities are amiable in the sense that were the values of such propensities viewed as utilities (Singpurwalla, 2009), then the propensities behave as if they are engaging in a two-person co-operative game. Assessing a system’s survivability under the premise of such co-operative behavior, motivates us to label inferences associated with such scenarios as amiable inference. Even though our motivation for amiable inference is systems science, we foresee other scenarios wherein positively dependent (unknown) parameters on the unit square may arise.

For statistical inference under the premise of adversarial or amiable parameters, a Bayesian approach seems natural. But to invoke this approach, suitable probability models that encapsulate the game theoretic character of the parameters are needed. There appears to be a dearth of such models, and a purpose of this paper is to fill this void. One such family of models is proposed here in Section 2. But before discussing these models, a perspective on the notion of propensity and its relevance to reliability and survival analysis is appropriate, and this is done in Section 1 below.

The rest of the paper is devoted to invoking the mechanics of the ideas presented in Sections 1 and 2 to the specific problems mentioned above.

1 Foundational Issues in Reliability and Risk Analysis

The relevance of the notion of propensity in the context of diagnostics has been discussed in the previous section of this paper. Here, we discuss its appropriateness in the contexts of reliability theory and survival analysis. There is much precedence to what we say below dating back to the writings of de Finetti, Jeffreys, Kolmogorov, Popper, and Savage. Relating the essence of these writings to the above disciplines is a contribution of this paper to the foundational aspects of reliability, risk, and survival analysis.

The conventional approach for assessing the performance of an item is based on the metric of reliability, where reliability is defined as a probability. This is also true of survival analysis. But there are many ways to interpret probability and this is where the foundational issues matter. Irrespective of interpretation, probability models entail unknown parameters that are estimated using frequentist or Bayesian methods. In the paragraph which follows, we make a case for the latter based on relevance to a user. With Bayesian methods, the unknown parameters are endowed with a prior distribution, and the prior to posterior conversion made via Bayes’ Law. A justification for introducing priors and invoking Bayes’ Law is de Finetti’s celebrated theorem on exchangeable sequences, and without the judgment of exchangeability, inductive inference is not possible. Inherent to de Finetti’s theorem is the notion of chance (or propensity), and the essence of the theorem is the existence of a personal probability on this chance. Thus appears the role of propensity in reliability and survival analysis in particular, and more generally, in applied probability as well.

To make a case for using Bayesian methods in the contexts of reliability and survival analysis, we start with the claim that it is an item’s survivability - not its reliability - that should be the metric of performance; see Singpurwalla (2006, p.289). This is because survivability can be operationalized via a two-sided bet, whereas reliability, which entails unknown parameters, cannot be operationalized. Reliability is better interpreted as a propensity (or chance). Conversationally, by propensity we mean a tendency, or a dispositional property of the physical world which manifests itself as a relative frequency: see Popper (1959) or Pierce [in Miller (1975)]; also Kolmogorov (1969, p.230). Despite Popper’s endless efforts to equate propensity with probability, it has been argued that propensity is not a probability (c.f. Humphreys, 1985). Probability, to Kolmogorov (1969, p.239) is an undefined primitive, to Jeffreys (1961, p.51) is a logical argument, to de Finetti (1937) is a disposition towards a two-sided bet, and to Savage (1954) is a strength of belief. Because notions like disposition and tendency are metaphysical, the term propensity, like experience, may best be seen as an undefined primitive. Support for this point of view is borne out in actuality, because layperson and even engineers are able to conceptualize and talk about reliability on intuitive grounds without an appreciation of its mathematical definition (c.f. Singpurwalla, 2001). The distinction between probability and propensity is best exposited in de Finetti’s theorem on exchangeability mentioned before, wherein one’s uncertainty about propensity is encapsulated via a personal probability (which can be operationalized).

The above lines of thinking motivate us to suggest a paradigm change in reliability and survival analysis, by proposing that an item’s reliability (as an undefined primitive) be interpreted as its tendency to survive (under specified conditions for a specified period of time), and that its survivability as ones personal probability about this propensity. Survivability being devoid of conditioning parameters is more appealing to a user because its operationalization via a two-sided bet induces transparency. Because survivability is obtained by averaging out reliability over its underlying parameters, reliability now becomes a stepping stone to survivability, and it is survivability that conveys an actionable import. The proposed shift in focus from reliability to survivability constitutes a perspective change in the assurance sciences.

But interpreting reliability (with its unknown parameters) as a propensity does something more fundamental, at least from a conceptual point of view. It paves the path for invoking de Finetti’s theorem, and in so doing provides a proper foundation for using Bayesian inferential and decision theoretic methods in reliability and survival analysis. Since the initial writings of Cornfield (1969), Arjas (1993), Barlow and Pereira (1993), and Spizzichino (1993), such methods have continued to gain much traction. Also noteworthy are several contributions in the monograph edited by Barlow, Clarotti and Spizzichino (1993).

2 A Family of Bivariate Distributions on the Unit Square

The diagnostic testing scenario of the introductory section spawns the need for a family of bivariate distributions on the unit square with negative dependence. By contrast, the system survivability scenario calls for multivariate distributions on the unit hypercube with positive dependence. Such multivariate distributions are in general difficult to construct, especially if the number of parameters is to be kept down to a minimum. Consequently, we restrict attention to bivariate distributions on the unit square with either positive and/or negative dependence. There is a price to be paid for doing so because it is unclear to us as to how a pairwise modularization of a multi-component system can be constituted to make inference about the entire system. All the same, a consideration of the bivariate case is instructional, and could serve as a first step towards addressing the multi-component case.

An archetypal strategy for constructing bounded bivariate distributions is the one adopted by Olkin and Liu (2003) – henceforth , and also by Arnold and Ng (2011) – henceforth . Here, one starts with independent gamma distributed random variables , with a scale (shape) parameter 1 (), . The construction has ; it starts by considering the bivariate random variable , where

The distribution of is a beta (distribution of the first kind) on with parameters []; it is denoted []. The joint distribution of is a bivariate beta on the unit square with a positive correlation, covering the entire range of 0 and 1. Jones (2001) has also obtained this distribution but via a different line of construction. Other examples of bivariate distributions with beta marginals appear in Gupta and Wong (1985), Nadarajah and Kotz (2005), Nadarajah (2009), Balakrishnan and Lai (2009) and Gupta, Orozco-Castañeda and Nagar (2010). Like the bivariate beta distribution of Jones-Olkin-Liu, these distributions also exhibit positive dependence. Whereas such distributions are suitable for what we have labeled amiable inference, adversarial inference requires bivariate distributions with negative dependence. The well-known bivariate Dirichlet distribution has a negative correlation and beta marginals, but the range of possible values that the variables take is restricted, because of the requirement that they sum to one. Its suitability as a vehicle for inference in diagnostic testing is therefore limited. Fortunately, by a simple complementation of one of the variables in the construction, we can obtain a bivariate beta distribution on the unit square with a negative correlation. We denote this distribution ; the superscripts associated with the style constructions denote positive (negative) correlation. To summarize, the bivariate random variable [or equivalently ] has the distribution, and this distribution is suitable candidate for the adversarial inference needs of diagnostic testing.

Since , we are motivated to consider expanded versions of the strategy to construct bivariate beta distributions on the unit square with both positive and negative correlations. This is indeed the motivation behind the Arnold and Ng (2011), , construction for which . Here,

from which it follows that and . Furthermore, by a judicious choice of , , both positive and negative correlations can be induced.

The distribution introduced above has some attractive properties. For example, with , it yields the bivariate Dirichlet distribution of Balakrishnan and Lai (2009), and for , it collapses to the distribution. A drawback of the construction is that it does not encompass the distribution, nor will it encompass, for , constructions based on complementation of the type and . Such lack of closure motivates us to seek a further expansion of the construction in the hope of generating a more encompassing family of bivariate beta distributions. This topic is delegated to the Appendix, with the comment that closure properties are relevant to Bayesian inference because they provide flexibility regarding the choice of prior distributions.

In the next two sections, we show how the material of this section can be used to discuss inference in diagnostics and system survivability. Whereas out approach to inference is Bayesian, it is not our intent to convey the impression that Bayesian approaches are the only viable ones for addressing the matter of adversarial and amiable inference. Our choice for a Bayesian approach is dictated by the considerations of Section 1.

3 Adversarial Inference in Diagnostic Testing

Diagnostic tests which play a key role in matters ranging from medicine to mathematical finance, are imperfect. For example, a test to detect antibodies of AIDS will occasionally diagnose a disease-free individual as being diseased, or will fail to diagnose a diseased individual (c.f. Gastwirth, 1987). Diagnostic tests that perform perfectly are sometimes available, such tests are called confirmatory tests. The less reliable, but cost-effective tests, are called screening tests. Our focus here is on screening tests whose efficacy we endeavor to address. As stated, the efficacy of screening tests is characterized by the two adversarial parameters, sensitivity , and specificity . Notwithstanding the several foundational issues on diagnostics raised by Dawid (1976) in his insightful paper, our goal is to develop an inferential mechanism for these parameters accounting for their adversarial nature.

3.1 Notation and Terminology

Let denote the event that an individual is actually diseased, and the complement of . The truth or falsity of is affirmed by a confirmatory test. Let () denote the event that a screening test declares an individual diseased (not diseased). Let be the probability (propensity) that a randomly chosen individual has the disease in question; is called the disease prevalence. Were and be interpreted as probabilities, then and are indeed and , the sensitivity and specificity, respectively, of the screening test. Whereas and encapsulate the quality of the screening test, and , encapsulate the predictive ability of the screening test. The parameters () are known as the predictive value of a positive (negative) screening test.

Interpreting and as probabilities, a Bayesian approach for inference about , and , was proposed by Gastwirth, Johnson and Reneau (1991) – henceforth GJR (1991) – based on independent beta prior distributions on and . A similar approach was taken by Pereira and Pericchi (1990). Besides a philosophical objection to endowing probabilities to probabilities, such priors do not account for the adversarial character of and . The posterior distributions of , and are then used by GJR (1991) approach to induce the posterior distribution of and . The GJR (1991) analysis based on screening data from AIDS patients, concluded that unless and are precisely known, inferences about , and are not credible. Thus, credible inferences about and are important, and our aim here is to work towards this goal. Our point of departure from the GJR (1991) is the use of joint priors on and that incorporate negative dependence, and the use of confirmatory (instead of screening) test data to develop our inferential mechanism. With and interpreted as propensities, inferences about and entail a strategy that is different from that of GJR (1991), and also that of Pereira and Pericchi (1990). This is articulated later in Section 3.5.

The prior distributions chosen here are the distribution and the distribution with parameters so chosen that and are negatively correlated. Recall that the family of distributions does not encompass the distribution. We have chosen the distribution instead of the more generalized bivariate beta distribution – namely the family of the Appendix – because the more parsimonious nature of the construction eases the computational burden. For convenience, we shall denote by the joint probability density function of the bivariate beta distribution, and by and its marginal density functions. This is because a closed form expression for the joint density function is not available. The marginal densities and are of course beta. The joint probability density function of the bivariate beta distribution is available in closed form; it will be given in Section 3.3.

3.2 Test Design and Likelihood

Suppose that a sample of size is chosen at random from a population of interest, and a confirmatory test given to each subject. This is in contrast to the sampling plan considered by GJR (1991) who give a confirmatory test only to individuals who screen positive.

Let be the number of individuals declared by the confirmatory test. Note that , and that

or equivalently

The individuals who test positive are then given the screening test whose efficacy we wish to assess. Let be the number of diseased individuals who are declared diseased [not diseased] by the screening test. Clearly,

Similarly, let be the number of non-diseased individuals who are declared non-diseased [diseased] by screening test. Then,

Thus, the results of the confirmatory and the screening tests given to individuals, yield as data the quantities , and . Both and depend on , where is random. Thus, and are conditionally (given ) independent, but unconditionally, they are dependent, this being the case irrespective of whether we condition or not on and . In what follows, we assume the independence of and conditional on , , and ; this assumption is meaningful. Under the above assumption of conditional independence, a likelihood for , , and , with , and as observed data, can be inducted via the following probability model (under the philosophical principle of conditionalization):

3.3 Posterior Analysis

Since , the disease prevalence parameter, is in no way influenced by the quality of the screening instrument, the prior on is assumed to be independent of the joint prior on and . It is taken to be a beta distribution with parameters and . As mentioned before, the joint priors on and are

-

(i)

the distribution whose probability density function is:

for , with marginals and , which are beta distributions, and

-

(ii)

the distribution with joint and marginal probability density functions , and , respectively.

The above priors and the likelihood, yield the joint posterior distribution of , , and as:

depending on whether the or the distribution is used as prior; here, the data is , and is the beta prior on .

Since factors out in the likelihood, and since its prior is assumed to be independent of joint prior of and , the posterior distribution of falls out as . Consequently, the joint posterior distribution of and is:

This joint posterior distribution is not available in closed form, irrespective of the choice of the prior. Thus, is to be assessed numerically. A direct approach is to construct an sized grid over the unit square, and denote the -th member of the grid by , . The joint posterior distribution of and , at the point is then approximated at all , as:

The larger the , the better is the approximation. Since the marginal posterior distributions of and are of practical interest, these will be approximated, for at the point , , as:

and similarly, for , , we obtain . This completes our discussion on posterior analysis.

3.4 Proof of Principle: Validation by Synthetic Data

It is difficult, if not impossible, to assess the quality of a diagnostic test via assessed values of its adversarial parameters and , unless these parameters are known with certainty. This means that it does not make sense to use actual (field) data to establish proof of principle of the proposed approach. Consequently, we need to generate synthetic data with known properties, and how such data are generated is described below. The priors for and under scrutiny here are the and the with negative correlation, and also the independent beta priors of GJR (1991). A use of this latter family of priors will enable us to assess the operational merit of incorporating a priori knowledge in the assessment exercise.

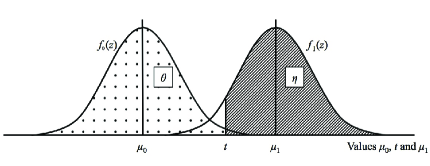

To generate , and under known values of , , and , we proceed as follows: Let denote the values taken by an observable diagnostic variable for members belonging to disease-free class , and denote the values taken by the variable for members belonging to the diseased class, . Assume that has a normal probability density function with mean and variance 1, for . Let be a “threshold”, where is between and . Any individual whose diagnostic measurement value exceeds is classified as diseased; otherwise the individual is classified as non-diseased. See Figure 1 which shows the dispositions of , and . Thus, given the distributions of and , and the threshold , and can be precisely determined.

For any pre-specified sample size , and a pre-specified disease prevalence probability , we obtain , the number of individuals in the sample that should belong to the class , as , where denotes the integer part of . We now generate observations from and denote these as ; similarly, we generate observations from and denote these as . Then, is the total number of ’s out of that are greater than , and is the number of ’s out of that are less than or equal to . A naive estimate of is , and that of is . Furthermore, if is the total number of ’s and ’s that are greater than , then a naive estimate of is . Thus, for any specified and , we have generated as our data with the true values of and determined via , the standard normal variate, as and .

In what follows we set , and choose a range of values for , namely , 30, 50 and 100. The means and are taken to be 3 and 4, respectively, and is set at 3.25. The above choices yield the true values for and as and .

For the two families of joint prior distributions of and , we choose (, , and ), and (, and ), respectively. The former set yields a beta distribution with parameters as the marginal prior for , and a beta distribution with parameters as the marginal prior for . The latter set ensures that the marginals for and under the model are comparable to the beta distributions given above vis-à-vis their means, which happen to be about 0.67 for both and . For the parameter choices given above, the theoretical correlation between and under the distribution is , and that under the distribution is .

Comparative Analysis: Results of Simulation

Using the schemata for generating the data described above, along with the choice of prior parameters given above, we obtain the joint posterior distributions for and , for , and 100. For purposes of calibration against the independence case, a joint prior that is the product of independent beta distributions, and , denoted Independent was also considered. The contours of the joint priors and their corresponding posterior distributions for the four choices of are shown in the second, third, and fourth columns of Table 1. The solid lines in each plot show the location of the true values of and , namely, 0.773 and 0.599. These facilitate a comparison of the true against the centroids of the posterior contours, which are shown by dashed lines.

Tables 2 and 3 are replicas of Table 1 save for the fact that they pertain to the marginal priors and posterior distributions of and respectively for the distributional choices mentioned above. As with Table 1, the solid lines on these plots display the true values of and ; this facilitates a comparison with the modes of the prior and posterior marginal distributions, shown by the dashed lines.

| Values of |

Independent

|

, , |

, |

|

(Prior) |

![[Uncaptioned image]](/html/1701.03462/assets/x2.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x3.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x4.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x5.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x6.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x7.png)

|

|

![[Uncaptioned image]](/html/1701.03462/assets/x8.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x9.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x10.png)

|

|

![[Uncaptioned image]](/html/1701.03462/assets/x11.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x12.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x13.png)

|

|

![[Uncaptioned image]](/html/1701.03462/assets/x14.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x15.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x16.png)

|

| Values of |

Independent

|

, , |

, |

|

(Prior) |

![[Uncaptioned image]](/html/1701.03462/assets/x17.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x18.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x19.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x20.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x21.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x22.png)

|

|

![[Uncaptioned image]](/html/1701.03462/assets/x23.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x24.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x25.png)

|

|

![[Uncaptioned image]](/html/1701.03462/assets/x26.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x27.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x28.png)

|

|

![[Uncaptioned image]](/html/1701.03462/assets/x29.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x30.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x31.png)

|

| Values of |

Independent

|

, , |

, |

|

(Prior) |

![[Uncaptioned image]](/html/1701.03462/assets/x32.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x33.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x34.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x35.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x36.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x37.png)

|

|

![[Uncaptioned image]](/html/1701.03462/assets/x38.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x39.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x40.png)

|

|

![[Uncaptioned image]](/html/1701.03462/assets/x41.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x42.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x43.png)

|

|

![[Uncaptioned image]](/html/1701.03462/assets/x44.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x45.png)

|

![[Uncaptioned image]](/html/1701.03462/assets/x46.png)

|

Qualitative Comments on Results

An examination of the contour plots of Table l shows that the centroids of these contours get closer to their true values as increases; this is to be expected of any meaningfully construed Bayesian procedure. Furthermore, the contours become more and more concentrated as increases, with the based prior contours showing the greatest movement; this is followed by the based contours. Convergence of the posterior centroid to its true value occurs for the prior, for as small as 30. This is followed by the based prior. For , all three priors appear to give similar results.

The negative correlation of the prior is retained by the posterior for all the values of . Surprisingly, the negative correlation of the based posterior distribution diminishes as increases, and almost vanishes when . In general, the centroids of the contour plots generated by the prior distribution tend to be closer to the true values of and as compared to the centroids of the contours provided by the other priors.

An examination of the plots of the marginal posterior distributions of given in Table 2 suggests that the modes of the posterior distributions get closer to the true values of as increases; again, this is to be expected. The dispersion of the posterior distribution of is the smallest for the distribution over all values of . Not withstanding the above, it appears that all three prior distributions provide satisfactory inferences for .

An examination of the plots of the marginal posterior distributions of given in Table 3 suggests a behavior that parallels the behavior of the plots in Table 2.

Based on the above, we are inclined to conclude that for small sample sizes, the as a joint prior distribution for and performs better vis-à-vis closeness of the centroid of the posterior distribution and the modes of the marginal distributions to the true values of and , than those under the and the independent priors. Also, the posterior contours are sharper under prior distribution than the others. When is large, say , the choice of the prior does not seem to matter, save for the fact that the based prior tends to retain, albeit slightly, the negative dependence between and .

3.5 Assessing Predictive Values of Screening Tests

With and interpreted as probabilities, and the joint posterior distribution of and together with the posterior of at hand, assessing and can be achieved by numerical methods, using the fact that:

However, with and interpreted as propensities, the above relations for and are not meaningful because the probability calculus cannot be invoked on propensities. All the same, if a new item subjected to a screening test reveals an , then interpreting as the likelihood of with known, can be used in conjunction with Bayes’ Law to obtain the posterior predictive probability of as

where is the posterior probability of the disease prevalence.

Similarly, were the item to reveal , then

The quantities and are those given in Section 3.3.

3.6 Discussion and Summary Remarks on Section 3

Test sensitivity and test specificity are the two key parameters that determine the quality of diagnostic tests used in a variety of fields. These parameters are adversarial in the sense that an increase in one results in a decrease in the other and vice versa. The aim of this paper was to develop a Bayesian inferential mechanism for assessing the above parameters. To do so one needs as a prior distribution a bivariate distribution on the unit square, where the said distribution should encapsulate a negative dependence. Two such families of bivariate distributions are considered, one due to Arnold and Ng (2011) and the other, a new family based on a transformation of one of the variables in a bivariate beta family of distributions developed by Olkin and Liu (2003). Both families of distributions share a common architecture, namely, the ratios of independent gamma distributions.

An analysis of some synthetically generated test diagnosis data is used to illustrate the workings of the approach proposed here. For purposes of comparison, independent priors for sensitivity and specificity are also considered. Whereas the analysis done here does not indicate a dramatically different inferential conclusion between a use of the independent and the negatively dependent priors, it does show that the latter have a edge over the former. More important, since sensitivity and specificity are known to be adversarial, coherence mandates that the priors encapsulate negative dependence. Of the two negatively dependent bivariate beta distributions considered here, the one by Arnold and Ng (2011) gives the sharper results, both with respect to closeness to the true values and narrowest bands of uncertainty.

In principle, all matters pertaining to diagnostics should be addressed from a decision-theoretic perspective. This would call for an assessment of utilities for a correct diagnosis, as well as for false diagnosis. This is a topic in its own right which remains to be addressed. There is a parallel between the work described here and that done by GJR (1991). The main difference lies not merely in the choice of the independent priors used by the above authors versus the negatively dependent priors used by us, but also in experimental design used to collect the data. GJR (1991) use retrospective (field) data and are therefore better grounded in practice than what is discussed here. The starting point for the above authors is the screening test data, whereas for us it is the confirmatory test data. In GJR (1991), confirmatory tests are then given to those who screen positive to see how effective the screening test is. In our case, it is the opposite; screening tests are given to those who are known to be diseased or not diseased. Both approaches suffer from the drawback that the first test given may not result in a diseased (or non-diseased) subject. Which of the two data generation approaches is optimum is another decision-theoretic issue that remains to be addressed.

Clearly, there is more that needs to be done in the arena of diagnostics than the matter of inference about its adversarial parameters. Paramount among these remaining problems is the choice of the sample size, and the choice of a sampling plan. The proposed work has a broader impact in the sense that it could be of value whenever one needs to estimate competing propensities.

4 Amiable Inference in System Performance Assessment

Consider a two-component series system, with , if the -th component is surviving (failed) at time , . Similarly, let if the entire system is surviving (failed) at . Let be the now time, normally set equal to zero. Let be the operating environment; we assume that is static and is known to us. We also assume that failed components are not repaired, nor replaced. Let represent all the background information about the components and the system that we have at time . Thus, and are the assumed known values of the set-up described above. The case of a two component parallel redundant system proceeds along the lines parallel to the ones given below with appropriate modifications.

We are required, at time , to specify our personal probability that at a future time , ; that is, the survivability of the system under the knowledge of and . Formally, we need to access . An implicit, but important, point in reliability/survival analysis is that there are two time indices to keep in mind. One is the “mission time” , and the other is the time of assessment . The assessment time is important, because as time marches on, changes, and with an expanding , ones personal probability that , may change as well. This feature has been carefully articulated by Arjas (1993) in a striking paper on information and reliability; also see Arjas and Norros (1984).

It is common to suppress , and , so that the explicit notation is simply written . The role of is important, because encapsulates the conditions under which a propensity occurs. With the above in mind, we may invoke the law of total probability by introducing a parameter , and writing

| (1) | |||||

where is interpreted as the propensity of each component to survive to time , and encapsulates our personal probability of .

The set-up of Equation (1) is meaningful when the two components are judged similar in some sense. For example, the components are randomly picked from a batch of identically manufactured units. This is made explicit by the feature that both and are conditioned on a common . The role of and is to help one specify for which a natural model is a beta distribution with parameter and ; that is, is .

If the judgment that and are in some sense similar cannot be justified, then we must introduce two parameters , , each interpreted as a propensity of its associated component surviving to . We then invoke the law of total probability to write

| (2) |

where encapsulates our joint uncertainty about and ; as before and help to guide its choice.

The exact specification of is facilitated by the materials of Section 2. However, whereas the focus in Section 3 was the adversarial character of and , with system survivability, the propensity parameters and tends to be amiable. Consequently, our choices for is the bivariate beta of Olkin and Liu (2003) with positive correlation, namely the family, or the family of Arnold and Ng (2011) with parameters so chosen that the correlation is positive. The question we address is how these choices of distributions impact system survivability? We also need to compare such assessments with those that would be obtained under the assumption of independent propensities, namely, when , and also when the two components are assumed to be similar; i.e., when , and is . In making such comparisons, we must ensure fairness via a judicious choice of parameters.

4.1 The Case of Exchangeable Lifetimes

With reference to Equation (1), suppose that is (conditionally) independent of given . Then,

| (3) | |||||

when is . With , the system’s survivability is 1/3, whereas the survivability of each component, is the expected value of , . We immediately notice that the answer for the system’s survivability is not the conventional 1/4. This is because the components lifetimes and are generated by the same , making and exchangeable in the sense of de Finetti (1937). Under what assumptions will the conventional answer, namely 1/4, be justified? This matter is articulated next.

4.2 The Case of Hierarchically Independent Lifetimes

With reference to Equation (2), suppose that given , is independent of both and , and that given , is independent of . Then, we have

| (4) |

Suppose further that (in the light of and ), is independent of . That is, a knowledge of the propensity of one component does not change ones assessment of the propensity of the other component. When such is the case , and now Equation (4) becomes

where , is the survivability of component , . Now the system survivability is the product of the survivability of each component, and if , , then

| (5) |

When , and , the above expression becomes , which for yields 1/4, the conventional answer.

Thus the conventional answer can only be justified under a hierarchy of independence assumptions. First, one assumes the independence of and , and then the conditional independence of and given and . This feature of hierarchical independence needs to be highlighted, not only in the reliability and the survival analysis literatures, but also in machine learning and classification. The latter go under the label of “naïve Bayes”, or more colorfully “idiot’s Bayes” (c.f. Hand and Yu, 2001). In all cases, it is implicitly assumed that it is only the lifetimes , , that are (conditionally) independent.

Recall that assessments of system survivability under the assumptions of exchangeability and of hierarchical independence yield and , respectively, as answers. This means that for series system, hierarchical independence results in a conservative assessment of system survivability. The difference is the term , and this also happens to be the variance of , when . An appreciation of the cause of this difference can be had by looking at the hierarchical construction of the two models for survivability. This will be done later in Section 4.4, once we look at the case of system survivability under interdependent propensities, the scenario which has motivated the materials of Section 2 of this paper.

4.3 System Survivability Under Interdependent Propensities

Suppose that the assumptions of conditional independence of the lifetimes leading to Equation (4) continue to hold, but the propensities and cannot be judged independent. The dependence between and is captured in the choice of vis-à-vis either the model or the model. Thus, our expression for system reliability can be written as:

To evaluate , we use the relationship

| (6) |

where is the correlation between and , and is the variance of , . Values of for selected values of the parameters that go to construct the and models have been tabulated by Olkin and Liu (2003) and by Arnold and Ng (2011), respectively.

Under the above set-up, the lifetimes and are unconditionally dependent. This is because and which spawns them are dependent. Intuitively, the strength of dependence between and is a function of the strength of dependence between and . The dependence is the strongest when a common generates and , because now ; thus the exchangeable case is a special case of interdependent propensities. The dependence vanishes when is independent of . Otherwise, the strength of dependence is intermediate between those two extreme cases. An appreciation of the nature of dependence between and is by examining the illustrations below which show the hierarchical construction of the three scenarios for system survivability discussed above.

4.4 Conceptualization of Hierarchically Constructed Lifetimes

Figure 2 provides a visualization of constructing the lifetime of each component under the three scenarios of exchangeability, independence and a dependence that is intermediate to that produced under exchangeability and independence. They describe the different mechanisms via which the two lifetimes are generated.

In Figure 2(a), one generates a single from the distribution , and then using this as a parameter, one generates two independent Bernoulli variable and . Because and are based on a common seed, namely , they are positively dependent; indeed exchangeable. Conditioned on , they are independent. In Figure 2(b), one starts with the same as in Figure 2(a), and generates two independent parameters and . Next, using as a parameter, one generates a Bernoulli variable , and then using as a parameter, one generates independently (of ), another Bernoulli variable . Here and are unconditionally independent. In Figure 2(c), one starts with a non-trivial joint distribution of and , namely , and then generates the parameter vector . The two-sided arrow linking and reveals the fact that and are dependent. Next, using as a parameter, one generates a Bernoulli variable , and then using as the parameter, one generates independently (of ) a second Bernoulli variable . Here, and are unconditionally dependent because and are linked. Contrast this with the architecture of Figure 2(b) wherein there is no link between and . In Figure 2(a), the link between and is so strong, that indeed and collapse to a single .

In all three constructions described above, and are, given their respective parameters, independent. An interesting generalization of the above constructive scheme would be to generate conditionally dependent Bernoulli vector ( and ), and investigate the survivability of the ensuing series system.

4.5 Comparison of Survivability of Series Systems

In this section, we explore the consequences of assuming the exchangeable, the , and the versions of the interdependent propensities on series system survivability. Our aim is to see if it is possible to draw some general conclusions based on an examination of the empirical results.

We start with the exchangeable case with , and different choices of and . Recall that here , , and – system survivability – is . Table 4 summarizes the results.

| Values of | : Component | : Variance | Series System |

|---|---|---|---|

| Survivability | of | Survivability | |

| (1, 1) | 0.50 | 0.080 | 0.333 |

| (3, 1) | 0.75 | 0.037 | 0.600 |

| (10.1, 1) | 0.90 | 0.006 | 0.835 |

| (5.5, 6) | 0.90 | 0.013 | 0.836 |

| (3, 0.3) | 0.90 | 0.020 | 0.845 |

| (1, 0.1) | 0.90 | 0.040 | 0.866 |

In Table 5, we give results when the interdependence between and is described by the distribution with the parameters , and so chosen that there is a match between the marginal distributions , , and the distribution of in Table 4.

| Distribution of | : Survivability | : Variance | : | Series System |

|---|---|---|---|---|

| , | of component | of | Correlation | Survivability |

| 0.50 | 0.080 | 0.478 | 0.290 | |

| 0.75 | 0.037 | 0.861 | 0.595 | |

| 0.90 | 0.020 | 0.859 | 0.845 | |

| 0.90 | 0.040 | 0.681 | 0.855 |

An examination of the entries in the last four rows of Table 4 suggests that the survivability of the series system increases with the variance of . The same is also true when we look at the last two rows of Table 5, and this is despite the fact that the entry for in row three is larger than the corresponding entry in row four.

Recall that the survivability of a two-component series system when , , and and independent, is 0.25 – see Equation (5). Comparing this 0.25 with entries in the last column of Tables 4 and 5 suggests that all else being equal, series system survivability increases with the strength of dependence between and .

Moving on to the scenario wherein the interdependence between and is described by an model, suppose that , and . Then, and , so that , , , and from Table 1 of Arnold and Ng (2011), . These entities yield 0.255 as the system survivability. The closest match to the above choices of , , and , is the first row of Table 5, for which the value of the system survivability is 0.29. This result could prompt the claim that an model for interdependence may yield conservative assessments of system survivability as compared to a suitably matched model. But any such claim should be tempered by the fact that in the case, , , is 0.08, whereas its value in a corresponding case is 0.012, and our previous conjecture that the greater the marginal variance, the larger is the survivability.

To affirm if the claim of conservative survivability assessment is generally true in all cases entailing the distribution, we consider two other combinations of values of the ’s, . Specifically, setting , , and , yields , , and ; this is a close match to row three of Table 5. By contrast, setting , , and , provides a close match to row four of Table 5. The only caveat here is that the marginal distributions of and are different; see rows three and four of Table 6, which summarizes the consequences of these choices. A match for row two of Table 5 has not been considered.

| Distribution of | : Survivability | : Variance | : | Series System |

|---|---|---|---|---|

| , | of component | of | Correlation | Survivability |

| 0.50 | 0.012 | 0.484 | 0.255 | |

| 0.90 | 0.007 | 0.755 | 0.815 | |

| 0.89 | 0.014 | 0.675 | 0.840 | |

| 0.94 | 0.004 | 0.675 | 0.840 |

4.6 Discussion and Summary Remarks on Section 4

Comparing the system survivability entry of row two of Table 6 with that of row four of Table 5, and row three (four) of Table 6 with that of row four of Table 5, reaffirms the claim, that all things being equal, the choice of an model for the interdependence between the propensities and results in conservative assessments of system survivability as compared to the model. But this model could be a feature of the fact that the distribution tends to be more concentrated than the distribution. From the viewpoint of safety and risk, conservative assessments of survivability may be more desirable than those that tend to be on the optimistic side. Thus, the choice of what joint distribution to use, the or the depends, in the case of a series system, to ones disposition to the risk of system failure. The bivariate beta distribution being more concentrated than a corresponding matched distribution tends to yield more conservative assessment of series system reliability.

The essential import of the material of Section 4 is two-fold. The first is approach for incorporating positive dependence for the survivability assessment of a (two-component) series system using bivariate beta distributions on a unit square. The extension to parallel systems is relatively straightforward. Generalization to multi-component systems and networks is a challenge that remains to be addressed. For this, an essential first step would be to develop families of joint distributions (with interdependence) on a unit cube. Alternatively, one could modularize a system in terms of independent pairs, each pair being a series (parallel) system of interdependent lifetimes.

The second import of this section is a closer look into the architecture of dependent and independent lifetimes; see Figure 2. The key point here is that any assumption of independent lifetimes has to be justified, at a minimum, via a two-stage argument. This latter point may not have been made transparent in the past.

Acknowledgements

Professor Vijay Nair, the Editor, hit the nail on the head by advising us how to re-organize and streamline the paper; deeply appreciated. The insightful comments of Referee III helped improve the technical content of the paper. Referee II, though unsupportive of this work, ended up making valuable comments which enabled added verbiage to improve clarity. The positive comments of Referee I who elegantly summarized the gist of the paper and suggested a sharper focus are deeply appreciated. Overall, the review process was both a pleasurable and productive experience.

Nozer D. Singupurwalla’s work was supported by The US Army Research Grant W911NF-09-1-0039, The US National Science Foundation Grant DMS-09-15156, The City University of Hong Kong [Project Numbers 9380068 and 9042083 (Hong Kong GRF)]. Hon Keung Tony Ng’s work was supported by a grant from the Simons Foundation (#280601 to Tony Ng).

References

- Arjas (1993) Arjas, E. (1993). Information and reliability: A Bayesian perspective. In Reliability and Decision Making, (eds. R. Barlow, C. Clarotti, and F. Spizzichino), pp. 115–136. London, UK: Chapman & Hall.

- Arjas and Norros (1984) Arjas, E. & Norros, I. (1984). Life lengths and association: A dynamic approach. Mathematics of Operations Research, 9, 151–158.

- Arnold and Ng (2011) Arnold, B.C. & Ng, H.K.T. (2011). Flexible bivariate beta distributions. Journal of Multivariate Analysis, 102, 1194–1202.

- Balakrishnan and Lai (2009) Balakrishnan, N. & Lai, C.D. (2009). Continuous Bivariate Distributions, Second Edition. New York, NY: Springer.

- Barlow, Clarotti and Spizzichino (1993) Barlow, R.E., Clarotti, C.A. & Spizzichino, F. (eds) (1993) Reliability and Decision Making. London, UK: Chapman & Hall.

- Barlow and Pereira (1993) Barlow, R.E. & Pereira, C. (1993). Influence diagrams and decision modelling. In Reliability and Decision Making, (eds. R. Barlow, C. Clarotti, and F. Spizzichino), pp. 87–100. London, UK: Chapman & Hall.

- Cornfield (1969) Cornfield, J. (1969). The Bayesian outlook and its application. Biometrics, 25, 617–657.

- Dawid (1976) Dawid, A.P. (1976) Properties of diagnostic data distributions. Biometrics, 32, 647–658.

- de Finetti (1937) de Finetti, B. (1937) Foresight: Its logical laws, its subjective sources. Ann. Inst. H. Poincaré, 7, 1–68.

- Gastwirth (1987) Gastwirth, J.L. (1987) The statistical precision of medical screening procedures: Application to polygraph and AIDS antibodies test data. Statistical Science, 2, 211–352.

- Gastwirth, Johnson and Reneau (1991) Gastwirth, J.L., Johnson, W.O. & Reneau, D.M. (1991). Bayesian analysis of screening data: Application to AIDS in blood donors. The Canadian Journal of Statistics, 19, 135–150.

- Gupta, Orozco-Castañeda and Nagar (2010) Gupta, A.K., Orozco-Castañeda, J.M. & Nagar, D.K. (2011). Non-central bivariate beta distribution. Statistical Papers, 52, 139–152.

- Gupta and Wong (1985) Gupta, A.K. & Wong, C.F. (1985). On three and five parameter bivariate beta distributions. Metrika, 32, 85–91.

- Hand and Yu (2001) Hand, D.J. & Yu, K. (2001). Idiot’s Bayes – Not so stupid after all? International Statistical Review, 69, 385–398.

- Humphreys (1985) Humphreys, P. (1985). Why Propensities Cannot be Probabilities? The Philosophical Review, 94, 557–570.

- Jeffreys (1961) Jeffreys, H. (1961). Theory of Probability, 3rd Edition. Clarendon: Oxford.

- Jones (2001) Jones, M.C. (2001). Multivariate and beta distributions associated with the multivariate distribution. Metrika, 54, 215–231.

- Kolmogorov (1969) Kolmogorov, A.N. (1969). The Theory of Probability. In Mathematics: Its Content, Methods, and Meaning, 2nd Edition, (eds. A. D. Aleksandrov, A. N. Kolmogorov, M. A. Lavrent’ev), pp. 229–264. Cambridge, MA: M.I.T. Press.

- Lindley and Singpurwalla (2002) Lindley, D.V. & Singpurwalla, N.D. (2002). On exchangeable, causal and cascading failures. Statistical Science, 17, 149–233.

- Miller (1975) Miller, R.W. (1975). Propensity: Popper or Peirce? British Journal for the Philosophy of Science, 26, 123–132.

- Nadarajah and Kotz (2005) Nadarajah, S. & Kotz, S. (2005). Some bivariate beta distributions. Statistics, 39, 457–466.

- Nadarajah (2009) Nadarajah, S. (2009). A bivariate distribution with gamma and beta marginals with application to drought data. Journal of Applied Statistics, 36, 277–301.

- Neyman (1957) Neyman, J. (1957). ‘Inductive behavior’ as a basic concept of philosophy of science. Review of the International Statistical Institute, 25, 7–22.

- Olkin and Liu (2003) Olkin, I. & Liu, R. (2003). A bivariate beta distribution. Statistics & Probability Letters, 62, 407–412.

- Pereira and Pericchi (1990) Pereira, C.A.B. & Pericchi, L.R. (1990). Analysis of diagnosability. Journal of the Royal Statistical Society Series C, Applied Statistics, 39, 189–204.

- Popper (1959) Popper, K.R. (1959). The Propensity Interpretation of Probability. The British Journal for the Philosophy of Science, 10, 25–42.

- Savage (1954) Savage, L.J. (1954). The Foundations of Statistics. New York, NY: Wiley.

- Singpurwalla (2001) Singpurwalla, N.D. (2001). Cracks in the empire of chance: flaws in the foundations of reliability. International Statistical Review, 10, 53–78.

- Singpurwalla (2006) Singpurwalla, N.D. (2006). Reliability and Risk: A Bayesian Perspective. New York, NY: Wiley.

- Singpurwalla (2009) Singpurwalla, N.D. (2009). The utility of reliability and survival. The Annals of Applied Statistics, 3, 1581–1596.

- Spizzichino (1993) Spizzichino, F. (1993). A unifying model for the optimal design of life-testing and burn-in In Reliability and Decision Making, (eds. R. Barlow, C. Clarotti, and F. Spizzichino), pp. 189–210. London, UK: Chapman & Hall.

Appendix: Generalized Bivariate Beta: Closure Under Complementation

For , Arnold and Ng (2011) introduced the distribution discussed below. However, its closure properties and their relevance for inference in diagnostics were not explored. This section pertains to a discussion of these matters, and in a sense is a contribution to the applied probability aspect of this paper.

We start our discussion about closure by noting that since , will also be ; thus the univariate beta is closed under complementation. However, the univariate beta distribution of the first kind is not closed under reciprocation, because , and has what is known as an inverted beta distribution (or a beta distribution of the second kind) with parameter , hence-forth, denote . In general, the beta distribution of the second kind with parameters and is the distribution of the ratio of two independent gamma distributed random variables with shape parameters and , respectively, and a common scale parameter. Contrast the beta distribution of the second kind with the beta distribution of the first kind which is the ratio of two dependent gamma distributed random variables. The probability density at of a beta distribution of the second kind with parameters and is

here , is the gamma function. Note that since , , and that . Thus, the beta distribution of the second kind is closed under reciprocation. The above observations enable us to argue that the distribution is closed under complementation. But before doing so, it is helpful to give a summarized perspective on the closure properties of the multivariate beta distribution.

Since the marginal distributions of the and the family of bivariate beta distributions are a univariate beta, we say that the and the family of distributions are closed under marginal complementation. The same is also true of the joint distribution of , the bivariate complementation of , henceforth denoted . By complementation of we mean a consideration of . A comparison of the joint probability density functions of the and the distributions shows that they are different. Similarly, with a comparison of the joint probability density functions of and , and and . Such comparisons lead to the claim that the , , and the are not closed under coordinate-wise and joint complementation. Since the family of distributions encompasses the family, we claim that like the family, the is not closed under coordinate-wise and joint complementation.

For , the construction begins with random variables and , where

Since and are ratios of independent gamma distributed random variables, their distributions are beta distributions of the second kind, but since and share common elements, their joint distribution is a bivariate beta distribution of the second kind, denoted or simply . It is easy to see that this bivariate beta distribution of the second kind is closed under coordinate-wise and joint complementation. That is,

If we now let

then the distribution of implies that the joint distribution of is a bivariate beta, namely, . This distribution is indeed the generalized bivariate beta which titles this section.

It is easy to see that the marginal distributions of and are beta distributions. The distribution includes the , the , and the as special cases, each encompassing the non-negative, the non-positive, and the non-negative dependencies, respectively. This is because the family is obtained by setting , the family by setting , or by setting , and the family by setting .

To see why the family is closed under coordinate-wise complementation, let , and note that

and this has a bivariate beta distribution because, as noted before, , and the result that if , then . Using an analogous argument considering , we can see that is also a bivariate beta, and so we may claim that the distribution is closed under both coordinate-wise and joint complementation.

We, therefore, have at hand an eight-parameter family of bivariate beta distributions, abbreviated , that is closed under complementation and which encompasses both positive and negative dependence (i.e., takes correlations in the full range ). It includes the , the and the distributions as special cases, and serves as a family of prior distributions for adversarial and amiable inference in a Bayesian setting. Its constructive definition based on ratios of independent gamma variates facilitates ease of simulation. Although the model encompasses the model and the other bivariate beta models, it may be criticized on grounds of parsimony.

Despite the fact that the family of distributions has not been used by us in the context of inference in diagnostics, the inclusion of this Appendix, which can be seen as a stand alone piece, is for methodological completeness.