Chebyshev Reduced Basis Function applied to Option Valuation. ††thanks: Research supported by Spanish MINECO under grants MTM2013-42538-P and MTM2016-78995-P. Both authors acknowledge the helpful comments of Michèle Breton and Peter Christoffersen.

Abstract

We present a numerical method for the frequent pricing of financial derivatives that depends on a large number of variables. The method is based on the construction of a polynomial basis to interpolate the value function of the problem by means of a hierarchical orthogonalization process that allows to reduce the number of degrees of freedom needed to have an accurate representation of the value function. In the paper we consider, as an example, a GARCH model that depends on eight parameters and show that a very large number of contracts for different maturities and asset and parameters values can be valued in a small computational time with the proposed procedure. In particular the method is applied to the problem of model calibration. The method is easily generalizable to be used with other models or problems.

Keywords: Derivative pricing, multidimensional interpolation, Chebyshev polynomials, Reduced basis functions.

1 Introduction

This paper concerns the design of a Reduced basis function approach to mitigate the impact of the “Curse of Dimensionality” which appears when we deal with multidimensional interpolation, in particular, when we price financial derivatives employing multivariable models, like GARCH, or whose price may depend on multiple assets which follow different stochastic processes.

Since the market prices change almost constantly, thousands of derivative prices have to be recomputed very fast, hence numerical techniques that allow fast evaluation of multidimensional models are of interest.

Several techniques can be found in the literature to solve multidimensional option pricing problems. For example, Monte Carlo methods are very popular since they are straightforward to implement and handle multiple dimensions, although their convergence rates tend to be slow. Several approaches, like variance reduction techniques can be employed to increase their velocity (see [17] or [18]). Lately, PDE methods have also been employed in financial problems (see, for example, [6], [16], [24] or [27]) due to their faster speed of convergence with respect to Monte Carlo methods. In [7], an adaptive sparse grid algorithm using the finite element method is employed for the solution of the Black-Scholes equation for option pricing. A Legendre series expansion of the density function is employed in [22] for option valuation. In [2], a proper orthogonal decomposition and non negative matrix factorization is employed to make pricing much faster within a given model parameter variation range. A general review of financial problems or models, numerical techniques and software tools can be found in [12].

The main objective of this work is to reduce the computing time and storing costs which may appear in multidimensional models. The proposed method has two differentiated steps. In the first one (off-line computation), an approximation to the option pricing function is computed through a polynomial Reduced Basis method. This step usually is expensive in terms of computational cost, but it is performed only once. In the second step (on-line computation), we employ the polynomial constructed in the previous step to price a large number of contracts or calibrate model parameters. In this second step, the big gain in computational time arises because, as the polynomial does not need to be recomputed, it can be used as many times as needed.

One way to compute numerical approximations of the value of multidimensional functions is to compute the function value in a given set of nodes and to use polynomial interpolation. Unfortunately, for a high number of dimensions, the memory requirements to store the interpolant and the computational time required for each evaluation grow exponentially. This effect is known as the “Curse of Dimensionality”.

A common approach to reduce the curse of dimensionality is to search the dimensions where increasing the number of interpolation nodes would reduce faster the interpolation error. The method that we propose here approaches, someway, the problem from the other side. Instead on focusing on the construction of the interpolation polynomial, what we propose is to obtain, from the interpolant, a new reduced polynomial which gives similar accuracy as the original one but requiring much less computational effort.

In order to fix ideas we present the method with Chebyshev interpolation although the techniques in this paper are easily generalizable. The properties of Chebyshev polynomials, [29], enable us to use time-competitive and accurate fast fourier transform methods for computing the coefficients, evaluation and differentiation of the polynomials.

In first place, we show how to build the interpolant and we design a very efficient evaluation algorithm which allows to compute the polynomial value for different values of each of the parameters simultaneously, something that will be referred as tensorial evaluation. Afterwards, for a fixed interpolant, we propose a reduced basis approach employing a Hierarchical orthonormalization procedure along each one of the dimensions. This procedure rewrites the interpolant in function of a set of orthonormal function basis which are ordered hierarchically depending on the amount of information of the interpolant that they posses. Afterwards, fixed a tolerance level for the error with respect to the interpolant, we retain the minimum number of functions in the basis such that this tolerance is fulfilled. Furthermore, since the function basis are written in function of Chebyshev polynomials, the evaluation algorithm previously designed can be adapted to the new approximation. The result is a polynomial which approximates the multidimensional function and requires much less memory capacity and computational time for evaluation.

The paper is organized as follows. In Section 2, a fast tensorial Chebyshev polynomial interpolation is developed. The precision is obtained increasing the number of interpolation nodes, which leads to the storage-cost problem. In Section 3 the reduced approximation is presented. Finally, in Section 4 we perform numerical experiments with the different techniques developed over a multidimensional model employed in pricing financial derivatives.

All the algorithms presented in this work have been implemented in Matlab vR2010a. All the numerical experiments have been realized in a personal computer with an Intel(R) Core(TM) i3 CPU , 540 @ 3.07GHz, memory RAM of 4,00 GB and a 64-bits operative system.

2 Polynomial Interpolation

We propose a Chebyshev polynomial interpolation procedure for multidimensional models. The interpolation is done using Chebyshev polynomials and nodes in the intervals where the parameters are defined.

Definition 2.1.

Let us define

| (1) |

where .

It is well known, [29], that this function is a polynomial of degree , called the Chebyshev polynomial of degree n.

Definition 2.2.

Let . The Chebyshev nodes in interval correspond to the extrema of and they are given by:

| (2) |

We also define the Chebyshev nodes in interval , where

| (3) |

Here we present just the definitions that are needed for the proposed method. The practical computation of the coefficients of the interpolant is postponed to Subsection 2.1.

Definition 2.3.

Let and be a continuous function defined in .

For , we define the function as

where

| (4) |

For , we define

| (5) |

For , let be the Chebyshev nodes in and be the Chebyshev nodes in .

We use the notation and .

Let be the n-dimensional interpolant of function at the Chebyshev nodes , i.e. the polynomial which satisfies

Polynomial is given by

| (6) |

where

Let and suppose that we need a numerical approximation for several different values in each of the variables. Let be a set of values such that for ,

| (7) |

where we note that the number of points in is .

The numerical approximation is computed with the polynomial , where the relation between and is given by formula (4). The algorithms presented in Subsection 2.2 allow us to evaluate the interpolation polynomial in a set of points like very fast, something that from now on will be referred as tensorial evaluation. This is achieved through a suitable defined multidimensional array operation and the employment of efficient algorithms described in Subsection 2.2.

2.1 Computation of the interpolating polynomial.

Univariate case

Let be a continuous function defined in and suppose that we want to compute the Chebyshev interpolant

It must hold that

where are the Chebyshev nodes in and .

There are several efficient algorithms that allow us to obtain the coefficients . For the univariate case, we employ the algorithm presented in [8].

Algorithm C1v:

1. Construct

2. Compute

3.

Multivariate case

Let and be as given in Definition 2.3 and suppose that we want to construct the interpolant

Definition 2.4.

Let be an array of dimension . We denote the vector

where .

Let be an array of dimension . We define the permutation operator such that if:

we have that and

Suppose that we have already computed the function value at the Chebyshev nodes, i.e.,

which are stored in an array such that

The coefficients of the interpolant are obtained through the following algorithm.

Algorithm Cnv:

1. .

2. For i=1 to

2.1. .

2.2. For to , for to , …, for to

2.3. .

3. .

We remark that the FFT routine in Matlab admits multidimensional evaluation so that, step 2.2 of the previous algorithm can be efficiently computed without using loops.

2.2 Tensorial Evaluation and Differentiation of the interpolation polynomial.

Definition 2.5.

Let and be two arrays, and respectively, and such that .

We define the tensorial array operation , as the array given by:

| (8) |

where is the usual product of matrix times a vector and is the permutation operator introduced in Definition 2.4.

It is easy to check that .

Concerning the implementation in Matlab of the tensorial array operation,

where permute is a standard procedure implemented in Matlab.

The algorithm multiprod, implemented by Paolo de Leva and available in Mathworks (see [10]), makes the required tensorial operation simultaneously in all variables in a very efficient way.

Suppose now that we have a polynomial

We want to evaluate the polynomial in a finite set of points , which was defined in (7).

For computational reasons, we impose that By default, multiprod algorithm does not recognize arrays of -dimension and collapses to -dimension. Since consists of multiprod and a permutation, if , a wrong dimension will be permuted in the evaluation algorithm.

The evaluation algorithm has two steps.

1. Evaluate the Chebyshev polynomials:

We use the recurrence property of Chebyshev polynomials:

that with the number of interpolation points involved in the option pricing problem works fairly well.

From the definition of (see (7)), the possible values of each variable are a finite number. We employ the notation to denote the corresponding values in after the change of variables (4). Using the recurrence property, we compute

and we store each result in a two dimensional array.

2. Evaluate the rest of the polynomial.

The evaluation of the polynomial for the whole set of points can be done at once using the tensorial array operation.

The polynomial coefficients are stored in a -dimensional array .

and we compute

| (9) |

where the result will be an -dimensional array which contains the evaluation of the interpolant in all the points of set .

We remark that the previous definition must not be seen as a product with the usual properties. The order of the parenthesis has to be strictly followed in order to be consistent with the dimensions.

Polynomial differentiation:

Sometimes, we may also need to compute an approximation to the derivative of the multidimensional function. For example, if we want to find the values of the parameters of the model that approximate best to a given a set of data, in the sense of a least square minimization.

Note that if and we have interpolated function

where

we can approximate, if function is regular enough (see [8]),

where (see [8, (2.4.22)]) for :

This implies that the coefficients of the derivatives of the polynomials need to be computed each time or stored in memory. Both options do not fit with the objective of this work.

If the coefficients are computed each time they are needed, that increases the total time cost. On the other hand, there is a memory storage problem in the polynomial interpolation technique. To store the coefficients of the derivative means to almost double the memory requirements of the method.

For these reasons, we prefer to employ, if possible, a fast computing way to approximate the derivative, which does not require any more memory storage. We approximate the derivative by finite differences as follows

where .

3 Reduced Basis Approach

The objective of this Section is to build a new polynomial which gives comparable accuracy as the interpolant built in the previous Section, but which has less memory requirements.

Suppose we are given a high degree polynomial . The objective is to construct from it a smaller polynomial, in memory terms but not in degree, which globally values as well as the original one.

The method we are going to develop could be exported to other kinds of polynomials, but since our evaluation algorithms are designed for the Chebyshev ones, the construction is focused to take advantage of their properties. It is also general enough to be applied to any n-variables polynomial.

3.1 Hierarchical orthonormalization

Suppose we have a polynomial

| (10) |

where denotes the degree in each one of the variables.

Our objective is, given a set of points and , to construct a polynomial from , such that

| (11) |

where polynomial has the smallest size (in memory terms) compatible with (11).

Although another set of points could be chosen, since we are continuing the work of the previous Section, i.e. , the interpolation polynomial of a certain function , the natural set of points will be the set of points used in the construction of the interpolation polynomial, i.e., the Chebyshev nodes .

Our approach is to use a basis of Orthonormal functions that are hierarchically chosen. All polynomials that appear in the procedure we are going to construct must be written in function of Chebyshev polynomials. Hence, it is natural to employ the weighted norm associated with them and to exploit all the related properties which simplify the calculus.

Definition 3.1.

Given two functions and , where , we define the weighted scalar product as:

We denote by the norm induced by this scalar product.

The following result is well known [29].

Lemma 3.1.

The Chebyshev polynomials, , are orthogonal with respect to the scalar product . Furthermore, if is a polynomial of degree less or equal to then

where are the Chebyshev nodes in [-1,1]. (Gauss-Lobato-Chebyshev cuadrature)

Definition 3.2.

Let and be two functions such that . We define the function

For simplicity in the notation, we denote .

The algorithm of the hierarchical Gram-Schmidt procedure has steps if the polynomial has variables.

Hierarchical orthonormalization procedure:

Let us consider . For simplicity assume that . Let us consider also a set of points .

Step 1:

Let denote the Chebyshev nodes in and define . It is easy to check that we can rewrite as:

where is a -degree polynomial such that for it holds that:

For , we set and and compute:

We define and .

For , we set and and compute

We define and .

We proceed iteratively, so that we eventually obtain a set of orthonormal polynomials such that

where .

We approximate now

where is the first index such that

| (12) |

Let us observe that the first polynomials were those that, in the sense of (12), had more “information” about . Indeed, usually with very few terms (depending on the variable), a good approximation to the original polynomial can be achieved.

Furthermore, the amount of storage required is considerably reduced.

Step 2:

Each of the is a variable polynomial, and we can proceed the same way as we did in Step 1.

For each of the , let be the Chebyshev nodes in and

where .

For , we set and and compute:

We define and .

Now, for , we set and . Again we compute

We define and .

We proceed iteratively, at the end we will obtain

where .

We will approximate by

where is the first index such that

| (13) |

We proceed iteratively until completing Step n-1 where we stop. We will have arrived to a new polynomial that can be written

Note that is the number of function basis used in each variable. Note also that, in general, the degree of is still .

We remark that the last value of is because the last variable remains untouched. An improved result (in memory terms) can be obtained if the variables of polynomial are reordered before the Reduced Basis procedure and is the smallest among the .

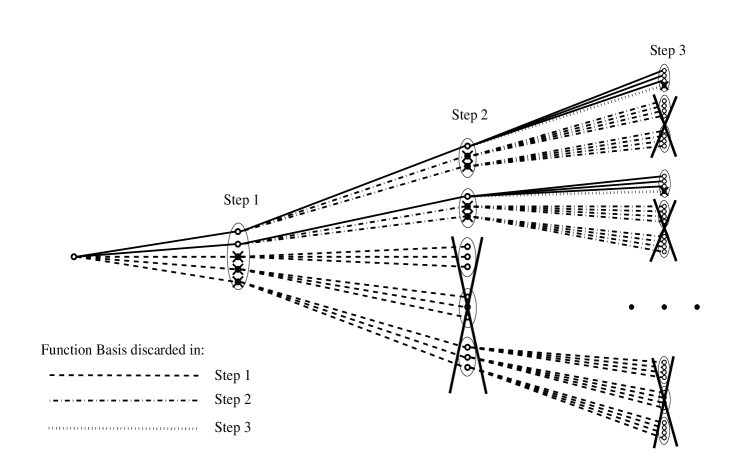

Visually, we can check the big memory saving. Figure 1 shows an example of the first three steps of the algorithm if .

The tree represents the orthonormal decomposition in each of the variables and the function basis that are discarded in each step: 3 function basis (Step 1-dashed lines), 2 function basis (Step 2-dash-dot lines) and 1 function basis (Step 3-dot lines). The proportion of the tree that has been discarded represents approximately the memory savings with respect to the original polynomial obtained by our method.

The last step is to adequate the algorithms for tensorial evaluation to .

3.2 Tensorial evaluation for Reduced Basis

Polynomial is rewritten for tensorial evaluation as

where we denote .

Each polynomial is written in function of the Chebyshev polynomials:

| (14) | ||||||

and is kept in memory storing the coefficient of the previous polynomials in different multidimensional arrays.

Suppose that we want to evaluate the polynomial in the finite set of points (see (7)).

We employ the notation , whose values are obtained from set after the change of variable given by (4).

The evaluation of polynomials , …, , when they are given by (14) can be done efficiently using the first algorithm from Subsection 2.2.

Thus, suppose that we have evaluated them and stored the results in arrays:

Definition 3.3.

Let , be two arrays such that and .

We define the special tensorial array operation as:

| (15) | ||||

where denotes the usual product of matrix times a vector.

From Definition 3.3, observe that in (15) we are using the usual matrix times vector multiplication. It is straightforward that .

multiprod command is employed again to implement the special tensorial array operation.

The tensorial evaluation for the reduced basis polynomial can be written as:

where again the order fixed by the parenthesis must be strictly followed in order to be consistent with the dimensions of the arrays.

The result will be a -dimensional array which contains the evaluation of the polynomial with all the possible combinations of the given values to each of the variables.

3.3 Comments about the Reduced Basis method.

Although in the numerical experiments we will see that the results are quite good in the sense of reduction of memory requirements and computing time, we must point that the procedure presented could be improved.

We remark that is not optimal in various senses. First of all, the hierarchical criteria to select the function basis is not necessarily optimal. For example, there might exist a combination of several function basis that give a less overall error than the ones chosen by our criterium. The selection criterium that we employ is fast because, when we have to order hierarchically the function basis in each step, we only need to reevaluate the function basis that have not already been ordered.

Another factor that could be improved is the criterium for truncation. We can orthonormally decompose the whole polynomial hierarchically

and notice that we can independently truncate one branch of the tree or another. For example:

or

Our procedure does not maximize memory savings over the whole polynomial. A method which maximizes the memory savings versus the deterioration of the error when we truncate function basis of one or other variable could be designed.

4 Numerical Results

We are now going to apply the techniques developed in Sections 2 and 3 to a multidimensional model employed in option pricing.

The outline of the Section is as follows. First, we will make a brief introduction about financial options and pricing models. Afterwards, we will build an interpolation polynomial of a particular pricing function and apply the Reduced Basis approach. Performance analysis when we employ both numerical approximations will be performed.

4.1 Option Pricing and GARCH models

An European Call Option is a financial instrument that gives the buyer the right, but not the obligation, to buy a stock or asset, at a fixed future date (maturity), and at a fixed price (strike or exercise price). The seller will have the obligation, if the buyer exercises his/her right, to sell the stock at the exercise price.

The stock is usually modelled as an stochastic process and empirical analysis show that the volatility of the process does not remain constant in time. ARCH models (AutoRegressive Conditional Heterodastic) introduced by Engle in [15] are a kind of stochastic processes in which recent past gives information about future variance. Several ARCH models have been proposed along the years, trying to capture some of the empirically observed stock properties. The objective of this work is not to give a deep review of the ARCH literature, and we refer to [4], [5], [9], [21] and references therein. Nevertheless, we point that ARCH models are broadly used in option pricing. [6], [14], [19], [28] and [30] are just a few examples where option prices are obtained through ARCH models.

In the present work, we are going to apply the techniques that we have developed to price options with the NGARCH(1,1) model. For pricing options, the dynamics of the stock in the risk-free measure of the NGARCH(1,1) model [11], [23] are,

| (16) |

where denotes the stock price, is the variance of the stock, is the risk-free rate, are the GARCH model parameters and is a normally distributed random variable with mean 0 and variance 1.

The dynamics in the Risk-free measure allow us to compute the European option price as:

| (17) |

which, taking into account the model parameters, is an 8-variable function.

For this model, there is no known closed form solution and several numerical methods can be employed, being Monte-Carlo based methods ([13], [30]), Lattice methods ([25], [28]), Finite Elements ([1]) or Spectral methods ([6]) some of them.

The principal drawback of GARCH models is their computational cost. It will depend on the numerical method employed, but all the ones mentioned (Monte-Carlo, Lattice, Spectral…) require several seconds to compute option prices and several minutes to estimate parameter values. This can result in an unpractical procedure, since option prices change almost continuously.

In this work, the numerical method employed for computing the option prices in the Chebyshev nodes will be the spectral method developed in [6] and will be referred as B-F method. This numerical method gives enough precision with few grid points, and the employment of FFT techniques makes it a low-time consuming method.

Fixed an enough precision for the B-F method, we assume for the rest of the work that the option price obtained with this method is the reference option price. The construction of the interpolating polynomial and the error analysis will be carried referencing to the values obtained with it.

4.2 Numerical analysis of Interpolation

First, we fix the intervals in which the interpolant of the option price will be constructed. The NGARCH(1,1) model is linear in the relation , so strike is fixed at . The rest of variables are defined as follows:

where these intervals are chosen because they cover usual parameter values of the model observed in the literature (see, for example, [9], [14] or [30]).

Although different number of nodes can be considered for each variable, for simplicity, consider .

We are going to carry out a standard error analysis doubling the number of nodes . We remark that the number of interpolation points of variable is and the storage cost of the polynomials is .

Once fixed , we compute the Chebyshev nodes with formula (2). We compute the function values with B-F method and construct with the algorithms developed in Subsection 2.1.

Independently, we have to build a control sample which allows us to measure how well the interpolation polynomial prices options in the domain . We have chosen a set uniformly defined over .

Definition 4.1.

For each variable and for a given we define

and the set of points

This set of equally spaced points will be used to build a control sample. Points that correspond to are not included because they always correspond to Chebyshev nodes. will denote the set of option prices for all the possible combinations of values in sets , i.e.

computed with B-F method.

We compute and numerate its elements. Let be the contract price of and be the contract price evaluated with polynomial .

We define

For the numerical examples, we have built Sample . The number of elements of this sample is .

Table 1 shows, for , the memory storage (bytes) requirements of , the computing time (seconds) of computing Sample with and the .

| Storage | Computing time (seconds) | ||

In Table 1 we can also check that the computing time of and is fairly good, but it blows to 91 seconds in the case of . Although this time might not seem too high for computing contracts, it is unacceptable for practical applications. In the markets, the stock price might have changed a few times before we have finished the computation, making the results worthless.

The reason why the computing time has increased so much is due to the “Curse of dimensionality”. We remark that is above the operational limit of the Matlab/computer employed in the analysis to be stored in just one single array. Although the storage problem can be handled, splitting the polynomial in several parts and loading/discarding the needed data, unfortunately, in velocity terms, this implies a large increment of computational time.

Concerning , let denote the 13 Chebyshev nodes in interval . For each value of we build the 7-variable interpolation polynomial for the rest of the variables. This way, we have polynomial stored as 13 smaller polynomials which can be handled.

In our example, the 91 seconds are mostly due to several uses of the function load when we call each of the 7-variable smaller polynomials.

We mention that if the polynomial was even bigger, the splitting procedure can be extended to other variables, so storage is not an unsolvable problem. Nevertheless, it worsens the computing time because it implies that we need to load data from the memory very frequently.

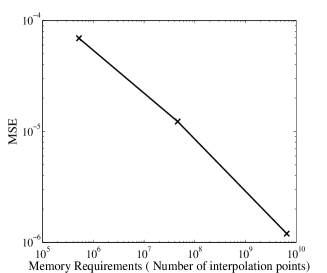

Concerning the error of the interpolation polynomials, Figure 2 shows the log-log of the Memory Storage versus the Mean Square Error.

The slope of the regression line in Figure 2 is . We have a good error behaviour, achieving a precision of with . If more precision is required, we can build bigger interpolation polynomials, which can be handled thanks to the splitting technique that we previously described.

4.3 Numerical analysis of Reduced Basis.

We now apply the Reduced Basis procedure developed in Section 3 to polynomial built in Subsection 4.2.

The set of points employed in the Hierarchical procedure will be the set of interpolation points employed in the construction of the interpolation polynomial , i.e. the Chebyshev nodes .

We also want to know how the new polynomial computes option prices over the whole domain . In order to check this, we employ ( contracts) defined in Subsection 4.2, whose points do not correspond to those of and are equally distributed over .

In Table 2 we study the numerical results when just Step 1 of the algorithm of the Hierarchical orthonormalization is applied. Once we have decomposed

for , we can check the performance of the method both in Sample and in .

In Table 2 are represented the number of function bases retained , the total storage cost in each case and the Mean Square Error when they are employed to compute the option prices of Sample and of .

| Function Basis | Storage (bytes) | ||

| 1 | |||

| 2 | |||

| 3 | |||

| 4 | |||

| 5 | |||

| 6 | |||

| 7 | |||

| 8 | |||

| 9 | |||

| 10 | |||

| 11 | |||

| 12 | |||

| 13 | |||

| 0 |

The global error is represented by . Note that with just 5 or 6 function bases for the first variable, we obtain a polynomial which has comparable accuracy as but which requires half the storage cost.

We run now the Hierarchical orthonormalization algorithm completely (Steps 1-7). We fix three different values of the parameter , where is the maximum Mean Square Error allowed when we evaluate Sample with the polynomials obtained from the procedure.

In Table 3, we include the memory requirements of each polynomial and the error committed when they are employed to compute the contracts of .

| MSE() | Storage (bytes) | Memory Savings | ||

| % | ||||

| % | ||||

| % |

Table 3 shows that with the Reduced Bases approach we obtain much smaller polynomials (in memory terms) which give an overall error of the same order as . We remark that, as expected, if , the error committed when evaluating converges to , the interpolation error of .

Concerning the computing time, consider the sets of points: 1 contract (one value for each variable), 210 contracts (7 different stock prices, 6 volatilities, 5 maturities) and (1679616 contracts).

We remark that evaluate would be equivalent to price options in the real market for several stocks with different parameter values.

In Table 4, we show the computing time of evaluating these sets of contracts with B-F method, the interpolation polynomial and different polynomials constructed from with the Reduced Bases approach.

| 1 contract | 210 contracts | () | |

| B-F method | s | s | s |

| s | s | s | |

| s | s | s | |

| s | s | s | |

| s | s | s |

In Table 4, we can see that B-F method needs the same time for computing 1 or 210 contracts (because it admits tensorial evaluation for and ). For computing , B-F method needs to be evaluated for each different value of , i.e. 7776 different evaluations of 41 seconds each.

requires the same computing time in the three examples because, as it was mentioned in Subsection 4.2, the polynomial is too big and it has to be stored in different parts. The computing time is due to several employments of function load.

With the polynomials obtained from the Reduced Bases, we have retrieved the tensorial evaluation velocity achieved when we were working with the polynomials , but with more precision (compare with Table 1).

Concerning the computing time of the In the Sample analysis (a least square search), we point out that while with the usual methods (Monte-Carlo, Lattice, Spectral) it takes several minutes to estimate the parameters of one negotiation day , this can be done in a few seconds with polynomials .

4.4 Model Calibration.

For finishing the numerical analysis, we check how this technique performs when we want to apply it to calibrate model parameters or predict the price of future European Option contracts.

The experiment has two parts. In the first one, given a set of European Call contracts that are being traded, we want to calibrate the model (In). Our objective, is to find the parameter values of the GARCH model that give the minimum mean square error (MSE) between the theoretical option prices and the traded ones. Therefore, our objective is to find, at a moment , the parameter values that minimize the function

| (18) |

where denotes the amount of contracts negotiated at and for each contract , is the market price and is the model’s price. The can be taken, for example, as the constant risk-free rate corresponding to the US bond negotiated at .

Once we have calibrated the model, we can employ the parameters obtained to predict future option prices (Out). In the market, stock prices change almost constantly. Furthermore, new contracts with different maturities and/or strikes, which where not traded previously, can be negotiated. Assuming that the rest of the model parameters have not changed, we will study how well the polynomial approximation predicts the contract prices for the new stock prices, strikes or maturities and we compare the results with the prices that were given by the market to those contracts.

The real option prices traded in the market are not driven by a discrete NGARCH model. There are many factors which affect the option prices and NGARCH model is just an approximation to them. In order to generate the sets (estimation and prediction) of artificial Option prices which play the role of “market” prices, we employ the continuous Stochastic Volatilty model developed by Heston (see [20]) given by

| (19) |

in the risk-neutral measure and where parameter denotes the instant correlation between processes and (see [20]).

This way, we are inducing a noise or error, since the discrete NGARCH model does not mimic completely the continuous SV model, neither in the estimation nor in the prediction. The sets of contracts that we employ as market contracts are computed with SV model.

We remark that our objective is not to study how well does NGARCH approximates SV model. Our objective is to compare the results in the estimation and prediction of the NGARCH model (B-F method) with the results of the interpolation polynomial and the polynomials obtained in the Reduced Basis approximation , and .

We fix the risk free rate . The risk-free rate can be considered as an observable data, for example, it can be obtained as the constant interest rate of the US-Bond Treasury Bond. We also fix values for the set which corresponds to the parameter values of SV model.

We compute the “market” option prices with SV model for a strike , stock prices and maturities days. The market usually trades contracts for different strikes, but we recall that the NGARCH model was linear in the relation so it is equivalent to fix the strike and compute option prices for different stock prices.

Table 5 represents the estimation of the parameter values with B-F and each of the polynomials.

| B-F | |||||

The number of contracts in the sample is 264. As we can see in Table 5, the numerical errors which raise from the interpolation or the Reduced Basis technique result in different parameter estimations, more observable in the values of . Nevertheless, note that the values obtained for , and are quite close, resulting probably in very close stochastic processes dynamics (maturities grow up to almost one year). Value is quite small, and its influence in the option price might be very small, being a more difficult parameter to estimate exactly.

Now let us check the errors in the estimation. Table 6 shows the maximum/mean contract prices and the highest/mean absolute errors committed in the estimation.

| Price | Error B-F | Error | Error | Error | Error | |

| Max | ||||||

| Mean |

We remark that there are several different errors in Table 6. The first one, the error labeled , is the error of the adequacy of the model. This error appears because we are approximating the continuous SV model with the discrete NGARCH model. Indeed, the literature shows that if we had employed real market data, this error would have been one or two orders of magnitude bigger.

The second error in Table 6 is the difference between column with respect to , which is the interpolation error. This difference can be made as small as we want just increasing the number of interpolation points (see Section 2).

The third error is the difference between columns , , with respect to . This difference comes from the Reduced Basis approach and can be made as small as we want just reducing the value (see (11)).

Now, let us try to predict future option prices (Out). Suppose that the stock price and maturities have changed. Let and days. We assume that the rest of the market parameter values have not changed. With the parameters estimated in Table 5 we compute the new option prices with each of the methods.

On the other side, we compute the exact option prices with the SV model and the parameter values and compare with the predictions. The errors with respect to the exact option prices are summarized in Table 7.

| Price | Error B-F | Error | Error | Error | Error | |

| Max | ||||||

| Mean |

If we compare with Table 6, we can check that the errors committed in the prediction are of the same magnitude with all the numerical methods. We also remark that the experiment that we have realized can be seen as a consistency analysis. Although the parameters obtained with each of the polynomials are slightly different (see Table 5), the prices obtained in the prediction are fairly closed to the exact ones. Therefore, the Reduced Basis method can be successfully applied to estimate model parameters/predict option prices. Furthermore, while we need several minutes to estimate/predict with B-F or , we can do the same computations in a few seconds with polynomials , or .

We remark again that our objective is not to study the approximation of the NGARCH model to the SV model, but to compare the results in the estimation and prediction of the NGARCH model (B-F method) with the results of the interpolation polynomial and the polynomials obtained in the Reduced Basis approximation , and . The experiment was repeated for several times with different values for of the SV model, both picked by the authors or parameters employed/estimated in [20] and [26]. Obviously, in the estimation we obtained different values for the parameters and the errors were slightly different, but the behaviour between the different errors ( vs B-F, vs ,…) remained the same.

5 Concluding remarks

In this paper, we have proposed a Chebyshev Reduced Basis Function method in order to deal with the “Curse of Dimensionality” which appears when we deal with multidimensional interpolation. The main objective of the work was to reduce the computing time and storing costs which appear in multidimensional models. We have also applied this technique to the practical problem of the real-time option pricing / model calibration problem in financial economics with satisfactory results.

Further work may include a formal comparison between the work presented and other numerical methods employed in option pricing. This is not a straightforward task. First of all (see [9], for example), it is not easy to determine which model (GARCH, SV, Jumps,…) may give the best results for option pricing. Each model employs a different number of dimensions, it may lead to different numerical problems and, probably, several numerical methods have been proposed to approximate option prices.

Other line of work, which we believe it might be of high interest, is to study if the ideas presented in this work could be combined someway with other numerical techniques which can be found in the literature.

References

- [1] Achdou Y., Pironneau O., Finite Element Method for Option Pricing, Université Pierre et Marie Curie, 2007.

- [2] Balajewicz M., Toivanen J., Reduced Order Models for Pricing American Options under Stochastic Volatility and Jump-diffusion Models, Procedia Computer Science, 80, 734-743, 2016.

- [3] Black F., Scholes M., The Pricing of Options and Corporate Liabilities, The Journal of Political Economy, 81, 637-654, 1973.

- [4] Bollerslev T., Generalized Autoregressive Conditional Heteroskedasticity, Journal of Econometrics, 31, 307-327, 1986.

- [5] Bollerslev T., Engle R., Nelson D., Arch Models, Handbook of Econometrics (IV), Elsevier, 2959-3038, 1994.

- [6] Breton M., de Frutos J., Option Pricing Under Garch Processes Using PDE Methods, Informs, Operations Research, 58, 1148-1157, 2010.

- [7] Bungartz H.J., Heinecke A., Pflüger D., Schraufstetter S., Option pricing with a direct adaptive sparse grid approach, Journal of Computational and Applied Mathematics, 236, 3741-3750, 2012.

- [8] Canuto C., Hussaini M.Y., Quarteroni A. and Zang Th.A., Spectral Methods. Fundamentals in single domains, Springer, Berlin, 2006.

- [9] Christoffersen P., Jacobs K., Which GARCH Model for Option Valuation?, Management Science, 50, 1204-1221, 2004.

- [10] de Leva P., Multiprod algorithm, www.mathworks.com/matlabcentral/ fileexchange/8773-multiple-matrix-multiplications–with-array-expansion-enabled

- [11] Duan J.C., The Garch Option Pricing Model, Mathematical Finance, 5, 13-32, 1995.

- [12] Duan J.C., Gentle J.E. and Härdle W.(eds) Handbook of Computational Finance, Springer, 2012.

- [13] Duan J.C., Simonato, Empirical Martingale Simulation for Asset Prices, Management Science, 44, 1218-1233, 1998.

- [14] Duan J.C., Zhang H., Pricing Hang Seng Index options around the Asian financial crisis. A GARCH approach, Journal of Banking & Finance, 25, 1989-2014, 2001.

- [15] Engle R., Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation, Econometrica, 50, 987-1007, 1982.

- [16] de Frutos J., Gatón V., A spectral method for an Optimal Investment problem with transaction costs under Potential Utility, Journal of Computational and Applied Mathematics, 319, 262-276, 2017.

- [17] Giles M.B., Multilevel Monte Carlo path simulation, Operations Research, 56, 607-617, 2008.

- [18] Glasserman P., Monte Carlo Methods in Financial Engineering, Springer, 2004.

- [19] Harrell F., Regression Modeling Strategies, Springer, 2001.

- [20] Heston S., A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options, The Review of Financial Studies, Volume 6, Issue 2, 327-343, 1993.

- [21] Higgins M.L., Bera A.K., A Class of Nonlinear ARCH Models, International Economic Review, 33, 137-158, 1992.

- [22] Hok J., Chan T.L., Option pricing with Legendre polynomials, Journal of Computational and Applied Mathematics, 322, 25-45, 2017.

- [23] Kallsen J., Taqqu M. Option pricing in ARCH-TYPE models, Mathematical Finance, 8, 13-26, 1998.

- [24] Linde G., Persson J., Von Sydow L., A highly accurate adaptive finite difference solver for the black-scholes equation, International Journal of Computer Mathematics 86, 2104-2121, 2009.

- [25] Lyuu Y.,Wu C., On accurate and Provably Efficient GARCH Option Pricing Algorithms, Quantitative Finance, 2, 181-198, 2005.

- [26] Papanicolaou A., Sircar R., A regime-switching Heston model for VIX and SP500 implied volatilities, Quantitative Finance, 14, 1811-1827, 2014.

- [27] Pironneau O., Hecht F., Mesh adaptation for the Black and Scholes equations, East West Journal of Numerical Mathematics 9, 15-25, 2000.

- [28] Ritchken P, Trevor R., Pricing Options under Generalized GARCH and Stochastic Volatility Processes, The Journal of Finance, 54, 377-402, 1999.

- [29] Rivlin T.J., Chebyshev Polynomials: From Approximation Theory to Algebra and Number Theory, Wiley, New York, MR1060735(92a:41016), 1990.

- [30] Stentoft L., Pricing American Options when the underlying asset follows GARCH processes, Journal of Empirical Finance, 12, 576-611, 2005.