Regression with Partially Observed Ranks on a Covariate:

Distribution-Guided Scores for Ranks

Abstract

This work is motivated by a hand-collected data set from one of the largest Internet portals in Korea. This data set records the top 30 most frequently discussed stocks on its on-line message board. The frequencies are considered to measure the attention paid by investors to individual stocks. The empirical goal of the data analysis is to investigate the effect of this attention on trading behavior. For this purpose, we regress the (next day) returns and the (partially) observed ranks of frequencies. In the regression, the ranks are transformed into scores, for which purpose the identity or linear scores are commonly used. In this paper, we propose a new class of scores (a score function) that is based on the moments of order statistics of a pre-decided random variable. The new score function, denoted by D-rank, is shown to be asymptotically optimal to maximize the correlation between the response and score, when the pre-decided random variable and true covariate are in the same location-scale family. In addition, the least-squares estimator using the D-rank consistently estimates the true correlation between the response and the covariate, and asymptotically approaches the normal distribution. We additionally propose a procedure for diagnosing a given score function (equivalently, the pre-decided random variable Z) and selecting one that is better suited to the data. We numerically demonstrate the advantage of using a correctly specified score function over that of the identity scores (or other misspecified scores) in estimating the correlation coefficient. Finally, we apply our proposal to test the effects of investors’ attention on their returns using the motivating data set.

Keywords: Concomitant variable; investors’ attention; linear regression; moments of order statistics; optimal scaling; partially observed ranks

1 Introduction

This paper is motivated by a hand-collected data set from Daum.net, the 2nd largest Internet portal in Korea. The Daum.net portal offers an on-line stock message board where investors can freely discuss specific stocks in which they might be interested. This portal also reports a ranked list of the top 30 stocks that are most frequently discussed by users on a daily basis. The data set was collected by the authors during the 537 trading days from October 4th, 2010, to November 23rd, 2012. Along with the rank data, we also collected financial data regarding individual companies from FnGuide (http://www.fnguide.com). These additional data include stock-day trading volumes classified in terms of different types of investors, stock prices, stock returns, and so on.

The purpose of analyzing the collected data is to investigate the shifts in stock returns caused by variations in investor attention. In finance, researchers are often interested in determining the motivations that drive buying and selling decisions in stock markets. It is commonly assumed that investors efficiently process relevant information in a timely manner, but in reality, it is nearly impossible to be efficient because of information overload. In particular, individual investors are often less sophisticated than are institutional investors and have a limited ability to process all relevant information. For this reason, individual investors may pay attention only to a limited amount of information, perhaps that which is relatively easy to access. The phenomenon of limited attention is a well-documented cognitive bias in the psychological literature (Kahneman, 1973; Camerer, 2003). This phenomenon affects the information-processing capacities of investors and thus may affect asset prices on the financial market. To empirically prove the effect of investor attention on stock returns, we regress the observed stock returns with respect to the partially observed ranks.

Regression on a (partially observed) rank covariate has not previously been extensively studied in the literature. A procedure that is commonly used in practice to address rank covariates is to (i) regroup the ranks into only a few groups (if the number of ranks is high) and (ii) treat the regrouped ranks as an ordinal categorical variable. Ordered categorical variables frequently arise in various applications and have been studied extensively in the literature. Score-based analysis is most commonly used for this purpose; see Hájek (1968), Hora and Conover (1984), Kimeldorf et al. (1992), Zheng, (2008), Gertheiss (2014) and the references therein. Thus, this typical two-step procedure for addressing a rank covariate is equivalent to defining a score function for the ranks. However, as in the case of ordinal categorical variables, such a score-based approach suffers from an inherent drawback related to the choice of the score function; different choices of scores may lead to conflicting conclusions in the analysis (Graubard and Korn, 1987; Ivanova and Berger, 2001; Senn, 2007). The recommendation for selecting the score function according to the literature is (i) to choose meaningful scores for the ordinal categorical variable based on domain knowledge of the data, (ii) to use equally spaced scores if scientifically plausible scores are not available (see Graubard and Korn (1987)), and (iii) to find a optimal scaling transformed scores that maximize the correlation with the responses while preserving the assumed characteristics of the ordinal values(Linting et al., 2007; Costantini et al., 2010; de Leeuw and Mair, 2009; Mair, and de Leeuw, 2010; Jacoby, 2016).

In this paper, we seek to provide an efficient tool for approach (i) described above, for the case in which some qualitative knowledge is available regarding the ranks or the ranking variable (the variable that is ranked). More specifically, we propose a new set of score functions, denoted by D-rank, and study their use in linear regression. The proposed score function is based on the moments of order statistics (MOS) of a pre-decided random variable . This score function has several interesting properties related with the regression model, if the pre-decided random variable is correctly specified as listed below. Here, the correct specification implies it is within the same location-scale family with the true (unobserved) covariate . First, the D-rank is asymptotically optimal in the sense that it maximizes the correlation between the response and score if the distribution of the D-rank is correctly specified. Second, the least-squares estimator using the D-rank consistently estimates the true correlation between the response and the covariate and asymptotically approaches the normal distribution. Finally, the residuals of the fitted regression allow us to diagnose the given score function (equivalently, the pre-decided random variable ) and to provide a tool for selecting a score function that is better suited to the data.

The remainder of this paper is organized as follows. In Section 2, we study the properties of the proposed D-rank. In this section, we show that the proposed D-rank is asymptotically optimal to maximize the correlation between the response and score. In addition, We also demonstrate the asymptotic equivalence between the proposed score function and the quantile function; the quantile function may provide a better illustration of the qualitative features of the score function. In Section 3, we apply the score function to estimate the regression coefficient of the linear model or, more precisely, to estimate the correlation coefficient between the response and the scoring variable . We prove that the least-squares estimator using the D-rank consistently estimates the correlation coefficient and is asymptotically normally distributed. In addition, we discuss the procedure for selecting an appropriate score function using the residuals. In Section 4, we numerically demonstrate that using the correctly specified score function significantly reduces the mean square error on the estimation of the correlation coefficient. In Section 5, we analyze the motivating data set to investigate the existence of the attention effect. Finally, in Section 6, we briefly summarize the paper and discuss the application of the proposed scores to regression using other auxiliary covariates.

2 Distribution-Guided Scores for Ranks (D-rank)

We consider a simple regression model in which only partial ranks of a covariate are observed. Specifically, suppose that is the complete set of observations, where is the variable of primary interest and is the covariate related to . For example, in our rank data from Daum.net, for , is a relevant outcome such as earning rate or trading volume, is the “unobserved” investors’ attention on the th company measured by the frequency of on-line discussions, and is the “observed” rank of among . We make certain assumptions regarding the distributions of and . We assume that the linear model of the relationship between and is

| (1) |

where the s are IID values from a distribution of mean and variance . The objective of this paper is the estimation and inference of (or the regression coefficient between and ) based on the observed data . To do it, we aim to define a good score function for the observed rank , and consider the regression of on , where is the response for .

The D-rank, we propose in this paper, is a set of the MOS of pre-decided random variable , which we assume is in the same location-scale family of the true covariate . To be specific, suppose that are independent and identically distributed (IID) copies of the random variable and that is the corresponding th-order statistic for . The D-rank defines the score of the rank as for .

We first show that the D-rank maximizes the sample correlation between and , , in asymptotic, among all increasing functions . Let and be the standardized scores (of and ) to make and . Let and be the collection of all increasing functions and , respectively.

Theorem 1.

Under the linear model (1), if is in the location-scale family of , the D-rank maximizes the limit of the sample correlation between and among :

| (2) |

where .

The proof of Theorem 1 is followed in Appendix.

Theorem 1 shows the asymptotic optimality of the D-rank for the regression in view of optimal scaling in the literature. The optimal scaling finds optimally transformed scores that explain mostly well the assumed statistical model. It arises in various contexts including Gifi classification of non-linear multivariate analysis(de Leeuw and Mair, 2009), the aspect (correlational and non-cprrelational aspects) of multivariable(Mair, and de Leeuw, 2010), and non-linear principal component analysis(Linting et al., 2007; Costantini et al., 2010). Here, we adopt the idea of the optimal scaling in Jacoby (2016), and find the transformation to maximize the correlation between the response and transformed scores. Theorem 1 above shows that the D-rank maximizes the correlation in asymptotic, if pre-determined distribution for the D-rank is correctly specified.

The proposed score is closely related to the quantile of the underlying distribution of . Let for and for be the cumulative distribution function (CDF) and the quantile function (QF), respectively, of . In the estimation of for , the th-order statistic is the -th percentile point of the empirical CDF, and thus, its expected value is approximately equal to . More specifically, given , , and , we can write

where and is the probability density function of , which is differentiable. We refer the reader to David (2003, Section 4.6) for the details of the relationship between the MOS and the quantiles.

Consideration of the QF may provide a better understanding of the qualitative features of the proposed score function. Suppose we expect the score function is convex in tail (for for a constant close to ); in other words, for . From the equivalence between the MOS and quantiles, it is known that the convexity of the scores is approximately equal to that of the quantile function . Furthermore, the convexity of for implies the following equivalent statements: (i) is concave in , (ii) or (iii) is decreasing in , all for .

3 Simple Linear Regression

In this section, we consider a simple regression model in which only partial ranks of a covariate are observed. Specifically, suppose that is the complete set of observations from the linear model (1), and is the rank of among . The rank of is indirectly measured by the frequency of on-line discussions of the th company.

In this paper, we consider the case in which the ranks are partially observed in the sense that we observe only that rather than , where is an arbitrary constant that is greater than . Finally, the observations are

We let for , and denote the above partially observed data by for notational simplicity.

The objective of this section is to identify a good estimator of (or the regression coefficient between and ) and to test versus or using the observed data .

3.1 Least-Squares Estimator

To estimate , we recall assumptions regarding the distributions of and . We assume that the linear model of the relationship between and is

where the s are IID values from a distribution of mean and variance . By ordering on the s, we have for

| (3) |

where and

| (4) | |||||

with

We are motivated by the identities (3) and (4) given above and propose the least-squares estimator

| (5) |

as an estimator of with , where, and are the empirical estimators of the mean and variance, respectively, of .

We claim that, if is drawn from a location-scale family generated by , then the least-squares estimator with in (5), that is calculated based on the partial observations , is consistent and asymptotically normally distributed with an appropriate scale, as shown in Theorem 2. Suppose that

where , and let , and be the limits of , and , respectively (under the assumption that they exist).

Theorem 2.

Under the assumption that is drawn from a distribution of a location-scale family with a finite variance, the distribution of converges to the normal distribution of mean and variance .

The proof of Theorem 2 is provided in the Appendix.

We conclude this section with two remarks regarding Theorem 2. First, in Theorem 2, from the tower property of the conditional expectation,

and when , the asymptotic variance of is larger than , which is the variance of the least-squares estimator in the case where is completely observed. Second, it is possible to test the hypothesis using the statistic which has an asymptotically normal distribution of mean and variance .

3.2 Residual Analysis

As in the classical linear model, the residuals can provide guidance for identifying a better model and score function. The residuals are defined as for . Statistical properties of the residuals, which are analogous to those in the classical linear model, are summarized as follows.

Theorem 3.

Under the assumptions of Theorem 2, the following statements are true for the residuals: (i) ; (ii)

(iii) ; and (iv) , where .

The proof of Theorem 3 requires only simple algebra and is thus omitted here. The theorem states that the residuals have mean and finite variance, and also states that they are uncorrelated with the scores and the predicted values . Thus, the residual plots, which are the plots of (i) versus , (ii) versus , and (iii) versus , have the same interpretations as those of the classical linear model. We plug in and with their empirical estimators and use .

The residual sum of squares may be another useful tool for measuring the goodness of fit of the proposed model, as in the classical linear model. The residual sum of squares in our model is defined as

and will be used along with the residual plots as a guide for selecting a better score function.

Finally, the proposed least-squares estimator (5) assumes that the regression line between and has an intercept (at the axis) of . Thus, if the model (or the score function) is correctly specified, then the intercept estimated by the regression (with intercept) should be close to , and the estimated intercept therefore serves as a measure for checking the correctness of the score function. Note that the regression (without intercept) performed in this paper is based on observations of the top ranks and assumes that the function passes through the origin (see Figure 4).

3.3 An Estimator with Unranked Observations

The least-squares estimator presented in Section 3.2 does not fully use the information contained in ; it is used only to estimate and , not to estimate itself. In this section, we briefly demonstrate how can be modified to incorporate these unranked observations.

We consider the following modified estimator:

where and . This modified estimator also asymptotically approaches the normal distribution. Specifically, suppose that

We also suppose that

, and

.

As in the previous section, -scaled

limits of , and exist; let

the limits be , and

, respectively.

Then, we can write the following theorem.

Theorem 4.

Under the same assumptions as those of Theorem 2, the distribution of converges to the normal distribution with mean and variance

Proof.

the distribution of which converges to the normal distribution with mean and variance

following the same arguments presented in the proof of Theorem 2.

∎

4 Numerical Study

In this section, we numerically investigate the advantage we can gain by choosing the correct score function to estimate . The performance of an estimator is measured in terms of its bias and its mean square error (MSE), which we numerically estimate based on simulated data sets and the estimators obtained therefrom.

The data sets are generated from the regression model where the are independently drawn from . We consider three distributions for : the uniform distribution on , the standard normal distribution, and the gamma distribution with mean and variance . As stated in Section 2, the score function of the uniform distribution is almost equivalent to the identity score function . However, the normal distribution and the gamma distribution have heavier tails than does the uniform distribution, and their score functions are convex in the right tail. We set the parameters to ensure that , , and , where . Finally, in each considered case, the sample size and the number of partially observed ranks are set to all possible combinations of or and , , or . When estimating , we apply four different scores, including the proposed MOS-based score functions obtained from the three distributions listed above and the identity score function, which is commonly used in practice. The approximated bias and MSE values are reported in Tables 1 and 2.

We can observe several interesting findings from these tables. First, the correctly specified score function performs better than do others when there exists a strong correlation between and (when is large). However, when , there is almost no difference among the four considered scores. Second, as the number of observations increases, in the sense that either or increases, the superiority of the correctly specified scores with respect to the others becomes apparent even when is not large. Third, as conjectured in the previous section, the scores based on the uniform distribution perform almost identically to the identity scores. Finally, the differences between the correctly specified scores and the others are significant regardless of or the sample size ( or ) when the distribution of has a heavier right tail (the gamma distribution).

| Dist | Bias | MSE | Bias | MSE | Bias | MSE | ||

| r=20 | 1:N | 0.0009 | 0.0167 | -0.0009 | 0.0165 | -0.0025 | 0.0184 | |

| U | - | -0.0027 | 0.0174 | 0.0051 | 0.0170 | |||

| N | -0.0032 | 0.0103 | 0.0008 | 0.0097 | ||||

| G | 0.0001 | -0.0044 | - | |||||

| 1:N | -0.0003 | 0.0161 | 0.0923 | 0.0243 | 0.2090 | 0.0600 | ||

| U | 0.0900 | 0.0256 | 0.2122 | 0.0603 | ||||

| N | -0.0715 | - | 0.0990 | 0.0194 | ||||

| G | -0.1287 | 0.0218 | -0.0794 | 0.0118 | - | |||

| 1:N | 0.0012 | 0.0127 | 0.1437 | 0.0336 | 0.3430 | 0.1327 | ||

| U | 0.1474 | 0.0351 | 0.3476 | 0.1354 | ||||

| N | -0.1217 | 0.0222 | 0.1566 | 0.0330 | ||||

| G | -0.2180 | 0.0518 | -0.1241 | 0.0197 | - | |||

| 1:N | -0.0025 | 0.2057 | 0.0522 | 0.4916 | 0.2535 | |||

| U | - | 0.2053 | 0.0517 | 0.4886 | 0.2505 | |||

| N | -0.1693 | 0.0334 | - | 0.2266 | 0.0584 | |||

| G | -0.3051 | 0.0958 | -0.1750 | 0.0338 | - | |||

| r=50 | 1:N | 0.0011 | 0.0077 | 0.0007 | 0.0076 | -0.0020 | 0.0069 | |

| U | - | -0.0005 | 0.0071 | 0.0034 | 0.0076 | |||

| N | -0.0038 | 0.0056 | 0.0008 | 0.0053 | ||||

| G | -0.0016 | 0.0004 | ||||||

| 1:N | -0.0033 | 0.0405 | 0.0083 | 0.1116 | 0.0196 | |||

| U | - | 0.0427 | 0.0082 | 0.1112 | 0.0187 | |||

| N | -0.0418 | 0.0067 | - | 0.0735 | 0.0110 | |||

| G | -0.0988 | 0.0131 | -0.0604 | 0.0066 | - | |||

| 1:N | 0.0022 | 0.0050 | 0.0657 | 0.0096 | 0.1878 | 0.0413 | ||

| U | - | 0.0687 | 0.0101 | 0.1882 | 0.0408 | |||

| N | -0.0717 | 0.0093 | 0.1217 | 0.0192 | ||||

| G | -0.1652 | 0.0298 | -0.0982 | 0.0123 | - | |||

| 1:N | -0.0006 | 0.0035 | 0.0897 | 0.0116 | 0.2655 | 0.0744 | ||

| U | 0.0975 | 0.0133 | 0.2641 | 0.0736 | ||||

| N | -0.0998 | 0.0127 | 0.1655 | 0.0307 | ||||

| G | -0.2293 | 0.0544 | -0.1401 | 0.0216 | ||||

| r=100 | 1:N | 0.0005 | 0.0042 | 0.0005 | 0.0042 | 0.0040 | 0.0042 | |

| U | - | 0.0000 | 0.0043 | -0.0021 | 0.0039 | |||

| N | 0.0003 | 0.0035 | - | -0.0012 | 0.0040 | |||

| G | 0.0003 | 0.0005 | ||||||

| 1:N | 0.0013 | 0.0035 | 0.0107 | 0.0034 | 0.0490 | 0.0061 | ||

| U | 0.0099 | 0.0036 | 0.0498 | 0.0062 | ||||

| N | -0.0210 | 0.0517 | 0.0063 | |||||

| G | -0.0714 | 0.0074 | -0.0479 | - | ||||

| 1:N | 0.0003 | 0.0028 | 0.0161 | 0.0031 | 0.0896 | 0.0110 | ||

| U | - | 0.0152 | 0.0031 | 0.0890 | 0.0108 | |||

| N | -0.0352 | 0.0036 | - | 0.0836 | 0.0096 | |||

| G | -0.1187 | 0.0159 | -0.0823 | 0.0088 | - | |||

| 1:N | 0.0008 | 0.0017 | 0.0230 | 0.0022 | 0.1210 | 0.0166 | ||

| U | 0.0225 | 0.0023 | 0.1247 | 0.0175 | ||||

| N | -0.0468 | 0.0038 | - | 0.1186 | 0.0158 | |||

| G | -0.1689 | 0.0297 | -0.1140 | 0.0143 | - | |||

| Dist | Bias | MSE | Bias | MSE | Bias | MSE | ||

| r=20 | 1:N | -0.0007 | 0.0173 | 0.0000 | 0.0168 | 0.0006 | 0.0165 | |

| U | 0.0029 | 0.0166 | 0.0066 | 0.0170 | ||||

| N | -0.0042 | 0.0072 | - | 0.0008 | 0.0068 | |||

| G | -0.0014 | 0.0017 | ||||||

| 1:N | -0.0020 | 0.1650 | 0.0433 | 0.3691 | 0.1519 | |||

| U | - | 0.1630 | 0.0427 | 0.3707 | 0.1537 | |||

| N | -0.1068 | 0.0174 | 0.1319 | 0.0249 | ||||

| G | -0.1680 | 0.0312 | -0.0925 | 0.0118 | ||||

| 1:N | -0.0053 | 0.0123 | 0.2821 | 0.0931 | 0.6109 | 0.3891 | ||

| U | 0.2714 | 0.0870 | 0.6163 | 0.3952 | ||||

| N | -0.1822 | 0.0387 | - | 0.2238 | 0.0566 | |||

| G | -0.2821 | 0.0821 | -0.1537 | 0.0263 | ||||

| 1:N | -0.0013 | 0.3825 | 0.1558 | 0.8650 | 0.7618 | |||

| U | 0.3859 | 0.1586 | 0.8623 | 0.7575 | ||||

| N | -0.2528 | 0.0671 | 0.3113 | 0.1026 | ||||

| G | -0.3936 | 0.1567 | -0.2182 | 0.0496 | ||||

| r=50 | 1:N | -0.0013 | 0.0071 | 0.0012 | 0.0070 | 0.0009 | 0.0071 | |

| U | 0.0020 | 0.0066 | -0.0008 | 0.0075 | ||||

| N | 0.0015 | 0.0036 | -0.0007 | 0.0033 | ||||

| G | 0.0002 | -0.0009 | ||||||

| 1:N | 0.0016 | 0.0062 | 0.1147 | 0.0196 | 0.2589 | 0.0737 | ||

| U | - | 0.1136 | 0.0192 | 0.2667 | 0.0776 | |||

| N | -0.0851 | 0.0102 | 0.1121 | 0.0159 | ||||

| G | -0.1456 | 0.0229 | -0.0818 | 0.0083 | ||||

| 1:N | 0.0025 | 0.0051 | 0.1953 | 0.0436 | 0.4396 | 0.1988 | ||

| U | - | 0.1928 | 0.0426 | 0.4389 | 0.1986 | |||

| N | -0.1486 | 0.0246 | - | 0.1854 | 0.0376 | |||

| G | -0.2457 | 0.0617 | -0.1371 | 0.0202 | - | |||

| 1:N | 0.0006 | 0.0035 | 0.2698 | 0.0767 | 0.6124 | 0.3806 | ||

| U | 0.2691 | 0.0761 | 0.6195 | 0.3882 | ||||

| N | -0.2019 | 0.0426 | 0.2578 | 0.0690 | ||||

| G | -0.3429 | 0.1184 | -0.1901 | 0.0372 | - | |||

| r=100 | 1:N | 0.0002 | 0.0036 | 0.0015 | 0.0038 | 0.0039 | 0.0034 | |

| U | - | 0.0013 | 0.0036 | -0.0002 | 0.0037 | |||

| N | 0.0012 | 0.0021 | -0.0029 | 0.0021 | ||||

| G | -0.0003 | -0.0014 | ||||||

| 1:N | 0.0031 | 0.0032 | 0.0791 | 0.0095 | 0.1863 | 0.0380 | ||

| U | - | 0.0764 | 0.0089 | 0.1847 | 0.0374 | |||

| N | -0.0698 | 0.0067 | 0.0920 | 0.0105 | ||||

| G | -0.1247 | 0.0167 | -0.0711 | 0.0062 | - | |||

| 1:N | -0.0008 | 0.1302 | 0.0196 | 0.3124 | 0.1006 | |||

| U | 0.1284 | 0.0191 | 0.3114 | 0.1000 | ||||

| N | -0.1107 | 0.0139 | 0.1530 | 0.0252 | ||||

| G | -0.2105 | 0.0453 | -0.1204 | 0.0155 | - | |||

| 1:N | -0.0012 | 0.0018 | 0.1793 | 0.0339 | 0.4344 | 0.1910 | ||

| U | 0.1793 | 0.0340 | 0.4365 | 0.1927 | ||||

| N | -0.1551 | 0.0251 | 0.2156 | 0.0479 | ||||

| G | -0.2923 | 0.0861 | -0.1691 | 0.0292 | - | |||

5 Data Examples

5.1 Data Description

To investigate how the attention of investors affects stock returns, we merge the hand-collected Daum.net rank data set and the financial data from FnGuide. We illustrate how the returns of attention-grabbing stocks fluctuate around the event dates when investors pay attention to these stocks. The variables to be used in the analysis are as follows. (1) “R”: The rank of an individual stock on day ; if the rank value is , then the stock is the most frequently discussed stock on the Daum stock message board on that day. This is the key variable that measures the degree of investor attention. (2) “RN”: Raw returns on day (the next day) (%), which is of primary interest and is the quantity that we wish to predict. (3)“ R0”: Raw returns on day (%). (4) “R1”: Raw returns on day (%). (5) “R2”: Raw returns on day (%). (6) “R3”: Raw returns on day (%). (7) “R4”: Raw returns on day (%). (8) “R5”: Raw returns on day (%). (9) “ME”: Market capitalization (1 trillion Korean won). (10) “T”: Turnover ratio defined as the trading volume divided by the number of outstanding shares. (11) “TA”: Turnover ratio defined as the trading volume divided by market capitalization.

5.2 Attention and Predictive Stock Returns

As stated previously, the primary goal of our analysis is to determine how the returns of attention-grabbing stocks will fluctuate around the event dates when investors pay attention to these stocks. The next-day return can also be influenced by several other factors in addition to investor attention. To account for the effects of these other factors, we consider the residuals obtained after regressing the next-day return against all other covariates except the rank, “R”. These residuals are obtained from the multiple linear regression model, which is defined as follows:

| (6) |

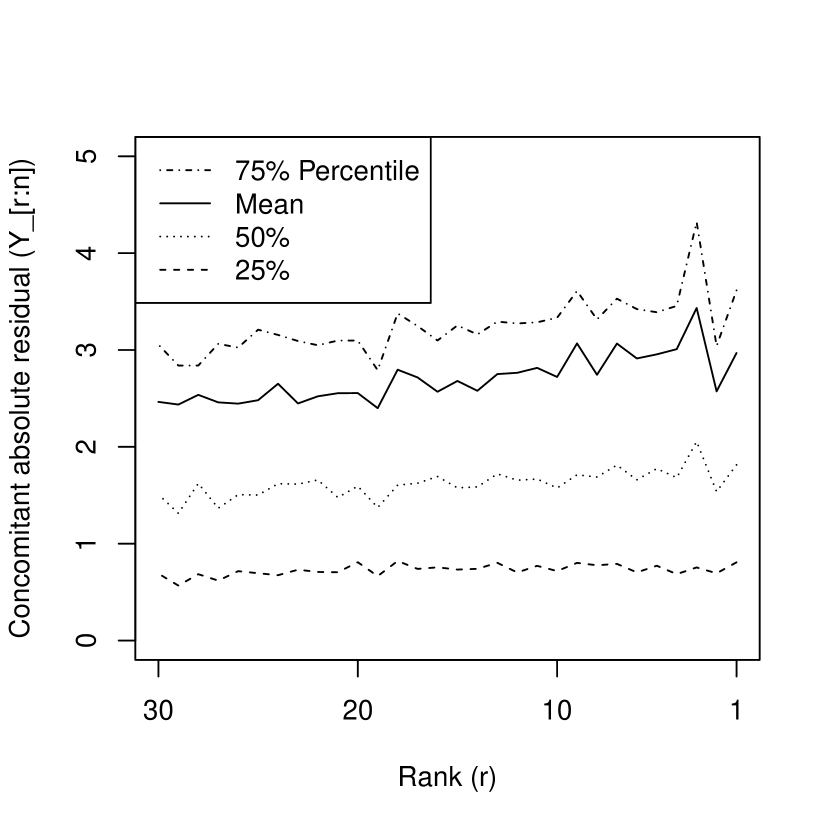

where is the total number of companies on the market. Let be the absolute (value of the) residual of company obtained from the regression (6). We then select the absolute residuals whose ranks are reported to be within the top 30 for the primary analysis. Below, is the absolute residual corresponding to rank on day for and .

In Figure 1, we plot the quantiles of for each . This figure reveals that is not increasing at and , which we hypothesize reflects the heterogeneity of investor expectations with regard to highly attention-grabbing stocks. In other words, the ranking of the Daum board is purely determined by the attention of individual investors, and stocks related to news, that is difficult to characterize as either good or bad, often receive the greatest attention and the highest ranks. We introduce an additional term to explain this apparent local non-monotonicity, and consider the model

| (7) |

for with and .

5.3 Regression with Ranks

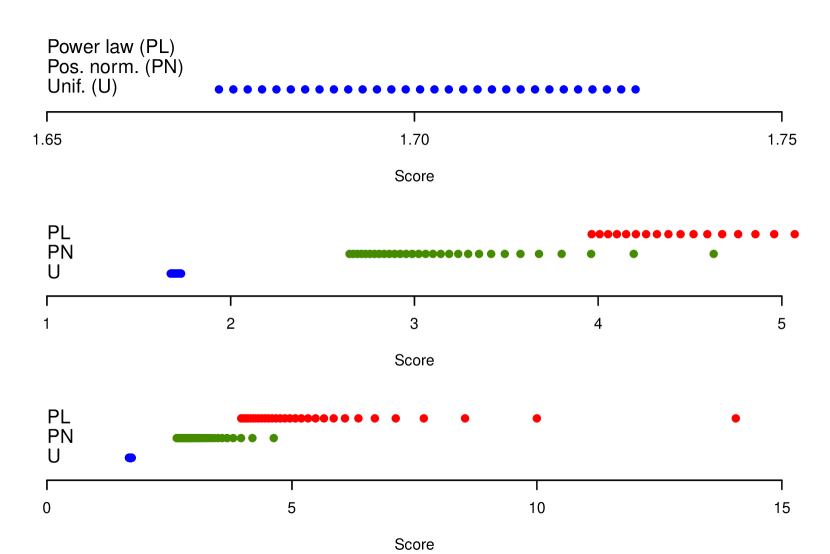

In the regression model, we consider the scores from the standardized distributions of the location-scale families generated by the following three distributions: (i) a uniform distribution on (called the uniform score), (ii) a positive normal distribution , (called the half-normal score), and (iii) a power-law distribution whose CDF is with (called the power-law score). The scores are illustrated on different scales in Figure 2.

We estimate and to minimize the empirical squared-error loss of the model (7) by iterating the following steps:

-

1.

Given the least-squares estimator of , denoted by , update the estimate of as follows:

-

2.

Given the estimate of , denoted by , update the estimate of using the LSE proposed in the previous section as follows:

In the analysis, the initial value is obtained from the preliminary linear regression on , , in which the data corresponding to are excluded. By contrast, and are estimated based on their empirical values as follows: and .

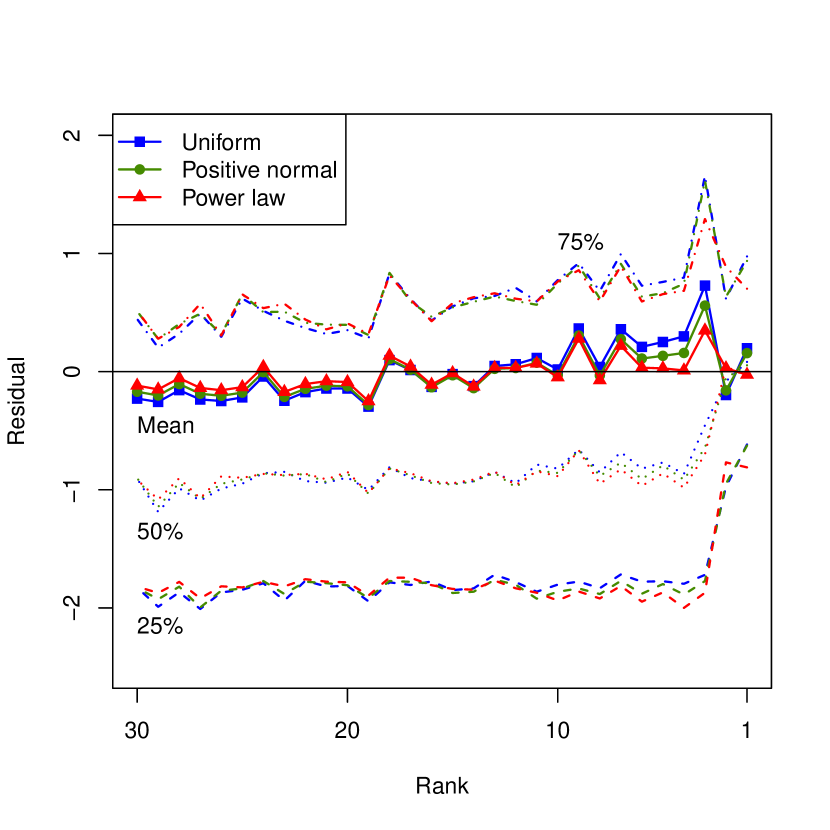

To choose the most appropriate score function among the three considered, we follow the guidelines presented in Section 3.2 and perform a residual analysis. First, we plot and the quantiles of the corresponding residuals to identify any remaining trend not explained by the model (see Figure 3). This figure shows that the uniform score and the half-normal score exhibit additional linear trends not explained by the linear model (7), whereas the power-law score performs well. Second, we plot

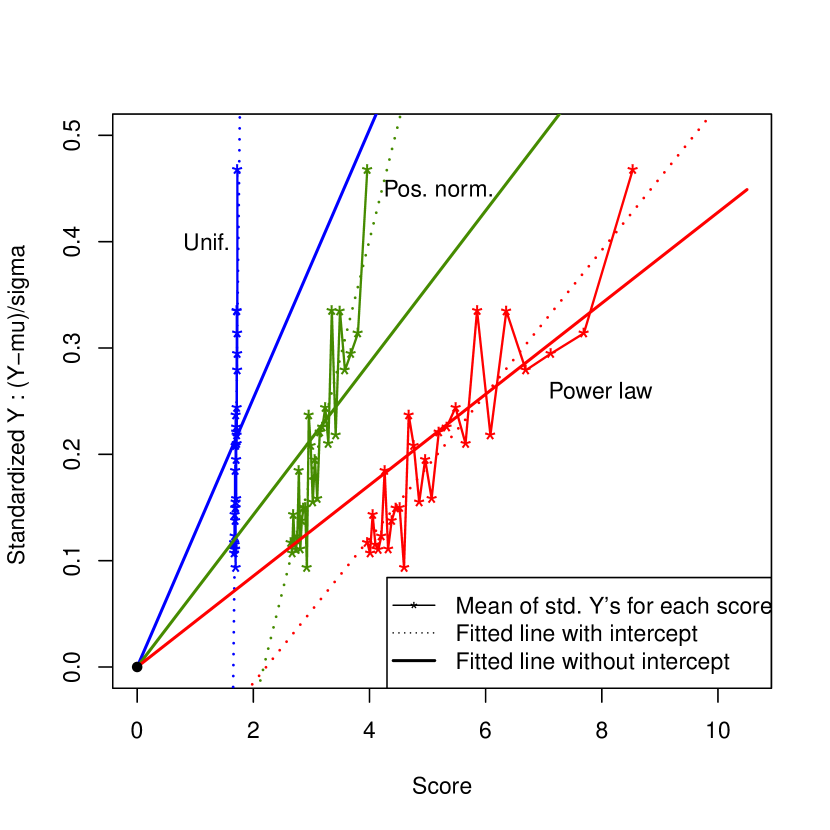

and apply the least-squares fits with/without intercept. As we know from the model (3), the estimated regression line with intercept should cross the origin if the scores are correctly specified. Figure 4 reveals that the (estimate of) the intercept of the power-law score is closest to zero among the intercepts of the three considered scores. Finally, the residual sums of squares of the three scores are found to be , , and , respectively. This finding also supports the superiority of the power-law score function, and in the following analysis, we focus on the power-law score function.

5.4 Test of the Effect of Investor Attention on the Next-day Returns

The primary goal of the analysis is to investigate whether the attention of investors affects the returns of a stock on the following day. Specifically, we are interested in testing under the assumption that for every . To test this hypothesis, we consider a combined statistic of , that is,

| (8) |

where . Here, the estimates of for each day , denoted by , are serially dependent on each other, as are the s. Thus, to obtain the reference distribution of , we further assume that is stationary and that for . Under these assumptions, the null distribution of is asymptotically normal with mean and variance

The variance can be empirically estimated from the observed values of as

for sufficiently large , where denotes the empirical covariance of the observed statistics . An additional interesting feature of the combined procedure is that the test statistic is a rough estimator of for all trading days (after the scaling). It is calculated as

| (9) | |||||

where is the least-squares estimator under the assumption that for all . The difference between the right- and left-hand sides of (9) lies in the definition of , which is defined using rather than .

The results of the test indicate that the average value of , which is an estimator of , is . The -value obtained when testing is less than and statistically supports the association between investor attention and the next-day returns of the stocks.

6 Conclusion

In this paper, we study a regression problem based on a partially observed rank covariate. We propose a new set of score functions and study their application in simple linear regression. We demonstrate that the least-squares estimator that is calculated based on the newly proposed score consistently estimates the correlation coefficient between the response and the unobserved true covariate if the score function is correctly specified. We also define procedures based on the obtained residuals to identify the correct score function for the given data. The proposed estimator and procedures are applied to rank data collected from Daum.net, and we empirically verify the association between investor attention and next-day stock returns.

We finally conclude the paper with two discussions on the proposed score function. First, the application of the proposed score function is not restricted to linear regression but may also be appropriate for other statistical procedures based on rank, including the well-known rank aggregation problem (Breitling et al., 2004; Eisinga et al., 2013). Second, the score function still can be used for the the multiple linear regression model

with an additional covariate vector . Similarly to the case of the simple linear regression, we have the representations

where and , , have mean and independent to each other. Again, the least-squares estimators of and are defined as the solutions to

and conjecture that they consistently estimate and .

Appendix

A.1 Proof of Theorem 2

Note that converges in probability to 1 as and

has the same limiting distribution with

| (10) |

Then, equation (10) can be written as

where and

| (11) | |||||

with and

Since converges in probability to 0, we only consider the and . Thus, the proof of the theorem is based on the functional central limit theorem for two partial sums of rank statistics, and .

We first consider the asymptotic distribution of the process of taking the weighted partial sum of the induced rank statistic, which is

| (12) | |||||

The main finding of Bhattacharya (1974) is the

conditional independence of given

(or equivalently, ).

Thus, given , (12) can be read as

| (13) |

where the are independent, with mean and variance . By applying the basic concept of Skorokhod embedding (Shorack and Wellner, 2009), we obtain a sequence of stopping times such that

-

•

these stopping times are conditionally independent given ,

-

•

,

-

•

, and

-

•

has the same distribution as , where is conventional Brownian motion.

We now consider the embedded partial-sum process that is defined by . As in Bhattacharya (1974), it suffices to show that

| (14) |

converges to probability.

For each , the strong law of large numbers states that almost certainly converges to . Both and are increasing functions of . Thus, using the same arguments (Shorack and Wellner, 2009, pp. 62), we find that their sup difference also converges to .

Second,

| (15) |

is a linear statistic of order statistics and converges to the normal distribution with mean and variance (David, 2003, Theorem 11.4). Here, we remark that both and can also be written as functionals of the distribution of , as shown in (David, 2003).

Finally, summing the asymptotic results of and , we find that converges to the normal distribution with mean and variance

This concludes the proof.

A.2 Proof of Theorem 1

We first decompose the sample correlation between and as :

where . In below, we compute the limit of each , and . First, similarly to the convergence of (with ) in Appendix A, we can show that converges in distribution to a normal random variable and, thus, converges to in probability. Second, similarly to the convergence of (with ) in Appendix A, we can show that converges in distribution to a normal random variable and, thus, converges to in probability. Lastly,

whose first term converges to in probability similarly to the convergence of (with ) in Appendix A. Hence, converges in probability to the limit of

| (16) |

Since and approaches , (16) is maximized when in asymptotic.

References

- Bhattacharya (1974) Bhattacharya, P. K. (1974). Convergence of sample paths of normalized sums of induced order statistics. The Annals of Statistics, 2, 1034–1039.

- Breitling et al. (2004) Breitling, R., Armengaud, P., Amtmann, A. and Herzyk, P. (2004). Rank products: a simple, yet powerful, new method to detect differentially regulated genes in replicated microarray experiments. FEBS Letters, 573, 83-92.

- Camerer (2003) Camerer, C. (2003). The behavioral challenge to economics: Understanding normal people. Conference Series, Proceedings, 48. Paper presented at Federal Bank of Boston 48th Conference on ’How humans behave: Implications for economics and policy’.

- Costantini et al. (2010) Costantini, P., Linting, M., and Porzio, G.C. (2010). Mining performance data through nonlinear PCA with optimal scaling. Applied Stochastic Models in Business and Industry, 26(1), 85-101.

- David and Galambos (1974) David, H.A. and Galambos, J. (1974). The asymptotic theory of concomitants of order statistics. Journal of Applied Probability, 11, 762-770.

- David (2003) David, H.A. (2003). Order Statistics. John Wiley and Sons, New Jersey.

- de Leeuw and Mair (2009) de Leeuw, J. and Mair, P. G (2009). Gifi methods for opti- mal scaling in R: The package homals. Journal of Statistical Software, 31(4), 2009.

- Eisinga et al. (2013) Eisinga, R., Breitling, R. and Heskes, T. (2013). The exact probability distribution of the rank product statistics for replicated experiments. FEBS Letters, 587, 677-682.

- Gertheiss (2014) Gertheiss, J. (2014). ANOVA for factors with ordered levels. Journal of Agricultural, Biological, and Environmental Statistics, 19, 258–277.

- Graubard and Korn (1987) Graubard, B.I. and Korn, E.L. (1987). Choice of column scores for testing independence in ordered 2K contingency tables. Biometrics, 43, 471-476.

- Ivanova and Berger (2001) Ivanova, A. and Berger, V.W. (2001). Drawbacks to integer scoring for ordered categorical data. Biometrics, 57, 567-570.

- Hájek (1968) Hájek, J. (1968). Asymptotic normality of simple linear rank statistics under alternatives. Annals of Mathematical Statistics, 39, 325-346.

- Hora and Conover (1984) Hora, S.C. and Conover, W.J. (1984). The F-statistic in the two-way layout with rank-score transformed data. Journal of the American Statistical Association, 79, 668-673.

- Jacoby (2016) Jacoby, W.G. (2016) opscale: A Function for Optimal Scaling. http://polisci.msu.edu/jacoby/icpsr/scaling/computing/alsos/acoby,%20opscale%20MS.pdf (August 31, 2016).

- Kahneman (1973) Kahneman, D. (1973). Attention and Effort. Prentice-Hall, New Jersey.

- Kimeldorf et al. (1992) Kimeldorf, G., Sampson, A.R. and Whitaker, L.R. (1992). Min and max scorings for two-sample ordinal data. Journal of the American Statistical Association, 87, 241-247.

- Linting et al. (2007) Linting, M., Meulman, J.J., Groenen, P.J.F., and Van der Kooji, A.J. (2007). Nonlinear principal components analysis: Introduction and application. Psychological Methods, 12(3), 336-358.

- Mair, and de Leeuw (2010) Mair, P. and de Leeuw, J. (2010). A general framework for multivariate analysis with optimal scaling: The R package aspect. Journal of Statistical Software, 32(9), 2010.

- Senn (2007) Senn, S. (2007). Drawbacks to noninteger scoring for ordered categorical data. Biometrics, 63, 296-298.

- Shorack and Wellner (2009) Shorack, G.R. and Wellner, J.A. (2009). Empirical Processes with Applications to Statistics, The Society for Industrial and Applied Mathematics, Philadelphia, PA.

- Zheng, (2008) Zheng, G. (2008). Analysis of ordered categorical data: two score-independent approaches. Biometrics, 64, 1276-1279.