Multinomial method for option pricing under Variance Gamma

Abstract

This paper presents a multinomial method for option pricing when the underlying asset follows an exponential Variance Gamma process. The continuous time Variance Gamma process is approximated by a continuous time process with the same first four cumulants, and then discretized in time and space. This approach is particularly convenient for pricing American and Bermudan options, which can be exercised before the expiration date. Numerical computations of European and American options are presented, and compared with results obtained with finite differences methods and with the Black-Scholes prices.

keywords:

American option, Lévy processes, Moment Matching, Multinomial tree, Variance Gamma.1 Introduction

Since the early nineties, a lot of research has been done on the topic of pure jump Lévy processes to describe the dynamics of the asset returns. The main contributions are [5], [11], [13], [20].

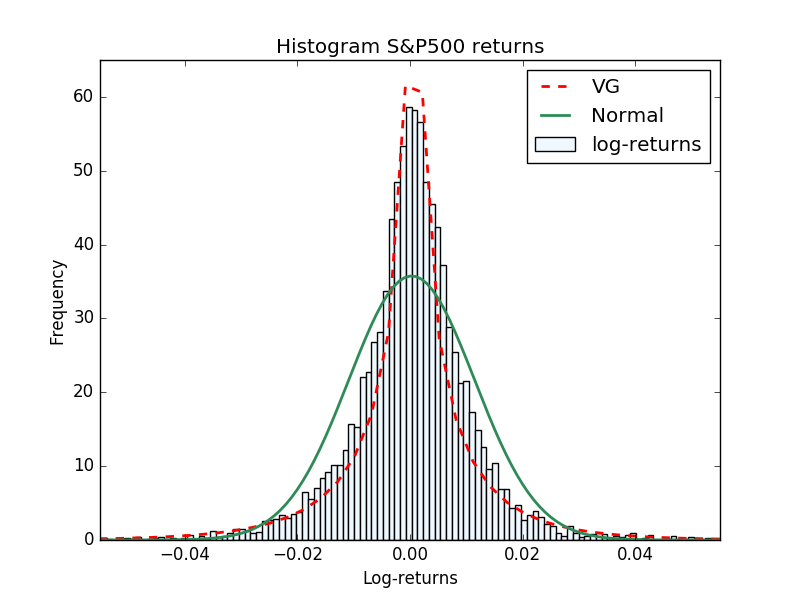

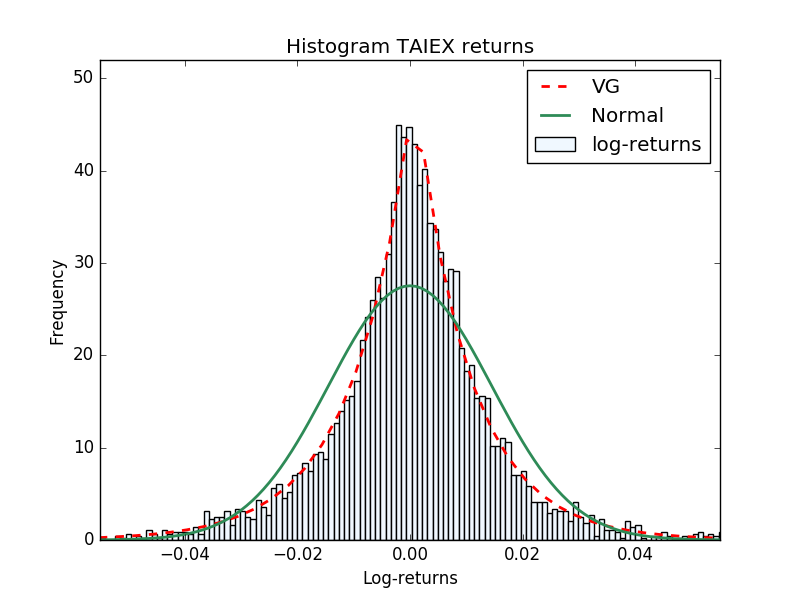

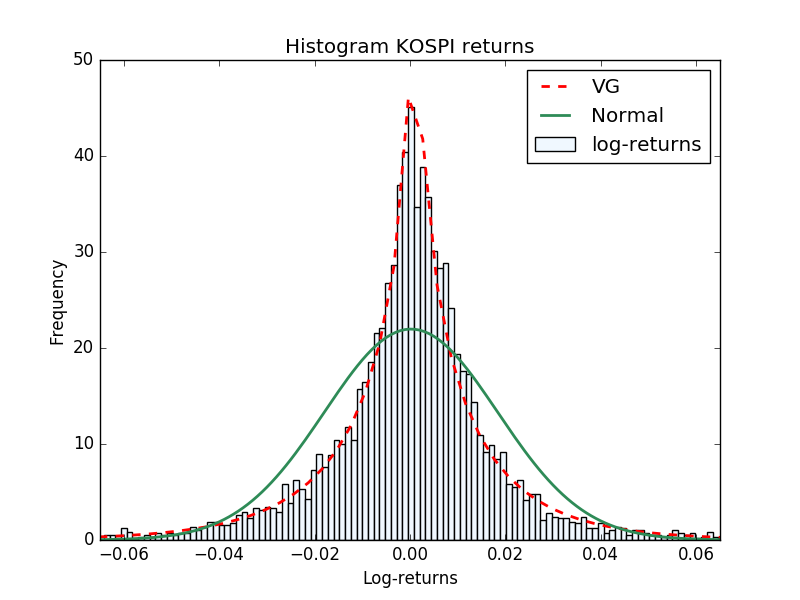

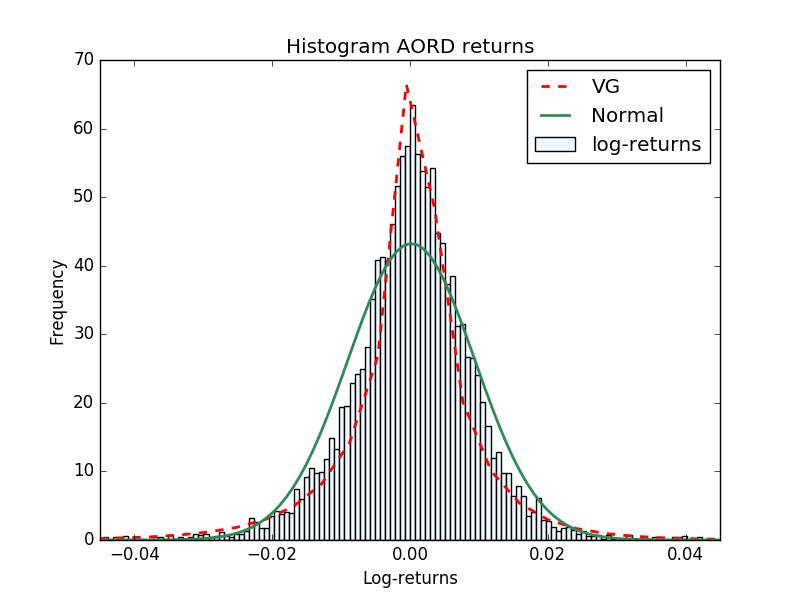

Lévy processes are stochastic processes with independent and stationary increments that have nice analytical properties and reproduce quite well the statistical features of the financial data (see for instance [1] and [8]). In Figure 1 we present as examples the histograms of the daily log-returns for four of the major indices: the S&P 500 Stock Index, the KOSPI (Korea Composite Stock Price Index), XAO (All Ordinaries Australian Index) and TAIEX (Taiwan Capitalization weighted Stock Index). In the pictures we show the Normal and Variance Gamma (VG) densities fitted with the market data. It is straightforward to check that the VG density reproduces much better the high peaks near the origin, and the heavy tails feature.

The Variance Gamma process is a pure jump Lévy process with infinite activity. This means that when the magnitude of the jumps becomes infinitesimally small, the arrival rate of jumps tends to infinity. The first complete presentation of financial applications of the symmetric VG model is given in [20] where, with respect to the Gaussian model, an additional parameter is introduced in order to control the kurtosis (the skewness is not considered). The authors model the log-returns with a driftless Brownian motion whose variance is Gamma distributed. This is the origin of the name “Variance Gamma”.

It is possible to give two representations to the VG process. In the first one, the VG process is obtained by time changing a Brownian motion with drift: the Brownian motion is evaluated at random times that are Gamma distributed. The economic interpretation is that the trading relevant times are indeed random. The non-symmetric VG process is described in [18], where the authors also present an explicit form of the density function, and a closed formula for the price of a vanilla European option. The authors consider a Brownian motion with a non-zero drift, and this additional parameter allows to control the skewness as well.

The VG process has an infinite number of jumps in any time interval and, unlike the Brownian motion, it does not have a continuous martingale component. Another important difference from the Brownian motion is that the VG process has finite variation, therefore the sum of the absolute value of the increments in any time interval converges. This fact can be derived easily from the second representation for VG processes: every VG can be represented as the difference of two (finite variation) Gamma processes. The proof can be found in [18], where the authors show that the two representations are equivalent, and also derive the VG characteristic function from the product of two Gamma characteristic functions. The second representation has an interesting economical interpretation: it can be seen as the difference of gains and losses. The Gamma processes are always increasing, therefore this representation is coherent with independent gains and losses processes.

The VG process was first presented in the context of option pricing in [19], where it has been used for pricing European options. European vanilla options can be easily priced by the analytical formula presented in [18] and exotics can be priced numerically by several techniques: Monte Carlo methods for VG are presented in [12]. A finite difference scheme for the VG Partial Integro-Differential Equation (PIDE) is described in [9]. In [7], the authors show how to price options by using a Fourier transform approach. The problem for American options is considered in [2], [3] and [15], where the authors present different finite difference schemes to solve the American VG PIDE.

The tree method was first introduced by [10] for a market where the log-price can change only in two different ways: an upward jump, or a downward jump. For this reason the model is called binomial model. The authors prove that when the number of time steps goes to infinity, the discrete random walk of the log-price converges to the Brownian motion and the option price converges to the Black-Scholes price ([6]). The multinomial model is a generalization of the binomial model, and at each time step it considers more than just two possible future states. A general multinomial method for pricing European and American options under exponential Lévy processes is described in [21]. In [16] the authors consider a multinomial method for general exponential Lévy processes based on the moment matching condition. Other methods based on the moment matching condition are for instance [14], with applications to the Normal Inverse Gaussian process, and [24] with applications to the VG process. In the present work we consider a multinomial discretization based on the cumulant matching condition as explained in [25], [26] and [27].

In Section 2 we present the basic features of Lévy processes, in particular finite variation processes. The VG process and exponential VG are introduced in the successive subsections. A short summary of some useful concepts such as integration with respect to the Poisson random measure, and the relation between the Lévy symbol and the cumulants are collected in the Appendices A and B. In Section 3 we review the construction of the multinomial tree, following the method of moment matching proposed in [25]. We prove that the multinomial tree converges to the continuous time jump process that we have introduced to approximate the VG process. In Section 4, which is the most important of the paper, we describe the algorithm for pricing options with the multinomial method and show the numerical results for European and American options. In Section 5 we present a topic that deserves further research. We show how to obtain the parameters of the discrete time Markov chain that approximates the jump process, by discretizing its infinitesimal generator. However, with this method the transition probabilities are not always positive. These probabilities, in general, are different from the probabilities obtained by the moment matching condition, but for a particular choice of the parameters we argue that the two must coincide. This topic needs to be further investigated. In Section 6 we present the conclusions.

2 Lévy processes

Let be a stochastic process defined on a probability space , is said to be a Lévy process if it satisfies the three properties:

-

1.

.

-

2.

has independent and stationary increments.

-

3.

is stochastically continuous:

The characteristic function of a Lévy process has the Lévy-Khintchine representation:

| (1) | ||||

where is called Lévy symbol, and are constants111The diffusion coefficient is usually called . Here we use because will be used for the VG process. and is the Lévy measure which satisfies:

| (2) |

The Lévy triplet completely characterizes a Lévy process. Every Lévy process can be written as the superposition of a drift, a Brownian motion and two pure jump processes. This is the so called Lévy-Itō decomposition:

| (3) |

where is a standard Brownian motion, and are the Poisson random measure and the compensated Poisson random measure (see Appendix A).

We are interested in particular in processes with finite variation and finite moments. We see that the Lévy measure contains all the information we need:

-

•

A Lévy process with triplet is of finite variation if and only if

(4) -

•

A Lévy process has a finite moment of order , , if and only if

(5)

For a proof see [4], Theorem 2.4.25 and Theorem 2.5.2. For processes with finite variation, the truncator term in (1) can be absorbed in the parameter . It is easy to verify that every finite variation Lévy process can be represented as an integral of a Poisson random measure:

| (6) |

The Lévy symbol is:

| (7) |

2.1 The Variance Gamma process

The VG process is obtained by time changing a Brownian motion with drift. The new time variable is a stochastic process with density222Usually the Gamma distribution is parametrized by a shape and scale positive parameters . The Gamma process has pdf and has moments and . Here we use a parametrization as in [18] such that and , so , .:

| (8) |

The Gamma process is a subordinator. A subordinator is a one dimensional Lévy process that is non-decreasing almost surely. Therefore it is suitable to represent a time variable. It is possible to prove that every subordinator is a finite variation process (see [4]).

Considering a Brownian motion with drift , with , let’s replace the time variable by the Gamma subordinator (with ). We obtain the Variance Gamma process:

| (9) |

It depends on three parameters:

-

•

, the drift of the Brownian motion,

-

•

, the volatility of the Brownian motion,

-

•

, the variance of the Gamma process.

The probability density function of can be computed conditioning on the realization of :

| (10) | ||||

where the function is a modified Bessel function of the second kind (see [18] for the computations). The characteristic function can be obtained by conditioning too:

| (11) | ||||

| (12) |

see proposition 1.3.27 in [4]. The Lévy symbol is:

| (13) |

Using the formula (70) in Appendix B for the cumulants we derive:

| (14) | ||||

The VG Lévy measure is333In [18] the authors derive the expression for the Lévy measure by representing the VG process as the difference of two Gamma processes.:

| (15) |

and it satisfies conditions (4) and (5). The VG process can be represented as a pure jump process as in (6) and (7), with no additional drift .

| (16) |

All the informations are contained in the Lévy measure (15), which completely describes the process. Even if the process has been created by Brownian subordination, it has no diffusion component. The Lévy triplet is . Using the formalism of Poisson integrals in Appendix A, the Lévy symbol (13) has the representation444See Example 8.10 in [22].:

| (17) |

2.2 Exponential VG model

Under the risk neutral measure , the dynamics of the stock price is described by an exponential Lévy model:

| (18) |

where is the risk free interest rate, and is a general Lévy process. Under , the discounted price is a -martingale:

| (19) |

and thus . The condition for the existence of the exponential moment is equivalent to:

| (20) |

as proved in Lemma 25.7 in [22]. The VG process has finite exponential moment. In order to satisfy the martingale condition555 To obtain the correction term we have to find the exponential moment of using its characteristic function: . we need to add a correction term to . The following process is a martingale:

| (21) |

where . Passing to the log-price , we get a process in the form of Eq. (6) with :

| (22) |

Let be the value of an option at time .

We assume that and has a polynomial growth at infinity.

By the martingale pricing theory, the discounted price of the option

is a martingale and it is possible to derive the PIDE for the price of the option:

| (23) |

where is the infinitesimal generator of the log-price process (22). The resulting PIDE is:

| (24) |

3 The multinomial method

In this section we introduce the multinomial method proposed in [27]. The stock price is considered as a Markov chain with possible future states at each time. In this setting, the time is discretized as for and . We denote the stock price at time as .

Consider the up/down factors and write the discrete evolution of the stock price as:

| (25) |

where each future state has transition probability , satisfying . The value of the stock at time can assume possible values:

| (26) |

The multinomial tree is recombining if for a constant , . Regarding the present work, we only consider five branches, . As explained in [27], this number of branches is enough to model the features of a stochastic process up to its fourth moment.

3.1 Moment matching

To determine the parameters of the Markov chain we require that its local moments are equal to that of the continuous process. First, we rewrite the continuous process (22) as the sum of a drift term and a martingale term:

| (27) | ||||

where is the expected value of the VG process in 16, when . The integral with respect to the compensated Poisson measure is a martingale (see Appendix A).

We can pass to log-prices in the discrete Eq. (25), and write it as the sum of a drift component and a random variable with possible outcomes:

| (28) | ||||

The term is the drift term, while is a random variable that assumes values in with probability . It has to satisfy the martingale condition:

with a function of .

The corresponding up/down factors have the following representation:

| (29) |

and we can readily see that if is constant the tree recombines.

Given the mean , the -central moment is:

| (30) |

The moment matching condition requires that the central moments of the discrete process (28) are equal to the central moments of the continuous process (27):

| (31) |

We fix , and using the relation between central moments and cumulants (Eq. (71) in Appendix B) we solve the linear system of equations for the transition probabilities:

| (32) | ||||

The drift parameter is . The only missing parameter to determine is . This is a function of the time increment and can be determined using the higher order terms in the moment matching condition together with the condition of positive probabilities.

Recall that the well known binomial model [10] assumes the value , that represents the volatility of the increments in the time interval . In the trinomial model, the parameter assumes value , see for instance [25]. For the multinomial method a good representation for is:

| (33) |

where is the excess of kurtosis666We use the bar over , to distinguish the kurtosis from the variance of the gamma process .. We refer to [27] for the derivation. This choice guarantees that the probabilities for are always positive and sum to one. We can replace the expression (33) inside (32), to obtain the simpler form:

| (34) | ||||

where is the skewness.

Remark 1.

The standard deviation of every Lévy process with finite moments follows the square root rule. This means that the term has to be proportional to the square root of . In the binomial and trinomial models, the proportionality constant is explicit, while for the pentanomial method it is implicit in the formula (33). Expanding the formula using the expression (14) for the cumulants, it is possible to check that the square root rule is satisfied at first order in .

3.2 Convergence

We call a generic jump process (6) with first four cumulants ,,, equal to the VG cumulants (14), the approximated process . The cumulant generating function of the increment has the following series representation (see Appendix (B)):

| (35) |

We are interested in the approximation of a VG process with drift (27), therefore we require that .

Theorem 3.1.

The increments of the discrete Markov chain (28) and the increments of the approximated process have the same distribution by construction.

Proof.

The idea of the proof is to show that the cumulant generating function of the discrete process (28) coincides with that of the approximated process (35). We prove it using the moment matching condition (31).

| (36) | ||||

We can expand the exponential function in Taylor series and use the moment matching condition (31) to obtain:

| (37) | ||||

∎

Remark 2.

All the cumulants of are equal to the cumulants of the Markov chain (28) by construction, but only the first four are equal to the VG cumulants. When all the cumulants , for , are equal to the VG cumulants, the approximated process converges to the original VG process for . To control cumulants, we need branches. Therefore, when the number of cumulants of equal to those of the VG process goes to infinity, the number of branches have to go to infinity as well. We assume that five branches () are enough to describe the features of the underlying process and, at the same time, keep the numerical problem simple.

Theorem 3.2.

The distribution of the pentanomial tree at time converges to the distribution of a compound Poisson process at time with possible jump sizes and activity , when .

For the proof of this theorem we refer to Section 4.2 of [27]. The authors first define the jump sizes and their respective probabilities, and then prove that when the characteristic function of the pentanomial tree converges to the characteristic function of the compound Poisson process.

4 Numerical results

In this section we present the steps to implement the algorithm for pricing European and American options with the multinomial method. Then we compare the results with those obtained by the PIDE method and Black-Scholes model.

4.1 Algorithm

We suggest the following algorithm for pricing with the multinomial method:

-

1.

Compute the transition probabilities vector (34).

- 2.

-

3.

Evaluate the payoff of the option at terminal time .

-

4.

Given the option’s values at time compute the values at time . The value is the conditional expectation:

(38) -

5.

If computing the price of an American option, the value at the previous time level is the maximum between the conditional expectation and the intrinsic value of the option. For an American put we have:

(39) -

6.

Iterate the algorithm until the initial time .

In the parameters calibration procedure, sometimes it is common to estimate first the historical parameters, and use them as initial guess for the least squares minimization that recovers the risk neutral parameters. In [23] are presented several methods for historical parameters estimation of the VG density. We use the simple method of moments to estimate the parameters for the data in Fig. 1. In all future calculations we consider the risk neutral VG parameters in Table 4.1.

is the risk free interest rate and are the risk neutral VG parameters. 0.06 -0.1 0.2 0.2

4.2 European options

We compare the numerical results for European call and put options obtained with the multinomial and the PIDE approaches.

-

•

VG PIDE: We solve the VG PIDE following the method proposed by [9]. The Lévy measure is singular in the origin and this is a problem for the computation of the integral term in (24). Fixing a truncation parameter , we approximate the infinite activity martingale jump component with sizes smaller than , with a Brownian motion with same variance. The resulting approximated PIDE has the “jump-diffusion-like” form:

(40) where we introduced the parameters , and . More details are in [8]. We solve the PIDE (40) using the implicit-explicit finite difference scheme proposed in [9], and choosing the truncator parameter , where is the size of the space step. It turns out that the solution of the discretized equation convergences very slowly to the option price, and therefore we required a grid with space steps and time steps. The algorithm is written in Matlab and runs on an Intel i7 (7th Gen) with Linux. It takes about 30 minutes to complete.

-

•

Multinomial: We follow the algorithm proposed in the previous section. The number of time steps for all the computations is . In the table 4.2 we show a convergence table for the prices of European calls, puts and American puts. It is straightforward to see that the convergence is quite fast.

Convergence table for ATM European and American options with strike and . The time unit is in seconds. Eu. Call Eu. Put Time Am. Put Time 50 4.41873125 2.08928091 0.001 2.36765911 0.007 100 4.41960265 2.09015381 0.002 2.37255454 0.02 200 4.41997010 2.09052201 0.004 2.37480218 0.07 400 4.42013640 2.09068869 0.01 2.37587117 0.29 800 4.42021515 2.09076762 0.03 2.37639131 1.09 1000 4.42023054 2.09078306 0.04 2.37649417 1.67 1500 4.42025089 2.09080345 0.06 2.37663070 3.79 2000 4.42026098 2.09081357 0.10 2.37669869 6.80 2500 4.42026701 2.09081962 0.16 2.37673941 10.65 3000 4.42027102 2.09082364 0.2 2.37676652 14.78

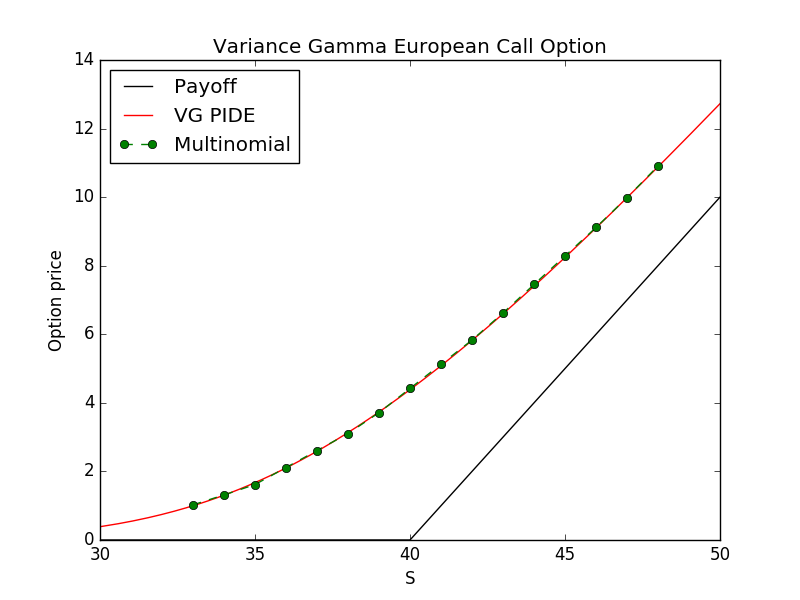

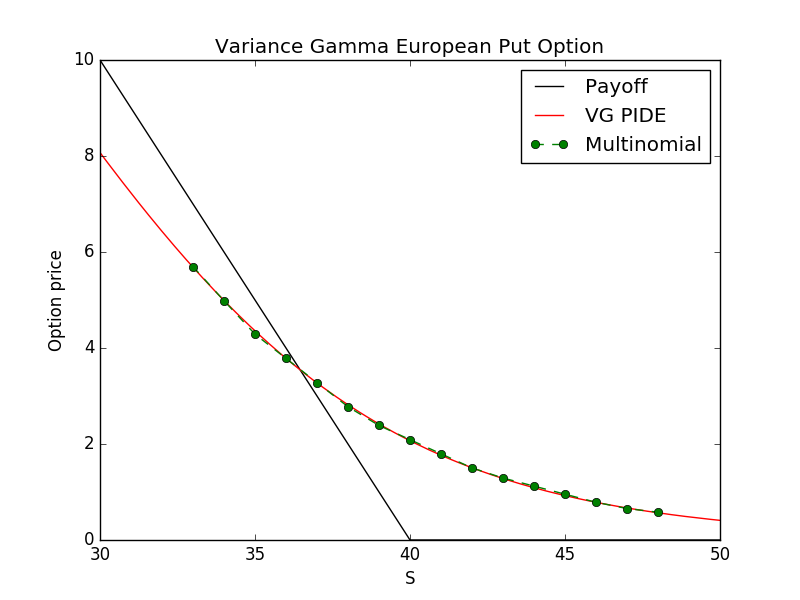

Figures (2) and (3) show the prices obtained by the multinomial method compared with those obtained by PIDE. In table 4.2 we compare directly the call/put numerical values obtained with the two methods.

Pricing vanilla call and put European options is quite simple and the best approach is to use the closed formula derived in [18]. The big advantage of the multinomial method is in the computation of American options prices, where there is no closed formula and all the other approaches, such as PIDEs and Least Squares Monte Carlo, are difficult to implement and much slower.

European Options, with strike and . Different methods PIDE Call Multi Call PIDE Put Multi Put 36 2.1036 2.1131 3.7842 3.7837 38 3.1163 3.1051 2.7893 2.7756 40 4.4162 4.4203 2.0852 2.0908 42 5.8335 5.8309 1.5050 1.5014 44 7.4417 7.4524 1.1132 1.1229

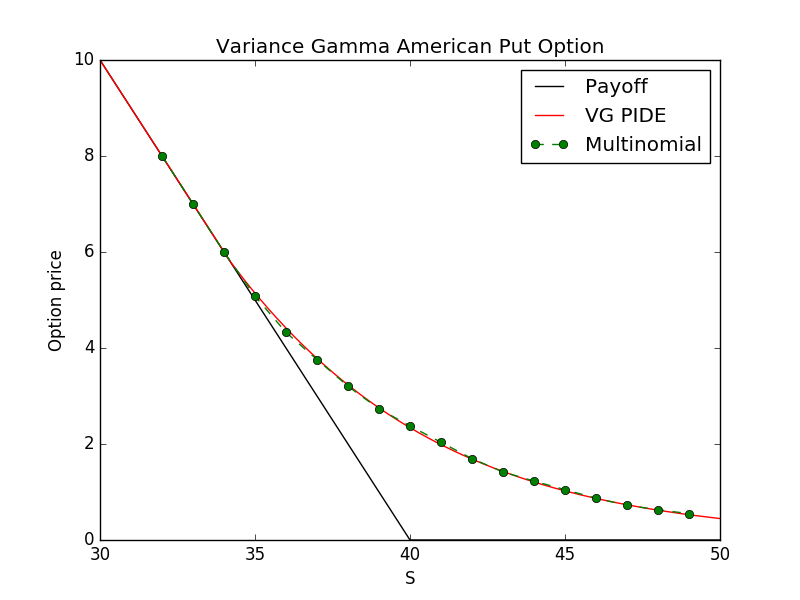

4.3 American options

In this section we present the numerical results obtained with the multinomial method algorithm for American put options, and compare them with the PIDE method (see fig. 4). The PIDE (40) is modified in order to take in account the early exercise feature:

| (41) | ||||

To solve this equation we use the same settings used for the Eq. (40): an implicit-explicit finite difference scheme, with 14000 space steps and 7000 time steps. The algorithm takes about 33 minutes to run.

The numerical values of the prices obtained with the multinomial and PIDE methods are collected in Tab. 4.3. The run times for the multinomial algorithm are shown in the convergence table 4.2.

Values for European and American put options using Black-Scholes and Variance Gamma model. Strike and . The BS volatility have same value of the VG volatility: . Prices comparison BS Eu. Put VG Eu. Put BS Am. Put VG Am. Put VG Am. PIDE Put 30 8.1316 8.0809 10 10 10 32 6.5292 6.4055 8 8 8 34 5.1169 4.9851 6.0894 6 6 36 3.9150 3.7837 4.5415 4.3173 4.3982 38 2.9263 2.7756 3.3264 3.2034 3.2195 40 2.1388 2.0908 2.3924 2.3767 2.3531 42 1.5322 1.5014 1.6911 1.6947 1.6849 44 1.0766 1.1229 1.1755 1.2267 1.2118 46 0.7433 0.7858 0.8043 0.8699 0.8650 48 0.5049 0.5787 0.5425 0.6310 0.6221 50 0.3384 0.4259 0.3612 0.4661 0.4480 52 0.2238 0.3015 0.2376 0.3242 0.3222 55 0.1178 0.1909 0.1243 0.2051 0.1990 60 0.0386 0.0880 0.0404 0.0942 0.0913

In Table 4.3, we consider also European and American put option prices calculated with the Black-Scholes (BS) models. The BS volatility is chosen equal to the VG volatility . As expected, the deep OTM (out of the money) prices computed under VG are higher than the corresponding prices computed under BS. This is a consequence of the shape of the VG density function (10), which has heavier tails than the normal distribution. This means that the probability of a deep OTM option to return in the money, is higher if calculated with the VG model than BS, and therefore we get higher option prices.

The Black-Scholes prices are computed using a binomial algorithm. For European options the prices converge to the BS closed formula prices. The same values can be obtained using the multinomial algorithm for the VG process and setting and . Recall that under the Black-Scholes model, the log-returns follow a Brownian motion. Looking at the definition of the VG process (9), it is evident that when and are zero, the process becomes a Brownian motion:

As a consequence, the price process (21) converges to the Geometric Brownian Motion:

where:

5 Finite difference approximation

Consider the VG PIDE (24):

| (42) |

We can expand using the Taylor formula up to the fourth order:

| (43) | ||||

and use the expression for the cumulants (see Appendix A). We denote with the cumulant evaluated at

| (44) |

The approximated equation is a fourth order PDE:

| (45) | |||

Consider the variable in the interval and discretize time and space, such that and for . Using the variables for and for , we use the short notation

We can use the following discretization for the time derivative, corresponding to an explicit method:

| (46) |

and the central difference for the spatial derivative:

| (47) | ||||

The discretized equation is:

| (48) | |||

Rearranging the terms we obtain:

| (49) | ||||

If we rename the coefficients, the equation is:

| (50) |

The coefficients can be interpreted as the (risk neutral) transition probabilities for the Markov chain:

It is straightforward to verify that . The space step has to to be chosen in order to satisfy the positivity condition of the transition probabilities, for . The value of the option in the previous time step is thus the discounted expectation under the risk neutral probability measure :

| (51) |

Define the increments . We check that the local properties for the moments of the Markov chain are satisfied:

| (52) | ||||

| (53) | ||||

| (54) | ||||

| (55) |

At first order in we can calculate the variance, skewness and kurtosis777Remind that and , with the central i-th moment. Remind also that and :

| (56) | ||||

| (57) | ||||

| (58) |

For , we confirm that the local variance, skewness and kurtosis are consistent with their definition in terms of cumulants.

We expect that the transition probabilities in (34) obtained by moment matching, can be recovered from the probabilities in (50) obtained by finite difference discretization, for a particular choice of the space step . We have not solved this issue yet, and we think it can be a topic for further research.

6 Conclusions

This article proposes a method to price options using a multinomial method when the underlying price is modeled with a Variance Gamma process. The multinomial method is well known in the literature, see for example [8], [16] ,[25], [26] and [27], but in this work we focus the analysis only on the VG process and compare our numerical results with other different methods.

The VG process is approximated by a general jump process that has the same first four cumulants of the original VG process. We proved that the multinomial method converges to this approximated process. We obtained numerical results for European and American options, and compared them with PIDE methods and with results computed within the Black Scholes framework. It turns out that the multinomial method is easier to implement than the finite differences method. The algorithm does not involve any matrix multiplication or matrix inversion as in the case of implicit/explicit method for PIDEs. This means that the computational time is much smaller.

We proposed a topic of further investigation in Section 5. The probabilities obtained by discretizing the approximated PDE are related with the probabilities obtained by moment matching for a particular choice of the space step parameter. Another possible topic of further research is the comparison of our results for American options with other numerical methods such as the Least Square Monte Carlo ([17]).

Acknowledgements

Our sincere thanks are for the Department of Mathematics of ISEG and CEMAPRE, University of Lisbon, http://cemapre.iseg.ulisboa.pt/. This research was supported by the European Union in the FP7-PEOPLE-2012-ITN project STRIKE - Novel Methods in Computational Finance (304617), and by CEMAPRE MULTI/00491, financed by FCT/MEC through Portuguese national funds. We wish also to acknowledge all the members of the STRIKE network, http://www.itn-strike.eu/.

Appendix A Poisson integration

A convenient tool to analyze the jumps of a Lévy process is the random measure of jumps. Within this formalism it is possible to describe jump processes with infinite activity, as the VG process. The jump process associated to the Lévy process is defined, for each , by:

| (59) |

where . Consider the set , the random measure of the jumps of is defined by:

| (60) | ||||

This measure counts the number of jumps of size in , up to time . We say that is bounded below if (zero does not belong to the closure of ). If is bounded below, then and is a Poisson process with intensity

| (61) |

(see [4] theorem 2.3.4 and 2.3.5). If is not bounded below, it is possible to have and is not a Poisson process because of the accumulation of infinite numbers of small jumps. The process is called Poisson random measure. The Lévy measure corresponds to the intensity of the Poisson measure. The Compensated Poisson random measure is defined by

| (62) |

which is a martingale.

The next step is to define the integration with respect to a random measure. Following [4], let be a Borel-measurable function. For any bounded below, we define the Poisson integral of as:

| (63) |

For the case of integration of the identity function, we see that every compound Poisson process can be represented by:

| (64) |

We can also define in the same way the compensated Poisson integral with respect the compensated Poisson measure. We can further define:

| (65) |

that represent the compensated sum of small jumps.

We present a last formula for computing the moments of a general compound Poisson process. Let be a measurable function such that , and , the characteristic function of is:

| (66) | ||||

Assuming that , all the moments can be computed from (66) by differentiation using eq:

| (67) |

For the case of identity function, , and satisfying the integrability conditions, using (70) we derive the expression for the cumulants:

| (68) |

The cumulants of are thus the moments of its Lévy measure.

Appendix B Cumulants

The cumulant generating function of is defined as the natural logarithm of its characteristic function (see [8]). Using the Lévy-Khintchine representation for the characteristic function (1), it is easy to find its relation with the Lévy symbol:

| (69) | ||||

The cumulants of a Lévy process are thus defined by:

| (70) |

The cumulants are closely related to the central moments :

| (71) |

For a Poisson process with finite firsts moments, all the information about the cumulants is contained inside the Lévy measure. Expand in Taylor series the exponential

The Lévy symbol from the representation (7) becomes:

| (72) | ||||

with .

References

- Ait-Sahalia and Jacod, [2012] Ait-Sahalia, Y. and Jacod, J. (2012). Analyzing the spectrum of asset returns: Jump and volatility components in high frequency data. Journal of Economic literature, 50(4):1007–1050.

- Almendral, [2005] Almendral, A. (2005). Numerical valuation of american options under the CGMY process. Eds., Exotic Option Pricing and Advanced Levy Models, Wiley, Hoboken.

- Almendral and Oosterlee, [2007] Almendral, A. and Oosterlee, C. W. (2007). On American options under the Variance Gamma process. Applied Mathematical Finance, 14(2):131–152.

- Applebaum, [2009] Applebaum, D. (2009). Lévy Processes and Stochastic Calculus. Cambridge University Press; 2nd edition.

- Barndorff-Nielsen, [1998] Barndorff-Nielsen (1998). Processes of Normal inverse Gaussian type. Finance and Stochastics, 2:41–68.

- Black and Scholes, [1973] Black, F. and Scholes, M. (1973). The pricing of options and corporate liabilities. The Journal of Political Economy, 81(3):637–654.

- Carr and Madan, [1998] Carr, P. and Madan, D. (1998). Option valuation using the Fast Fourier transform. Journal of Computational Finance, 2:61–73.

- Cont and Tankov, [2003] Cont, R. and Tankov, P. (2003). Financial Modelling with Jump Processes. Chapman and Hall/CRC; 1 edition.

- Cont and Voltchkova, [2005] Cont, R. and Voltchkova, E. (2005). A finite difference scheme for option pricing in jump diffusion and exponential Lévy models. SIAM Journal of numerical analysis, 43(4):1596–1626.

- Cox et al., [1979] Cox, J., Ross, S., and Rubinstein, M. (1979). Option pricing: A simplified approach. Journal of financial economics, 7:229–263.

- Eberlein and Keller, [1995] Eberlein, E. and Keller, U. (1995). Hyperbolic distributions in finance. Bernoulli, 1(3):281–299.

- Fu, [2000] Fu, M. C. (2000). Variance-Gamma and Monte Carlo. Advances in Mathematical Finance., pages 21–34.

- Geman et al., [1998] Geman, H., Madan, D., and Yor, M. (1998). Asset prices are Brownian motion: only in business time. Quantitative Analysis in Financial Markets: Collected Papers of the New York University Mathematical Finance Seminar, 2(1):103–146.

- Hainaut and MacGilchrist, [2010] Hainaut, D. and MacGilchrist, R. (Winter 2010). An interest tree driven by a lévy process. The Journal of Derivatives, 18(2):33–45.

- Hirsa and Madan, [2001] Hirsa, A. and Madan, D. (2001). Pricing American options under Variance Gamma. Journal of Computational Finance, 7.

- Kellezi and Webber, [2006] Kellezi, E. and Webber, N. (2006). Valuing Bermudan options when asset returns are Lévy processes. Quantitative Finance, 4(1):87–100.

- Longstaff and Schwartz, [2001] Longstaff, F. A. and Schwartz, E. S. (2001). Valuing American options by simulation: A simple Least-Squares approach. Review of Financial Studies, pages 113–147.

- Madan et al., [1998] Madan, D., Carr, P., and Chang, E. (1998). The Variance Gamma process and option pricing. European Finance Review, 2:79–105.

- Madan and Milne, [1991] Madan, D. and Milne, F. (1991). Option pricing with V.G. martingale components. Mathematical Finance, 1:39–55.

- Madan and Seneta, [1990] Madan, D. and Seneta, E. (1990). The Variance Gamma (V.G.) model for share market returns. The journal of Business, 63(4):511–524.

- Maller et al., [2006] Maller, R., Solomon, D., and Szimayer, A. (2006). A multinomial approximation for american option prices in levy process models. Mathematical Finance, 16(4):613–633.

- Sato, [1999] Sato, K. I. (1999). Lévy processes and infinitely divisible distributions. Cambridge University Press.

- Seneta, [2004] Seneta, E. (2004). Fitting the Variance-Gamma model to financial data. Journal of Applied Probability, 41:177–187.

- Ssebugenyi and Konlack, [2013] Ssebugenyi, C.S. Mwaniki, I. and Konlack, V. (2013). On the minimal entropy martingale measure and multinomial lattices with cumulants. Applied Mathematical Finance, 20(4):359–379.

- Yamada and Primbs, [2001] Yamada, Y. and Primbs, J. (2001). Construction of multinomial lattice random walks for optimal hedges. Proc. of the 2001 international conference of Computational Science, pages 579–588.

- Yamada and Primbs, [2003] Yamada, Y. and Primbs, J. (2003). Mean square optimal hedges using higher order moments. Proc of the 2003 international conference on Computational Intelligence for Financial Engineering.

- Yamada and Primbs, [2004] Yamada, Y. and Primbs, J. (2004). Properties of multinomial lattices with cumulants for option pricing and hedging. Asia-Pacific Financial Markets, 11:335–365.