1in1in1in1in

Path stability of the solution of stochastic differential equation driven by time-changed Lévy noises

Abstract.

This paper studies path stabilities of the solution to stochastic differential equations (SDE) driven by time-changed Lévy noise. The conditions for the solution of time-changed SDE to be path stable and exponentially path stable are given. Moreover, we reveal the important role of the time drift in determining the path stability properties of the solution. Related examples are provided.

Keywords: Path stability;exponential path stability; time-changed Lévy noise; SDEs driven by time-changed Lévy; Lyapunov function method.

1. Introduction

Study of stochastic differential equations (SDE) is a mature field of research. Numerous types of SDEs have been used to model different phenomena in various areas, such as unstable stock prices in finance [11], dynamics of biological systems [4], and Kalman filter in navigation control. In 1892, Lyapunov [8] introduced the concept of stability of a dynamical system. Since then, the concept of stability have been studied widely in different senses, including stochastical stability, almost sure stability, exponential stability, etc. In [9], Mao investigated various types of stabilities for the following SDE

| (1.1) |

with , where is the standard Brownian motion.

Siakalli [14] extended Mao’s results to SDEs driven by Lévy noise

| (1.2) |

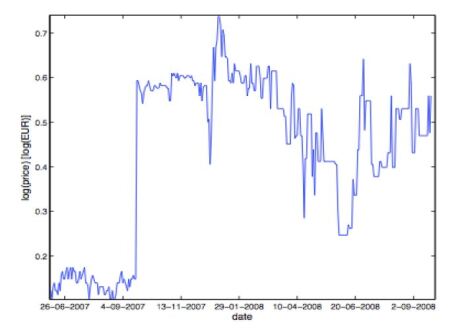

with , where is the compensated Poisson measure. This type of SDEs provide as a tool of modeling the price of financial assets with continuous change. However, we also observe such special behavior in financial market that prices are on the same level during a period of time, see Figure 1. But this phenomena can be modeled by the time-changed SDEs, which allow more flexibility in modelling and thus become popular among researchers, see [13] and [15].

Kobayashi [6] introduced the duality theorem between time-changed SDEs and the corresponding non-time-changed SDEs, and established the Itô formula for time-changed SDEs. Soon after Kobayashi’s fruitful results, Wu [15] established the stochastic and moment stabilities of the solution to the SDEs driven by time-changed Brownian motion

| (1.3) |

with , where is specified as the inverse of an -stable subordinator, . In our recent paper [12], we focus on the following time-changed SDE

| (1.4) | ||||

with , where is the inverse of a strictly increasing subordinator, and discuss stability of its solution in probability and moment senses, including stochastical stability, stochastical asymptotic stability, global stochastic asymptotic stability, th moment exponential stability and th moment asymptotic stability.

In this paper, we analyze the path stabilities of the solution to (1.4) and the following stochastic differential equation with linear jumps

| (1.5) | ||||

with , where is the inverse of a ”mixed” subordinator.

In the remaining parts of this paper, further needed concepts and related background will be given in section 2. In section 3, the conditions for the solution to our target time-changed SDEs to be almost sure exponential path stability and almost sure path stability will be given. Connections between stability of the solution to time-changed SDE and that of the corresponding non-time-changed SDE will be disclosed and some examples will be provided.

2. Preliminaires

Let be a filtered probability space satisfying usual hypotheses of completeness and right continuity. Assume that -adapted Poisson random measure on is independent of the drift and the standard Brownian motion, define its compensator , where is a Lévy measure satisfying .

Let be a RCLL increasing Lévy process that is called subordinator starting from 0 with Laplace transform

| (2.1) |

where Laplace exponent .

Define its inverse

| (2.2) |

The concept of regular variation is needed to introduce the mixed stable subordinator. A measurable function R is regularly varying at infinity with exponent , denoted by , if R is eventually positive and as , for any . Similarly, a measurable function R is regularly varying at zero with exponent , denoted by , if R is positive in some neighborhood of zero and as , for any .

Given a measurable function such that for some , let and . Without loss of generality, let , then is a probability density of Lévy measure of the -stable subordinators. Let be a subordinator such that has Lévy-Khinchin representation and the Lévy measure is defined as , then is the so called ”mixed” stable subordinator. In this case the Laplace exponent is given by

| (2.3) |

By Theorem 3.9 in [10], there exists a function such that

| (2.4) |

We require in (1.4) and (1.5) to be real-valued functions and satisfy the following Lipschitz condition in Assumption 2.1, growth condition in Assumption 2.2 and Assumption 2.3. Under these assumptions, by Lemma 4.1 in [6], both of the equations (1.4) and (1.5) have unique -adapted solution processes .

Assumption 2.1.

(Lipschitz condition) There exists a positive constant such that

| (2.5) | ||||

for all and .

Assumption 2.2.

(Growth condition) There exists a positive constant such that, for all and ,

| (2.6) |

Assumption 2.3.

If is right continuous with left limits (rcll) and a -adapted process, then

| (2.7) |

where denotes the class of rcll and -adapted processes.

Note that the Stochastic differential equation (1.4) involves only Lévy process with small jumps and general scalars for the drift and the standard Brownian motion and Poisson jump; while the linear stochastic differential equation (1.5) contains both small and large Poisson jumps with linear scalars. Next, we define two different types of stability.

Definition 2.4.

Definition 2.5.

The trivial solution of the time-changed SDE (1.4) is said to be almost surely path stable if there exists a function such that

| (2.9) |

and

| (2.10) |

for all .

The Itô formula is heavily used in our proofs. We derive the following Itô formula for time-changed Lévy noise and will utilize it frequently in the remaining sections.

Lemma 2.6.

(Itô formula for time-changed Lévy noise) Let be a rcll subordinator and its inverse process . Define a filtration by . Let be a process satisfying the following:

| (2.11) | ||||

where are measurable functions such that all integrals are defined, is a positive constant.

Then, for all in , we have with probability one,

| (2.12) | ||||

where

| (2.13) | ||||

Note that the proof of the Itô formula for time-changed Lévy noise follows by similar ideas as in the proof of Lemma 3.1 in [12], thus the details are omitted. To perform future analysis, we need some conditions under which the solutions of (1.4) can not reach the origin after certain time given that .

Assumption 2.7.

For any there exists , such that

| (2.14) |

and

| (2.15) |

Proof.

We follow the idea in the proof of Lemma 3.4.4 in [14] and prove this result by contradiction. Suppose that (2.16) is not true, that is, there exists initial condition and stopping time with where

| (2.17) |

Since the paths of are right continuous with left limit (rcll), there exist and sufficiently large such that , where

| (2.18) |

Next, define another stopping time

| (2.19) |

for each .

Let be a constant and define . Since is except at , and by definition of , will not reach 0 for , so Itô formula can be applied to .

The penultimate inequality is derived from lemma 3.4.2 on page 54 of [14], which states that for , thus

| (2.21) | ||||

Observe that the last two terms in the last line of the inequality (2.20) are martingales. Then by taking expectations of both sides, we derive that

| (2.22) |

If , then and , then

| (2.23) |

Recall the reverse Hölder’s inequality: for all

We use the reverse Hölder’s inequality with , and . Since , this gives

Since the inverse subordinator has finite exponential moment, is finite for any fixed time , see Lemma 8 in [5]. Then, letting , we obtain , which contradicts the assumption, thus the desired result is correct. ∎

Remark 2.9.

When the Laplace exponent of the subordinator is given by (2.3), an alternative method to show that the expectation is finite is to use the moments of . Since is nonnegative and nondecreasing, we have . Because , is a strictly positive and increasing function, . Thus, it is sufficient to show that is finite. By Theorem 3.9 in [10], there exists a function such that for any , and sufficiently large ,

| (2.24) |

By Taylor expansion and Fubini theorem,

| (2.25) | ||||

Hence, for fixed large , is finite.

Lemma 2.10.

(Time-Changed Exponential Martingale Inequality)

Let be a rcll subordinator and its inverse process . Let T, be any positive numbers, . Assume and satisfy and , then

| (2.27) | ||||

Proof.

Define a sequence of stopping times as below

| (2.28) | ||||

Note that as a.s.

Define the following Itô process

| (2.29) | ||||

with for all . Then for all

| (2.30) | ||||

Let , by the time-changed Itô’s formula (2.12),

| (2.31) | ||||

thus is a local martingale. Since we have

| (2.32) |

there exists a sequence of stopping times with as such that for all

| (2.33) |

By Dominated Convergence Theorem, we have

| (2.34) |

that is, is a martingale for all with .

Apply Doob’s martingale inequality

| (2.35) |

equivalently,

| (2.36) |

writing explicitly, we have

| (2.37) | ||||

Define

| (2.38) | ||||

then .

Since

| (2.39) |

and

| (2.40) |

also

| (2.41) |

where

| (2.42) | ||||

thus

| (2.43) |

∎

The next result can be considered as a strong law of large numbers for the inverse subordinator.

Lemma 2.11.

Proof.

Fix and define

| (2.45) |

then, by Markov’s inequality and equation (2.4), as , for some ,

| (2.46) | ||||

By the ratio test, . Applying Borel-Cantelli lemma, we have

| (2.47) |

∎

Remark 2.12.

Lemma 2.11 can also be proved for discrete case with the help of Laplace transform. Let be an inverse of the subordinator with Laplace exponent , where and . Then the Laplace transform of the moment of is .

By a Karamata Tauberian theorem (see [2], Theorem 1 and Lemma on pp. 443-446), since as then as . Utilizing this result, , thus . Applying Borel-Cantelli lemma, we have

Remark 2.13.

We believe that Lemma 2.11 should hold for the inverse of any strictly increasing subordinator. But we could not prove this in this paper. We are missing the moment asymptotics for the inverse of any strictly increasing subordinator. We will work on this result in a future project.

3. Main Results

In this section, we will analyze conditions for almost sure exponential path stability and almost sure path stability for the SDEs in equations (1.4) and (1.5), followed by some examples.

3.1. Stochastic Differential Equations driven by Time-Changed Lévy Noise with Small Jumps

Theorem 3.1.

Suppose that Assumption 2.7 holds. Let and let such that for all and ,

| (3.1) |

Then when and a.s.,

| (3.2) |

and if , the trivial solution of (1.4) is almost surely exponentially path stable; when (i.e. no time drift in the SDE),

| (3.3) |

and if , the trivial solution of (1.4) is almost surely path stable.

Proof.

Define

| (3.7) | ||||

then, applying conditions (ii) and (iii),

| (3.8) | ||||

By exponential martingale inequality (2.27), for where and . Then for every integer , we find that

| (3.9) | ||||

Since , by Borel-Cantelli lemma , we have

| (3.10) | ||||

Hence for almost all there exists an integer such that for all , ,

| (3.11) | ||||

Thus,

| (3.12) | ||||

for .

Letting , we have

| (3.13) |

The details can be found in Theorem 3.4.8 in Siakalli’s [14] with certain simple modifications. By condition (v), , thus applying condition (i)

| (3.14) |

| (3.16) |

When , then , thus

| (3.17) |

consequently,

| (3.18) |

∎

Remark 3.2.

From the proof of the previous theorem, when , we can deduce the following. When a.s., the following estimation is also true.

| (3.19) |

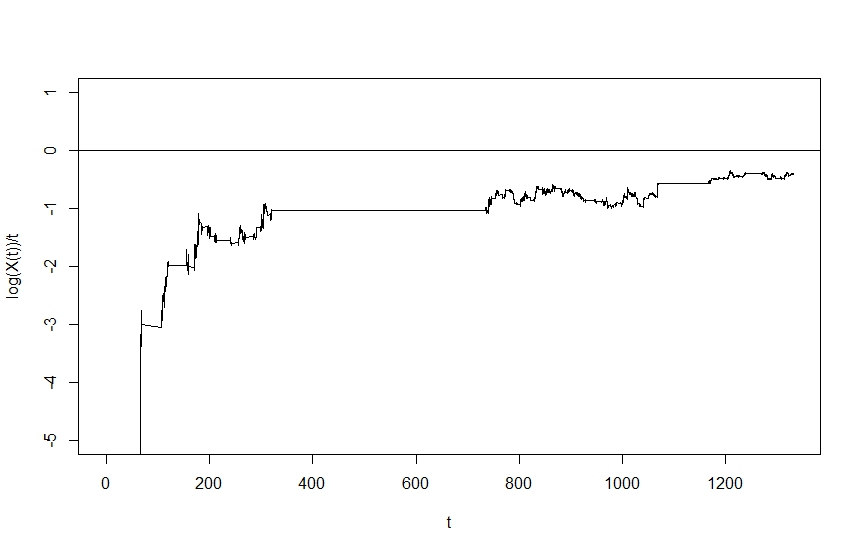

Example 3.3.

Consider the following stochastic differential equation

| (3.20) |

with , is uniform distribution .

Choose the Lyapunov function as which satisfies the conditions (i) and (ii) in Theorem 3.1. Furthermore,

| (3.21) | ||||

The last inequality is derived by the following argument, Let , then for and for . Thus , for . Since is assumed to be the standard normal distribution, Thus,

In addition, and

| (3.22) | ||||

Similar as above, the last inequality can be proved as following. Let , then for and for . Thus

| (3.23) | ||||

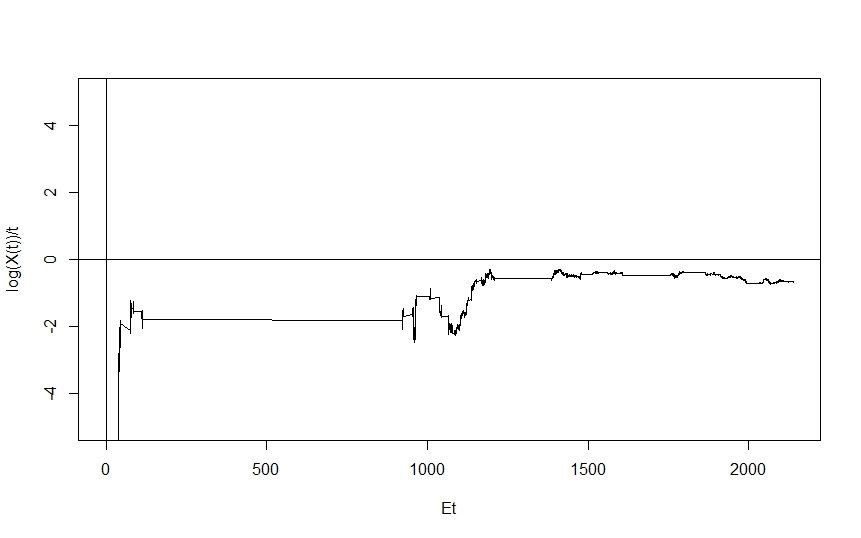

The constants of Theorem 3.1 are , then , thus the trivial solution of stochastic differential equation (3.20) is almost surely path stable. A simulation of a path of SDE in equation (3.20) is given in Figure 2, it can be observed that is strictly below when is large, which illustrates our analysis above.

Remark 3.4.

Remark 3.5.

In the figures of all examples, we assume that is the inverse of stable subordinator with parameter .

3.2. Stochastic Differential Equation (1.5) driven by Time-Changed Lévy Noise including Large Jumps

First, let us discuss exponential stability of the following time-changed SDE with noise that has only small linear jump

| (3.24) | ||||

with , which is a special case of (1.4) when . Then we extend (3.24) to (1.5) by adding large jumps .

Assumption 3.6.

| (3.25) |

for all .

Theorem 3.7.

Given Assumptions 2.7 and 3.6, suppose that there exist such that the following conditions

| (3.26) | ||||

are satisfied for all and . Then when and a.s., we have

| (3.27) |

for any , the trivial solution of (3.24) is almost surely exponential path stable if ; when , we have

| (3.28) |

for any , the trivial solution of (3.24) is almost surely path stable if .

Proof of Theorem 3.7.

Fix , then by Itô formula for time-changed SDE, see Lemma 3.1 in [12], we have

| (3.29) | ||||

where

| (3.30) |

| (3.31) | ||||

| (3.32) | ||||

Note that both

| (3.33) |

and

| (3.34) |

are martingales.

Now,

| (3.35) | ||||

Define corresponding non-time-changed stochastic process by

| (3.36) |

with . By the duality theorem 4.2 in [6], for .

By the result on page 282 in Mao [9],

| (3.37) | ||||

Define , then

| (3.38) |

then

| (3.39) |

By Theorem 10 of Chapter 2 in [7],

| (3.40) |

Similarly,

| (3.41) | ||||

so

| (3.42) |

As a result,

| (3.43) |

In the end, since

| (3.44) |

and

| (3.45) | ||||

thus,

| (3.46) |

When ,

| (3.47) |

thus,

| (3.48) |

∎

Other than the direct proof above, the following is an alternative proof utilizing Theorem 3.1.

Alternate Proof of Theorem 3.7.

Let , then and condition (i) in Theorem 3.1 is satisfied.

Next, by applying the time-changed Itô formula to , , thus condition (ii) in Theorem 3.1 is satisfied;

| (3.49) | ||||

thus, condition (iii) in Theorem 3.1 is satisfied by Assumption 3.6 and setting .

Condition (iv) is satisfied since

| (3.50) |

For the last condition (v), by denoting we have

| (3.51) | ||||

Since all five conditions in Theorem 3.1 are satisfied, we have that when ,

| (3.52) |

and that when ,

| (3.53) | ||||

as desired.

∎

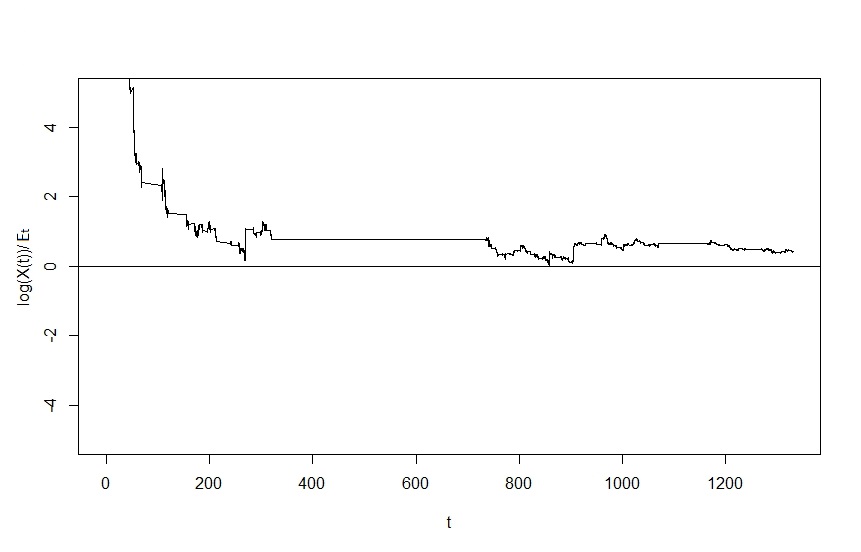

Example 3.8.

Consider the following stochastic differential equation

| (3.54) |

with , is uniform distribution .

Applying Theorem 3.7, , and , thus .

| (3.55) | ||||

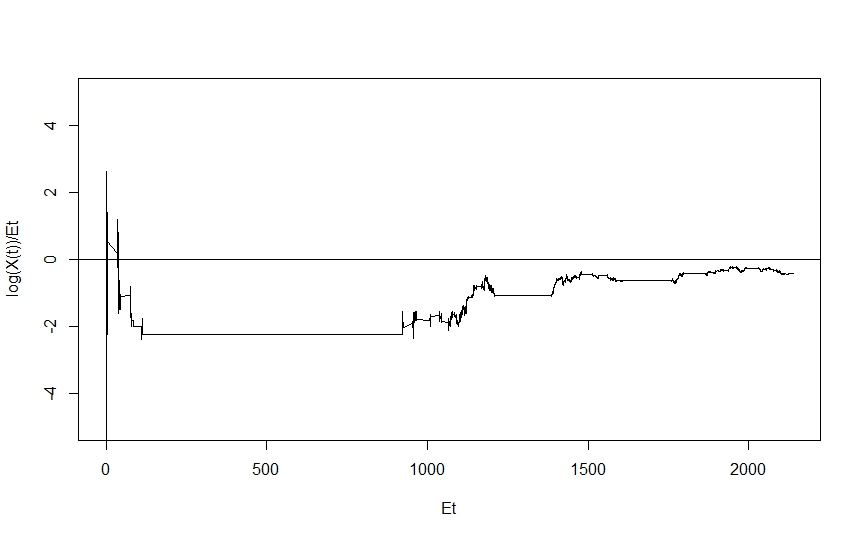

Hence, stochastic differential equation (3.54) is almost surely path stable. The simulated path of SDE (3.54) is given in Figure 3. The ratio of is strictly below for large time t, this is consistent with above analysis.

Next, we analyze the following time-changed stochastic differential equation involving large jumps,

| (3.56) |

with and is a measurable function.

Before stating the next theorem, we need another assumption, see [14].

Assumption 3.9.

Assume that

| (3.57) |

and that for .

By above assumption, the function satisfies Lipschitz and growth conditions, assuring the existence and uniqueness of solution to equation (3.56). In addition, implies that , this is an application of interlacing technique in [1], details can be found in Lemma 4.3.2 in [14] with simple modification.

Theorem 3.10.

Proof.

Fix , apply Itô formula (2.12) to , then for any ,

| (3.60) | ||||

Let , similar ideas as in the proof of the corresponding inequality for in the proof of Theorem (3.7), we have

| (3.61) |

thus

| (3.62) | ||||

∎

Next, by similar ideas as the proof of Theorem 4.6.1 in [14], it is not difficult to derive the following theorem for the following time-changed SDE

| (3.63) | ||||

with .

Theorem 3.11.

Given assumptions 2.7, 3.6 and 3.9, suppose that there exist such that the following conditions

| (3.64) | ||||

are satisfied for all and . Then when and a.s., we have

| (3.65) |

for any , the trivial solution of (1.5) is almost surely exponentially path stable if ; when , we have

| (3.66) |

where , for any , and the trivial solution of (1.5) is almost surely path stable if .

Remark 3.12.

Next, we list some examples to illustrate the results of above theorems.

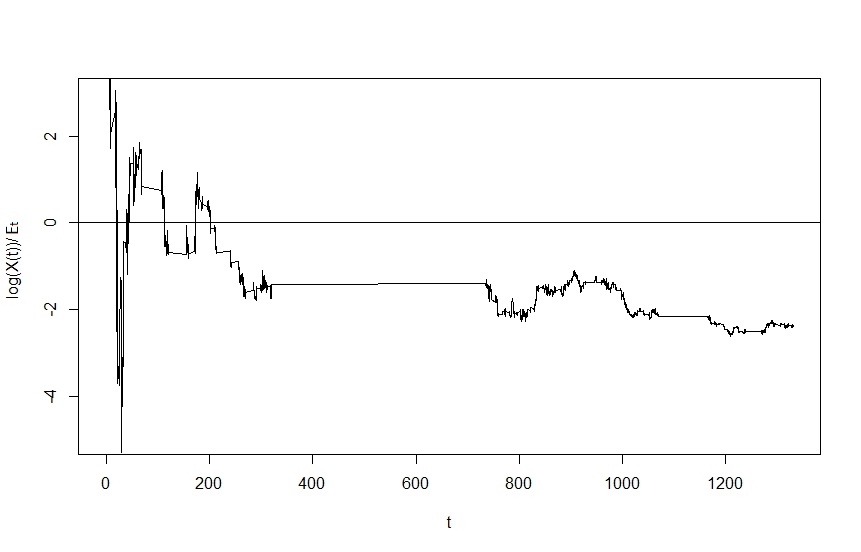

Example 3.13.

Consider the following two stochastic differential equations

| (3.67) |

with and is standard normal distribution,

and

| (3.68) | ||||

with and is standard normal distribution.

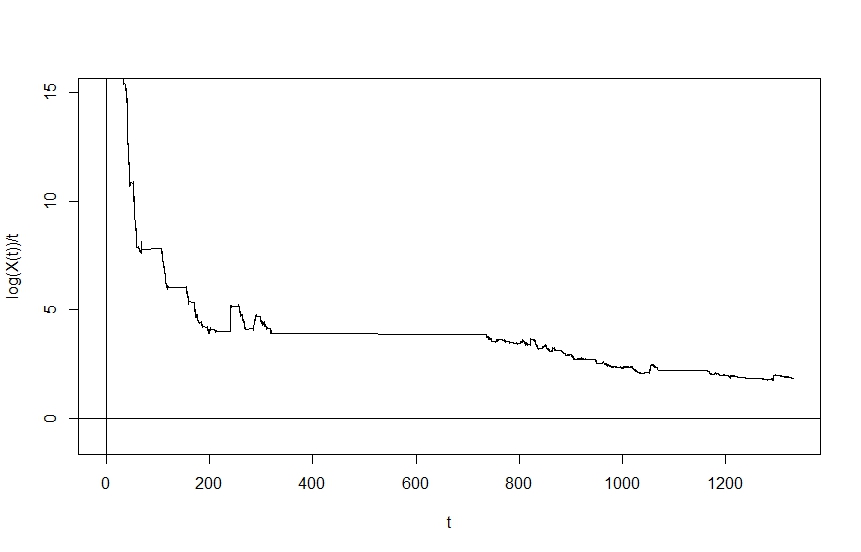

Figure 4 illustrates that stochastic differential equation (3.67) is not almost surely exponentially path stable, this is because ”dt” component exists in the linear stochastic system, such component plays dominant role in determining almost sure exponential path stability and has positive scalar 1, thus , this is not enough for almost sure exponential path stability.

Example 3.14.

Consider following two stochastic differential equations

| (3.69) | ||||

with , and

| (3.70) | ||||

with .

In both of the equations (3.69) and (3.70), component is missing, thus almost sure exponential path stability is no longer possible. However, almost sure path stability is possible, depending on the scalars of time-changed drift, Brownian motion, and Possion jump.

References

- [1] D. Applebaum. Lévy processes and stochastic calculus, Cambridge University Press, 2009.

- [2] W. Feller. An Introduction to Probability Theory and Its Applications, 2nd ed., vol. II, Wiley, New York, 1971.

- [3] J. Janczura and A. Wyloma nska. Subdynamics of financial data from fractional Fokker-Planck equation, Acta Physica Polonica B 40 (2009) 1341 -1351.

- [4] S.K. Jha, C.J. Langmead. Exploring behaviors of stochastic differential equation models of biological systems using change of measures, BMC bioinformatics Vol 13 (2012): 1.

- [5] E. Jum, and K. Kobayashi. A strong and weak approximation scheme for stochastic differential equations driven by a time-changed Brownian motion, arXiv preprint arXiv:1408.4377, (2014).

- [6] K. Kobayashi. Stochastic calculus for a time-changed semimartingale and the associated stochastic differential equations, Journal of Theoretical Probability 24.3 (2011): 789–820.

- [7] R.Sh. Liptser and A.N. Shiryayev. Theory of martingales, Kluwer Academic Publishers Group, Dordrecht, 1989.

- [8] A. M. Lyapunov. The general problem of the stability of motion, International Journal of Control 55.3 (1992): 531–534.

- [9] X. Mao. Stochastic differential equations and applications, Horwood Publishing Limited, Chichester, 2008.

- [10] M. M. Meerschaert and H. P. Scheffler. Stochastic model for ultraslow diffusion, Stochastic processes and their applications 116.9 (2006): 1215–1235.

- [11] R.C. Merton. Option pricing when underlying stock returns are discontinuous, Journal of financial economics 3.1-2 (1976): 125–144.

- [12] E. Nane and Y. Ni. Stability of stochastic differential equation driven by time-changed Lévy noise, Proceedings of the American Mathematical Society (to appear), 2016.

- [13] F. Shokrollahi, A. Kilicman and M. Magdziarz. Pricing European options and currency options by time changed mixed fractional Brownian motion with transaction costs, International Journal of Financial Engineering, Vol 3 (2016), no.1, 1650003 (20 pages).

- [14] M. Siakalli. Stability properties of stochastic differential equations driven by L vy noise, Diss. University of Sheffield, 2009.

- [15] Q. Wu. Stability of stochastic differential equations with respect to time-changed Brownian motions, arXiv preprint arXiv:1602.08160 (2016).