Instrumental Variable Quantile Regression with Misclassification††thanks: First version: October, 2016. I am grateful to Peter C. B. Phillips, Arthur Lewbel and four anonymous referees for comments and suggestions that have significantly improved this paper. I would like to thank Alexandre Belloni, Stéphane Bonhomme, Federico A. Bugni, A. Colin Cameron, V. Joseph Hotz, Shakeeb Khan, Jia Li, Matthew A. Masten, Arnaud Maurel, Adam M. Rosen, and seminar participants at Duke, UC Berkeley, Shanghai University of Finance and Economics, Hakodate Conference in Econometrics, IAAE Annual Conference, Econometric Society North American Summer Meeting, and Econometric Society Asian Meeting for very helpful comments. The usual disclaimer applies.

Abstract

This paper investigates the instrumental variable quantile regression model (Chernozhukov and Hansen, 2005, 2013) with a binary endogenous treatment. It offers two identification results when the treatment status is not directly observed. The first result is that, remarkably, the reduced-form quantile regression of the outcome variable on the instrumental variable provides a lower bound on the structural quantile treatment effect under the stochastic monotonicity condition (Small and Tan, 2007; DiNardo and Lee, 2011). This result is relevant, not only when the treatment variable is subject to misclassification, but also when any measurement of the treatment variable is not available. The second result is for the structural quantile function when the treatment status is measured with error; the sharp identified set is characterized by a set of moment conditions under widely-used assumptions on the measurement error. Furthermore, an inference method is provided in the presence of other covariates.

-

Keywords: Misclassification; Instrumental variable quantile regression; Partial identification; Binary endogenous treatment

1 Introduction

The instrumental variable quantile regression model (Chernozhukov and Hansen, 2005, 2013) aims to investigate heterogeneous treatment effects in the presence of an endogenous binary treatment variable. In many empirical applications, the treatment variable is potentially mismeasured, so it is empirically relevant how researchers can use the instrumental variable quantile regression model with a mismeasured treatment variable. For example, Chernozhukov and Hansen (2004) use the instrumental variable quantile regression model to investigate the quantile treatment effect of 401(k) participation on saving behaviors, but the pension plan type is subject to measurement error in survey datasets. Using the Health and Retirement Study, Gustman et al. (2008) estimate that around one-fourth of the survey respondents misclassified their pension plan type. To the best of my knowledge, however, no paper has investigated the instrumental variable quantile regression model when a binary regressor is potentially misclassified and endogenous.

This paper has two identification results on the structural quantile function under the rank similarity condition.111Wüthrich (2019) investigates the instrumental variable quantile regression model without the rank similarity condition and characterizes the estimand of Chernozhukov and Hansen (2005) when the rank similarity condition fails. Dong and Shen (2018), Frandsen and Lefgren (2018), Kim and Park (2018), and Yu (2017) propose a test for the rank invariance or similarity condition. The first identification result considers a reduced-form parameter, that is, the coefficient of the instrumental variable when running the quantile regression of the outcome variable on the instrumental variable. Under the rank similarity condition and the stochastic monotonicity condition (Small and Tan, 2007; DiNardo and Lee, 2011), this reduced-form parameter can be used as a lower bound for the structural quantile treatment effect. Although it has been used by empirical studies (e.g., Bitler et al., 2016), the reduced-form quantile regression on the instrumental variable has not been formally related to the structural quantile treatment effect. Moreover, this result does not depend on the treatment variable or its measurement, and therefore it is relevant even when a measurement does not exist.

The second identification result is to derive moment conditions for the structural quantile function when the treatment variable is measured with exogenous errors. The exogeneity of the measurement error is widely assumed in the measurement error literature (e.g., Bound et al., 2001) and yields exclusion restrictions similar to Henry et al. (2014). Given the structure of the moment conditions, the structural quantile function can be under-identified even if the order condition for point identification holds. In other words, additional assumptions or variables are necessary to achieve point identification for the structural quantile function. As an example of additional restrictions, this paper considers two observed measurements for one latent treatment variable, and point-identify the structural quantile function. Point identification results from combining two existing methods: misclassification correction techniques (Mahajan, 2006; Lewbel, 2007; Hu, 2008), and the identification results in Chernozhukov and Hansen (2005, 2013).

Based on the partial identification result, an inference method for the structural quantile function is provided by incorporating the misclassification probabilities in the inference method of Chernozhukov and Hansen (2008). The proposed inference method can include covariates other than the treatment variable, and it is computationally feasible by imposing a linear-in-parameters structure on the structural quantile function. Simulation studies and an empirical illustration demonstrate the finite sample performance for the proposed inference method.

Related to this paper, several papers have considered the problem of mis-measured regressors in the quantile regression framework, e.g., Chesher (1991, 2017), Schennach (2008), Galvao and Montes-Rojas (2009), Wei and Carroll (2009), Firpo et al. (2017), and Song (2018). They focus on the case in which the mismeasured regressor is continuously distributed, whereas this paper focuses on a binary treatment variable in which the measurement error has to be nonclassical.

Mahajan (2006), Lewbel (2007), and Hu (2008) consider identification of the average treatment effect (or, more generally, the conditional density function of the outcome variable given the true treatment variable) when a discrete treatment variable is mismeasured. Their identification strategy is based on the assumption that the true treatment variable (or the individual treatment effect in Lewbel, 2007) is exogenous, and there is no straightforward way to modify their results to the endogenous treatment.

Calvi et al. (2017); Yanagi (2019); Ura (2018) investigate the local average treatment effect model with a mismeasured binary treatment. The local average treatment effect model is also a model for heterogeneous treatment effects in the presence of endogeneity but has a different structure than the instrumental variable quantile regression model.

Frazis and Loewenstein (2003), DiTraglia and García-Jimeno (2019) and Nguimkeu et al. (2019) study a linear regression model in which a binary regressor is potentially misclassified and endogenous. Their approach is based on a homogenous treatment effect, which does not hold in the quantile treatment effect framework.

The remainder of this paper is organized as follows. Section 2 introduces the instrumental variable quantile regression model (Chernozhukov and Hansen, 2005, 2013) with a misclassified treatment variable. Section 3 studies the reduced-form quantile regression of the outcome variable on the instrumental variable. Section 4 presents the identified set for the structural quantile function. Section 5 proposes an inference method based on the identification analysis in Section 4. Section 6 provides an empirical illustration and simulation studies. Section 7 concludes. The appendix includes the proofs and additional results.

The rest of this paper uses the following notations. denotes the true probability measure for the observed and unobserved random variables. is the -th conditional quantile of a continuous random variable given a random variable . is the conditional cumulative distribution function of a random variable given a random variable . is the conditional probability density function of a random variable given a random variable .

2 Instrumental variable quantile regression model with misclassification

This section presents notations and assumptions that are essentially those of the instrumental variable quantile regression model (Chernozhukov and Hansen, 2005, 2013), though the treatment variable is not observed in this paper. For the sake of simplicity, covariates are omitted other than the treatment variable when analyzing the identification problem. In the instrumental variable quantile regression model, is an outcome variable, is a binary (true but latent) treatment variable taking values in , and is an instrumental variable. means that the individual is treated; otherwise, .

In Chernozhukov and Hansen (2004) and Section 6.1 of this paper, the outcome variable is the net amount of financial assets in dollars, the treatment variable is the participation status in a 401(k) program, and the instrumental variable is the 401(k) eligibility indicator of whether an employer offers a 401(k) program to employees.

The goal of this paper is to investigate treatment effects of on . The error term and the (unknown) structural quantile function are used to model the relationship between the outcome variable and the binary treatment variable :

The random variable is the potential outcome variable when . The parameter of interest is the -th quantile of the counterfactual outcome variable, , for a given value of .

To identify even partially, it is necessary to impose some structure on the unknown function, , and on the unobserved variable, . The following assumptions are based on Chernozhukov and Hansen (2005, 2013). Unlike their papers, the condition is local at the given value of , which is sufficient for deriving the testable implication in Chernozhukov and Hansen (2005, Theorem 1) for the structural quantile function at .222The local restriction is a weaker condition than full independence between and (Chesher, 2003). Technically speaking, ’s are not necessarily uniform random variables in this paper since the assumptions are only about the given value of , but the subsequent discussions in terms of the quantile treatment effect hold only when ’s are uniform random variables.

Assumption 1.

The mapping is strictly increasing and left-continuous for every , and has the inverse .

Assumption 2.

(i) . (ii) .

Assumption 1 requires that the outcome variable is continuously distributed. Assumption 2 (i) is the exogeneity of the instrumental variable . This assumption allows for the endogeneity of the treatment variable . Assumption 2 (ii) is the rank similarity condition on . It is a relaxation of the rank invariance condition, , that an individual’s rank, , is the same regardless of whether the individual is treated or controlled. The rank similarity condition allows the two unobserved heterogeneity terms, and , to be different, though it still requires them to have the same distribution given the endogenous treatment assignment and the instrumental variable. It enables the -th quantile of the counterfactual outcome variable, , to be compared between the control group () and the treatment group (). The rank similarity condition is a restriction on the unobserved heterogeneity in the outcome variable equation and has been widely used for investigating heterogenous treatment effects (e.g., Doksum, 1974; Heckman et al., 1997; Chernozhukov and Hansen, 2004).

Under the rank similarity condition, Chernozhukov and Hansen (2005) obtain the following relationship between the distribution of and the structural quantile function .

The rest of this paper adds the complication that the binary treatment variable may not be observed. Then the equality (1) cannot be directly used for identifying the structural quantile function.

3 Quantile regression of on

This section does not use any measurement of ; instead the relationship between the outcome variable and the instrumental variable is used to provide a lower bound on the structural quantile treatment effect . Namely, can be a lower bound on , when is a binary variable taking and . This analysis provides a new structural interpretation to , which is computed as the regression coefficient from the quantile regression of on . When takes more than two values, the discussion in this section can be applied by selecting any two values in the support of or partitioning the support into two parts. It is worth clarifying that the results in this section and the following sections are valid regardless of whether is binary, discrete, continuous, or mixed.

The result in this section uses the stochastic monotonicity condition (Small and Tan, 2007 and DiNardo and Lee, 2011). It assumes a positive relationship between the treatment variable and the instrumental variable in which, for every possible realization of , the probability of being treated is weakly increasing in , and the probability of being untreated is weakly decreasing in . The condition is weaker than the deterministic monotonicity condition (Imbens and Angrist, 1994; Angrist et al., 1996) because it allows for defiers, i.e., some individuals who change from to when increases.

Definition 1.

The stochastic monotonicity condition is that

| (2) |

for every .

Theorem 1 shows that, under the stochastic monotonicity condition in (2), is biased towards zero compared to the structural quantile treatment effect .

Theorem 1.

This theorem provides a one-sided bound on : if ; and if . This bound gives researchers a justification for using , which is a lower bound for the structural quantile treatment effect. Note that is a simple object to compute; it is obtained as the quantile regression coefficient on and various statistical software packages include linear and nonlinear quantile regressions (e.g., the qreg command in Stata).

The stochastic monotonicity condition cannot be removed from Theorem 1, but Lemma 5 in the appendix shows that Eq. (3) holds with even if the stochastic monotonicity condition does not hold. In other words, the inequality still holds without the stochastic monotonicity condition. It is possible to use this inequality to test the significance of by testing .

4 Identified set for the structural quantile function

This section considers use of a potentially misclassified treatment variable and provides the sharp identified set for the structural quantile function . To extract some information about the true treatment from its measurement , the following restrictions on the misclassification probabilities are imposed.

Assumption 3.

(i) for some constants . (ii) .

Assumption 3 (i) is that the measurement error does not depend on . Assumption 3 (ii) is that the measurement is positively correlated with the true treatment variable . These assumptions are widely used in the literature on misclassification (e.g., Hausman et al., 1998, Mahajan, 2006; Lewbel, 2007; and Hu, 2008).

The sharp identified set for is the set of values for that exhausts all the information from the model and the data distribution. Let be a subset of the set of functions of to , and be a subset of the set of probability distributions for .333 and are subsets because there can be restrictions on and the distribution for . Also note that the distribution for can be characterized by and the distribution for can be characterized by The distribution for is induced by via Given a distribution for , the sharp identified set for is the set of elements of such that is the distribution for under .444In this paper, is a generic element of and is a generic element of , whereas is the true structural quantile function and is the true distribution for . The sharp identified set for is defined as the projection of the sharp identified set for on the component .

The following theorem characterizes the sharp identified set for under Assumptions 1, 2, and 3, by using moment equalities and inequalities.

Theorem 2.

The moment equality condition in Eq. (4) is equivalent to the main testable implication in Chernozhukov and Hansen (2005) when where are the true unknown misclassification probabilities defined in Assumption 3. The moment inequality conditions about are derived from the following calculations:

As a corollary to Theorem 2, it is possible to compare the identified set for and the estimand in Chernozhukov and Hansen (2005), which does not consider measurement error in .

Corollary 1.

Suppose all the assumptions in Theorem 2 (b) hold. Every solution to , belongs to the sharp identified set for .

As another corollary to Theorem 2, it is possible to relate to the identified set for . Although can be used as a lower bound for , it does not always belong to the identified set.

Corollary 2.

Consider two points, and , in the support of , and suppose all the assumptions in Theorem 2 (b) hold. Then belongs to the sharp identified set for if and only if a.s. and a.s.

Note that, by the exogeneity of , if . Corollary 2 is roughly related to the observation that, under Assumption 3, implies

The precise derivations are found in the proof in the Appendix.

4.1 Under-identification even with large variation in

This section shows that the structural quantile function is not point identified in general unless there is additional information on the model primitives . The failure of point identification is due to the rank condition and happens regardless of the order condition based on Eq. (4), where the number of the parameters is , and the number of the equations is the number of the support points of . Theorem 3 presents this failure for a class of data generating processes. In particular, the theorem states that the quantile treatment effect can be under-identified if one cannot exclude that the treatment is exogenous. Based on the result, it is necessary to impose additional assumptions (other than the ones maintained in this paper) to achieve point identification when the treatment variable is potentially misclassified.

Theorem 3.

Consider or . Assume (i) the mapping is Lipschitz continuous, (ii) , (iii) is independent of , (iv) , and (v) for sufficiently small , the following three statements holds:

-

1.

for every strictly increasing bijection of to such that for every , where and .

- 2.

Then the sharp identified set for has more than one element.

Condition (i) is a regularity condition. Condition (ii) is that the treatment variable can have a non-zero effect on the outcome variable at quantile index . Condition (iii) is that the treatment variable can be exogenous. Condition (iv) is that there is a non-zero measurement error. Condition (v) is a condition about the size of the parameter space . A sufficient condition for (v) is that includes all ’s satisfying Assumptions 1, 2, and 3.

Condition (iii) needs a careful discussion. Theorem 3 states that the quantile treatment effect is not always point identified unless the treatment is assumed to be endogenous. This theorem is more relevant when one cannot exclude that is exogenous than when is known to be exogenous. When one cannot exclude that is exogenous, there is a possibility for the lack of point identification. It can be possible to point-identify the quantile treatment function if one can assume that is not exogenous.

4.2 Point identification with second measurement

Given the under-identification result in Theorem 3, this section considers the case of two measurements for to achieve point identification of the structural quantile function. The identification strategy is based on existing results in the econometric literature. First, the results in Mahajan (2006), Lewbel (2007), and Hu (2008) are applied to identify . Given identification of , the identification result in Chernozhukov and Hansen (2005, 2013) recovers the structural quantile function.

Assumption 4.

(i) The two measurements, and , are conditionally independent given . (ii) . (iii) There are two points, and , in the support of such that

is invertible. (iv) . (v) There are two points, and , in the support of .

Chernozhukov and Hansen (2013) provide a simple sufficient condition for the the global identification of the structural quantile function given . The following assumption and identification result are borrowed from Chernozhukov and Hansen (2013, Section 3.1).

Assumption 5.

There is a cube with such that

for all .

5 Inference procedure with covariates

This section proposes an inference method for the structural quantile function. The method extends the inference method in Chernozhukov and Hansen (2008) to incorporate misclassification probabilities. To include control variables , a linear-in-parameters structure is imposed on the structural quantile function:

| (5) |

This section focuses on constructing a confidence interval for .

Assumption 6.

With probability one, the mapping is strictly increasing and left-continuous for every .

Assumption 7.

(i) . (ii) .

Assumption 8.

(i) For each , is a constant, denoted by . (ii) .

Given i.i.d. copies of , a confidence interval for is constructed via the following two steps. The first step constructs a confidence interval for . Given each point in the confidence interval for , the second step constructs a confidence interval for . The size control comes from the Bonferroni correction for the first and second steps.

The following condition is imposed on a confidence region, , for .

Assumption 9.

.

In the empirical illustration, is constructed by inverting the one-tailed -tests based on and , where for each -test. In the empirical illustration, the confidence interval for is bounded by using and .

At the true value of , the following testable implications (cf. Chernozhukov and Hansen, 2008) hold. As in Chernozhukov and Hansen (2008), it is possible to replace with a function of .

This paper assumes that has a unique minimizer over for the true parameter value , which is implied by Assumption 12 (1). Since is unknown, an estimator for is computed as a function of :

where is a estimator for , and

The objective function is convex in , which is the result of using instead of . This transformation comes from Buchinsky and Hahn (1998) and Abadie et al. (2002).555I am thankful to a referee for proposing this transformation. To simplify the arguments, a parametric model is imposed with a parametric estimator for and the following assumptions.

Assumption 10.

(i) is bounded away from zero and one. (ii) where . (iii) , where

(iv) There are random variables, , such that with . (v) There is an estimator, , for , that satisfies . (vi) There is an estimator for that satisfies . (vii) .

The optimization of is implemented in the same way as the linear quantile regression. Namely, the objective function can be written as , where

for .666Note that for every and . Since the weights, and , are non-negative, Therefore,

The asymptotic variance for is estimated with a kernel function and a bandwidth . For every value of , the asymptotic variance for estimated by

where

Denote by the asymptotic variance for .

The proposed confidence interval for is

where is the parameter space for , the test statistic is

and the critical value is the quantile of the distribution with degrees of freedom. The proposed confidence interval satisfies the asymptotic size control under the following assumptions.

Assumption 11.

is in the interior of a compact parameter space .

Assumption 12.

(i) is invertible. (ii) is finite. (iii) and . (iv) There is a constant such that a.s.

Assumption 13.

(i) and as . (ii) is differentiable with , , , and .

Assumption 11 is a regularity condition on the parameter. Assumption 12 (i) is that the Hessian matrix is non-singular, and it implies point identification of given the true value . Assumption 12 (ii)-(iv) is a regularity condition on the distribution of the observables. Assumption 13 is a restriction on the bandwidth and the kernel function, which is used to estimate the asymptotic variance .

6 Empirical illustration and Monte Carlo simulations

This section investigates the finite sample performance of the proposed method using an existing empirical application and simulated datasets. As emphasized in Section 4.1, the inference results presented in this section are valid regardless of whether the structural quantile function is point or partially identified.

6.1 Empirical illustration

This empirical illustration studies the quantile treatment effects of the 401(k) participation on financial savings (Chernozhukov and Hansen, 2004) and consider the problem of mis-measured 401(k) participation.777Ura (2018) uses the same empirical setting to investigate the local average treatment effect under treatment misclassification. It uses the same dataset as Chernozhukov and Hansen (2004), which is an extract from the Survey of Income and Program Participation (SIPP) of 1991. The sample consists of households in which at least one person is in employment, and which has no income from self-employment. The resulting sample size is 9,915.

The model is based on Chernozhukov and Hansen (2004). The outcome variable is the net amount of financial assets in dollars, and the measured treatment variable is self-reported participation in a 401(k) program. Participation in a 401(k) program may be endogenous because participants may be concerned more about retirement plans than non-participants. To control for endogeneity, an instrumental variable is 401(k) eligibility, an indicator variable of whether an employer offers a 401(k) program, where means eligibility and means ineligibility. The control variables include a constant, family income, age, age squared, marital status, and family size. The summary statistics for are in Table 1.

| sample size | mean | std. dev. | |

|---|---|---|---|

| : family net financial assets (in $1000) | 9,915 | 18.05 | 63.52 |

| : 401(k) participation | 9,915 | 0.26 | 0.44 |

| : 401(k) eligibility | 9,915 | 0.37 | 0.48 |

The details for the the confidence intervals are as follows. The pre-specified sizes are , where is used to construct a confidence interval for unknown misclassification probabilities and is used for the critical value . The confidence interval for is for , where follows from and comes from the one-tailed -test for with size . The conditional probability of given is estimated by probit regression of on all the interactions of and the cubic polynomials of .888The interaction terms can be written as . Using and grid points for , is constructed by .

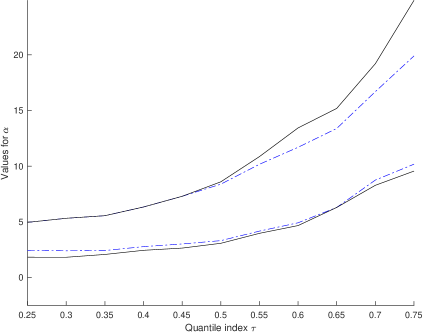

Figure 1 (left) shows the confidence intervals based on Section 5, with the specification in Eq. (5) and the same list of covariates as Benjamin (2003) and Chernozhukov and Hansen (2004).999 includes a constant, age, age2, income categories, family size, education dummies, marital status dummy, two-earner status dummy, defined benefit pension status dummy, IRA participation status dummy, and homeownership status dummy. The number of the covariates in is 18. The figure also shows the confidence intervals that assume , i.e., no misclassification. The confidence intervals that assume are exactly the same as the confidence intervals proposed in Chernozhukov and Hansen (2008, Section 3). All the confidence intervals are point-wise, that is, computed separately for each quantile index .

In this empirical exercise, the confidence intervals proposed in this paper are comparable in lengths to those that assume no misclassification. There are several features of this empirical exercise that make the confidence intervals tight (compared to those that assume no misclassification). First, in this empirical exercise, implies , so under-identification for mainly comes from under-identification for the scalar parameter . It makes the degree of under-identification smaller than when and are both under-identified. Second, the confidence intervals that assume , are large enough to include the confidence interval with another value of . Figure 1 (right) shows the confidence intervals that assume and that with , where the points and are the two endpoints for . The confidence intervals that assume include those that assume for almost all the values of .

6.2 Monte Carlo simulations

Monte Carlo simulations are based on the following data generating process. The instrumental variable takes with probability and with probability . The error term is a two-dimensional mean-zero normal random vector with variance and correlation coefficient , independent of . The covariate is , where is a four-dimensional standard normal random vector with identity covariance matrix, independent of . The latent treatment variable is determined by

and the outcome variable is determined by

where is the standard normal cumulative distribution function and . The binary measurement is determined by , where . The true values for is .

In this simulation exercise coverage frequencies are computed for two inference methods over . One is the proposed inference method and the other is the inference method that assumes no misclassification, that is, . All the results are based on , , and 5,000 simulations.101010 The details about the confidence interval is as follows. where the value of comes from the one-tailed -test for with size and the value of comes from the one-tailed -test for with size . As in the empirical exercise, is estimated by the probit regression of on all the interactions of and the cubic polynomials of . Using 1% grid points , is .

Figure 6.a summarizes the simulation results when there is no misclassification, that is, . In this case, both the proposed method and the method that assumes have correct size, i.e., the coverage frequency at the true value of is at least 95%. The proposed inference method is less powerful than that with , but this is the cost for achieving robustness to misclassification.

Figures 6.b-6.h summarize the simulation results when there is some misclassification. The method that assumes does not have correct size as becomes far from , but the proposed method always has correct size. This is consistent with Theorem 5, which shows that the proposed method has correct size even in the presence of misclassification.

To summarize these simulation results, the proposed inference method covers the true parameter value at least with the pre-specified significance level in finite samples. A practitioner could obtain a narrower confidence interval by assuming no misclassification, but the confidence interval may not cover the true parameter with correct size when there is non-negligible misclassification.

To investigate Monte Carlo simulations, Online Appendix provides a comparison between the proposed inference method and the infeasible method with knowing . The details are provided online in supplementary material associated with this article, available at Cambridge Journals Online (journals.cambridge.org/ect).

7 Conclusion

This paper extends the instrumental variable quantile regression model (Chernozhukov and Hansen, 2005, 2013) for a binary regressor, to situations when this binary regressor is potentially misclassified. The first identification result is that under the rank similarity condition and the stochastic monotonicity condition, the reduced-form question effect, , is biased towards zero compared to the structural quantile treatment effect . The second identification result characterizes the sharp identified set for under widely-used assumptions. An inference method for the structural quantile function is provided, and its finite sample performance is demonstrated in simulation studies and an empirical illustration.

Figure 6.a: .

Figure 6.b: and .

Figure 6.c: and .

Figure 6.d: and .

Figure 6.e: .

Figure 6.f: and .

Figure 6.g: and .

Figure 6.h: and .

Figure 6 (continued): Coverage frequencies. The dash-dot () curve represents the proposed inference method, and the dashed () curve represents the inference method that assumes .

References

- Abadie et al. (2002) Abadie, A., J. Angrist, and G. Imbens (2002): “Instrumental Variables Estimates of the Effect of Subsidized Training on the Quantiles of Trainee Earnings,” Econometrica, 70, 91–117.

- Angrist et al. (1996) Angrist, J. D., G. W. Imbens, and D. B. Rubin (1996): “Identification of Causal Effects using Instrumental Variables,” Journal of the American Statistical Association, 91, 444–455.

- Benjamin (2003) Benjamin, D. J. (2003): “Does 401(k) Eligibility Increase Saving?: Evidence from Propensity Score Subclassification,” Journal of Public Economics, 87, 1259 – 1290.

- Bitler et al. (2016) Bitler, M. P., H. W. Hoynes, and T. Domina (2016): “Experimental Evidence on Distributional Effects of Head Start,” Working paper.

- Bound et al. (2001) Bound, J., C. Brown, and N. Mathiowetz (2001): “Measurement Error in Survey Data,” in Handbook of Econometrics, ed. by J. Heckman and E. Leamer, Elsevier, vol. 5, chap. 59, 3705–3843.

- Buchinsky and Hahn (1998) Buchinsky, M. and J. Hahn (1998): “An Alternative Estimator for the Censored Quantile Regression Model,” Econometrica, 66, 653.

- Calvi et al. (2017) Calvi, R., A. Lewbel, and D. Tommasi (2017): “LATE With Mismeasured or Misspecified Treatment: An Application To Women’s Empowerment in India,” Working paper.

- Chernozhukov and Hansen (2004) Chernozhukov, V. and C. Hansen (2004): “The Effects of 401(K) Participation on the Wealth Distribution: An Instrumental Quantile Regression Analysis,” Review of Economics and Statistics, 86, 735–751.

- Chernozhukov and Hansen (2005) ——— (2005): “An IV Model of Quantile Treatment Effects,” Econometrica, 73, 245–261.

- Chernozhukov and Hansen (2008) ——— (2008): “Instrumental Variable Quantile Regression: A Robust Inference Approach,” Journal of Econometrics, 142, 379 – 398.

- Chernozhukov and Hansen (2013) ——— (2013): “Quantile Models with Endogeneity,” Annual Review of Economics, 5, 57–81.

- Chesher (1991) Chesher, A. (1991): “The Effect of Measurement Error,” Biometrika, 78, 451–462.

- Chesher (2003) ——— (2003): “Identification in Nonseparable Models,” Econometrica, 71, 1405–1441.

- Chesher (2017) ——— (2017): “Understanding the Effect of Measurement Error on Quantile Regressions,” Journal of Econometrics, 200, 223 – 237.

- DiNardo and Lee (2011) DiNardo, J. and D. S. Lee (2011): “Program Evaluation and Research Designs,” in Handbook of Labor Economics, ed. by O. Ashenfelter and D. Card, Elsevier, vol. 4, Part A, chap. 5, 463–536.

- DiTraglia and García-Jimeno (2019) DiTraglia, F. J. and C. García-Jimeno (2019): “On Mis-measured Binary Regressors: New Results and Some Comments on the Literature,” Journal of Econometrics, 209, 376–390.

- Doksum (1974) Doksum, K. (1974): “Empirical Probability Plots and Statistical Inference for Nonlinear Models in the Two-Sample Case,” Annals of Statistics, 2, 267–277.

- Dong and Shen (2018) Dong, Y. and S. Shen (2018): “Testing for Rank Invariance or Similarity in Program Evaluation,” Review of Economics and Statistics, 100, 78–85.

- Firpo et al. (2017) Firpo, S., A. F. Galvao, and S. Song (2017): “Measurement Errors in Quantile Regression Models,” Journal of Econometrics, 198, 146–164.

- Frandsen and Lefgren (2018) Frandsen, B. R. and L. J. Lefgren (2018): “Testing Rank Similarity,” Review of Economics and Statistics, 100, 86–91.

- Frazis and Loewenstein (2003) Frazis, H. and M. A. Loewenstein (2003): “Estimating Linear Regressions with Mismeasured, Possibly Endogenous, Binary Explanatory Variables,” Journal of Econometrics, 117, 151–178.

- Galvao and Montes-Rojas (2009) Galvao, A. F. and G. Montes-Rojas (2009): “Instrumental Variables Quantile Regression for Panel Data with Measurement Errors,” Working paper.

- Gustman et al. (2008) Gustman, A. L., T. Steinmeier, and N. Tabatabai (2008): “Do Workers Know About Their Pension Plan Type? Comparing Workers’ and Employers’ Pension Information,” in Overcoming the Saving Slump; How to Increase the Effectiveness of Financial Education and Saving Programs, ed. by A. Lusardi, Chicago: University of Chicago Press, 47–81.

- Hausman et al. (1998) Hausman, J. A., J. Abrevaya, and F. M. Scott-Morton (1998): “Misclassification of the Dependent Variable in a Discrete-Response Setting,” Journal of Econometrics, 87, 239–269.

- Heckman et al. (1997) Heckman, J. J., J. Smith, and N. Clements (1997): “Making the Most Out of Programme Evaluations and Social Experiments: Accounting For Heterogeneity in Programme Impacts,” The Review of Economic Studies, 64, 487–535.

- Henry et al. (2014) Henry, M., Y. Kitamura, and B. Salanié (2014): “Partial Identification of Finite Mixtures in Econometric Models,” Quantitative Economics, 5, 123–144.

- Hu (2008) Hu, Y. (2008): “Identification and Estimation of Nonlinear Models with Misclassification Error using Instrumental Variables: A General Solution,” Journal of Econometrics, 144, 27–61.

- Imbens and Angrist (1994) Imbens, G. W. and J. D. Angrist (1994): “Identification and Estimation of Local Average Treatment Effects,” Econometrica, 62, 467–75.

- Kim and Park (2018) Kim, J. H. and B. Park (2018): “Testing Rank Similarity in the Local Average Treatment Effect Model,” Working paper.

- Lewbel (2007) Lewbel, A. (2007): “Estimation of Average Treatment Effects with Misclassification,” Econometrica, 75, 537–551.

- Mahajan (2006) Mahajan, A. (2006): “Identification and Estimation of Regression Models with Misclassification,” Econometrica, 74, 631–665.

- Newey and McFadden (1994) Newey, W. K. and D. McFadden (1994): “Large Sample Estimation and Hypothesis Testing,” in Handbook of Econometrics, ed. by R. F. Engle and D. L. McFadden, Elsevier, vol. 4, chap. 36, 2111–2245.

- Nguimkeu et al. (2019) Nguimkeu, P., A. Denteh, and R. Tchernis (2019): “On the Estimation of Treatment Effects with Endogenous Misreporting,” Journal of Econometrics, 208, 487–506.

- Pollard (1991) Pollard, D. (1991): “Asymptotics for Least Absolute Deviation Regression Estimators,” Econometric Theory, 7, 186–199.

- Schennach (2008) Schennach, S. M. (2008): “Quantile Regression with Mismeasured Covariates,” Econometric Theory, 24, 1010–1043.

- Small and Tan (2007) Small, D. S. and Z. Tan (2007): “A Stochastic Monotonicity Assumption for the Instrumental Variables Method,” Working paper.

- Song (2018) Song, S. (2018): “Nonseparable Triangular Models with Errors in Endogenous Variables,” Working paper.

- Ura (2018) Ura, T. (2018): “Heterogeneous Treatment Effects with Mismeasured Endogenous Treatment,” Quantitative Economics, 9, 1335–1370.

- Wei and Carroll (2009) Wei, Y. and R. J. Carroll (2009): “Quantile Regression With Measurement Error,” Journal of the American Statistical Association, 104, 1129–1143.

- Wüthrich (2019) Wüthrich, K. (2019): “A Comparison of Two Quantile Models with Endogeneity,” Journal of Business and Economic Statistics, forthcoming.

- Yanagi (2019) Yanagi, T. (2019): “Inference on Local Average Treatment Effects for Misclassified Treatment,” Econometric Reviews, 38, 938–959.

- Yu (2017) Yu, P. (2017): “Testing Conditional Rank Similarity With and Without Covariates,” Working paper.

Appendix

Appendix A discusses the identified set when the outcome variable is discrete, and Appendix B provides the proofs for the results in the main text.

Appendix A: Identified set with a discrete outcome variable

This appendix demonstrates how to modify Theorem 2 when the outcome variable is discrete. Assumptions 1-2 are modified into the following two conditions.

Assumption 14.

The mapping is weakly increasing and left-continuous for every .

Assumption 15.

(i) and . (ii) .

Under the above two assumptions, Theorem 2 can be modified as follows:

Theorem 6.

Proof.

The proof for (a) is as follows. Define . By Assumption 3,

| (7) |

Using Eq. (7),

Since Assumption 14 implies , it follows that , and then Eq. (6) holds. Moreover, by Eq. (7), implies and .

In the proof for (b), it is necessary to find such that and that is the distribution for under . For each , there is a strictly increasing bijection such that . For each and every , define . Define the distribution for by

where

| (8) |

By construction, the distribution for under is , and for each . To show , it suffices to show that Assumptions 14 and 3 hold for . The rest of the proof is going to show Assumption 2 (i).111111Assumption 14 follows from the definition of . Assumption 2 (ii) follows from the definition of . Assumption 3 follows from . By rearranging Eq. (6),

Using Eq. (8), . The definition of and implies

which is Assumption 2 (i). ∎

Appendix B: Proofs of the results in the main text

Proof of Theorem 1

Proof.

By Lemma 5, the statement of theorem holds if . The rest of the proof is going to focus on . By Lemma 5, there is some such that . Here it is sufficient to show for Theorem 1 (a) and for Theorem 1 (b). Since is a convex combination of and , it follows . Since

it follows that . Using the monotonicity of , . Using the density function , the above equation can be rewritten as

| (9) |

Proof of Theorem 2

The proof for (a) is as follows. By Assumption 3,

In the proof for (b), it is necessary to find such that and that is the distribution for under . For each , there is a strictly increasing bijection such that . For each and every , define . Define the distribution for by

where

| (11) |

By construction, the distribution for under is , and for each . To show , it suffices to show that Assumptions 1, 2, and 3 hold for . The rest of the proof is going to show Assumption 2 (i). By rearranging Eq. (4),

Using Eq. (11), . The definition of and implies

Proof of Corollary 1

Use . Then satisfies the conditions in Theorem 2.

Proof of Corollary 2

In this proof, assume without loss of generality. The “only if” part of this corollary is shown as follows. By Theorem 2, Eq. (4) holds for some with a.s. and a.s. Using , Eq. (4) becomes

Since a.s. and a.s., it follows that a.s. and a.s.

The “if” part of this corollary is shown by choosing and .

Proof of Theorem 3

Assume for simplicity. Note that from Condition (iii). Take sufficiently small and define

Condition (iv) guarantees . Consider and define by

By Condition (ii), and as long as is positive. To establish the statement of this theorem, the rest of the proof is going to show that and that is observationally equivalent to .

First, . The Lipschitz continuity in Condition (i) guarantees that is a strictly increasing bijection of into for sufficiently small , where . Therefore, Condition (v) implies for sufficiently small . To show , it suffices to show Assumption 2 (i) because Assumption 2 (ii) holds for . By the definition of and independence between and given ,

where the second equality uses . By the definition of and ,

where the last equality uses .

Second, is observationally equivalent to . By the definition of ,

Therefore,

and it can be similarly shown that .

Proof of Lemma 2

Proof of Lemma 3

It follows from Theorem 2 of Chernozhukov and Hansen (2013).

Proof of Theorem 4

Proof of Lemma 4

Note that

because

Since , Chernozhukov and Hansen (2008, p.383) derives . Therefore,

Note that and , because

Proof of Theorem 5

The following proof assumes and without loss of generality, because is bounded away from zero and one, and then

with probability approaching one.

Lemma 6.

, where and .

Proof.

The proof of this lemma is to check the conditions in Newey and McFadden (1994, Lemma 2.9). Since is compact and is continuous, it suffices to show for every and for every . This proof uses

The pointwise convergence of to is shown by demonstrating and . Since

Assumption 10 (ii) implies . Moreover, is shown by checking the second moment of : follows from

The in-probability Lipschitz condition is shown as follows. Since and , it follows that . ∎

Lemma 7.

, where .

Proof.

The proof of this lemma is to check the conditions in Newey and McFadden (1994, Theorem 2.1) to establish the consistency. Since is compact, is continuous, and Lemma 6 establishes the uniform convergence of , it suffices to show that is uniquely minimized at . As in the proof of Lemma 4,

Since

it follows that and is positive semidefinite everywhere and positive definite at . Therefore, is uniquely minimized at . ∎

Lemma 8.

, where .

Proof.

By Assumption 10 (iii)-(iv), . ∎

Lemma 9.

Define

Then .

Proof.

If pointwise in , it is possible to the convexity lemma in Pollard (1991) to , and then . Therefore, it suffices to show that pointwise in . Note that

where the equality uses the law of iterated expectation, and . Therefore, and , so that

Therefore,

where the last equality follows from .

First, converges to zero in . By the definitions of and ,

where and . By the definition of , the two terms, and , can be bounded as follows:

| (15) | |||||

| (16) | |||||

As long as and ,

| (17) | |||||

| (18) | |||||

Now it is possible to bound as follows:

Since , it follows that

so that

Lemma 10.

and therefore as , where

Proof.

Lemma 11.

and .

Proof.

Lemma 12.

.

Proof.

The weak law of large numbers implies , and then it suffices to show . Since

and

it suffices to show that , that , , , and are , and that the sample averages of the following variables are : (1) , (2) , (3) , (4) , (5) , (6) , (7) , (8) , (9) , (10) , and (11) . The convergence comes from the weak law of large numbers, and the other parts come from a combination of Assumption 10 (iv)-(vii) and the following equalities:

| (19) | |||

| (20) | |||

| (21) |

Note that Eq. (19) follows from and .

Lemma 13.

.

Proof.

Since

the weak law of large numbers implies . It suffices to show that . Using the mean value expansion,

where , and is a value between and . Using the above mean value expansion,

Since each entry in has a finite variance, it suffices to show that

| (22) | |||

| (23) |

for a random variable such that is a function of and . The rest of the proof is going to focus on (22) because the proof for (23) is similar. The mean of the left-hand side of (22) is , because

The variance of the left-hand side of (22) is , because

∎

Lemma 14.

.

Supplemental Online Appendix for “Instrumental Variable Quantile Regression with Misclassification” by Takuya Ura

Additional simulation results

This supplemental online appendix provides additional simulation results in the simulation designs in Section 6.2. The proposed inference method uses the Bonferroni size correction for the parameters . To evaluate the conservatism of the Bonferroni correction, the proposed inference method is compared with the infeasible method with knowing . The infeasible inference method is based on the true parameter , and uses and in Section 5 with .

For all the simulation designs, the proposed method rejects the alternatives less often than the infeasible method. The power comparisons are different between the alternatives larger and smaller than . On one hand, the power of the proposed method for the alternative smaller than is comparable to that of the infeasible method. On the other hand, the powers are significantly different for the alternative larger . I conjecture that the value of might not be relevant to reject the alternative smaller than , because, as in Section 3, it is possible to get a lower bound for without using the variable .

Figure 16.a: .

Figure 16.b: and .

Figure 16.c: and .

Figure 16.d: and .

Figure 16.e: .

Figure 16.f: and .

Figure 16.g: and .

Figure 16.h: and .

Figure 16 (continued): Coverage frequencies. The dash-dot () curve represents the proposed inference method, and the dashed () curve represents the infeasible inference method with knowing .