On the Number of Conjugate Classes of Derangements

Abstract

The number of conjugate classes of derangements of order is the

same as the number of the restricted partitions with every

portion greater than . It is also equal to the number of isotopy

classes of Latin rectangles. Sometimes the exact value

is necessary, while sometimes we need the approximation value. In

this paper, a recursion formula of will be obtained, also

will some elementary approximation formulae with high accuracy for

be presented. Although we may obtain the value of

in some computer algebra system, it is still meaningful to find an

efficient way to calculate the approximate value, especially in engineering,

since most people are familiar with neither programming nor CAS software.

This paper is mainly for the readers who need a simple and practical

formula to obtain the approximate value (without writing a program)

with more accuracy, such as to compute the value in an pocket science

calculator without programming function. Some methods used here can

also be applied to find the fitting functions for some types of

data obtained in experiments.

1. School of Information and Mathematics, Anhui International Studies

University, Hefei, China, 231201

2. School of Mathematical Science, University of Science and Technology

of China, Hefei, China, 230026

3. School of Mathematics and Physics, Anhui Jianzhu University, Hefei,

China, 230601

Correspondence should be addressed to Wen-Wei Li, liwenwei@ustc.edu

Published in Journal of Mathematics, Volume 2021, Article ID

6023081, 20 pages,

https://doi.org/10.1155/2021/6023081

1 Introduction

Below is a positive integer greater than 1.

On some occasions, it is necessary to know the number of conjugate

classes of derangements.

When generating the representatives of all the isotopy classes of

Latin rectangles of order by some method, we need to know the

number of the isotopy classes of Latin rectangles for

verification. In some cases, we need the approximate value in a

simple and efficient method. (When writing a C program to generate

the representatives of all the isotopy classes of Latin rectangles

of order , we need to prepare some space in the memory module

(RAM) to store the cycle structures of derangements so as to make

the program more efficient, otherwise, we have to allocate memory

dynamically, which will cost more time in memory addressing when writing

and reading data frequently in the particular position in the memory

module. So we need to know the number of the isotopy classes of

Latin rectangles for verification. )

Let be the symmetry group of the set

= {1, 2, , }, i.e., the set (together with the operation

of combination) of the bijections from to itself. An

element in the symmetry group is also

called a permutation (of order ). If ,

(), will be

called a derangement of order . If

a permutation transforms any element in to

a distinct element, then the sequence

will also be called a derangement. The number of derangements

of order is denoted by (or in some literature).

It is mentioned in nearly every combinatorics textbook that,

Here is the floor function, which

stands for the maximum integer that is less than or equal to the real

.

For , if , s.t.

, then and will be called conjugate,

and is called

the conjugation of . Of course the

conjugacy relation is an equivalence relation. So the set of derangements

of order can be divided into some conjugate classes. This paper

is mainly concerned on the number of conjugate classes of derangements

of order . The main method is similar to that described in reference

[1].

A matrix of size () with

every row being a reordering of a fixed set of elements and every

column being a part of a reordering of the same set of elements,

is called a Latin rectangle. Usually,

the set of the elements is assumed to be { 1, 2, 3, ,

}. (in some literatures, the members in a Latin rectangle

is assumed in the set { 0, 1, 2, , }.)

A Latin rectangle with the first row in increasing

order could be considered as a derangement. An isotopy class of

Latin rectangles will correspond to a unique conjugate class of derangements.

So the number of isotopy classes of Latin rectangles

is the same as the number of conjugate classes of derangements of

order .

All the members in a conjugate class of derangements in

share the same cycle structure. Here we define the cycle structure

of a derangement as the sequence in non-decreasing order of the lengths

(with duplicate entries) of all the cycles in the cycle decomposition

of the derangement. A cycle structure of a derangement of order

could be considered as an integer solution of the equation

(1)

where , , , are unknowns.

For a fixed , designate the number of integer solutions of the

equation (1) as ,

where is less than

(otherwise is defined by 0), and denote the number

of all the integer solutions of Equation (1)

for all possible ,

i.e.,

So the number of conjugate classes of derangements of order is

. Since is the number of a type of restricted partitions,

it is tightly connected with the partition number .

Following the notation of [2], denote by

the number of integer solutions of equation

(2)

for a fixed , where , and by

the number of all the (unrestricted) partitions of . It is clear

that 111 In a lot of articles, is used in stead of ,

but in some other literatures, stands for some other number.

(3)

There is a brief introduction of the important results on the partition

number (or partition function) and in reference

[2], such as the recursion formula of

and . More information about the partition number

may be found in reference [3]. There is a list

of some important papers and book chapters on the partition number

in [4] (including the “LINKS” and “REFERENCES

”) and [5]. Reference [1]

presented some estimation formulae with high accuracy for ,

which are revised from the Hardy-Ramanujan’s asymptotic formula.

There are also a lot of literatures on the number of some types of

restricted partitions of (such as [6],

[7], [8], [9],

[10], [11],

[12], [13])

or on the congruence properties of (restricted) partition function

(such as [14], [15],

[16], [17], [18],

[19], [20],

[21]).

In [22], we can find many cases of Restricted

Partitions (some of them are introduced in [23],

[24] or [25]). One class are concerned

on the restriction of the sizes of portions, such as portions restricted

to Fibonacci numbers, powers (of 2 or 3), unit, primes, non-primes,

composites or non-composites; another class are related to the restriction

of the number of portions, such as the cases that the number of parts

will not exceed ; the third class are about the restrictions for

both, for example, the cases that the number of parts is restricted

while the parts restricted to powers or primes. But the author has

not found too much information on the number , especially on

the approximate calculation, although we can find a lot of information

on other restricted partition numbers.

The basic method of function fitting (curve fitting) could be found

in any textbook of numerical analysis, such as [26]

and [27]. Some tricks used here may be found in

some books of data analysis such as [28].

They may be helpful for understanding the methods described in Section

3.

Section 2 will deduce the recursion formula

for and will show the relation of and . Subsection

3.1 will deduce the asymptotic formula

of from Hardy and Ramanujan’s Asymptotic formula of

(mentioned in [1]). This new asymptotic

formula coincides with Ingham’s result (refer

[29] and [30]).

By bringing in two parameters and in the new

asymptotic formula , we have reached several estimation

formulae for with high accuracy in subsection 3.3,

using the same ideas described in [1].

By fitting , we have another two estimation

formulae for in subsection 3.4. When ,

we have a more accurate estimation formula for in subsection

3.5. The relative errors of these estimation

formulae will be presented to shown the accuracy.

2 Some Formulae for

In this section, we will derive a recursive formula from the method

mentioned in reference [2] (page 53~55).

By definition, = 0 when , but here we assume that

= 0 when , and , for convenience.

It is mentioned in [2] (page 52) that in 1942

Auluck gave an estimation of by when is large enough.

By the same method shown in reference [2] (page

53, 57), we can obtain the generation function of :

(4)

and a formula

(5)

where , , and is a contour around the original

point.

It is difficult to get a simple formula to count the solutions of

Equation (1) in general. But for a fixed integer

, the number of solutions is (when )

or

=

= = = (when ).

It is not difficult to find out that

(6)

And there is a recursion for in reference [2]

(page 51)

(7)

where , so there is no difficulty to obtain the

values of and when is small.

For the value of there is a recursion,

(8)

where

(9)

and assume that . (Refer [2], page

55). Here we assume that = 0 when .

We can obtain the same recursion for ,

(10)

where and are determined by Equation (9)

and assume that , = 0 when .

We can easily obtain the solutions of Equation (1)

by hand when < 13. By Equation (10), we can

obtain the number of solutions of Equation (1)

by writing a small program in some Computer Algebra System (CAS)

softwares such as “maple”, “maxima”, “axiom” or some other

softwares likewise (be aware of that 0 is not a valid index value

in some software such like maple).

Table 1: The value of when

Table 2: The value of when

Table 3: The number of solutions of Equation (1) for different

The value of when < 250 are shown on Table 3

(on page 3) and Table 3 (on

page 3). Some value of are shown

on Table 3 (on page 3).

Obviously, < holds by definition (when ). As

grows much more slowly than exponential functions, i.e., for

any , will hold when is large enough, which

means we can not estimate and by an exponential function.

As grows faster than any power of , which means we can

not estimate by a polynomial function. (refer [2],

page 53) So, can not be estimated by a polynomial function,

either.

3 The Estimation of

The recursion formula Equation (10) for

is not convenient in practical for a lot of people who do not want

to write programs. Sometimes we need the approximation value, such

as the cases mentioned in [1], so

an estimation formula is necessary.

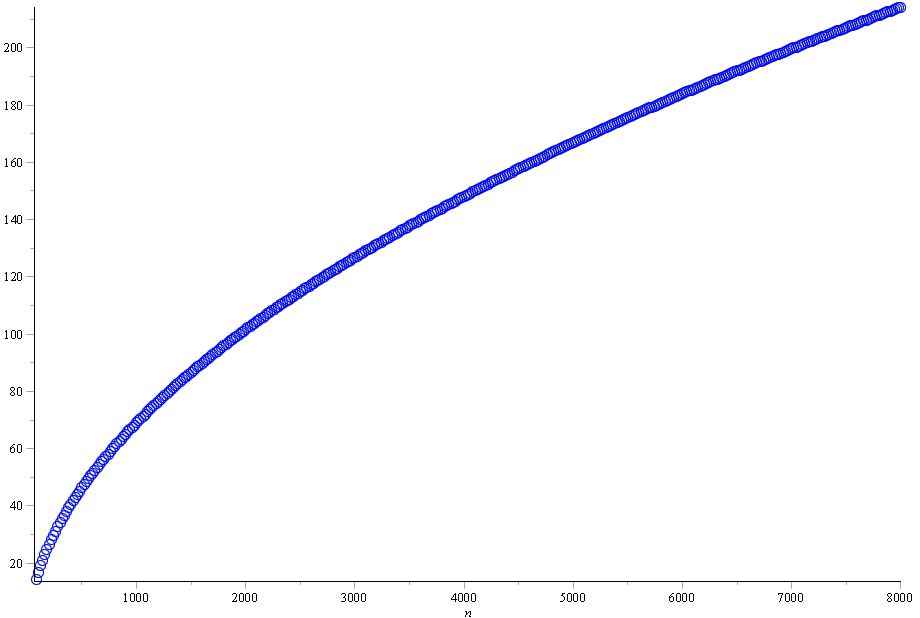

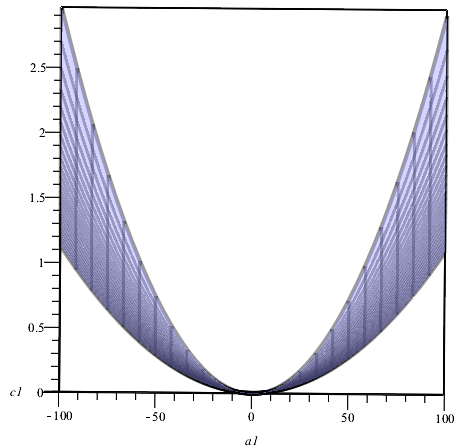

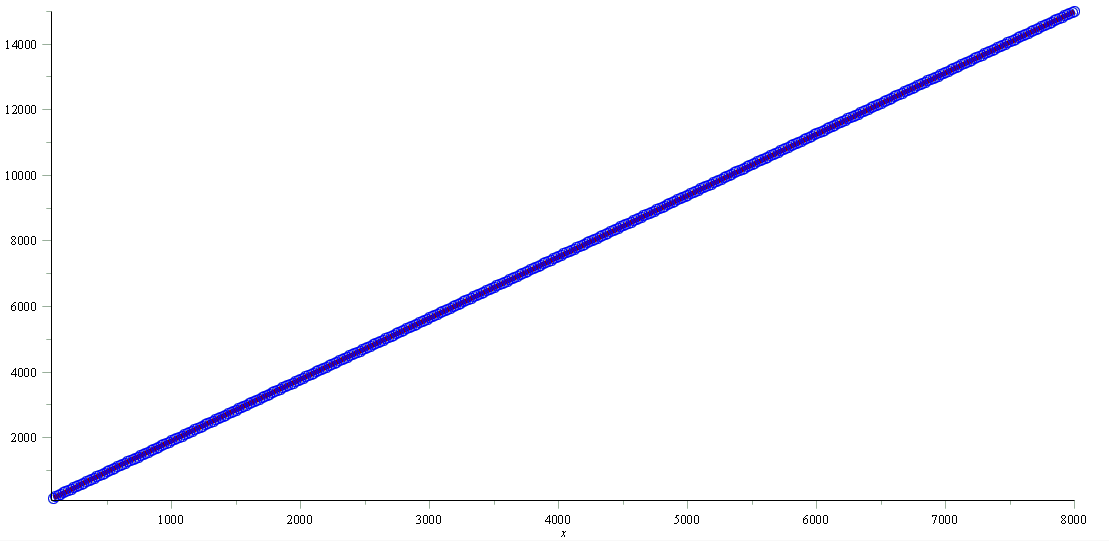

The figure of the data ( = ,

= 1, 2, , 397) are shown on Figure 1 on page 1.

Here the data points are displayed by small hollow circles, and

the circles are very crowded that we may believe that the circles

themselves be a very thick curve if we notice only the right-hand

part. In this figure, the data points in the lower left part are sparse

(compared with the points in the upper right part), and we may find

some hollow circles easily. If there is a curve passes through these

hollow circles, we will notice it (as shown on Figure 22

on page 22). But later in Figure

18, the circles distribute uniformly on a

curve, it will be difficult to distinguish the circles and the curve

passes through the centers of the them.

The author has not found a practical estimation formula with high

accuracy of the number before.

Figure 1: The graph of the data

Actually, it is very difficult to find directly a simple function

to fit the data on Figure 1 with high accuracy. The main reason

is that the fitting functions obtained by the methods used frequently

could not reach satisfying accuracy.

Since we have several accurate estimation formula of (refer

[1]), such as

and the error of this formula will not exceed twice of the error

of or . Of course, this

formula is not as simple as we want, but the accuracy is very good.

3.1 Asymptotic Formula

As , by Hardy-Ramanujan’s asymptotic formula

(refer [31], [32],

[33], [34],

[3], [35], [1]),

we assume that, when ,

.

So,

=

So,

(17)

Table 4: The relative error of to when .

Table 5: The relative error of

to when .

In coincidence, half a year after the main results were obtained in

this paper, the author found an asymptotic formula

which coincides with the asymptotic formula obtained here.

The formula (17) will be called the

Ingham-Meinardus asymptotic formula

in this paper, since Daniel mentioned in [30]

that this general asymptotic formula (18) was first given

by A. E. Ingham in [29] and the proof was

refined by G. Meinardus later in another two papers written in German.

Later in this paper,

will be denoted by for short.

It is not satisfying to estimate by when

is small. The relative error of to

is greater than 6% as shown on Table 5

(on page 5). The round approximation

will not change the accuracy distinctly, as shown on Table 5

(on page 5). So it is necessary

to modify the asymptotic formula for better accuracy.

3.2 Method A: Modifying the exponent

In this subsection we consider fitting by ,

or fitting

( = , = 1, 2, , 397) by a function

(20)

Let = .

The reason that we fit by the function in the form displayed

in (20) is the same as that described in section

3 of [1] (although the data differs

distinctly). Many other types of functions have been tested, but they

can not fit these data very well.

But here it is not valid to obtain the constants in

by iteration method described in reference [1].

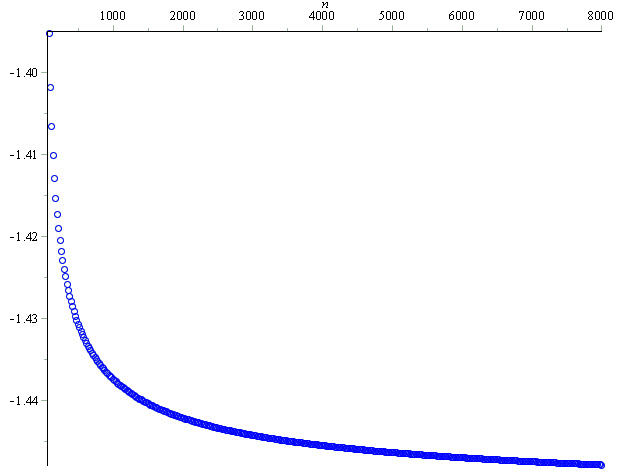

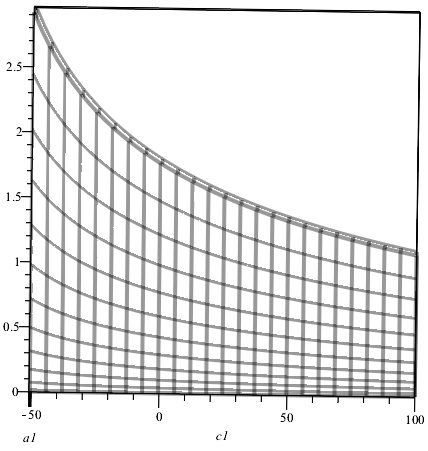

The figure of the data

( = , = 1, 2, , 397) is shown on Figure

2 on page 2.

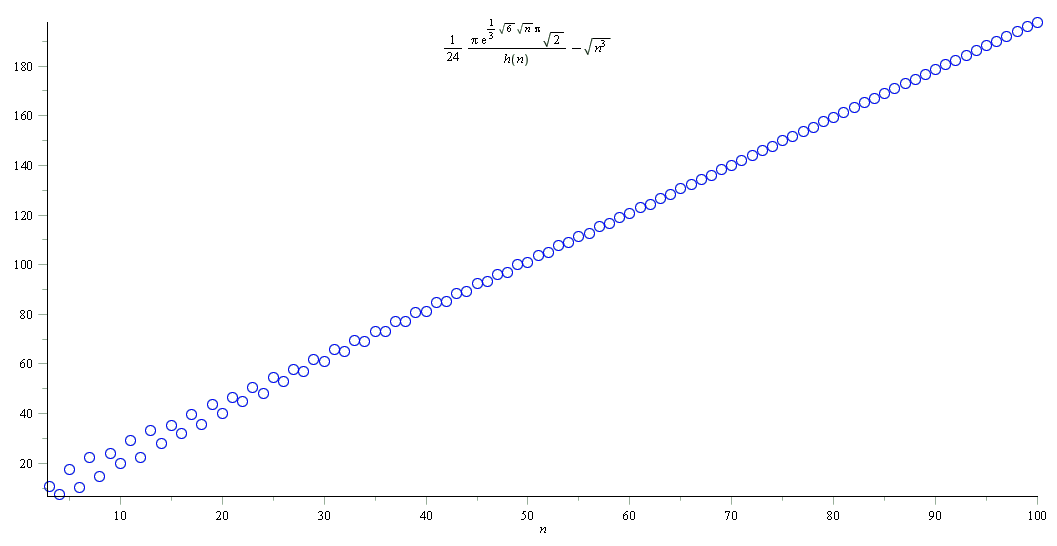

Figure 2: The graph of the data

First, we try to fit

( = , = 1, 2, , 397) by a function in

the form

(21)

That means we have assumed that , temporarily. We will

explain the reason in subsection 3.2.3.

The average error of is

(22)

,

where = 397, ranges from 80 to 8000, by step 20. Here

only , , and are unknown, so we can consider

as a function of the variables .

We want to find a triple such that

reaches its minimum, or to make as small as possible.

Since a lot of functions have several local minimum points, it is

necessary to find out whether =

has more than one local minimum before we start to calculate the minimum

point by numeral method. But =

is too complicate, it is very difficult to know all the critical points

in the range we are considering.

3.2.1 Preparation work

For a given pair , by the property of the

arithmetic mean, 222 For some given data ( = 1, 2, , ;

), the function

reaches its minimum at = . it is clear that reaches its minimum when

(23)

where = .

Let

be the average error of the the fitting function .

(Here and are undetermined coefficients.)

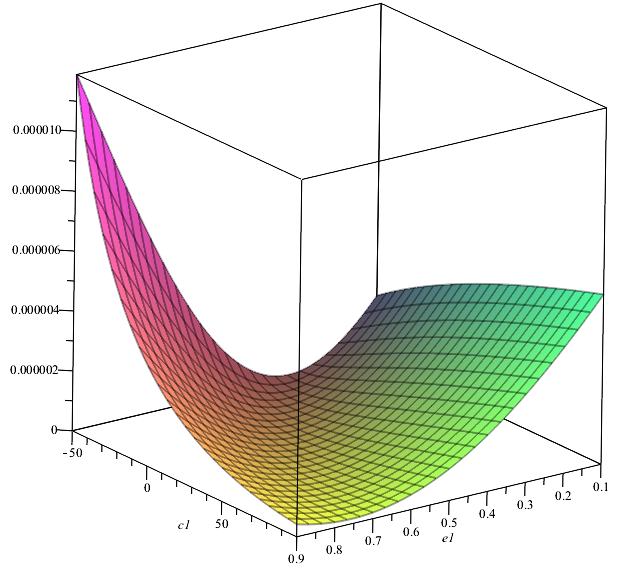

Let

Here only and are unknowns. could be

considered as a function of . In order

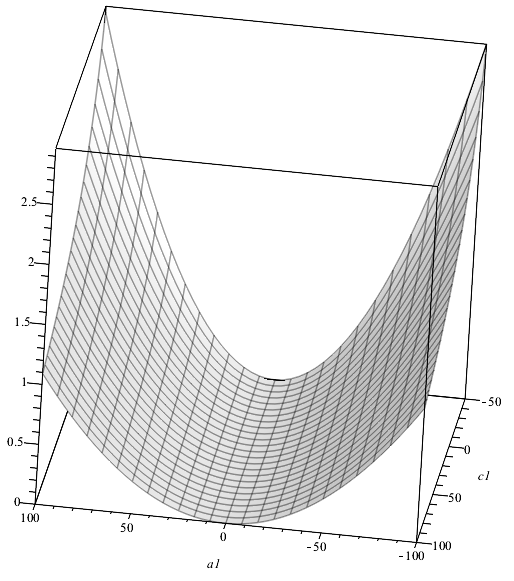

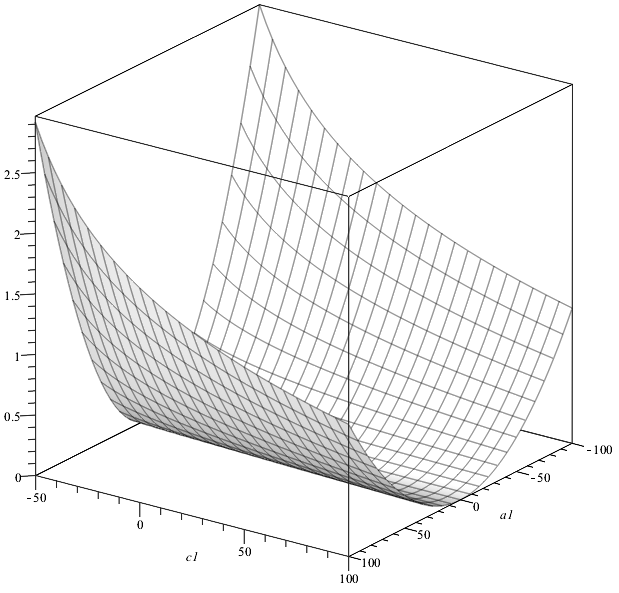

to find the minimum point of , we can draw the figure of

the function , (In a cube coordinate

system with axis and ) as shown on Figure 6,

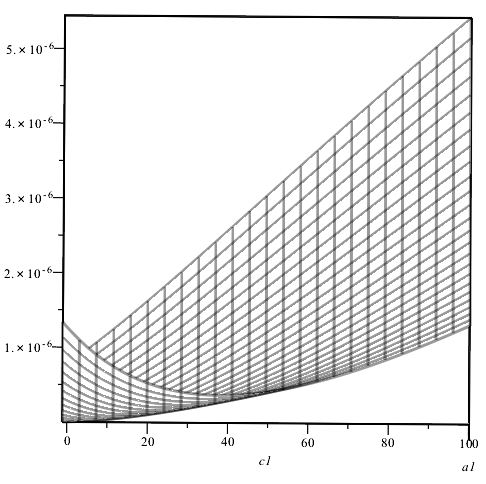

Figure 6 and Figure 10.

Figure 6 and Figure 6

are the projection of the graph of

(when 100,

100, which is a part of a surface) on the

plane (spanned by the axis and ) and plane,

respectively.

From these figures, we can find out that the influence of

to is much less than that of . In Figure 10,

we find that when reaches its minimum, is between

0.50 and 0.53, but there is not a definite range for .

It is possible that for different range of , the range of

when reaches its minimum will be different. But

considering that is a real,

should be greater than in theory. (For the fitting

data used here, should be greater than .) From Figure

6, we can see that touches its bottom

when 15. Although we can

not see clearly the exact value of of in the minimum points,

we can draw another figure of when

15 and

100 to observe more details (the figure is not

presented here), then we will find that the more detailed range of

for the minimum points is in the new figure (not

presented), next, draw the figures of

when 3,

1,

0.8 or 0.6, respectively,

while 100, we will find the

range of of the minimum points of is about [0.50,

0.53]. The projections of the figure 10 of

when

0.6 and 100

is shown on Figure 10 and Figure 10.

In Figure 6, for the curves on the bottom,

decrease with at first then increases with ,

but it is difficult to find the critical point in the figure, since

different curves have different critical points.

Figure 3: The graph of the data when

100,

100

Figure 4: The graph of the data when

100,

100 version 2

Figure 5: The projection of the graph of the data

on the plane when

100, 100

Figure 6: The projection of the graph of the data

on the plane when

100, 100

Figure 7: The graph of the data when

0.60,

100

Figure 8: The projection of the graph of the data

on the plane when

0.60, 100

Figure 9: The projection of the graph of the data

on the plane when

0.60, 100

Figure 10: Example of a surface with more than one bottom.

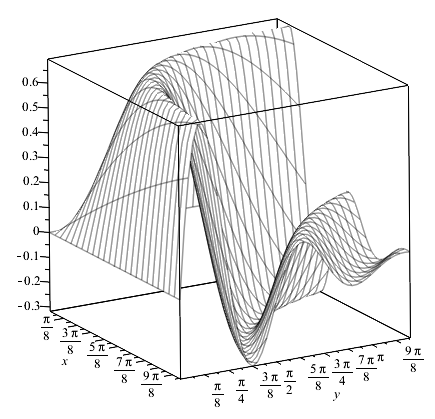

Although we can not find an satisfying value of or

from the figures above to construct a fitting function ,

these pictures show that the figure of

has only one bottom in the domain we are considering, unlike the figure

of another function shown on Figure 10,

so the existence of the minimum point is almost confirmed, therefore

we are confident to find the value of or in the

minimum point by numerical method. This guarantees the validity

of the numerical calculation by loop in next step.

3.2.2 Find

On the other hand, by the least square method, to fit the data

( = 1, 2, , ) by a linear function ,

the result is that

(24)

(25)

where =

is the average value of , = ,

= ,

= .

By definition, =

is the square of the average value of . So, by the least square

method, and are uniquely determined by the given data

( = 1, 2, , ).

For every given value of (greater than ), we can fit

( = , = 1, 2, ,

397) by a function

by the least square method, if we consider

and as and , respectively. Then

=

= ,

=

= ,

=

= ,

=

= ,

,

.

So and could both be considered as functions

of , denoted by , ,

since they are uniquely determined by with the given data.

Then

is a function of .

It will cost some time to plot the figure of the function

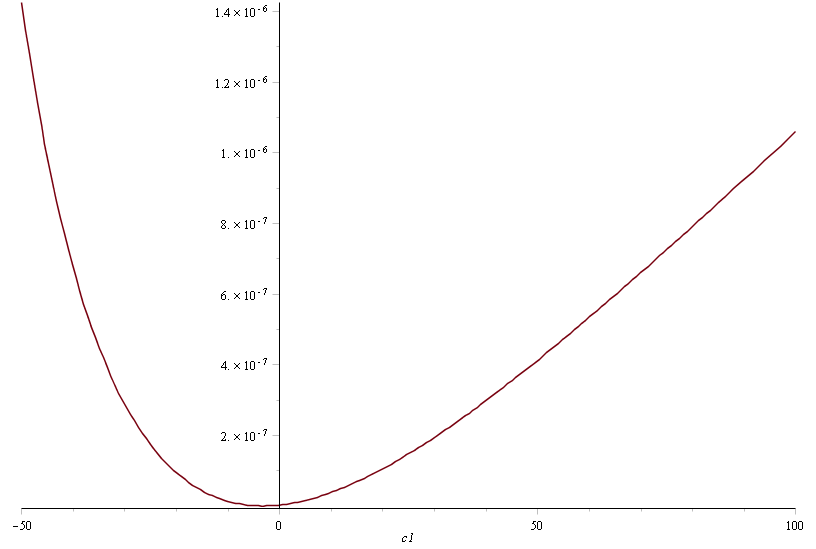

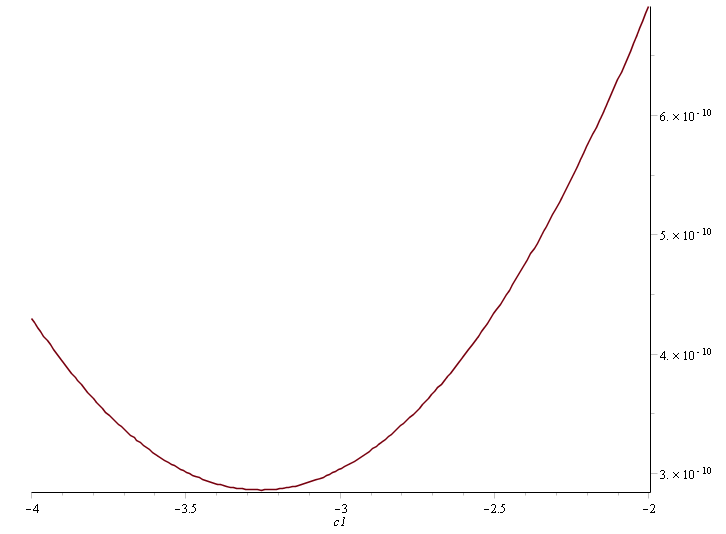

= in a CAS software.

If we plot the figure of the function = on

the coordinates (as shown on Figure 13, Figure 13

and Figure 13), we will find that reaches

its minimum when . On Figure 13,

we find that the curve of = is not so smooth.

The reason is that we hold up 18 significant digits in the process.

If we compute more significant digits in the process, the curve on

Figure 13 will be more smooth, at the cost of much

more time. By writing a small program (since the default function

to find the minimum provide by the software Maple 18 are unable to

deal with such a complicated function = involving

so much data), we can obtain a more accurate value of the critical

point

When the value of is obtained, we can find the value of

and by the least square method without difficulty,

i.e.,

But here is less than , so the estimation formula

for constructed from these coefficients is invalid when .

Figure 11: The graph of the function = when

100

Figure 12: The graph of the function = when

-2

Figure 13: The graph of the function = when

3.2.3 Confirm

In [1] we fit =

by by a function

when estimating , and found that

by iteration. Here the iteration method does not work well, so we

fit =

by a function

directly, which means that we have assumed that .

Here we may doubt that whether is the best

option for us?

Here we use the same idea described in subsection 3.2.1.

For every pair , we can obtain corresponding

and by the least square method, just like (24)

and (25), except that here .

So the square of the average error

could be considered as a function of and , as both

and

could be expressed by certain elementary functions of and

.

If we draw the figure of the function = ,

we will find that the surface has only one bottom when

,

, as shown on Figure 14. But the process to

draw the figure is time-consuming. It costs more than 5 hours on a

notebook (ThinkPad E40 Edge, with 6 GB RAM and AMD P360 Dual-Core

Processor 2.30GHz) by Maple 18 in Ubuntu 14.04.1 system.

Figure 14: The graph of the function = when

,

Figure 15: The graph of the data

and the fitting curve

Figure 16: The graph of the data and the

fitting curve

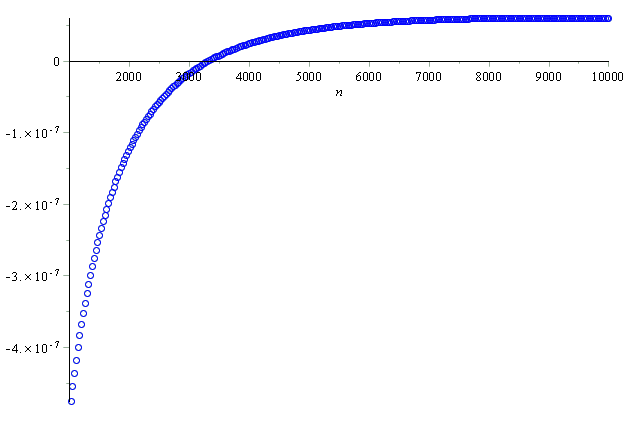

Figure 17: The Relative Error of when 1000

10000, step 300

After that, by written another program, we can obtain the approximate

value of where touches the bottom, i.e.

, , when 18

significant digits are involved in the process, which still costs

tens of minutes. Considering that we have used only a small part of

data, we can not afford the time for computing more significant digits

in process, and the computing is so complicated hence error accumulation

effect is considerable, so we choose while it

differs very little with . Another reason is that we prefer

simple exponent, as the time spend on computing a square root is much

less than that to compute a power with exponent in general.

Here the value of is obviously different from

the value obtained at the end of subsection (3.2.2),

because of the little difference on . Therefore, it will be

fine to use the result in subsection (3.2.2).

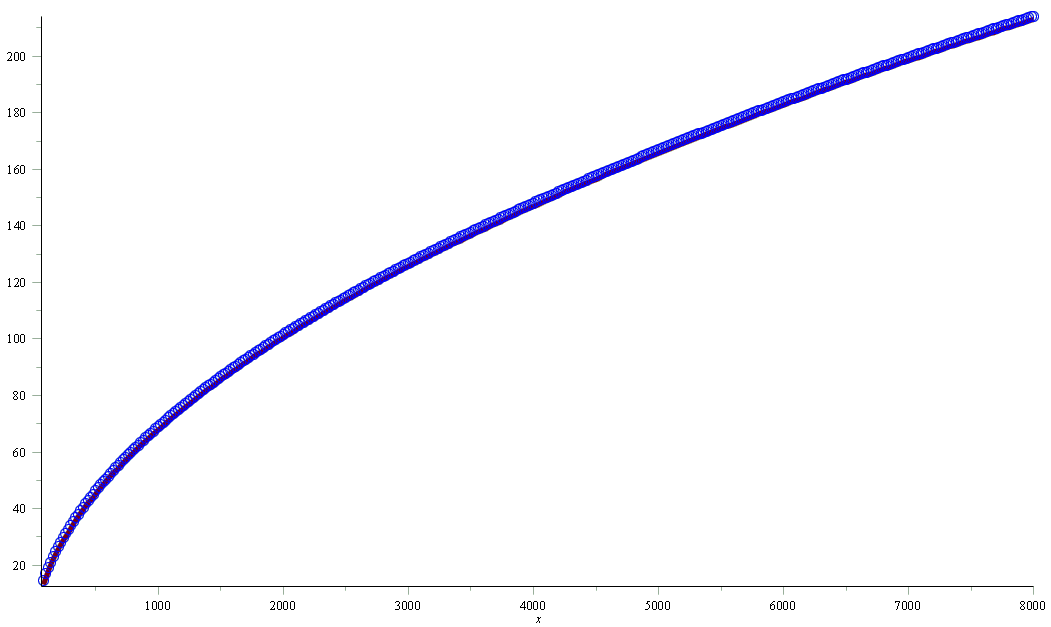

Figure 18: The graph of the data

and the fitting curve

In this figure, the points are shown as small circles which are very

close to each other. Theses crowded circles seams like a thick curve.

A fitting curve passes though the center of these circles. The fitting

curve might not be found in reduce printing. That means the curve

fits the points (displayed as circles) very well.

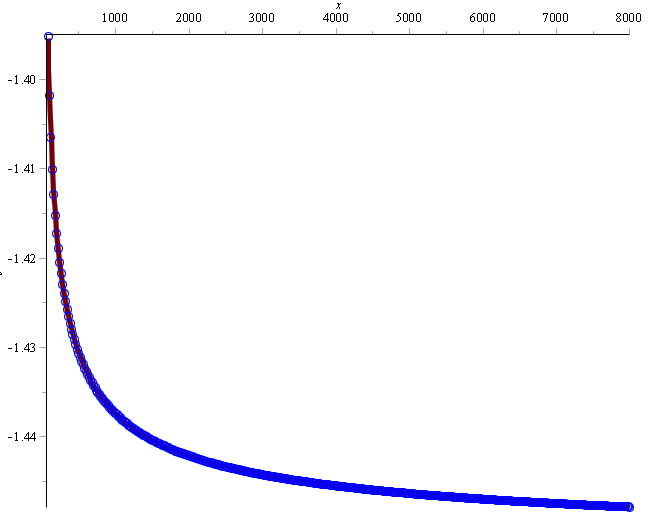

3.2.4 The Result

By the value = 0.5097429624, = 1.453552800,

= obtained in subsection 3.2.2,

we will have a fitting function

.

The figure of (when

8000) together with the figure of the data

( = , = 1, 2, , 397) are shown on Figure

17. It shows that fits

very well.

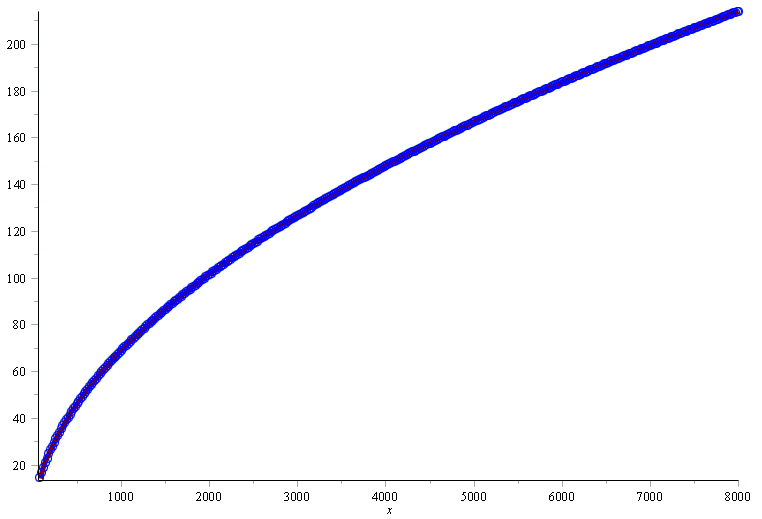

Then we could fit by

(26)

The figure of the function

together with the figure of the data

( = , = 1, 2, , 397) are shown on Figure

17. It seems that

fits very well.

The relative error of is shown on Table 7

(when ) and Figure 17 (when

1000 ).

When , the relative error of is still greater

than . Although it is much better than the error of ,

it is not as good as expect when . If we take the round approximation

by

(27)

the relative error will be obviously smaller with a few exceptions,

as shown on Table 7.

Later we will find out that it is obviously greater than the relative

error of and obtained in the

next subsection by modifying the denominator part; when ,

the relative error of is about 1000 times of that

of .

Table 6: The relative error of to when .

Table 7: The relative error of

to when .

When 30

1000, the relative error of

is closed to that of .

3.3 Method B: Modifying the Denominator

Since ,

we consider estimating by

,

(i.e., fit

by a function ), where is a cubic function

or a function like

But the results are worse, as the relative errors are obviously much

greater than the relative error of when .

Then we consider estimating by ,

or fit

by a function

(28)

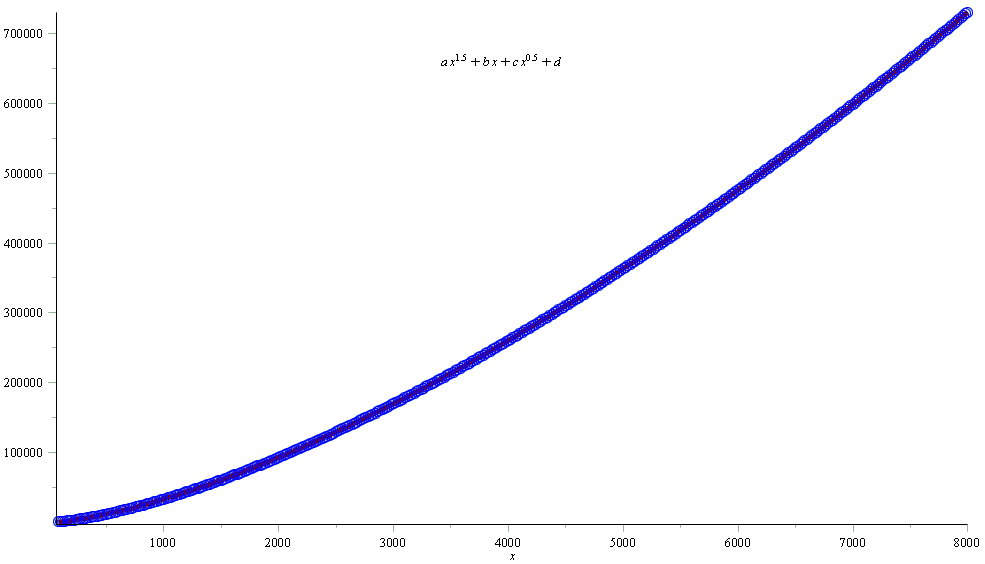

The result is very good. The figure of the data

and the fitting curve are shown on Figure 18

on page 18. Here the fitting curve is

displayed by a thick continuous curve, which lies in the middle of

the area the circles occupied. Since the circles are too crowded,

the circles themselves look like a very thick curve.

Table 8: The relative error of to when .

Table 9: The relative error of

to when .

Figure 19: The graph of the data and the fitting curve

Figure 20: The Relative Error of when 1000

10000, step 300

Figure 21: The graph of the data

and the fitting curve

Figure 22: The Relative Error of when 1000

10000, step 300

The values of the coefficients in the expression of are

as follow,

The value of is very close to 1, which means that this fitting

function coincides with the Ingham-Meinardus asymptotic formula very

well.

So we have an estimation formula

(29)

We may call it the Ingham-Meinardus revised estimation formula

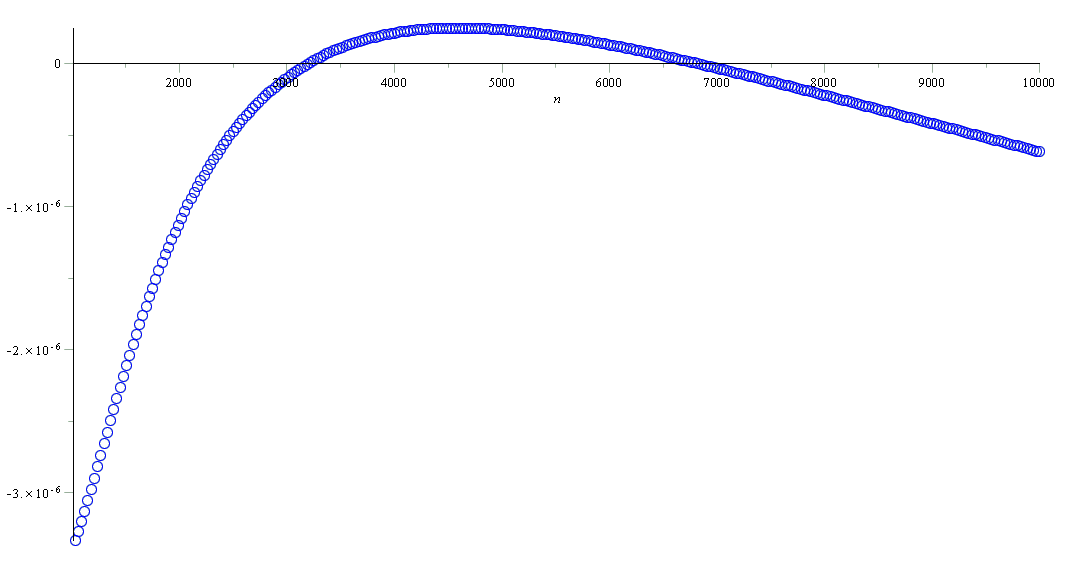

1. The graph

of is shown on Figure 22

on page 22, together with the

data points of . This revised estimation

formula is much more accurate than the asymptotic formula. The relative

error is less than when > 2000 (as shown on

Figure 22 on page 22),

and less than when 30 (as shown on

Table 9 on page 9).

The relative error of the round approximation

is shown on Table 9 on page 9.

But Equation (29) is not so satisfying when

, especially when as the relative error is not negligible

for some value of .

As we already know that ,

or

,

which means that when fitting

by a function shown in Equation (28),

the coefficient should be exactly 1, hence we should fit

by a function , or fit

by a function

(30)

The figure of the data

is shown on Figure 22 on page 22

(together with the figure of the fitting function generated

by the least square method).

The values of the coefficients in Equation (30)

are as follow

So we have another estimation formula for ,

(31)

Table 10: The relative error of to when .

Table 11: The relative error of

to when .

We may call it the Ingham-Meinardus revised estimation formula

2. The graph

of is nearly the same as that

of shown on Figure 22

on page 22. The second revised

estimation formula is much more accurate than the first one. The relative

error is less than when > 3000 (as shown on

Figure 22 on page 22),

about of the relative error of .

When < 10, the relative error is also distinctly less than that

of (as shown on Table 11

on page 11). The relative error

of the round approximation

is shown on Table 11 (on page

11).

It should be mentioned that in Figure 22

on page 22, the graph of the data points

lie in a line, so we might be willing to fit this line by a first

order equation. The result is

If we use this fitting function instead of generated

above, the relative error to fit will be about 10000 times

more, that is about 20 times more than that of .

So we did not use linear function to fit the data

before.

Table 12: The relative error of

to when .

Table 13: The relative error of

to when .

3.4 Method C: Fittong

We wonder whether we can fit by a function

, then estimate by which

may be believed more accurate than at the price

of being more complicated.

By the same tricks used at the beginning of this subsection, we will

have

So we may fit by

where is a quadratic function or a function like

That means, we can fit

by a function . But the result is useless. Although

will fit the data

very well, but the relative error of

to is much greater than that of or ,

and the relative error differs very little with that of

when is small. Besides, the formula

are much more complicated than and .

If we use the trick mentioned in 3.3, to fit

by

where is a function like

as we already know that the coefficient of should be 1 in

theory. The result will be a little better, but useless too. The accuracy

is not as good as that of .

Then we consider fitting

by a function . If is in the form

or , the result is useless, too. If

is in the form , it will be barely

satisfactory. If is in the form

or , the result

will be much better than the previous forms, but the accuracy (when

estimating ) is not as good as that of

and .

The result of is

or

The relative error of

(32)

and

(33)

to when 1000 10000 are shown

on Figure 25 and Figure 25

(page 25), respectively. In this

interval (1000, 10000), is obviously more accurate than

When 1000 the relative error of

and are shown

on Table 13 (page 13)

and Table 13 ( page 13).

In this case, is better than . But neither

of them is as good as or ,

although they are more complicated than and

.

Figure 23: The Relative Error of when 1000

10000, step 300

Figure 24: The Relative Error of when 1000

10000, step 300

Figure 25: The graph of the data

3.5 Estimate When

All the estimation function for found now are with very good

accuracy when is greater than 1000, but they are not so accurate

when , especially when . Although

and are better than others, the relative error

are still greater than when .

Table 14: The relative error of to when .

Table 15: The relative error of to when .

When , it is too difficult to fit

by a simple smooth function with high accuracy, as shown on Figure

25 (on page 25).

The figure of the points

( = 3, 4, , 100) is not so complicated (as shown on

Figure 25). It seems that we can fit them by

a simple piecewise function with 2 pieces, as the even points (where

is even) lie roughly on a smooth curve, so do the odd points.

If we try to fit them respectively, we will have the fitting function

below:

(34)

Hence we can calculate ( ) by

(35)

Consider that is an integer, we can take the round approximation

of Equation (35),

(36)

Here begins from 3, not 1 or 2, because

is meaningless since , and differs

from a lot. Besides, the value of and are

clear by definition, so there is no need to use a complicated formula

to estimate them.

The relative error of (or )

to are shown on Table 15 (or

Table 15) on page 15.

Compared them with Table 11 on

page 11, we will find that

when , is more accurate than

; when , is better.

4 Conclusion

We have presented a recursion formula and several practical estimation

formulae with high accuracy to calculated the number of conjugate

classes of derangements of order , or the number of isotopy classes

of Latin rectangles.

If we want to obtain the accurate value of , we can use the

recursion formula (10) and write a program based

on it, while sometimes we need to know the estimation value in a

program for technique reason especially when we use a general programming

language.

If we want to obtain the approximation value of with high

accuracy, we can use the formulae (31), (36),

(29), etc.

When , we can use

(Equation (36)) , with a relative error

less than 0.11% (while ) or mainly 0 with

very few exceptions (while ); when ,

we can use (Equation (31)).

When , formulae (Equation (27)),

(Equation (29)),

(Equation (32)) and (Equation

(33)) are also very accurate although they

are not as good as Equations (31).

With the asymptotic formula (18) described in [30],

we can obtain some estimation formulae with high accuracy for some

other types of restricted partition numbers by the methods mentioned

in this paper or in [1].

Data Availability

The figures and tables used to support this study are included within

the article. The other data used to support this study are obtained

from a program made by the first author.

Conflicts of Interest

The authors declare that there are no conflicts of interest regarding

the publication of this paper.

Acknowledgements

This work was supported in part by the Fund of Research Team of Anhui

International Studies University, NO. awkytd1909.

The author would like to express the gratitude to the anonymous reviewers

for their valuable advice.

References

[1]

W.-W. Li, “Estimation of the Partition Number: After Hardy and Ramanujan,”

ArXiv e-prints, Dec. 2016.

arXiv:1612.05526 [math.NT].

[2]

M. Hall, Jr., “A survey of combinatorial analysis,” in Some aspects

of analysis and probability (I. Kaplansky and etc, eds.), vol. IV of Surveys in applied mathematics, pp. 35 – 104, John Wiley and Sons, Inc.

[New York] and Chapman and Hall, Limited [London], 1958.

[3]

E. W. Weisstein, ““Partition Function P." From MathWorld – A Wolfram Web

Resource.” Internet: http://mathworld.wolfram.com/PartitionFunctionP.html

(accessed September 20, 2015), 1999-2015.

[4]

N. J. A. Sloane, “ A000041, number of partitions of (the partition

numbers). (Formerly M0663 N0244) , in “The On-Line Encyclopedia of Integer

Sequences (OEIS ®)".” Internet: http://oeis.org/A000041 (accessed

September 20, 2015).

[5]

Anonymous, ““Bibliography on Partitions" in “Mathematical BBS".”

Internet:

http://felix.unife.it/Root/d-Mathematics/d-Number-theory/b-Partitions

(accessed September 12, 2016), December 2007.

[6]

M. Newman, “Weighted restricted partitions,” Acta Arithmetica,

vol. 5, no. 4, pp. 371 – 380, 1959.

[7]

D. B. Lahiri, “Some restricted partition functions: Congruences modulo 3,”

Pacific Journal of Mathematics, vol. 28, no. 3, pp. 575 – 581, 1969.

Subjects: Primary: 10.48, MR0241377, Zentralblatt MATH identifier:

0172.05602.

[8]

D. B. Lahiri, “Some restricted partition functions: Congruences modulo 5,”

Journal of the Australian Mathematical Society, vol. 9,

pp. 424 – 432, May 1969.

[9]

D. B. Lahiri, “Some restricted partition functions: Congruences modulo 7,”

Transactions of the American Mathematical Society, vol. 140,

pp. 475 – 484, Jun. 1969.

Subjects: Primary 10.48, MR 0242784 (39 #4111).

[10]

R. Jakimczuk, “Restricted Partitions: Elementary Methods,” International Journal of Contemporary Mathematical Sciences, vol. 4, no. 2,

pp. 93 – 103, 2009.

[11]

B. Kronholm, “A result on Ramanujan-like congruence properties of the

restricted partition function p(n,m) across both variables,” INTEGERS:

The Electronic Journal of Combinatorial Number Theory, vol. 12, p. A63,

November 2012.

[12]

A. Folsom, Z. A. Kent, and K. Ono, “-adic properties of the partition

function,” Advances in Mathematics, vol. 229, pp. 1586 – 1609,

February 2012.

[13]

E. Belmont, H. Lee, A. Musat, and S. Trebat-Leder, “-adic properties of the

partition function,” Monatshefte für Mathematik, vol. 173,

pp. 1 – 34, January 2014.

[14]

K. Thanigasalam, “Congruence Properties of Certain Restricted Partitions,”

Mathematics Magazine, vol. 47, pp. 154 – 156, May 1974.

[15]

D. R. Hickerson, “A note on congruence properties of certain restricted

partitions,” Mathematics Magazine, vol. 48, p. 102, Mar. 1975.

[16]

M. Culek and A. Knecht, “Congruences of Restricted Partition Functions.”

Internet: http://citeseerx.ist.psu.edu/viewdoc/download?doi=

10.1.1.509.2649&rep=rep1&type=pdf (accessed October 02, 2015), 2002.

[17]

B. Kronholm, “On Congruence Properties of p(n, m),” Proceedings of the

American Mathematical Society, vol. 133, pp. 2891 – 2895, Oct. 2005.

[18]

B. Kronholm, “On Congruence Properties of Consecutive Values of ,”

INTEGERS: The Electronic Journal of Combinatorial Number Theory,

vol. 7, Mar. 2007.

#A16.

[19]

B. C. Berndt, “Ramanujan’s congruences for the partition function, modulo 5,

7, and 11,” International Journal of Number Theory, vol. 03,

pp. 349 – 354, September 2007.

[20]

G. E. Andrews and B. C. Berndt, “Ramanujan’s Unpublished Manuscript on the

Partition and Tau Functions,” in Ramanujan’s Lost Notebook: Part

III, pp. 89 – 180, Springer Science+Business Media New York, 2012.

[21]

B. Kronholm, “Generalized congruence properties of the restricted partition

function ,” The Ramanujan Journal, vol. 30, pp. 425 – 436,

April 2013.

[22]

N. J. A. Sloane, ““Restricted partitions" in OEIS wiki.” Internet:

http://oeis.org/wiki/Restricted_partitions (accessed September 20, 2015),

December 2011.

[23]

D. M. Bressoud, “Integer Partitions: Restricted Number and Part Size,” in

NIST Digital Library of Mathematical Functions (DLMF) (F. W. J.

Olver, D. W. Lozier, and R. F. Boisvert, eds.), August 2015.

Online companion to [25].

[24]

F. W. J. Olver, D. W. Lozier, and R. F. Boisvert, “Integer Partitions: Other

Restrictions,” in NIST Digital Library of Mathematical Functions

(DLMF) (F. W. J. Olver, D. W. Lozier, and R. F. Boisvert, eds.), National

Institute of Standards and Technology (NIST), August 2015.

Online companion to [25].

[25]

F. W. J. Olver, D. W. Lozier, and R. F. Boisvert, eds., NIST Handbook of

Mathematical Functions.

New York, NY: Cambridge University Press, May 2010.

Print companion to [24].

[26]

A. Greenbaum and T. P. Chartier, Numerical Methods: Design, Analysis, and

Computer Implementation of Algorithms.

New Jersey, NJ: Princeton University Press, Apr 2012.

[27]

D. Kincaid and W. Cheney, Numerical Analysis: Mathematics of Scientific

Computing, Third Edition, vol. 2 of Pure and Applied Undergraduate

Texts.

American Mathematical Society, 2002.

[28]

W. Lichten, Data and Error Analysis.

Prentice Hall, Oct 1998.

[29]

A. E. Ingham, “A Tauberian Theorem for Partitions,” Annals of

Mathematics, Second Series, vol. 42, pp. 1075 – 1090, Dec. 1941.

[30]

D. M. Kane, “An elementary derivation of the asymptotics of partition

functions,” The Ramanujan Journal, vol. 11, pp. 49 – 66,

February 2006.

[31]

G. H. Hardy and S. R. Ramanujan, “Asymptotic Formulae in Combinatory

Analysis,” Proceedings of the London Mathematical Society, s2,

vol. XVII, pp. 75 – 115, January 1918.

[32]

P. Erdős, “The Evaluation of the Constant in the Formula for the Number

of Partitions of ,” Annals of Mathematics. Second Series, vol. 43,

pp. 437 – 450, July 1942.

[33]

D. J. Newman, “The evaluation of the constant in the formula for the number of

partitions of ,” American Journal of Mathematics, vol. 73,

pp. 599 – 601, July 1951.

[34]

D. J. Newman, “A simplified proof of the partition formula,” The

Michigan Mathematical Journal, vol. 9, pp. 283 – 287, Jan. 1962.

MR0142529, ZMI 0105.26701.

[35]

T. M. Apostol, “Functions of Number Theory, Additive Number Theory:

Unrestricted Partitions,” in NIST Digital Library of Mathematical

Functions (DLMF) (F. W. J. Olver, D. W. Lozier, and R. F. Boisvert, eds.),

August 2015.

http://dlmf.nist.gov/27.14, Release 1.0.10 of 2015-08-07, (accessed

November 12, 2015).

![[Uncaptioned image]](/html/1612.08186/assets/x1.png)

![[Uncaptioned image]](/html/1612.08186/assets/x2.png)

![[Uncaptioned image]](/html/1612.08186/assets/x3.png)

![[Uncaptioned image]](/html/1612.08186/assets/x4.png)

![[Uncaptioned image]](/html/1612.08186/assets/x5.png)

![[Uncaptioned image]](/html/1612.08186/assets/x6.png)

![[Uncaptioned image]](/html/1612.08186/assets/x7.png)

![[Uncaptioned image]](/html/1612.08186/assets/x8.png)

![[Uncaptioned image]](/html/1612.08186/assets/x9.png)

![[Uncaptioned image]](/html/1612.08186/assets/x10.png)

![[Uncaptioned image]](/html/1612.08186/assets/x11.png)

![[Uncaptioned image]](/html/1612.08186/assets/x12.png)

![[Uncaptioned image]](/html/1612.08186/assets/x13.png)

![[Uncaptioned image]](/html/1612.08186/assets/x14.png)

![[Uncaptioned image]](/html/1612.08186/assets/x15.png)