Nonparametric estimation of conditional value-at-risk and expected shortfall based on extreme value theory111We thank Peter C. B. Phillips, Eric Renault, an Associate Editor and an anonymous referee for comments that improved the paper substantially. Any remaining errors are the authors’ responsibility.

| Carlos Martins-Filho | ||

|---|---|---|

| Department of Economics | IFPRI | |

| University of Colorado | 2033 K Street NW | |

| Boulder, CO 80309-0256, USA | & | Washington, DC 20006-1002, USA |

| email: carlos.martins@colorado.edu | email: c.martins-filho@cgiar.org | |

| Voice: + 1 303 492 4599 | Voice: + 1 202 862 8144 | |

| Feng Yao | ||

|---|---|---|

| Department of Economics | School of Economics and Trade | |

| West Virginia University | Guangdong University of Foreign Studies | |

| Morgantown, WV 26505, USA | & | Guangzhou, Guangdong 510006, P. R. China |

| email: feng.yao@mail.wvu.edu | email: 201470006@oamail.gdufs.edu.cn | |

| Voice: +1 304 293 7867 | Voice: + 86 20 3932 8858 | |

| Maximo Torero |

|---|

| IFPRI |

| 2033 K Street NW |

| Washington, DC 20006-1002, USA |

| email: m.torero@cgiar.org |

| Voice: + 1 202 862 5662 |

October, 2016

Abstract. We propose nonparametric estimators for conditional value-at-risk (CVaR) and conditional expected shortfall (CES) associated with conditional distributions of a series of returns on a financial asset. The return series and the conditioning covariates, which may include lagged returns and other exogenous variables, are assumed to be strong mixing and follow a nonparametric conditional location-scale model. First stage nonparametric estimators for location and scale are combined with a generalized Pareto approximation for distribution tails proposed by Pickands (1975) to give final estimators for CVaR and CES. We provide consistency and asymptotic normality of the proposed estimators under suitable normalization. We also present the results of a Monte Carlo study that sheds light on their finite sample performance. Empirical viability of the model and estimators is investigated through a backtesting exercise using returns on future contracts for five agricultural commodities.

Keywords and phrases. conditional value-at-risk, conditional expected shortfall, extreme value theory, nonparametric location-scale models, strong mixing.

JEL classifications. C14, C15, C22, G10.

AMS-MS classifications. Primary: 62G32, 62G07, 62G08, 62G20.

1 Introduction

Conditional value-at-risk (CVaR) and conditional expected shortfall (CES) are two of the most used synthetic measures of market risk in empirical finance (see Duffie and Singleton (2003), McNeil et al. (2005) and Danielsson (2011)). From a statistical perspective they have straightforward definitions. Let denote a stochastic process representing the returns111Let denote the price of a financial asset at time . In this paper a “return” is defined as . We adopt this definition because in practice, regulators, portfolio and risk managers are mostly concerned with the distribution of losses, i.e., negative values of . on a given stock, portfolio or market index, where indexes a discrete measure of time, and denote the conditional distribution of given . The vector normally includes lag returns , for some , as well as other relevant conditioning variables that reflect economic or market conditions. Then, for , -CVaR() is defined to be the -quantile associated with and -CES() is defined to be the conditional expectation of given that exceeds -CVaR(), i.e., -CES()=.222For and an arbitrary distribution function , we define the -quantile associated with as .

In this paper we consider the estimation of -CVaR() and -CES() for processes that admit a location-scale representation

| (1) |

where and are nonparametric functions defined on the range of , is independent of , and is an independent and identically distributed (IID) innovation process with , and distribution function belonging to a suitably restricted class (see section 2). This representation can be viewed as a nonparametric generalization of certain autoregressive conditionally heteroscedastic (ARCH) structures and has been studied by Masry and Tjøstheim (1995), Härdle and Tsybakov (1997), Masry and Fan (1997) and Fan and Yao (1998), among others.333We rule out more general innovation processes, such as those appearing in semi-strong GARCH processes, that are simply stationary, ergodic with satisfying a martingale difference condition. See, e.g., Drost and Nijman (1993), Escanciano (2009) and Linton et al. (2010). Under (1) we have

| (2) |

and

| (3) |

where denotes the conditional -quantile associated with and is the -quantile associated with .

In insurance and empirical finance, where regulators and portfolio managers are interested in high levels of risk, with in the vicinity of 1 (Chernozhukov and Umantsev (2001); Tsay (2010)), an important concern for inference is that conventional asymptotic theory does not apply sufficiently far in the tails of (see Chernozhukov (2005, p. 807)). Hence, we focus on proposing and characterizing the asymptotic behavior of nonparametric estimators for -CVaR() and -CES() when . In the conditional quantile (regression) literature this is commonly referred to as extreme quantile regression (Chernozhukov (2005)) and in empirical finance the corresponding notion is that of extreme CVaR, see e.g., Embrechts et al. (1997, p. 349) and Chernozhukov and Umantsev (2001, p. 273).

Nonparametric estimators of -CVaR and -CES for the non-extreme case, where is fixed in , have been proposed and studied in several papers. Since -CVaR() is a conditional quantile, estimation can naturally proceed using nonparametric regression quantiles as in Yu and Jones (1998), Cai (2002), Cosma et al. (2007) or Cai and Wang (2008). These estimators for -CVaR() can then be used to produce nonparametric estimators for -CES() as in Scaillet (2005), Cai and Wang (2008), Kato (2012) and Linton and Xiao (2013). Also, for the non-extreme case, there exists a large literature on nonparametric estimation of unconditional value-at-risk and expected shortfall, see e.g., Scaillet (2004), Chen and Tang (2005), Chen (2008), Linton and Xiao (2013) and Hill (2015), that is indirectly related to our work.

We propose a two-stage estimation procedure for -CVaR and -CES. First, motivated by (1), nonparametric estimators for and are obtained and used to produce standardized residuals. Second, these residuals are used to obtain estimators for and using a likelihood procedure to estimate the parameters of a Generalized Pareto Distribution (GPD) that approximates the upper right tail of . This stage is motivated by Theorem 7 in Pickands (1975) and extends the work of Smith (1987). These estimators for and are then combined with the first stage estimators for and to produce estimators for -CVaR() and -CES(). To our knowledge, this two stage estimation approach was first proposed by McNeil and Frey (2000) in the case where and are indexed by a finite dimensional parameter. They provided no asymptotic characterization or finite sample properties for the resulting estimators of conditional value-at-risk or expected shortfall. However, their backtesting exercise on several time series of selected market indexes provided encouraging evidence of the estimators’ performance. Martins-Filho and Yao (2006) generalized the estimation framework of McNeil and Frey to the case where and are nonparametric functions. They demonstrated via an extensive Monte Carlo simulation, and through backtesting, that accounting for nonlinearities in and can be important in improving the estimators’ finite sample performance. Martins-Filho et al. (2015) provides an asymptotic characterization of the two stage estimation procedure for -CVaR when in a model with constant and unknown variance () and a process ( indicates the transposition of the vector ) that is IID. Their results, however, are of limited use in empirical finance where the IID assumption is untenable and cannot be adequately modeled as a constant function of . Furthermore, by restricting attention to the case where , i.e., a scalar, they failed to elucidate the restrictions that the dimension may impose on nonparametric estimation of conditional value-at-risk and expected shortfall.

Here, we extend Martins-Filho et al. (2015) in three important directions: a) we relax the assumption that is an IID process and instead consider the case where the process is strictly stationary and strong mixing of a suitable order. This allows for the presence of lagged values of in the conditioning vector , a possibility not covered in our earlier paper and of significant practical interest; b) we allow the conditional variance to be a non-constant function of ; and c) we consider the estimation of -CVaR() and -CES(). We first establish consistency and asymptotic normality of the estimators for and based on the maximum likelihood estimators for the parameters of the (approximating) GPD using residuals from the first stage estimation. From a technical perspective, this extends the results in Smith (1987) to the case where only residuals, rather than the actual sequence , are observed. These results are used to obtain consistency and asymptotic normality of our proposed estimators for -CVaR() and -CES(). Estimators, like ours, that rely on tail approximations based on the GPD are normally asymptotically biased and require bias correction for valid inference. Hence, we provide bias-corrected versions of our estimators that can be easily used for inference as their asymptotic distributions are correctly centered.

Besides this introduction, this paper has five more sections and two appendices. Section 2 provides a discussion of the main restrictions we impose on , as well as a motivation, description and discussion of the estimation procedure. Section 3 contains a list of assumptions needed to study the estimators for and and the main theorems that describe the asymptotic behavior of our estimators. Section 4 contains a Monte Carlo study that sheds light on the finite sample behavior of our estimators and contrasts their performance with the estimators proposed by Cai and Wang (2008). Section 5 provides an empirical application in which -CVaR and -CES are estimated using time series of returns on future contracts for five widely traded agricultural commodities. A backtesting exercise is also conducted for each of the time series. Section 6 provides concluding remarks and gives some directions for future research. Tables and figures associated with the Monte Carlo study and the empirical exercise are provided in Appendix 1. The proofs for Theorems 2 through 5 are provided in Appendix 2. Supporting lemmas and their proofs, as well as the proof of Theorem 1, can be found in the online supplement to this article available at Cambridge Journals Online (journals.cambridge.org/ect).

2 Estimation of -CVaR and -CES

As stated in the introduction, our estimation procedure has two stages. In the first stage we produce a sequence of standardized nonparametric residuals based on the estimation of and . Given a sample , we consider a local linear (LL) estimator for , denoted by , where , is a multivariate kernel function and is a bandwidth. For the estimation of , we follow the procedure proposed in Fan and Yao (1998), where we obtain a sequence and define , where , is a multivariate kernel function and is a bandwidth, both potentially different from those used in the definition of .444Since may contain up to lagged values of , the effective sample size used in the estimation of and is . However, for notational ease, we assume that are observed as needed to define the relevant sums of length . The estimators and are used to produce a sequence of standardized nonparametric residuals , where

| (4) |

In the second stage, we use these residuals to construct estimators for and , appearing in (2) and (3), which are combined with and to produce our estimators for and . Whereas to motivate the first stage of estimation, the only restrictions imposed on were that it has mean zero and variance one, the motivation for the second stage requires additional restrictions. First, we assume

Assumption FR1: a) is strictly monotonic and absolutely continuous with positive density such that for some , ; b) is such that for some ; c) is -times continuously differentiable with for some constant and .

Remarks on FR1: 1. By Proposition 1.15 in Resnick (1987), if satisfies FR1 a), then it belongs to the maximum domain of attraction of a Fréchet distribution with parameter , denoted here by .555See Leadbetter et al. (1983), Resnick (1987) or Embrechts et al. (1997) for the definition of maximum domains of attraction. This, in turn, is equivalent to being slowly varying as (see Gnedenko (1943)). Thus, any satisfying FR1 a) is such that is slowly varying at infinity.

2. The restriction that belongs to the domain of attraction of a Fréchet distribution is not entirely arbitrary. There are only two other possibilities: a) belongs to the domain of attraction of a (reverse) Weibull distribution, in which case has a finite right endpoint, a restriction that is not commonly placed on the innovation associated with location-scale models; b) belongs to the domain of attraction of a Gumbel distribution, in which case, when has an infinite right endpoint is rapidly varying at infinity (Resnick (1987)), a case we must avoid to derive the asymptotic properties of our estimators. Thus, distribution functions where decays exponentially fast as are ruled out by FR1 a).

3. We note that assumptions FR1 a) and b) imply that . This ensures that the (right) tail decays sufficiently fast as . It rules out distribution functions with right tails that are “too thick” in the sense of . Hence, is in a class of distributions that can have thick tails, but not so thick as to prevent the existence of moments slightly larger than four. The restriction is critical for the asymptotic results we derive and can be empirically binding in that many financial time series appear to have heavy tails with (Embrechts et al. (1997)).

4. FR1 c) is needed to provide asymptotic characterizations of our proposed estimators (see, e.g., the proof of Lemma 5), but is not required to provide a motivation for their definition.

Theorem 7 in Pickands (1975) shows that if , then its extreme upper tail is uniformly close to a generalized Pareto distribution (GPD). Formally, for and some function with ,

| (5) |

where and with . As in Davis and Resnick (1984, p. 1471) and Smith (1987, p. 1176), we use the equivalence in (5) to motivate our estimator for . To this end, let be a nonstochastic subsequence on such that and as . For notational simplicity put and define . Then, and as . Since (5) is valid for any sequence , we put and note that by strict monotonicity of , . Then, putting and noting that we have where provided . Note that since , we have as . By (5) we have that for sufficiently large Rearranging the terms, we have

| (6) |

which motivates our proposed estimator for . We first use the residuals to estimate by integrating a Rosenblatt kernel estimator for the density , i.e.,

| (7) |

where is a univariate kernel and is a bandwidth. Then, we define the estimator for as the solution for . We note that a simpler estimator is , the -quantile associated with the empirical distribution of the nonparametric residuals . We prefer because it is well known from the unconditional distribution and quantile estimation literature (Azzalini (1981); Falk (1985); Yang (1985); Bowman et al. (1998); Martins-Filho and Yao (2008)) that smoothing beyond that attained by the empirical distribution can produce significant gains in finite samples with no impact on asymptotic rates of convergence.

To estimate and we follow the maximum likelihood procedure suggested by Smith (1987) using the approximation provided by . To this end we define the ascending order statistics and construct a sequence of exceedances , which are used to obtain maximum likelihood estimators for and based on the density associated with the GPD. Here, it is important to note that the number of residuals that exceed , i.e., is stochastic and generally different from . Our estimators are a solution for the likelihood equations

| (8) |

where . Then, based on (6) our estimator for is given by

| (9) |

To motivate our estimator for we place the following additional restriction on ,

Assumption FR2: For we have for each , where as is regularly varying with index and .

If the exceedances over the quantile were distributed exactly as , then integration by parts gives (Embrechts et al. (1997, p. 165)). In the general case where the exceedances are not distributed as , but satisfies assumptions FR1 a), b) and FR2 it can be easily shown (see Lemma 8 in the online supplement) that . This motivates our proposed estimator for which is given by

| (10) |

Remarks on FR2: 1. Assumption FR2 is equivalent to requiring that the error in approximating the tail by a Pareto distribution be given by as (see Theorem 2.2.2, in Goldie and Smith (1987, p. 48)). Assumptions on how the approximating error decays are necessary for an asymptotic characterization of estimators for the parameters of the GPD. Our FR2 is similar to the condition SR2 in Smith (1987), whereas a stronger version of it is assumed by Hall (1982). Goldie and Smith (1987) provides a comprehensive discussion of these second order assumptions on the characterization of estimators that, like ours, depend on Extreme Value Theory.

2. FR2 is necessary in providing a first order approximation for the expected value of the score associated with the likelihood procedure, which is used in characterizing and correcting the asymptotic bias. For example, in the case of the parameter (see Appendix 2)

| (11) |

providing a handle on how the asymptotic bias of the estimators we propose depends on and .

3. A zero-mean and suitably scaled (to have variance 1) Student-t distribution with degrees of freedom satisfies assumptions FR1, FR2 and the restrictions on the innovation in our location-scale model. In this case, FR1 is satisfied with .

3 Asymptotic characterization of the proposed estimators

3.1 Assumptions and existence of and

We begin the study of the asymptotic behavior of our estimators by establishing that a solution for equation (8) exists and corresponds to a local maximum of the likelihood function. Our strategy is to show that score functions associated with are uniformly asymptotically equivalent in probability to those associated with , where , are ascending order statistics associated with and is the stochastic number of exceedances over the nonstochastic threshold .

This is accomplished in two steps. First, we show in Lemma 1 (see online supplement) that the score functions associated with are uniformly asymptotically equivalent in probability to those associated with where , and . That is, is the quantile of order associated with the empirical distribution , where . This, together with Lemma 5 in Smith (1985), establishes the important result that Theorem 3.2 in Smith (1987) is valid for the case where a stochastic threshold, in this case , is used in conjunction with our nonstochastic .666Smith (1987, pp. 1180-1181) observes that the use of Theorem 3.2 normally involves taking either or as being stochastic and the other as being nonstochastic. Throughout this paper we take as nonstochastic and let thresholds be sample dependent (stochastic). The validity of Theorem 3.2 for stochastic thresholds was discussed in Smith (1987, pp. 1180-1181), but no formal proof was given.

Second, we show in the proof of Theorem 1 that the score functions associated with and are uniformly asymptotically equivalent in probability. This, in combination with Lemma 5 in Smith (1985), establishes the existence of and , and characterizes them as a local maximum for . Since establishing this equivalence involves the nonparametric residuals that appear in , additional assumptions are needed to ensure that the nonparametric estimators and converge uniformly in probability to and at suitable rates.

We adopt the following notation in our assumptions and proofs: a) will represent an inconsequential and arbitrary constant taking different values; b) denotes a compact subset of ; c) denotes the integer part of ; d) denotes the probability of event associated with a probability space or a probability measure, depending on the context; e) for any function whose order partial derivatives exist, we denote by the first order partial derivatives of with respect to its argument for and the -order partial derivatives are denoted by for . The gradient of the function is denoted by and its Hessian by ; f) the joint density of the vector of conditioning variables is denoted by . For a vector with components that are non-negative integers, we write and .

Assumption A1: is a product kernel with such that: 1) for all and ; 2) for ; 3) , for , ; 4) is continuously differentiable on with for all and ; 5) The kernel is symmetric and twice continuously differentiable in with , , , for , , , and .

The kernel is used to construct where for . Furthermore, for we have , for , and whenever or for some . The order for and is needed to establish that the biases for and are, respectively, of order for in Lemmas 3 and 4. The order for is necessary in the proof of Lemma 5. All other assumptions are common in the nonparametric estimation literature and are easily satisfied by a variety of commonly used kernels.

Assumption A2: 1) is a strictly stationary -mixing process with for some ; 2) and all of its partial derivatives of order s are differentiable and uniformly bounded on ; 3) .

A2 1) implies that for some and , , a fact that is needed in our proofs. We note that -mixing is the weakest of the mixing concepts (Doukhan (1994)) and its use here is only possible due to Lemma A.2 in Gao (2007), which plays a critical role in the proof of Lemma 5.

Assumption A3: 1) and all of its partial derivatives of order are differentiable on . The partial derivatives are uniformly bounded on ; 2) and all of its partial derivatives of order are differentiable and uniformly bounded on ; 3) for some .

The degree of smoothness of , and (in A2 and A3), the dimension and the mixing size are, as expected, tightly connected with the speed at which and converge (uniformly) to and . These parameters also interact in specific ways to determine the asymptotic behavior of and .

A3 3) and FR1 b) imply, by the -Inequality, that . Linton and Xiao (2013) and Hill (2015) have proposed nonparametric estimators for unconditional expected shortfall (ES) and studied their asymptotic behavior for fixed for cases where and . Our model is more restrictive regarding tail behavior than theirs, but in contrast we are able to study conditional VaR and ES when .

Assumption A4: 1) The joint density of , denoted by is continuous; 2) The joint density of , denoted by is continuous.

Assumption A4 is necessary in Lemma 5 and is directly related to the verification of the existence of bounds required to use Lemma A.2 in Gao (2007).

Assumption A5: , , , for some and .

The following Theorem 1 establishes the existence of and and characterizes them as a local maximum. It will be convenient to re-parametrize the likelihood functions and represent arbitrary values as , where , and as for with as . Note that these arbitrary values belong to a shrinking neighborhood ( as ) of the true values and . Hence, we write .

Theorem 1.

Assume FR1, FR2 and A1-A5. Let , , , as and denote arbitrary and by and , respectively. We define the log-likelihood function where , , and are as defined in section 2. Then, as (and consequently ), has, with probability approaching , a local maximum on at which and .

The vector implies values and which are solutions for the likelihood equations

Hence, there exists, with probability approaching 1, a local maximum on that satisfies the first order conditions in equation (8).

The proof of Theorem 1 (see online supplement) depends critically on two sets of results. First, since is unobserved and is estimated by , we must obtain convergence of both and to the true and uniformly in at suitable rates. This is addressed in Lemmas 3 and 4. Second, Lemma 5 shows that is asymptotically close to by satisfying . It is in this lemma that the stochasticity of the estimated threshold is explicitly handled and where the full set of restrictions in FR1 and FR2 on the class of functions to which belongs are needed. It is also in Lemma 5 that the stochasticity of , and the fact that it may differ from in finite samples, is handled by showing that .

We note that, as in Smith (1987), we require and . The restriction that is for convenience and places no stochastic constraint on our model, whereas is necessary to provide first order approximations for the expected value of the scores associated with the likelihood function (see, e.g., equation (12) below).

The influence of the dimension of the conditioning space manifests itself on the asymptotic results in a strong manner via the requirement that the degree of smoothness of the functions and be such that . We believe that alleviation of this strong requirement can only result from further constraints on the class of functions containing and .

3.2 Asymptotic normality of

The following theorem shows that, under suitable normalization, is asymptotically distributed as a bivariate normal random vector. The theorem has two parts. Part a) shows that carries a bias that does not decay to zero at the rate , a problem that is similar to that encountered in Theorem 3.2 in Smith (1987). Inspired by Peng (1998), who proposed a moments based bias corrected version of the traditional Hill (1975) estimator, we provide in part b) a bias corrected version of , which we denote by .

It will be useful to make two clarifying comments before stating Theorem 2. First, by Theorem 3.4.5 (b) in Embrechts et al. (1997) and Theorem 7 in Pickands (1975), is a function satisfying as . Hence, as in Smith (1987) we set, without loss of generality, . Second, since the only requirements on in FR2 are that it decays to zero and be regularly varying at infinity with , a full characterization of the limiting normal distribution of requires, as in Smith (1987), that have a limit. Given FR2 and the expectation of the scores associated with (see, e.g., equation (11)) we set

| (12) |

for some . As a limit, is unique for given , but since there exist many that satisfy FR2 for a given pair , there correspondingly exist many associated with such a pair. Thus, the bias we encounter due to approximating the upper right tail of by a GPD is, as a result of assumption FR2, a function of , and .

Theorem 2.

Assume FR1, FR2, A1-A5 and as defined in (12). Then, for we have

a) where

b) Let , , be a consistent estimator for and define

where , an estimator for . Then,

where with

and

Remark: Part b) of Theorem 2 calls for a consistent estimator of , which we now provide. For an arbitrary constant we let , and define

Lemma 9 shows that .

It is instructive to compare Theorem 2 to Theorem 3.2 in Smith (1987). There, he obtains

where and maximize . Part a) shows that the use of instead of to define the exceedances used in the estimation of the parameters of the GPD impacts the variance of the asymptotic distribution. It is easy to verify that is positive definite, implying a (expected) loss of efficiency that results from estimating nonparametrically. However, any additional bias introduced by the nonparametric estimation is of second order effect as the asymptotic bias derived in Smith (1987) is precisely the same as the one we obtain in part a) of Theorem 2. The presence of such bias manifests itself in other estimation procedures for that rely on Extreme Value Theory (Hill (1975); Pickands (1975)). Also, as in Peng (1998), bias correction may increase the variance of the asymptotic distribution. Hence, although our bias correction produces correctly centered asymptotic distributions, the cost may be an increase in the variance of the asymptotic distribution. In our Monte Carlo experiment, we compare the root mean squared error of the uncorrected and bias corrected estimators (see Table 1). There, it is seen that the benefits from bias correction are far larger than any cost associated with variance increase.

3.3 Asymptotic normality of , , -CVaR() and -CES()

The asymptotic distributions of the ML estimators given in parts a) and b) of Theorem 2 are the basis for obtaining the asymptotic distributions of and . First, in the case of , we rely on the asymptotic properties of and Theorem 2 parts a) and b). Second, since , its asymptotic distribution can be derived directly from the results for and . The estimators and inherit an asymptotic bias that derives from the result in part a) of Theorem 2. Hence, Theorems 3 and 4 include bias-corrected versions of the estimators we propose, which we denote by and . It is important to emphasize, as mentioned in section 2, that in Theorems 3, 4 and 5 both and approach 1 as with . We also note that we assume that with . In the extreme (regression) quantile literature this is called the “intermediate order” type asymptotics (Chernozhukov (2005, p. 809)) and in the extreme CVaR literature this is described as asymptotics for “high quantiles within the sample” (Embrechts et al. (1997, p. 349)).

Theorem 3.

Assume FR1, FR2, A1-A5 and as defined in (12). Then, for and for some , if we have

a) , where

b) Let , where and . Then, where , and

Remark: Under the assumption that , the constant is the limit of as . Thus, it captures the variation of the quantile associated with as we approach its endpoint, which in this case is infinity. Bias correction in part b) of the theorem requires a consistent estimator for .

Theorem 4.

Assume FR1, FR2, A1-A5 and as defined in (12). Then, for and for some , if we have

From Theorems 3 and 4 we obtain our main results, the asymptotic normality and consistency of and . Since these estimators also inherit an asymptotic bias, we present only results for estimators of -CVaR() and -CES() that are constructed using and , respectively. So we define, and , where , , , , are as defined in Theorem 2 and and are as defined in Theorem 3.

Theorem 5.

Assume FR1, FR2, A1-A5 and as defined in (12). Then, for and for some , if we have

a) , where is defined in Theorem 3.

As we have observed following Theorem 2, it is also the case that bias correction in Theorems 3, 4 and 5 has an impact on the variance of the asymptotic distribution of the estimators. The following corollary to Theorem 5 shows that the benefit of bias correction, in terms of asymptotic mean squared error, depends critically on the parameters and , and how they relate to the constants and , of which is not uniquely determined by .777Corollary 2.1 in Peng (1998, p.109) gives a similar result for a much simpler model. But even in his model, as in the case for the estimators in our Theorem 2, the benefits of bias reduction depend on the interplay of model parameters and his constant (playing the same role as our ), which varies with his (playing the same role as our ). See the discussion following our equation (12). The corollary is most useful for given , in which case the value of is fixed. This theoretical indeterminacy manifests itself in our simulations (see section 4). For example, when is a Student-t distribution with degrees of freedom, and (Ling and Peng (2015)), the benefit of bias reduction in the estimation of the parameters of the GPD seems quite clear. In contrast, bias reduction in the estimation and is not apparent, at least from the point of view of reduced root mean squared error. These simulation results suggest that satisfies threshold levels for reduced MSE under bias correction for the estimators in Theorem 2 but not for those in Theorem 5. Evidently, alternative data generating processes may produce different results.

Corollary 1.

Assume the conditions of Theorem 5 hold. Let denote the mean squared error of the estimator . Then,

where and

where

Theorem 5 provides the basis for inference regarding extreme CVaR() and CES(). The covariance matrices depend on , and which can be consistently estimated as described in Theorem 3 and Lemma 9. In section 4 we implement these estimators, construct confidence intervals and report on empirical coverage probabilities. As a direct consequence of Theorem 5 we have as , therefore establishing consistency of the estimators.

4 Monte Carlo study

We perform a Monte Carlo study to investigate the finite sample properties of the parameter estimator , the -CVaR() estimator , the -CES() estimator , as well as their bias-corrected versions given by , and . To simplify the notation, we put , , , and with corresponding true values given by and . The underlying values of and will be clear in context.

We generate data from the following location-scale model

| (13) |

We choose to be and consider for , where and . The quadratic type heteroskedasticity function was considered in Cai and Wang (2008), where we add the function to make the nonlinearity more prominent, and has been considered in Martins-Filho and Yao (2006). is set to be or .888We only report results for . All results for are available from the first author upon request. However, in the text we discuss the results for and highlight the differences when needed. Our estimators are based on a model where , but the model with and without the function corresponds to the popular GARCH model, and it would be interesting to investigate the performance of our estimators under this structure. Note also that is unbounded, therefore violating assumption A3. Initial values of and are set to be zero and is generated recursively according to equation (13). We discard the first observations so that the samples are not heavily influenced by the choice of initial values.

We generate independently from a Student-t distribution with degrees of freedom. It can be easily shown that , so we have for and for . We note that only the case where conforms to the assumptions needed to establish asymptotic normality of our estimators, but we consider the other case to investigate the behavior of the estimators when our asymptotic results may not hold. Here, the variance of is larger with and we expect that in this case estimation will be relatively more difficult. In contrast, when the Student-t distribution resembles the normal distribution. For identification purposes, we standardize so that it has unit variance.999We have also performed our study using the log-gamma distribution, a density that is also in the domain of attraction of the Fréchet distribution. Since its support is bounded from below, it is much less commonly used to model financial returns. Though the relative rankings regarding estimators’ performances change somewhat in specific experiment designs, we do not report these results to save space and focus on the more popular Student-t distribution and a more detailed exposition.

Implementation of our estimator requires the choice of bandwidths , and . Since and are utilized to estimate the conditional mean and variance, we select them using the rule-of-thumb data driven plug-in method of Ruppert et al. (1995) and denote them by and . Specifically, and are obtained from the following regressand and regressor sequences and , respectively. We select by using the rule-of-thumb bandwidth as in (2.52) of Pagan and Ullah (1999), where is the sample interquartile range of , and we set so that it satisfies our assumption on the bandwidth. The second order Epanechnikov kernel is used for our estimators.

In estimating the parameters, we consider our estimators , our bias-corrected estimators , Smith type estimators and Smith type bias-corrected estimators , where the bias correction is conducted as in . Both and utilize the true conditional mean , variance and available in the simulation. Without having to estimate and , we expect that Smith’s estimators ( and ) will perform best and serve as a benchmark to evaluate our estimators. In estimating the conditional value-at-risk () and expected shortfall (E), we include our estimators (, ), our bias-corrected estimators (, ), the Smith type estimators (), the Smith type bias-corrected estimators (), where the bias correction is performed as in (, ), and the estimators () proposed by Cai and Wang (2008). We follow their instructions for implementation and utilize the theoretical optimal bandwidths available in the simulation for () to minimize the noise.

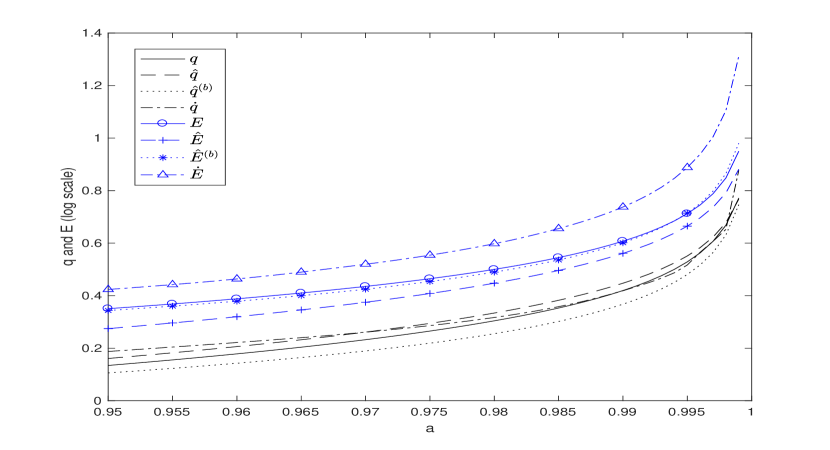

Figure 1 plots the true and estimated conditional value-at-risk and expected shortfall evaluated at the sample mean of for values of between and , since we are interested in higher order quantiles. The estimation utilizes sample data points generated from equation (13) with , and Student-t distributed with degrees of freedom. We use in constructing our estimates, where and gives the nearest integer. We note that all estimators are smooth functions of , and they seem to capture the shape of the true value-at-risk and expected shortfall well. It seems more difficult to estimate expected shortfall than value-at-risk as the gap between the estimates and the true value is noticeably larger for expected shortfall.

The performance of our estimators is fairly robust to our choice of in the simulations for and . In the expression for , we set so that we use less than of the total number of observations as tail observations in the second stage estimation, giving and , respectively. Thus, with being doubled, the effective sample size in the second stage of our estimation is less than doubled, as required by the assumption on . Each experiment is repeated times. We summarize the performance of all parameter estimators in terms of their bias (B), standard deviation (S) and root mean squared error (R) in Table 1 for .

We consider the performance of the conditional value-at-risk and expected shortfall estimators for and evaluated at , the most recent observation in the sample. Specifically, the performances in terms of the bias (B), standard deviation (S) and relative root mean squared error (R) for are detailed in Tables 2 and 3 for and , respectively. To facilitate comparison, we report the relative root mean squared error as the ratio of the root mean squared error of each estimator over that of the estimator with the smallest root mean squared error in each experiment design. To reduce the impact of extreme experiment runs, we truncate the smallest and largest estimates from the repetitions for all estimators. We give the empirical coverage probability for the bias-corrected estimators , , and in Table 4 for . As the results for are qualitatively similar, we only report detailed results for and .

To implement the bias-corrected estimators, we need the second order parameter , which is estimated by , where , are as defined in Theorem 2. Here and we choose for some positive constant . We let so that for the sample sizes and considered, and are less than . The moments based estimator is utilized to construct the bias-corrected parameter estimate , which is then used to construct and . We use the asymptotic distributions of and to construct confidence intervals, since they are asymptotically unbiased. Specifically, we estimate the confidence interval for the -CVaR() as , where is the quantile for the standard normal distribution. For the -CES(), its confidence interval estimates are , where is estimated by .

In the case of estimating parameters, we notice that both and overestimate , while the bias-corrected estimators and often underestimate . As the sample size increases, all estimators’ performance improves, in the sense that B, S and R decrease, with a few exceptions for B of and . This confirms the asymptotic results in the previous section. When is decreased (smaller in Table 1), we generally find that all estimators exhibit smaller B, larger S and smaller R, since the drop in B dominates the increase in S, with a few exceptions in the case of estimating . We think that this is related to the bias and variance trade-off for the parameter estimation. As mentioned above, the variance of without standardization is larger with smaller , and the distribution of exhibits heavier tail behavior, thus the more representative extreme observations have a larger probability to show up in a sample, which explains the lower bias. It is generally harder to estimate than when using and , as estimates of exhibit larger R. However, under this criterion, it is harder to estimate than , when using and . In terms of relative performance, we notice that and are much better than and , as they exhibit much lower B and R. Thus, the bias-corrected parameter estimators significantly reduce B without inflating S. When , , generally outperform , respectively, in terms of smaller B, S and R, though the difference diminishes with larger sample sizes. When , , frequently perform better than , respectively, especially in estimating . Again the difference is fairly small and diminishes with larger sample sizes. The results suggest that our proposed estimators and are well supported by the nonparametric kernel estimators for the functions and .

In the case of estimating conditional value-at-risk and expected shortfall, we observe that performances of all estimators generally improve with the sample sizes in terms of smaller B, S and R, with some exceptions for B. This confirms the consistency of our estimators for conditional value-at-risk and expected shortfall. In the case of estimating conditional value-at-risk, and carry positive bias for and , but exhibit negative bias for . is frequently positively biased, while and are negatively biased. In the case of estimating expected shortfall, all estimators are generally negatively biased. There is mixed evidence on the impact an increase in has on the S of , , and , especially for larger values. This is expected since the distribution of exhibits less heavy tails with larger . The performance of does not seem to depend on in a clear fashion. With a few exceptions on B, we notice that it is more difficult to estimate the conditional expected shortfall relative to the value-at-risk, judged by the larger B, S and R for all estimators across different experiment designs. It is also harder to estimate higher order conditional value-at-risk and expected shortfall, as demonstrated by the larger B, S and R for all estimators, with some exceptions for B.

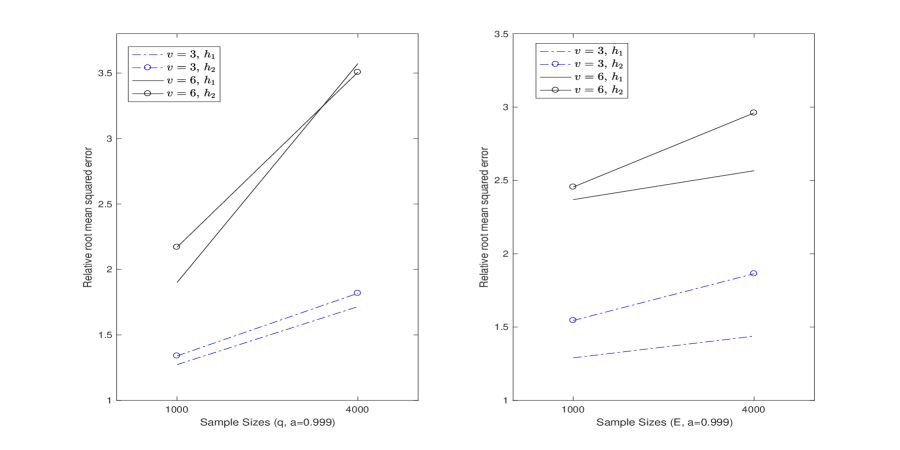

Across all experiment designs, the best estimator for in terms of R is and the best estimator for is either or , where the latter is often the best when sample sizes are large and . Thus, the root mean squared errors are constructed for the other estimators relative to or . For the estimation of the -CVaR(), we notice that the biases of (, ) do not seem to be smaller than those of (, ). As expected, S for and are smallest, followed by that of and , with exceptions when and , where the S for is smaller than that for . always carries the largest S. In terms of R, is the best estimator, followed in order by , , and , with exceptions for and . In these cases the performance of is better than that of . For the estimation of the -CES(), we notice that the bias-corrected estimators () exhibit smaller B than their counterparts (), though with a cost of larger . When , the best estimators in terms of R are either or , followed in order by , and . When , is the best estimator, followed by or , and then by . does not always carry the largest R, on occasions it performs better than . Thus, in terms of estimation performance, our proposed estimators and can offer finite sample improvement over . We notice that the improvement could be sizable when . To illustrate, we plot in Figure 2 the relative root mean squared error of and , and and across sample sizes and for and . We observe that the relative root mean squared errors are all greater than one. Furthermore, as the sample size increases, the relative root mean squared error generally becomes larger, illustrating that the finite sample improvement of over gets magnified with sample sizes. As is increased, the advantage of over is more prominent. For example, in the case of estimating , the relative root mean squared error of is over for , so the reduction in the root mean squared error of over is more than . In the case of estimating , the relative root mean squared error is over for , so the reduction in the root mean squared error of over is more than .

We conclude that our estimators have good finite sample performance and can be especially useful when estimating higher order conditional value-at-risk and expected shortfall. provide reasonable alternatives and their asymptotic distributions are bias free, which enable us to construct confidence intervals. The -empirical coverage probability (ECP) in Table 4 gives an indication of the performance of the confidence interval estimates. The ECP seems to improve when is decreased for all estimators at least when is considered. The ECP for the bias-corrected estimators is similar to that for , indicating that the estimation of and does not pose a significant challenge in constructing confidence intervals. The ECP for the -CES() seems to be closer to the target of . The ECP for the -CVaR() can be relatively far from the target for lower values of , but it gets much closer to the target when is larger.

The simulation results for the estimators do not change qualitatively across different values of , which suggests that accounting for the nonlinearity in the conditional mean and variance functions is important for estimating high order and . Overall, the study suggests that utilizing Extreme Value Theory and properly accounting for nonlinearities seems to pay off in finite samples.

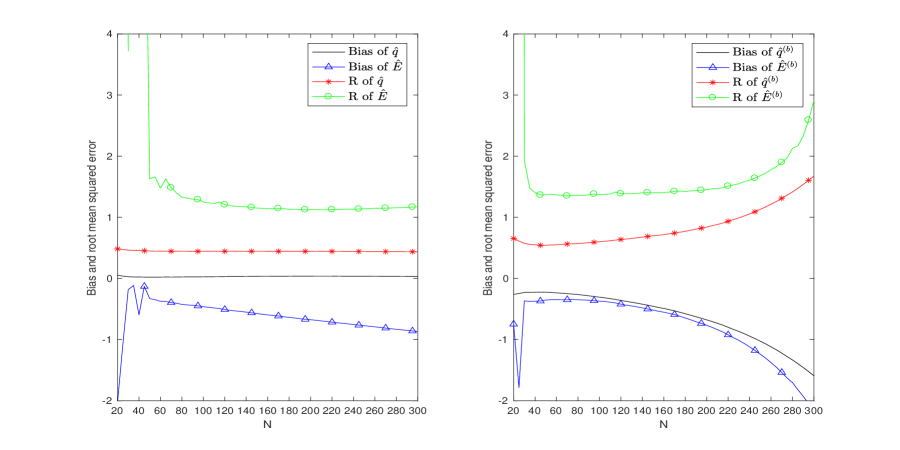

The choice of could be an important issue because the number of residuals exceeding the threshold is based on . We need to choose a large to reduce the bias from approximating the tail distribution with a GPD, but we need to keep large (or small) to control the variance of the estimates.101010Note that the number of exceedances over is asymptotically of the same order as , since (Lemma 5). We suggested earlier that our estimators are relatively robust to the choice of , and here we specifically illustrate the impact from different ’s on the performance of our estimators for the conditional value-at-risk and expected shortfall with a simulation. We set , , and use a Student-t distributed with . We graph the bias and root mean squared error of and against in the left panel of Figure 3, and plot those of and in the right panel. The other experiment designs give graphs of similar general pattern. We observe that carries a small positive bias and is generally negatively biased. As we have mentioned above, it is harder to estimate the conditional expected shortfall than the value-at-risk, judged by the larger bias and root mean squared error of . The performance of is fairly robust in the range of considered, with slight improvement when is greater than The bias of seems to be smallest when is between and , but its magnitude increases with smaller , and grows steadily with larger . The root mean squared error of decreases sharply from to and drops gradually until . It remains fairly stable for a wide range of and eventually increases slowly for greater than .

The performance of the bias-corrected estimators and could depend on the choice of in a delicate fashion, since it requires the estimation of the second order parameter . From our discussion above, the estimation of depends on a fine-tune parameter , which assures that for and , and are less than . We adopt the same estimate described above for all considered, so that we can focus attention on the impact of from the bias correction made other than the estimation of . We observe that and are generally negatively biased. Again, it is harder to estimate conditional expected shortfall than value-at-risk, judged by the larger B and R of . The B and R of are smallest for between and , beyond which they start to increase but remain fairly small until . Their performances start to deteriorate quickly for larger than . On the other hand, the bias of remains small for to , beyond which it starts to increase. The root mean squared error drops sharply from to , then it remains low for a wide range (), beyond which it starts to increase. Thus, we conclude that the performance of , , and is fairly robust in a wide range of values for . Relative to and , the choice of is more crucial for the bias-corrected estimators, especially for .

5 Empirical illustration with backtesting

We illustrate the empirical applicability of our estimators using five historical daily series on the following log returns of future prices (contracts expiring between 1 and 3 months): (1) Maize from August 10, 1998 to July 28, 2004. (2) Rice from August 1, 2002 to July 18, 2008. (3) Soybean from July 25, 2006 to July 6, 2012. (4) Soft wheat from August 15, 1996 to July 31, 2002. The data are obtained from the Chicago Board of Trade. We also obtain (5) Hard wheat from August 1, 1996 to July 18, 2002 from Kansas City Board of Trade.

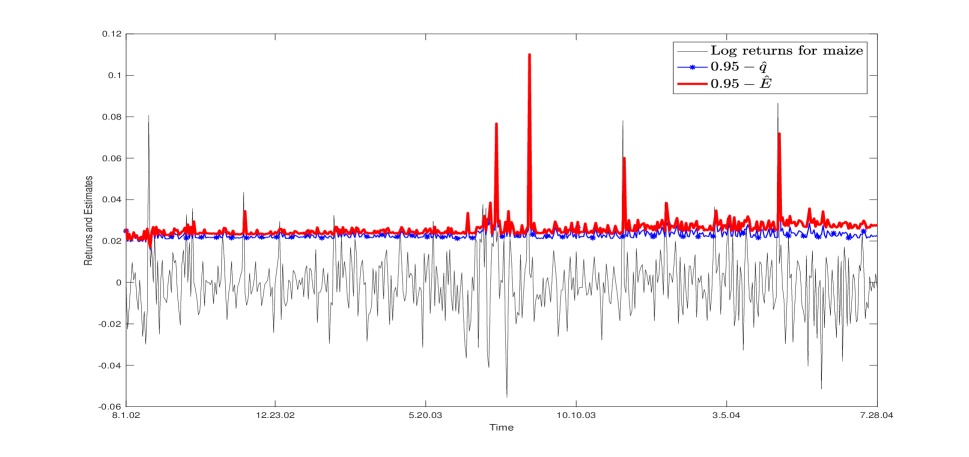

To backtest on a data set , we utilize the previous observations to estimate the -CVaR by and the -CES by for and , where , . We fix , , let and implement our estimators as in the simulation study. We provide in Figure 4 the plot of log returns of Maize futures prices against time together with the conditional value-at-risk and expected shortfall estimates. Clearly our estimates respond quickly to changing prices.

To backtest the -CVaR estimator, we define a violation as the event . Under the null hypothesis that the dynamics of are correctly specified, where is the indicator function. Consequently, . We perform a two sided test with the alternative hypothesis that the quantile is not correctly estimated with too many or too few violations. Since is not observed, we estimate it with and construct the empirical version of the test statistic as . Under the null hypothesis, the standardized test statistic is distributed asymptotically as a standard normal. We report the violation numbers together with the p-values based on the normal distribution for our estimator on the left part of Table 5. For all five daily series and across all values of considered, the actual number of violations is fairly close to the expected number, with large p-values indicating no rejection of the null hypothesis. The only relatively large deviation of the violation numbers from expected is for on Maize, but its p-value is still larger than .

If the dynamics of are correctly specified, the violation sequences are expected to be independent and have a correct conditional coverage. The above coverage test and the first-order Markov test proposed by Christoffersen (1998) on the independence of the violation sequences are shown to have relatively small power in Christoffersen and Pelletier (2004) and Christoffersen et al. (2009). The duration based likelihood ratio tests ( and ) proposed by Christoffersen and Pelletier (2004) have considerably better power in many cases. The tests are based on the duration of days between the violations of the value-at-risk. The first test statistic corresponds to the independence assumption under the null, and the durations have an exponential distribution (memory-free distribution) but with a rate parameter that can be different from , where denotes the value-at-risk coverage rate. The second test statistic corresponds to the conditional coverage assumption under the null, and the durations have an exponential distribution with a rate parameter equal to . We implement the two duration based tests111111We use the Matlab code by C. Hurlin available at http://www.runshare.org/CompanionSite/site.do?siteId=68. Note the p-value entries for and in Table 5 for Soybean are not available at since with only two violations, and one being at the end of the evaluation sample, the log-likelihood can not be evaluated numerically. constructed with our estimate and provide the corresponding p-values in the middle part of Table 5. With exceptions on Rice and Soybean for and , the p-values are reasonably large, indicating that the violations constructed with our estimate exhibit reasonable conditional coverage and independence.

To backtest the -CES we consider the normalized difference between and as . If the return dynamics are correctly specified, given that , is independent and identically distributed with mean zero. Since is not observed, we use the estimated residuals , where . Without making specific distributional assumptions on the residuals, we perform a one-sided bootstrap test as described in Efron and Tibshirani (1993, pp.224-227) to test the null hypothesis that the mean of the residuals is zero against the alternative that the mean is greater than zero, since underestimating conditional expected shortfall is likely to be the direction of interest. The p-values of the test for the five series across all values of are provided on the right part of Table 5. Given a significance level for the test, the null hypothesis for our -conditional expected shortfall estimator is not rejected for and for all series, but it is rejected for . The empirical results seem to confirm our Monte Carlo study, in that our estimators can be especially useful in estimating higher order conditional value-at-risk and expected shortfall.

6 Summary and conclusion

The estimation of conditional value-at-risk and conditional expected shortfall has been the subject of much interest in both empirical finance and theoretical econometrics. Perhaps the interest is driven by the usefulness of these measures for regulators, portfolio managers and other professionals interested in an effective and synthetic tool for measuring risk. Most stochastic models and estimators proposed for conditional value-at-risk and expected shortfall are hampered in their use by tight parametric specifications that most certainly impact performance and usability. In this paper we have proposed fully nonparametric estimators for value-at-risk and expected shortfall, showed their consistency and obtained their asymptotic distributions. Our Monte Carlo study has revealed that our estimators outperform those proposed by Cai and Wang (2008) indicating that the use of the approximations provided by Extreme Value Theory may indeed prove beneficial.

We see an important direction for future research related to the contribution in this paper. The fact that we require presents a strong requirement on the smoothness of the location and scale functions. This perverse manifestation of the curse of dimensionality requires a solution. Perhaps restricting and to belong to a class of additive functions, such that and may be sufficient to substantially relax the restriction that .

Appendix 1 - Figures and Tables

| B | S | R | B | S | R | B | S | R | B | S | R | |||

| 3 | 1 | .294 | .062 | .300 | .126 | .102 | .162 | .294 | .061 | .300 | .126 | .101 | .162 | |

| 3 | 1 | .320 | .084 | .331 | .127 | .107 | .166 | .274 | .073 | .283 | .133 | .110 | .173 | |

| 3 | 1 | -.019 | .059 | .062 | -.030 | .081 | .087 | -.019 | .060 | .063 | -.030 | .083 | .088 | |

| 3 | 1 | -.011 | .055 | .057 | -.028 | .088 | .092 | -.043 | .049 | .065 | -.024 | .095 | .098 | |

| 3 | 4 | .251 | .037 | .253 | .091 | .057 | .107 | .250 | .036 | .252 | .088 | .057 | .105 | |

| 3 | 4 | .266 | .052 | .271 | .087 | .061 | .106 | .211 | .048 | .217 | .085 | .069 | .109 | |

| 3 | 4 | .002 | .038 | .038 | -.035 | .041 | .054 | .004 | .038 | .039 | -.037 | .041 | .056 | |

| 3 | 4 | .010 | .034 | .035 | -.038 | .045 | .059 | -.030 | .032 | .044 | -.041 | .054 | .068 | |

| 6 | 1 | .466 | .073 | .472 | .161 | .097 | .188 | .464 | .068 | .469 | .161 | .093 | .186 | |

| 6 | 1 | .464 | .072 | .470 | .169 | .097 | .195 | .415 | .068 | .420 | .163 | .096 | .189 | |

| 6 | 1 | .025 | .058 | .063 | -.050 | .080 | .094 | .025 | .055 | .060 | -.051 | .076 | .092 | |

| 6 | 1 | .026 | .054 | .060 | -.043 | .081 | .091 | .009 | .049 | .049 | -.047 | .080 | .093 | |

| 6 | 4 | .407 | .038 | .409 | .124 | .052 | .134 | .408 | .038 | .409 | .124 | .051 | .134 | |

| 6 | 4 | .404 | .038 | .405 | .125 | .052 | .136 | .363 | .036 | .364 | .121 | .052 | .132 | |

| 6 | 4 | .051 | .034 | .061 | -.059 | .040 | .072 | .051 | .034 | .061 | -.059 | .039 | .070 | |

| 6 | 4 | .051 | .031 | .059 | -.058 | .040 | .070 | .033 | .029 | .043 | -.060 | .040 | .072 | |

| B | S | R | B | S | R | B | S | R | ||

| 1 | .008 | .067 | 1 | .018 | .219 | 1 | -.400 | 1.052 | 1 | |

| 1 | .024 | .132 | 1.991 | .043 | .321 | 1.472 | -.354 | 1.259 | 1.162 | |

| 1 | -.183 | .086 | 2.999 | -.499 | .336 | 2.732 | -1.043 | 1.482 | 1.610 | |

| 1 | -.183 | .143 | 3.446 | -.505 | .414 | 2.967 | -1.056 | 1.659 | 1.748 | |

| 1 | .036 | .296 | 4.428 | .148 | .578 | 2.710 | -.144 | 1.659 | 1.480 | |

| 4 | .002 | .035 | 1 | .030 | .110 | 1 | -.219 | .565 | 1 | |

| 4 | .013 | .089 | 2.581 | .064 | .195 | 1.800 | -.116 | .735 | 1.228 | |

| 4 | -.081 | .036 | 2.544 | -.277 | .160 | 2.810 | -.517 | .790 | 1.558 | |

| 4 | -.075 | .094 | 3.455 | -.261 | .244 | 3.136 | -.451 | .960 | 1.751 | |

| 4 | -.004 | .195 | 5.605 | .056 | .444 | 3.929 | .139 | 1.270 | 2.108 | |

| 1 | -.481 | .221 | 1.293 | -.636 | .616 | 1 | -1.705 | 2.188 | 1 | |

| 1 | -.467 | .290 | 1.342 | -.609 | .743 | 1.085 | -1.648 | 2.489 | 1.076 | |

| 1 | -.288 | .291 | 1 | -.590 | .870 | 1.187 | -.920 | 3.247 | 1.217 | |

| 1 | -.292 | .369 | 1.147 | -.601 | 1.003 | 1.320 | -.926 | 3.604 | 1.341 | |

| 1 | .088 | .484 | 1.200 | -.150 | 1.125 | 1.281 | -.902 | 3.744 | 1.388 | |

| 4 | -.428 | .134 | 2.348 | -.514 | .342 | 1.163 | -1.307 | 1.246 | 1.028 | |

| 4 | -.406 | .202 | 2.375 | -.455 | .458 | 1.217 | -1.137 | 1.510 | 1.076 | |

| 4 | -.135 | .135 | 1 | -.290 | .444 | 1 | -.276 | 1.735 | 1 | |

| 4 | -.116 | .209 | 1.249 | -.246 | .565 | 1.162 | .127 | 2.039 | 1.163 | |

| 4 | .089 | .368 | 1.982 | -.088 | .793 | 1.504 | -.564 | 2.658 | 1.547 | |

| B | S | R | B | S | R | B | S | R | ||

| 1 | .004 | .035 | 1 | .009 | .112 | 1 | -.211 | .553 | 1 | |

| 1 | .007 | .160 | 4.500 | .018 | .338 | 3.020 | -.203 | .995 | 1.717 | |

| 1 | -.106 | .060 | 3.448 | -.282 | .208 | 3.124 | -.587 | .817 | 1.701 | |

| 1 | -.111 | .177 | 5.898 | -.298 | .398 | 4.431 | -.649 | 1.169 | 2.260 | |

| 1 | .021 | .285 | 8.062 | .238 | .586 | 5.639 | .183 | 1.348 | 2.301 | |

| 4 | .001 | .018 | 1 | .018 | .058 | 1 | -.092 | .300 | 1 | |

| 4 | .003 | .143 | 7.976 | .042 | .279 | 4.649 | -.017 | .725 | 2.308 | |

| 4 | -.050 | .025 | 3.118 | -.156 | .100 | 3.056 | -.275 | .428 | 1.619 | |

| 4 | -.048 | .150 | 8.783 | -.144 | .309 | 5.615 | -.238 | .808 | 2.680 | |

| 4 | -.003 | .198 | 11.013 | .216 | .516 | 9.217 | .501 | 1.220 | 4.197 | |

| 1 | -.252 | .146 | 1.234 | -.333 | .343 | 1 | -.896 | 1.190 | 1 | |

| 1 | -.258 | .320 | 1.744 | -.337 | .647 | 1.526 | -.900 | 1.811 | 1.357 | |

| 1 | -.167 | .166 | 1 | -.340 | .480 | 1.231 | -.542 | 1.731 | 1.217 | |

| 1 | -.177 | .338 | 1.619 | -.371 | .744 | 1.739 | -.635 | 2.268 | 1.580 | |

| 1 | -.084 | .358 | 1.559 | -.754 | .657 | 2.091 | -1.914 | 2.469 | 2.097 | |

| 4 | -.216 | .099 | 2.181 | -.251 | .196 | 1.096 | -.625 | .687 | 1 | |

| 4 | -.215 | .274 | 3.203 | -.221 | .501 | 1.884 | -.516 | 1.274 | 1.479 | |

| 4 | -.078 | .076 | 1 | -.162 | .241 | 1 | -.139 | .919 | 1.001 | |

| 4 | -.064 | .257 | 2.435 | -.129 | .520 | 1.842 | -.037 | 1.439 | 1.549 | |

| 4 | -.062 | .315 | 2.946 | -.654 | .559 | 2.959 | -1.825 | 1.799 | 2.758 | |

| B | S | R | B | S | R | B | S | R | ||

| 1 | .007 | .063 | 1 | .024 | .144 | 1 | -.167 | .497 | 1 | |

| 1 | .007 | .111 | 1.738 | .004 | .199 | 1.364 | -.241 | .543 | 1.134 | |

| 1 | -.322 | .115 | 5.364 | -.731 | .304 | 5.426 | -1.209 | .842 | 2.811 | |

| 1 | -.324 | .154 | 5.629 | -.743 | .337 | 5.597 | -1.254 | .855 | 2.895 | |

| 1 | .099 | .417 | 6.716 | .363 | .695 | 5.376 | .320 | 1.083 | 2.154 | |

| 4 | -.003 | .032 | 1 | .026 | .072 | 1 | -.073 | .257 | 1 | |

| 4 | -.004 | .069 | 2.167 | .018 | .118 | 1.543 | -.100 | .306 | 1.208 | |

| 4 | -.167 | .049 | 5.430 | -.469 | .152 | 6.401 | -.745 | .453 | 3.269 | |

| 4 | -.168 | .089 | 5.913 | -.473 | .194 | 6.634 | -.757 | .489 | 3.380 | |

| 4 | .074 | .364 | 11.580 | .327 | .658 | 9.535 | .549 | 1.011 | 4.314 | |

| 1 | -.586 | .158 | 1.227 | -.643 | .331 | 1 | -1.035 | .841 | 1 | |

| 1 | -.601 | .210 | 1.288 | -.688 | .381 | 1.087 | -1.147 | .876 | 1.082 | |

| 1 | -.527 | .255 | 1.184 | -.885 | .558 | 1.446 | -1.227 | 1.394 | 1.393 | |

| 1 | -.546 | .289 | 1.249 | -.922 | .582 | 1.507 | -1.321 | 1.382 | 1.434 | |

| 1 | .002 | .494 | 1 | -.540 | 1.061 | 1.647 | -1.218 | 3.194 | 2.563 | |

| 4 | -.543 | .114 | 1.643 | -.561 | .191 | 1 | -.830 | .477 | 1 | |

| 4 | -.548 | .160 | 1.692 | -.577 | .247 | 1.059 | -.867 | .535 | 1.065 | |

| 4 | -.313 | .126 | 1 | -.558 | .294 | 1.064 | -.673 | .764 | 1.063 | |

| 4 | -.320 | .163 | 1.063 | -.569 | .330 | 1.110 | -.699 | .794 | 1.105 | |

| 4 | .030 | .380 | 1.128 | -.418 | .937 | 1.729 | -1.162 | 2.343 | 2.731 | |

| B | S | R | B | S | R | B | S | R | ||

| 1 | .002 | .038 | 1 | .010 | .088 | 1 | -.112 | .296 | 1 | |

| 1 | -.014 | .147 | 3.822 | -.014 | .244 | 2.768 | -.146 | .507 | 1.665 | |

| 1 | -.201 | .093 | 5.741 | -.450 | .232 | 5.731 | -.747 | .551 | 2.929 | |

| 1 | -.213 | .191 | 7.433 | -.467 | .359 | 6.665 | -.772 | .718 | 3.327 | |

| 1 | .066 | .352 | 9.294 | .398 | .614 | 8.282 | .574 | .991 | 3.614 | |

| 4 | -.002 | .019 | 1 | .015 | .044 | 1 | -.045 | .154 | 1 | |

| 4 | -.017 | .117 | 6.239 | -.000 | .183 | 3.957 | -.055 | .345 | 2.171 | |

| 4 | -.107 | .044 | 6.103 | -.290 | .127 | 6.835 | -.457 | .294 | 3.381 | |

| 4 | -.115 | .139 | 9.555 | -.296 | .257 | 8.480 | -.459 | .472 | 4.098 | |

| 4 | .065 | .292 | 15.803 | .418 | .586 | 15.551 | .784 | .939 | 7.610 | |

| 1 | -.352 | .152 | 1.022 | -.389 | .240 | 1 | -.633 | .548 | 1 | |

| 1 | -.374 | .280 | 1.243 | -.419 | .420 | 1.298 | -.675 | .785 | 1.236 | |

| 1 | -.327 | .185 | 1 | -.549 | .374 | 1.454 | -.774 | .852 | 1.375 | |

| 1 | -.346 | .300 | 1.220 | -.572 | .516 | 1.685 | -.806 | 1.032 | 1.564 | |

| 1 | -.291 | .467 | 1.464 | -.846 | .756 | 2.481 | -1.839 | 1.752 | 3.034 | |

| 4 | -.323 | .125 | 1.592 | -.333 | .156 | 1 | -.492 | .322 | 1 | |

| 4 | -.337 | .236 | 1.892 | -.347 | .323 | 1.290 | -.498 | .551 | 1.263 | |

| 4 | -.196 | .095 | 1 | -.347 | .199 | 1.088 | -.425 | .449 | 1.051 | |

| 4 | -.206 | .210 | 1.354 | -.352 | .347 | 1.345 | -.417 | .639 | 1.297 | |

| 4 | -.232 | .425 | 2.228 | -.718 | .669 | 2.672 | -1.565 | 1.544 | 3.738 | |

| .439 | .849 | .986 | .210 | .850 | .999 | ||

| .438 | .811 | .963 | .255 | .860 | .995 | ||

| .413 | .593 | .979 | .030 | .138 | .999 | ||

| .391 | .582 | .935 | .096 | .159 | .991 | ||

| .995 | .996 | 1 | .999 | 1 | 1 | ||

| .962 | .981 | .967 | .987 | .997 | .998 | ||

| .995 | .999 | 1 | .997 | 1 | 1 | ||

| .955 | .966 | .964 | .984 | .997 | .999 | ||

| .395 | .829 | .989 | .179 | .847 | .999 | ||

| .383 | .682 | .933 | .371 | .801 | .989 | ||

| .304 | .538 | .973 | .017 | .102 | 1 | ||

| .149 | .397 | .776 | .155 | .359 | .966 | ||

| .999 | .996 | .999 | 1 | 1 | 1 | ||

| .920 | .949 | .942 | .988 | .995 | .991 | ||

| .999 | .998 | 1 | 1 | 1 | 1 | ||

| .761 | .852 | .905 | .964 | .988 | .992 | ||

| Expected violations | Duration based tests | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Maize | 18 (.151) | 5(1) | 2(.751) | .176 | .096 | .173 | .356 | .619 | .494 | 0 | .161 | .735 |

| Rice | 29(.412) | 4(.653) | 2(.751) | .052 | .126 | .040 | .076 | .018 | .033 | 0 | .081 | .248 |

| Soybean | 21(.412) | 3(.369) | 2(.751) | .199 | .259 | .012 | .014 | - | - | 0 | .302 | .244 |

| Soft Wheat | 30(.305) | 6(.653) | 2(.751) | .839 | .717 | .283 | .562 | .712 | .523 | .001 | .339 | .273 |

| Hard Wheat | 25(1) | 5(1) | 2(.751) | .294 | .566 | .055 | .142 | .739 | .529 | 0 | .082 | .239 |

Appendix 2 - Proofs

We rely, throughout the proofs, on results from Smith (1985) and Smith (1987). For a nonstochastic positive sequence as and , we have , , , and , where all expectations are taken with respect to the unknown distribution . Evidently, these approximations are based on a sequence of thresholds that approach the end point of the distribution as .

Theorem 2. Proof..

a) Let , and note that

| (14) |

For some let , ,

where , , , are as defined in Theorem 1. By a Taylor’s expansion of the first order condition in (14) around we have

| (15) |

We start by investigating the asymptotic properties of . Let , and observe that from Theorem 1, Lemma 5 and the fact that we have

By Lemma 6 and the fact that

where for . Hence, by letting and we have

| (17) |

Note that we can write

Also, from Lemma 5, is distributed asymptotically as where and for arbitrary . It can be easily verified that . In addition, , where the last equality follows from the results listed in section 3.1. Using similar arguments we obtain and from Lemma 5 we have that . We now define the vector and for arbitrary we consider . From above, we have that and . First, we consider which can be written as where . Since and we have that since . Now, from Smith (1987) we have that , and from Lemma 7 we have that Combined with the orders obtained for the other components of the expectation give . We now turn to which can be written as where . We note that

from Lemma 5, and since is asymptotically equivalent to , the second term in the covariance expression is of order . We now turn to , the first term in the covariance expression. Since is asymptotically equivalent to , we have by the Cauchy-Schwartz inequality

Hence, . In a similar manner we obtain . Hence, , where

.

By Liapounov’s CLT provided that . To verify this condition, it suffices to show that:

.

was verified in Lemma 5, so we focus on and . For , note that provided , which is easily verified by noting that

Lastly,

provided given the bound we obtained in case . By FR1 a) and integrating by parts we have

Three repeated applications of L’Hôpital’s rule and Proposition 1.15 in Resnick (1987) give . For we have that given FR 1 a) and again integrating by parts and letting

It is easy to verify that and consequently which verifies . By the Cramer-Wold theorem we have that . Consequently, for any vector we have where . Again, by the Cramer-Wold theorem . Hence, given equation (15), provided that we have

To see that , first observe that whenever we have and consequently . In addition, from Theorem 1 and the results from Smith (1987) we have uniformly on . By Theorem 21.6 in Davidson (1994) we conclude that .

b) Let and note that using (15) we can write

Since , and , we have

where . In addition, using the arguments in the proof of part a) we have

where , and . As a consequence, we obtain

| (18) |

We rewrite (17) as where and . Since, and we have,

| (21) | |||

| (24) |

Note that , , from part a). We put , and observe that,

where the second equalities in both expressions follow from the fact that , and thus . Using arguments similar to those in part a) of the proof we obtain, , , , , , , , and .

Now, integrating by parts . Consequently, and . Consequently, by Liapounov’s CLT and the Cramer-Wold device we have

since . ∎

Theorem 3. Proof..

a) Let , and write . By assumption , where is an arbitrary constant satisfying , which we set at for . Then, if for , by FR2 . Consequently, as . Now, we write

By Theorem 2 and the fact that we have

| (25) |

Let , and since , we have . By the MVT, there exists such that

Since , and by the MVT, Theorem 2 and Lemma 5, we have

| (30) |

Letting for , we have by FR2, Theorem 2, the MVT and the fact that ,

| (31) |

Using equations (25), (30) and (31) we write,

where . From the proof of Lemma 5 we have that

In addition, from the proof of Theorem 2 (adopting its notation) we have that

where . Hence, letting we can write where . Since and we have that . Hence, given the structure of , we conclude , where and .

b) Since , and , we have . From equation (Theorem 2. Proof..) we can write Using the MVT as in part a) we have

| (32) |

Also, from part a), substituting by in equation (25) we have

| (33) |

Now, since , by the MVT

| (34) |

By equations (32) and (34), and since we have

| (35) |

and consequently we have . Now, we write

Using equations (30), (33) and (35) we have

Given equation (24) and the fact that we have, using the notation in Theorem 2, that for , where and

Since from part b) of Theorem 2, the proof is complete. ∎

Theorem 4. Proof..

Theorem 5. Proof..

a) Since , we write

From Lemma 3, the fact that as and assumption A3 2), we have . Given A5 and we have . By Corollary 1 (in the online supplement), A5 and the fact that is bounded for fixed we have . From part b) of Theorem 3 we have , which gives . Lastly, since as , for fixed we have and by part a) of Theorem 3 .

b) We write

As in part a), since as , given Lemma 3 and A5 and , . Similarly, and . Now, consider

By Lemma 8, and by part b) of Theorem 4, , which is asymptotically . Hence . We note that if , , and are as defined in Theorem 2, then . Since, we write . Given that we have that

Furthermore, as in Theorem 3, with and . Since, is regularly varying with index , as , hence . Consequently,

Thus, letting we have

∎

References

- Azzalini (1981) Azzalini, A., 1981. A note on the estimation of a distribution function and quantiles by a kernel method. Biometrika 68, 326–328.

- Bowman et al. (1998) Bowman, A., Hall, P., Prvan, T., 1998. Bandwidth selection for the smoothing of distribution functions. Biometrika, 799–808.

- Cai (2002) Cai, Z., 2002. Regression quantiles for time series. Econometric Theory 18, 169–192.

- Cai and Wang (2008) Cai, Z., Wang, X., 2008. Nonparametric estimation of conditional VaR and expected shortfall. Journal of Econometrics 147, 120–130.

- Chen (2008) Chen, S. X., 2008. Nonparametric estimation of expected shortfall. Journal of Financial Econometrics 6, 87–107.

- Chen and Tang (2005) Chen, S. X., Tang, C., 2005. Nonparametric inference of value at risk for dependent financial returns. Journal of Financial Econometrics 3, 227–255.

- Chernozhukov (2005) Chernozhukov, V., 2005. Extremal quantile regression. The Annals of Statistics 33, 806–839.

- Chernozhukov and Umantsev (2001) Chernozhukov, V., Umantsev, L., 2001. Conditional Value-at-Risk: aspects of modelling and estimation. Empirical Economics 26, 271–292.

- Christoffersen (1998) Christoffersen, P., 1998. Evaluating internal forecasts. International Economic Review 39, 841–862.

- Christoffersen et al. (2009) Christoffersen, P., Berkowitz, J., Pelletier, D., 2009. Evaluating value-at-risk models with desk level data. Tech. Rep. 2009-35, CREATES.

- Christoffersen and Pelletier (2004) Christoffersen, P., Pelletier, D., 2004. Backtesting Value-at-Risk: A Duration-Based Approach. Journal of Financial Econometrics 2, 84–108.

- Cosma et al. (2007) Cosma, A., Scaillet, O., von Sachs, R., 2007. Multivariate wavelet-based shape preserving estimation for dependent observations. Bernoulli 13, 301–329.

- Danielsson (2011) Danielsson, J., 2011. Financial risk forecasting. John Wiley and Sons, New York, NY.

- Davidson (1994) Davidson, J., 1994. Stochastic limit theory. Oxford University Press, New York.

- Doukhan (1994) Doukhan, P., 1994. Mixing: properties and examples. Springer-Verlag, New York.

- Drost and Nijman (1993) Drost, F. C., Nijman, T. E., 1993. Temporal aggregation of GARCH processes. Econometrica 61, 909–927.

- Duffie and Singleton (2003) Duffie, D., Singleton, K., 2003. Credit risk: pricing, measurement and management. Princeton University Press, Princeton, NJ.

- Embrechts et al. (1997) Embrechts, P., Kluppelberg, C., Mikosh, T., 1997. Modelling extremal events for insurance and finance. Springer Verlag, Berlin.

- Escanciano (2009) Escanciano, J. C., 2009. Quasi-Maximum Likelihood Estimation of Semi-Strong Garch Models. Econometric Theory 25, 561–570.

- Falk (1985) Falk, M., 1985. Asymptotic normality of the kernel quantile estimator. Annals of Statistics 13, 428–433.

- Fan and Yao (1998) Fan, J., Yao, Q., 1998. Efficient estimation of conditional variance functions in stochastic regression. Biometrika 85, 645–660.

- Gao (2007) Gao, J., 2007. Nonlinear time series: nonparametric and parametric methods. Chapman and Hall, New York.

- Gnedenko (1943) Gnedenko, B. V., 1943. Sur la distribution limite du terme d’une série aléatoire. Annals of Mathematics 44, 423–453.

- Goldie and Smith (1987) Goldie, C. M., Smith, R. L., 1987. Slow variation with remainder: a survey of the theory and its applications. Quarterly Journal of Mathematics 38, 45–71.

- Hall (1982) Hall, P., 1982. On some simple estimates of an exponent of regular variation. Journal of Royal Satistical Society Series B 44, 37–42.

- Härdle and Tsybakov (1997) Härdle, W., Tsybakov, A. B., 1997. Local polynomial estimators of the volatility function in nonparametric autoregression. Journal of Econometrics 81, 233–242.

- Hill (1975) Hill, B. M., 1975. A simple general approach to inference about the tail of a distribution. Annals of Statistics 3, 1163–1174.

- Hill (2015) Hill, J. B., 2015. Expected shortfall estimation and Gaussian inference for infinite variance time series. Journal of Financial Econometrics 13, 1–44.

- Kato (2012) Kato, K., 2012. Weighted Nadaraya-Watson estimation of conditional expected shortfall. Journal of Financial Econometrics 10, 265–291.

- Leadbetter et al. (1983) Leadbetter, M., Lindgren, G., Rootzen, H., 1983. Extremes and related properties of random sequences and processes. Springer Verlag, New York.

- Ling and Peng (2015) Ling, C., Peng, Z., 2015. Approximations of Weyl fractional-order integrals with insurance applications. http://arxiv.org/find/grp_physics/1/au:+Ling_Chengxiu/0/1/0/all/0/1, ArXiv.

- Linton et al. (2010) Linton, O. B., Pan, J., Wang, H., 2010. Estimation on nonstationary semi-strong GARCH(1,1) model with heavy-tailed errors. Econometric Theory 26, 1–28.

- Linton and Xiao (2013) Linton, O. B., Xiao, Z., 2013. Estimation of and inference about the expected shortfall for time series with infinite variance. Econometric Theory 29, 771–807.

- Martins-Filho and Yao (2006) Martins-Filho, C., Yao, F., 2006. Estimation of value-at-risk and expected shortfall based on nonlinear models of return dynamics and extreme value theory. Studies in Nonlinear Dynamics & Econometrics 10, Article 4.

- Martins-Filho and Yao (2008) Martins-Filho, C., Yao, F., 2008. A smoothed conditional quantile frontier estimator. Journal of Econometrics 143, 317–333.

- Martins-Filho et al. (2015) Martins-Filho, C., Yao, F., Torero, M., 2015. High order conditional quantile estimation based on nonparametric models of regression. Econometric Reviews 34, 906–957.

- Masry and Fan (1997) Masry, E., Fan, J., 1997. Local polynomial estimation of regression functions for mixing processes. Scandinavian Journal of Statistics 24, 1965–1979.

- Masry and Tjøstheim (1995) Masry, E., Tjøstheim, D., 1995. Nonparametric estimation and identification of nonlinear ARCH time series: strong convergence and asymptotic normality. Econometric Theory 11, 258–289.

- McNeil and Frey (2000) McNeil, A., Frey, B., 2000. Estimation of tail-related risk measures for heteroscedastic financial time series: an extreme value approach. Journal of Empirical Finance 7, 271–300.

- McNeil et al. (2005) McNeil, A. J., Frey, B., Embrechts, P., 2005. Quantitative risk management: concepts, techniques and tools. Princeton University Press, Princeton, NJ.

- Pagan and Ullah (1999) Pagan, A., Ullah, A., 1999. Nonparametric econometrics. Cambridge University Press, Cambridge, UK.

- Peng (1998) Peng, L., 1998. Asymptotically unbiased estimators for the extreme-value index. Statistics and Probability Letters 38, 107–115.

- Pickands (1975) Pickands, J., 1975. Statistical inference using extreme order statistics. Annals of Statistics 3, 119–131.

- Resnick (1987) Resnick, S. I., 1987. Extreme values, regular variation and point processes. Springer Verlag, New York.

- Ruppert et al. (1995) Ruppert, D., Sheather, S., Wand, M. P., 1995. An effective bandwidth selector for local least squares regression. Journal of the American Statistical Association 90, 1257–1270.

- Scaillet (2004) Scaillet, O., 2004. Nonparametric estimation and sensitivity analysis of expected shortfall. Mathematical Finance 14, 115–129.

- Scaillet (2005) Scaillet, O., 2005. Nonparametric estimation of conditional expected shortfall. Revue Assurances et Gestion des Risques/Insurance and Risk Management Journal 72, 639–660.

- Smith (1985) Smith, R. L., 1985. Maximum likelihood estimation in a class of nonregular cases. Biometrika 72, 67–90.

- Smith (1987) Smith, R. L., 1987. Estimating tails of probability distributions. Annals of Statistics 15, 1174–1207.

- Tsay (2010) Tsay, R., 2010. Analysis of Financial Time Series, 3rd Edition. Wiley.

- Yang (1985) Yang, S.-S., 1985. A Smooth nonparametric estimator of a quantile function. Journal of the American Satistical Association 80, 1004–1011.

- Yu and Jones (1998) Yu, K., Jones, M. C., 1998. Local linear quantile regression. Journal of the American Statistical Association 93, 228–237.