About tests of the “simplifying” assumption for conditional copulas

Abstract

We discuss the so-called “simplifying assumption” of conditional copulas in a general framework. We introduce several tests of the latter assumption for non- and semiparametric copula models. Some related test procedures based on conditioning subsets instead of point-wise events are proposed. The limiting distribution of such test statistics under the null are approximated by several bootstrap schemes, most of them being new. We prove the validity of a particular semiparametric bootstrap scheme. Some simulations illustrate the relevance of our results.

Keywords: conditional copula, simplifying assumption, bootstrap.

MCS: 62G05, 62G08, 62G09.

1 Introduction

In statistical modelling and applied science more generally, it is very common to distinguish two subsets of variables: a random vector of interest (also called explained/exogenous variables) and a vector of covariates (explanatory/endogenous variables). The objective is to predict the law of the former vector given the latter vector belongs to some subset, possibly a singleton. This basic idea constitutes the first step towards forecasting some important statistical sub-products as conditional means, quantiles, volatilities, etc. Formally, consider a -dimensional random vector . We are faced with two random sub-vectors and , s.t. , , , and our models of interest specify the conditional law of knowing or knowing for some subset . We use the standard notations for vectors: for any set of indices , means the -dimensional vector whose arguments are the , . For convenience and without a loss of generality, we will set and .

Besides, the problem of dependence among the components of -dimensional random vectors has been extensively studied in the academic literature and among practitioners in a lot of different fields. The raise of copulas for more than twenty years illustrates the need of flexible and realistic multivariate models and tools. When covariates are present and with our notations, the challenge is to study the dependence among the components of given . Logically, the concept of conditional copulas has emerged. First introduced for pointwise (atomic) conditioning events by Patton (2006a, 2006b), the definition has been generalized in Fermanian and Wegkamp (2012) for arbitrary measurable conditioning subsets. In this paper, we rely on the following definition: for any borel subset , a conditional copula of given is denoted by . This is the cdf of the random vector given . Here, denotes the conditional law of knowing , . The latter conditional distributions will be assumed continuous in this paper, implying the existence and uniqueness of (Sklar’s theorem). In other words, for any ,

Note that the influence of on is twofold: when changes, the conditioning event changes, but the conditioned random vector changes too.

In particular, when the conditioning events are reduced to singletons, we get that the conditional copula of knowing is a cdf on s.t., for every ,

With generalized inverse functions, an equivalent definition of a conditional copula is as follows:

for every and , setting .

Most often, the dependence of w.r.t. to is a source of significant complexities, in terms of model specification and inference. Therefore, most authors assume that the following “simplifying assumption” is fulfilled.

Simplifying assumption : the conditional copula does not depend on , i.e., for every , the function is a constant function (that depends on ).

Under the simplifying assumption, we will set . The latter identity means that the dependence on across the components of is passing only through their conditional margins. Note that is different from the usual copula of : is always the cdf of the vector whereas, under , is the cdf of the vector (see Proposition 4 below). Note that the latter copula is identical to the partial copula introduced by Bergsma (2011), and recently studied by Gijbels et al. (2015b), Spanhel and Kurz (2015) in particular. Such a partial copula can always be defined (whether is satisfied or not) as the cdf of , and it satisfies an interesting “averaging” property: .

Remark 1.

The simplifying assumption does not imply that is , the usual copula of . This can be checked with a simple example: let be a trivariate random vector s.t., given , and . Moreover, and are independent given . The latter variable may be , to fix the ideas. Obviously, with our notations, , , and . Therefore, for any couple and any real number , and does not depend on . Assumption is then satisfied. But the copula of is not the independence copula, simply because and are not independent.

Basically, it is far from obvious to specify and estimate relevant conditional copula models in practice, especially when the conditioning and/or conditioned variables are numerous. The simplifying assumption is particularly relevant with vine models (Aas et al. 2009, among others). Indeed, to build vines from a -dimensional random vector , it is necessary to consider sequences of conditional bivariate copulas , where is a couple of indices in , , , and is a node of the vine. In other words, a bivariate conditional copula is needed at every node of any vine, and the sizes of the conditioning subsets of variables are increasing along the vine. Without additional assumptions, the modelling task becomes rapidly very cumbersome (inference and estimation by maximum likelihood). Therefore, most authors adopt the simplifying assumption at every node of the vine. Note that the curse of dimensionality still apparently remains because conditional marginal cdfs are invoked with different subsets of increasing sizes. But this curse can be avoided by calling recursively the non-parametric copulas that have been estimated before (see Nagler and Czado, 2015).

Nonetheless, the simplifying assumption has appeared to be rather restrictive, even if it may be seen as acceptable for practical reasons and in particular situations. The debate between pro and cons of the simplifying assumption is still largely open, particularly when it is called in some vine models. On one side, Hobæk-Haff et al. (2010) affirm that this simplifying assumption is not only required for fast, flexible, and robust inference, but that it provides “a rather good approximation, even when the simplifying assumption is far from being fulfilled by the actual model”. On the other side, Acar et al. (2012) maintain that “this view is too optimistic”. They propose a visual test of when and in a parametric framework. Their technique was based on local linear approximations and sequential likelihood maximizations. They illustrate the limitations of by simulation and through real datasets. They note that “an uncritical use of the simplifying assumption may be misleading”. Nonetheless, they do not provide formal test procedures. Beside, Acar et al. (2013) have proposed a formal likelihood test of the simplifying assumption but when the conditional marginal distributions are known, a rather restrictive situation. Some authors have exhibited classes of parametric distributions for which is satisfied: see Hobæk-Haff et al. (2010), significantly extended by Stöber et al. (2013). Nonetheless, such families are rather strongly constrained. Therefore, these two papers propose to approximate some conditional copula models by others for which the simplifying assumption is true. This idea has been developed in Spanhel and Kurz (2015) in a vine framework, because they recognize that “it is very unlikely that the unknown data generating process satisfies the simplifying assumption in a strict mathematical sense.”

Therefore, there is a need for formal universal tests of the simplifying assumption. It is likely that the latter assumption is acceptable in some circumstances, whereas it is too rough in others. This means, for given subsets of indices and , we would like to test

against that opposite assumption. Hereafter, we will propose several test statistics of , possibly assuming that the conditional copula belongs to some parametric family.

Note that several papers have already proposed estimators of conditional copula. Veraverbeke et al. (2011), Gijbels et al. (2011) and Fermanian and Wegkamp (2012) have studied some nonparametric kernel based estimators. Craiu and Sabeti (2012), Sabeti, Wei and Craiu (2014) studied bayesian additive models of conditional copulas. Recently, Schellhase and Spanhel (2016) invoke B-splines to manage vectors of conditioning variables. In a semiparametric framework, i.e. assuming an underlying parametric family of conditional copulas, numerous models and estimators have been proposed, notably Acar et al. (2011), Abegaz et al. (2012), Fermanian and Lopez (2015) (single-index type models), Vatter and Chavez-Demoulin (2015) (additive models), among others. But only a few of these papers have a focus on testing the simplifying assumption specifically, although convergence of the proposed estimators are necessary to lead such a task in theory. Actually, some tests of is invoked “in passing” in these papers as potential applications, but without a general approach and/or without some guidelines to evaluate p-values in practice. As an exception, in a very recent paper, Gijbels et al. (2016) have tackled the simplifying assumption directly through comparisons between conditional and unconditional Kendall’s tau.

Example 2.

To illustrate the problem, let us consider a simple example of in dimension . Assume that and . For simplicity, let us assume that follows a Gaussian distribution conditionally on , that is :

| (1) |

Obviously, is a parameter that only affects the conditional margins. Moreover, the conditional copula of given is gaussian with the parameter . Six possible cases can then be distinguished:

-

a.

All variables are mutually independent.

-

b.

is independent of , but and are not independent.

-

c.

and are both marginally independent of , but the conditional copula of and depends on .

-

d.

(or ) and are not independent but and are independent conditionally given .

-

e.

(or ) and are not independent but the conditional copula of and is independent of .

-

f.

(or ) and are not independent and the conditional copula of and is dependent of .

These six cases are summarized in the following table:

| is not constant | |||

|---|---|---|---|

| a | b | c | |

| is not constant | d | e | f |

In the conditional Gaussian model (1), the simplifying assumption consists in assuming that we live in one of the cases , whereas the alternative cases are and . In this model, the conditional copula is entirely determined by the conditional correlation. Note that, in other models, the conditional correlation can vary only because of the conditional margins, while the conditioning copula stay constant: see Property 8 of Spanhel and Kurz (2015).

Note that, in general, there is no reason why the conditional margins would be constant in the conditioning variable (and in most applications, they are not). Nevertheless, if we knew the marginal cdfs’ were constant with respect to the conditioning variable, then the test of (i.e. b against c) would become a classical test of independence between and .

Testing is closely linked to the -sample copula problem, for which we have different and independent samples of a -dimensional variable . In each sample , the observations are i.i.d., with their own marginal laws and their own copula . The -sample copula problem consists on testing whether the latter copulas are equal. Note that we could merge all samples into a single one, and create discrete variables that are equal to when lies in the sample . Therefore, the -sample copula problem is formally equivalent to testing with the conditioning variable .

Conversely, assume we have defined a partition of composed of borelian subsets such that for all , and we want to test

Then, divide the sample in different sub-samples, where any sub-sample contains the observations for which the conditioning variable belongs to . Then, is equivalent to a -sample copula problem. Note that looks like a “consequence” of when it is not the case in general (see Section 3.1), for continuous variables.

Nonetheless, conveys the same intuition as . Since it can be led more easily in practice (no smoothing is required), some researchers could prefer the former assumption than the latter. That is why it will be discussed hereafter. Note that the 2-sample copula problem has already been addressed by Rémillard and Scaillet (2009), and the -sample by Bouzebda et al. (2011). However, both paper are designed only in a nonparametric framework, and these authors have not noticed the connection with the simplifying assumption.

The goal of the paper is threefold: first, to write a “state-of-the art” of the simplifying assumption problem; second to propose some “reasonable” test statistics of the simplifying assumption in different contexts; third, to introduce a new approach of the latter problem, through “box-related” zero assumptions and some associated test statistics. Since it is impossible to state the theoretical properties of all these test statistics, we will rely on “ad-hoc arguments” to convince the reader they are relevant, without trying to establish specific results. Globally, this paper can be considered also as a work program around the simplifying assumption for the next years.

In Section 2, we introduce different ways of testing . We propose different test statistics under a fully nonparametric perspective, i.e. when is not supposed to belong into a particular parametric copula family, through some comparisons between empirical cdfs’ in Subsection 2.1, or by invoking a particular independence property in Subsection 2.2. In Subsection 2.3, new tools are needed if we assume underlying parametric copulas. To evaluate the limiting distributions of such tests, we propose several bootstrap techniques (Subsection 2.4). Section 3 is related to testing . In Subsection 3.1, we detail the relations between and . Then, we provide tests statistics of for both the nonparametric (Subsection 3.2) and the parametric framework (Subsection 3.3), as well as bootstrap methods (Subsection 3.4). In particular, we prove the validity of the so-called “parametric independent” bootstrap when testing . The performances of the latter tests are assessed and compared by simulation in Section 4. A table of notations is available in Appendix A and some of the proofs are collected in Appendix B.

2 Tests of the simplifying assumption

2.1 “Brute-force” tests of the simplifying assumption

A first natural idea is to build a test of based on a comparison between some estimates of the conditional copula with and without the simplifying assumption, for different conditioning events. Such estimates will be called and respectively. Then, introducing some distance between conditional distributions, a test can be based on the statistics . Following most authors, we immediately think of Kolmogorov-Smirnov-type statistics

| (2) |

or Cramer von-Mises-type test statistics

| (3) |

for some weight function of bounded variation , that could be chosen as random (see below).

To evaluate , we propose to invoke the nonparametric estimator of conditional copulas proposed by Fermanian and Wegkamp (2012). Alternative kernel-based estimators of conditional copulas can be found in Gijbels et al. (2011), for instance.

Let us start with an iid -dimensional sample . Let be the marginal empirical distribution function of , based on the sample , for any . Our estimator of will be defined as

| (4) |

where

and is a -dimensional kernel. Obviously, for , we have introduced some estimates of the marginal conditional cdfs’ similarly:

| (5) |

Obviously, is the term of a usual bandwidth sequence, where when tends to the infinity. Since is a nearest-neighbors estimator, it does not necessitate a fine-tuning of local bandwidths (except for those values s.t. is close to one or zero), contrary to more usual Nadaraya-Watson techniques. In other terms, a single convenient choice of would provide “satisfying” estimates of for most values of . For practical reasons, it is important that belongs to and that is a true distribution. This is the reason why we use a normalized version for the estimator of the conditional marginal cdfs.

To calculate the latter statistics (2) and (3), it is necessary to provide an estimate of the underlying conditional copula under . This could be done naively by particularizing a point and by setting . Since the choice of is too arbitrary, an alternative could be to set

for some function that is of bounded variation, and . Unfortunately, the latter choice induce -dimensional integration procedures, that becomes a numerical problem rapidly when is larger than three.

Therefore, let us randomize the “weight” functions , to avoid multiple integrations. For instance, choose the empirical distribution of as , providing

| (6) |

An even simpler estimate of , the conditional copula of given under the simplifying assumption, can be obtained by noting that, under , is the joint law of (see Property 4 below). Therefore, it is tempting to estimate by

| (7) |

when , for some consistent estimates of . A similar estimator has been promoted and studied in Gijbels et al. (2015a) or in Portier and Segers (2015), but they have considered the empirical copula associated to the pseudo sample instead of its empirical cdf. It will be called . Hereafter, we will denote one of the “averaged” estimators , and we can forget the naive pointwise estimator . Therefore, under some conditions of regularity, we guess that our estimators of the conditional copula under will be -consistent and asymptotically normal. It has been proved for in Gijbels et al. (2015a) or in Portier and Segers (2015), as a byproduct of the weak convergence of the associated process.

Under , we would like that the previous test statistics or are convergent. Typically, such a property is given as a sub-product by the weak convergence of a relevant empirical process, here . Unfortunately, this will not be the case in general seing the previous process as a function indexed by , at least for wide ranges of bandwidths. Due to the difficulty of checking the tightness of the process indexed by , some alternative techniques may be required as Gaussian approximations (see Chernozhukov et al. 2014, e.g.). Nonetheless, they would lead us far beyond the scope of this paper. Therefore, we simply propose to slightly modify the latter test statistics, to manage only a fixed set of arguments . For instance, in the case of the Kolmogorov-Smirnov-type test, consider a simple grid , and the modified test statistics

In the case of the Cramer von-Mises-type test, we can approximate any integral by finite sums, possibly after a change of variable to manage a compactly supported integrand. Actually, this is how they are calculated in practice! For instance, invoking Gaussian quadratures, the modified statistics would be

| (8) |

for some conveniently chosen constants , . Note that the numerical evaluation of is relatively costly. Since quadrature techniques require a lot less points than “brute-force” equally spaced grids (in dimension , here), they have to be preferred most often.

Therefore, at least for such modified test statistics, we can insure the tests are convergent. Indeed, under some conditions of regularity, it can be proved that is consistent and asymptotically normal, for every choice of and (see Fermanian and Wegkamp, 2012). And a relatively straightforward extension of their Corollary 1 would provide that, under and for all and ,

converges in law towards a Gaussian random vector. As a consequence, and tends to a complex but not degenerate law under the .

Remark 3.

Other test statistics of can be obtained by comparing directly the functions , for different values of . For instance, let us define

| (9) | |||||

or

| (10) |

for some function of bounded variation . As above, modified versions of these statistics can be obtained considering fixed -grids. Since these statistics involve higher dimensional integrals/sums than previously, they will not be studied more in depth.

The -type statistics and involve at least summations or integrals, which can become numerically expensive when the dimension of is “large”. Nonetheless, we are free to set convenient weight functions. To reduce the computational cost, several versions of are particularly well-suited, by choosing conveniently the functions . For instance, consider

where and denote the empirical cdf of and the empirical copula of respectively. Therefore, simply becomes

| (11) |

where , . Similarly, we can choose

To deal with a single summations only, it is even possible to propose to set

where denotes the empirical cdf of . This means

We have introduced some tests based on comparisons between empirical cdfs’. Obviously, the same idea could be applied to associated densities, as in Fermanian (2005) for instance, or even to other functions of the underlying distributions.

Since the previous test statistics are complicated functionals of some “semi-smoothed” empirical process, it is very challenging to evaluate their asymptotic laws under analytically. In every case, these limiting laws will not be distribution free, and their calculation would be very tedious. Therefore, as usual with copulas, it is necessary to evaluate the limiting distributions of such tests statistics by a convenient bootstrap procedure (parametric or nonparametric). These bootstrap techniques will be presented in Section 2.4.

2.2 Tests based on the independence property

Actually, testing is equivalent to a test of the independence between the random vectors and strictly speaking, as proved in the following proposition.

Proposition 4.

The vectors and are independent iff does not depend on for every vectors and . In this case, the cdf of is .

Proof: For any vectors and any subset ,

If and are independent, then

for every and . This implies for every and every in the support of . This means that does not depend on , because does not depend on any by definition.

Reciprocally, under , is the cdf of . Indeed,

Moreover, due to Sklar’s Theorem, we have

implying the independence between and .

Then, testing is formally equivalent to testing

Since the conditional marginal cdfs’ are not observable, keep in mind that we have to work with pseudo-observations in practice, i.e. vectors of observations that are not independent. In other words, our tests of independence should be based on pseudo-samples

| (12) |

for some consistent estimate , of the conditional cdfs’, for example as defined in Equation (5). The chance of getting distribution-free asymptotic statistics will be very tiny, and we will have to rely on some bootstrap techniques again. To summarize, we should be able to apply some usual tests of independence, but replacing iid observations with (dependent) pseudo-observations.

Most of the tests of rely on the joint law of , that may be evaluated empirically as

Now, let us propose some classical strategies to build independence tests.

-

•

Chi-square-type tests of independence: Let (resp. ) some disjoint subsets in (resp. ).

(13) -

•

Distance between distributions:

(14) (15) for some (possibly random) weight function . Particularly, we can propose the single sum

(16) -

•

Tests of independence based on comparisons of copulas: let and be the empirical copulas based on the pseudo-sample , and respectively. Set

and in particular

The underlying ideas of the test statistics and are similar to those that have been proposed by Deheuvels (1979,1981) in the case of unconditional copulas. Nonetheless, in our case, we have to calculate pseudo-samples of the pseudo-observations and , instead of a usual pseudo-sample of .

Note that the latter techniques require the evaluation of some conditional distributions, for instance by kernel smoothing. Therefore, the level of numerical complexity of these test statistics of is comparable with those we have proposed before to test directly.

2.3 Parametric tests of the simplifying assumption

In practice, modelers often assume a priori that the underlying copulas belong to some specified parametric family . Let us adapt our tests under this parametric assumption. Apparently, we would like to test

Actually, requires two different things: the fact that the conditional copula is a constant copula w.r.t. its conditioning events (test of ) and, additionally, that the right copula belongs to (classical composite Goodness-of-Fit test). Under this point of view, we would have to adapt “omnibus” specification tests to manage conditional copulas and pseudo observations. For instance, and among of alternatives, we could consider an amended version of Andrews (1997)’s specification test

recalling the notations in (12). For other ideas of the same type, see Zheng (2000) and the references therein.

The latter global approach is probably too demanding. Here, we prefer to isolate the initial problem that was related to the simplifying assumption only. Therefore, let us assume that, for every , there exists a parameter such that . To simplify, we assume the function is continuous. Our problem is then reduced to testing the constancy of , i.e.

For every , assume we estimate consistently. For instance, this can be done by modifying the standard semiparametric Canonical Maximum Likelihood methodology (Genest et al., 1995, Tsukahara, 2005): set

through usual kernel smoothing in , where for and . Alternatively, we could consider

instead of See Abegaz et al. (2012) concerning the theoretical properties of and some choice of conditional cdfs’. Those of remain to be stated precisely, to the best of our knowledge. But there is no doubt both methodologies provide consistent estimators, even jointly, under some conditions of regularity.

Under , the natural “unconditional” copula parameter of the copula of the will be estimated by

| (17) |

Surprisingly, the theoretical properties of the latter estimator do not seem to have been established in the literature explicitly. Nonetheless, the latter M-estimator is a particular case of those considered in Fermanian and Lopez (2015) in the framework of single-index models when the link function is a known function (that does not depend on the index). Therefore, by adapting their assumption in the current framework, we easily obtain that is consistent and asymptotically normal if is sufficiently regular, for convenient choices of bandwidths and kernels.

Now, there are some challengers to test :

-

•

Tests based on the comparison between and :

(18) for some weight function .

-

•

Tests based on the comparison between and :

(19) for some distance between cdfs’.

-

•

Tests based on the comparison between copula densities (when they exist):

(20)

Remark 5.

It might be difficult to compute some of these integrals numerically, because of unbounded supports. One solution is to to make change of variables. For example,

Therefore, the choice allows us to simplify the latter statistics to , which is rather easy to evaluate. We used this trick in the numerical section below.

2.4 Bootstrap techniques for tests of

It is necessary to evaluate the limiting laws of the latter test statistics under the null. As a matter of fact, we generally cannot exhibit explicit - and distribution-free a fortiori - expressions for these limiting laws. The common technique is provided by bootstrap resampling schemes.

More precisely, let us consider a general statistics , built from the initial sample . The main idea of the bootstrap is to construct new samples following a given resampling scheme given . Then, for each bootstrap sample , we will evaluate a bootstrapped test statistics , and the empirical law of all these statistics is used as an approximation of the limiting law of the initial statistic .

2.4.1 Some resampling schemes

The first natural idea is to invoke Efron’s usual “nonparametric bootstrap”, where we draw independently with replacement for among the initial sample . This provides a bootstrap sample .

The nonparametric bootstrap is an “omnibus” procedure whose theoretical properties are well-known but that may not be particularly adapted to the problem at hand. Therefore, we will propose alternative sampling schemes that should be of interest, even if we do not state their validity on the theoretical basis. Such a task is left for further researches.

An natural idea would be to use some properties of under , in particular the characterization given in Proposition 4: under , we known that and are independent. This will be only relevant for the tests of Subsection 2.2, and for a few tests of Subsection 2.1, where such statistics are based on the pseudo-sample . Therefore, we propose the following so-called “pseudo-independent bootstrap” scheme:

Repeat, for to ,

-

1.

draw among ;

-

2.

draw independently, among the observations , .

This provides a bootstrap sample .

Note that we could invoke the same idea, but with a usual nonparametric bootstrap perspective: draw with replacement a -sample among the pseudo-observations for each bootstrap sample. This can be called a “pseudo-nonparametric bootstrap” scheme.

Moreover, note that we cannot draw independently among , and beside among independently. Indeed, does not imply the independence between and . At the opposite, it makes sense to build a “conditional bootstrap” as follows:

Repeat, for to ,

-

1.

draw among ;

-

2.

draw independently, along the estimated conditional law of given . This can be down by drawing a realization along the law , for instance (see (4)). This can be done easily because the latter law is purely discrete, with unequal weights that depend on and .

This provides a bootstrap sample .

Remark 6.

Note that the latter way of resampling is not far from the usual nonparametric bootstrap. Indeed, when the bandwidths tend to zero, once is drawn, the procedure above will select the other components of (or close values), i.e. the probability that is “high”.

In the parametric framework, we might also want to use an appropriate resampling scheme. As a matter of fact, all the previous resampling schemes can be used, as in the nonparametric framework, but we would not take advantage of the parametric hypothesis, i.e. the fact that all conditional copulas belong to a known family. We have also to keep in mind that even if the conditional copula has a parametric form, the global model is not fully parametric, because we have not provided a parametric model neither for the conditional marginal cdfs , , nor for the cdf of .

Therefore, we can invoke the null hypothesis and approximate the real copula of by . This leads us to define the following “parametric independent bootstrap”:

Repeat, for to ,

-

1.

draw among ;

-

2.

sample from the copula with parameter independently.

This provides a bootstrap sample .

Remark 7.

At first sight, this might seem like a strange mixing of parametric and nonparametric bootstrap. If , we can nonetheless do a “full parametric bootstrap”, by observing that all estimators of our previous test statistics do not depend on , but on realizations of (see Equations (4) and (5)). Since the law of latter variable is close to a uniform distribution, it is tempting to sample at the first stage, , and then to replace with to get an alternative bootstrap sample.

Without using , we could define the “parametric conditional bootstrap” as:

Repeat, for to ,

-

•

draw among ;

-

•

sample from the copula with parameter .

This provides a bootstrap sample .

Note that, in several resampling schemes, we should be able to keep the same as in the original sample, and simulate only in step 2, as in Andrews(1997), pages 10-11. Such an idea has been proposed by Omelka et al. (2013), in a slightly different framework and univariate conditioning variables. They proved that such a bootstrap scheme “works”, after a fine-tuning of different smoothing parameters: see their Theorem 1.

2.4.2 Bootstrapped test statistics

The problem is now to evaluate the law of a given test statistic, say , under by the some bootstrap techniques. We recall the main technique in the case of the classical nonparametric bootstrap. We conjecture that the idea is still theoretically sound under the other resampling schemes that have been proposed in Subsection 2.4.1.

The principle for the nonparametric bootstrap is based on the weak convergence of the underlying empirical process. Formally, if in an iid sample in , and if denotes its empirical distribution, it is well-known that tends weakly in towards a -dimensional Brownian bridge . And the nonparametric bootstrap works in the sense that converges weakly towards a process , an independent version of , given the initial sample .

Due to the Delta Method, for every Hadamard-differentiable functional from to , there exists a random variable s.t. Assume a test statistics of can be written as a sufficiently regular functional of the underlying empirical process as

where under the null assumption. Then, under , we can rewrite this expression as

| (21) |

Given any bootstrap sample and the associated empirical distribution , the usual bootstrap equivalent of is

from Equation (21). See van der Vaart and Wellner (1996), Section 3.9, for details and mathematically sound statements.

Applying these ideas, we can guess the bootstrapped statistics corresponding to the tests statistics of , at least when the usual nonparametric bootstrap is invoked.

Let us illustrate the idea with . Note that and for some smoothed functional and . Under , and . Therefore, its bootstrapped version is

Obviously, the functions and have been calculated as and respectively, but replacing by . Similarly, the bootstrapped versions of some Cramer von-Mises-type test statistics are

When playing with the weight functions , it is possible to keep the same weights for the bootstrapped versions, or to replace them with some functionals of . For instance, asymptotically, it is equivalent to consider

Similarly, the limiting law of

given is unchanged replacing by .

The same ideas apply concerning the tests of Subsection 2.2, but they require some modifications. Let be some cdf on . Denote by and the associated cdf on the first and components respectively. Denote by , and their empirical counterparts. Under , and for any measurable subsets and , . Our tests will be based on the difference

Therefore, a bootstrapped approximation of the latter quantity will be

To be specific, the bootstrapped versions of our tests are specified as below.

-

•

Chi-square-type test of independence:

-

•

Distance between distributions:

and is obtained replacing by (or even ).

-

•

A test of independence based on the independence copula: Let , and be the empirical copulas based on a bootstrapped version of the pseudo-sample , and respectively. This version can be obtained by nonparametric bootstrap, as usual, providing new vectors at every draw. The associated bootstrapped statistics are

In the case of the parametric statistics, the situation is pretty much the same, as long as we invoke the nonparametric bootstrap. For instance, the bootstrapped versions of some previous test statistics are

in the case of the nonparametric bootstrap. We conjecture that the previous techniques can be applied with the other resampling schemes that have been proposed in Subsection 2.4.1. Nonetheless, a complete theoretical study of all these alternative schemes and the statement of the validity of their associated bootstrapped statistics is beyond the scope of this paper.

Remark 8.

For the “parametric independent” bootstrap scheme, we have observed that the test powers are a lot better by considering

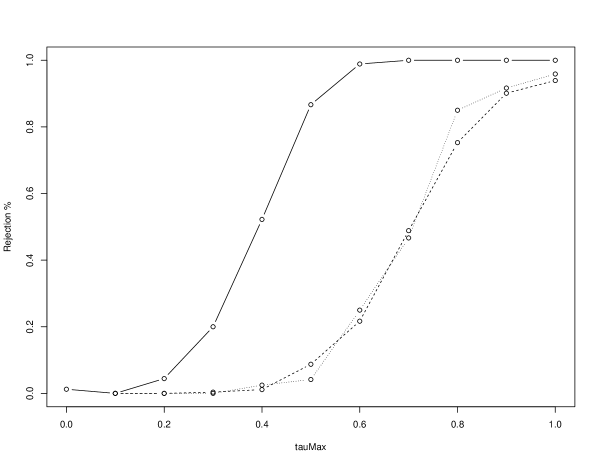

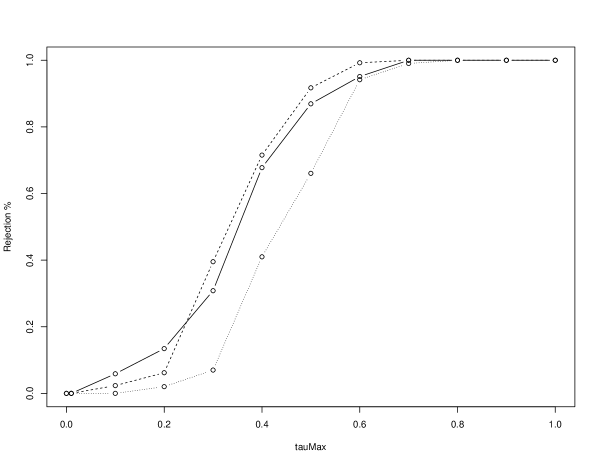

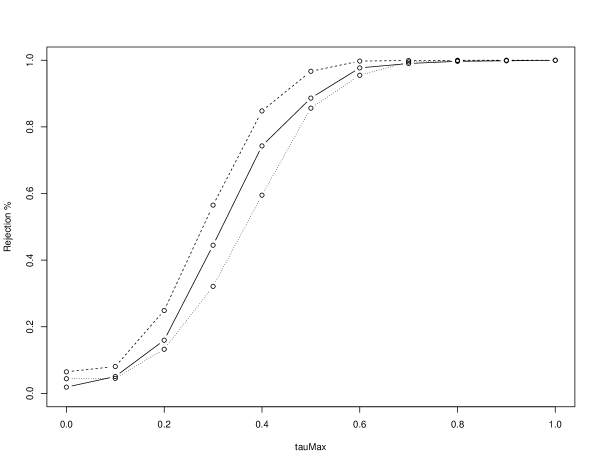

instead. The relevance of such statistics may be theoretically justified in the slightly different context of “box-type” tests in the next Section (see Theorem 14). Since our present case is close to the situation of “many small boxes”, it is not surprising that we observe similar features. Note that, contrary to the nonparametric bootstrap or the “parametric conditional” bootstrap, the “parametric independent” bootstrap scheme uses . More generally, and following the same idea, we found that using the statistic for the pseudo-independent bootstrap yields much better performance than . In our simulations, we will therefore use as the bootstrap test statistic (see Figures 1 and 2).

Remark 9.

For testing at a node of a vine model, the realizations of the corresponding explanatory variables are not observed in general. In practice, they have to be replaced with pseudo-observations in our previous test statistics. Their calculation involves the bivariate conditional copulas that are associated with the previous nodes in a recursive way. The theoretical analysis of the associated bootstrap schemes is challenging and falls beyond the scope of the current work.

3 Tests with “boxes”

3.1 The link with the simplifying assumption

As we have seen in Remark 1, we do not have in general, when for every . This is the hint there are some subtle relations between conditional copulas when the conditioning event is pointwise or when it is a measurable subset. Actually, to test in Section 2, we have relied on kernel estimates and smoothing parameters, at least to evaluate conditional marginal distributions empirically. To avoid the curse of dimension (when is “large” i.e. larger than three in practice), it is tempting to replace the pointwise conditioning events with for some borelian subsets , . As a shorthand notation, we shall write the set of all such . We call them “boxes” because choosing -dimensional rectangles (i.e. intersections of half-spaces separated by orthogonal hyperplans) is natural, but our definitions are still valid for arbitrary borelian subsets in . Technically speaking, we will assume that the functions are Donsker, to apply uniform CLTs’ without any hurdle. Actually, working with -“boxes” instead of pointwise will simplify a lot the picture. Indeed, the evaluation of conditional cdfs’ given does not require kernel smoothing, bandwidth choices, or other techniques of curve estimation that deteriorate the optimal rates of convergence.

Note that, by definition of the conditional copula of given , we have

for every point and every subset in . So, it is tempting to replace by

For any , consider a sequence of boxes s.t. . If the law of is sufficiently regular, then for any . Therefore, implies . This is stated formally in the next proposition.

Proposition 10.

Assume that the function , defined by is continuous everywhere. Then, for every and any sequence of boxes such that , we have

for every .

Proof: Consider a particular . If one component of is zero, the result is obviously satisfied. If one component of is one, this component does not play any role. Therefore, we can restrict ourselves on . By continuity, there exists s.t. for every . Let the sequences such that for every and every . First, let us show that when tends to the infinity. Indeed, by the definition of conditional probabilities (Shiryayev 1984, p.220), we have

and

By substracting the two latter identities, we deduce

| (22) | |||||

But, by assumption, tends towards when tends to , for any (pointwise convergence). A straightforward application of Dini’s Theorem shows that the latter convergence is uniform on : tends to zero when . From (22), we deduce that . By the continuity of , we get , for any .

Second, let us come back to conditional copulas: setting , we have

Since tends to when and invoking the continuity of at , we get that when .

Unfortunately, the opposite is false. Counter-intuitively, does not lead to a consistent test of the simplifying assumption. Indeed, under , we can see that depends on in general, even if does not depend on !

This is due to the nonlinear transform between conditional (univariate and multivariate) distributions and conditional copulas. In other words, for a usual -dimensional cdf , we have

| (23) |

for every measurable subset and . At the opposite and in general, for conditional copulas,

| (24) |

for . And even if we assume , we have in general,

| (25) |

As a particular case, taking , this means again that .

Let us check this rather surprising feature with the example of Remark 1 for another subset . Recall that is true and that for every . Consider the subset , for any real number . The probability of this event is . Now, let us verify that

for some in . Clearly, for every real number , we have

In particular, . Therefore, set and we get

In this example, for every , even if is satisfied.

Nonetheless, getting back to the general case, we can easily provide an equivalent of Equation (23) for general conditional copulas, i.e. without assuming .

Proposition 11.

For all and all ,

Proof: From (23), we get :

We can conclude by using the following definition of the conditional copula

Now, we understand why (24) (and (25) under ) are not identities: the conditional copulas, given the subset , still depend on the conditional margins of given pointwise in general.

Note that, if is independent of for every , then, for any such ,

and we can revisit the identity of Proposition 11: under , we have

This means and are equivalent. We consider such circumstances as very peculiar and do not have to be confused with a test of . Therefore, we advise to lead a preliminary test of independence between and (or at least between and for any ) before trying to test itself.

Now, let us revisit the characterisation of in terms of the independence property, as in Subsection 2.2. The latter analysis is confirmed by the equivalent of Proposition 4 in the case of conditioning subsets . Now, the relevant random vector would be

that has straightforward empirical counterparts. Then, it is tempting to test

Nonetheless, it can be proved easily that this is not a test of , unfortunately.

Proposition 12.

and are independent for every measurable subset iff and are independent.

Proof: For any measurable subset and any , under , we have

Consider . Due to the continuity of the conditional cdfs’, there exists s.t. , . Then, using the invertibility of , we get This implies that is equivalent to the following property: for every and ,

The previous result shows that a test of is a test of independence between and . When the latter assumption is satisfied, and then are true too, but the opposite is false.

Previously, we have exhibited a simple trivariate model where is satisfied when and are not independent. Then, we see that it is not reasonable to test whether the mapping is constant over , the set of all such that , with the idea of testing .

Nonetheless, one can weaken the latter assumption, and restrict oneself to a finite family of subsets with positive probabilities. For such a family, we could test the assumption

To fix the ideas and w.l.o.g., we will consider a given family of disjoint subsets in hereafter. Note the following consequence of Proposition 11.

Proposition 13.

Assume that, for all and for all ,

| (26) |

Then, implies .

Obviously, if the family is too big, then (26) will be too demanding: will be close to a test of independence between and , and no longer a test of . Moreover, the chosen subsets in the family do not need to be disjoint, even if this would be a natural choice. As a special case, if , the previous condition is equivalent to the independence between and for every .

Note that (26) does not imply that the vector of explanatory variables should be discretized. Indeed, the full model requires the specification of the underlying conditional copula too, independently of the conditional margins and arbitrarily. For instance, we can choose a Gaussian conditional copula whose parameter is a continuous function of , even if (26) is fulfilled. And the law of given will depend on the current value of .

A test of may be relevant in a lot of situations, beside technical arguments as the absence of smoothing. First, the case of discrete (or discretized) explanatory variables is frequent. When is discrete and takes a value among , set , . Then, there is identity between testing and , with . Second, the level of precision and sharpness of a copula model is often lower than the models for (conditional) margins. To illustrate this idea, a lot of complex and subtle models to explain the dynamics of asset volatilities are available when the dynamics of cross-assets dependencies are often a lot more basic and without clear-cut empirical findings. Therefore, it makes sense to simplify conditional copula models compared to conditional marginal models. This can be done by considering only a few possible conditional copulas, associated to some events , . For example, Jondeau and Rockinger (2006) (the first paper that introduced conditional dependence structures, beside Patton (2006a)) proposed a Gaussian copula parameter that take a finite of values randomly, based on the realizations of some past asset returns. Third, similar situation occur with most Markov-switching copula models, where a finite set of copulas is managed. In such models, the (unobservable, in general) underlying state of the economy determines the index of the box: see Cholette et al. (2009), Wang et al. (2013), Stöber and Czado (2014), Fink et al. (2016), among others.

Therefore, testing is of interest per se. Even if this is not equivalent to (i.e. the simplifying assumption) formally, the underlying intuitions are close. And, particularly when the components of the conditioning variable are numerous, it can make sense to restrict the information set of the underlying conditional copula to a fixed number of conveniently chosen subsets . And the constancy of the underlying copula when belongs to such subsets is valuable in a lot of practical situations. Therefore, in the next subsections, we study some specific tests of itself.

3.2 Non-parametric tests with “boxes”

To specify such tests, we need first to estimate the conditional marginal cdfs’, for instance by

for every real and . Similarly the joint law of given may be estimated by

The conditional copula given will be estimated by

Therefore, it is easy to imagine tests of , for instance

| (27) |

| (28) |

for some nonnegative weight functions , or even

| (29) |

where denotes a distance between cdfs’ on . More generally, define the matrix

and any statistic of the form can be used as a test statistics of , when is a norm on the set of -matrices. Obviously, it is easy to introduce similar statistics based on copula densities instead of cdfs’.

3.3 Parametric test statistics with “boxes”

When we work with subsets instead of pointwise conditioning events , we can adapt all the previous parametric test statistics of Subsection 2.3. Nonetheless, the framework will be slightly modified.

Let us assume that, for every , belongs to the same parametric copula family . In other words, for every . Therefore, we could test the constancy of the mapping , i.e. to test

Clearly, for every , we can estimate by

It can be proved that the estimate is consistent and asymptotically normal, by revisiting the proof of Theorem 1 in Tsukahara (2005). Here, the single difference w.r.t. the latter paper is induced by the random sample size, modifying the limiting distributions. The proof is left to the reader.

Under the zero assumption , the parameter of the copula of given is the same for any . It will be denoted by , and we can still estimate it by the semi-parametric procedure

Obviously, under some conditions of regularity and under , it can be proved that is consistent and asymptotically normal, by adapting the results of Tsukahara (2005).

For convenience, let us define the “box index” function for any . In other words, is the index of the box that contains . It equals zero, when no box in contains . Let us introduce the r.v. that stores only all the needed information concerning the conditioning with respect to the variables . We can then define the empirical pseudo-observations as

for any . Since we do not observe the conditional marginal cdfs’, we define the observed pseudo-observations that we calculate in practice: for

Note that we can then rewrite the previous estimators as

Now, let us revisit some of the previously proposed test statistics in the case of “boxes”.

-

•

Tests based on the comparison between and :

(30) for some weights .

-

•

Tests based on the comparison between and :

(31)

and others.

3.4 Bootstrap techniques for tests with boxes

In the same way as in the previous section, we will need bootstrap schemes to evaluate the limiting laws of the test statistics of or under the null. All the nonparametric resampling schemes of Subsection 2.4.1 (in particular Efron’s usual bootstrap) can be used in this framework, replacing the conditional pseudo-observations by , . The parametric resampling schemes of Subsection 2.4.1 can also be applied to the framework of “boxes”, replacing by and by . In the parametric case, the bootstrapped estimates are denoted by and . They are the equivalents of and , replacing by .

The bootstrapped statistics will also be changed accordingly. Writing them explicitly is a rather straightforward exercise and we do not provide the details, contrary to Subsection 2.4. For example, the bootstrapped statistics corresponding to (30) is

where is the result of the program , in the case of Efron’s nonparametric bootstrap.

As we noticed in Remark 8, some changes are required when dealing with the “parametric independent” bootstrap. Indeed, under the alternative, we observe , because we have precisely generated a bootstrap sample under . As a consequence, the law of would be close to the law of but under the alternative, providing very small powers. Therefore, convenient bootstrapped test statistics of under the “parametric independent” scheme will be of the type

Such a result is justified theoretically by the following theorem.

Theorem 14.

Assume that is satisfied, and that we apply the parametric independent bootstrap. Set

Then there exists two independent and identically distributed random vectors and , and a real number such that

The proof of this theorem has been postponed in Appendix B.

As a consequence of the latter result, applying the parametric independent bootstrap procedures for some test statistics based on comparisons between and the is valid. For instance, and will converge jointly in distribution to a pair of independent and identically distributed variables. Indeed, we have

The same reasoning applies with and , for sufficiently regular copula families.

Remark 15.

We have to stress that the first-level bootstrap, i.e. resampling among the conditioning variables , is surely necessary to obtain the latter result. Indeed, it can be seen that the key proposition 16 is no longer true otherwise, because the limiting covariance functions of the two corresponding processes and will not be the same: see remark 22 below.

4 Numerical applications

Now, we would like to evaluate the empirical performances of some of the previous tests by simulation. Such an exercise has been led by Genest et al. (2009) or Berg (2009) extensively in the case of goodness-of-fit test for unconditional copulas. Our goal is not to replicate such experiments in the case of conditional copulas and for tests of the simplifying assumption. Indeed, we have proposed dozens of test statistics and numerous bootstrap schemes. Moreover, testing the simplifying assumption through or some “box-type” problems through doubles the scale of the task. Finally, in the former case, we depend on smoothing parameters that induce additional degrees of freedom for the fine tuning of the experiments (note that Genest et al. (2009) and Berg (2009) have renounced to consider tests that require additional smoothing parameters, as the pivotal test statistics proposed in Fermanian (2005)). In our opinion, an exhaustive simulation experiment should be the topic of (at least) one additional paper. Here, we will restrict ourselves to some partial numerical elements. They should convince readers that the methods and techniques we have discussed previously provide fairly good results and can be implemented in practice safely.

Hereafter, we consider bivariate conditional copulas and a single conditioning variable, i.e. and . The sample sizes will be , except if it is differently specified. Concerning the bootstrap, we will resample times to calculate approximated p-values. Each experiment has been repeated times to calculate the percentages of rejection. The computations have been made on a standard laptop, and, for the non-parametric bootstrap, they took an average time of seconds for ; s for , s for , s for and s for .

In terms of model specification, the margins of will depend on as

We have studied the following conditional copula families: given ,

-

•

the Gaussian copula model, with a correlation parameter ,

-

•

the Student copula model, with degrees of freedom and a correlation parameter ,

-

•

the Clayton copula model, with a parameter ,

-

•

the Gumbel copula model, with a parameter ,

-

•

the Frank copula model, with a parameter .

In every case, we calibrate such that the conditional Kendall’s tau satisfies , for some constant . By default, is equal to one. In this case, the random Kendall’s tau are uniformly distributed on .

Test of : we calculate the percentage of rejections of , when the sample is drawn under the true law (level analysis) or when it is drawn under the same parametric copula family, but with varying parameters (power analysis). For example, when the true law is a Gaussian copula with a constant parameter corresponding to , we draw samples under the alternative through a bivariate Gaussian copula whose random parameters are given by . The chosen test statistics are , (nonparametrics test of ), and (nonparametric tests of based on the independence property) and (a parametric test of ). To compute these statistics, we use the estimator of the simplified copula defined in Equation (6).

Test of : in the case of the test with boxes, the data-generating process will be

where , so that the boxes are all of equal probability. As , we recover the continuous model for which .

In the same way, we calibrate the parameter of the conditional copulas such that the conditional Kendall’s tau satisfies .

The choice of “the best” boxes is not an easy task. This problem happens frequently in statistics (think of Pearson’s chi-square test of independence, for instance), and there is no universal answer. Nonetheless, in some applications, intuition can be fuelled by the context. For example, in finance, it makes sense to test whether past positive returns induce different conditional dependencies between current returns than past negative returns. And, as a general “by default” rule, we can divide the space of into several boxes of equal (empirical) probabilities. This trick is particularly relevant when the conditioning variable is univariate. Therefore, in our example, we have chosen boxes of equal empirical probability for , with equal weights.

We have only evaluated for testing . In the following tables, for the parametric tests,

-

•

“bootNP” means the usual nonparametric bootstrap ;

-

•

“bootPI” means the parametric independent bootstrap (where is drawn under and under the usual nonparametric bootstrap);

-

•

“bootPC” means the parametric conditional bootstrap (nonparametric bootstrap for , and is sampled from the estimated conditional copula );

-

•

“bootPseudoInd” means the pseudo-independent bootstrap (nonparametric bootstrap for , and draw independently, among the pseudo-observations );

-

•

“bootCond” means the conditional bootstrap (nonparametric bootstrap for , and is sampled from the estimated conditional law of given ).

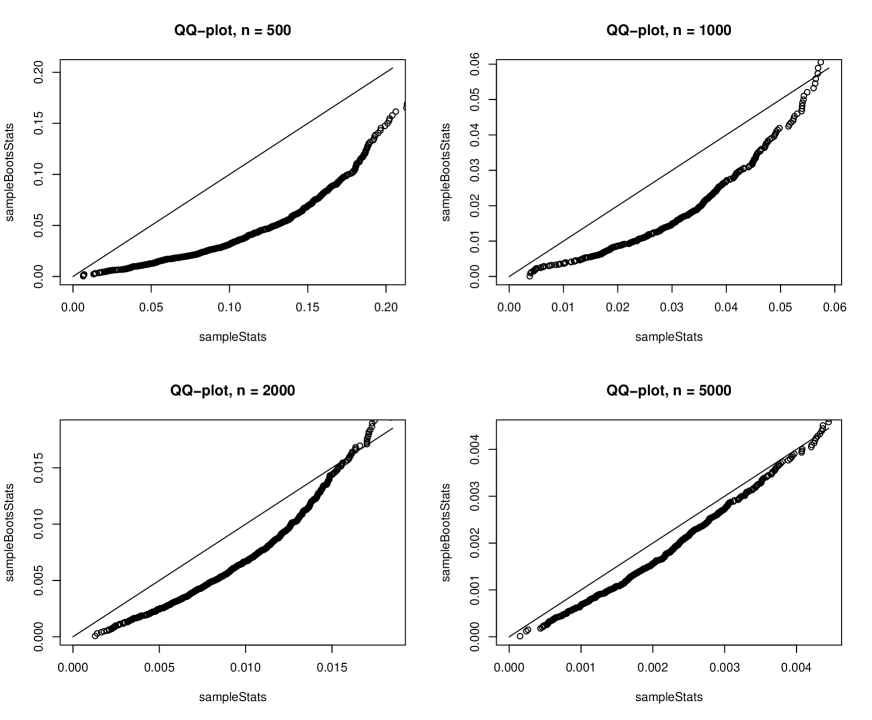

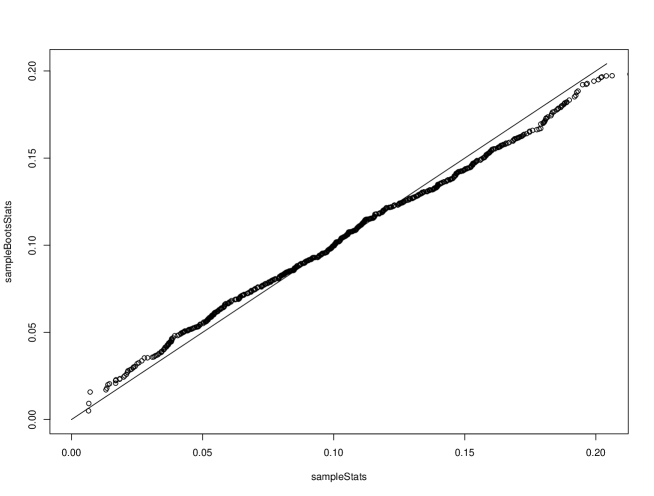

Concerning tests of , the results are relatively satisfying. For the nonparametric tests and those based on the independence property (Tables 1 and 2) the rejection rates are large when , and the theoretical levels () are underestimated (a not problematic feature in practice). This is still the case for tests of the simplifying assumption under a parametric copula model through : see Tables 3 and 4. The three bootstrap schemes provide similar numerical results. Remind that the bootstrapped statistics is with bootPI (Remark 8). Tests of under a parametric framework and through confirm such observations. To evaluate the accuracy of the bootstrap approximations asymptotically, we have compared the empirical distribution of some test statistics and their bootstrap versions under the null hypothesis for two bootstrap schemes (see Figures 5 and 6). For the nonparametric bootstrap, the two distributions begin to match each other at whereas is enough for the parametric independent bootstrap.

We have tested the influence of : the smaller is this parameter, the smaller is the percentage of rejections under the alternative, because the simulated model tends to induce lower dependencies of copula parameters w.r.t. : see Figures 1, 2, 3, and 4. Note that, on each of these figures, the point at the left corresponds to a conditional Kendall’s tau which is constant, and equal to (because ) whereas the rejection percentages in Tables 1 and 3 correspond to a conditional Kendall’s tau constant, and equal to . As the two data-generating process are not the same, the rejection percentages can differ even if both are under the null hypothesis. Nevertheless, in every case, our empirical sizes converge to as the sample size increases. When , we found that the percentage of rejections are between % and %.

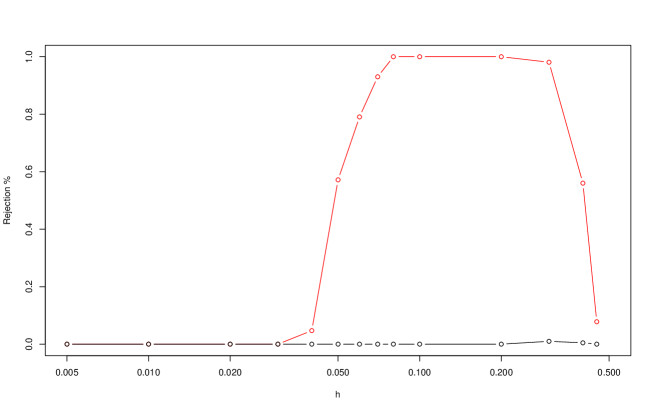

We have not tried to exhibit an “asymptotically optimal” bandwidth selector for our particular testing problem. This could be the task for further research. We have preferred a basic ad-hoc procedure. In our test statistics, we smooth w.r.t. (or its estimate, to be specific), whose law is uniform on . A reasonable bandwidth is given by the so-called rule-of-thumb in kernel density estimation, i.e. . Such a choice has provided reasonable results. The typical influence of the bandwidth choice on the test results is illustrated in Figure 7. In general, the latter belongs to reasonably wide intervals of “convenient” bandwidth values, so that the performances of our considered tests are not very sensitive to the bandwidth choice.

To avoid boundary problems, we have slightly modified the test statistics: we remove the observations such that or . This corresponds to changing the integrals (resp. max) on to integrals (resp. max) on .

| Family | (8) | (10) | (13) | (15) |

|---|---|---|---|---|

| Gaussian | 0 | 0 | 0 | 0 |

| Student | 0 | 0 | 0 | 0 |

| Clayton | 0 | 0 | 1 | 0 |

| Gumbel | 1 | 1 | 0 | 1 |

| Frank | 0 | 0 | 0 | 0 |

| Family | (8) | (10) | (13) | (15) |

|---|---|---|---|---|

| Gaussian | 98 | 100 | 100 | 93 |

| Student | 100 | 99 | 98 | 90 |

| Clayton | 99 | 99 | 99 | 98 |

| Gumbel | 99 | 98 | 100 | 95 |

| Frank | 98 | 100 | 98 | 50 |

| Family | (18) | (30) | ||||

|---|---|---|---|---|---|---|

| bootPI | bootPC | bootNP | bootPI | bootPC | bootNP | |

| Gaussian | 4 | 0 | 0 | 6 | 4 | 1 |

| Student | 6 | 0 | 2 | 4 | 5 | 3 |

| Clayton | 7 | 0 | 1 | 7 | 1 | 1 |

| Gumbel | 3 | 1 | 0 | 9 | 2 | 2 |

| Frank | 4 | 0 | 6 | 3 | 5 | 1 |

| Family | (18) | (30) | ||||

|---|---|---|---|---|---|---|

| bootPI | bootPC | bootNP | bootPI | bootPC | bootNP | |

| Gaussian | 100 | 100 | 100 | 100 | 100 | 100 |

| Student | 100 | 100 | 100 | 100 | 100 | 100 |

| Clayton | 100 | 62 | 98 | 100 | 98 | 100 |

| Gumbel | 100 | 100 | 34 | 100 | 99 | 76 |

| Frank | 100 | 100 | 100 | 100 | 100 | 100 |

5 Conclusion

We have provided an overview of the simplifying assumption problem, under a statistical point of view. In the context of nonparametric or parametric conditional copula models (with unknown conditional marginal distributions), numerous testing procedures have been proposed. We have developed the theory towards a slightly different but related approach, where “box-type” conditioning events replace pointwise ones. This open a new field for research that is interesting per se. Several new bootstrap procedures have been detailed, to evaluate p-values under the zero assumption in both cases. In particular, we have proved the validity of one of them (the “parametric independent” bootstrap scheme under ).

Clearly, there remains a lot of work. We have opened the Pandora box rather than provided definitive answers. Open questions are still numerous: precise theoretical convergence results of our test statistics (and others!), validity of these new bootstrap schemes, bandwidth choices, empirical performances,… All these dimensions would require further research. We have made a contribution to the landscape of problems related to the simplifying assumption, and proposed a working program for the whole copula community.

References

- [1] Aas, K., Czado, C., Frigessi, A., and H. Bakken (2009). Pair-copula constructions of multiple dependence. Insurance Math. Econom. 44(2), 182-198.

- [2] Abegaz, F., Gijbels, I. and N. Veraverbeke (2012). Semiparametric estimation of conditional copulas. J. Multivariate Anal. 110, .

- [3] Acar, E.F., Craiu, R.V. and F. Yao (2011). Dependence Calibration in Conditional copulas: A Nonparametric Approach. Biometrics 67, 445-453.

- [4] Acar, E.F., Genest, C. and J. Nešlehová (2012). Beyond simplified pair-copula constructions. J. Multivariate Anal. 10, .

- [5] Acar, E.F., Craiu, R.V., and F. Yao (2013). Statistical testing of covariate effects in conditional copula models. Electron. J. Stat. 7, .

- [6] Andrews, D. (1997). Conditional Kolmogorov-Smirnov test. Econometrica 65, 1097-1128.

- [7] Berg, D. (2009). Copula goodness-of-fit testing: An overview and power comparison European J. Finance 15, 675-701.

- [8] Bergsma, W.P. (2011). Nonparametric testing of conditional independence by means of the partial copula. arXiv 1101.4607.

- [9] Bouzebda, S., Keziou, A. and T. Zari (2011). K-Sample Problem Using Strong Approximations of Empirical Copula Processes. Math. Methods Statist. 20, 14-29.

- [10] Chernozhukov, V. Chetverikov, D. and Kato, K. (2014). Gaussian approximations of suprema of empirical processes. Ann. Statist. 42, 1564-1597.

- [11] Cholette, L., Heinen, A. and Valdesogo, A. (2009). Modeling international financial returns with a multivariate regime-switching copula. J. Financial Econometrics 7, 437-480.

- [12] Craiu, R.V. and A. Sabeti (2012). In mixed company: Bayesian inference for bivariate conditional copula models with discrete and continuous outcomes. J. Multivariate Anal. 110, 106-120.

- [13] Deheuvels, P. (1979). La fonction de dépendance empirique et ses propriétés. Un test non paramétrique d’indépendance, Acad. Roy. Belg. Bull.Cl. Sci. (5)65, 274–292.

- [14] Deheuvels, P. (1981). A Kolmogorov–Smirnov Type Test for Independence and Multivariate Samples. Rev. Roumaine Math. Pures Appl. 26, 213–226.

- [15] Fermanian, J-D (2005). Goodness-of-fit tests for copulas. J. Multivariate Anal. 95, 119-152.

- [16] Fermanian J-D and M. Wegkamp (2012). Time-dependent copulas. J. Multivariate Anal. 110, 19-29.

- [17] Fermanian J.-D. and O. Lopez (2015). Single-index copulas. Working paper Crest 2015-12.

- [18] Fink, H., Klimova, Y., Czado, C. and Stöber, J. (2016). Regime switching vine copula models for global equity and volatility indices. arXiv:1604.05598.

- [19] Genest, C., Ghoudi, K. and L.-P. Rivest (1995). A semiparametric estimation procedure of dependenceparameters in multivariate families of distributions. Biometrika 82, 543-552.

- [20] Genest, C. and B. Rémillard (2008). Validity of the parametric bootstrap for goodness-of-fit testing in semiparametric models. Ann. Inst. Henri Poincaré Probab. Stat. 44 (6), 1096-1127.

- [21] Genest, C., Rémillard, B. and A. Beaudoin (2009). Goodness-of-fit tests for copulas: A review and a power study. Insurance Math. Econom. 44, 199-213

- [22] Gijbels, I., Veraverbeke, N. and M. Omelka (2011). Conditional copulas, association measures and their applications. Comput. Statist. Data Anal. 55 1919-1932.

- [23] Gijbels, I., Veraverbeke, N.and M. Omelka (2015a). Estimation of a Copula when a Covariate Affects only Marginal Distributions. Scand. J. Stat. 42 1109-1126.

- [24] Gijbels, I., Omelka, M. and N. Veraverbeke (2015b). Partial and average copulas and association measures. Electr. J. Statist. 9, 2420-2474.

- [25] I. Gijbels, M. Omelka, N. Veraverbeke (2016). Nonparametric testing for no covariate effects in conditional copulas. Statistics, online.

- [26] Hobæk Haff, I., Aas, K. and A. Frigessi (2010). On the simplified pair-copula construction–simply useful or too simplistic? J. Multivariate Anal. 101 1296–1310.

- [27] Jondeau, E. and Rockinger, M. (2006). The copula-garch model of conditional dependencies: An international stock market application. J. of Internat. Money and Finance 25, 827-853.

- [28] Nagler, T. and C. Czado (2016). Evading the curse of dimensionality in nonparametric density estimation with simplified vine copulas. arXiv:1503.03305

- [29] Omelka, M., Veraverbeke, N. and I. Gijbels (2013). Bootstrapping the conditional copula. J. Statist. Plann. Inference 143, 1-23.

- [30] Patton, A. (2006a) Modelling Asymmetric Exchange Rate Dependence, Internat. Econom. Rev. 47, 527-556.

- [31] Patton, A. (2006b) Estimation of multivariate models for time series of possibly different lengths, J. Appl. Econometrics 21, 147-173.

- [32] Portier, F. and J. Segers (2015). On the weak convergence of the empirical conditional copula under a simplifying assumption. arXiv:1511.06544.

- [33] Rémillard, B. and O. Scaillet (2009). Testing for Equality between Two copulas. J. Multivariate Anal. 100, 377-386.

- [34] Sabeti, A., Wei, M. and R.V. Craiu (2014). Additive models for conditional copulas Stat 3, 300-312.

- [35] Shiryaev, A.N. (1984). Probability. Graduate Texts in Mathematics 95. Springer.

- [36] Spanhel, F. and M.S. Kurz (2015). Simplified vine copula models: Approximations based on the simplifying assumption. arXiv:1510-06971.

- [37] Stöber, J., Joe, H. and C. Czado (2013). Simplified pair copula constructions—limitations and extensions. J. Multivariate Anal. 119 101–118.

- [38] Stöber, J., Czado, C. (2014). Regime switches in the dependence structure of multivariate financial data. Computational Statistics and Data Analysis 76, 672-686.

- [39] Tsukahara, H. (2005). Semiparametric estimation in copula models. Canad. J. Statist. 33, 357-375.

- [40] van der Vaart, A. and J. Wellner (1996). Weak convergence and empirical processes. Springer.

- [41] Vatter, T. and V. Chavez-Demoulin (2015). Generalized additive models for conditional dependence structures. J. Multivariate Anal. 141, 147-167.

- [42] Veraverbeke, N., Omelka, M. and I. Gijbels (2011). Estimation of a Conditional Copula and Association Measures. Scand. J. Stat. 38, 766-780.

- [43] Wang, Y.-C., Wu, J.-L. and Lai, Y.-H. (2013). A Revisit to the Dependence Structure between the Stock and Foreign Exchange Markets: A Dependence-Switching Copula Approach. J. Banking Finance 37, 1706-1719.

- [44] Zheng, J.X. (2000). A consistent test of conditional parametric distributions. Econometric Theory 16 667-691.

Appendix A Notations

| random vector of size | |

| , | and |

| initial sample of i.i.d. observations | |

| measurable subset in | |

| collection of all measurable subsets of | |

| such that is in each set with positive probability | |

| partition of into sets | |

| such that is in each set with positive probability | |

| box index, i.e. is the such that | |

| -th pseudo-observation of the -th variable | |

| conditional observation of given | |

| conditional observation of given the box index | |

| copula family indexed by the elements of a set | |

| copula of the family with the parameter | |

| density of the copula | |

| unconditional parameter of the copula of | |

| parameter of the conditional copula of given | |

| unconditional parameter of the copula of | |

| conditional parameter of the copula of given | |

| marginal cdf of , | |

| conditional marginal cdf of given , | |

| conditional marginal cdf of given , | |

| conditional joint cdf of given | |

| conditional joint cdf of given | |

| joint cdf of | |

| conditional copula of given | |

| conditional copula of given | |

| simplified copula of given |

| (3) | brute-force test statistic of , constructed with the distance |

|---|---|

| between the conditional and the simplified copula | |

| (resp. (2)) | (resp. distance) |

| (resp. (8)) | (resp. distance using a fixed number of points) |

| (10) | brute-force test statistic of , constructed with the -distance |

| (resp. (9)) | (resp. -distance) between all pairs of conditional copulas |

| (13) | chi-square-type test statistic of the independence between and |

| (14) | test statistic based on the distance between the joint empirical cdf |

| of and the product of their empirical cdf, using the norm | |

| (resp. (15)) | (resp. using the norm) |

| (resp. (16)) | (resp. using the norm, weighted by the joint empirical cdf as weight) |

| (18) | test statistic based on the distance between the parameter of the |

| conditional copula and the constant parameter of the simplified copula | |

| (resp. (18)) | (resp. distance) |

| (resp. (19)) | (resp. using some distance between the estimated copulas) |

| (resp. (20)) | (resp. using the distance between the estimated copula densities) |

| (29) | brute-force test statistic of constructed with the distance |

| between all pairs of conditional copulas with Borelian subsets | |

| (resp. (27)) | (resp. with the distance) |

| (resp. (28)) | (resp. with the distance) |

| (30) | test statistic based on the distance between the parameters |

| estimated on each set and the simplified parameter | |

| (resp. (30)) | (resp. based on the distance) |

| (resp. (31)) | (resp. based on some distance between the copulas whose parameters are |

| estimated on each set and the copula with the simplified parameter) | |

| , | bootstrap statistics corresponding to a general test statistic |

Appendix B Proof of Theorem 14

B.1 Preliminaires

Let be a sequence of i.i.d random vectors in , being drawn from the true cdf . They have the same law as the previously called vectors or under the zero assumption . Let be a sequence of i.i.d random vectors in , . Let be an independent sequence of i.i.d random vectors in , where exactly as . The three samples , and are mutually independent. Let be a sequence of i.i.d random vectors in , which are drawn from , the empirical cdf of , and independently of both and .

In the following, we shall use the notation when , are two real functions, possibly from different spaces. Set . We will need some conditions of regularity.

Assumption (R): is three times differentiable with respect to , for every . Moreover, for every ,

The latter technical assumption can be weakened through some trimming techniques, as in Fermanian and Lopez (2015). Since this would require to change the definitions of the parametric estimators, we do not try to improve towards this direction. We will set and .

We associate to every (resp. ) its corresponding index (resp. ) s.t. (resp. ). For convenience, we assume that is a partition of . Otherwise, we have to restrict our sample to the observations for which belongs to some “box” , . Therefore, denote by , , and the empirical laws of , , and respectively. The joint law of (resp. ) will be denoted by (resp. ), with , . Denote by (resp. ) the empirical law of (resp. ) Moreover, and will be the empirical distributions of and respectively. Let be the joint probability distribution of

The following proposition is key. It will be proved in Subsection B.3.

Proposition 16.

Consider the empirical process defined on by

and the corresponding bootstrapped empirical process

or, equivalently, . Then there exist two independent and identically distributed Gaussian processes and such that converges to weakly in .

As a Corollary, we deduce the same results when the discrete variables replace the variables .

Proposition 17.

Under the assumptions of Proposition 16, let the empirical process defined on by

and its bootstrapped empirical process

or equivalently , being the empirical proportion of -observations into . Then, there exist two independent and identically distributed processes and such that converges to weakly in .

Remark 18.

The covariance function of (or ) is given by

As a “toolbox”, we will need the following lemma.

Lemma 19.

Let and be the estimators based on the pseudo-sample (and then on the sample ) as

We will assume they lie in the interior of . Set , and, for , . Moreover, for any distribution on , set

-

(i)

For ,

-

(ii)

For every discrete law with values in , the corresponding distribution satisfies .

-

(iii)

is Hadamard-differentiable at every cdf , and its differential is given by

-

(iv)

Proof : Note that is an explicit measurable function of the sample . Indeed, for any and ,

| (32) |

We deduce that and are measurable functions of the unobservable random variables and , for .

(i). Let . Applying successively the first order condition for the estimator and some Taylor series expansions, we have

implying

Now, invoking (32), let us compute the numerator of this expression:

In the same way, the denominator can be rewritten as

(ii). We now prove the second part of the lemma. Since , we get

(iii). We remark that the law appears three times in : two times in the log-density and one time at the end of the main integral. By separating the effect of a change from to in the main integral only (first term of the differential) and the effect of a change in , and using the standard rule of differential calculus ( is differentiable), we obtain the second part of the given result.

(iv). As in the proof of (i), we apply successively the first order condition for and some Taylor series expansion to get

We deduce

Lemma 20.

Let be defined by

If there exists a random vector such that under , then we have

where is independent of the sample and is the Fisher information matrix

Proof : By a Taylor expansion, we obtain

First, we have

by Assumption (R). By the usual CLT, we know that is independent of as a limit of a sequence of variables that have the same property. Using the law of large numbers, we have also

B.2 Proof of Theorem 14

We first reason under as in Theorem 1 in Genest and Rémillard (2008). By Proposition 17, under , there exist two independent and identically distributed processes and such that

weakly in . By (iii) of Lemma 19, is Hadamard-differentiable and so, using the functional Delta-method, we deduce

By (ii) of Lemma 19, , implying

By Slutsky’s theorem, we have

By (i) of Lemma 19, the latter convergence result implies

Moreover, and are independent and identically distributed under , by construction. Because of (iv) of Lemma 19, can asymptotically be seen as a mean of the and this provides

Therefore, by the continuous mapping theorem, we deduce

and we still have that and are independent and identically distributed under .

Now, we will work under the probability measure over whose density with respect to is

where is the estimator of when applied to the “sample” . We remark that

Since we have shown that under , use Lemma 20 and obtain

Therefore, under , we have

where . Note that because and are independent, and . This corresponds to condition (iii) of Theorem 3.10.5 of Van der Waart and Wellner (1996), and we deduce is contiguous with respect to . We can then apply Le Cam’s Third Lemma (Theorem 3.10.7 of Van der Waart and Wellner (1996)), and we get that, under ,

where for any simple function . Choose and and set . Then, we have

Therefore, we have proven the following equality:

where . To finish the proof, it remains to show that for all , i.e.

Actually, the reasoning is exactly the same when dealing with and , , replacing by . We get

Second, note that, when ,

Third, let us calculate , . From Lemma 19, we have

for . Since , we can simplify the latter equalities:

Since , we have

Then, we can rewrite and , where

Substituting by , we get

Fourth, since is the weak limit of under , this implies , with

Finally, by (i) of the following Lemma 21, we have , By (ii) of the latter lemma, we have for all and . Finally, we obtain , which finishes the proof.

Lemma 21.

Assume that is satisfied. Then,

-

(i)

For ,

-

(ii)

The expectations

do not depend on .

Proof : (i) By simple calculations, we obtain