Decompositions of Dependence for High-Dimensional Extremes

Abstract

Employing the framework of regular variation, we propose two decompositions which help to summarize and describe high-dimensional tail dependence. Via transformation, we define a vector space on the positive orthant, yielding the notion of basis. With a suitably-chosen transformation, we show that transformed-linear operations applied to regularly varying random vectors preserve regular variation. Rather than model regular variation’s angular measure, we summarize tail dependence via a matrix of pairwise tail dependence metrics. This matrix is positive semidefinite, and eigendecomposition allows one to interpret tail dependence via the resulting eigenbasis. Additionally this matrix is completely positive, and a resulting decomposition allows one to easily construct regularly varying random vectors which share the same pairwise tail dependencies. We illustrate our methods with Swiss rainfall data and financial return data.

Keywords: regular variation, tail dependence, dimension reduction, angular measure.

1 Introduction

Despite many noteworthy models which have been developed to capture extremal dependence like the extremal- (Opitz,, 2013), Hüsler–Reiss (1989), and mixture-Dirichlet (Boldi and Davison,, 2007), describing dependence for high-dimensional extremes remains a challenge. Multivariate regular variation is intricately linked to the study of extremes as it can be tied to characterizations of the multivariate extreme value distributions or used directly to model threshold exceedances. Tail dependence of a multivariate regularly varying random vector of dimension is described by the angular (or spectral) measure on the dimensional unit ball. Estimating a dimensional measure is challenging, and this challenge is exacerbated as extremes practice retains only a small subset of extreme data for estimation. Recent efforts to describe or model high dimensional extremes include Strokorb and Schlather, (2015) who determine a max-stable model from pairwise and higher-dimensional summaries of extremal dependence, and Chautru, (2015) who proposes a clustering approach to group variables.

In the non-extreme setting, the covariance matrix or its estimate is widely used to summarize dependence information for multivariate distributions or data, even when non-Gaussian. Many multivariate methods arise by performing linear operations on the sample covariance matrix. For example, principal component analysis (Johnson and Wichern,, 2007, Ch. 8) is performed by an eigendecomposition of the covariance matrix.

We aim to provide tools for exploring extremal dependence in high dimensions. We will work within the framework of multivariate regular variation, producing a matrix which summarizes tail dependence, and ultimately obtain two useful decompositions of this matrix. The first decomposition provides an ordered orthonormal basis useful for examining the modes of extremal dependence. The second provides a method for constructing a random vector with a simple dependence structure, yet which shares the same pairwise tail dependencies. To produce these decompositions we link the seemingly disparate ideas of inner product spaces to multivariate regular variation on the nonnegative orthant, thus enabling us to perform transformed linear operations on multivariate regularly varying random vectors.

Resnick, (2007) gives a comprehensive treatment of multivariate regular variation. Roughly speaking, a random vector is multivariate regularly varying if its joint tail decays like a power function; i.e., it is jointly heavy-tailed. Although regular variation can be defined on (Resnick,, 2007, §6.5.5), we model in the nonnegative orthant, as this allows one to focus attention to the direction for which one wants to assess risk. Let be a random vector which takes values in . The vector is regularly varying if there exists a sequence and a limit measure for sets in such that , as , where denotes vague convergence in , the space of nonnegative Radon measures on (Resnick,, 2007, §6). It can be shown that , where is some slowly varying function and is called the tail index of . We denote a regularly varying vector with tail index . The measure has the scaling property for any set and any .

The scaling property implies that can be more easily understood for sets defined by polar, rather than Cartesian, coordinates. Given any norm, define the unit ball . Let for some , and some Borel set . Then , where is a measure, termed the angular measure, on . Consequently, . The scale of is related to and or . Consider replacing the sequence by for some . For any and such that is a continuity set of , where and . We will acknowledge this scaling relationship between , , and by saying that has limiting (angular) measure (respectively, ) when normalized by .

2 Inner product space via transformation

In this section, we describe a framework to produce an inner product space on a target open set, yielding, among other things, the notion of basis. We later use this framework to produce a particular inner product space on the positive orthant whose operations will preserve regular variation. Let be a bijection from onto some open set , and let be its inverse. We refer to as the ‘transform’. Define as the set of -dimensional vectors whose elements are in . Let denote element-wise application of to the elements of , and other functions applied to vectors will similarly be applied element-wise. Define vector addition in as . For , define scalar multiplication of a vector in as . Define the additive identity in , , and define the additive inverse of any as . We show that meets the ten conditions required of a vector space in the supplemental materials.

Continuing to let and , we define a linear combination in the obvious way:

As is a -dimensional vector space, any set of vectors which are linearly independent in (i.e., if ) form a basis for .

Let be a matrix of real numbers. For , define matrix multiplication as , and note . If is the usual -dimensional identity matrix, then . Also note that if is , then .

As in , linear combinations can be written as matrix operations. However, because the constants and the vectors , the relationship changes slightly:

| (1) |

where is the matrix whose columns are .

For , define the scalar product . In the supplemental materials, we show that the four conditions of a scalar product are met. Define , and define two vectors to be orthogonal if , denoted . Vectors and their preimages share the same inner product value. Consequently, , and in if and only if in .

Consider nonsingular matrix , and think of as an operator defined by . We define the inverse operator to be a matrix such that , and note that the inverse operator coincides with the usual matrix inverse. Define an eigenvalue/eigenvector pair , of to be such that , and assume . If and are an eigenvalue/eigenvector pair in , then and is an eigenvalue/eigenvector pair in :

Further, assume that is symmetric positive-definite (i.e., for any ), and define a positive quadratic form in as . Note that

where . Thus, and its preimage share the same quadratic form with symmetric positive definite matrix . Consequently, relationships between the eigenvectors and eigenvalues of and bounds on the quadratic forms in carry over to yielding the following proposition, whose justification follows from linear algebra results in (Johnson and Wichern,, 2007, p. 80).

Proposition 1

Let and be the ordered eigenvalue/eigenvector pairs for in , and let . Then,

Further, the sequence of vectors where each is such that is maximized subject to , , is and .

In §3, we apply the ideas of this section with the specific transform defined as

This bijection, known as the softplus function in neural networks (Dugas et al.,, 2001), is continuous and infinitely differentiable. Its inverse is . Importantly for our purposes, ; that is, the transform and its inverse negligibly affect large values. For use in §3, extend such that , , and . As defined, , where and . The additive zero vector in is a vector of components .

3 Transformed-linear operations on multivariate regularly varying random vectors

We now consider ‘transformed-linear’ operations applied to regularly varying random vectors with the aforementioned specific transform . For regular variation to be preserved we need the following assumption on the lower tail of our random vectors: assume verifies

| (2) |

as . Condition (2) does not seem overly restrictive as goes to zero very rapidly, but it does preclude any of the marginals from having nonzero mass at 0. Standard regularly varying distributions such as the Pareto and the Fréchet meet this condition.

Propositions 2 and 3 below show that regular variation is preserved by the transformed linear operations. Proofs for all propositions are given in the appendix. Used to prove Propositions 2 and 3, Lemmas A1 and A2 require the definition of regular variation on , which we recall here and which is used in Section 5. is regularly varying in (denoted as ) if there exists such that in (Basrak et al.,, 2002; Resnick,, 2007, §6.5.5). Analogous to before, if for some set , then for some angular measure on . Notationally for , let applied componentwise.

Proposition 2

Let be independent, , and . Then , and

Proposition 3

Let be such that . Then for ,

Informally, the condition (2) is necessary because if had enough mass near and , could interfere with the regular variation in the upper tail.

One outcome of propositions 2 and 3 is a method for constructing a regular varying random vector by applying a matrix to a vector of independent regularly varying random variables.

Corollary 1

Let be a matrix where for all , and let be a vector of independent and identically distributed regularly varying random variables with such that , , and for any , . Then and when normalized by has angular measure , where is the Dirac mass function.

Different matrices can result in the same limiting angular measure. Let If but , .

The class of regularly varying random vectors produced by the construction method in Corollary 1 is similar to the family of random vectors defined by max-linear combinations of independent regularly varying random variables (e.g., Schlather and Tawn,, 2002; Fougères et al.,, 2013). Let be a matrix and let be a vector of independent and identically distributed regularly varying random variables as in Corollary 1. Constructing one can show that . If is max-stable, then is also max-stable. We choose to work within the framework of regular variation rather than max-stability, but given knowledge of the angular measure it is easy to determine the distribution of the max-stable random vector whose domain of attraction includes the regularly varying random vector. One difference between the two constructions is in their realizations. Large realizations of the max-linear combination tend to have angular components which correspond exactly to the discrete locations for which the angular measure has mass, whereas large realizations of the transformed-linear construction have angular components close but not equal to these discrete locations.

Similar to Fougères et al., (2013) who show that the class of max-linear combinations of independent Fréchet random variables is dense in the class of -dimensional multivariate extreme value distributions with Fréchet marginals, Proposition 4 below shows the class of angular measures arising from the construction method in Corollary 1 is dense in the class of possible angular measures. To construct the dense class one only needs to consider matrices with nonnegative elements, and the approximation to a continuous angular measure is improved by increasing the number of columns of .

Proposition 4

Given any angular measure , there exists a sequence of nonnegative matrices , , such that .

4 Tail pairwise dependence matrix

Inspired by statistical practice in non-extreme settings, we aim to summarize dependence of a regularly varying random vector via second-order properties of its angular measure. Henceforth, we restrict our attention to the case , and to employ the norm when making the radial/angular transformation.

Assume such that

| (3) |

and is a Radon measure on the unit ball . We have specified the normalizing sequence to be , thus pushing all scaling information into . If one begins with a random vector in , then a marginal transformation can be applied to achieve a random vector which meets the above conditions (Resnick,, 2007, Theorem 6.5).

Define a matrix of summary pairwise dependencies by letting

We refer to as the tail pairwise dependence matrix of , and corresponds to the extremal dependence measure, defined in the bivariate case by Larsson and Resnick, (2012).

It is straightforward to show that is positive semidefinite. Let . Let be a random vector such that for any set . Then , and , for . The inequality becomes strict if no element of is a linear combination of the others.

Like a covariance matrix, the diagonal elements of yield information about the scale of the elements of . Since ,

Thus, is equal to the square of the scale of , since if has scale 1 (defined as: ), then . Also since we use the norm, the sum of the diagonal elements is equal to the total mass of the angular measure as

Asymptotic independence (Sibuya,, 1960; Ledford and Tawn,, 1996) of the components and is equivalent to , which follows from the fact that if and only if .

Importantly, has a relationship to random vectors constructed according to Corollary 1. Let be a -dimensional random vector of independent random variables such that () and such that for any , . Let be a matrix with for all . Further, assume . The results of §3 give us that with angular measure on the unit ball of

and the total mass of is . The th element of is

since . Thus .

The tail pairwise dependence matrix has the additional property of being completely positive. A matrix is completely positive if there exists a nonnegative (not necessarily square) matrix such that .

Proposition 5

If has tail pairwise dependence matrix , there exists a , nonnegative matrix such that .

While Proposition 4 loosely says that a regularly varying random vector with any angular measure can be represented by an infinite linear combination of independent regularly varying random variables, Proposition 5 says that if one restricts attention to , this dependence structure can be represented by a finite linear combination.

As contains incomplete information, it is natural to ask how much information is lost by summarizing the tail dependence of only in terms of the bivariate metrics it contains. We investigated the extremal behavior of seven different five-dimensional random vectors which all share a common by calculating the measures of two different extremal sets. We determined the probabilities that each of these random vectors takes a value in these extremal sets were similar, and the coefficients of variation of these calculated measures were 0.14 and 0.20 (see supplementary materials).

5 Eigendecomposition and principal components

In a non-extreme setting, eigendecomposition of the covariance matrix can be motivated in two ways: (1) the eigenvectors form an orthonormal basis ordered in the sense of Proposition 1, and (2) the principal components defined from the eigendecomposition form an uncorrelated random vector of basis coefficients with decreasing variance. We investigate both below.

Let such that (3) holds with and the limiting and angular measures, and let be its tail pairwise dependence matrix. As is positive-semidefinite, we can perform the standard eigendecomposition to obtain , where is the diagonal matrix with elements , is a unitary matrix and is an eigenvalue/eigenvector pair of for . Without loss of generality, we assume that none of the vectors is composed of all nonpositive elements. The columns of form an orthonormal basis for , and form an orthonormal basis for . This basis is ordered and is most efficient in the sense of Proposition 1 and quadratic forms induced by . Properties of matrix trace yield

If we assume that for any , , we can define

| (4) |

We refer to as the extremal principal components of . Lemma A4 in the appendix implies . Reversing (4) and using (1), we obtain an implicit definition for :

| (5) |

Thus the elements of are the stochastic basis coefficients when is decomposed into the basis .

To fully express the regular variation properties of would require explicit knowledge of . However, we can summarize the second-order properties of similar to before. Define

where , and is the angular measure of . Proposition 6 below shows that these extreme principal components have analogous properties to their non-extreme counterparts.

Proposition 6

for all , and for .

The eigenvalues relate to the scale of the magnitude of the elements of as for ,

Unlike for , the fact that does not imply that elements and are asymptotically independent. Instead it implies

| (6) |

6 Completely positive decomposition

The eigendecomposition of can be used as an exploratory tool for tail dependence, but it does not provide a method for constructing random vectors such that . Because contains negative entries, . However, given that there exists a nonnegative matrix such that , if one can find such a matrix, one can construct as in §4.

Berman et al., (2015) provides an overview of current knowledge and the status of several open problems concerning completely positive matrices. One open problem is finding the cp-rank; that is, the minimum number of columns such that there exists a matrix satisfying . It is known for -dimensional completely positive matrices that the cp-rank is less than (Barioli and Berman,, 2003). Thus the factorized matrix might be quite large. Ding et al., (2005) and Groetzner and Dür, (2016) describe algorithms to perform the factorization of to obtain . These algorithms are able to factorize matrices of moderate dimension , which is sizable for extremes studies. Typically, one can find multiple completely positive factorizations.

7 Applications

7.1 Estimation of

To apply to data, we must estimate . Our estimator replaces the true angular measure with an empirical estimate. Let () be independent and identically distributed vectors of observations from a random vector whose distribution satisfies (3), let , and . We define

| (7) |

where is some high threshold for the radial components, , , and is an estimate of . The estimator in (7) is the same as that given by Larsson and Resnick, (2012) in the bivariate case. Because we preprocess the data to have a common unit scale in the two applications below, and does not need to be estimated. When the data are not preprocessed to have a common scale an empirical estimator is . For principal component analysis, preprocessing the data to have unit scale is analogous to performing the eigendecomposition on the correlation rather than the covariance matrix in the non-extreme setting.

As where is the matrix whose rows are the vectors for which , the estimate is positive semidefinite and completely positive. The observed matrix provides a perhaps inefficient completely positive factorization of : . In applications we will find a completely positive factorization with fewer columns thereby reducing the dimension compared to the inefficient factorization. In addition to the two examples below, we perform a simulation study which shows that eigenvectors of retain the interpretable dependence information of the eigenvectors of . Furthermore, eigenvalues of have similar behavior to eigenvalues of estimated covariance matrices (see supplementary materials).

7.2 Extreme precipitation in Switzerland

We analyze precipitation measurements from stations located near Zürich, Switzerland, obtained from MétéoSuisse. Measurements are daily precipitation amounts (in mm) for June, July, and August for the years 1962–2012, yielding observations. The same data were analyzed by Thibaud and Opitz, (2015) and were found to be asymptotically dependent.

The data appear to be heavy-tailed (location-wise estimates for have a median of ); however, our framework requires that . Since extremal dependence is often described assuming conditions on the univariate marginals, it is common practice to incorporate marginal transformations within an extreme value analysis (Resnick,, 2007, §§6.5.3, 9.2.3). Letting be the random vector representing the precipitation measurements on day , a marginal transformation can be applied so that has the desired marginal properties given in (3).

We perform a nonparametric marginal transformation. We define , so that . With this transformation, the scale of is 1 for . We employ a linearly-interpolated empirical cumulative distribution function for . We let which corresponds to the empirical quantile, yielding large observations to estimate .

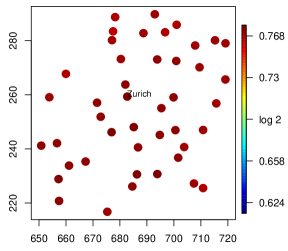

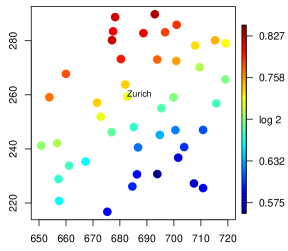

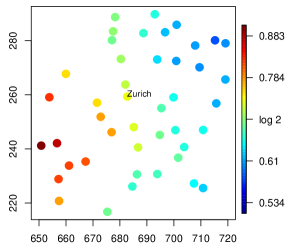

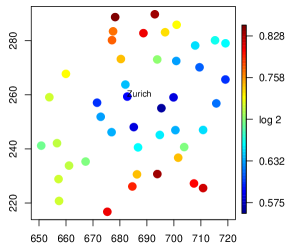

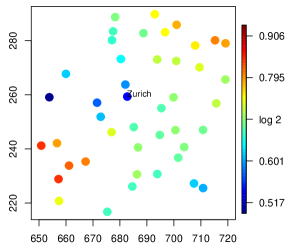

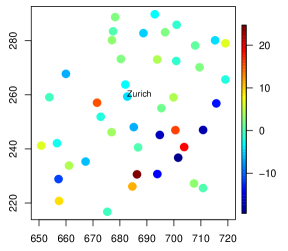

We perform the eigendecomposition to find . Figure 1 shows , the first five eigenvectors of in , plotted according to each station’s location. As the zero element of is , we will refer to values less than as “negative”. Although our analysis does not use location information, the leading eigenvectors clearly large-scale spatial behavior whose resolution increases with order. The first eigenvector has values ranging only from to , implying that the leading eigenvector accounts for the overall magnitude of the precipitation event. The second and third eigenvectors show basically linear trends; the second eigenvector decreases from positive values in the northwest to negative values in the southeast, and the third has decreasing values southwest to northeast. The fourth eigenvector shows behavior which is roughly quadratic, with the lowest values in the center of the region and higher values in the north and south, and, to a lesser extent, west. The fifth eigenvector shows saddle-like behavior with moderate values in the center, low values to the northwest and southeast, and high values to the southwest and northeast.

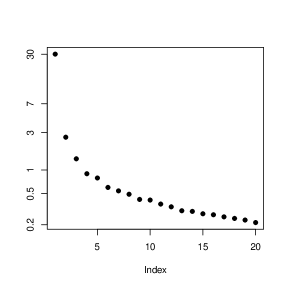

Also shown in Figure 1 is a scree plot of the eigenvalues. Because of preprocessing . The first five eigenvalues are , , , , , and the scree plot shows that the magnitudes of the eigenvalues become quite small after the first few values.

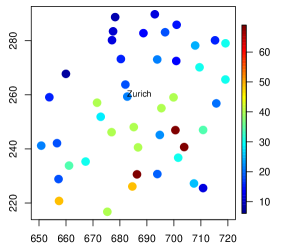

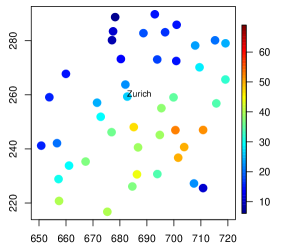

We find the sample principal components by letting . Figure 2 illustrates a partial basis reconstruction of an event. The left panel displays the transformed observations from the day with the third-largest value of in our record. For reference, and , so values at all locations on this day are large. Observations from this day are generally increasing from the northwest to the southeast, until one reaches the extreme southeast corner of the study region. Letting denote this particular day, we could represent exactly as a linear combination of the basis

| (8) |

from (1). The center panel of Figure 2 shows (8) truncated after the first ten terms in the transformed linear combination. We see that the general nature of the event is largely reconstructed from these leading basis vectors, with the increase from northwest to southeast, and the lower values in the extreme southeast corner. As expected, some of the fine-scale behavior is not reproduced using only the leading ten basis vectors, as is shown in the difference plot in the right panel. It is also interesting to look at the observed principal components . The large value of the first principal component when paired with gives large values to all locations. The large negative value of the second principal component when paired with the largely contributes the northwest to southeast increase shown in the reconstruction.

We obtain a completely positive factorization of using the method of Groetzner and Dür, (2016). We find with only columns such that . We define where are independent and (). Although shares the same tail pairwise dependence matrix as the one estimated for , they do not share the same angular measure.

Because the angular measure of is discrete, probabilities of extreme events (i.e. for some set of interest ) can be calculated easily. We define an initial risk region on the scale of the original data: , and then calculate where . Letting be the elements of , , and our probability estimate is . An empirical estimate of is 2/4691 = . Uncertainty in the probability estimate arises from two sources: uncertainty in the estimate and the non-uniqueness of the completely-positive factorization. A bootstrap based confidence interval could include both sources of uncertainty, but this is infeasible as there are not readily-available methods for repeatedly obtaining completely-positive factorizations for . Interestingly, using the with 235 columns arising from the inefficient factorization (see §7.1) yields an estimate of .

7.3 Extreme losses for financial data

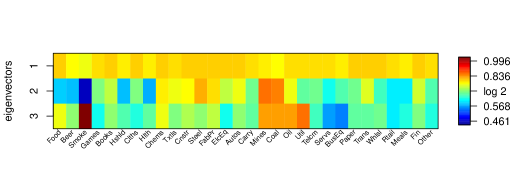

Our data are the ‘value-averaged’ daily returns of 30 industry portfolios compiled and posted as part of the Kenneth French Data Library. We analyze data for 1950–2015, yielding observations. We transform the data to perform our analysis. Let denote the vector of returns for day . Then, let , negating the returns since we are interested in extreme losses, setting negative values (gains) to zero, and then applying our transform to bound the values away from thereby meeting the lower-tail requirements for . Importantly, this transformation leaves the magnitudes of the large losses essentially unchanged. We use the Hill estimator (Hill,, 1975) at the empirical quantile to obtain estimates for each marginal. The estimates range from to with the heaviest tails belonging to the categories Finance (Fin), Steel, Textiles (Txtls), Coal, and Telecom (Telcm). Estimated scales of the variables also varied widely and eigenvectors of the tail pairwise dependence matrix of the unscaled data were dominated by the variable scales. Consequently, we let () where is the th component’s scale estimate, allowing us to assume a tail index of and a scale of 1 for all marginals. is then estimated as before, employing data whose radial components exceed the 0.99 quantile.

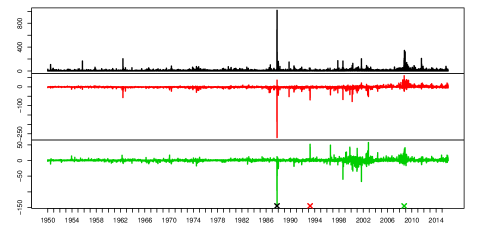

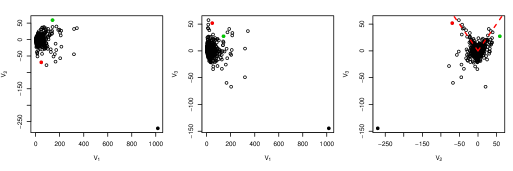

We perform an eigendecomposition of and is 0.680, 0.052, and 0.036 for . The top panel of Figure 3 shows the values of the first three eigenvectors , values less than are again referred to as “negative”. Eigenvector gives an overall magnitude, contrasts “heavy” and “non-heavy” industries with Mines, Coal, and Steel having the largest positive values versus Smoke, Food, Beer, Consumer Goods (Hshld), and Healthcare (Hlth) with the largest negative values. The third eigenvector contrasts Smoke, and several heavy industries (Mines, Coal, Oil, and Utilities (Util)) versus “office/executive” sectors Services (Servs) and Business Equipment (BusEq). The middle panel shows the time series of the first three principal components (); note the different scales for the time series plots. The time series clearly shows “Black Monday”, October 19, 1987, marked with a black ‘X’. The large positive value of the first coefficient arises from the large losses across the market, while the large negative value of the second coefficient helps to mitigate this affect for Mines and Coal. The median of log-returns across sectors on Black Monday was , but Mines and Coal were not as severely affected with log returns of and respectively. Also, it is interesting that the third coefficient experiences volatility in 1999–2002 time period and the first and second do not. This likely reflects that this time period corresponding to the American tech bubble was troublesome for Business Equipment and Services whose definitions include many computer-related items. The bottom panel shows the pairwise scatterplots of the first three principal components. Clearly these principal components are not asymptotically independent as large values do not occur on the axes. The right plot of principal component three versus two shows extreme behavior in two directions: and which are marked. The two points indicated in red and green are the points with the largest values (other than Black Monday which is marked in black) when projected in these directions. The red point corresponds to April 2, 1993, known as “Marlboro Friday”, and the green point corresponds to October 2, 2008 which occurred during the financial crisis of 2008, and these dates are indicated in the time series plots. The change in sign of the second principal component implies the market behaves very differently in these two directions. Marlboro Friday had large losses across the market (median log-return of ), particularly large losses for Food and Smoke ( and respectively), but moderate gains for Mines and Coal ( and ). October 2, 2008 shows very different behavior with a median log return of across all sectors, but particularly big losses for Mines and Coal ( and respectively). The fact that there are a number of large values in these directions indicates this type of behavior is not unique to just these two days.

8 Discussion

This work novelly applies linear algebra constructs within the context of extremes, achieved by defining a vector space for the positive orthant via a transform . Importantly, the vector space yields the idea of basis for the space in which our regularly varying random vectors take values, and the specific transform preserves regular variation.

Extremal dependence is summarized by the tail pairwise dependence matrix . Although we are not the first to summarize tail dependence via a collection of summary metrics (e.g., Strokorb and Schlather,, 2015), we believe the similarities between the tail pairwise dependence matrix and the covariance matrix are appealing. The eigendecomposition of allows interpretation of dependence via the eigenbasis, very similar to traditional principal component analysis. The fact that the eigendecomposition does not lead to a construction method for a random vector with the desired tail pairwise dependence matrix is overcome by the completely positive decomposition.

Importantly, we do not attempt to characterize the dimensional angular measure, as we think this is very difficult when is large. Much of traditional multivariate analysis is based on second-moment characterizations, and it is often found that having all pairwise summaries provides adequate information for the dependence to be understood, for models to be constructed and used to estimate quantities of interest, and ultimately, for decisions to be made.

Beyond the decompositions described in this work, the connection between extremes and linear algebra warrants further investigation. Given the prevalence of linear manipulations in multivariate analysis, spatial statistics, and time series, these linear algebra connections could lead to further models and methodological development for extremes.

Acknowledgment

D. Cooley and E. Thibaud were both partially supported by NSF DMS-1243102. We thank Patrick Groetzner and Mirjam Dür for their help with completely positive matrix factorizations, and Piotr Kokoszka for helpful discussion. The financial data were obtained from http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html. We thank the editors and reviewers for helpful comments.

Appendix A Appendix

A.1 Lemmas

Before considering ‘transformed-linear’ operations applied to regularly varying random vectors, the two following lemmas show the transform and its inverse preserve regular variation between and .

Lemma 1

Let such that and condition (2) holds. Then , and

| (9) |

Intuitively, because negligibly affects large positive values, if , then . The lower-tail condition (2) on the marginals of implies that if then , i.e., has no mass outside the nonnegative orthant.

Lemma 2

Assume , . Then , and

where applied componentwise.

Intuitively Lemma A2 says that the mass of outside the nonnegative orthant is projected on the boundary of when applying the transform to . If where meets the lower-tail condition (2) then only has mass on , and consequently, for any , .

Before proving Lemma A1, we first prove the convergence in (9) for rectangular sets. Being a componentwise function, and its inverse apply nicely to rectangular sets.

Lemma 3

Assume is as in Lemma A1. Let be a rectangle in where for all . Then

Remark: The reason Lemma A3 excludes rectangles with vertices or is that these rectangles would have edges at after applying the transform, and therefore would not scale radially as increases, and thus their limiting measure is unknown.

Proof of Lemma A1: Our proof of regular variation for is similar to the proof of Lemma 6.1 in Resnick, (2007) or the proof of Basrak et al., (2002, §2): first we show that the sequence of measures is tight in , and second we show that all subsequential limits agree on a -system that generates the Borel -algebra.

First, any bounded Borel set is contained in the union of a finite number of rectangles in and with no edges on the axes, so that

by Lemma A3. Hence the sequence of measure is tight in . Second, the convergence in Lemma A3 occurs on the -system of rectangles with no edges on the axis and thus occurs on the -algebra generated by these rectangles, which coincides with the Borel algebra on (rectangles with no edges on the axes are sufficient to construct any open rectangle of using countable union).

A.2 Proofs of propositions and corollaries

Proof of Proposition 2: From Lemma A1 the random vectors with respective measures and when normalized by . Proposition 7.4 of Resnick, (2007), easily extended from to , implies that , and has measure when normalized by . From Lemma A2, , and when normalized by , has measure . Further, noting that , and thus only have mass on , for any , .

Proof of Proposition 3: First consider . For continuity set ,

| (10) |

by Lemma A1. Hence , and we define to be its limiting measure when normalized by . Let , and let . By Lemma A2 and (10),

If , , which implies the first part of the proposition. If , , as , which implies the second part.

We give the following corollary and its proof prior to proving Corollary 1.

Corollary 2

Let where . Let be a regularly varying random variable with index and assume that is chosen such that , . Also assume for any . Then and when normalized by has angular measure .

Proof of Corollary A2: By Resnick, (2007, Lemma 6.1), proof of convergence for sets for which are continuity points of the limit is sufficient for convergence on . Note,

Note , thus .

Proof of Corollary 1: As is independent of for , Corollary 1 follows from Corollary A2 and Proposition 2.

The proof of Proposition 4 is in the supplementary materials as it is analogous to the proof found in Fougères et al., (2013).

Proof of Proposition 5: By Proposition 4, there exists a sequence , , of nonnegative matrices such that . For any fixed , let , and note that is completely positive. As the set of completely positive matrices is a closed convex cone (Berman and Shaked-Monderer,, 2003, Theorem 2.2), then is completely positive, and thus there exists a finite and a matrix such that .

Lemma 4

Let be such that . Suppose the matrix is invertible. Then .

Proof of Lemma A4: For any where is a continuity set of ,

| (11) |

where the last equality follows from the fact that only has mass on the positive orthant. Hence, .

Proof of Proposition 6:

References

- Barioli and Berman, (2003) Barioli, F. and Berman, A. (2003). The maximal cp-rank of rank k completely positive matrices. Linear Algebra and its Applications, 363:17–33.

- Basrak et al., (2002) Basrak, B., Davis, R. A., and Mikosch, T. (2002). A Characterization of Multivariate Regular Variation. The Annals of Applied Probability, 12:908–920.

- Berman et al., (2015) Berman, A., Dür, M., and Shaked-Monderer, N. (2015). Open problems in the theory of completely positive and copositive matrices. Electronic Journal of Linear Algebra, 29:46–58.

- Berman and Shaked-Monderer, (2003) Berman, A. and Shaked-Monderer, N. (2003). Completely Positive Matrices. World Scientific.

- Boldi and Davison, (2007) Boldi, M.-O. and Davison, A. C. (2007). A mixture model for multivariate extremes. Journal of the Royal Statistical Society, Series B, 69:217–229.

- Chautru, (2015) Chautru, E. (2015). Dimension reduction in multivariate extreme value analysis. Electronic Journal of Statistics, 9:383–418.

- Ding et al., (2005) Ding, C., He, X., and Simon, H. D. (2005). On the equivalence of nonnegative matrix factorization and spectral clustering. In Proceedings of the 2005 SIAM International Conference on Data Mining.

- Dugas et al., (2001) Dugas, C., Bengio, Y., Bélisle, F., Nadeau, C., and Garcia, R. (2001). Incorporating second-order functional knowledge for better option pricing. In Advances in neural information processing systems, pages 472–478.

- Fougères et al., (2013) Fougères, A.-L., Mercadier, C., and Nolan, J. P. (2013). Dense classes of multivariate extreme value distributions. Journal of Multivariate Analysis, 116:109–129.

- Groetzner and Dür, (2016) Groetzner, P. and Dür, M. (2016). Finding decompositions of completely positive matrices using orthogonal transformations. In preparation.

- Hill, (1975) Hill, B. M. (1975). A Simple General Approach to Inference About the Tail of a Distribution. The Annals of Statistics, 3:1163–1174.

- Hüsler and Reiss, (1989) Hüsler, J. and Reiss, R.-D. (1989). Maxima of normal random vectors: between independence and complete dependence. Statistics & Probability Letters, 7(4):283–286.

- Johnson and Wichern, (2007) Johnson, R. A. and Wichern, D. W. (2007). Applied Multivariate Statistical Analysis. Pearson/Prentice Hall, New Jersey, 6th edition.

- Larsson and Resnick, (2012) Larsson, M. and Resnick, S. I. (2012). Extremal dependence measure and extremogram: the regularly varying case. Extremes, 15:231–256.

- Ledford and Tawn, (1996) Ledford, A. W. and Tawn, J. A. (1996). Statistics for near independence in multivariate extreme values. Biometrika, 83:169–187.

- Opitz, (2013) Opitz, T. (2013). Extremal t processes: Elliptical domain of attraction and a spectral representation. Journal of Multivariate Analysis, 122:409–413.

- Resnick, (2007) Resnick, S. I. (2007). Heavy-Tail Phenomena: Probabilistic and Statistical Modeling. Springer Series in Operations Research and Financial Engineering. Springer, New York.

- Schlather and Tawn, (2002) Schlather, M. and Tawn, J. A. (2002). Inequalities for the Extremal Coefficients of Multivariate Extreme Value Distributions. Extremes, 5:87–102.

- Sibuya, (1960) Sibuya, M. (1960). Bivariate extreme statistics, I. Ann. Inst. Statist. Math., 11:195–210.

- Strokorb and Schlather, (2015) Strokorb, K. and Schlather, M. (2015). An exceptional max-stable process fully parametrized by its extremal coefficients. Bernoulli, 21:276–302.

- Thibaud and Opitz, (2015) Thibaud, E. and Opitz, T. (2015). Efficient inference and simulation for elliptical pareto processes. Biometrika, 102:855–870.