To appear in The Mathematical Scientist (Applied Probability Trust), 1st issue of 2017

Should we opt for the Black Friday discounted

price

or wait until the Boxing Day?

Jiang Wu1, 2 and Ričardas Zitikis2

1School of Economics, Central University of Finance and Economics, Beijing 100081, P.R. China. E-mail: jwu447@uwo.ca

2Department of Statistical and Actuarial Sciences, University of Western Ontario, London, Ontario N6A 5B7, Canada. E-mail: zitikis@stats.uwo.ca

Abstract. We derive an optimal strategy for minimizing the expected loss in two-period economy when a pivotal decision needs to be made during the first time-period and cannot be subsequently reversed. Our interest in the problem has been motivated by the classical shopper’s dilemma during the Black Friday promotion period, and our solution crucially relies on the pioneering work of McDonnell and Abbott on the two-envelope paradox.

Key words and phrases: decision theory; two-period economy; price discrimination; strategy; game theory; conditional probability; statistical modelling

1 Motivation

When needing a laptop in the Fall of 2015, one of the authors of this article was looking for a good on-line deal. Benefiting from the advantages of on-line shopping, he acquired considerable information on the Lenovo T540 laptop price. Two forthcoming time periods were of immediate interest: the Black Friday promotion from 27 November to 3 December 2015, and the Boxing Day promotion from 26 December 2015 to 3 January 2016.

Obviously, it was prudent to wait until the Black Friday promotion period, which revealed the discounted price of 1,431.01 Canadian dollars for the laptop, but it was not obvious at that moment whether he wanted to buy the laptop at that price or wait until the Boxing Day promotion. (The price of Lenovo T540 laptop during the Boxing Day promotion period turned out to be 1,461.60 Canadian dollars, which was not, of course, known during the Black Friday promotion period.) Can there be a strategy for making good decisions during the Black Friday promotion period?

The present article aims at answering this question by deriving an optimal strategy that minimizes the expected buying price. The idea for tackling this problem stems from the pioneering work of McDonnell and Abbott (2009) on the two-envelope paradox, with further far-reaching considerations by McDonnell et al. (2011). It also relies on some of the techniques put forward by Egozcue et al. (2013) who have extended the aforementioned works beyond the two-envelope paradox. We next recall the paradox itself and in this way clarify its connection with our current problem. This will also provide useful hints on how we have resolved the problem and what challenges encountered.

Namely, there are two sealed and identically looking envelopes, with one containing twice more money than the other one. We randomly pick one envelope and open it. Let be the amount of money that we find. Should we keep the amount or swap the envelopes and have only what we find in the second envelope? The paradox is that if we swap, then with the probability we shall find either or amount of money, and this gives us the average , which is larger than that we have found in the first envelope. This argument suggests to always swap the envelopes.

For many years economists, engineers, mathematicians, statisticians, and others have worked on this paradox, with various competing and complementing solutions suggested. McDonnell and Abbott (2009) put the idea that the optimal strategy should be based on the information (i.e., the amount ) that we acquire after opening the first envelope, and then incorporating additional considerations in order to arrive at a threshold, say , that would delineate those values of that would suggest swapping, or not swapping, the envelopes. This pioneering and inspiring solution of the paradox by McDonnell and Abbott (2009), with further refinements by McDonnell et al. (2011), has been extensively discussed in the scientific and popular literature.

In the present paper we demonstrate how this solution can be adjusted and extended to solve other problems, spanning well beyond the two-envelope paradox. In particular, just like McDonnell and Abbott (2009), we also derive a threshold-based strategy for accepting or rejecting the price offered during the first time-period. Challenges naturally arise, including the arbitrariness of prices, which are not the aforementioned , or anymore. The need for incorporating elements of behavioural economics and rational decision-making arise. These and other considerations inevitably introduce additional mathematical and probabilistic challenges, which we shall discuss in great detail below, and within the context of the shopper’s dilemma noted earlier.

The rest of this paper is organized as follows. In Section 2, which contains our main results, we first lay out the necessary mathematical background and then derive two optimal strategies: one when there is no guessing of the second time-period price, and the other when such a guessing can take place. Section 3 concludes the main part of the paper with a brief overview of our main contributions. In technical Appendices A and B, we discuss price modeling and parameter specifications of practical relevance. Proofs of the main results are given in Appendix C.

2 Main results

We start out by carefully describing the decision-making process, and also introduce the necessary notation. First, the prospective buyer contacts a salesperson during the first time-period. To somewhat simplify the problem, we assume that there are two kinds of salespersons:

-

i)

those, call them , who tend to offer larger discounts and thus lower prices ;

-

ii)

others, say , who tend to offer smaller discounts and thus higher prices .

Both and are random variables. We denote their joint cumulative distribution function (cdf) by and assume that it is absolutely continuous, that is, has a density , which is a natural assumption in the current context.

Let denote the random variable that takes the values and depending on which (kind of) salesperson takes the prospective buyer’s call during the first time-period. Hence, when , then the price is , and when , then . Note that for the management and the salespersons, the actual prices might be pre-determined and thus known, but for the buyer they are unknown and thus treated as random variables and following some distributions, with an outcome of one of the random variables observed during the first time-period.

Once the prospective buyer learns the price during the first time-period (i.e., Black Friday), he has two options: to either accept the offer or reject it and then inevitably wait till the second time-period (i.e., Boxing Day). If the buyer thinks that the first time-period offer is good enough, he accepts it and the purchasing process ends, but if the buyer rejects the offer, then he has to wait until the second time-period and then inevitably accept whatever offer is made to him at that time, because he needs a laptop and the regular price is less attractive than any of the discounted ones.

Let denote the random variable that represents the prospective buyer’s decision during the first time-period: if the buyer accepts the first-period offer and if he rejects it. The aim of the present article is to offer an optimal strategy that minimizes the expected value of the buying price , which could be either or depending the the buyer’s decision during the first time-period.

It is natural to assume – unless the buyer possesses insider’s information but we do not consider this case in the paper – that the buyer does not know who, or , is making offers during the first time-period. Hence, the buyer’s decision to accept the price offered during the first time-period does not depend on who, or , makes the offer – it depends only on the price, or , being offered, where and . In rigorous probabilistic terms, this means that the probability is equal to for all possible outcomes of the prices and , and for every salesperson . We note in passing that the just noted probability will later define a certain strategy function (equation (C.10) in Appendix C) which will play a crucial role in deriving actionable strategies that we spell out in Theorems 2.1 and 2.2 below. One may rightly argue further and suggest that in the context of our motivating problem, the probability of the decision does not depend on the second price , and we shall indeed tackle this case most prominently (Theorem 2.1; also equation (C.17) in Appendix C)

Finally before formulating Theorem 2.1, we introduce yet another quantity, , which plays a pivotal role throughout the rest of the paper. Namely, conditionally on the prices and , let be the probability that the salesperson is in charge of making offers during the first time-period. Naturally, the company’s management knows who, or , is making offers during the first time-period, but the decision making process that we are concerned with is from the perspective of the buyer, who can only use her/his intuition or some educated arguments such as those offered by economic theories in order to guess who, or , could possibly be, and with what likelihood, in charge of making offers during the first time-period. Hence, or, in other words, for all possible outcomes and of the random prices and , respectively. We shall discuss the probability in great detail in Appendix B, including its modelling and accompanying economic considerations.

Theorem 2.1.

When the price of the first time-period is and there is no attempt to guess the possible price to be offered during the second time-period, then the strategy that minimizes the expected buying price is to accept the offer when and to reject it when , where the “no guessing strategy” function is

| (2.1) |

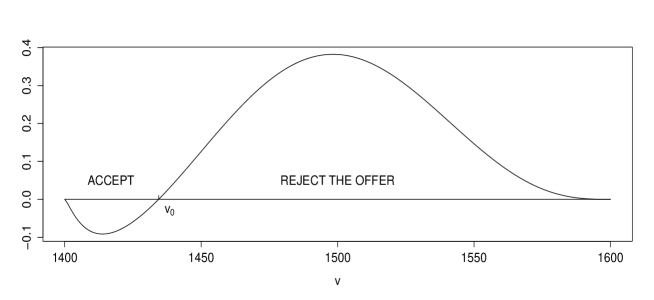

We have visualized the strategy function in Figure 2.1

with its properties, modelling, and specific parameter choices to be discussed next. To begin with, it is natural to think of the joint density as a continuous function with compact support , where is the reservation price from the supply side (i.e., computer technology company) and is the reservation price from the demand side (i.e., consumer). Hence, when or , or both, are outside the interval .

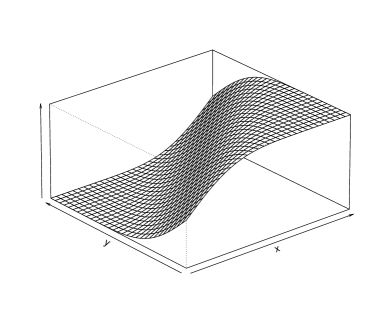

We also expect that under normal circumstances there should be a point such that (accept the offer) for all and (reject the offer) for all , with . We indeed see this pattern in our illustrative Figure 2.1, where and elsewhere when graphing in this paper we set the reservation prices to and Canadian dollars. For other specifications, including the underlying economic theories, modelling, and choices of and , we refer to Appendices A and B.

We note that under the aforementioned specifications, the point where the function crosses the horizontal axis is , which delineates the acceptance (to the left) and rejection (to the right) regions. It should also be noted that the inclusion of the point into the acceptance region is arbitrary: whenever is such that , we could very well flip a coin to decide whether to accept the offer or reject it and wait until the next promotion period. In general, the form of the function is of interest because its lows and highs tell us how confident we can be when making decisions (accept or reject) depending on the price and the likelihood of this price being offered.

Theorem 2.2.

When the price of the first time-period is and the guessed price to be offered during the second time-period is , then the strategy that minimizes the expected buying price is to accept the offer when and to reject it when , where the “guessing strategy” surface is

| (2.2) |

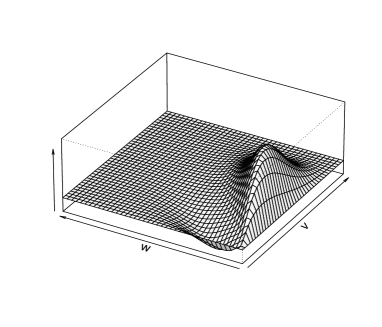

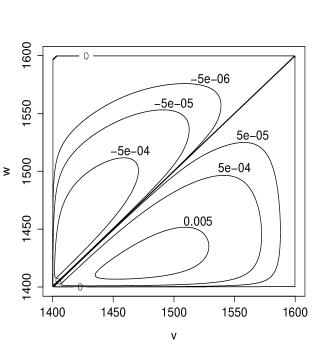

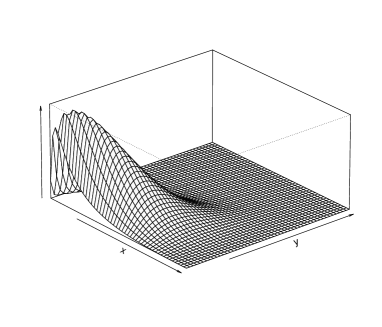

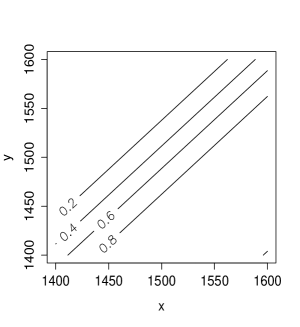

Note that when , which is natural. It is also natural to expect that (i.e., accept the first time-period price ) whenever , and (i.e., reject the first time-period price ) whenever . These features are of course clearly seen from formula (2.2) because the functions and are positive in the interior of their supports. We also see these features in Figure 2.2

where we have depicted the surface and its contours in the case of the functions and specified in Appendices A and B. The lows and highs of the surface tell us how confident we can be when making decisions (accept or reject) depending on the prices and , as well as on the likelihood of these prices being offered.

We finish this section with a brief discussion of possible models for , with further details provided in Appendix B below. Namely, upon recalling that is the probability that makes an offer during the first time-period, given that the offers of and are and respectively, it is natural to model as with some cdf such that . In Appendix B, for example, we shall use the beta cdf with identical shape parameters, in which case we have the equation for all and thus, in particular, the requirement . The following corollary to Theorems 2.1 and 2.2 deals with this special case.

Corollary 2.3.

Let for all and . Then the guessing-strategy surface is

and the no-guessing-strategy function is

The earlier drawn Figures 2.1 and 2.2 are based on Corollary 2.3 with practically relevant modelling of the functions and discussed in Appendices A and B. For the definition of , we refer to equation (A.3), and for that of to equation (B.1). Since closed-form formulas are unwieldy, we therefore employed numerical integration techniques, which proved to be fast and efficient and thus appealing from the practical point of view.

3 Conclusions

Decision making in two-period economy has been a topic of much interest for researchers in various fields, including economics, engineering, and finance. Mathematicians, philosophers, and statisticians have also contributed significantly to the area. In the present paper we have tackled this topic in the setup that concerns shoppers facing two price-discount periods and needing a strategy for making beneficial (for them) decisions. Guided by economic theories and rigorous probabilistic considerations, we have developed a practically sound model for making such decisions. In particular, we have shown how to derive, analyze, and use strategy functions, which not only delineate the acceptance and rejection regions for the first-come offers but also tell us how confident we can be when making such decisions.

Appendix A Background price models and the choice of

If the salespersons and were in total isolation, their offered prices would be outcomes of two independent random variables, which we denote by and , both taking values in the interval . It is natural to assume, for example, that and are beta distributed on with positive shape parameters and , respectively, that is,

and

where

is the range of possible prices. Given the earlier noted numerical values of and , we have . When graphing throughout this paper, we always set the parameter values to and .

The observable prices offered by and are, however, not and but those that have been influenced by, e.g., the company’s marketing team or management. This naturally leads us to the background price model, called the background risk model in the economic and insurance literature, which we choose to be multiplicative (cf., e.g., Franke et al. 2006, 2011; Asimit et al. 2016; and references therein).

Namely, suppose that is the (random) price that the company’s management would think appropriate, and which therefore influences the actual decisions of and . The multiplicative background model would suggest that the observable prices and are of the form and , but when defined in this way they are outside the natural price-range . To rectify the situation, we first standardize the prices , , and using the equations , , and , and then model the observable prices as and . Throughout the rest of this section, we assume that , and are independent and thus, in turn, their standardized versions , and are such as well. We shall soon find this assumption convenient; in fact, it is a natural assumption.

Let, for example, follow the beta distribution on the interval with some (positive) shape parameters . Then the pdf of is equal to

The marginal pdf’s of and are

| (A.1) |

and

| (A.2) |

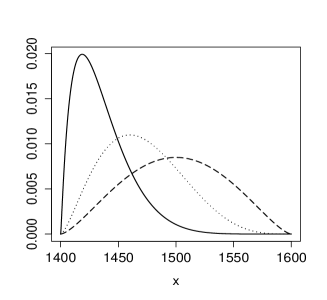

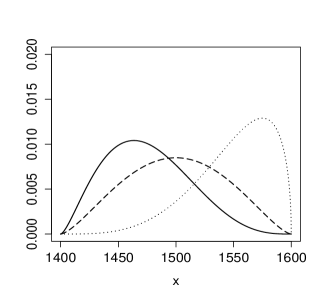

respectively, where . We have depicted the pdf’s in Figure A.1

using and the earlier noted parameter choices for and .

Note A.1.

Pdf’s (A.1) and (A.2) can be written in terms of the hypergeometric function as follows:

and an analogous expression holds for . These expressions follow from well-known formulas for the pdf of the product of two independent type-I beta random variables (Nagar and Zarrazola, 2004; also Nagar et al., 2014; and references therein).

Similarly to equations (A.1) and (A.2), we derive the joint pdf

| (A.3) |

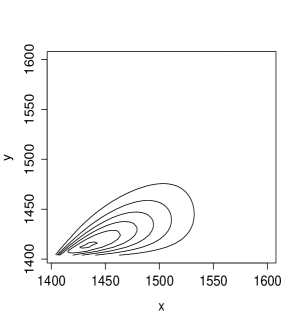

where . We have depicted this pdf in Figure A.2.

Appendix B Economic justification and modelling of

To begin with, we view our problem within the context of two-period (also known as two-stage) economy. Indeed, it is reasonable to assume that many consumers who buy laptops during the first time-period have stronger buying intentions than most of the consumers who buy laptops during the second time-period. That is, the demand curves during the two periods have different demand elasticities of price: during the first time-period, the demand elasticity of price is smaller than that during the second time-period. Considering this difference, the buyers during the two periods can be viewed as two separate markets with different demand curves and different demand elasticities, and monopolistic firms would tend to enforce the division of selling prices during the two periods.

This leads us to the topic of third-degree price discrimination (e.g., Schwartz, 1990; Aguirre et al., 2010), which in the monopolistic competitive market means that the same provider would charge different prices for similar goods or services in different consumer groups having different demand curves and demand elasticities, such as those who buy laptops during the first time-period and those who buy during the second period. In general, product differentiation is one of the key factors why firms have some degree of control over the prices, and the more successful a firm is at differentiating its products from other firms selling similar products, the more monopoly power the firm has. Product differences arise due to quality, functional features, design, and so on, and so there is imperfect substitution between products even when they are in the same category (e.g., Krugman, 1980; Head and Ries, 2001).

Hence, in the case of our problem concerning laptops, there is arguably a tendency to offer higher prices during the first time-period because the demand curve in the first period is a relatively inelastic demand curve, due to stronger buying intention. Hence, it is natural that firms would take advantage of this buying intention and offer higher prices during the first time-period. Consequently, it would seem that the higher the price is offered by , the higher the probability that the consumer will receive an offer from during the first time-period. The higher the laptop price is offered by , the lower the probability that an offer will come from during the first time-period. When and offer laptops at the same or similar price, then the probability of getting an offer from would be more or less the same as the probability of getting an offer from . In view of these arguments, the following properties seem natural:

-

1)

is non-decreasing in , for every fixed ;

-

2)

is non-increasing in , for every fixed ;

-

3)

whenever .

We next suggest an example of by setting it to be , where can be any cdf such that . For example, let be the beta cdf on the interval with and equal shape parameters, say . That is,

| (B.1) |

depicted in Figure B.1 with the parameter , which we always use when graphing.

Appendix C Proofs of Theorems 2.1 and 2.2

Our goal is to derive a strategy that leads to the minimal expected value of the buying price , which could be either or depending on the outcomes of the random variables and . We start with the equation

| (C.1) |

and then work with the conditional expectation inside the integral. Since the prices are non-negative, all the integrals throughout the proofs are from to .

Given and , the random variable can take only the values or . Consequently, we have the equation

| (C.2) |

We next calculate the two probabilities on the right-hand of equation (C.2) based on which of the two salespersons, or , is making offers during the first time-period, and also on the consumer behavior during this period, who can either accept or reject the first-come offer.

To begin with, we employ the random variable and have

| (C.3) |

We next tackle the four probabilities on the right-hand side of equation (C), starting with the first probability.

Using the random variable , we have the equation

| (C.4) |

The first probability on the right-hand side of equation (C) is equal to , and the third probability is equal to . Hence, equation (C) simplifies to

| (C.5) |

Similarly, we obtain the expression

| (C.6) |

for the third probability on the right-hand side of equation (C). Using equations (C.5) and (C.6) on the right-hand of equation (C), we have

| (C.7) |

where () is the salesperson who offers prices during the second time-period.

We now recall the assumption preceding Theorem 2.1 that tells us that the decision to accept or reject the first-come offer does not depend on who makes the offer – the decision depends only on the size of the offer. In probabilistic language, this means the equation

that must hold for every decision (i.e., accept or reject) and for every salesperson , where denotes the salesperson who makes the offer during the second time-period. Hence, we have the equations

| (C.8) |

and

| (C.9) |

Note C.1.

Given the description of our problem, we might naturally think that the decision variable is independent of the hypothetical/speculative future value of , and thus the right-hand sides of equations (C.8) and (C.9) simplify by leaving out the second conditions associated with . We shall indeed consider this situation later, but at the moment we admit the possibility (cf. Theorem 2.2) that some clues about possible price offerings during the second time-period might be available to the buyer.

With the notation

| (C.10) |

the right-hand side of equation (C.8) is equal to and the right-hand side of equation (C.9) is equal to . Consequently, equation (C) turns into the following one

| (C.11) |

This is a desired expression for the first probability on the right-hand side of equation (C.2). As to the second probability, analogous considerations lead to the equations

| (C.12) |

Applying equations (C.11) and (C) on the right-hand side of equation (C.2), we have

which becomes

| (C.13) |

with the probability

whose meaning was discussed before the formulation of Theorem 2.1. We next rearrange the terms on the right-hand side of equation (C.13) by separating the strategy-free and strategy-dependent terms:

| (C.14) |

Combining equations (C.14) and (C.1), we obtain the decomposition

| (C.15) |

where the strategy-free term is

and the strategy-dependent term is

Rewriting the latter equation in terms of the joint density , and also slightly changing some notation, we arrive at the equation

| (C.16) |

where is defined by equation (2.2). Since is a probability and can therefore take values only in the unit interval , integral (C.16) achieves its minimal value when

This completes the proof of Theorem 2.2.

We next deal with the case (cf. Theorem 2.1) when the decision random variable is independent of and thus does not depend on the price offered during the second time-period. Hence, instead of , we now deal with the strategy function

| (C.17) |

Consequently, the above defined reduces to the integral

| (C.18) |

where is defined by equation (2.1). Integral (C.18) achieves its minimal value when

This completes the proof of Theorem 2.1.

Acknowledgements

We are indebted to the Editor and an anonymous referee for constructive criticism, queries, and suggestions that have greatly influenced our work on the revision. We are also grateful to Martín Egozcue for his much appreciated advice and generosity. The research of both authors has been supported by the grant “From Data to Integrated Risk Management and Smart Living: Mathematical Modelling, Statistical Inference, and Decision Making” (2016–2021) awarded to the second author by the Natural Sciences and Engineering Research Council of Canada.

References

- [1] Aguirre, I., Cowan, S. and Vickers, J. (2010). Monopoly price discrimination and demand curvature. American Economic Review, 100, 1601–1615.

- [2] Asimit, A. V., Vernic, R. and Zitikis, R. (2016). Background risk models and stepwise portfolio construction. Methodology and Computing in Applied Probability, 18, 805–827.

- [3] Egozcue, M., Fuentes García, L. and Zitikis, R. (2013). An optimal strategy for maximizing the expected real-estate selling price: accept or reject an offer? Journal of Statistical Theory and Practice, 7, 596–609.

- [4] Franke G., Schlesinger H. and Stapleton, R. C. (2006). Multiplicative background risk. Management Science, 52, 146–153.

- [5] Franke G., Schlesinger H. and Stapleton, R. C. (2011). Risk taking with additive and multiplicative background risks. Journal of Economic Theory, 146, 1547–1568.

- [6] Head, K. and Ries, J. (2001). Increasing returns versus national product differentiation as an explanation for the pattern of U.S.-Canada trade. American Economic Review, 91, 858–876.

- [7] Krugman, P. (1980). Scale economies, product differentiation, and the pattern of trade. American Economic Review, 70, 950–959.

- [8] McDonnell, M. D. and Abbott, D. (2009). Randomized switching in the two-envelope problem. Proceedings of the Royal Society A, 465, 3309–3322.

- [9] McDonnell, M. D., Grant, A. J., Land, I., Vellambi, B. N., Abbott, D. and Lever, K. (2011). Gain from the two-envelope problem via information asymmetry: on the suboptimality of randomized switching. Proceedings of the Royal Society A, 467, 2825–2851.

- [10] Nagar, D. K. and Zarrazola, E. (2004). Distributions of the product and the quotient of independent Kummer-beta variables. Scientiae Mathematicae Japonicae Online, e-2004, 45–53.

- [11] Nagar, D. K., Zarrazola, E. and Sánchez, L. E. (2014). Distribution of the product of independent extended beta variables. Applied Mathematical Sciences, 8, 8007–8019.

- [12] Schwartz, M. (1990). Third-degree price discrimination and output: generalizing a welfare result. American Economic Review, 80, 1259–1262.