Optimal Kernel Estimation of Spot Volatility of Stochastic Differential Equations

Abstract

Kernel Estimation is one of the most widely used estimation methods in non-parametric Statistics, having a wide-range of applications, including spot volatility estimation of stochastic processes. The selection of bandwidth and kernel function is of great importance, especially for the finite sample settings commonly encountered in econometric applications. In the context of spot volatility estimation, most of the proposed selection methods are either largely heuristic (e.g., cross-validation methods) or just formally stated without any feasible implementation (e.g., plug-in methods). In this work, an objective method of bandwidth and kernel selection is proposed, under some mild conditions on the volatility, which not only cover classical Brownian motion driven dynamics but also some processes driven by long-memory fractional Brownian motions or other Gaussian processes. Under such a unifying framework, we characterize the leading order terms of the Mean Squared Error, which are also ratified by central limit theorems for the estimation error. As a byproduct, an approximated optimal bandwidth is then obtained in closed form, which is shown to be asymptotically equivalent to the true optimal bandwidth. This result allows us to develop a feasible plug-in type bandwidth selection procedure, for which, as a sub-problem, we propose a new estimator of the volatility of volatility. The optimal selection of kernel function is also discussed. For Brownian Motion type volatilities, the optimal kernel function is proved to be the exponential kernel, which is also shown to have desirable computational properties. For fractional Brownian motion type volatilities, numerical results to compute the optimal kernel are devised and, for the deterministic volatility case, explicit optimal kernel functions of different orders are derived. Finally, simulation studies further confirm the good performance of the proposed methods.

Keywords: spot volatility estimation; kernel estimation; bandwidth selection; kernel function selection; vol vol estimation.

1 Introduction

It is no mystery that mathematical finance is greatly influenced by the Geometric Brownian Motion in the Black-Scholes-Merton’s option pricing model, which assumes a constant volatility parameter. The latter assumption has greatly been refuted by many empirical studies performed on both asset and option price data. Two nonexclusive general approaches, namely local and stochastic volatility, have been proposed in the literature to incorporate the stylized features of market volatilities. As a more general setting, the log price of an asset is usually assumed to follow the dynamics , where the volatility may vary through time, in either deterministic or stochastic ways. As a result, the estimation of the spot volatility has become an important and attractive problem, especially with the availability of high frequency data (HFD). Accurate estimation of the spot volatility not only helps market participants to better assess and characterize the behavior of the volatility through time but is also crucial in many problems of finance such as option pricing, portfolio selection, and risk management.

In this work, we revisit the problem of spot volatility estimation by kernel methods. Kernel estimation has a long history, starting with Rosenblatt et al. (1956) for density estimation. Extensive treatments of the method can be found in many textbooks, such as, Tsybakov (2008). The basic idea is to take a weighted average of the data where the weights are given by a kernel function that is appropriately scaled by a bandwidth parameter. The selection of the bandwidth and the kernel function are of great importance for the performance of the kernel estimator in a finite sample setting. Bandwidth selection methods have been thoroughly studied for density estimation and kernel regression. Broadly there are two general approaches: plug-in type and cross validation methods. We refer the reader to Hall (1983), Park and Marron (1990), Park and Turlach (1992), Cao et al. (1994), and Jones et al. (1996), for a more in depth introduction and comparison of these methods. The problem of kernel selection has also been considered by, for instance, Epanechnikov (1969) and van Eeden (1985).

In the context of spot volatility estimation, Foster and Nelson (1996) studied a rolling window estimator, which can be seeing as a kernel estimator with a compactly supported kernel function. They established the point-wise asymptotic normality of the estimator, and drew some conclusions about the optimal window length (i.e., bandwidth) and the optimal weight functions (kernel functions). However, in spite of the non-parametric model setting, the volatility is constrained to have a specific degree of smoothness (see Assumption A (vii) and (viii) therein). Also, the selection of bandwidth and kernel function is not studied systematically, since it presumed a strict relationship between the window’s length and the sample size (see Assumption D therein). Under such a relationship, they obtained the optimal kernel weights and separately established the optimal constant appearing in the formula for the window length, though only for the flat-weights case (i.e., a uniform kernel function). Fan and Wang (2008) also shows a point-wise asymptotic normality for a general kernel estimator under some conditions on the order of smoothness of the volatility processes (in the sense of convergence in probability) and a specific constraint on the rate of convergence of the bandwidth (Condition A4 therein), without any considerations on the optimal bandwidth selection problem. The latter assumption on the bandwidth allows them to neglect the error coming from approximating the spot volatility by a kernel weighted volatility (we refer the reader to Section 6 for details), but the achieved convergence rates of the kernel estimator are suboptimal. Also, the optimal selection of the kernel function was not considered111Indeed, with a suboptimal convergence rate, the selection of kernel function is generally not well defined. A recent paper in the same vein is Mancini et al. (2015), where the asymptotic normality of a more general class of spot volatility estimators, which includes kernel estimators, is studied without considering the kernel and bandwidth selection problems. Besides asymptotic normality, Kristensen (2010) also studied optimal bandwidth selection method, but under a strong path-wise smoothness condition, which has several practical and theoretical drawbacks. Indeed, even for simple volatility processes, it is not possible to verify the Hölder continuity needed for a central limit theorem with optimal rate. Furthermore, even though an ‘optimal’ bandwidth is deduced in closed form therein, this is not well-defined if we want to attain optimal convergence rates for the estimation error (see Remark 2.2 below for further details). Based on a heuristic argument, an alternative cross-validation method of bandwidth selection was also proposed by Kristensen (2010), but this algorithm has high computational complexity and the asymptotic properties were not studied.

Having discussed some previous work on the kernel estimation of spot volatility, we now mention some motivating factors and objectives of the present research. To begin with, we wish to adopt easily verifiable and general enough conditions to cover a wide range of frameworks without imposing strong constraints on the degree of smoothness of the volatility process. From a theoretical point of view, we also aim to provide a formal justification of the optimal convergence rate of the kernel estimator and to establish central limit theorems (CLT) and asymptotic estimates of the mean square errors with optimal rates. From the practical side, the two factors that affects the performance of the estimator, bandwidth and kernel function, ought to be optimized jointly, not separately, and meanwhile, the proposed method should remain feasible and sufficiently efficient to be implementable for HFD.

In this present work, we introduce a natural and relatively mild assumption on the volatility processes, which allows us to obtain feasible solutions to the optimal bandwidth and kernel selection problems. The assumption imposes a local homogeneous or scaling property for the covariance structure of the volatility process. This assumption covers a wide range of frameworks including deterministic differentiable volatility processes and volatilities driven by Brownian Motion, long-memory fractional Brownian Motion, and more generally, functions of suitable Gaussian processes. Under the referred assumption, we characterize the leading order terms of the Mean Squared Error (MSE). As a byproduct, we are then able to derive an approximated optimal bandwidth in closed form, which is shown to be asymptotically equivalent to the true optimal bandwidth. From this, the theoretical optimal convergence rate for the estimation error is rigorously identified. We then proceed to show that our optimal bandwidth formulas are feasible by proposing an iterated plug-in type algorithm for their implementation. An important intermediate step is to find an estimate of the volatility of volatility (vol vol), for which we propose a new estimator based on the two-time scale realized variance of Zhang et al. (2005). Consistency and convergence rate of our vol vol estimator are also established.

Equipped with an explicit formula for the asymptotically optimal MSE, we proceed to setup a well posed problem for optimal kernel selection. Concretely, for Brownian motion driven volatilities, we prove that the optimal kernel function is the exponential kernel: . Such a result formalizes and extends a previous result of Foster and Nelson (1994), where only kernels of bounded support were considered. We also show that, due to the nature of the data we are analyzing (namely, HFD), exponential kernel function enjoys outstanding computational advantages, as it reduces the time complexity for estimating the whole path of the volatility on all grid points from to . We also consider the volatility processes driven by the long-memory fractional Brownian motion and, in such a case, we provide numerical schemes to compute the optimal kernel function. For sufficiently smooth volatilities, we also consider higher order kernel functions and, by using calculus of variation with constraints, we obtain optimal kernel functions of different orders. The second order optimal kernel is exactly Epanechnikov (1969) kernel and, for higher order cases, we provide ways to calculate those optimal kernel functions.

To complement our asymptotic results based on MSE, asymptotic normality of the kernel estimators is also established for two broad types of volatility processes: Itô processes and continuous function of some Gaussian processes. In this way, our results cover volatility processes with flexible degrees of smoothness. The results are consistent with the leading order approximation of the MSE, so that CLT’s with the optimal convergence rate are obtained. By contrast, as mentioned above, the CLT’s of Fan and Wang (2008) and Kristensen (2010) have suboptimal convergence rate, while the analogous result of Foster and Nelson (1994) is limited to a specific smoothness order and strong constraints on the kernel function and bandwidth.

In the big picture, our results can be connected to several related topics in Statistical estimation of stochastic processes. For example, our approach can be combined with the Threshold Realized Power Variation (TPV) (cf. Mancini (2001, 2004), Figueroa-López and Nisen (2013)). Furthermore, market micro-structure noise can also be included and methods like two-time scale (cf. Zhang et al. (2005)), multi-time scale (cf. Zhang (2006)) and kernel methods (cf. Barndorff et al. (2004)) could potentially be combined with our kernel-based spot volatility estimators, though this problem is out of the scope of the present work.

The rest of the paper is organized as follows. In Section 2, we introduce the kernel estimator and our assumptions, and verify that common volatility processes satisfy our assumptions. In Section 3, we deduce the leading order approximation of the MSE of the kernel estimator and solve the optimal bandwidth selection problem. Then, in Section 4, we deal with the optimal kernel function selection problem for different types of volatility processes. A feasible implementation approach of the optimal bandwidth is discussed in Section 5, where we also introduce the TSRVV estimator of vol vol. Central Limit Theorems of the kernel estimator are discussed in section 6. Finally in Section 7, we perform Monte Carlo studies. Some technical proofs are deferred to appendices.

2 Kernel Estimators and Assumptions

In this section, we first introduce the classical kernel estimator for the spot volatility. We then discuss some needed smoothness conditions on the volatility processes and verify that most common volatility processes used in the literature indeed satisfy our assumptions. Finally, we discuss some regularity conditions on the kernel function and state some needed technical lemmas.

2.1 Framework and Estimators

Throughout the paper, we will consider the following dynamic for the log price of an asset:

| (1) |

where all stochastic processes (, etc.) are defined on a complete filtered probability space and where is a class of probability measures, defined on and indexed by . We also assume that and are adapted to the filtration and is a standard Brownian Motion (BM) adapted to . We suppose throughout the paper that we observe the log price process at the times , . We will use to denote the increments of log prices and to denote the time increments. From standard theory of stochastic analysis, the integrated volatility has a classical estimator, the Realized Quadratic Variation or Variance, which is defined as:

| (2) |

Above, is the quadratic variation or integrated variance process. In some literature, is also sometimes called the integrated volatility of the process. A natural way of turning the integrated variance estimator into a spot volatility estimator is to take a weighted average of the squared increments. Throughout, we consider the estimation of , for a fixed time , and we use a kernel function as weights so that more weights are given to points closer to . Concretely, the Kernel weighted spot variance (c.f. [8] and [15]) is defined as

| (3) |

where is the kernel function such that and we denote , where is the so-called bandwidth. Some basic analysis shows us that as , under some mild regularity conditions such as continuity. By replacing with , we then elucidate the Kernel weighted realized volatility estimator:

| (4) |

At the first glance, we may expect that, similarly to (3), , as . However, since we are facing a finite sample of log prices, if we simply set , the behaviour of is irregular. Therefore, in order to construct a consistent kernel estimator of the spot volatility, the bandwidth has to be selected carefully.

As discussed in the introduction, the literature on bandwidth and kernel selection methods for the spot volatility estimator (4) is rather scarce. [8] does not shed any light on this problem, while the conditions proposed by [15] to address this problem are hard to be verified and do not covered most of the models proposed in the literature (see Remark 2.2 below for further details). In this work, we go further with better crafted conditions that are satisfied by most common volatility processes while enabling us to obtain explicit expressions for the optimal bandwidth and the optimal kernel function.

Let us close by introducing some notations that will be used throughout this paper. We will mainly consider limits when and . Without ambiguity and for brevity, we will use the simplified notations: , etc. However, when we encounter , we will always use to denote the kernel function itself and never drop the subscript of .

2.2 Assumptions on the Volatility Process

In this section, we give the required assumptions on the volatility process that allow us to examine the rate of convergence of the kernel estimator defined in (4). Our first assumption is a non-leverage assumption. This simplifying assumption will make the problem more tractable and is widely used in the literature (see, e.g., [15]).

Assumption 1.

is independent of .

Another assumption that we need later is the boundedness of some moments of and .

Assumption 2.

There exists such that , for all .

Remark 2.1.

Note that this assumption implies , , and , for all . We will use the notation later.

Since we aim to study the problem of minimizing the Mean Squared Error of the estimator, we should correspondingly assume some smoothness of the expectation of the squared increments. The following assumption is of this type, and, as it turns out, is satisfied by most volatility processes driven by BM (see Proposition 2.4 below for details).

Assumption 3.

Suppose that for a locally bounded function , a function , and real numbers such that , the variance process satisfies

| (5) |

Although the assumption above is enough for BM type volatility processes, we are also interested in other types of volatilities, such as those driven by a fractional Brownian motion, that do not satisfy this condition. To this end, we also consider the following more general assumption.

Assumption 4.

Suppose that for and certain functions , , such that is not identically zero and

| (6) |

the variance process satisfies

| (7) |

Hereafter, we will also denote .

As shown in the next section, Assumption 4 is satisfied by most common volatility models.

Remark 2.2.

We now draw some connections with the assumptions and work in [15]. Therein, the variance process is assumed to satisfy the following pathwise condition

| (8) |

where is a slowly varying random function. To gain some intuition about the plausibility of this assumption, let us suppose that is a Brownian motion. In that case, the above holds for all , but such choices of can only produce suboptimal convergence rate of the kernel estimator. On the other, in light of Lévy’s modulus of continuity,

the condition (8) holds for , but only if , as . But, in that case, the optimal bandwidth selection formulas obtained in [15] are not well defined as they presume that is finite.

A function satisfying the condition (6) is said to be homogeneous of order . There are several preliminary properties we need to establish regarding the previous assumption and the function therein. Firstly, it is easy to see that Assumption 3 is a special case of Assumption 4 with and . Therefore, throughout the paper we will refer to Assumption 4 rather than Assumption 3.

The next result shows the non-negative definiteness of the function .

Proposition 2.1.

Under Assumption 4, both and are integrally non-negative definite. That is,

| (9) |

for all functions for which the integral therein is well-defined.

Proof.

To prove the result, we write (7) as where , as . We first show that is non-negative definite. Indeed, for , , and , we have

On the right-hand side of the previous equation, we let and we have that the first term is always non-negative, while the second term converges to zero. This shows the non-negative definiteness of . The integral non-negative definiteness follows then, since the Riemann integration is defined to be the limit of finite sum, which is always non-negative. ∎

The next result establishes the uniqueness of and in (7).

Proposition 2.2.

Proof.

First we prove the uniqueness of . Suppose there are such that , and correspondingly, and , that satisfies (7). Since is non-zero, there exists , such that . Then,

Note now that in the right two parts, all the terms are except . Since we have assumed that , this is impossible. Therefore, and, thus, must be unique. Now with the same , suppose at some , we have . Then, a similar argument shows that this leads to a contradiction. This proves the uniqueness of and . ∎

It is worth mentioning that we are assuming a fixed , for any . Intuitively, this means that the covariance structure does not change over time. For example, we are not considering the case where the volatility is BM type in and is deterministic and smooth in . We shall see in the next section that most volatility processes that are studied in the Mathematical Finance literature satisfy Assumption 4 with a function of the form:

| (10) |

for some . The case of covers volatility processes driven by BM, while corresponds to volatility processes driven by fractional Brownian Motions (fBM) with Hurst parameter . Deterministic and sufficiently smooth volatility processes can also be incorporated by taking .

Let us note that although most of the volatility models considered in the literature are covered by (10), mathematically one can consider more general models as long as Assumption 4 is satisfied. For instance, we will see in the next section that for a suitable Gaussian processes and a smooth function , satisfies Assumption 4. Furthermore, for any valid non-negative definite symmetric function that is homogeneous to order , one can define a zero-mean continuous Gaussian process such that . In such a case, if we define as a stochastic integral with respect to , then generally would satisfy Assumption 4.

To close this part, we briefly summarize the advantages of our key Assumption 4:

-

•

The assumption is natural since the spirit of kernel estimator is to focus on data points closed to the estimated point. Therefore, the convergence of such an estimator should be determined by a local property of the volatility process near the estimated point.

-

•

The assumption enables us to consider the randomness of log price process and volatility process simultaneously. Although we assume independence of and , the randomness of does create some subtleties. Also this makes it possible for future work to incorporate leverage effect of the volatility process.

-

•

The assumption provides us the possibility of obtaining an explicit asymptotic characterization of the Mean Squared Error (approximated to the first order) of the kernel estimator, so that we will then be able to setup a well-posed optimal selection problem for the bandwidth and kernel function.

2.3 Common Volatility Processes

In this section, we demonstrate that common volatility processes satisfy the Assumption 4. There are four fundamental cases that we would like to investigate. The simplest case is when the volatility process is deterministic and is differentiable. The second case is the solutions of a classical Stochastic Differential Equation (SDE) driven by BM. A prototypical example of this case is the Heston model [12]. The third case is the solution of a SDE driven by fBM. As a fundamental example of this case, we prove that a fractional Ornstein Uhlenbeck (fOU) process satisfies Assumption 4. Finally, we consider a volatility that is a smooth function of a Gaussian process satisfying the Assumption 4. This covers a wide range of different processes of fractional order and with different distribution laws.

2.3.1 Deterministic Volatility Process

This is the simplest type of volatility process, but still worth mentioning since it demonstrates the generality of Assumption 4. The proof of the following result is standard and is omitted for the sake of brevity.

Proposition 2.3.

Suppose the squared volatility process is given by a deterministic function , , such that, for some , is -times differentiable at , , for , and . Then, satisfies Assumption 4 with and .

2.3.2 Brownian Motion Case

We next consider the solutions of a standard SDE driven by BM. This is one of the most popular approaches to generalize the Black-Scholes-Merton model to non-constant volatility and is widely used in practice. The following is our main result, whose proof is deferred to the Appendix B.

Proposition 2.4.

Consider a complete filtered probability space and an Itô process that satisfies the SDE

| (11) |

where is a standard Wiener process adapted to . Assume that and are adapted and progressively measurable with respect to , , for , and is continuous for . Then, Assumption 4 is satisfied with , , and . Furthermore, is an integrable positive definite function; i.e., we have strict inequality in (9) for all such that .

Example 2.1 (Heston Model).

Consider the following Heston model, which was studied in [12]:

| (12) |

where parameters are restricted to , so that is always positive. This is one of the most widely used stochastic volatility models in Finance. The volatility process appearing above follows the so-called CIR model, which was introduced in [5]. As an immediate consequence of Proposition 2.4, we deduce that the Heston model satisfies Assumption 4 with , a positive definite , and .

2.3.3 Fractional Brownian Motion Case

We now proceed to study a volatility process driven by a fBM with Hurst parameter . Recall that a stochastic process is called a (two-sided) fractional Brownian Motion with Hurst parameter if this is a zero-mean Gaussian process with covariance function

In particular, when , we have for , and, thus, is the standard BM. We refer the reader to [25] for a detailed survey of fBM.

An important property of fBM, that is relevant to our problem, is self similarity. Concretely, is such that, for any , the process has the same finite-dimensional distributions as , because the covariance function is homogeneous of order . This gives us some intuition as to why Assumption 4 holds. The hurst parameter characterizes several important properties of fBM. For example, for , the process exhibits the so-called long-range dependence property, which broadly states that the autocorrelation of the increments of the process, , vanishes rather slowly so that the following holds:

Some empirical studies (see, e.g., [1]) have suggested that the volatility in real markets exhibits some type of long-memory and, due to this, we focus on the case .

In what follows, we show that some processes defined as integrals with respect to fBM satisfy Assumption 4. It is worth mentioning that, when , the fBM is not a semimartingale and the problem of defining the stochastic integral with respect to fBM is more subtle. There are several approaches to this problem. In our paper, we only focus on integrals of deterministic functions for which the integral can be defined on a path-wise sense under the following condition (cf. [25]):

| (13) |

Since there is no guarantees that the stochastic integral of with respect to fBM is nonnegative, which is a requirement of a volatility process, we also consider the exponential of such a process. This is our result, whose proof is deferred to the Appendix B.

Proposition 2.5.

As a prototypical example, the fractional Ornstein-Uhlenbeck process (fOU) (cf. [4]), which is frequently used to model volatility processes, satisfies Assumption 4. The fOU process, with Hurst parameter , is defined as the solution of the following SDE,

| (14) |

It is known that the previous SDE admits the stationary solution:

| (15) |

We have the following result (see Appendix B for a proof).

2.3.4 Functions of Gaussian Processes

We now proceed to define another class of processes satisfying Assumption 4. The following proposition guarantees that if a Gaussian process satisfies Assumption 4, so does a suitable smooth function of the process. See Appendix B for a proof.

Proposition 2.6.

Assume that is a Gaussian process that satisfies Assumption 4 uniformly over ,222The Assumption 4 is satisfied uniformly over if , as , and, also, . This implies the existence of a positive constant such that , for all . with , , and defined as in (7). For each fixed and a function , further assume the following:

-

(a)

, , as .

-

(b)

, for some .

Then, the process , , satisfies Assumption 4 with and .

Remark 2.3.

Note that the condition (a) in Proposition 2.6 is not a consequence of Assumption 4. This is satisfied by a large class of Gaussian processes, such as a fBM with zero mean and covariance structure given by (10). Intuitively, this condition states that, although and may not be independent, its correlation coefficient vanishes, as , fast enough as compared with standard deviation of .

2.4 Conditions on the Kernel and Preliminary Results

In this part, we introduce the assumptions needed on the kernel function, together with some required lemmas.

Assumption 5.

Given and as defined in Assumption 4, we assume that the kernel function satisfies the following conditions:

-

(1)

;

-

(2)

is Lipschitz and piecewise on its support , where ;

-

(3)

(i) ; (ii) , as ; (iii) , (iv) , where is the total variation;

-

(4)

.

Remark 2.4.

Note that (4) above does not put substantial restriction on since, in any case, is non-negative definite (see Proposition 2.1) and, furthermore, is strictly positive definite in some important cases such as BM type volatilities. In the case of deterministic volatility, it is possible to find such that , which actually will lead to even a faster rate of convergence of the estimation mean-squared error. This will be discussed further in Section 4.4.

The following two technical lemmas will be used throughout the paper, and the proofs are deferred to the Appendices.

Lemma 2.2.

For , assume the following for a function and functions , :

-

(i)

, as for any given , where is a function such that

-

(ii)

.

-

(iii)

For , satisfies Conditions (2) and (3) of Assumption 5 with a support .

Let

where . Then, for each , we have the following:

as and . If, furthermore, the condition (i) above is satisfied uniformly over , then the approximation above is also uniform over .

Remark 2.5.

It is worth mentioning that here has similar meaning as the one appeared in Assumption 4, so we use the same notation . It is also worth noticing that if but still , then we again have , but the constant before depends on not only through .

Lemma 2.3.

For , assume the following for a function and a function :

-

(i)

satisfies the conditions (i) and (ii) of Lemma 2.2,

-

(ii)

satisfies the conditions (2) and (3) of Assumption 5 with a support .

Let

Then, for all , we have:

The result remains the same if the integration domain of the first term in is , instead of . Furthermore, if the condition (i) of Lemma 2.2 is satisfied uniformly over , the approximation above holds true uniformly over .

3 Approximation of MSE and Optimal Bandwidth Selection

In this section, we assume that the processes , , and, satisfy Assumptions 1, 2, and 4, and we consider a kernel function that satisfies Assumption 5. In what follows, we first deduce an explicit leading order approximation (up to and terms) of the . After this, we proceed to study the approximated optimal bandwidth , which is defined as the bandwidth that minimizes the leading order approximation of the MSE. Finally, we prove that our approximated optimal bandwidth is asymptotically equivalent to the true optimal bandwidth that minimizes the true MSE.

3.1 Approximation of the Mean Squared Error

Let us start by writing the MSE as

| MSE | |||

By Lemmas 2.2 and 2.3 with , we have and, thus,

| (16) |

which, applying Lemmas 2.2 and 2.3 together with Assumption 1 and 2 (we refer to the Appendix C for more details), can further be written as

| (17) |

Next, by Assumption 1, it readily follows that

| (18) |

We now proceed to analyze and . Firstly, for , note that

To analyze the contribution of each of the three terms above to , we use Lemma 2.2 and 2.3 with kernel function and the following three different functions :

respectively. It then follows that

where the second line above follows from the fact that . Putting together the previous relationships, we conclude that

Next, applying directly Lemmas 2.2 and 2.3 and Assumption 4, can be written as

Finally, we conclude the following explicit asymptotic expansion for the MSE of our kernel estimator.

Theorem 3.1.

Theorem 3.1 will be the main tool to obtain the approximated optimal bandwidth and kernel function. As a direct consequence, we also have the following consistency result for the kernel estimator.

Corollary 3.1.

With the same assumptions as those in Theorem 3.1, when and .

It is not very hard to see from the previous proof that all terms are uniform for if the condition given by (7) is satisfied uniformly in , and, therefore, the following explicit asymptotic expansion for the integrated mean-squared error (IMSE) holds.

3.2 Approximated Optimal Bandwidth

Based on the approximations above, it is natural to analyze the behavior of the approximated MSE of the kernel estimator:

| (21) |

Correspondingly, the approximated IMSE of the kernel estimator is defined as

| (22) |

Obviously, , while, by Assumption 5, we also have that . We then obtain the following approximated optimal bandwidth:

Proposition 3.1.

A direct yet considerably important consequence of Theorem 3.1 and Proposition 3.1 is the following proposition about the optimal convergence rate. This provides a rigorous justification of the optimal convergence rate of the kernel estimator. It is worth mentioning that (4) of Assumption 5 is necessary for this proposition.

Proposition 3.2.

With the same assumptions as those in Theorem 3.1, the optimal convergence rate of the kernel estimator is given by . This is attainable if the bandwidth is selected to be .

Corresponding to Corollary 3.2, we have the following proposition for the approximated “uniform” optimal bandwidth that minimizes the approximated IMSE.

Proposition 3.3.

It is worthwhile to draw some connections with [15] by considering the case of , which corresponds to a deterministic variance function that is continuously differentiable at and such that . In that case, the approximated MSE (21) is given by

| (27) |

which coincides with the approximation obtained in [15]. However, it is evident that, in the case that the volatility is stochastic and non-smooth, our results are different from those in [15]. In Section 4.4, we will see that in the case of deterministic and smooth volatility, we are able to use “higher order” kernels to improve the rate of convergence of the kernel estimator, but in other situations, for example BM type volatility, this is not possible. This is one of the major difference between our work and [15]. Intuitively, this is due to the assumption of a stochastic volatility model, which in reality is more reasonable.

An important problem is to formalize the connection between the approximate optimal bandwidth and the “true” optimal bandwidth, whenever it exists, which is denoted by and is defined as a value of the bandwidth that minimizes the actual MSE of the kernel estimator, . In Appendix A, we show that, under a mild additional condition, they are equivalent in the sense that

4 Kernel Function Selection

As an important application of the well-posed optimal bandwidth selection problem defined in Section 3, we now proceed to consider the problem of selecting an optimal kernel function. Although the theoretical optimal convergence rate can be attained with a bandwidth of the form , and we indeed obtained the coefficient that optimizes the first order approximation of the MSE of the kernel estimator for a given kernel function , we can achieve further variance reduction by choosing an appropriate kernel function. This is particularly important for finite sample settings encountered in practice.

As shown by (24), the optimal kernel function only depends on the covariance structure, . There are two possible situations. The first one is when is positive definite. In such a case, we cannot improve the rate of convergence of the MSE, but we can minimize the constant appearing before the asymptotic MSE and IMSE. Another situation is when is simply non-negative definite. In such a case, if we relax (4) of Assumption 5, it is possible to improve the rate of convergence of the MSE by choosing a so-called “higher order” kernel function.

More concretely, in this section, we consider three different cases. The first case, which is of fundamental importance in finance, is when and (Brownian driven volatilities). In such a case, an explicit form of the optimal kernel function can be obtained and an efficient algorithm is available for its implementation. The second case is when the covariance structure is given by (10) with , which can be obtained, for instance, when the volatility is driven by long-memory fBm’s. The final case is when and (e.g., deterministic smooth volatilities). Such a covariance structure is not positive definite, so it will be possible to use “higher order” kernels to improve the rate of convergence.

4.1 Optimal Kernel Selection for a BM driven Volatility

In this part, we consider the first case, i.e. the BM type volatility with and . We will show that the exponential kernel function is the optimal kernel function.

Exponential kernel function has been shown to be optimal for different problems in previous literature. For example, van Eeden (1985) showed that it is the optimal kernel function for the density estimation problem under some conditions. Foster and Nelson (1994) argued that the exponential kernel is the optimal kernel function to estimate spot volatility, under similar but different assumptions as we have. Their result is more general in the sense that they allow the leverage. However, their proof lacks rigor, due to their bounded support assumption on the kernel function. Also they did not draw any connection between optimal bandwidth and optimal kernel, while our results show that the optimal bandwidth and kernel function are jointly optimal.

To start with, from (24), the objective function that we need to minimize is the following:

| (28) |

with the restriction . Here we notice that is always positive, as shown by the proof of Proposition 2.4. We divide the problem of minimizing (28) in three steps.

Step 1. Symmetric kernel

Firstly, we claim that we only need to consider symmetric kernel functions. To this end, we prove that , where . Indeed, we have and for the first factor of ,

| (29) |

where the equality holds if and only if for all , i.e., is symmetric.

For the second factor of , let and note that

where the equality holds if and only if for all , i.e., is symmetric. From here, we see that we only need to consider symmetric kernel functions, and the problem is changed to minimize

Step 2. Changing to an equivalent optimization problem

By writing as , we have

We define and note that, by definition of , there are only finite many points where does not exist (note that is not assumed to be continuous, and at those points, where is not continuous, is not differentiable, though left and right derivatives exist). Then, can be written as

and the problem is changed to minimize for functions with the following restrictions:

-

(1)

is continuous and piece-wise twice differentiable on .

-

(2)

and .

Note that the restrictions above are equivalent to the conditions we put on . Since we are not assuming a non-negative kernel function, it is not necessary that is non-increasing.

Step 3. Derivation of the exponential kernel

Using Cauchy-Schwartz inequality, we get

where the first inequality becomes equality if and only if there exist non-zero constants and such that

Notice that is continuous on and . So we have two possible cases: (1) there exists , such that , for all and ; (2) , for all .

For the first case, we have that for ,

whose solution is . It is then impossible that . Therefore, only the second case is possible. By solving the same differential equation, and together with and , we have

Therefore, the optimal kernel function is . Here, different values of do not change the value of , so we can choose for simplicity.

As a summary, we have the following theorem for the optimal kernel function.

Theorem 4.1.

We now do some calculations and demonstrate to what extent the exponential kernel decreases the MSE.

Example 4.1.

As we can see from (24), , where the constant does not depend on the kernel function . Below, we show the value of for the exponential, uniform, triangular, and the Epanechnikov kernels:

Interestingly enough, the triangle kernel performs better than Epanechnikov kernel and Epanechnikov kernel performs better than the uniform kernel. The intuition behind this is that a kernel function with a shape more similar to the exponential kernel generally performs better.

4.2 Efficient Implementation of the Uniform and Exponential Kernel

In this subsection, we demonstrate that the exponential kernel function not only minimizes the MSE of the kernel estimator, as shown in the previous subsection, but also enables us to substantially reduce the computational complexity of the volatility estimation.

Let us recall that denotes the number of observations we have. In general, the evaluation of for a fixed time requires (respectively, ) computations for a kernel function with unbounded (respectively, bounded) support, as long as the bandwidth has already been fixed. However, if we hope to get an estimation of the whole discrete skeleton of the volatility, one would then require a time of or for a general kernel function with unbounded or bounded support, respectively. In particular, if, in addition, we were to use the approximated optimal bandwidth given by (23), the best possible complexity, which is achieved by kernels with bounded supports, is . This computational time might be substantially long considering our goal to use high frequency data.

We now show that, for both the uniform and exponential kernels, we can do substantially better. Indeed, for the uniform kernel and any , we can use the idea of moving average as the following:

where and .

For the exponential kernel, we write and we introduce the following notations:

where . Note that . Then, by the idea of geometric moving average, we can use the following recurrent algorithm:

| (30) |

It is then clear that, in order to estimate the “whole path” of using an exponential kernel, we need a time of , instead of or . The difference between the two time complexities mentioned above is quite significant, since we are considering high frequency data. For example, suppose that we want to compute the whole discrete skeleton of the volatility for a trading day with data every second so that . Let us also assume that we consider volatility process generated by Brownian motion, i.e. . In such case, the recurrent algorithm described above requires about computations, while the standard algorithm requires about or , for kernels with bounded or unbounded supports. Actually the recurrent algorithm is at least about times faster than the naive algorithm.

In practice, kernel estimators suffer of biases at times closer to the boundary. As proposed in [15], we can correct such boundary effects by using the following estimator:

| (31) |

where the superscript denotes boundary effect. We can still implement our fast estimation algorithm to calculate this estimator since we only need to calculate , which can be calculated similarly as (30) except that all are replaced by .

Another important problem, usually encountered in high frequency trading, is to calculate the current spot volatility as quickly as possible, based on the previous volatility estimate and the newly observed return. Under such a setting, the exponential kernel can perform pretty well in both time and space complexity. Indeed, an “online” type algorithm can be implemented by setting . Because of this, in order to update the estimation of the current volatility, we only need time and space, instead of or for other kernel functions with unbounded or bounded supports.

4.3 Optimal Kernel Function for a fBM driven Volatility

In this section, we now consider a general fBM covariance structure, i.e. and given by (10). From (24), our goal is to minimize

Our first step is still to prove that we only need to consider symmetric kernel functions. In particular, we have that , where . To this end, it is useful to note we can write as follows

with , for a certain constant (see [21] for details). The first factor of can be treated as in (29), while, for the second factor, since , we have

| (32) |

Therefore, we only need to consider symmetric kernel functions.

Unfortunately, the problem of finding an explicit form for the optimal kernel function is much more challenging in this case. Therefore, we instead seek for a numerical method to find the optimal kernel function. We notice that , for any , and, thus, our goal is then changed to minimize

| (33) |

where . Since our problem is unchanged with scaled by a small bandwidth, we will limit the support of to be . Note that this excludes those kernels with unbounded support. However, since all unbounded support kernels can be approximated, to an arbitrary precision, by a kernel with a bounded support, we will limit our consideration to bounded support kernels at this point.

A way to solve such an optimization problem numerically is to approximate the kernel function by step functions and then use gradient descent to directly optimize (33). Indeed, the kernel function can be approximated by

With such an approximation, it is then natural to consider the following optimization problem:

| (34) |

where , with , .

We notice that this is an optimization problem with high dimensional independent variables. In fact, in order for the resulting approximated optimal kernel to converge to the true optimal kernel function, we need . However, the numerical optimization problem is still tractable, since the gradient can be calculated explicitly, which allows us to use a gradient descent method to calculate the optimal kernel function numerically. Of course, there are some practical issues to consider when dealing with gradient descent. The first problem is that the method may yield a local minima, but not the global minima. In order to alleviate the latter issue, we choose several initial values randomly and select the best final result. Another problem is how to determine the step size for each iteration. There are several standard ways to solve this problem. In our implementation, we first choose a step size that is large enough. If the objective function decreases when walking through the gradient direction with the selected step size, we update the point and go on to the next iteration. Otherwise, we shrink the step size to a half.

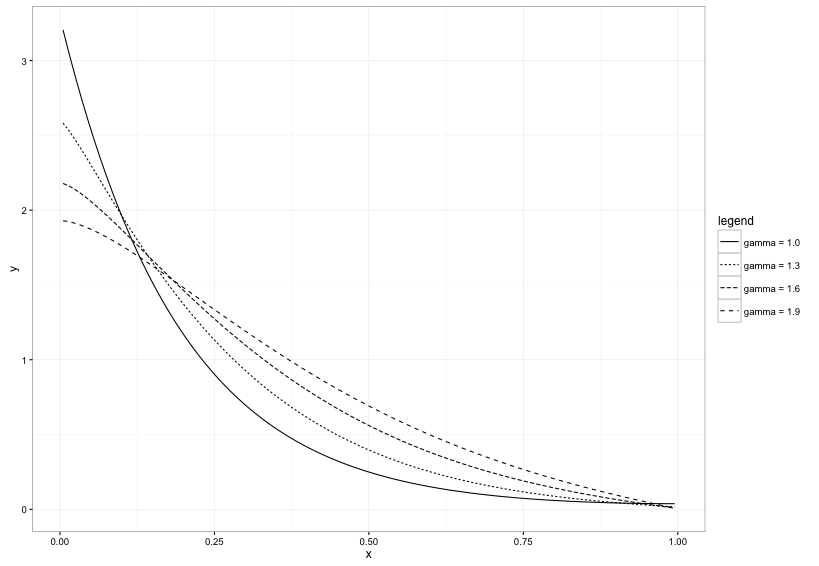

Figure 1 shows the resulting optimal kernel functions for . Note that the resulting approximated optimal kernel for is consistent with true optimal kernel that was proved to be exponential in Section 4.1. We also observe from Figure 1 that, as increases, the optimal kernel function becomes flatter and less convex. This indeed makes sense, since a higher indicates less chaos of the volatility, and thus more weights should be given to data farther from the estimated point.

4.4 Optimal Kernel for a Deterministic Volatility Function

Lastly, we consider the case , for a deterministic function . As seen in Subsection 2.3.1, we have that and . Obviously, such a is not strictly positive definite, so theoretically we can consider “higher order” kernels to improve the convergence rate of the estimation MSE. Specifically, we generalize the condition (4) of Assumption 5 as follows:

Such a kernel is said to be of order . We also extend Assumption 4 as follows:

where the function is such that , for any , , and . In that case, with a similar procedure as that of Section 3, we can prove that the approximated MSE (21) is given by

We can then select an optimal bandwidth. The optimal bandwidth and corresponding optimal convergence rate are the same as those obtained in [15].

Remark 4.1.

For the construction of higher order kernel functions, we refer to Section 1.2.2 in [26]. However, as was already pointed out by [15], “higher order” kernels cannot be non-negative333Indeed, it is not possible to have both and , for all . and, thus, in principle, may yield non-positive estimates of the volatility. Therefore, there is some tradeoff between accuracy and positivity.

An interesting application, which was not considered in [15], is to find the kernel that minimizes the resulting optimal approximated MSE. Concretely, if we limit ourselves to symmetric kernels of order , the goal is to minimize

| (35) |

For such a problem, we further limit ourself to kernel function with support and use calculus of variation to derive the optimal kernel function. For any continuous function such that and a real number , we consider

Next, in order to find a local minimum point of , we take the derivative of with respect to to get

Then, we solve , which is equivalent to solve

In order for the above to hold for any satisfying the stated properties, needs to have the form for . By plugging such a in, we get

Solving such an equation yields a unique solution and, by solving , we can get . Therefore, we get a local minimum point of (35) as the following:

It is worth mentioning that when , we have , which is exactly the Epanechnikov kernel.

There is still a problem for such a kernel. Take as an example. Although is a local minimum point of (35), it does not satisfy . Therefore, we propose to consider instead the following optimization problem with constraints:

| (36) |

To solve such a problem, we consider the Lagrangian

| (37) |

where are Lagrangian multipliers. In order to solve such an optimization problem, we set and . After some simplifications, these yield the system of equations:

Therefore, needs to take the form . Then, by plugging in such a , we get equations:

Solving such a system of equations for and provide us a candidate of global optimal kernel function.

5 Plug-In Bandwidth Selection Methods

In this section we propose a feasible plug-in type bandwidth selection algorithm, for which, as a sub-problem, we also develop a new estimator of the volatility of volatility based on the kernel estimator of the spot volatility and a type of two-time scale realized variance estimator.

Let start by giving a brief overview of the different methods for bandwidth selections. There are generally two types of methods: cross-validation and plug-in type methods. In [15], a leave-one-out cross validation method for determining the optimal bandwidth is proposed, which does provide good results, as shown by simulations (see Section 7 below for further details). The advantage of the cross validation method is its generality and portability across different settings (e.g., different ’s and ’s). However, this method has two main drawbacks. On one hand, the method generally suffers from loss of accuracy. One reason is that the cross-validation method yields a single bandwidth for the whole time period, in spite of the fact that, as seen from (23), the optimal bandwidth varies from time to time. Also, even if we restrict ourselves to homogeneous bandwidths, cross validation method is still not as accurate as a properly implemented plug-in type method. On the other hand, the cross validation method is computationally expensive since it involves to carry out a numerical optimization scheme to find the bandwidth. More specifically, as mentioned in Section 4.2, for each proposed bandwidth , we need steps to calculate the objective function for a general kernel function with unbounded support (even though, as it was mentioned before, such a complexity can be reduced to when using an exponential kernel). Therefore, even with a good initial guess, it would generally take quite a long time to find a satisfactory bandwidth by cross validation.

As previously mentioned, we proceed to propose a feasible plug-in bandwidth selection method based on the explicit formula of the global bandwidth (25). The proposed method slightly sacrifices generality for the advantage of higher accuracy and faster speed. We shall focus on the case of a BM type volatility, while similar methods can be developed for other types of volatility structures. For easy reference, let us recall that the global approximated optimal bandwidth takes the form:

| (38) |

To implement (38), it is natural to first use the integrated quarticity of , , and the quadratic variation of , , instead of their expected values. Intuitively, this approach makes the estimator more data adaptive and, in the absence of parametric constraints, these are the only estimable quantities with only one path. As it is well known, a popular estimate for is the so-called realized quarticity, which is defined by . The estimation of is a more subtle problem and, below, we propose an estimator, which we call Two-time Scale Realized Volatility of Volatility (TSRVV) and is hereafter denoted by . With these estimators, the final bandwidth can then be written as

| (39) |

Iterative Algorithm

The previous bandwidth estimator involves the spot volatility itself, through , which, of course, we do not know in advance. To deal with this problem, we propose to use an iterative algorithm in the same spirit of a fixed-point type of procedure. Concretely, we start with an initial “guess” for the bandwidth. For example, we can take (39) and simply set , which gives:

| (40) |

With such a bandwidth, we can obtain initial estimates of the spot volatility at all the grid points. Such an initial spot volatility estimation can then be applied to compute , which, in turn, can be used to obtain another estimation of the optimal bandwidth. This procedure is continued iteratively until a predetermined stopping criteria is met. In reality, our simulations in Section 7 show that one or two iterations are enough to obtain a satisfactory result and more iterations do not generally produce any improvement. Algorithm 1 below outlines the proposed procedure for a global bandwidth given by (39).

5.1 A Two-time Scale Estimator of Integrated Volatility of Volatility

In this subsection, we propose an estimator of the quadratic variation of , , which is often referred to as the Integrated Volatility of Volatility (IVV) of . This is based on the natural idea of using the realized quadratic variation of some estimated spot volatility . However, the estimated spot volatilities have errors and a direct construction of the realized quadratic variation will be highly biased due to the errors of the estimation. This is similar to the case of estimating the integrated volatility of an Itô semimartingale based on high-frequency observations subject to micro-structure noise, which has received a great deal of attention in the literature. In this part, we adapt the so-called Two-time Scale Realized Volatility (TSRV) estimator of [31] to estimate the IVV. For completeness, we first introduce the idea of TSRV and, then proceed to defined our estimator of IVV.

The theory of microstructure noise, put forward by [31] and others, postulates that the true log prices of the asset cannot directly be observed from the market and, instead, the log prices with an additive noise term, denoted by , are observed. In the simplest case, is white-noise (i.e., independent identically distributed with mean and constant variance ), which is independent from the true price process . In that case, the Realized Volatility estimator of the integrated volatility has a bias and variance of order and , respectively. Indeed, the following result is proved by [31]:

| (41) |

where and represents the conditional law given the whole path of . Here, we follow the notation used in [31] to denote the realized quadratic variation based on all the observations . As proposed in [31], one way to alleviate the problem is to average the realized variations obtained at coarser time scale as the following:

where . Then, the biased corrected Two-time Scale Realized Volatility (TSRV) estimator is then defined as

| (42) |

Such a TSRV estimator can be proved to converge to the true Integrated Volatility and a convergence rate of can be achieved with (see [31, Theorem 4]).

Back to our problem, let us first note that, at each observation time , the estimated spot volatility can be written as , where is the estimation error. The difference of our problem and the problem in [31] is that our estimation errors are not independent. In fact, they are correlated. Such a correlation becomes more significant when we take the difference . To alleviate such a problem, we propose to use one-sided kernel estimators and take the difference between the right and left side estimators to find . Concretely, define and to be the left and right side estimator of , respectively, defined as the following:

| (43) |

Next, we define the following two difference terms: , . Finally, we can construct the following Two-time Scale Realized Volatility of Volatility (TSRVV):

| (44) |

Here, is a small enough integer, when compared to . The purpose of introducing such a number is to alleviate the boundary effect of the one sided estimators, since, for instance, it is expected that will be more inaccurate as gets smaller. It is worth to noting that might become negative. In this case, a possible solution is to take simple . Similar to [31], we can simply take in our case. There is some work to do if one wants to optimize such a TSRVV estimator, but this is outside the scope of the present work. Nevertheless, as our simulations in Section 7 show, the accuracy of spot volatility is good enough even without refining such a TSRVV estimator.

The following result shows the consistency of our estimator and shed some light on the rate of convergence. Its proof is deferred to the Appendix section.

Theorem 5.1.

For the model (1) with and satisfying Assumptions 1, 2, and being an squared integrable Itô process as in Eq. (11) (thus satisfying Assumption 4), and a kernel function satisfying Assumption 5, for any fixed , (44) is a consistent estimator of with . The convergence rate is given by and, thus, can be chosen to be of the form so that to attain the ‘optimal’ convergence rate .

Remark 5.1.

(1) The proof of Theorem 5.1 actually holds even if we use two-sided kernel estimation. The main reason for using one-side kernels is to correct the estimation bias. Also, according to [31], (58) actually converge to a normal distribution. Therefore, although we have not investigated in detail the asymptotic distribution of (57), it is expected that for any , with , converges to normal distribution with a rate .

(3) The estimation of integrated volatility of volatility has also been studied in other literature, for example, [28], using a different method. In the simulation study, we compare these two methods and found that our method works better under some widely used settings. Intuitively, the reason is that our estimation of volatility of volatility is based on more accurate estimation of spot volatility and our iterative methods further help enhance the accuracy.

6 Central Limit Theorems

In this section, we seek to characterize the limiting distribution of the estimation error of the kernel estimator and prove feasible Central Limit Theorems (CLT) for the estimation error of kernel estimators. The starting point is to decompose the error into the following two parts:

| (45) |

In order to obtain a CLT for the kernel estimator, we need to deal with the two error terms above. The first error term is easier to handle and has already been studied in the literature of kernel estimation of spot volatility (see, e.g., [15]). By contrast, the limiting distribution of the second error term of (45) is more involved. We can find two general type of results in the literature:

-

(1)

In the case that follows an Itô process, the limiting distribution of the second error term can be determined by Martingale Central Limit Theorems (cf. [10] Theorem 1 and 2).

-

(2)

A second approach consists of using a ‘suboptimal’ bandwidth so that only the first error term in (45) is significant. This would be the case if, for instance, we choose , in which case the order of the second term in (45) becomes and is negligible compared to the order of the first term, which is . Instances of this type of results can be found in [8] (see Assumption A4 and Theorem 1 therein), and [15] (Theorem 3 therein).

The two previous approaches have some obvious limitations. The results obtained using the first approach only deal with one level of smoothness in the volatility process, while the results obtained using the second approach can only yield suboptimal convergence rates. In this work, we obtain a CLT for two relatively broad frameworks that are closely related to Assumption 4 and cover all the examples mentioned in Section 2.3. On both cases, the CLT has the optimal convergence rate, and the second case covers a wide range of models of different smoothness order.

We begin with an analysis of the first error term, which, as mentioned above, has already been studied in the literature (see, e.g., [15]). Concretely, we have the following CLT for this term. A sketch of the proof is also provided for the sake of completeness.

Theorem 6.1.

Proof.

In the proof, we condition on the whole path of so that we can assume that these processes are deterministic. Let us start by noting the following relationship, which can be justified by Lemma 2.2:

| (48) |

Next, define

Then, for each , are independent. By applying Lemma 2.2 and with some similar calculation as in the proof of Theorem 3.1, we have the following as :

Therefore, (46) follows by Lindeberg-Feller Theorem. By using (48) together with (46), (47) follows. ∎

Next, we consider the second error term in (45).

Theorem 6.2.

Suppose that the coefficient processes and in the model (1) satisfy Assumptions 1, 2, and 4, and the kernel function satisfies Assumption 5. Furthermore, suppose that either one of the following conditions holds:

-

(1)

is an Itô process given by , where we further assume that , , and as .

-

(2)

, for a deterministic function and a Gaussian process satisfying all requirements of Proposition 2.6.

Then, on an extension of the probability space , equipped with a standard normal variable independent of , we have, for each ,

| (49) |

where, under the condition (1) above, , while, under the condition (2), .

Proof.

(1) The proof in the Itô process setting of (1) is inspired by that of Theorems 1 and 2 in [10], but in our case, we do not assume a bounded support for the kernel function, and work directly with the continuous model, which makes the assumptions and proof clearer. For simplicity, we will use the following notations:

It is easy to see from Lemma 2.4 that and both satisfy Assumption 4 with and . Now, since

we can conclude that the drift term of has a negligible contribution to the final error, i.e.

| (50) |

Therefore, it suffices to work with the process and only to consider the weak convergence of the following:

For the sake of clarity, we will first assume a one-sided kernel function, i.e. for all . Applying the integration by parts formula, we have that

where so that . Since our assumptions on imply that , as 444 Indeed, we have assumed that , as , where in this case . Then, by L’Hopital, it is easy to check that we have that ., we can conclude that . For the other term , let us consider the following approximation

We first observe that . Indeed, Assumption 5 implies that , so we have

We also observe that conditional on , is Gaussian with mean and the following variance:

where . Therefore, where .

We now consider the general two-sided kernel case. Let

and note that, by the integration by parts formula,

Same as in the one-sided kernel case, our assumptions imply . For , we still consider the following approximation

and we still have . It is also true that vanishes as . This can be justified by considering its second moment as the following:

Therefore, we have

where the second equality holds since

Note that since

and, finally, we conclude that , as .

(2) We then move on to consider case (2). In the whole proof, the superscript means that the quantity corresponds to process , while quantities without such a superscript corresponds to the process . Let us start by noting that, since is a Gaussian process, we have

Now, for any , and for any , there exists , such that . Then, we have

For the second term, once we select small enough such that and for all , we have that

Now for the first term, we have

where the standard normal appearing above is independent from . The latter convergence in distribution can be justified similar as Proposition 2.6. Write

We have that is bi-variate normal for all and, thus, whenever the limit exists, is bivariate normal variable. There exist and such that , such that is independent with and , for some and , as . Note that and are given by

By our assumption, we have , which implies that

With such representations, we are able to obtain the desired result:

Here, and is independent from . ∎

Remark 6.1.

It is worth noting that in both of the cases covered in Theorem 6.2, we have

which is exactly the coefficient of the second term appearing in (19). Similarly, the mean of the asymptotic conditional variance in the CLT of Theorem 6.1, , coincides with the coefficient of the first term in (19). Therefore, the CLT obtained from Theorems 6.1 and 6.2 are consistent with the asymptotic behavior of the MSE derived in Theorem 3.1. Note, however, that the framework of Theorem 3.1 is more general.

7 Simulation Results

In this section, we perform some simulation studies to further investigate the results that we developed before and compare our method with methods proposed in previous literature. Throughout, we will consider the Heston model (12). As to the parameters values, we adopt the following widely used setting (cf. [31]), unless otherwise specified:

The initial values are set to be . We also assume both a non-leverage setting (), as required by our Assumption 1, and a negative leverage situation () to investigate the robustness of our method against non-zero values.

We will consider several different scenarios of observed data. First of all, we consider 5 days and 21 days data, which correspond to 1 week and 1 month data. For each trading day, we consider 6.5 trading hours and as for the frequency of the observations, we consider 5 minutes data and 1 minute data. Take 21 trading days and 5 minutes data, for example, totally we have observations and .

In order to alleviate boundary effect, we use estimator (31) throughout all the simulation. For each simulated discrete skeleton , we estimate the corresponding discrete-skeleton of the variance process , and calculate the average of the squared errors, , for each simulation. (We incorporate an to focus on evaluating the performance of the estimator without boundary effects. is generally taken to be .) Then, we take the sample average of such ASE’s to estimate the mean ASE, defined as .

7.1 Bandwidth Selection with Plug-In Method

In this section, we investigate the plug-in method that we developed in Sections 3 and 5. In the first part, we will see how the number of iterations, as described in Algorithm 1, affects the MASE of the kernel estimator. In the second part, we compare our plug-in method with the leave-one-out cross-validation method proposed in [15]. In the third part, we investigate the performance of the TSRVV estimator of volatility of volatility proposed in Section 5.1.

7.1.1 Number of Iterations

Let us start by investigating how the number of iterations can affect the accuracy of the plug-in type kernel estimation of spot volatility. An exponential kernel is implemented. Table 1 shows the MASE of the kernel estimator when we use 0 to 5 iterations for the plug-in method, where 0 iteration means we only use the initial value of the bandwidth given by (40) to estimate the volatility.

From the results, we first observe that the initial guess has unstable performance, as one may expect. We also find out that after the initial guess, the MASE does not change a lot, and gradually move to a specific fix point value. It is interesting to notice that, after the first iteration, MASE does not always decrease as the number of iteration increases. This indeed makes sense, since our approximated optimal bandwidth and all the estimated parameters have errors, so the fix point that the estimator converges to, after several iterations, might be slightly different from the true optimal value, and it is possible that the initial guess leads to some bandwidth that performs better than the fix point. In conclusion, after one or at most two iterations, there is no significant performance enhancement with more iterations.

5 Days Data

nData/h

0

1

2

3

4

5

12

0

2.5664

2.5241

2.5482

2.5747

2.5804

2.5845

60

0

1.2180

1.0132

1.0100

1.0138

1.0150

1.0154

12

-0.5

2.5792

2.5177

2.5494

2.5742

2.5810

2.5842

60

-0.5

1.2336

1.0238

1.0206

1.0237

1.0248

1.0248

21 Days Data

nData/h

0

1

2

3

4

5

12

0

2.8439

2.3712

2.3607

2.3620

2.3626

2.3625

60

0

1.3265

1.0454

1.0385

1.0379

1.0373

1.0375

12

-0.5

2.8923

2.4088

2.4006

2.4051

2.4055

2.4055

60

-0.5

1.3335

1.0459

1.0395

1.0391

1.0388

1.0388

7.1.2 Comparison Between Plug-In Method and Cross-Validation

In this part, we compare the plug-in method with the cross-validation method under the three different sampling scenarios described above. In Table 2, we report the MASE for the kernel estimator obtained by the different methods. The first column is the plug-in method, where we use the approximated homogeneous optimal bandwidth (25) with parameters estimated as proposed in Section 5. Concretely, we use the formula

| (51) |

to find , where is the estimated volatility at the -iteration. In the second column, we report the result for the leave-one-out cross validation. In the third column, we report the result for an oracle plug-in method, where the true and are used to compute and in the formula (25). Concretely, we use the formula

The final column shows a “semi-oracle” result, which assumes the knowledge of the volatility of volatility of the Heston model, but not . That is, the formula

is used to compute the volatility at the iteration.

For this simulation, we only sample 2000 paths, since the cross-validation method is very time consuming. However, we do believe that the result is representative, since for each sample path, the ASE that we calculate already kills a lot of noises.

As expected, the plug-in method runs significantly faster than cross validation. As to the accuracy of the kernel estimator, simulation results show that, in almost all sampling frequencies, the plug-in method outperforms the cross-validation method. However, we do observe that for 1 month and 1 minute data case, the cross validation is slightly better than the plug-in method. This is due to the inaccuracy of the estimation of the vol vol for this sampling setting and the lack of optimal tuning of the estimation parameters for the vol vol estimator. Indeed, when there are fewer data, the plug-in method outperforms cross validation significantly in accuracy. And when there are more data, the computational efficiency becomes a crucial issue. Although both methods tend to have similar performance in accuracy, plug-in method has superior advantage in speed.

It is worth to notice that, in all cases, there is still significant loss of accuracy for the plug-in method compared to the oracle ones. From the two oracle results, it can be easily observed that such a loss of accuracy is mainly due to the estimation error of the volatility of volatility. Further investigation of the estimation of the volatility of volatility is an interesting and important topic for future research.

5 Days Data

nData/h

12

0

1.0796E-07

1.3386E-07

9.1266E-08

9.0402E-08

60

0

7.1439E-09

8.0542E-09

6.7286E-09

6.7074E-09

12

-0.5

1.0296E-07

1.4180E-07

9.2620E-08

9.2009E-08

60

-0.5

7.3872E-09

8.2567E-09

6.9356E-09

6.9060E-09

21 Days Data

nData/h

12

0

1.9088E-08

2.1221E-08

1.8265E-08

1.8178E-08

60

0

1.7064E-09

1.6868E-09

1.5984E-09

1.5961E-09

12

-0.5

1.9039E-08

1.9495E-08

1.7587E-08

1.7506E-08

60

-0.5

1.6652E-09

1.6011E-09

1.5509E-09

1.5505E-09

7.1.3 Estimation of Volatility of Volatility

In this section, we test the TSRVV estimator that we proposed in Section 5.1. We use one month data as demonstration, and, in order to see how the estimator performs with different sampling sequence, we consider 5 min and 1 min data. Since we are considering the Heston model, we will not report the integrated volatility of volatility, but instead, we report the following estimator of vol vol parameter of the Heston model:

Generally, is a rule of thumb value, but we will use and to test the estimator.

The result is reported in Table 3 and as we can see, the estimator performs better when when the sampling frequency increases or the value of get larger. However, it is also clear that estimation error is quite large, so further development of estimation of vol vol should be possible.

| nData/h | Bias | Std | |||

|---|---|---|---|---|---|

| 12 | 0 | 0.2 | -0.0006 | 0.0990 | 0.0990 |

| 12 | 0 | 0.5 | -0.0584 | 0.1979 | 0.2063 |

| 60 | 0 | 0.2 | -0.0122 | 0.0772 | 0.0782 |

| 60 | 0 | 0.5 | -0.0411 | 0.1549 | 0.1603 |

| 12 | -0.5 | 0.2 | -0.0002 | 0.0987 | 0.0987 |

| 12 | -0.5 | 0.5 | -0.0571 | 0.1984 | 0.2065 |

| 60 | -0.5 | 0.2 | -0.0138 | 0.0779 | 0.0791 |

| 60 | -0.5 | 0.5 | -0.0443 | 0.1551 | 0.1613 |

7.2 Comparing Different Kernel Functions

In this section, we compare the performance of different kernel functions. Specifically, we consider the following four different kernels:

The first kernel is the optimal kernel we obtained previously. The other three kernels are finite domain kernels with different order of polynomial. The fourth kernel is the so called Epanechnikov kernel, which is claimed to be the optimal kernel in [15]. In the formula for optimal bandwidth, (23), we encounter some constants that depends on the kernel . As a summary, we calculate them for all the four kernels in Table 4. The results of the simulation are shown by Table 5. Here we consider both the case of , and plug-in method with uniform bandwidth. Note that the estimator becomes considerably slow for some kernels, we only simulate 2000 sample paths.

| Kernel | |||

|---|---|---|---|

As shown from the result, the exponential kernel performs the best in all cases. As the calculation we had in Example 4.1, we can see that the second best kernel is the triangle kernel, since its shape is more similar to exponential kernel. Similarly, the uniform kernel performs the worst, since it is the farthest to the optimal exponential kernel.

| length | exponential | uniform | triangle | Epanechnikov | |

|---|---|---|---|---|---|

| 5 days | 0 | 2.5974E-05 | 2.8721E-05 | 2.6441E-05 | 2.7085E-05 |

| 5 days | -0.5 | 2.5233E-05 | 2.8252E-05 | 2.5759E-05 | 2.6490E-05 |

| 21 days | 0 | 2.3406E-05 | 2.8047E-05 | 2.4988E-05 | 2.5914E-05 |

| 21 days | -0.5 | 2.3692E-05 | 2.8603E-05 | 2.5248E-05 | 2.6173E-05 |

Appendix A A Equivalence of the Approximated Optimal Bandwidth

In Section 2, we proposed several assumptions on the volatility processes, which, as shown in Section 3, are enough to construct a well posed optimal kernel estimation problem. In this subsection, we compare the performance of the resulting approximated optimal bandwidth to that of the true optimal bandwidth, whenever it exists.

In what follows, stands for the “the true” optimal bandwidth, which is defined to “minimize” the actual MSE of the kernel estimator, . However, since the mapping is not continuous, it is possible that such a global minimum might not exist or be unique. Hence, in what follows, is an extended nonnegative real number such that for a sequence satisfying that and a sequence of positive reals converging to . Let us also recall that denotes the approximated optimal bandwidth given by (23). Our goal is to find the relationship between and , and between and .