Polynomial jump-diffusions on the unit simplex111Acknowledgment: The authors wish to thank Thomas Bernhardt and Thomas Krabichler for useful comments and fruitful discussions. Martin Larsson and Sara Svaluto-Ferro gratefully acknowledges financial support by the Swiss National Science Foundation (SNF) under grant 205121_163425.

Abstract

Polynomial jump-diffusions constitute a class of tractable stochastic models with wide applicability in areas such as mathematical finance and population genetics. We provide a full parameterization of polynomial jump-diffusions on the unit simplex under natural structural hypotheses on the jumps. As a stepping stone, we characterize well-posedness of the martingale problem for polynomial operators on general compact state spaces.

Keywords:

Polynomial processes, unit simplex, stochastic models with jumps,

Wright-Fisher diffusion, stochastic invariance

MSC (2010) Classification: 60J25, 60H30

1 Introduction

Tractable families of Markov processes on the unit simplex, featuring both diffusion and jump components, are challenging to construct, yet play an important role in a host of applications. These include population genetics (Etheridge, 2011; Epstein and Mazzeo, 2013), dynamic modeling of probabilities (Gourieroux and Jasiak, 2006), and mathematical finance, in particular stochastic portfolio theory (Fernholz, 2002; Fernholz and Karatzas, 2005). The present article addresses this challenge by specifying Markovian jump-diffusions on the unit simplex that are polynomial, meaning that the (extended) generator maps any polynomial to a polynomial of the same or lower degree.

Polynomial processes were introduced in Cuchiero et al. (2012), see also Filipović and Larsson (2016), and are inherently tractable. Indeed, any polynomial jump-diffusion

-

(i)

is an Itô semimartingale, meaning that its semimartingale characteristics are absolutely continuous with respect to Lebesgue measure. This justifies the name jump-diffusion in the sense of Jacod and Shiryaev (2003, Chapter III.2);

-

(ii)

admits explicit expressions for all moments in terms of matrix exponentials.

The computational advantage associated with the second property has been exploited in a large variety of problems. In particular, applications in mathematical finance include interest rates (Delbaen and Shirakawa, 2002; Filipović et al., 2017), credit risk (Ackerer and Filipović, 2016), stochastic volatility models (Ackerer et al., 2016), stochastic portfolio theory (Cuchiero, 2017; Cuchiero et al., 2016), life insurance liabilities (Biagini and Zhang, 2016), and variance swaps (Filipović et al., 2016).

In addition, polynomial jump-diffusions are highly flexible in that they allow for a wide range of state spaces – the unit simplex being one of them – and a multitude of possible jump and diffusion phenomena. This stands in contrast to the thoroughly studied and frequently used sub-class of affine processes. Any affine jump-diffusion that admits moments of all orders is polynomial, but there are many polynomial jump-diffusions that are not affine. In particular, an affine process on a compact and connected state space is necessarily deterministic; see Krühner and Larsson (2017). Thus our interest in the unit simplex forces us to look beyond the affine class.

Polynomial diffusions (without jumps) on the unit simplex have already appeared numerous times in the literature. In population genetics, prototypical diffusion processes on the unit simplex known as Wright-Fisher diffusions, or Kimura diffusions, arise naturally as infinite population limits of discrete Wright-Fisher models for allele prevalence in a population of fixed size; see Etheridge (2011) for a survey. In finance, similar processes have appeared in Gourieroux and Jasiak (2006) under the name of multivariate Jacobi processes. All these diffusions turn out to be polynomial, and a full characterization is provided in Filipović and Larsson (2016, Section 6.3) by means of necessary and sufficient parameter restrictions on the drift and diffusion coefficients. One could also study other compact state spaces, as has been done in Larsson and Pulido (2017), where polynomial diffusions on compact quadric sets are considered.

As these papers all focus on the case without jumps, it is natural to ask what happens in the jump-diffusion case, where the literature is much less developed. This case is considered by Cuchiero et al. (2012), however without treating questions of existence, uniqueness, and parameterization for polynomial jump-diffusions on specific state spaces. To analyze these questions on the unit simplex, the technical difficulties associated with the diffusion case remain, arising from the fact that the unit simplex is a non-smooth stratified space (Epstein and Mazzeo, 2013, Chapter 1), and that the diffusion coefficient degenerates at the boundary. This complicates the analysis, and precludes the use of standard results regarding existence and regularity of solutions to the corresponding Kolmogorov backward equations. Additionally, in the jump case, the drift and diffusion interact with the (small) jumps orthogonal to the boundary, which leads to further mathematical challenges.

Allowing for jumps is however not only of theoretical interest, but has practical relevance as well. A concrete illustration of this fact comes from stochastic portfolio theory (Fernholz, 2002; Fernholz and Karatzas, 2009), where one is interested in the market weights computed from the market capitalizations , , of the constituents of a large stock index such as the S&P 500 or the MSCI World Index. The time evolution of the vector of market weights is thus a stochastic process on the unit simplex (see Figure 2). To model the market weight process, polynomial diffusion models without jumps have been found capable of matching certain empirically observed features such as typical shape and fluctuations of capital distribution curves (Fernholz and Karatzas, 2005; Cuchiero, 2017; Cuchiero et al., 2016) when calibrated to jump-cleaned data. However, the absence of jumps is a deficiency of these models. Indeed, an inspection of market data shows that jumps do occur and are an important feature of the dynamics of the market weights. This is clearly visible in Figure 2 where, for illustrative purposes, we have extracted three companies from the MSCI World Index, whose market weights exhibit jumps in the period from August 2006 to October 2007. This application from stochastic portfolio theory underlines the importance of specifying jump structures within the polynomial framework. We elaborate on this in Section 7.1.

Another natural application of the results developed in this paper arises in default risk modeling following the framework of Jarrow and Turnbull (1998) and Krabichler and Teichmann (2017). One is then interested in modeling a -valued stochastic recovery rate which remains at level for extended periods of time, while occasionally performing excursions away from . Polynomial jump-diffusion specifications turn out to be capable of producing such behavior, while at the same time maintaining tractability. Further details are given in Section 7.2.

Let us now briefly summarize our main results. Our starting point is a linear operator whose domain consists of polynomials on a compact state space (initially general, but soon taken to be the unit simplex) and which maps polynomials to polynomials of the same or lower degree. We study the corresponding martingale problem for which well-posedness holds if and only if satisfies the positive maximum principle and is conservative. In this case it is of Lévy type, specified by a diffusion, drift, and jump triplet ; see Theorem 2.3 and Theorem 2.8. We emphasize that not only existence, but also uniqueness of solutions to the martingale problem is obtained. This is yet another attractive feature of polynomial jump-diffusions on compact state spaces; in general, uniqueness is notoriously difficult to establish in the absence of ellipticity or Lipschitz properties. Next, our main focus is on jump specifications with affine jump sizes, namely,

| (1.1) |

where is a non-negative measurable function, a Lévy measure and is of the affine form

| (1.2) |

see Definition 3.1. This is the most general specification in the class of jump kernels with polynomial dependence on the current state; see Theorem 3.3. Under the structural hypothesis of affine jump sizes, we classify all polynomial jump-diffusions on the unit interval (i.e. the unit simplex in ); see Theorem 4.3. This classification is subsequently extended – under an additional assumption – to higher dimensions; see Theorem 6.3. Referring to the unit interval for notational convenience, we can distinguish four types of jump-diffusions, in addition to the pure diffusion case without jumps:

-

Type 1: is constant and the support of is contained in ;

-

Type 2: is (essentially) a linear-rational function with a pole of order one at the boundary, and the process can only jump in the direction of the pole;

-

Type 3: is (essentially) a quadratic-rational function with a pole of order two in the interior of the state space. There is no jump activity at the pole, but an additional contribution to the diffusion coefficient.

-

Type 4: is a quadratic-rational function whose denominator has only complex zeros, and in (1.1) is of infinite variation.

This classification already gives an indication of the diversity of possible behavior, an impression which is strengthened in Section 5, where we provide a number of examples both with and without affine jump sizes. On the one hand, these examples clearly show that without any structural assumptions like (1.1)–(1.2), a full characterization of all polynomial jump-diffusions on the simplex, or even the unit interval, is out of reach. On the other hand, the examples illustrate the richness and flexibility of the polynomial class.

The remainder of the paper is organised as follows. Section 1.1 summarizes some notation used throughout the article. Section 2 is concerned with polynomial operators on general compact state spaces and their associated martingale problems. Section 3 introduces affine jump sizes. In Section 4 we classify all polynomial jump-diffusions on the unit interval with affine jump sizes. It is followed by Section 5 which deals with examples. Section 6 treats the simplex in arbitrary dimension. Finally, Section 7 discusses applications in stochastic portfolio theory and default risk modeling. Most proofs are gathered in appendices.

1.1 Notation

We denote by the natural numbers, the nonnegative integers, and the nonnegative reals. The symbols , , and denote the real, real symmetric, and real symmetric positive semi-definite matrices, respectively. For any subset , we let as usual denote the space of continuous functions on . For any sufficiently differentiable function we write for the gradient of and for the Hessian of . Next, stands for the th canonical unit vector, denotes the Euclidean norm of the vector , is the Kronecker delta, is the Dirac mass at , and is the vector whose entries are all equal to 1. We denote by the vector space of all polynomials on and the subspace consisting of polynomials of degree at most . A polynomial on is the restriction to of a polynomial . Its degree is given by

We then let denote the vector space of polynomials on , and write for those elements whose degree is at most . We frequently use multi-index notation so that, for instance, for .

2 Polynomial operators on compact state spaces

Let be a compact subset of that will play the role of the state space for a Markov process. Later we will specialize to the case where is the unit interval or the unit simplex. In this paper we are concerned with operators of the following type, along with solutions to the corresponding martingale problems.

Definition 2.1.

A linear operator is called polynomial if

Given a linear operator and a probability distribution on , a solution to the martingale problem for is a càdlàg process with values in defined on some probability space such that and the process given by

| (2.1) |

is a martingale with respect to the filtration for every . We say that the martingale problem for is well-posed if there exists a unique (in the sense of probability law) solution to the martingale problem for for any initial distribution on . If is polynomial, then is called a polynomial jump-diffusion; this terminology is justified by Theorem 2.8 and the subsequent discussion.

2.1 The positive maximum principle

Definition 2.2.

A linear operator satisfies the positive maximum principle if holds for any and with .

Roughly speaking, the positive maximum principle is equivalent to the existence of solutions to the martingale problem. A typical result in this direction is Theorem 4.5.4 in Ethier and Kurtz (2005). For polynomial operators on compact state spaces more is true: we also get uniqueness.

Theorem 2.3.

Let be a polynomial operator. The martingale problem for is well-posed if and only if and satisfies the positive maximum principle.

Proof.

The existence of a solution to the martingale problem for for any initial distribution on , is guaranteed by Theorem 4.5.4 and Remark 4.5.5 in Ethier and Kurtz (2005). To prove uniqueness in law, by compactness of it is enough to prove that the marginal mixed moments of any solution to the martingale problem for are uniquely determined by and ; see Lemma 4.1 and Theorem 4.2 in Filipović and Larsson (2016). To this end, fix any , let be a basis of , and set . The operator admits a unique matrix representation with respect to this basis, so that

where has coordinate representation , that is, ; cf. Section 3 in Filipović and Larsson (2016) and the proof of Theorem 2.7 in Cuchiero et al. (2012). Following the proof of Theorem 3.1 in Filipović and Larsson (2016) we use the definition of a solution to the martingale problem, linearity of expectation and integration, and the fact that polynomials on the compact set are bounded, to obtain

for any and any . For each fixed this yields a linear integral equation for , whose unique solution is . Consequently,

| (2.2) |

which in particular shows that all marginal mixed moments are uniquely determined by and , as required.

For the converse implication, observe that since every solution to the martingale problem for is conservative, the condition follows directly by the martingale property of (2.1) with . The necessity of the positive maximum principle is standard; see for instance the proof of Lemma 2.3 in Filipović and Larsson (2016). ∎

Remark 2.4.

Observe that a solution to the martingale problem is conservative by definition since it is supposed to take values in . This is reflected by the condition of Theorem 2.3 and in the definition of Lévy type operator in the next section. Let us remark that the condition in Theorem 2.3, namely that the positive maximum principle and are satisfied, is equivalent to the maximum principle, that is, holds for any and any with .

Remark 2.5.

While existence of a solution to the martingale problem is equivalent to the maximum principle in very general settings, it is remarkable that in the case of polynomial operators on compact state spaces uniqueness also follows. Indeed, without the assumption that is polynomial, it is well-known that the maximum principle is not enough to guarantee uniqueness. For example, with and , the functions and are two different solutions to the martingale problem for . In the polynomial case, well-posedness is deduced from uniqueness of moments, which is a consequence of (2.2). Let us emphasize that (2.2) gives more than mere uniqueness: it gives an explicit formula for computing the moments via a matrix exponential. This tractability is crucial in applications, and was used as a defining property of this class of processes in Cuchiero et al. (2012).

2.2 Lévy type representation

Definition 2.6.

An operator is said to be of Lévy type if it can be represented as

| (2.3) | ||||

where the right-hand side can be computed using an arbitrary representative of , and the triplet consists of bounded measurable functions and , and a kernel from into satisfying

| (2.4) |

Polynomial operators satisfying the positive maximum principle are always Lévy type operators, as is shown in Theorem 2.8 below. This parallels known results regarding operators acting on smooth and compactly supported functions, see Courrège (1965) or Böttcher et al. (2013, Theorem 2.21) for Feller generators, and also Hoh (1998). A crucial ingredient in the proof of Theorem 2.8 is the classical Riesz-Haviland theorem, which we now state. A proof can be found in Haviland (1935) and (1936), or e.g. Marshall (2008).

Lemma 2.7 (Riesz-Haviland).

Let be compact, and consider a linear functional . Then the following conditions are equivalent.

-

(i)

for all and a Borel measure concentrated on .

-

(ii)

for all such that on .

We now state Theorem 2.8 regarding the Lévy type representation of operators satisfying the positive maximum principle. The proof is given in Section A.

Theorem 2.8.

Consider a linear operator . If and satisfies the positive maximum principle, then is a Lévy type operator.

Suppose is a linear operator with that satisfies the positive maximum principle, and let be a solution to the associated martingale problem. Then is a semimartingale, as can be seen by taking in (2.1). We claim that its diffusion, drift, and jump characteristics (with the identity map as truncation function) are given by

where is the triplet of the Lévy type representation (2.3). To see this, first note that can be extended to functions on using (2.3). Then, an approximation argument shows that in (2.1) remains a martingale for such functions . The claimed form of the characteristics of now follows from Theorem II.2.42 in Jacod and Shiryaev (2003); see also Proposition 2.12 in Cuchiero et al. (2012). This justifies referring to as a polynomial jump-diffusion. Since the martingale problem is well-posed by Theorem 2.3, such a polynomial jump-diffusion is a Markov process, and hence a polynomial process in the sense of Cuchiero et al. (2012).

The following lemma provides necessary and sufficient conditions on the triplet in order that be polynomial.

Lemma 2.9.

Let be a Lévy type operator with triplet . Then is polynomial if and only if

for all and .

Proof.

This result is well-known, see for instance Cuchiero et al. (2012), and the proof is simple. Indeed, direct computation yields , , , and for . Thus, if is polynomial, one can show that the triplet satisfies the stated conditions. The converse implication is immediate from the observation that for any . ∎

2.3 Conic combinations of polynomial operators

Due to Theorem 2.3 and Theorem 2.8, every member of the set

is of Lévy type (2.3). The set also possesses the following stability properties, which are useful for constructing examples of polynomial jump-diffusions; we do this in Section 5. The proofs of the following two results are given in Section B.

Theorem 2.10.

The set is a convex cone closed under pointwise convergence, in the sense that if for and exists and is finite for all and , then .

If an operator is the limit of as in Theorem 2.10, then its triplet can be expressed in terms of the triplets of the operators .

Lemma 2.11.

Suppose that , and let , , and be the coefficients of its Lévy type representation, for all . Then exists and is finite for all and if and only if the coefficients

converge pointwise as for all and . In this case the triplet of the Lévy type representation of is given by

for all and , where the kernel is uniquely determined by

Remark 2.12.

The diffusion coefficient is the limit of if and only if the weak limit of exists and has no mass in zero. If the weak limit does have mass in zero, then this mass is equal to the difference between and the limit of .

3 Affine and polynomial jump sizes

Throughout this section we continue to consider a compact state space . In the absence of jumps it is relatively straightforward to explicitly write down a complete parametrization of polynomial diffusions on the unit interval or the unit simplex; see Filipović and Larsson (2016). With jumps this is no longer the case. Indeed, examples in Section 5 illustrate the diversity of behavior that is possible even on the simplest nontrivial state space . Therefore, in order to make progress we will restrict attention to specifications whose jumps are of the following state-dependent type. Consider a jump kernel from into satisfying (2.4).

Definition 3.1.

The jump kernel is said to have affine jump sizes if it is of the form

| (3.1) |

where is a nonnegative measurable function, is of the affine form

| (3.2) |

and is a measure on satisfying . Here we use the notation for the vector of coefficients appearing in (3.2).

Remark 3.2.

By (2.4) and compactness of , the measure can always be chosen compactly supported. In this case, all its moments of order at least two are finite.

Intuitively, (3.1) means that the conditional distribution of the jump , given that it is nonzero and the location immediately before the jump is , is the same as the distribution of under ; at least when is a probability measure. The jump intensity is state-dependent and given by , which may or may not be finite.

Jump kernels with affine jump sizes can be used as building blocks to obtain a large class of specifications by means of Theorem 2.10. The jump kernels obtained in this way are of the form

where each jump kernel has affine jump sizes. We refer to such specifications as having mixed affine jump sizes.

The affine form of is a particular case of the seemingly more general situation where is allowed to depend polynomially on the current state . However, this would not actually lead to an increase in generality in the context of polynomial jump-diffusions. Indeed, at least in the case when has nonempty relative interior in its affine hull, the following result shows that whenever jump sizes are polynomial, they are necessarily affine. The proof is given in Section C.

Theorem 3.3.

Assume that has nonempty relative interior in its affine hull. Let be a jump kernel from into of the form (3.1) and satisfying (2.4), where is nonnegative and measurable, is given by

for some , and is a measure on with . Assume also that satisfies

| (3.3) |

and that has nonempty interior. Then one can choose so that a.e. for all and all . That is, has affine jump sizes.

Remark 3.4.

Note that if has affine jump sizes and satisfies (3.3), then the function is can be expressed as the ratio of two polynomials of degree at most four,

at points where the denominator is nonzero. At points where the denominator vanishes, we have for -a.e. , whence due to (3.1). Thus we may always take at such points.

Remark 3.5.

Jump specifications of the form (3.1) are convenient from the point of view of representing solutions to the martingale problem for as solutions to stochastic differential equations driven by a Brownian motion and a Poisson random measure. Indeed, such a stochastic differential equation has the following form:

where denotes the matrix square root, is a -dimensional Brownian motion and is a Poisson random measure on whose intensity measure is . See also, for instance, Dawson and Li (2006, Section 5), regarding analogous representations of affine processes. Note that a representation of the form (3.1) always exists, even with , if one allows to lie a suitable Blackwell space; see Jacod and Shiryaev (2003, Remark III.2.28). Thus, in view of Theorem 3.3, our restriction to affine jump sizes in the sense of Definition 3.1 is essentially equivalent to a polynomial dependence of on , somewhat generalized by allowing a state dependent intensity . Note also that once depends polynomially on , there is no loss of generality to assume that lies in an Euclidean space.

4 The unit interval

Throughout this section we consider the state space

Our goal is to characterize all polynomial jump-diffusions on with affine jump sizes. The general existence and uniqueness result Theorem 2.3, in conjunction with Lemma 2.9, leads to the following refinement of Theorem 2.8, characterizing those triplets that correspond to polynomial jump-diffusions. The proof is given in Section D.

Lemma 4.1.

Observe that condition (i) guarantees that is of Lévy Type.

Remark 4.2.

Condition (ii) implies that for . Intuitively, this means that the solution to the martingale problem for has a purely discontinuous martingale part which is necessarily of finite variation on the boundary of .

We now turn to the setting of affine jump sizes in the sense of Definition 3.1. We thus consider Lévy type operators of the form

| (4.1) | ||||

where is nonnegative and measurable, and is affine in . The main result of this section, Theorem 4.3 below, shows that the generator must be of one of five mutually exclusive types, which we now describe.

Type 0.

Let , , where , , and , and set . Then is a polynomial operator whose martingale problem is well-posed. The solution corresponds simply to the well-known Jacobi diffusion, which is the most general polynomial diffusion on the unit interval.

Type 1.

Let , , and , where , , and . Furthermore, writing we define and let be a nonzero measure on . If the boundary conditions

are satisfied, then is a polynomial operator whose martingale problem is well-posed.

Note that the boundary conditions imply that is bounded. Thus, the resulting process behaves like a Jacobi diffusion with summable jumps. The arrival intensity of the jumps is , which may or may not be finite. Figure 5 illustrates the form of , and the support under .

Type 2.

Let , , and where , , , and . Furthermore, define and let be a nonzero square-integrable measure on . Notice that is scalar. If the boundary condition

is satisfied, then is a polynomial operator whose martingale problem is well-posed.

The boundary condition implies, if , that is bounded. Thus, in this case, the solution to the martingale problem for has summable jumps. If , the jumps need not be summable. The arrival intensity of the jumps is and hence, even if is a finite measure, the jump intensity is unbounded around . Moreover, due to the form of , can only jump to the left, and since , cannot leave by means of a jump. Figure 5 illustrates the form of , and the support under .

By reflecting the state space around the point , we obtain a similar structure which we also classify as Type 2, where now the jump intensity is unbounded around . The diffusion and drift coefficients remain as before, while for some , the jump sizes are , and is a nonzero square-integrable measure on as before. The boundary condition becomes .

Type 3.

Let ; this will be a “no-jump” point. Let and set

where , , and are real numbers such that the numerator of is nonnegative on without zeros at . Furthermore, define , and let be a nonzero square-integrable measure on . Finally, let where

If the boundary conditions

are satisfied, then is a polynomial operator whose martingale problem is well-posed.

If for some constant , the solution to the martingale problem for may have non-summable jumps. If the numerator of is not of this form, then the boundary conditions imply that has summable jumps. The arrival intensity of the jumps is

As a result, even if is a finite measure, the jump intensity has a pole of order two at , which results in a contribution of size to the diffusion coefficient. Moreover, due to the form of , the jumps of are always in the direction of the “no-jump” point . Although the jumps may overshoot , they always serve to reduce the distance to . In particular, since , cannot leave by means of a jump. Figure 5 illustrates the form of , and the support under .

Type 4.

Suppose is a non-real complex number such that and let be a nonzero square-integrable measure on such that

| (4.2) |

and . Let and set

where , , and . Furthermore, define and let

for some . Then is a polynomial operator whose martingale problem is well-posed.

Having described five types of processes which are polynomial jump-diffusions due to the conditions of Lemma 4.1, we are now ready to state the converse result, namely that all polynomial jump-diffusions on with affine jump sizes are necessarily of one of these types. The proof is given in Section D.

Theorem 4.3.

Let be a polynomial operator whose martingale problem is well-posed. If the associated jump kernel has affine jump sizes, then necessarily belongs to one of the Types 0-4.

Remark 4.4.

Let us end this section with some remarks regarding Type 4. First, note that implies that cannot be a product measure since in this case would be infinite too, which however contradicts square integrability. Second, after passing to polar coordinates , the condition (4.2) becomes

| (4.3) |

where is the compactly supported measure given by

for all measurable subsets . It can then be shown that and cannot be independent, i.e., cannot be a product measure. These observations indicates that natural attempts to find combinations of and satisfying (4.2) do not work. In fact, it is unknown to us what a potential example of Type 4 might look like. Note also that Type 4 is distinct from all other types in the following respect. For Types 1–3, is a polynomial on (outside the “no-jump” point) of degree for all , whereas for Type 4 this property holds true only for the integrated quantity .

5 Examples of polynomial operators on the unit interval

In this section we present a number of examples that illustrate the diverse behavior of polynomial jump-diffusions on . While the diffusion case is simple – the Jacobi diffusions (Type 0) are the only possibilities – the complexity increases significantly in the presence of jumps. For instance, in Example 5.5 we obtain jump intensities with a countable number of poles in the state space.

5.1 Examples with affine jump sizes

Example 5.1.

We start with a well-known example of a polynomial jump-diffusion on ; see Cuchiero et al. (2012, Example 3.5). Consider the Jacobi process, which is the solution of the stochastic differential equation

where and . This process can also be regarded as the unique solution to the martingale problem for , with the Type 0 operator

This example can be extended by adding jumps, where the jump times correspond to those of a Poisson process with intensity and the jump size is a function of the process level. One can for instance specify that if a jump occurs, then the process is reflected in . In this case the process would be the unique solution to the martingale problem for , where

which is an operator of Type 1 with , , , and . ∎

Example 5.2.

The following example features a simple state-dependent jump distribution. Consider a Lévy type operator whose jump kernel is chosen such that is uniformly distributed on , where and for all . This in particular implies that and can be written as

for some and . Choosing the drift coefficient suitably, the operator is then of Type 1 for being the pushforward of the uniform distribution on under the map .

The solution to the corresponding martingale problem is a Jacobi process extended by adding jumps, where the jump times correspond to those of a Poisson process with unit intensity, and the jump’s target point is uniformly distributed on , given that the process is located at immediately before the jump. ∎

Example 5.3.

Polynomial operators are not always easy to recognize at first sight. Consider a Lévy type operator whose diffusion and drift coefficients and are zero, and whose jump kernel is given by

Despite the presence of the sine function, the operator satisfies all the conditions of Lemma 4.1. It is thus polynomial and its martingale problem is well-posed. In fact, this operator is of Type 2. Using the periodicity of the sine function, one can show that has affine jump sizes with , , and being the pushforward of Lebesgue measure on under the map . The associated polynomial jump-diffusion is a martingale since . Moreover, the arrival intensity of the jumps is given by , which is unbounded around zero. ∎

Example 5.4.

The Dunkl process with parameter is a polynomial jump-diffusion on , see e.g. Cuchiero et al. (2012, Example 3.7), and can be characterized as the unique martingale whose absolute value is the Bessel process of dimension ; see Gallardo and Yor (2006). The corresponding polynomial operator is of Lévy type with diffusion and jump coefficients and , and jump kernel

The arrival intensity of its jumps is thus given by , which is a rational function with a pole of second order in .

Observe that exhibits several similarities with jump kernels of operators of Type 3, such as the form of the arrival intensity of the jumps, and the extra contribution to the diffusion coefficient at the “no-jump” point . In fact, defining and

we obtain a polynomial operator of Type 3 with “no-jump” point . ∎

5.2 Constructions using conic combinations

We provide two examples illustrating the usefulness of Theorem 2.10 for combining operators with affine jump sizes to achieve specifications with interesting properties.

Example 5.5.

We now construct a polynomial operator whose martingale problem is well-posed, such that the arrival intensity of the jumps is unbounded around infinitely many points, but finite for all .

Let , , be operators of Type 3 with “no-jump” points . Let their diffusion coefficients be given by

the drift coefficients be 0, and the parameters of the jump kernels be given by

and be Lebesgue measure on . Note that for all we have

| (5.1) |

By Theorem 2.10 and Lemma 2.11 this implies that the operator is again polynomial and its martingale problem is well-posed. In particular, is a Lévy type operator with coefficients and , and jump kernel . As a result, the arrival intensity of the jumps is given by

which is unbounded around each but finite for all . At the jump intensity is infinite. Figure 6 contains an illustration. ∎

Example 5.6.

This example shows that the operator of a polynomial diffusion, or equivalently an operator of Type 0, can always be written as the limit of “pure jump” polynomial operators, i.e. with zero diffusion coefficients. Consider the Jacobi diffusion with operator given by

for some , , and . Let then be an operator of Type 2 and suppose that its diffusion coefficient is zero, the drift coefficient is given by , and the parameters of the jump kernel are

Observe that, trivially, we have . Also,

By Lemma 2.11 we thus conclude that in sense of Theorem 2.10. ∎

5.3 Mixed affine jump sizes

Consider now a Lévy type polynomial operator whose jump kernel has mixed affine jump sizes in the sense of Section 3, i.e.,

| (5.2) |

where each kernel has affine jump sizes. Suppose the martingale problem for is well-posed, or equivalently, its triplet satisfies the conditions of Lemma 4.1. A natural question is now whether the individual kernels also satisfy the conditions of Lemma 4.1. If this were to be true, it would have the pleasant consequence that could be represented as a sum of operators of Types 0–4. Unfortunately this is not the case, which we illustrate in Example 5.7 below. In fact, there exist kernels of the form (5.2) that cannot even be obtained as an infinite conic combination of the kernels appearing in Types 0–4.

Example 5.7.

Consider a Lévy type operator , whose coefficients are given by , , and whose jump kernel is given by (5.2) for , where and have affine jump sizes with parameters , , and , . Observe that

One can verify that satisfies all the conditions of Lemma 4.1, and is thus polynomial and its martingale problem is well posed.

Assume now for contradiction that for some kernels that satisfy the conditions of Lemma 4.1 for some coefficients and . By Theorem 4.3, each then follows one of Types 0–4. Let and be the parameters of the jump kernel .

Since , we also have for all , or equivalently,

| (5.3) |

for some . This already excludes that is of Type 3 or 4, and gives us that for all

for some and . In particular note that for all and ,

| (5.4) |

and hence, since is closed under pointwise convergence,

for all and some . Since by assumption, we obtain

for all , . The shortest way to see that this condition cannot be satisfied is to use that if two polynomials coincide on they have to coincide on , too. But, choosing we obtain

for all , which is clearly not possible. ∎

Example 5.8.

It is possible to show that operators with jump kernels of the form (5.2) can have intensities with multiple poles of multiple order outside the state space. On the other hand, under some non-degeneracy conditions, they can only have a single pole of order at most 2 inside the state space. We develop this idea in more detail for the case when consists of finitely many atoms for all .

Let be an operator of the form described in Lemma 4.1 and suppose that its jump kernel is supported on , where , , are pairwise distinct polynomials with for all . As a result, we have

| (5.5) |

for some functions . For , set , and recall that for all and that is bounded on . Using the nonnegativity of and the boundary conditions for , one can then establish the following properties, which we state here without proof.

-

(i)

If has a pole at a point , then . Moreover in this case, analogously to Types 2 and 3, if , the order of the pole is 1 and if , the order of the pole is 2. Note that nonnegativity of and the fact that imply that can have a pole in at most one point of the state space.

-

(ii)

, where denotes the zero of , and we have

(5.6) where and on it is given by

- (iii)

Conversely, fix a sequence of polynomials , , such that for all . If for some affine functions as above, the functions given by equation (5.6) satisfy (i) and are all nonnegative on , one can conclude that for as in (5.5), as in (5.7), and a suitably chosen , the corresponding Lévy type operator is polynomial and its martingale problem is well-posed. ∎

Remark 5.9.

It is interesting to observe that Shur polynomials appear naturally in the context of Example 5.8. Indeed, by point (ii) we know that each , and thus every moment of the measures , is uniquely determined by and . More precisely for all we can write

where is the partition given by

and is the corresponding Shur polynomial.

We now propose two interesting applications of Example 5.8, showing that it can happen that have poles of high order and in several points outside the state space.

Example 5.10.

Consider a kernel of the form described in (5.5) for

Defining through expression (5.6) where we set

we obtain

for all . Note that the rational functions satisfy point (i) of Example 5.8 and are all nonnegative on . As a result, choosing the diffusion and drift coefficients suitably, is a polynomial operator whose martingale problem is well-posed. Observe that each has a pole in and . ∎

Example 5.11.

Consider a kernel of the form described in (5.5) for

Defining through expression (5.6) where we set

we obtain

for all . Note that the rational functions satisfy point (i) of Example 5.8 and are all nonnegative on . As a result, choosing the diffusion and drift coefficients suitably, is a polynomial operator whose martingale problem is well-posed. Observe that each has a pole of second order in . ∎

6 The unit simplex

Throughout this section the state space is the unit simplex of dimension , which we denote by

Similarly as in Section 4 our goal is to provide a characterization of polynomial jump-diffusions on with affine jump sizes. Again, we combine Theorem 2.3 and Lemma 2.9 to specialize Theorem 2.8 to the state space . The proof is given in Section E.

Lemma 6.1.

Observe that conditions (i) and (iii) guarantee that is of Lévy Type. This in particular ensures that the right-hand side of (2.3) can be computed using an arbitrary representative.

Remark 6.2.

Condition (ii) implies that for all . Analogously to the unit interval case, this give us some intuition about the behavior of the solution on the boundary segment . Indeed, even if the component orthogonal to the boundary of the purely discontinuous martingale part of is necessarily of finite variation, the other components do not need to satisfy this property. Moreover, since , condition (ii) also implies that for all .

We now focus on the setting of affine jump sizes in the sense of Definition 3.1. We thus consider Lévy type operators of the form

| (6.1) | ||||

where is nonnegative and measurable, and is affine in . In order to describe the form of the jump sizes, let us introduce the set which is given by

Type 0.

For some , , such that for and , let

| (6.2) | ||||

| (6.3) |

and set . Then is a polynomial operator whose martingale problem is well-posed. The solutions are multivariate Jacobi-type diffusion processes which have been characterized in this form by Filipović and Larsson (2016, Section 6.3). In the special case where for all , they correspond to Wright-Fisher diffusions, which are also known under the name multivariate Jacobi process; see Gourieroux and Jasiak (2006).

Type 1.

Let and be given by (6.2) and (6.3). For all set

| (6.4) |

and let be a nonzero measure on . If the boundary conditions

hold for all , then is a polynomial operator whose martingale problem is well-posed.

Note that the boundary conditions imply that

is bounded. Hence the resulting process behaves like a multivariate Jacobi-type diffusion process in the spirit of Filipović and Larsson (2016, Section 6.3), generalized to include summable jumps. The arrival intensity of the jumps is , which may or may not be finite.

Type 2.

Fix . Let be given by (6.2) and (6.3), and let for some nonnegative such that is not constant on . Furthermore, for we define

and let be a nonzero square-integrable measure on . If the boundary conditions

| (6.5) |

hold for all and , then is a polynomial operator whose martingale problem is well-posed.

If for some and , the jumps need not to be summable. More precisely, we can have . Otherwise, if is not proportional to on for any , the expression is bounded, and the solution to the martingale problem for has thus summable jumps. Indeed,

which is bounded due to (6.5) and the existence of some such that ; see Lemma E.1 in Section E for more details on the second point.

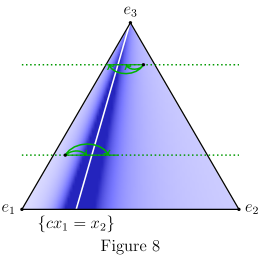

The arrival intensity of the jumps is and hence, even if is a finite measure, the jump intensity is unbounded around . Moreover, due to the form of , can only jump in the direction of the boundary segment , and since whenever , cannot leave this boundary segment by means of a jump. Figure 8 illustrates the form of and the support of under .

Type 3.

Let be such that , and fix some constant . Consider the hyperplane which will be a “no-jump” region. Let be given by (6.3) and set

for some given by , where are chosen such that is nonnegative, and nonconstant on . Furthermore, define

and let be a nonzero square-integrable measure on . Finally, let

where is of form (6.2), is a symmetric matrix given by , , and if , and where

If the boundary conditions

| (6.6) |

are satisfied for all and , then is a polynomial operator whose martingale problem is well-posed. Note in particular that for , the condition (6.6) coincides with on .

If the numerator of is of the form for some , the solution to the martingale problem for may have nonsummable jumps. If is not of this form, then by similar reasoning as for Type 2, the boundary conditions imply that and thus has summable jumps. The arrival intensity of the jumps is

As a result, even if is a finite measure, the jump intensity has a singularity of order two along , which results in a contribution of to the diffusion coefficient. Moreover, due to the form of , the jumps of are always in the direction of the “no-jump” hyperplane . Although the jumps may overshoot , they always serve to reduce the distance to . In particular, since for all , cannot leave by means of a jump. Figure 8 illustrates the form of and the support of under .

In order to simplify the analysis, in particular in view of the arguments outlined in Remark 4.4, we do not consider operators corresponding to Type 4 on the unit simplex. A condition on the jump kernel excluding this class is given by the following assumption.

Assumption A.

The condition holds for all and all .

The polynomial property of implies that the integrated quantities lie in . Assumption A strengthens this by requiring that the functions themselves lie in . This is a natural assumption, in particular in view of Types 1-3 on the unit interval. Moreover, it will turn out in the course of the proof of Theorem 6.3 that Assumption A implies under the condition of affine jump sizes and nonconstant that

where is a -measurable function and . Analogous to the unit interval, the “no-jump” region is the intersection of with the hyperplane given by the zero set of a polynomial of first degree. The following theorem states the announced characterization of polynomial jump-diffusions with polynomial jump sizes under Assumption A. The proof is given in Section E.

Theorem 6.3.

Let be a polynomial operator whose martingale problem is well-posed. If the associated jump kernel has affine jump sizes and satisfies Assumption A, then necessarily belongs to one of the Types 0-3.

7 Applications

In this section we outline two natural applications in finance of polynomial jump-diffusions on the unit simplex. The first application concerns stochastic portfolio theory, while the second application is in the area of default risk.

7.1 Market weights with jumps in stochastic portfolio theory

In the context of stochastic portfolio theory (SPT), polynomial diffusion models for the process of market weights have been found capable of matching certain empirically observed properties when calibrated to jump-cleaned data; see Cuchiero (2017); Cuchiero et al. (2016). This concerns the typical shape and dynamics of the capital distribution curves, but also features such as high volatility for low capitalized stocks. As mentioned in the introduction, a crucial deficiency of these models is the lack of jumps since they are present in typical market data; see Figure 2.

We now demonstrate how the results of Section 6 can be used to construct polynomial jump-diffusion models for the market weights. We focus on a concrete specification that extends the volatility stabilized models introduced by Fernholz and Karatzas (2005) by including jumps of Type 2. In the standard (diffusive) volatility stabilized model, the market weights follow a Wright-Fisher diffusion, which is a special case of Type 0 with parameters

for some . These models have two key properties which are of particular relevance in SPT: First, the market weights remain a.s. in the relative interior of , denoted by . Second, the model allows for relative arbitrage opportunities. We may preserve these features by adding jumps of Type 2. More precisely, we consider a model for the market weights of the form

where denotes the integer-valued random measure associated to the jumps of , and a -dimensional standard Brownian motion. The jump specification is given as a sum of Type 2 jumps,

where for some nonnegative such that is not constant on , and the measures are supported on and satisfy . Economically, this specification means that downward jumps occur with higher and higher intensity the closer the assets are to , and can therefore be used to model downward spirals in stock prices. We require that for all ,

which ensures that remains in the relative interior . This can be proved similarly as in Filipović and Larsson (2016, Theorem 5.7). Furthermore, this model admits relative arbitrage opportunities. To see this, we argue that no equivalent probability measure can turn into a martingale. Indeed, Lemma 5.6 in Cuchiero (2017) implies that, under any martingale measure, must reach the relative boundary of with positive probability on any time horizon, contradicting equivalence. Since no equivalent martingale measure exists for the market weights, the model admits relative arbitrage.

Clearly any other polynomial diffusion model on the simplex can be enhanced by jumps of this form, which yields a large class of tractable jump-diffusion models applicable in the realm of SPT.

7.2 Valuation of defaultable zero–coupon bonds

Polynomial jump-diffusions on the unit interval can be brought to bear on default risk modeling. We consider the stochastic recovery rate framework of Jarrow and Turnbull (1998) and Krabichler and Teichmann (2017). For further references, see also Filipović and Trolle (2013), Zheng (2006), and Jeanblanc et al. (2009, Chapter 7) for an overview, as well as Duffie (2004) for the classical approach using affine processes. Note also that polynomial diffusion models for credit risk have appeared in Ackerer and Filipović (2016).

Let with be a filtered probability space satisfying the usual conditions. Here is a risk neutral measure. Let be the value of the risk-free bank account with initial value of one monetary unit. For any , we denote by the price at time of a defaultable zero–coupon bond with maturity and unit notional. Due to default risk, its actual payoff at maturity is random and lies between zero and one. Under the premise that all discounted defaultable zero–coupon bond prices are true martingales under , we get

where is known as the recovery rate. Suppose now for simplicity that and are conditionally independent under . Then

where is the price of a non-defaultable zero–coupon bond with maturity and unit notional.

Motivated by the typically long and complicated unwinding process after a default occurs, Krabichler and Teichmann (2017) drop the assumption that the recovery rate is known when default happens. Excursions of below 1 are interpreted as liquidity squeezes resulting in a delay of due payments, which may or may not turn into a default. In this framework, the risk-neutral recovery rate typically starts with a constant trajectory at level 1. Once the recovery has jumped below 1, it pursues an unsteady course. Downward moves of the recovery rate are self-exciting, as deterioration of the counterparty’s credit quality typically makes full recovery more unlikely. Nonetheless, may return to 1 and remain there for some period of time.

A polynomial model for the recovery rate can be constructed as follows. Let be a polynomial jump-diffusion of Type 2 with “no-jump” point . Assume that ; this condition guarantees that if reaches level 1, it can leave it only by means of a jump. More precisely, persists at level 1 until its first jump, which occurs according to an –exponentially distributed stopping time and a downward -distributed jump size. Moreover, since the jump intensity is the positive branch of a hyperbola with a pole in zero, downward jumps of get more and more likely as the process approaches zero.

In view of the discussion above, polynomial transformations of , where is increasing and satisfies , are well-suited to describe the recovery rate. The polynomial property of permits to express the forward recovery rate in closed form. We provide two concrete specifications, by choosing and . In the first case, , the moment formula (2.2) yields

In the second case, , we find

where and .

Appendix A Proof of Theorem 2.8

We assume that is a linear operator that satisfies the positive maximum principle and .

Fix and define the linear functionals for by

as well as for by

Here and throughout the proof we view as a polynomial on to avoid the more cumbersome notation .

If on , then is minimal at , which by the positive maximum principle yields . The Riesz-Haviland theorem, Lemma 2.7, thus provides measures concentrated on such that

By polarisation we have , whence

The triplet is now defined at by

| (A.1) |

and

Next, observe that

for all . By Weierstrass’s theorem and dominated convergence, this actually holds for all , whence . Consequently,

| (A.2) |

Consider now any polynomial , and choose a representative , . Note that is of the form

for some polynomials . Let . Then the linearity of , the fact that , and (A.1) and (A.2) yield

Thus, with for a polynomial , we obtain the desired form (2.3), where the right-hand side is computed using a representative of , the choice of which is arbitrary.

It remains to verify that the , , and satisfy the additional stated properties. First, is positive semidefinite since , and clearly satisfies the support conditions and . Next, since maps polynomials to continuous functions, it is clear from (A.1) that is bounded and measurable. Similarly, is continuous, hence bounded and measurable, for every , and so by the monotone class theorem is measurable for every Borel set . Thus is a kernel, from which it follows that is measurable and is a kernel. Finally, continuity in of

implies that and are bounded on . ∎

Appendix B Proof of Theorem 2.10 and Lemma 2.11

Proof of Theorem 2.10.

Let and , and fix for some . Then, since , we have that

as well, proving that it is polynomial. By Theorem 2.3, the well-posedness of the martingale problem for follows directly by the well-posedness of the martingale problems of and . For the second part, set as in the statement of the theorem and recall that is closed under pointwise convergence for each . Fixing , since by the polynomial property of , we can conclude that as well. Again, existence and uniqueness of a solution to the martingale problem is guaranteed by Theorem 2.3, since and the positive maximum principle is preserved in the limit. ∎

Proof of Lemma 2.11.

In order to prove the first part of the lemma, it is enough to observe that for all and ,

| (B.1) |

For the second part of the lemma, if is well-defined we know from Theorem 2.10 that it has a Lévy-Khintchine representation, for some coefficients and , and a kernel . As a result, the analog of (B.1) holds true for and by definition of the limit we thus obtain

and similarly

| (B.2) |

for all . Since does not have mass in 0, . Moreover, using that moments completely determine compactly supported finite distribution, the kernel , and thus , is uniquely determined by (B.2). ∎

Appendix C Proof of Theorem 3.3

Throughout the proof we assume without loss of generality that has nonempty interior. Suppose that is the zero measure for all . Setting , the form of and the measure are irrelevant and we are thus free to choose . We may therefore suppose that is nonzero for some , and thus in particular

| (C.1) |

for at least one . As in Remark 3.2, we can assume without loss of generality that is compactly supported and hence all its moments of order at least two are finite. Set then

and note that, by the integrability conditions on and condition (3.3) respectively, and are polynomials on for all . In particular, is a nonzero polynomial for at least one by (C.1), and thus

| (C.2) |

for all .

Since has nonempty interior by assumption, each polynomial has a unique representative such that . In particular, the degree of a polynomial on always coincides with the maximal degree of its monomials. Assume now for contradiction that cannot be chosen less than or equal one. Let

be the multi-index corresponding to the leading monomial of , with respect to some graded lexicographic order. Choose such that and note that by the maximality of and since we have that

Analogously, and thus (C.2) holds true for . Since , using that we can compute

and obtain the desired contradiction. As a result, can always be chosen smaller than or equal one. ∎

Appendix D The unit interval: Proof of Lemma 4.1 and Theorem 4.3

Proof of Lemma 4.1.

Assume is a polynomial operator and its martingale problem is well-posed. Theorem 2.3 and Theorem 2.8 imply that is of Lévy type for some triplet , so that in particular (i) holds. Condition (iii) follows from Lemma 2.9. To verify (ii), let be polynomials on with , , , and for . For example, one can choose . Let . Then has a minimum at , so by the positive maximum principle,

where the dominated convergence theorem was used to pass to the limit. Similarly, is nonnegative on with a minimum at , so the monotone convergence theorem yields

We have thus shown (ii) for the boundary point . The case is similar.

We now prove the converse. Lemma 2.9 and (iii) imply that is polynomial. Next, clearly . Thus, by Theorem 2.3 it only remains to verify the positive maximum principle in order to deduce that the martingale problem for is well-posed. To this end, let be an arbitrary polynomial having a maximum over on some . If it follows that , , and for all . Hence, using that on , we conclude that . On the other hand, if we use that and the integrability of with respect to to write

The Karush-Kuhn-Tucker conditions (see e.g. Proposition 3.3.1 in Bertsekas (1995)) imply that if and if , and thus the first summand is nonnegative by (ii). Using as before that for all , we conclude that . ∎

Proof of Theorem 4.3.

By assumption is polynomial and its martingale problem is well-posed. Hence, conditions (i)-(iii) of Lemma 4.1 are satisfied. As in Remark 3.2, we can assume without loss of generality that is compactly supported. In particular, all its moments of order at least two are finite. For all set then

| (D.1) |

Note that for all by the integrability conditions on , and for all by condition (iii) of Lemma 4.1. By Remark 3.4 we know that

and hence the condition of (2.4) implies that can be chosen to be supported on and such that -a.s. By Lemma 4.1(iii) we also know that and, by Lemma 4.1(ii), that the boundary conditions

| (D.2) |

hold. We consider now five complementary assumptions, which will lead to Types 0 to 4.

Assume that . Then Lemma 4.1 implies that for some . This proves that is an operator of Type 0.

Assume now that and can be chosen to be constant. We can then without loss of generality set . Moreover, since in this case , we can conclude as before that for some . This proves that is an operator of Type 1.

Assume that , cannot be chosen to be constant, and for some . By definition of this automatically implies that , and in particular , for -a.e. . As a result, lies in , and setting we obtain . Moreover, since -a.s., we can conclude that it is square-integrable and takes values in the set -a.s. By (D.1) we can then write

for some , for all . Since in this case we are free to choose . By Lemma 4.1 we also know that is bounded on . Therefore, noting that

it follows that , and thus for some and all in . This in particular implies that and hence . Knowing that has to be continuous by condition (iii) of Lemma 4.1, we can finally deduce that

Suppose now . Then, since on and , we conclude that , for some , and thus for some . For , respectively , the nonnegativity of implies that , respectively , for some . As a result, is an operator of Type 2.

On the other hand, if , using again that on and , we conclude that

for some , proving that is an operator of Type 3.

Assume now that , cannot be chosen to be constant, and for all . We must argue that is then necessarily of Type 4. By (D.1) we have on , and thus on . Consequently, is locally bounded, nonnegative, and non-constant. Moreover, (D.1) yields the expression for all with . These facts combined with the fundamental theorem of algebra imply that

| (D.3) |

for some positive and . Without losing generality we choose to satisfy . Note that no further cancellation of polynomial factors is possible in (D.3) since is non-constant. Furthermore, condition (iii) of Lemma 4.1 yields for all . Therefore, since due to (D.1) and (D.3), it follows that for all and , for some . This already implies (4.2) for , i.e.,

| (D.4) |

Next, we will establish (4.2) also for . In preparation for an application of Lemma D.1 later on, choose a constant such that

| (D.5) |

for all . Define

and note that and for all . By dominated convergence we then obtain

| (D.6) |

where the last equality follows since, for each , the integral on the right-hand side is a linear combination of with , and therefore vanishes due to (D.4). Hence, (4.2) holds also for .

We now derive some consequences. First, and hence for some . Moreover, since

holds -a.s., (D.6) implies that , or equivalently, . In the description of Type 4 it is claimed in addition that the inequality is strict, i.e.

| (D.7) |

To see this, observe that in case of equality, (D.6) would imply that for -a.e. , which is clearly incompatible with having for some nontrivial measure .

Next, we claim that . We prove this by excluding the complementary possibilities. First, assume for contradiction that and . Then . Proceeding as with (D.6) we then deduce

which is clearly not possible since -a.s. This is the desired contradiction.

Suppose instead and . Define

| (D.8) |

Set and observe that due to the fact that in view of (D.7). Then define the set

Choosing small enough such that , by Lemma D.1 we have that

We can then compute

for all and -a.e. . Fatou’s lemma then yields

using in the last step that . Again we arrive at a contradiction.

Finally, suppose and . We may then repeat the arguments from the first case, using the function instead of to obtain the required contradiction. In summary, we have shown that , as claimed.

Lemma D.1.

Fix and set for all . Then there is some such that

for all .

Proof.

Fix and let such that and . Define then and compute

Let , note that and moreover

| (D.9) |

Since , it is then enough to show that for big enough this expression is smaller than or equal to 1 for all and .

Let be the first minimum of the numerator. Observe that for the denominator converges to uniformly on compact sets. As a result, for big enough, we have that

for all . Since expression (D.9) takes value for and is decreasing in on , we conclude the proof. ∎

Appendix E The unit simplex: Proof of Lemma 6.1 and Theorem 6.3

Proof of Lemma 6.1.

Assume is a polynomial operator and its martingale problem is well-posed. Theorem 2.3 and Theorem 2.8 imply that is of Lévy type for some triplet , so that in particular (i) holds. Condition (iv) follows from Lemma 2.9. To prove (ii), fix . Let and , where and are the functions on described in the proof of Lemma 4.1. Then by the positive maximum principle we conclude that

The positive semidefiniteness of then implies that for all . In order to verify (iii), note that setting , by the positive maximum principle we have

where denotes the th column of .

Conversely, Lemma 2.9 and (iv) imply that is polynomial. Thus by Theorem 2.3, the martingale problem for is well-posed, provided that and satisfies the positive maximum principle. The first condition is clearly satisfied. For the second one, let and be an arbitrary polynomial having a maximum over at some . Observe that

and let be the set of all active inequality constraints at point , that is, is the set of all such that . By the necessity of the Karush-Kuhn-Tucker conditions (see e.g. Proposition 3.3.1 in Bertsekas (1995)), there exist multipliers and such that for all ,

and for all such that and for all . Since for -a.e. , by (iii), and for all by (ii), we can thus write

We must argue that . The second term on the right-hand side is nonpositive by (ii). The last term is also nonpositive since is maximal over at . It remains to show that the first term is nonpositive. To this end, let denote the symmetric and positive semidefinite square root of . Condition (iii) yields and thus . By symmetry of we deduce

Moreover, by (ii) we also have that , and hence , for all . This implies that and thus , for all and . As a result,

which implies that is negative semidefinite. This gives the desired inequality

showing that . This completes the proof of the lemma. ∎

Before starting the proof of Theorem 6.3, we prove three auxiliary lemmas.

Lemma E.1.

Consider a polynomial .

-

(a)

If vanishes on , it can be written as

(E.1) -

(b)

If vanishes on for some , it can be written as

(E.2) -

(c)

If vanishes on for some and , it can be written as

(E.3)

Proof.

Since every affine function on can be written as a linear one, there is a real collection such that for all . Observe that for all we have that

Assume without loss of generality that and (resp. if ) and note that, the polynomial given by

where , is a homogeneous polynomial vanishing on the simplex. This directly implies that and hence for all such that . We can thus conclude that satisfies (E.1).

Proceeding as before for the second part, we obtain that for all such that or and can thus conclude that satisfies (E.2).

Finally, for the third part it is enough to note that the polynomial given by

vanishes on . By (a) this gives us that

on and thus on , proving that satisfies (E.3). ∎

Lemma E.2.

Let be a nonzero measure on . The function given by can be represented as

| (E.4) |

for a measurable function and , if and only if one of the following cases holds true

-

(a)

for some .

-

(b)

for some and . In this case -a.s.

Proof.

First assume that (E.4) holds true. Since , and as every affine function on has a linear representation, we can write for some . If , the support of has to be contained in , which is not possible by assumption.

If for some , item (a) follows if for all .

If and are nonzero for some , item (b) follows if for all . Indeed, by assumption we have for and thus

Since -a.s., we can conclude that for all and hence

| (E.5) |

proving that the conditions of item (b) hold true. In this case -a.s. by (E.5).

Finally, if for at least three different values of , the same reasoning as for case (b) implies for all and thus -a.s., which is not possible by assumption.

The converse direction is clear. ∎

Lemma E.3.

The following assertions are equivalent.

-

(i)

The matrix satisfies , , and .

-

(ii)

The matrix satisfies

for some .

Proof.

We start by proving (i) (ii): By Lemma E.1 we already know that for all we have for some . Moreover, as on , we also have that

for all . Since on and for all , it follows that , which finishes the proof of the first direction. Concerning (ii) (i), the only condition which is not obvious is positive semidefiniteness of on , which follows exactly as in the proof of Proposition 6.6 in Filipović and Larsson (2016). ∎

Proof of Theorem 6.3.

As is polynomial and its martingale problem is well-posed, the conditions of Lemma 6.1 are satisfied. As in Remark 3.2, we can assume without loss of generality that is compactly supported and all its moments of order greater or equal two are thus finite. Analogously to (D.1) we set then

| (E.6) |

for all . Note that for all by the integrability conditions on . By condition (iv) of Lemma 6.1 we also have that for all . By Remark 3.4 we know that

and hence condition implies that can be chosen supported on and such that

By definition of affine jump sizes, the measure has to be square-integrable.

Concerning the statement on the drift this is a consequence of Lemma 6.1. Indeed (iv) yields the affine (and thus linear) form of the drift, (ii) leads to

| (E.7) |

and finally is a consequence of (iii), namely for all . Since condition (E.7) yields , choosing we get for and for all . We will now consider four complementary assumptions, which will lead to Type 0 to 3.

Assume that . Then by Lemma 6.1 we can apply Lemma E.3 to conclude that satisfies (6.2). This proves that in this case is an operator of Type 0.

Assume now that and can be chosen to be constant. We can then without loss of generality set . Moreover, since in this case for all , condition (iv) of Lemma 6.1 implies that the entries diffusion matrix . We can thus conclude as before that can be chosen to be of form (6.2). Finally, condition (E.7) can be rewritten as for all , which yields for all . As a result, is an operator of Type 1.

Assume now that and cannot be chosen to be constant. We already know that for some . Supposing without loss of generality that and are coprime polynomials, we necessarily have due to Assumption A that is a divisor of for each and -a.e. . Since -a.s., this in turn implies that -a.s. with a measurable function and .

Choose now such that . By equation (E.6) we have that

for some , for all . Since in this case for all , we are free to choose on this set. By Lemma 6.1 we also know that has to be a bounded function on . Noting that for all

we see that this condition holds true if and only if for all . Since we know by Lemma E.2 that for some , by Lemma E.1 we thus have that

for some . This in particular implies that and hence, by condition (iv) of Lemma 6.1, for all . By the same condition we also have that for all

| (E.8) |

and thus in particular, by positive semidefiniteness of and condition (ii) of Lemma 6.1,

| (E.9) |

for all . Setting be such that , we obtain that satisfies the conditions of Lemma E.3 and thus can be chosen to be of the form (6.2). By (E.8) we can then conclude that

By Lemma E.2, we know that there are only two complementary choices of and .

References

- Ackerer and Filipović (2016) D. Ackerer and D. Filipović. Linear credit risk models. 2016. URL http://ssrn.com/abstract=2782455.

- Ackerer et al. (2016) D. Ackerer, D. Filipović, and S. Pulido. The Jacobi Stochastic Volatility Model. 2016. URL http://ssrn.com/abstract=2782486.

- Bertsekas (1995) D.P. Bertsekas. Nonlinear Programming. Athena Scientific, 1995.

- Biagini and Zhang (2016) S. Biagini and Y. Zhang. Polynomial diffusion models for life insurance liabilities. Insurance: Mathematics and Economics, 71:114 – 129, 2016.

- Böttcher et al. (2013) B. Böttcher, R. Schilling, and J. Wang. Lévy Matters III: Lévy-Type Processes: Construction, Approximation and Sample Path Properties. Springer, 2013.

- Courrège (1965) P. Courrège. Sur la forme intégro-différentielle des opérateurs de dans satisfaisant au principe du maximum. Séminaire Brelot-Choquet-Deny (Théorie du Potentiel), 10(2), 1965.

- Cuchiero (2017) C. Cuchiero. Polynomial processes in stochastic portfolio theory. ArXiv e-prints, 2017. URL http://arxiv.org/abs/1705.03647.

- Cuchiero et al. (2012) C. Cuchiero, M. Keller-Ressel, and J. Teichmann. Polynomial processes and their applications to mathematical finance. Finance and Stochastics, 16:711–740, 2012.

- Cuchiero et al. (2016) C. Cuchiero, K. Gellert, M. Guiricich, A. Platts, S. Sookdeo, and J. Teichmann. Polynomial models for market weights at work in stochastic portfolio theory: theory, tractable estimation, calibration and implementation. Working paper, 2016.

- Dawson and Li (2006) D. A. Dawson and Z. Li. Skew convolution semigroups and affine Markov processes. Annals of Probability, 34(3):1103–1142, 2006.

- Delbaen and Shirakawa (2002) F. Delbaen and H. Shirakawa. An interest rate model with upper and lower bounds. Asia-Pacific Financial Markets, 9:191–209, 2002.

- Duffie (2004) D. Duffie. Credit risk modeling with affine processes. Publications of the Scuola Normale Superiore. Scuola Normale Superiore, 2004.

- Epstein and Mazzeo (2013) C. L. Epstein and R. Mazzeo. Degenerate diffusion operators arising in population biology. Number 185. Princeton University Press, 2013.

- Etheridge (2011) A. Etheridge. Some Mathematical Models from Population Genetics: École D’Été de Probabilités de Saint-Flour XXXIX-2009. Springer, 2011.

- Ethier and Kurtz (2005) S.N. Ethier and T.G. Kurtz. Markov Processes: Characterization and Convergence. Wiley Series in Probability and Statistics. Wiley, 2005.

- Fernholz (2002) R. Fernholz. Stochastic Portfolio Theory. Applications of Mathematics. Springer-Verlag, New York, 2002.

- Fernholz and Karatzas (2005) R. Fernholz and I. Karatzas. Relative arbitrage in volatility-stabilized markets. Annals of Finance, 1(2):149–177, 2005.

- Fernholz and Karatzas (2009) R. Fernholz and I. Karatzas. Stochastic portfolio theory: an overview. Handbook of numerical analysis, 15:89–167, 2009.

- Filipović and Larsson (2016) D. Filipović and M. Larsson. Polynomial diffusions and applications in finance. Finance and Stochastics, 20(4):931–972, 2016.

- Filipović and Trolle (2013) D. Filipović and A. B. Trolle. The term structure of interbank risk. Journal of Financial Economics, 109(3):707 – 733, 2013.

- Filipović et al. (2016) D. Filipović, E. Gourier, and L. Mancini. Quadratic variance swap models. Journal of Financial Economics, 119(1):44–68, 2016.

- Filipović et al. (2017) D. Filipović, M. Larsson, and A. Trolle. Linear-rational term structure models. The Journal of Finance, 72(2):655–704, 2017.

- Gallardo and Yor (2006) L. Gallardo and M. Yor. Some remarkable properties of the Dunkl martingales, pages 337–356. Springer, 2006.

- Gourieroux and Jasiak (2006) C. Gourieroux and J. Jasiak. Multivariate jacobi process with application to smooth transitions. Journal of Econometrics, 131(1):475–505, 2006.

- Haviland (1935) E. K. Haviland. On the momentum problem for distribution functions in more than one dimension. American Journal of Mathematics, 57(3):562–568, 1935.

- Haviland (1936) E. K. Haviland. On the momentum problem for distribution functions in more than one dimension. ii. American Journal of Mathematics, 58(1):164–168, 1936.

- Hoh (1998) W. Hoh. Pseudo differential operators generating Markov processes. Habilitationsschrift, Univeristät Bielefeld, 1998.

- Jacod and Shiryaev (2003) J. Jacod and A.N. Shiryaev. Limit Theorems for Stochastic Processes. Springer-Verlag, second edition, 2003.

- Jarrow and Turnbull (1998) R. Jarrow and S. Turnbull. A unified approach for pricing contingent claims on multiple term structures. Review of Quantitative Finance and Accounting, 10(1):5–19, 1998.

- Jeanblanc et al. (2009) M. Jeanblanc, M. Yor, and M. Chesney. Mathematical Methods for Financial Markets. Springer Finance. Springer London, 2009.

- Krabichler and Teichmann (2017) T. Krabichler and J. Teichmann. The Jarrow & Turnbull Setting Revisited. Working paper, 2017.

- Krühner and Larsson (2017) P. Krühner and M. Larsson. Affine processes with compact state space. arXiv:1706.07579, 2017.

- Larsson and Pulido (2017) M. Larsson and S. Pulido. Polynomial diffusions on compact quadric sets. Stochastic Processes and their Applications, 127(3):901–926, 2017.

- Marshall (2008) M. Marshall. Positive Polynomials and Sums of Squares. Mathematical surveys and monographs. American Mathematical Society, 2008.

- Zheng (2006) H Zheng. Interaction of credit and liquidity risks: Modelling and valuation. 30:391–407, 02 2006.