Abstract

In this paper the fractional trading ansatz of money management is reconsidered with special attention to chance and risk parts in the

goal function of the related optimization problem. By changing the goal function with due regards to other risk measures like

current drawdowns, the optimal fraction solutions reflect the needs of risk averse investors better than the original optimal

solution of Vince [8].

The aspects of money and risk management contribute a central scope to investment strategies. Besides the “modern portfolio theory”

of Markowitz [7] in particular the methods of fractional trading are well known.

In the 50’s already Kelly [3] established a criterion for an asymptotically optimal investment strategy. Kelly as well as Vince [8] and [9] used the fractional trading ansatz for position sizing of portfolios. In “fixed fractional trading” strategies

an investor always wants to risk a fixed percentage of his current capital for future investments given some distribution of historic trades of his trading strategy. In Section 2 we introduce Kelly’s and Vince’s methods more closely and introduce a common generalization of both models. Both of these methods have in common that their goal function (e.g. =“terminal wealth relative”) solely optimizes wealth growth in the long run, but neglects risk aspects such as the drawdown of the equity curve.

At this point our research sets in. With one of our results (Theorem 4.6 and 4.7) it is possible to split the goal function

of Vince into “chance” and “risk” parts which are easily calculable by an easy representation. In simplified terms, the usual goal function now

takes the form of the expectation of a logarithmic chance — risk relation

(1.1)

Moreover, further research (see Section 5) revealed an explicitly calculable representation for the expection of new risk measures, namely

the current drawdown in the framework of fractional trading.

Having said this, it now seems natural to replace the risk part in (1.1) by the new risk measure of the current drawdown in order to obtain

a new goal function for fractional trading which fits the needs of risk averse investors much better. This strategy is worked out in Section 6

including existence and uniqueness results for this new risk averse optimal fraction problem.

The reason such risk averse strategies are deeply needed, lies in the fact that usual optimal strategies yield not only optimal wealth growth in the

long run, but also tremendous drawdowns, as shown by empirical simulations in Maier-Paape [6] (see also simulations in section 6).

Apparently this problem has also been recognized in the trader community where optimal strategies are often viewed as “too risky”

(cf. van Tharp [12]). The awareness of this problem has also initiated other research to overcome “too risky” strategies. For instance,

Maier-Paape [5], proved existence and uniqueness of an optimal fraction subject to a risk of ruin constraint. Risk aware strategies in

the framework of fractional trading are also discussed in de Prado, Vince and Zhu [4], and Vince and Zhu [11] suggest

to use the inflection point in order to reduce risk. Furthermore a common strategy to overcome tremendous drawdowns is diversification as ascertained by

Maier-Paape [6] for the Kelly situation.

2 Combing Kelly betting and optimal theory

In this still introductory section we reconsider two well-known money management strategies, namely the Kelly betting system [1], [3] and the optimal model of Vince [8], [9]. Our intention here is not only to introduce the general concept

and notation of fractional trading, but also to find a supermodel which generalizes both of them (which is not obvious). All fractional trading concepts assume that a given trading system offers a series of reproducible profitable trades and ask the question which (fixed) fraction of the current capital should be invested such that in the long run the wealth growth is optimal with respect to a given goal function. This typically yields an optimization problem in the variable whose optimal solution is searched for. Both Kelly betting and Vince’s optimal theory are stated in that way.

Setup 2.1.

(Kelly betting variant)

Assume a trading system with two possible trading result: either one wins with probability or one loses with probability .

The trading system should be, profitable, i.e. the expected gain should be positive .

The goal function introduced by Kelly is the so called log–utility function

(2.1)

which has to be maximized. The well-known Kelly formula gives the unique solution of (2.1).

Setup 2.2.

(Vince optimal model)

Assume a trading system with absolute trading results , is given with at least one negative trade result.

Again the trading system should be profitable, i.e. .

As goal function Vince introduced the so called “terminal wealth relative”

(2.2)

where is the maximal loss. The is the factor between terminal wealth and starting wealth,

when each of the trading results occurs exactly once and each time a fraction of the current capitals is put on risk for the new trade.

How can one combine these models? The following setup is a generalization of both:

Setup 2.3.

(general TWR model)

Assume a trading system with absolute trades is given and each trade occurs times.

Again we need at least one negative trade and profitability, i.e. .

The terminal wealth goal function is easily adapted to with .

Since for all the following equivalences are straight forward:

where is the weighted geometric mean and

are the relative frequencies. In this sense trading system indeed generalizes both trading systems and .

In particular alternatively to Setup 2.3 it seems natural to formulate the trading system in a probability setup with trades

which are assumed with a probability . This is done in the next section (cf. Setup 3.1), where we give an existence and uniqueness results

for the related optimization problem.

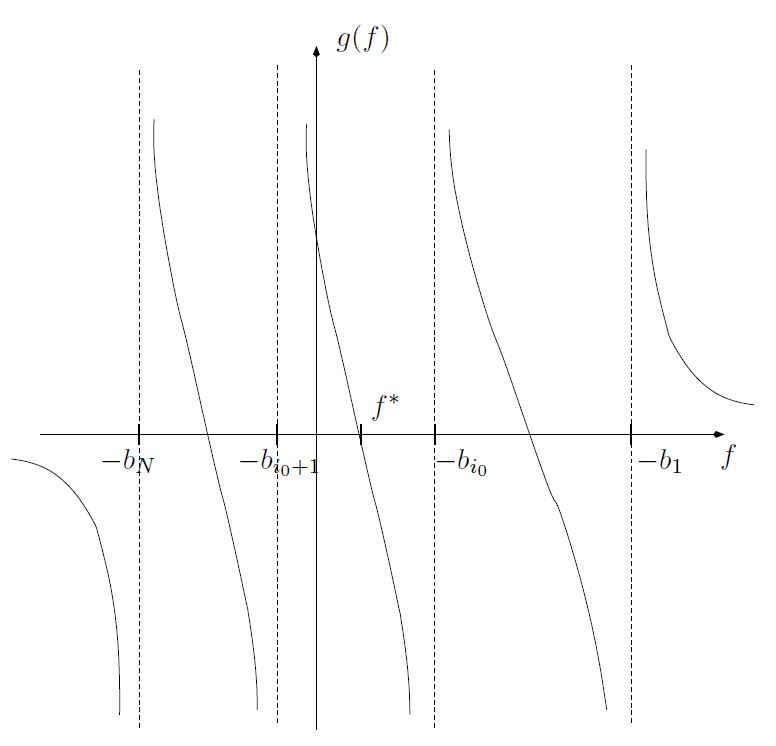

3 Existence of an unique optimal

Setup 3.1.

Assume a trading system with trade results , maximal loss and relative frequencies

, where and . Furthermore should have positive expectation .

Theorem 3.2.

Assume Setup 3.1 holds. Then to optimize the terminal wealth relative

(3.1)

has a unique solution which is called optimal .

Proof.

The proof is along the lines of the “optimal lemma” in [5]:

where and . Assume w.l.o.g that are

ordered and .Then . Since is strictly monotone decreasing for , so is for . This yields existence

of exactly one zero of in and since we have .

Hence is the unique solution of (3.1) (see Figure 1).

∎

Figure 1: Zeros of yielding the existence of

Remark 3.3.

Theorem 3.2 holds true even if are probabilities, and

(3.2)

I.e. the optimization problem (3.2) has an optimal solution as well.

It is important to note that the result so far uses no probability theory at all.

4 Randomly drawing trades

Setup 4.1.

Assume a trading system with trade results and with maximal loss .

Each trade has a probability of , with . Drawing randomly and independent times from this distribution

results in a probability space and a terminal wealth relative

(for fractional trading with fraction )

(4.1)

Theorem 4.2.

The random variable has expectation value

(4.2)

where is the weighted geometric mean of the holding period returns for all .

Proof.

Case : Here and

The induction step : Using for and

we get

by induction.

∎

As a next step, we want to split up the random variable into chance and risk part.

Since corresponds to a winning trade series and

analogously corresponds to a loosing trade series we define the random variables:

The rest of this section is devoted to find explicitly calculable formulas for and . By definition

(4.6)

Assume is fixed for the moment and the random variable counts how many of the are equal

to . I.e. if of the ’s in are equal to . With similar counting random variables we obtain counts

and thus

(4.7)

with obviously . Hence for this fixed we get

(4.8)

Therefore the condition on in the sum (4.6) is equivalent to

(4.9)

To better understand the last sum, we use Taylor expansion to obtain

Lemma 4.5.

Let real numbers , with and for be given. Then the following holds:

(a)

for all sufficiently small ,

(b)

for all sufficiently small .

Proof.

„“:

An easy calculation shows and yielding this

direction for (a) and (b) since .

„“:

From the above we conclude that no matter what is, always

for sufficiently small holds. The claim of the backward direction now follows by contradiction.

∎

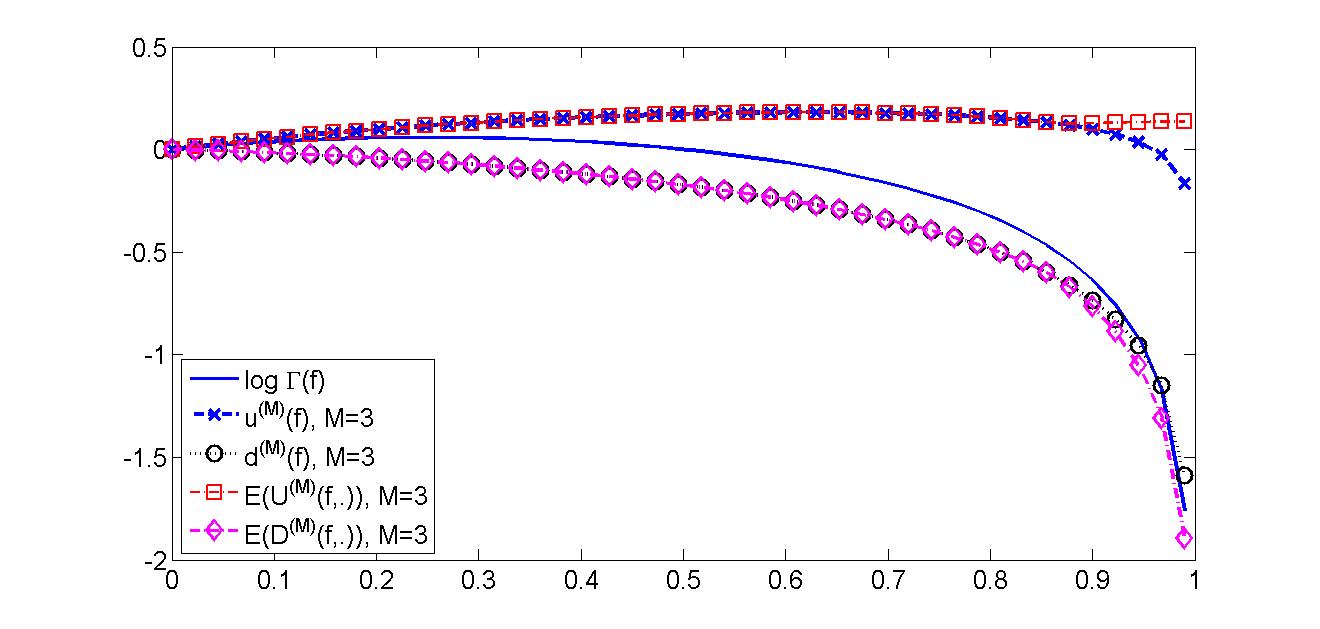

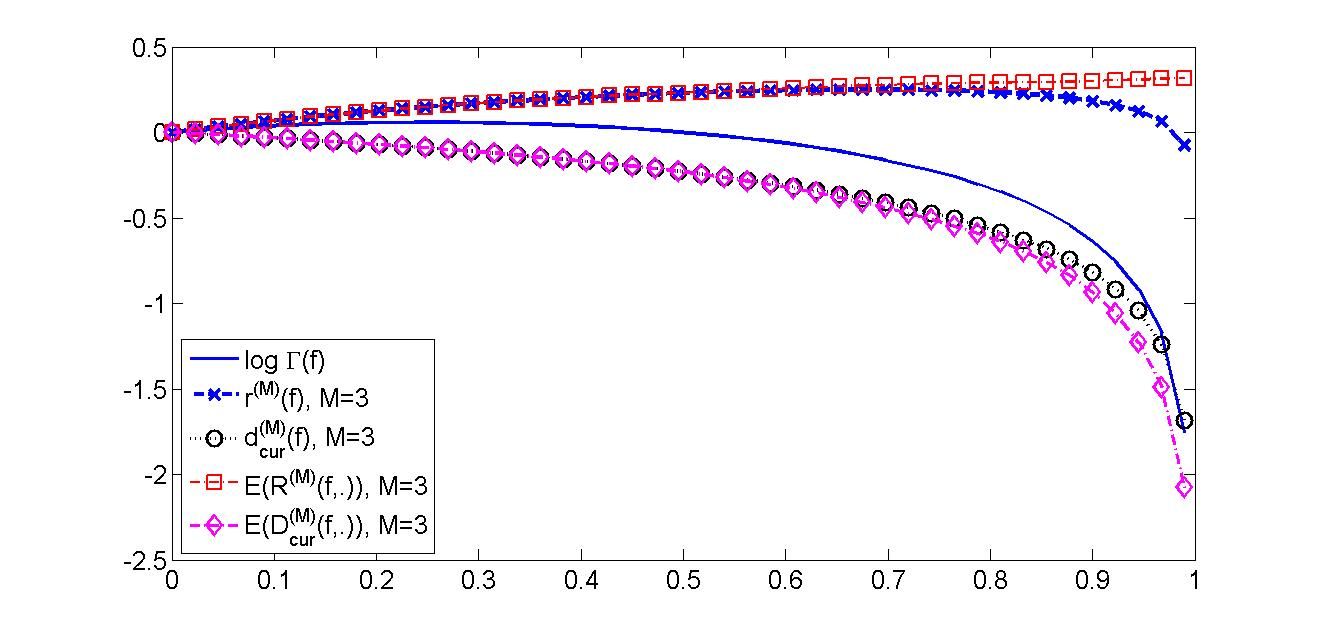

At next we want to apply our theory to the toss game, where a coin is thrown. In case coin shows head, the stake is doubled,

whereas in case of tail it is lost.

Example 4.9.

( toss game; )

Here , , , and .

In this case (4.12) simplifies to

Letting now from and we get for and only.

Therefore

(4.16)

and similarly

(4.17)

for sufficiently small. In Figure 2 one can see that these approximations are quite accurate

up to .

Figure 2: and with their approximations of

(4.11) and (4.13)

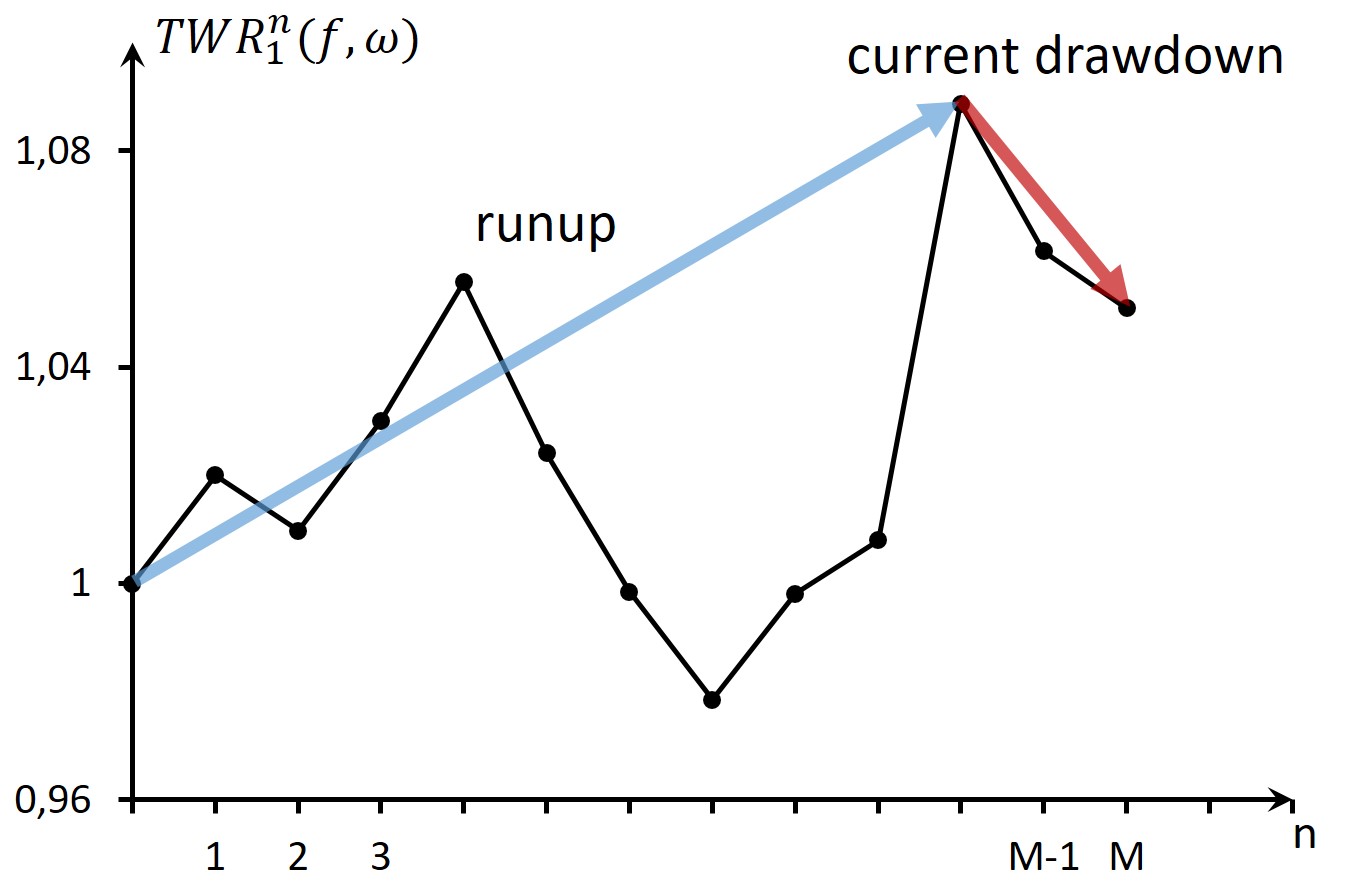

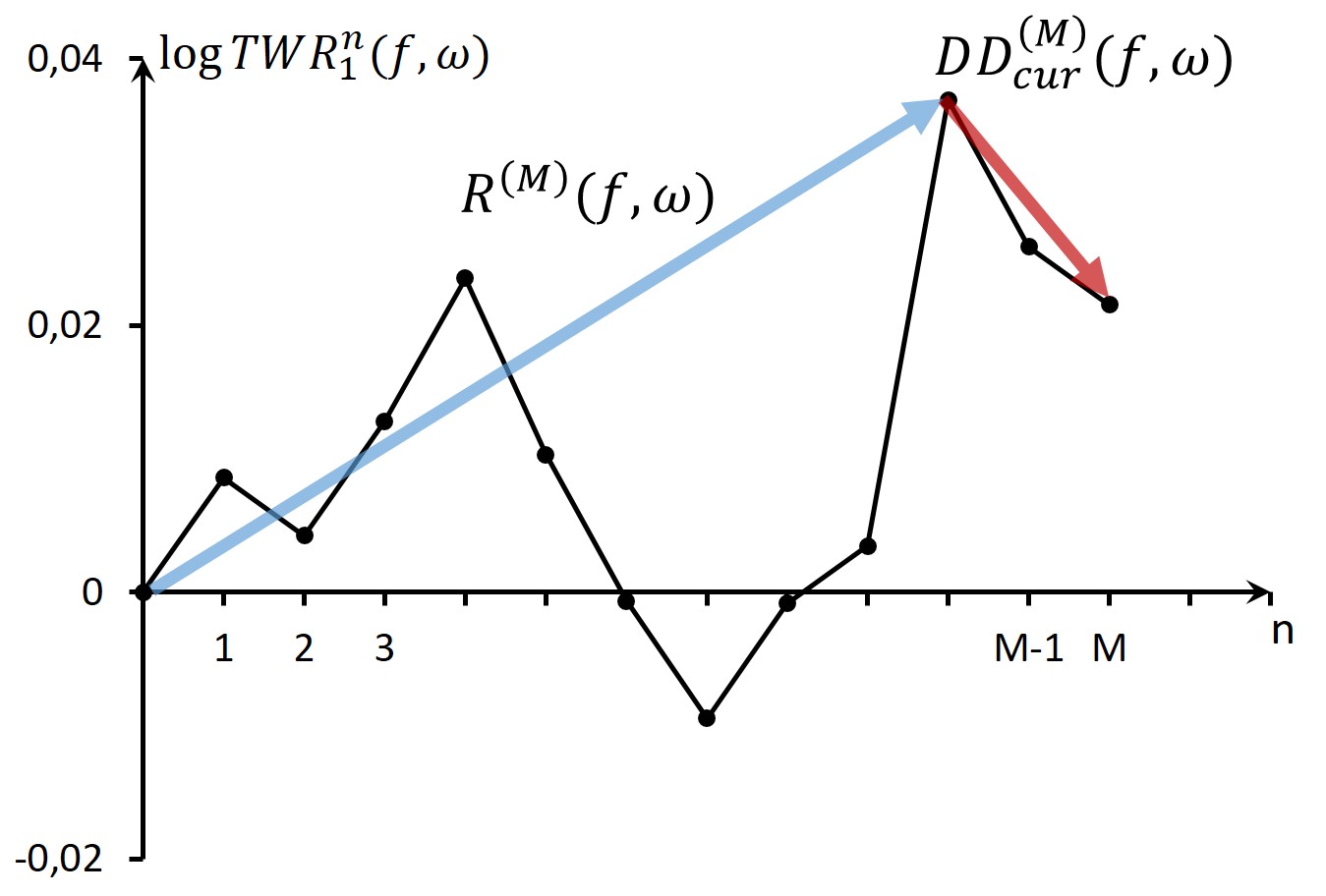

5 The current drawdown

We keep discussing the trading system with trades and probabilities from Setup 4.1 and draw

randomly and independent times from that distribution. At next we want to investigate the resulting terminal wealth relative from fractional trading

from (4.1) with respect to the current drawdown realized after the th draw.

More generally, in the following we will use

The idea here is that is viewed as a discrete „equity curve“ for time (with and fixed).

The current drawdown -series is the logarithm of the drawdown of this equity curve realized from the maximum of the curve til the end (time ).

As we will see below, this series is the counter part of the runup (cf. Figure 3).

Figure 3: In the left figure the run-up and the current drawdown is plotted for an instance

of the TWR “equity”–curve and to the right are their series.

Definition 5.1.

The current drawdown log series is set to

and the run-up log series is defined as

The corresponding trade series are connected in that way that the current drawdown starts after the run-up has stopped.

To make that more precise, we fix that where the run-up topped.

Definition 5.2.

For fixed , define with

(a)

in case

(b)

and otherwise choose such that

(5.1)

where should be minimal with that property.

By definition one easily sees

(5.2)

and

(5.3)

As in Section 4 we immediately get and therefore by Theorem 4.2:

Corollary 5.3.

For

(5.4)

holds.

Again explicit formulas for the expectation of and are of interest.

By definition and with (5.2)

(5.5)

Before we proceed with this calculation we need to discuss further for some fixed .

By Definition 5.2, in case , we have

(5.6)

since is the first time the run-up topped and, in case

(5.7)

For instance the last inequality may for all sufficiently small be rephrased as

(5.8)

by an argument similar to Lemma 4.5. Analogously one finds

(5.9)

We may now state the main result on the expectation of the current drawdown.

Theorem 5.4.

Let a trading system as in Setup 4.1 with fixed be given.

Then for all sufficiently small the following holds:

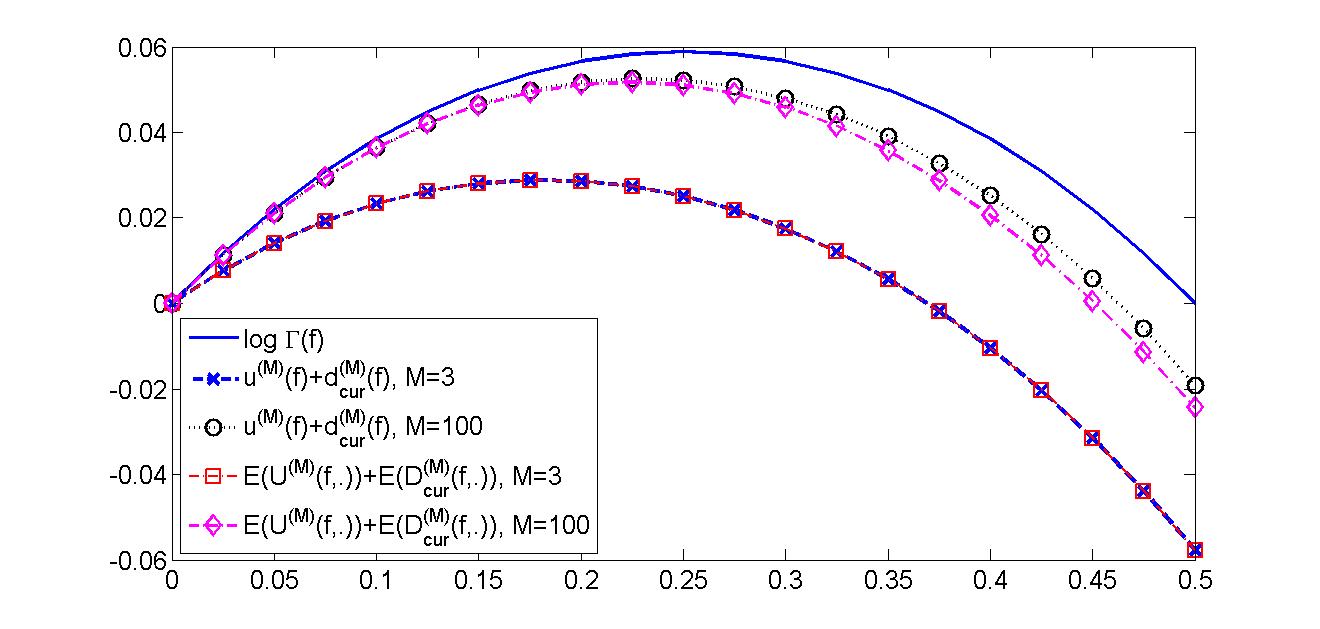

( toss game; )

As before , , , and . The loss will occur if the coin shows tail (T) and corresponds to head (H).

Depending on with sufficiently small we get the following trade series realizing their maximum with the th toss.

(cf. Definition 5.2)

for all sufficiently small. Analogously from and and

Theorem 5.5 we get

(5.15)

for all sufficiently small.

Remark 5.7.

The representations of and from Theorems 5.4 and 5.5 clearly hold true

only for sufficiently small . For no longer small

the formulas for these expectation values change since the topping position

changes. To see that, consider for the 2:1 toss game from above, but assume now that

is so large such that the gain of the last toss does not compensate the loss of the toss from the 2nd toss, i.e. in case

For those , which immediately results in different formulas for the expectation values of run-up and current drawdown.

Figure 4: and with their approximations of (5.10) and (5.12)

Again the approximations of current drawdown and run-up are quite accurate up to (see Figure 4).

6 Optimal for risk averse fractional trading using the current drawdown

Now we bring together the results of the previous sections. We saw in Theorem 4.2 that the usual optimal problem which maximizes the

terminal wealth relative

is equivalent to maximizing

where and are all trades occurring with the same probability .

By Corollary 4.4 this is equivalent to maximize

This optimization problem clearly differentiates between chance () and risk ()

parts. A drawdown averse investor may, however, not only take a look at the downtrade log series but may as well look at the

current drawdown , because the current drawdown is in a way that part of the investment process in risky assets, which “hurts”

every day. Since

(6.1)

we propose

(6.2)

as a more risk averse optimization problem. From the discussion in the sections before, it got clear that those , which contribute non-trivial values to the calculation of the above two expectation values, do depend on . Therefore (6.2) might be too hard to solve

in general at least for large. Nevertheless, the Theorems 4.6 and 5.4 give explicitly calculable formulas for and for all

sufficiently small . We therefore propose as alternative to maximize

(6.3)

with the hope, that the yield for no longer small still good approximations for (6.2).

Fortunately the problem (6.3) was “solved” already in Section 3.

Corollary 6.1.

For a trading system as in Setup 4.1 with fixed the optimization problem (6.3) with

(6.4)

has a unique solution if and in case

.

Proof.

Set and . The claim follows from Theorem 3.2 and Remark 3.3.

∎

Remark 6.2.

Since the optimization problem (6.3) was derived as approximation of the optimization problem (6.2) for

small, it is reasonable that small solutions may be good approximations to solutions of (6.2)

We want to make the difference clear with the toss game:

Example 6.3.

( toss game; )

Using , , , and the usual optimal solves

Since this is also the situation of the Kelly formula

(6.5)

for a game where the win occurs with probability and the loss occurs with probability , we use and to obtain

From Example 4.9, (4.16) and Example 5.6, (5.14) we already know

and again with the Kelly formula (6.5) with and we get .

Figure 5: for and including

their approximations

In Figure 5 we can see that the optimization problems (6.2) and (6.3)

for are completely equivalent and even for the approximated problem comes very close. Therefore the solutions

of (6.2) and (6.3) should be close too.

2

3

4

5

6

7

8

9

10

15

0,1667

0,1818

0,1739

0,1613

0,1839

0,1758

0,1685

0,1870

0,1802

0,1926

20

25

30

40

50

60

70

80

90

100

0,1898

0,1980

0,2043

0,2094

0,2145

0,2197

0,2229

0,2258

0,2283

0,2302

Table 1: Optimal fraction for the risk aware optimization problem (6.3) in the 2:1 toss game from Example 6.3.

In Table 1 we see the optimal solution of (6.3) for the 2:1 toss game and for a selected

set of values. It seems that, as increases, the optimal solutions approach the optimal Kelly fraction . To invest more risk averse it therefore would be natural to use the minimum of the optimal solutions from Table 1, which is close to .

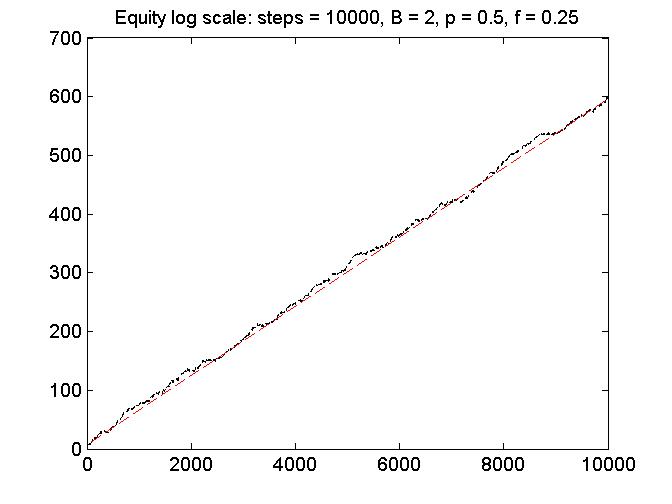

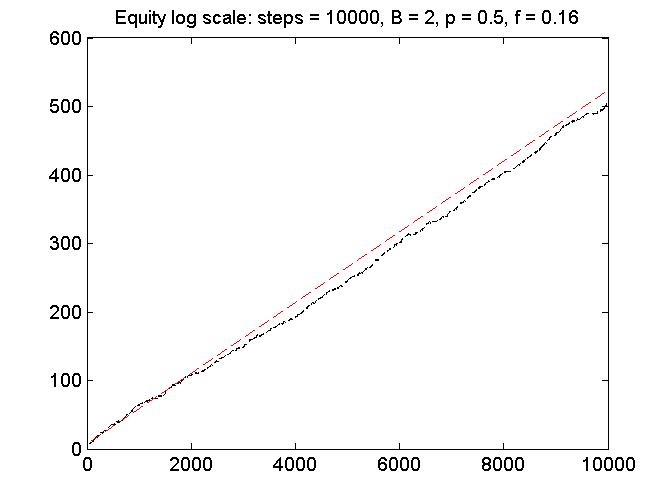

In the remainder of this section we would like to give a simulation of the 2:1 toss game to see the difference of the above mentioned two fractions.

Each of the following simulations uses a starting capital of and draws instances of the 2:1 toss game independently. In Figure 6

we see the resulting –equity curves for in black and as a reference the expected –equity lines dotted

Figure 6: Log–equity curve for the 2:1 toss game with

vs

Clearly the wealth growth according to is less than the wealth much growth of ,

but the reduction is reasonable. The question remains how better is the risk side for the risk aware strategy. In the Figure 7 we see

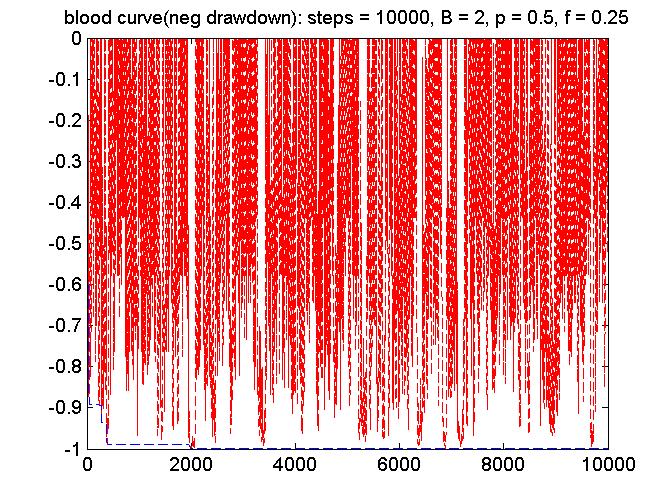

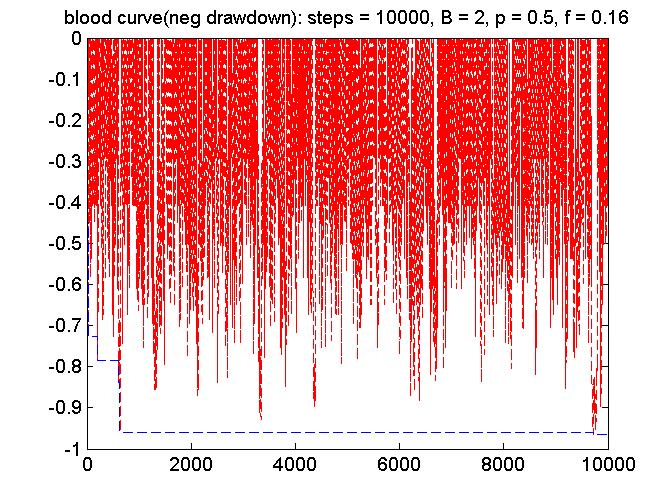

a plot of the current relative drawdown (negative) displayed as a so called “blood curve”.

Figure 7: Current relative drawdown (negative) for the 2:1 toss game with

vs

One can see that the maximal relative drawdown for lies around whereas for

it comes close to for this simulation. More importantly, relative drawdowns of more than become rare events for the risk

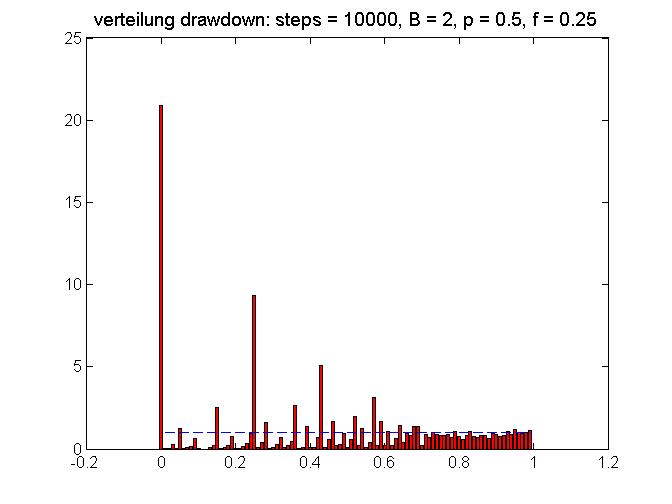

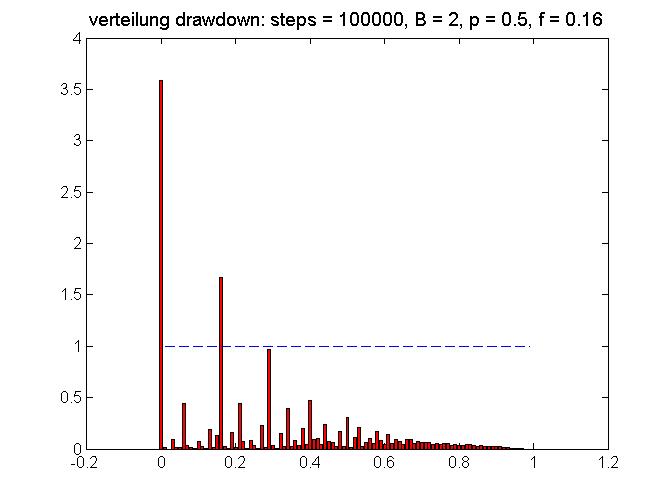

averse strategy which was not the case for the Kelly optimal strategy. Looking at the distribution of the relative drawdowns

(see Figure 8) this will became explicit.

Figure 8: Distribution of the current relative drawdown (positive) for the 2:1 toss game with

vs

7 Conclusion

The splitting of the goal function of fractional trading into “risk” and “chance” parts made it possible to introduce new

more risk aware goal functions. This is carried out using the current drawdown and results in more defensive money management

strategies. However, as simulations in section 6 show, even the new risk averse strategy might still be too risky for

investing with real money. One alternative might be to use the maximal drawdown (on trades) instead of the current drawdown

in the risk averse optimization problem (6.2). Therefore a similar result as Theorem 5.4 would be

desirable for the maximal drawdown as well. Whether or not that is possible remains an open question.

So far these strategies only work for single asset portfolios. The theory of fractional trading of portfolios was introduced

by Vince [10] with his leverage space trading model. Furthermore, Hermes [2] has extended

the portfolio theory of fractional trading to trading results with continuous distributions. Nevertheless, also the question

how risk averse strategies may be used for portfolios with many different assets to be traded simultaneously is still open.

References

[1]T. Ferguson,The Kelly Betting System for Favorable Games,

Statistics Department, UCLA.

[2]A. Hermes,A mathematical approach to fractional trading, PhD–thesis,

Institut für Mathematik, RWTH Aachen, (2016).

[3]J. L. Kelly, Jr.A new interpretation of information rate,

Bell System Technical J. 35:917-926, (1956).

[4]Marcos Lopez de Prado, Ralph Vince and Qiji Jim Zhu,Optimal risk budgeting under a finite investment horizon,

Availabe at SSRN 2364092, (2013).

[5]S. Maier–Paape,Existence theorems for optimal fractional trading,

Institut für Mathematik, RWTH Aachen, Report Nr. 67 (2013).

[6]S. Maier–Paape,Optimal and diversification,

International Federation of Technical Analysis Journal, 15:4-7, (2015).

[7]Henry M. Markowitz,Portfolio Selection,

FinanzBuch Verlag, (1991).

[8]R. Vince,Portfolio Management Formulas: Mathematical Trading Methods for the Futures, Options, and Stock Markets,

John Wiley & Sons, Inc., (1990).

[9]R. Vince,The Mathematics of Money Management, Risk Analysis Techniques

for Traders,

A Wiley Finance Edition, John Wiley & Sons, Inc., (1992).

[10]R. Vince,The Leverage Space Trading Model: Reconciling Portfolio Management

Strategies and Economic Theory,

Wiley Trading, (2009).

[11]Ralph Vince and Qiji Jim Zhu,Inflection point significance for the investment size,

Availabe at SSRN 2230874, (2013).

[12]K. van Tharp,Van Tharp’s definite guide to position sizing,

The International Institute of Trading Mastery, (2008).