Extending one-factor copulas

Abstract

So far, one-factor copulas induce conditional independence with respect to a latent factor. In this paper, we extend one-factor copulas to conditionally dependent models. This is achieved through new representations which allow to build new parametric factor copulas with a varying conditional dependence structure. We discuss estimation and properties of these representations. In order to distinguish between conditionally independent and conditionally dependent factor copulas, we provide a novel statistical test which does not assume any parametric form for the conditional dependence structure. Illustrations of our framework are provided through examples, numerical experiments, as well as a real data analysis.

Keywords: Archimedean copula, dependence, conditional, hierarchical Archimedean copula, factor, copula, latent, independence, test.

1 Introduction

Factor copulas refer to copulas which can be expressed by means of unobserved variables, the factors. Most of the time, only one univariate (and continuous) factor is used, and thus one talks about one-factor copulas. They are a hot topic of research at the moment, being written about by Krupskii and Joe (2013), Joe (2014), Krupskii and Joe (2015), Mazo et al. (2015) or Oh and Patton (2015). Nonetheless, the scope of current one-factor copulas is still limited when it comes to the construction of parametric models.

First, only factors with a uniform distribution are currently considered to the literature. Yet, in applications, the identification of a factor may implicitely assume estimating its distribution. Second, studying the factor’s impact on the dependence structure is not allowed, either. Indeed, in current one-factor copulas, only conditional independence is allowed. That is, the variables , whose joint distribution is a copula, are independent conditionally on the factor . This means that, for all ,

As a result, current one-factor copulas are written (Krupskii and Joe, 2013) as

| (1.1) | ||||

where is some bivariate copula and has a uniform distribution.

As (1.1) allows to see, the task of modeling only amounts to choose a parametric form for . What if the practitioner assumes that the dependence grows with the factor’s value? Or, what if the dependence structure remains the same, but is not conditional independence?

This paper introduces new representations for one-factor copulas, allowing one to construct novel parametric models. These representations cover many models of the literature in a nontrivial way, as seen in Section 5. Section 3 explores various properties of the new representations, while Section 6 explores estimation and also proposes a novel test to assess whether conditional independence may hold or not, without assuming any parametric form for the dependence structure. Section 7 presents the numerical experiments used to illustrate the testing procedure as well as a real data analysis.

2 Extended one-factor copulas and nested extended one-factor copulas

Consider the the law of total probability,

| (2.1) |

where the integral is taken over the support of and denotes its density. Equation (2) is the one from which the formula of current one-factor copulas originated, given by (1.1). One can easily see that one-factor copulas are a reformulation of the law of total probability in which the factor is uniformly distributed on and the variables are assumed to be independent conditionally on the factor.

To extend one-factor copulas, in addition to letting the density of , , be unspecified, it is proposed to reconsider the decomposition of

Given , certainly the vector has a distribution function, but it is not, in general, a copula, because is not, in general, uniformly distributed. By Sklar’s theorem (Sklar, 1959; Nelsen, 2006),

can be decomposed as a copula and a set of marginal distributions, that is,

| (2.2) |

If we let vary, both the copula and the margins , , will be, in fact, conditional distributions.

Example 2.1.

Consider (2) with following an exponential distribution, as

| (2.3) |

Moreover, in (2.2), assume that

where

| (2.4) |

is the well known Gamma function. Finally, assume that the density of , is

| (2.5) |

where , is the quantile of order of the standard normal distribution, is the identity matrix, and

| (2.6) |

where

In Example 2.1, for a fixed , the copula is a multivariate Gaussian copula with an exchangeable correlation matrix with parameter . Likewise, the distribution of given is a beta distribution with parameters and . By Sklar’s theorem, and can be set independently.

Example 2.2.

In Example 2.2, for a fixed , the copula is recognized to be a Gumbel-Hougaard copula with parameter , see Nelsen (2006, p. 153). The margins , were not specified.

While examples such as Example 2.1 and Example 2.2 could be multiplied endlessly, there is a representation, presented below, which permits to get them all, and build general parametric one-factor copulas quite easily. So, in view of both the law of total probability (2) and the “conditional Sklar’s theorem” (2.2), every one-factor copula can be written as

| (2.8) |

where, as in Examples 2.1 and 2.2, is to be understood as a collection, running over , of well defined -variate copulas and where the integral is taken over the support of . In representation (2), as well as in Example 2.1 and Example 2.2, letting vary induces a collection of copulas which reflects the change in the dependence structure as the factor varies. For instance, in the Example 2.1, (pointwise) as , where denotes the independence copula, that is, for all . On the other hand, if , then , where denotes the Fréchet-Hoeffding bound for copulas, that is, represents the complete positive dependence structure, with for all . The opposite happens in Example 2.2. We have that whenever and whenever .

Representation (2) can be recast in terms of standard uniform variables only. Let be the inverse of the factor’s distribution function . By the change of variables in (2), we have

| (2.9) |

where , .

Example 2.3 (continuation of Example 2.1).

From (2.3), we have , hence, for a fixed , is a multivariate Gaussian copula with correlation matrix given by

Furthermore, since , we have

so that the underlying bivariate copula is

for .

In Example 2.3, note that implies , and thus is the Fréchet-Hoeffding bound . Likewise, implies (by continuity), and thus is the independence copula.

Example 2.4 (continuation of Example 2.2).

From (2.7), we have , hence, for a fixed ,

that is, is a multivariate Gumbel-Hougaard copula with parameter given by

In Example 2.4, implies , and thus is the independence copula. Likewise, implies (by continuity), and thus is the Fréchet-Hoeffding bound. In short, we simply replaced the ’s of Example 2.1 and Example 2.2 by .

Mathematically, both representations (2) and (2) are of course equivalent. It is worth stressing that these representations are better not to be taken as plain mathematical results, but rather as a convenient way to generate new parametric one-factor copula models, as was shown in the above examples. The advantage of the representation in (2) is that it involves copulas only and allows an easy comparison with (1.1). This last equation indeed corresponds to (2) with , and . Representation (2) is however more convenient when one adopts a point of view centered on the factor itself.

Both representations (2) and (2) contain two -dimensional copulas: one, or , that’s part of the integrand, and one, , that’s the result of the integral. In the rest of this paper, the latter will often be referred to as the outer copula, while the former will often be referred to as the inner copula. In the rest of this paper, the copulas in (2) will be referred to as the bivariate copulas or linking copulas.

The inner copula in both representations is usually assumed to be a copula with one parameter, this parameter being explicitly related to through in representation (2). However, many -dimensional copula have more than one parameter. In such cases, each parameter can be assumed to be related to through a different mapping , , where is the number of parameters of the related inner copula, and one can write:

In general however, we will just write as or even .

Since any -dimensional copula can be used in representations (2) and (2) as inner copula, one can also consider using an outer copula as inner copula, nesting our construction in itself.

Let us rewrite expression (2) as

| (2.10) |

that is, we rewrite as , replace by and by .

Next, define as

where is some -variate copula, the parameters of which being each related to through a different mapping, and where , being a set of bivariate copulas, with .

The outer copula in Equation (2.10) is then

Note that in the above nesting scheme, the -variate copula actually does not depend on . In general, we will always assume that only the last -variate copula in a nesting chain actually depends on its related variable , in order to avoid an extra layer of complexity. While working with this last assumption, a nested extended one-factor copula (NEOFC), hereafter denoted as , can be written as

| (2.11) |

where , is

| (2.12) |

and , with

| (2.13) |

As an example, if , we have

The block of equations (2.13) reveals that there is a set of bivariate copulas underlying . Since , this means that there is always a set of bivariate copulas underlying any NEOFC. The set , , is the first layer of linking copulas, while the set corresponds to the last layer of linking copulas.

To summarize, a one-factor copula (OFC) can be written as

| (2.14) |

an extended one-factor copula (EOFC) as

| (2.15) |

and a nested extended one-factor copual (NEOFC) as

| (2.16) |

Note that EOFCs are a special case of NEOFCs: setting in the last expression above means falling back to extended one-factor copulas. Also note that, while the inner copula of a NEOFC is assumed to depend on only one factor, , a nested extended one-factor copula actually encompasses more than one factor: from to .

3 Properties of EOFCs and NEOFCs

In this section, various properties of EOFCs and NEOFCs are given. Identifiability issues are also addressed.

3.1 On the inner copula

In order to generate new parametric families of one-factor copulas using (2) or (2), one can act on 3 components: the bivariate or linking copulas , , the factor’s distribution, represented either by its density or by its quantile function , and the set of multivariate copulas . Depending on the choice for the inner copula , three different forms of factor copulas can be made. This is illustrated by the following example.

Example 3.1.

Let follow an exponential distribution with parameter ,

For , let be a Clayton copula so that

| (3.1) |

In Example 3.1, we have built a parametric model for one-factor copulas which allow for different features. First, the number of parameters, , is linear in , the dimension. Second, as will be seen in Section 6, assuming a parametric form for the factor’s distribution, one can estimate the related parameter by maximum pseudo-likelihood, thus learning valuable information about a variable which, by definition, is never directly observed. Finally, one can control the growth rate of the dependence structure, relative to the change of the factor’s value. For instance, in (3.2), a decrease in leads to an increase in , being the correlation parameter. If one set , then , and thus the correlation parameter, hence the conditional copula , does not depend on anymore: we call this conditional invariance, not to be mistaken with conditional independence. This last feature happens when , implying a correlation parameter .

The three different forms of factor copulas are now formalized.

- Conditional independence.

-

Conditional independent one-factor copulas are those such that the inner copula is the independence copula. They correspond exactly to copulas of the form (1.1), described in Krupskii and Joe (2013), and their interpretation is such that, given the factor’s value , the variables are independent. Let us note that, even in this simple case, the obtained models are quite reasonable and useful, as was demonstrated not only in Krupskii and Joe (2013) or Oh and Patton (2015), but also in view of the vast literature about conditional independent models, see Skrondal and Rabe-Hesketh (2007). In Section 6.2, we provide a novel procedure in order to test the assumption of conditional independence.

- Conditional invariance.

-

Conditional invariant one-factor copulas are those such that, in (2) for instance, for any and . That is, there is conditional dependence, but this conditional dependence remains the same regardless of the factor’s value.

- Conditional noninvariance.

-

Conditional noninvariant one-factor copulas are those which are not conditionally invariant. Note that, a fortiori, they are not conditionally independent either. Here, the conditional dependence structure is allowed to change with the factor’s value. In Example 2.1, as and therefore , the independence copula. On the opposite, as and thus , the Fréchet-Hoeffding upper bound, characterizing complete positive dependence.

Natural parametric one-factor copulas can be built with the help of Kendall’s tau and Spearman’s rho. Recall that, given a bivariate copula , Kendall’s tau is a dependence coefficient in defined by

| (3.3) |

A value of hints at independence, and (respectively ) indicates negative (respectively positive) dependence. Example 3.2 illustrates the procedure.

Example 3.2.

Let follow a standard uniform distribution and let be as

where is the inverse map of

| (3.4) |

In Example 3.2, for a fixed , is recognized to be a Clayton copula with parameter for . In general, the procedure works as follows. First, choose a parametric family of copulas, here the family of Clayton copulas

| (3.5) |

Second, compute Kendall’s tau (there is only one, since all pairs have the same distribution), which in this case is given by (3.4). Third, choose the distribution of so that its support corresponds to the range of the map induced by (3.4), here . Fourth and last, replace by in (3.5).

The conditional dependence structure in Example 3.2 goes from conditional independence to conditional complete dependence. Indeed, when , and . If instead, and , the Fréchet-Hoeffding upper bound for copulas. If one rather defines , then when and . Hence, in one case the dependence increases with respect to the factor, while in the other case it decreases.

3.2 Densities of EOFCs and NEOFCs

The density of an EOFC, as defined by (2.10) is straighforward to get:

| (3.6) |

which is the integral of the product of one -variate density and bivariate densities, and where is the density of while is the density of .

The density of a NEOFC, as defined by (2.11), is however less straighforward to obtain and requires first to figure out the result of , also refer to (2.12) and (2.13). Observe that (chain rule):

Using this last result, can now be written as

| (3.7) |

The last expression in (3.7) is the product of fractions. The last one is a bivariate copula density and the others each involve a bivariate density. Starting with the fraction on the right of the last expression in (3.7), we indeed have that

If we replace by so that

we see that

| (3.8) |

Therefore, we can write that

| (3.9) |

As an example, we can expand (3.9) for :

| (3.10) |

The density of a NEOFC can now be written:

| (3.11) |

where is the density of and .

The density of a NEOFC, as displayed in the last expression of (3.11), is thus made of two parts: a -variate copula density on the left, , and a product that involves bivariate copula densities on the right of .

3.3 On the margins of EOFCs and NEOFCs

The multivariate margins of an EOFC are still EOFCs.

Proof.

This can be easily seen by integrating out of Equation (3.6):

The integral requires the following change of variable to be solved:

leading to

After reorganizing this last expression, one gets:

The integral related to is the margin of in when its first argument is integrated out. The final result is

which is the density of an EOFC. ∎

In general, in order to get a given margin from an EOFC, one just needs to drop the variables that are no longer needed in (3.6).

Similarly to this last result, the multivariate margins of a NEOFC are also NEOFCs.

Proof.

The proof is similar to what was done in the case of EOFCs. Start from (3.11) and integrate out:

| (3.12) |

Perform a change of variable:

leading to

Reorganize this last expression:

The integral related to is just the margin of in . One can now write:

| (3.13) |

which is the expression of a NEOFC density. ∎

In general, the margins of a NEOFC are easy to get: just drop in expression (3.11) the elements corresponding to the variables that are no longer of interest.

3.4 The upper and lower Fréchet-Hoeffding bounds

The upper Fréchet–Hoeffding bound is defined as . It is always a copula, and corresponds to comonotone random variables.

Proposition 3.3.

In (2), let and let , where is the upper Fréchet-Hoeffding bound on . Then, .

Proof.

The outer copula is

and since is 0 as soon as , one can write:

Moreover, as long as , we have that . Therefore, we have

∎

This result will turn out very useful to show that OFCs are not suited to model hierarchical dependence in Section 5.

The 2-dimensional lower Fréchet-Hoeffding bound is usually written as . Note that, in contrast to the upper Fréchet-Hoeffding bound, its generalization, , is not a copula anymore.

Proposition 3.4.

In (2), let , , and . Then,

Proof.

The outer copula is

and since the integrand is 0 as long as , one can write that

Since, , , one can write

and the proof is complete.

∎

3.5 Two degenerate cases

Proposition 3.5.

In Equation (2.15), let , , be such that . Then, .

Proof.

The reasoning is the same for a NEOFC: one just needs to let all linking copulas, for all layers, be the independence copula. Note that in case of conditional invariance, we have that and , that is, the outer copula is directly equal to the inner one. This result is important as it means that any -dimensional copula in the literature is an EOFC where the linking copulas are the independence copula and the inner copula is equal to the -dimensional copula of interest.

A second degenerate case, regarding the linking copulas, is now presented.

Proposition 3.6.

Let the inner copula be the independence copula and set all linking copulas to the upper Fréchet-Hoeffding bound, except for one, . In , set now all arguments to 1, except for and , where is an arbitrary element of . The resulting bivariate margin of , , is then equal to .

Proof.

Let us write the expression of when the inner copula is the independence one and is the upper Fréchet-Hoeffding bound:

The function will return as long as . Otherwise, is returned. Therefore, one can write

∎

Proposition 3.6 can be generalized for the case of a NEOFC as follows: if is the linking copula of interest, , , then the -margin of is if is the independence copula while the linking copulas related to are set to the upper Fréchet-Hoeffding bound, except for , and the remaining linking copulas are set to the independence copula. The proof that the result of this setup is is trivial in view of the proof of Proposition 3.6 and is therefore left to the reader.

3.6 Dependence properties

To start, let us write representation (2) when :

| (3.14) |

Let’s also recall some dependence properties from Nelsen (2006).

A copula is positively quadrant dependent (PQD) if for any , where is the independence copula. Similarly, a copula is negatively quadrant dependent (NQD) if for any .

If is the copula of , then is said to be stochastically decreasing in if is an increasing function of , . This can be written as and it will often be said that is SD in or that is SD in its second argument.

Similarly, if is the copula of , then is said to be stochastically increasing in if is a decreasing function of , . This can be written as and it will often be said that is SI in or that is SI in its second argument.

Finally, note that if a copula is stochastically increasing in either or , then it is PQD. The same applies if is stochastically decreasing in either or : is then NQD. The reverse is however not true: being SI or SD for a copula is a stronger dependence property than being PQD or NQD.

Proposition 3.7.

Let the inner copula in (3.14), , be a PQD copula, . Then if is NQD and is or if is PQD and is , the outer copula is PQD, too.

Proof.

If is PQD, then . Therefore, it is clear that

| (3.15) |

Using integration by parts, one can then show that

Since is and is NQD, we have that

and therefore

Using integration by parts again, we have that

leading to

∎

A similar proposition as the one above can be made, ensuring that the outer copula is this time NQD. The proof is almost the same as the one from the previous proposition and is therefore left to the reader.

Proposition 3.8.

Let the inner copula in (3.14), , be a NQD copula, . Then if is NQD and is or if is PQD and is , the outer copula is NQD, too.

Corollary 3.9.

Let the inner copula in a 2-dimensional EOFC be the independence copula, that is, we fall back to Equation (1.1), where . Then if is PQD, is and since the independence copula is PQD, by Proposition 3.7, the outer copula is PQD. Similarly, if is NQD, is and since the independence copula is NQD, by Proposition 3.8, the outer copula is NQD.

Note that Proposition 1 in Krupskii and Joe (2013) offers a similar result as the one from the above corollary, where it is shown that if both and are SI in , the outer copula is PQD. Proposition 3.7 shows that both and do not need to be SI in for the outer copula to be PQD: as long as one of the two linking copulas is SI and the remaining one is just PQD, then the outer one is PQD.

Let us now write the expression of a NEOFC when . Then:

| (3.16) |

The following proposition ensures that the outer copula is going to be PQD.

Proposition 3.10.

Let the inner copula in (3.16), , be a PQD copula, . Then if is NQD and is SD in , while is NQD and is SD in , the outer copula, , is PQD.

Proof.

Let us write as

| (3.17) |

where

| (3.18) |

Proposition 3.10 can be generalized as follows:

Proposition 3.11.

Let the inner copula in a 2-dimensional NEOFC be PQD. If for each we have that is NQD and is SD with respect to the factor or that is NQD and is SD with respect to the factor , then the outer copula, , is PQD.

The proof of this last proposition is trivial in regard of the proof of Proposition 3.10. Proposition 3.11 can also be expressed so that the resulting outer copula is NQD:

Proposition 3.12.

Let the inner copula in a 2-dimensional NEOFC be NQD. If for each we have that is NQD and is SI with respect to the factor or that is NQD and is SI with respect to the factor , then the outer copula, , is NQD.

Hereafter is an example of NEOFC meeting the requirements of Proposition 3.11.

Example 3.13.

Start from 3.16. Replace the inner copula by the Frank copula, with parameter

that is, we use the inverse CDF of an exponential distribution on in order to calculate , where is the rate, that is, the maximum value of the corresponding exponential probability density function. Since the support of the exponential is , the parameter is always positive and therefore is PQD .

Next, set both and to be a Mardia copula with a negative parameter’s value, ensuring the copula is NQD (Nelsen, 2006, p. 188), while both and are AMH copulas, each with a negative parameter’s value, to ensure that is SD in and is SD in . Indeed, for an AMH copula , one have that

which is a positive quantity as long as .

The outer copula resulting from this construction is, by Proposition 3.11, PQD.

Next we introduce an important conjecture, which describes the relationship between the inner copula and the outer copula of an EOFC.

Conjecture 3.14.

The motivation of this conjecture is now given.

Let . Note that , and therefore that . Also note that if is SI in , then is a decreasing function of . Similarly, if is SD in , then is an increasing function of .

Using integration by parts, one can show that

| (3.19) |

the integral on the left remaining positive if is SI in while is PQD. Likewise, the integral on the left remains negative if is SI in while is NQD.

Let us now write the Taylor expansion for a bivariate copula :

| (3.20) |

If one neglects the remainder term , then one can write that the outer copula in Equation (3.14) is, taking into account that is conditionally invariant,

| (3.21) |

Note that both

| (3.22) |

and

| (3.23) |

are positive since the inner copula is stochastically decreasing in both its arguments and is necessarily positive .

Moreover, by Equation (3.19),

is a positive quantity, since is NQD and is SD in . Therefore the outer copula can be approximated by plus some positive quantity, , leading to the claim of the conjecture that .

It is also possible to express a similar conjecture for :

Conjecture 3.15.

Let the inner copula in (3.14), , be stochastically increasing in both its arguments and be conditionally invariant. If, moreover, is NQD while is SI in , then , .

The motivation is almost exactly the same as that of Conjecture 3.14 and is therefore left to the reader.

Of course, one might wonder at this point how reasonable it is to neglect the remainder term in (3.20). In what follows, an attempt at detecting at least one example where Conjecture 3.15 fails is presented.

Let the inner copula be one of the 9 following copulas:

- •

- •

-

•

or a Frank copula with a parameter’s value of 2.5, 6 or 14 (again, in an effort to have low, moderate and high dependence).

All these inner copulas are conditionally invariant and SI in both arguments as required by Conjecture 3.15. Hereafter is the proof that the proposed FGM copulas are SI in both arguments.

The expression of a FGM copula is

where .

One can calculate that

and that

In order for the copula to be SI in both its arguments, these two expressions have to be negative. Obviously, this will be the case as long as is positive.

Let now be one of the following copulas:

-

•

a Plackett copula with a parameter’s value of 3, 12 or 64,

-

•

a Frank copula with a parameter’s value of 2.5, 6 or 14,

-

•

or a FGM copula with a parameter’s value of 0.25, 0.5, 1.

These copulas are all SI in (at least) their second argument, as requested by Conjecture 3.15.

Finally, let be one of the following 9 copulas:

-

•

a Mardia copula with a parameter’s value of -0.25, -0.5 or -0.75,

-

•

a Frank copula with a parameter’s value of -2.5, -6 or -14,

-

•

or a FGM copula with a parameter’s value of -0.25, -0.5 or -1.

These copulas are all NQD, as required by Conjecture 3.15. A Mardia copula (Mardia, 1970; Nelsen, 2006) is defined as

| (3.24) |

where is the upper Fréchet–Hoeffding bound and the lower one, with . A Mardia copula is NQD as long as (Nelsen, 2006, p. 188).

In total, there are combinations or setups of interest for the 27 presented copulas. For each of these 729 combinations, it is checked if , that is, if the outer copula is below the inner one, for a grid of 100 points in . Since is calculated through numerical integration, one must take into account the error on before being able to conclude that . This is performed through the following hypothesis test:

| , | |

| , |

with the following test statistic:

and where the p-value is the surface on the left of this test statistic.

Since for a given a setup, the test has to be run over a grid of 100 points, 100 p-values is obtained for each of the setups. To summarize all these p-values, the average p-value is calculated for each setup.

![[Uncaptioned image]](/html/1612.02848/assets/table3-1.png) |

Results: For all setups except the one using as inner copula a Frank copula with a parameter’s value of 14, the average p-value was less than 1e-7. Results for the inner Frank copula with a parameter’s value of 14 are reported in Table 1, where the rows are the various presented earlier, while the columns are the various presented earlier.

3.7 Identifiability

A model is said to be identifiable if it is theoretically possible to learn the true values of this model’s underlying parameters after obtaining an infinite number of observations from it. Mathematically, this is equivalent to saying that different values of the parameters must generate different probability distributions of the observable variables. That is, if is a statistical model, with a probability measure on a fixed space, the model is identifiable if implies that .

Example 3.16.

In Equation (2.14), let and be Farlie-Gumbel-Morgenstern copulas, that is,

with . The outer copula can be showed to be

Thus, one can see that

whenever , and the last equation can be satisfied even if .

Example 3.17.

In Equation (2.14), let be the independance copula for . Then, the outer copula is

which can be simplified to

The model is thus not identifiable: all values of lead to the same model, the independence copula.

Example 3.18.

In Equation (2.15), let , be a Gaussian copula with correlation and be a Gaussian copula with correlation . Moreover, let be a Gaussian copula with correlation . Then, it can be shown that the outer copula is a Gaussian copula with correlation

Even in the case where , this becomes

In order to shed more light on identifiability issues, a few case studies based on the Fisher information matrix are presented. The Fisher information matrix can indeed be used to check if a model is locally identifiable, see Rothenberg (1971) or Iskrev et al. (2010). If the model is not locally identifiable all over its parameter space, then it is not, in general, identifiable in that parameter space. Let be the density of an EOFC. Then, the related Fisher information is defined as

| (3.25) |

Checking if a model is locally identifiable everywhere in is the same as checking where in this matrix is singular (Iskrev et al., 2010).

Numerical computation of this matrix at a point can be done in various ways. First, one can generate observations from the target model at point using Algorithm 1 and then compute

where is numerically approached.

So, for instance, if , we have

for set to an arbitrary small value.

Another approach to compute the Fisher information in (3.25) is through numerical integration. Indeed,

where has to be numerically approached, too.

Note that in both approaches, the computation of itself requires numerical integration, which is performed, in this paper, using adaptative multidimensional integration (Steven and Balasubramanian, 2013) or naive Monte Carlo integration.

Case study 1 to 3. Let be a Frank copula with a parameter’s value such that and 0.75. The inner copula in all three cases is a normal copula with correlation . The model turned out to be locally identifiable for each of the 3 cases. Table 2 displays the results for case 3.

| 0.09 | 0.18 | 0.27 | 0.36 | 0.45 | 0.55 | 0.64 | 0.73 | 0.82 | 0.91 | |

| 0.595 | 0.745 | 0.949 | 1.246 | 1.698 | 2.438 | 3.908 | 6.762 | 15.617 | 58.255 |

Case study 4. In this case study, the inner copula is the independence one, is a Gumbel copula with a fixed parameter value corresponding to a moderate dependence and is the copula with the parameter of interest, . Table 3 shows a rapid decrease of the Fisher information as the parameter of interest increases.

| 0.09 | 0.18 | 0.27 | 0.36 | 0.45 | 0.55 | 0.64 | 0.73 | 0.82 | 0.91 | |

| 1.30 | 0.73 | 0.43 | 0.24 | 0.13 | 0.06 | 0.02 | ¡1e-2 | ¡1e-3 | ¡1e-5 |

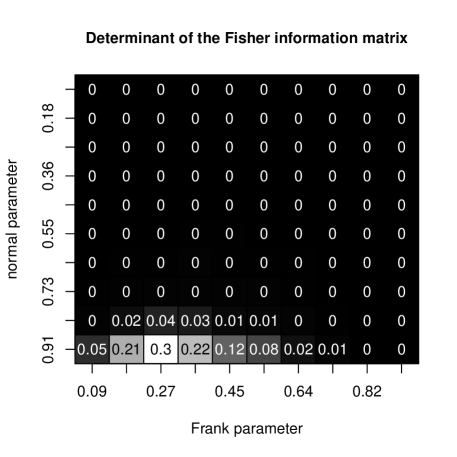

Case study 5. In this last case study, is the independence copula, is the Frank copula with parameter and the inner copula is the normal copula with parameter . The Fisher information is this times a matrix. Figure 1 shows the determinant of the matrix as a function of , expressed as a Kendall’s tau for convenience, and .

|

As one can see, the model is locally identifiable in a narrow part of the space of the parameters, picking at around (0.91, 0.27).

4 Data generation

To generate one realization of the random vector with distribution given by (2), one takes the second part of , from to , a realization of , where is the latent factor. Remembering that, given , the distribution of can be split into the inner copula and a set of univariate margins , with denoting the inverse function, , the following algorithm produces the desired output.

Note that, in the presence of conditional invariance, step 1 in the above algorithm is not required for step 2. Needless to say, in the first step, one could have sampled from , the distribution of , and in the second step, one would have sampled from instead of .

Data generation for a NEOFC can be performed using a generalized version of Algorithm 1. The main hurdle for this generalization is to define , such that

or, in short, such that .

Recall that

and that .

Now define as the inverse function of , that is,

This is the same as writing

Since is just a composition of the form , we can extract back using the composition . The inverse of is therefore:

| (4.1) |

Input. A NEOFC, that is, a -variate copula , the related mappings, bivariate copulas , and the related parameters.

Output. One observation from the input NEOFC, as a -dimensional vector.

The end result of the last step of Algorithm 2 is a vector , one observation from the input NEOFC. Run Algorithm 2 multiple times to get multiple observations.

Critical to both algorithms in this section is the inversion of with respect to in the case of an EOFC or of with respect to in the case of a NEOFC. This is usually not hard to get symbolically. In the worst cases, or can be get numerically.

5 Models

In this section, several models built from Equation (2) or Equation (2.11) are presented, including many well-known copula models from the literature.

Krupskii-Huser-Genton copulas.

In their paper, Krupskii et al. (2016) offer a new family of one-factor copulas that can be used to model replicated spatial data. Let be a -variate Gaussian copula with correlation matrix . Let

where is some univariate CDF, while is the CDF of the univariate standard Gaussian distribution. Then, the KHG family of copulas corresponds to an EOFC where and , .

As shown by Krupskii et al. (2016), tail dependence and tail asymmetry for this model is possible, based on the choice of and .

Let , , be a bivariate margin of , the outer copula. Recall that the lower tail dependence of a bivariate copula, such as , is (Hartmann et al., 2004; McNeil et al., 2015):

while the upper one is defined as

As an example, if

Krupskii et al. (2016) showed that for any bivariate margin of , as long as , and , or as long as , and ,

A more interesting case however arises if , and . Then,

meaning that tail asymmetry becomes possible through the correlation matrix .

The upper tail dependence coefficient can also be made such that : one need to let , and .

For more examples and details, refer to Krupskii et al. (2016).

Farlie-Gumbel-Morgenstern copulas.

Let the inner copula of a bidimensional EOFC be such that , while are Farlie-Gumbel-Morgenstern copulas with parameters and . Then, the resulting outer copula is a FGM copula with parameter . Although a bit tedious, the proof is trivial. Also refer to Example 3.16.

Note that in a bivariate FGM with parameter , the related Kendall’s tau is (Nelsen, 2006, p. 162). This means that even if the parameters and of and are set to their upper limit, the parameter of the resulting FGM will be 1/3, corresponding to a rather low Kendall’s tau of 0.074. The model where , while are FGM copulas, is thus trapped between a correlation of -0.074 and 0.074 only. This can be fixed using EOFCs.

In an EOFC, the inner copula can be viewed as the baseline level of dependence. Instead of letting , one could let , where is the upper Fréchet-Hoeffding bound. In this scheme, the two FGM copulas can only be used to decrease the dependence between the two random variables of interest, and . Figure 2 shows the empirical Kendall’s tau calculated (sample size = 1000) for various combinations of and when the inner copula is . As one can see, the improved model is now trapped between a correlation of and 1. This range can thus be tuned by changing the inner copula.

|

Archimedean copulas.

Let be a completely monotonic function on , that is, for all integers and all , and such that while

If a copula can be written as

then it is called an Archimedean copula with generator (McNeil, 2008). Let us note that, in order to make sure is a proper copula, the above-mentioned conditions on are sufficient, but not necessary. For sufficient and necessary conditions, see McNeil and Nešlehová (2009).

Proposition 5.1.

Proof.

Checking that is a copula is straightforward. Moreover, since

it holds that

∎

Note that a reformulation of the above construction can be found in Joe (2001).

Hierarchical Archimedean copulas.

Archimedean copulas can be nested in order to get more flexible models. Hierarchical or Nested Archimedean copulas (HACs or NACs) were introduced by Joe (2001) and have been the main topic of many research papers since, see for instance McNeil (2008), Hofert and Pham (2013), or Okhrin et al. (2013). The simplest hiearchical Archimedean copula consists of a bivariate Archimedean copula

which is nested into another bivariate Archimedean copula

in order to get a copula of the form

| (5.1) |

In general, an arbitrary pair of generators does not ensure that the copula in Equation (5.1) is a proper copula. See Joe (2001) and McNeil (2008) for more on this matter.

Proposition 5.2.

Hierarchical NEOFCs.

OFCs are not suited to model hierarchical dependence. Assume that one wishes to build a one-factor copula on such that the resulting model is described by the matrix of Kendall’s taus in (5.3).

| (5.3) |

Since and are related through the maximum value of 1, it means that their bivariate margin must be

Similarly, the bivariate margin of and is

Therefore, the OFC on has to be

By proposition 3.3 however, this corresponds to , for which the correlation matrix is not (5.3). A OFC will never be able to reproduce a matrix of Kendall’s taus such as the one in (5.3). In general, OFCs do not seem to be suited to model matrices of the form

| (5.4) |

in which .

On the other hand, it is possible to build NEOFCs for which the matrix of Kendall’s taus is as in (5.4).

Start from Equation (2.11), and let , that is, we have a triple layer of linking copulas. Let . For , let all linking copulas be a Frank copula with a same parameter . This layer gives the baseline level of dependence between the four random variables of interest. Next, use the second layer, , to couple and , that is, let and be a Frank copula with a common paramater , while and are set to the independence copula. Finally use the first layer, , to couple and , that is, let and be a Frank copula with a common paramater , while and are set to the independence copula. Table 4 allows one to visualize this scheme.

| Frank | Frank | ||||

| Frank | Frank | ||||

| Frank | Frank | Frank | Frank | ||

Example 5.3.

In Table 4, set to a value of 5.74, corresponding to a Kendall’tau of 0.5 for the related linking copulas and to a value of 6.73, corresponding to a Kendall’s tau of 0.55 for the related linking copulas. The empirical Kendall’s taus based on 10000 observations generated from the model through Algorithm 2 are as shown hereafter.

> round(cor(generated.data, method="kendall"), 3)

[,1] [,2] [,3] [,4]

[1,] 1.000 0.559 0.119 0.123

[2,] 0.559 1.000 0.118 0.121

[3,] 0.119 0.118 1.000 0.563

[4,] 0.123 0.121 0.563 1.000

While the correlation between , and , is strong, one can note that even though corresponds to a correlation of 0.5, the correlation for the couples , , and appears to have dampen to . Pushing towards higher values can help: if is set to a value of 14.14, corresponding to a Kendall’s tau of 0.75, the empirical Kendall’s taus become as shown hereafter.

> round(cor(generated.data, method="kendall"), 3)

[,1] [,2] [,3] [,4]

[1,] 1.000 0.743 0.220 0.222

[2,] 0.743 1.000 0.219 0.222

[3,] 0.220 0.219 1.000 0.738

[4,] 0.222 0.222 0.738 1.000

This increase remains however slow and even with a high value for , such as 38.28, corresponding to a Kendall’s tau of 0.9, the correlation between and will not exceed 0.27.

To overcome the issue of low dependence between the pairs , , and , one can make use of the inner copula to set the baseline level of dependence, rather than using a layer of identical linking copulas. See Table 5.

| Frank | Frank | ||||

| Frank | Frank | ||||

| Frank | |||||

Example 5.4.

In Table 5, set to a value of 14.14, corresponding to a Kendall’s of 0.75, to 1.38, corresponding to a Kendall’s tau of 0.15, and to 6.73, corresponding to a Kendall’s of 0.55. The empirical Kendall’s taus based on 10000 observations generated from the related hierarchical NEOFC are shown hereafter.

> round(cor(generated.data, method="kendall"), 3)

[,1] [,2] [,3] [,4]

[1,] 1.000 0.755 0.388 0.385

[2,] 0.755 1.000 0.387 0.385

[3,] 0.388 0.387 1.000 0.809

[4,] 0.385 0.385 0.809 1.000

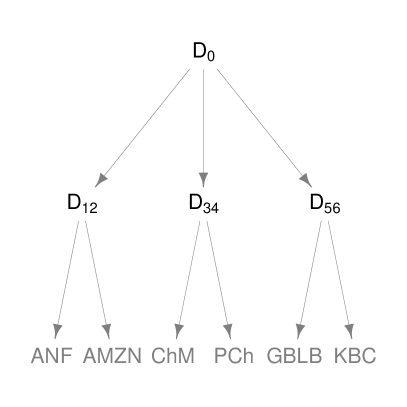

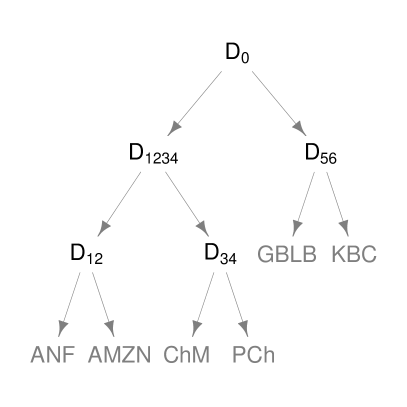

As last example of a hierarchical NEOFC, we revisit the tree on the right of Figure 11 in Segers and Uyttendaele (2014), this tree corresponding to an attempt to map the dependencies between daily log returns using hierarchical Archimedean copulas. Figure 11 in Segers and Uyttendaele (2014) is, for convenience, reproduced in this paper as Figure 3.

|

|

The tree on the right of Figure 3 corresponds to the hierarchical NEOFC from Table 6, where the symbols on the right of the table are there to help one compare the table with the tree on the right of Figure 3.

| Frank | Frank | ||||||

| Frank | Frank | ||||||

| Frank | Frank | ||||||

| Frank | Frank | Frank | Frank | ||||

| Frank | |||||||

Note that, given the tree structure of a hierarchical Archimedean copula, the corresponding NEOFC will have as many layers as there are internal nodes in the tree when the inner copula is set to independence, or, when the inner copula is used as root node, as many layers as there are internal nodes in the tree minus one.

Example 5.5.

Set the various parameters of Table 6 to the arbitrary values shown in Table 7. The empirical Kendall’s taus based on 10000 observations generated from the related hierarchical NEOFC are shown hereafter.

> round(cor(generated.data, method="kendall"), 3)

[,1] [,2] [,3] [,4] [,5] [,6]

[1,] 1.000 0.776 0.400 0.406 0.476 0.478

[2,] 0.776 1.000 0.404 0.407 0.475 0.475

[3,] 0.400 0.404 1.000 0.775 0.485 0.483

[4,] 0.406 0.407 0.775 1.000 0.489 0.487

[5,] 0.476 0.475 0.485 0.489 1.000 0.755

[6,] 0.478 0.475 0.483 0.487 0.755 1.000

Note that, in contrast to what is usually required for hierarchical Archimedean copulas, the dependence in hierarchical NEOFCs is not required to be a nondecreasing function as one goes farther away from the root node. The empirical matrix from the last example indeed shows that the dependence at node is , that of node is lower, around , but that of the root is higher than , at around 0.475.

Gaussian copulas.

A Gaussian copula is a copula whose density satisfies

| (5.5) |

where is a invertible correlation matrix, and is the quantile of order of the standard normal distribution. A Gaussian copula can be represented as in (2). Let be a real vector in and let be a diagonal matrix with elements given by . Finally let be a -variate Gaussian copula with correlation matrix .

Proposition 5.6.

Let and let be a bivariate Gaussian copula with correlation , . Then the outer copula in (2) is a Gaussian copula with correlation matrix given by .

Proof.

Let be a symmetric nonnegative matrix whose diagonal elements are equal to and whose element in the -th row and -th column is denoted . Let be distributed according to a -variate centered Gaussian distribution with variance-covariance matrix given by

so that . The partial correlations are given by

or, in other words, the partial correlation matrix is . Given , the margins are , hence

and, moreover, the corresponding copula is a Gaussian copula , with correlation matrix .

Calculate the copula corresponding to . Let be the cumulative distribution function of the univariate standard Gaussian distribution.

This expression corresponds exactly to the copula given in (2), with

see Meyer (2013) for details.

∎

Note: in the case , the outer copula is a Gaussian copula with correlation given by

Also see Example 3.18.

C-Vine copulas.

Let be a random vector following a C-Vine copula distribution truncated after the second level. The density of this truncated C-Vine is given by

| (5.6) |

where , , is a set of arbitrary bivariate copulas, and is a set of abritrary copula densities for each . Due to their extreme flexibility and ease of use (one only has to specify sets of bivariate copulas), Vine copulas have been used in an increasing number of applications and are still a hot topic of research, see for instance Aas et al. (2009), Kurowicka and Joe (2011) or Bedford and Cooke (2002).

Proposition 5.7.

-factor models.

Define respectively -factor and -factor copulas as copulas of the form

| (5.7) | |||

| (5.8) |

where for and , and where the are (arbitrary) bivariate copulas. -factor and -factor copulas have been studied in Krupskii and Joe (2013, 2015) as copula models for conditionally independent variables given respectively one and two latent factors.

The following (trivial) proposition aims at recovering -factor and -factor copulas as special cases of the model (2).

Proposition 5.8.

Note that in the above proposition actually does not depend on hence we have conditional invariance. This restriction can be easily removed as follows. Let, for each , be a set of bivariate copulas and

where . The outer copula is then

6 Inference

This section discusses estimation of models of the form (2) or (2.11), as well as how one can test for conditional independence for models of the form (2).

6.1 Estimation

Let, in (2), and

where is a mapping which, to each in the support of , associates a parameter in the appropriate parameter space. If the mapping depends on a vector of parameters, as in (3.2), we also denote this vector by . Likewise, we denote the parameter vector which contains the parameters of the quantile function of by . Accordingly, the notation for the copula of becomes . Finally, let us denote by , , the sample of the distribution with margins and copula .

The pseudo log likelihood function to maximize is

| (6.1) |

where stands for the complete parameter vector, that is, , and denotes an estimate of , . There are many ways to estimate . For instance, may be the empirical distribution function, as in Genest et al. (1995), or may be a parametric estimate, as in Joe and Xu (1996).

6.2 Testing for conditional independence

This section provides procedures to test for conditional independence in models based on the representation (2). Indeed, being able to assess if the variables of interest are dependent or independent conditioned on the latent factor seems a crucial issue. Conditional independence would mean that the factor captures all the dependence in the data whereas no conditional independence would mean that there is a remaining, intrinsic dependence in the variables even though the factor has been accounted for.

Throughout this subsection, the bivariate copulas , , are assumed to belong to some known parametric families. The inner copula , however, can be left fully unspecified: either nothing is known about it, either a parametric form is assumed. The possibility to carry out a hypothesis test in this setting is new to the literature.

The hypothesis test for conditional independence is of the form

| versus |

(recall that stands for the independence copula or the product function), where for two functions and , means that for all in their domain.

If a certain parametric form is assumed for , such as in Section 2, then most likely the test will reduce to testing for a parameter to equate a certain value, and no conceptual difficulties refrain the task. For instance, in (3.2), testing for conditional independence amounts to testing for or (conceptually). Let us remark that testing for conditional invariance is also feasible: one need to test .

If is left fully unspecified, the alternative hypothesis needs to be slightly restricted in order for a test to exist. Consider

| versus | (6.2) |

Then, the alternative hypothesis is: “conditioned on the factor, the variables of interest are positively dependent”.

Let be the risk of type I error. One rejects if , where is chosen so that and where

| (6.3) |

where is the Fréchet-Hoeffding upper bound for copula and

| (6.4) |

is the empirical estimator of ; , , being the data ; and being the empirical distribution function of .

The heuristic underlying the expression of , the test statistic, is as follows. Denote by the outer copula under , that is, one substitutes for the inner copula in (2) and gets

| (6.5) |

If is true, then the true copula verifies . But if is false, implies . In order to reject the null, one could therefore compare the empirical copula to , the latter being an estimate of , and reject the null if is too large. However, as the distribution of this difference under is unknown, one would need to use bootstrap and fit to simulated data a large number of times, a process far too expensive for most hardware.

To overcome this issue, the comparison of to is done indirectly using the Fréchet-Hoeffding upper bound as a baseline (note that the Fréchet-Hoeffding lower bound for copulas could also be considered as a baseline for comparison, the upper one was however picked since it has the nice property to be a copula , although this property is by no means required for the test). The result of this suggestion is (6.3), which describe a test statistic always positive and expected to take small values when is false.

The bootstrap of is now described. Note that under , the outer copula in (6.5) is fully parametric: one can obtain an estimate by maximum pseudo-likelihood (Krupskii and Joe, 2013). New bootstrap samples (say of them) are then drawn using Algorithm 1 in order to get test statistics . These can be used, for instance, to compute a p-value as . In other words, the p-value is estimated by counting how many test statistics in , are lower or equal than the test statistic , built using the data from the original sample.

Finally, let us note that the test against can be carried out by considering (6.3) again, but this time with a rejection region on the right, that is, we reject if , where is chosen so that .

7 Illustrations

The purpose of this section is to illustrate how one can take advantage of the framework presented in Section 2 in practice and to study the power of the test statistic in (6.3) by means of a simulation experiment. We first provide a few technical details on how some numerical operations were performed.

7.1 Computational aspects

In this section, log-likelihoods are maximized using either gradient descent algorithms, which can be found in the optim function of the statistical software R, or differential evolution (Storn and Price, 1997; Qin and Suganthan, 2005; Price et al., 2006), for which a R package also exists: DEoptim (Mullen et al., 2011).

Note that gradient descent algorithms usually require to provide a starting parameter vector. It is advised to try several such points and retain the best result for the likelihood.

For the numerical evaluation of the integral in (6.1), either naive Monte-Carlo integration was used, where the integration space is sampled a thousand times according to a uniform distribution that stretches over the integration space, or adaptative multidimensional integration was used (Steven and Balasubramanian, 2013).

Note that in case of a one-factor copula or of an extended one-factor copula, the integration space is the segment . However, with a nested extended one-factor copula, the integration space becomes and is therefore multi-dimensional.

7.2 Revisiting the daily log returns from Segers and Uyttendaele (2014)

In Segers and Uyttendaele (2014), raw daily log returns from January 2010 to December 2012 of the following indices were gathered with the help of Yahoo! Finance:

-

•

Abercrombie & Fitch Co. (ANF), traded in New York;

-

•

Amazon.com Inc. (AMZN), traded in New York;

-

•

China Mobile Limited (ChM), traded in Hong Kong;

-

•

PetroChina (PCh), traded in Hong Kong;

-

•

Groupe Bruxelles Lambert (GBLB), traded in Brussels;

-

•

and KBC Group (KBC), traded in Brussels.

They then analyzed the filtered data using hierarchical Archimedean copulas. The result was the estimation of the two tree structures in Figure 3. Refer to their paper for more details.

In this subsection, we fit the hierarchical NEOFC described by Table 6 on the same filtered data, in an effort to reproduce their results. The fit is the result of the maximization of the related likelihood using the DEoptim function. The estimated parameters for the model in Table 6 are, expressed as Kendall’s taus for convenience,

-

•

,

-

•

,

-

•

,

-

•

,

-

•

and .

Also refer to Table 7.

The Kendall’s taus between the random variables of interest induced by the fitted model are however unknown but can be calculated through simulation. Hereafter is the matrix of Kendall’s taus between the random variables of interest, calculated using 10000 observations from the fitted hierarchical NEOFC.

ANF AMZN ChM PCh GBLB KBC

ANF 1.00 0.28 0.13 0.14 0.12 0.12

AMZN .... 1.00 0.12 0.12 0.13 0.13

ChM .... .... 1.00 0.34 0.10 0.11

PCh .... .... .... 1.00 0.10 0.11

GBLB .... .... .... .... 1.00 0.36

KBC .... .... .... .... .... 1.00

This can be compared to the matrix of Kendall’s taus induced by the tree structure on the right of Figure 3, also see Segers and Uyttendaele (2014):

ANF AMZN ChM PCh GBLB KBC

ANF 1.00 0.31 0.08 0.08 0.18 0.18

AMZN .... 1.00 0.08 0.08 0.18 0.18

ChM .... .... 1.00 0.35 0.18 0.18

PCh .... .... .... 1.00 0.18 0.18

GBLB .... .... .... .... 1.00 0.44

KBC .... .... .... .... .... 1.00

The Kendall’s taus from the fitted hierarchical NEOFC however match the ones induced by the model on the left of Figure 3 more:

ANF AMZN ChM PCh GBLB KBC

ANF 1.00 0.31 0.14 0.14 0.14 0.14

AMZN .... 1.00 0.14 0.14 0.14 0.14

ChM .... .... 1.00 0.35 0.14 0.14

PCh .... .... .... 1.00 0.14 0.14

GBLB .... .... .... .... 1.00 0.44

KBC .... .... .... .... .... 1.00

7.3 Power of the test for conditional independence

In this section, we study the power of the test statistic in (6.3) by means of a simulation experiment. We considered the test (6.2) and set the type I error risk to . We drew datasets of size and from the model (2), with and being Clayton copulas as in (3.1) with parameters , , such that Kendall’s coefficients are equal to 0.4 for , 0.5 for and 0.6 for . The inner copula was a normal copula as in (5.5) with correlation matrix

| (7.1) |

for , and, finally, . (There are samples of size and for each ). Note that corresponds to the null hypothesis .

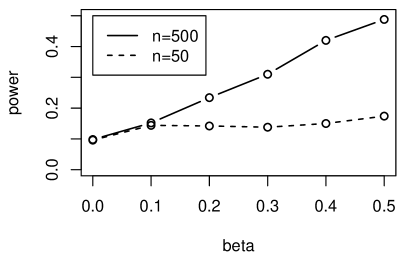

For each sample, , we calculated a -value based on 200 boostrap replications. That is, we calculated the proportion of 200 simulated test statistics that where lower or equal than the observed one. As rejection occurs whenever the -value is lower or equal to the type I error risk , we approximated the power by the proportion of the falling below . See Section 6.2 for details.

Figure 4 shows the estimated power of in (6.3). As it was expected, the power of the test increases as and grow. Furthermore the power is equal to the type I error risk under the null, that is when .

|

8 Conclusion

In this paper, we extended the scope of one-factor copulas thanks to Equations (2), (2) and (2.11). Models built using these equations can now feature a varying conditional dependence structure and a factor’s distribution not restricted to be the standard uniform. General dependence properties for these models were given and explicit examples were discussed. The usefulness of these models was illustrated by considering the estimation of the dependence of 6 daily log returns already analyzed in Segers and Uyttendaele (2014). Furthermore, a novel hypothesis test was constructed in order to assess whether conditional independence holds or not, and the power of that test was studied through a simulation experiment.

References

- Aas et al. (2009) Kjersti Aas, Claudia Czado, Arnoldo Frigessi, and Henrik Bakken. Pair-copula constructions of multiple dependence. Insurance: Mathematics and Economics, 44(2):182–198, 2009.

- Balakrishnan and Lai (2009) Narayanaswamy Balakrishnan and Chin-Diew Lai. Continuous bivariate distributions. Springer Science & Business Media, 2009.

- Bedford and Cooke (2002) Tim Bedford and Roger M. Cooke. Vines - a new graphical model for dependent random variables. The Annals of Statistics, 30(4):1031–1068, 2002.

- Genest et al. (1995) Christian Genest, Kilani Ghoudi, and Louis-Paul Rivest. A semiparametric estimation procedure of dependence parameters in multivariate families of distributions. Biometrika, 82(3):543–552, 1995.

- Hartmann et al. (2004) Philipp Hartmann, Stefan Straetmans, and Casper G. De Vries. Asset market linkages in crisis periods. Review of Economics and Statistics, 86(1):313–326, 2004.

- Hofert and Pham (2013) Marius Hofert and David Pham. Densities of nested Archimedean copulas. Journal of Multivariate Analysis, 118:37–52, 2013.

- Iskrev et al. (2010) Nikolay Iskrev et al. Evaluating the strength of identification in DSGE models. An a priori approach. In Society for Economic Dynamics, 2010 Meeting Papers, 2010.

- Joe (2001) Harry Joe. Multivariate models and dependence concepts. Chapman & Hall/CRC, 2001.

- Joe (2014) Harry Joe. Dependence Modeling with Copulas. Chapman & Hall, 2014.

- Joe and Xu (1996) Harry Joe and James Jianmeng Xu. The estimation method of inference functions for margins for multivariate models. Technical report, Department of Statistics, University of British Columbia, Vancouver, 1996.

- Kemp et al. (1992) A.W. Kemp, T.P. Hutchinson, and Chin Diew Lai. Continuous bivariate distributions, emphasising applications, 1992.

- Krupskii and Joe (2013) Pavel Krupskii and Harry Joe. Factor copula models for multivariate data. Journal of Multivariate Analysis, 120:85–101, 2013.

- Krupskii and Joe (2015) Pavel Krupskii and Harry Joe. Structured factor copula models: Theory, inference and computation. Journal of Multivariate Analysis, 138:53–73, 2015.

- Krupskii et al. (2016) Pavel Krupskii, Raphael Huser, and Marc G. Genton. Factor copula models for replicated spatial data. arXiv:1511.03000, 2016.

- Kurowicka and Joe (2011) D. Kurowicka and H. Joe. Dependence Modeling: Vine Copula Handbook. World Scientific, 2011.

- Mardia (1970) Kantilal Varichand Mardia. Families of bivariate distributions, volume 27. Griffin London, 1970.

- Mazo et al. (2015) Gildas Mazo, Stephane Girard, and Florence Forbes. A flexible and tractable class of one-factor copulas. Statistics and Computing, pages 1–15, 2015.

- McNeil (2008) Alexander J. McNeil. Sampling nested Archimedean copulas. Journal of Statistical Computation and Simulation, 78(6):567–581, 2008.

- McNeil and Nešlehová (2009) Alexander J. McNeil and Johanna Nešlehová. Multivariate Archimedean copulas, -monotone functions and -norm symmetric distributions. The Annals of Statistics, 37:3059–3097, 2009.

- McNeil et al. (2015) Alexander J. McNeil, Rüdiger Frey, and Paul Embrechts. Quantitative risk management: Concepts, techniques and tools. Princeton university press, 2015.

- Meyer (2013) Christian Meyer. The bivariate normal copula. Communications in Statistics-Theory and Methods, 42(13):2402–2422, 2013.

- Mullen et al. (2011) Katharine Mullen, David Ardia, David Gil, Donald Windover, and James Cline. DEoptim: An R package for global optimization by differential evolution. Journal of Statistical Software, 40(6):1–26, 2011.

- Nelsen (2006) Roger B. Nelsen. An introduction to copulas. Springer, New York, 2006.

- Oh and Patton (2015) Dong Hwan Oh and Andrew J. Patton. Modelling dependence in high dimensions with factor copulas. Journal of Business & Economic Statistics, 2015.

- Okhrin et al. (2013) Ostap Okhrin, Yarema Okhrin, and Wolfgang Schmid. Properties of hierarchical Archimedean copulas. Statistics & Risk Modeling, 30(1):21–54, 2013.

- Price et al. (2006) Kenneth Price, Rainer Storn, and Jouni Lampinen. Differential Evolution - A Practical Approach to Global Optimization. Natural Computing. Springer-Verlag, January 2006.

- Qin and Suganthan (2005) Kai Qin and Ponnuthurai Suganthan. Self-adaptive differential evolution algorithm for numerical optimization. In 2005 IEEE congress on evolutionary computation, volume 2, pages 1785–1791. IEEE, 2005.

- Rothenberg (1971) Thomas J. Rothenberg. Identification in parametric models. Econometrica: Journal of the Econometric Society, pages 577–591, 1971.

- Segers and Uyttendaele (2014) Johan Segers and Nathan Uyttendaele. Nonparametric estimation of the tree structure of a nested Archimedean copula. Computational Statistics & Data Analysis, 72:190–204, 2014.

- Sklar (1959) Abe Sklar. Fonction de répartition dont les marges sont données. Institut de statistique de l’Université de Paris, 8:229–231, 1959.

- Skrondal and Rabe-Hesketh (2007) Anders Skrondal and Sophia Rabe-Hesketh. Latent variable modelling: A survey. Scandinavian Journal of Statistics, 34(4):712–745, 2007.

- Steven and Balasubramanian (2013) Johnson Steven and Narasimhan Balasubramanian. Cubature: Adaptive multivariate integration over hypercubes, 2013. R package version 1.1-2.

- Storn and Price (1997) Rainer Storn and Kenneth Price. Differential evolution–a simple and efficient heuristic for global optimization over continuous spaces. Journal of global optimization, 11(4):341–359, 1997.