Analysis of Multi-Index Monte Carlo Estimators

for a Zakai SPDE

Abstract

In this article, we propose a space-time Multi-Index Monte Carlo (MIMC) estimator for a one-dimensional parabolic stochastic partial differential equation (SPDE) of Zakai type. We compare the complexity with the Multilevel Monte Carlo (MLMC) method of Giles and Reisinger (2012), and find, by means of Fourier analysis, that the MIMC method: (i) has suboptimal complexity of for a root mean square error (RMSE) if the same spatial discretisation as in the MLMC method is used; (ii) has a better complexity of if a carefully adapted discretisation is used; (iii) has to be adapted for non-smooth functionals. Numerical tests confirm these findings empirically.

1 Introduction

Stochastic partial differential equations (SPDEs) have become an area of active research over the last few decades. Several classes of methods have been developed to solve SPDEs numerically, including finite difference schemes [13, 11, 12, 5], finite element schemes [28, 19], and stochastic Taylor schemes [16, 17].

This article is motivated by Zakai SPDEs of the form (see [9]),

| (1.1) |

where is a standard Brownian motion and , and suitably chosen coefficient functions. This Zakai equation arises from a nonlinear filtering problem: given an observation process and a signal process , we want to estimate the conditional distribution of given . If satisfies

where and are independent standard Brownian motions, and the distribution function has a density , it is proved in [21] that satisfies (1.1) with

The conditional (on ) distribution function is then

and it is the goal of this article to estimate the expectation of functionals of this form.

For simplicity, we restrict ourselves to the special case

| (1.2) |

where , is a standard Brownian motion, and and are real-valued parameters. This is a special case of (1.1) where .

Moreover, in (1.2) describes the limit empirical measure, as , of a large exchangeable particle system [21],

| (1.3) |

where and are independent standard Brownian motions.

A direct application of this model is the large portfolio credit model [3]. Assume the market consists of different firms where are “distance-to-default” processes. Then the functional of interest is the loss

| (1.4) |

i.e., the mass lost at the absorbing boundary. In the credit risk application of [2], describes the loss in a structural credit model, i.e., the fraction of firms whose values have crossed zero and which are considered defaulted. The values of credit products are often functions of the loss .

Generally, the solution to (1.1) is not known analytically and has to be approximated numerically. A survey of methods is given in [9], and we focus here on recent applications of multilevel methods as they pertain to this article. Giles and Reisinger [8] used an explicit Milstein finite difference approximation to the solution of (1.2). By using Fourier analysis, this scheme can be shown to give first order of convergence in the timestep and second order in the spatial mesh size. One constraint in this paper is that the timestep needs to be small enough to ensure stability. Inspired by the numerical analysis of SDEs in [27, 1], [25] extended the discretisation to an implicit method on the basis of the - time-stepping scheme, where the drift and the deterministic part of the double stochastic integral are taken implicit. Fourier analysis shows that the convergence order is the same as in the explicit Milstein scheme, however, this scheme is unconditionally mean-square stable under a constraint on the correlation in (1.2). This unconditional stability is essential for our application as detailed below.

In this paper, we compare a new Multi-index Monte Carlo (MIMC) scheme in the spirit of [14], with the Multilevel Monte Carlo (MLMC) method of [6]. The MLMC method utilises a sequence of approximations to a random variable with increasing accuracy but also higher cost for increasing . In the simulation of an SDE, would typically be the refinement level of the time mesh, with time steps. The MLMC estimator is based on recursive control variates embedded in the identity

where is a maximum refinement level. The goal is to estimate by independent estimation of the summands, in a way that the root mean square error (RMSE) is comparable to the bias, but with a much reduced computational complexity. If fewer samples are needed for higher levels, the total computational cost is much lower than when using the standard Monte Carlo method (see Theorem 1 in [7]). In a second step, is adapted for a given RMSE target.

The MLMC method has been extended to SPDEs, in which case it gives even better savings due to the additional spatial dimensions. Giles and Reisinger [8] applied MLMC to simulate the SPDE (1.2) and the functional of its solution given in (1.4). Both timestep and mesh size decrease geometrically on different levels of refinement , with fixed . Thus, the variance of the estimators for is small for large , compared to the estimator for . As a result, for a fixed accuracy , the cost can be reduced significantly to instead of by the standard Monte Carlo estimator.

The approach taken here is to approximate this SPDE (1.2) by multi-index Monte Carlo simulation as introduced in [14]. The goal of MIMC is to improve the total complexity for higher-dimensional problems, where the cost of each sample on higher levels increases faster than the variance of MLMC estimators decays, such that the optimal complexity of is lost in MLMC. Multi-index Monte Carlo can be viewed as a combination of sparse grids [29] and MLMC methods. The level is now a vector of integer indices, corresponding to the refinement level in the different dimensions. Sparse grids, and hence MIMC, use high order mixed differences instead of only taking first order differences to construct a hierarchical approximation. More specifically, for a -dimensional problem, [14] first defines first order difference operators , such that

where is the unit vector in direction and is the estimator of level . Then the telescoping sum becomes

The strategy is to neglect terms with large where the cost is large and the contribution to the estimator is small. Instead of choosing an index as in MLMC, one now has to choose an index set of terms to include.

The main selling point of MIMC methods applied to higher-dimensional SPDEs, similar to sparse grid methods for high-dimensional PDEs, is that they can give a computational complexity with a fixed polynomial order multiplied by a log term, with an exponent which grows with the dimension . Both the sparse grid combination technique and the MIMC framework are based on certain specific expansions of the discretisation error in the mesh parameters. These have been proven for a growing class of PDEs [23, 24, 10]; [14] studies PDEs with random coefficients and refers to these PDE results in a path-wise sense, [7] analyses MIMC for nested simulation.

In this paper, we

-

•

apply MIMC to the SPDE (1.2) on a space-time mesh with an implicit Milstein time-stepping scheme and central spatial differences;

-

•

demonstrate that the expectation and variance of the multi-index estimators can be analysed by Fourier analysis, even if the required error expansions do not hold pathwise;

-

•

show that an extra term appears in the error expansion which explodes for small spatial mesh sizes, but by a suitable adaptation of the MIMC estimator a theoretical complexity of can be obtained, while the practically observed complexity is still as in the MLMC method [8];

-

•

give a seemingly innocuous variant of this approximation scheme, i.e., with the spatial approximation studied in [8], and show that the “standard” assumptions on the error expansion are only satisfied with lower order, such that the MIMC estimator is less efficient with complexity ;

-

•

give an example of a discontinuous functional and a simple approximation where we show that multiple leading order error terms appear, such that the optimal index set is not triangular, and demonstrate how MIMC can be adapted to this case.

Hence we show that although MIMC can be expected to work well in multi-dimensional situations compared to MLMC, this is not always true. In this paper, we only consider cases where MLMC gives optimal complexity order. Therefore, the results herein can be considered negative in the practical sense that worse performance, is obtained for MIMC than MLMC. In addition to these “negative” results being interesting in their own right, we provide a methodology to analyse MIMC estimators for a class of SPDEs. This method carries over to the higher-dimensional setting, where MIMC has complexity advantages over MLMC (as explained further in Section 8).

The rest of this article is structured as follows. We define two implicit Milstein finite difference schemes in Section 2, and the MIMC estimators in Section 3. The main theoretical result is provided in Section 4, where we analyse the convergence order of a MIMC estimator using Fourier analysis. Section 5 gives an “optimal index set” for this MIMC estimator and derives the total complexity for fixed accuracy. Section 6 derives further results for alternative approximations, while Section 7 shows numerical experiments confirming the above findings. Section 8 offers conclusions and directions for further research.

2 Two implicit Milstein finite difference schemes

Let be a probability space, on which there is given a one-dimensional standard Brownian motion . We study the parabolic stochastic partial differential equation

| (2.1) |

where , is a standard Brownian motion, and and are real-valued parameters, subject to the Dirac initial data

| (2.2) |

where is given. A classical result states that, for a class of SPDEs including (2.1), with initial condition in , there exists a unique solution [20]. This does not include Dirac initial data (2.2), but in fact, the solution to (2.1) and (2.2) at time is analytically known (see [8]) to be the smooth (in ) function

| (2.3) |

Integrating (2.1) over a time interval , we have

We then use a spatial grid with uniform spacing and a timestep , and let be the approximation to , , , where . We approximate by

| (2.4) |

Here denotes the closest integer to . To improve the accuracy of the approximation of in the present case of Dirac initial data, we subsequently choose such that is on the grid, then is an integer.

By an explicit Milstein scheme [8] with standard central difference approximation to the spatial derivatives, we have

where are independent standard normal random variables, and are first and second central difference operators,

However, there is a condition for the mean-square stability of this explicit scheme (see [8]), This is an obstacle for the use of the MIMC scheme where timestep and mesh size are varied independently. We can avoid the constraint on the timestep by using an implicit scheme instead [25]. Two implicit Milstein finite difference discretisations are conceivable for the SPDE (2.1):

-

1.

Discretise the spatial derivatives first, then apply the Milstein scheme to the resulting system of SDEs, i.e.,

(2.5) where .

-

2.

Apply the Milstein scheme first, then discretise the spatial derivatives. This gives

(2.6)

These two schemes have the same effect on the multilevel algorithm, and (2.6) is used in [8]. However, we will show that (2.6) is less efficient using the multi-index algorithm, as these two schemes result in different orders of variance for the MIMC estimators. Since the scheme (2.5) is more efficient, we will explore it in detail in Section 4, and the analysis of (2.6) in Section 6.1 is then similar.

Let and .

The implicit schemes are unconditionally stable and converge in mean-square sense ( sense) under a constraint on the correlation [25], as the following theorems describe for (2.6), and an analogous result holds for (2.5).

Theorem 2.1 (Theorem 2.1 in [25])

The implicit Milstein scheme (2.6) is unconditionally stable in the mean-square sense, provided .

Theorem 2.2 (Theorem 2.2 in [25])

Proposition 2.1

Proof See Appendix A.

Remark 2.1

If for some , and a constant independent of and ,

| (2.8) |

or equivalently,

| (2.9) |

then the implicit Milstein scheme (2.5) has the error expansion

Remark 2.2

We consider a specific linear functional of for fixed , the random variable

| (2.10) |

as discussed in the introduction, where is the solution to (2.1) and (2.2).

By introducing integer multi-indices as the index of space and time separately, we denote as the discrete approximations to , with mesh size , and timestep ,

| (2.11) |

where the integral is approximated by the trapezoidal rule and is determined by (2.5).

Proposition 2.2

Let be the random variable given by (2.10). Let be the approximation to given by (2.11). Assume . Then there exists a real number , such that for any , any , and any such that

where , , are the same constants as in Remark 2.1, the following holds:

For any , ,

where .

Proof Denote the trapezoidal approximation of with mesh size by

where . Since both and use the theoretical, smooth , we have

Therefore

From the proof of Theorem 2.2 in [25], there exist random variables , and a constant , all of which are independent of , such that

where

Combining above equations, we have

Therefore, by choosing , we have for all , ,

3 Multi-index Monte Carlo discretisation on a space-time mesh

Following the idea in [14], we introduce , the first order difference operator along directions , defined as

| (3.1) |

with being the canonical vectors in , i.e., . Then define the first order mixed difference operator . Hence, for , we have

| (3.2) | ||||

A telescoping sum then gives, for any ,

By setting and , with satisfy the condition (2.8). Then the weak error between can be formed as

| (3.3) |

However, this is not necessarily the most efficient way of approximating , since the approximations with close to are highly accurate but also costly to compute. Instead, we only compute the levels in a minimal index set (adapted to the convergence in and ) which satisfies

| (3.4) |

for a given error . Then it can be easily proved that

| (3.5) |

The MIMC estimator is now defined by (see [14])

| (3.6) |

where is an index set, and is the number of samples for each . The key point in the algorithm is that the quantity comes from four discrete approximations using the same Brownian path, therefore the variance of is small, in a sense made precise in Theorem 4.1. Thus the moments of are small not only if both and are small, but it suffices that either or is small. This allows the omission of computationally costly indices. The MIMC algorithm is based on a good choice of and, for given , to balance bias and variance for a given accuracy target.

Denote , , and the average work required for a realization of for a single path. Then the total work corresponding to the estimator is

| (3.7) |

As the paths are chosen independently for different , the variance of the estimator is

| (3.8) |

The mean square error can be expressed as the sum of two contributions, bias and variance,

| (3.9) |

To achieve a root mean square error of , we split the accuracy as follows,

where . By optimising the total work with respect to given the variance constraint (3.8) and a fixed , we can derive (see also [14]) the optimal number of samples for each level to be

| (3.10) |

In the numerical implementation, we take the integer ceiling of in (3.10), as a result we assume the bound

Therefore the total work is bounded by

| (3.11) |

where the second term is usually negligible.

In [14], Theorem 2.2 shows the total computational cost using an optimal index set with the MIMC method given bounds on and . Based on these ideas, we first consider the Fourier analysis of each level , then find an index set to achieve the optimal order of the total work. Though the complexity is the same for both schemes (2.5) and (2.6) when using the multilevel method, we will see that it is different using the multi-index method.

4 Fourier analysis of MIMC estimators

In this section, we show that the MIMC increments (3.2) for scheme (2.5) satisfy the moment conditions required for the analysis of [14]. We then derive the optimal index set and the resulting complexity of the MIMC estimator in Section 5. In what follows, we will use to stand for generic positive real constants dependent only on model parameters, and their values may change between occurrences.

4.1 Main results

The following theorem is concerned with the first and second moments of with schemes (2.5) and (2.11).

Theorem 4.1

Consider from (2.11) with the implicit Milstein scheme (2.5). Assume . Then there exists a real number , such that for any , any , and any such that

where , , are the same constants as in Remark 2.1, the following holds:

For any , , the first and second moments of satisfy

| (4.1) |

where , .

Proof See Section 4.3.

Remark 4.1

Remark 4.2

It follows from Theorem 4.1 that the MIMC increments (3.2) (for scheme (2.5) and approximation (2.11) of ) satisfy

| (4.2) | |||

| (4.3) | |||

| (4.4) |

where are positive constants, and the constants will be used in the numerical implementation.

These are the Assumptions 1, 2, 3 in [14]. We will follow their approach in Section 5 to construct the index set , choose the number of samples and derive the complexity.

Similar to the proof of Theorem 4.1, we have the following.

Remark 4.3

Assume . Then there exists a real number , such that for any , any , and any such that

where , , are the same constants as in Remark 2.1, the following holds:

4.2 Fourier transform of the solution

Define the Fourier transform pair

The Fourier transform of (2.1) yields

| (4.5) |

subject to the initial data from (2.2). We assume that in the following for simplicity, since the results will not change when a drift term appears. (See Remark 2.3 in [25].)

For the discretised equation, we can use a discrete-continuous Fourier decomposition

for defined above (2.4), where

Since we approximate the Dirac initial data by (2.4), it follows that Then by linearity of the equation, we have

| (4.7) |

where we make the ansatz

| (4.8) |

Following [15, 25], we say that the implicit Milstein scheme is mean-square stable, provided

Therefore, by stationarity we need

i.e.,

This gives a condition on the correlation for mean-square stability (see [25]), stated previously as Theorem 2.1.

Now that the stability is ensured, we can approximate the functional of the solutions.

4.3 Fourier analysis of MIMC estimators (proof of Theorem 4.1)

To simplify the notation, we define

| (4.12) |

where as before. Note that is defined in a distributional sense, and it only appears multiplied by the smooth, fast decaying function and in integral form, hence this is well-defined. Then has the form

| (4.13) |

Now we derive the leading order term of , assuming that holds.

Let be the final timestep for level . We write as , and from (4.13) we have

| (4.14) | ||||

We introduce as the integrand in (4.14),

| (4.15) |

Hence we can express as

| (4.16) |

Moreover, after some computation we have for ,

| (4.17) | ||||

Following the analysis in [4], we compare the numerical solution to the analytical solution by splitting the domain into two wave number regions. Assume is a constant satisfying . Then we define the low wave number region by

| (4.18) |

and the high wave number region by

| (4.19) |

Then we have the following lemmas.

Lemma 4.1 (Low wave region)

For introduced in (4.15), there exists a constant , such that for any ,

where is a random variable with bounded first and second moments satisfying

Proof See Section 4.4.

Lemma 4.2 (High wave region)

There exists a real number , such that for any , any , and any such that

where , , are the same constants as in Remark 2.1, the following holds for :

where is a random variable with bounded first and second moments satisfying

Proof See Section 4.5.

Hence there exists a constant independent of , such that the first and second moments of satisfy

4.4 Low wave number region (proof of Lemma 4.1)

First consider the case where is small, such that . To analyse the mean and the variance of in (4.17), it suffices to analyse the mean and the variance of

Now we consider the numerical approximation of (4.20), written as

where

| (4.21) |

and is the logarithmic error between the numerical solution and the exact solution introduced during . Aggregating over timesteps, at ,

where is the exact solution at time . Therefore

| (4.22) | ||||

In the following, for a small parameter , , , , denote, respectively,

Then one can derive from Taylor expansion of ,

where we have

Moreover, this discretisation scheme satisfies

This is important since the term vanishes in this case, and it follows that

where is an odd degree polynomial function, is an even degree polynomial function, and is a random variable with bounded second moments such that

Note that the level has mesh size and timestep , such that it has time steps. To reduce the variance, we use the same Wiener process in these two levels, hence the Brownian increment on level satisfies

As a result, we have

| (4.24) | ||||

where

Since

it follows that

Therefore we derive

| (4.25) | ||||

where

So we have

Here, for ,

is the numerical approximation to

Because of the exponential decay of in , there exists independent of , such that

Then there exists a constant independent of and , such that

where are random variables with bounded moments satisfying

Then Lemma 4.1 follows by letting

4.5 High wave number region (proof of Lemma 4.2)

Now we consider the case where is large, such that . By (4.10), we have

denoting

Note that when . We have

| (4.26) |

and

Since we have assumed that , the numerator is positive.

When , the high wave region is

In this case,

When , following the proof of Proposition 2.1 in Appendix A, we have

| (4.27) |

where are constants independent of and . As satisfies the condition

or, equivalently,

by using (4.17) and a similar argument as in Appendix A, it follows that there exists independent of and , such that for all ,

since in (4.27),

This concludes the proof of Lemma 4.2.

5 Optimal index set and complexity

So far, we have derived the first and second moments of . Based on these, we now need to find an appropriate index set for the MIMC estimator (3.6). We first do this for scheme (2.5) and approximation (2.11).

Finding the optimal (with respect to the computational cost required for a given prescribed accuracy ) index set is equivalent to solving the optimisation problem

| (5.1) |

where is the total work as in (3.7) and the MIMC estimator for as in (3.6), . From (3.5), we have

where defined in (3.3) is the error between and , and defined in (3.4) is the error between two index sets. We let with , , and . Then the weak error between and has a higher order, and the dominant weak error of the MIMC estimator would be .

Firstly we find the and . From Proposition 2.2, we have

For

it is sufficient to have

| (5.2) | ||||

Hence we have

| (5.3) | ||||

We follow the idea in [14], and introduce the term “profit” as

| (5.4) |

Here , defined as the expectation of as before, can be regarded as the contribution to the solution (if included) or error (if not included) originating from level . The denominator is proportional to the total work on level , which is given by

from (3.10). This can be regarded as a knapsack problem, where we try to include those levels with small work and large bias. This gives rise to the following heuristic optimisation.

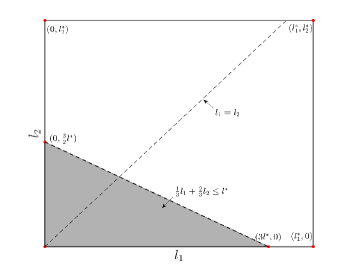

Following Lemma 2.1 in [14], we define a candidate index set as

Note that this class may not contain the optimal index set, but we will see that it is sufficiently rich to obtain optimal complexity order. From (4.2) to (4.4), we deduce

| (5.5) |

for some constant , where

We introduce strictly positive normalized weights as

Then .

Now the index set is denoted as

| (5.6) |

where can be derived from the bias constraint

| (5.7) |

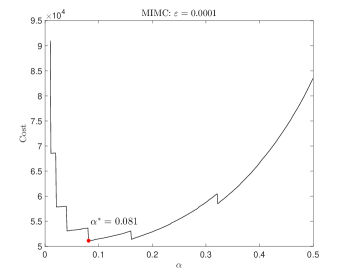

We try to find the minimal such that this bias constraint holds. See Figure 1.

Now we compute the computational cost under this index set. Recall from (3.11) that

Since the first term dominates the second one, we only need to compute

where is a positive constant. Therefore, using discretisation (2.5) and (2.11), the order of the total computational cost is

| (5.9) |

Although theoretically there is a log term in the complexity, it usually does not affect the numerical tests, as is small, and dominates .

6 Some sub-optimal approximations

6.1 The alternative discretisation (2.6)

Recall the alternative discretisation scheme given in (2.6), in which we apply the Milstein scheme first, then apply a second finite difference with step size . This makes no difference in the convergence order of the multilevel scheme, of which the second moment of satisfies

| (6.1) |

where , As in order to balance the bias, is a higher order term in (6.1). However, in the multi-index scheme, is no longer a higher order term due to the independence of and . This leads to the difference in complexity between the MLMC and MIMC methods.

Proposition 6.1

Consider the approximation (2.6) and (2.11). Assume . Then there exists a real number , such that for any , any , and any such that

where , , are the same constants as in Remark 2.1, the following holds:

For any , with , , the first and second moments of satisfy

| (6.2) |

Proof In this discretisation scheme,

Hence we have

| (6.3) |

where

Following the previous analysis, in the low wave region (see Section 4.4) we can derive that

In this case, is no longer zero, so that

where satisfies

Now we have

However,

for some constant . Hence similar to the proof of Theorem 4.1, there exists a constant , such that

For in the high wave region, the proof is the same as in Theorem 4.1.

By a similar computation to Section 5, the index set is now

and the total computational cost satisfies

The corresponding numerical results are demonstrated at the end of Section 7.1.

6.2 An alternative functional approximation

Instead of approximating the loss by (2.11), consider a simpler approximation,

| (6.4) |

where . Using the discretisation from the previous subsection, we have the following results.

Proposition 6.2

Consider the approximation (2.6) and (6.4). Assume . Then there exists a real number , such that for any , any , and any such that

where , , are the same constants as in Remark 2.1, the following holds:

For any , with , , the first and second moments of satisfy

| (6.5) |

Proof Similar to the proof of Theorem 4.1.

By the choice of and above, we get

which gives

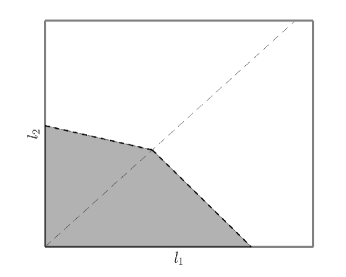

As a consequence, the convergence rate varies between and , depending on which refinement path is chosen.

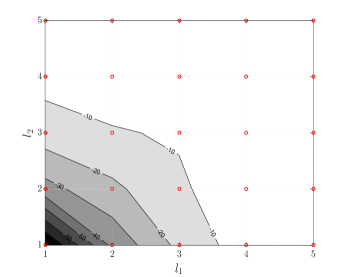

The peculiarity of this scheme is that it has two leading terms of different orders in the variance, such that the assumptions of the framework in [14] (in this case, Assumption 2) are not satisfied. However, the fundamental principles of the MIMC concept still apply and we can split the domain into two parts: and , and the optimal index set is as shown in Figure 2, where the analysis from Section 5 can be applied separately in the two parts. The total computational cost satisfies

7 Numerical implementation

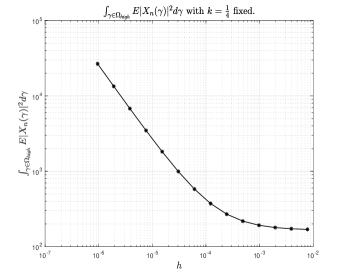

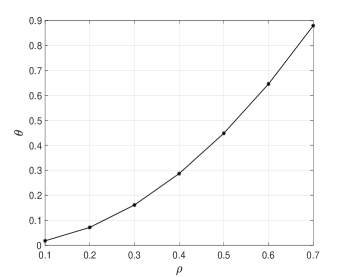

Here, we present numerical tests for the schemes above to illustrate the theoretical convergence results and compare the complexity among MLMC and two MIMC schemes. Moreover we solve the SPDE on an interval with zero boundary conditions. We choose the parameters , , and the initial density is .

Figure 3 shows the values of from (2.7) corresponding to different correlation , where is derived from the following equation

| (7.1) |

For and , . So if , we can choose for , and for , as then , where and . Therefore does not matter much in this problem.

7.1 Mean and variance of

In this section, we conduct numerical tests for and . The analysis shows that for (2.5) and (2.11),

where

such that

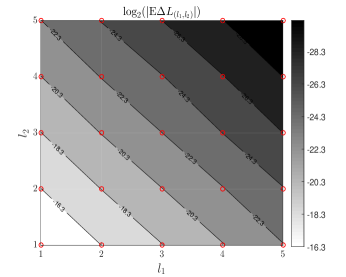

Table 1 shows with different levels of timestep and mesh size, using Monte Carlo samples.

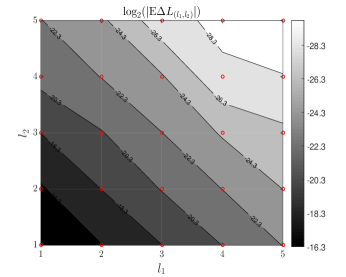

The data in Table 1 suggest that for , from given to (i.e., from one diagonal to the next), the values decrease by around 2, in line with (4.2). Figure 4(a) is the contour plot of the values of .

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| -14.3384 | -16.2991 | -18.2382 | -20.1987 | -22.2193 | |

| -16.2725 | -18.3163 | -20.2538 | -22.1928 | -24.2061 | |

| -18.2749 | -20.3508 | -22.2862 | -24.2709 | -26.2991 | |

| -20.2770 | -22.3616 | -24.2059 | -26.2203 | -28.3113 | |

| -22.2776 | -24.3644 | -26.2984 | -28.2543 | -30.2064 |

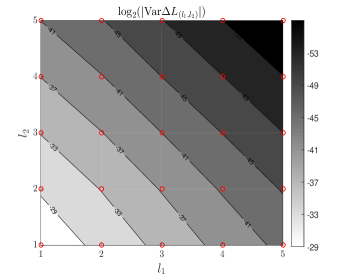

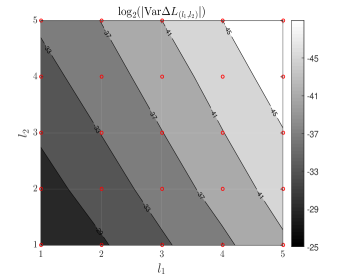

Table 2 shows the corresponding . We can see from the table that from given to , the values decrease by approximately 4, in line with (4.3). Figure 4(b) is the contour plot of the values of .

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| -26.2614 | -30.0205 | -34.0963 | -38.1821 | -42.0136 | |

| -29.3889 | -33.1355 | -37.2427 | -41.3587 | -45.2778 | |

| -33.1243 | -36.8837 | -41.0030 | -44.9869 | -48.9696 | |

| -37.0547 | -40.8191 | -44.9404 | -48.9230 | -52.9080 | |

| -41.0371 | -44.8028 | -48.8718 | -52.9715 | -56.9993 |

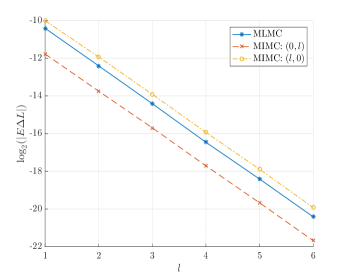

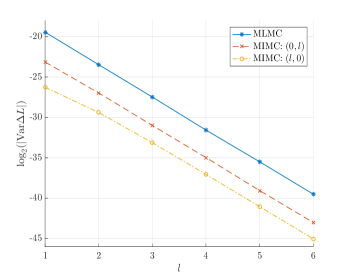

Figure 5 compares MLMC and MIMC at boundary levels, i.e., or . We can see from the plots that they have the same rate of convergence, which is consistent with Remark 4.3.

Now we compare the results with the alternative discretisation scheme (2.6) but the same from (2.11). The analysis in Section 6.1 shows that under that scheme,

Figure 6 shows the contour plots of and using the alternative discretisation scheme (2.6) and (2.11), with and .

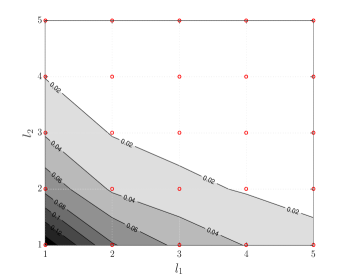

We compute the optimal index set based on the profit (5.4). Figure 7(a) shows the profit using scheme (2.5) and (2.11). This provides the basis for the optimal index set (5.6). For scheme (2.6) and (6.4), there are two leading orders of variance, hence the index set is not triangular, as one can deduce from Figure 7(b).

7.2 Complexity

The analysis shows that the total computational cost of the scheme (2.5) and (2.11) for a RMSE is . As does not matter much in this problem, we can choose fixed for , and the computational cost is expected to have the order . We test the total cost given different accuracy , and compare the results with the multilevel algorithm. The mean square error for the estimator can be expressed as the sum of the variance of the estimator and the square of the weak error, as in (3.9),

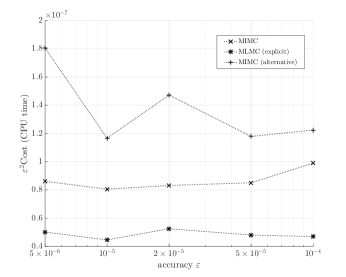

Since , the variance decays more rapidly with the level than the cost increases, so that the dominant cost is on level . For each fixed accuracy, we find the global minimum of the total cost with respect to and choose that optimal , thus reducing the total cost. Figure 8(a) shows how the total cost varies with when . Figure 8(b) plots the CPU time of of two multi-index and the multilevel algorithms. As does not affect much in this problem, the total computational costs of the MLMC algorithm and MIMC with schemes (2.5) and (2.11) are approximately proportional to , hence should not vary much with different accuracy . However, the cost of the alternative discretisation scheme (2.6) with MIMC has the order . We can see from the figure that is no longer a constant but is slightly increasing as .

The costs of the MLMC and MIMC schemes are very similar across a wide range of parameters (not reported here), which is to be expected as the dominant cost comes from the coarsest level. The MLMC scheme is slightly more efficient here, because it allows explicit time-stepping with a slightly lower computational cost. When an implicit scheme (2.5) is used for MLMC as well, giving better stability properties, the MIMC scheme outperforms. This is useful for locally refined meshes.

8 Conclusions and further work

We have analysed the accuracy and complexity of a MIMC estimator for a one-dimensional parabolic SPDE using Fourier analysis. Specifically, we analysed a functional of the solution. We showed that, by using the implicit Milstein finite difference discretisation (2.5), the order of the first and second moments of are and , with . For a fixed RMSE , the theoretical complexity is . However, practically the order of complexity is still . Moreover, under a different discretisation (2.6), the first and second moments of are and , and practically the total complexity of this scheme is . We further used a simpler approximation of as (6.4) with discretisation (2.6). This gave two leading terms of different orders in the variance, which violated the simplest form of assumptions of the framework in [14]. After some adaptation, theoretically we achieved a complexity of .

Although MLMC has already achieved optimal complexity in this case, one shortcoming of MLMC is that the efficiency still depends on the dimensionality. For high-dimensional problems, when the level increases, the decay of the variance will be slower than the increase of the cost. In that case, the total computational cost is no longer . For example, consider a two-dimensional version of the SPDE,

with , , real parameters. Assuming second order convergence in both spatial directions and first order in time, the total MLMC cost given a fixed accuracy is expected to be . Although this is much lower than the expected for the standard Monte Carlo method, the order is not optimal as in the one-dimensional case. Further work will include analysing high-dimensional SPDEs using the MIMC method. Preliminary results suggest that MIMC achieves a better complexity than the multilevel method.

Another further research is to apply an absorbing boundary condition to this Zakai type SPDE [3]. Now the particle system involves a barrier such that once the particle touches the barrier, the value would be zero afterwards. Then the density process of the system satisfies a SPDE with a zero boundary condition. Specifically, for the one-dimensional SPDE (2.1), it becomes

| (8.1) | ||||

The solution has a smooth density process and shows degeneracy near the absorbing boundary [22]. In this case, the convergence order of the finite difference scheme does not follow from the Fourier analysis of the unbounded case. The analysis of this type of SPDE with boundary conditions is still an open area for research, especially for higher dimensions. One possible way is to use combination technique which combines the Galerkin solutions on certain full tensor product spaces [10].

Acknowledgements

The authors would like to thank Raul Tempone, Abdul-Lateef Haji-Ali, and Mike Giles for helpful discussions on Multi-index Monte Carlo methods in this context.

References

- [1] E. Buckwar and T. Sickenberger. A comparative linear mean-square stability analysis of Maruyama-and Milstein-type methods. Mathematics and Computers in Simulation, 81(6):1110–1127, 2011.

- [2] K. Bujok and C. Reisinger. Numerical valuation of basket credit derivatives in structural jump-diffusion models. Journal of Computational Finance 15(4):115–158, 2012.

- [3] N. Bush, B. M. Hambly, H. Haworth, L. Jin, and C. Reisinger. Stochastic evolution equations in portfolio credit modelling. SIAM Journal on Financial Mathematics, 2(1):627–664, 2011.

- [4] R. Carter, and M. B. Giles. Sharp error estimates for discretizations of the 1D convection–diffusion equation with Dirac initial data. IMA Journal of Numerical Analysis 27(2):406–425, 2007.

- [5] A. M. Davie and J. Gaines. Convergence of numerical schemes for the solution of parabolic stochastic partial differential equations. Mathematics of Computation, 70(233):121–134, 2001.

- [6] M. B. Giles. Multilevel Monte Carlo path simulation. Operations Research, 56(3):607–617, 2008.

- [7] M. B. Giles. Multilevel Monte Carlo methods. Acta Numerica, 24:259–328, 2015.

- [8] M. B. Giles and C. Reisinger. Stochastic finite differences and multilevel Monte Carlo for a class of SPDEs in finance. SIAM Journal on Financial Mathematics, 3(1):572–592, 2012.

- [9] E. Gobet, G. Pages, H. Pham, and J. Printems. Discretization and simulation of the Zakai equation. SIAM Journal on Numerical Analysis, 44(6):2505–2538, 2006.

- [10] M. Griebel and H. Harbrecht. On the convergence of the combination technique. Sparse Grids and Applications, volume 97 of Lecture Notes in Computational Science and Engineering, Springer, 55–74, 2014.

- [11] I. Gyöngy. Lattice approximations for stochastic quasi-linear parabolic partial differential equations driven by space-time white noise I. Potential Analysis, 1(9):1–25, 1998.

- [12] I. Gyöngy. Lattice approximations for stochastic quasi-linear parabolic partial differential equations driven by space-time white noise II. Potential Analysis, 11(1):1–37, 1999.

- [13] I. Gyöngy and D. Nualart. Implicit scheme for stochastic parabolic partial differential equations driven by space-time white noise. Potential Analysis, 7(4):725–757, 1997.

- [14] A. L. Haji-Ali, F. Nobile, and R. Tempone. Multi-index Monte Carlo: when sparsity meets sampling. Numerische Mathematik, 132(4):767–806, 2015.

- [15] D. J. Higham. Mean-square and asymptotic stability of the stochastic theta method. SIAM Journal on Numerical Analysis, 38(3):753–769, 2000.

- [16] A. Jentzen and P. Kloeden. The numerical approximation of stochastic partial differential equations. Milan Journal of Mathematics, 77(1):205–244, 2009.

- [17] A. Jentzen and P. Kloeden. Taylor expansions of solutions of stochastic partial differential equations with additive noise. The Annals of Probability, 38(2):532–569, 2010.

- [18] A. Kebaier. Statistical Romberg extrapolation: a new variance reduction method and applications to option pricing. The Annals of Applied Probability, 15(4):2681–2705, 2005.

- [19] R. Kruse. Optimal error estimates of Galerkin finite element methods for stochastic partial differential equations with multiplicative noise. IMA Journal of Numerical Analysis, 34(1):217–251, 2014.

- [20] N. V. Krylov and B. L. Rozovskii. Stochastic evolution equations. Journal of Soviet Mathematics, 16(4):1233–1277, 1981.

- [21] T. G. Kurtz and J. Xiong. Particle representations for a class of nonlinear SPDEs. Stochastic Processes and their Applications, 83(1):103–126, 1999.

- [22] S. Ledger. Sharp regularity near an absorbing boundary for solutions to second order SPDEs in a half-line with constant coefficients. Stochastic Partial Differential Equations: Analysis and Computations 2(1):1–26, 2014.

- [23] C. Pflaum and A. Zhou. Error analysis of the combination technique. Numerische Mathematik, 84(2):327–350, 1999.

- [24] C. Reisinger. Analysis of linear difference schemes in the sparse grid combination technique. IMA Journal of Numerical Analysis, 33(2):544-581, 2013.

- [25] C. Reisinger. Mean-square stability and error analysis of implicit time-stepping schemes for linear parabolic SPDEs with multiplicative Wiener noise in the first derivative. International Journal of Computer Mathematics, 89(18):2562–2575, 2012.

- [26] G. Strang and K. Aarikka. Introduction to Applied Mathematics, volume 16. Wellesley-Cambridge Press Wellesley, MA, 1986.

- [27] L. Szpruch. Numerical approximations of nonlinear stochastic systems. PhD thesis, University of Strathclyde, 2010.

- [28] J. B. Walsh. Finite element methods for parabolic stochastic PDE’s. Potential Analysis, 23(1):1–43, 2005.

- [29] C. Zenger. Sparse grids. Parallel Algorithms for Partial Differential Equations (W. Hackbusch, ed.), Vol. 31 of Notes on Numerical Fluid Mechanics, Vieweg, Braunschweig/Wiesbaden, 1991.

Appendix A Proof of Proposition 2.1

As for the mean-square convergence, Proposition 2.1, we compare the numerical solution to the analytical solution by splitting the domain into two wave number regions. Assume is a constant satisfying . Then, we define the low wave number region as in (4.18),

and the high wave number region as in (4.19),

For in the low wave region, the analysis is the same as [25], Theorem 2.1, that the Fourier transform of the numerical solution is very close to the theoretical solution, with error . However, when , there is an extra term in the high wave region. So here we only analyse the contribution from the high wave region.

Proof [Proposition 2.1] For the case , we divide the high wave region into two parts, and , and we integrate separately. Note that .

where , and

| (A.1) | ||||

Denote , and

we have

So

where . Therefore we have

The equation has solutions as follows:

| (A.2) | ||||

| (A.3) | ||||

| (A.4) |

So for and , decreases over the high wave region:

-

1.

For ,

Therefore,

This is for any as , i.e.,

-

2.

For ,

The function is strictly decreasing in and increasing in for . So we have,

Therefore,

Consequently, for ,

where and are constants independent of and .

For and , is decreasing before , and increasing afterwards, where solves the equation (A.3) such that

So

We analyse separately the two parts, and .

-

1.

When , is strictly decreasing. Similar to the previous analysis, we have

This is for any as .

-

2.

For , decreases first, then increases if . Therefore,

We will show both terms are strictly less than 1.

Similar to the previous analysis,

On the other hand,

and this is strictly decreasing in and increasing in , so

Therefore, if we let , we have

Consequently, for ,

where and are constants independent of and .

Numerical results confirm this as well. Figure 9 shows the integral over the high wave region with , fixed, and , .