Hybrid continuous and periodic barrier strategies in the dual model: optimality and fluctuation identities

Abstract.

Avanzi et al. [3] recently studied an optimal dividend problem where dividends are paid

both periodically and continuously with different transaction costs.

In the Brownian model with Poissonian periodic dividend payment opportunities, they showed that the optimal strategy is either of the pure-continuous, pure-periodic, or hybrid-barrier type. In this paper, we generalize the results of their previous study to the dual (spectrally positive Lévy) model. The optimal strategy is again of the hybrid-barrier type and can be concisely expressed using the scale function. These results are confirmed through a sequence of numerical experiments.

AMS 2010 Subject Classifications: 60G51, 93E20, 91B30

Keywords: dividends; Lévy processes; periodic strategies; scale functions; dual

model.

1. Introduction

In de Finetti’s optimal dividend problems, the aim is to maximize the expected net present value (NPV) of the dividends accumulated until ruin. In other words, the objective is to find the optimal dividend strategy, namely the one that always strikes a balance between maximizing dividends and minimizing the risk of ruin. Because the surplus process is typically assumed to be a time-homogeneous Markov process, the optimal strategy can reasonably be assumed to be of barrier type: dividends are paid such that the surplus does not exceed a certain level. Given this conjecture, one can follow the classical “guess and verify” procedure: the candidate barrier (or free boundary) is chosen by the continuous/smooth fit principle, and the optimality is shown via verification arguments. While the optimality of a barrier strategy can fail in some cases (see [15]), all existing explicit solutions are, to the best of our knowledge, barrier strategies or variations thereof.

In this paper, we consider the version of the optimal dividend problem considered in [3], where dividends are paid both periodically and continuously. The periodic dividend decision times arrive at the jump times of an independent Poisson process, as described in [2] and [19], and, in addition, one has the option to pay dividends at any time but at a different (proportional) transaction cost. Avanzi et al. [3] studied the case wherein the surplus is driven by a (drifted) Brownian motion. In this paper, we show that analogous results can be attained when the surplus process is generalized to be a spectrally positive Lévy process.

The objective is to show the optimality of the hybrid (continuous and periodic) barrier strategy. Namely, for some periodic barrier and continuous barrier such that , the surplus process is pushed down to whenever it is above at the periodic dividend decision times, while it is also pushed down continuously so that it does not go above uniformly in time. In particular, this strategy reduces to the pure continuous barrier strategy when , and to the pure periodic barrier strategy when . For a more detailed discussion of this strategy, see [3].

To solve this problem, we take the following steps:

-

(1)

First, the expected NPVs of the (both periodically and continuously collected) dividends under the hybrid barrier strategy for any choice of and are computed. The controlled surplus process under the hybrid barrier strategy is the dual of the Parisian reflected process studied in Avram et al. [5] with additional classical reflection caused by the continuous barrier strategy. We shall extend these results to obtain semi-analytical expressions for the expected NPV of the dividends via the scale function.

-

(2)

Second, the values for the periodic and continuous barriers, defined as and , respectively, are selected. As this combines the classical singular control case [6] and the periodic case [19], the value function is clearly expected to satisfy analogous smoothness conditions at these two barriers.

More precisely, at the level where the process is reflected in the classical sense [6], the value function is continuously differentiable (resp. twice continuously differentiable) when the driving Lévy process is of bounded (resp. unbounded) variation. In contrast, at the level where the process is reflected in the Parisian sense, as in [19], it is twice continuously differentiable (resp. thrice continuously differentiable) if it is of bounded (resp. unbounded) variation. See [9] and [23] for similar conditions in the optimal stopping case.

These conditions at and provide us with two equations, defined as and , respectively. Under the assumption that the driving process drifts to infinity, we shall show that either there exists a pair or corresponding to the case of a hybrid barrier strategy, or that we should choose a pure continuous strategy (i.e., ) or a pure periodic barrier strategy (i.e., ). When , and are simultaneously satisfied, whereas if , and a weaker version of (with the equality replaced by an inequality) are satisfied. The cases and are treated separately.

-

(3)

Finally, optimality is verified. Again, because the problem is the combination of the classical singular and periodic cases, the candidate value function is expected to simultaneously satisfy the sufficient conditions given in [6] and [19]. We show that these conditions are indeed sufficient, and that the candidate value function, with the barriers selected in the previous steps, satisfies these conditions.

To confirm the analytical results obtained, we also conduct numerical experiments for the case driven by the phase-type Lévy process as described in [1]. In this case, the scale function can be represented as a linear combination of (complex) exponentials (see [10]), and hence the optimal barriers and as well as the value function can be computed instantaneously. We illustrate this computation process, and confirm both optimality and the convergence to the cases wherein pure continuous/periodic barrier strategies are optimal.

To the best of our knowledge, this is the first paper on the joint optimization of periodic and continuous strategies for Lévy processes. When there are jumps in the underlying process, the solution methods used in [3] for the Brownian motion model can no longer be applied. However, by expressing the expected NPVs via the scale function, a direct approach is possible without restricting the underlying Lévy measure. The same techniques are expected to be applied to other stochastic control problems, such as inventory control [22] and dividend problems with capital injections [4, 6], when considering their extensions with periodic and continuous strategies.

In most optimal dividend problems, a single barrier separates the waiting region from the controlling region. However, in this problem, three regions are separated by two barriers that are identified by the smooth fit conditions. For this reason, the biggest challenges are to show the existence of a pair of barriers satisfying these conditions and to conduct the analysis on each of these three regions that are required for verification. The former can be handled by observing that the desired barriers are such that a function of two variables and its partial derivative vanish simultaneously. For the latter, although the shape of the value function differs in these three regions, finding a unifying expression is possible using the scale function. Moreover, the variational inequalities can be efficiently proven using this unifying expression.

The rest of this paper is organized as follows. Section 2 reviews the spectrally positive Lévy process and formulates the problem considered in this paper. Section 3 then defines the hybrid barrier strategy and constructs the corresponding controlled surplus process. Section 4 obtains the verification lemma (sufficient conditions for optimality). In Section 5, we review scale functions and compute the expected NPV of the dividends under the hybrid barrier strategy. Sections 6 and 7 provide solutions for the case wherein the hybrid barrier strategy is optimal: we select the candidate optimal barriers in Section 6 and show that the corresponding candidate value function solves the required variational inequalities in Section 7. Section 8 considers the case where pure continuous/periodic barrier strategies are optimal. Finally, we conclude the paper by presenting some numerical results in Section 9. Some proofs are deferred to the appendix.

Throughout the paper, and are used to indicate the right- and left-hand limits, respectively, for any function whenever they exist. We also let and for any process with left-hand limits.

2. Problem formulation

2.1. Spectrally positive Lévy processes

Let be a Lévy process defined on a probability space . For , we denote by the law of when it starts at , and, for convenience, we write in place of . Accordingly, we write the associated expectation operators as and . In this paper, we assume that is spectrally positive, which means that it has no negative jumps and is not a subordinator. We also assume throughout this work that its Laplace exponent , i.e.,

is given by the Lévy-Khintchine formula

| (2.1) |

where , , and is a measure on , known as the Lévy measure of , which satisfies .

It is well known that has paths of bounded variation if and only if and ; in this case, can be written as

where

| (2.2) |

and is a driftless subordinator. Note that , since we have ruled out the case where has monotone paths. In this case, its Laplace exponent is given by

As is commonly assumed in the literature, we assume that drifts to infinity, i.e.,

| (2.3) |

2.2. Problem

We assume that dividend payments are made both periodically and continuously.

The set of periodic dividend decision times is denoted as , where , for each , represents the arrival time of the Poisson process with intensity , which is independent of the Lévy process . Let be the filtration generated by the process .

A strategy is a nondecreasing, right-continuous, and -adapted process, where the cumulative dividend amount has the following decomposition:

Here, is a non-decreasing, right-continuous, and -adapted process with that models the aggregate dividend until for the continuous strategy. In contrast, is a non-decreasing and -adapted process of the form

| (2.4) |

for some -adapted càglàd process . We note from (2.4) that the periodic dividend payment at time is given by for all .

The surplus process obtained after dividends are deducted is such that

where is the corresponding ruin time. We let at this instance and other instances throughout the paper. While the payment of dividends can cause immediate ruin by setting , it cannot exceed the surplus amount that is currently available. In other words, we assume that

| (2.5) |

We let be the set of all admissible strategies that satisfy all the constraints described above.

The problem is to maximize, for , the expected NPV of the dividends associated with the strategy , defined as, for ,

| (2.6) | ||||

where is the ratio between the net proportion of continuous and periodic dividends received per dollar (see Remark 2.1). Hence the problem is to compute the value function

and to obtain the optimal strategy that achieves it, if such a strategy exists.

3. Hybrid barrier strategies

In this section, we define the hybrid barrier strategy for . At each of the periodic dividend decision times where the surplus is above , the excess is paid (Parisian reflection). In contrast, as with the classical barrier strategy, dividends are also paid such that the surplus never exceeds (classical reflection). The resulting controlled surplus process then becomes the following Lévy process with Parisian and classical reflection above:

| (3.1) |

where and are the respective amounts of Parisian and classical reflection (dividends under the periodic and continuous barrier strategies) accumulated up to time . The formal construction of is given in Section 3.2.

3.1. Lévy processes with Parisian reflection above

Before constructing the process given in (3.1), we first review the spectrally positive Lévy process with Parisian reflection above (and without classical reflection above), which is denoted by for a fixed (Parisian) barrier . The dual of this process is exactly the one studied in [5].

This process is only observed at times and is pushed down to if and only if it is above . More specifically, we have

| (3.2) |

where

| (3.3) |

The process then jumps down by so that . For , we have . The process can be constructed by repeating this procedure.

Suppose is the cumulative amount of (Parisian) reflection up to time . We then have

with

| (3.4) |

where can be constructed inductively using (3.3) and

3.2. Lévy processes with Parisian and classical reflection above

We now construct the process by adding classical reflection in . For , let

| (3.5) |

be the process classically reflected from above at (see Bayraktar et al. [6]).

We have

| (3.6) |

where . The process then jumps down by so that . For , the process is the classical reflected process (in the form (3.5)) of the shifted process . The process can be constructed by repeating this procedure. This process admits the decomposition (3.1) because the cumulative periodic dividend process becomes (3.4) when is replaced with , whereas, between periodic payments, the process behaves like the classical reflected process (3.5) with different starting points.

3.3. Hybrid barrier strategies and their special cases

For , the hybrid barrier strategy is an admissible strategy, with taking the form (2.4).

The pure periodic barrier strategy corresponds to the case . This strategy is clearly admissible and the resulting aggregate periodic dividend and controlled surplus processes become and , respectively, as described in Section 3.1. The aggregate continuous dividend process is uniformly zero.

The pure continuous barrier strategy corresponds to the case . It is an admissible strategy, and the resulting aggregate continuous dividend and controlled surplus processes are and , respectively, as in (3.5). The aggregate periodic dividend process is uniformly zero.

Finally, if , liquidation occurs at the first periodic dividend payment opportunity.

4. Sufficient conditions for optimality

The aim of this paper is to to show the optimality of a hybrid barrier strategy as defined in Section 3. Toward this end, we first derive the verification lemma and obtain sufficient conditions for optimality. This is a generalization of Lemma 4.1 of [3]. For verification of related stochastic control problems driven by spectrally one-sided Lévy processes, see Section 5.4 of [4], Lemma 4.1 of [11], and the proof of Lemma 6.1 in [22].

We call a measurable function sufficiently smooth if is (resp. ) when has paths of bounded (resp. unbounded) variation. We let be the operator for acting on a sufficiently smooth function , defined by

| (4.1) |

Lemma 4.1 (Verification lemma).

Suppose is such that is sufficiently smooth on , and satisfies

| (4.2) | ||||

| (4.3) |

Then for all and hence is an optimal strategy.

Proof.

By the definition of as a supremum, it follows that for all . We write and show that for all and .

Fix , , and the corresponding surplus process . Let be the sequence of stopping times defined by . Since is a semi-martingale and is sufficiently smooth on by assumption, we can use the change of variables for the bounded variation case (Theorem II.31 of [21]) and Itô’s formula (Theorem II.32 of [21]) for the unbounded variation case to the stopped process . Because and do not jump simultaneously, we can write under that

where is the continuous part of and is a local zero-mean martingale as in (A.1) of [19].

On the other hand, using (4.3), we obtain that

Now taking expectations in (4.4) and letting and go to infinity ( -a.s.), the monotone convergence theorem gives . This completes the proof. ∎

5. Computation of the expected NPV of dividends under

In this section, we compute the expected NPV of the dividends under the hybrid barrier strategy as defined in Section 3:

| (5.1) |

where . The pure periodic case () and the pure continuous case () are given in [19] and [6], respectively. Here, we focus on the case .

Toward this end, we first review the scale function.

5.1. Review on scale functions.

Fix . We use for the scale function of the process . This is the mapping from to that takes value zero on the negative half-line, while on the positive half-line it is a strictly increasing function that is defined by its Laplace transform:

| (5.2) | ||||

where is as defined in (2.1) and

| (5.3) | ||||

We also define, for ,

Define also

In particular, , , and, for ,

Remark 5.1.

In this paper, we use the following versions of the scale function: for and ,

| (5.7) | ||||

5.2. The expression for in terms of the scale function

We will now present some preliminary results that will allow us to express the function given by (5.1) in terms of scale functions. The proofs of the following results are lengthy and hence are deferred to Appendix A.

Define

| (5.8) |

Proposition 5.1.

For , , and ,

| (5.9) |

where

Proposition 5.2.

For , , and ,

| (5.10) |

where

Let, for and ,

where, in particular,

| (5.11) | ||||

Combining Propositions 5.1 and 5.2 and after simplification, we have the following result. The proof is given in Appendix A.

Theorem 5.1.

For and ,

| (5.12) |

where, in particular, for , we have .

6. The selection of and

For the optimality of the hybrid barrier strategy constructed in Section 3, we shall assume the following relation on the parameters , , and .

Assumption 6.1.

We assume that .

This is assumed throughout this section and also in Section 7. The cases and , where the pure continuous and periodic barrier strategies, respectively, are shown to be optimal, are deferred to Section 8.

6.1. Smoothness conditions.

In order to obtain the optimal thresholds, which we call and , we will ask that the value function is smooth enough. For any choice of , it is clear that is continuous for . Its derivatives, whenever they exist, are given by

Fix . We shall first compute, in the following lemma, the derivatives of and . Its proof is given in Appendix B.

Lemma 6.1.

Fix . (i) For ,

| (6.1) | ||||

where we assume that and exist for the second and third equalities, respectively.

(ii) For ,

| (6.2) | ||||

where we assume in the third equality that and exist.

In view of the first and second equalities in (6.1) and (6.2) and Remark 5.1, is (resp. ) when has paths of bounded (resp. unbounded) variation. We now analyze the smoothness at the barriers and .

6.1.1. Smoothness at

6.1.2. Smoothness at

For the case of bounded variation, suppose exists. By the second equalities in (6.1) and (6.2),

| (6.4) |

On the other hand, by straightforward differentiation (using Remark 5.2),

| (6.5) |

where

For the case of unbounded variation, suppose exists. By the third equalities in (6.1) and (6.2) and Remark 5.1 (2), we obtain

| (6.7) |

Hence is thrice continuously differentiable at if (6.3) and (6.6) hold simultaneously.

In summary, we have the following.

Lemma 6.2.

Suppose are chosen so that is satisfied. Then, the following holds:

-

(1)

is (resp. ) on for the case of bounded (resp. unbounded) variation.

-

(2)

Suppose in addition that is satisfied. Then,

-

(a)

for the case of bounded variation and if exists, then is twice continuously differentiable at ;

-

(b)

for the case of unbounded variation and if exists, then is thrice continuously differentiable at .

-

(a)

6.2. Existence of

Hence, in view of (6.5), for , there exists a minimizer of the mapping such that it is strictly decreasing on and strictly increasing on . In particular,

| (6.9) |

where is such that

| (6.10) |

this exists and is unique because, by Assumption 6.1, the left hand side is strictly decreasing in to minus infinity and

With this , we have and

| (6.11) |

In summary, we have the following:

Lemma 6.3.

Fix .

-

(1)

If , the mapping is monotonically (strictly) increasing and .

-

(2)

Otherwise, decreases (strictly) on and increases (strictly) on . It attains a local minimum at and hence .

We now show the following monotonicity property.

Lemma 6.4.

The function is (strictly) increasing to .

Proof.

By Remark 5.2, for ,

By this and Assumption 6.1, we obtain a uniform lower bound

| (6.12) |

Recall such that (6.10) holds. Fix such that (or ).

- (1)

- (2)

Finally, it is clear by (6.12) that . ∎

In view of Lemma 6.4, we first start at and increase the value of until we attain the desired pair such that

For the case , by (2.3),

| (6.13) |

Hence we shall increase the value of until we get such that . Here, there are two scenarios:

-

(1)

is attained at a local minimizer ;

-

(2)

is attained at zero .

In both cases, we have (or ). In addition, for (1), holds as well, while for (2), we must have that is monotonically increasing (or ) and hence (6.9) gives the inequality:

We summarize these in the following lemma.

Lemma 6.5.

There exist a pair such that one of the following holds.

-

(1)

such that .

-

(2)

such that and .

6.3. Convergence results

We conclude this section with convergence results with respect to and . The following results indicate that the optimal hybrid barrier strategies approach the pure continuous/periodic barrier strategies, which are shown in the following section to be optimal when Assumption 6.1 does not hold.

Lemma 6.6.

-

(1)

As , we have .

-

(2)

As (and then ), we have .

-

(3)

As , we have .

7. Optimality of the hybrid barrier strategies

In this section, we show the optimality of under Assumption 6.1. By Lemma 6.5, is always satisfied and hence, by (5.12),

| (7.1) |

We show that this solves the variational inequalities given in Lemma 4.1.

Recall the mapping as in (4.1) for any sufficiently smooth function of .

Lemma 7.1.

We have, for ,

for ,

and, for , .

Proof.

By how and are chosen as in Lemma 6.5, we have the following.

Lemma 7.2.

-

(1)

We have when and when .

-

(2)

We have .

-

(3)

The function is concave on .

Proof.

(1) By differentiating (7.1), , where, in particular, equation (6.2) gives

For the case , because , given by (6.6), is satisfied by Lemma 6.5 (1),

For the case , by Lemma 6.5 (2),

(2) By (6.2), it is clear that for all .

(3) (i) For , integration by parts applied to the third equality of Remark 5.2 gives

By differentiating this,

Hence, by (7.1) and Assumption 6.1,

(ii) For , by (6.2) and Assumption 6.1,

By (i) and (ii), together with the continuity of as in Lemma 6.2, is concave. ∎

Lemma 7.3.

For , we have

Proof.

8. Optimality of pure periodic and continuous strategies

In this section, we consider the case Assumption 6.1 does not hold. We show when that a pure periodic barrier strategy as defined in Section 3.3 is optimal; when , a pure continuous barrier strategy is optimal.

8.1. Optimality of the pure periodic barrier strategy

Here we assume , and show that it is optimal not to activate the continuous strategy ().

Let be the set of strategies such that uniformly. Pérez and Yamazaki [19] studied the optimization problem over the restricted set . By Section 4.3 in [19], we have

where is the value function under the periodic barrier strategy with the barrier , which is given as follows:

-

(1)

For the case , we have

(8.1) where is the unique root of

-

(2)

If , then and

(8.2)

8.2. Optimality of the pure continuous barrier strategy

We now assume that , and show that it is optimal not to exercise the periodic strategy (i.e. ).

Let be the set of strategies such that uniformly. Bayraktar et al. [6] studied the optimization problem over the restricted set . By equation (2.5) in [6] (with normalization), we have

| (8.3) |

where

| (8.4) |

On the other hand, (4.3) holds because for all .

9. Numerical Results

In this section, we confirm the analytical results obtained in the previous sections through a sequence of numerical experiments. Here, we assume that the underlying process is a spectrally positive version of the phase-type Lévy process (with Brownian motion) as discussed in [1]. Its scale function can be expressed analytically as discussed in [10], and this process is particularly important because it can approximate any spectrally positive Lévy process (see [1] and [10]).

We assume that

| (9.1) |

where, , , is standard Brownian motion, and is a Poisson process with arrival rate . In addition, is an i.i.d. sequence of phase-type-distributed random variables with representation , or equivalently the first absorption time in a continuous-time Markov chain consisting of a single absorbing state and transient states with initial distribution and transition matrix (see [1] for details). The processes , , and are assumed to be mutually independent. We refer the reader to [10, 13] for the forms of the corresponding scale functions.

9.1. Computing and the value function

For the process in (9.1), we set and , and, for , we use a phase-type distribution with that approximates a (folded) normal random variable with mean and variance (see [14] for the values of and ). For the drift parameter , we consider Case 1: and Case 2: , obtaining the cases and , respectively. For the other parameters, let , , and so that Assumption 6.1 is satisfied.

The first implementation step is computing the optimal barriers as described in Lemma 6.5. As discussed in Section 6.2, we choose these such that and . Thanks to Lemma 6.3 (i.e., the fact that is monotone), the minimizer of can be obtained by the bisection method. In addition, using Lemma 6.4, another bisection can be used to obtain (and ). With these and values, the value function becomes , as in (7.1).

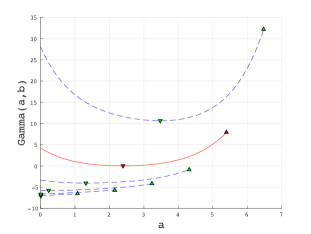

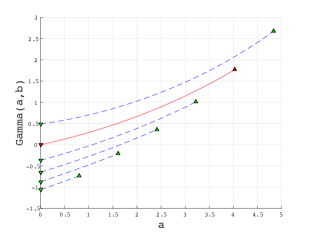

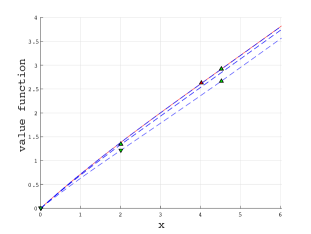

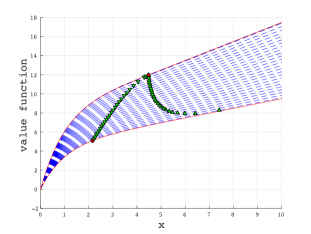

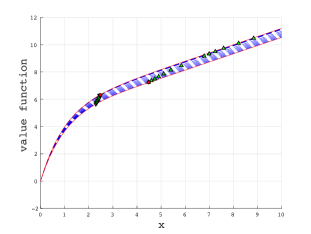

In the first two rows of Figure 1, we plot, for Cases 1 and 2, the mappings and for various values of . As in (6.12), is uniformly increasing. The values correspond to the points (indicated by the down-pointing triangles) at which is minimized and vanishes (if ). The optimal pair is such that the minimum is zero. In Figure 2, we plot the corresponding value functions (solid lines) along with the suboptimal NPVs (dotted lines) given in (5.12) where . It can be confirmed in both cases that dominates , for , uniformly in .

|

|

|

|

| Case 1 | Case 2 |

|

|

| Case 1 | Case 2 |

9.2. Sensitivity and convergence with respect to and

Next, we study the behavior of the value function with respect to and to confirm the results discussed in Sections 6.3 and 8. Here we use the same parameters as in Case 1 above unless stated otherwise.

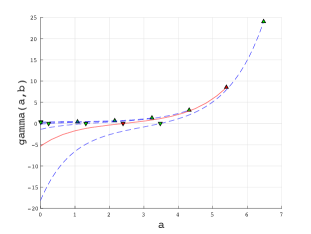

On the left of Figure 3, we plot the value function , for , along with and , as in (8.1) and (8.3), respectively, for the cases and . This confirms that increases with for each . As in Lemma 6.6 (1), as , the value of goes to infinity and consequently converges decreasingly to (which is independent of the value of ). In contrast, as in Lemma 6.6 (3), as , the distance between and shrinks to zero and consequently the value function converges increasingly to (when ).

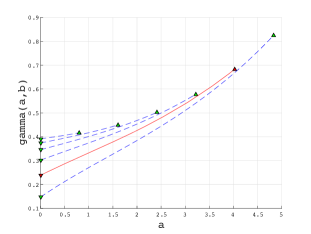

On the right of Figure 3, we plot the value function , for , along with the value functions and , as in (8.1) and (8.3), respectively, for the cases (equivalently ) and . This confirms that increases with for each . As in Lemma 6.6 (2), as , the value of increases to infinity and consequently the value function converges increasingly to (which is independent of the value of ). In contrast, as , periodic dividend opportunities vanish and hence the problem gets closer to the one defined in (8.3). Consequently and converge to the values defined in (8.4) and (8.3), respectively.

|

|

| convergence in | convergence in |

Appendix A Proofs of Propositions 5.1 and 5.2 and Theorem 5.1

In this appendix, we prove Propositions 5.1 and 5.2 as well as Theorem 5.1. Define, for and ,

with = for short. Note that these have the following relation with , as in (5.8):

| (A.1) |

For , define the hitting times of the processes and , as defined in Section 3, as

Throughout this appendix, let be the first periodic dividend decision time, which is an independent exponential random variable with parameter .

A.1. Proof of Proposition 5.1.

Let us denote the left hand side of (5.9) by . By applying the strong Markov property at , noticing that

| (A.2) |

and using Theorems 3.1 and 3.2 in [5], we obtain, for ,

| (A.3) | ||||

Here,

In contrast, by the strong Markov property, (3.6), and the fact that has no negative jumps,

| (A.4) |

Here, by the Laplace transform of given on page 228 of [12],

| (A.5) |

and, using the resolvent for given in Theorem 8.11 of [12] and integration by parts, we obtain

Substituting these into (A.4), we have

Hence, by (A.3), for all ,

| (A.6) |

where

Now, setting and solving for (using the fact that and ), we obtain that, by (A.1),

| (A.7) |

A.2. Proof of Proposition 5.2.

To prove Proposition 5.2, we first compute the following identity:

The case has already been considered in Theorem 3.1 of [5]. Here, we generalize this using Lemma 2.1 in [16] and Corollary 4.1 in [5].

Proposition A.1.

For any , , , and ,

| (A.8) |

Proof.

We prove this proposition in three steps.

(1) For , by the strong Markov property and the fact that has no negative jumps, we obtain

By (5.4), for ,

This, together with the second equality in (5.4), gives

| (A.9) |

We note that on and for . Hence, for , by the strong Markov property and (A.9),

Here, using Corollary 4.1 in [5] and Lemma 2.1 in [16], we have

Hence,

| (A.10) |

(2) (i) For the case where is of bounded variation, by setting in (A.10) and solving for (using , and ), we obtain

| (A.11) |

(ii) Now suppose is of unbounded variation. To show that we obtain the same identity (A.11), it suffices to modify the proof of (3.21) in [5] (which considers the case). Define the spectrally negative Lévy process , and construct the dual process with the lower Parisian reflection barrier , as in [5], and its hitting times and for . Then, we have

Now, following the proof of (3.21) from Section 5 in [5], we arrive at

| (A.12) |

with

where and are defined analogously to and for and is the time-shift operator and n denotes the excursion measure of the spectrally negative Lévy process away from zero (see [17] for more details). Here,

where we have used the strong Markov property for the first equality, (5.4) for the second equality and a slight modification of Lemma 6.3 in [20] for the last equality. By substituting this into (A.12), we obtain (A.11).

(3) Now, by using (A.11) in (A.10), the proof is complete for both the bounded and unbounded variation cases.

∎

Using the proposition above, we have the following.

Corollary A.1.

For any , , and ,

where

Proof.

A.2.1. Proof of Proposition 5.2.

First, denote the left hand side of (5.10) by . By applying the strong Markov property at , Proposition A.1, Corollary A.1, and (A.2), we have, for ,

| (A.14) | ||||

On the other hand, by applying the strong Markov property at and because on , and does not have negative jumps,

| (A.15) |

Here, as in the proof of Theorem 1 in [4], the first term on the right hand side is

| (A.16) |

Hence, using (A.5) and (A.16) in (A.15),

Substituting this in (A.14) and using (A.1) (which holds for all ),

| (A.17) | ||||

where

Hence setting and solving for (using and ) gives us that . Substituting this in (A.17), we obtain

This equals the right hand side of (5.10) because

A.3. Proof of Theorem 5.1.

Appendix B Proof of Lemma 6.1

For and , integration by parts gives

References

- [1] Asmussen, S., Avram, F., and Pistorius, M.R. Russian and American put options under exponential phase-type Lévy models. Stochastic Process. Appl. 109(1), 79–111, (2004).

- [2] Avanzi, B., Tu, V., and Wong, B. On optimal periodic dividend strategies in the dual model with diffusion. Insur. Math. Econ. 55, 210-224, (2014).

- [3] Avanzi, B., Tu, V., and Wong, B. On the interface between optimal periodic and continuous strategies in the presence of transaction costs. ASTIN Bull. 46(3), 709-746, (2016).

- [4] Avram, F., Palmowski, Z., and Pistorius, M.R. On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl. Probab. 17, 156-180, (2007).

- [5] Avram, F., Pérez, J.L., and Yamazaki, K. Spectrally negative Lévy processes with Parisian reflection below and classical reflection above. Stochastic Process. Appl., 128 (1), 255-290, (2018).

- [6] Bayraktar, E., Kyprianou, A.E., and Yamazaki, K. On optimal dividends in the dual model. ASTIN Bull. 43(3), 359-372, (2013).

- [7] Chan, T., Kyprianou, A.E., and Savov, M. Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Relat. Fields 150, 691-708, (2011).

- [8] Egami, M. and Yamazaki, K. Precautionary measures for credit risk management in jump models. Stochastics, 85(1), 111–143, (2013).

- [9] Egami, M. and Yamazaki, K. On the continuous and smooth fit principle for optimal stopping problems in spectrally negative Lévy models. Adv. in Appl. Probab., 46(1), 139–167, (2014).

- [10] Egami, M. and Yamazaki, K. Phase-type fitting of scale functions for spectrally negative Lévy processes. J. Comput. Appl. Math. 264, 1–22, (2014).

- [11] Hernández-Hernández, D., Pérez, J.L., and Yamazaki, K. Optimality of refraction strategies for spectrally negative Lévy processes. SIAM J. Control Optim. 54(3), 1126-1156, (2016).

- [12] Kyprianou, A.E. Introductory lectures on fluctuations of Lévy processes with applications. Springer, Berlin, (2006).

- [13] Kuznetsov, A., Kyprianou, A.E., and Rivero, V. The theory of scale functions for spectrally negative Lévy processes. Lévy Matters II, Springer Lecture Notes in Mathematics, (2013).

- [14] Leung, T., Yamazaki, K., and Zhang, H. An analytic recursive method for optimal multiple stopping: Canadization and phase-type fitting. Int. J. Theor. Appl. Finance 18(5), 1550032, (2015).

- [15] Loeffen, R. On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. Ann. Appl. Probab. 18(5), 1669-1680 (2008).

- [16] Loeffen, R.L., Renaud, J-F. and Zhou, X. Occupation times of intervals until first passage times for spectrally negative Lévy processes with applications. Stochastic Process. Appl., 124 (3), 1408–1435, (2014).

- [17] Pardo, J.C., Pérez, J.L. and Rivero, V. The excursion measure away from zero for spectrally negative Lévy processes. Ann. Inst. H. Poincaré, (forthcoming).

- [18] Pérez, J.L. and Yamazaki, K. On the refracted-reflected spectrally negative Lévy processes. Stochastic Process. Appl., 128 (1), 306–331, (2018).

- [19] Pérez, J.L. and Yamazaki, K. On the optimality of periodic barrier strategies for a spectrally positive Lévy process. Insur. Math. Econ., 77, 1–13, (2017).

- [20] Pérez, J.L. and Yamazaki, K. Mixed periodic-classical barrier strategies for Lévy risk process. arXiv 1609.01671, (2016).

- [21] Protter, P. Stochastic integration and differential equations. 2nd Edition, Springer, Berlin, (2005).

- [22] Yamazaki, K. Inventory control for spectrally positive Lévy demand processes. Math. Oper. Res., 42(1), 212–237, (2017).

- [23] Yamazaki, K. Contraction options and optimal multiple-stopping in spectrally negative Lévy models. Appl. Math. Optim., 72(1),147–185, (2015).