A multi-asset investment and consumption problem with transaction costs

Abstract.

In this article we study a multi-asset version of the Merton investment and consumption problem with proportional transaction costs. In general it is difficult to make analytical progress towards a solution in such problems, but we specialise to a case where transaction costs are zero except for sales and purchases of a single asset which we call the illiquid asset.

Assuming agents have CRRA utilities and asset prices follow exponential Brownian motions we show that the underlying HJB equation can be transformed into a boundary value problem for a first order differential equation. The optimal strategy is to trade the illiquid asset only when the fraction of the total portfolio value invested in this asset falls outside a fixed interval. Important properties of the multi-asset problem (including when the problem is well-posed, ill-posed, or well-posed only for large transaction costs) can be inferred from the behaviours of a quadratic function of a single variable and another algebraic function.

Alex Tse: Cambridge Endowment for Research in Finance, Judge Business School, University of Cambridge, Cambridge, CB2 1AG, UK. S.Tse@jbs.cam.ac.uk

Yeqi Zhu: Credit Suisse, London, UK. (The opinions expressed in the paper are those of the author and not of Credit Suisse.) Yeqi.Zhu@credit-suisse.com

1. Introduction

In one of his seminal works, Merton [20] considers a portfolio and consumption problem faced by a price-taking agent in a continuous-time stochastic financial model consisting of a risk-free bond and a risky asset. The agent is assumed to have the objective of maximising the expected discounted utility from consumption over an infinite horizon. In a model in which the single risky asset follows an exponential Brownian motion with constant parameters and the agent has constant relative risk aversion, Merton shows that the optimal behaviour is to consume at a rate which is proportional to wealth, and to invest a constant fraction of wealth in the risky asset. The result generalises easily to multiple risky assets.

Constantinides and Magill [9] were the first to add proportional transaction costs to the model. In a model with a single risky asset they conjectured the form of the optimal strategy, namely it is optimal to keep the fraction of wealth invested in the risky asset in an interval. Subsequently Davis and Norman [11] gave a precise statement of the result and showed how the solution could be expressed in terms of local times. The optimal behaviour is to trade in a minimal fashion so as to keep the variables (cash wealth, wealth in the risky asset) in a wedge-shaped region in the plane, and this is achieved by sales and purchases of the risky asset in the form of singular stochastic controls.

The approach in Davis and Norman [11] is to write down the Hamilton-Jacobi-Bellman (HJB) equation, and to characterise the candidate value function as a solution to this equation. Shreve and Soner [23] reproved the results of [11] using viscosity solutions and gave several extensions. These approaches remain the main methods for solving portfolio optimisation problems with transaction costs, although recently a different technique based on shadow prices has been proposed, see Guasoni and Muhle-Karbe [14] for a users’ guide. Kallsen and Muhle-Karbe [18], Choi et al [7] and Herczegh and Prokaj [1] use the dual approach to characterise the solution to the problem with transaction costs and one risky asset.

The results in Davis and Norman [11] are limited to a single risky asset, and it is of great interest to understand how they generalise to multiple risky assets. In his survey article on consumption/investment problems with transaction costs Cadenillas [5, page 65] says that ‘most results in this survey are limited to the case of only one bond and only one stock. It is then important to see if these results can be extended to cover a realistic number of stocks’. Although there has been some progress since that paper was published, similar sentiments are echoed in recent papers by Chen and Dai [27, page 2]: ‘most of the existing theoretical characterisations of the optimal strategy are for the single risky-asset case. In contrast there is a relatively limited literature on the multiple risky-asset case’ and Guasoni and Muhle-Karbe [14, page 194]: ‘In sharp contrast to frictionless models, passing from one to several risky assets is far from trivial with transaction costs …multiple assets introduce novel effects, which defy the one-dimensional intuition’. In summary therefore, there is great interest in both theoretical and numerical results on the multi-asset case, and this paper can be considered as a contribution to that literature.

In the multi-asset case, and on the computational side, Muthuraman and Kumar [21] use a process of policy improvement to construct a numerical solution for the value function and the associated no-transaction region, Collings and Haussmann [8] derive a numerical solution via a Markov chain approximation for which they prove convergence, and Dai and Zhong [10] use a penalty method to obtain numerical solutions. On the theoretical front Akian et al [2] show that the value function is the unique viscosity solution of the HJB equation (and provide some numerical results in the two-asset case) and Chen and Dai [27] identify the shape of the no-transaction region in the two-asset case. Explicit solutions of the general problem remain very rare.

One situation when an explicit solution is possible is the rather special case of uncorrelated risky assets, and an agent with constant absolute risk aversion. In that case the problem decouples into a family of optimisation problems, one for each risky asset, see Liu [19]. Another setting for which some progress has been made is the problem with small transaction costs, see Whalley and Wilmott [26], Janecek and Shreve [17], Bichuch and Shreve [4], Soner and Touzi [24], and, for a recent analysis in the multi-asset case, Possamaï et al [22]. These papers use an expansion method to provide asymptotic formulae for the optimal strategy, value function and no-transaction region.

Our focus is on optimal investment/consumption problems, but there is a parallel literature on optimal investment problems involving maximising expected utility at a distant terminal horizon, see, for example, Dumas and Luciano [12] for an explicit solution in the one-asset case and Bichuch and Guasoni [3] for recent work in a setting similar to ours with liquid and illiquid assets.

In this paper we consider the problem with a risk-free bond and two risky assets. Transactions in the first risky asset are costless, but transactions in the second risky asset, which we term the illiquid asset, incur proportional costs. This is also the setting of a recent paper by Choi [6]. More generally, we may have several risky assets on which no transaction costs are payable. By a mutual fund theorem, this general case can be reduced to the case with a single liquid, risky asset.

This paper is an extension of Hobson et al [15] which considers a similar problem with a bond and an illiquid asset but with no other risky assets111This paper can also be viewed as a development of the results of Hobson and Zhu [16]. The model in Hobson and Zhu includes both a liquid risky asset and an illiquid asset, but assumes that transaction cost on sales of the illiquid asset is infinite. This case might be called the “perfectly illiquid” case: the illiquid asset can be sold, but not bought, and the problem is an optimal liquidation problem. This paper extends Hobson and Zhu [16] to allow for finite transaction costs and purchases of the illiquid asset.. Many of the techniques of [15] carry over to the wider setting of this paper. (Similarly, the paper of Choi [6] extends the work of Choi et al [7] to include a risky liquid asset.) However, since there are fewer parameters when the financial market includes just one risky asset, the problem in [15] is significantly simpler and much more amenable to a comparative statics analysis. In contrast, this paper treats the multi-asset problem which has proved so difficult to analyse in full generality, albeit in a rather special case. The multi-asset setting brings new challenges and complicates the analysis.

It is straightforward to write down the Hamilton-Jacobi-Bellman (HJB) equation for our problem. The value function is a function of four variables (wealth in liquid assets, price of the illiquid asset, quantity of illiquid asset held, time) and satisfies a HJB equation which is second order, non-linear and subject to value matching and smooth fit at a pair of unknown free boundaries. (The smooth fit turns out to be of second order.) Our first achievement is to show that the problem of finding the free boundaries and the value function can be reduced to the study of a boundary crossing problem for a family of solutions to a class of first order ordinary differential equations parametrised by the initial values. This allows us to characterise precisely the parameter combinations for which the problem is well-posed (Theorem 1), and in those cases to give an expression for the value function (Theorem 2). These results extend Choi et al [7] and Hobson et al [15] to the case of multiple risky assets.

As mentioned above, Choi [6] studies a similar problem. The main difference between this paper and Choi [6] is that we analyse the HJB equation, whereas Choi takes the dual approach and studies shadow prices. Choi [6][Remark 2.2, Assumption 2.4] assumes that the corresponding two-asset problem with zero transaction costs is well-posed, and hence the problem with liquid and illiquid assets is well-posed whatever the value of transaction costs. In contrast, in addition to the unconditionally well-posed case, we also consider the case where the problem is ill-posed for zero and small transaction costs, but well-posed for large transaction costs. (Note that analysis of this situation is beyond the scope of approaches which rely on expansions in a (small) transaction cost parameter.) In fact we show (Corollary 1) that the problem is well-posed for sufficiently large transaction costs provided the problem is well-posed when the liquid asset is omitted. We call the case when the problem is well-posed only for large transaction costs the conditionally well-posed case.

Our second achievement is to make definitive statements about the comparative statics for the problem. We focus on the boundaries of the no-transaction wedge and the certainty equivalent value of the holdings in the illiquid asset. Amongst other results, we prove (see Theorem 3 and Corollary 2 for precise statements) that as the drift on the illiquid asset improves, the agent aims to keep a larger fraction of his total wealth in the illiquid asset, in the sense that the critical ratios at which sales and purchases take place are increasing in the drift. Conversely, as the agent becomes more impatient, the agent keeps a smaller fraction of wealth in the illiquid asset. Further, we prove (Theorem 4 and Corollary 3) that as the drift on the illiquid asset improves, or as the agent becomes less impatient, the certainty equivalent value of the holdings in the illiquid asset increases. See Section 6 for a more detailed discussion.

The remainder of the paper is as follows. In the next section we formulate the problem. In Section 3 we derive the HJB equation and give heuristics showing how it can be converted to a free boundary value problem involving a first order differential equation. Then we can state our main results on the existence of a solution (Section 4). In Section 5 we discuss the various cases which arise. In Section 6 we discuss the comparative statics of the problem, before Section 7 concludes. Materials on the solution of the free boundary value problem, the verification argument for the HJB equation, and other lemmas on the analysis of solutions of the differential equations are relegated to the appendices.

2. The problem

The economy consists of one money market instrument paying constant interest rate and two risky assets, one of which is liquidly traded while the other one is illiquid. There are no transaction costs associated with trading in the liquid asset. Meanwhile, trading in the illiquid asset incurs a proportional transaction cost on purchases and on sales, where not both and are zero. Let be the price processes of the liquid and illiquid assets respectively. The price dynamics are given by

where is a pair of Brownian motions with correlation coefficient . Write and for the Sharpe ratio of the liquid and illiquid asset respectively.

Let be the number of units of the illiquid asset held by an agent at time . Then where and are both increasing, non-negative processes representing the cumulative units of purchases and sales respectively of the illiquid asset. Let be the non-negative consumption rate process of the agent and be the cash value of holdings in the risky liquid asset. We assume , and are progressively measurable and right-continuous. If is the total value of the liquid instruments (cash and the liquid risky asset) then, assuming transaction costs are paid in cash, and consumption is from the cash account,

We say that a portfolio is solvent at time if its instantaneous liquidation value is non-negative, that is

A consumption/investment strategy is said to be admissible if the resulting portfolio is solvent at the current time and at all the future time points. Write for the set of admissible strategies with initial time- value .

We assume the agent has a CRRA utility function with risk aversion parameter . His objective is to find an optimal strategy which maximises the expected lifetime discounted utility from consumption. The problem is thus to find

| (1) |

where is the agent’s subjective discount rate.

We will call the paper wealth of the agent. In our parametrisation a key quantity will be , the proportion of paper wealth invested in the illiquid asset.

3. The HJB equation and a free boundary value problem

3.1. Deriving the HJB equation

Let

be the forward-starting value function from time . Inspired by the analysis in the classical case involving a single risky asset only, we postulate that the value function has the form

| (2) |

for some strictly positive function to be determined and a convenient scaling constant which will help simplify the HJB equation. We take where and are constants to be defined in Section 3.2 below in terms of the financial parameters associated with the underlying problem. For the present we assume that is smooth and use heuristic arguments to derive a characterisation of the candidate value function. Later we will outline a verification argument that this candidate value function coincides with the solution of the corresponding optimal investment/consumption problem, and therefore deduce the necessary smoothness properties of and .

Building on the intuition developed by Constantinides and Magill [9] and Davis and Norman [11] we expect that the optimal strategy of the agent is to trade the illiquid asset only when falls outside a certain interval to be identified. Due to the solvency restriction, we must have and . Whenever , the agent purchases the illiquid asset to bring back to . Hence for an initial position such that , the number of units of illiquid asset to be purchased is given by such that . The value function does not change on this transaction, and hence we deduce that for ,

and in turn

| (3) |

where . Similar consideration leads to the conclusion that

| (4) |

for where .

Consider defined via

We expect to be a supermartingale in general, and a martingale under the optimal strategy. Suppose is . Then applying Ito’s lemma we find

Further assume is strcitly increasing and concave in . Then on maximising the drift term with respect to and and setting the resulting maxima to zero, we obtain the HJB equation over the no-transaction region:

| (5) |

3.2. Reduction to a first order free boundary value problem

Define the auxiliary parameters , , and as

It will turn out that the optimal investment and consumption problem depends on the original parameters only through these auxiliary parameters and the risk aversion level .

Here plays the role of a ‘normalised discount factor’, which adjusts the discount factor to allow for numeraire growth effects and for investment opportunities in the transaction-cost free risky asset. is a simple function of the ‘idiosyncratic volatility’ of the illiquid asset. The parameter is the ‘effective Sharpe ratio, per unit of idiosyncratic volatility’ of the illiquid asset. The parameter is the hardest to interpret: essentially it is a nonlinearity factor which arises from the multi-dimensional structure of the problem. Note that .

In the sequel we will work with the following assumption.

Standing Assumption 1.

Throughout the paper we assume , and .

The rationale for imposing is that is necessary to ensure well-posedness of the Merton problem in the absence of the illiquid asset. (If and , the value function is infinite for the Merton problem. Conversely, if and , then for every admissible strategy the expected discounted utility of consumption equals . If the Merton problem is ill-posed in the absence of the illiquid asset, then our problem is necessarily ill-posed.)

In contrast, the assumption is not necessary. However, the advantage of working with a positive effective Sharpe ratio of the illiquid asset () is that the no-transaction wedge is contained in the first two quadrants of the plane. The assumption reduces the number of cases to be considered in our analysis, and facilitates the clarity of the exposition, but the methods and results developed in this paper can be extended easily to the case of an illiquid asset with negative effective Sharpe ratio222If the agent chooses never to invest in the illiquid asset. In this case agent closes any initial position in at time zero and thereafter the problem reduces to a standard Merton problem with the single risky asset and no transaction costs..

The case is rather special and we exclude it from our analysis. One scenario in which we naturally find is if . In this case there is neither a hedging motive, nor an investment motive for holding the liquid risky asset333More generally, the position in the liquid asset is a combination of an investment position to take advantage of the expected excess returns in and a hedging position to offset the risk of the position in the illiquid asset . If then when these terms exactly cancel. In particular, if the half-line is inside the no-transaction region, then since consumption takes place from the cash account, if ever then wealth can only go negative. Then the subspace is absorbing, and no further purchases of the liquid asset are ever made.. Essentially then, the investor can ignore the presence of the liquid risky asset, reducing the dimensionality of the problem. This problem is the subject of [15]. If then the solution we define in the next paragraph may pass through singular points. See Choi et al [7] or Hobson et al [15] for a discussion of some of the issues.

We adopt the same transformation as [15] to reduce the order of the HJB equation. Recall the relationship between and in (2) and the definition . Away from , set , , , let be the inverse function to and set . Then, we show in Appendix A that (5) can be transformed into a first order differential equation

| (6) |

where

| (7) |

with

Define the quadratic

| (8) |

and the algebraic function

| (9) |

Note that has a turning point (a minimum if and a maximum if ) at and set .

The following are the key properties of the function . They are special cases of a more complete set of properties given in Lemma 2 below.

Lemma 1.

-

(1)

can be extended to by continuity on ;

-

(2)

if and only if ;

-

(3)

For given and the sign of depends only on the signs of and .

Now we apply the same transformations which took (5) to (6) to the value function on the purchase and sale regime. For , as given by (3). Then

and . It follows that . This expression holds for on which . The equivalent range in is thus given by . Similarly on the sale region we have for .

The smoothness of the original value function now translates into smoothness of the transformed value function . Hence we are looking for a continuously differentiable function and boundary points solving (6) on with for and for . First order smoothness of at the boundary points forces . By Lemma 1, if and only if . Hence the free boundary points must be given by the -coordinates where intersects the quadratic . The free boundary value problem now becomes solving on subject to and .

As an example, suppose and . Fix . Then the solution to (6) started at is decreasing; we are interested in when this solution crosses again; call this point . Then we have a family of solutions to (6) with and . The solution we want is the one which is consistent with the given transaction costs. Our approach is based on the same idea as in [15]. Let be the round-trip transaction cost. Suppose for now and in turn . Exploiting the relationships that and , we have

Then, using the definitions of , and ,

| (10) | |||||

where to get the last line we use the fact that . Hence the required solution from the free boundary value problem is the one such that

| (11) |

holds.

In the case where or equivalently , the integrals and are not well defined. But it can be shown that (11) still holds using a limiting argument, see Appendix G.

To summarise, we would like to solve the following:

(The free boundary value problem) find a positive function and a pair of boundary points solving

(12) and (11).

In Section 5, we distinguish several different cases and discuss how to construct the solution in each of these cases.

The central role played by the quadratic is clear from (12). The function acts as a bound on the feasible solutions to , at least for . Suppose, for example, that . Then for we have by construction, but also for . Moreover, the value is crucial in determining when the problem is ill-posed.

4. Main results

In Section 3 we converted the original HJB equation into the free boundary value problem (12). Now we argue that, given a solution to (12) we can reverse the transformations and construct a candidate value function.

Suppose there exists a solution to (12) with being strictly positive. Define and . Let , and . We would like to construct the candidate value function from where solves . The main subtlety is that is not well-defined at . Nonetheless, the definition of at can be understood in a limiting sense. To this end, we distinguish two different cases based on whether and have the same sign or not, or equivalently whether the no-transaction wedge, plotted in space, includes the vertical axis (corresponding to ).

Proposition 1.

(i) Suppose . Define via

| (13) |

on . Then (13) is equivalent to

| (14) |

and (14) is an alternative definition of .

Let

Then is a function on . Moreover is strictly increasing and strictly concave in .

(ii) Suppose . Define via

Let

with . Then , and is a function on . Moreover is strictly increasing and strictly concave in .

The first pair of main results of this paper are summarised in the following two theorems. For a given set of risk aversion parameter , discount factor and market parameters , , , , , , we say the problem is (unconditionally) well-posed if the value function is finite on the interior of the solvency region for all values of the transaction costs and with . We say the problem is ill-posed if the value function is infinite for all and . We say the problem is conditionally well-posed if the problem is well-posed for large values of the round-trip transaction cost, but ill-posed for small values. Theorems 1 and 2 are proved in Appendix D.

Theorem 1.

The investment/consumption problem is:

-

(1)

well-posed in either of the following cases:

-

(a)

,

-

(b)

and ;

-

(a)

-

(2)

ill-posed if , and ;

-

(3)

conditionally well-posed if , and . In this case the problem is well-posed if and only if where is defined in (18) below.

Note that, if then is necessary and sufficient for the problem with transaction costs set to zero to be well-posed. Further, if and and (a case we have excluded) then the problem is ill-posed for zero transaction costs, but well-posed for non-zero transaction costs.

The following result follows from the proof of Theorem 1 in the ill-posed case and relies on the fact that in this case there is an admissible strategy which generates infinite expected utility without investing in the liquid risky asset .

Corollary 1.

The problem with one risky liquid asset and one illiquid risky asset is ill-posed (for all values of transaction costs) if and only if the problem with the risky liquid asset omitted is ill-posed (for all values of transaction costs).

5. Solutions to the free boundary value problem

Let be the set . On define . Extend the definition of to where possible by taking appropriate limits. We begin this section with a list of useful results regarding the functions and and operators and . The proof of Lemma 2 is given in Appendix E.

Lemma 2.

-

(1)

-

(a)

For , on . Moreover, on , crosses exactly once from below at some point above ;

-

(b)

For , on . Moreover, on , either does not cross at all, or touches exactly once in the open interval , or crosses twice on .

-

(a)

-

(2)

For , is well defined at .

-

(3)

For and , is well-defined and

(15) Also, for and we have (and if ). For and (and for ) we have

(16) -

(4)

if and only if . Moreover,

-

(a)

for :

-

(i)

On , for and for or ;

-

(ii)

At , for and for . is not well-defined for ;

-

(iii)

On , for and for ;

-

(i)

-

(b)

for :

-

(i)

On , for and for or ;

-

(ii)

At , for and for . is not well-defined for ;

-

(iii)

On , for and for ;

-

(iv)

On , for and for or .

-

(i)

-

(a)

Recall is the extreme point of the quadratic (a minimum when and a maximum when ) with . The key analytical properties of the problem only depend on the signs of the three parameters . We classify four different cases using the decision tree in Figure 1.

We parameterise the family of solutions to (12) by the left boundary point. Fix and denote by the solution to the initial value problem

Let denote where first crosses to the right of . Define

| (17) |

Lemma 3.

Suppose . Then is a strictly decreasing, continuous mapping with and .

Now suppose . Let be the roots of . Set

| (18) |

Then is a strictly decreasing, continuous mapping with and . Moreover, and .

5.1. The cases

5.1.1. Case 1: and

For any initial value , . Thus must initially be larger than for being close to . By part 4 of Lemma 2, is negative on . Also, cannot cross from below on since . By considering the sign of , we conclude must be decreasing until it crosses . This guarantees the finiteness of , and the triple represents one possible solution to problem (12). Notice that the family of solutions cannot cross, and thus is decreasing in . The solutions corresponding to initial values and can be understood as the appropriate limit of a sequence of solutions.

Although has singularities at and , part 3 of Lemma 2 shows that a well-defined limit exists on and . Hence there exists a continuous modification of and a solution can actually pass through these singularity curves. See Figure 2(a) for some examples.

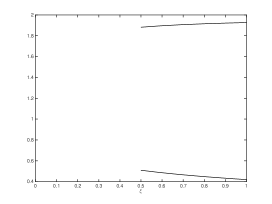

From the analysis leading to (11), the correct choice of should satisfy . From Lemma 3, for every given level of round-trip transaction cost , there exists a unique choice of the left boundary point given by and then the desired solution to the free boundary value problem is given by . Figure 2(b) gives the plots of and representing the boundaries under different levels of transaction cost.

Based on Figure 2 we can make a series of simple observations about the behaviour of and (which hold in the other cases too) some of which will be proved in Section 6 on the comparative statics of the problem. First, the lower and upper boundaries of the no transaction region, expressed in terms and , are monotonic decreasing and monotonic increasing respectively. In particular, the no-transaction region gets wider as transaction costs increase. Second, the no-transaction region may be contained in the first quadrant , or the upper-half plane , depending on and for other parameter values we may have that the no-transaction region is contained in the second quadrant (). Third, . Moreover, the numerics are suggestive of and so that there is a part of the solvency space close to the solvency limit which, even in the regime of very large transaction costs, is inside the region where a sale of at is necessary. Fourth, is less sensitive to changes in than so that the no-transaction wedge is not centred on the Merton line.

5.1.2. Case 2: , ,

Let be the root of on . Since the solution of must be bounded below by zero and above by for , for any initial value for which , the corresponding solution must hit . Hence there does not exist any positive solution which crosses again to the right of . See Figure 3. In this case, there is no solution to the free boundary value problem and indeed the underlying problem is ill-posed for all levels of transaction costs and thus the value function cannot be defined.

5.1.3. Case 3: , ,

Let with be the two roots of . The parameterisation of the solution is the same as in Case 1 except the left boundary point should now be restricted to to ensure a positive initial value. The function defined in (17) is still a strictly decreasing map with except its domain is now restricted to .

Unlike Case 1, we now only consider on the range . For such a given high level of round-trip transaction cost, the required left boundary point is given by and , see Figure 4. In this case, the problem is conditionally well-posed, ie it is well-posed only for a sufficiently high level of transaction cost.

5.1.4. Case 4: .

In this case the quadratic has a positive maxima at and on . By checking the sign of using part 4 of Lemma 2, one can verify that the solution of the initial value problem is always increasing for any choice of left boundary point . In this case the family of solutions is increasing in . The solution crosses from below at . The correct choice of is again the one solving using the same definition in (17). As in Case 1, the function is onto from to and hence always exists uniquely for any . See Figure 5. Indeed for , the agent’s utility function is always bounded above by zero and hence the value function always exists and is finite.

6. Comparative statics

In this section, we investigate how the no-transaction wedge and the value function change with the market parameters and level of transaction costs.

6.1. Monotonicity with respect to market parameters

Proposition 2.

Suppose is the solution to the free boundary value problem. Then:

-

(1)

and are decreasing in ;

-

(2)

For , and are increasing in .

Recall that and . Then, Proposition 2 gives immediately:

Theorem 3.

-

(1)

and are decreasing in ;

-

(2)

For , and are increasing in .

Theorem 3 describes the comparative statics in terms of the auxiliary parameters.444Since the free boundary value problem does not depend on , and are trivially independent of . We have strong numerical evidence that is decreasing in and is increasing in , but we have not been able to prove this result. In general, it is difficult to make categorical statements about the comparative statics with respect to the original market parameters since many of the market parameters enter the definitions of more than one of the auxiliary parameters. However, we have the following results concerning the dependence of and on the discount rate, and on the drift of the illiquid asset.

Corollary 2.

and are decreasing in . If then and are increasing in .

The corollary confirms the intuition that as the return on the illiquid asset asset increases, it becomes more valuable and the agent elects to buy the illiquid asset sooner, and to sell it later. Moreover, as his discount parameter increases, he wants to consume wealth sooner, and since consumption takes place from the cash account he elects to keep more of his wealth in liquid assets, and less in the illiquid asset.

Now we consider the cash value of the holdings in the illiquid asset. We compare the agent with holdings in the illiquid asset to an otherwise identical agent (same risk aversion and discount parameter, and trading in the financial market with bond and risky asset with price ) who has a zero initial endowment in the illiquid asset and is precluded from taking any positions in the risky asset.

Consider the market without the illiquid asset. For an agent operating in this market a consumption/investment strategy is admissible for initial wealth (we write ) if and are progressively measurable, and if the resulting wealth process is non-negative for all . Here solves

subject to . Let be the value function for a CRRA investor:

The problem of finding is a classical Merton consumption/investment problem without transaction costs. We find

Define to be the certainty equivalent value of the holding of the illiquid asset, i.e. the cash amount which the agent with liquid wealth and units of the illiquid asset with current price , trading in the market with transaction costs, would exchange for his holdings of the illiquid asset, if after this exchange he is not allowed to trade in the illiquid asset. (We assume there are no transaction costs on this exchange, but they can be easily added if required.) Then solves

which becomes

Theorem 4.

-

(1)

is decreasing in ;

-

(2)

is increasing in .

Corollary 3.

is decreasing in and increasing in .

Both these monotonicities are intuitively natural. For the monotonicity in , since the agent only ever holds long555Note, if he starts with a solvent initial portfolio, but with a negative holding in the illiquid asset, then the agent makes an instantaneous transaction at time zero to make his holding positive. positions in the illiquid asset, we expect him to benefit from an increase in drift and hence price of the illiquid asset. (Note, some care is needed in making this argument precise. Part of the optimal strategy is to sometimes purchase units of the illiquid asset, and this will be more costly if the price is higher.) If we consider monotonicty in then for , increasing reduces the magnitude of the discounted utility of consumption, and reduces the value function. However, this is not the same as decreasing the certainty equivalent value of the holding of risky asset. Indeed, when , increasing reduces the magnitude of the discounted utility of consumption, but since the terms are negative, this increases the value function. Nonetheless, is decreasing in .

6.2. Monotonicity with respect to transaction costs

From the discussion in Section 5, we have seen that transformed boundaries only depends on the round-trip transaction cost . In particular, and are respectively strictly decreasing and increasing in . However, the purchase/sale boundaries in the original scale still depend on the individual costs of purchase and sale. Write

and recall that . If then and the Merton line lies inside the no-transaction wedge. However, if then we have and and the Merton line may fall outside the no-transaction region. We have

so that the critical ratio of wealth in the illiquid asset to paper wealth at which the agent purchases more illiquid asset is decreasing in the transaction cost on sales. However, perhaps surprisingly, the dependence of the critical ratio at which purchases occur on the transaction cost on purchases is not unambiguous in sign:

is not necessarily negative, for we may have . This issues are discussed further in Hobson et al [15] where examples are given in which the Merton line lies outside the no transaction region and in which the boundaries to the no-transaction region are not monotonic in the transaction cost parameters.

7. Conclusion

Merton’s solution [20] of the infinite horizon, consumption and investment problem is elegant and insightful but assumes a perfect market with no frictions. Building on this work, there is a large literature, starting with Constantinides and Magill [9] and Davis and Norman [11] investigating the form of the solution in the presence of transaction costs. When there is a single asset Choi et al [7] (via shadow prices) and Hobson et al [15] (via an analysis of the HJB equation) are able to characterise precisely when the problem is well-posed. However, [11], [7] and [15] all assume the financial market includes just a single risky asset.

In this paper we have extended the results to two risky assets, and give a complete characterisation of the solution, but in the special case where transaction costs are payable on only one of the risky assets. This is also the model studied by Choi [6] using different methods. The presence of the second risky asset, which may be used for hedging and investment purposes, makes the problem significantly more complicated than the single risky asset case, but we can extend the methods of [15] to give a complete solution. Indeed, up to evaluating an integral of a known algebraic function, we can determine exactly when the problem is well-posed and up to solving a free boundary value problem for a first order differential equation we can determine the boundaries of the no-transaction wedge.

At the heart of our analysis is this free boundary value problem. Although the utility maximisation problem depends on many parameters describing the agent (his risk aversion and discount rate), the market (the interest rate and the drifts, volatilities and correlations of the traded assets) and the frictions (the transaction costs on sales and purchases) the ODE depends on the risk aversion parameter and just three further parameters, and the solution we want can be specified further in terms of the round-trip transaction cost.

Building on the work of Choi et al [7], in our previous work [15] we give a solution to the problem in the case of a single risky asset. The major issue in [7] and [15] is to understand the solution of an ODE as it passes through a singular point. In this paper the problem is richer, and the ODE is more complicated, but in other ways the analysis is much simpler because although the key ODE has singularities, these can be removed.

In the paper we have assumed a single illiquid asset and just one further risky asset, but the analysis extends immediately to the case of a single illiquid asset and several risky assets on which no transaction costs are payable, at the expense of a more complicated notation. This observation is a form of mutual fund theorem — the agent chooses to invest in the additional liquid financial assets in fixed proportions and these assets may be combined into a representative market asset. Details of the argument in a related context may be found in Evans et al [13]. Nonetheless, the extension to a model with many risky assets with transaction costs payable on all of them remains a challenging open problem.

References

- [1] Herczegh A. and Prokaj V. Shadow price in the power utility case. Annals of Applied Probability, 25(5):2671–2707, 2015.

- [2] M Akian, Menaldi J.L., and Sulem A. Multi-asset portfolio selection problem with transaction costs. Mathematics and Computers in Simulation, 38(1-3):163–172, 1995.

- [3] M Bichuch and P. Guasoni. Investing with liquid and illiquid assets. SSRN: ssrn.com/abstract=2523538, 2016.

- [4] M Bichuch and S.E. Shreve. Utility maximisation trading two futures with transactio costs. SIAM Journal of Mathamtical Finance, 4(1):26–85, 2013.

- [5] A. Cadenillas. Consumption-investment problems with transaction costs: survey and open problems. Mathematical Methods of Operations Research, 51:43–68, 2000.

- [6] Jin Hyuk Choi. Optimal investment and conumption with liquid and illiquid assets. ArXiV: arXiv preprint 1602.06998, 2016.

- [7] Jin Hyuk Choi, Mihai Sirbu, and Gordan Zitkovic. Shadow prices and well-posedness in the problem of optimal investment and consumption with transaction costs. SIAM Journal on Control and Optimization, 51(6):4414–4449, 2013.

- [8] P. Collings and Hausmann U.G. Optimal portfolio selection with transaction costs. In: Proceedings of the Conference on Control of Distributed and Stochastic Systems, Hangzhou, China, pages 189–197, 1999.

- [9] G.M. Constantinides and M.J.P. Magill. Portfolio selection with transaction costs. Journal of Economic Theory, 13:264–271, 1976.

- [10] M Dai and Y. Zhong. Penalty methods for continuous-time portfolio selection with proportional transaction costs. Journal of Computational Finance, 13(3):1–31, 2010.

- [11] Mark HA Davis and Andrew R Norman. Portfolio selection with transaction costs. Mathematics of Operations Research, 15(4):676–713, 1990.

- [12] B. Dumas and E. Luciano. An exact solution to a dynamic portfolio choice problem under transaction costs. Journal of Finance, 46:577–595, 1991.

- [13] J.D. Evans, Henderson V., and D. Hobson. Optimal timing for an indivisible asset sale. Mathematical Finance, 18(4):545–567, 2008.

- [14] P. Guasoni and Muhle-Karbe J. Portfolio choice with transaction costs: a user’s guide. Available at SSRN 2120574, 2012.

- [15] David Hobson, Alex Sing Lam Tse, and Yeqi Zhu. Optimal consumption and investment under transaction costs. ArXiV preprint arXiv:1612.00720, 2016.

- [16] David Hobson and Yeqi Zhu. Multi-asset consumption-investment problems with infinite transaction costs. ArXiV preprint arXiv:1409.8307, 2014.

- [17] K. Janacek and Shreve S.E.. Asymptotic analysis for optimal investment and consumption with transaction costs. Finance and Stochastics, 18(2):181–206, 2004.

- [18] J. Kallsen and Muhle-Karbe J. On using shadow prices in portflio optimization with transaction costs. Annals of Applied Probability, 20(4):1341–1358, 2010.

- [19] H. Liu. Optimal consumption and investment with transaction costs and multiple risky assets. The Journal of Finance, 59(1):289–338, 2004.

- [20] R.C. Merton. Life portfolio selection under uncertainty: the continuous-time case. The Review of Economics and Statistics, 51:247–257, 1969.

- [21] K. Muthuraman and S. Kumar. Multi-dimensional portfolio optimisation with proportional transaction costs. Mathematical Finance, 16(2):301–335, 2006.

- [22] D. Possamaï, H.M. Soner, and N. Touzi. Homogenization and asymptotics for small transaction costs: the multidimensional case. Communications in Partial Differential Equations, 40:609–692, 2015.

- [23] S.E. Shreve and Soner H.M. Optimal investment and consumption with transaction costs. Annals of Applied Probability, 4:609–692, 1994.

- [24] H.M. Soner and N. Touzi. Homogenization and asymptotics for small transaction costs. SIAM Journal of Control and Optimization, 51(4):2893–2921, 2013.

- [25] Alex Sing Lam Tse. Dynamic economic decision problems under behavioural preferences and market imperfections. PhD thesis, University of Warwick, 2016.

- [26] A.E. Whalley and Wilmott P. An asymptotic analysis of an optimal hedging model for option pricing with transaction costs. Mathematical Finance, 7(3):307–324, 1997.

- [27] Chen X.F. and Dai M. Characterisation of optimal strategy for multi-asset investment and consumption with transaction costs. SIAM Journal on Financial Mathematics, 4(1):857–883, 2013.

Appendix A Transformation of the HJB equation

Looking at the HJB Equation (5), and using intuition gained from similar problems, we expect that can be written as for a function of a single variable representing the ratio of wealth in the illiquid asset to wealth in the liquid assets. The equation for contains expressions of the form and and so can be made into a homogeneous equation by the substitution . The second-order equation for can then be reduced to a first order equation by setting and making the subject of the equation, see [13] or [15] for details of a similar order-reduction in a related problem. However, there are cases where lies inside the no-transaction region and at this point is undefined, and the above approach does not work. Hence, we need to use a different parametrisation. We use a parametrisation based on representing the proportion of paper wealth which is held in the illiquid asset. The delicate point at (or ) becomes a delicate point at , but as we show by a careful analysis any singularities can be removed.

Using the form of value function in (2) to compute all the relevant partial derivatives, (5) can be rewritten as

| (19) |

Let666The assumption means that the agent would like to hold positive quantities of the illiquid asset, and that the no-transaction wedge is contained in the half-space . To allow for it is necessary to consider . This case can be incorporated into the analysis by incorporating an extra factor of into the definition of , so that . This then leads to extra cases, but no new mathematics, and the problem can still be reduced to solving where is given by (7), but now for . and . Then

| (20) |

and in turn

| (21) |

This gives

| (22) | |||||

We expect that and hence that this expression is positive. It follows that . Then

| (23) | |||||

and

Substituting back into (19), and dividing through by we obtain

| (25) |

Recall the definitions , and . Then . Put in (25) and divide by . Then we have

| (26) |

Recall the definitions of the auxiliary constants given at the very start of Section 3.2. Rearranging (26) and multiplying by

| (27) | |||||

This can be viewed as a quadratic equation in . Note that the coefficients , , depend on the market parameters only through the auxiliary parameters , , .

We want the root corresponding to . This is equivalent to

| (28) |

Using (24) and the fact that , and multiplying (28) by we find we want the solution for which

| (29) |

Consider (26) and write . Then for fixed and , (26) is of the form where are constants with and . It is easily seen that this equation has two solutions, one on each side of , and that from (29) the one we want is the smaller root. Thus

where , , are the constants in (27). Note that . Then, we have

After some algebra, we arrive at

Appendix B Continuity and smoothness of the candidate value function

Proof of Case (i) of Proposition 1.

Suppose we have a solution to (12) with being strictly positive. Let , and . We set where solves . For notational convenience (and to allow us to write derivatives as superscripts) write as shorthand for .

First we check that is . Outside the no-transaction interval this is immediate from the definition, and on it follows from the fact that and are continuous. This property is inherited by the pair and then on integration by the trio and finally .

It remains to check the continuity of , and at and . We prove the continuity at ; the proofs at are similar. Using for the penultimate equivalence, we have

Then continuity of at follows from (22) where

Finally, from (24),

and we conclude that is continuous at .

Now we argue that is strictly increasing and strictly concave. Outside this is immediate form the definition. On the increasing property will follow if . But this is trivial since

Meanwhile, is concave on is equivalent to (28), or, by the analysis leading to (29) to . But this follows from our choice of root in (27).

∎

Proof of Case (ii) of Proposition 1.

Note that the integrand of is everywhere negative and therefore exists in . Hence .

For , the smoothness of follows as in the first case of Proposition 1. We will focus on the case of .

Suppose first that . Continuity of and at can be established if we can show that both

| (30) |

and

| (31) |

For (31) we have,

Suppose . Then using the definition of ,

Letting and using the fact that , we obtain

| (32) |

A similar calculation for gives as well. Hence (31) holds. As a byproduct, we can establish

Consider now continuity of at . We show exists. Consider:

Then,

| (33) |

Note that since . The limit is thus always well defined and can be used to obtain an expression for .

Finally we consider the case where or . Suppose we are in the former scenario. Then to show the continuity of at it is sufficient to show that

But when and thus . The above expression then holds immediately. Values of and can again be inferred from (31) and (33). A similar result follows in the case .

∎

Appendix C The candidate value function and the HJB equation

In this section we verify that the candidate value function given in Proposition 1 solves the HJB variational inequality

| (34) |

where , and are the operators

Note that for which is strictly increasing and concave in we have

and thus it is equivalent to show that . From construction of , it is trivial that , and on the no-transaction region, purchase-region and sale-region respectively. Hence it remains to show that

On the purchase region , direct substitution reveals that

and

where we have used the facts that , and the quadratic is decreasing (respectively increasing) over when (respectively ). Similar calculations can be performed on the sale region to show that and .

Now we show that on the no-transaction region . The inequality can be proved in an identical fashion. Again writing as shorthand for , we have

Since , it is necessary and sufficient to show

But for , and then

and the required inequality becomes

| (35) |

We are going to prove (35) for . Then will hold at as well by smoothness of .

By construction . Since is monotonic and is monotonic except possibly at it follows that is an increasing function of . Then, starting from the identity

and following the substitutions leading to (10), we find

Since the expression on the left hand side is increasing in , we deduce

Define . then is a solution to the ODE where . Note that .

Suppose . Then for and in turn we have , and we conclude for . Then

which establishes (35). If instead , we can arrive at the same result by showing for and in turn .

It remains to consider the case of . The only issue is that the comparison of derivatives of and may not be trivial at because of the singularity in . But by direct computation, we find . On the other hand,

due to (32) and similarly we have . Then is well-defined, and moreover since we have

Together with the fact that , we must have that is an upcrossing of at . From this we conclude on and on . (35) then follows.

Appendix D Proof of the main results

Proof of Theorems 1 and 2.

We prove the two theorems together. Suppose we are in the well-posed cases. From the analysis in Section 5, there exists a solution to the free boundary value problem with being strictly positive. By the smoothness of , is . Moreover, in Appendices B and C we saw that is a strictly concave function in solving the HJB variational inequality (34).

Let . Applying Ito’s lemma, we obtain

Suppose . Then , and the sum of the stochastic integrals is a local martingale bounded below by and in turn it is a supermartingale. Thus which gives

On sending , we obtain by monotone convergence and thus since is arbitrary.

If , then the above argument does not go through directly since the local martingale will not be bounded below. But using the argument of [11], we can consider a perturbed candidate value function which is bounded on the no-transaction region and define a version of the value process which will be a supermartingale. The result can be obtained by considering the limit of the perturbed candidate value function.

To show , it is sufficient to demonstrate the existence of an investment/consumption strategy which attains the value . Suppose the initial value is such that . Define feedback controls and with and where

and a finite variation, local time strategy in form of which keeps within . Let be the liquid wealth process evolving under these controls. Now since is always located in the no-transaction wedge, this strategy is clearly admissible.

Let be the process evolving under this controlled system. Then

By construction of and , . Moreover, is carried by the set over which . Hence , and similarly . Following ideas similar to Davis and Norman [11], it can be shown (see Tse [25]) that the local-martingale stochastic integrals and are martingales. Then on taking expectation we have

| (36) |

Further, it can also be shown (see Tse [25]) that . Then letting in (36) gives

Now suppose the initial value is such that . Then consider a strategy of purchasing number of shares at time zero such that the post-transaction proportional holding in the illiquid asset is , and then follow the investment/consumption strategy as in the case of thereafter. By construction of , . Using (36) we have

and from this we can conclude . Similar argument applies for initial value .

Now we consider the set of parameters which leads to unconditional ill-posedness. It is sufficient to show that the problem without the liquid asset (which is the classical transaction cost problem involving one single risky asset only) is ill-posed. Note that is equivalent to and this inequality can be restated as . But this is exactly the ill-posedness condition in the one risky asset case. See [15] or [7].

Finally we consider the conditionally well-posed case. From the discussion in Section 5, it is clear that as long as there still exists a solution to the free boundary value problem and thus one could show following the same argument in the proof for the unconditionally well-posed cases. Moreover, from Lemma 3 we can see that as , in turn from its construction. But and thus we conclude as . This shows the ill-posedness of the problem at , and using the monotonicity of in this conclusion extends to any .

∎

Appendix E The first order differential equation

For convenience, we recall some notations, and introduce some more:

| (37) |

We begin with a useful lemma.

Lemma 4.

has an alternative expression

| (38) |

Proof.

Consider

Then, noting that ,

and multiplying by ,

Writing this last expression as the difference of two squares we find

Then

The result then follows since

∎

Proof of Lemma 2.

(1) Observe that

where . Hence the crossing points of and away from are given by the roots of if such roots exist. Note that , since by assumption, .

If , then since is inverse U-shaped and there must be two distinct solutions of the quadratic equation . As , we must have on , and the two roots must be found outside this interval. If , the minima of is given by . Note that , and since , the root(s) of must be contained on the interval if they exist. The desired results can be established easily using these properties of .

(2) The behaviour at is only relevant for so we write this as . Note that explodes at . It is sufficient to check the denominator of is not equal to zero at . Direct calculation gives

and hence

| (39) |

(3) The following lemma records some useful identities.

Lemma 5.

Proof.

Most of these identities follow easily on substitution. For we have

which simplifies to give the stated expression. ∎

Return to the proof of Part (3) of Lemma 2. Note that . Assume we are in the range . Then , and

Further, after some algebra we can show .

Consider . Then both the numerator and denominator of are zero at . Nonetheless, we can apply L’Hôpital’s rule to calculate to deduce the expression in (15).

Now consider . Suppose first . Then

which is non-zero and has . It follows that for , and , and for and , .

Now suppose , and if that . Then

Then, in order to determine the value of via L’Hôpital’s rule we need

| (40) |

It follows that

and hence we obtain (16).

(4) We prove the results for . The results for can be obtained similarly, the only issue being that sometimes there is an extra case which arises when changes sign.

Note that for fixed , the ordering of and is given by Part 1 of Lemma 2. The monotonicity of in for can be obtained from (15).

If , then since

we conclude from (40) that is increasing in . Since it follows that for and for . Hence, if and only if , and we have

This gives the desired sign properties of on the range .

Now consider the case . From Part 3 of this proof, we have . We can compute the second derivative of with respect to as

so that (recall ) is convex in . Since , it follows that on the regime of we must have when lies between and and otherwise. Thus . Then

Finally, note that can be zero only if or . But for the limiting expression at is given by Part 3 of Lemma 2. Hence if and only if .

∎

The following lemma on further properties of is key in the proofs of the monotonicity property of and in results on comparative statics:

Lemma 6.

For and , and for and , we have .

Proof.

Direct computation gives

where is defined in (37). Differentiating we have

Hence for and , is increasing in for and decreasing in for . If , then is decreasing in for and increasing in for .

Now we calculate the limiting value of as . Clearly as . Then,

and

Observe that

and thus

Now we compute the limiting value of as . In this case is no longer converging. But consider

Using the fact that is independent of , we can obtain

and thus

after some algebra.

Suppose . For we have increasing in for and decreasing in for . Since on this range of and , we conclude for all .

If then . But attains its maximum at , hence we have for . Putting the cases together, and .

Now suppose . Suppose or . Then decreasing in for and increasing in for . Since and , we conclude for all . If then attains its minimum of zero at . Hence for . Again we find and .

It remains to check the result at and, if , at . At the result follows from (15). For , using (39) we have

and the monotonicity of in follows from the monotonicity of in .

∎

Proof of Lemma 3.

For any , then since is decreasing in and , can only cross at some . Moreover, for , .

Since , we have and in turn . Then .

Now consider . From the fact that we have

where we have used Lemma 6 and the monotonicity of to make the conclusion about the sign.

We now show that . We assume ; the proof for is similar. Consider a quadratic function . Then trivially . Choose a constant such that where is the negative root of . Then and equivalently . Now let . It is clear from the definition of that and then

and

Then for all , there exists such that for . Choose such that . Then we have on and solutions to cross from below. Let . Then for , . Moreover, there also exists such that for . Hence on , and then . On the other hand, for , and hence . We conclude for .

Hence, using (38) and L’Hôpital’s rule,

For the denominator, and for we have

where . For the numerator, note that for

Then,

where . Since is linear and , we can choose to work on a small interval such that . For sufficiently small such that , we have on .

Putting everything together and setting , for we deduce that

Letting and noting that does not depend on we conclude that .

∎

Appendix F Comparative Statics

Proof of Proposition 2.

(1) Set and similarly and . The idea behind this transformation is that is constructed such that it does not depend on . has a similar property. The free boundary value problem can be written as to find such that subject to and . Here .

Note that .

Define , and . Then, as functions of and , , and are all independent of .

We have

By the above remarks the only dependence on is through the term . Further

where given by

does not depend on . By Lemma 6, is decreasing in the second argument.

Let be two positive values of . Define and the solutions to the initial value problem with under parameters and respectively. We extend this notation to , , and in a similar fashion.

If is a solution to the initial value problem with we must have and hence is decreasing in . Then cannot upcross and since , we must have at least up to . From this we conclude . On the other hand, depends on only through . It follows that

But, by the monotonity of and in

where we use and and the fact that is decreasing in over the relevant range. We conclude that and hence .

To prove the monotonicity of the sale boundary , one can parameterise the family of solutions via its right boundary point . See [15] for the use of a similar idea.

(2) Now we consider the monotonicity of the limits of the no-transaction wedge in . We use a different transformation and comparison result. Set . Then the original free boundary value problem becomes to solve subject to boundary conditions where

Observe that does not depend on . Further,

and are both independent of . Hence and

are independent of . Recall we are assuming . Then over the relevant range and

Suppose . Using similar ideas in Part 1 of the proof we can deduce and for . Hence, using the fact that does not depend on

where we use the monotonicity of and the property that is decreasing in and hence is decreasing in . Thus . The monotonicity property of the sale boundary can be proved in a similar fashion by parameterising the family of solutions with their right boundary points.

∎

Proof of Theorem 4.

(1) We write out the proof assuming . The case follows similarly.

Further, is independent of and from this we deduce and hence over the continuation region we have . Using the signs of and together with the fact that is decreasing in , we conclude is increasing in . If we extend the domain of definition of to by setting for and for then we have being increasing in on .

Starting from the fact that is increasing in , we can deduce that each of , , and is increasing in . Then for (and using the overscripts to label the functions and parameters under the corresponding choice of ), we have

| (41) |

Recall that and on the purchase and sale region respectively. Using the monotonicity of in we conclude over .

Suppose is not decreasing in . Then since is continuous, must cross at least twice, with the first cross being an upcross and the last cross being a downcross. Denote the -coordinate of the first upcross and last downcross by and respectively.

Away from , (41) implies that cannot downcross . Then the only possibility is that there are precisely two crossings with . But if such that , the relationship gives

contradicting the hypothesis that is a downcross.

(2) Now consider the monotonicity in . For a similar argument to the above can be applied if we can show that is decreasing in . But this follows immediately as and is increasing in .

For we cannot use this argument. However, the monotonicity of the value function in , and hence the monotonicity of can be proved by a comparison argument. The value function only depends on the parameters through and the auxiliary parameters, so when comparing two models which differ only through we may equivalently compare two models which differ only in .

Consider a pair of models, the only difference being that in the first model has drift , whereas in the second model has drift where . Write . Suppose that parameters are such that Standing Assumption 1 holds in the first model; then necessarily Standing Assumption 1 holds in the second model. Let be given by

so that . Let be an admissible strategy for an agent in the first model. Suppose is non-negative, and note that the optimal strategy has this property, even if the initial endowment in the illiquid asset is negative, since in that case there is an initial transaction into the no-transaction wedge which is contained in the half-plane . We may assume we start in the no-transaction region. Then and solves

Define the absolutely continuous, increasing process by and set

Then and the corresponding wealth process solves

If then solves the same equation as and . Then, for any admissible strategy in the first model for which is positive, including the optimal strategy in this model, there is a corresponding admissible strategy in the second model with strictly larger consumption at all future times. Hence the value function is strictly greater in the second model. ∎